international and national standards and norms of financial reporting: monopoly or competitive...

Post on 19-Dec-2015

229 views

TRANSCRIPT

International and National Standards and Norms of Financial Reporting: Monopoly or Competitive Coexistence

Shyam Sunder, Yale University

Journée IFRS, CNAM, Paris

September 14, 2007

Summary• Traditionally, financial reporting was a matter of social norms of society• In recent years, financial accounting has shifted from social norms towards

national standards, and then towards international standards• In US, federal regulation of securities induced transition from norms towards

written standards in accounting thought, practice, regulation, instruction, and research; same may happen in EU

• Generally accepted accounting principles—no longer a description in its plain English meaning of a generally accepted societal norm

• Capitalized: Generally Accepted Accounting Principles• Social norms maintained by internal and external sanctions• Standards enforced by authority with power to punish • Recent failures; wisdom of transition from norms to standards?• Norms in professional, neighborhood, national, legal aspect of life• Consequences of transition from norms to national and intl. standards• Has the pendulum of standardization has swung too far?• What should be the balance between norms and standards in accounting?• Example: the consequences of the so-called “fair” value accounting

Long Tradition of Social Norms in Financial Reporting

Recent Shift from Social Norms towards National Standards

• and then towards International Standards

In US, Securities Regulation induced transition from norms towards written standards in

• Accounting thought,

• Practice,

• Regulation,

• Instruction, and

• Research;

• The same may happen in EU

Generally accepted accounting principles

• No longer a description in its plain English meaning of a generally accepted societal normCapitalized: Generally Accepted Accounting Principles

Social Norms vs. Standards

• Maintained by internal and external sanctionsStandards enforced by authority with power to punish

Use of Social Norms in all Walks of Life

• Professional,

• Neighborhood,

• National,

• Legal,

• Family

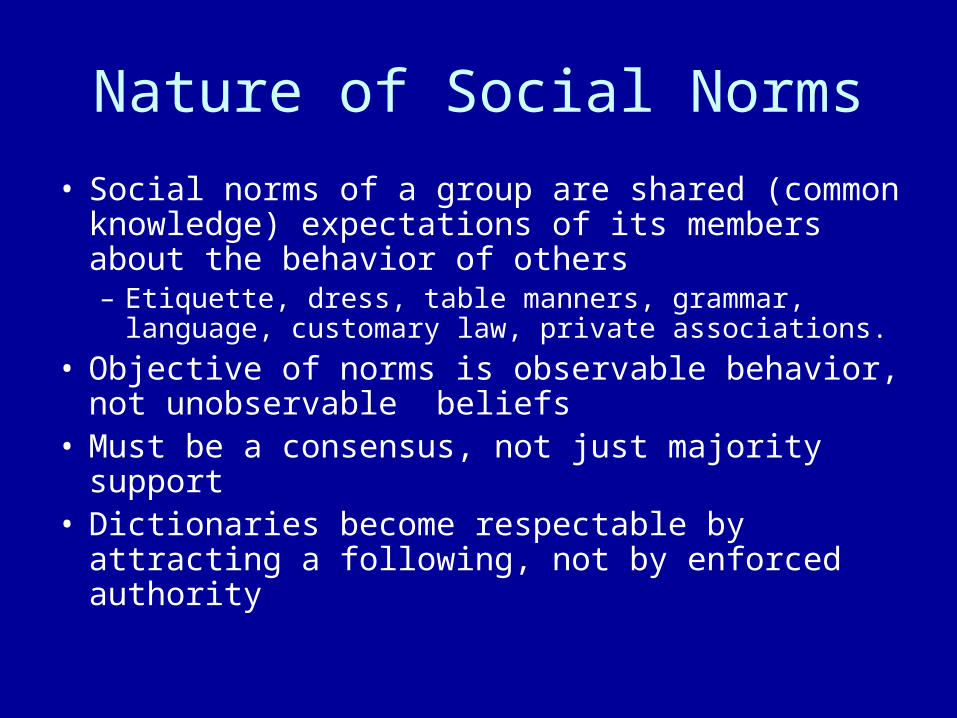

Nature of Social Norms

• Social norms of a group are shared (common knowledge) expectations of its members about the behavior of others– Etiquette, dress, table manners, grammar, language,

customary law, private associations.

• Objective of norms is observable behavior, not unobservable beliefs

• Must be a consensus, not just majority support• Dictionaries become respectable by attracting a

