improving us access success indicators: testing...

TRANSCRIPT

Improving US Access Success Indicators: Testing Benefit Design Assumptions

Kevin Fitzpatrick, Principal, IMS Consulting

On average, how many different benefit designs do you think are offered by the

top 18 MCOs?

Options A: 27 B: 72 C: 104 D: 176

Benefit Design: For simplicity, let’s think about benefit design as being the co-pay amounts assigned to Tier 2

and Tier 3; for example $25-50 or $30-60.

2 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators

On average, how many different benefit designs do you think are offered by the

top 7 PBMs?

Options A: 57 B: 102 C: 323 D: 622

Benefit Design: For simplicity, let’s think about benefit design as being the co-pay amounts assigned to Tier 2

and Tier 3; for example $25-50 or $30-60.

3 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators

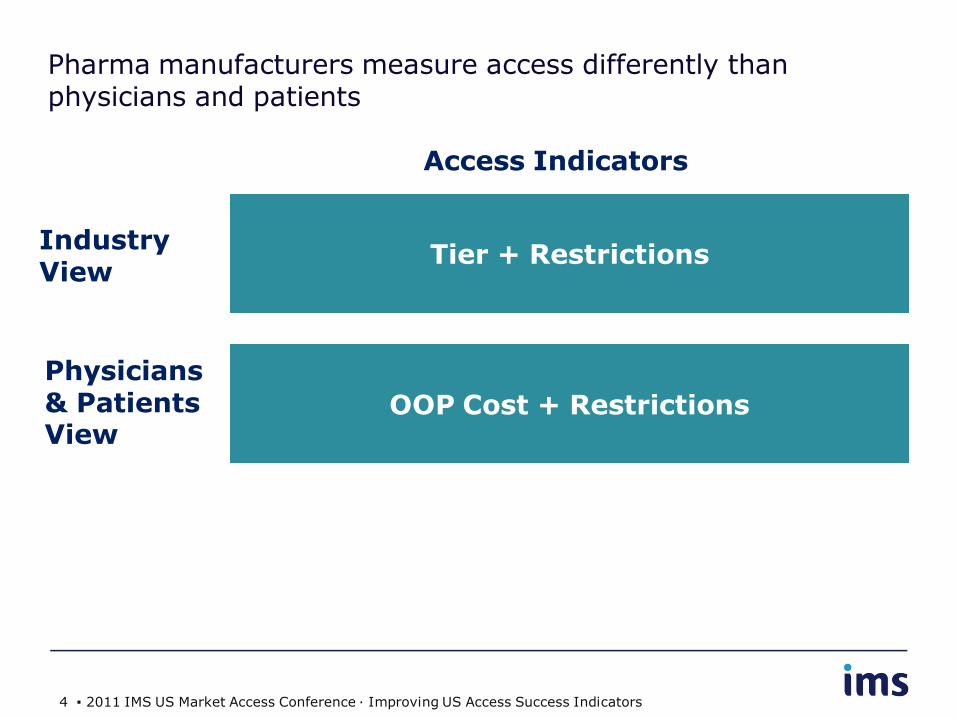

Pharma manufacturers measure access differently than physicians and patients

Tier + Restrictions

OOP Cost + Restrictions

Industry View

Physicians & Patients View

Access Indicators

4 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators

The bridge that links Tier and OOP Cost is Benefit Design, so that is what we will explore

Today’s Goal

Test common assumptions related to benefit design and determine whether or not they are based on sound evidence

5 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators

Assumption #1: What you see is what you get

Fact #1

Fact #2

Fact #3

Most Common Benefit Design (MCBD) is an appropriate measure to understand the benefit design of a plan

6 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators

Assumption #1: What you see is what you get

Fact #1

Fact #2

Fact #3

For the majority of top 25 payers in the US, MCBD represents less than one quarter of the script volume

Most Common Benefit Design (MCBD) is an appropriate measure to understand the benefit design of a plan

