industry analysis varun pharma

DESCRIPTION

1233333TRANSCRIPT

Strategic Analysis of Pharmaceutical Industry

Assignment Submission By:

Varun Ramachandran FT151022

Industry Analysis

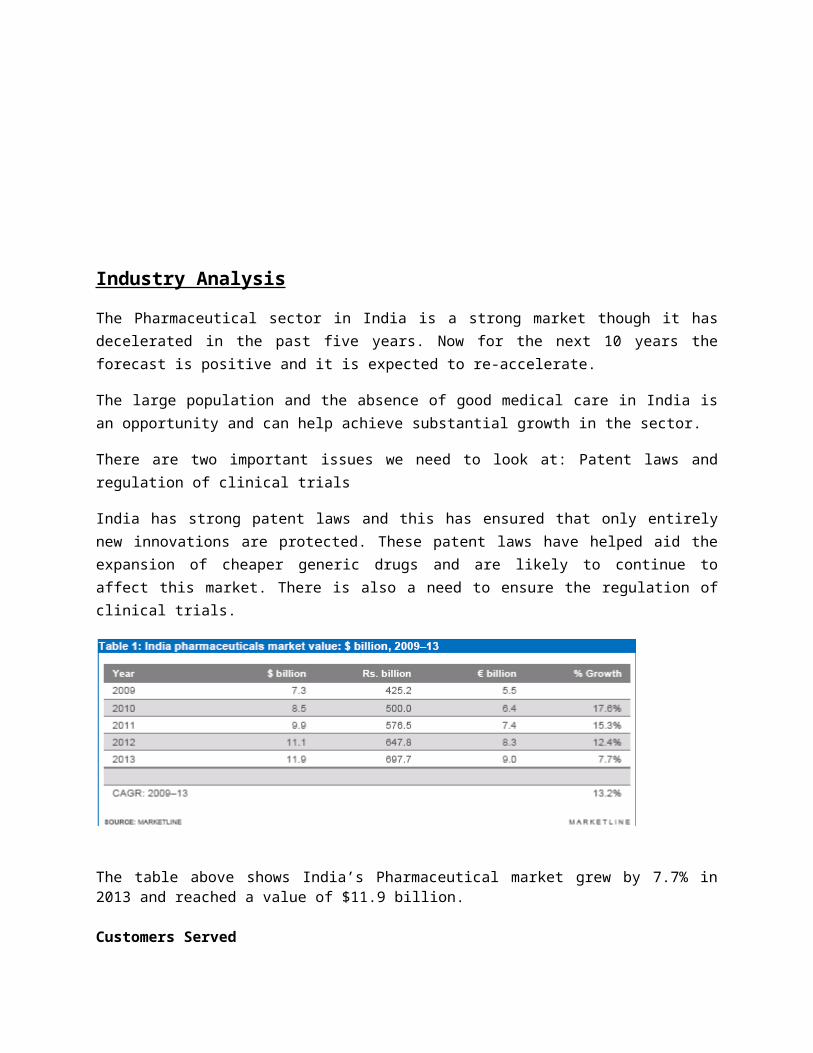

The Pharmaceutical sector in India is a strong market though it has decelerated in the past five years. Now for the next 10 years the forecast is positive and it is expected to re-accelerate.

The large population and the absence of good medical care in India is an opportunity and can help achieve substantial growth in the sector.

There are two important issues we need to look at: Patent laws and regulation of clinical trials

India has strong patent laws and this has ensured that only entirely new innovations are protected. These patent laws have helped aid the expansion of cheaper generic drugs and are likely to continue to affect this market. There is also a need to ensure the regulation of clinical trials.

The table above shows India’s Pharmaceutical market grew by 7.7% in 2013 and reached a value of $11.9 billion.

Customers Served

The key buyers for the Pharmaceutical manufacturing market include hospitals, pharmacies, health insurance providers and government health care programs. The suppliers would include companies which provide manufacturing/laboratory equipment, pharmaceutical ingredients and clinical trial services.

Value delivered

Well-being of the patients is the primary value delivered by the industry. Their secondary aim as in any industry is to generate value for the stakeholders. This would include hospitals, pharmacies, health insurance providers and government. They do this by providing the finest pharmaceutical products.