following, not by enforced authority

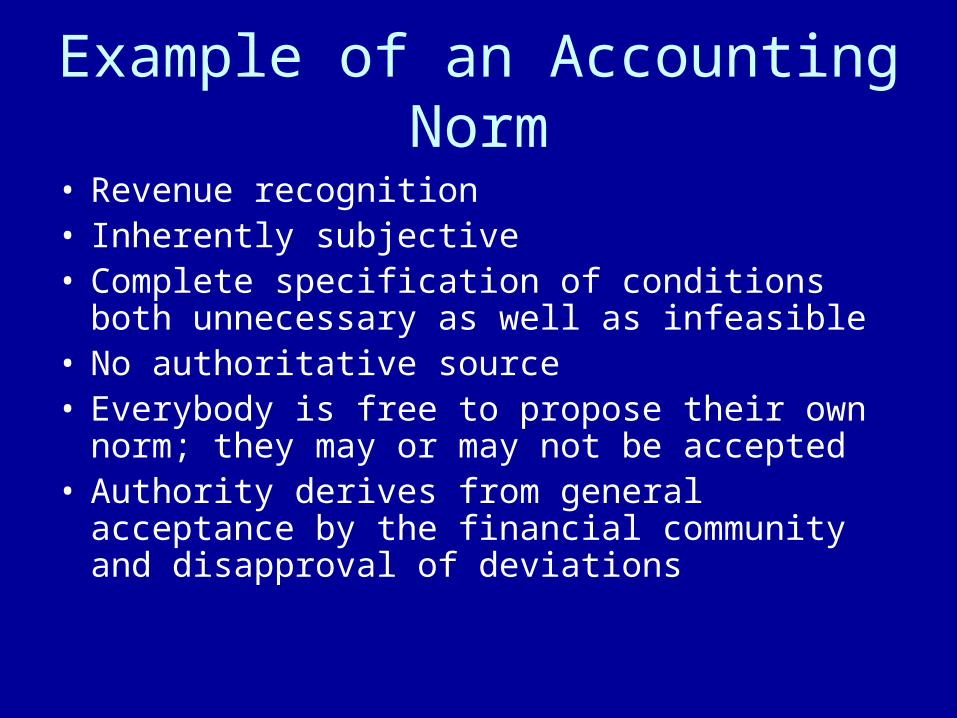

Example of an Accounting Norm

• Revenue recognition• Inherently subjective• Complete specification of conditions both

unnecessary as well as infeasible• No authoritative source• Everybody is free to propose their own norm;