7 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators

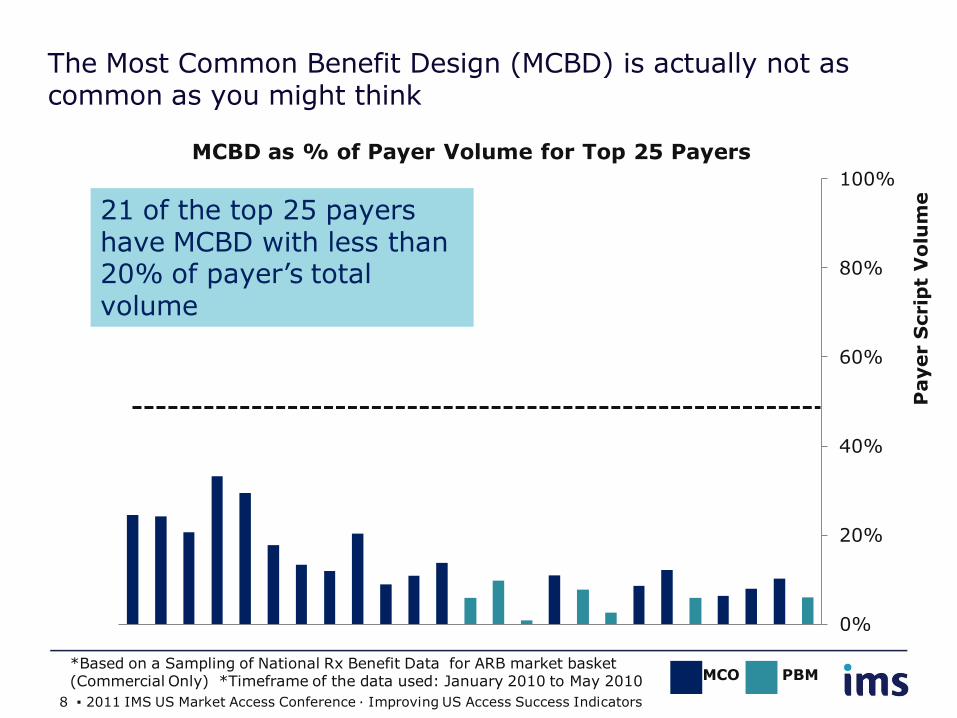

The Most Common Benefit Design (MCBD) is actually not as common as you might think

MCO PBM

21 of the top 25 payers have MCBD with less than 20% of payer’s total volume

0%

20%

40%

60%

80%

100%

MCBD as % of Payer Volume for Top 25 Payers

Payer S

crip

t V

olu

me

*Based on a Sampling of National Rx Benefit Data for ARB market basket (Commercial Only) *Timeframe of the data used: January 2010 to May 2010

8 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators

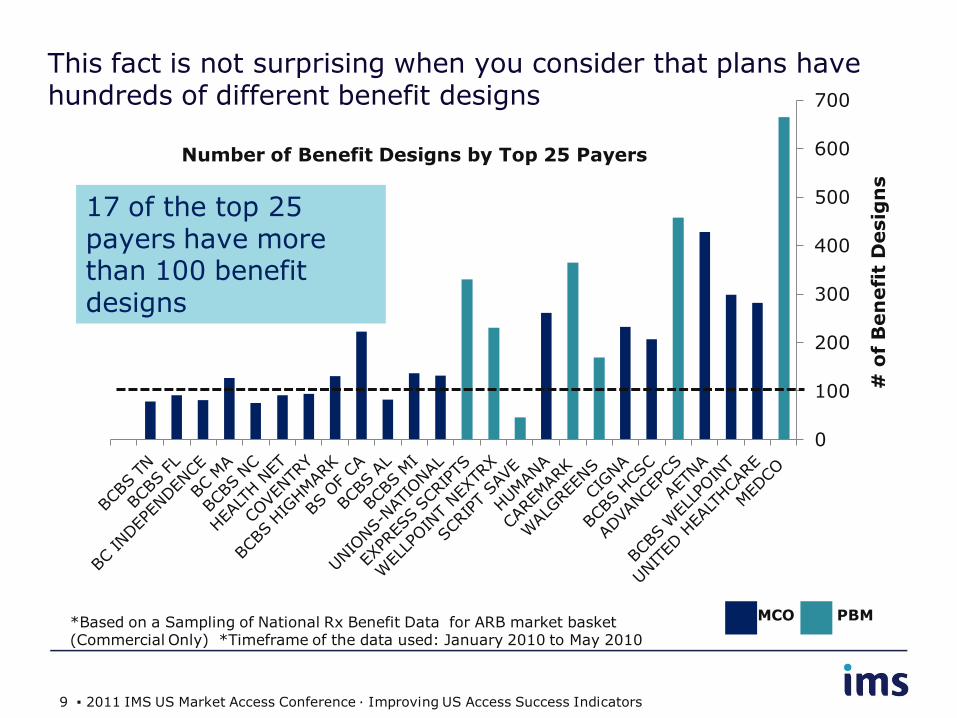

This fact is not surprising when you consider that plans have hundreds of different benefit designs

0

100

200

300

400

500

600

700

# o

f B

en

efi

t D

esig

ns

MCO PBM

Number of Benefit Designs by Top 25 Payers

17 of the top 25 payers have more than 100 benefit designs

*Based on a Sampling of National Rx Benefit Data for ARB market basket (Commercial Only) *Timeframe of the data used: January 2010 to May 2010

