internal auditors and job stress

TRANSCRIPT

Internal auditors and job stressLinda Lee Larson

College of Business/Department of Accounting, Ball State University,Muncie, Indiana, USA

Keywords Internal auditing, Management stress, Stress

Abstract This study used the Ivancevich and Matteson Stress Diagnostic Survey to gather dataconcerning job stress for a large national sample of internal auditors in the USA. Surveyrespondents indicated that the organizational job stressors in their work environment were more asource of stress than the so-called individual job factors. Specifically, respondents would like to bepaid more and participate more in the decision-making processes relating to their jobs. Companypolitics and lack of training and development opportunities were other major sources of stress.Implications for the profession are clear. Internal audit managers should be aware of the job stressinherent in the nature of the work of an internal auditor and take appropriate steps to reduceorganizational job stressors rather than face the risk of increased staff job turnover.

IntroductionInternal auditing is considered a stressful occupation because the job is oftencharacterized by heavy workloads, many deadlines, and time pressures. Internalauditors are often under pressure to produce quality work, and yet may be underserious budget constraints to accomplish the work in less time (Brown andMendenhall, 1995). The work may also involve extensive business travel andfrequently changing work locations, which can further increase the job stress levels ofinternal auditors (Sears, 1992). In addition, continually dealing with auditees instressful situations may lead to mental and physical distress for the internal auditor(Chau, 1998). These working conditions may cause increased levels of job stress for theinternal auditor (Wood and Wilson, 1988).

High job stress has been proposed as one cause of internal auditor jobdissatisfaction (Gavin et al., 1985). The initial effects of job dissatisfaction may includeincreased absenteeism and/or psychological withdrawal. Later on, the end result ofhigh levels of job stress is often increased job turnover, which can have a negativeimpact on the efficiency, effectiveness, and staff morale of the internal auditdepartment. Therefore, it is important for internal audit managers and directors tobetter understand job stress and the negative impact excessive job stress may have ontheir internal audit staff.

This study used a well-known job stress questionnaire to gather data concerningjob stress for a large national sample of US internal auditors. The most troublesome jobstressors for internal auditors in this survey were the so-called “organizational” jobstressors, rather than the “individual” job stressors. These results provide new insightsregarding the aspects of the job that are causing the most job stress for internalauditors.

Internal auditorsInternal auditors are employees of an organization whose job is to review companyoperations to determine whether acceptable policies and procedures are followed,whether established standards are met, whether resources are used efficiently, and

The Emerald Research Register for this journal is available at The current issue and full text archive of this journal is available at

www.emeraldinsight.com/researchregister www.emeraldinsight.com/0268-6902.htm

Internal auditorsand job stress

1119

Managerial Auditing JournalVol. 19 No. 9, 2004

pp. 1119-1130q Emerald Group Publishing Limited

0268-6902DOI 10.1108/02686900410562768

whether the organization’s objectives are being achieved (Sawyer, 1988). This is a tallorder for any internal audit department. In the light of recent events such as the Enronand WorldCom debacles in the USA, the potential of the internal audit department tostrengthen internal controls, improve performance, and reduce the likelihood offraudulent activities has become more widely recognized. At the same time, internalaudit departments are often under pressure to keep their operating costs down. As aresult, the internal audit manager may try to accomplish more with less, with the endresult being increased job stress for their internal auditors.

StressThe stress response is a mobilization of the body’s natural energy resources whenconfronted with a stressor in his or her environment. A stressor may be defined as any“demand made by the internal or external environment that upsets a person’s balanceand for which restoration is needed” (Matteson, 1987, p. 33).

“Stress is necessary for a person’s growth, change, development, and performanceboth at work and at home” (Quick and Quick, 1984, p. 1), but how an individual willrespond to a particular stressor depends on a variety of individual factors. However,once an individual’s stress threshold is exceeded, stress symptoms will be experienced.

Stress can be considered as good stress or bad stress. Bad stress could result froman unpleasant situation such as losing one’s job. An example of good stress would be asituation that creates excitement, stimulation, and arousal for the individual. A jobpromotion might be an example of a positive, invigorating type of stressor. Any type ofstress puts a strain on the person. However, good stress results in a less negative effecton the person (Selye, 1976).