they may or may not be accepted• Authority derives from general acceptance by

the financial community and disapproval of deviations

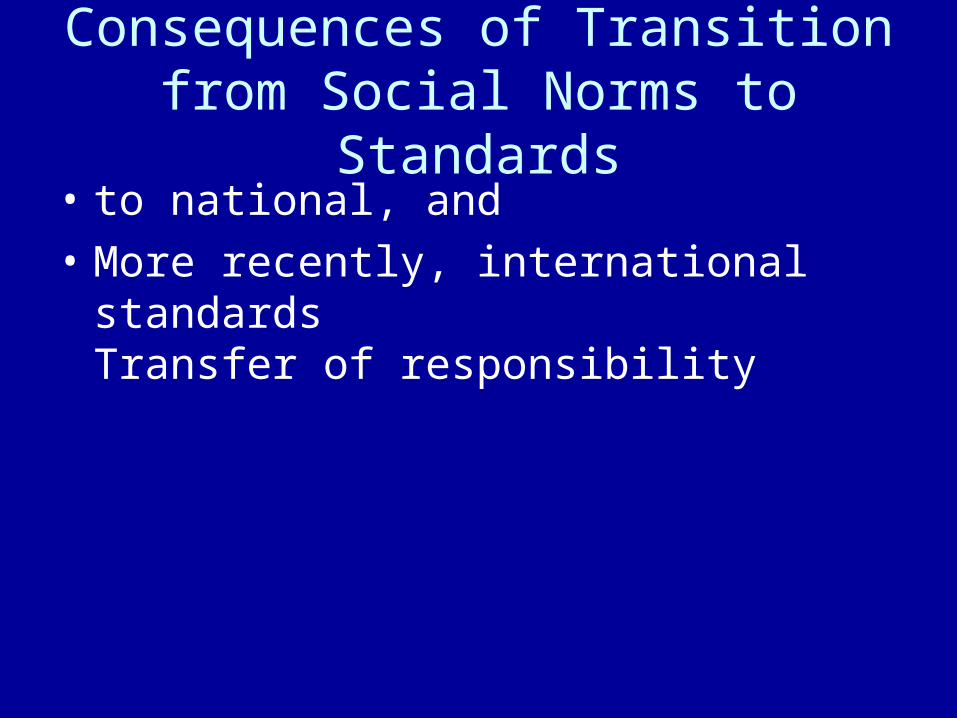

Consequences of Transition from Social Norms to Standards

• to national, and

• More recently, international standardsTransfer of responsibility

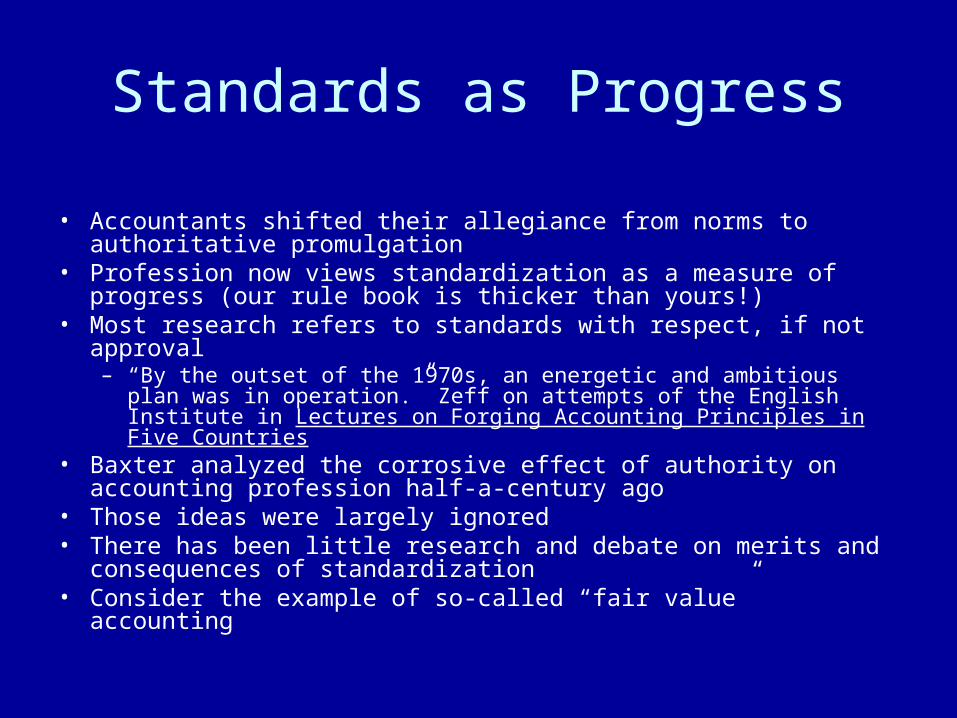

Standards as Progress

• Accountants shifted their allegiance from norms to authoritative promulgation

• Profession now views standardization as a measure of progress (our rule book is thicker than yours!)

• Most research refers to standards with respect, if not approval– “By the outset of the 1970s, an energetic and ambitious plan was in

operation.” Zeff on attempts of the English Institute in Lectures on Forging Accounting Principles in Five Countries

• Baxter analyzed the corrosive effect of authority on accounting profession half-a-century ago

• Those ideas were largely ignored• There has been little research and debate on merits and

consequences of standardization• Consider the example of so-called “fair value” accounting

Limits of Written Standards• Legal scholarship and practice is careful in recognizing the limits of the

efficacy of written rules• When it is not possible to write a rule that will improve the state of affairs

compared to a judgment-based system, the law leaves the judgment in place

• When a judge asks the jury to determine if the accused is guilty beyond reasonable doubt, lay jurors would want to know how much doubt is reasonable: ten percent, two percent, or one percent?

• Law does not attempt to codify answers to such questions• People who write and practice law understand all too well the consequences

of clarifying such questions would be even less desirable than the consequences of leaving the answers to the best judgment, even of lay people

• The SEC and the U.S. Congress refuse to clarify the definition of insider trading beyond “trading on non-public information”

• Again, the consequences of clarification are even less desirable than the consequences of leaving such matters to judgment.

Clear Rules or Road Maps for Evasion

• A law or rule must strive for clarity and enforceability without being a road map for evasion– Documents for entering a country– Schedules and routes of border petrol– Bright line accounting standards (3% SPEs, etc.)

remove the uncertainty for financial engineers

• Many clarifications facilitate financial fraud• Standard-writing agencies become unwitting

accomplices of evaders

Structural Weakness of a Standard Setting Body

• A permanent rule-making bureaucracy must make rules to justify its budget and existence– FASB (until recently) depended on revenues

from sale of its publications; IASB’s revenue model?

– Challenge to publish-or-perish very real– Inevitably, rulebook must get thicker over time

Incentives Created by Private Rule Making Institutions

• Existence of rule making institution encourages requests for “clarifications”– Lower resistance to client requests– General principles are questioned: Yes, it

says “Thou Shalt Not Steal,” but I only borrowed the car

– Competition among auditors makes it worse– After the change in auditors’ code of ethics,

partners rewarded for rainmaking, not their technical mastery or professional judgment

Effect of Rule Makers on Behavior of Auditors

• Pushed by clients to cite line and verse to support their positions

• Calls to FASB/IASB: the rule is not clear• Inability of FASB/IASB to respond in timely

fashion becomes basis for client to have his way• Absent rule making agency, the auditor would

have had to worry about the fair representation requirement under the security laws

• Existence of FASB/IASB as an unwitting supporter of the attitude: “if it is not proscribed, it must be OK”

Hide-and-Seek at the Wall Street

• Investment banker calls the FASB/IASB• Financial engineering to get around the rules• Reasonable body of rule might be devised to

deal with a given set of transactions• No rules can be devised when transactions are

continually redesigned to get around a slowly adapting body of rules

• Minimal changes to get over the bar• Wall Street/City of London calls to FASB/IASB

can have the character of the thief asking when you plan to be away from home

Rule-Making Monopolies

• Monopolies in US and EU deprive the economies and rule makers of the benefits of observation from experimentation with alternatives

• Difficulty of discovering efficient rules• Cost-of-capital consequences unclear• Self-serving arguments by constituents• Why deny ourselves the benefits of

information derived from competition

Recent Accounting Failures

• Questions about the wisdom of transition from norms to standards?

Has the pendulum of standardization has swung too far?

• Misunderstanding of the role of social norms in law• Popularity/promotion of stock and accounting-based

compensation for senior managers• Promotion of competition in the market for audit services• Creation of full-time private rule making agencies• Has this shift gone too far? How do we know and

decide?• What should be the balance between norms and

standards in accounting?

Example: the consequences of the so-called “fair” value accounting

Labels Matter

• What is common to:– Unified Budget Act (1964, Lyndon B.

Johnson)– Patriot Act (2002, George W. Bush)– Fair Values (1999, FASB/IASB)

“Pernicious changes with deceptively reassuring titles”

• Choose labels to put potential opponents on defensive before the debate begins

• Oldest trick in the book of policy rhetoric– Johnson wanted to use the social security surpluses to

finance increased spending on Great Society programs and the Vietnam War (who can argue for non-unified budget?)

– Bush wanted to fight the war on terror (who is against patriotism?)

– FASB wants to use current values (who can be against fair values in accounting?)

