incorporating environmental, social and …documents.worldbank.org/.../pdf/125442-wp-public.pdf ·...

TRANSCRIPT

Incorporating ENVIRONMENTAL,

SOCIAL and GOVERNANCE (ESG)Factors into FIXED INCOME

INVESTMENTGeorg Inderst and Fiona Stewart

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

© 2018 The World Bank Group

1818 H Street NW Washington, DC 20433 Telephone: 202-473-1000 Internet: www.worldbank.org All rights reserved.

This volume is a product of the staff of the World Bank Group. The World Bank Group refers to the member institutions of the World Bank Group: The World Bank (International Bank for Reconstruction and Development); International Finance Corporation (IFC); and Multilateral Investment Guarantee Agency (MIGA), which are separate and distinct legal entities each organized under its respective Articles of Agreement. We encourage use for educational and non-commercial purposes.

The findings, interpretations, and conclusions expressed in this volume do not necessarily reflect the views of the Directors or Executive Directors of the respective institutions of the World Bank Group or the governments they represent. The World Bank Group does not guarantee the accuracy of the data included in this work.

Rights and Permissions

The material in this publication is copyrighted. Copying and/or transmitting portions or all of this work without permission may be a violation of applicable law. The World Bank encourages dissemination of its work and will normally grant permission to reproduce portions of the work promptly.

All queries on rights and licenses, including subsidiary rights, should be addressed to the Office of the Publisher, The World Bank Group, 1818 H Street NW, Washington, DC 20433, USA; fax: 202-522-2422; e-mail: [email protected].

Photo Credits: IFC and World Bank Photo Libraries and Shutterstock

Citation: Inderst, G. and Stewart, F., Incorporating Environmental, Social and Governance (ESG) Factors into Fixed Income Investment. World Bank Group publication, April 2018.

INCORPORATING ENVIRONMENTAL, SOCIAL AND GOVERNANCE (ESG) FACTORS INTO FIXED INCOME INVESTMENT | I

TABLE of CoNTENTS

| I

ACRONYMS AND ABBREVIATIONS III

ACKNOWLEDGMENTS V

EXECUTIVE SUMMARY VII

1. INTRODUCTION AND BACKGROUND 1Definition of ESG Investing 2Investor Motivations 3ESG and Impact Investment Approaches 6

2. WHAT IS ESG ANALYSIS IN FIXED INCOME INVESTING? 9Corporate Issuers 11Sovereign Issuers 12Other Debt and Securities 14

3. ESG AND FINANCIAL PERFORMANCE – MAIN RESEARCH FINDINGS 17Corporate Bonds 17Sovereign Bonds 19Fixed Income Funds 19

4. ESG INVESTMENT TOOLS FOR FIXED INCOME 23Credit Ratings and ESG 23ESG Scores/Rankings 24Country Scores 26ESG Fixed Income Indices 27

5. HOW IS ESG BEING IMPLEMENTED BY FIXED INCOME INVESTORS? 31Green, Social, Sustainable and Other Thematic Bonds 32Passive Investing 35Active Investing 36ESG ‘Holistic’ 36

II | TABLE OF CONTENTS

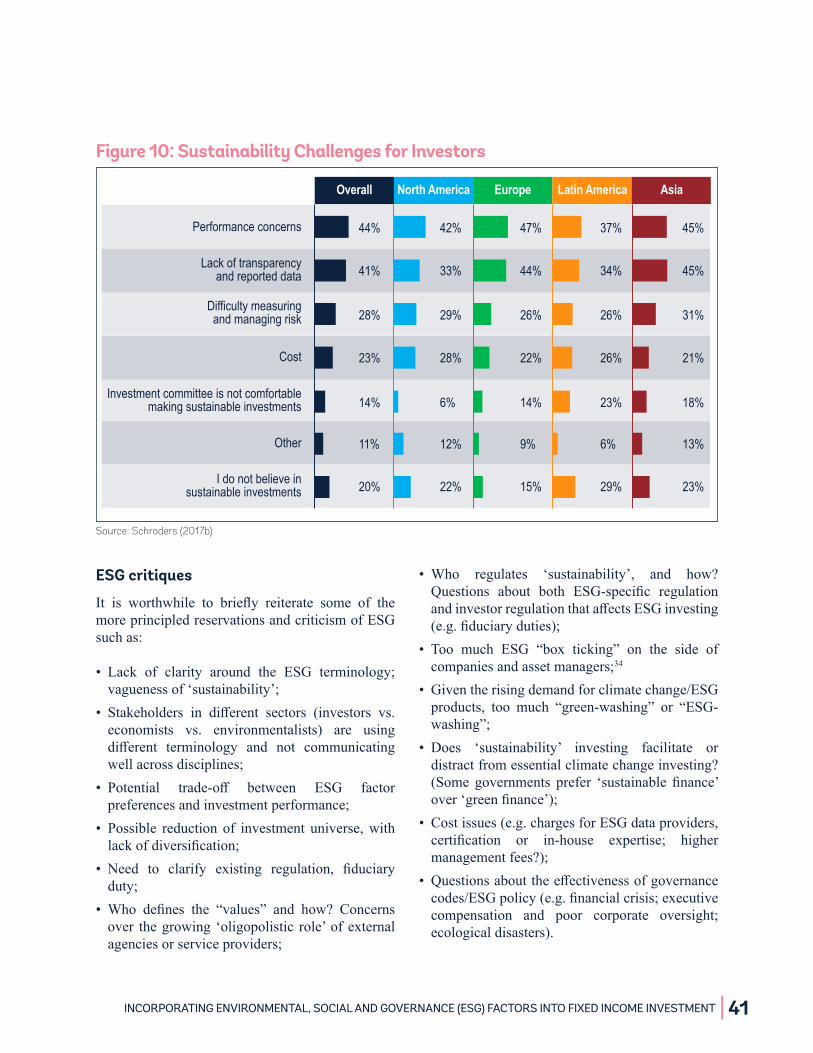

6. MAIN TRENDS AND CHALLENGES 39State of the Art 39Issues with ESG Investing 40

7. CONCLUSIONS: FROM PROCESS TO IMPACT 45Key Lessons for Investors 45Ways Forward 46

APPENDICES 49

REFERENCES 55

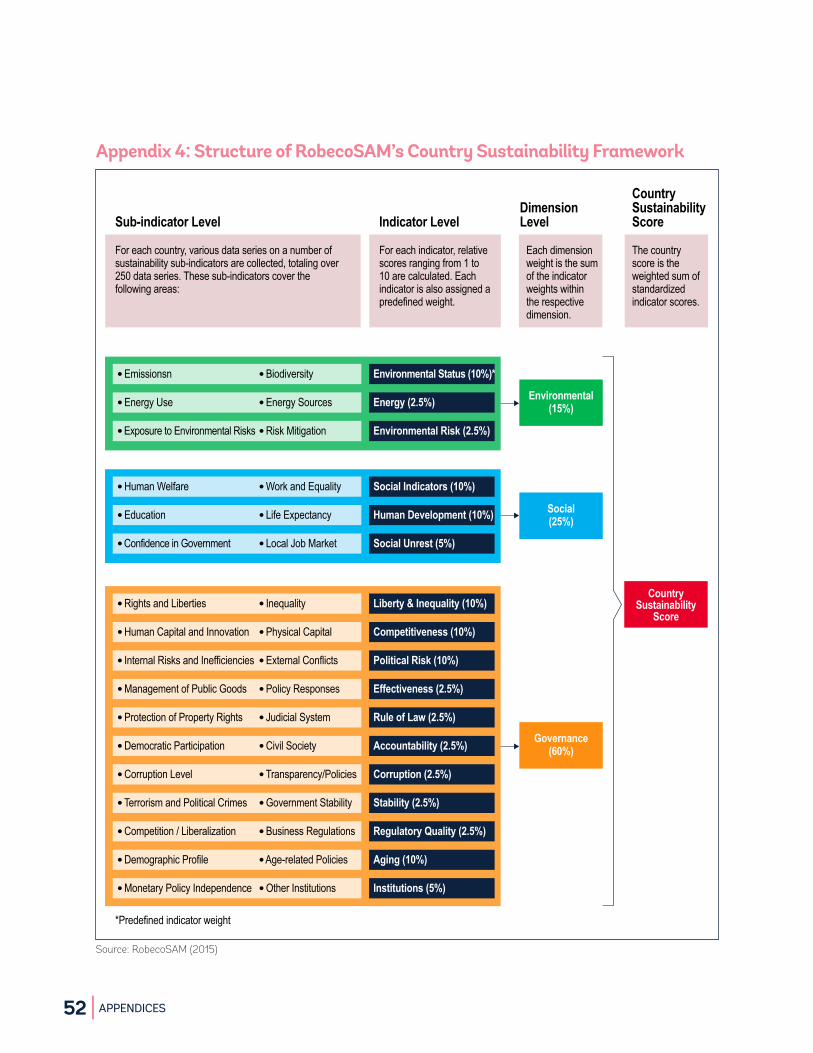

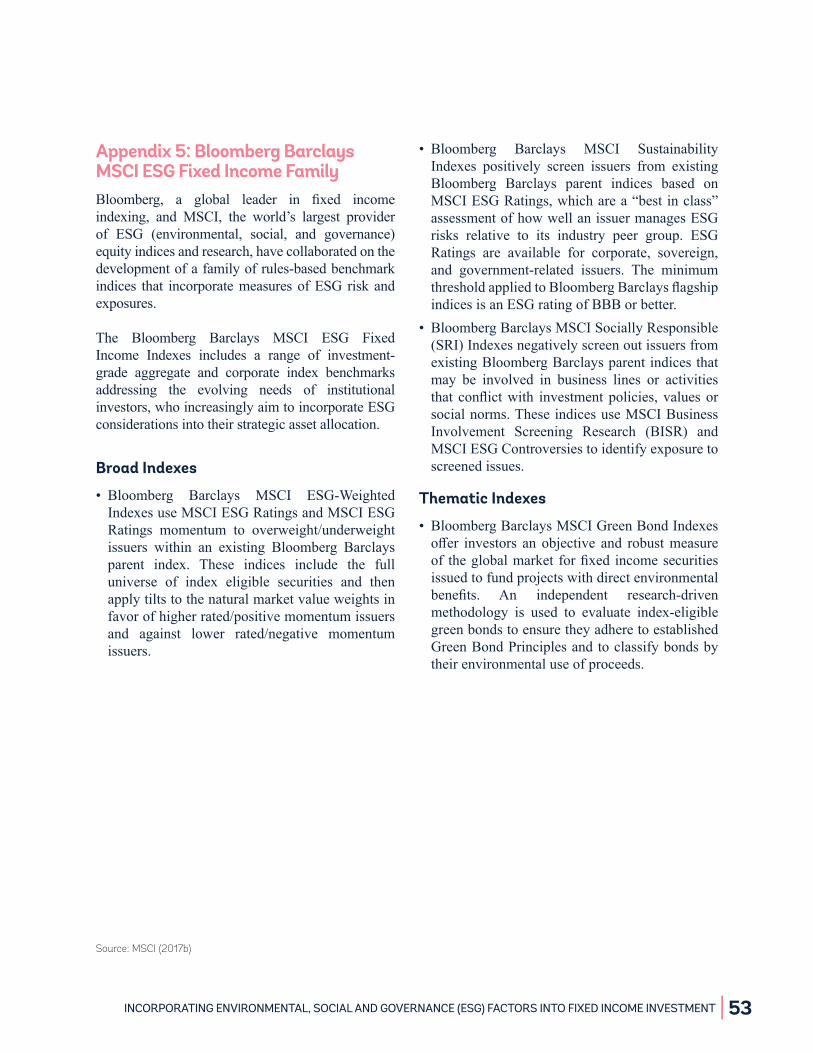

Appendix 1: Institutions Interviewed for This Report 49Appendix 2: ESG Criteria 50Appendix 3: Characteristics of Fixed Income and Implications for ESG 51Appendix 4: Structure of RobecoSAM’s Country Sustainability Framework 52Appendix 5: Bloomberg Barclays MSCI ESG Fixed Income Family 53

ENDNOTES 61

BOXES

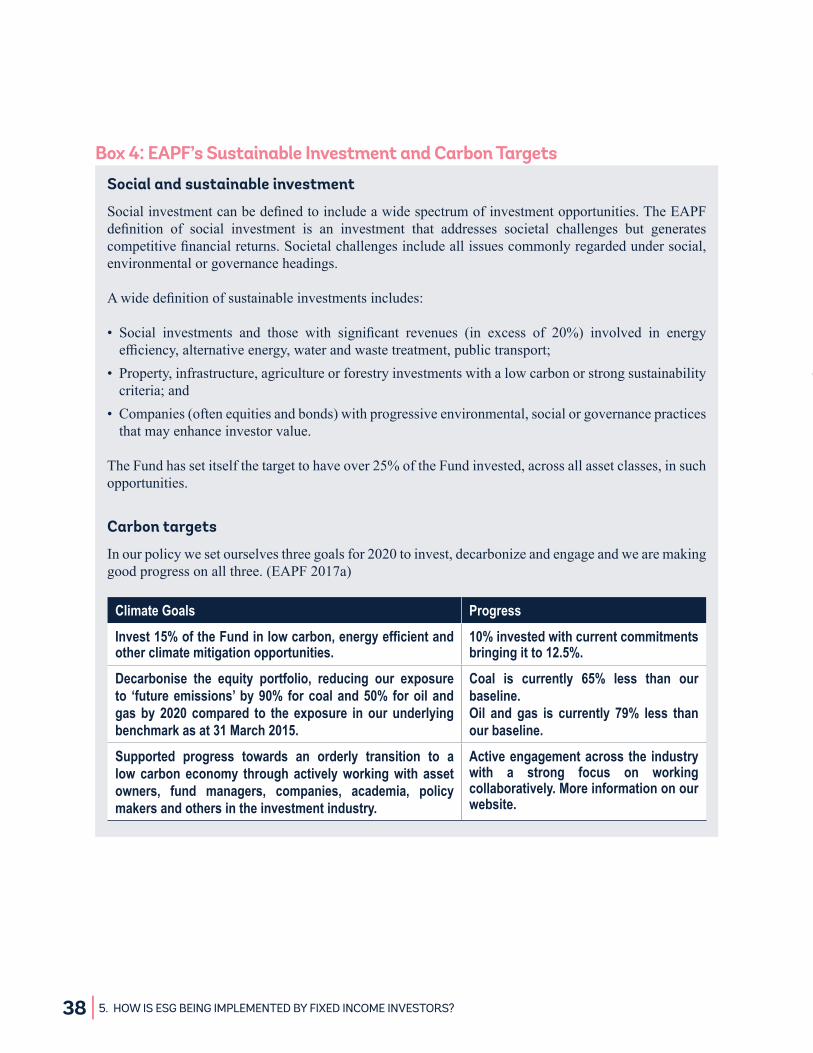

Box 1: ESG Investor Associations, Standards and Codes 4Box 2: ESG and Regulation 5Box 3: Climate Investing 6Box 4: EAPF’s Sustainable Investment and Carbon Targets 38

