intermediate financial accounting i inventories: measurement

TRANSCRIPT

Intermediate Financial Accounting I

Inventories: Measurement

Inventories: Measurement 2

Objectives of this Chapter1. Discuss the importance of inventory

valuation.

2. Study perpetual and periodic inventory systems and the ending period adjustments for inventory.

3. Study and compare the inventory cost flow assumptions.

4. Explain the effect of LIFO liquidations.

Inventories: Measurement 3

Objectives of this Chapter (contd.)5. Identify the items that should be

included in the inventory count.

6. Discuss the lower of cost or market (LCM) rule.

7. Study the accounting treatment of changing to LIFO cost flow assumption and the use of LIFO reserve account.

8. LIFO Inventory Pools

9. Dollar-value LIFO technique.

Inventories: Measurement 4

1. Inventories: the Importance of Inventory Valuation

How would the valuation and cost flow assumptions of inventory affect the income measurement? Valuation Methods: Historical Cost, Current

Exist Value, Current Entry Value, Present Value, LCM.

Cost Flow Assumptions: LIFO, FIFO, Average, Specific Identification.

CGS = Beginning Inventory + Net Purchase - Ending Inventory

Inventories: Measurement 5

Inventories: the Importance of Inventory Valuation (contd.)

Different valuation methods and different cost flow assumptions will result in different cost of ending inventories and therefore different cost of goods sold.

Inventories: Measurement 6

The Impact of Valuation of Ending Inventory on The CGS & IncomeYear 1 Income CGS = Beg. Inv. + Net Pur. - End. Inv.

under over under a

over under over b

Year 2 over under underunder over over

a. either understating the units or the valueb. either overstating the units or the value

Inventories: Measurement 7

Impact on Omitting Goods from Purchases

CGS = Beg. Inventory + N.P. - End. Inventory

B/S I/SEnding Inv. understated Purchase understatedR/E no effect CGS no effectA/P under N/I no effectWorking Capital no effect Inventory (End.) understatedCurrent Ratio overstatinga

a. When CA > CL

Inventories: Measurement 8

Defining Inventory

1. Assets held for resale purpose in a normal course of business

2. Assets used to produce products for resale purpose Merchandising Firms: Inventories Manufacturing Firms: Raw materials

Work-in-processFinished goods

Presentation of Inventory for Merchandising and Manufacturing Companies (Illustration 8-1, KWW, 14th e)

Inventories: Measurement 9

Inventory Cost Flow (Illustration 8-3, KWW, 14th e)

Inventories: Measurement 10

Inventories: Measurement 11

How to Determine Inventory Value Presented on the Balance Sheet? Applying either the periodic inventory

system or the perpetual inventory system and select a cost flow assumption to determine the value of inventories.

Both inventory systems require a physical count of inventory at the end of a period to determine the units which can be included in the inventory account.

Inventories: Measurement 12

2. Inventory Systems and Ending Period Adjustments

Types of Inventory Systems

A. Perpetual Inventory System

B. Periodic Inventory System

Comparing Perpetual and Periodic Systems (Source: KWW, 14th e, p438) Assuming that Fesmire Company had the

following transactions during the current year:

Inventories: Measurement 13

Inventory Units Unit Cost Total

Beginning Inv. 100 $6 $600

Purchases 900 $6 $5,400

Sales 600 $12 $7,200

Ending Inventory

400 $6 $2,400

Comparative Entries- Perpetual vs. Periodic (Illustration 8-4, KWW, 14th e)

Inventories: Measurement 14

Inventories: Measurement 15

Perpetual Systems – Cost of Goods Sold and the Ending Inventory

Since the inventory and the cost of goods sold (CGS) accounts are updated with all purchases and sales transactions, the balances of these two accounts are known at all time.

The CGS is determined by selecting a cost flow assumption.

Perpetual Systems – Cost of Goods Sold and the Ending Inventory (contd.)

Physical inventory count is still needed at the end of a period to determine whether inventory loss occurred.

A write down is required in the case of inventory loss.

Inventories: Measurement 16

Periodic Inventory System – the Ending Inventory and the Cost of Goods Sold

For the periodic system, the inventory balance is only determined at the end of a period after an inventory count and applying a cost flow assumption.

The cost of goods sold (CGS)is derived as: CGS = Beg. Inv. + Net purchases – cost of ending inventory

Inventories: Measurement 17

Inventory Cost Flow Assumptions

Fist-In, First-Out (FIFO) Last-In, First-Out (LIFO) Weighted-Average Cost (W-A) Specific Identification

Inventories: Measurement 18

Inventories: Measurement 19

Perpetual Inventory System - AnExample

Date Purchase Sell FIFOBalance

LIFOW-A

3/1 (Beg. Bal.) 100 $5 100 $5 100 $5

3/5 150 $6100 $5 150 $6

100 $5 150 $6

250 $5.6

3/7 200a 50 $6 50 $5 50 $5.6

3/14 100 $750 $6

100 $750 $5

100 $7150 $6.53

3/28 30b 20 $6 100 $7

50 $5 70 $7

120 $6.53

a. Sales price is $10 per unit. b. Sales price is $11 per unit.c.LIFO is not permiitted under IFRS

Inventories: Measurement 20

Example (contd.) - Journal Entries (Perpetual vs. Periodic)

3/5 Inventory 900 3/5 Purchases 900Cash 900 Cash 900

3/7 Cash 2,000 3/7 Cash 2,000Sales Rev. 2,000 Sales Rev. 2,000

CGS 1,100Inventory 1,100

3/14 Inventory 700 3/14 Purchases 700Cash 700 Cash 700

3/28 Cash 330 Cash 330Sales Rev. 330 Sales Rev. 330

CGS 180Inventory 180

Perpetual (FIFO) Periodic

Inventories: Measurement 21

Perpetual Inventory System Example (contd.)

Inventory (WA)

500 1120900 195.9700784.1

Inventory a (FIFO)

B.B.500 1100900 180700

E.B.820

Inventory (LIFO)

500 1150900 210700740

a. The balance of inventory is known at all time under the perpetual inventory system.

Inventories: Measurement 22

Perpetual Inventory System Example (contd.)

CGS (W-A)

1120 195.91315.9

CGS (FIFO)

3/7...11003/28...180

1280

CGS(LIFO)

1150 2101360

The balance of cost of goods sold account1 :

1.The balance of inventory is known at all time under the perpetual inventory system.

Inventories: Measurement 23

Ending Period Adjustments Perpetual Inventory System

a. Adjustments for lost units.

b. Adjustments for LCM valuation.

