income statement

TRANSCRIPT

Preparation of Financial Statements

Year End Process

At the end of the year the income accounts and the expenditure accounts are

balanced off and the balance are transferred to the Income statement.

By balancing the Income Statement the profit or loss for the period is calculated

which is transferred to the capital account.

Account Dr Cr

Profit Income Statement Capital Account

Loss Capital Account Income Statement

The drawing account is balanced and transferred to the capital account.

The remaining assets the liabilities accounts are balanced off and carried forward to

the next accounting period. These will appear in the balance sheet prepared as at

the last date of the accounting year.

Peter Ltd

Question

The following Trial Balance was extracted from Peter Ltd on 31st December 2004.

$ $

Turnover 300

Expenses 100

Drawings 20

MV 240

Bank 110

Payables 30

Capital 140

470 470

You are required to complete the4 following accounts are prepare the for the year ended

31.12.2004

Turnover Expenses

B/D 300 B/D 100

Income statement

Exp Turnover

Income Statement

Turnover

Expenses

Profit

Drawing Account Capital Account

B/D 20 B/D 140

Peter Ltd

Balance Sheet

Non Current Assets

MV

Current Assets

Bank

Capital & Liabilities

Capital at Liabilities

+ Profit

- Drawings

Capital at End

Current Liabilities

Payables

Question

You’ve been provided with the trial balance of J Sparks for the year ended 31st of December

2009.

Description

Dr

($)

Cr

($)

Sales 500,000

Purchase 100,00

Long Term Loan 50,000

Land & Building 300,000

Motor vehicles 100,000

Carriage Inwards 4,000

Carriage Outwards 6,000

Return Inwards 10,000

Return outwards 15,000

Electricity 2,000

Rent & Rates 3,000

Heating & Lighting 6,000

Postage & Stationary 1,000

Bad Debts 4,000

Discounts 5,000 7,000

Advertising 8,000

Salesman Salary 6,000

Wages 8,000

Interest Expenses 9,000

Commission Income 13,00

Interest Income 15,000

Debtors 50,000

Creditors 20,000

Bank balance 200,000

Cash Balance 75,000

Drawings 10,000

Capital 287,000

907,000 907,000

You are required to

Prepare an Income statement for the year ended 31.12.2009 and a balance sheet as at that

date.

I Ching

Question

From the following trial balance I Ching extracted after one year’s trading. Prepare an

Income Statement for the year ended 31 December 2003. A Balance sheet is also required.

Trial Balance as at 31 December 2003

DR

($)

CR

($)

Sales 28,462

Purchase 14,629

Salaries 2,150

Motor expenses 520

Rent 670

Insurance 111

General expenses 105

Premises 1,500

Motor Vehicles 1,200

Debtors 1,950

Creditors 1,538

Cash at bank 11,654

Cash in hand 40

Drawings 895

Capital 5,424

35,424 35,424

You are required to

Prepare an Income Statement for the year ended 31.12.2003 and a balance sheet as at that

date.

D Blacksmith

Question

From the following trial of D Blacksmith after his first year’s trading. You are required to

draw up an Income statement for the year ended 30 June 2008. A balance sheet is also

required.

Trail Balance as at 30 June 2008.

You are required to

DR

($)

CR

($)

Sales 48,794

Purchase 23,803

Rent 854

Lightening & heatining Expenses 422

Salaries & Wages 3,164

Insurance 105

Building 70,000

Fixtures 1,000

Debtors 3,166

Sundry Expenses 506

Creditors 1,206

Cash at bank 3,847

Drawings 2,400

Vans 5,500

Capital 1,133

115,900 115,900

Prepare an Income Statement for the year ended 30.06.20083 and a balance sheet as at

that date.

Adjusting For Closing Stocks

Stocks held a company would be one of its current assets. When ever goods are purchased

it is debited to the purchases account as an expense. The asset is not recognized at this

point. At the end of a given year a company would normally possess a certain amount of

stocks which could not be sold during that year. The purchases account would contain all

purchases made during the year including the closing stock.

It would be incorrect to match the sales revenues with total purchases in a situation like

this.

Such closing stock held by the company would amount to be one of the current assets as at

the balance sheet date.

The following adjustments are now needed to rectify the situation.

(i) To recognize the asset of stock.

(ii) To adjust cost sales, so that it would reflect the cost of the goods sold

and not total purchases.

* Account Dr ($) Cr ($)

Stock Account XX

Cost of Sales XX

This stock is referred to as the closing stock as at the end of the year.

As at beginning of the next year the same stock would be referred to as the opening stock.

During the second year if these goods are sold the balance in the stock account would be

charged to cost of sales as follows.

* Account Dr ($) Cr ($)