• “Fair” is a personal judgment, not a fact• To avoid misuse of language, put the rhetoric of “fair” aside,

and talk about current values of which generations of accountants and researchers have thought and written about

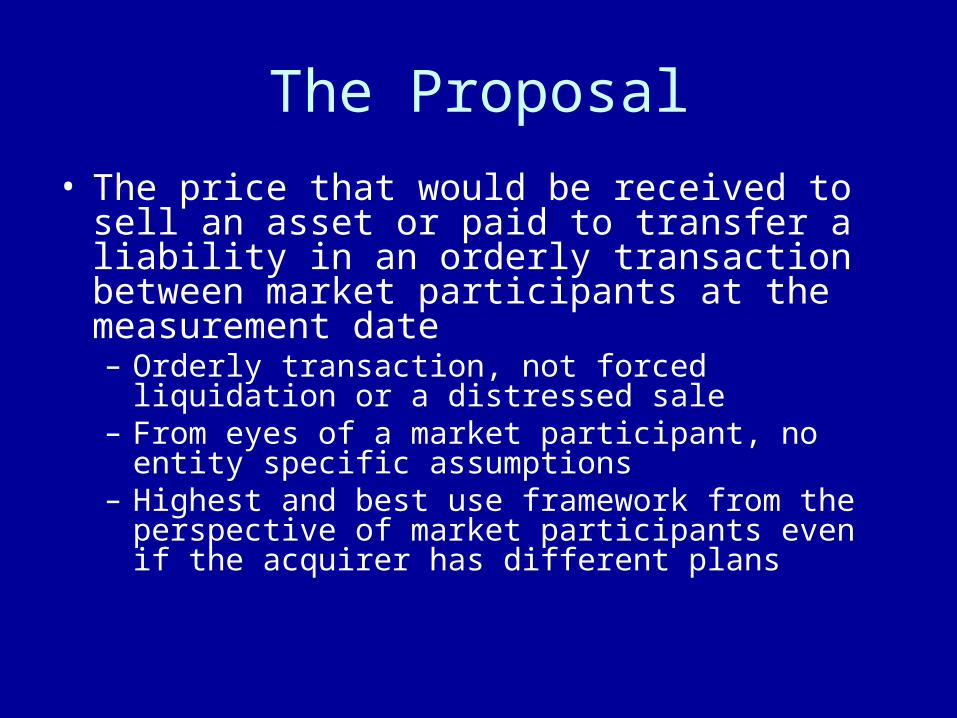

The Proposal

• The price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date– Orderly transaction, not forced liquidation or a

distressed sale– From eyes of a market participant, no entity specific

assumptions– Highest and best use framework from the perspective

of market participants even if the acquirer has different plans

The Valuation Debates

• Relevance to investment decisions

• Relevance to stewardship, management of enterprise resources, and contract enforcement

• Other criteria for evaluation: reliability, bias, timeliness, representational faithfulness, cost of implementation

Qualitative versus Quantitative

• Valuation debates have been largely been about qualitative characteristics of rules

• Without a framework for quantified comparison, debates can go on for ever– People don’t change their minds– Theories are supposed to die only with their

proponents (“science advances funeral by funeral”)– Even that is not true in case of fair values– Resurrection of current values under the new label

after an interval of almost 70 years• How do we bring an element of quantified

rationality to this debate?

Econometrics

• Great achievements of econometrics arise from our willingness to– Postulate an underlying structure and unknown parameters of

the problem– Characterize the properties of alternative estimators (e.g., OLS,

GLS, 2SLS, etc.) as a function of the underlying environment– Choose an estimator appropriate to the postulated environment– Use data to estimate the unknown parameters, holding the

structure constant– Examine propositions about the underlying parameter on the

basis of estimates– Use alternative datasets of examine the propriety of assumed

structure– When found inappropriate, change the assumed structure

Econometrics of Valuation

• Can we use a similar strategy for documenting the properties of valuation rules in various environments?

• It may not entirely get rid of judgments• But still, will move the debates among valuation rules

from the domain of opinion into data• Let me explain, starting with one postulated structure• Remember, we can always change the postulated

structure if we find a better one later • For now, let us focus on thinking about choice of