Industry Characteristics

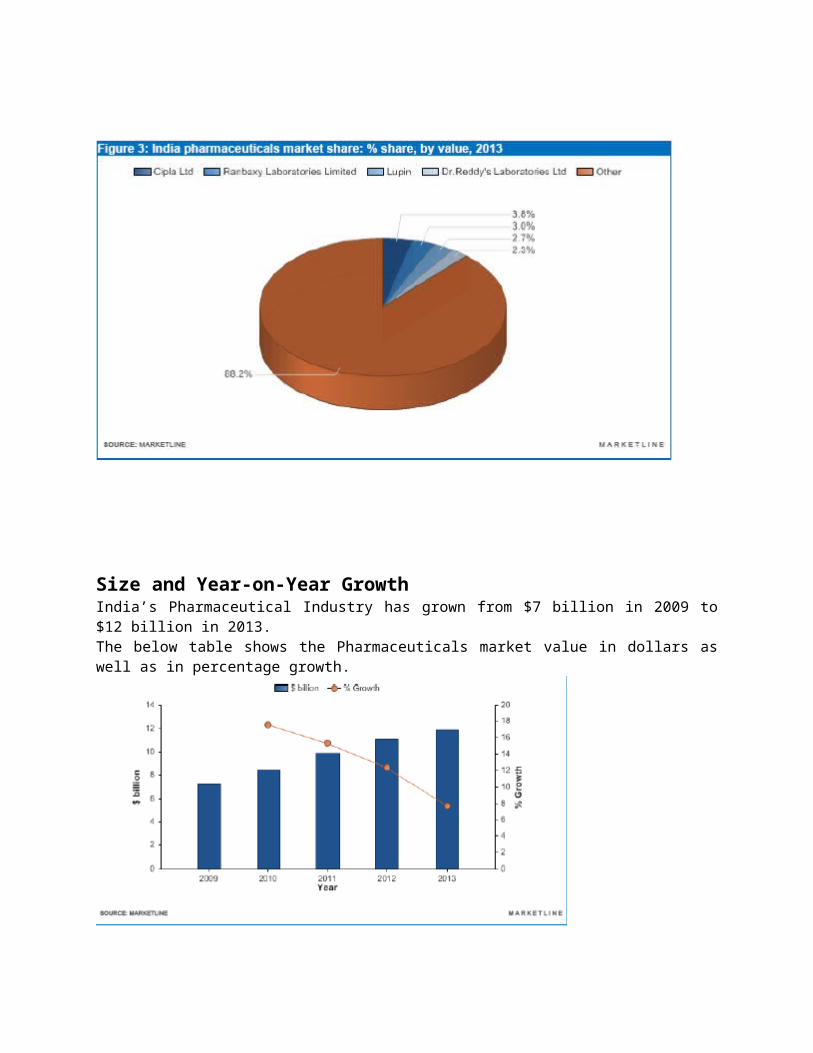

Market Share

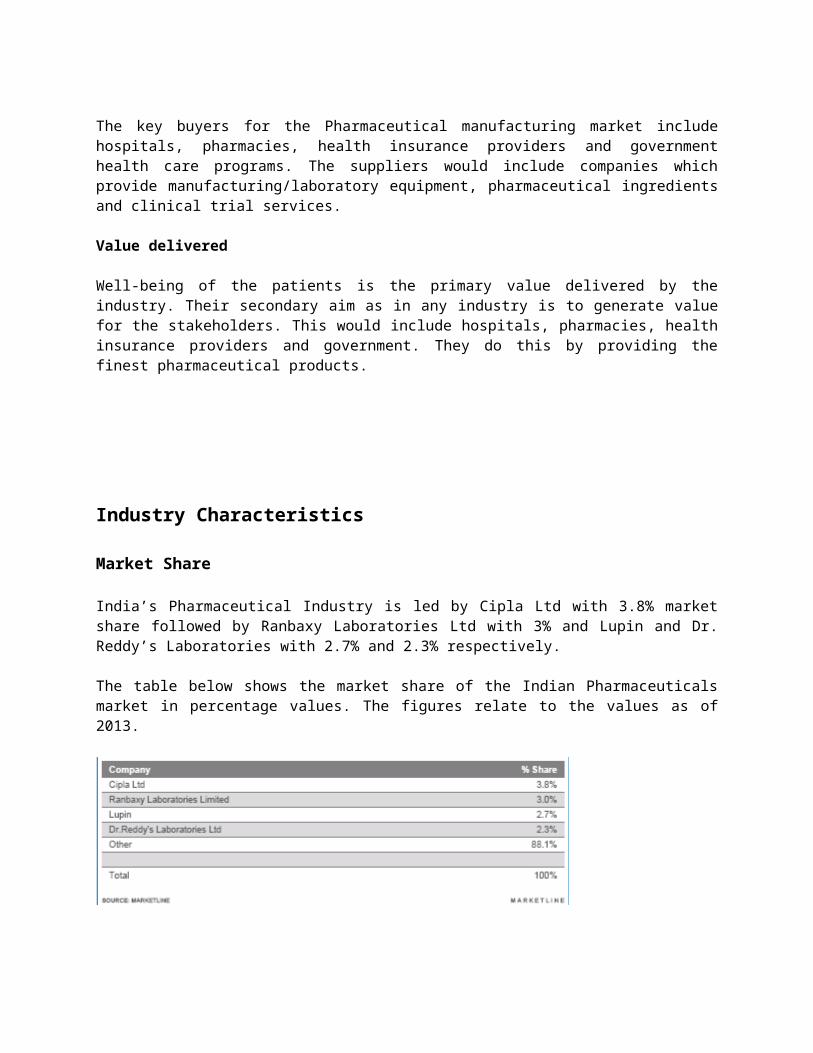

India’s Pharmaceutical Industry is led by Cipla Ltd with 3.8% market share followed by Ranbaxy Laboratories Ltd with 3% and Lupin and Dr. Reddy’s Laboratories with 2.7% and 2.3% respectively.

The table below shows the market share of the Indian Pharmaceuticals market in percentage values. The figures relate to the values as of 2013.

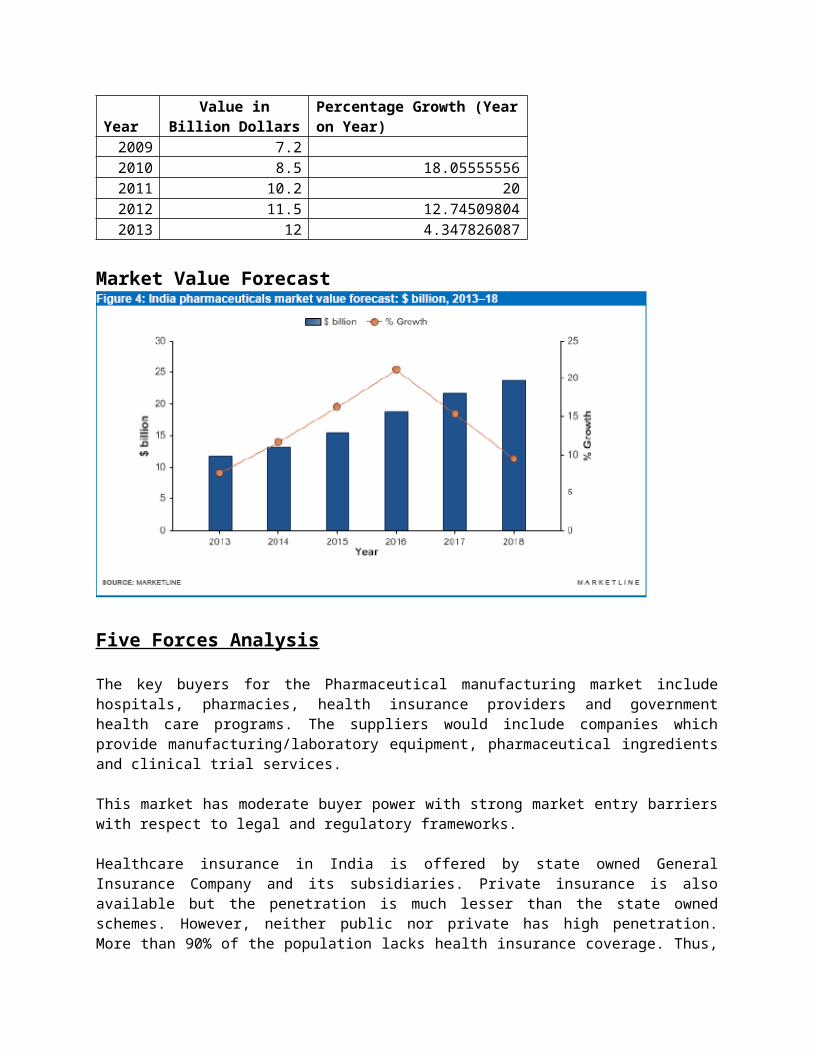

Size and Year-on-Year GrowthIndia’s Pharmaceutical Industry has grown from $7 billion in 2009 to $12 billion in 2013.The below table shows the Pharmaceuticals market value in dollars as well as in percentage growth.

YearValue in Billion

DollarsPercentage Growth (Year on Year)

2009 7.2 2010 8.5 18.055555562011 10.2 202012 11.5 12.745098042013 12 4.347826087

