india market updates - knavcpa.com update march... · deals snapshot dear clients and associates:...

TRANSCRIPT

DEALS SNAPSHOT

January - March 2017

INDIA MARKET UPDATESINDIA MARKET UPDATES

DEALS SNAPSHOT

Dear Clients and Associates:

Welcome to the KNAV India Market Updates for the quarter ended March 2017.

This update includes an analysis of private equity/venture capital investments and the key M&A deals in the quarterended March 31, 2017.

Key highlights:

• The quarter had around 253 private equity/venture capital investments rounding up to a value of USD~7.95 bn. Some notable deals include:o Bharti Airtel’s sale of 10.3% stake in Bharti Infratel to KKR and Canada Pension Plan Investment Board (‘CPPIB’); &o Flipkart’s successful fund-raising of USD 1 bn from E-bay, Tencent Holdings and others, leading to a possible

merger between E-bay India and Flipkart.• The quarter had around 89 M&A transactions rounding up to USD~4.67 bn. The prominent deals are:o Vedanta’s acquisition of a USD 2.45 bn stake in Anglo American; &o Merger between Vodafone India and Aditya Birla Group-owned Idea Cellular.

• An insight into the evolution of Indian startup ecosystem is presented over the last 10 years.• A detailed analysis and a selected listing of a few notable deals are presented in this update.

Do share your comments and/or feedback on [email protected].

Thank you.

Vaibhav ManekPartner - Advisory services

Suparna DuaPartner - Investment banking

DEALS SNAPSHOT

Private equity/venture capital investments : Key deals

January - March 2017

3

DEALS SNAPSHOT

Of the total 193 deals in this quarter, the highest number

of deals were in the technology sector (48 deals), followed

by e-tail (20 deals) and education (14 deals).

Of the total USD 2.45 bn invested in this quarter, the

highest amount of funds were invested in the e-tail (USD

1.3 bn), followed by travel (USD 511 mn) and logistics

(USD 119 mn).

4

Consumer internet | PE/VC dealsThe following charts provide a sector-wise analysis of private equity/venture capital investments in theconsumer internet space in terms of number of deals and transaction value for the quarter.

1420

48

0

10

20

30

40

50

60

Ad

vert

isin

g

Co

nte

nt

Edu

cati

on

E-ta

il

Fin

ance

Fitn

ess

Foo

d &

Bev

erag

es

Gro

cery

Hea

lth

care

Hyp

erlo

cal

Logi

stic

s

Mar

ketp

lace

Med

ia &

…

Mo

bile

Pay

men

ts

Pro

fess

ion

al S

ervi

ce

Rea

l est

ate

Rec

ruit

men

t

Soci

al

Tech

no

logy

Trav

el

Number of deals1,313.4

119.4

510.6

0

200

400

600

800

1000

1200

1400

Transaction value in USD mn

DEALS SNAPSHOT

5

1825.4

1115.2

1864.0

0.0

500.0

1000.0

1500.0

2000.0

Transaction value in USD mn

10783

197

0

50

100

150

200

250

Number of deals

Of the total 1022 deals in this financial year, the highest

number of deals were in the technology sector (197

deals), followed by e-tail (107 deals) and healthcare (83

deals).

Of the total USD~8.5 bn invested in this financial year,

the highest amount of funds were invested in the

technology (USD 1.86 bn), followed by e-tail (USD 1.83

bn) and finance (USD 1.12 bn).

Consumer internet | PE/VC deals FY16-17 SnapshotThe following charts provide a sector-wise analysis of private equity/venture capital investments in theconsumer internet space in terms of number of deals and transaction value.

DEALS SNAPSHOT

Brick and mortar| PE/VC deals These charts provide a sector-wise analysis of private equity/venture capital investments in the brickand mortar area in terms of number of deals and transaction value for the quarter.