9 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators

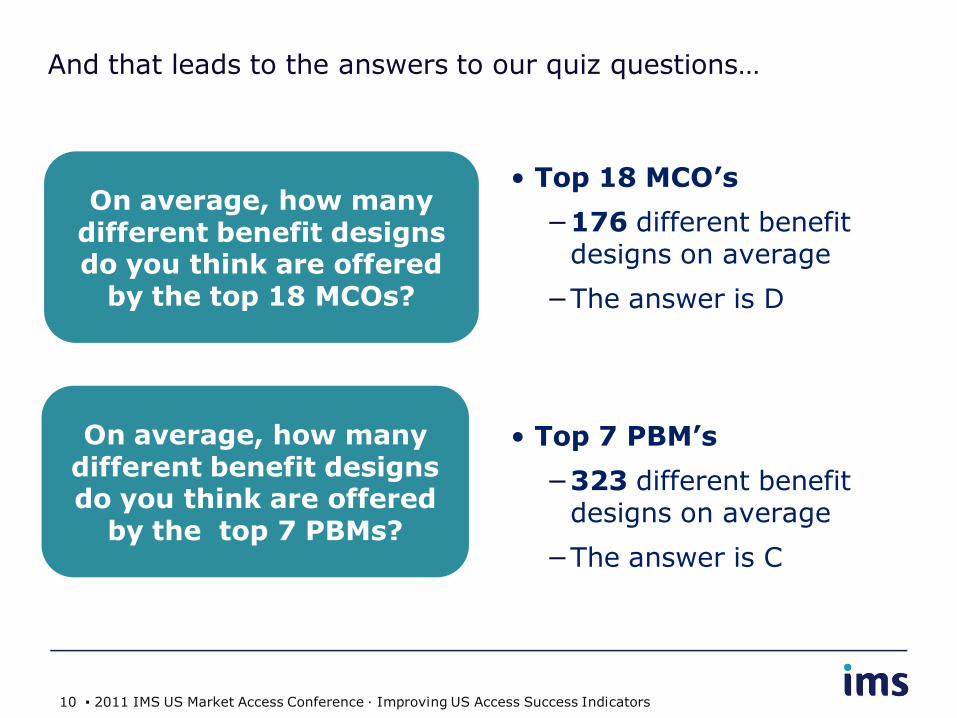

And that leads to the answers to our quiz questions…

• Top 18 MCO’s

−176 different benefit designs on average

−The answer is D

• Top 7 PBM’s

−323 different benefit designs on average

−The answer is C

On average, how many different benefit designs do you think are offered

by the top 18 MCOs?

On average, how many different benefit designs do you think are offered

by the top 7 PBMs?

10 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators

Assumption #1: What you see is what you get

Fact #1

Fact #2

Fact #3

MCBD masks the underlying basket of benefit designs and the relative influence they can exert

Most Common Benefit Design (MCBD) is an appropriate measure to understand the benefit design of a plan

11 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators

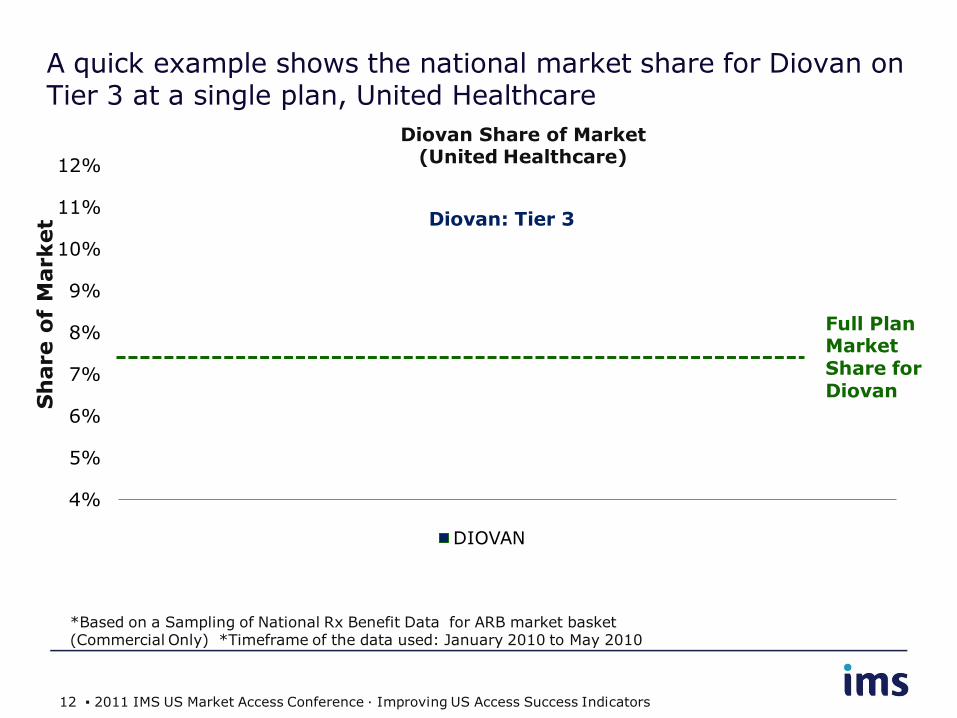

A quick example shows the national market share for Diovan on Tier 3 at a single plan, United Healthcare

4%

5%

6%

7%

8%

9%

10%

11%

12%

DIOVAN

Sh

are o

f M

arket

Diovan Share of Market (United Healthcare)

Full Plan Market Share for Diovan

Diovan: Tier 3

*Based on a Sampling of National Rx Benefit Data for ARB market basket (Commercial Only) *Timeframe of the data used: January 2010 to May 2010

12 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators

Looking more closely across benefit designs shows the impact of T2:T3 differentials on market share for Diovan