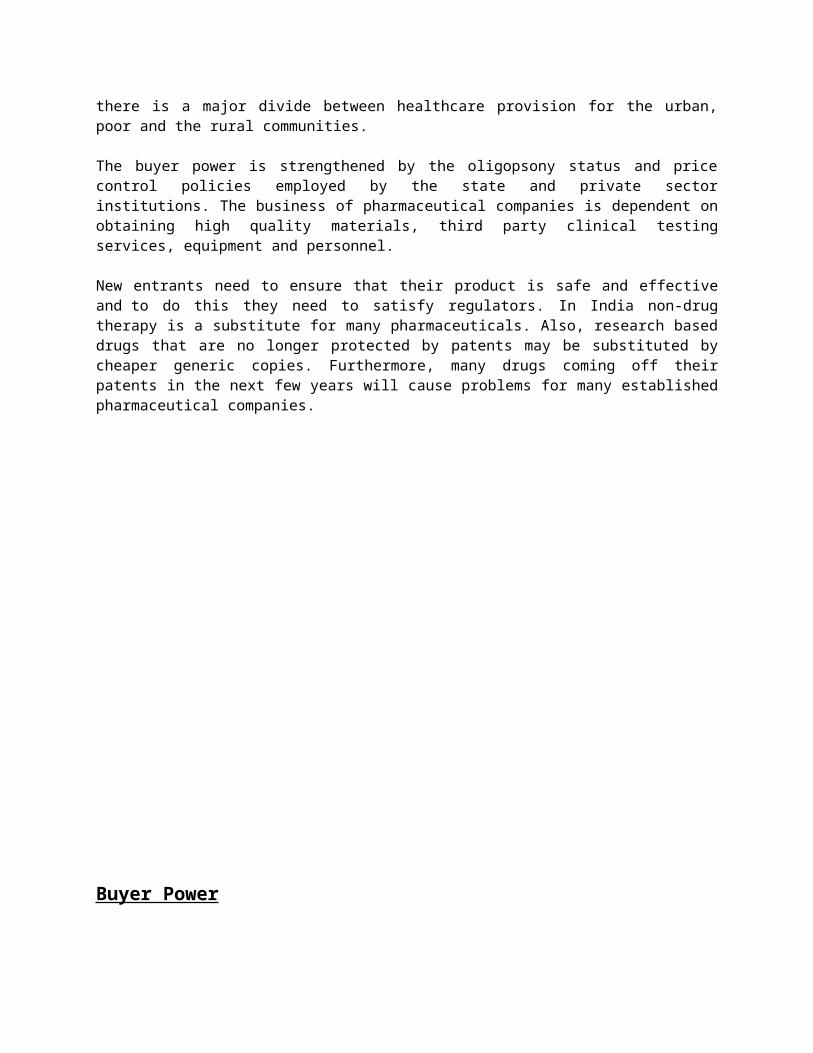

Market Value Forecast

Five Forces Analysis

The key buyers for the Pharmaceutical manufacturing market include hospitals, pharmacies, health insurance providers and government health care programs. The suppliers would include companies which provide manufacturing/laboratory equipment, pharmaceutical ingredients and clinical trial services.

This market has moderate buyer power with strong market entry barriers with respect to legal and regulatory frameworks.

Healthcare insurance in India is offered by state owned General Insurance Company and its subsidiaries. Private insurance is also available but the penetration is much lesser than the state owned schemes. However, neither public nor private has high penetration. More than 90% of the population lacks health insurance coverage. Thus, there is a major divide between healthcare provision for the urban, poor and the rural communities.

The buyer power is strengthened by the oligopsony status and price control policies employed by the state and private sector institutions. The business of pharmaceutical companies is dependent on obtaining high quality materials, third party clinical testing services, equipment and personnel.

New entrants need to ensure that their product is safe and effective and to do this they need to satisfy regulators. In India non-drug therapy is a substitute for many pharmaceuticals. Also, research based drugs that are no longer protected by patents may be substituted by cheaper generic copies. Furthermore, many drugs coming off their patents in the next few years will cause problems for many established pharmaceutical companies.

Buyer Power

Pharmaceutical companies sell their products to drug wholesalers, who then sell to pharmacies or hospitals and it then finally reaches the customer. In countries like India, which is still not in a mature market, it is becoming increasingly important for manufacturers given the pricing pressures in mature markets.

Prescriptions are generally required for buying most pharmaceutical products and thus marketing of these drugs is largely directed at medical practitioners. India advertising such products directly to consumer is usually illegal. Depending on the condition of the patient there may be several different treatments available. Thus differentiation in these cases weakens buyer power. Product differentiation under pharmaceutical products includes efficacy, ease of use, side effects and cost-effectiveness. The move towards genetic research is giving rise to the possibility of personalized medicine is also likely to decrease buyer power. On the other hand, in cases where generic equivalents exist, differentiation is decreased and buyer power increases.

A public or private-sector health insurer fund purchases directly, or they may reimburse an end-user’s purchase. This exponentially increases buyer power. These large purchasers exert monopsony market power and it is very common for them to use one or more specific price control strategies. But, as the majority of the Indian market is uninsured, funding in India comes from private out-of-pocket expenditure.

Governments sets drug prices directly and thus it becomes illegal to sell at a different price. In cases where government is responsible for reimbursement of the consumer it may set a very low reimbursement price for new or existing drugs.

For some drugs, price-volume or profit controls exist. Price-volume or profit controls set a limit to the volume of a drug sold in the country, or to the amount of profit a drug company can make. If a manufacturer sells beyond tis limit, they must offer compensatory payments to the government or reduce the price of their product.

Such anomalies are treated as market distortions. But, where such policies are implemented it is because policy makers consider that the social benefits of lower-cost drugs such as improved access to healthcare outweigh the social harms such as a potential reduction in pharmaceutical companies’ ability to invest in R&D.

India's National Pharmaceutical Pricing Authority employs control over the price of a list of drugs. This list is called "scheduled" drugs. It also observes price trends for other pharmaceutical products and enforces a maximum limit of 10% on yearly price increases.

Aspects weakening buyer power comprise the high importance of pharmaceuticals in healthcare. The ultimate users of pharmaceuticals interact with the pharmaceutical market through the political system rather than a straightforward value chain. But, they still have a significant impact on the purchasing process. Overall, buyer power is assessed as temperate.

Supplier Power

Major suppliers to the pharmaceutical markets are producers of pharmaceutical ingredients, which form a sub-sector of the chemical market. The leading pharmaceutical companies have major capital investments in chemical manufacturing. This provides them with a degree of self-sufficiency and reduces supplier power.

Ingredients are supplied on the basis of a contract and hence the pharmaceutical company is likely to risk high switching costs if it considers taking its business elsewhere. Therefore, pharmaceutical companies hire sourcing managers who can help minimize costs and diminish supplier power. The development of new beneficial agents requires the sourcing of newer ingredients. Chemical manufacturers can charge pharmaceutical companies higher prices for this service.

Market players tend to purchase their raw materials from various suppliers thereby reducing their reliance on any specific company. Laboratory equipment and chemicals illustrate little differentiation among suppliers. Customers utilize a high degree of choice in order to obtain the best quality and cost relationship and thus reduce supplier power. But, there are cases where specialized raw materials are required. In such cases, supplier power is much stronger. It is not likely that suppliers would forward-integrate into the pharmaceutical market. But, at the same time, their capabilities in chemicals make them model candidates for forward integration into the manufacture of generic drugs. In the past few years, larger pharmaceutical companies have turned to manufacturing their own chemicals to be able to enhance profits, however smaller companies do not have the resources required to do this and continue to be reliant on ingredient manufacturers.

It is common for pharmaceutical corporations to outsource their clinical trials and drug testing to third-party test service providers. These service providers are also important suppliers as these trials are very important for regulatory approvals. India has been restructuring its regulations around clinical trials through the Drug Standard Control Organization in order to make itself a more attractive location for the industry.

Overall, supplier power is moderate.