6

Of the total 60 deals in the quarter, the highest number

of investments were in the finance sector (16), followed

by healthcare and real estate(7 each) and logistics (6).

Of the total USD 5.5 bn invested in the quarter, the

highest amount of funds were invested in the power

sector (USD 1.56 bn) followed by technology (USD

1.5 bn) and telecom (USD 952 mn).

16

76

7

0

3

6

9

12

15

18

Number of deals

1564 1500

952

0

300

600

900

1200

1500

1800

Transaction value in USD mn

DEALS SNAPSHOT

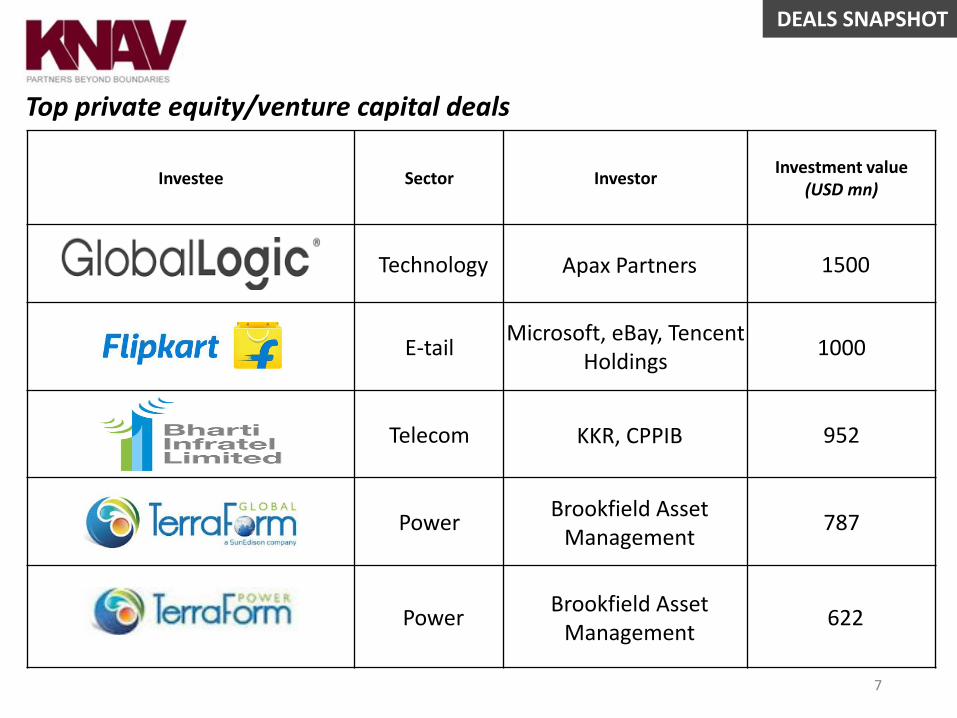

Investee Sector InvestorInvestment value

(USD mn)