4%

5%

6%

7%

8%

9%

10%

11%

12%

$5 $10 $15 $20 $25 $30 $35 $40

DIOVAN Linear (DIOVAN)

Tier2:Tier3 Co-Pay Differentials ($)

Diovan Shares of Market by T2:T3 Co-Pay Differentials

Diovan: Tier 3

Sh

are o

f M

arket

Full Plan Market Share for Diovan

*Based on a Sampling of National Rx Benefit Data for ARB market basket (Commercial Only) *Timeframe of the data used: January 2010 to May 2010

13 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators

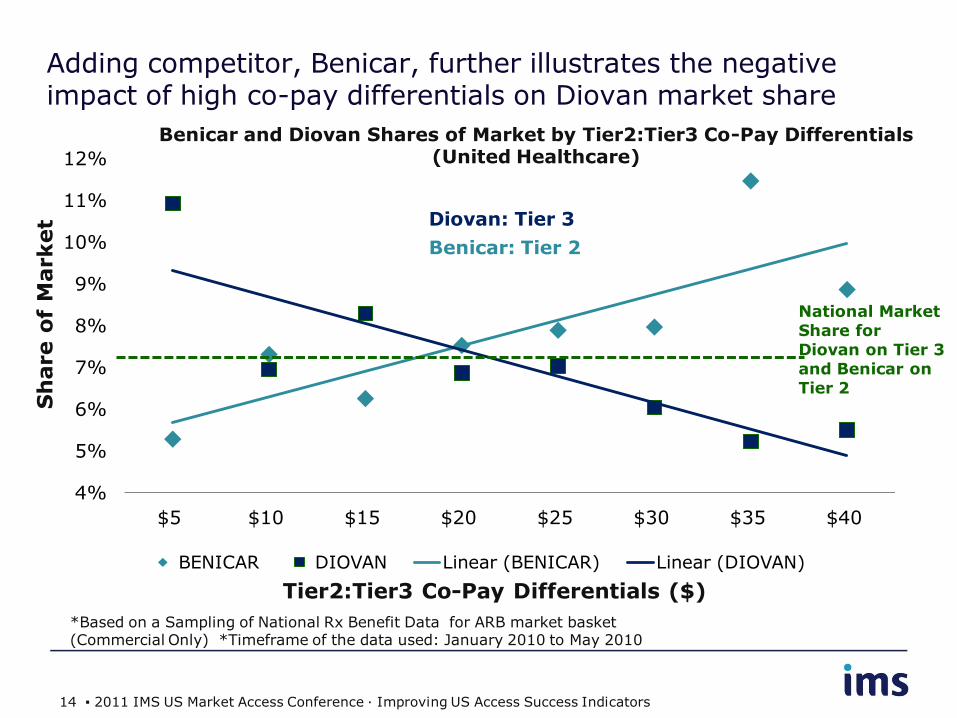

Adding competitor, Benicar, further illustrates the negative impact of high co-pay differentials on Diovan market share

4%

5%

6%

7%

8%

9%

10%

11%

12%

$5 $10 $15 $20 $25 $30 $35 $40

BENICAR DIOVAN Linear (BENICAR) Linear (DIOVAN)

Tier2:Tier3 Co-Pay Differentials ($)

Benicar and Diovan Shares of Market by Tier2:Tier3 Co-Pay Differentials (United Healthcare)

Benicar: Tier 2

Diovan: Tier 3

Sh

are o

f M

arket

National Market Share for Diovan on Tier 3 and Benicar on Tier 2

*Based on a Sampling of National Rx Benefit Data for ARB market basket (Commercial Only) *Timeframe of the data used: January 2010 to May 2010

14 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators

Assumption #1: What you see is what you get

Fact #1

Fact #2

Fact #3

Just because two plans have similar MCBD, doesn’t mean their overall mix of benefit designs is the same

Most Common Benefit Design (MCBD) is an appropriate measure to understand the benefit design of a plan