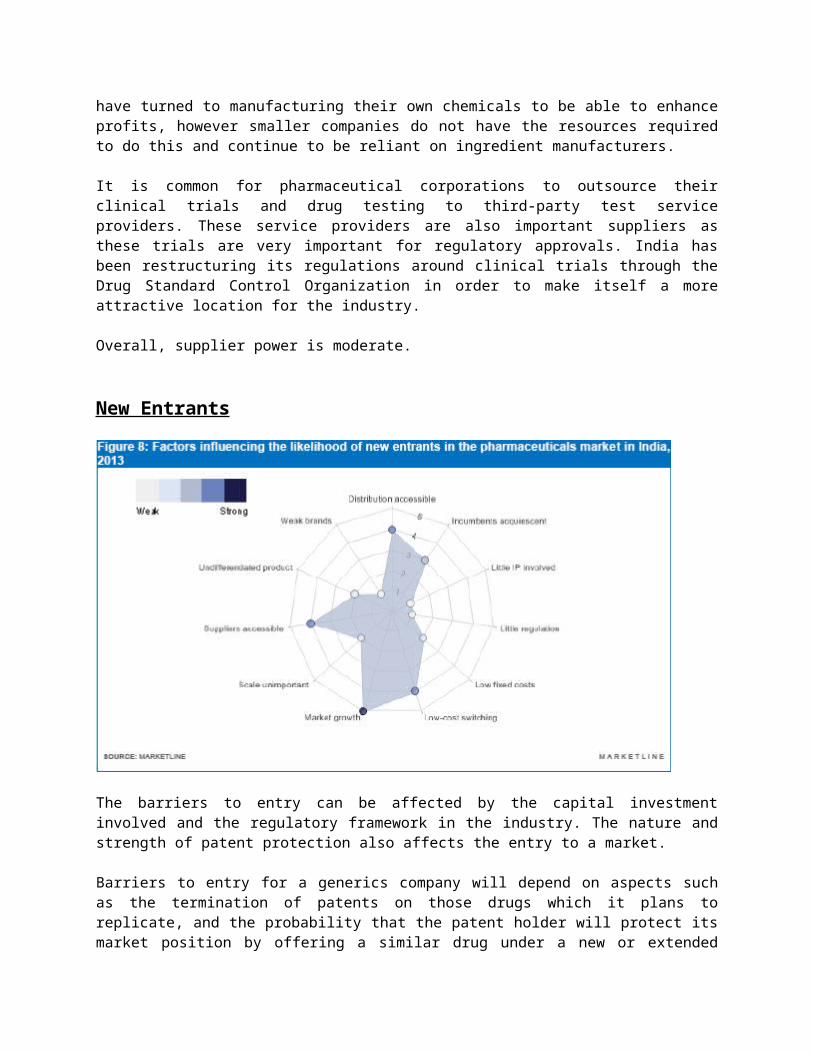

New Entrants

The barriers to entry can be affected by the capital investment involved and the regulatory framework in the industry. The nature and strength of patent protection also affects the entry to a market.

Barriers to entry for a generics company will depend on aspects such as the termination of patents on those drugs which it plans to replicate, and the probability that the patent holder will protect its market position by offering a similar drug under a new or extended patent. Also, regulations defending intellectual property differ from country to country. Patent laws may be undeveloped in some countries. In others, governments may explicitly rank public health requirements over private intellectual property rights.

India did not allow drugs to be patented until 2005 (in line with WTO requirements), and at present only awards patents to completely new drugs rather than enhancements to existing products.

Overall, while the barriers to market entry are relatively high, robust market growth means that the threat of new entrants is moderate.

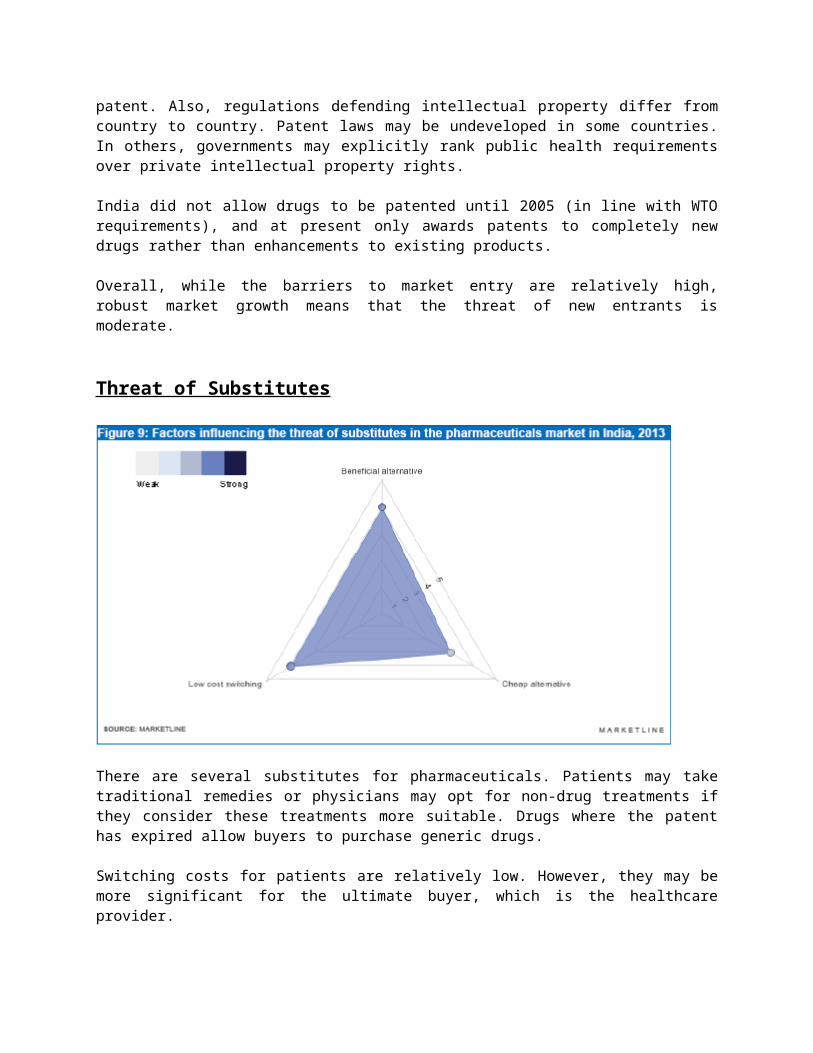

Threat of Substitutes

There are several substitutes for pharmaceuticals. Patients may take traditional remedies or physicians may opt for non-drug treatments if they consider these treatments more suitable. Drugs where the patent has expired allow buyers to purchase generic drugs.

Switching costs for patients are relatively low. However, they may be more significant for the ultimate buyer, which is the healthcare provider.

The main substitutes to branded drugs are generics and biosimilars. Biosimilars are also known as follow-on biologics. Biosimilars are a very important segment of the Indian market, accounting for more than 90% of drug volumes. In-spite of the volumes, they have a much lower proportion of market value.

Producers of generics can offer the identical drug at a much lower price and do not have to conduct costly clinical trials. Similarly, there is a growing threat from biosimilars.

The threat of substitutes is strong.