Technology Apax Partners 1500

E-tailMicrosoft, eBay, Tencent

Holdings1000

Telecom KKR, CPPIB 952

PowerBrookfield Asset

Management787

PowerBrookfield Asset

Management622

Top private equity/venture capital deals

7

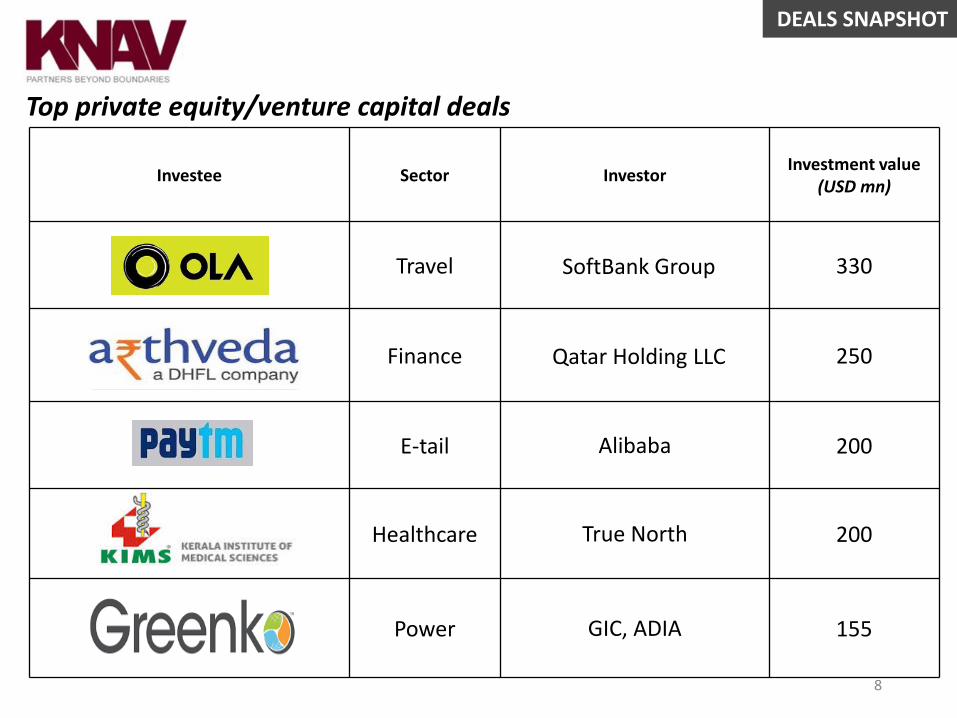

DEALS SNAPSHOT

Investee Sector InvestorInvestment value

(USD mn)

Travel SoftBank Group 330

Finance Qatar Holding LLC 250

E-tail Alibaba 200

Healthcare True North 200

Power GIC, ADIA 155

Top private equity/venture capital deals

8

DEALS SNAPSHOT

Evolution of Indian startups in last 10 years

9

DEALS SNAPSHOT

Company

Founders Sachin Bansal & Binny Bansal Ashish KashyapNaveen Tewari , Mohit Saxena, Amit Gupta, Abhay Singhal

Business segment Online retailer Online travel group Global mobile ad network

Prominent investorsTiger Global, Accel Partners, Naspers, Morgan Stanley, E-bay, DST Global

Naspers, TencentSoftBank, Mumbai Angels, Kleiner Perkins Caufield & Byers (KPCB), Sherpalo

Total funding till date

USD 4.15 bn USD 250 mnUSD 220.6 mn + USD 100 mn in debt capital

Valuation USD 10 bnUSD 720 mn (transaction value)

USD 2.5 bn (Peak valuation)

AcquisitionMyntra, Phonepe, Lets Buy, Jabong (via Myntra), FX Mart

Redbus, Yourbus, Gaadi WebOverlay Media, Metaflow, Sproutinc, Appgalleries, Appstores, Appbistro

Current scenario

Striving to achieve profitability and retaining its market leadership while facing stiff competition.

Merged with MakeMyTrip in October 2016.

Successful Chinese market entry, dealing with the challenge of exodus of talent.