15 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators

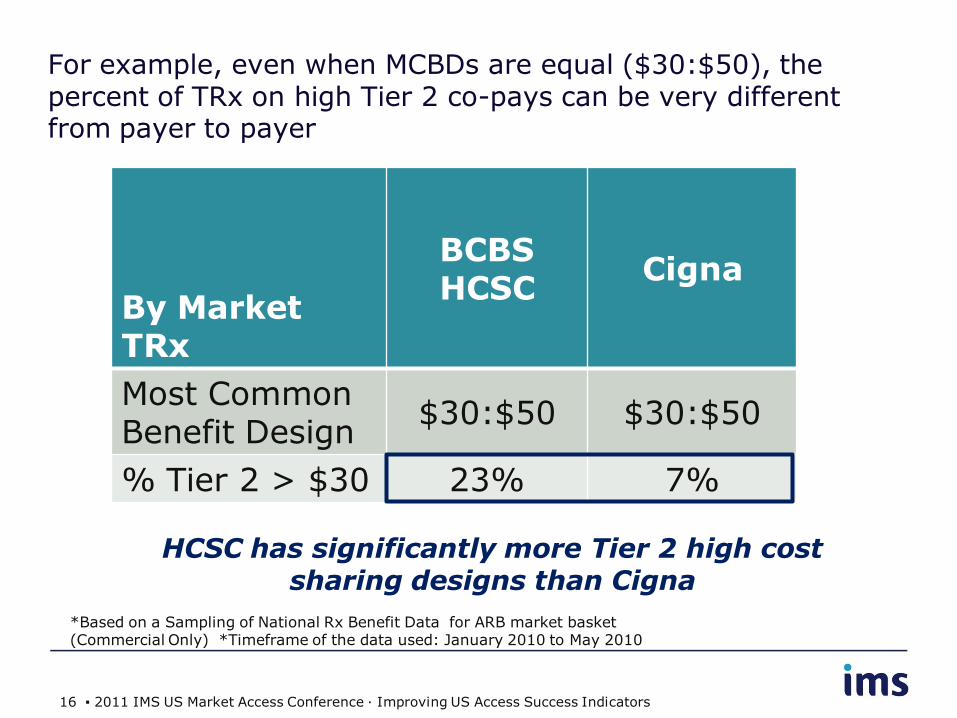

For example, even when MCBDs are equal ($30:$50), the percent of TRx on high Tier 2 co-pays can be very different from payer to payer

By Market TRx

BCBS HCSC

Cigna

Most Common Benefit Design

$30:$50 $30:$50

% Tier 2 > $30 23% 7%

HCSC has significantly more Tier 2 high cost sharing designs than Cigna

*Based on a Sampling of National Rx Benefit Data for ARB market basket (Commercial Only) *Timeframe of the data used: January 2010 to May 2010

16 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators

Assumption #2: The Price is Right

Fact #2

Fact #1

Tier 2 co-pay is $20-30

17 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators

Assumption #2: The Price is Right

Fact #1

Fact #2

Tier 2 co-pay is $20-30

Co-pay on Tier 2 varies significantly… …and so does Tier 3 co-pay

18 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators

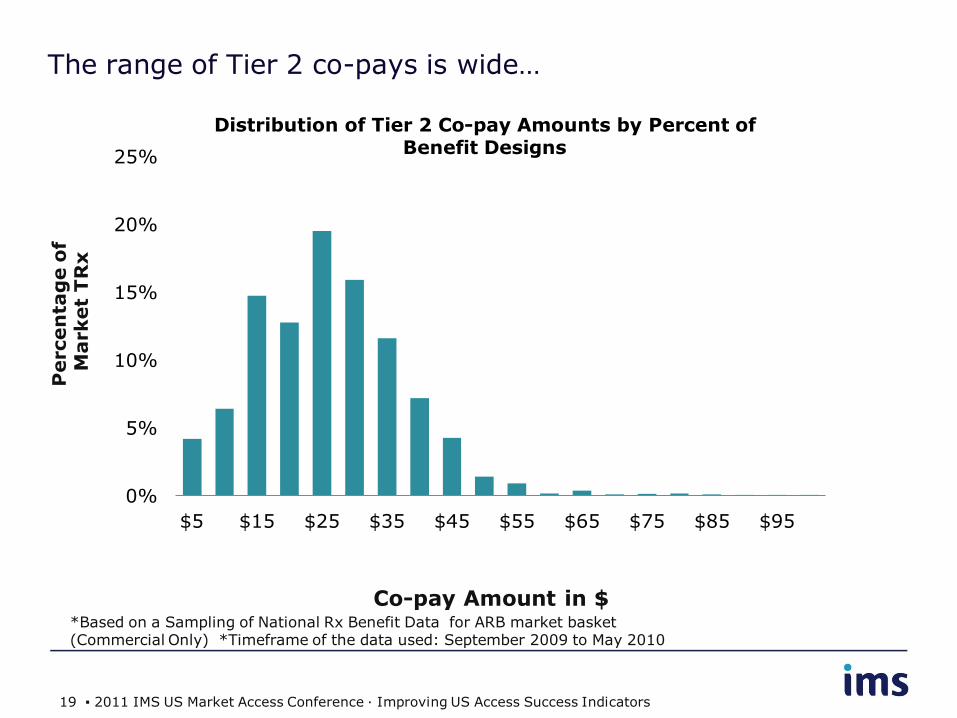

The range of Tier 2 co-pays is wide…

Co-pay Amount in $

0%

5%

10%

15%

20%

25%

$5 $15 $25 $35 $45 $55 $65 $75 $85 $95

Distribution of Tier 2 Co-pay Amounts by Percent of Benefit Designs

Percen

tag

e o

f M

arket

TR

x

*Based on a Sampling of National Rx Benefit Data for ARB market basket (Commercial Only) *Timeframe of the data used: September 2009 to May 2010

