international bank for reconstruction and...

TRANSCRIPT

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No: 92248-CV

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

INTERNATIONAL DEVELOPMENT ASSOCIATION

INTERNATIONAL FINANCE CORPORATION

MULTILATERAL INVESTMENT GUARANTEE AGENCY

COUNTRY PARTNERSHIP STRATEGY

FOR

THE REPUBLIC OF CABO VERDE

FOR THE PERIOD FY15-17

November 18, 2014

Country Department for Cabo Verde (AFCF1) Africa Region International Finance Corporation Multilateral Investment Guarantee Agency

This document has a restricted distribution and may be used by recipient only in the performance of their official duties. Its contents may not otherwise be disclosed without World Bank authorization

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

The date of the previous World Bank Country Assistance Strategy for Cabo Verde Progress Report (FY09-12) was January 13, 2011

CURRENCY EQUIVALENTS

(as of November 10, 2014)

Currency Unit: Cabo Verdean Escudo

CVE 129.0287 = 1SDR US$1 = 87.74 CVE 1 SDR 1 = 1.47058

FISCAL YEAR

January 1 – December 31

ABBREVIATIONS AND ACRONYMS

AAA Analytic and Advisory Activities AECID Spanish Agency for International Cooperation and Development AfDB African Development Bank AFRVP Vice President, Africa Region (World Bank) AMP Port and Maritime Agency APL Adaptable Program Loan BADEA Banque Arabe pour le Développement Economique en Afrique (Arab Bank

for Economic Development in Africa) BCV Banco de Cabo Verde (Central Bank) BNPP Bank Netherlands Partnership Program BSG Budget Support Group CAS Country Assistance Strategy CCT Conditional Cash Transfer CEM Country Economic Memorandum CFTD Competitiveness for Tourism Development Project CPIA Country Policy and Institutional Assessment CPPR Country Portfolio Performance Review CPS Country Partnership Strategy CPSPR Country Partnership Strategy – Progress Report CVE Cabo Verdean Escudo CVI Cabo Verde Investments DFID Department for International Development (United Kingdom) DGALF General Directorate of Customs DGT General Directorate of Tourism DSA Debt Sustainability Analysis EC European Commission ECOWAS Economic Community of West African States ECREEE ECOWAS Center for Renewable and Energy Efficiency EPA Economic Partnership Agreement ERDF European Regional Development Fund ETS Economic Transformation Strategy ESW Economic and Sector Work

EU European Union FDI Foreign Direct Investment FSAP Financial Sector Assessment Program FY Fiscal Year GDP Gross Domestic Product GEF Global Environment Facility GNI Gross National Income GPRSP Growth and Poverty Reduction Strategy Paper GTFP Global Trade Finance Program HIV/AIDS Human Immunodeficiency Virus/Acquired Immunodeficiency Syndrome IBRD International Bank for Reconstruction and Development ICIEG Institute for Gender Equality and Equity ICR Implementation Completion Report ICT Information and Communications Technology IDA International Development Agency IDF Institutional Development Fund IDRF Inquérito às Despensas e Receitas Familiares (Family Expenditure and

Income Survey) IE Instituto de Estradas (Road Agency) IFC International Finance Corporation IMF International Monetary Fund IMP Instituto Maritimo Portuario (Maritime Port Institute) INE Instituto National de Estatística (National Statistics Institute) IPP Independent Power Production ISR Implementation Status and Results Report JSAN Joint Staff Advisory Note JSDF Japan Social Development Fund LDC Least Developed Country LPRP Luxembourg Poverty Reduction Partnership M&E Monitoring and Evaluation MCA Millennium Challenge Account MCC Millennium Challenge Corporation MDG Millennium Development Goal MIGA Multilateral Investment Guarantee Agency MpD Movimento para a Democracia (Movement for Democracy) MTEF Medium-Term Expenditure Framework NIS National Investment System NPL Nonperforming Loan ODA Official Development Assistance PAICV Partido Africano da Independência de Cabo Verde (African Party for the

Independence of Cabo Verde) PBC Performance-Based Contract PEMFAR Public Expenditure Management and Financial Accountability Review PER Public Expenditure Review PFM Public Finance Management PIM Public Investment Management PIP Public Investment Program PPP Public-Private Partnership PREM Poverty Reduction and Economic Management Department (World Bank) PRG Partial Risk Guarantee PRSC Poverty Reduction Support Credit

PSI Policy Support Instrument (IMF) QUIBB Questionário Unificado de Indicadores Básicos de Bem Estar (Unified

Survey of Core Welfare Indicators) RRESP Recovery and Reform of the Electricity Sector Project SIGOF Sistema Integrado de Gestão Orçamental e Financeira (Integrated Budget

and Financial Management System) SIL Sector Investment Loan SIM Sistema de Informação Municipal (Municipal Information System) SME Small and Medium Enterprises SOE State-Owned Enterprise SPA Special Partnership Agreement SPE State Participation Service SSA Sub-Saharan African TA Technical Assistance TFP Total Factor Productivity TTCI Travel & Tourism Competitiveness Index TSRP Transport Sector Rehabilitation Project TACV Transportes Aéreos de Cabo Verde (Cabo Verde Airlines) TVET Technical and Vocational Education and Training USD United States Dollar VAT Value-added Tax WAAPP West Africa Agricultural Productivity Program

IDA IFC MIGA

Vice President: Makhtar Diop Jean Philippe Prosper Keiko Honda

Country Director Vera Songwe Saran Kebet-Koulibaly Ravi Vish

Task Team Leader Marie-Chantal Uwanyiligira

Jerome Cretegny Conor Healy

The CPS Core Team was composed of: IDA/IBRD: Vera Songwe (AFCF1), Demetrios Papathanasiou (AFCF1), Eric Brintet (GGODR), Jean Michel N. Marchat (GTCDR), Raja Bentaouet Kattan (AFCF1), Philip English (AFCF1), Mademba Ndiaye (AFREC), Marie-Chantal Uwanyiligira (AFCSN), Sidy Diop (GGDOR), Upulee Iresha Dasanayake (AFCF1), Aifa Fatimata Niane Ndoye (GFADR), Fabrice Karl Bertholet (GEEDR), Jean-Philippe Tre (GFADR), , Pierre Graftieaux (EACNF); Tojoarofenitra Ramanankirahina (GTIDR), Isabelle Celine Kane (GSURR); Evelyn Awittor (AFCF1), Fernando Blanco (GMFDR); Marek Hanusch (GMFDR), Ehui Adovor (DECFP), Andres F. Garcia (GTCDR), Eneida Fernandes Mateev (GTCDR), Kjetil Hansen (GGODR), Andrew Asibey (AFTDE), Edgardo S. Mimica (GGODR), Kofi-Boateng Agyen (GTCDR), Julian Casal (GFMDR), Ndeye Aissatou Diagne Diouf (AFCF1), Ramatulay Barbosa (AFCSN), Anta Loum Lo (AFCSN), IFC Jerome P Cretegny (CAFW3), Elsa Perrine Fabienne Le Borgne (CNGS6), MIGA: Conor Healy (MIGEC).

CABO VERDE

COUNTRY PARTNERSHIP STRATEGY (CPS) FY15-17 TABLE OF CONTENTS

EXECUTIVE SUMMARY ........................................................................................................... I

I. INTRODUCTION ................................................................................................................. 1

II. COUNTRY DIAGNOSIS .................................................................................................. 1

2.1. OVERVIEW..................................................................................................................... 1

2.2. MAJOR DEVELOPMENT CHALLENGES AND THE WAY FORWARD .................. 5

2.3. OTHER DEVELOPMENT CHALLENGES ................................................................. 16

III. GOVERNMENT VISION ............................................................................................... 17

IV. WORLD BANK GROUP COUNTRY PARTNERSHIP STRATEGY ...................... 18

4.1. LESSONS LEARNED AND PROCESS OF CONSULTATION ................................. 18

4.2. WBG COUNTRY PARTNERSHIP STRATEGY FOR FY15-17 ................................ 21

4.3. FINANCING OF THE PROGRAM .............................................................................. 26

4.4. RISKS AND MITIGATION .......................................................................................... 27

List of Figures Figure 1: Cabo Verde’s Polity IV Score Independence ................................................................................ 2

Figure 2: CPIA Scores for SSA, 2013 .......................................................................................................... 2

Figure 3: Changes in Poverty Incidence from 2000 to 2007 ........................................................................ 3