Three factors will determine whether a situation is placing sufficient demands on aperson to result in stress (Beehr and Bhagat, 1985). These three factors are importance,uncertainty, and duration. The more important the event is to the person, the greaterthe stress potential. Uncertainty refers to a lack of clarity about an outcome. The moreuncertainty in a situation, the more stressful the condition typically is for the person.Finally, duration is an important factor. The longer special demands are on a person,the more stressful the situation is for that person.

The individual symptoms of stress may be categorized into three types:physiological, psychological, and behavioral (Beehr and Newman, 1978).Physiological stress symptoms may be further divided into short term (such as aheadache), long term (such as ulcers, high blood pressure, or heart attack), andnon-specific (such as having an acid stomach). Psychological responses include suchsymptoms as apathy, forgetfulness, dissatisfaction, irritability, and dissatisfaction.Individual behavioral consequences of stress may include loss of appetite, weight gainor loss, change in smoking habits, change in use of alcohol, and sudden change inappearance.

Almost every system of the body is involved in the stress response (Everly andGirdano, 1980). However, the responses of the cardiovascular, digestive, and muscularsystems are the most pronounced. This response is recognized as the “fight or flight”response. No matter what the type of stressor, the body prepares to react in the sameway. It increases the blood supply to the heart and muscles, elevates the bloodpressure, and releases adrenaline into the system. The digestive system slows downdigestion and dumps sugar into the blood stream to serve as an immediate source of

MAJ19,9

1120

energy. The muscles tense up in order to be ready to spring into action. As stressincreases, a person’s “fight or flight” response occurs more frequently and may resultin a drain of the person’s energy reserves.

A person’s response to stressors will be somewhat mediated by various individualpersonality characteristics. Individual qualities affect how a person will respond tostress in three major ways (Schuler, 1980). First, because individual needs and valuesdefine the person’s desires, the individual qualities determine the relative importance ofevents or occurrences to the person. Second, individual abilities and past experiencesaffect the choice of strategies to deal with stressful events. Finally, the individual’schoice of strategies to deal with the stress is influenced by the individual’s personalitycharacteristics. Consequently, individuals will differ in the ways they respond to anidentical event depending on these individual qualities. Events that are very stressfulto one individual may not be stressful to another. Consequently, individuals vary in theamount of stress they can tolerate without showing signs of job-related tension(Ivancevich and Matteson, 1980).

To summarize, stress is a naturally occurring experience that may have eitherbeneficial or destructive consequences. Stress is a physical response, but the stressorsthat trigger the response are typically social, psychological, or symbolic, andconsequently require no physical action. Stress is so hard on the human body becausethe body is preparing for a physiological response to a non-physical demand. Thecumulative result is a major strain on a person’s body that can lead to illness. The morefrequently the person is in a stress-response mode, the more susceptible that individualis to fatigue, disease, disability, aging, and death (Matteson and Ivancevich, 1987).

Job stressJob stressors may refer to any characteristic of the workplace that poses a threat to theindividual. These job stressors can relate to either job demands a person cannot meetor the lack of sufficient resources to meet job needs (French and Caplan, 1972). Forstress to exist, the demand from the environment (the job) versus the capability of theindividual (the employee) will typically be considerably out of balance. Individualsexperience job stress when they have little or no control over their jobs or when workdemands exceed their abilities (Donovan and Kleiner, 1994). Job stress also occurswhen conditions on a job inhibit, stifle, or thwart the attainment of expectations andgoals.

Not all job stress is bad because a certain amount of job stress has been shown toimprove both effectiveness and performance (Brief et al., 1981). For example, apromotion is an opportunity and can be a challenging, exciting experience. However,mismanaged organizational stress can produce individual stresses and strains that aredetrimental both to the individual and to the organization. And because stress isadditive, the more stressors in the work environment, the higher the individual’soverall job stress level. Whether factors in the work environment will be perceived byindividuals as being stressful will depend on how the particular individual perceivesthe event, and this will vary from individual to individual. To summarize, too muchstress of any kind may lead to physical, psychological, and behavioral problems aswell as job dissatisfaction.

