instructor’s manual - testbankcarttestbankcart.com/wp-content/uploads/2017/01/downloadable... ·...

TRANSCRIPT

Instructor’s Manual to accompany

ACCOUNTING FOR DECISION MAKING & CONTROL

SEVENTH EDITION

JEROLD L. ZIMMERMAN

WILLIAM E. SIMON GRADUATE SCHOOL OF BUSINESS ADMINISTRATION

UNIVERSITY OF ROCHESTER

THIS MATERIAL IS FOR CLASSROOM USE ONLY AND MAY NOT BE COPIED OR USED FOR ANY OTHER PURPOSE

COPYRIGHT 2011 ALL RIGHTS RESERVED

DO NOT COPY OR DUPLICATE WITHOUT PERMISSION

Using the Text ©The McGraw-Hill Companies, Inc., 2011 Instructor’s Manual, Accounting for Decision Making and Control i

CONTENTS

PREFACE ii PART I: USING THE TEXT Suggested Course Outlines iii Chapter Teaching Suggestions vii Suggested Assignment Problems & Cases xxiii Alphabetical Listing of Problems and Cases xxxi PART II: SOLUTIONS TO PROBLEMS AND CASES 1. Introduction 1-1 2. The Nature of Costs 2-1 3. Opportunity Cost of Capital and Capital Budgeting 3-1 4. Organizational Architecture 4-1 5. Responsibility Accounting and Transfer Pricing 5-1 6. Budgeting 6-1 7. Cost Allocation: Theory 7-1 8. Cost Allocation: Practices 8-1 9. Absorption Cost Systems 9-1 10. Criticisms of Absorption Cost Systems: Incentive to Overproduce 10-1 11. Criticisms of Absorption Cost Systems: Inaccurate Product Costs 11-1 12. Standard Costs: Direct Labor and Materials 12-1 13. Overhead and Marketing Variances 13-1 14. Management Accounting in a Changing Environment 14-1 PART III: TEST BANK AND SOLUTIONS T-1

Using the Text ©The McGraw-Hill Companies, Inc., 2011 ii Instructor’s Manual, Accounting for Decision Making and Control

PREFACE

This Instructor’s Manual for Accounting for Decision Making & Control contains

three parts. The first part describes how the text can be used in a variety of courses: a

seven week executive MBA, a quarter-length course, and a semester-length course.

Sample class outlines are provided for each type of course. The first part also contains

detailed chapter-by-chapter teaching summaries (including suggested problems and

cases) of how I teach each chapter, what topics to emphasize, and the strategy for

presenting the subject matter. Also included is a classification of the end-of-chapter

problems and cases by level of difficulty and degree of classroom discussion generated,

and an alphabetical index to all problems and cases.

The second part of this Instructor’s Manual contains detailed solutions to the end-

of-chapter problems and cases. Many of these problems developed out of discussions

with students in actual situations at their companies, or are based on my consulting

experience. All of the problems have been used on exams and have been taught in class

several times. However, no amount of prior usage can guarantee that a bright student

will not see a new interpretation or solution. Thought-provoking problems have this

characteristic. I am very interested in receiving feedback on the problems and cases, as

well as the text. Please e-mail me at [email protected].

The third part of this Manual is a test bank, including solutions. Producing good

exam problems and solutions is difficult. Textbook authors are always welcome

recipients and grateful acknowledgers of such material.

Using the Text ©The McGraw-Hill Companies, Inc., 2011 Instructor’s Manual, Accounting for Decision Making and Control iii

PART I: USING THE TEXT

Suggested Course Outlines

Quarter, Semester, and Executive Courses

Accounting for Decision Making & Control can be used in quarter- and semester-

length introductory MBA managerial accounting courses and 7-8 week executive MBA

courses. The following three tables suggest course outlines for quarter, semester, and

executive MBA courses. None of the outlines cover capital budgeting (Chapter 3).

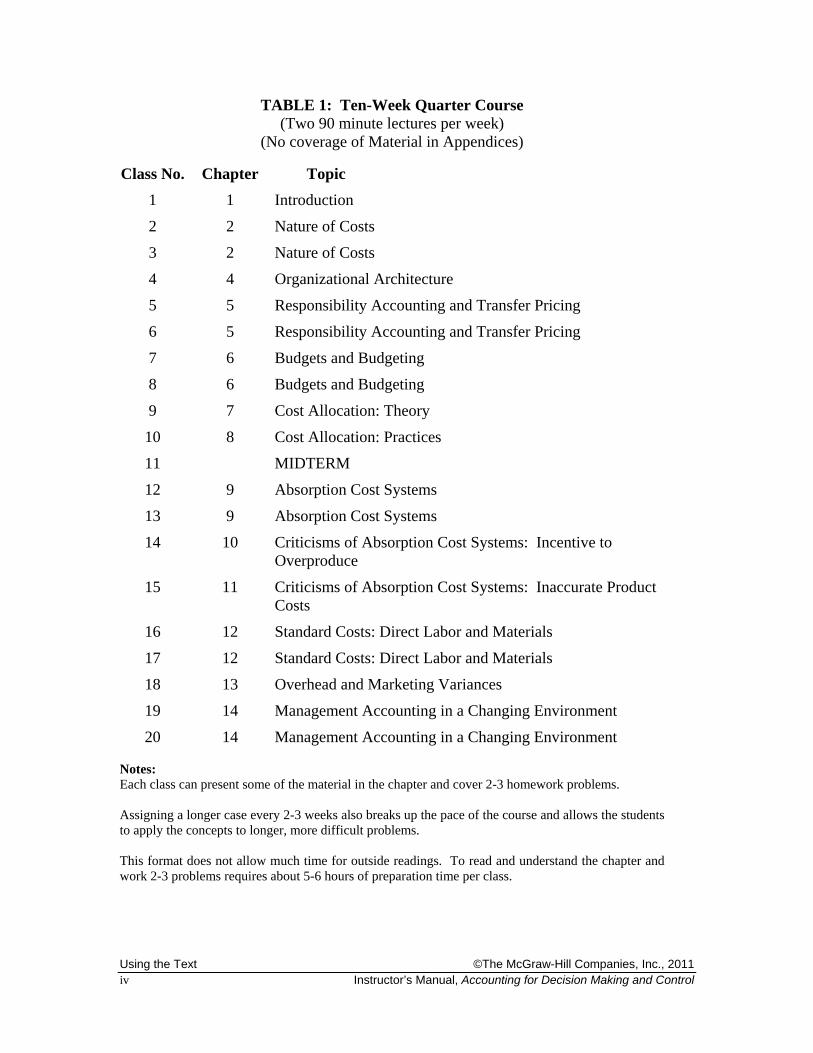

Quarter-length courses. Table 1 presents a ten-week quarter course. The text

contains too much material to cover it all comfortably in a ten week quarter course.

Chapter 3 on capital budgeting, and all the appendices must be omitted. This allows time

for covering the crucial problems and a few supplemental cases, but limited opportunity

for outside readings.

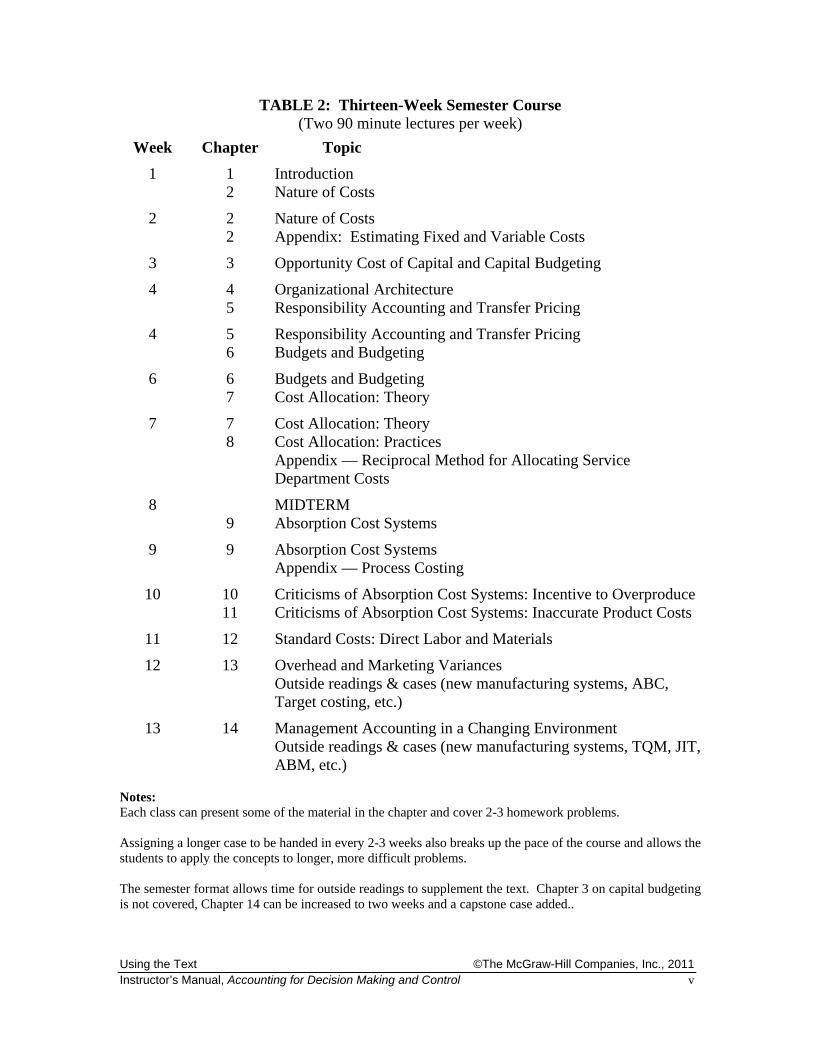

Semester-length courses. Table 2 presents a thirteen-week semester course. A

semester format gives the instructor added flexibility for covering Chapter 3 on capital

budgeting, appendices, outside readings, additional topics, or cases. Depending on the

instructor’s interest and program demands, the book complements additional topics on

ethics, international examples, new manufacturing advances, quality management, ABC

and ABM, balanced score card, lean manufacturing, etc. These topics fit naturally

toward the end of the course after developing the underlying framework and an

understanding of the evolution of costing systems.

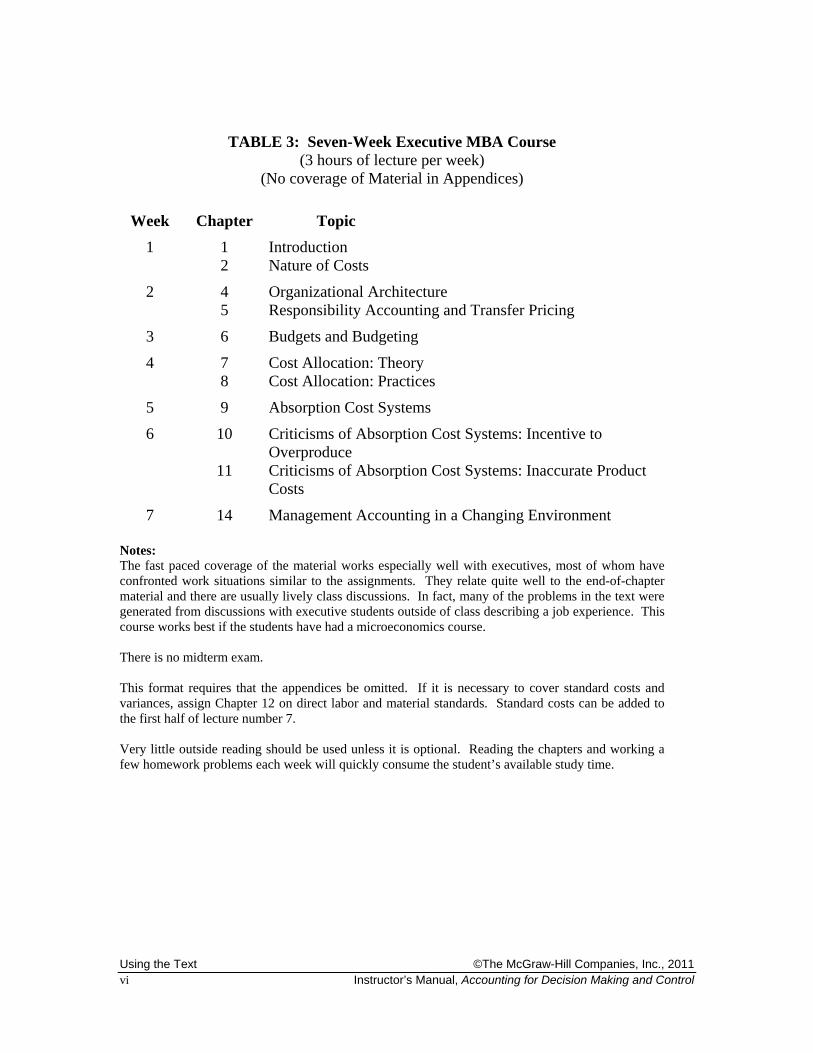

Executive MBA courses. Table 3 presents the outline for a seven-week executive

course. The book has been used successfully with executive MBA students. In a seven

week, one-day-a-week setting with three hours of lectures per week, the course is fast

paced. Executive students, having encountered similar situations, find the problems very

realistic, and are especially receptive to integrating the accounting, economics, and

organizational aspects of the material. However, much of the material must be pared

back. Delete all of the appendices, Chapter 3 on capital budgeting, and Chapters 12 and

13 on standard costs and variances.

Using the Text ©The McGraw-Hill Companies, Inc., 2011 iv Instructor’s Manual, Accounting for Decision Making and Control

TABLE 1: Ten-Week Quarter Course (Two 90 minute lectures per week)

(No coverage of Material in Appendices)

Class No. Chapter Topic

1 1 Introduction

2 2 Nature of Costs

3 2 Nature of Costs

4 4 Organizational Architecture

5 5 Responsibility Accounting and Transfer Pricing

6 5 Responsibility Accounting and Transfer Pricing

7 6 Budgets and Budgeting

8 6 Budgets and Budgeting

9 7 Cost Allocation: Theory

10 8 Cost Allocation: Practices

11 MIDTERM

12 9 Absorption Cost Systems

13 9 Absorption Cost Systems

14 10 Criticisms of Absorption Cost Systems: Incentive to Overproduce

15 11 Criticisms of Absorption Cost Systems: Inaccurate Product Costs

16 12 Standard Costs: Direct Labor and Materials

17 12 Standard Costs: Direct Labor and Materials

18 13 Overhead and Marketing Variances

19 14 Management Accounting in a Changing Environment

20 14 Management Accounting in a Changing Environment Notes: Each class can present some of the material in the chapter and cover 2-3 homework problems. Assigning a longer case every 2-3 weeks also breaks up the pace of the course and allows the students to apply the concepts to longer, more difficult problems. This format does not allow much time for outside readings. To read and understand the chapter and work 2-3 problems requires about 5-6 hours of preparation time per class.