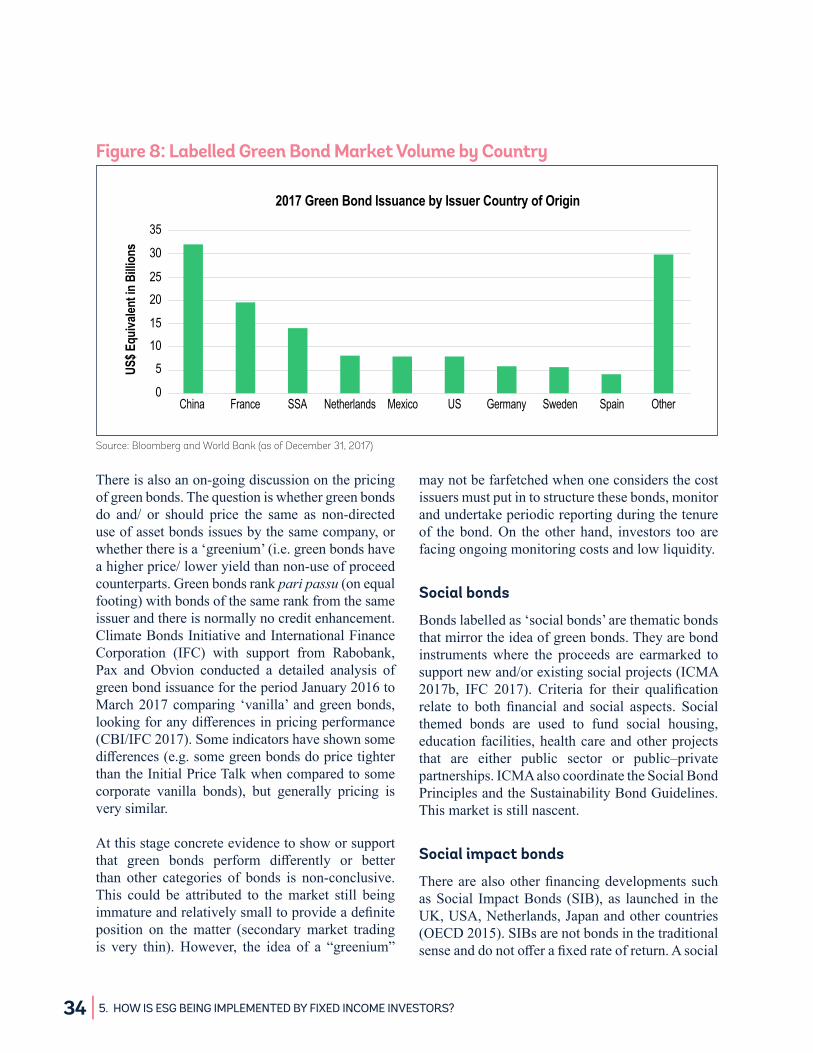

FIGURESFigure 1: Impact Investment Drivers 8Figure 2: Suitability of ESG Investment Strategies for Equity and Fixed Income Investing 10Figure 3: Level of ESG Incorporation in Fixed Income 15Figure 4: Main Research Findings 20Figure 5: RobecosSAM ESG Weightings 27Figure 6: Level of ESG Integration 32Figure 7: Labelled Green Bond Market Volume by Type of Issuer 33Figure 8: Labelled Green Bond Market Volume by Country 34Figure 9: PGGM ESG Approach 37

TABLESTable 1: Engagement for Equity and Bond Investors 11Table 2: Screening Criteria for Different Types of Issuers 13Table 3: MSCI ESG Key Issues for Companies 25Table 4: Categories Available for Bespoke Screening 28Table 5: ESG Strategies in Fixed Income (by Volume of Assets) 31

INCORPORATING ENVIRONMENTAL, SOCIAL AND GOVERNANCE (ESG) FACTORS INTO FIXED INCOME INVESTMENT | III

ACroNymS ANd ABBrEviATioNS

ABS Asset-backed Securities AI ArtificialIntelligenceAIGCC AsiaInvestorGrouponClimate ChangeAIM AffirmativeInvestmentManagementALM AssetandLiabilityManagementAODP AssetOwnersDisclosureProjectCAT CatastropheBondsCCM ConventiononClusterMunitionsCDP CarbonDisclosureProjectCDS CreditDefaultSwapCFP CorporateFinancialPerformanceCRA CreditRatingAgencyCSR CorporateSocialResponsibilityEAPF EnvironmentAgencyPensionFundEIB EuropeanInvestmentBankETF ExchangeTradedFundsESG Environmental,SocialandGovernanceGBP GreenBondPrinciplesGIC GlobalInvestorCoalitiononClimate ChangeGIIN GlobalImpactInvestingNetworkGP GeneralPartnerGPIF GovernmentPensionInvestmentFundGRI GlobalReportingInitiativeGSIA GlobalSustainableInvestmentAllianceGSSB GlobalSustainabilityStandardsBoard

ICGN International Corporate GovernanceNetworkICMA InternationalCapitalMarket AssociationIFC InternationalFinanceCorporationIG Investment-gradeIGCC InvestorGrouponClimateChangeIIGCC InstitutionalInvestorsGroupon ClimateChangeILS Insurance- linkedSecuritiesIRIS ImpactReportingandInvestment StandardsJFSA Japan’sFinancialServiceAuthorityLDI Liability-drivenInvestmentMBS Mortgage-BackedSecurityOECD OrganizationforEconomic Co-operationandDevelopmentPE PrivateEquityPRI UNPrinciplesofResponsibleInvestingRI ResponsibleInvesting

III

IV | ACRONYMS AND ABBREVIATIONS

SASB SustainabilityAccountingStandards BoardSBP SocialBondPrinciplesSDGs SustainableDevelopmentGoalsSDSN SustainableDevelopmentSolutions NetworkSI SustainableInvestingSIB SocialImpactBonds

SPV SpecialPurposeVehicleSRI SociallyResponsibleInvestmentTCFD TaskForceonClimate-related FinancialDisclosuresTIPP TheInvestmentIntegrationProjectUNEP UnitedNationsEnvironment ProgrammeUNGC UNGlobalCompact

INCORPORATING ENVIRONMENTAL, SOCIAL AND GOVERNANCE (ESG) FACTORS INTO FIXED INCOME INVESTMENT | V

ACkNowLEdgmENTS

This research report is the result of apartnership between theWorldBankGroup(WBG)andGovernmentPensionInvestmentFund

(GPIF)ofJapan,initiatedbytheWorldBankGroup’sPresident,JimYongKim, andGPIF’sChief InvestmentOfficer,HiroMizuno.TheaimisfortheWorldBankandIFC–memberoftheWorldBankGroupfocusedontheprivatesector–andGPIFtocollaborateoninitiativesthatpromotestrategiesforincludingenvironmental,socialandgovernance(ESG)criteriaininvestmentdecisionsacrossassetclasses.Ultimately,thegoalistodirectmorecapitaltowardssustainableinvestmentsandleveragetheprivatesectortoachievethescaleofinvestmentneededtomeettheSustainableDevelopmentGoals.

The partnership reflects GPIF’s strategiccommitment to advancing the integrationofESGconsiderationsintoallassetclassesofitsportfolio.The research report is focused on integration ofESG considerations for fixed income. From theWorld BankGroup side, the research contributesto the commitment to maximizing finance fordevelopment and catalyzing the developmenttowardsmoresustainablecapitalmarkets.

The authors of the paper are Georg Inderst andFiona Stewart. Georg Inderst is an independentExpert Consultant, specializing in green financeand infrastructure investment (Inderst Advisory,London).FionaStewart is aLeadFinanceSectorSpecialist in the Finance, Competitiveness andInnovation Global Practice of the World Bank.Theauthorswould,inthefirstplace,thankalltheasset owners, investment managers, international

associations, private sector service providersand individual experts for sharing their expertiseand experiences. In addition, Joaquim Levy,ManagingDirector andWorldBankGroupCFO,Arunma Oteh, World Bank Treasurer and VicePresident, JingdongHua, IFCVice President andTreasurer,MonishMahurkah,IFCVicePresident,forspearheadingthisworkwithintheWorldBankGroup. Heike Reichelt and Atiyah Curmally forleadingthepartnershipwithGPIF,andthefollowingfor their support and input to the study:AlfonsoGarciaMora,JohnGandolfo,GeorgeRichardson,andAndrewCrossandSamuelMunzeleMaimbo.The authors are particularly grateful to ColleenKeenan, Marcelo Jordan, Martijn Regelink,HarunDogo,SvetlanaKlimenko,BeritLindholdt-Lauridsen and Alex Berg for their expert input.Yoshiyuki Arima, Kenichiro Shiozawa and MisaYanagifromtheTokyoofficeforalltheirassistance

VI | ACKNOWLEDGMENTS

–includingarrangingforthereporttobetranslatedintoJapanese.AichinLimJonesforgraphicdesignand layout, Luidmila Uvarova andNinaVucenikfor knowledge management and communicationssupport, and InnaRemizova andLeahKusenselaforbeingexcellent researchassistants.The reportbenefited from comments from peer reviewersincludingAkinchanJain,GregRosenberg,Eivind

Oy,andJudithMoore.Finally,ithasbeenapleasureworking with the GPIF team. We would like tothank Norihiro Takahashi and Hiro Mizuno andfortheirsupportandleadership,andTetsuyaOishi,GenzoKimura,DaikiNishida,andKeijiWatanabefor theirhelpful inputandcollaboration.We lookforward to continuing the dialogue and workingwiththeminfuture.

INCORPORATING ENVIRONMENTAL, SOCIAL AND GOVERNANCE (ESG) FACTORS INTO FIXED INCOME INVESTMENT | VII

ExECuTivE SummAry

A growing body of research shows thatEnvironmental, Social and Governance(ESG) factors are material credit risk for fixed

incomeinvestors.TheevidencesuggeststhatincorporatingESGintofixed income investing should be part of the overall credit riskanalysisandshouldcontributetomorestablefinancialreturns.ItalsodispelsthemyththatincorporatingESGmeanshavingtosacrificefinancialreturns.ESGinvestingisincreasinglybecomingpartofthemainstreaminvestmentprocessforfixedincomeinvestors,asopposedtoaspecialist,segregatedactivity,oftenconfinedtogreenbonds.

Though fixed income has its own challenges withintegratingESGissues,itiscatchingupfastwiththeequityspace(particularlycorporateandsupranationalbonds but less - so far - sovereign issuers, asset-backedorprivatedebt).LeadinginvestorsaregoingfurtherandviewingESGnotjustasanaspectofriskandreturn,butmergingESGand‘impact’investing.Thisincludesmeasuringtheimpactoftheirportfoliosontargetedenvironmentalandsocialoutcomes,andbeyond,suchasmappingimpactusingtheSustainableDevelopmentGoals(SDGs).

Different methods for applying ESG are beingadoptedbyfixedincomeinvestors:frompurchasing‘labelled’(green,social,and/orsustainable)bondsand setting up or investing inESG/SRI (SociallyResponsible Investment) funds; to followingESG indices; to hiring ESG active managers; toincorporating and embedding ESG across thewhole investment process. This can be done byeither following the methodology of different

external serviceprovidersand /orbycustomizingsuchproductswiththeinstitutionalinvestor’sownphilosophyandgoals.

Yet, many investors find implementing ESG inpractice a challenge, which can be exacerbatedwhen it comes to their fixed income portfolios.There are still no standard definitions of ESG– with diverse views particularly in the ‘social’area. Data – though improving and coming fromincreasingly varied sources – is still wantingparticularlyinemergingmarkets.Infixedincome,there are additional issues such as how to pursueengagementwithissuers(particularlysovereigns),the role ESG plays in credit ratings, the lack ofchoiceofindicescomparedtotheequityspace,aswellasadearthofspecificESG-focusedproducts.Therearealsochallengesinthegreenbondmarketswithdemandoutstrippingsupply.ConceptualworkonESGandfixedincomealsoneedstogobeyondcreditrisk(suchastherelationshipofESGissueswithliquidityandothermarketrisks).

VIII | EXECUTIVE SUMMARY

ESGinvestingisdevelopingfromapurelyprocess-driven to a more outcome-driven activity. Goingforward,first,initiativestoimprovethebreadthanddepthofESGdatashouldcontinuetobesupported.Second,morerigorousresearchontherelationshipbetweenESGfactorsandfinancialrisksandreturnsinfixedincomeisalsorequired.Third,standards,

principles and metrics for applying ESG andimpactinvestingcanberefinedtoallowinvestorsto customize their approach from a robust basis.Finally, more innovative, scalable products toaccommodatethegrowingdemandforfixedincomesustainableinvestmentscouldbedeveloped.

INCORPORATING ENVIRONMENTAL, SOCIAL AND GOVERNANCE (ESG) FACTORS INTO FIXED INCOME INVESTMENT | 1

1. iNTroduCTioN ANd BACkgrouNd

Capital markets play a vital role inchanneling investment into the economy tohelp drive growth and prosperity. Asset owners

andfinancialintermediariesareaskedtocontributetofinancingsustainabledevelopment thatmeets theneedof thepresent,withoutcompromisingtheabilityoffuturegenerationstomeettheirownneeds.

Sustainable investment, including sociallyresponsible, ethical, and ESG (environmental,social and governance) investing, is increasinglygainingafootholdinmainstreamfinancialmarkets.Globally,sustainableinvestmentsgrewbyaquarterto$23trillionoverthelasttwoyears,accordingtotheGlobalSustainableInvestmentAlliance(GSIA2017). This equates to around one-quarter of‘professionallymanaged’assetsglobally.1

ESGinvestinghasbeengatheringattentionsincethe1990s.Fromitsoriginsintheequitymarketswithreligious,values-basedorthematic(environmental)investors,themovementspreadwiththelaunchoftheUNPrinciplesofResponsibleInvestment(UNPRI) in2006andwascatalyzed forfixed incomewiththeissuanceoflabelledbondsbymultilateralorganizations from 2007. The issue has receivedrenewedhigh-profilesupportinrecentyearsthroughthe European Commission’s High-Level ExpertGroup on Sustainable Finance and the FinancialStability Board’s (FSB) Task Force on Climate-relatedFinancialDisclosure (TCFD) initiative, aswell as public interventions by stakeholders such

as the Bank of England Governor MarkCarney.2

Traditionally, the main focus of ESG investinghas been on equity markets. In recent years,however,ESGhasspreadoutincreasinglytootherasset classes, in particular fixed income, giventhat bonds constitute a substantial percentageof institutional investors’ assets.3 Considerableacademicandindustryresearchhasbeenconductedon the relationship between ESG investing andperformance in equity markets, but far less isavailableonitseffectonthefixedincomemarkets.

As a further development, many asset ownersare looking to increase investments that make apositivesocialandenvironmentalimpactontopoftheir financial objectives. Some have also startedtore-assesstheirinvestmentpoliciesinthelightofclimatechangerisksandpoliciespostParisCOP21,as well as the 2015 UN Sustainable InvestmentGoals (SDG).All assets, including fixed income,will increasingly bemeasured also by social andenvironmentaloutcomesandexternalities.