Internal auditorsand job stress

1121

Prior studiesStress among accountants has been studied extensively in the USA. Most of the earlystudies focused primarily on accountants in public accounting. (See Sorensen (1990) fora review.) In their study, Collins and Killough (1992) used the individual job stressorscale from the Ivancevich and Matteson (1983) Stress Diagnostic Survey (SDS) togather data concerning the various types of job stressors among a national sample ofUS public accountants. They reported that career progress, job scope, and roleambiguity were the job stressors most associated with job dissatisfaction and thepropensity to leave public accounting. Sanders et al. (1995) used the same SDSindividual scales in their study of job stress in public accounting and reported similarresults.

Gavin and Dileepan (2002) used both the organizational and individual job stressorscales from the SDS questionnaire in for their study of management accountants. Theyreported that rewards and human resource development were among the moststressful organizational stressors. The most stressful individual job stressors identifiedwere time pressure, quantitative overload, and career progress.

A few studies have focused on internal auditor job stress. Wilson and Wood (1989)conducted a major research project concerning the behavioral aspects of internalauditing for The Institute of Internal Auditors. As part of this study they identified rolestress as a major issue among internal auditors. Pei and Davis (1989) studied theimpact of organizational structure on internal auditor organizational-professionalconflict (OPC) and role stress. Their results indicated a direct positive relationshipbetween OPC and role stress.

Brown and Mendenhall (1995) investigated the stress involved with specificcomponents of the internal auditor’s job. They reported that high stress levels arerelated to time pressures, relationships with auditees and supervisors, and businesstravel. However, none of these studies of internal auditor job stress utilized theIvancevich and Matteson (1983) Stress Diagnostic Survey.

The studyData for this study were obtained by mailing a survey questionnaire to a nationalsample of 1,500 internal auditors who were members of the American Institute ofCertified Public Accountants. To encourage subjects to respond to the instrument, amodified Dillman (1978) approach was used. Desktop publishing software was used toproduce a professional-looking survey booklet, and all letters were personalized andhand-signed. A self-addressed, stamped envelope was included with the surveyinstrument. A small gift, a custom-designed “World Class Internal Auditor” bookmark,was enclosed with each booklet.

The SDS (Ivancevich and Matteson, 1983), a very comprehensive job stressquestionnaire by Ivancevich and Matteson, was used in this study. The majoradvantage of the SDS is that the instrument was designed to identify specific areas ofhigh job stress in a work environment, rather than merely provide an overall measureof job-related stress. In addition, it was specifically designed to be used withmanagerial and professional employees.

The SDS considers job stress to consist of 15 separate job stressors that may bedivided into two groups: individual stressors and organizational stressors. Individualjob stressors are factors that primarily relate to the individual himself and how he or

MAJ19,9

1122

she relates to the specific work on the job. The individual stressors are role conflict, roleambiguity, job scope, time pressure, career progress, responsibility for others,qualitative work overload, and quantitative work overload. Organizational stressorsare factors that relate primarily to the working environment and working conditionsthat the employee has to cope with. The seven organizational stressors are politics,rewards, participation, underutilization, supervisory style, organization structure, andhuman resource development. See Table I for a description of each job stressor.

When taking the SDS, subjects are asked to respond to 60 statements concerningtheir job. The respondents were asked to indicate the extent each of the 60 items is asource of job stress to him or her using a seven-point Likert scale. Responses rangefrom 1 (never a source of stress) to 7 (always a source of stress). For example, a jobstress question about rewards is: “People are not rewarded on the basis of solidperformance.” Separate scores are calculated for each of the 15 categories ofwork-related stressors.

At the end of the questionnaire was a set of demographic questions concerning age,gender, marital and family status, educational level, professional credentials, and jobtitle. Respondents were also asked to indicate how long they have been an internalauditor, the industry they worked in, and the number of internal auditors in theirorganization.

Demographic resultsOf the 1,500 persons who were mailed a survey, 683 usable responses were received,resulting in an overall response rate of 53 percent. Of the survey respondents, over 64percent (438) of the 683 respondents were men. (The sample as a whole consisted ofapproximately two-thirds men.) The average age was 37 years old, but respondentsranged in age from 22 to 69 years of age. The majority of respondents (71.9 percent)were married and about half (47.3 percent) reported that they were parents living withchildren under the age of 16. All but three respondents had earned at least a Bachelorsdegree, and 25.3 percent of the survey respondents had also earned a Masters degree.