Using the Text ©The McGraw-Hill Companies, Inc., 2011 Instructor’s Manual, Accounting for Decision Making and Control v

TABLE 2: Thirteen-Week Semester Course (Two 90 minute lectures per week)

Week Chapter Topic

1 1 2

Introduction Nature of Costs

2 2 2

Nature of Costs Appendix: Estimating Fixed and Variable Costs

3 3 Opportunity Cost of Capital and Capital Budgeting

4 4 5

Organizational Architecture Responsibility Accounting and Transfer Pricing

4 5 6

Responsibility Accounting and Transfer Pricing Budgets and Budgeting

6 6 7

Budgets and Budgeting Cost Allocation: Theory

7 7 8

Cost Allocation: Theory Cost Allocation: Practices Appendix — Reciprocal Method for Allocating Service Department Costs

8 9

MIDTERM Absorption Cost Systems

9 9 Absorption Cost Systems Appendix — Process Costing

10 10 11

Criticisms of Absorption Cost Systems: Incentive to OverproduceCriticisms of Absorption Cost Systems: Inaccurate Product Costs

11 12 Standard Costs: Direct Labor and Materials

12 13 Overhead and Marketing Variances Outside readings & cases (new manufacturing systems, ABC, Target costing, etc.)

13 14 Management Accounting in a Changing Environment Outside readings & cases (new manufacturing systems, TQM, JIT, ABM, etc.)

Notes: Each class can present some of the material in the chapter and cover 2-3 homework problems. Assigning a longer case to be handed in every 2-3 weeks also breaks up the pace of the course and allows the students to apply the concepts to longer, more difficult problems. The semester format allows time for outside readings to supplement the text. Chapter 3 on capital budgeting is not covered, Chapter 14 can be increased to two weeks and a capstone case added..

Using the Text ©The McGraw-Hill Companies, Inc., 2011 vi Instructor’s Manual, Accounting for Decision Making and Control

TABLE 3: Seven-Week Executive MBA Course (3 hours of lecture per week)

(No coverage of Material in Appendices)

Week Chapter Topic

1 1 2

Introduction Nature of Costs

2 4 5

Organizational Architecture Responsibility Accounting and Transfer Pricing

3 6 Budgets and Budgeting

4 7 8

Cost Allocation: Theory Cost Allocation: Practices

5 9 Absorption Cost Systems

6 10

11

Criticisms of Absorption Cost Systems: Incentive to Overproduce Criticisms of Absorption Cost Systems: Inaccurate Product Costs

7 14 Management Accounting in a Changing Environment Notes: The fast paced coverage of the material works especially well with executives, most of whom have confronted work situations similar to the assignments. They relate quite well to the end-of-chapter material and there are usually lively class discussions. In fact, many of the problems in the text were generated from discussions with executive students outside of class describing a job experience. This course works best if the students have had a microeconomics course. There is no midterm exam. This format requires that the appendices be omitted. If it is necessary to cover standard costs and variances, assign Chapter 12 on direct labor and material standards. Standard costs can be added to the first half of lecture number 7. Very little outside reading should be used unless it is optional. Reading the chapters and working a few homework problems each week will quickly consume the student’s available study time.

Using the Text ©The McGraw-Hill Companies, Inc., 2011 Instructor’s Manual, Accounting for Decision Making and Control vii

Chapter Teaching Suggestions My teaching approach is to require the students not only to read the assigned chapter, but also to prepare and submit a few problems at the beginning of class. This not only provides a foundation for constructive class discussion, but also ensures that students do not fall behind. Throughout the course I emphasize that students of managerial accounting will develop the very valuable skill of knowing how to take a diverse set of facts and figures and reduce them to a cogent financial analysis. They will become more skilled in constructing spreadsheets and doing financial analysis. This skill is similar to learning a foreign language, and similarly requires constant practice. The daily assignments provide this discipline. Chapter 1. Introduction Chapter 1 summarizes the course and contains a number of important concepts, including: internal versus external accounting; the trade-off between using the accounting system for decision making versus using it for control; single versus multiple accounting systems; the role of the controller; and economic Darwinism. A good way to begin the first lecture is to hand out a copy of the Vortec problem statement (Chapter 1, section F) and give the students five minutes to sketch out the solution. Then ask them, how many would accept the special order? This is a good way to generate class discussion the first day. By following the text’s analysis of Vortec in Chapter 1, several questions naturally arise, including: • What additional information is required? • What is the difference between variable and average costs? • How do the incentives of various managers to accept the order differ? Vortec is a good ice breaker which allows the students to see that the accounting costs are being used for a variety of purposes; in particular, they are being used for both decision making and control. Since the trade-off between decision making and control is an important organizing feature of the text, it is useful to introduce this key pedagogy early in the course. (Point out that Chapter 2 elaborates on decision making and Chapters 4 and 5 describe the general issues involving control.) I also like to reinforce the multiple roles of accounting using Figure 1-1. Finally, it is important to spend a few minutes discussing the importance of Economic Darwinism. Many of the topics we discuss (cost allocations, budgeting, product costing) have survived in competitive industries for long periods of time. For the average firm, these accounting procedures must be yielding benefits at least as large as their costs. This does not mean that these procedures are cost beneficial for every firm. Nor does it mean that these accounting systems operate at zero costs (including the costs of dysfunctional decision making).

Using the Text ©The McGraw-Hill Companies, Inc., 2011 viii Instructor’s Manual, Accounting for Decision Making and Control

Chapter 2. The Nature of Costs I begin this lecture by defining opportunity costs, “The sacrifice forgone from a specific decision.” Students find this definition too abstract to have much meaning. Plan on spending 20 - 30 minutes giving examples and working through text problems. A good example to use to illustrate opportunity costs is: “How do you decide what to do this Saturday night?” First you think about the opportunities (movie, concert, watching TV, studying managerial accounting). (The last gets a good laugh.) Then you think about what you give up if you do a particular activity. You forgo cash in some cases as well as the opportunity to do something else. If your managerial accounting final exam is on Monday, going to a concert precludes studying for the final. If you fail the final and have to repeat the course in the summer, this can impose large costs, especially if you are unable to get a good summer internship. This simple example illustrates all the key points of opportunity costs:

• opportunity costs involve both pecuniary and non-pecuniary considerations, • opportunity costs are forward looking, • opportunity costs vary with the opportunity set (e.g., which movies are

playing and when assignments are due).

Two problems in the text are very good at driving home the concept of opportunity costs: P2-10 Emrich Processing P2-26 Eastern University Parking Emrich (P2-10) always generates a 15 minute discussion. Ask the students what cost of the remaining acid should be considered in setting the price for the new contract. Possible answers will be $700, $500, $0, and -$400. The correct answer is -$400. In this case opportunity costs are negative because the firm can avoid the disposal costs. This then leads into a question of what price to charge. Since we don’t know the customer’s demand curve, we can’t set a price, but the discussion helps illustrate the relation between costs and pricing (a point that arises throughout the course). Appendix A discusses the relation between costs and pricing. Eastern University Parking (P2-26) can generate as much as 20 to 30 minutes of discussion. Parking is a universal problem on all campuses, and hence, this problem hits a strong emotional nerve. Most students initially overlook the opportunity cost of land in setting the parking fees and will discuss other problems with the parking system for five minutes or so before someone hits on the problem of how land is being valued. It isn’t. And this creates the bias towards surface lots. Once everyone understands this, then ask, “Why has the University systematically priced its land at zero?” “Are the administrators dumb?” Most students are willing to stop here and say yes. But prompt them by asking, “What are the organizational consequences of including land costs in parking fees?” The solution describes the organizational issues. This problem illustrates dramatically how accounting costs have both decision making and organizational implications.

Using the Text ©The McGraw-Hill Companies, Inc., 2011 Instructor’s Manual, Accounting for Decision Making and Control ix

Mastich Counters (P2-28) is a great problem for student discussion, especially for executive students because it involves primarily a human resources question that they have all encountered – should firms adopt a take-it or loose-it policy for vacation accruals? At this point I usually compare opportunity and accounting costs. The key point is that most accounting costs are historical in nature and hence backward-, not forward-looking. The final point to emphasize is that estimating opportunity costs is itself a costly process. Much analysis is usually required to define the opportunity set and to estimate the benefits forgone from each alternative. Because opportunity costs are costly to estimate, proxies are often used, such as accounting costs. After introducing opportunity costs, I spend the rest of the time on cost variability and review total, average, fixed, variable, and marginal costs. Students will remember these terms from their economics course, and are reassured when told that we simplify the economics treatment by assuming cost curves are straight lines, thus eliminating derivatives from this course. This discussion is very important because it is one of the first times in the curriculum that two courses are integrated with and build on each other. A good break-even problem is Amy’s Boards (P2-44), which illustrates that the snow boards are a variable cost before they are purchased, but become a fixed cost once purchased. In later chapters, students have difficulty knowing how to handle fixed costs. Amy’s Boards provides a simple, intuitive example of how fixed costs arise from making the capacity decision. Recommended Problem Assignment

2-9 Taylor Chemicals 2-10 Emrich Processing 2-15 Home Auto Parts 2-22 iGen3 2-25 Oppenheimer Visuals 2-26 Eastern University Parking 2-28 Mastich Counters 2-31 News.com 2-34 Candice 2-41 Happy Feet 2-42 Digital Convert 2-43 APC Electronics 2-44 Amy’s Boards Case 2-1 Old Turkey Mash

Using the Text ©The McGraw-Hill Companies, Inc., 2011 x Instructor’s Manual, Accounting for Decision Making and Control

Chapter 3. Opportunity Cost of Capital and Capital Budgeting This chapter is a fairly traditional treatment of capital budgeting. It can be omitted without interrupting the flow of the material, or it can be postponed until later in the course. The later chapters and problems do not rely on this material. Like other managerial accounting texts, to simplify the analysis, topics in Chapters 4–14 are treated as single-period decision problems. As our students have already taken a basic corporate finance and capital budgeting course, I do not cover this chapter in my managerial accounting course. Teaching this chapter depends on the students’ prior exposure to discounting, and the instructor’s objectives. Chapter 4. Organizational Architecture Since Rochester students have had two managerial economics courses that cover the basic topics in Chapter 4, this chapter largely constitutes a review and is presented in conjunction with Chapter 5, with Chapter 5 being used to reinforce and illustrate the general theoretical issues raised in Chapter 4. The key points to emphasize include: the importance of agency problems: how the organizational architecture can reduce these problems, and the accounting system as an integral part of the performance evaluation system in most organizations. I spend a few minutes reviewing the major concepts and terminology used later in the course: • Organizational architecture (three-legged stool) Performance evaluation Rewards and punishments Partitioning decision rights • Importance of linking decision rights and knowledge • Administrative devices for the three-legged stool Separation of decision management and decision control Initiation - decision management Ratification - decision control Implementation - decision management Monitoring - decision control Hierarchies Recommended Problem Assignment

4-5 Voluntary Financial Disclosure 4-17 Private Country Clubs 4-18 Tipping 4-24 Repro Corporation

Using the Text ©The McGraw-Hill Companies, Inc., 2011 Instructor’s Manual, Accounting for Decision Making and Control xi

Chapter 5. Responsibility Accounting and Transfer Pricing The purpose of Chapter 5 is to illustrate the role of the accounting system in the firm’s organizational architecture. Two examples are used: performance evaluation of responsibility centers, and accounting-based transfer pricing. The first part of the chapter on responsibility accounting is a good example of the linkage between the assignment of decision rights and performance evaluation. I review Table 5-1 and point out that evaluating cost centers based on minimizing average cost does not necessarily maximize firm profits. I also like to spend a few minutes discussing EVA and asking the question, “How does EVA differ from residual income?” Except for some measurement refinements in the cost of capital and accounting income, the two are the same. They differ in that some EVA consultants emphasize linking EVA to compensation. The second topic of the chapter is transfer pricing. Traditional managerial accounting courses cover transfer pricing towards the end of the course. I believe it is best covered at the beginning as part of the topic of organizational architecture. Cost allocations and cost recharges pervade all organizations. To understand the incentive issues of cost allocations, the general topic of transfer pricing provides an underlying theoretical foundation for cost allocations in general. I do not lecture extensively on transfer pricing. Our students have had the economics of transfer pricing in their managerial economics course. Instead, I emphasize several key points:

• Accounting-based transfer prices are prevalent, even when market prices are available.

• The ideal transfer price is opportunity cost. • Transfer pricing is not a zero-sum game, and all transfer pricing methods have

both advantages and disadvantages (no method is best in all situations). • With variable cost transfer pricing, someone must have the decision rights to

determine which costs are fixed and which costs are variable. Since lower-level managers usually have more specialized knowledge of the cost behavior patterns, they can use this knowledge opportunistically to reclassify “fixed” costs as “variable” for calculating the variable cost transfer price. This same argument also arises again in Chapter 10 when discussing variable costing.

I usually start class with Royal Resort and Casino (Case 5-4) to illustrate the interdependencies among divisions and how difficult it is for accounting systems to capture these interdependencies. Next, I spend about 15 minutes reviewing these major points, the remainder of class time is used discussing assigned problem material. A number of our students are marketing majors, so Stale-Mart (P5-18) always goes over well in class. XBT Keyboards (P5-25) provides a good example for demonstrating the incentives of managers operating under a variable costing transfer pricing rule to outsource those production methods with high fixed costs, thereby converting them into

Using the Text ©The McGraw-Hill Companies, Inc., 2011 xii Instructor’s Manual, Accounting for Decision Making and Control

variable costs. I always assign Celtex (Case 5-2), which is a shortened and simplified version of the old Birch Paper case. The students never suggest my solution, which always produces a lively and interesting class discussion. Recommended Problem Assignment

5-11 Cogen 5-12 University Lab Testing 5-18 Stale-Mart 5-20 Flat Images 5-24 Transfer Price Company 5-25 XBT Keyboards 5-26 Infantino Saab 5-28 Serviflow Case 5-2 Celtex Case 5-3 Executive Inn Case 5-4 Royal Resort and Casino

Chapter 6. Budgeting I begin the topic of budgeting by having the students prepare solutions to Potter-Bowen (P6-10) and Madden International (P6-24). These problems, drawn from actual company histories, use their budgeting systems in two very different ways. Potter-Bowen’s is a top-down decision control system, whereas Madden International’s is a bottom-up decision management scheme, designed to stimulate the assembly of specialized knowledge within the firm. These two polar extremes illustrate some key points:

• Firms make trade-offs involving decision management versus decision control in designing their budgeting system.

• Budgeting systems, like other parts of the firm’s organizational architecture,

must be matched and coordinated to the other parts of the architecture. There are complementarities among the various components.

These two problems also highlight the multiple roles served by budgeting systems. I emphasize that virtually all firms use budgets and that budgeting has survived for centuries. Thus, budgets are important financial mechanisms used by managers. To help illustrate what budgets do, use the simple dichotomy of decision management and decision control. Decision management versus control also helps explain a number of budgeting phenomena, such as long-term budgets, budget lapsing, line-item budgets, and zero-based budgets. A useful feature of this topic is that budgeting may be used to illustrate the ability of organizational architecture to explain observed institutional practices, such as why some firms use line item budgets and others do not.