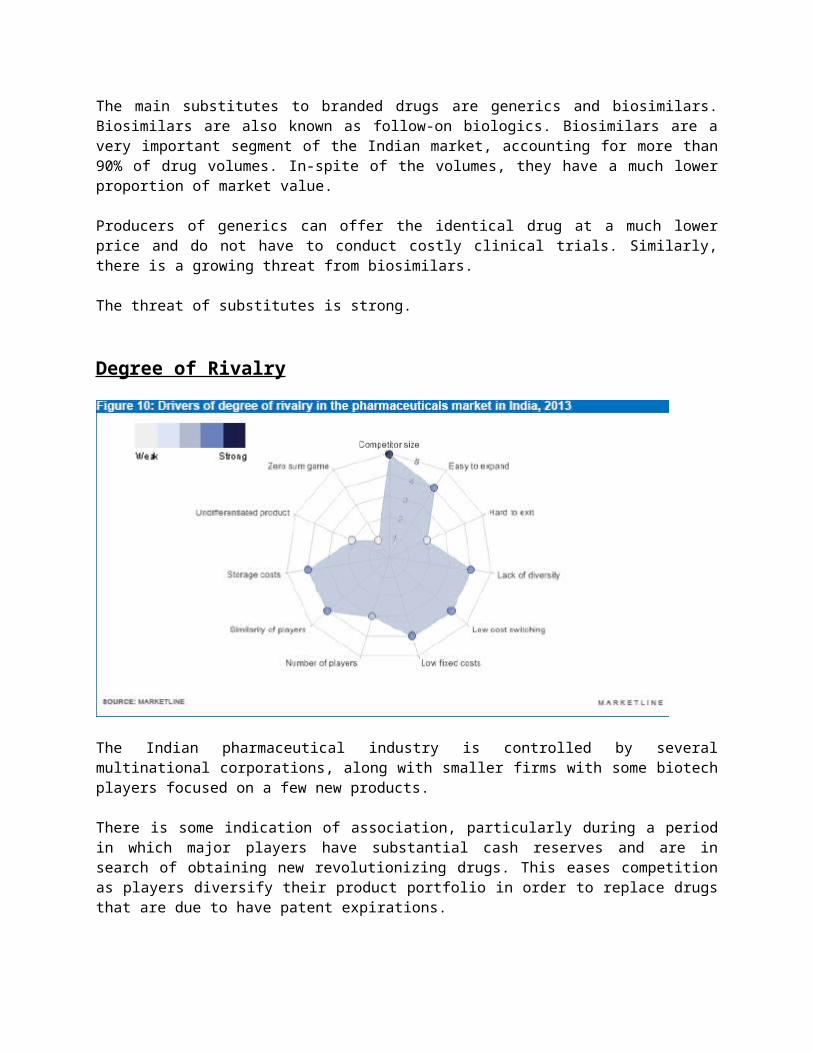

Degree of Rivalry

The Indian pharmaceutical industry is controlled by several multinational corporations, along with smaller firms with some biotech players focused on a few new products.

There is some indication of association, particularly during a period in which major players have substantial cash reserves and are in search of obtaining new revolutionizing drugs. This eases competition as players diversify their product portfolio in order to replace drugs that are due to have patent expirations.

However, the overall market concentration is not precisely high. There might be a superior actual concentration within definite therapy areas, and this is a market where goods can be highly differentiated through their clinical usefulness. For example, one corporation might have a patented drug which is very effective in treating a specific illness. It would be problematic to contest directly with such a player, though other businesses will undoubtedly be managing expansion pipelines in order to exploit this market when the drug patent expires.

Research-based pharmaceutical companies are like media businesses. They rely on initially creating valuable intellectual property at a high cost, which can then be used to create mass-produced products

at a comparatively lower cost. The skill of generics companies to be lucrative while marketing the identical product at a much lower price than the inventor, after patent cessation, shows that instituting high-quality manufacturing processes is not excessively costly. A secondary result of this is that it is relatively easy for research-based companies to increase production, for example through licensing contracts with other companies, without the need to expand their own production facilities.

It is reasonably easy to exit the market. Many of the assets– patents, trademarks and synthetic methods can be sold relatively easily. Many of the R&D and manufacture facilities and equipment will have usages external to pharmaceutical research or production.

Overall, the degree of rivalry is moderate.

Macroeconomic Factors

Country Population

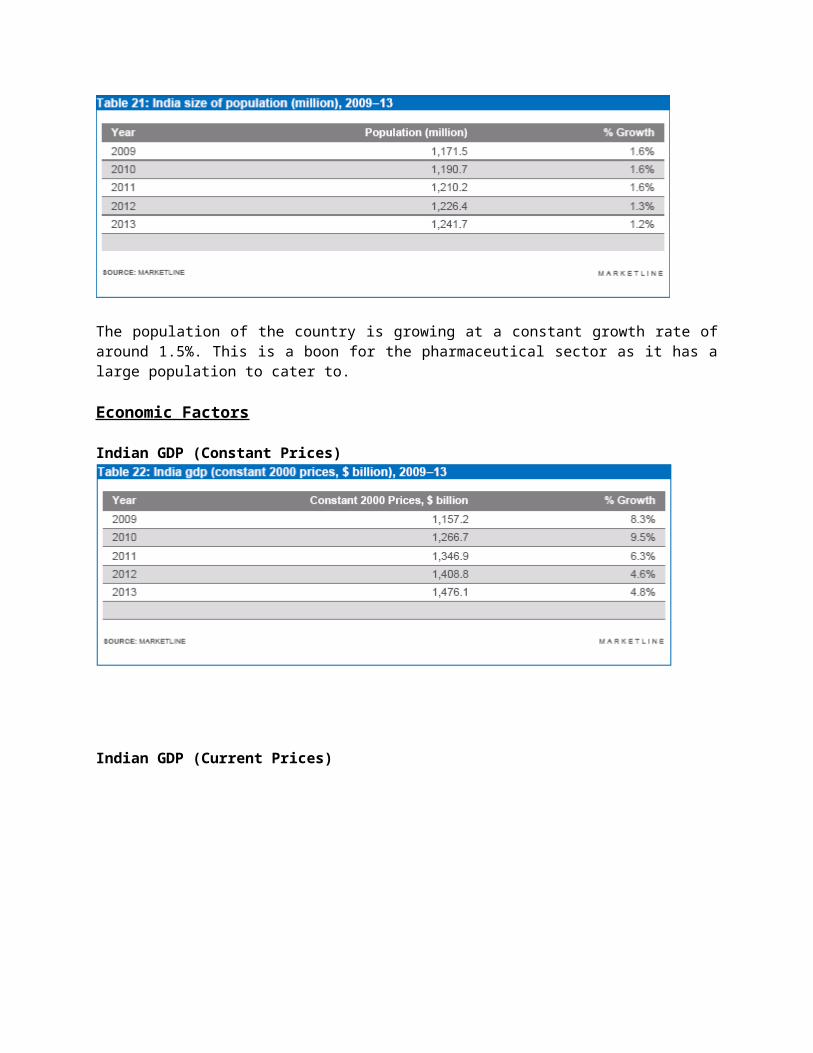

The population of the country is growing at a constant growth rate of around 1.5%. This is a boon for the pharmaceutical sector as it has a large population to cater to.