valuation rules as we think about choice of econometric estimators

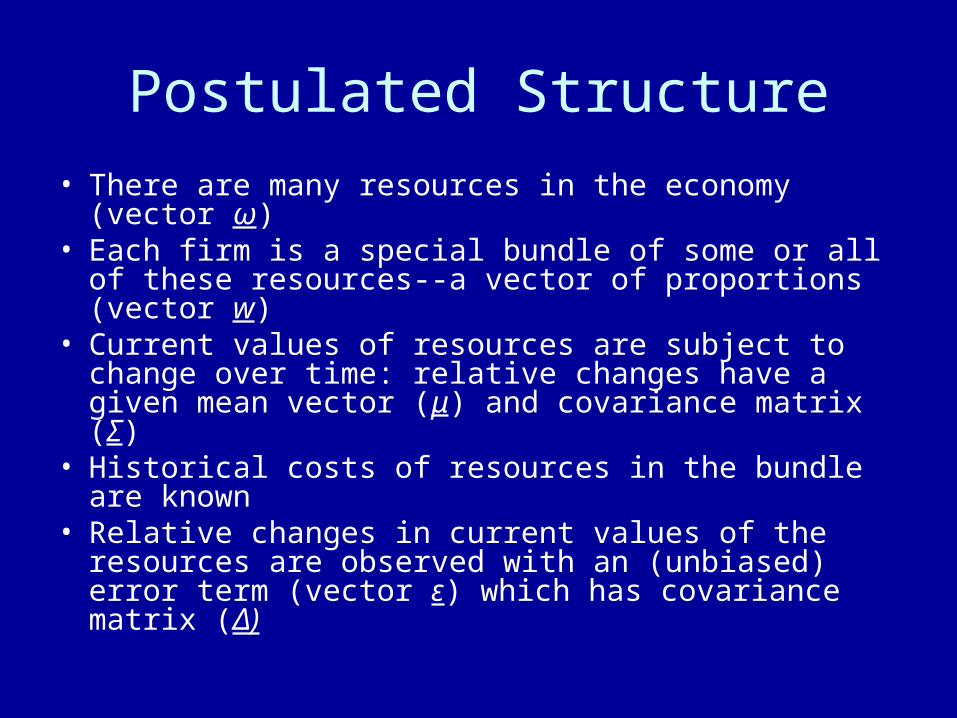

Postulated Structure

• There are many resources in the economy (vector ω)

• Each firm is a special bundle of some or all of these resources--a vector of proportions (vector w)

• Current values of resources are subject to change over time: relative changes have a given mean vector (μ) and covariance matrix (Σ)

• Historical costs of resources in the bundle are known

• Relative changes in current values of the resources are observed with an (unbiased) error term (vector ε) which has covariance matrix (Δ)

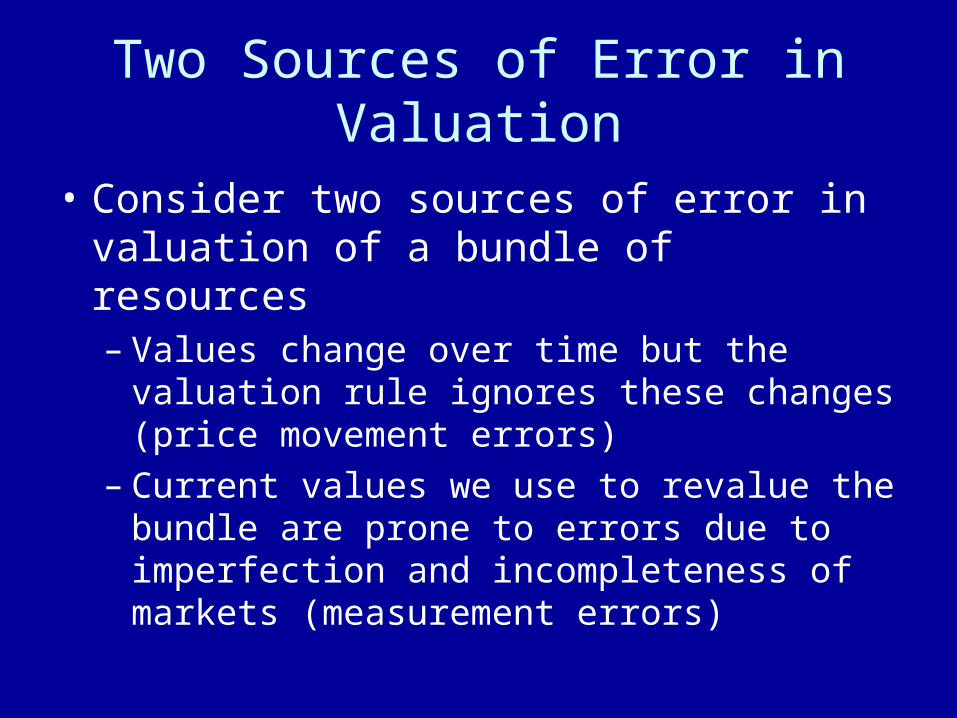

Two Sources of Error in Valuation

• Consider two sources of error in valuation of a bundle of resources– Values change over time but the valuation

rule ignores these changes (price movement errors)

– Current values we use to revalue the bundle are prone to errors due to imperfection and incompleteness of markets (measurement errors)