Using the Text ©The McGraw-Hill Companies, Inc., 2011 Instructor’s Manual, Accounting for Decision Making and Control xiii

I like to teach the budgeting material right after introducing organizational architecture because, although not a technically demanding topic, it directly reinforces the organizational architecture material and allows some good examples of how to use the theoretical material in Chapter 4 to analyze actual company practice. Recommended Problem Assignment

6-7 Golf World 6-10 Potter-Bowen 6-17 Panarude Airfreight 6-20 Webb & Drye 6-21 Spa Ariana 6-22 Picture Maker 6-24 Madden International 6-25 Brehm Vineyards

Chapter 7. Cost Allocation: Theory I begin this chapter by having the students discuss their solutions to the Corporate Jet problem (P7-3). This is an example from an actual company that quickly piques the students’ interests in cost allocations. This problem also illustrates quite nicely that cost allocations are really just questions of transfer pricing. After about 15 minutes of student discussion, I review the major points from the first part of the chapter: the pervasiveness of cost allocations and some reasons for allocating costs. Since corporate income taxes and third-party reimbursements cannot explain the pervasiveness of allocations, issues of motivation and control must also be important considerations in those cases where taxes and reimbursement do not apply (e.g., non-profits). The analysis in this chapter is used to demonstrate how cost allocations can be used to affect behavior. Reviewing this material requires about 30 minutes of class time. The isoquants and budget lines in the Appendix are standard topics covered in every economics text. Using these microeconomic tools in the managerial accounting course helps to integrate the curriculum for the students. Applying the concepts they learned in economics reinforces the earlier material and shows them the benefits of how microeconomic tools can be applied to understand other management practices such as cost allocations. The topic of insulating versus noninsulating allocations again illustrates the inter-relations between performance measurement and other parts of the firm’s organizational architecture. For example, a firm might sometimes choose a noninsulating allocation scheme to foster cooperation. I also like to assign Avid Pharmaceuticals (P7-5), Encryption Inc. (P7-11), or Scanners Plus (P7-20) to illustrate how noninsulating cost allocations induce risk sharing. This discussion works to integrate the finance course with managerial accounting. Numerous problems highlight how cost allocation schemes affect behavior. My favorite problems are listed below. Students find this material very engaging. Plan to spend at least two hours of class time on this chapter, and make sure you assign enough

Using the Text ©The McGraw-Hill Companies, Inc., 2011 xiv Instructor’s Manual, Accounting for Decision Making and Control

class time to cover at least four or five problems. Also, continue to stress that cost allocations represent nothing more than transfer pricing problems. Recommended Problem Assignment

7-3 Corporate Jet 7-5 Avid Pharmaceuticals 7-6 Wasley 7-7 Hallsite Imaging 7-11 Encryption, Inc. 7-16 Vorma 7-17 Bio Labs 7-18 World Imports 7-19 Painting Department 7-20 Scanners Plus 7-22 Allied Adhesives 7-24 Plastic Chairs 7-25 Woodley Furniture 7-26 Transmation 7-27 BFR Ship Building Case 7-2 Durango Plastics

Chapter 8. Cost Allocation: Practices

Chapter 8 continues the discussion in Chapter 7, describing some of the practical problems encountered in cost allocations, including allocating service department costs and joint costs. In particular, with reciprocal service flows, the actual mechanics of cost allocation become fairly complicated. I use the allocation of service department costs (e.g., direct vs. step-down) to illustrate that, no matter how complex the calculations appear, in the end a transfer price results which can create incentives for managers to outsource the product or service. In some cases, this can lead to a death spiral. It is important that students understand the mechanical details of the various service department cost allocation methods because it builds their confidence that they can successfully analyze complex algorithms. Ultimately, they must address the joint questions of: do the resulting cost allocations approximate opportunity costs, and what incentives are likely created by the allocations? I spend about 10 minutes of class time having the students discuss and critique each others’ answers to Karsten Mills (P8-22). This is a real company death-spiral example which demonstrates that there are no simple solutions to many cost allocation/transfer pricing problems. I end this topic with Carlos Sanguine Winery (Case 8-1). This is another actual company. Several interesting aspects of this case include:

• This is a joint cost problem that the company did not recognize; • Allocating grape costs based on gallons was distorting the relative profitability

of the product lines;

Using the Text ©The McGraw-Hill Companies, Inc., 2011 Instructor’s Manual, Accounting for Decision Making and Control xv

• They were about to close a product line because it appeared unprofitable; • Before they could change accounting systems, they were acquired in an

unfriendly takeover (and my involvement with the firm ended). Recommended Problem Assignment

8-4 Mystic Herbals 8-10 Enzymes 8-11 Sunder Toys 8-12 WWWeb Marketing 8-15 Vigdor Wood Products 8-16 Advanced Micro Processors 8-21 RBB Brands 8-22 Karsten Mills 8-25 Littleton Medical Center 8-27 Grove City Broadcasting 8-31 IVAX Case 8-1 Carlos Sanguine Winery

Chapter 9. Absorption Cost Systems This chapter is a straightforward presentation of a traditional absorption costing system, focusing on the mechanics of absorption costing and leaving most of the analysis to the next two chapters. This chapter is kept simple and descriptive to insure that the students have a thorough grounding and understanding of the mechanics before a detailed analysis is presented. I like to give the students the “big picture” of the accounting system by presenting the usual cost flows through the accounts (Figure 9-1). This helps tie the managerial accounting course back to their financial accounting course. It also demonstrates that all manufacturing costs eventually flow through to the income statement. Tables 9-3 and 9-4 on costs and pricing in an oil change outlet is a unique way to introduce the idea of normal volume and tie it into the pricing decision. Thus, this material again allows the integration of the managerial economics and managerial accounting courses. This example provides a nice vehicle to illustrate how shifts in the demand curve cause volume and price changes, but as long as marginal cost is constant, prices should not be raised when demand falls (and average costs rise). Appendix B presents this material in more rigorous fashion. I begin the class by reviewing the mechanics for 15 minutes: the job order cost sheet and cost flows through the accounts (Figure 9-1). I then have the class discuss Hurst Mats (9-25), which illustrates how focusing on decision management versus decision control affects the choice of the allocation base to make sure everyone understands the technical details. The balance of class time is spent having the students discuss their answers to MacGiver Brass (P9-4) and Welding Robots (P9-17). MacGiver Brass involves a bank loan decision, which provides of the finance majors with an

Using the Text ©The McGraw-Hill Companies, Inc., 2011 xvi Instructor’s Manual, Accounting for Decision Making and Control

illustration of the importance of understanding cost accounting. Welding Robots integrates and reviews a number of key concepts: opportunity costs, fixed and variable costs, and job order costing. I do not cover the mechanics of process costing (Appendix A). Most of the students in the course are non-accounting majors and find the technical aspects of process costing dull. Instead, I make a few brief remarks that parallel the material in the last section of the chapter and refer them to Appendix A if they are interested. Recommended Problem Assignment

9-4 MacGiver Brass 9-5 Pool Scrubbers 9-6 Termalloy 9-12 Simple Plant 9-18 Digiear 9-20 Pebble Beach Sandal 9-25 Hurst Mats 9-27 Amalfi Texts 9-28 Pyramid Products

Chapter 10. Criticisms of Absorption Cost Systems: Incentive to Overproduce Having introduced the mechanics of absorption costing in Chapter 9, Chapters 10 and 11 analyze these systems. Chapter 10 discusses the incentives to overproduce, which leads to variable costing. Chapter 11 discusses the assertion that an absorption costing system miscosts some products, which leads to activity-based costing. Both of these chapters increase the students’ understanding of how traditional, absorption cost systems work. I begin the class with either Zipp Cards (P10-5) or Medford Mug Company (P10-11). These problems illustrate the incentive to overproduce under an absorption costing system. Having made sure everyone understands how overproduction lowers average cost (as long as marginal cost is not increasing), I then return to the text and review the numerical example in Tables 10-4 through 10-6. This illustration reintroduces the often overlooked, important question of who has the decision rights to determine fixed and variable cost. Managers still have the incentive to overproduce under a variable costing system if, at the end of the year, they can classify cost overruns as variable and thereby inventory them by overproducing. The incentive to reclassify fixed costs as variable is also present if a variable cost transfer pricing method is chosen. This again is another good opportunity to link absorption costing to transfer pricing. Absorption-based product costs are in fact transfer prices. Hence, the general theoretical issues discussed under transfer pricing also apply to absorption costing. Linking the discussion in Chapter 10 back to that in Chapter 5 helps to unify the course and to demonstrate that managerial accounting is not a set of unrelated computational methods. Transpacific Bank (P10-6) is another good problem for finance majors.

Using the Text ©The McGraw-Hill Companies, Inc., 2011 Instructor’s Manual, Accounting for Decision Making and Control xvii

Recommended Problem Assignment 10-5 Zipp Cards 10-6 Transpacific Bank 10-7 Zeflax Bottles 10-9 Aspen View 10-10 CLIC Lighters 10-11 Medford Mug Company 10-12 Kothari Inc. 10-13 Mystic Mugs 10-15 Taylor Chains 10-17 Dim 10-19 Weststar Appliances 10-22 Sants Brake Co. Case 10-1: Joon

Chapter 11. Criticisms of Absorption Cost Systems: Inaccurate Product Costs Chapter 11 discusses another criticism of absorption costing systems – inaccurate product costs. The proposed solution, activity-based costing, is also described. I introduce this topic by having the students discuss their solutions to several problems which demonstrate that traditional unit-level allocation bases can produce misleading product costs. Milan Pasta (P11-4) is a good example of miscosting. Having introduced the topic with this example, I spend about 20 minutes on ABC, describing how it differs from traditional unit-based absorption costing, and its advantages. I then ask the students, why haven’t more firms fully implemented ABC into their general ledger? Why are product costs for performance evaluation still based on unit-level allocations? These firms have already incurred the cost of calculating ABC product costs. Why don’t more firms change their performance measures to an ABC system? The ensuing discussion inevitably raises organizational issues. When you change the product costing system, some managers are made better off and some are made worse off, which leads to high influence costs. Some key points that should be made are:

• Adopting ABC constitutes a change in performance measures, requiring compensating changes in the performance reward system in order to keep the three-legged stool from becoming unbalanced. Tie this point back to Chapter 4.

• Lower-level managers with specialized knowledge of cost drivers must be

given the decision rights over choice of the cost drivers. These decision rights can be exercised opportunistically.

• Exercising this discretion over choice of cost drivers imposes control costs on

the firm. Usually decision control is harder under ABC than under a more centrally-managed absorption costing system.

Using the Text ©The McGraw-Hill Companies, Inc., 2011 xviii Instructor’s Manual, Accounting for Decision Making and Control

• Again, we see that the decision to use ABC versus absorption costing involves a trade-off between decision management and decision control. ABC is likely better for decision management, but worse for decision control. As with budgeting, a trade-off must be made between decision management and decision control. Figure 11-4 illustrates there is an optimum number of cost drivers.

Finally, I end the lecture by discussing Friendly Grocer (P11-9), Sanchez Gadgets (P11-11), Goodstone Tires (P11-15), or Familia Insurance Company (P11-18). The marketing majors like these problems. The key point of these problems is that, while ABC may give you a better understanding of your costs, it does not help in understanding revenues and the interdependencies among demand for various products offered by the firm. In Friendly Grocer (P11-9), even with ABC, shelf space costs are based on the historical cost of occupancy. Yet, the opportunity cost of shelf space is not the historical cost, it is the contribution margin of not stocking some other item and the effect of that item on the sales of other items stocked. If the grocery store did not stock milk, the sales of other products would fall. Neither an absorption costing nor an ABC system can capture these demand-side interdependencies. SnapOn Fasteners (Case 11-2) is based on the Mueller-Lehmkuhl case, but is shorter. It contains the essential features of Mueller-Lehmkuhl, but with a very different solution. Recommended Problem Assignment

11-4 Milan Pasta 11-6 Astin Car Stereos 11-8 True Cost Manufacturing, Inc. 11-9 Friendly Grocer 11-11 Sanchez Gadgets 11-14 Kay Enterprises 11-15 Goodstone Tires 11-18 Familia Insurance Company Case 11-2 SnapOn Fasteners

Chapter 12 Standard Costs: Direct Labor and Materials This chapter describes the mechanics and incentives of standard costs and variances. To prevent the lecture from becoming overly mechanical and dry, I continually emphasize the organizational issues and incentive effects of standard cost variances. I remind the class that agency problems require control mechanisms and that standard costs provide that control. By splitting the total direct material variance into a price variance and a quantity variance, the purchasing department is controlled by the price variance, and the production department is controlled by the quantity variance. But these are noisy measures of performance. Moreover, there are substantial interaction effects (externalities) among the various departments. And so while it is important that

Using the Text ©The McGraw-Hill Companies, Inc., 2011 Instructor’s Manual, Accounting for Decision Making and Control xix

students understand the computation of the variances, they should also be able to analyze the incentive effects of standard costs. I like to begin the lecture by discussing Great Southern Furniture (P12-15). The production setting being very intuitive and simple illustrates quite nicely how standards can be used for decision making (in this case how much to bid on the job) and decision control (a benchmark to evaluate actual performance). This problem also illustrates how a time study is used to set standards – a few sets of furniture are assembled and the time to assemble them is used as the standard. One of the more interesting issues in standard costing involves determining who has the decision rights to set and revise the standards and how frequently standards are revised. This involves the usual trade-off between decision management and decision control described in Chapter 6 (Budgets and Budgeting). The frequency of standard revisions also involves trading off decision management and decision control. One company has the policy, “We never, never revise the standards, except when we have to” (Changing Standards, P12-6). While this statement sounds silly on the surface, it really does have content. I use the 1970s example of the Hunt brothers, who tried to corner the silver market. In less than a year, silver prices roughly tripled. Silver is a major input to making photographic materials because silver compounds are light sensitive. If Kodak did not change its standard costs when silver prices tripled, poor decisions would result. For example, higher silver prices dictate that more resources should be expended in reclaiming spent silver from manufacturing and film processing. But managers will only expend more resources in silver reclamation if the standard price of silver is raised. Thus, the rule, “We never change our standards, except when we have to” makes sense in the following way. Changing standards involves a trade-off between decision management and decision control. Frequent standard changes reduce the ability of a standard cost system to hold managers accountable and reduce the control value of standard costs. However, if standards are not revised after very large changes, dysfunctional decision making occurs. Students should understand that standard costs and budgeting are closely related. To help reinforce this understanding, I use Oaks Auto Supply (P12-4) to introduce the topic of target costing. After working this problem and discussing target costing in general, I ask the students a couple of questions: With target costing, is the knowledge at the top or at the bottom of the organization? Is target costing a bottom-up or top-down system? What about standard costing? How do incentives change with target costing as opposed to standard costing? I then refer back to Chapter 6 on budgeting and remind them that some budgeting processes are top-down and others are bottom-up (participative budgeting). The best system for the firm is determined by the firm’s goals and other parts of the organizational architecture. Emphasize that “one size doesn’t fit all.” Covering the mechanics of calculating material and labor variances takes about an hour of class time. While the students generally understand the formulas after reading the chapter, a little class review reduces their anxiety level. I like to emphasize that all material and labor variances are unfavorable, in the sense that they indicate a deviation from plan. “Favorable” labor and material variances could indicate lower quality products are being produced.