Figure 4: Growth in Cabo Verde and Europe ............................................................................................... 5

Figure 5: The Current and New Fiscal Diamonds ........................................................................................ 9

Figure 6: Key Economic Activities as a Share of GDP, 1998 to 2011 ....................................................... 11

Figure 7: Growth Accounting with Raw Labor .......................................................................................... 13

Figure 8: Growth Accounting with Human Capital .................................................................................... 13

Figure 9: Global Competitiveness of Cabo Verde’s Economy (min = 0, max = 7) .................................... 13

Figure 10: Legal Environment for Business in Cabo Verde and Comparators ........................................... 14 List of Tables Table 1: Poverty by Gender of Household Head, 2007 ................................................................................ 4

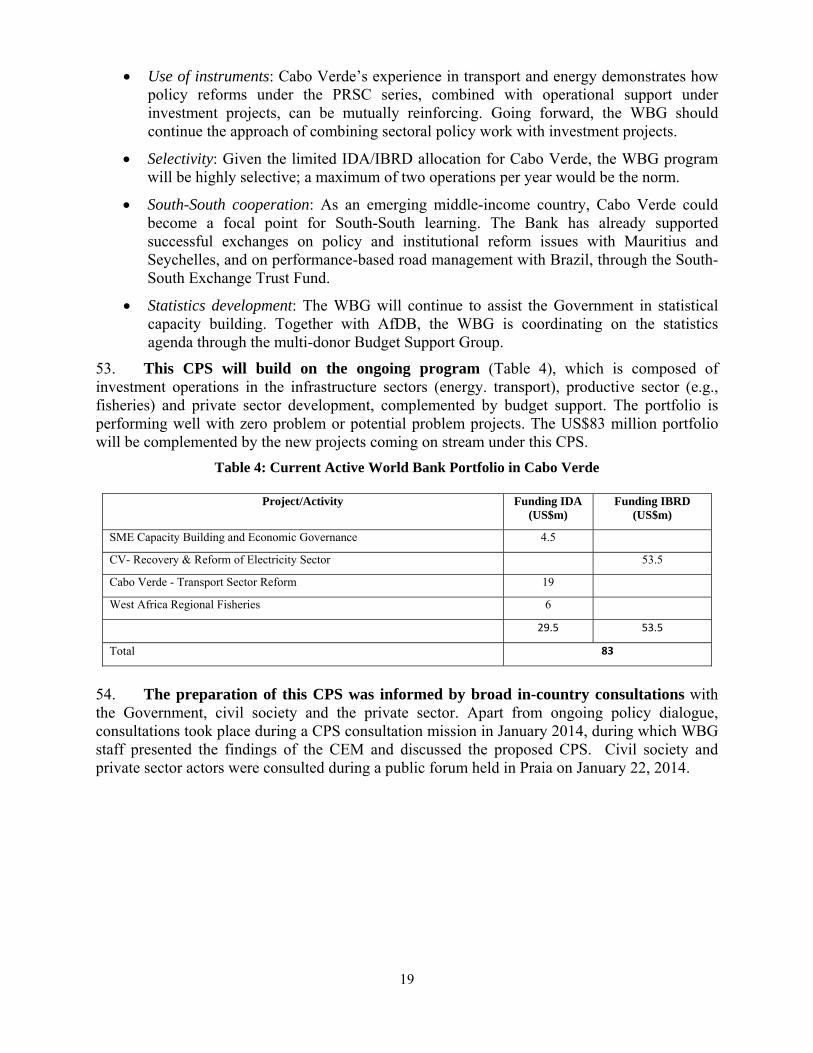

Table 2: Analytical Underpinnings of the CPS ............................................................................................. 5

Table 3: Key macroeconomic indicators: 2011 – 2017 ................................................................................ 7

Table 4: Current Active World Bank Portfolio in Cabo Verde .................................................................. 19

Table 5: Pillar I: Outcomes and Indicators* ............................................................................................... 22

Table 6: Pillar II Outcomes and Indicators* ............................................................................................... 24

Table 7: Proposed Lending and Non-Lending Activities ........................................................................... 27 List of Boxes Box 1: Combination of DPL and Sector Operations Instrumental in Advancing Structural Reforms ....... 10

Box 2: Summary of CPS Consultations ..................................................................................................... 20

List of Annexes Annex 1: Cabo Verde CPS Results Framework ......................................................................................... 29

Annex 2: Development Partners: Division of Labor .................................................................................. 32

Annex 3: Statistics in Cabo Verde .............................................................................................................. 33

Annex 4: CPS Completion Report (FY09-12) ............................................................................................ 34

Annex 5: Cabo Verde at a Glance ............................................................................................................... 65

Annex 6: Selected Indicators* of Bank Portfolio Performance and Management ..................................... 68

Annex 7: Summary of Non-lending Services ............................................................................................. 69

Annex 8: Key Economic Indicators ............................................................................................................ 70

Annex 9: Key Exposure Indicators ............................................................................................................. 72

Annex 10: Operations Portfolio – (IBRD/IDA and Grants) ....................................................................... 73 MAP IBRD No. 33383

i

EXECUTIVE SUMMARY

i. Cabo Verde’s strong growth from 2000 to 2008, driven by steadily growing tourism services and accelerated capital accumulation, translated into considerable poverty reduction and boosted shared prosperity. During those years, GDP growth averaged 6 percent annually and the economy grew from US$0.5 billion in 2000 to US$1.8 billion in 2012. Per capita Gross National Income (GNI, Atlas method) reached US$3,630 in 2013, more than four times what it was in 1990, placing the country firmly in the World Bank’s lower-middle-income category. In 2007, Cabo Verde became one of the few nations to graduate from the United Nations list of Least Developed Countries (LDC). The poverty rate dropped from 37 percent in 2001/2002 to 27 percent in 2007. The extreme-poverty rate dropped from 21 percent in 2002 to 12 percent in 2007, while the Gini coefficient fell from 0.55 to 0.48 over the same period. The income of the bottom 40 percent of the population increased as a share of total income from 9.9 percent to 21 percent; its share of consumption expenditures increased from 7 percent to 19 percent. The country also made such steady progress towards achievement of the Millennium Development Goals (MDGs) that achieving all of them by 2015 is within reach.

ii. However, since 2008, Cabo Verde has been severely affected by the global financial crisis and the impact of the European sovereign debt crisis on markets. GDP growth fell from an average of 6.7 percent in the pre-global crisis period (2000-08) to an average of 1.2 percent since then (2009-12). The global crisis has also affected macroeconomic stability, reflected in weakened fiscal and debt sustainability. The adverse external context marked a strong shift in the Government’s fiscal stance. The Government has accelerated its public investment program since 2008 as part of an ambitious drive to draw on remaining concessional resources to provide key infrastructure. The Public Investment Program (PIP) provided a modest impetus to economic growth but resulted in large fiscal deficits and increasing indebtedness.

iii. Cabo Verde understands the need to reset its diversified sources of growth. The Government recognizes that capital accumulation alone cannot sustain high growth rates indefinitely, and that the positive external circumstances that contributed to strong growth in the past have now become significantly less favorable. In the face of a difficult macroeconomic position and a highly uncertain global scenario, the Government’s Third Growth and Poverty Reduction Strategy Paper (GPRSP III) articulates a macroeconomic adjustment in the short to medium term, with a strong structural reform agenda to enhance productivity as the new source of growth and to promote shared and more diverse growth.

iv. Enhancing macroeconomic resilience and ensuring sustained growth through improvements in productivity are two interdependent endeavors. It will be crucial to contain expenditure, and especially to maintain the commitment toward decelerating the Public Investment Program. Fiscal consolidation implies a smaller fiscal envelope, which means that the public sector will need to increase its efficiency in expenditure management and promote a greater role for the private sector in Cabo Verde’s economic growth. A dynamic economy will be a crucial ingredient for reducing the debt-to-GDP ratio and thus strengthening fiscal and debt sustainability.

v. Cabo Verde will have to prepare itself for financing at market terms given that graduating from the UN list of LDCs in 2007 means that access to concessional financing is phasing out. Domestic public borrowing is limited by the need to support the currency peg and the risk of crowding out private investment. Thus, the government will have to mobilize new external resources to finance its existing and future debt obligations. Strong fiscal discipline and

ii

a downward-trending debt-to-GDP ratio will be indispensable for accessing financing at market terms, both from development partners and international capital markets more generally.

vi. Tourism will remain the key driver for growth and enhancing its performance will be critical. Over the past 15 years, the country has succeeded to position itself as a “sun, sea and sand” destination, and in 2013, for the first time the number of tourists visiting in one year exceeded the population of Cabo Verde. The contribution of tourism to local GDP grew from 5 percent in 2000 to around 20 percent in 2012. Given the sustained inflow of Foreign Direct Investment (FDI) in tourism, the sector is expected to continue being a driver of growth and a source of employment in the medium and long term.

vii. Against this backdrop, the FY15-17 Country Partnership Strategy (CPS) aims at supporting Cabo Verde in enhancing macro-fiscal stability and addressing growth challenges. The CPS outlines the financial and technical support of the World Bank Group (WBG), organized around two complementary programmatic pillars: (a) enhancing macro-fiscal stability in order to set the foundation for sustained growth, and (b) improving competitiveness and private sector development. The latter includes support to establish a conducive investment climate and improve the performance of the tourism sector and other sectors (e.g. fisheries and agriculture) that are potential drivers of poverty reduction. Knowledge products will include, among others, technical assistance to help the country develop external financing tools as part of its transition for financing at market terms.