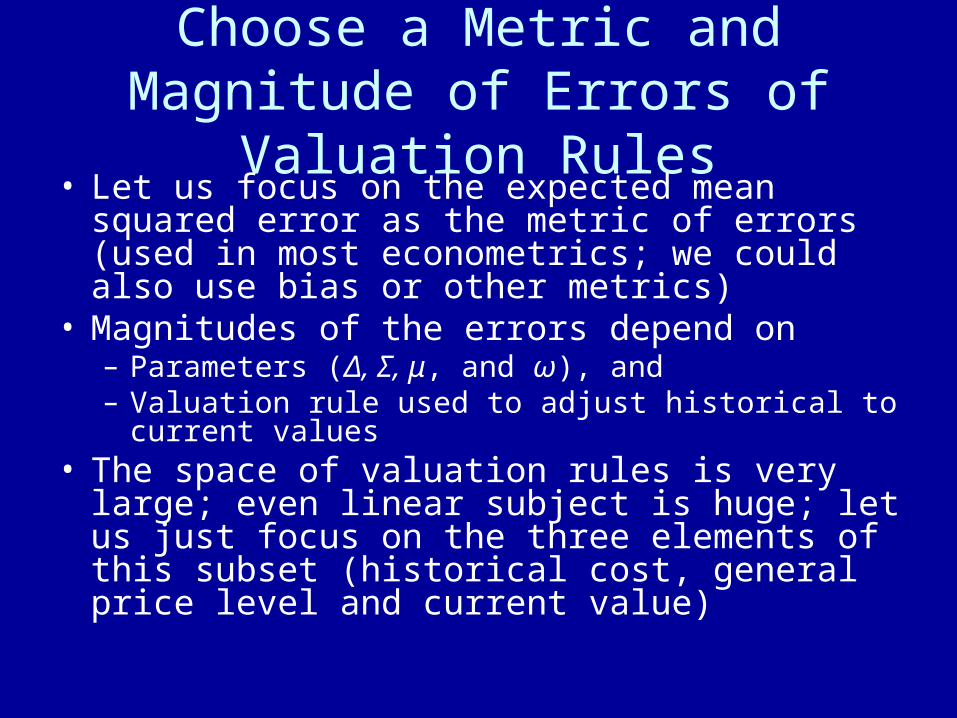

Choose a Metric and Magnitude of Errors of Valuation Rules

• Let us focus on the expected mean squared error as the metric of errors (used in most econometrics; we could also use bias or other metrics)

• Magnitudes of the errors depend on– Parameters (Δ, Σ, μ, and ω), and – Valuation rule used to adjust historical to current

values• The space of valuation rules is very large; even

linear subject is huge; let us just focus on the three elements of this subset (historical cost, general price level and current value)

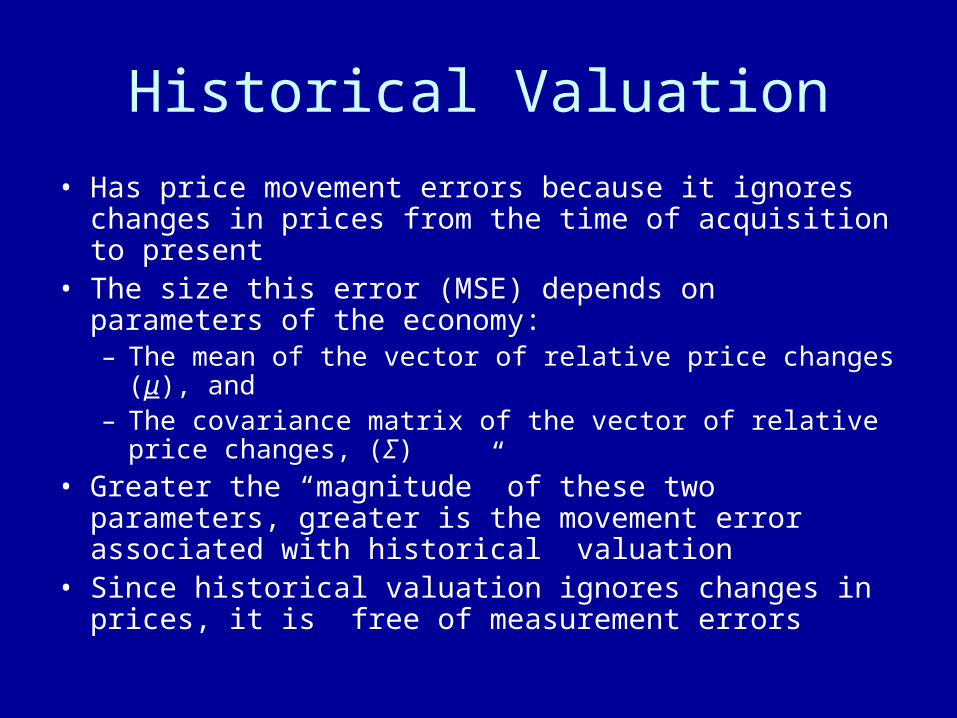

Historical Valuation

• Has price movement errors because it ignores changes in prices from the time of acquisition to present

• The size this error (MSE) depends on parameters of the economy: – The mean of the vector of relative price changes (μ), and – The covariance matrix of the vector of relative price

changes, (Σ)• Greater the “magnitude” of these two parameters,

greater is the movement error associated with historical valuation

• Since historical valuation ignores changes in prices, it is free of measurement errors

Current Valuation

• It has price measurement errors arising from assessment of current values

• Again, the size this error (MSE) also depends on parameters of the economy: – If we assume that the relative changes in current values

are measured without bias (ε = 0), the MSE arising from the mean of measurement errors is zero

– The error arises from the covariance matrix of the vector of measurement errors in relative price changes (Δ)

• Greater the “magnitude” of this covariance matrix, greater is the measurement error associated with current valuation

• Since current valuation takes into account the changes in prices, it is free of price movement errors