Inventories: Measurement 24

a. Adjustments for Lost Units (Perpetual Inventory System)

Assuming ending units = 110 units.On 3/31, the lost units = 10.Cost of 10 lost units => $6 x 10 = $60 (FIFO)

$7 x 10 = $70 (LIFO)$6.53 x 10 = 65.3 (W-A)

Adjusting Entry:3/31 Loss on Inventory Units a 60

Inventory 60

a. or use the account of Inventory over and short

Inventories: Measurement 25

b. Adjustments for LCM Valuation (Perpetual Inventory System)

Inventory (FIFO)B.B 500 1,100 900 180 700 820 60 -- 3/31 (Adj. for lost

units) 760

LCM=$600

Ending Inv. Cost (on 3/31, FIFO) = $760 Assuming market price = $600 LCM = $600

Inventories: Measurement 26

Adjustments for LCM Valuation (contd.)

Adjusting entry => Given that Allowance for Declining in Market Value of inventory has a beginning balance of zero:

Allowance 3/31 0 -- 3/1 Loss Due to Market Value

160 Decline of Inventory 160160 -- 3/31 Allowance to Reduce

Inventory to Market 160B/S (3/31) Inventory 760Allowance (160) Inv. At LCM 600

Inventories: Measurement 27

Adjustments for LCM Valuation (contd.)

If the allowance account had a beginning balance of $20, the adjusting entry would be:

Allowance20 -- 3/1 Loss 140140 Allowance 140160 -- 3/31

Inventories: Measurement 28

Adjustments for LCM Valuation (contd.)

If the Allowance account had a beginning balance of 200, the adjusting entry would be:

Allowance Allowance 40 40 200 Gain from Recovery

160 of M.V. of Inventory40

Inventories: Measurement 29

Periodic Inventory System At the end of an accounting period, the

following steps must be followed to determine the cost of ending inventory and cost of goods sold:1. Do an inventory count.

2. Applying a cost flow assumption to determine the cost of ending inventory.

3. Determine the cost of goods sold using: CGS = Beg. Inv. + Net Pur. - Ending Inv.a

a. No adjusting entries are required.

Inventories: Measurement 30

Periodic Inventory Systema : An Example

Using the example on Page 10 and assuming the physical count of inventory indicates 105 units on hand on 3/31, the cost of ending inventory (105 units) would be (given a FIFO cost flow assumption):

$7 100 + $6 5 = $730

a. For journal entries, see page 20.

Inventories: Measurement 31

Periodic Inventory System Example (contd.)

Inventory Data:

UnitsCost3/1 (B.B) 100 $53/5 Pur. 150 $63/14 Pur. 100 $7

The CGS under FIFO is:$500 + 1,600 - 730 = $1,370.

If a LIFO assumption is used, the cost of end. Inv. is: $5 x 100 + $6 x 5 = $530.

The CGS is: $500 + 1600 - 530 = $1,570.

Inventories: Measurement 32

Ending Period Adjustments (Periodic Inventory System)

1. No adjustment is needed for lost units (because the cost of lost units is embedded in the CGS).

Inventories: Measurement 33

Ending Period Adjustments (Periodic Inventory System)

2.Adjustment for the LCM valuation assuming FIFO: Cost of E.I. = $730 LCM AllowanceMarket = $600 = $600 0 --

3/1(assumed) 130

130 --3/31Adjusting entry:

Loss Due to Market Decline of Inv. 130Allowance to Reduce Inv. to Market

130

An Alternative of LCM Adjustment

Many companies (i.e., Cisco Systems, inc. 2001, source: Spiceland, etc.)record the adjustment of LCM as follows:

Cost of Goods Sold 160

Inventory 160 Note: Recording the loss as an increase in CGS will

have the same impact on earnings as reporting it as a loss from value decline in the holding inventory. However, this treatment will distort the cost of goods sold and therefore, the gross profit..

Inventories: Measurement 34

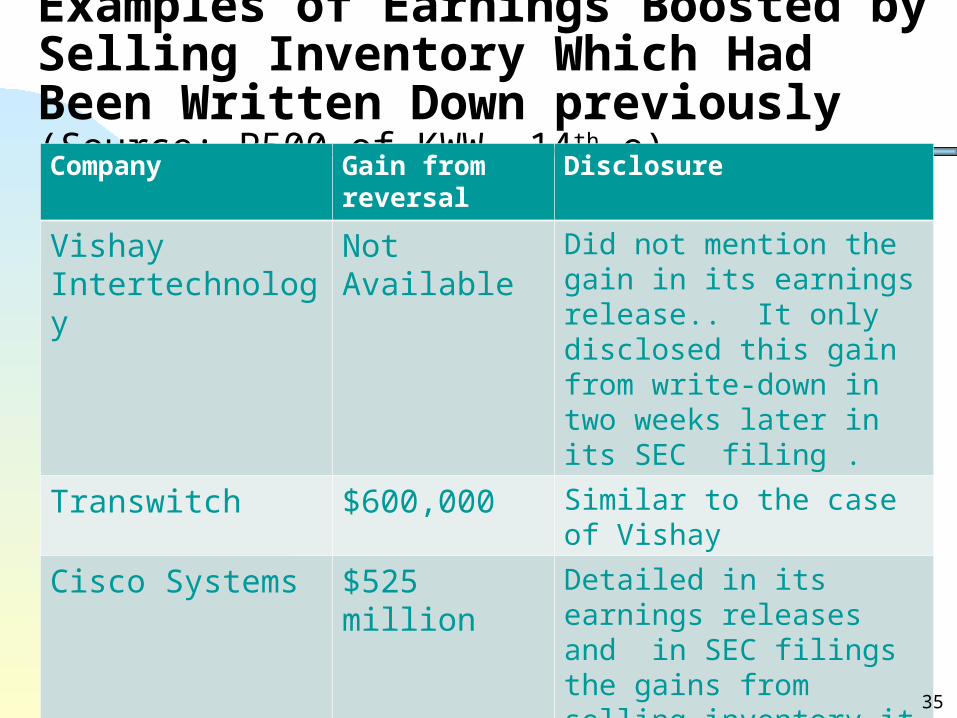

Examples of Earnings Boosted by Selling Inventory Which Had Been Written Down previously (Source: P500 of KWW, 14th e)Company Gain from

reversalDisclosure

Vishay Intertechnology

Not Available Did not mention the gain in its earnings release.. It only disclosed this gain from write-down in two weeks later in its SEC filing .

Transwitch $600,000 Similar to the case of Vishay

Cisco Systems $525 million Detailed in its earnings releases and in SEC filings the gains from selling inventory it had previously written off.