Startups - 10 year snapshot

10

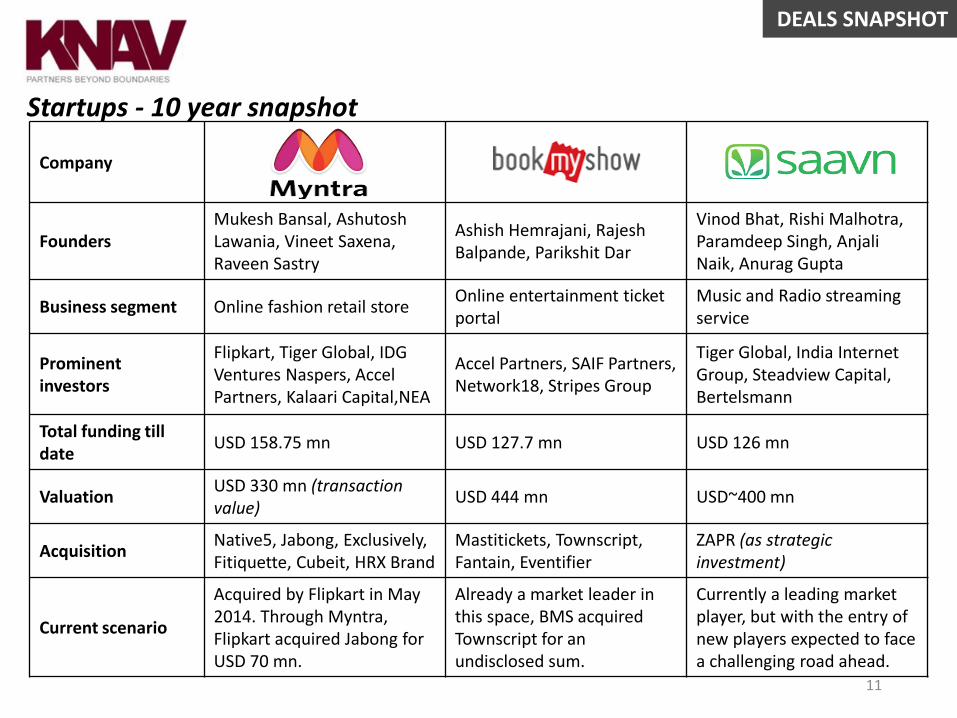

DEALS SNAPSHOT

Company

FoundersMukesh Bansal, Ashutosh Lawania, Vineet Saxena, Raveen Sastry

Ashish Hemrajani, Rajesh Balpande, Parikshit Dar

Vinod Bhat, Rishi Malhotra, Paramdeep Singh, Anjali Naik, Anurag Gupta

Business segment Online fashion retail store Online entertainment ticket portal

Music and Radio streaming service

Prominent investors

Flipkart, Tiger Global, IDG Ventures Naspers, Accel Partners, Kalaari Capital,NEA

Accel Partners, SAIF Partners, Network18, Stripes Group

Tiger Global, India Internet Group, Steadview Capital, Bertelsmann

Total funding till date

USD 158.75 mn USD 127.7 mn USD 126 mn

ValuationUSD 330 mn (transaction value)

USD 444 mn USD~400 mn

AcquisitionNative5, Jabong, Exclusively, Fitiquette, Cubeit, HRX Brand

Mastitickets, Townscript, Fantain, Eventifier

ZAPR (as strategic investment)

Current scenario

Acquired by Flipkart in May 2014. Through Myntra, Flipkart acquired Jabong for USD 70 mn.

Already a market leader in this space, BMS acquired Townscript for an undisclosed sum.

Currently a leading market player, but with the entry of new players expected to face a challenging road ahead.

Startups - 10 year snapshot

11

DEALS SNAPSHOT

Company

Founders Neeraj GuptaPranay Chulet and Jiby Thomas

Deepinder Goyal and Pankaj Chaddah

Business segment Radio taxi aggregator Classified ads portalPlatform for food discovery and online ordering

Prominent investors

India Value Fund Advisors/ True North, Brand Capital

Brand Capital, Tiger Global Management, Kinnevik AB, NVP, Warburg Pincus

Vy Capital, Info Edge, Temasek Holdings,

Total funding till date

USD 75 mn USD 370.15 mn USD 225 mn

Valuation NA USD 1.5 bn USD 500 mn- USD 1 bn

Acquisition -Grabhouse, Stayglad, Stepni.com, CommonFloor, Realty Compass, Hiree

Sparse Labs, Mekanist, Urbanspoon, NexTable, MapleGraph Solutions Pvt. Ltd.

Current scenario

Although being one of the pioneers in radio taxi service, it has seen the likes of Ola & Uber disrupt the market, thus losing significant market share.