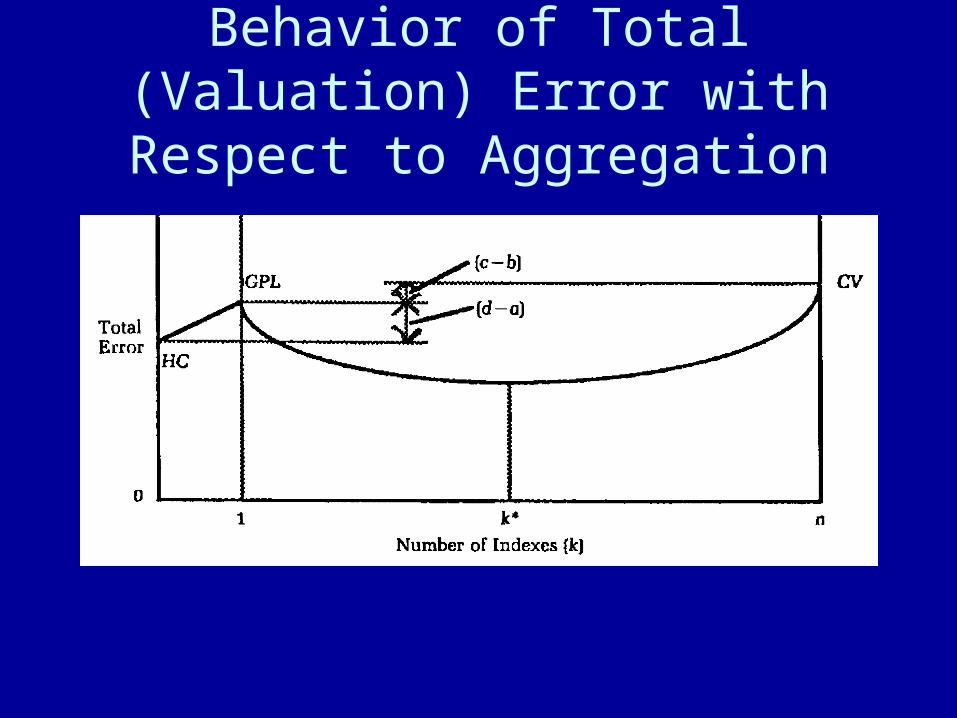

General Price Level Valuation

• GPL uses a single price index to adjust historical values towards current values

• The use of a single price index reduces the price movement error associated with the historical estimator but does not eliminate it

• The use of a single price index also introduces some measurement error, although it is not as large as the error associated with current value estimator

• The total error associated with GPL estimator depends on the values of the parameters μ, Σ, Δ and ω.

