intelligent objects. futuristic applications smart appliances smart appliances smart appliances...

TRANSCRIPT

Intelligent Objects

Futuristic Applications

Smart AppliancesSmart Dressing RoomsSmart StoreSmart Room

Business Models From products to services From products to services

(subscription)(subscription)Medtronics, OnStarMedtronics, OnStar

Improving product or service Improving product or service differentiationdifferentiationProgressive insurance, Coke Vending Progressive insurance, Coke Vending

MachineMachine

Reducing cost structureReducing cost structureWal-MartWal-Mart

Enhancing efficiencyEnhancing efficiencySmart machines, smart MetersSmart machines, smart Meters

What had to come together?

Reduction in sizeReduction in sizeReduction in costReduction in costAbility to communicateAbility to communicateSolve power supply problemsSolve power supply problems

There are 2 main types

PassivePassiveActiveActive

The key elements of an Intelligent Object is its ability to:

Who it is (identity)Who it is (identity)Where it is (location)Where it is (location)What is happening to it (Status)What is happening to it (Status)What is going on around it What is going on around it

(environment)(environment)

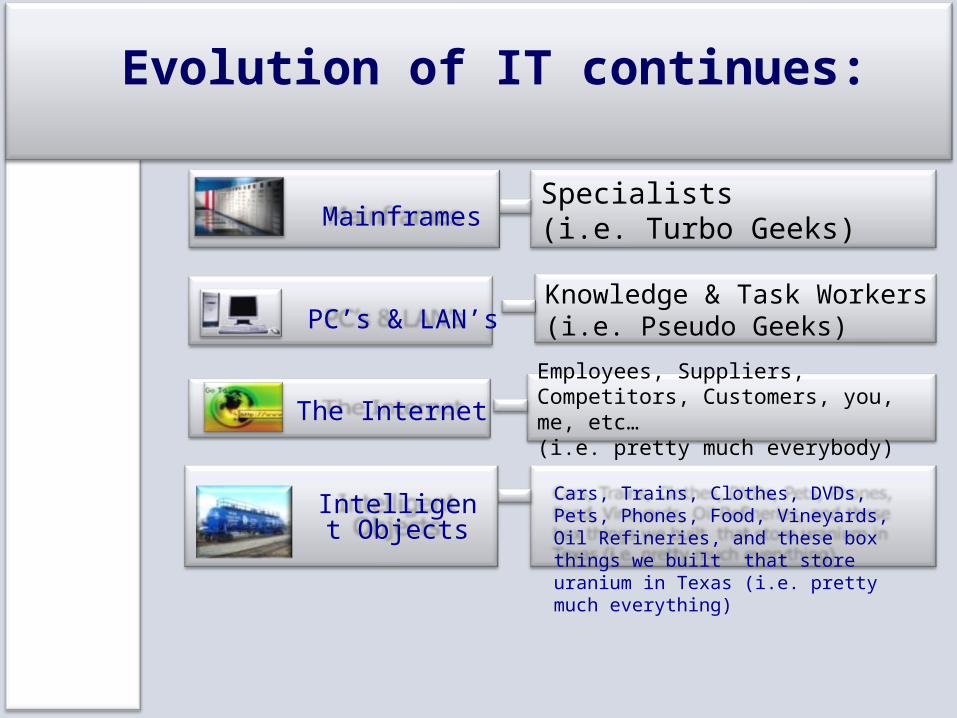

Evolution of IT continues:

Specialists (i.e. Turbo Geeks)Mainframes

Knowledge & Task Workers(i.e. Pseudo Geeks)PC’s & LAN’s

Employees, Suppliers, Competitors, Customers, you, me, etc…(i.e. pretty much everybody)

The Internet

Cars, Trains, Clothes, DVDs, Pets, Phones, Food, Vineyards, Oil Refineries, and these box things we built that store uranium in Texas (i.e. pretty much everything)

Intelligent Objects

Threats of Smart SystemsPrivacy and ControlPrivacy and ControlHacking & being used for evilHacking & being used for evilMore inequality & unemploymentMore inequality & unemploymentToo much data .. No way to Too much data .. No way to

retrieve itretrieve itOver reliance on machines under Over reliance on machines under

reliance on human brainsreliance on human brains

Technology and the Insurance Business

What is the critical element in the success and profitability in the car insurance business (or any insurance business for that matter?