Economic Factors

Indian GDP (Constant Prices)

Indian GDP (Current Prices)

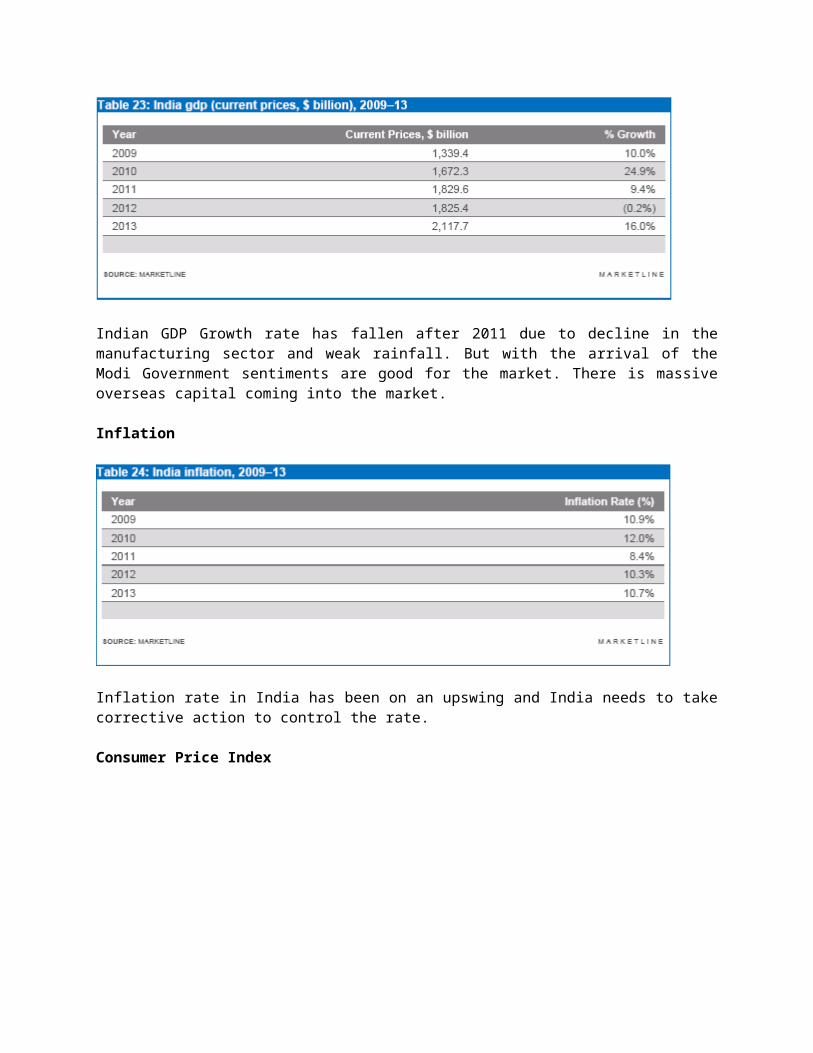

Indian GDP Growth rate has fallen after 2011 due to decline in the manufacturing sector and weak rainfall. But with the arrival of the Modi Government sentiments are good for the market. There is massive overseas capital coming into the market.

Inflation

Inflation rate in India has been on an upswing and India needs to take corrective action to control the rate.

Consumer Price Index

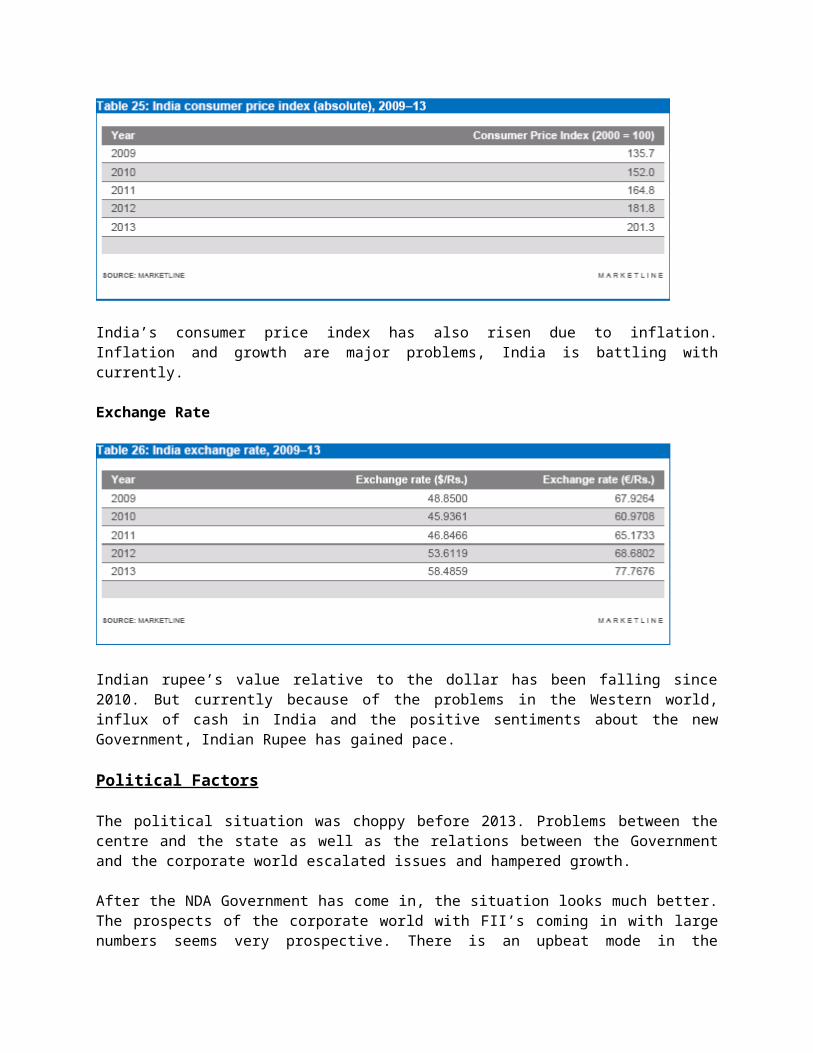

India’s consumer price index has also risen due to inflation. Inflation and growth are major problems, India is battling with currently.

Exchange Rate

Indian rupee’s value relative to the dollar has been falling since 2010. But currently because of the problems in the Western world, influx of cash in India and the positive sentiments about the new Government, Indian Rupee has gained pace.

Political Factors

The political situation was choppy before 2013. Problems between the centre and the state as well as the relations between the Government and the corporate world escalated issues and hampered growth.

After the NDA Government has come in, the situation looks much better. The prospects of the corporate world with FII’s coming in with large numbers seems very prospective. There is an upbeat mode in the industry as a whole. Along with the government change, policies regarding FDI have also helped boost businesses.

Social factors

India has always been plagued by poverty and malnutrition. These factors are a precursor for all the diseases affecting the residents. These include the spread of malaria and tuberculosis. Though these diseases are easily avoidable, they have still not been eradicated from the country.

Problems like improper sanitation and pollution worsen the problems. Superstition and homemade medicines are also reasons for improper care given to sick patients.

People need to start believing and trusting in pharmaceutical products for treating illnesses.

Legal factors

Legal factors affecting the pharmaceutical industry revolves around patents and trials. The pharmaceutical need to be pre-tested extensively before they are offered to consumers. Also, sufficient patent life must be given so that the companies can recover the costs of research and development.

The sector needs to work with the government in order to create a supervisory process that offers access to methodically thorough and morally right trials so that the aids of such trials can support patients.

Environmental Factors

Environmental pollution is one major challenge faced by the country. Waste is being dumped in rivers without any treatment polluting the rivers. Farmers use this water for irrigation and this leads to a bad harvest.

Big drug corporations have been presenting practices for pollution stoppage and cleaner business processes throughout the life cycle of the product which will help to reduce the chemical waste. We need to view environmental benefits as a means to reduce cost and increase efficiency rather than just minimizing environmental hampering.

The pharmaceutical companies need to set standards for themselves and these need to be much higher than the governmental imposed standards.

Major Companies in the Pharmaceutical Industry and their markets

We will start with a brief overview of the companies and dive into the financials later.