Cost of Sales XX

Stock Account XX

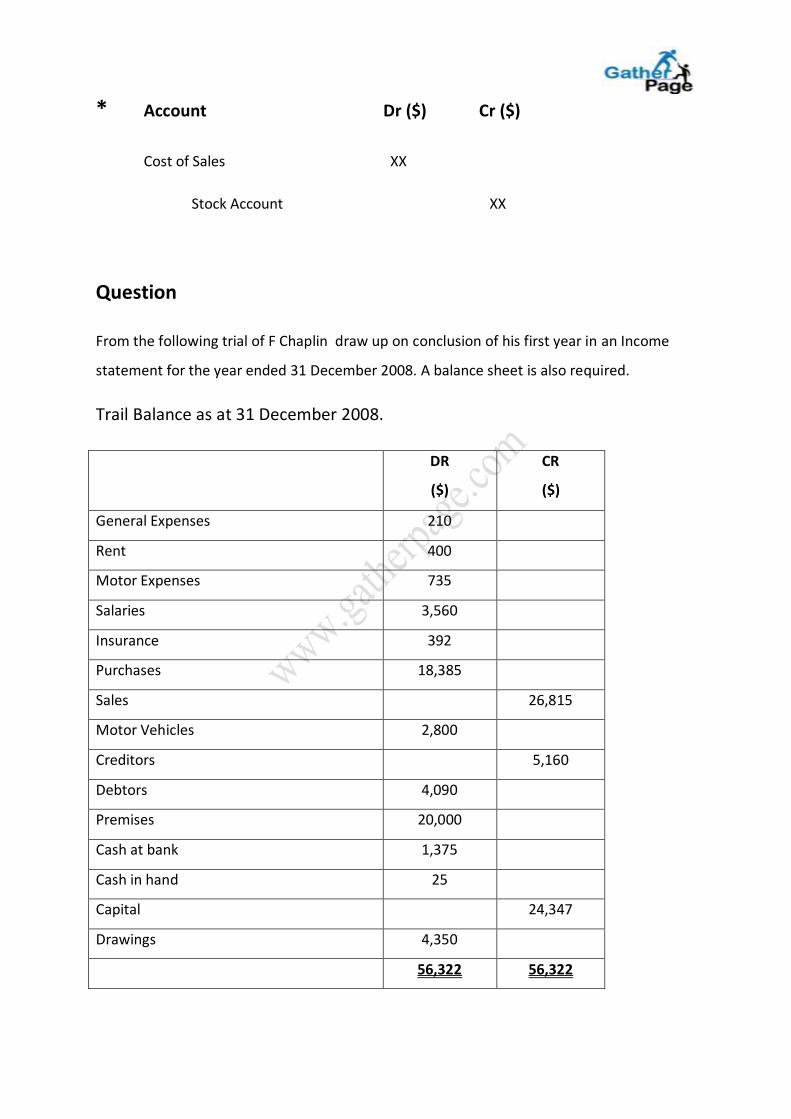

Question

From the following trial of F Chaplin draw up on conclusion of his first year in an Income

statement for the year ended 31 December 2008. A balance sheet is also required.

Trail Balance as at 31 December 2008.

DR

($)

CR

($)

General Expenses 210

Rent 400

Motor Expenses 735

Salaries 3,560

Insurance 392

Purchases 18,385

Sales 26,815

Motor Vehicles 2,800

Creditors 5,160

Debtors 4,090

Premises 20,000

Cash at bank 1,375

Cash in hand 25

Capital 24,347

Drawings 4,350

56,322 56,322

Stock at December 2008 was $ 4,960.

You are required to

Prepare an Income Statement for the year ended 31.12.2008 and a balance sheet as at that

date.

F Kidd

Question

The Trial Balance of Kidd as at 30th June 2008 is as follows.

DR

($)

CR

($)

Rent 1,560

Insurance 305

Lightning & heating expenses 516

Motor expenses 1,960

Salaries & Wages 4,850

Sales 35,600

Purchases 30,970

Sundry expenses 806

Vans 3,500

Creditors 3,250

Debtors 6,810

Fixtures 3,960

Buildings 28,000

Cash at bank 1,134

Drawings 6,278

Capital 51,799

90,649 90,649

You are required to

Prepare an Income Statement for the year ended 30.06.2008 and a balance sheet as at that

date.

Question

From the following trial of R Graham draw up an Income statement for the year ended 30

September 2009, and a balance sheet as at that date.

DR

($)

CR

($)

Stock 1 October 2008 2,368

Carriage Outwards 200

Carriage inwards 310

Returns inwards 205

Return outwards 322

Purchase 11,874

Sales 18,600

Salaries & Wages 3,862

Rent 304

Insurance 78

Motor expenses 664

Office expenses 216

Lighting and heating expenses 166

General expenses 314

Premises 5,000

Motor Vehicles 1,800

Fixtures and fitting 350

Debtors 3,896

Creditors 1,731

Cash at bank 482

Drawings 1,200

Capital 12,636

33,289 33,289

Stock at 30 September 2009 was $2,946.

You are required to

Prepare an Income Statement for the year ended 30.09.2009 and a balance sheet as at that

date.

Question

The Following trial balance was extracted from the books of B Jackson on 30 April 2007.

From it, and the note about stock, prepare his Income statement the year ended 30 April

2007 and a balance sheet as at that date.

DR

($)

CR

($)

Sales 18,600

Purchases 11,556

Stock 1 May 2006 3,776

Carriage outwards 326

Carriage Inwards 234

Return Inwards 440

Return outwards 355

Salaries & Wages 2,447

Motor expenses 664

Rent 576

Sundry expenses 1,202

Motor Vehicle 2,400

Fixtures and fittings 600

Debtors 4,577

Creditors 3,045

Cash at bank 3,876

Cash in hand 120

Drawings 2,050

Capital 12,844

34,844 34,844

You are required to

Prepare an Income Statement for the year ended 30.04.2007 and a balance sheet as at that

date.

Question

The Following is Trial Balance of J Smailes as at 31 March 2009. Draw up a set of financial

statements for the year ended 31 March 2009.

DR

($)

CR

($)

Stock 1 April 2008 18,160

Sales 92,340

Purchases 69,185

Carriage Inwards 420

Carriage outwards 1,570

Return outwards 640

Wages & Salaries 10,240

Rent & rates 3,015

Communication expenses 624

Commissions payable 216

Insurance 405

Sundry Expenses 318

Buildings 20,000

Debtors 14,320

Creditors 8,160

Fixtures 2,850

Cash at bank 2,970

Cash in hand 115

Drawings 7,620

Capital 50,888

152,028 152,028

Stock at 31 March 2009 was $ 22,390.

You are required to

Prepare an Income Statement for the year ended 31.03.2009 and a balance sheet as at that

date.