19 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators

…and overlaps significantly with Tier 3 Co-pays

Co-pay Amount in $

0%

5%

10%

15%

20%

25%

$5 $15 $25 $35 $45 $55 $65 $75 $85 $95

Distribution of Tier 2 and Tier 3 Co-pay Amounts by Percent of Benefit Designs

T2 Co-pay T3 Co-pay

Percen

tag

e o

f M

arket

TR

x

*Based on a Sampling of National Rx Benefit Data for ARB market basket (Commercial Only) *Timeframe of the data used: September 2009 to May 2010

20 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators

Assumption #2: The Price is Right

Fact #1

Fact #2

Tier 2 co-pay is less than Tier 3 co-pay

That’s true, but how much lower is it? Tiers 2 and 3 co-pay differentials vary markedly

21 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators

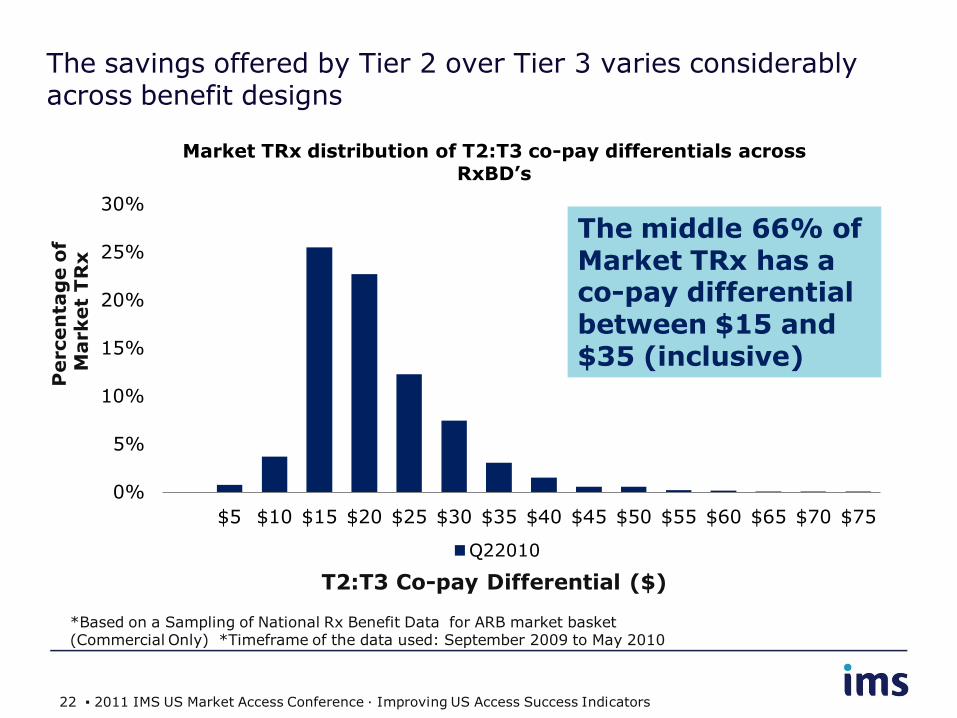

The savings offered by Tier 2 over Tier 3 varies considerably across benefit designs

0%

5%

10%

15%

20%

25%

30%

$5 $10 $15 $20 $25 $30 $35 $40 $45 $50 $55 $60 $65 $70 $75

Market TRx distribution of T2:T3 co-pay differentials across RxBD’s

Q22010

Percen

tag

e o

f M

arket

TR

x

T2:T3 Co-pay Differential ($)

The middle 66% of Market TRx has a co-pay differential between $15 and $35 (inclusive)

*Based on a Sampling of National Rx Benefit Data for ARB market basket (Commercial Only) *Timeframe of the data used: September 2009 to May 2010