1

I. INTRODUCTION

1. Cabo Verde is an archipelago of 10 islands located off the west coast of Africa. Nine of these islands are inhabited by approximately 500,000 inhabitants. The country has few natural resources and suffers from serious water shortages exacerbated by cycles of long-term drought, one of the main causes of emigration in Cabo Verde’s earlier history. It is believed that now at least as many Cabo Verdeans (and descendants) live abroad as on the archipelago.

2. The preparation of the proposed CPS (FY15-17) was delayed in order to give time to the government and the World Bank Group to assess the severe impact of the global financial crisis and the European sovereign debt crisis on Cabo Verde’s economy. This assessment has informed the design of the proposed CPS. The CPS was also informed by broad consultations with all stakeholders, including government officials and members of civil society and the private sector.

3. The CPS is in line with the GRSP III, and guided by the WBG’s two strategic goals of reducing poverty and boosting shared prosperity. Cabo Verde has already made great strides in reducing extreme poverty and increasing the welfare of the bottom 40 percent. Through the WBG’s focus on agriculture as a cornerstone of poverty reduction, and on strengthening the linkages of tourism to the agriculture and fisheries sectors, the WBG program will support the Government’s target of reducing the poverty rate to 20 percent by 2016. Through support to private sector development, in particular to the tourism sector, the WBG program will boost shared prosperity.

II. COUNTRY DIAGNOSIS

2.1. OVERVIEW

4. Cabo Verde is a robust democracy. The Polity IV index, which measures the strength of a country’s democratic institutions, rates Cabo Verde high in the region. Cabo Verde has not experienced a single coup d’état, a West African record shared only by Senegal. Since the adoption of a multiparty system in 1991, Cabo Verde has enjoyed remarkable political stability. The African Party for the Independence of Cabo Verde (PAICV) and the Movement for Democracy (MpD) have dominated Cabo Verdean politics, with each party having ruled for about a decade and alternating power regularly and peacefully.1 In 2003, Freedom House lauded Cabo Verde’s achievements since independence (Figure 1). Cabo Verde’s strong institutions are reflected in its score in the World Bank’s Country Policy and Institutional Assessment (CPIA) (Figure 2): it ranks at the top among IDA-recipient countries in the Sub-Saharan African (SSA) region, and third among all IDA countries.

1 In fact, currently both parties are in the Government, with the PAICV controlling the cabinet and the MpD the presidency. This power sharing arrangement, in place since the 2011 elections, has been functioning smoothly.

2

Figure 1: Cabo Verde’s Polity IV Score Independence

Figure 2: CPIA Scores for SSA, 2013

Source: Polity IV Project. Note: -10 denotes most autocratic and +10 most democratic. Graph displays West African countries, data availability permitting.

Source: World Bank. Note: SSA average only includes IDA countries.

5. A steadily expanding tourism sector and accelerated capital accumulation were the drivers of economic growth. Fueled by strong external demand, tourism export receipts grew from US$40 million in 2000 to more than US$400 million in 20122, an annual growth rate of 19 percent, much higher than the 6 percent observed for worldwide tourism in this period. The boom in tourism was driven by large FDI inflows, while the extensive utilization of Official Development Assistance (ODA) enabled the Government of Cabo Verde to increase public investment to about 10 percent of GDP over the last two decades. Consequently, Cabo Verde now has a relatively well-developed stock of infrastructure assets. Pivotal to the economic success was the establishment of the exchange rate regime, pegged to the euro, as a new mechanism for conducting monetary and exchange rate policy, which was supported by prudent fiscal policies. In addition, the fixed exchange rate facilitated the growth of FDI, remittances and migrant deposits, producing positive effects on growth, consumption and national savings, and providing liquidity to the domestic financial sector.

6. There has been noticeable progress in terms of poverty reduction and boosting shared prosperity. The poverty rate dropped from 49 percent in 1988/89 to 37 percent in 2001/2002 and then to 27 percent in 2007. The proportion of the population in extreme poverty also dropped significantly, from 21 percent in 2002 to 12 percent 2007. Income distribution and shared prosperity have improved. The Gini coefficient fell from 0.55 in 2002 to 0.48 in 2007, while the income of the bottom 40 percent as a share of total income increased from 9.9 percent in 2002 to 21 percent in 2007. Moreover, the share of expenditures of the bottom 40 percent in total expenditures increased from 7 percent in 2002 to 19 percent in 2007, demonstrating that the welfare of the bottom 40 percent has improved substantially. The GPRSP III projects a reduction in the poverty rate to 20 percent by 2016, to be achieved by promoting modernization of the agriculture and fisheries sectors, in which poverty incidence is most acute, thereby enhancing employment prospects for poor and vulnerable groups.

7. A poverty mapping exercise revealed that tourism growth in Cabo Verde has the potential to lift more people out of poverty. Poverty is particularly low in Sal and Boa Vista, the islands that have experienced much of the tourism growth (Figure 3). These islands were two

2 Latest available official data.

‐10

‐8

‐6

‐4

‐2

0

2

4

6

8

10

1975 1980 1985 1990 1995 2000 2005 2010

3

of the three islands that reduced poverty the most between 2000 and 2007, when tourism grew from 7 percent of GDP to nearly 20 percent. The large drop in poverty rates is largely due to the migration of Cabo Verdeans from other islands to seek economic opportunities in the relatively well-paying tourism sector. While the national poverty headcount is about 27 percent, the poverty headcount among agriculture and fisheries workers is 44 percent and 35 percent, respectively. Poverty among households linked to the tourism sector is just 12 percent. Falling poverty rates on other islands have likely been fueled by internal remittances from relatives working in the tourism sector in Sal and Boa Vista.

Figure 3: Changes in Poverty Incidence from 2000 to 2007

Poverty Incidence (%)

Island 2000 2007

Sal 25 10

S. Nicolau 44 21

Boa Vista 23 11

S. Vicente 29 17

Maio 34 21

Santiago 37 28

S. Antão 48 41

Brava 43 38

Fogo 42 40

Total 37 27

Contribution of population growth and poverty reduction between 2000 and 2010 to the fall in the poverty rate, displayed as changes in natural logarithms to approximate percentage changes.

8. Cabo Verde has also improved its social indicators. Cabo Verde ranks 132nd out of 187 countries in the UNDP’s 2013 Human Development Index (HDI), the third-highest ranking in SSA, putting it in the “medium human development” category. Cabo Verde’s average life expectancy, estimated at 71 years, is the highest in SSA. The infant mortality rate fell from 26 per 1,000 live births in 2007 to 15 in 2011. The maternal mortality rate fell from 36 per 100,000 live births in 2006 to 26 in 2011. By 2011, 94 percent of children under one year of age were fully immunized, and the percentage of the total population living less than half an hour from a health center reached 86 percent. Similarly, education outcomes put Cabo Verde at the top of Sub-Saharan Africa. The adult literacy rate is estimated at 87 percent, although disparities persist between men and women.