35

Inventories: Measurement 36

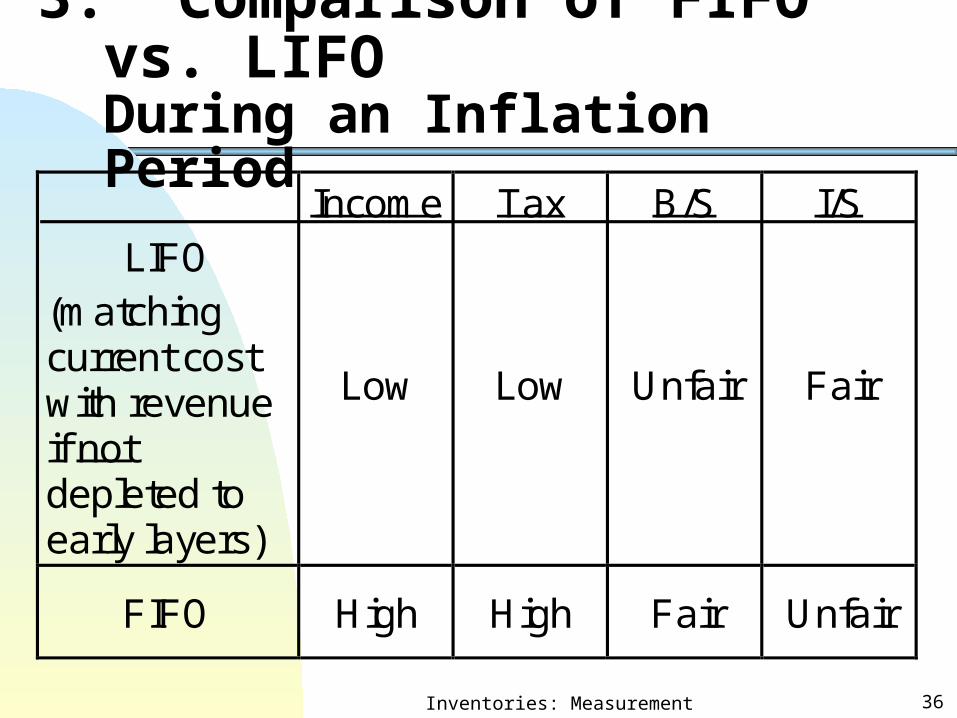

3. Comparison of FIFO vs. LIFODuring an Inflation Period

LIFO(matchingcurrent costwith revenueif notdepleted toearly layers)

Income

Low

Tax

Low

B/S

Unfair

I/S

Fair

FIFO High High Fair Unfair

Inventories: Measurement 37

Survey: (Source: Accounting Trends & Techniques and footnote 16 of Chapter 8 , KWW 14th e) a, b,c

Yearl Total LIFO FIFO W-A Others1984 1061 408 38% 366 30% 225 22% 52 5%

1988 1038 379 37% 396 38% 213 21% 50 5%

1991 1032 361 35% 421 41% 200 19% 50 5%

2000 887

283 32% 386 44% 180 20% 38 4%

2006 802 228 28% 385 48% 159 20% 30 4%

2010 666 176 26% 325 49% 147 22% 18 3%

Inventories: Measurement 38

Survey: (Source: Accounting Trends & Techniques) (contd.)a. Sample firms are 600 firms. Most

companies adopt more than one inventory method.

b. Due to low inflation, the number of firms adopting LIFO has declined since mid-1980s.

c. IAS No. 2 does not permit LIFO, and therefore, multinational companies use LIFO for all or most of their domestic inventories while use FIFO or average cost for their foreign subsidiaies.

Inventories: Measurement 39

Switching to LIFODuring an Inflation Period

Reason of switching to LIFO:

Tax savings.

Inventories: Measurement 40

Income Manipulation When LIFO Is Used (assuming price is rising)

1. To increase income (by decreasing CGS): Strategy:

2.To decrease income (by increasing CGS):

Strategy:

Inventories: Measurement 41

Advantages of FIFO

a. Less likely to be subject to management manipulation;

b. Produce higher income during an inflation period;

c. Inventory cost reported on the B/S is close to the replacement cost.

Inventories: Measurement 42

Disadvantage of FIFO

a. Bad matches of sales revenue and CGS; match current sales revenue with old costs;

b. Producing higher income during an inflation period results in paying more income tax.

Inventories: Measurement 43

Advantages of LIFO

a. Good match of sales revenue with CGS.

b. Produce lower income during an inflation period; result in tax savings.

Inventories: Measurement 44

Disadvantages of LIFO

a. Inventory cost presented on the B/S is not fair.

b. Subject to management manipulation.

Note: International Accounting Standard No. 2 does not allow LIFO.

Inventories: Measurement 45

IRS

1. Does not allow firms to use LCM if firms are using LIFO.

2. LIFO conformity rule.The non-LIFO income numbers are allowed on the supplementary reports since 1981.

Inventories: Measurement 46

IRS (contd.)

3. LIFO is not acceptable by the IRS till 1939.

Inventories: Measurement 47

4. LIFO Liquidations

A LIFO Liquidation profit can occur when units purchased are less than units sold in the period.

Inventories: Measurement 48

An Example of LIFO Liquidation Profit

20x5 Beg. Inv. 400 $5 Pur. 300 $6 Pur. 500 $7 Pur. 600 $8

During 20x5, 1,700 units were sold. What is the LIFO liquidation profit?

Total purchases of 20x5 are 1,400 units. The LIFO liquidationprofit is:(1,700-1,400) x ($8-$5) = $900

Inventories: Measurement 49

Choice of Inventory Cost-Flow Assumptions and Conversion of FIFO to LIFO for Comparison Purposes*

a. Choice of inventory cost-flow assumptions.

b. Inventory Management (JIT system, Inventory turnover rate, etc.): the example of Dell Inc.

c. Adjustment of inventory cost-flow assumption on the same basis before making comparison of financial statements.

Inventories: Measurement 50

Adjustment of Inventory Cost-Flow Assumption – An Example Information: ABC is currently adopting

FIFO assumption. IF LIFO were adopted, thecost of ending inventory would be $1,000 and $3,000 lower for x1 and x2, respectively.

Question: How much would the CGS and income be different when LIFO is adopted rather than FIFO for x2?

Inventories: Measurement 51

Adjustment of Inventory Cost-Flow Assumption- An Example (contd.)CGS = Beg. Inv. + Net Pur. – End. Inv.

Impact => -1000 -3000

of LIFO Thus, the CGS of x 2 should be increased by

$2,000 when adopting LIFO rather than FIFO.

The income before tax would be decreased by $2,000.

Inventories: Measurement 52

LIFO Reserve: An Account to Adjust Ending Inventory Value from FIFO to LIFO The difference in the inventory between

the inventory method used for internal (i.e., FIFO) vs. external (i.e., LIFO) reporting purposes is referred to as LIFO Reserve or the Allowance to Reduce Inventory to LIFO .