2 | 1. INTRODUCTION AND BACKGROUND

This research report provides an overview onsustainableinvestinginfixedincomethatisdevelopingfastthesedays.Itdiscussesthecoreareasof:

• thespecificnatureandissuesofESGinvestinginthisassetclass;

• therationaleforESGanalysisinfixedincome–includingresearchfindings;

• ESGinvestmenttoolsandwaysofimplementingESGstrategiesinfixedincome;

• on-goingchallengestogreaterintegrationofESGintomainstreaminvesting;and

• suggestions for how to catalyze the furtheradoptionofESGapproaches.

The study builds on both research and practicalexperiences to date onESG approaches for fixedincome portfolios.An extensive literature reviewwas conducted to inform the findings. Itwas notpossibletoundertakenewprimaryresearchforthispaper,butsuggestionsforfurtheranalysisaremade.Thepaperalsoincludesfindingswhichdrawonthepractical experience of a number of stakeholders(assetowners,assetmanagers,dataprovidersetc.)whoareintegratingESGfactorsintofixedincomeinvestmentsandwereinterviewedandparticipatedin aworkshop and roundtablediscussions as partofthisresearchproject.Theirinsightsarereflectedacrossthepaper,andtheirinputismostappreciated.4

Thefocusofthereportisprimarilyonthemainfixedincomeinvestmentinstruments,suchassovereign,supranational, and corporate bonds. Researchand application of ESG for other fixed incomeinvestments (sub-sovereigns, covered bonds andotherassetbackedsecurities,privatedebtetc.)arestill very limited.However, thematic investmentssuch as green, social and sustainable bonds aregrowingandarefacilitatingtheintegrationofESGforfixed income.Therefore, thediscussion isnotlimitedonlytothelabelledbondmarket,butisalsoon incorporating ESG factors into fixed incomeportfoliosmorebroadly.

Definition of ESG InvestingESGinvestingincorporatesenvironmental,social,andgovernance issues into the analysis, selectionand management of investments. Key issues forconsiderationtypicallyinclude:

E: climate change, carbon emissions, pollution,resourceefficiency,biodiversity;S: human rights, labor standards, health &safety, diversity policies, community relations,developmentofhumancapital(health&education);G: corporate governance, corruption, rule of law,institutionalstrength,transparency.

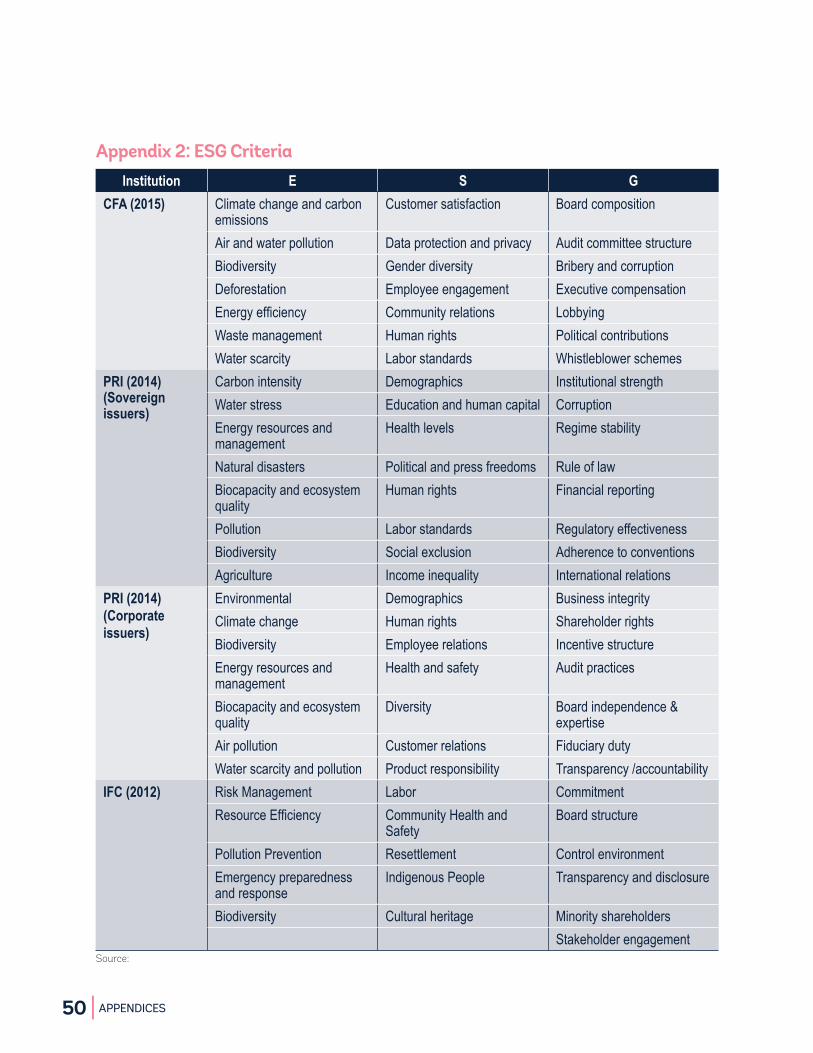

Historically, governance-related investmentcodeswere probably first relevant for investmentstrategies,withgreenandsocial issues,andmoregenerallyaviewtosustainableinvesting,growingin relevanceover the last twodecades.There aremanydifferent,andmorespecific,definitionsinthemarketplace.Appendix2showsalistofstandardESG criteria applied by the CFA (2015), and forsovereignandcorporatebondsbytheUNPrinciplesofResponsible Investing (PRI) (2014), and thoseusedintheIFCPerformanceStandards(2012)andCorporateGovernanceMethodology.

AdefinitivelistofESGissuesdoesnotexist–anditlooksimpossibletoagreeon.Markets,technologies,policies, values and social preferences change allthetime,andvaryfromregiontoregion,countrytocountryandevenwithincountries. Therefore,anopenanddynamicapproachtodefining“green”or“sustainable”investmentsispreferable–andisusedinthispaper–embeddedinaclearandtransparentgovernance framework (Inderst, Kaminker andStewart2012).5

Forfixedincome,asurveybyPRI(2017a)foundslightly more investors follow governance thansocial and environmental factors. Russell (2017)also found that governance is widely beingconsideredthemostimportantfactor.

Other common terms in this context includesustainable investing (SI), responsible investing

INCORPORATING ENVIRONMENTAL, SOCIAL AND GOVERNANCE (ESG) FACTORS INTO FIXED INCOME INVESTMENT | 3

(RI) and socially responsible investing (SRI).Theyareoftenbeingusedsynonymously in themarketplace. So does this report, for simplicity, beingaware that some industry practice and academiadifferentiatetheseterms.

There are other related investment strategies witha somewhat different focus (such as long-term investing, universal ownership6), or strategies thatconcentrateonaparticularaspectofESG(e.g.green, climate change, social, ethical, religious investing).7

Finally,thereisanincreasingfocusonnon-financialoutcomesandexternalitiesofinvestments.Impact investingaimstogenerateameasurable,beneficialsocialorenvironmentalresultalongsideafinancialreturn.8 Blended finance is the strategic use ofdevelopment finance and philanthropic funds tomobilize private capital flows to emerging andfrontier markets (e.g. OECD 2018). The newlydevelopingSDG investing takesconsiderationsofissues beyond traditional ESG, using the UnitedNations’ Sustainable Development Goals (SDGs)asaframework.

Investor MotivationsEach investor has specific investment objectivesandstrategy,itsownlegalmandate,andparticularexpectations placed on it by its beneficiaries andthe society within which it operates. Therefore,responsibleinvestmenthasnosingularmotivation,andthereisnosinglestrategyorsetofapproachesthatisfolloweduniversally(Dimsonetal.2013).9

Therearemanyinvestorquestionnairesundertakenon ESG, and they varywidely inmany respects,which may reflect different universes, conceptsandlanguages,amongotherreasons.Mostsurveysconfirm that ESG is most prevalent in listedequities.According toCFA (2017), 45% of fixedincomeinvestorsintegrateESGanalysiscomparedto76%forlistedequities(andmuchfewerforotherasset classes). However, many investors plan toenhanceESGinthefutureinfixedincome,privateassets and alternative asset classes. There areseveraldriversforthisdevelopment:preferencesof

members,clientsandotherstakeholders;increasingawarenessofclimatechangerisksandpoliciesbyinvestorboards;socialandpoliticalconcerns;legalandregulatorychanges;voluntarycodes;fiduciaryduty; technology change and disruption; andreputationalrisks;publicandpeerpressure.

Financial and non-financial objectives

InstitutionalinvestorsmustbeabletoreconciletheiractionsintermsofESGissueswiththeirobligationstomembers,beneficiaries,policyholdersandclients,andlooktousetheirinvestmentsforapositivesocialpurpose.Formostinvestors,themainobjectivesarefinancialresults(e.g.risk-adjustedreturns,liability-matchingcashflows).Someinvestorsalsohavenon-financialobjectives(e.g.ethical,religious,political,cultural values and preferences) beside financialobjectives. ‘Reputational/ brand’ motivations canalso play a part. The potential trade-off betweenfinancial return and ESG is still being debated byinvestors.This is not so clear, even in theory, andthereforethedebateismostlydrivenby‘beliefs’.Ontheonehand,consideringESGasriskfactorsshouldcontributetomorestablereturnsovertime.However,bynarrowingthepotentialuniverseofinvestments,ESG could lower returns. Further theoretical andempiricalwork on this issue – particularly for thefixedincomeuniverse–isrequired.

Short-termism and long-term investing

The priority, or even exclusiveness, of financialobjectives does not preclude the consideration of non-financial factors in the analysis andmanagementof investments.Thismay lead to animprovedunderstandingoflong-termtrends.Assetowners are trying to move towards longer-terminvestmentframeworksthaninthepast.

ESG as risk factors vs ESG as an investment opportunity

Investor motivations are often driven by risk management, i.e. the relevance of environmental,social or governance risks. The risk aspect isnaturallyamainconcernofinsurancecompaniesand

4 | 1. INTRODUCTION AND BACKGROUND

otherlow-riskinvestors.However,someinvestorsalso look at ESG as an investment opportunity,seeking “alpha”.For example,ESGanalysismayimprove the understanding of longer-term trends.Someinvestorsevenfindnewinvestmenttargetsinthegreenandsocialspace.

Inpractice,ESGinvestorscanbroadlybeclassifiedintothreegroups:

• Fora largegroupof investors, thesolepurposeremainsfinancialperformance,butwithabeliefthat ESG factors have a material effect oninvestmentrisksandreturns.

Box 1: ESG Investor Associations, Standards and Codes

Asset owners and investment managers haveformedor joinedarangevoluntaryassociationsand networks in the field of ESG, corporategovernance, climate change, and related issues.There are also other voluntary codes manyinvestorscomplywith.Manyofthemareatthenationallevel(e.g.bypensionfundorganizations).Herearesomeimportantinternationalexamples:

Responsible and sustainable investment• UNGlobalCompact(UNGC)• UNPrinciplesforResponsibleInvestment(PRI)• EuroSIF, UKSIF, USSIF, SIF Japan, ASrIA,RIACanada,RIAAustralasia,etc.

• GlobalSustainableInvestmentAlliance(GSIA)• EquatorPrinciples• International Capital Market Association(ICMA) Green Bond Principles (GBP) andSocialBondPrinciples(SBP)

Corporate governance, accounting and disclosure• International Corporate Governance Network(ICGN)

• Global Reporting Initiative (GRI); GlobalSustainabilityStandardsBoard(GSSB)

• Sustainability Accounting Standards Board(SASB)

• The FSB Task Force on Climate-relatedFinancialDisclosures(TCFD)

Green and climate change investment Associations• Institutional Investors Group on ClimateChange(IIGCC)

• InvestorGrouponClimateChange(IGCC)• Asia Investor Group on Climate Change(AIGCC)

• GICglobalplatform• Ceres

Initiatives• CarbonDisclosureProject(CDP)• AssetOwnersDisclosureProject(AODP)• MontrealCarbonPledge• PortfolioDecarbonizationCoalition• Action100+

Impact investing• GlobalImpactInvestingNetwork(GIIN)

Industry guidesPracticalinvestorguidanceonESGinvestingcanbefoundinmanypublicationsbytheindustryandorganizationssuchastheCFA,PRI,SSF(2017),BNPParibas (2016).Morespecificallyonfixedincome,see,e.g.,PRI(2014),Klein(2015).Forguidanceonclimatechangeinvesting,includingtheimplicationsforfixedincome,see,e.g.,IIGCC(2015),Mercer(2015),ForumEthibel(2017).

• Increasingly investors seek to combine certainnon-financial objectives (e.g. ethical, religious,political,cultural,societalvaluesandpreferences)withouthamperingfinancialobjectives.

• Certaininvestorsarewillingandabletosacrificesomeorallfinancialreturntoachieveothersocialor environmental benefits (impact/communityinvesting;charityinvesting).

There is plenty of general ESG guidance alreadyavailable for all types of investors, offered byvariousorganizations(Box1).

INCORPORATING ENVIRONMENT, SOCIAL AND GOVERNANCE (ESG) FACTORS INTO FIXED INCOME INVESTMENT | 5

Box 2: ESG and RegulationIt is important to distinguish between ESG-specific regulation (e.g. for companies), investorregulation,andotherrulesandlawsthatmayaffectESG investing positively or negatively. Investorregulation may include funding and accountingregulation,orevenoutrightinvestmentconstraintson certain asset classes and instruments.Regulation also applies at different levels:company, investmentmanager/fund, asset owner(e.g. PRI 2016a, Northern Trust 2015). OECD(2017)summarizesthemaindevelopments:• Regulatory frameworks for investmentgovernance rarely make explicit referenceto ESG issues, although this is changing in anumber of jurisdictions such as France, theNetherlands,Chile.

• Several countries have some form of ESGreportinganddisclosurerequirementsforinvestors(e.g.Australia,France,Germany,Sweden,UK).

• Regulatoryframeworksforthemostpartdonotprevent ESG integration, and other legislationorvoluntarycodesmayencourageinstitutionalinvestorstotakeESGfactorsintoaccount(e.g.USA,UK,SouthAfrica,Ontario).

• However, institutional investors may lackclarityastohowESGintegrationfitswiththeircountry’slegal,regulatoryandotherobligations.ManyassetownersconsideredfiduciarydutyasanobstacletoESGintegrationbutthereseemsto be a shift from a “narrow” to “broader”interpretations(OECD2017).

• TheEUHigh-LevelExpertGrouponSustainableFinance published several investor-relatedproposals (EU 2018). In 2018, The EuropeanCommissions announced plans for establishingan EU taxonomy/classification system forsustainableactivities,creatingEUlabelsforgreenfinancial products, clarifying fiduciary dutiesof asset managers and institutional investors,enhancecorporatereporting,amongothers.

• In2015,Article173ofFrance’slawon‘EnergyTransition for Green Growth’ introducedmandatoryclimatechangereportingforfinancialinstitutions. This has been hailed as groundbreakingwithpotentiallyfarreachingimplications.

• Furthermore,manycountrieshavestewardshipcodes, corporate disclosure codes or stockexchangerulesthatcovergovernanceandotherESG issues. The Stewardship Code issued byJapan’s Financial Services Authority (JFSA),releasedin2014(revised2017)issaidtohavebeen particularly influential, and indeed wasone of the drivers for theGPIF to adoptESGprincipleswithin their investmentapproach. Inaddition, there are variousprinciples andbest-practice guides available for governments andinvestorsbyinternationalorganizationssuchastheUNandtheOECD.