9. Despite its rapid economic growth in the 2000s, Cabo Verde continues to experience high unemployment, currently at 16.4 percent, as the rate of job creation has been lower than the growth of the economically active population. The current and projected demographic structure will likely generate a high and growing number of young workers entering the labor force. An analysis of the dynamics of labor force participation by gender indicates that an increasing number of women will enter the workforce. Without a comparable increase in the demand for labor, this trend will increase the unemployment rate, and likely affect women disproportionately. Female unemployment is almost 3 percentage points higher than male unemployment. Cabo Verde’s unemployment is not only biased towards women but also towards youth, and is especially acute among low-skilled workers. Large regional differences in

‐1.1

‐0.9

‐0.7

‐0.5

‐0.3

‐0.1

0.1

due to population growth

due to poverty reduction

4

unemployment are also observed. In addition to high unemployment, the islands of Santiago, Santo Antão and São Vicente show evidence of significant skill gaps.

10. Unemployment is not the only problem affecting Cabo Verde’s young and female populations. Young people and women generally have lower skills and labor productivity and tend to work in low-quality jobs. The available data show that informality is higher than average among women and youth. Individuals younger than 25 years old are mainly employed in the informal sector, the population between 25 and 35 years old is mainly formal, and the population between 35 and 60 years old is distributed almost evenly between formality and informality. The majority of elderly workers are employed in the informal sector. Results also show that informality is highly correlated with female workers, disadvantaging them in the labor market. Table 1 show that households headed by women are significantly poorer than households headed by men across all of the nine inhabited islands.

Table 1: Poverty by Gender of Household Head, 2007

11. In Cabo Verde, the importance of the diaspora is indisputable. The Cabo Verdean diaspora is large and estimated to number at least as many as the population of the archipelago. The vast majority are based in European countries and the United States. Indeed, emigration has been essential to the archipelago and today it is one of the main channels through which the country participates in the global economy. The diaspora supports the Cabo Verdean economy in four ways. First, they send home remittances. Second, they deposit a considerable amount of savings in Cabo Verdean banks, accounting for 40 percent of total deposits. Through financial intermediation, these deposits can support domestic investment and growth. Third, some members of the diaspora have invested in domestic enterprises through FDI. And fourth, it is estimated that Cabo Verdeans returning for holidays and vacations comprise about 20 percent of the total tourism industry.

12. While the diaspora has played and continues to play a critical role in the country’s economic and social life, there is untapped potential to engage the diaspora in supporting the transition of Cabo Verde to a higher income country, either as investors or as agents for the transfer of know-how in several areas of expertise. Furthermore, with about two-thirds of Cabo Verde’s tertiary-educated population living abroad, the diaspora can generate human capital gains. The GPRSP III recognizes the central role that the diaspora can play in the economic development of the country

Island Total Men Women

Santo Antão 0,28 0,26 0,32

Fogo 0,28 0,28 0,30

Brava 0,30 0,25 0,34

Santiago 0,18 0,14 0,21

S. Nicolau 0,12 0,10 0,15

Maio 0,14 0,14 0,14

S. Vicente 0,10 0,08 0,12

Boavista 0,06 0,05 0,06

Sal 0,04 0,04 0,04

.

Poverty at the household level

5

2.2. MAJOR DEVELOPMENT CHALLENGES AND THE WAY FORWARD

13. Cabo Verde faces three interrelated development challenges. First, it is confronted with a difficult external macroeconomic environment, compounded by weakened fiscal accounts and vulnerable external accounts. Second, while economic growth will continue to be mainly driven by the tourism industry, the sector needs to be more closely linked to the rest of the economy, to increase tourism’s multiplier effect. Third, Cabo Verde needs to increase its competitiveness by fostering private sector investment as its future growth has to rely less on physical capital accumulation and more on improvements in productivity.

14. Analytical work prepared in the last 4 years has informed the identification of the country challenges, in particular the recently completed Country Economic Memorandum (CEM).

Table 2: Analytical Underpinnings of the CPS

Cabo Verde: Country Economic Memorandum (2014)

Cabo Verde: Assessment of the performance of the tourism sector (2014)

Cabo Verde: A Diagnosis of Cabo Verde’s Public Investment Management System (2012)

Cabo Verde: Public Expenditure Management and Financial Accountability Review – PEMFAR (2012)

ELECTRA: From Recovery to Sustainability Study (PPIAF) (2011)

Policy Note on SOEs institutional arrangements (2012)

Cabo Verde: Inter-island Transport Study (2011)

Review of the air and port sectors in Cabo Verde (IFC), (2012)

Cabo Verde: Shaping the Future: How Higher Education can Support the Economic and Social Transformation Agenda in Cabo Verde (2012)

Cabo Verde : Policy Note on Macro-Financial Sector Vulnerabilities (2013)

2.2.1 A difficult macro-fiscal scenario and the need to enhance stability

15. The global financial crisis and double-dip recession in the Eurozone exacted a heavy toll on Cabo Verde’s economic growth and macroeconomic stability (Figure 4). After strong GDP growth that averaged 6.7 percent annually since 2000, Cabo Verde experienced a recession in 2009 as GDP contracted by 1.3 percent, recovering modestly to 1.5 percent in 2010 and to 4 percent in 2011. Another recession in the Eurozone in 2012 contributed to renewed economic weakening. Falling imports, decelerating credit to the private sector, contracting FDI, frail business confidence, flat inflation, and increases in unemployment and non-performing loans, suggest that growth has remained anemic since then, estimated at 0.5 percent for 2013 and 1.0 percent for 2014. Overall, Cabo Verde’s average GDP growth rate in the post-crisis period (2009-13) fell to 1.2 percent from 6.7 percent in the pre-crisis period.

Figure 4: Growth in Cabo Verde and Europe

Source: INE, Eurostat, and World Bank staff.

‐6

‐4

‐2

0

2

4

6

8

10

12

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Eurozone

Cabo Verde

6

16. The fall in revenues as a consequence of the economic slowdown accounted for almost 40 percent of the deterioration of fiscal balances.3 Due to the simultaneous drop in both tax revenues and donor grants, Government revenues fell from an average of 28.7 percent of GDP in 2006-08 to 25.2 percent in 2009-2013. Tax revenues fell from an average of 21.5 percent of GDP in 2006-08 to 18.6 percent in 2009-13. As a result of the economic crisis among Cabo Verde’s main development partners in Europe, external grants fell from an average of 4.9 percent of GDP to 3.6 percent in 2009-13. In 2014, the government made a considerable effort to increase revenues to counteract the fall in revenues, including the raising of VAT rates to the national level of 15 percent for sectors, including hotels and restaurants, which were previously only subjected to a 6 percent rate. The revenue outturn of the first half of 2014 shows that this has translated into considerable revenue gains on VAT; however, persistent economic weakness continues to moderate the overall revenue outturn. This CPS, through the PSRCs series, will continue to support government’s efforts in improving tax revenues.

17. Increases in total spending, and in particular investment, have been responsible for the remaining 60 percent of the worsening fiscal balances. The wage bill has remained stable at around 11 percent of GDP, which is comparable to that of other small economies in which economies of scale are not available. As a result of the recent elimination of energy subsidies, price-supporting measures in Cabo Verde are very low, at less than 1 percent of GDP. However, the authorities have undertaken an ambitious investment program, mostly financed by concessional borrowing. When the Public Investment Program was initiated in 2008, public investment more than doubled. Since then, public investment as a percentage of GDP (including investments through SOEs) has remained in double-digits. To some extent, strong public investment constituted a counter-cyclical policy response against strong economic headwinds from 2009 onward—although its economic multiplier effect tends to be small due to an import content of about 90 percent. Expansionary fiscal policy led to increased deficits and reversed the declining trajectory of the public debt, which reached an estimated 99 percent of GDP in 2013. However the debt is largely concessional, with an average maturity of 23 years and an average interest rate of only 0.75 percent, such that interest payments are low, at about 2 percent of GDP.

18. A stochastic Debt Sustainability Analysis (DSA) prepared by the Bank team indicates that the trajectory of public debt is sustainable, but significant vulnerabilities will persist in the short term. Based on the authorities’ Medium-Term Expenditure Framework (MTEF) and Medium-Term Debt Strategy (MTDS) for 2014-17, which were agreed by the Bank and authorities, the DSA indicates that the debt-to-GDP ratio is expected to reverse its increasing trend in 2016, when it will reach a peak of about 120 percent of GDP. It is then expected to fall slowly to about 80 percent of GDP by 2030.