Using the Text ©The McGraw-Hill Companies, Inc., 2011 xx Instructor’s Manual, Accounting for Decision Making and Control

I usually discuss either AN7-X1 (P12-5) or Zinc Faucets (P12-11) to justify why price variances are calculated when materials are purchased. This allows timely reporting of price variances instead of waiting until raw materials enter the manufacturing process. Hence, price (and wage rate) variances are computed based on actual quantities, not standard quantities. Since price changes of raw materials are useful data for pricing and production decisions, the timely reporting of price variances is useful for decision making, as well as control. I end the lecture by having the students discuss Domingo Cigars (Case 12-1). This problem provides a good combination of calculations and analysis of the incentive effects of the manufacturing process. Recommended Problem Assignment

12-1 Medical Instruments 12-4 Oaks Auto Supply 12-5 AN7-X1 12-6 Changing Standards 12-11 Zinc Faucets 12-15 Great Southern Furniture 12-16 Cibo Leathers 12-18 Starling Coatings Case 12-1 Domingo Cigars

Chapter 13. Overhead and Marketing Variances Chapter 13 illustrates how standard costs and variances can be defined in a variety of different contexts. The first part of the chapter concludes the calculation of manufacturing by computing overhead variances introduced in Chapter 12. A simple three overhead variance structure illustrates most of the substantive issues. I have found that more complicated four and five fixed and variable overhead variance systems add few insights to justify the additional computational complexity. The second half of the chapter describes marketing variances. I devote some time to discussing standard volume and how it differs from budgeted and actual volumes, an issue, which requires clarification for most students. I then spend 15 minutes discussing marketing variances, which marketing majors find more interesting than the manufacturing variances. I try to cover Chapter 13 in about an hour of class time.

Using the Text ©The McGraw-Hill Companies, Inc., 2011 Instructor’s Manual, Accounting for Decision Making and Control xxi

Recommended Problem Assignment 3-5 Oneida Metal 13-9 Western Sugar 13-10 Soldering Department 13-11 Commando Force 13-14 Turow Trailers 13-16 UOP 13-19 Ultrasonic 13-21 MRI Department

Chapter 14. Management Accounting in a Changing Environment

Chapter 14 is the most important chapter in the book, providing not only a conclusion (in contrast to other managerial accounting texts), but also a framework for understanding how managerial accounting changes in a dynamic world. The chapter also contains some end-of-chapter problems that review most of the major topics discussed in the book. I spend at least two hours of class time on Chapter 14. I begin the lecture by discussing Figure 14-1, a simplified version first introduced in Chapter 1. This important figure provides a framework that describes:

• How the internal accounting system is part of the firm’s organizational architecture;

• How the architecture is related to the firm’s business strategy; • How the firm’s business strategy depends on aspects of the external

environment, such as technology, market competition, and government regulation.

Figure 14-1 illustrates that the internal accounting system is not isolated from other policies of the firm. Based on Figure 14-1, several important insights are emphasized:

• Changes in the accounting system rarely occur in a vacuum. Accounting system changes generally occur at the same time as changes in the firm's business strategy and other organizational changes, particularly with regard to the partitioning of decision rights and the performance evaluation and reward systems.

• Alterations in the firm's organizational architecture, including changes in the

accounting system, are likely a response to changes in the firm's business strategy caused by external shocks from technology and shifting market conditions.

Using the Text ©The McGraw-Hill Companies, Inc., 2011 xxii Instructor’s Manual, Accounting for Decision Making and Control

• Before implementing an accounting or other organizational change, it is important to understand what is driving the change.

• An accounting system should not be adopted merely because other firms are

doing so; they may have different external shocks causing their previous systems to become obsolete.

• An accounting system should not be changed without concurrent, consistent

changes in the way decision rights are partitioned as well as in the performance reward systems. All three parts of the organization's architecture must be internally consistent and coordinated.

After describing Figure 14-1, I demonstrate how it applies to various organizational innovations: total quality management, JIT, Six Sigma and Lean Manufacturing, and the balanced score card. An assigned problem for each innovation is worked in class to ensure the students understand the basics. Then each innovation is analyzed, including the accounting system changes. I like to end the course by having the students discuss their solution to Telephone Computer Corporation (case 14-2). This case, which is based on an actual company, is a good comprehensive problem that reviews many of the topics discussed in the course. It requires the student to analyze a rather complicated business decision. In addition, the student must understand the organizational architecture/culture into which this particular decision fits.

Recommended Problem Assignment

14-2 Chateau Napa 14-3 Fiedler International 14-4 Guest Watches 14-8 Software Development, Inc. 14-9 Stirling Acquisition 14-12 Warren City Parts Manufacturing 14-13 Secure Servers Inc. Case 14-1 Global Oil Case 14-2 Telephone Computer Corporation (TCC)

Using the Text ©The McGraw-Hill Companies, Inc., 2011 Instructor’s Manual, Accounting for Decision Making and Control