Attheendof2017,centralbanksandregulatorsinitiatedanewNetworkonGreeningtheFinancialSystem, aimed at sharing supervisory practicesonclimatechangeandotherenvironmentalrisks.

ESG and regulation

RegulationcanbebothadriverandabarrierforESGinvesting. For example, a relatively prescriptiveapproach is being proposed in Europe, whilstinterpretationsofregulationinAsiahavebeenmorevoluntarybutsupportive.InNorthAmerica,alackofinterpretationaroundexistinglawsisstillfelttobeabarriertofurtherESGintegrationbysomeinvestors.SomemaintrendsaresummarizedinBox2.

The debate over whether ESG investing iscompatiblewithinvestorsfiduciaryduty10hasalso

been developing over time. From initial rulingsrequiring fiduciaries to only consider financialreturnswhenactingintheinterestofbeneficiaries,interpretation developed so that considerationof other factors was not seen a fiduciary breach.Guidance is now going a step further and insome cases requiring fiduciaries to incorporateESG factors into their investment decisions.For example, the United Nations EnvironmentProgramme (UNEP publication (UNEP 2015)concluded that: “failing to consider all long-terminvestmentvaluedrivers,includingESGissues,isafailureoffiduciaryduty”.

6 | 1. INTRODUCTION AND BACKGROUND

ESG and Impact Investment ApproachesInvestorsusearangeofmethodsforbringingESGconsiderations into their decision-making. Theyweretraditionallyappliedtoequityinvestments,butarealsobeingusedforfixedincomeandotherassetclasses.Thesemethodsarenotmutuallyexclusiveandareoftenusedincombination.Furthermore,thevariousESGapproachescanbeimplementedwithactiveorpassiveinvestmentstyles.ESGintegration,engagement and screening capture about 99% ofassets,withthemedandimpactinvestmentsmakinguptheremaining1%.11

Negative/exclusionary screening:

This involves excluding securities of specificactivitiesorindustries(e.g.controversialweapons,tobacco,fossilfuels)deemedunacceptable.Reasonsmaybeethical,legalorothernormsandstandards(e.g.humanrights,laborconditions,corruption).

Positive screening/best-in-class selection:

This is a positive selection or overweighting ofcompanies or countries with better or improvingESGperformancerelativetosectorpeers.ItcanbeimplementedoneitherthelevelofESGmeasuresortheirpotentialforchange(ESGmomentum).

Animmediateconcernwithexclusionsorbest-in-class is the potential reduction of the investmentuniverse.Also, screeningmay lead to unintended

sector and factor biases in the portfolios. Suchissuesneedtobewellmanaged.

Active ownership/voting/engagement/stewardship:

This refers to the practice of entering into adialogue with companies or countries on ESGissues and exercising both ownership rights(including.voting)and“voice”(especiallyrelevantincaseswhereinvestorsdonothavevotingrights,such as bondholders) to effect change.This is analternativeto“exit”,i.e.sellingofftheinvestmentswithquestionablepractices,ordivestingbasedonspecific issues (e.g. removing exposure to fossilfuelsas‘strandedassets’).SomeinvestorsalsoliketolobbyforESGthemesmorewidelyinpolitics.

ESG integration:

This is thesystematic inclusionofESGrisksandopportunities in investment analysis, portfolioconstruction and risk management. It is beingimplemented in different ways across investmentorganizations.12

Thematic investing:

AnumberofinvestmentthemesarebasedonESGissues, including clean technology, renewableenergy,energyefficiency, sustainable forestryandagriculture,water,education,healthanddiversity.Climate investing more broadly is receivingincreasingattention(seeBox3).

Box 3: Climate Investing

SinceParisCOP21,moreinvestorshavedevelopedpracticalclimatechangepolicies.Theyareoftensimple green thematic investing or included intraditionalESGpolicies.Forsomeinvestors,theygowellbeyond.Theyinclude,amongothers:• climatechangescenarioanalysisinassetallocation;• measurementofcarbonemission/carbonfootprint;

• gradualdecarburizationtargetsforportfolios;• exclusions/underweightofparticularindustries/companies(e.g.coal,fossilfuels);

• energyefficiencytargets(e.g.inrealestate);• greeninfrastructureinvestments(e.g.cleanenergy,climatechangeadaptation);

• greenandclimatebonds;• divesting,andtheconceptof“strandedassets”.13

INCORPORATING ENVIRONMENTAL, SOCIAL AND GOVERNANCE (ESG) FACTORS INTO FIXED INCOME INVESTMENT | 7| 7

Impact investing:

Ingeneralterms,thisisinvestingwiththeintentiontogenerateandmeasuresocialandenvironmentalbenefits alongside a financial return.14 Impactinvestorstypicallysetoutcomegoalsortargetsexante, make and monitor the investment and thenmeasureexpostresults.Theytrytostrikeabalancebetween an economic and social return – with avaryingemphasis,dependingonthespecificimpactproject/fund.

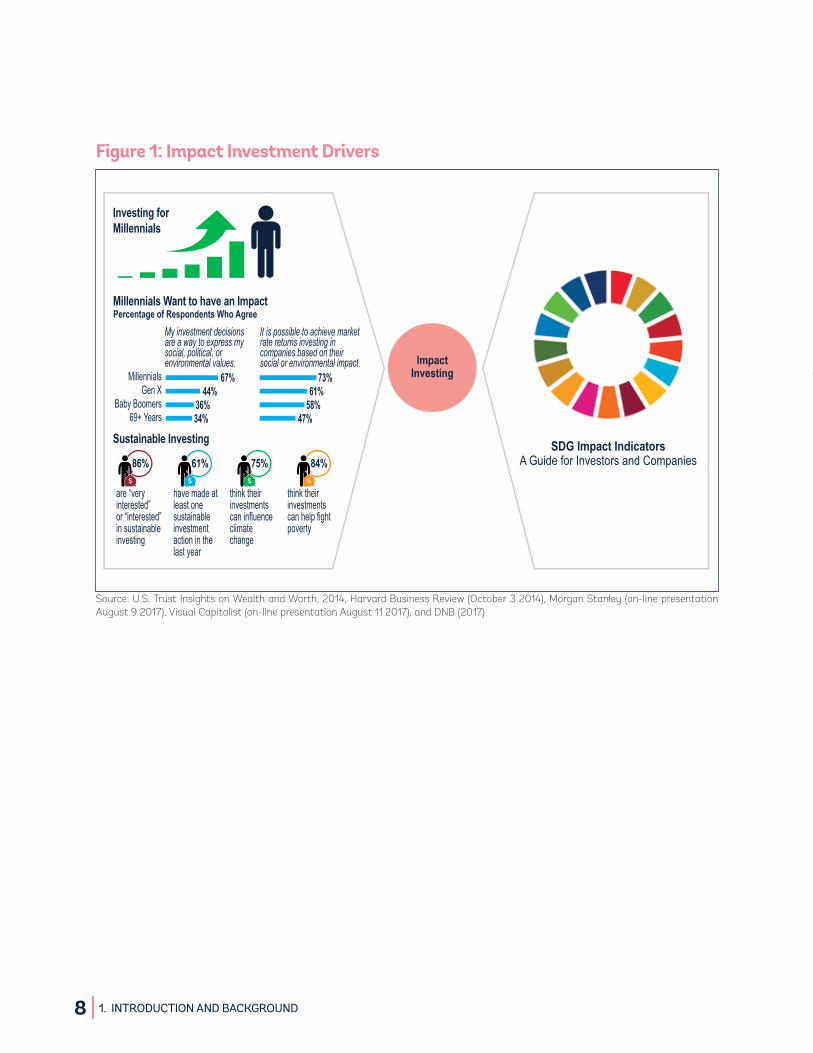

Therearedifferentapproachestoimpactinvesting.Theearlydevelopmentsweremore in thewayof“community investing”, i.e. investments by smallfundstohelpfundsmallersocialorenvironmentalprojects in municipalities/regions. As a newdevelopment, impact investing has spread also tonon-specialist investors. Mainstream investorsnow feel urged to measure the ‘impact’ of theirportfolios,butaregenerallynotmandated togiveupfinancialreturn.

There are various motivations behind this move,but two in particular standout (Figure 1). First isthe increasing influence of millennial investors.According to a survey conducted in the UnitedStatesbyMorganStanley (TheEconomist2017),75% of millennials agreed that their investmentscouldinfluenceclimatechange,comparedwith58%of the overall population.They are also twice aslikelyasinvestorsingeneraltoinvestincompaniesthat espouse social or environmental objectives.As ‘TheEconomist’ article quotes: “boomers see doing good as separate from investing; whereas millennials don’t see how you could possibly separate the two.”

Impactinvestingcoversallassetclasses,includingbonds (e.g. social impact bonds), private equityand private debt (GIIN 2017). Returns can showlowcorrelationswithmainstreamasset classes asincomeistypicallynotrelatedtofinancialmarkets(SSF2017).

Measuring “impact” is not an easy task. ManyinvestorsarestillnotclearwhatappropriatemetricsshouldbeforthemeasuringimpactonE,SandGindividually, and collectively or indeed whetherthereshouldbea‘onesizefitsall’approach.Themost advancedmetrics in this respect appears tobe carbon emissions/footprint. GIIN developedimpactreportingandinvestmentstandards(IRIS),i.e.acatalogueofperformancemetricsforvarioussectors.New research is being undertaken in thisfield.15

SDG investing

Thesecondmajordriver for impact investinghasbeen the publishing of the SDGs. In 2015, theUnited Nations approved the 17 SDGs and 169individual targets. The SDGs were not primarilymade for investors but achievement of theGoalsrecognizes the necessary contribution of all,includingtheprivatesectorandinvestors.Itislessclear what these contributions look like for sucha broad range of targets. Sometimes it is easierto address anSDG through investmentdecisions;sometimes it is easier to incorporate the SDG inactiveownership(PRI2017b).

SDG-relatedinvestment isstill in its infancy.Theanalysis currently focuses on mapping investorscorporate holdings to a selection of the SDG.Several investors such as the Dutch APG andPGGM, or the SwedishAP2 are trying to workoutinvestmentpossibilitiesassociatedwithSDGs.One of the commonly stated obstacles is thechallengesurroundingimpactmeasurement.Someorganizations are working on investor-relevantSDG impact indicators and metrics (e.g. DNB2017, Trucost 2017). The Investment IntegrationProject(TIIP)isafurtherinitiativelookingtohelpinvestorsmapthelinkbetweentheinvestmentsintheirportfolioandtheSDGs(TIPP2018).16

8 | 1. INTRODUCTION AND BACKGROUND

Figure 1: Impact Investment Drivers

ImpactInvesting

SDG Impact IndicatorsA Guide for Investors and Companies75% 84%61%86%

are “very interested”or “interested” in sustainable investing

think theirinvestmentscan influenceclimatechange

think theirinvestmentscan help fightpoverty

have made atleast onesustainableinvestmentaction in thelast year

Millennials Want to have an Impact

Sustainable Investing

Investing forMillennials

44%

34%36%

67%Gen X

69+ YearsBaby Boomers

Millennials61%

47%58%

73%

My investment decisions are a way to express my social, political, or environmental values.

It is possible to achieve marketrate returns investing in companies based on their social or environmental impact.

Percentage of Respondents Who Agree

Source: U.S. Trust Insights on Wealth and Worth, 2014, Harvard Business Review (October 3 2014), Morgan Stanley (on-line presentation August 9 2017), Visual Capitalist (on-line presentation August 11 2017), and DNB (2017)

INCORPORATING ENVIRONMENTAL, SOCIAL AND GOVERNANCE (ESG) FACTORS INTO FIXED INCOME INVESTMENT | 9

2. whAT iS ESgANALySiS iN

fixEd iNComE iNvESTiNg?

Since most ESG research has beenundertakenonequities,itislesscleartowhatextent, howandwhenESGconsiderations canbe

applied to fixed income investments.Applying ESG to otherassetclassesrequires adaptation(e.g.Johnson2017).Fixed incomemanagementconsistsof severalbuildingblocks, including theanalysisofinterestrates,inflation,creditqualityandliquidityrisks.Fixedincomeinvestmentisverymuchaquantitativeprocess.ManagersfinditdifficulttoincludeESGcriteriaintheirfinancialmodels,andmaythereforebemore‘resistant’toESG-relatedchange.17

There are a number of key differences betweenequities and fixed income, especially the focus ondownside capital risk and cash flow stability vs.upside,capitalappreciation:

• Creditworthinessandtheabilitytopaybackdebtarekey-therefore,thereisafocusoncreditanddefaultrisk

• Asymmetricaldownside riskvs.upsidepotentialoffixedincomeinvestments;

• Duration(fixedincomeinvestmentshaveafiniteperiodvs.equityholdingswhichcanbeperpetual);

• Position in capital structure, and with differentlayers(e.g.senior,subordinateddebt,hybrid);

• Trading of fixed income products largely OTC/off-market;

• The difference between bondholder rights andshareholderrights;

• The importance of sovereign, sub-sovereign,supranationalandagencyissuers;

• Different analytical approaches (e.g. duration,yieldcurve,spreadmanagement);

• The specifics of asset-backed securities, projectbondsandotherinstruments;

• The high share of institutional participation incorporatebondissuance;

• Theuseofbondsinlong-termliabilitymanagementbyinsurancecompaniesandpensionfunds;

• Issues around market capitalization-weightedindices(withheavyweightstodebt-riddenissuers);

• Therisingimportanceofprivatedebt in investorportfolios.

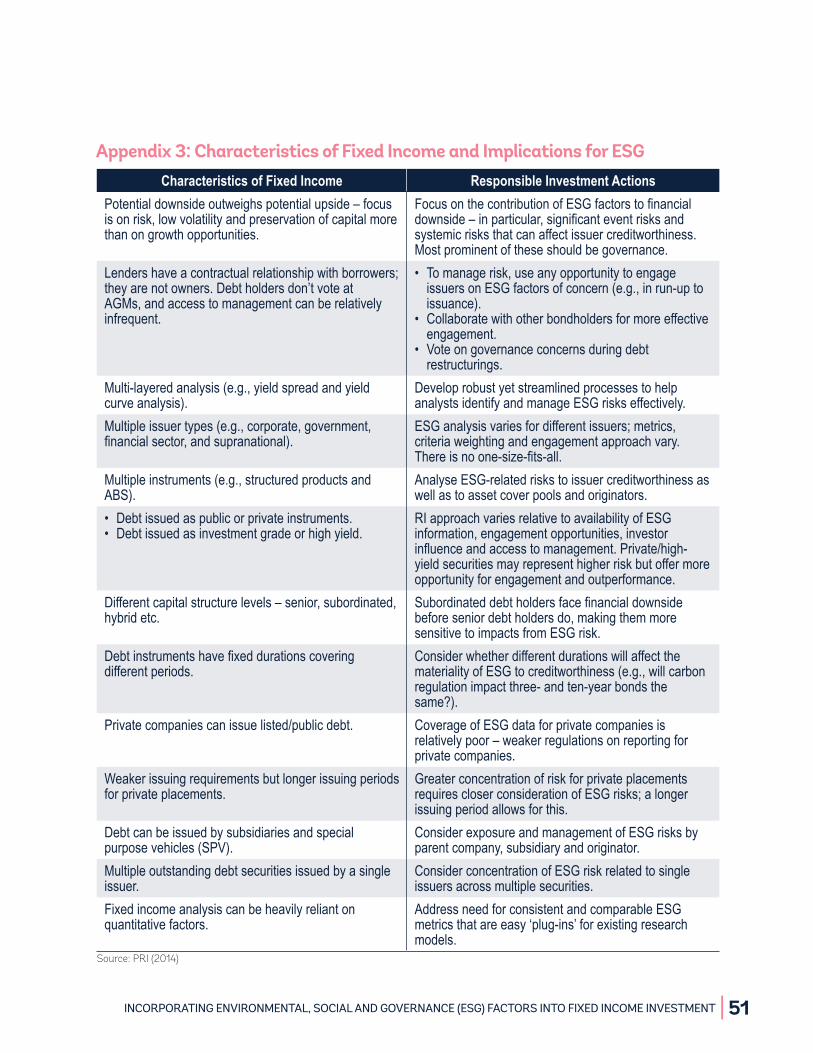

There are implications of these differences forESGinvestinginfixedincomecomparedtoequityanalysis (seeAppendix 3 for an overview by thePRI2014):

10 | 2. WHAT IS ESG ANALYSIS IN FIXED INCOME INVESTING?