19. Financing its debt obligations will become a key challenge for the country, as concessional resources decline. The Public Investment Program is almost entirely financed by project loans from bilateral and multilateral development partners. Gaps in the operating balance4 and amortizations are financed mainly with domestic public borrowing and budget support. Both are limited: domestic public borrowing is limited by law to 3 percent of GDP, and budget support is limited by the financing allocations of development partners—which are either phasing out or becoming less concessional following the country’s graduation from LDC status. Future borrowing will increasingly be devoted to servicing the outstanding debt (i.e. interest payments and amortizations). Gross Financing Needs (GFN) are expected to fall, driven by the retrenchment of the Public Investment Program, and by recent efforts to mobilize domestic

3 The CEM (2013) provides details on the contributing factors of the fiscal expansion 2009-13. 4 The operating balance is the fiscal balance, excluding capital expenditure.

7

revenue. However, it will be a crucial challenge for Cabo Verde to access new non-concessional external financing to service its debt obligations. Table 3 presents the key economic indicators for 2011-2017.

Table 3: Key macroeconomic indicators: 2011 – 2017

8

Medium term outlook

20. The challenge for fiscal policy in the coming years is to strike the right balance between supporting growth and preserving macroeconomic discipline and debt sustainability. The Government should pursue a gradual medium-term fiscal adjustment trajectory. On the revenue side, building on the achievements of the tax reform5, the Government should continue the revenue reform by closing tax loopholes, and consolidate achievements in tax administration.

21. On the expenditure side, the Government should pursue the gradual declining trajectory of public investment. Both the 2015 budget and the Medium-Term Expenditure Framework (MTFF) for 2014-2017 indicate that the retrenchment of public investment and net lending has commenced in earnest. Some large foreign-financed investments, including a social housing program, expansion of the Praia airport, the renovation of the Boa Vista seaport, and an energy project financed by IBRD, will keep investment spending relatively high until the completion of these projects. The Government will not add any new projects to the PIP but focus on execution of existing projects. Furthermore, the Government has begun developing a new national public investment system with Bank support whereby all investment projects will be subject to a rigorous technical assessment to calculate financial, economic and social returns based on reliable statistics. This should help the Government select investment projects that guarantee value for money.

22. The fiscal adjustment required over the medium term to maintain debt sustainability is feasible and consistent with the Government’s new economic growth model. Reducing debt levels implies lower spending, which suggests that growth-enhancing fiscal policies will come not from higher public investment, but mainly from expenditure reallocations and efficiency enhancements. At the same time, falling ODA needs to be offset by increased efficiency in tax collection. The “fiscal diamond” (Figure 5) illustrates Cabo Verde’s shifting fiscal priorities, with a stronger emphasis on domestic revenue and expenditure efficiency. Reducing borrowing in a context of declining ODA flows requires efforts to increase domestic resource mobilization and reducing public expenditures, especially public investment. Not only do these have short-term macroeconomic implications, but they should also shape the country’s new fiscal policy for growth: less aid, less borrowing, more domestic revenue and more efficiency. Implementation of the PEMFAR6 recommendations through the modernization of public finance management (PFM), enhancement of the public investment management (PIM) system, and improvements in the performance of SOEs, will be critical for the fiscal consolidation.

5 To strengthen domestic revenue mobilization, the Government adopted a tax package that increased the value-added tax (VAT) rate paid by hotels and restaurants from 6 to the standard rate of 15 percent; broadened the base of the VAT to include public utilities and oil; introduced a tourism fee of 2 euros per guest per night and a fee for the statistical registration of customs transactions; and expanded the base of the ecological tax on non-biodegradable imports. 6 The recent Public Expenditure Management and Financial Accountability Review (PEMFAR, 2013) prepared by the Bank, the AfdB, the EU and the Spanish Agency for International Cooperation (EACID), provides a more detailed assessment of Cabo Verde’s government expenditure management. This assessment covers expenditure management in the health, energy and environment sectors

9

Figure 5: The Current and New Fiscal Diamonds

Source: Bank staff, Country Economic Memorandum, 2014

23. Finally, the Government will need to prepare itself for financing at market terms. Expanding the financing envelope and reducing reliance on concessional budget support, while staying within the statutory limit for domestic borrowing, will be crucial for the Government to finance its debt. The African Development Bank has already phased out concessional budget support to Cabo Verde; the European Union will stop providing concessional budget support grants in 2020. In the future, World Bank budget support will be provided under IBRD terms. Moreover, as any emerging economy, Cabo Verde will increasingly have to access international capital markets. The small volumes of bond issues associated with a small economy, and high indebtedness resulting in weak sovereign credit ratings, will pose hindrances.

2.2.2 Improving state-owned enterprise (SOE) performance and public sector efficiency

24. Contingent liabilities incurred through state-owned enterprises pose significant fiscal risks and exacerbate medium-term vulnerabilities. SOEs in Cabo Verde provide vital services, especially in the strategic areas of transport, water, and electricity. The five largest SOEs in Cabo Verde are Empresa Nacional de Aeroportos e Segurança Aréa (ASA, operating the country’s airports); Empresa Nacional de Administração dos Portos (ENAPOR, operating the country’s harbors); Transportes Aéreos de Cabo Verde (TACV, the state airline); Empresa de Electricidade e Águas (ELECTRA, the national water and electricity utility); and Imobiliária, Fundiária e Habitat (IFH, providing housing services). These five SOEs account for 70 percent of state-owned capital and hold assets equivalent to 32 percent of GDP. Four of the five focus on transport and utilitiesvital areas for economic development and poverty reduction.

25. These SOEs have long been a source of contingent liabilities for the government, due to their generally weak commercial and financial performance. Given that the central government is the main shareholder, it directly or indirectly bears all risks of the SOEs’ poor financial performance. The total debt of SOEs reached 26 percent of GDP in 2012. While the SOE debt guaranteed by the state amounts to just 4 percent of GDP, the critical services that SOEs provide mean that the state is effectively obligated to lend financial support to the SOEs even on non-guaranteed obligations. The SOEs sometimes cover their losses by postponing maintenance or reducing services, but normally they induce financial transfers from the central government by defaulting on debts or accumulating arrears with providers. Cumulative debts and triggered contingent liabilities result in periodic recapitalization and debt swaps. Therefore, the effective contingent liabilities generated are actually much higher than the SOE debt officially guaranteed by the state. According to a recent Ministry of Finance report on SOEs (2013),

0

2

4

6Aid

Domestic Revenue

Debt

Expenditureefficiency

Current New

10

Box 1: Combination of DPL and Sector Operations Instrumental in Advancing Structural Reforms

The PRSC series and the transport sector credits have been supporting each other and helping advance the reform agenda in the transport sector. Actions supported under PRSC VIII related to publication of the consolidated report on the 2011 SOE financial statements by the Ministry of Finance. The audited statements of the main SOEs provided the detailed financial information needed to analyze the weaknesses of those SOEs, and to define the needs of the transport SOEs in terms of technical assistance and reforms. TA in the air transport sector (funded by the Road Sector Support Project closed in June 2013) helped define short-term strategic cost-saving measures, including actions under the PRSC VIII, such as shutting down losing routes and reviewing the free travel policies for staff and families.

The signing of performance agreements between the Government and ASA, ENAPOR, and TACV is a proposed action for PRSC X. The drafting of these agreements will be supported by the TA component of the new Transport Sector Reform Project (TSRP). In the road sector, the TSRP is funding performance-based road rehabilitation and maintenance contracts covering four islands and about 35 percent of the national road network, contributing to the 65 percent target objective set for 2015 in the PRSC series. PRSC IX supported the revised fare policies for ENAPOR (ports), also supported by the TSRP, which finances the necessary consulting services.

In the electricity sector, reforms supported by the PRSC series led to the resolution of longstanding legislative and regulatory issues (passage of legislation securing electricity bill payment by municipalities, and more recently final adoption of new legislation to strengthen judicial enforcement of measures against electricity theft). This was complemented by the IBRD-funded Recovery and Reform of the Electricity Sector Project (RRESP) which is financing energy mix investments and ELECTRA reform that have reduced the frequency and duration of load shedding and fuel costs.

underlying contingent liabilities in SOEs amounted to 11.6 percent of GDP in 2012 (including both guaranteed and non-guaranteed debt). The same report states that aggregate financial losses reached 1.4 percent of GDP in 2011 and 1 percent of GDP in 2012. A social housing project, Casa Para Todos, implemented by IFH, is financed with a loan equivalent to about 11 percent of 2013 GDP.