The change in the balance of LIFO Reserve from one period to another is referred as the LIFO Effect , an impact on income.

Inventories: Measurement 53

LIFO Reserve – An Example

Assume that Acme Boot Company uses FIFO method for internal reporting purposes and a LIFO for external reporting purposes.

On 12/31/x5, the LIFO Reserve balance is $20,000 and the value of ending inventory on 12/31/x6 under LIFO is $50,000 less than that of FIFO.

Inventory on 12/31/x5 at FIFO = $320,000 Inventory on 12/31/x6 at FIFO =$360,000

Inventories: Measurement 54

LIFO Reserve – Example (contd.)

(Inventory Disclosure, note D)12/31/x6 12/31/x5

Inventory at FIFO $360,000 $320,000 LIFO Reserve (50,000) (20,000) Inventory at LIFO $310,000 $300,000 Thus, $30,000 should be added to the LIFO

Reserve account. The LIFO effect (i.e., the impact on income) for 20x6 is $30,000.

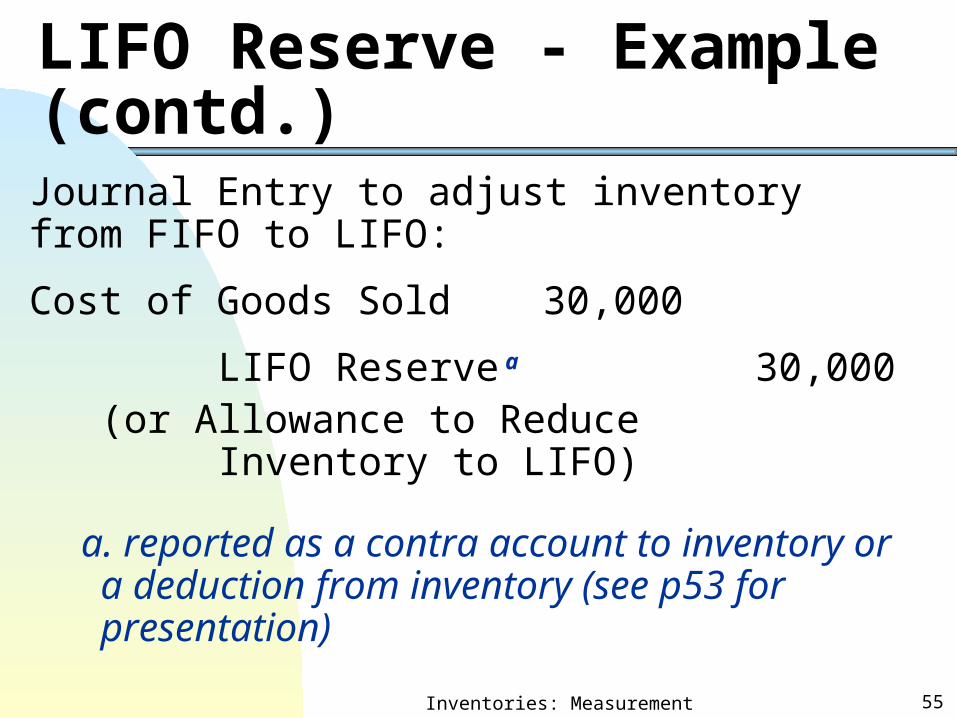

Inventories: Measurement 55

LIFO Reserve - Example (contd.)

Journal Entry to adjust inventory from FIFO to LIFO:

Cost of Goods Sold 30,000

LIFO Reserve a 30,000(or Allowance to Reduce Inventory to LIFO)

a. reported as a contra account to inventory or a deduction from inventory (see p53 for presentation)

Inventories: Measurement 56

Inventory Presentation and Footnote Disclosure (also see Illustration 8-19 of KWW, 14th e)

12/31/x6: Inventories, net of adjustment to LIFO Reserve (Note D) $310,000

Note D (contd.): Inventories. Inventories are valued at the lower of cost or market determined principally by the LIFO method. If the FIFO cost method had been used, inventories would have been $50,000 higher.

Illustration 8-19 (KWW, 14th e)

Inventories: Measurement 57

Inventories: Measurement 58

5. Items to Be Included in Inventory

Any goods with the legal title transferred to the buyer should be included in the inventory of the buyer (including goods in transit with a F.O.B. shipping point term).

Inventories: Measurement 59

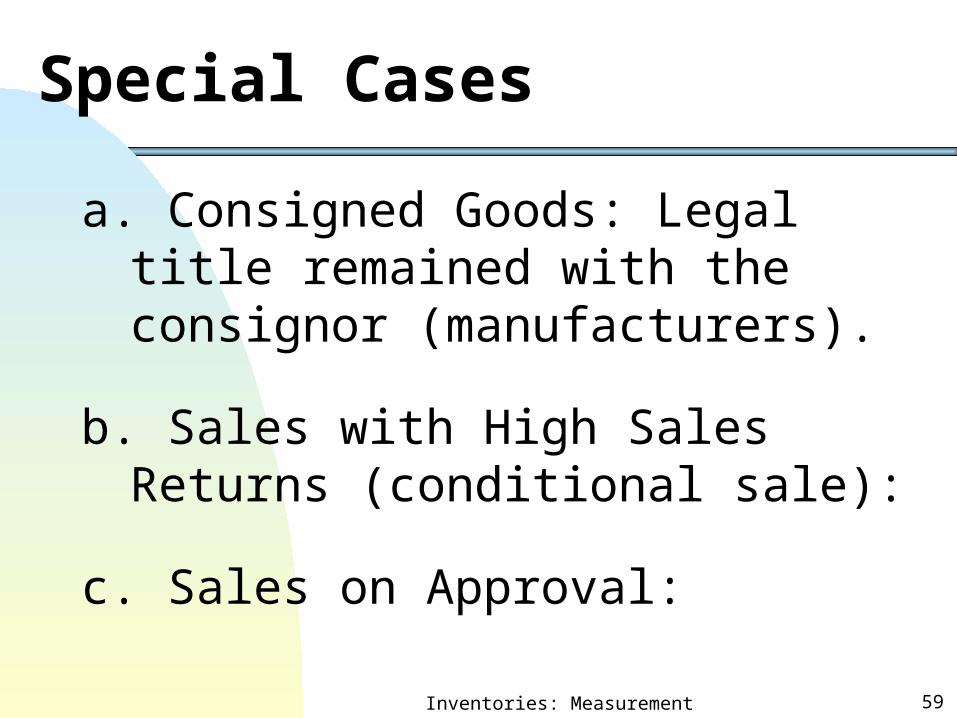

Special Cases

a. Consigned Goods: Legal title remained with the consignor (manufacturers).