22 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators

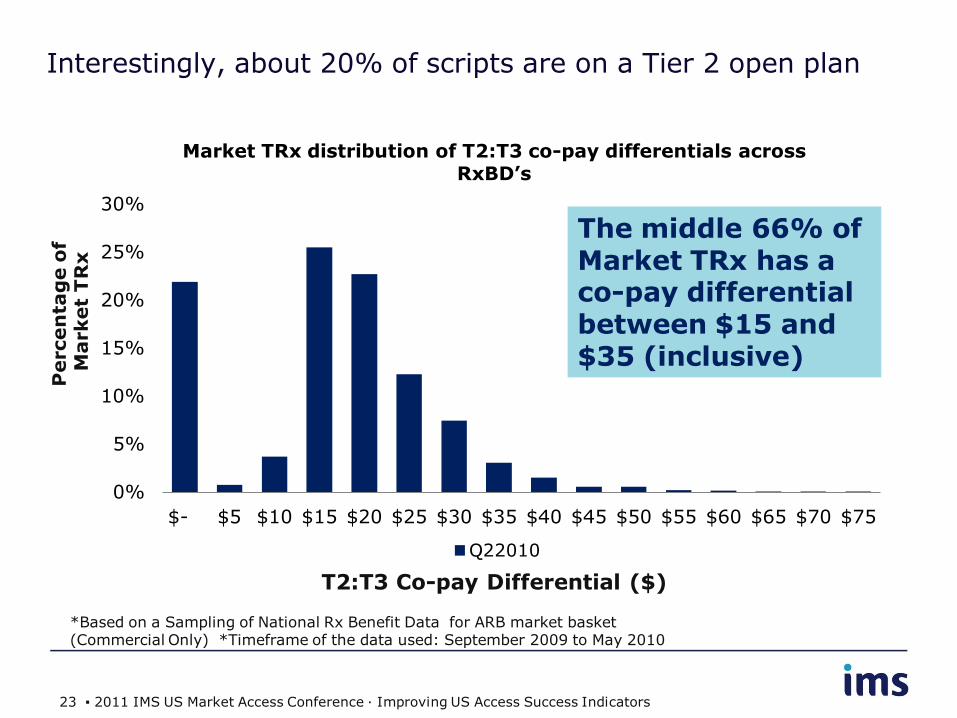

Interestingly, about 20% of scripts are on a Tier 2 open plan

0%

5%

10%

15%

20%

25%

30%

$- $5 $10 $15 $20 $25 $30 $35 $40 $45 $50 $55 $60 $65 $70 $75

Market TRx distribution of T2:T3 co-pay differentials across RxBD’s

Q22010

Percen

tag

e o

f M

arket

TR

x

T2:T3 Co-pay Differential ($)

*Based on a Sampling of National Rx Benefit Data for ARB market basket (Commercial Only) *Timeframe of the data used: September 2009 to May 2010

The middle 66% of Market TRx has a co-pay differential between $15 and $35 (inclusive)

23 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators

Assumption #3: Location, Location, Location

Benefit design varies geographically

Fact #1

24 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators

Assumption #3: Location, Location, Location

The assumption is true – there are important differences in benefit design across the US

Fact #1

Benefit design varies geographically

25 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators

Which US City (MSA) has the highest percentage of benefit designs with T2:T3 co-pay differentials

greater than or equal to $35?

Options A: Houston B: Detroit C: Atlanta D: Cleveland

26 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators

And the answer is… Atlanta

Atlanta has approximately 16% of scripts falling under

such a design

Which major US City (MSA) has the

highest percentage of benefit designs with T2:T3 co-pay

differentials greater than or equal to

$35?

27 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators

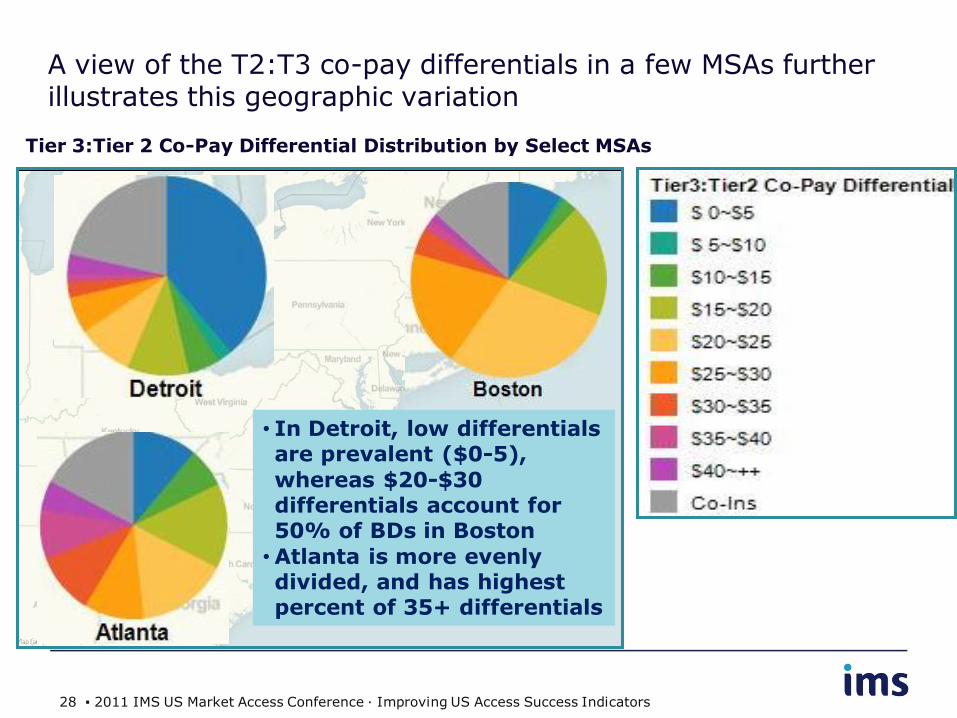

A view of the T2:T3 co-pay differentials in a few MSAs further illustrates this geographic variation

• In Detroit, low differentials are prevalent ($0-5),

whereas $20-$30 differentials account for 50% of BDs in Boston

• Atlanta is more evenly divided, and has highest percent of 35+ differentials

Tier 3:Tier 2 Co-Pay Differential Distribution by Select MSAs

28 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators

So What?