xxiii

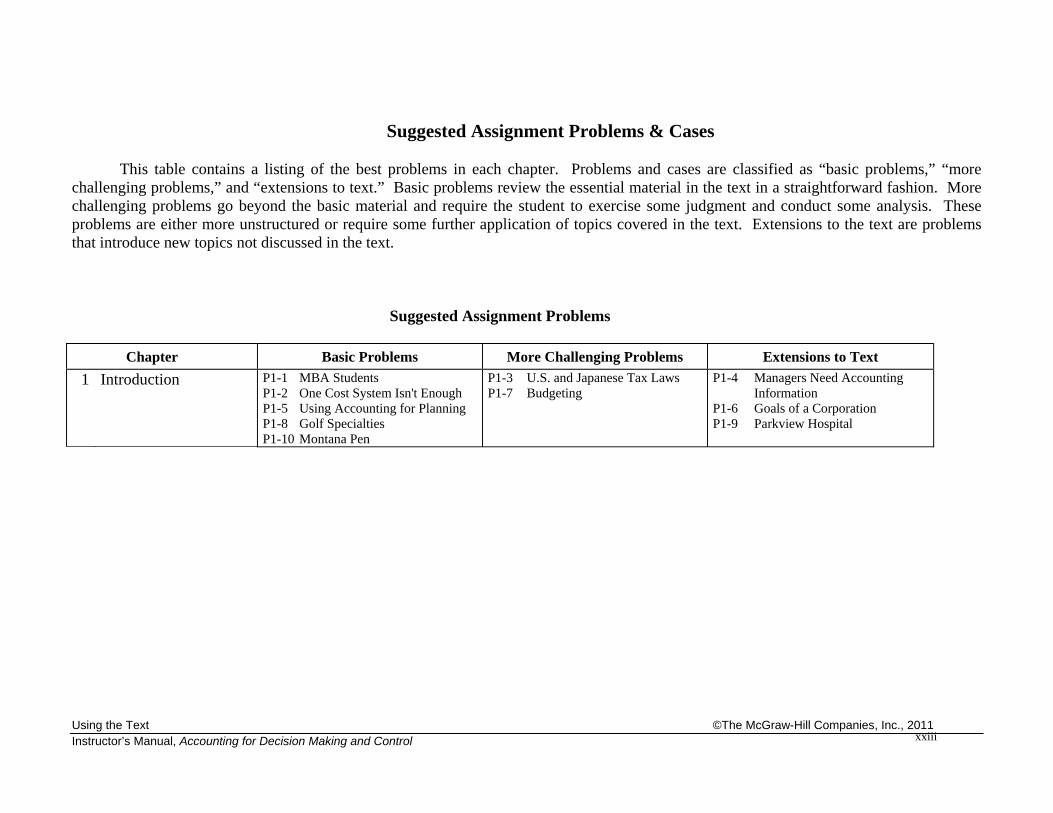

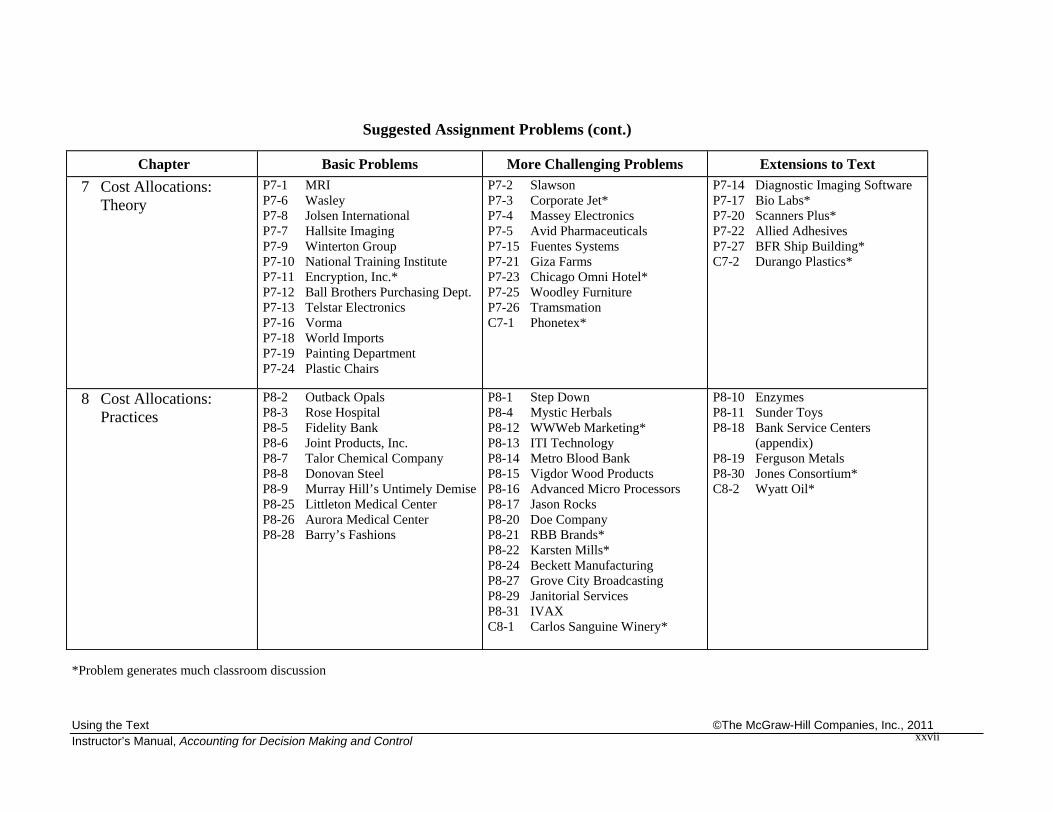

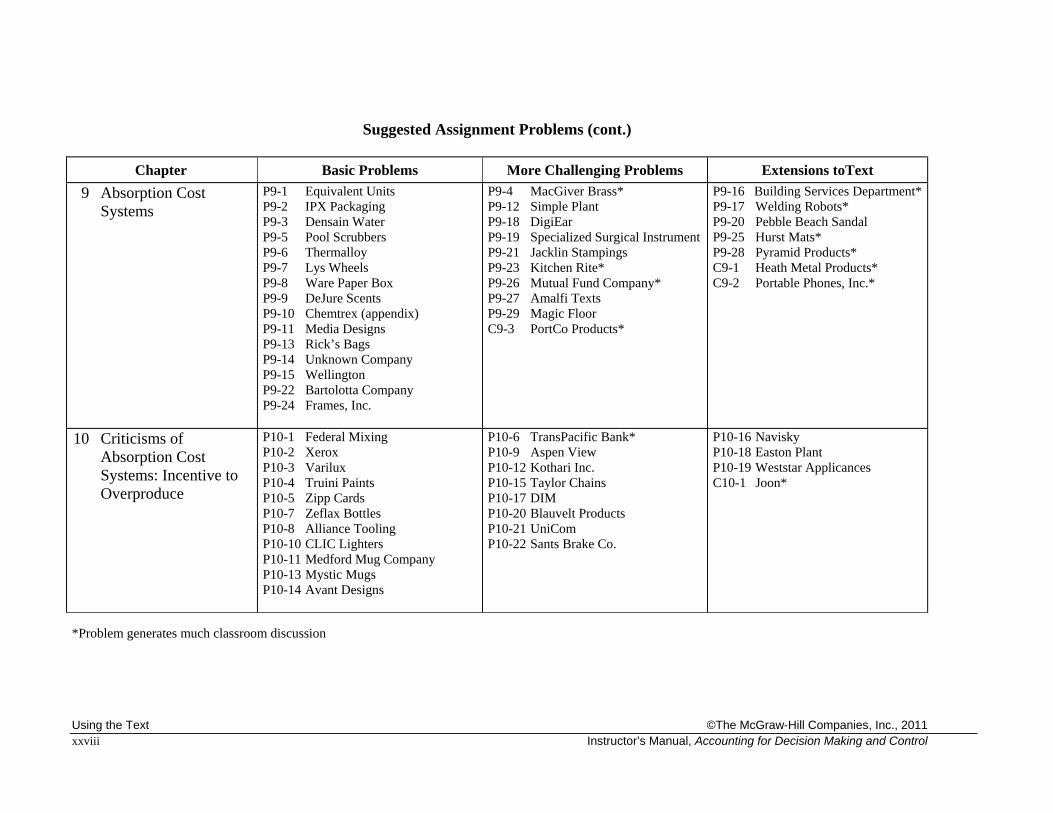

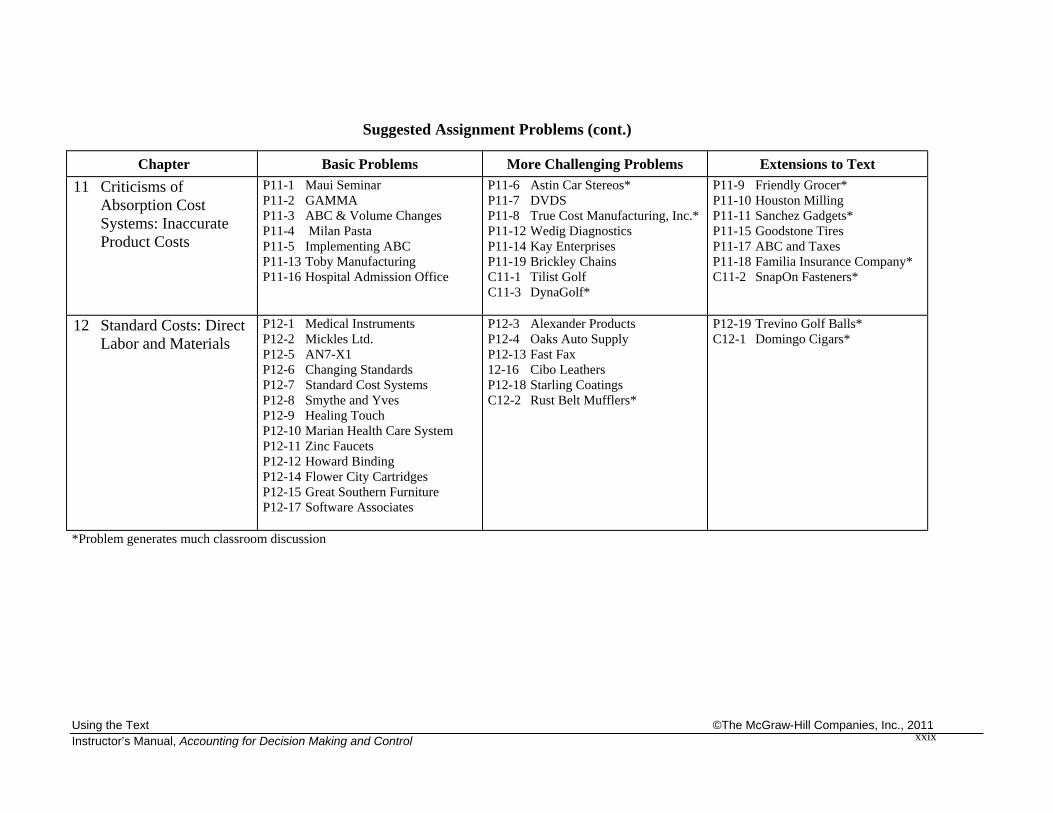

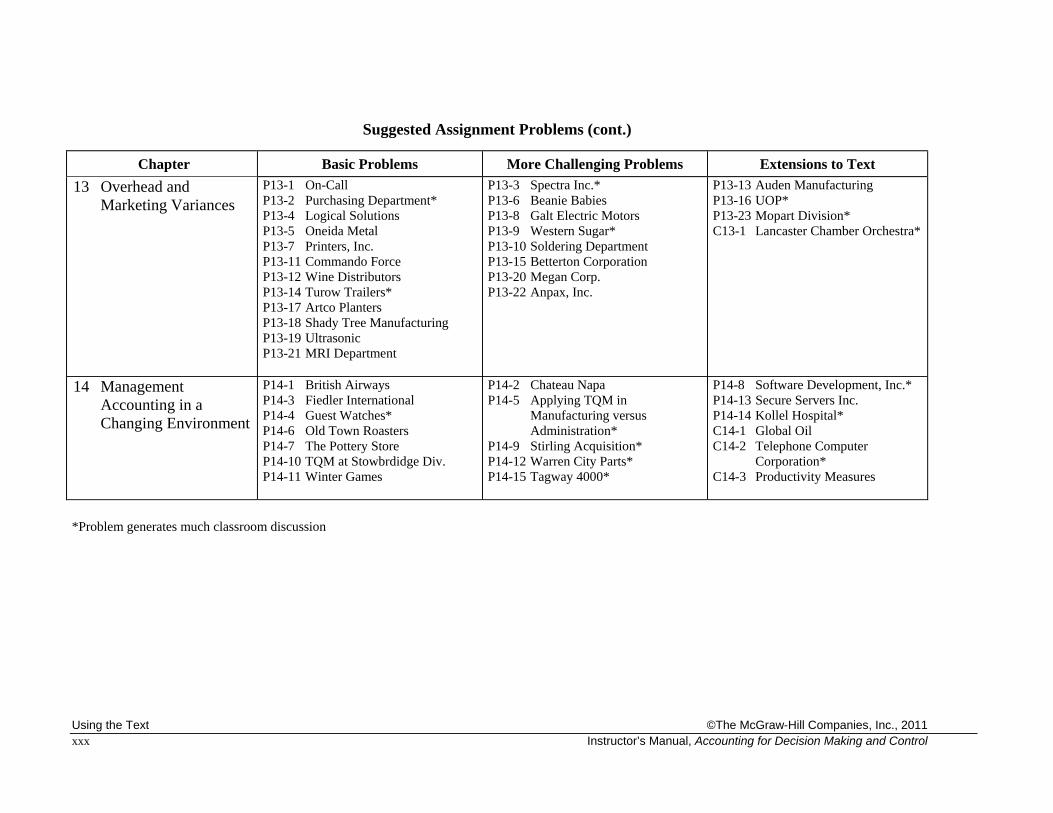

Suggested Assignment Problems & Cases

This table contains a listing of the best problems in each chapter. Problems and cases are classified as “basic problems,” “more

challenging problems,” and “extensions to text.” Basic problems review the essential material in the text in a straightforward fashion. More challenging problems go beyond the basic material and require the student to exercise some judgment and conduct some analysis. These problems are either more unstructured or require some further application of topics covered in the text. Extensions to the text are problems that introduce new topics not discussed in the text.

Suggested Assignment Problems

Chapter Basic Problems More Challenging Problems Extensions to Text

1 Introduction P1-1 MBA Students P1-2 One Cost System Isn't Enough P1-5 Using Accounting for Planning P1-8 Golf Specialties P1-10 Montana Pen

P1-3 U.S. and Japanese Tax Laws P1-7 Budgeting

P1-4 Managers Need Accounting Information

P1-6 Goals of a Corporation P1-9 Parkview Hospital

Using the Text ©The McGraw-Hill Companies, Inc., 2011 xxiv Instructor’s Manual, Accounting for Decision Making and Control

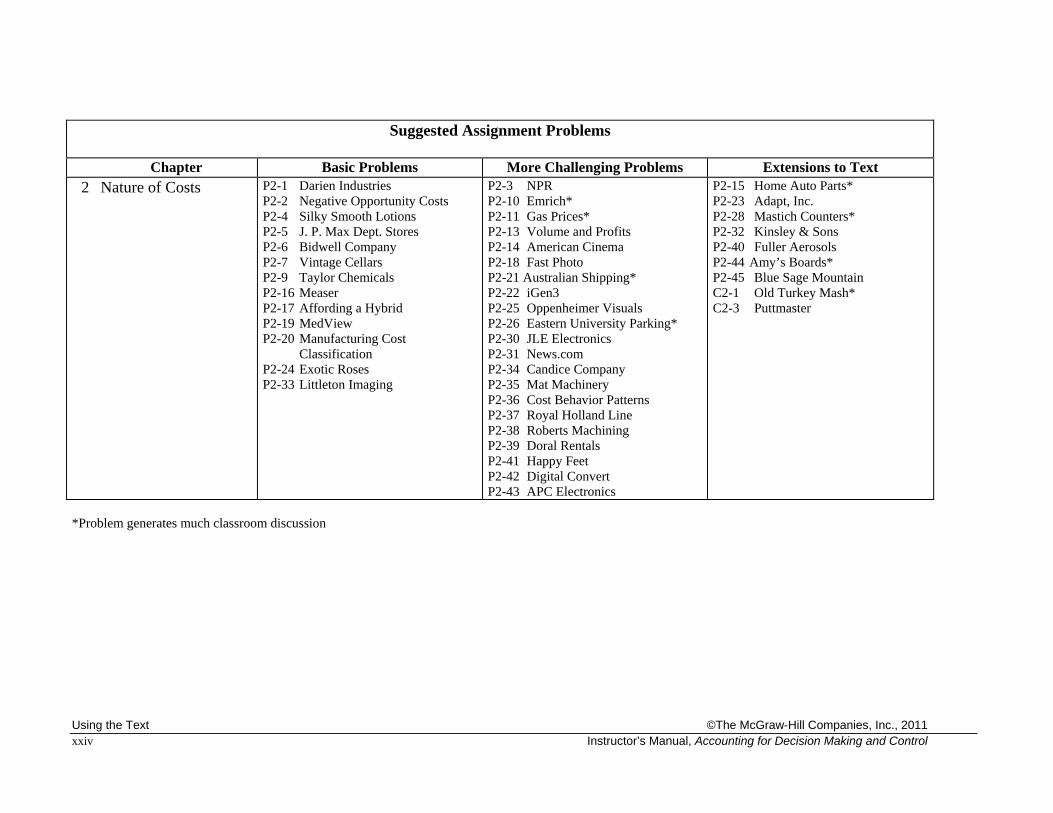

Suggested Assignment Problems

Chapter Basic Problems More Challenging Problems Extensions to Text

2 Nature of Costs P2-1 Darien Industries P2-2 Negative Opportunity Costs P2-4 Silky Smooth Lotions P2-5 J. P. Max Dept. Stores P2-6 Bidwell Company P2-7 Vintage Cellars P2-9 Taylor Chemicals P2-16 Measer P2-17 Affording a Hybrid P2-19 MedView P2-20 Manufacturing Cost

Classification P2-24 Exotic Roses P2-33 Littleton Imaging

P2-3 NPR P2-10 Emrich* P2-11 Gas Prices* P2-13 Volume and Profits P2-14 American Cinema P2-18 Fast Photo P2-21 Australian Shipping* P2-22 iGen3 P2-25 Oppenheimer Visuals P2-26 Eastern University Parking* P2-30 JLE Electronics P2-31 News.com P2-34 Candice Company P2-35 Mat Machinery P2-36 Cost Behavior Patterns P2-37 Royal Holland Line P2-38 Roberts Machining P2-39 Doral Rentals P2-41 Happy Feet P2-42 Digital Convert P2-43 APC Electronics

P2-15 Home Auto Parts* P2-23 Adapt, Inc. P2-28 Mastich Counters* P2-32 Kinsley & Sons P2-40 Fuller Aerosols P2-44 Amy’s Boards* P2-45 Blue Sage Mountain C2-1 Old Turkey Mash* C2-3 Puttmaster

*Problem generates much classroom discussion

Using the Text ©The McGraw-Hill Companies, Inc., 2011 Instructor’s Manual, Accounting for Decision Making and Control

xxv

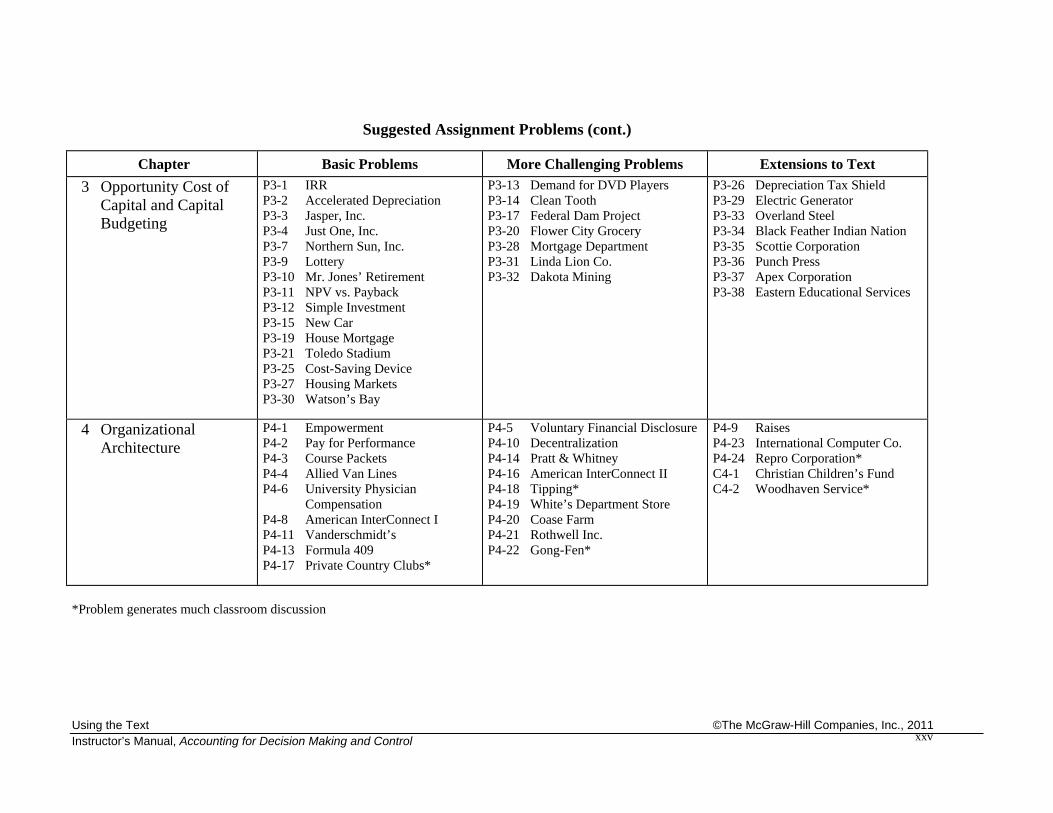

Suggested Assignment Problems (cont.)

Chapter Basic Problems More Challenging Problems Extensions to Text

3 Opportunity Cost of Capital and Capital Budgeting

P3-1 IRR P3-2 Accelerated Depreciation P3-3 Jasper, Inc. P3-4 Just One, Inc. P3-7 Northern Sun, Inc. P3-9 Lottery P3-10 Mr. Jones’ Retirement P3-11 NPV vs. Payback P3-12 Simple Investment P3-15 New Car P3-19 House Mortgage P3-21 Toledo Stadium P3-25 Cost-Saving Device P3-27 Housing Markets P3-30 Watson’s Bay

P3-13 Demand for DVD Players P3-14 Clean Tooth P3-17 Federal Dam Project P3-20 Flower City Grocery P3-28 Mortgage Department P3-31 Linda Lion Co. P3-32 Dakota Mining

P3-26 Depreciation Tax Shield P3-29 Electric Generator P3-33 Overland Steel P3-34 Black Feather Indian Nation P3-35 Scottie Corporation P3-36 Punch Press P3-37 Apex Corporation P3-38 Eastern Educational Services

4 Organizational Architecture

P4-1 Empowerment P4-2 Pay for Performance P4-3 Course Packets P4-4 Allied Van Lines P4-6 University Physician

Compensation P4-8 American InterConnect I P4-11 Vanderschmidt’s P4-13 Formula 409 P4-17 Private Country Clubs*

P4-5 Voluntary Financial Disclosure P4-10 Decentralization P4-14 Pratt & Whitney P4-16 American InterConnect II P4-18 Tipping* P4-19 White’s Department Store P4-20 Coase Farm P4-21 Rothwell Inc. P4-22 Gong-Fen*

P4-9 Raises P4-23 International Computer Co. P4-24 Repro Corporation* C4-1 Christian Children’s Fund C4-2 Woodhaven Service*

*Problem generates much classroom discussion

Using the Text ©The McGraw-Hill Companies, Inc., 2011 xxvi Instructor’s Manual, Accounting for Decision Making and Control