26. Reforming SOEs to ensure their financial sustainability is one of the major challenges for the near future. Support under the previous CPS has yielded tangible results (Box 1). But analytical work conducted by the WBG confirms that there is room to significantly improve SOE performance in delivering services. Over the last five years, the Government has been working to strengthen SOE management and oversight. In 2009, the Govenment adopted a new law restructuring the legal and governance framework for SOEs (Lei do Setor Empresarial do Estado). However, the effectiveness of state oversight and ownership continues to be limited by weak institutional capacities. Reforming the governance of SOEs need not only address inefficiencies in service delivery, but also improve financial performance to reduce contingent liabilities and improve the sustainability of public debt. In particular, ensuring that Casa Para Todos is implemented as originally anticipated will make a major contribution to reducing the debt-to-GDP burden.

2.2.3 Enhancing the performance of the tourism sector

27. Since 2007, tourism has been the main driver of growth in Cabo Verde (Figure 6). Tourism in Cabo Verde began when the Government started buying vast tracts of land in Sal and Boa Vista, two islands with attractive beaches and small populations; and also created special tourism development zones to encourage FDI. In 2010, hotels and restaurants generated 83 percent more jobs than in 2000, underlining the sector’s ability to generate employment. Sixty-four percent of those jobs were held by women. The World Travel and Tourism Council7

7 World Travel and Tourism Council. 2013. Cabo Verde Economic Impact Report.

11

estimates that the tourism and travel sector generates around one-eighth of all jobs in Cabo Verde. If indirect jobs are added to the equation, the sector generates more than 30 percent of employment with its linkages to other sectors such as construction, and to a lesser extent, agriculture, and fisheries.

Figure 6: Key Economic Activities as a Share of GDP, 1998 to 2011

Source: Central Bank 2012a and 2012b.

28. The capacity to design and implement a second generation tourism strategy is very limited and dispersed among several stakeholders. The tourism sector is currently overseen by the General Directorate of Tourism (DGT) within the Ministry of Tourism, Industry, and Energy. Tourism investment promotion is handled by Cabo Verde Investments (CVI), but its activities are limited in scope. As highlighted in the GPRSP III, the CVI’s inadequate capacity and dispersion are reflected in poor promotion and marketing, lack of data8 analysis to support decision-making, weak regulatory capacity, limited dialogue with the private sector, and lack of product diversity and supply. As identified in the GPRSP III, the Government needs to establish a national tourism organization with strong private sector involvement to provide much-needed leadership.

29. Environmental quality is a matter of serious and growing concern, particularly given the importance of natural capital to the tourism industry. Maplecroft, in its 2015 climate change vulnerability index (CCVI)9 identifies West Africa coastal areas as at high risk. Coastal erosion, sand extraction, the mismanagement of limited water resources and various forms of pollution all pose a significant threat to the country’s growth prospects. In addition, as a small island nation, Cabo Verde faces significant challenges associated with climate change—especially rising sea levels and the greater frequency of severe weather patterns—which could increase the likelihood and severity of droughts and flooding. Rapid economic growth is often associated with environmental degradation, and environmental issues are particularly pertinent for Cabo Verde, as the health of the tourism industry largely depends on the natural beauty of the archipelago.

30. The country’s tourism potential and the corresponding development impact remain to be fully exploited. Tourism development in general, and especially more recent projects, have 8 Cabo Verde’s 2013 ranking of 111 (of 140 countries) in “Comprehensiveness of Travel & Tourism Data” by the World Economic Forum’s Travel & Tourism Competitiveness Index (TTCI). The TTCI assesses 140 countries against 75 indicators under 14 different pillars. 9 Climate Change and Environmental Risk Atlas (CCERA) released by global risk analytics company Maplecroft on 29 October 2014.

0%

5%

10%

15%

20%

25%

1998 2000 2002 2004 2006 2008 2010% o

f G

ross

Dom

estic

Pro

duct

Tourism

Air transport

Primary sector

Industry

12

tended to favor the model of large-scale, all-inclusive resorts, with smaller accommodations on more populated islands often catering to the local population rather than to international visitors. A recent World Bank study finds that all-inclusive resorts and larger bed and breakfasts, especially those targeting high-end tourism, have the biggest effect on the economy. Apart from their considerable contribution to the national budget through taxation and the generation of employment, they can also have a considerable effect on national production through linkages with other sectors, especially services, fishing and agriculture (fresh food and vegetables). However, such linkages are underdeveloped due to the weakness of inter-island transport and local agriculture, which limits the ability of the tourism sector to reduce poverty and increase shared prosperity.

31. Investing in agriculture value chain development will focus on increasing agricultural productivity and promoting links between producers and the tourism sector. Efforts in the agriculture sector have focused on managing irrigation, dam and reservoir construction, expanding the area under drip irrigation; introducing new technologies10; extension services, rural road construction; and improving access to finance. In total eight dams are planned in order to supply 7 million m³ of water to irrigate 700 ha of land and allow several crop rotations a year. The result is a clear increase in output and a more commercial orientation away from subsistence and reliance on staples, but more efforts are needed to improve agriculture productivity through the adoption of improved technologies. In addition, to enable producers to enter the tourism value chain will require promoting contract farming mechanisms with local food traders and hotels and ensuring that the local supply is of the quality required for targeted markets. There is a clear opportunity for job creation for youth and women in particular in the areas of services, production, processing and marketing. This will help address some of the country’s major development challenges, including the high rate of poverty among farmers (44 percent) as well as the high rate of unemployment among local youth and women.

2.2.4 Improving competitiveness and private sector development

32. In Cabo Verde, total factor productivity (TFP) has been weak in recent years. Different growth decomposition exercises undertaken for the 2014 Country Economic Memorandum indicate that TFP has had a negligible or even negative impact on growth. A simple decomposition exercise using physical capital and labor force shows that after a negative contribution since independence in 1974, only in the period of 19952000 did TFP have a positive contribution to growth. Factoring in Cabo Verde’s considerable improvements in education, as well as a growth dividend from an expanding labor force, the calculations suggest that TFP has made a consistent and negative contribution to GDP growth (Figures 7 and 8).

33. To continue to enhance its growth potential and move up the income ladder, Cabo Verde will need to make productivity its new driver of growth. Intensifying investment in human capital is one element of this story. Reallocation of factors from low to high-productivity sectors will also be necessary, with improvements in labor force skills and labor market flexibility to enable these reallocations. This implies enhancing the performance of the main source of growth—the tourism sector—as well as the supporting sectors (such as infrastructure, financial sector, and skills development). The public sector will increasingly have to assume an enabling role for private sector-led growth.

10 For example new varieties, micro irrigation, hydroponics.

13

2.2.4.1 Investment climate

34. Cabo Verde needs to undertake further investment climate reforms and address a number of cross-cutting constraints to improve its global competitiveness. Some of Cabo Verde’s key weaknesses identified by the 2014 Global Competitiveness Report (Figure 9) include its market size (due to its limited domestic market); infrastructure (constraints relating to electricity supply, mobile phone subscriptions, availability of airline seats); innovation (limited availability of scientists and engineers, weak spending on R&D, limited patents); financial market development (high cost of financial services, difficult access to credit); and technological readiness (relatively limited internet bandwidth and internet penetration).

Figure 9: Global Competitiveness of Cabo Verde’s Economy (min = 0, max = 7)

Source: Global Competitiveness Report 2013-2014, World Economic Forum.

35. In terms of the legal environment, Cabo Verde was 122nd out of 189 countries in the overall 2015 Doing Business ranking (Figure 10): There has been significant progress in some areas. For example, the One-Stop-Shop reduced the registration process from 52 to 10 days, and the number of procedures from 12 to 7, between 2008 and 2014. However, from an international

0

1

2

3

4

5

6

7Institutions

Infrastructure

Macroeconomicenvironment

Health and primaryeducation

Higher education andtraining

Goods marketefficiency

Labor marketefficiency

Financial marketdevelopment

Technologicalreadiness

Market size

Businesssophistication

Innovation

Cabo Verde (122th) Switzerland (1st)

Figure 7: Growth Accounting with Raw Labor

Figure 8: Growth Accounting with Human Capital

‐8

‐4

0

4

8

12

16

80‐85 85‐90 90‐95 95‐00 00‐05 05‐10

Capital:a*dlnK

Labor:(1‐a)*dlnL

Productivity:dtfp

‐10

0

10

20

80‐85 85‐90 90‐95 95‐00 00‐05 05‐10

Capital:a*dlnK

Human Capital: (1‐a)*dlnH

Productivity:dtfp

14

perspective, although the country performs better than immediate neighbors such as Mauritania, Senegal or The Gambia, it ranks well below the best African performer—Mauritius—which is ranked 28th. Cabo Verde still lags behind in many areas, including (a) lengthy procedures to get construction permits; (b) difficulty in obtaining credit; (c) complexity of trade procedures; (d) the lack of a bankruptcy law; an ineffective court system (e.g., it takes many years for banks to redeem collateral in case of loan default); and (f) the high cost of electricity. Investment climate reforms in these and other areas are critically needed if the private sector is to play the envisioned leading role in economic growth. This is especially important for the tourism sector, as it operates in a very competitive global market, where the high cost of doing business translates into a less price competitive sector.