The largest group (42.7 percent) of respondents was composed of internal auditmanagers and directors. The next largest group (30.3 percent) was composed of seniorauditors. Only 59 (8.7 percent) of the survey respondents were staff internal auditors.The largest percentage (76.2 percent) of survey respondents worked on small internalaudit staffs (defined as staffs composed of 15 or fewer internal auditors).

Respondents represented a wide range of industries. The largest industry group ofinternal auditors (180) represented banking and financial services. The next largestgroup (119) represented manufacturing. Survey respondents had worked in internalaudit an average of eight years.

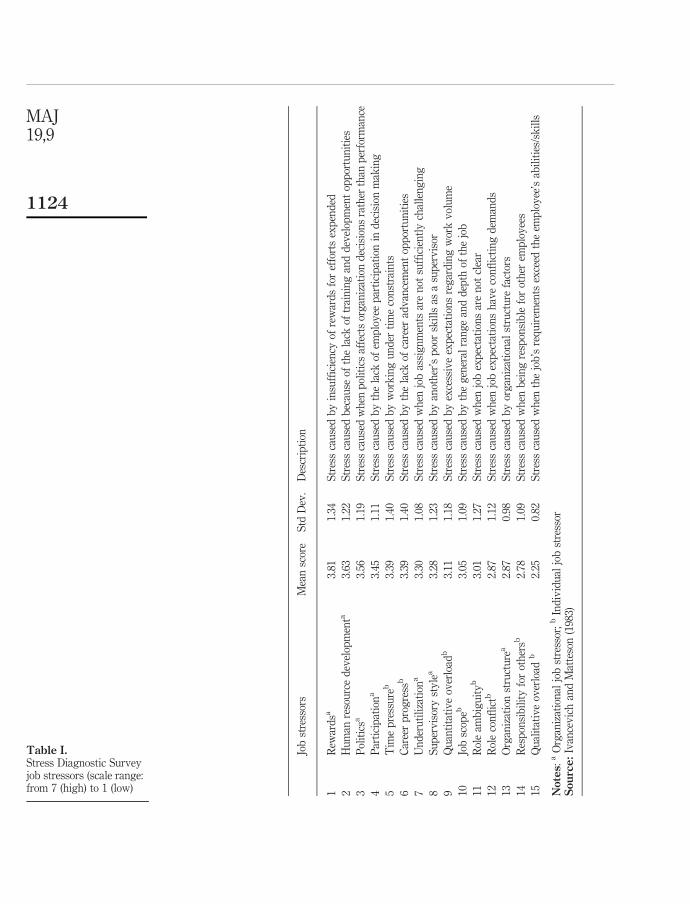

ResultsJob stress scores for each of the 15 job stress variables were calculated for eachrespondent by averaging the responses for the four questions related to that specificvariable. Table I displays the overall mean scores (and standard deviations) for eachvariable, with variables listed by mean score, from high to low. As Table I shows, themean scores for all respondents ranged from 3.81 down to 2.25 (on a seven point scalewith 7 being high and 1 being low).

Internal auditorsand job stress

1123

Jobstressors

Meanscore

Std

Dev.