Cipla

Cipla is involved in the development, manufacture, and sales of pharmaceutical products. The company exports raw materials, intermediates, prescription drugs, over-the-counter products and veterinary

products to more than 150 nations. The corporation manufactures more than 2,000 products in 65 therapeutic categories in its 34 facilities located across India.

The company's products consist of prescription drugs, animal health care products, OTC products, bulk drugs, agrochemicals and flavors and fragrances.

In the bulk drugs category, the company offers drug intermediates and pharmaceutical ingredients.

Cipla provisions flavors to food and beverages and pharmaceutical industries. The company's flavors are used in products ranging from fruit juices and medicinal liquids to baked goods and oral hygiene products.

Dr. Reddy’s Laboratories Ltd

Dr. Reddy's Laboratories Ltd is a pharmaceutical company involved in manufacturing generics, pharmaceutical ingredients, and patented products. It mainly operates in India, North America, Europe, Russia and other countries of the former Soviet Union.

The company functions through three segments: global generics, proprietary products and pharmaceutical services and active ingredients.

Dr. Reddy's Laboratories’ global generics segment involves finished pharmaceutical products that are ready for consumption by the patient. These products are marketed underneath a brand name or as generic complete doses with therapeutic correspondence to branded formulations. The branded generics portfolio offers around 200 products in the therapeutic areas of gastro-intestinal, cardiovascular, pain management, oncology, anti-infective, pediatrics and dermatology. The sector is also involved in over-the counter drugs.

The pharmaceutical services and active ingredients segment entails the company's pharmaceutical products or bulk drugs, which are the main constituents for finished pharmaceutical products. The sector also manufactures and sells ingredients and steroids in accordance to the specific customer requirements. In addition, the pharmaceutical services and active ingredients segment provides contractual research services.

The company's patented products segment is involved in the innovation of chemical units and differentiated inventions for successive commercialization and out-licensing. It comprises the company's specialty pharmaceuticals business which sells and markets in-licensed and co-developed dermatology products. The therapeutic areas of attention include inflammation, bacterial infections, pain and metabolic disorders.

Lupin Limited

Lupin Limited manufactures and sells generic and branded formulations and active pharmaceutical ingredients. The company primarily functions in India, Asia, the Americas and Europe.

The company provides various formulations in gastro intestinal (GI), cardiovascular system (CVS), central nervous system (CNS), anti-asthma, anti-tuberculosis (TB), diabetology, cephalosporins, dermatology, and other therapy areas. The company runs its formulations trade through a number of subsidiaries in India: Lupin Pharma, Blue Eyes, Endeavour, Maxter, Pinnacle CVS, Lupin CVN, Lupin Diabetes Care, Lupin Respira, Mindvision, Femina, and IKONIC.

Ranbaxy Laboratories Ltd

Ranbaxy Laboratories Limited is a research based, international pharmaceutical company manufacturing a variety of generic drugs. The corporation sells its products in around 150 countries, with manufacturing set-ups in eight nations and ground operations in 43 nations. A Japan-based pharmaceutical company, Daiichi Sankyo, owned 63.54% of Ranbaxy's overall common shareholding as of December 31, 2012.

The company operates only through a pharmaceutical business sector.

The pharmaceutical segment comprises the manufacture and sale of active pharmaceuticals ingredients, formulations, and generics, consumer health care products and drug discovery.

The products of the company are divided into two segments: dosage forms and API. The dosage forms manufactured by the business comprise of a variety of prescription and non-prescription drugs. The division places an importance on anti-bacterials and anti-infectives. The other products offered by the company include gastrointestinal, cardiovascular and central nervous system disorders, therapeutics for orthopedics, pain management; and nutritionals, multivitamins and dermatologicals.

The corporation has three research facilities located at Gurgaon, New Delhi. The first two research and development centers are dedicated to the progress of generics and novel drug delivery systems research; while the third research and development center is involved in innovative drug discovery research.

The divisions of the company include Ranbaxy Egypt, Ranbaxy Australia, Ranbaxy Farmaceutica, and Ranbaxy Do Brazil.

Aurobindo Pharma

Aurobindo Pharma was instituted in 1986 by Mr. K. Nityananda Reddy and Mr. P. V. Ramaprasad Reddy. It started its business with a solitary unit producing semi synthetic penicillin (SSPs) at Pondicherry.

The company functions in beneficial sectors like CNS, cardio-vascular, SSPs, cephalosporins, antivirals and gastroenterology. Aurobindo Pharma is the frontrunner in the market in semi-synthetic penicillin drug.

Financial Analysis

Sales growth, Margin and Market share

On an average of 5 years, Lupin has the highest sales growth and market share growth. Ranbaxy Laboratories needs catch up with its competitors. Cipla and Dr. Reddy’s have been performing well in margin growth in the past few years.

Efficiency Ratios

1. Receivables turnover rate has been good for Cipla and Lupin. This indicates that these companies gathers its receivables at a rate much higher than its competitors.

2. Inventory turnover has also been highest for Lupin. This indicates that Lupin does not retain much inventory and therefore the cost of maintaining inventory is much lesser as compared to the competitors.

3. The payables turnover is lowest for Lupin and Ranbaxy labs. This indicates that the two companies enjoy a sufficient payback period as compared to its competitors.

4. Total Assets turnover has been highest for Lupin.

5. Lupin has the lowest operating expense ratios. Operating expenses are the day-to-day costs that are associated with running a business' basic operations.

6. Lupin has the higher ROI among the other players in the industry. ROI is a good indicator of a company’s competence.

Solvency Ratios

1. The debt-to-assets ratio is highest for Aurobindo Pharma. A higher debt helps the company take advantage of the tax benefits involved. But at the same time too much debt will cause problems for the company in the long run in terms of interest payments.

2. The asset-to-equity ratio has been high for Ranbaxy Labs and Aurobindo Pharma. Asset to equity ratio indicates the amount of the assets that can be financed for each dollar of equity. It helps to assess the company’s leverage used to finance the firm.

3. Interest coverage ratio indicates the capability of a firm to meet its interest expenses. The lesser the interest coverage ratio, the higher a company’s debt burden and higher is the likelihood of nonpayment. This ratio has consistently been low for Aurobindo Pharma.

4. The dividend yield has been consistently good for Lupin Ltd. The dividend yield value has been low for the players in the industry.

5. Net debt change has been highest for Cipla and Lupin and this indicates that supplementary financing decisions have been undertaken by borrowing more debt in order to finance the processes of the firm.

Profitability and Growth

1. The gross profit margin and net margin has been highest for Cipla and Lupin. This indicates better profitability when compared to their competitors.

2. ROA and ROE values have been highest for Ranbaxy Labs. This indicates effectiveness in the assets that the company consumes to complete its operations.

3. EPS has highest for Dr. Reddy’s when compared to the other players.

Liquidity Ratios

1. The Working Capital Ratio/Net working capital shows if a firm has enough short term assets to cover its short term debts. Anything below 1 and any value over 2 is not advisable for any company. The working capital ratio has been adequate for Lupin in the past five years.

2. The quick ratio is an indicator of the short term liquidity for a firm. The quick ratio has been high for Cipla and Lupin. This indicates that the two companies have sufficient liquid assets for paying back their current liabilities.

Export Intensity

1. Companies surface around opportunity cost while examining the best use for their funds. They can either invest their money to obtain physical assets, real estate, wealth enhancements, or they can spend in R&D.