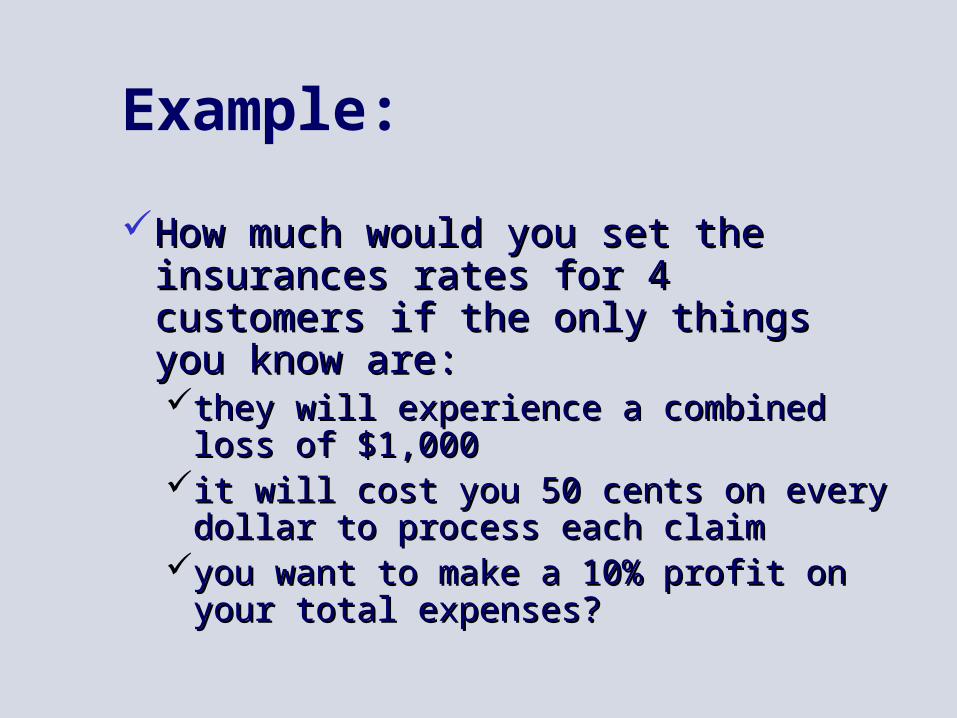

Example:

How much would you set the How much would you set the insurances rates for 4 customers insurances rates for 4 customers if the only things you know are:if the only things you know are:they will experience a combined loss they will experience a combined loss

of $1,000 of $1,000 it will cost you 50 cents on every it will cost you 50 cents on every

dollar to process each claimdollar to process each claimyou want to make a 10% profit on you want to make a 10% profit on

your total expenses?your total expenses?

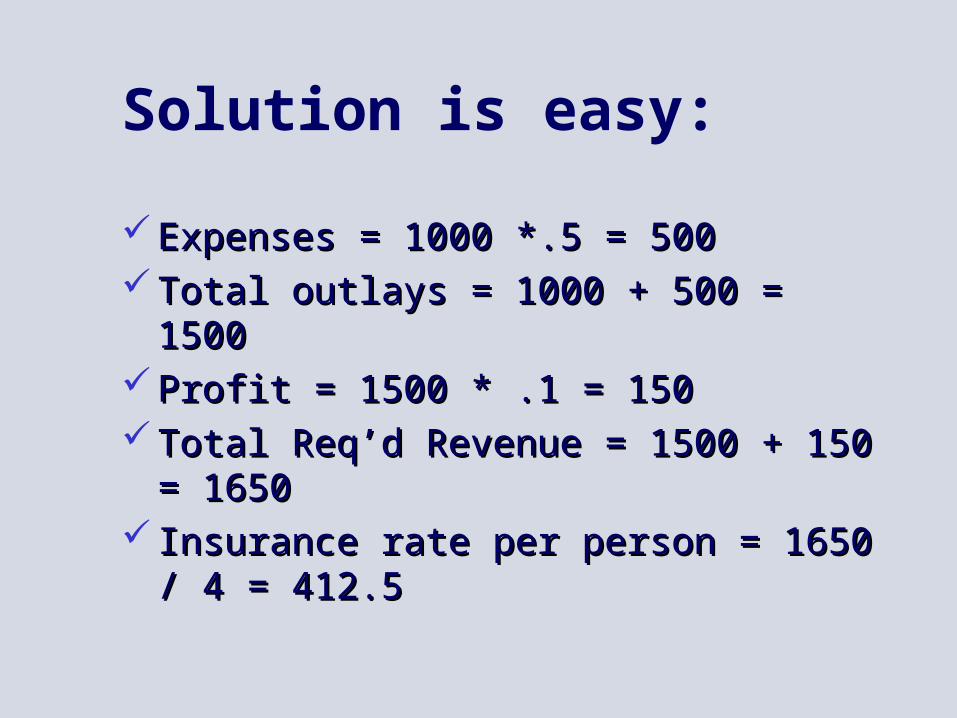

Solution is easy:

Expenses = 1000 *.5 = 500Expenses = 1000 *.5 = 500 Total outlays = 1000 + 500 = 1500Total outlays = 1000 + 500 = 1500 Profit = 1500 * .1 = 150Profit = 1500 * .1 = 150 Total Req’d Revenue = 1500 + 150 = Total Req’d Revenue = 1500 + 150 =

16501650 Insurance rate per person = 1650 / 4 = Insurance rate per person = 1650 / 4 =

412.5412.5

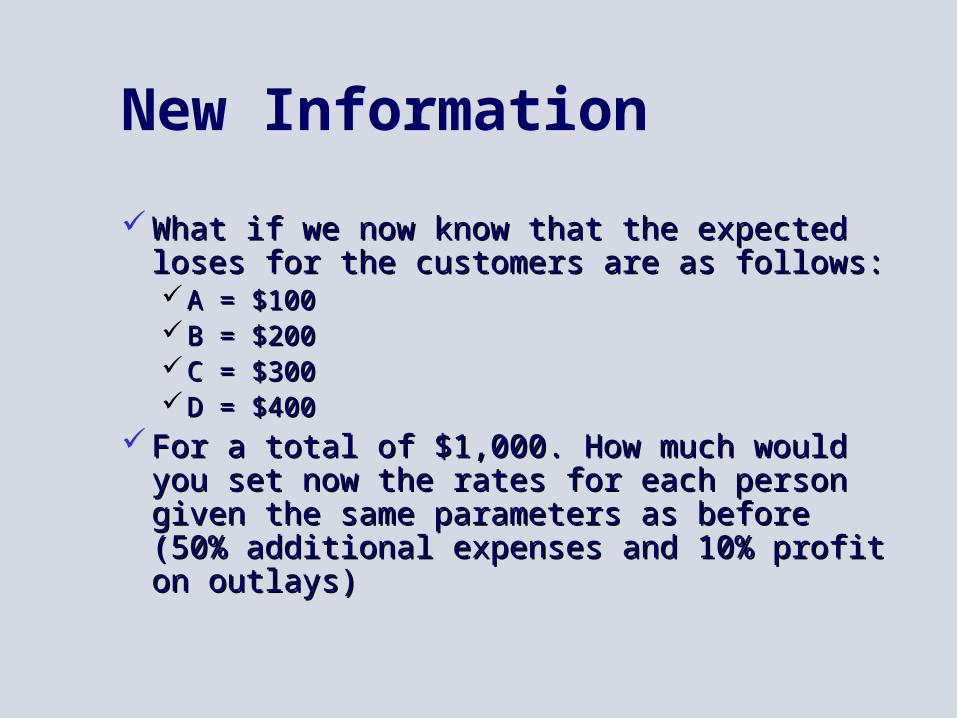

New Information

What if we now know that the expected What if we now know that the expected loses for the customers are as follows:loses for the customers are as follows:A = $100A = $100B = $200B = $200C = $300C = $300D = $400D = $400

For a total of $1,000. How much would you For a total of $1,000. How much would you set now the rates for each person given set now the rates for each person given the same parameters as before (50% the same parameters as before (50% additional expenses and 10% profit on additional expenses and 10% profit on outlays)outlays)