Figure 10: Legal Environment for Business in Cabo Verde and Comparators

Source: The World Bank

36. Despite substantial progress in human capital development over the past two decades, improving human capital productivity remains a challenge. The Government has spent a considerable share of its budget on improving the education system. Between 2000 and 2010, total economically active population increased by 28 percent and the employed population by 25 percent, even as total population increased only 13 percent. Increased labor force participation resulted in a demographic dividend for the economy. However, the World Economic Forum 2012 Competitiveness Report scores Cabo Verde poor on labor market efficiency (124th out of 142 countries). A better functioning of the labor market is another element of the reform agenda to ensure that improvements in the qualifications of the labor force are reflected in higher labor productivity.

2.2.4.2 Ensuring financial stability and expanding access to credit

37. Cabo Verde’s financial sector is relatively well developed, with credit to the economy close to 60 percent of GDP. The financial sector is dominated by eight commercial banks (four larger and four smaller), which together account for about 80 percent of financial sector assets. There are 10 non-bank financial institutions including a venture capital firm, three currency exchange bureaus, a payment services provider, a leasing company, three securities fund management companies, and a money services provider. A public-private risk guarantee agency has been established to support lending to small and medium enterprises (SMEs), but it is not yet operational. The stock exchange has four listed companies with a total market capitalization of US$91 million. There are also a number of offshore national banks, which have very limited linkages with the domestic economy and are poorly regulated, making them a source of reputational risk for the country. Most Cabo Verdeans have bank accounts at commercial banks. There are 1,138 bank accounts per 1,000 adults, about twice as many as in peer countries, which have a median of 545 accounts. The Government has started a number of

15

initiatives to improve financing for SMEs, including Novo Banco (a publicly owned commercial bank), CV Garante (a credit guarantee scheme), a venture capital fund, and a fund to foster entrepreneurship. The Government is also improving the conditions for microfinance.

38. However, access to finance for small and medium enterprises remains a major obstacle in Cabo Verde. While large corporations can borrow relatively easily and at interest rates comparable to those in the Eurozone, SMEs, which account for 95 percent of Cabo Verde’s private sector companies, struggle to obtain finance. In the 2014 Global Competitiveness Report, access to finance is rated as the single most important constraint to doing business in Cabo Verde, with almost a quarter of survey respondents identifying it as a major obstacle. In addition, the global financial crisis and Eurozone recession have not left Cabo Verde’s banks unscathed, aggravating existing vulnerabilities. Some of the vulnerabilities in Cabo Verde’s financial sector are a consequence of the small size of the market. For example, most banks are exposed to the same large clients, mostly in the real estate and construction sector. This increases the risk of contagion from shocks across financial institutions.

39. Regulatory capital ratios have been falling as asset quality has declined due to weak profitability. Non-performing loans (NPLs) have increased considerably since the onset of the global financial crisis, reaching 20 percent in September 2013. Capital asset ratios fell as banks built provisions, accounting for rising NPLs. The Central Bank has taken an increasingly proactive role in supervising banks, with a considerable amount of technical assistance from partners to closely monitor and address vulnerabilities in the financial sector.

2.2.4.3 Improving infrastructure management

40. Cabo Verde has taken significant steps to close its infrastructure deficits through high rates of public investment, which have largely been financed through an intense effort to mobilize external revenues. Cabo Verde now has a relatively well-developed stock of basic infrastructure. Nearly all of the nine inhabited islands have both marine and air access, and more than 72 percent of the national road network is paved, however maintenance is still an issue. The country has four international airports and three local airports, as well as nine seaports, seven of which have been modernized and expanded in the last five years. Its energy generation capacity is 156 MWs, of which almost 25 percent is renewable. As of 2014, more than 98 percent and 60 percent of the population have access to electricity and running water services, respectively.

41. Maintaining and making the most of the country’s infrastructure has become a top priority for Cabo Verde. For example, while the national electrification rate is high—as a consequence of large investments in energy—the 2014 Global Competitiveness Report ranks the quality of Cabo Verde’s electricity supply as very poor, with frequent and lengthy power cuts. And whereas much of the transport infrastructure is in good condition, inter-island connectivity is a major bottleneck for economic integration. Therefore, one of the most crucial challenges at this stage is to improve the management of electricity and transport SOEs, bringing in the private sector through private-public partnerships (PPPs) to improve services and maintain existing infrastructure.

42. Energy: With support of World Bank investments and TA and development policy loans, since 2011, notable progress has taken place in the electricity sector, including the resolution of longstanding legislative and regulatory issues (passage of legislation securing electricity bill payment by municipalities, and more recently final adoption of new legislation to strengthen judicial enforcement of measures against electricity theft). Since 2012, Cabo Verde is unique in West Africa in having adopted and successfully implemented tariff regulation mechanisms which ensure full cost recovery on a sustained basis. While much remains to be done to improve

16

ELECTRA’s operational performance, the measures implemented by the GoCV since 2011, have allowed the utility company to make significant progress in key areas such as addressing the backlog of gen-set maintenance and improving the generation mix. In particular, the frequency and duration of load shedding have improved markedly since 2011 and 2012, and fuel costs have decreased significantly thanks to renewable generation penetration. The government is pursuing the reform of ELECTRA and the scale up of its energy mix, including increasing the share of renewable energy.

43. Ports: In 2013, the Government undertook a series of reforms with WBG support, aimed at increasing private sector participation in the operation and delivery of port services. These included review and amendment of the Law of Ports of 2010; a new regulatory framework for the sector; changes in the statutes of the Maritime Port Institute (Instituto Maritimo Portuario, IMP), which became the Port and Maritime Agency (AMP), charged with economic and technical regulation of the sector; and changes in ENAPOR to turn it into a concessionaire of existing ports, with a new legal basis for entering into sub-concession contracts.

44. Air transport: One of the most difficult challenges facing the transportation sector is air transport. At the core of these challenges is the difficult financial position of Cabo Verde’s national airline, Transportes Aereos de Cabo Verde (TACV). Due to the geographic disposition of the Cabo Verde archipelago and the unreliability of maritime transportation between islands, air transportation has become the dominant transport mode for the development of tourism beyond the three islands with international airports, and the only practical option for reaching certain destinations. TACV’s financial solvency has been hampered for years by an array of managerial and structural issues, such as the lack of proper assessment of economically viable routes and ticket pricing, high labor costs, revenue leakages, lack of appropriate controls and financial reporting, and rapidly accumulating arrears. Large resulting losses have required capitalizations by the central government, which have made TACV, as currently managed, a fiscal liability for the state.

2.3. OTHER DEVELOPMENT CHALLENGES

2.3.1 Regional Integration

45. While Cabo Verde is a very open economy, its links with the global economy are highly concentrated in Western Europe. The increasing importance of the tourism industry has led to a commensurate dependence on the Eurozone economies. The United Kingdom, France, Germany, Portugal, and Spain are the most important consumer markets for Cabo Verde’s tourism service exports, as well as the most important sources of imports and FDI inflows. These countries are also among the major destinations for Cabo Verdean emigrants, and together with the United States they represent the main source of remittances. In addition, donor institutions of Portugal, Spain, and the European Union (EU) have been major sources of ODA inflows. The exchange rate peg to the euro also reinforces the ties with Europe. In addition, in 2007, Cabo Verde and the EU signed a Special Partnership Agreement (SPA), which offers Cabo Verde access to European internal markets as well as the possibility to gradually take part in certain EU policies and programs. The agreement also encompasses the possibility of funding from the European Regional Development Fund (ERDF) in the framework of cooperation with the outermost regions and other budget lines managed by the European Commission.