• Let us look at the picture as a schematic graph

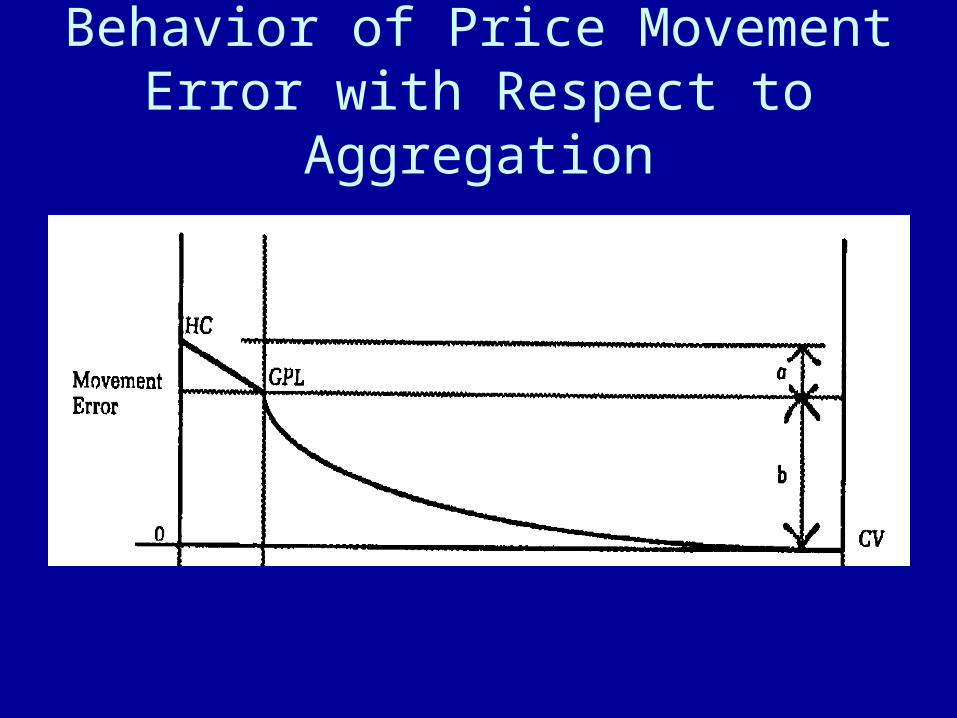

Behavior of Price Movement Error with Respect to Aggregation

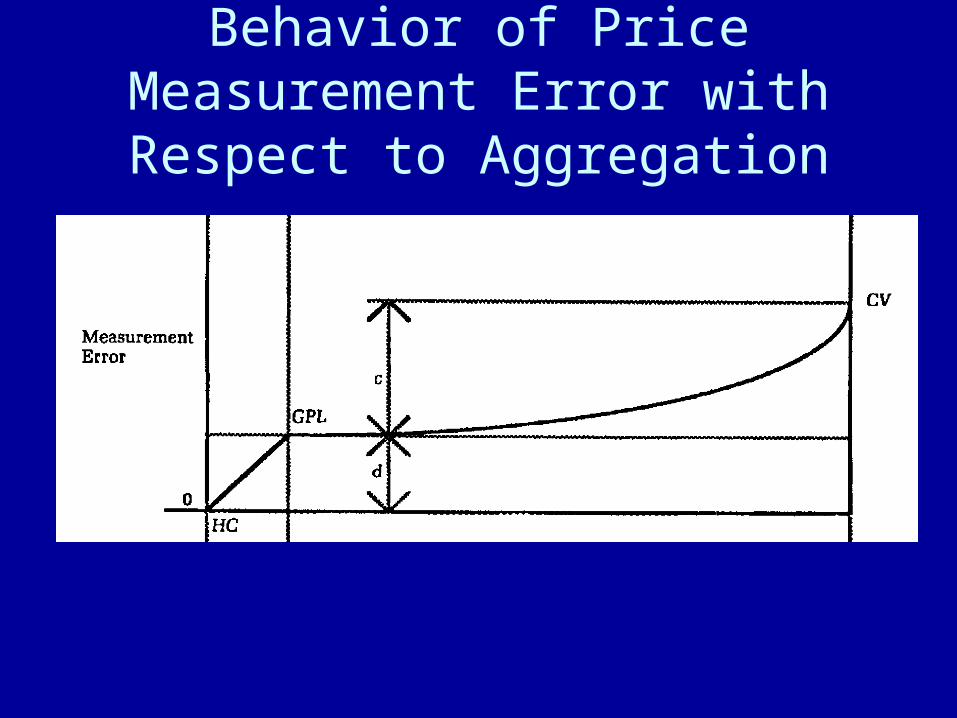

Behavior of Price Measurement Error with Respect to Aggregation

Behavior of Total (Valuation) Error with Respect to Aggregation

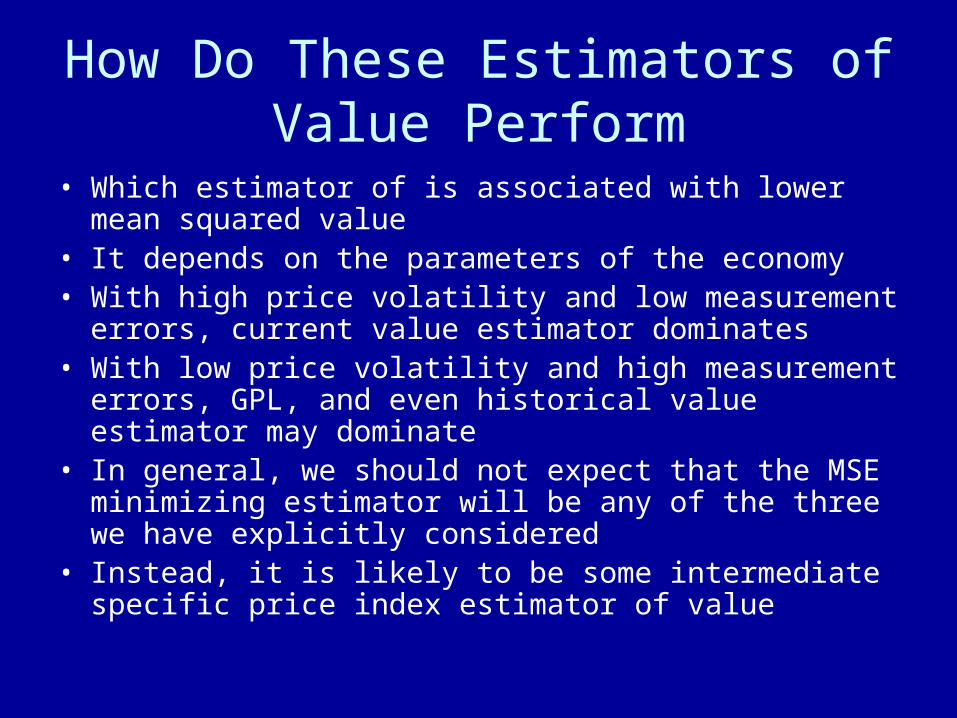

How Do These Estimators of Value Perform

• Which estimator of is associated with lower mean squared value

• It depends on the parameters of the economy• With high price volatility and low measurement errors,

current value estimator dominates• With low price volatility and high measurement errors,

GPL, and even historical value estimator may dominate• In general, we should not expect that the MSE

minimizing estimator will be any of the three we have explicitly considered

• Instead, it is likely to be some intermediate specific price index estimator of value

Testable Implications of Theory

• Current valuation would be more informative for firms and industries whose– Assets have a large mean rate of price change– Assets have more variability in price changes– Assets are traded in relatively perfect and complete

markets (accurately measured CV)• Real estate, mineral deposits, films, software,

patents have large measurement errors• Instead of cross-sectional tests (e.g., Gheyara

and Boatsman 1980, Ro 1980), we could benefit from paying more attention to characteristics of assets of firms and industries

Testable Implications of Theory

• Efficient valuation rules would vary across assets, firms and industries

• Level of aggregation at which current values are chosen has a major impact on the properties of valuation (left open in FASB/IASB’s proposal)

What Do We Learn from This Theory?

• Theories of valuation can be integrated into a framework to facilitate direct comparison of their properties in specified environments

• When current prices change, and are prone to measurement errors, neither the current nor general price level valuation is necessarily the min(MSE) estimator of the unobserved economic value of assets

• Generally, min (MSE) estimator is likely to be a specific price index rule

• If the measurement errors are sufficiently large relative to movement errors, historical cost can be the min (MSE) estimator

• Which valuation rule has min (MSE) is a matter of econometrics, not theory or principle (depends of relative magnitude of parameters of the economy)

An Agenda for Reforms• The pendulum seems to have swung too far in the direction of

written standards• Reconsider a stronger role of social norms and personal and

professional responsibility in accounting and business– Reconsider virtues of promoting competition among auditors (a

“market for lemons”)– Better use of social norms: “fair representation” as a moral

compass of accounting• As “guilty beyond reasonable doubt” in criminal law• Neither can be captured in written standards• Creation of accounting courts to judge “fairly represent”

– Assist evolution of accounting norms through competition among multiple accounting rule makers (no collusion, no convergence)

– Remove rule-making monopolies in U.S., Europe (and elsewhere)

Thank You

• Please send comments to• [email protected]• The paper and the presentation will be available

at• www.som.yale.edu/faculty/sunder/research