2. Expenditure on R&D has been quite high for Ranbaxy Laboratories when compared to its competitors. Also, the RORC has been high for Aurobindo Pharma.

3. Aurobindo Pharma has the highest ratio of export to total sales.

Sustainable Competitive Advantage (Ranbaxy Laboratories)

Ranbaxy Laboratories Ltd

Ranbaxy Laboratories Ltd has ground presence in over 43 countries and markets its goods in more than 150 countries across the developed, developing and lesser developed markets of the world. These sectors have their exceptional features and growth drivers, such as proprietary generics and quality connect by end-customer for the emerging markets, and commoditized, genericization, in the urbanized parts of the world. Ranbaxy has a sturdy sales and distribution network, local presence of manufacturing centres and trained manpower. The company is well placed to develop across these markets. Its worldwide presence helps the company alter and adapt to variations in the macro-environment. Also, with more than 60% of revenues from the emerging markets, which are expected to grow at a rate faster than the market as a whole and investments largely in place, the worldwide presence gives it a unique lead.

The emphasis of the company is on its strategy of Focus, Run & Win. It achieves growth through its range and choice of products, critical processes, key customers and human resource development.

The strength of Ranbaxy is in building brands. A large number of its brands feature in the list of Top 30 brands in the industry.

Many of the segments of Ranbaxy have grown slower than the overall pharma market, but it has still has managed to record a gain in market share for most of its brands. This speaks volumes about its strengths.

The company has introduced the anti-malarial drug in India called Synriam which has been constantly expanding its patient and prescriber base in India.

In addition to consumer information enhancement programs, the company carries out several patient centric market growth initiatives. These initiatives are targeted at increasing the illness awareness/education, diagnosis and treatment in areas such as of Osteoporosis, BPH, Diabetes, Hypertension, Epilepsy and Anaemia etc.

Hybrid Business Model

Ranbaxy and Daiichi Sankyo developed on the hybrid business model with cooperation between the front-end in key markets as well as the back-end in R&D, supply chain, IT and social contribution.

The motive of the two companies is that any collaborations that both companies work towards will always be distinct and apart and beneficial for both, independently and jointly.

1. Front-end

The company continues to discover collaboration opportunities in important markets with the objective of aligning front-end that would help in reducing duplication.

In markets where Ranbaxy is already a solid player, it takes the lead to promote both its own generic products and support Daiichi Sankyo's newly discovered products, regardless of the nature of the market.

2. Back-end

The hybrid business has led to multiple synergies on the back-end, including supply chain, chemistry, manufacturing, procurement and controls. To further cooperation, the two companies have worked on an employee exchange programme, whereby personnel of one company are transferred to the other. This helps build mutual appreciation and encourages a new attitude.

With regard to the launch of generic products, both corporations functioned collectively to find products for joint progress.

3. Social Contribution

The two companies collaborated together with an aim to contribute towards the success of UN Millennium Development Goals about fighting malaria, improving maternal health, decreasing child mortality, HIV/AIDS and other illnesses. The two corporations started a joint enterprise in District Dewas, Madhya Pradesh from end to end with the introduction of 2 well equipped healthcare vans with the help of doctors and paramedics. The initiative is being realized by the Ranbaxy Community Health Care Society. The plan has made noteworthy progress with the persistent backing by the Government.

Mobile health facilities are being primarily delivered to 20 villages which has a population of more than 31,000 people.

Outlook on Threats, Risks and Concerns

Apart from the risks met by the pharmaceuticals sector at large, international generic companies face additional perils connected with patent litigations, product liability and regulatory challenges. While the generic companies have an opportunity to genericize patented products in the advanced markets, such opportunities reflect the possibility of products going off-patent and not being substituted by newer patent openings. Pharmaceutical companies also incessantly work to discover methods to innovate their patented drugs to postpone the entry of generic versions of innovator drugs.

Moreover, the innovator businesses have also begun to join in this segment, with a view to retain market share, despite the multifarious competitiveness and price erosion in the generics market owing to development opportunities in off-patent goods. Also, competition in generics is not only in the industrialized world, but also in the developing markets, which are expected to grow at a higher growth rate than industrialized markets.

Other risks consist of postponement in approval or cancellation of drug sanctions previously approved, postponement in obtaining approvals for new products, product recalls of current drugs sold in the market and ban on the sale or import of non-complying goods.

Regulators universally continue to raise the slab for quality expectancy and compliance requirements.

Focus

Ranbaxy’s focus has always been on building a sustainable international trade by leveraging opportunities timely and firming up their proprietary business. Their front end focus is on erection of a robust and talented marketing organization, producing international brands and introducing differentiated goods in fast growing markets, while maximizing revenues from business segments where it already has a robust and recognized presence.

Ranbaxy’s focus has been on improving revenue from operations across markets in several ways. It does this by employing the following ways:

Market share improvement in target marketplaces through better product offerings

Focusing on brand markets to improve its product mix

Working towards achieving international leadership in specific generic goods

Supporting business structure for superior marketing synergies

Initiate cost-efficiency all over the business

Incessantly increase manufacturing competences

Human Resources

Ranbaxy is put together by the robust base of its people. In an information driven pharmaceutical sector, individuals are the most important drivers of growth. The company has always tried to shape the organization from end to end by individual and team assistance. It is a company which ideals respect and performance. Creation of a strong Employee Value Proposition is the cornerstone of this strategy.

Talent Management, learning and development, benefits and engagement are the four pillars on which the company is building Employee Value Proposition.

Ranbaxy has a performance oriented philosophy where there is importance given to meritocracy, independence and transparency.

There is a continuous emphasis on Learning and Development initiatives, personalized to address the needs of each of our business subdivisions and refurbishing other procedures and practices.

Ranbaxy values the ambitions and the opinion of the employees through an international engagement survey. The objective of this survey is to build a cohesive work culture.

Fine and Possible Takeover

The company is embroiled in a controversy in the United States over overcharging on one or more drugs in the state of Texas under its public funded Medicaid program. The state has imposed a fine of over 240 crores on the company. This is the second fine imposed on the company. The first fine was on account of the company’s previous slippages from the US-prescribed manufacturing practices. The company has already paid a fine of 500 million dollars in May, 2013.

Mumbai based pharmaceutical company, Sun Pharmaceuticals had agreed to acquire Ranbaxy in early 2014. The deal is estimated to be valued at 4 billion dollars and Sun Pharmaceuticals wants to complete the acquisition by the end of 2014.

References

1. EBSCO2. Indian Pharmaceutical Association3. Company Annual Reports4. www.moneycontrol.com 5. www.morningstar.com 6. www.ibef.org/industry/pharmaceutical-india.aspx 7. www.brandindiapharma.in/infographic-on-pharma-sector-business/ 8. www.icra.in 9. www.indiastat.com 10. www.equitymaster.com 11. www.in.kpmg.com 12. www.pharmaceuticals.gov.in 13. www.in.reuters.com 14. Marketline industry profile- Pharmaceuticals in India15. www.pwc.in 16. www.livemint.in 17. www.business.gov.in 18. www.mea.gov.in 19. www.indiainfoline.com 20. www.ey.com 21. www.ipapharma.org 22. Company and competitor websites23. www.pharmabiz.com 24. www.idma-assn.org/ 25. www.articles.economictimes.indiatimes.com