Description

1Rew

ardsa

3.81

1.34

Stresscausedbyinsufficiency

ofrewardsforeffortsexpended

2Human

resourcedevelopmenta

3.63

1.22

Stresscausedbecause

ofthelack

oftraininganddevelopmentopportunities

3Politicsa

3.56

1.19

Stresscausedwhen

politicsaffectsorganizationdecisionsrather

than

perform

ance

4Participationa

3.45

1.11

Stresscausedbythelack

ofem

ployee

participationin

decisionmaking

5Tim

epressure

b3.39

1.40

Stresscausedbyworkingunder

timeconstraints

6Careerprogress

b3.39

1.40

Stresscausedbythelack

ofcareer

advancementopportunities

7Underutilization

a3.30

1.08

Stresscausedwhen

jobassignments

arenot

sufficientlychallenging

8Supervisorystylea

3.28

1.23

Stresscausedbyanother’spoorskillsas

asupervisor

9Quantitativeoverload

b3.11

1.18

Stresscausedbyexcessiveexpectationsregardingworkvolume

10Jobscopeb

3.05

1.09

Stresscausedbythegeneral

rangeanddepth

ofthejob

11Roleam

biguityb

3.01

1.27

Stresscausedwhen

jobexpectationsarenot

clear

12Roleconflictb

2.87

1.12

Stresscausedwhen

jobexpectationshaveconflictingdem

ands

13Organizationstructure

a2.87

0.98

Stresscausedbyorganizational

structure

factors

14Responsibilityforothersb

2.78

1.09

Stresscausedwhen

beingresponsibleforother

employees

15Qualitativeoverload

b2.25

0.82

Stresscausedwhen

thejob’srequirem

ents

exceed

theem

ployee’sabilities/skills

Notes:aOrganizational

jobstressor;bIndividual

jobstressor

Source:IvancevichandMatteson(1983)

Table I.Stress Diagnostic Surveyjob stressors (scale range:from 7 (high) to 1 (low)

MAJ19,9

1124

1. RewardsRewards stress (with a mean score of 3.81) was the top-ranking job stressor for internalauditors in this study. Employees, including internal auditors, expect to be rewardedfor their efforts in terms of salary and benefits. They become unhappy if they receivewhat they consider low financial rewards or if they perceive inequity in wages. Stressis created when rewards are not based on performance. A common problem is that ofpay compression, when the salaries of new hires come close to or even exceed thesalaries of existing employees. Other extrinsic rewards may include job security andpromotional opportunities. Workers also seek intrinsic rewards from their jobs. Theseintrinsic rewards include recognition, a sense of accomplishment, and beingappreciated for their efforts. Survey responses indicated that the lack of sufficientrewards was a serious job stress issue for internal auditors.

2. Human resource development stressThe second highest mean job stress score for internal auditors in this study was humanresource development. Human resource development, with a mean score of 3.63, refersto whether or not an organization provides opportunities for further training anddevelopment for its employees. A lack of training and development opportunities canbe stressful for professionals because they are very likely to become dissatisfied with ajob position that does not allow them to develop and grow professionally. Training canserve to energize employees by exposing them to new ideas and different ways ofperforming their job. Internal auditors want learning opportunities that enable them tokeep current in their profession and to improve technical expertise. The lack of suchopportunities increases the job stress of internal auditors.

3. PoliticsPolitics in the workplace was the third leading cause of job stress, with a mean score of3.56 for internal auditors in this study. Stress is created when politics rather thanperformance affect organizational decisions. Office politics can be profoundly stressfulfor professional and white-collar workers. A common problem is rivalry betweencolleagues. Political parlaying often results in many inefficiencies, rather than anatmosphere of teamwork that is conducive to organizational effectiveness. If workrelations are strained and co-workers are not supportive of each other, job stress tendsto escalate. Internal auditing is often a very politically charged job. In highly politicalorganizations the political forces and rivalries within the organization may makeworking there extremely stressful for an internal auditor.

4. Participation in decision makingLack of participation in decision making (with a mean score of 3.45) was the fourthleading cause of job stress for internal auditors in this study. Stress may be created ifmanagement is not receptive to ideas and suggestions from employees. Internalauditors find it stressful when they have little or no participation in thedecision-making process for their work. Employees desire a certain perceived senseof control over their work environment. Because of this, persons with greateropportunities for participation in decision making often report greater job satisfactionand lower job-related stress.

Internal auditorsand job stress

1125

5. Time pressureTime pressure, an individual job stressor with a mean score of 3.39 and a largestandard deviation, was tied for the fifth leading cause of job stress for internalauditors in this study. Time pressure stress refers to the extent to which unreasonabledeadlines and time demands are imposed. For example, a worker experiences timepressure stress when the employee has insufficient time to complete required tasks.

Internal auditors typically have to record how their time is spent in great detail.Therefore, deadlines that are too tight will result in time pressures, particularly whenthe ability to meet time demands is an important factor in performance evaluations.Some supervisors have been known to create artificial time pressures as a way of“motivating” their subordinates. However, with increased stress, performanceincreases only up to a certain point and then typically declines.