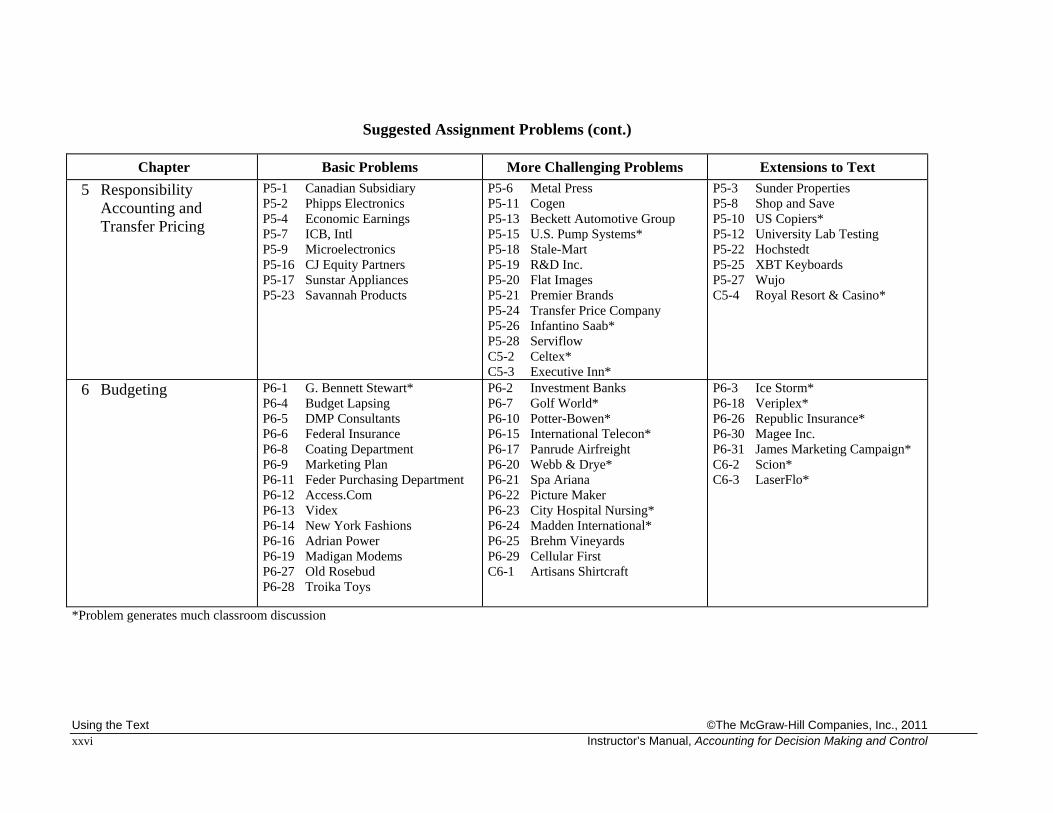

Suggested Assignment Problems (cont.)

Chapter Basic Problems More Challenging Problems Extensions to Text

5 Responsibility Accounting and Transfer Pricing

P5-1 Canadian Subsidiary P5-2 Phipps Electronics P5-4 Economic Earnings P5-7 ICB, Intl P5-9 Microelectronics P5-16 CJ Equity Partners P5-17 Sunstar Appliances P5-23 Savannah Products

P5-6 Metal Press P5-11 Cogen P5-13 Beckett Automotive Group P5-15 U.S. Pump Systems* P5-18 Stale-Mart P5-19 R&D Inc. P5-20 Flat Images P5-21 Premier Brands P5-24 Transfer Price Company P5-26 Infantino Saab* P5-28 Serviflow C5-2 Celtex* C5-3 Executive Inn*

P5-3 Sunder Properties P5-8 Shop and Save P5-10 US Copiers* P5-12 University Lab Testing P5-22 Hochstedt P5-25 XBT Keyboards P5-27 Wujo C5-4 Royal Resort & Casino*

6 Budgeting P6-1 G. Bennett Stewart* P6-4 Budget Lapsing P6-5 DMP Consultants P6-6 Federal Insurance P6-8 Coating Department P6-9 Marketing Plan P6-11 Feder Purchasing Department P6-12 Access.Com P6-13 Videx P6-14 New York Fashions P6-16 Adrian Power P6-19 Madigan Modems P6-27 Old Rosebud P6-28 Troika Toys

P6-2 Investment Banks P6-7 Golf World* P6-10 Potter-Bowen* P6-15 International Telecon* P6-17 Panrude Airfreight P6-20 Webb & Drye* P6-21 Spa Ariana P6-22 Picture Maker P6-23 City Hospital Nursing* P6-24 Madden International* P6-25 Brehm Vineyards P6-29 Cellular First C6-1 Artisans Shirtcraft

P6-3 Ice Storm* P6-18 Veriplex* P6-26 Republic Insurance* P6-30 Magee Inc. P6-31 James Marketing Campaign* C6-2 Scion* C6-3 LaserFlo*

*Problem generates much classroom discussion

Using the Text ©The McGraw-Hill Companies, Inc., 2011 Instructor’s Manual, Accounting for Decision Making and Control

xxvii

Suggested Assignment Problems (cont.)

Chapter Basic Problems More Challenging Problems Extensions to Text

7 Cost Allocations: Theory

P7-1 MRI P7-6 Wasley P7-8 Jolsen International P7-7 Hallsite Imaging P7-9 Winterton Group P7-10 National Training Institute P7-11 Encryption, Inc.* P7-12 Ball Brothers Purchasing Dept. P7-13 Telstar Electronics P7-16 Vorma P7-18 World Imports P7-19 Painting Department P7-24 Plastic Chairs

P7-2 Slawson P7-3 Corporate Jet* P7-4 Massey Electronics P7-5 Avid Pharmaceuticals P7-15 Fuentes Systems P7-21 Giza Farms P7-23 Chicago Omni Hotel* P7-25 Woodley Furniture P7-26 Tramsmation C7-1 Phonetex*

P7-14 Diagnostic Imaging Software P7-17 Bio Labs* P7-20 Scanners Plus* P7-22 Allied Adhesives P7-27 BFR Ship Building* C7-2 Durango Plastics*

8 Cost Allocations: Practices

P8-2 Outback Opals P8-3 Rose Hospital P8-5 Fidelity Bank P8-6 Joint Products, Inc. P8-7 Talor Chemical Company P8-8 Donovan Steel P8-9 Murray Hill’s Untimely DemiseP8-25 Littleton Medical Center P8-26 Aurora Medical Center P8-28 Barry’s Fashions

P8-1 Step Down P8-4 Mystic Herbals P8-12 WWWeb Marketing* P8-13 ITI Technology P8-14 Metro Blood Bank P8-15 Vigdor Wood Products P8-16 Advanced Micro Processors P8-17 Jason Rocks P8-20 Doe Company P8-21 RBB Brands* P8-22 Karsten Mills* P8-24 Beckett Manufacturing P8-27 Grove City Broadcasting P8-29 Janitorial Services P8-31 IVAX C8-1 Carlos Sanguine Winery*

P8-10 Enzymes P8-11 Sunder Toys P8-18 Bank Service Centers

(appendix) P8-19 Ferguson Metals P8-30 Jones Consortium* C8-2 Wyatt Oil*

*Problem generates much classroom discussion

Using the Text ©The McGraw-Hill Companies, Inc., 2011 xxviii Instructor’s Manual, Accounting for Decision Making and Control

Suggested Assignment Problems (cont.)

Chapter Basic Problems More Challenging Problems Extensions toText

9 Absorption Cost Systems

P9-1 Equivalent Units P9-2 IPX Packaging P9-3 Densain Water P9-5 Pool Scrubbers P9-6 Thermalloy P9-7 Lys Wheels P9-8 Ware Paper Box P9-9 DeJure Scents P9-10 Chemtrex (appendix) P9-11 Media Designs P9-13 Rick’s Bags P9-14 Unknown Company P9-15 Wellington P9-22 Bartolotta Company P9-24 Frames, Inc.

P9-4 MacGiver Brass* P9-12 Simple Plant P9-18 DigiEar P9-19 Specialized Surgical Instrument P9-21 Jacklin Stampings P9-23 Kitchen Rite* P9-26 Mutual Fund Company* P9-27 Amalfi Texts P9-29 Magic Floor C9-3 PortCo Products*

P9-16 Building Services Department*P9-17 Welding Robots* P9-20 Pebble Beach Sandal P9-25 Hurst Mats* P9-28 Pyramid Products* C9-1 Heath Metal Products* C9-2 Portable Phones, Inc.*

10 Criticisms of Absorption Cost Systems: Incentive to Overproduce

P10-1 Federal Mixing P10-2 Xerox P10-3 Varilux P10-4 Truini Paints P10-5 Zipp Cards P10-7 Zeflax Bottles P10-8 Alliance Tooling P10-10 CLIC Lighters P10-11 Medford Mug Company P10-13 Mystic Mugs P10-14 Avant Designs

P10-6 TransPacific Bank* P10-9 Aspen View P10-12 Kothari Inc. P10-15 Taylor Chains P10-17 DIM P10-20 Blauvelt Products P10-21 UniCom P10-22 Sants Brake Co.

P10-16 Navisky P10-18 Easton Plant P10-19 Weststar Applicances C10-1 Joon*

*Problem generates much classroom discussion

Using the Text ©The McGraw-Hill Companies, Inc., 2011 Instructor’s Manual, Accounting for Decision Making and Control

xxix

Suggested Assignment Problems (cont.)

Chapter Basic Problems More Challenging Problems Extensions to Text

11 Criticisms of Absorption Cost Systems: Inaccurate Product Costs

P11-1 Maui Seminar P11-2 GAMMA P11-3 ABC & Volume Changes P11-4 Milan Pasta P11-5 Implementing ABC P11-13 Toby Manufacturing P11-16 Hospital Admission Office

P11-6 Astin Car Stereos* P11-7 DVDS P11-8 True Cost Manufacturing, Inc.* P11-12 Wedig Diagnostics P11-14 Kay Enterprises P11-19 Brickley Chains C11-1 Tilist Golf C11-3 DynaGolf*

P11-9 Friendly Grocer* P11-10 Houston Milling P11-11 Sanchez Gadgets* P11-15 Goodstone Tires P11-17 ABC and Taxes P11-18 Familia Insurance Company* C11-2 SnapOn Fasteners*

12 Standard Costs: Direct Labor and Materials

P12-1 Medical Instruments P12-2 Mickles Ltd. P12-5 AN7-X1 P12-6 Changing Standards P12-7 Standard Cost Systems P12-8 Smythe and Yves P12-9 Healing Touch P12-10 Marian Health Care System P12-11 Zinc Faucets P12-12 Howard Binding P12-14 Flower City Cartridges P12-15 Great Southern Furniture P12-17 Software Associates

P12-3 Alexander Products P12-4 Oaks Auto Supply P12-13 Fast Fax 12-16 Cibo Leathers P12-18 Starling Coatings C12-2 Rust Belt Mufflers*

P12-19 Trevino Golf Balls* C12-1 Domingo Cigars*

*Problem generates much classroom discussion

Using the Text ©The McGraw-Hill Companies, Inc., 2011 xxx Instructor’s Manual, Accounting for Decision Making and Control

Suggested Assignment Problems (cont.)

Chapter Basic Problems More Challenging Problems Extensions to Text

13 Overhead and Marketing Variances

P13-1 On-Call P13-2 Purchasing Department* P13-4 Logical Solutions P13-5 Oneida Metal P13-7 Printers, Inc. P13-11 Commando Force P13-12 Wine Distributors P13-14 Turow Trailers* P13-17 Artco Planters P13-18 Shady Tree Manufacturing P13-19 Ultrasonic P13-21 MRI Department

P13-3 Spectra Inc.* P13-6 Beanie Babies P13-8 Galt Electric Motors P13-9 Western Sugar* P13-10 Soldering Department P13-15 Betterton Corporation P13-20 Megan Corp. P13-22 Anpax, Inc.

P13-13 Auden Manufacturing P13-16 UOP* P13-23 Mopart Division* C13-1 Lancaster Chamber Orchestra*

14 Management Accounting in a Changing Environment

P14-1 British Airways P14-3 Fiedler International P14-4 Guest Watches* P14-6 Old Town Roasters P14-7 The Pottery Store P14-10 TQM at Stowbrdidge Div. P14-11 Winter Games

P14-2 Chateau Napa P14-5 Applying TQM in

Manufacturing versus Administration*

P14-9 Stirling Acquisition* P14-12 Warren City Parts* P14-15 Tagway 4000*

P14-8 Software Development, Inc.* P14-13 Secure Servers Inc. P14-14 Kollel Hospital* C14-1 Global Oil C14-2 Telephone Computer

Corporation* C14-3 Productivity Measures

*Problem generates much classroom discussion

Using the Text ©The McGraw-Hill Companies, Inc., 2011 Instructor’s Manual, Accounting for Decision Making and Control