Has successfully diversified into car, real estate and jobs platforms. In competition with firms like OLX.

Processes 2 mn online orders in a month. Has presence in 23 countries like USA, UAE and Brazil.

Startups - 10 year snapshot

12

DEALS SNAPSHOT

Company

Promoter Shashank ND, Abhinav Lal Byju Raveendran Amit Jain

Business segmentPractice management tool for doctors and a directory to search doctors

Hybrid test preparation & learning platform

Auto portal for car research and buying/selling deals

Prominent investors

Tencent Holdings, Sequoia Capital, Altimeter, CapitalG, INRI Fund

Chan Zuckerberg Initiative, Sequoia Capital, Aarin Capital, Times Internet

CapitalG, Sequoia Capital, HDFC Bank, Hillhouse Capital Group, RNT Associates

Total funding till date

USD 179.5 mn USD 204 mn USD 65 mn

Valuation USD 600-650 mn USD 500 mn USD 380 mn (May 2016)

AcquisitionEnlightiks, Instahealth, Fitho, Qikwell Technologies, Geni Technologies

Vidyartha (SPAN Thoughtworks Pvt. Ltd.)

Zigwheels, Gaadi Web, Zolob Technologies

Current scenario

Focus on global expansion. Aims to enter the health insurance segment through partnerships with existing service providers.

Competing with US based edtech companies like Cousera, Udacity, Udemy. Focussing on acquisitions for content delivery.

Has branched out to provide new car services after it acquired Gaadi Web. Revenue generation from advertisements.

Startups- 10 year snapshot

13

DEALS SNAPSHOT

Mergers & acquisitions : Key deals January - March 2017

14

DEALS SNAPSHOT

15

• Technology is placed at #1 position with 18 dealsSome of the highlights in the technology sector deals were: Tech Mahindra acquired CJS Solutions, Zensar acquiredKeystone Logic, Freshdesk Inc. acquired Pipemonk and WNS Ltd acquired Denali Sourcing Services.

• Finance is placed at #2 position with 8 dealsSome of the prime deals in the finance sector were: IDFC Bank acquired stake in IIFL Holdings from JP Morgan,Anand Rathi acquired Religare's wealth management business, KredX acquired HummingBill and IndusInd Bankacquired IL&FS Securities Services Ltd.

• Pharmaceuticals is placed at #3 position with 7 dealsSome of the deals in pharmaceutical sector were: Zydus Cadila acquired Sentynl Therapeutics, Ascendis Health Ltd acquired Cipla Agrimed Proprietary Ltd and Cipla Vet Proprietary Ltd, Sun Pharma acquired Thallion Pharmaceuticals and Aurobindo Pharma acquired Portugal's Generis Farmaceutica from Magnum Capital.

Top M&A sectors

FinancePharmaceuticals

Technology

DEALS SNAPSHOT

Sector-wise analysis | M&A deals

16

The ensuing charts provide an analysis of the M&A transactions in the quarter of the number of deals and the transaction value.

There were 89 M&A deals in the this quarter. Thetechnology sector bagged the highest number of deals (18deals) followed by finance (8 deals) and pharmaceutical (7deals). The deals in technology were in data analytics, ITservices and cloud.

In the quarter, the total transaction value of all dealsamounted to USD 4.6 bn compared to USD 5.2 bn in theprevious quarter. In terms of the transaction value, thehighest M&A deals were witnessed by mining sector(USD 2.45 bn) followed by pharmaceutical (USD 515 mn)and telecom (USD 244 mn).