• Engagementpolicieswilllookdifferentforequityandbondholders;

• Sovereign (along with sub-sovereign andsupranational)issuersarefundamentallydifferentfromcorporateissuers;

• Eventriskscandominateissuers’creditworthinessanddowngrades;

• In fixed income, liquidity can suddenly dry upevenforlargeissues;

• Riskanalysisneedstoapplytovariouscorporatelevels (holding company, subsidiaries, specialpurposevehicles(SPVs),originators);

• Bonds can be complex contracts (e.g. attachedcovenants,embeddedoptions),alsoinrelationtoESGrisks;

• Concentrationriskrisesforissuerswithmultiplesecurities;

• Debt-related benchmarks may be even moreproblematic from an ESG perspective (e.g. therelationship between a highdebt load andpoorgovernance/institutions);

• Fixedincomeindicesaremoredifficulttocompile(asfixedincomeindicesincludemultiplebondsperissuer,multipleissuerspercorporatefamily,privatecompanieswheredata ishard togather,and non-corporate entities, covered bonds andotherasset-backedsecuritiesetc.).

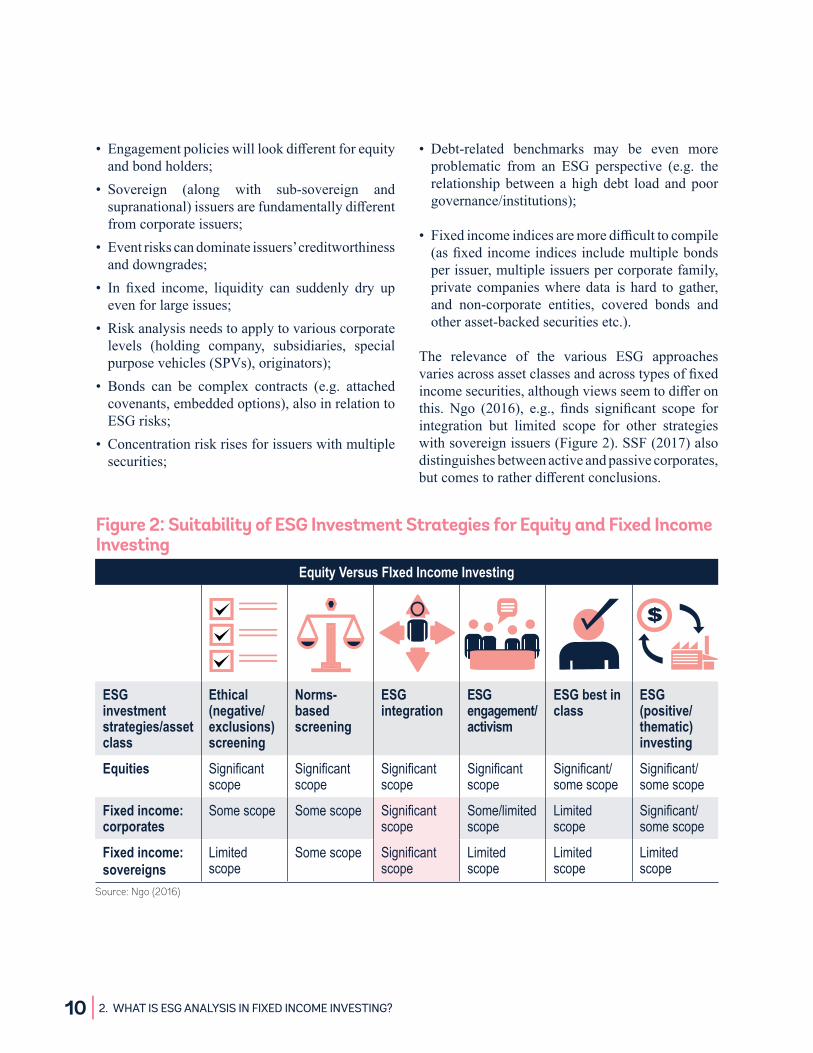

The relevance of the various ESG approachesvariesacrossassetclassesandacrosstypesoffixedincomesecurities,althoughviewsseemtodifferonthis. Ngo (2016), e.g., finds significant scope forintegration but limited scope for other strategieswithsovereignissuers(Figure2).SSF(2017)alsodistinguishesbetweenactiveandpassivecorporates,butcomestoratherdifferentconclusions.

Figure 2: Suitability of ESG Investment Strategies for Equity and Fixed Income Investing

Source: Ngo (2016)

Equity Versus FIxed Income Investing

ESG investment strategies/asset class

Ethical (negative/exclusions) screening

Norms-based screening

ESG integration

ESG engagement/activism

ESG best in class

ESG (positive/thematic) investing

Equities Significant scope

Significant scope

Significant scope

Significant scope

Significant/some scope

Significant/some scope

Fixed income: corporates

Some scope Some scope Significant scope

Some/limited scope

Limited scope

Significant/some scope

Fixed income: sovereigns

Limited scope

Some scope Significant scope

Limited scope

Limited scope

Limited scope

INCORPORATING ENVIRONMENTAL, SOCIAL AND GOVERNANCE (ESG) FACTORS INTO FIXED INCOME INVESTMENT | 11

Wenow lookat thevarious typesof securities inmoredetail.

Corporate IssuersCorporate governance factors (e.g., a company’saccountability, risk management and directorindependence)havestronglinkstocreditstrength.Goodcorporategovernanceshouldleadtoahighercredit rating and lower cost of debt, and viceversa.Well-managed companies tend to be morealigned with bondholder interests, and corporatetransparencykeepsbondholdersbetterinformedofexposureandmanagementofrisk.

Poor environmental or social management mayleadtolowercreditratingsandhighercostofdebt.ThematerialityofEandSfactorsvaryconsiderablyacross sectors and industries. For example,environmentalissuesareoftenrelevantinenergy,utilities, resources and other heavy industries.Water stress is likely to be material for certainsectors, such as extractives, food and beverage,andagriculturalcompanies.Forairlinecompanies,fuel efficiency may be a key environmental andfinancialmetric.

ESG investing for corporate bonds is closelyrelated to established ESG process for listedequities. For example, exclusion lists and ESGscreenstendtobeverysimilar.However,therearesomesignificantdifferences.

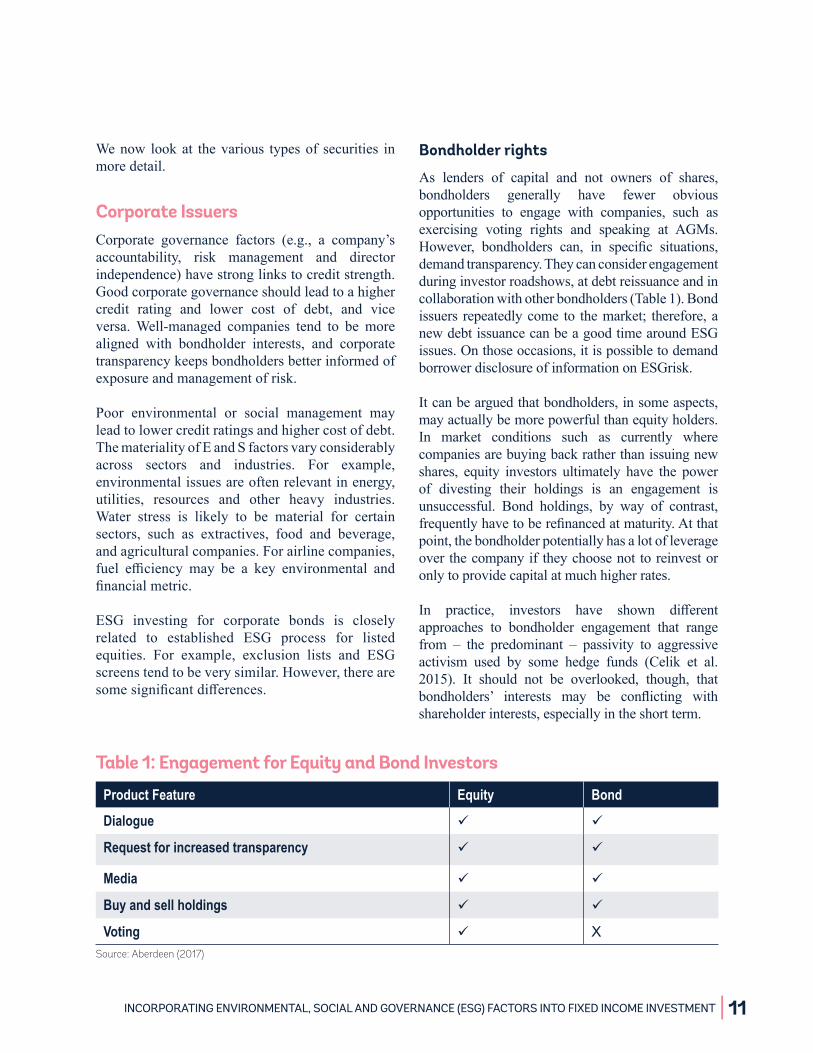

Bondholder rights

As lenders of capital and not owners of shares,bondholders generally have fewer obviousopportunities to engage with companies, such asexercising voting rights and speaking at AGMs.However, bondholders can, in specific situations,demandtransparency.Theycanconsiderengagementduringinvestorroadshows,atdebtreissuanceandincollaborationwithotherbondholders(Table1).Bondissuers repeatedlycome to themarket; therefore,anewdebtissuancecanbeagoodtimearoundESGissues.Onthoseoccasions,itispossibletodemandborrowerdisclosureofinformationonESGrisk.

Itcanbearguedthatbondholders,insomeaspects,mayactuallybemorepowerfulthanequityholders.In market conditions such as currently wherecompaniesarebuyingbackratherthanissuingnewshares, equity investors ultimately have the powerof divesting their holdings is an engagement isunsuccessful. Bond holdings, by way of contrast,frequentlyhavetoberefinancedatmaturity.Atthatpoint,thebondholderpotentiallyhasalotofleverageoverthecompanyif theychoosenottoreinvestoronlytoprovidecapitalatmuchhigherrates.

In practice, investors have shown differentapproaches to bondholder engagement that rangefrom – the predominant – passivity to aggressiveactivism used by some hedge funds (Celik et al.2015). It should not be overlooked, though, thatbondholders’ interests may be conflicting withshareholderinterests,especiallyintheshortterm.

Table 1: Engagement for Equity and Bond Investors

Source: Aberdeen (2017)

Product Feature Equity Bond

Dialogue ü ü

Request for increased transparency ü ü

Media ü ü

Buy and sell holdings ü ü

Voting ü X

12 | 2. WHAT IS ESG ANALYSIS IN FIXED INCOME INVESTING?

Duration management

Different ESG factors will present greater risksover different time periods. In the short term,investors face a greater threat from the fallout oflow-frequency,high-impacteventssuchasextremeweatheror industrialdisasters.Longer term,ESGtrends such as demographic changes and climatechange,are likely tohavea significant impactonbondyields,buttheextentofthisismoreuncertain.

Liquidity

Liquiditytendstodryupwhenneededmost,i.e.attimesofcrisis,leadingtoexpensiverestructuringsof portfolios. Liability-driven investment (LDI)strategieshavetypicallylong-timehorizons.Abuy-and-holdstrategyforinvestinginrelativelyilliquidbonds requires consideration of all pertinent riskfactors-ESGandothers-overtherelevantperiod.

Low liquidity of bonds can also be a potentialthreat against apoorcompany.The saleofbondsby one investor can lead to price volatility, andsubsequently, tohighercostsofcapital forsuchacompany.

High yield bonds

Specific segments are potentially more exposedto ESG risks. For example, high-yield issuerstend to be smaller; many are private companiesand, therefore, do not have to report the sameinformationoroperatetothesamestandards.Theyaremorelikelytohaveunconventionalgovernancestructures that may be misaligned with creditorinterests. The amount of leverage used by highyield issuersmakes bondholders a critical sourceofcapitalalongsideequityownersandcanprovidemeaningful opportunities for engagement withcompanymanagementteams(Aristotle2016).

Private placements

They tend to have low transparency, largeticket sizes, long maturities, and are difficult todivest. However, large creditors may be able tonegotiatemore favorable covenants and reportingrequirementstoaddressESGconcerns.

Sovereign IssuersAnalysisofcompanyandsovereigncreditworthinessis markedly different in all aspects of ESG. Thepolitical and institutional system,macroeconomicdevelopment,andgovernmentpoliciesplayakeyroleinassessingacountry’sabilityandwillingnessto repay itsdebton time.Therelationshipof riskandreturninsovereigninstrumentsiscomplex,andnotlinear(Schroders2017a).

IntermsofG,amongthecrucialfactorsaretheruleof law, the strength of the country’s institutions,political stability, regulatory consistency andcorruption. Energy/water/other resource reservesand management, as well as green/climatechange policies are of varying importance forcreditworthinessacrosscountriesandperiods.

Social factors tend to be given greaterweight byanalysts than environmental factors because oflinksbetweenpoliticalstability,governanceandacountry’sabilitytoraisetaxesormakereforms.Keysocialfactorsincludehumanrights,laborstandards,educationsystem,healthcare,anddemographics.