xxxi

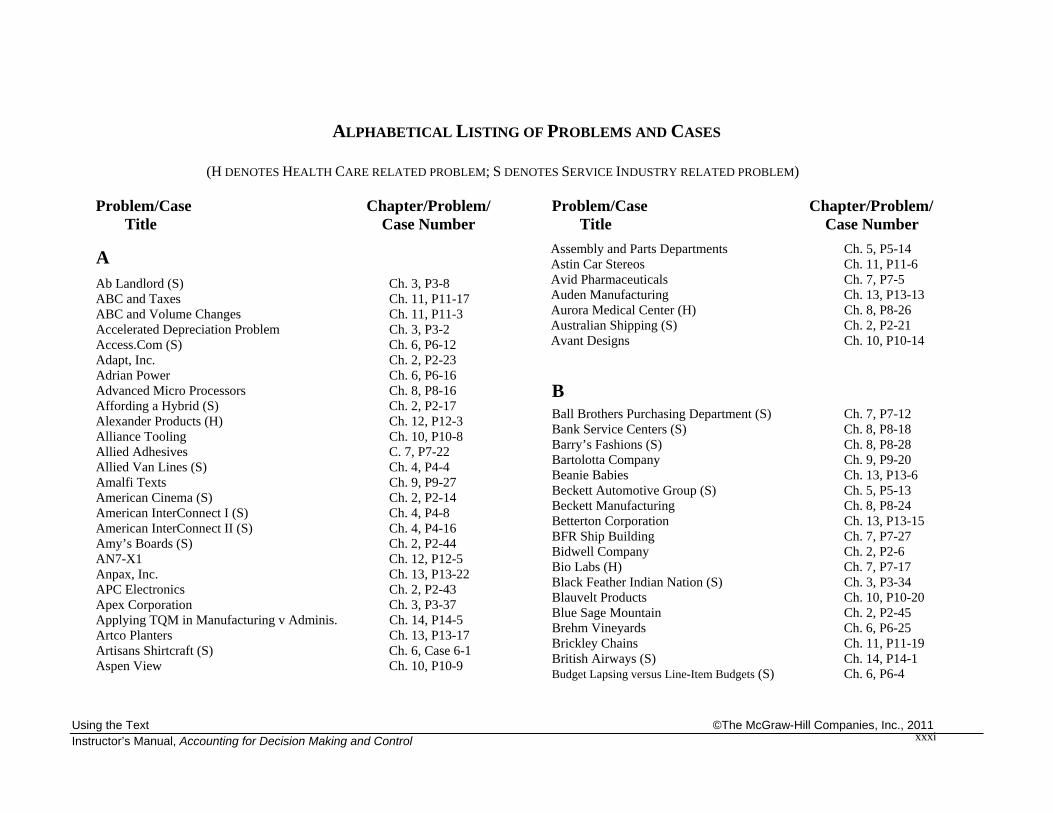

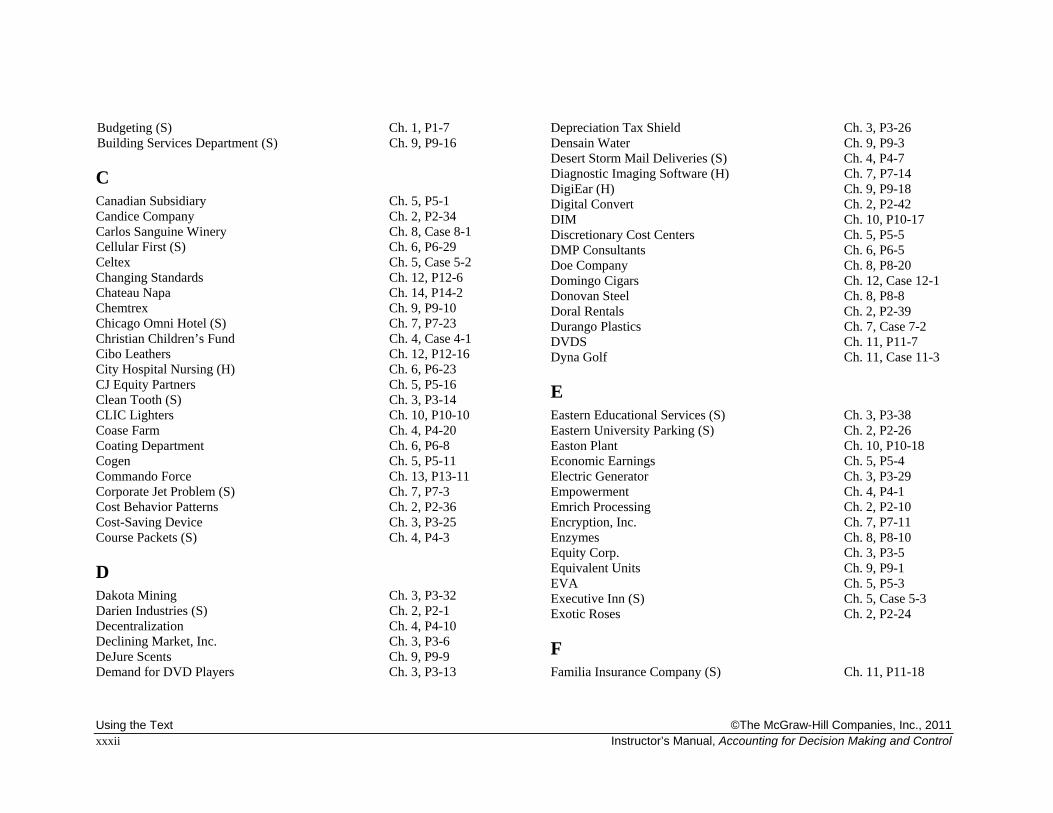

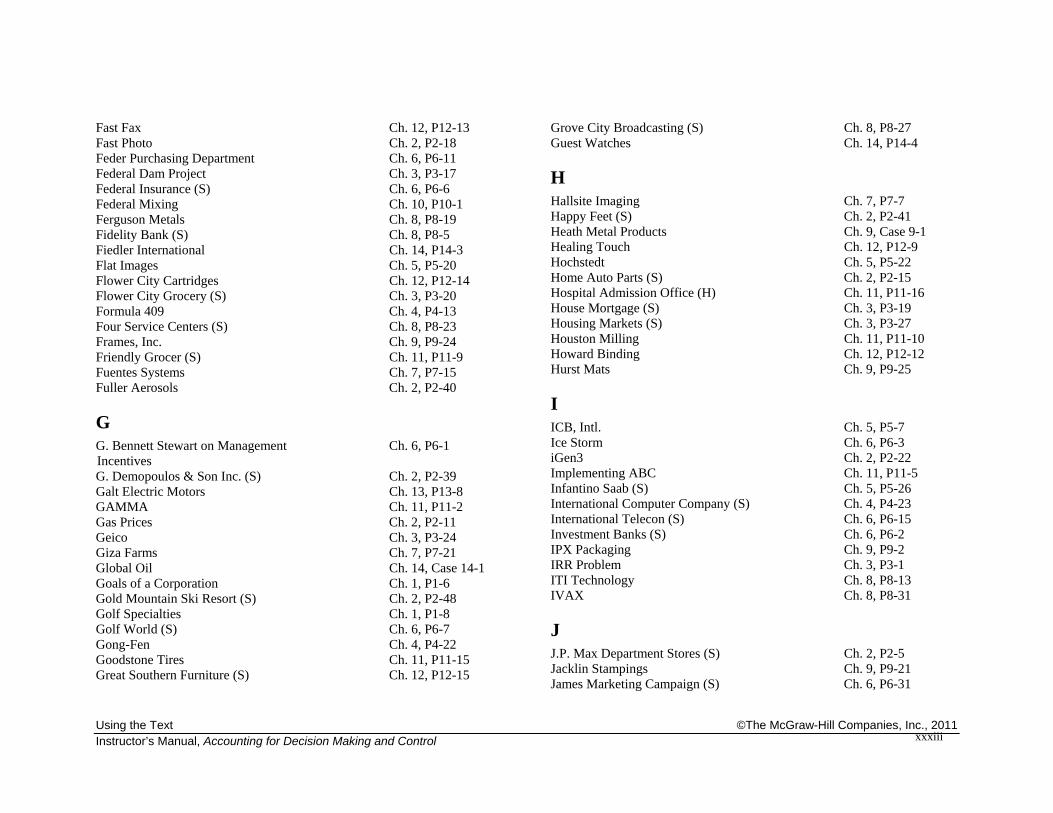

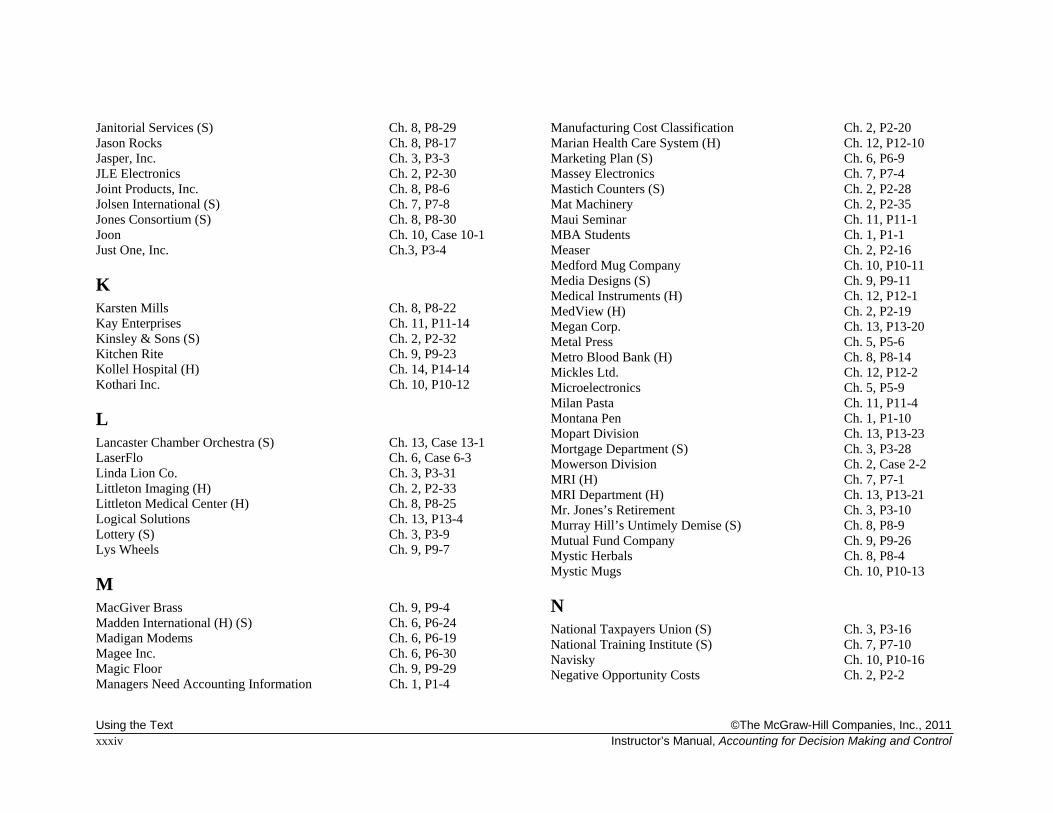

ALPHABETICAL LISTING OF PROBLEMS AND CASES

(H DENOTES HEALTH CARE RELATED PROBLEM; S DENOTES SERVICE INDUSTRY RELATED PROBLEM)

Problem/Case Title

Chapter/Problem/ Case Number

A

Ab Landlord (S) Ch. 3, P3-8 ABC and Taxes Ch. 11, P11-17 ABC and Volume Changes Ch. 11, P11-3 Accelerated Depreciation Problem Ch. 3, P3-2 Access.Com (S) Ch. 6, P6-12 Adapt, Inc. Ch. 2, P2-23 Adrian Power Ch. 6, P6-16 Advanced Micro Processors Ch. 8, P8-16 Affording a Hybrid (S) Ch. 2, P2-17 Alexander Products (H) Ch. 12, P12-3 Alliance Tooling Ch. 10, P10-8 Allied Adhesives C. 7, P7-22 Allied Van Lines (S) Ch. 4, P4-4 Amalfi Texts Ch. 9, P9-27 American Cinema (S) Ch. 2, P2-14 American InterConnect I (S) Ch. 4, P4-8 American InterConnect II (S) Ch. 4, P4-16 Amy’s Boards (S) Ch. 2, P2-44 AN7-X1 Ch. 12, P12-5 Anpax, Inc. Ch. 13, P13-22 APC Electronics Ch. 2, P2-43 Apex Corporation Ch. 3, P3-37 Applying TQM in Manufacturing v Adminis. Ch. 14, P14-5 Artco Planters Ch. 13, P13-17 Artisans Shirtcraft (S) Ch. 6, Case 6-1 Aspen View Ch. 10, P10-9

Problem/Case Title

Chapter/Problem/ Case Number

Assembly and Parts Departments Ch. 5, P5-14 Astin Car Stereos Ch. 11, P11-6 Avid Pharmaceuticals Ch. 7, P7-5 Auden Manufacturing Ch. 13, P13-13 Aurora Medical Center (H) Ch. 8, P8-26 Australian Shipping (S) Ch. 2, P2-21 Avant Designs Ch. 10, P10-14

B Ball Brothers Purchasing Department (S) Ch. 7, P7-12 Bank Service Centers (S) Ch. 8, P8-18 Barry’s Fashions (S) Ch. 8, P8-28 Bartolotta Company Ch. 9, P9-20 Beanie Babies Ch. 13, P13-6 Beckett Automotive Group (S) Ch. 5, P5-13 Beckett Manufacturing Ch. 8, P8-24 Betterton Corporation Ch. 13, P13-15 BFR Ship Building Ch. 7, P7-27 Bidwell Company Ch. 2, P2-6 Bio Labs (H) Ch. 7, P7-17 Black Feather Indian Nation (S) Ch. 3, P3-34 Blauvelt Products Ch. 10, P10-20 Blue Sage Mountain Ch. 2, P2-45 Brehm Vineyards Ch. 6, P6-25 Brickley Chains Ch. 11, P11-19 British Airways (S) Ch. 14, P14-1 Budget Lapsing versus Line-Item Budgets (S) Ch. 6, P6-4

Using the Text ©The McGraw-Hill Companies, Inc., 2011 xxxii Instructor’s Manual, Accounting for Decision Making and Control

Budgeting (S) Ch. 1, P1-7 Building Services Department (S) Ch. 9, P9-16

C

Canadian Subsidiary Ch. 5, P5-1 Candice Company Ch. 2, P2-34 Carlos Sanguine Winery Ch. 8, Case 8-1 Cellular First (S) Ch. 6, P6-29 Celtex Ch. 5, Case 5-2 Changing Standards Ch. 12, P12-6 Chateau Napa Ch. 14, P14-2 Chemtrex Ch. 9, P9-10 Chicago Omni Hotel (S) Ch. 7, P7-23 Christian Children’s Fund Ch. 4, Case 4-1 Cibo Leathers Ch. 12, P12-16 City Hospital Nursing (H) Ch. 6, P6-23 CJ Equity Partners Ch. 5, P5-16 Clean Tooth (S) Ch. 3, P3-14 CLIC Lighters Ch. 10, P10-10 Coase Farm Ch. 4, P4-20 Coating Department Ch. 6, P6-8 Cogen Ch. 5, P5-11 Commando Force Ch. 13, P13-11 Corporate Jet Problem (S) Ch. 7, P7-3 Cost Behavior Patterns Ch. 2, P2-36 Cost-Saving Device Ch. 3, P3-25 Course Packets (S) Ch. 4, P4-3

D

Dakota Mining Ch. 3, P3-32 Darien Industries (S) Ch. 2, P2-1 Decentralization Ch. 4, P4-10 Declining Market, Inc. Ch. 3, P3-6 DeJure Scents Ch. 9, P9-9 Demand for DVD Players Ch. 3, P3-13

Depreciation Tax Shield Ch. 3, P3-26 Densain Water Ch. 9, P9-3 Desert Storm Mail Deliveries (S) Ch. 4, P4-7 Diagnostic Imaging Software (H) Ch. 7, P7-14 DigiEar (H) Ch. 9, P9-18 Digital Convert Ch. 2, P2-42 DIM Ch. 10, P10-17 Discretionary Cost Centers Ch. 5, P5-5 DMP Consultants Ch. 6, P6-5 Doe Company Ch. 8, P8-20 Domingo Cigars Ch. 12, Case 12-1 Donovan Steel Ch. 8, P8-8 Doral Rentals Ch. 2, P2-39 Durango Plastics Ch. 7, Case 7-2 DVDS Ch. 11, P11-7 Dyna Golf Ch. 11, Case 11-3

E

Eastern Educational Services (S) Ch. 3, P3-38 Eastern University Parking (S) Ch. 2, P2-26 Easton Plant Ch. 10, P10-18 Economic Earnings Ch. 5, P5-4 Electric Generator Ch. 3, P3-29 Empowerment Ch. 4, P4-1 Emrich Processing Ch. 2, P2-10 Encryption, Inc. Ch. 7, P7-11 Enzymes Ch. 8, P8-10 Equity Corp. Ch. 3, P3-5 Equivalent Units Ch. 9, P9-1 EVA Ch. 5, P5-3 Executive Inn (S) Ch. 5, Case 5-3 Exotic Roses Ch. 2, P2-24