b. Sales with High Sales Returns (conditional sale):

c. Sales on Approval:

Inventories: Measurement 60

Special Cases (contd.)

d. Product Financing Arrangements: Parking Transactions; sales with buyback agreements.

e. Sales on Installment (revenue recognition on accrual basis if uncollectible amounts can be estimated)

Inventories: Measurement 61

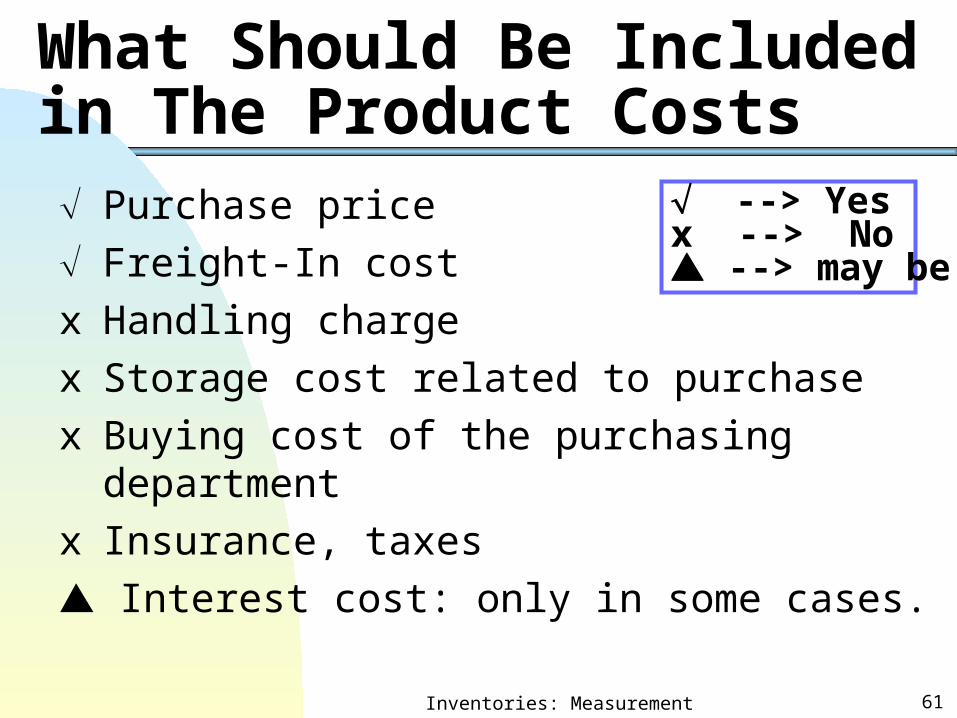

What Should Be Included in The Product Costs

Purchase price

Freight-In cost

x Handling charge

x Storage cost related to purchase

x Buying cost of the purchasing department

x Insurance, taxes

Interest cost: only in some cases.

--> Yesx --> No --> may be

Inventories: Measurement 62

What Should Be Included in the Product Costs (contd.) Purchase Discount account should be

treated as a contra account to purchases.

Inventories: Measurement 63

6. Inventory Valuation - the LCM Rule

Departure from Historical Cost AssumptionLCM: Lower of Cost or Market.

Reasons: Conservatism.

Market ==> Replacement Cost constrained by:Ceiling => Net Realizable Value

= Selling price - estimated cost to complete and sellFloor => NRV - normal profits

IFRS: Market is the NRV.

Inventories: Measurement 64

Inventory Valuation - Example

Selling price = 12

Package cost = $1

Transportation cost = $3

Normal profits = $3

NRV = Selling price - Package - Transportation = $12 - $1- $3 = $8

NRV - Normal profit = $5

Inventories: Measurement 65

Inventory Valuation - Example (contd.)

a.Example of the ceiling can prevent future unexpected loss.

b.Example of preventing the recognition of abnormal loss in the current period.

Acquisition Cost

Replacement

CostNRV

NRV - Profit

Market LCM

$10 $6 $8 $5 $6 $6a$10 $9 $8 $5 $8 $8b$10 $4 $8 $5 $5 $5$10 $12 $8 $5 $8 $8

Inventories: Measurement 66

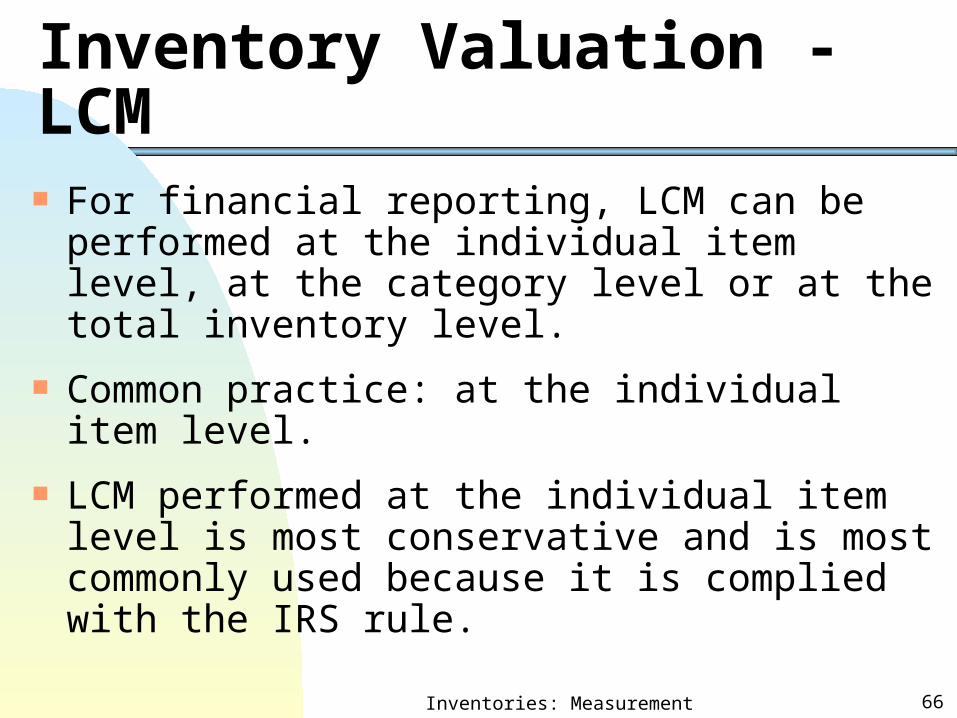

Inventory Valuation - LCM

For financial reporting, LCM can be performed at the individual item level, at the category level or at the total inventory level.

Common practice: at the individual item level.

LCM performed at the individual item level is most conservative and is most commonly used because it is complied with the IRS rule.