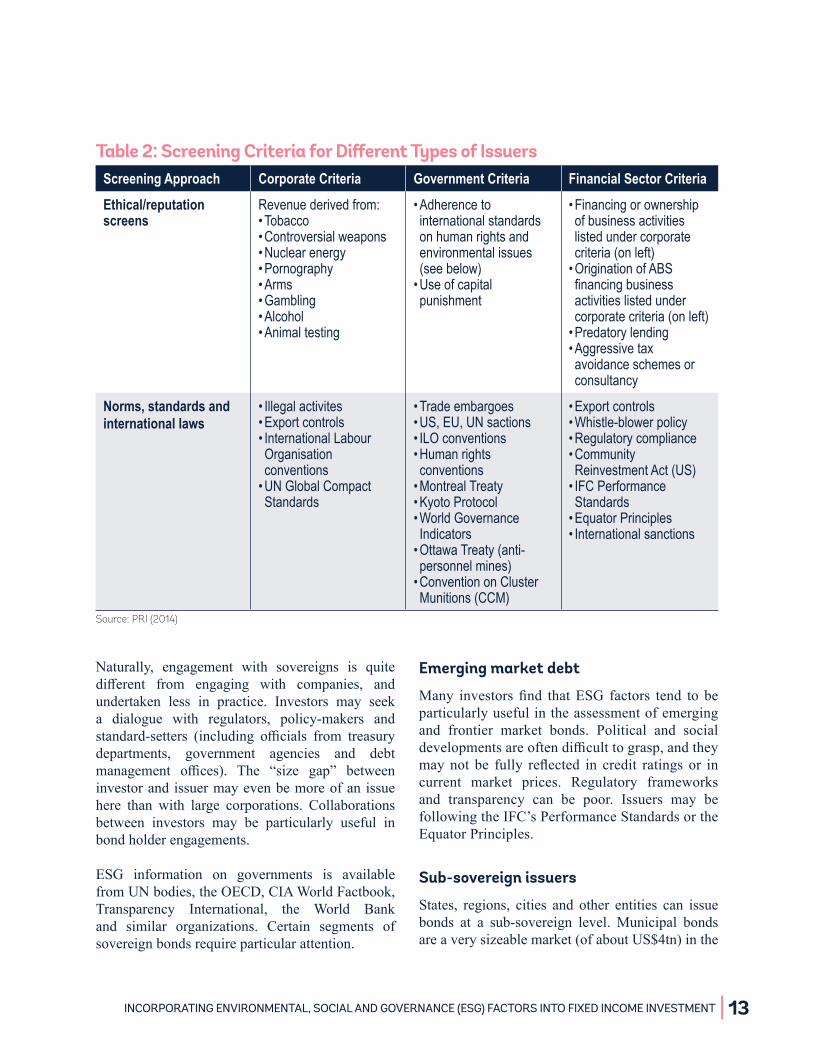

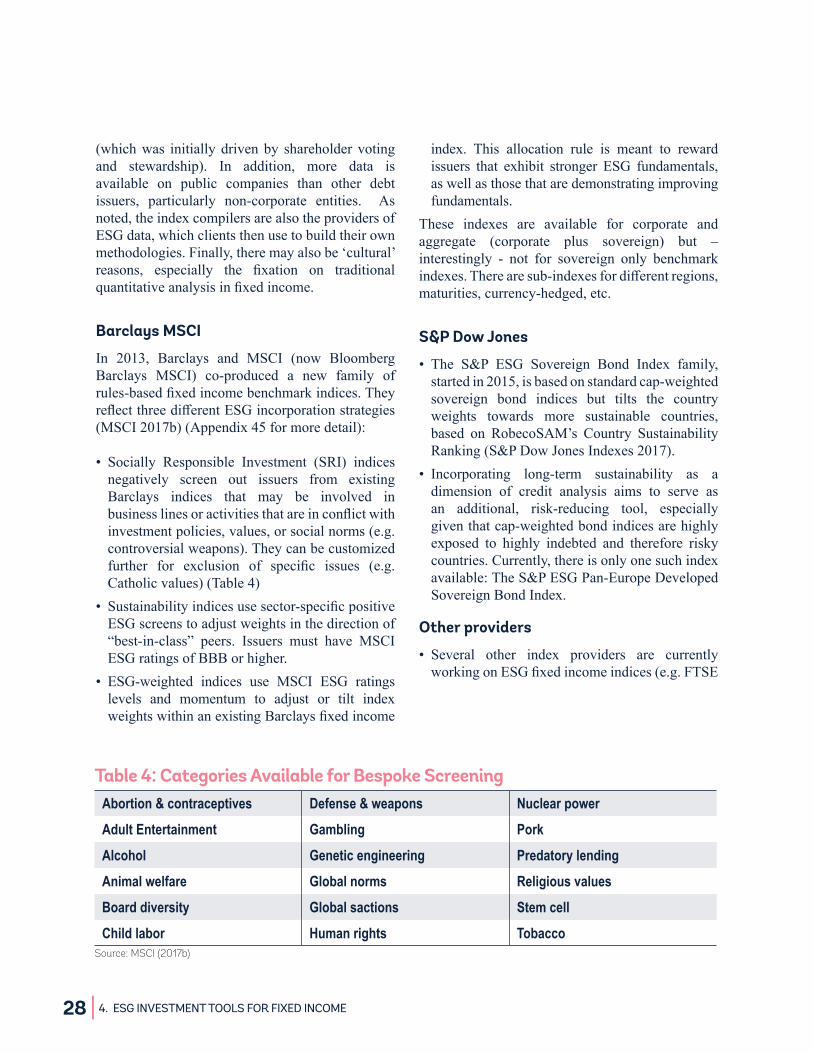

TherearepronounceddifferencesintheapplicationofESGinvestmentapproachestosovereignbonds,andtheycanbepoliticallysensitive.Forexample,itimpliesthepossibleexclusionofwholecountryissuancesbasedonbeingoutsideofcertaintreatiesorconventions(Table2).Awidespreadpracticeisto overweight “good” countries and underweight“bad”countriesbasedonanESGscoringsystem.

INCORPORATING ENVIRONMENTAL, SOCIAL AND GOVERNANCE (ESG) FACTORS INTO FIXED INCOME INVESTMENT | 13

Table 2: Screening Criteria for Different Types of Issuers

Source: PRI (2014)

Naturally, engagement with sovereigns is quitedifferent from engaging with companies, andundertaken less in practice. Investors may seeka dialogue with regulators, policy-makers andstandard-setters (including officials from treasurydepartments, government agencies and debtmanagement offices). The “size gap” betweeninvestorandissuermayevenbemoreofanissuehere than with large corporations. Collaborationsbetween investors may be particularly useful inbondholderengagements.

ESG information on governments is availablefromUNbodies,theOECD,CIAWorldFactbook,Transparency International, the World Bankand similar organizations. Certain segments ofsovereignbondsrequireparticularattention.

Emerging market debt

Many investorsfind thatESG factors tend to beparticularlyusefulintheassessmentofemergingand frontier market bonds. Political and socialdevelopmentsareoftendifficulttograsp,andtheymaynot be fully reflected in credit ratings or incurrent market prices. Regulatory frameworksand transparency can be poor. Issuers may befollowingtheIFC’sPerformanceStandardsortheEquatorPrinciples.

Sub-sovereign issuers

States, regions, cities and other entities can issuebonds at a sub-sovereign level. Municipal bondsareaverysizeablemarket(ofaboutUS$4tn)inthe

Screening Approach Corporate Criteria Government Criteria Financial Sector Criteria

Ethical/reputation screens

Revenue derived from:• Tobacco• Controversial weapons• Nuclear energy• Pornography• Arms• Gambling• Alcohol• Animal testing

• Adherence to international standards on human rights and environmental issues (see below)

• Use of capital punishment

• Financing or ownership of business activities listed under corporate criteria (on left)

• Origination of ABS financing business activities listed under corporate criteria (on left)

• Predatory lending• Aggressive tax avoidance schemes or consultancy

Norms, standards and international laws

• Illegal activites• Export controls• International Labour Organisation conventions

• UN Global Compact Standards

• Trade embargoes• US, EU, UN sactions• ILO conventions• Human rights conventions

• Montreal Treaty• Kyoto Protocol• World Governance Indicators

• Ottawa Treaty (anti-personnel mines)

• Convention on Cluster Munitions (CCM)

• Export controls• Whistle-blower policy• Regulatory compliance• Community Reinvestment Act (US)

• IFC Performance Standards

• Equator Principles• International sanctions

14 | 2. WHAT IS ESG ANALYSIS IN FIXED INCOME INVESTING?

USA,andusedinothercountries.Localgovernmentbondscanbedividedinto twocategories:generalobligationbondsbackedbytaxinflows,andrevenuebondsbackedbyrevenues fromaspecificprojectsuchastollroads.Suchinstrumentsareoftenusedforeconomicinfrastructure(e.g.transport,energy,water,waste)orsocial infrastructure(e.g.schoolsand hospitals). Local and project-specific ESGfactorscomeintoplay.

Supranational issuers

Supranationalorganizations,suchastheWorldBank(IBRD),IFC,AsianDevelopmentBank,EuropeanInvestmentBank,EuropeanBankforReconstructionandDevelopment,regularlyissuebondstofinancedevelopment–relatedprojectsandbusinesses.Theseorganizations are typically considered low risk,with good ESG practices and issue investment-grade (AAA)bonds.Asa result,ESGanalysisonsupranationalstendstobemorefocusedontheiruseofproceeds rather thanon thecreditworthinessoftheissueritself.Supranationalhaveissuedlabelledbondssuchasgreen,socialand/orsustainablebondstoraiseawarenessforcertaintypesofdevelopmentprograms and priorities, responding to investorinterestininvestingforpurpose.

Other Debt and SecuritiesThere is a range of other fixed income securitiesin investor portfolios, often issued by banks orfinancialsectorcompanies.

Asset-backed securities (ABS)

ESGanalysisofABSneedstocapturerisksrelatingtotheoriginatorofthesecurities,theservicerandthe ‘cover pool’ of assets, respectively. Investorsshould also consider how ESG factors mightaffectthefinancialsustainabilityof‘assetpools’orstandalone projects covering the security, such asautoloansandmortgages.Insomecases,investorsfocusontheuseofproceedsforaparticularABSissued(monitoringthecompositionandchangesinthepoolofassets).

Covered bonds

Covered bonds ae a particular type of ABS,predominantlyfinancingresidentialmortgagesandpublic-sectorloans.AswithABS,investorsshouldconsider ESG risks relating to the issuer and thesustainability of the assets themselves. If a bankseizesadefaultedissuers’assets,italsotakesonitsliabilities,whichmayincludefines,ongoinglegalcostsandenvironmentalclean-ups.

Insurance-linked securities

Insurance-linked securities (ILS) are financialinstrumentstiedtocertainriskevents,e.g.weather.Catastrophe bonds (CAT bonds) are risk-linkedsecuritiesthattransferaspecifiedsetofrisksfrom(re)insurance companies to investors. There is anatural connotation to climate change risks here,and, asproceedsareused to rebuildcommunitiesafter disasters, a link is sometimes also made tosocialinvesting.

Structured products

There are many other structured fixed incomeproductsthatarebeingusedininvestorportfolios.Theytypicallycarryaugmentedrisksofcomplexityandtransparency.ThemappingofESGfactorswillbeparticularlytricky.

Private debt

Private equity appeared much later on the ESGradar screen than listed equity.Privatedebt playsan increasing role in the portfolios of insurancecompanies and pension funds, e.g. corporate,realestateand infrastructure loans.Thishasbeenspurredbyalengthyperiodoflowinterestratesandbythepartialwithdrawaloftraditionalbanksfromlonger-term lending following tighter regulation(e.g.BaselIII).Asforallprivateassets, thereareaugmented issues of liquidity and transparency.ThereisstilllittleexperienceonthesideofinvestorsontheconnectiontoESGissues.

INCORPORATING ENVIRONMENTAL, SOCIAL AND GOVERNANCE (ESG) FACTORS INTO FIXED INCOME INVESTMENT | 15

Tosummarize,ESGinvestinginthefixedincomespace is gradually catching up with equities -althoughitisfacingitsownchallenges.Itismoreadvancedforcorporatebondswhere,forexample,engagementteamsareworkingacrossassetclassesand interacting with companies where they have

debt aswell as equityholdings.A surveybyPRI(2017a) finds corporate bonds are better coveredthan sovereign bonds by ESG analysis, whilesecuritizedassetsarefarbehindinthisrespect–butmoreresearchanddevelopmentscanbeexpectedintheseotherclasses(Figure3).

Figure 3: Level of ESG Incorporation in Fixed Income

Source: Authors

16 | 2. WHAT IS ESG ANALYSIS IN FIXED INCOME INVESTING?

INCORPORATING ENVIRONMENTAL, SOCIAL AND GOVERNANCE (ESG) FACTORS INTO FIXED INCOME INVESTMENT | 17

3. ESg ANd fiNANCiAL PErformANCE

– mAiN rESEArCh fiNdiNgS

Many studies have been published withthepurpose to establish an empirical linkbetweenESGandfinancial indicators.Muchof

theresearchfocusinthepastwasonequitiesbutmorestudiesrelevantforfixedincomehavebeenundertakeninrecentyears.18

A comprehensive survey article summarizesthe results of 2,200 primary and review studies(Friede et al. 2015). Roughly 90% of studies findanonnegativerelationbetweenESGandcorporatefinancialperformance(CFP).However,thefindingsaremore neutral/mixed for ‘portfolio studies’, i.e.using portfolio data19 (including ESG funds andindices)ratherthansinglefirmdata.Thereareonlya comparatively small number of studies for non-equityassetclasses.“Theshareofpositivevotesforthe36analyzedbondstudiesstandsat63.9%–with13neutralormixedfindings(36.1%).”(p.222)

How do ESG factors influence the financialperformanceoffixedincomeinvestments?

Thevariousresearcherstakedifferentapproaches,anduseverydifferentmethodologies,datasetsandtimeframes.Theytrytogiveabetterunderstandingon a number of key questions of the relationshipbetweenESGfactorsand:

• costofcapital(debtandequity);• creditrisks;creditspreads;• creditratings;

• default risk; credit default swap(CDS)spreads;

• bondpriceperformance;yields;• marketrisk;• companyvalue;• country economic growth and other macrovariables;

• otherproxyvariablesforperformance.

Fixed income investors are particularly interestedintherelationshipbetweenESGandcreditrisk,i.e.howenvironmental,socialandgovernancefactorsmayaffectcreditworthiness.Therearetwofurtherstrandsofresearchasstudiestypicallyconcentrateoneithercompanies/corporateissuersorcountries/sovereign issuers.The formerappears tobemoreadvanced while the latter had been surprisinglyoverlookedforalongtime.

Corporate BondsSeveral studies have looked at the relationshipbetween corporate bond performance and ESG.Herearesomeexamplesofindustryandacademicresearch.

18 | 3. ESG AND FINANCIAL PERFORMANCE – MAIN RESEARCH FINDINGS

Barclays (2015, 2016) studied the impact ofESGon theperformanceofUS investment-gradecorporate bonds (between 2007 and 2015) andfound that a high ESG rating results in a smallbutsteadyperformanceadvantage.Theeffectwasstrongest for a positive tilt towards the G factor,whilefavoringissuerswithastrongEandSratingwasnotdetrimental tobondreturns.Also, issuerswithhighGscoresexperiencedlowerincidenceofdowngradesbycreditratingagencies.

InadifferentapproachtopricingESGrisk,Hermes(2017)relatesitsproprietarymeasureofESGrisk–theQESGScore–forcompaniestocreditdefaultswap (CDS) indices. Companies with the lowestQESGScorestendtohavethewidestCDSspreadsandbroadestdistributionsofaverageannualCDSspreads.Moreover,creditratingsdonotaccuratelyreflect ESG risks and thereby do not serve as asufficientproxyforESGrisk.