Survey respondents reported that they worked an average of 46 hours per week andspent an average of 39 nights a year out of town for work. As would be expected, theinternal auditors who were working the longest hours (the high overtime group) reportedan extremely high time pressure stress score (4.3 as compared to 2.7 for the no overtimegroup). When the respondents were grouped according to the volume of overnight travel,similar results were reported. The respondents in the high travel group reported a 3.8mean job stress score for time pressure as compared to 3.0 for the no travel group.

6. Career progressCareer progress (with a mean score of 3.39 and tied for fifth) was a relatively highsource of job stress for internal auditors. Career progress stress refers to how theindividual perceives the quality of his or her career development. In someorganizations, being in internal audit may put a person on the fast track tomanagement. In contrast, in other organizations internal audit is considered a “deadend” job. Because career progress stress will adversely affect a person’s jobsatisfaction, job turnover is likely to be high if an internal auditor can see no clearchannel for advancement.

Career progress concerns frequently arise for individuals in mid-career and maybecome sources of concern, anxiety, or frustration for the individual. Professionals mayfeel very disappointed when they find themselves at their “career ceiling”. Internalaudit supervisors as a group had the highest mean job stress scores on this item (3.75).In contrast, internal auditor directors and managers as a group reported much lowerjob stress levels on this item than did other respondents.

7. UnderutilizationUnderutilization stress (with a mean score of 3.30) occurs if job assignments are notpersonally challenging. Professionals have a large investment in their skills and trainingand want to be able to use them on the job. Being assigned tasks that do not challenge themis very stressful for professionals. Underutilization of abilities leads to job dissatisfaction,boredom, depression, and workload dissatisfaction and often leads to turnover. Supervisorsshould constructively challenge their subordinates whenever possible.

8. Supervisory styleStress may be created by poor supervision (with a mean score of 3.28). Lack ofmanagerial support and lack of feedback are very stressful for professional employees.

MAJ19,9

1126

Employees want a supervisor to be concerned about their personal welfare, to beaccessible, and to treat them with respect. Stress-producing supervisors include thosewho do not give criticism in a helpful way, those who play favorites with subordinatesand those who “pull rank” or who take advantage of their subordinates. Supervisorswho rule with an iron hand and rarely try out new ideas or allow participation indecision making may also cause serious stress problems for their subordinates. Asupervisor’s autocratic management style often results in high turnover, highabsenteeism, and low morale among their subordinates.

9. Quantitative overloadQuantitative overload stress (with a mean score of 3.11) occurs when an employee isassigned too great a volume of work to accomplish in a specified time frame.Quantitative overload is very prevalent in our achievement-oriented society and isassociated with job tension, job dissatisfaction, and various physical and psychologicalstrain symptoms. Whereas the stress of overload is unhealthy for the individual, heavyemployee workloads may be beneficial for the organization. This situation often resultsin conflicts between employees and employers over workloads. Surprisingly,quantitative overload was not a high cause of job stress for internal auditors whoresponded to this survey.

10. Job scopeJob scope stress (with a mean score of 3.05) relates to stress caused by the generalrange and depth of the job. It occurs when an individual perceives the job asunimportant or lacking in variety. Variety in the work environment enhances interestand challenge and has been reported as a key factor in employee job satisfaction. Jobscope stress has a number of other facets. Low job complexity has been identified as asource of job scope stress. Job scope stress may occur when an individual holding ademanding position receives little feedback, has limited latitude in decision making, orwhen a person’s job has a lack of responsibility. Job scope was a relatively low cause ofinternal auditor job stress in this study.

11. Role ambiguityJob ambiguity (with a mean score of 3.01) occurs when a job has unclear workobjectives or working procedures, confusing expectations, or a person receives a lack offeedback. It also occurs when an employee has inadequate information to perform hisrole. Role ambiguity is costly both for the employee and for the organization. Roleambiguity has been reported as being associated with lower job satisfaction andincreased job-related tension. Role ambiguity was not a major cause of source forinternal auditors in this study.