87

18

0

4

8

12

16

20

Au

tom

ob

ile

Bea

uty

& W

elln

ess

Ch

em

ical

s

E-ta

il

Fin

ance

Fitn

ess

Foo

d &

Bev

erag

es

Hea

lth

care

Infr

astr

uct

ure

Man

ufa

ctu

rin

g

Med

ia &

En

tert

ain

me

nt

Pac

kagi

ng

Pay

men

ts

Ph

arm

aceu

tica

l

Po

wer

Pro

fess

ion

al S

ervi

ce

Rea

l Est

ate

Tech

no

logy

Tele

com

Trav

el

Number of deals

2450

515244

0

500

1000

1500

2000

2500

3000

Transaction value in USD mn

DEALS SNAPSHOT

Top M&A deals for the quarter

Target Acquirer SectorTransaction value

(USD mn)

Manufacturing 2450

(4G Business)

Telecom 244

(White goods and electronics business)

Consumer 230

Power 200

Pharmaceuticals 171

17

DEALS SNAPSHOT

Target Acquirer SectorTransaction value

(USD mn)

(Select portfolio drugs)

Pharmaceuticals 171

(Wealth management)

Finance 160

Pharmaceuticals 142

(UK business)

Infrastructure 125.6

(CJS Solutions Group LLC)

Technology 89.5

18

Top M&A deals for the quarter

DEALS SNAPSHOT

Analysis of a few transactions

January - March 2017

19

DEALS SNAPSHOT

• The confluence of Vodafone (India's # 2 telecom operator) and Idea,

(India’s # 3 telecom operator), lays the foundation of an entity with a

value of INR 1.55 lakh crore (USD 23.5 bn)*, making it India's largest

telecom company that will surpass Bharti Airtel and the global #2 after

China Mobile.

• Initially, Aditya Birla Group backed – Idea will acquire 4.9% from

Vodafone for INR 3,874 crore (USD 586 mn), or INR 108 a share, to take

its stake to 26%, with Vodafone holding 45.1%.

• Mr. Kumar Mangalam Birla shall be the Chairman of the merged

enterprise, while the CFO shall be appointed by Vodafone. The CEO and

COO shall be jointly appointed before the closure of the merger.

• Prior to completion of the transaction, Vodafone and Idea intend to sell

their standalone tower assets and Idea’s 11.15% stake in Indus Towers to

reduce leverage in the combined company.

• The merger is likely to create cost and capex synergies for the merged

entity.

• The new entity may also face some regulatory hurdles, mainly on account

of liberalising administratively allocated airwaves and exceeding

spectrum holding.

*(Source: Economic Times and KNAV Internal Research)20

• Combined entity with a value

of INR 1.55 lakh crore;

• India's largest telecom

company; &

• Global #2 after China Mobile.

Vodafone-Idea merger

Deal analysis

DEALS SNAPSHOT

• Post the Vodafone-Idea merger, Airtel lost its market leadership position

maintained for over 15 years to the merged entity.

• With the aggressive strategy adopted by Jio for subscriber aggregation,

domination over 'data' oriented subscriber base will define the market

leadership.

• In this quarter, Bharti Airtel has successfully acquired Telenor India

operations for USD 300 mn and Tikona 4G Business for USD 244 mn to

counter the competition and maintain its domination.

• Telenor deal will help Airtel to gain spectrum and subscriber base and

provide 4G data edge.

• Tikona deal shall give Airtel the access to 4G airwaves in Gujarat, UP (East

and West), Himachal Pradesh and Rajasthan.

• It has also hived off 10.3% stake in Bharti Infratel to Kohlberg Kravis

Roberts (‘KKR’) and CPPIB for INR 6,194 cr (USD 952 mn).

• This hive-off is likely to give Airtel the flexibility to step up capital

expenditure for the Indian wireless business to expand its data network

coverage and capacity.