Insight Investment (2016) looks at one particularapproach, i.e., exclusions, in a corporate bondportfolio.Broadethical screensare likely tohavea minimal effect on long-term returns but morefocused screens could have a larger impact. Thedirection of impact – i.e. whether the exclusionsleadtoperformancebeingbetterorworsethantherelevantindex–cannotbepredicted.

For corporate bond issuers, good/bad ESGmanagementcorporatesocialresponsibility(CSR)behavior is rewarded/penalized by lower/higherbond yield spreads, according to research byOikonomouetal. (2014).Similar resultsapply tobond ratings. In their research, Bauer and Hann(2010) conclude that environmental concerns areassociated with a higher cost of debt financingand lower credit ratings, and that proactiveenvironmentalpracticesareassociatedwithalowercostofdebt.

Hsu and Cheng (2015) found that sociallyresponsible firms usually perform better in termsof their credit ratings and have lower credit risk(in termsof loanspreads,defaults).PositiveESG

ratings are associated with reduced financial riskwhile negative ESG performance scores lead toincreasedfinancialdistress.InvestorsrespondmoretopositiveESGratings.20

In contrast,Amiraslani et al. (2017) detected norelationshipbetweencorporatesocialresponsibilityand bond spreads over the period 2005-2013.However, during the 2008-2009 financial crisis,high-CSRfirmsbenefitedfromlowerbondspreads.HoepnerandNilsson(2017a)arguethatbondsissuedbycompanieswith“nostrengths,noconcerns,andno controversies” significantly outperform themarket. These findings are particularly strong intimesofmarketturmoil.

Infrastructure bonds are a growing segmentin investor portfolios. Kiose and Keen (2017)testedthefinancialrisk implicationsofsocialandenvironmental risk factors.Carbon emissions andindependentdirectorson theboardare significantinthisrespect.

A review of research for investment grade (IG)corporatesbyAllianz(2017a)summarizes:

• Within investment grade bonds, issuers withmaterial ESG risks and persistently low ESGscoresaretobeavoided(alsofortailrisks);

• ExpectedESGmomentum(positiveornegative)maynotbefullypricedintothemarkets;

• Anexclusionfilterseemstoleadtonosignificantperformanceimpairment.

Therearecontrastingviews.Cantinoetal.(2017)conclude, fromtheir reviewofESGandfinancialcapital structure, that there is some consensus onthe positive effect of ESG on the cost of equity.However, “results concerning the relationshipbetweenESGsustainabilityanddebtfinancingareambiguousandnoclear-cutdefined”(p.124).Inhistheses, Bektić (2018) argues that the conclusionsonESGfactors incorporate level returnsarestillmixedandthereforepremature.

INCORPORATING ENVIRONMENT, SOCIAL AND GOVERNANCE (ESG) FACTORS INTO FIXED INCOME INVESTMENT | 19

Sovereign BondsInsovereigndebtanalysis,inadditiontoassessingan issuer’s ability to repay its debt, investorsare using ESG information to assess an issuer’swillingnesstorepay.Todate,mostoftheattentionhasbeenongovernancefactors,suchasinstitutionalstrengthandpoliticalrisks.

OneofthefewacademicresearchpaperstostudytherelationshipbetweenESGandsovereignbondperformance isCapelle-Blancard et al. (2017). Ina comprehensive analysis of OECD sovereigns,it concludes that countries with good ESGperformance tend to have less default risk andthuslowerbondspreads.Moreover,theeconomicimpactisstrongerinthelong-run,suggestingthatESG performance is a long-lasting phenomenon.The environmental dimension appears tohavenofinancialimpactwhereasgovernanceweighsmorethansocialfactors.

New industry research had been undertaken onsovereignbonds,muchofitfocusedonESGandcredit ratings.Allianz (2017b)findsevidence thatESGriskfactorsarenotfullyreflectedinsovereigncredit ratings. Bad governance is a key risk,followed by social risks. Tail risk may be bettermitigated through ESG factor integration intosovereignissuercreditanalysis.

Sustainalytics(2017a)revealsapositivecorrelationbetween countries’ ESG and credit rating agency(CRA)ratings,andtheirESGmomentumandGDPpercapitagrowth.BlendingCRAratingswithESGscoresandmomentummayhelpidentifycountriesthatareundervaluedorovervalued.

OtherindustryresearchfocusesonESGandcreditspreads.Lazard(2017)estimatestheportionoftheyield spread attributable to ESG considerations.A strong relationship between a country’s ESGstandardsanditscreditworthiness/costofborrowingisparticularlydiscernibleinemergingmarkets.

High institutional quality is widely seen as animportant factor for sovereign creditworthiness.

Research by international institutions providessome evidence. For example, using a data setof 90 countries, Qian (2012), shows that stronginstitutions are associated with fewer sovereigndefault crises. In addition, when institutions areweak,amorepolarizedgovernmenttendstodefaultmoreoften.

Several individual governance factors suchas corruption or transparency have also beenscrutinized in this context. For example, UnionInvestment (2014) considers corruption a keyindicatorofsovereigncreditstrengthinfundamentalevaluations because of the relationship betweenfraud,taxavoidance,financialmanagementandanissuer’sabilitytorepayitsdebtobligations.Therearestrongcorrelationsbetweencorruptionandthenumberofsovereigndefaults.ChoiandHashimoto(2017) show that data transparency policyreforms, reflected in subscriptions to the IMF’sData Standards Initiatives, reduce the spreads ofemergingmarketsovereignbonds.

Fixed Income FundsSome researchers looked at the performance ofESG/SRIfixed income fundsand fundmanagers.Forexample,Henke(2016)detectedthatduringtheperiod2001–2014,sociallyresponsiblebondfundsoutperformed by half a percent annually. This ismainlyduetotheexclusionofcorporatebondissuerswithpoorcorporatesocialresponsibilityactivities.Outperformanceisespeciallylikelytooccurduringrecessionsorbearmarketperiods.LeiteandCortez(2016)detectcyclicalpatterns:EuropeanSRIfundsprovidesomeprotectioninmarketdownturns,butotherwisetheverdictismixed.

HoepnerandNilsson(2017b)investigatedtheESGengagement activities of fixed income managers.Funds from fund management companies notinvolved in ESG engagement activities performsignificantly worse indicating the materiality ofESG expertise and ESG engagement in fixedincomeinvestments.

20 | 3. ESG AND FINANCIAL PERFORMANCE – MAIN RESEARCH FINDINGS

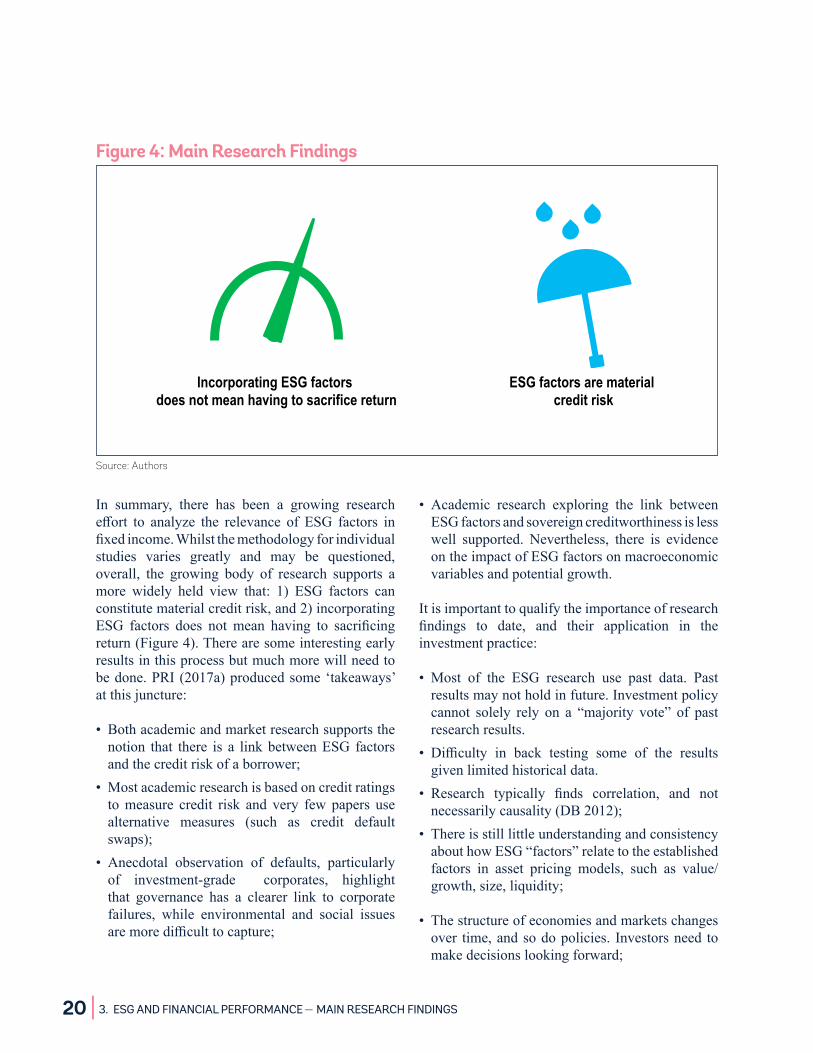

Figure 4: Main Research Findings

Source: Authors

ESG factors are material credit risk

Incorporating ESG factors does not mean having to sacrifice return

In summary, there has been a growing researcheffort to analyze the relevance of ESG factors infixedincome.Whilstthemethodologyforindividualstudies varies greatly and may be questioned,overall, the growing body of research supports amore widely held view that: 1) ESG factors canconstitutematerialcreditrisk,and2)incorporatingESG factors does not mean having to sacrificingreturn(Figure4).Therearesomeinterestingearlyresultsinthisprocessbutmuchmorewillneedtobedone.PRI(2017a)producedsome‘takeaways’atthisjuncture:

• Bothacademicandmarketresearchsupportsthenotion that there is a linkbetweenESG factorsandthecreditriskofaborrower;

• Mostacademicresearchisbasedoncreditratingstomeasure credit risk and very few papers usealternative measures (such as credit defaultswaps);

• Anecdotal observation of defaults, particularlyof investment-grade corporates, highlightthat governance has a clearer link to corporatefailures, while environmental and social issuesaremoredifficulttocapture;

• Academic research exploring the link betweenESGfactorsandsovereigncreditworthinessislesswell supported. Nevertheless, there is evidenceontheimpactofESGfactorsonmacroeconomicvariablesandpotentialgrowth.

Itisimportanttoqualifytheimportanceofresearchfindings to date, and their application in theinvestmentpractice:

• Most of the ESG research use past data. Pastresultsmaynotholdinfuture.Investmentpolicycannot solely rely on a “majority vote” of pastresearchresults.

• Difficulty in back testing some of the resultsgivenlimitedhistoricaldata.

• Research typically finds correlation, and notnecessarilycausality(DB2012);

• ThereisstilllittleunderstandingandconsistencyabouthowESG“factors”relatetotheestablishedfactors in asset pricing models, such as value/growth,size,liquidity;

• Thestructureofeconomiesandmarketschangesover time,andsodopolicies. Investorsneed tomakedecisionslookingforward;

INCORPORATING ENVIRONMENTAL, SOCIAL AND GOVERNANCE (ESG) FACTORS INTO FIXED INCOME INVESTMENT | 21

• There may be (selection, data, size and other)biasesatwork.AsESGresearchmatures,itwillfacestrongerscrutiny;

• Research on ESG in fixed income is still verylimited;

• Mostofitisfocusedoncreditrisks.ThereisstilllittleanalysisoftherelationshipofESGfactorson market risks, inflation, liquidity, maturity,termstructuresandyieldcurves,incomestability,totalreturns,andotherrisks/opportunitiessuchasdefaultriskorrecoveryrates;

• Implementation costs (e.g. for transactions,management,reporting)needtobeconsidered;

• Investorsareadvisedtoapplytheirownadditionalresearchandinsights;

• Differentreportingstandardsresultsinalackofcomparabilitybetweenfindings.

Finally,someobserversfeelthat–whilecertainlyrelevant – financial performance has receivedtoo much attention in recent times compared toconceptual research and empirical evidence onextra-financialperformances(e.g.Capelle-BlancardandMonjon2012).Overall,itisstillearlydaysforresearchonfinancialperformance,andevenmoresofornon-financialperformance,ofESGinfixedincome.

MorerobustresearchisneededonthelinkbetweenESG and financial performance of fixed incomeinvestments. Further academic, as opposed toindustry studies are needed, looking at the linkbetween fixed income and ESG factors usingtransparent methodologies, over longer timeperiods, across a broader range of fixed incomeassetsandcountries.Consideringfactorsotherthancredit risk is required to provide a solid base ofevidenceasESGfixedincomeinvestingbecomesmoremainstream.

22 | 3. ESG AND FINANCIAL PERFORMANCE – MAIN RESEARCH FINDINGS

INCORPORATING ENVIRONMENTAL, SOCIAL AND GOVERNANCE (ESG) FACTORS INTO FIXED INCOME INVESTMENT | 23

4. ESg iNvESTmENT TooLS for

fixEd iNComE

A number of tools have been created overtimetoassistinvestorsintheanalysisofESGrisksandopportunities.Here, too,fixedincomeis

lagging equities.21 Nonetheless, a number of ESG frameworkshavebeendevelopedinrecenttimesforbonds,inparticularESGscores22 andrankingsforcompanies,countriesandotherissuesaswellasESGfixedincome indices. First, an immediate question arising is, howESG relates to thetraditionalcreditratingsthatareacoreelementintraditionalfixedincomemanagement.

Credit Ratings and ESGAdiscussionisongoingontheextenttowhichESGfactorsarerelevantforcreditrisks,andinparticularcredit ratings. Some investors have asked for aclarification of the role of ESG factors in creditratings,ordemandanexplicit integrationofESGbycreditratingagencies(CRA)(PRI2017a).23

ESG incorporation

AllmajorratingagenciessaytheyalreadyincorporateESGconsiderationsintheirtraditionalanalysis(S&PGlobalRatings2017,Moody’s2017,FitchRatings2017).At the same time, they are deepening andwidening the researchofESG topics, in particularonclimatechangerisks.Theyalsowanttoimprovecommunicationonthesematters.

Materiality

“Fitch Ratings’ criteria and analysis incorporateenvironmental, social and governance (ESG) risk

factors, but only where they are relevant to theassessmentofcreditrisk.”(FitchRatings2017,p.1)“Ourobjectiveisnottocaptureallconsiderationsthatmaybe labelledgreen,sustainableorethical,but rather those that have a material impact oncreditquality.”(Moody’s2017,p.3)

Time horizon

The focus is not on an exact time frame but on“the most forward-looking view that visibilitypermits” (Moody’s 2017, p.3). S&Ps forecastsgenerallycoveratimehorizonofuptotwoyearsfor speculative-grade corporate entities (that is,those rated ‘BB+’ and below), and nomore thanfive years for investment-grade entities, but theycangolonger.Forexample,forEfactorsthataffectsovereignratings,thetimehorizonis5-10years.

Sectors

ESGthemesvarywidelyacrosssectors.AccordingtoMoody’s,forexample,14sectorshaveelevated

24 | 4. ESG INVESTMENT TOOLS FOR FIXED INCOME

credit exposure to carbon regulations. S&Pcounted106 cases in theperiod2015-2017whenenvironmentalandclimateriskswereakeyreasonfor a rating action, most notably in the energy,resourcesandvehicleindustries.