Inventories: Measurement 67

LCM Application - at Individual Level versus at Group Level

Item Cost Market LCM (at individual level)

A $50 $60 $50B* $140 $100 $100C $300 $360 $300Total $490 $520 $450_____ _____ __________ _____ _____

LCM at group level ==> $490

The difference of $40 is resulting from item B: $140 - 100 = $40

LCM and iGAAP

IAS No. 2 requires inventory to be valued at LCM which can be applied at different levels of inventory as in GAAP.

The market value of IAS is the NRV, not the replacement cost as in US GAAP.

IAS allows the reversal of inventory write-down when the conditions for write-down do not exist.

US GAAP does not allow the reversal of inventory write-down.

Inventories: Measurement 68

Inventories: Measurement 69

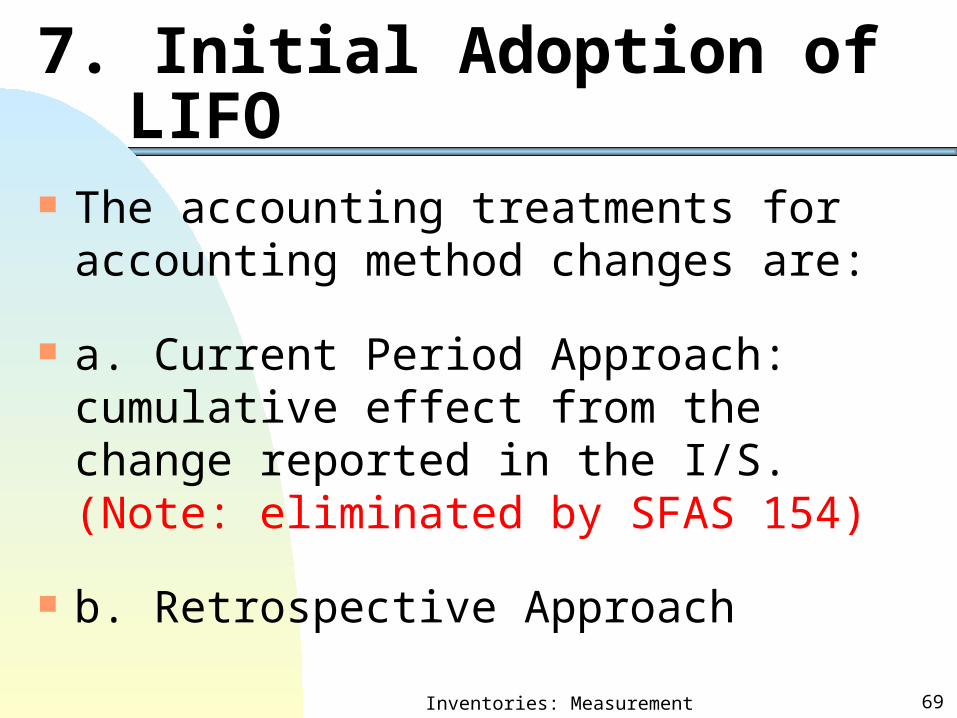

7. Initial Adoption of LIFO

The accounting treatments for accounting method changes are:

a. Current Period Approach: cumulative effect from the change reported in the I/S. (Note: eliminated by SFAS 154)

b. Retrospective Approach

Inventories: Measurement 70

Initial Adoption of LIFO

When change from other method to LIFO, neither a cumulative effect nor a retrospective adjustment can be made.

The base year inventory for all following years is the beginning inventory of the year In which LIFO is adopted.

Inventories: Measurement 71

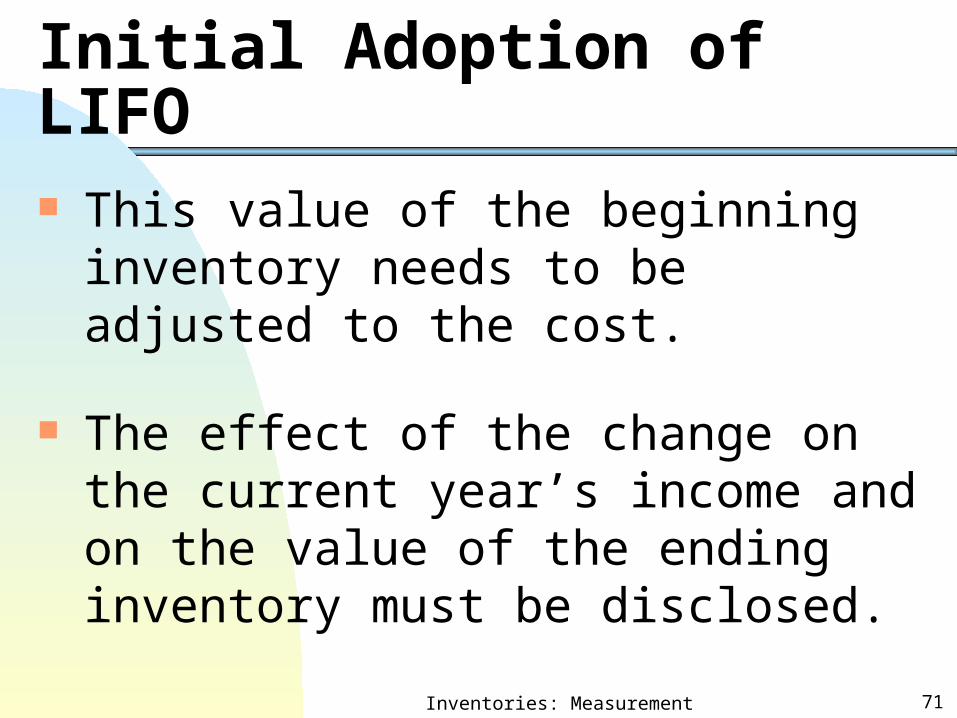

Initial Adoption of LIFO

This value of the beginning inventory needs to be adjusted to the cost.

The effect of the change on the current year’s income and on the value of the ending inventory must be disclosed.