India Operations

4G network

Sells 10.3%

21

Bharti Airtel’s business strategy

Deal analysis

DEALS SNAPSHOT

22

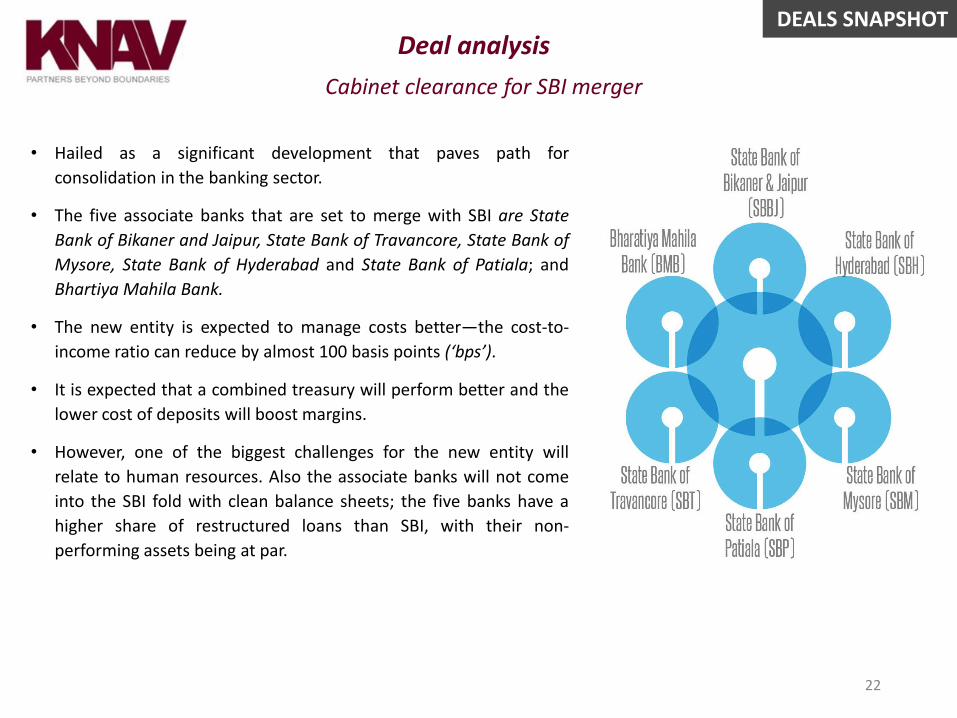

• Hailed as a significant development that paves path for

consolidation in the banking sector.

• The five associate banks that are set to merge with SBI are State

Bank of Bikaner and Jaipur, State Bank of Travancore, State Bank of

Mysore, State Bank of Hyderabad and State Bank of Patiala; and

Bhartiya Mahila Bank.

• The new entity is expected to manage costs better—the cost-to-

income ratio can reduce by almost 100 basis points (‘bps’).

• It is expected that a combined treasury will perform better and the

lower cost of deposits will boost margins.

• However, one of the biggest challenges for the new entity will

relate to human resources. Also the associate banks will not come

into the SBI fold with clean balance sheets; the five banks have a

higher share of restructured loans than SBI, with their non-

performing assets being at par.

Cabinet clearance for SBI merger

Deal analysis

DEALS SNAPSHOT

• Havells India has acquired white goods and electronics business of

Lloyd Electrical and Engineering Ltd for a value of USD 230 mn.

• Lloyd’s 12% market share in the air conditioners industry

gives Havells a good start into the white goods segment.

• The acquisition comes at a time when Havells’ core business —

switchgears — is facing problems on volume and profitability fronts;

and with the onset of summer, white goods like air conditioners and

refrigerators are expected to drive the sales.

• The manufacturing units along with the low margin Original

Equipment Manufacturer (‘OEM’) and the projects business (AC

supplier to Railways) have been kept out of this deal.

• Lloyds is expected to utilise the net proceeds from sale to partially

bring down the debt and for investments in its other interests.

23

White Goods Business

Acq

uires

Havell’s acquisition of white goods business of Lloyds

Deal analysis

DEALS SNAPSHOT

• Tech Mahindra acquired US-based healthcare software provider CJS

Solutions Group LLC, part of The HCI Group for USD 110 mn.