12. Role conflictRole conflict (with a mean score of 2.87) is created when an individual is presented withconflicting job demands such that compliance with one set of pressures makescompliance with another set difficult, objectionable, or impossible. The strength of therole conflict will depend on the strength of the role pressures. At times it may beimpossible for the demands of one role to be fulfilled without ignoring the demands of

Internal auditorsand job stress

1127

another role. Role conflict was a relatively low source of job stress for the internalauditors in this study.

13. Organization structureStress may be caused by organization structure factors (with a mean score of 2.87).Working in a large, hierarchical, bureaucratic organization where employees have littlecontrol over their jobs can be very stressful. Structural factors include administrativepolicies and procedures that restrict employee behavior. For example, arbitrary workplace rules may be a threat to an individual’s freedom, autonomy and identity. Anorganization structure with overly restrictive company policies and procedures is verystressful. Employees may not be kept informed concerning matters that directly affecttheir job or the organization as a whole. A lack of effective communication within anorganization, excessive red tape, and seemingly endless paperwork can be verystressful for employees, including internal auditors. Organization structure was not avery important source of job stress for internal auditors in this study.

14. Responsibility for othersResponsibility for others is often associated with significant job stress. The moreresponsibility for others that a person has, generally the greater the job stress. Thishappens because the individual is spending significant amounts of time interactingwith others, attending meetings, and trying to work with and motivate others to meetdeadlines and schedules. Responsibility for others can be particularly stressful formanagerial and professional workers. For the internal auditors in this study the meanscore was 2.78, which is relatively low in comparison to other stressors in the survey.

15. Qualitative overloadQualitative overload (with a mean score of 2.25) occurs when the work requires skills,abilities, and knowledge beyond what the person has. It occurs when employees feelthat they lack the ability to do the job regardless of the amount of time available tothem to complete the job. It may also result when performance standards are set sohigh as to appear unattainable. For internal auditors in this study, this potentialstressor had the lowest mean score. Therefore, qualitative overload does not appear tobe a major problem among the respondents to the study.

Discussion of results and conclusionOrganizational job stressors, including rewards, participation, politics, and careerdevelopment, were serious sources of job stress for the internal auditors in this study.These organizational job stressors were much more a source of job stress for internalauditors than the individual job stressors, such as time pressure and overload stress.The internal auditors in the survey would like to be paid more and participate more inthe decision-making processes relating to their jobs. They also find company politicsand lack of training and development opportunities a source of stress. Whereas theformer may not easily be resolved, the matter of increasing training and developmentopportunities could be. Lack of career progress opportunities for internal auditors whowish to leave internal auditing could be addressed by company managementdeveloping more career path opportunities for their internal auditors.

MAJ19,9

1128

Results of this study may be compared to two other studies of US accountants thatused the SDS instrument. Interestingly, the results of this internal auditor study werevery similar to the results reported by Gavin and Dileepan (2002) in their study ofmanagement accountants. In their study, reward and human resource developmentwere the top common organizational job stressors, and time pressure, quantitativeoverload and career progress were the leading common individual job stress variables.

Because the Collins and Killough (1992) study of job stress among publicaccountants did not administer the organizational portion of the SDS, only theindividual job stressors can be compared. Time pressure, the highest of the individualjob stressors for internal auditors in this study, was also the job stress variable withthe highest score for public accountants. However, as expected, the average timepressure stress score of the internal auditors in this study, 3.39, was considerably lowerthan the average score of 4.50 reported by Collins for the public accountants in herstudy. Also as expected, the career progress stress score average of 2.81 for publicaccountants was low when compared to scores of either internal auditors ormanagement accountants.

Implications for the profession are clear. Internal audit managers and directorsshould be aware of the job stress factors inherent in the nature of the work of aninternal auditor and take steps to reduce job stress for individuals who are showing theearly signs of job stress. For if the stress is allowed to progress, job dissatisfaction willlikely occur, and the individual will typically seek out a new job. Therefore it is in thebest interest of the organization to take appropriate steps to reduce job stress of itsinternal auditors rather than risk increased job turnover.

References

Beehr, T.A. and Bhagat, R.S. (1985), “Introduction to human stress and cognition inorganizations”, in Beehr, T.A. and Bhagat, R.S. (Eds), Human Stress and Cognition inOrganizations: An Integrated Perspective, John Wiley & Sons, New York, NY, pp. 3-19.