Inventories: Measurement 72

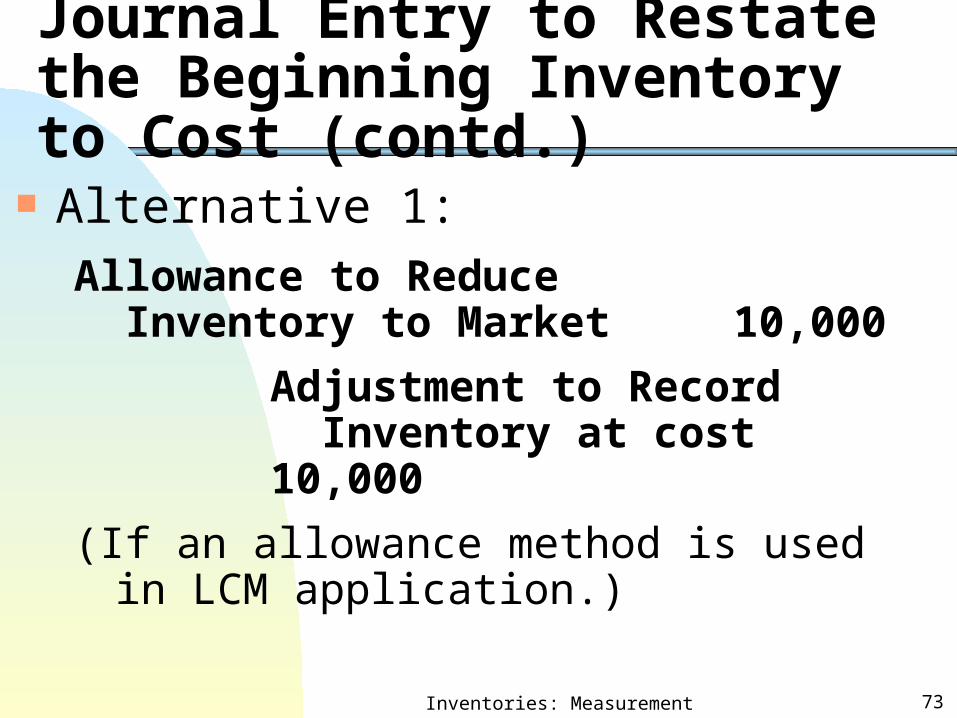

Journal Entry to Restate the Beginning Inventory to Cost Assume that Rooms, Inc. decided to

switch from FIFO to LIFO in 20x9. The beginning inventory of 20x9 has a cost basis of $100,000 but is reported at $90,000 on the balance sheet because market is lower than cost. The following entry is made to restate the inventory to a cost basis (ignoring tax effects):

Inventories: Measurement 73

Journal Entry to Restate the Beginning Inventory to Cost (contd.)

Alternative 1:

Allowance to Reduce Inventory to Market 10,000

Adjustment to Record Inventory at cost 10,000

(If an allowance method is used in LCM application.)

Inventories: Measurement 74

Journal Entry to Restate the Beginning Inventory to Cost (contd.)

Alternative 2:

Inventory 10,000

Adjustment to Record Inv. at Cost10,000

(only If a direct write-off method is used in LCM application)

Inventories: Measurement 75

Footnote Disclosure of Changing from FIFO to LIFONote: Inventory Pricing. In the fourth quarter, the

company expanded its use of the LIFO method of inventory to additional portion of its inventories in order to more closely match current costs with current revenues. The effect of this change was to reduce net income for the current year by $2,804,000 or $0.49 per share. As of December 31, inventories valued on a LIFO basis amounted to $74,166,000. If valued on a FIFO basis, such inventories would be increased to $90,551,000.

Inventories: Measurement 76

8. LIFO Inventory Pools (Specific Goods Pooled LIFO) (source: Spiceland, etc.)*

Problems associated with the Unit LIFO (i.e., the LIFO concept applies to units of inventory as described in previous sections; also called specific goods LIFO):

Costly to implement: It requires the records of each unit of inventory.

LIFO liquidations: When units of a specific inventory purchased are less than units sold during the period, the beginning layers are eroded.

Inventories: Measurement 77

LIFO Inventory Pools (contd.)*

LIFO inventory pools technique can: 1) simplify recordkeeping by grouping

inventory into pools, and 2)reduce the probability of LIFO layer

liquidation/erosion.

Inventories: Measurement 78

LIFO Inventory Pools (contd.) Within pools, all purchases of goods in the

pool are considered to be made at the same time during the period and at the average cost.

When the quantity of ending inventory in the pool increases (i.e., the quantity of ending inv. is greater than that of the beg. Inv.), the ending inventory of the pool will consist of the beg. Inv. and the layer of the period.

Inventories: Measurement 79

LIFO Inventory Pools: An Example (contd.) (skip 78-81) The 2008 beg. inventory (BI)of Cole Glass Inc.

LIFO inventory pool consisted of the following:Quantity (squared foot (SF))

Cost (per SF)

Total Cost

Grade A Window Glass

10,000 $3.00 $30,000

Grade B 14,000 $2.50 $35,000

Grade C 11,000 $2.20 $24,200

Totals 35,000 $89,200

Average SF Cost of the Pool -BI

$2.55 = ($89,200/ 35,000)

Inventories: Measurement 80

LIFO Inventory Pools: An Example During 20x8, Cole sold 48,000 squared feet of

window glass and purchased 51,000 squared feet as follows:

Quantity (squared foot (SF))

Cost (per SF) Total Cost

Grade A Window Glass

20,000 $3.10 $62,000

Grade B 15,000 $2.60 $39,000

Grade C 16,000 $2.45 $39,200

Totals 51,000 $140,200

Average 2008 SF Cost of the Pool

$2.75 = ($140,200/ 51,000)

Inventories: Measurement 81

LIFO Inventory Pools: An Example (contd.) The average cost of 2008 beg. inventory

and 2008 window glass inventory pool is $2.55 and $2.75, respectively.

The ending inventory quantity for the pool is:

35,000+51,000-48,000=38,000 units

Inventories: Measurement 82

LIFO Inventory Pools: An Example (contd.) Since the ending inventory of 2008

exceeds its beg. Inventory, the ending inventory will include the beginning inventory (i.e., 35,000 units ) and a LIFO layer of 3,000 units from 2008 .

Thus, the cost of 2008 ending inventory equals:

$2.55 x 35,000+ $2.75x 3,000 = $97,500

Inventories: Measurement 83

Problems Associated with LIFO Inventory Pools When a product in an inventory pool is

discontinued, the old costs of the discontinued item will become the cost of goods sold and therefore, result in LIFO liquidation.

Even if the product is replaced, it may not be similar to the old item and cannot be included in the same pool.

Therefore, LIFO inventory pool requires redefine pools periodically when there are changes in the product mix of the pool.