Sovereign issuers

For all CRAs, different sets of ESG factors arerelevantforcorporate,sovereignandotherissuers.Forsovereigns,S&PconsidersESGfactorsinthecontextoftheassessmentofinstitutionalqualityandgovernanceeffectiveness,butalsosocialcohesion,climate change and other key factors. Moody’snames 5 key ESG trends for sovereigns: countrycompetitiveness,governmenteffectiveness,controlof corruption, rule of law or physical climatechange.ForFitch,governanceindicatorshavethegreatestweightingforsovereignratings.

Overall, credit ratings can only partially accountfor long-term sustainability risks,mainly becauseof the focusonmateriality for credit riskand therelativelyshorttimehorizon.Othermethodologieshave been developed to compensate for thatlimitation,but falloutside thecredit ratingspace.SomeinvestorswouldliketheCRAtoextendtheirESGoutput,including:

• longertimehorizonsforratings;• separateE,SandGfactors;• moreextensiveESGdisclosures;• anESGratingalongsidethetraditionalcreditrating.

CRAshavestartedtodevelopseparateassessmentsspecifically for environmental and ESG risks.On example of a specialist “E” product for apopular financial instrument is Moody’s GreenBondsAssessment.24 In2016,S&PpublishedtwoproposalsforapotentialnewESGevaluationtoolaswellasforagreenbondscoringframework,bothseparatefromtraditionalcreditratings.

ESG Scores/RankingsGenerally speaking, an ESG score is measure ofenvironmental, social, and governance factors.

Each ESG category has numerous underlyingfactors that are analyzed and ranked, and thencombinedinanaggregateESGscoreforasector,regionandanoverallportfolioscore.ThescoringmethodsandweightingsfortheE,theSandtheG,andtheunderlyingfactorsmayvaryacrosssectorsandcountries.

The most common ESG scores are at the microlevel and provide somemeasure of a company’sESG performance. There are also country-levelESG scores that complement traditional methodsof assessing a country’s long-term economicprospects, creditworthiness as well as potentialreputationalrisks.

There are external, commercial providers of ESGscores.Althoughthemethodologiesarequantitative,the assessments are inherently qualitative. Someinvestorsthereforealsosetupin-house,proprietaryESG scoring systems, overlaying externalinformationwith their own analysis.According toRussell(2017),52%oftherespondentfixedincomemanagersutilize third-partyvendorsexclusively toobtain ESG scores. 35% utilize external vendorswith an in-house ESG analysis overlay. 15% onlyuseinternalanalysis.ThetwomarketleadersinfixedincomearecurrentlySustainalyticsandMSCI,withinvestors and product providers overwhelminglyrelyingonthesesources.

Sustainalytics

Sustainalytics’ ESG scores give individual pointsforcompanies’E,SandGelements (0-100).Theoverall ESG score provides an absolute measureof a company’s ESG performance as well as itsrelative position within an industry. The set ofissues and specific weights vary by industry; atleast 70 indicators in each industry are covered(Sustainalytics2017b).

Forsovereignbondinvestors,thereisalsoacountryESGscorethatisbasedon36third-partyindicatorsthatshouldcomplementtraditionalmacroanalyses.ItresultsincountryscoresforE,SandGseparately,andanoverallESGscore(0-100).Finally, there is

INCORPORATING ENVIRONMENTAL, SOCIAL AND GOVERNANCE (ESG) FACTORS INTO FIXED INCOME INVESTMENT | 25

a country ESG rating ranging fromA to E that isallocatedonsetstandarddeviationsfromtheaverage.

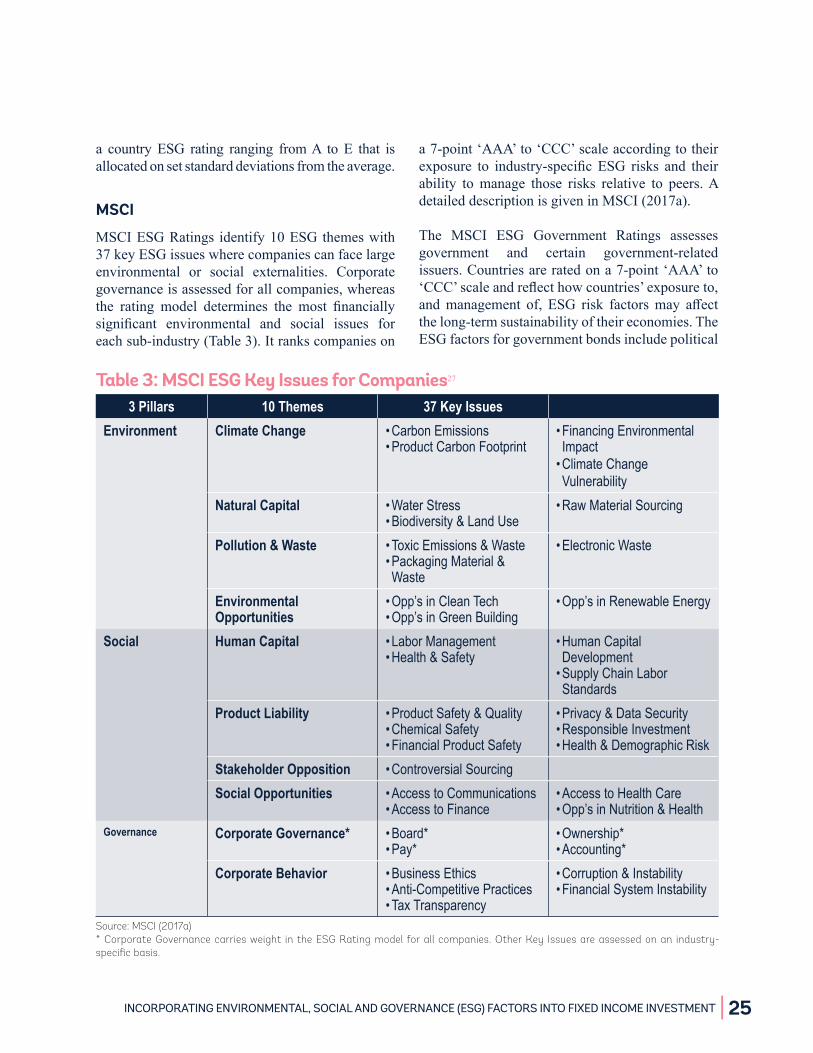

MSCI

MSCIESGRatings identify10ESGthemeswith37keyESGissueswherecompaniescanfacelargeenvironmental or social externalities. Corporategovernanceisassessedforallcompanies,whereasthe rating model determines the most financiallysignificant environmental and social issues foreachsub-industry(Table3).Itrankscompanieson

a7-point‘AAA’to‘CCC’scaleaccordingtotheirexposure to industry-specificESG risks and theirability tomanage those risks relative to peers.AdetaileddescriptionisgiveninMSCI(2017a).

The MSCI ESG Government Ratings assessesgovernment and certain government-relatedissuers.Countriesareratedona7-point‘AAA’to‘CCC’scaleandreflecthowcountries’exposureto,andmanagement of, ESG risk factorsmay affectthelong-termsustainabilityoftheireconomies.TheESGfactorsforgovernmentbondsincludepolitical

Table 3: MSCI ESG Key Issues for Companies27

3 Pillars 10 Themes 37 Key IssuesEnvironment Climate Change • Carbon Emissions

• Product Carbon Footprint• Financing Environmental Impact

• Climate Change Vulnerability

Natural Capital • Water Stress• Biodiversity & Land Use

• Raw Material Sourcing

Pollution & Waste • Toxic Emissions & Waste• Packaging Material & Waste

• Electronic Waste

Environmental Opportunities

• Opp’s in Clean Tech• Opp’s in Green Building

• Opp’s in Renewable Energy

Social Human Capital • Labor Management• Health & Safety

• Human Capital Development

• Supply Chain Labor Standards

Product Liability • Product Safety & Quality• Chemical Safety• Financial Product Safety

• Privacy & Data Security• Responsible Investment• Health & Demographic Risk

Stakeholder Opposition • Controversial SourcingSocial Opportunities • Access to Communications

• Access to Finance• Access to Health Care• Opp’s in Nutrition & Health

Governance Corporate Governance* • Board*• Pay*

• Ownership*• Accounting*

Corporate Behavior • Business Ethics• Anti-Competitive Practices• Tax Transparency

• Corruption & Instability• Financial System Instability

Source: MSCI (2017a)* Corporate Governance carries weight in the ESG Rating model for all companies. Other Key Issues are assessed on an industry-specific basis.

26 | 4. ESG INVESTMENT TOOLS FOR FIXED INCOME

risks, human rights and environmental issues.Asa practical example, Swiss Re (2017) applies aconceptofminimumESGratingstandardsintheirassetliabilitymanagement(ALM)approach.

Other providers

There are several more specialist services on themarket of company ESG scores of some sort,includingRepRisk,ISS-Ethix,Bloomberg,ThomsonReuters/Eikon.25VeriskMaplecroft,VigeoEirisandOekom Research also offer a sustainability ratingalso for countries. Beyond Ratings and severalFrenchbankshaveannouncedplansforafirstcreditratings agency to systematically integrate ESGfactors into financial ratings and provide investorswithan“augmentedassessmentofcreditworthiness”in2018. Inpractice, investorsoftenusemore thanoneexternalproviderofESGscores.

Sustainability rating for funds

ESG ratings for funds have been introducedby a number of companies, including MSCI,Barron’s and Corporate Knights. One example,theMorningstarSustainabilityRatingisameasureof how well the companies held by a fund aremanaging their ESG risks and opportunitieswhen compared with similar funds. It is basedon company-level ESG data from Sustainalytics.Scores are aggregated to a portfolio ESG scoreusing an asset-weighted average of all coveredsecurities (equity and fixed-income). Funds aresorted into five normally distributed groups (1-5stars).

However,criticismhasbeenleviedthattheanalysisbehind the ratings does not fully reflect the trueESGlevelofintegrationorimpactofthefunds.Forexample,norecognitionisgiventoinvestorseffortson shareholder engagement and public advocacy.Furthermore, there is no considerationof the realimpactandmanagerswithspecificimpact-focusedmandates–includingthoseoperatinginemergingmarketsordevelopingcountries–canbepenalized(e.g.,Krosinsky2018).26

Country ScoresIn addition, several fund managers and assetowners have developed their own ESG scoringsystems,orvariationsusing rawdata fromMSCIor Sustainalytics in a different way, especially atcompany level.Herearesomeexamples forESGcountryscores.Developedcountriestypicallyfarebetterthanemerging,frontiermarkets-especiallywhenlookingat‘levels’ratherthan‘changes’.Thisraises serious questions on ESG analysis in thesovereignspace.

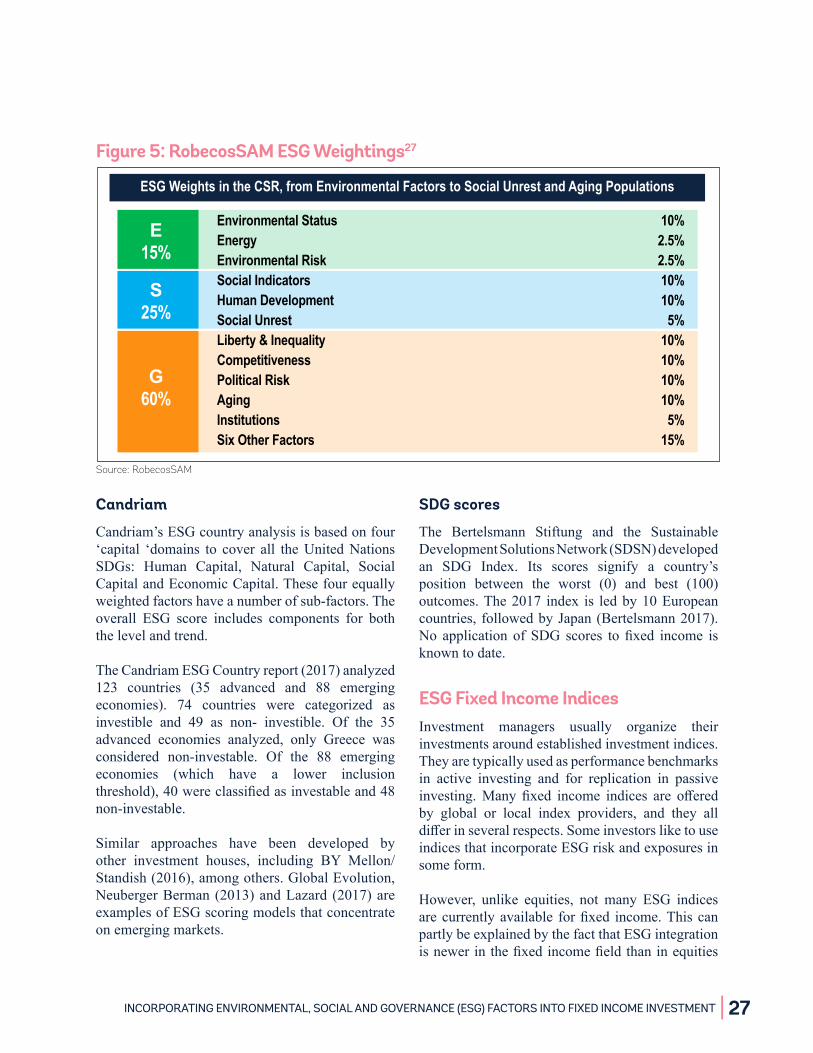

RobecoSAM

RobecoSAM’s is one of the more transparentcountrysustainabilityframeworks.Itevaluates65countries(22developedand43emergingmarkets).Standardizedscoresandindicatorweightsresultinacountrysustainabilityscorerangingfrom1to10(RobecoSAM,2015).The framework isbasedon17environmental,socialandgovernanceindicators(each of which is based on various data series,or sub-indicators). They are grouped in the threeE,S,&Gdimensions,whichreceiveaweightof15%,25%and60%ofthetotalscore,respectively(Figure 5 and Appendix 4). The selection andweightings of the indicators was primarily basedon their financial relevance for the assessment ofsovereignbondmarkets.ThelistiscurrentlybeingledbyfourNordicstates,Switzerland,CanadaandAustralia.

DZ Bank

DZ Bank developed a sustainability rating forcountriesthatcombinesanESGmethodology(withraw data from Sustainalytics) with an economicsustainability dimension, i.e. a four-dimensionalEESGanalysismodel.TheweightingofEfactorsis 20%, S 30%, G 30% and economic factors30%. Countries are grouped into “sustainable”,“transformation states” and “unsustainable”. Thecurrent list is being led by Nordic and middleEuropeanstates(DZBank2015).

INCORPORATING ENVIRONMENTAL, SOCIAL AND GOVERNANCE (ESG) FACTORS INTO FIXED INCOME INVESTMENT | 27

Candriam

Candriam’sESGcountryanalysisisbasedonfour‘capital ‘domains to cover all theUnitedNationsSDGs: Human Capital, Natural Capital, SocialCapitalandEconomicCapital.Thesefourequallyweightedfactorshaveanumberofsub-factors.Theoverall ESG score includes components for boththelevelandtrend.