• Tech Mahindra will pay USD89.5 mn upfront for around 84.7% of CJS'

stake, with the remainder acquisition over the next three years.

• CJS Solutions provides complete implementation of Electronic Health

Record (‘HER’) and Electronic Medical Record (‘EMR’) software.

• The acquisition will not only position Tech Mahindra as a significant

player in the healthcare provider space, but will also provide an

opportunity to go deeper in this space through the EMR

implementation and its related services route.

• This transaction showcases that Indian companies are speeding up

acquisitions of U.S. firms to avoid challenges posed by an expected

tightening of visa rules in their biggest market.

24

Acq

uires

CJS Solutions Group LLC

Tech Mahindra’s acquisition of CII Solutions Group LLC

Deal analysis

DEALS SNAPSHOT

About KNAV

KNAV refers to one or more of the member firms of KNAV International Limited (‘KNAV International’), which itself is a not-for-profit, non-practicing, non-trading corporation incorporated in Georgia, USA.

KNAV International is a charter umbrella organization that does not provide services to clients. Services of audit, tax, valuation, risk and business advisory are delivered by KNAV's independent member firms in their respective global jurisdictions. All member firms of KNAV in India and North America are member firms of the US$ 1.6 billion, US headquartered Allinial Global.

Website - www.knavcpa.com

Reach us

If you want to know more about KNAV or its services please contact Ms. Suparna Dua at the KNAV Mumbai office on: +91 97696 57090

Suggestions/feedback

For suggestions/feedback on this newsletter please contact Mr. Vaibhav Manek at the KNAV Mumbai office on: [email protected]. We will be glad to hear from you.

Editorial credits

Deals Snapshot Editorial Hardik Adenwala and Akshay Mahalaxmikar–– KNAV Mumbai

The source of our data is our market research, publicly available reports and press items, and independent databases. While KNAV has made reasonable endeavors to ensure that the information provided in this newsletter is accurate and up to date as at the time of issue, KNAV shall not be liable for any errors, inaccuracies or delays in the information, nor for any actions taken in reliance thereon, nor does it endorse any views or opinions. KNAV disclaims all warranty, express or implied, as to the accuracy or completeness of any of the content provided, or as to the fitness of the content for any purpose to the extent permitted by law. The content herein is not appropriate for the purposes of making a decision to carry out a transaction or trade and does not provide any form of advice (investment, tax, legal) amounting to investment advice, nor make any recommendations or solicitations regarding particular financial instruments, investments or products, including the buying or selling of securities. KNAV has not undertaken any liability or obligation relating to the purchase or sale of securities for or by any person in connection with this document.

This newsletter is intended only for the individuals addressed. The information contained in this newsletter is privileged, confidential, and may be protected from disclosure; please be aware that any other use, printing, copying, disclosure or dissemination of this communication may be subject to legal restriction or sanction. Copyright and any other intellectual property rights in its contents are the sole property of KNAV.

CANADA | FRANCE | INDIA | NETHERLANDS | SINGAPORE | SWITZERLAND | UK | USA

25

DEALS SNAPSHOT

26

ContactAmsterdam

Drs. Henk Burke

Tel: +312 066 44 054

Atlanta

Atul Deshmukh

Tel: +1 678 584 1200

Bangalore

Shrenik Kataria

Tel: +91 80 4113 1896

Geneva

Claude Rey

Tel: +41 24 466 77 27

Hyderabad

Dayaniwas Sharma

Tel: +91 40 2324 0700

London

Amanjit Singh

Tel: +44 20 3617 6200

Lyon

Martine Chabert

Tel: +33 478 182 694

Mumbai

Khozema Anajwalla

Tel: +91 22 6164 4800

New Delhi

Monish Chatrath

Tel: +91 11 4106 9400

Singapore

Wayne Soo

Tel: +65 6846 8376

Toronto

Harshad Parekh

Tel: +1 416 229 1411