F

Familia Insurance Company (S) Ch. 11, P11-18

Using the Text ©The McGraw-Hill Companies, Inc., 2011 Instructor’s Manual, Accounting for Decision Making and Control

xxxiii

Fast Fax Ch. 12, P12-13 Fast Photo Ch. 2, P2-18 Feder Purchasing Department Ch. 6, P6-11 Federal Dam Project Ch. 3, P3-17 Federal Insurance (S) Ch. 6, P6-6 Federal Mixing Ch. 10, P10-1 Ferguson Metals Ch. 8, P8-19 Fidelity Bank (S) Ch. 8, P8-5 Fiedler International Ch. 14, P14-3 Flat Images Ch. 5, P5-20 Flower City Cartridges Ch. 12, P12-14 Flower City Grocery (S) Ch. 3, P3-20 Formula 409 Ch. 4, P4-13 Four Service Centers (S) Ch. 8, P8-23 Frames, Inc. Ch. 9, P9-24 Friendly Grocer (S) Ch. 11, P11-9 Fuentes Systems Ch. 7, P7-15 Fuller Aerosols Ch. 2, P2-40

G

G. Bennett Stewart on Management Incentives

Ch. 6, P6-1

G. Demopoulos & Son Inc. (S) Ch. 2, P2-39 Galt Electric Motors Ch. 13, P13-8 GAMMA Ch. 11, P11-2 Gas Prices Ch. 2, P2-11 Geico Ch. 3, P3-24 Giza Farms Ch. 7, P7-21 Global Oil Ch. 14, Case 14-1 Goals of a Corporation Ch. 1, P1-6 Gold Mountain Ski Resort (S) Ch. 2, P2-48 Golf Specialties Ch. 1, P1-8 Golf World (S) Ch. 6, P6-7 Gong-Fen Ch. 4, P4-22 Goodstone Tires Ch. 11, P11-15 Great Southern Furniture (S) Ch. 12, P12-15

Grove City Broadcasting (S) Ch. 8, P8-27 Guest Watches Ch. 14, P14-4

H

Hallsite Imaging Ch. 7, P7-7 Happy Feet (S) Ch. 2, P2-41 Heath Metal Products Ch. 9, Case 9-1 Healing Touch Ch. 12, P12-9 Hochstedt Ch. 5, P5-22 Home Auto Parts (S) Ch. 2, P2-15 Hospital Admission Office (H) Ch. 11, P11-16 House Mortgage (S) Ch. 3, P3-19 Housing Markets (S) Ch. 3, P3-27 Houston Milling Ch. 11, P11-10 Howard Binding Ch. 12, P12-12 Hurst Mats Ch. 9, P9-25

I

ICB, Intl. Ch. 5, P5-7 Ice Storm Ch. 6, P6-3 iGen3 Ch. 2, P2-22 Implementing ABC Ch. 11, P11-5 Infantino Saab (S) Ch. 5, P5-26 International Computer Company (S) Ch. 4, P4-23 International Telecon (S) Ch. 6, P6-15 Investment Banks (S) Ch. 6, P6-2 IPX Packaging Ch. 9, P9-2 IRR Problem Ch. 3, P3-1 ITI Technology Ch. 8, P8-13 IVAX Ch. 8, P8-31

J

J.P. Max Department Stores (S) Ch. 2, P2-5 Jacklin Stampings Ch. 9, P9-21 James Marketing Campaign (S) Ch. 6, P6-31

Using the Text ©The McGraw-Hill Companies, Inc., 2011 xxxiv Instructor’s Manual, Accounting for Decision Making and Control

Janitorial Services (S) Ch. 8, P8-29 Jason Rocks Ch. 8, P8-17 Jasper, Inc. Ch. 3, P3-3 JLE Electronics Ch. 2, P2-30 Joint Products, Inc. Ch. 8, P8-6 Jolsen International (S) Ch. 7, P7-8 Jones Consortium (S) Ch. 8, P8-30 Joon Ch. 10, Case 10-1 Just One, Inc. Ch.3, P3-4

K

Karsten Mills Ch. 8, P8-22 Kay Enterprises Ch. 11, P11-14 Kinsley & Sons (S) Ch. 2, P2-32 Kitchen Rite Ch. 9, P9-23 Kollel Hospital (H) Ch. 14, P14-14 Kothari Inc. Ch. 10, P10-12

L

Lancaster Chamber Orchestra (S) Ch. 13, Case 13-1 LaserFlo Ch. 6, Case 6-3 Linda Lion Co. Ch. 3, P3-31 Littleton Imaging (H) Ch. 2, P2-33 Littleton Medical Center (H) Ch. 8, P8-25 Logical Solutions Ch. 13, P13-4 Lottery (S) Ch. 3, P3-9 Lys Wheels Ch. 9, P9-7

M

MacGiver Brass Ch. 9, P9-4 Madden International (H) (S) Ch. 6, P6-24 Madigan Modems Ch. 6, P6-19 Magee Inc. Ch. 6, P6-30 Magic Floor Ch. 9, P9-29 Managers Need Accounting Information Ch. 1, P1-4

Manufacturing Cost Classification Ch. 2, P2-20 Marian Health Care System (H) Ch. 12, P12-10 Marketing Plan (S) Ch. 6, P6-9 Massey Electronics Ch. 7, P7-4 Mastich Counters (S) Ch. 2, P2-28 Mat Machinery Ch. 2, P2-35 Maui Seminar Ch. 11, P11-1 MBA Students Ch. 1, P1-1 Measer Ch. 2, P2-16 Medford Mug Company Ch. 10, P10-11 Media Designs (S) Ch. 9, P9-11 Medical Instruments (H) Ch. 12, P12-1 MedView (H) Ch. 2, P2-19 Megan Corp. Ch. 13, P13-20 Metal Press Ch. 5, P5-6 Metro Blood Bank (H) Ch. 8, P8-14 Mickles Ltd. Ch. 12, P12-2 Microelectronics Ch. 5, P5-9 Milan Pasta Ch. 11, P11-4 Montana Pen Ch. 1, P1-10 Mopart Division Ch. 13, P13-23 Mortgage Department (S) Ch. 3, P3-28 Mowerson Division Ch. 2, Case 2-2 MRI (H) Ch. 7, P7-1 MRI Department (H) Ch. 13, P13-21 Mr. Jones’s Retirement Ch. 3, P3-10 Murray Hill’s Untimely Demise (S) Ch. 8, P8-9 Mutual Fund Company Ch. 9, P9-26 Mystic Herbals Ch. 8, P8-4 Mystic Mugs Ch. 10, P10-13

N

National Taxpayers Union (S) Ch. 3, P3-16 National Training Institute (S) Ch. 7, P7-10 Navisky Ch. 10, P10-16 Negative Opportunity Costs Ch. 2, P2-2

Using the Text ©The McGraw-Hill Companies, Inc., 2011 Instructor’s Manual, Accounting for Decision Making and Control

xxxv

New Car Ch. 3, P3-15 New York Fashions Ch. 6, P6-14 News.Com (S) Ch. 2, P2-31 Neweway Plastics Ch. 9, P9-31 Northern Sun, Inc. Ch. 3, P3-7 NPR (S) Ch. 2, P2-3 NPV vs. Payback Ch. 3, P3-11

O

Oaks Auto Supply Ch. 12, P12-4 Old Rosebud Farms Ch. 6, P6-27 Old Town Roasters (S) Ch. 14, P14-6 Old Turkey Mash Ch. 2, Case 2-1 On-Call (S) Ch. 13, P13-1 One Cost System Isn’t Enough Ch. 1, P1-2 Oneida Metal Ch. 13, P13-5 Oppenheimer Visuals Ch. 2, P2-25 Optometry Practice (H) Ch. 2, P2-31 Outback Opals Ch. 8, P8-2 Overland Steel Ch. 3, P3-33

P

Painting Department Ch. 7, P7-19 Panarude Airfreight (S) Ch. 6, P6-17 Parkview Hospital (H) Ch. 1, P1-9 Pay for Performance Ch. 4, P4-2 Pebble Beach Sandal Ch. 9, P9-20 Penury Company Ch. 2, P2-13 Phipps Electronics Ch. 5, P5-2 Phonetex Ch. 7, Case 7-1 Picture Maker (S) Ch. 6, P6-22 Plastic Chairs Ch. 7, P7-24 Pool Scrubbers Ch. 9, P9-5 Portable Phones, Inc. Ch. 9, Case 9-2 PortCo Products Ch. 9, Case 9-3

Potter-Bowen (S) Ch. 6, P6-10 PQR Coal Ch. 3, P3-22 Pratt & Whitney Ch. 4, P4-14 Premier Brands Ch. 5, P5-21 Printers, Inc. Ch. 13, P13-7 Private Country Clubs (S) Ch. 4, P4-17 Productivity Measures Ch. 14, Case 14-3 Punch Press Ch. 3, P3-36 Purchasing Department Ch. 13, P13-2 Puttmaster (S) Ch. 2, Case 2-3 Pyramid Products Ch. 9, P9-28

Q

R

R&D Inc. Ch. 5, P5-19 Raises Ch. 4, P4-9 RBB Brands Ch. 8, P8-21 Reed Park, Inc. (S) Ch. 7, P7-23 Repro Corporation Ch. 4, P4-24 Republic Insurance (S) Ch. 6, P6-26 Rick’s Bags Ch. 9, P9-13 Roberts Machining Ch. 2, P2-38 Roderiques Ch. 11, P11-9 Rose Hospital (H) Ch. 8, P8-3 Rothwell Inc. (S) Ch. 4, P4-21 Royal Holland Line (S) Ch. 2, P2-37 Royal Resort and Casino (S) Ch. 5, Case 5-4 Rust Belt Mufflers Ch. 12, Case 12-2

S

Sales Commissions Ch. 4, P4-12 Sanchez Gadgets Ch. 11, P11-11 Sants Brakes Co. Ch. 10, P10-22

Using the Text ©The McGraw-Hill Companies, Inc., 2011 xxxvi Instructor’s Manual, Accounting for Decision Making and Control

Savannah Products Ch. 5, P5-23 Scanners Plus Ch. 7, P7-20 Scion Corp. Ch. 6, Case 6-2 Scottie Corporation Ch. 3, P3-35 Secure Servers Inc. (S) Ch. 14, P14-13 Serviflow Ch. 5, P5-28 Shady Tree Manufacturing Ch. 13, P13-18 Shop and Save (S) Ch. 5, P5-8 Silky Smooth Lotions Ch. 2, P2-4 Simple Investment Ch. 3, P3-12 Simple Plant Ch. 9, P9-12 Slawson Ch. 7, P7-2 Smythe and Yves Ch. 12, P12-8 SnapOn Fasteners Ch. 11, Case 11-2 Software Development, Inc. (S) Ch. 14, P14-8 Software Associates (S) Ch. 12, P12-17 Soldering Department Ch. 13, P13-10 South American Mining Ch. 3, P3-18 Spa Ariana (S) Ch. 6, P6-21 Specialized Surgical Instruments (H) Ch. 9, P9-19 Spectra Inc. Ch. 13, P13-3 Stale-Mart (S) Ch. 5, P5-18 Standard Cost Systems Ch. 12, P12-7 Starling Coatings Ch. 12, P12-18 Step-Down Ch. 8, P8-1 Stirling Acquisition (S) Ch. 14, P14-9 Student Loan Program (S) Ch. 3, P3-23 Sunder Properties (S) Ch. 5, P5-3 Sunder Toys Ch. 8, P8-11 Sunnybrook Farms (S) Ch. 2, P2-9 Sunstar Appliances Ch. 5, P5-17 Swan Systems Ch. 5, Case 5-1

T

Tagway 4000 Ch. 14, P14-15 Talor Chemical Company Ch. 8, P8-7

Taylor Chains Ch. 10, P10-15 Taylor Chemicals Ch. 2, P2-9 Telephone Computer Corporation (TCC) Ch. 14, Case 14-2 Telstar Electronics Ch. 7, P7-13 The Pottery Store (S) Ch. 14, P14-7 Theory X – Theory Y Ch. 4, P4-15 Thermalloy Ch. 9, P9-6 Tilist Golf Ch. 11, Case 11-1 Tipping (S) Ch. 4, P4-18 Toby Manufacturing Ch. 11, P11-13 Toledo Stadium (S) Ch. 3, P3-21 TQM at the Stowbridge Division Ch. 14, P14-10 Transfer Price Company Ch. 5, P5-24 Transmation Ch. 7, P7-26 TransPacific Bank (S) Ch. 10, P10-6 Trevino Golf Balls Ch. 12, P12-19 Troika Toys (S) Ch. 6, P6-28 Troy Industrial Designs Ch. 5, Case 5-1 True Cost Manufacturing, Inc. Ch. 11, P11-8 Truini Paints Ch. 10, P10-4 Turow Trailers Ch. 13, P13-14

U

U.S. and Japanese Tax Laws Ch. 1, P1-3 U.S. Pump Systems Ch. 5, P5-15 Ultrasonic (H) Ch. 13, P13-19 UniCom Ch. 10, P10-21 University Lab Testing (H) Ch. 5, P5-12 University Physician Compensation (H) Ch. 4, P4-6 Unknown Company Ch. 9, P9-14 UOP Ch. 13, P13-16 US Copiers Ch. 5, P5-10 Using Accounting for Planning Ch. 1, P1-5

Using the Text ©The McGraw-Hill Companies, Inc., 2011 Instructor’s Manual, Accounting for Decision Making and Control

xxxvii

V

Vanderschmidt’s (S) Ch. 4, P4-11 Varilux Ch. 10, P10-3 Veriplex Ch. 6, P6-18 Videx Ch. 6, P6-13 Vigdor Wood Products Ch. 8, P8-15 Vintage Cellars Ch. 2, P2-7 Volume and Profits Ch. 2, P2-13 Voluntary Financial Disclosure Ch. 4, P4-5 Vorma Ch. 7, P7-16

W

Ware Paper Box Ch. 9, P9-8 Warren City Parts Manufacturing Ch. 14, P14-12 Wasley Ch. 7, P7-6 Watson’s Bay Ch. 3, P3-30 Webb & Drye (S) Ch. 6, P6-20 Wedig Diagnostics (H) Ch. 11, P11-12 Welding Robots Ch. 9, P9-17 Wellington Ch. 9, P9-15 Western Sugar Ch. 13, P13-9 Weststar Appliances Ch. 10, P10-19 White’s Department Store (S) Ch. 4, P4-19 William Company (S) Ch. 2, P2-29 Wine Distributors (S) Ch. 13, P13-12 Winter Games Ch. 14, P14-11 Winterton Group (S) Ch. 7, P7-9 Woodhaven Service (S) Ch. 4, Case 4-2 Woodley Furniture Ch. 7, P7-25 World Imports (S) Ch. 7, P7-18 Wujo (H) Ch. 5, P5-27 WWWeb Marketing Ch. 8, P8-12 Wyatt Oil Ch. 8, Case 8-2

X, Y, Z

XBT Keyboards Ch. 5, P5-25 Xerox Ch. 10, P10-2 Zeflax Bottles Ch. 10, P10-7 Zinc Faucets Ch. 12, P12-11 Zipp Cards (S) Ch. 10, P10-5