Inventories: Measurement 84

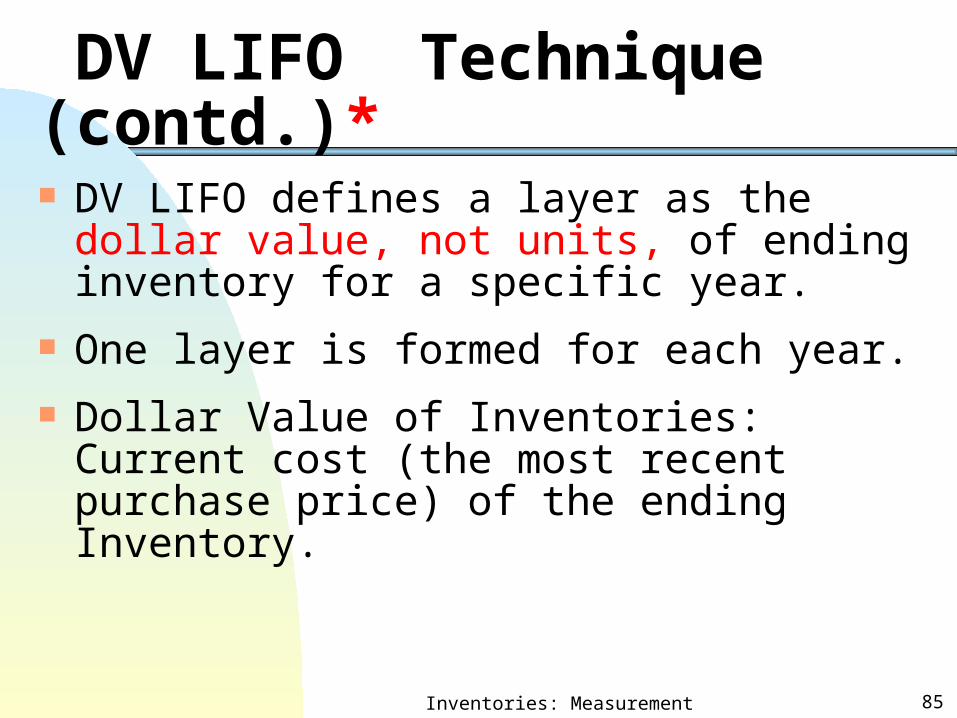

9. Dollar-Value LIFO (DV LIFO) Technique* DV LIFO technique simplifies the

recordkeeping procedures (due to no need to keep unit flows).

DV LIFO technique helps to protect LIFO layers from erosion (i.e., reduce the probability of LIFO liquidations; more than the LIFO inventory pool technique).

This technique is commonly used in practice for companies adopting LIFO assumption..

Inventories: Measurement 85

DV LIFO Technique (contd.)*

DV LIFO defines a layer as the dollar value, not units, of ending inventory for a specific year.

One layer is formed for each year. Dollar Value of Inventories: Current cost

(the most recent purchase price) of the ending Inventory.

Inventories: Measurement 86

DV LIFO Technique (contd.)*

To determine whether a new LIFO layer is added under DV LIFO, the DV of ending inventory (EI) is compared with that of the beg. Inventory (BI).

If the DV of EI exceeds that of the BI, the EI layers will consist of the DV of the BI layer plus a new DV layer created for the current year (i.e., the DV of EI – the DV of BI).

Inventories: Measurement 87

The Cost Index When the price level of the EI differs from

that of BI, a cost index should be used to adjust the DV of EI at the price level of the BI before forming the layers for the EI.

Cost index of a layer year =

Cost in layer year/Cost in base year Base year is the year in which DV LIFO is

adopted and a layer year is any subsequent year in which an inv. Layer is created..

Inventories: Measurement 88

Dollar Value LIFO – An Example

Layer Current Cost Cost EI at Value ofYear of Ending (Price) Base year Inv. At

Inventory Index Price Levl. D-V LIFO20x0 a $20,000 100 $20,000 $20,00020x1 $30,000 120 $25,000 $26,00020x2 $35,100 130 $27,000 $28,60020x3 $40,600 140 $29,000 $31,400

a. the base year

Inventories: Measurement 89

Example (contd.) Forming of layers: 20x0 20x1 20x2 20x3 20,000 ... L1 20,000...L1 20,000...L1 20,000...L1

5,000...L2 5,000...L2 5,000...L22,000...L3 2,000...L3

2,000 ..L4

Converting to the corresponding year’s index level: 20x0 20x1 20x2 20x3 20,000x1 20, 000x1+ 20,000x1+ 20,000x1+ =20,000 5 ,000x1.2 5,000x1.2+ 5,000x1.2+

=26,000 2,000x1.3 2,000x1.3+=28.600 2,000x1.4

=31,400

Inventories: Measurement 90

Comments on Dollar-Value LIFO

Items with similar economic, not physical, characteristics (i.e., subject to similar cost change pressure) will be pooled together.

The more items are included in an inventory pool, the less likely the erosion of the LIFO layers can occur.

Inventories: Measurement 91

Comments on Dollar-Value LIFO (contd.)* Income number can be manipulated by

changing the number of inventory pools.

On average, retailers form 6 pools for their inventories and non-retailers form 3 pools for their inventories with about a third of non-retailers use a single pool. (source: footnote 6 of chapter 8, KWW, 14th e).

Inventories: Measurement 92

An Example of Manipulating Income by Changing the Number of Inventory Pools

Stauffer Chemical Company had increased LIFO pools from 8 to 280 , boosting its net income by $16,515,000 (13%) (source: KWW, 14th edition, p461).

Inventories: Measurement 93

Types of Indexes Internal Index: Internal price index

computed by the company for its own product.

External Index: Computed by an outside party such as the government, commodity exchange, or trade association.

General Index: Composed of several commodities, goods or services.

Specific Index: For one commodity, good or service.

Inventories: Measurement 94

External Price Index*

The Consumer Price Index for urban consumers (CPI-U) is an example of an external general price index.

CPI-U is published monthly by the Bureau of Labor Statistics of the federal government.

Specific external price indexes (i.e., for gold, silver, corn…) are also available from trade associations.

Inventories: Measurement 95

The Internal Indexes

A Double-Extension Method (i.e., the value of inv. units extended at both current and base-year prices):Internal Index for the Current Year =

End. Inv*. at Current Year’s CostEnd. Inv. at Base-Year Cost

End. Inv. is the ending inventory of the current year.

The cost index for the base year equals one.

Inventories: Measurement 96

Example

To compute specific internal price indexes:

Year Current Units of Cost Cost End. Inv. Index(%)

20x0 (base year) $19 300 100a

20x1 $22.8 400 120b

20x2 $24.7 450 130c

20x3 $26.6 370 140d

a. 19*300/19.0*300=100% c.24.7*450/19*450=130% b. 22.8*400/19*400=120% d.26.6*370/19*370=140%

Inventories: Measurement 97

Example (contd.) General internal price index:

(for more than one inventory in the pool): Inv. A Inv. B

Current Units of Current Units of Cost End. Inv. Cost End. Inv.20x0(base year) $19 100 $20 15020x1 $22.8 110 $22 120

General internal price index of 20x0:(19x100+20x150) / (19x100+20x150)=100%

General internal price index of 20x1:(22.8x110+22x120) / (19x110+20x120)=114.6%