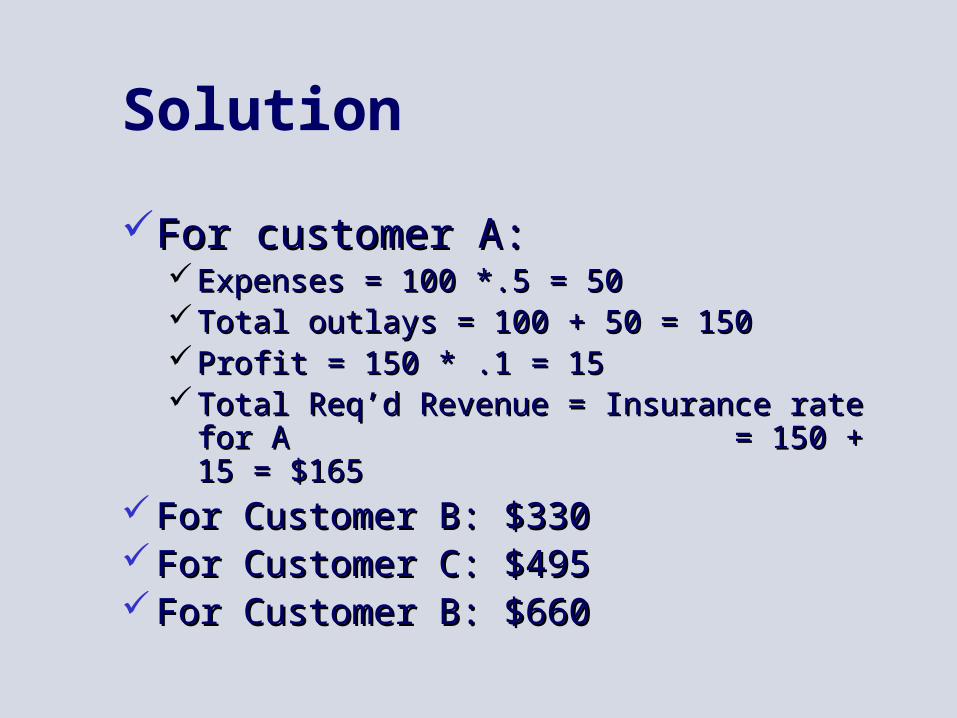

Solution

For customer A:For customer A:Expenses = 100 *.5 = 50Expenses = 100 *.5 = 50Total outlays = 100 + 50 = 150Total outlays = 100 + 50 = 150Profit = 150 * .1 = 15Profit = 150 * .1 = 15Total Req’d Revenue = Insurance rate for A Total Req’d Revenue = Insurance rate for A

= 150 + 15 = $165 = 150 + 15 = $165 For Customer B: $330For Customer B: $330 For Customer C: $495For Customer C: $495 For Customer B: $660For Customer B: $660

Solution cont’d

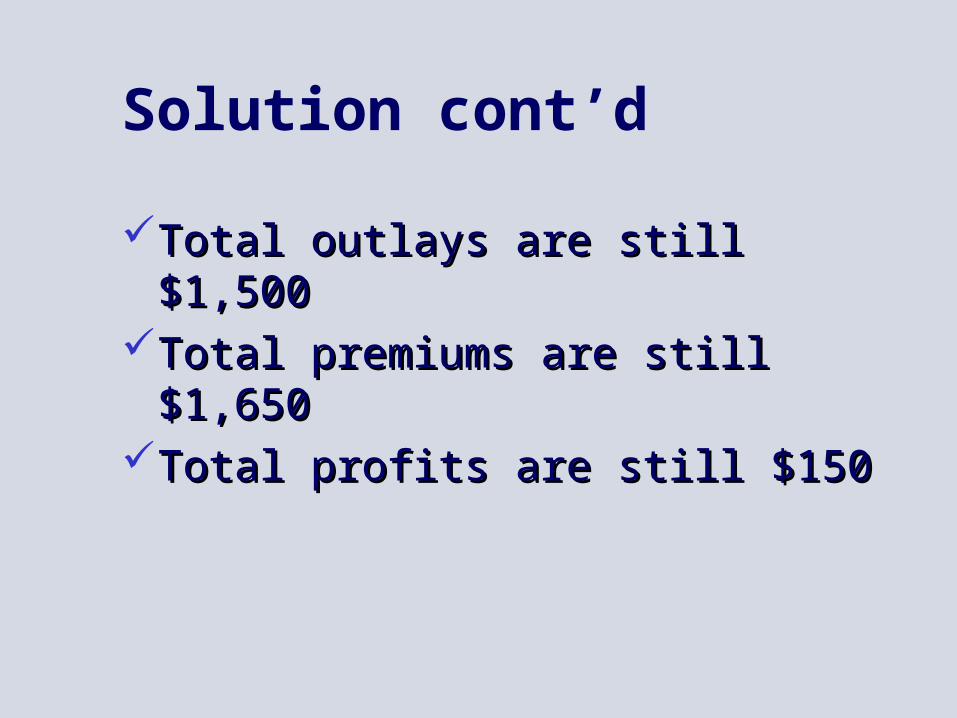

Total outlays are still $1,500Total outlays are still $1,500Total premiums are still $1,650Total premiums are still $1,650Total profits are still $150Total profits are still $150