Beehr, T.A. and Newman, J.E. (1978), “Job stress, employee health, and organizationaleffectiveness: a facet analysis, model, and literature review”, Personnel Psychology, Vol. 31No. 4, pp. 665-99.

Brief, A.P., Schuler, R.S. and Van Sell, M. (1981),Managing Job Stress, Little Brown & Company,Boston, MA.

Brown, D. and Mendenhall, S. (1995), “Stress and components of the internal auditor’s job”,Internal Auditing, Vol. 10, Winter, pp. 31-9.

Chau, C.-T. (1998), “Career plateaux”, The Internal Auditor, Vol. 55, October, pp. 48-52.

Collins, K.M. and Killough, L.N. (1992), “An empirical examination of stress in publicaccounting”, Accounting, Organizations & Society, Vol. 17 No. 6, pp. 535-47.

Dillman, D.A. (1978), Mail and Telephone Surveys, John Wiley & Sons, New York, NY.

Donovan, S.B. and Kleiner, B.H. (1994), “Effective stress management”, Managerial AuditingJournal, Vol. 9 No. 6, pp. 31-4.

Everly, G.S. Jr and Girdano, D.A. (1980), The Stress Mess Solution: The Causes and Cures ofStress on the Job, Brady Company, Bowie, MD.

French, J.R.P. Jr and Caplan, R.D. (1972), “Organizational stress and individual strain”, TheFailure of Success, AMACOM, New York, NY.

Internal auditorsand job stress

1129

Gavin, T.A. and Dileepan, P. (2002), “Stress!!! Analyzing the culprits and prescribing a cure”,Strategic Finance, Vol. 4 No. 5, pp. 50-5.

Gavin, T., Hammer, E. and Taylor, L. (1985), “Job satisfaction of internal auditors”, InternalAuditing, Vol. 1, Fall, pp. 64-73.

Ivancevich, J.M. and Matteson, M.T. (1980), Stress and Work: A Managerial Perspective, Scott,Foresman and Company, Glenview, IL.

Ivancevich, J.M. and Matteson, M.T. (1983), Stress Diagnostic Survey, University of Houston,Houston, TX.

Matteson, M.T. and Ivancevich, J.M. (1987), Controlling Work Stress, Jossey-Bass, San Francisco,CA.

Pei, B.K.W. and Davis, F.G. (1989), “The impact of organizational structure on internal auditororganizational-professional conflict and role stress: an exploration of linkages”, Auditing:A Journal of Practice & Theory, Vol. 8 No. 2, pp. 101-15.

Quick, J.C. and Quick, J.D. (1984), Organizational Stress and Preventive Management,McGraw-Hill, New York, NY.

Sanders, J.C., Fulks, D.L. and Knoblett, J.K. (1995), “Stress and stress management in publicaccounting”, The CPA Journal, Vol. 65, August, pp. 46-9.

Sawyer, L.B. (1988), Sawyer’s Internal Auditing, The Institute of Internal Auditors, AltamonteSprings, FL.

Schuler, R.S. (1980), “Definition and conceptualization of stress in organizations”, OrganizationalBehavior & Human Performance, Vol. 25 No. 2, pp. 184-215.

Sears, B.P. (1992), “Travel trauma”, Internal Auditor, Vol. 49, June, pp. 53-8.

Selye, H. (1976), The Stress of Life, revised ed., McGraw-Hill, New York, NY.

Sorensen, J.E. (1990), “The behavioral study of accountants: a new school of behavioral researchin accounting”, Managerial and Decision Economics, Vol. 11 No. 5, pp. 327-48.

Wilson, J.A. and Wood, D.J. (1989), Roles and Relationships in Internal Auditing, The Institute ofInternal Auditors, Inc., Altamonte Springs, FL.

Wood, D.J. and Wilson, J.A. (1988), “Stress and coping strategies in internal auditing”,Managerial Auditing Journal, Vol. 3 No. 2, pp. 8-16.

Further reading

McGrath, J.E. (1976), “Stress and behavior in organizations”, in Dunnette, M.D. (Ed.), Handbookof Industrial and Organizational Psychology, Vol. 1, Rand McNally College PublishingCompany, Chicago, IL, pp. 1351-95.

MAJ19,9

1130