46. Despite some increase in the last years, Cabo Verde’s trade, investments and migration flows with the Africa Region are marginal. Cabo Verde is part of ECOWAS, but its share of exports and imports to the other 13 members of ECOWAS constitute barely 2 percent of total trade flows. For many years, ECOWAS regional integration was slow and uneven, but this

17

process has recently been accelerated, especially due to the adoption of the ECOWAS common external tariff, expected to begin in January, 1, 2015, and the ongoing negotiations on the West Africa Economic Partnership Agreement (EPA) with the EU. Furthermore, the protracted recovery of the Eurozone countries and Cabo Verde’s overall diversification strategy suggest that integration with the Africa Region and other markets needs to be explored, in view of the potential now arising from trade with emerging economies. The GPRSP III recognizes the need to diversify Cabo Verde’s partnerships, and this CPS will further strengthen Cabo Verde’s regional cooperation, with the inclusion of Cabo Verde in West Africa regional programs, including the ongoing West Africa Regional Fisheries Program and the upcoming West Africa Agricultural Productivity Program.

2.3.2 Statistical capacity

47. Cabo Verde’s statistical development is weak for a middle-income country (Annex 3). According to the World Bank’s statistical capacity index, Cabo Verde scored 66 in 2013, above the averages of 63 and 60 for IDA countries and Sub-Saharan African countries respectively, but well below the IBRD average of 75. The main constraints include lack of predictable funding, dependence on donor support for the implementation of surveys and censuses, and the scarce human resource capacities associated with the small size and geographic fragmentation of the country. The low and unpredictable funding and limited technical capacity led to (a) infrequent and limited quality of micro- and macro-data; (b) weak systems and analytical capacity to monitor and evaluate the effectiveness of public policies; (c) undeveloped systems to archive, disseminate and grant access to statistical products and indicators. Several donors, including the World Bank through the Trust Fund for Statistical Capacity Building, as well as the African Development Bank, the IMF, and bilateral donors are currently providing TA to the National Statistics Institute (INE).

III. GOVERNMENT VISION

48. The challenges identified above are reflected in the GPRSP III, which lays out Cabo Verde’s transition to a productivity-driven economic model. The GPRSP III entails several important policy shifts compared with previous poverty reduction strategies. The most important is significantly greater emphasis on the structural reforms needed to improve the country’s competitiveness. The GPRSP III sets out an ambitious structural reform agenda to improve the efficiency of public sector investment and SOE service delivery, enhance the investment climate, and reform the labor market to raise productivity and foster private sector development. Gender is identified as a cross-cutting issue in the GPRSP III, with the Cabo Verde Institute for Gender Equality and Equity (ICIEG) responsible for implementing its gender-related objectives. The CPS and the GPRSP III are closely aligned across all these areas.

49. A notable shift is the focus on eliminating extreme poverty through the development and modernization of the agriculture and fisheries sectors, and promoting shared prosperity by strengthening the linkages of the tourism sector with these primary sectors. Because of the untapped potential of the agriculture sector, and, given the strong incidence of extreme poverty in rural areas, the GPRSP III directs special attention to enhancing agricultural productivity and its linkages with the tourism sector by, for example, increasing the use of Cabo Verdean agriculture products by tourism operators. In addition, policies on human capital development, in particular TVET, are priority areas to boost shared prosperity

50. The GPRSP III supports the development of these seven economic clusters through interventions organized under five areas of intervention, or axes:

18

Infrastructure. Policies under this axis are designed to alleviate remaining infrastructure bottlenecks through completion of the Government’s public investment program in energy, multi-modal transportation (seaports, airports and road transportation), and water mobilization and irrigation facilities. The GPRSP III pays particular attention to institutional and managerial reforms in the energy and transportation sectors, as infrastructure assets in these sectors have been completed in the recent years.

Developing Human Capital. Interventions under this axis have two objectives: (a) to create a more competitive labor force and ensure that growth is sufficiently inclusive to improve income distribution; and (b) to strengthen Cabo Verde’s global competitiveness in technology-intensive industries. Programs under this pillar are viewed as fundamental for the promotion of sustainable and shared prosperity.

Good Governance. The objectives of this axis are to (a) bolster the country’s resilience to adverse shocks by strengthening its macro-fiscal position; and (b) increase the effectiveness of public service delivery, including new initiatives in critical areas such as the national planning system, public investment management, the government-wide M&E system, statistical development, and the oversight and reform of SOEs.

Support to the Private Sector. The overarching focus of the GPRSP III is to shift responsibility for the country’s economic development to the private sector. This axis includes specific measures to expand trade openness, improve the tax system, promote financial sector stability, and enhance the overall business and investment climate, and increased private sector participation in infrastructure service delivery. The GPRSP III clearly depicts the Government’s role as a catalyst and facilitator of the new economic model it proposes.

Development of Global Partnerships. In an environment of declining aid flows and reduced access to concessional financing, Cabo Verde still requires intense resource mobilization and technical assistance from both traditional and new partners. Hence the GPRSP III calls for comprehensive plan to diversify sources of funding to include new bilateral trading partners such as China, Brazil, the Middle East, and the West Africa region.

IV. WORLD BANK GROUP COUNTRY PARTNERSHIP STRATEGY

4.1. LESSONS LEARNED AND PROCESS OF CONSULTATION

51. The proposed CPS builds on the achievements of the previous CPS11. The Bank Group’s CPS for Cabo Verde and its program of support activities were designed to assist the Government in achieving the higher-level development goals that were outlined in its second Growth and Poverty and Reduction Strategy Paper for 2008-2011. The performance of the previous CPS-supported program (FY09-FY12) was rated Moderately Unsatisfactory, mainly due to slow implementation of pillar three (Strengthening Human Capital and Social Inclusion). As detailed in Annex 4, substantial outcomes were achieved under pillar 1 (Promoting Good Governance and Public Sector Capacity), and to some extent under pillar II (Improving Competitiveness and the Investment Climate for Private Sector Growth).

52. The approach of the CPS is informed by lessons learned from the implementation of the previous CPS, including:

11 The previous CPS was not a joint a WBG product; it was only a World Bank product.

19

Use of instruments: Cabo Verde’s experience in transport and energy demonstrates how policy reforms under the PRSC series, combined with operational support under investment projects, can be mutually reinforcing. Going forward, the WBG should continue the approach of combining sectoral policy work with investment projects.

Selectivity: Given the limited IDA/IBRD allocation for Cabo Verde, the WBG program will be highly selective; a maximum of two operations per year would be the norm.

South-South cooperation: As an emerging middle-income country, Cabo Verde could become a focal point for South-South learning. The Bank has already supported successful exchanges on policy and institutional reform issues with Mauritius and Seychelles, and on performance-based road management with Brazil, through the South-South Exchange Trust Fund.

Statistics development: The WBG will continue to assist the Government in statistical capacity building. Together with AfDB, the WBG is coordinating on the statistics agenda through the multi-donor Budget Support Group.

53. This CPS will build on the ongoing program (Table 4), which is composed of investment operations in the infrastructure sectors (energy. transport), productive sector (e.g., fisheries) and private sector development, complemented by budget support. The portfolio is performing well with zero problem or potential problem projects. The US$83 million portfolio will be complemented by the new projects coming on stream under this CPS.

Table 4: Current Active World Bank Portfolio in Cabo Verde

Project/Activity Funding IDA (US$m)

Funding IBRD (US$m)

SME Capacity Building and Economic Governance 4.5

CV- Recovery & Reform of Electricity Sector 53.5

Cabo Verde - Transport Sector Reform 19

West Africa Regional Fisheries 6

29.5 53.5

Total 83

54. The preparation of this CPS was informed by broad in-country consultations with the Government, civil society and the private sector. Apart from ongoing policy dialogue, consultations took place during a CPS consultation mission in January 2014, during which WBG staff presented the findings of the CEM and discussed the proposed CPS. Civil society and private sector actors were consulted during a public forum held in Praia on January 22, 2014.

20

Box 2: Summary of CPS Consultations

Key Messages and Priority Areas Identified from Consultations

Government (Ministerial and

Technical Levels)

CPS is well aligned with Government Strategy – GPRSP III Proposed program is potentially a transformative agenda for medium to long-term sustained

growth, and welcomed the new focus on tourism and agriculture sectors Worried about the small IDA and IBRD allocation Welcomed IFC increased role in Cabo Verde as this was not the case for past CPS

Private Sector

Welcomed the focus of the WBG on private sector development Welcomed the WBG focus on tourism sector, as this remains by far the fastest growth sector, and

asked WBG to explore potential links between tourism and agriculture. Suggested consideration of the fishery sector, which is potentially transformative