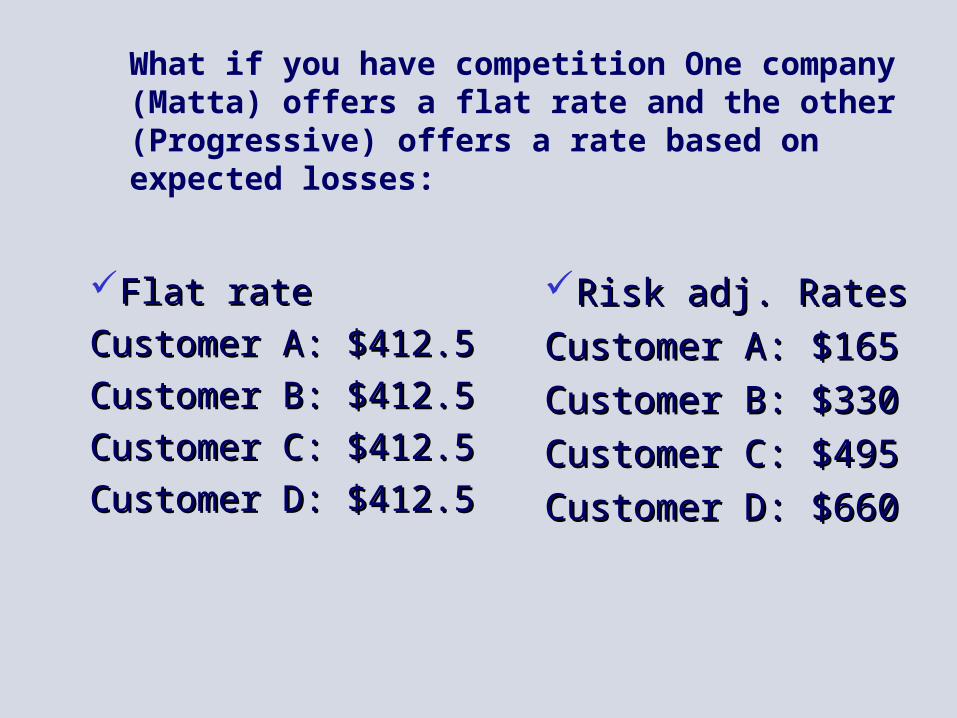

What if you have competition One company (Matta) offers a flat rate and the other (Progressive) offers a rate based on expected losses:

Flat rateFlat rate

Customer A: $412.5Customer A: $412.5

Customer B: $412.5Customer B: $412.5

Customer C: $412.5Customer C: $412.5

Customer D: $412.5Customer D: $412.5

Risk adj. RatesRisk adj. Rates

Customer A: $165Customer A: $165

Customer B: $330Customer B: $330

Customer C: $495Customer C: $495

Customer D: $660Customer D: $660

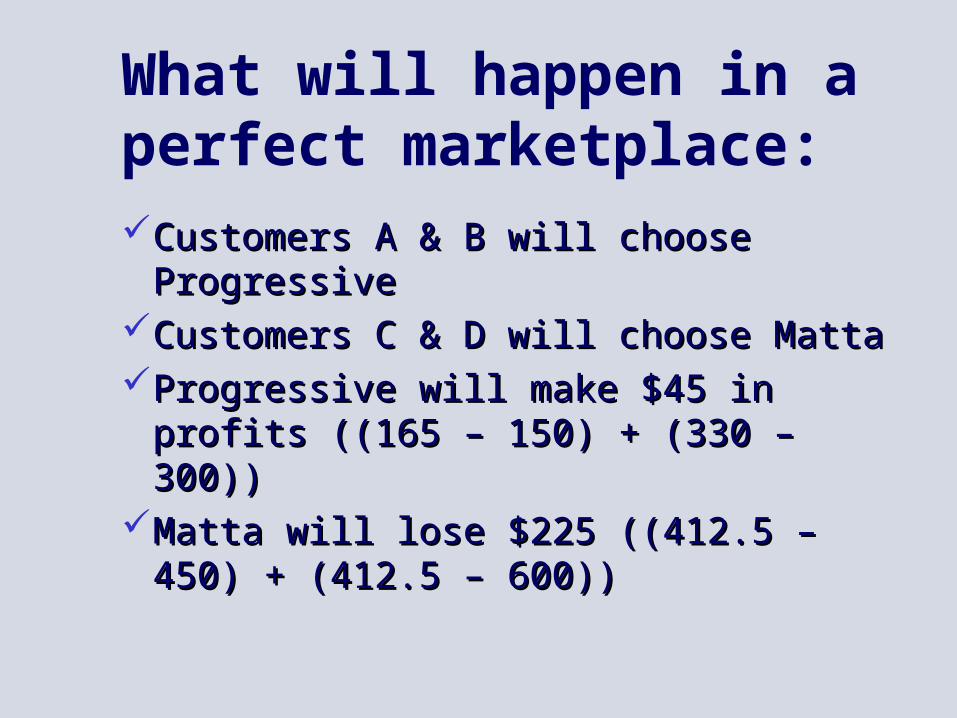

What will happen in a perfect marketplace:Customers A & B will choose Customers A & B will choose

ProgressiveProgressiveCustomers C & D will choose MattaCustomers C & D will choose MattaProgressive will make $45 in Progressive will make $45 in

profits ((165 – 150) + (330 – 300))profits ((165 – 150) + (330 – 300))Matta will lose $225 ((412.5 – 450) Matta will lose $225 ((412.5 – 450)

+ (412.5 – 600))+ (412.5 – 600))

Reason for profit and lossProgressive has a prefect Progressive has a prefect

information on losses & riskinformation on losses & riskMatta has no information Matta has no information

regrading loss & riskregrading loss & riskMost insurance companies are Most insurance companies are

somewhere in betweensomewhere in between

Stratifying Customers based on Risk profileAgeAgeDriving historyDriving historyLocationLocationCredit ScoreCredit ScoreEducationEducationSexSexEtc..Etc..

Is there a better way to measure risk in the car insurance business?

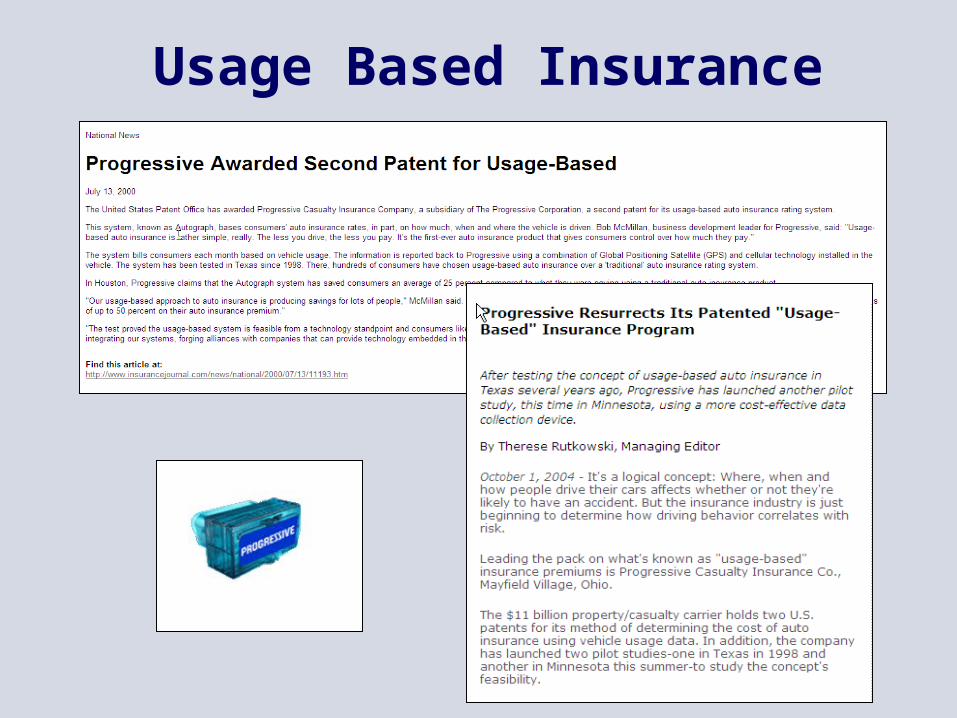

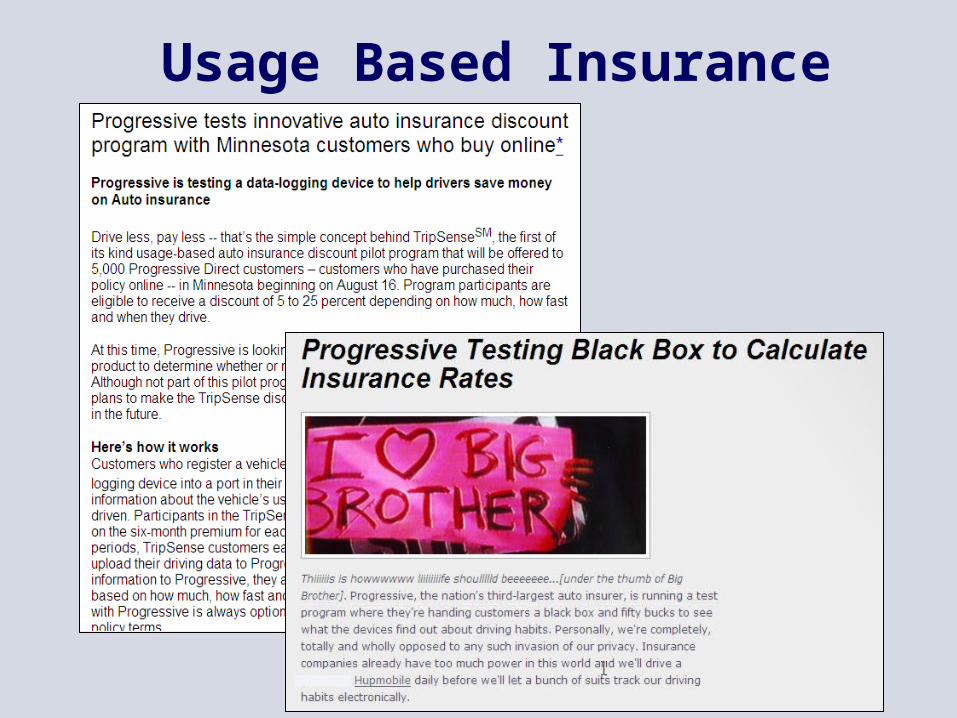

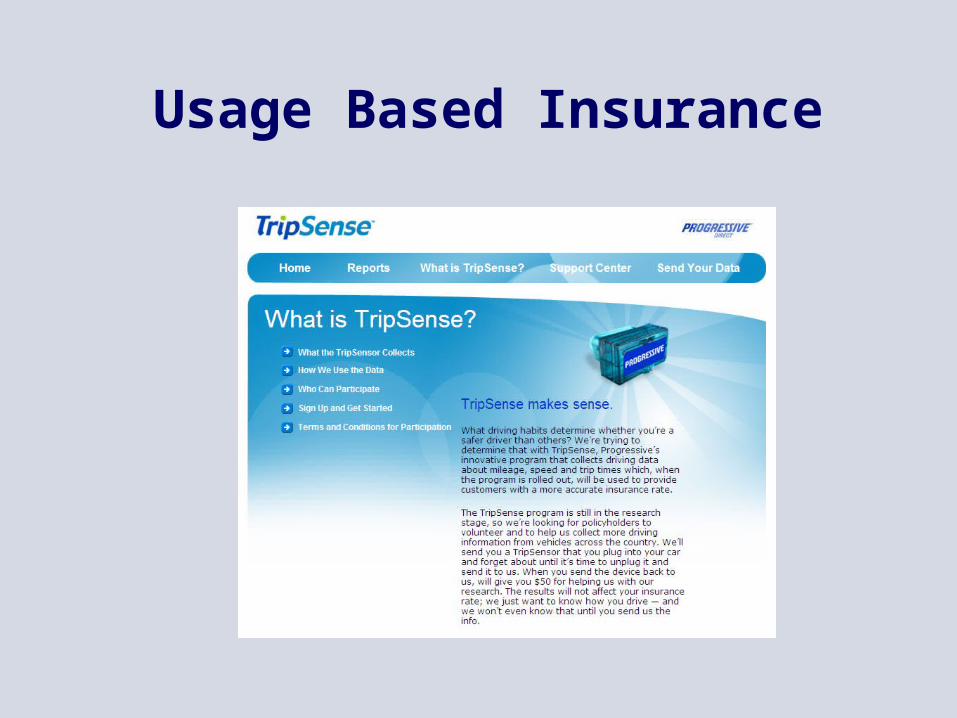

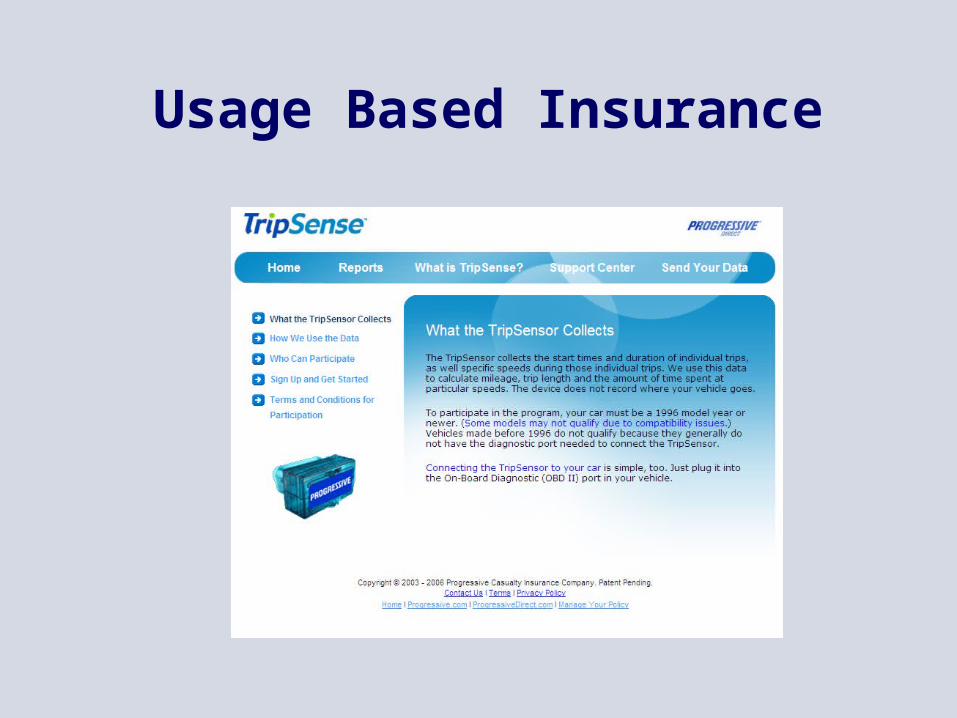

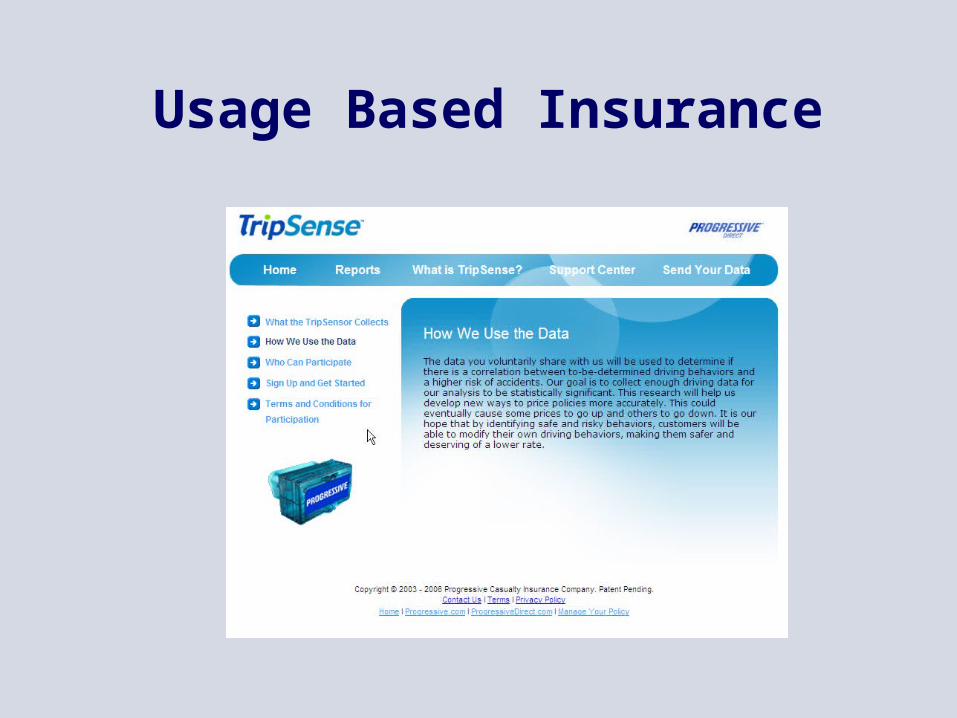

Usage Based Insurance

• Past driving record (accidents, violations, prior

claims) is a great predictor of future losses

• Current driving practices may be another important predictor of future losses, even in the absence of incidents on the driving record.

Understand risk better than the competition, allowing us to provide more accurate rates to policyholders.

Business Strategy:

Usage Based Insurance

Usage Based Insurance

Usage Based Insurance

Usage Based Insurance

Usage Based Insurance

Usage Based Insurance