29 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators

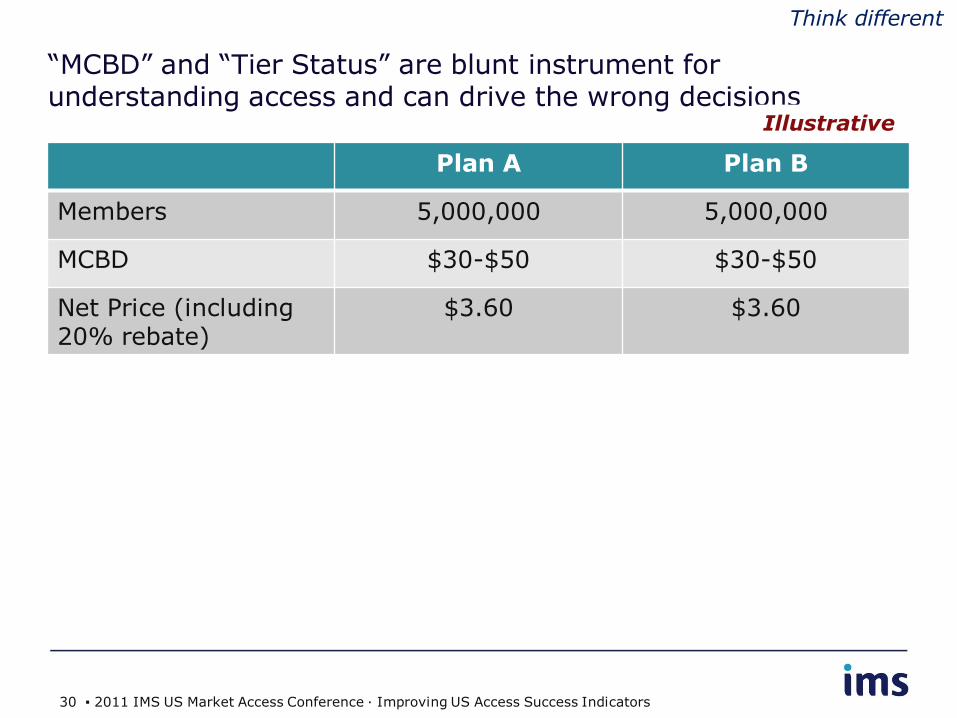

“MCBD” and “Tier Status” are blunt instrument for understanding access and can drive the wrong decisions

Plan A Plan B

Members 5,000,000 5,000,000

MCBD $30-$50 $30-$50

Net Price (including 20% rebate)

$3.60 $3.60

Illustrative

Think different

30 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators

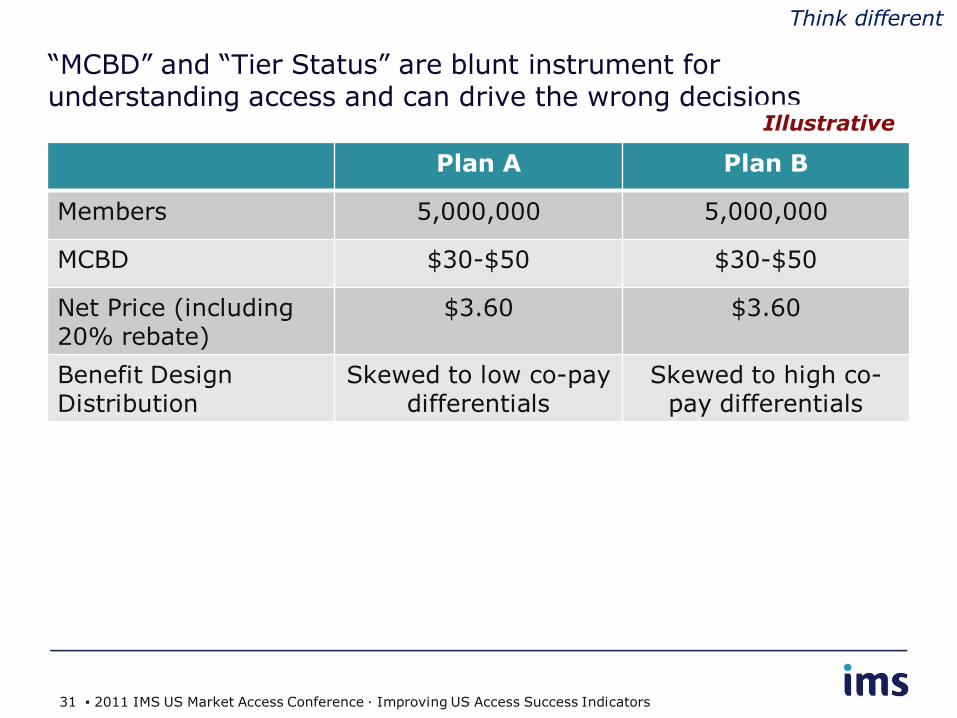

“MCBD” and “Tier Status” are blunt instrument for understanding access and can drive the wrong decisions

Plan A Plan B

Members 5,000,000 5,000,000

MCBD $30-$50 $30-$50

Net Price (including 20% rebate)

$3.60 $3.60

Benefit Design Distribution

Skewed to low co-pay differentials

Skewed to high co-pay differentials

Illustrative

Think different

31 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators

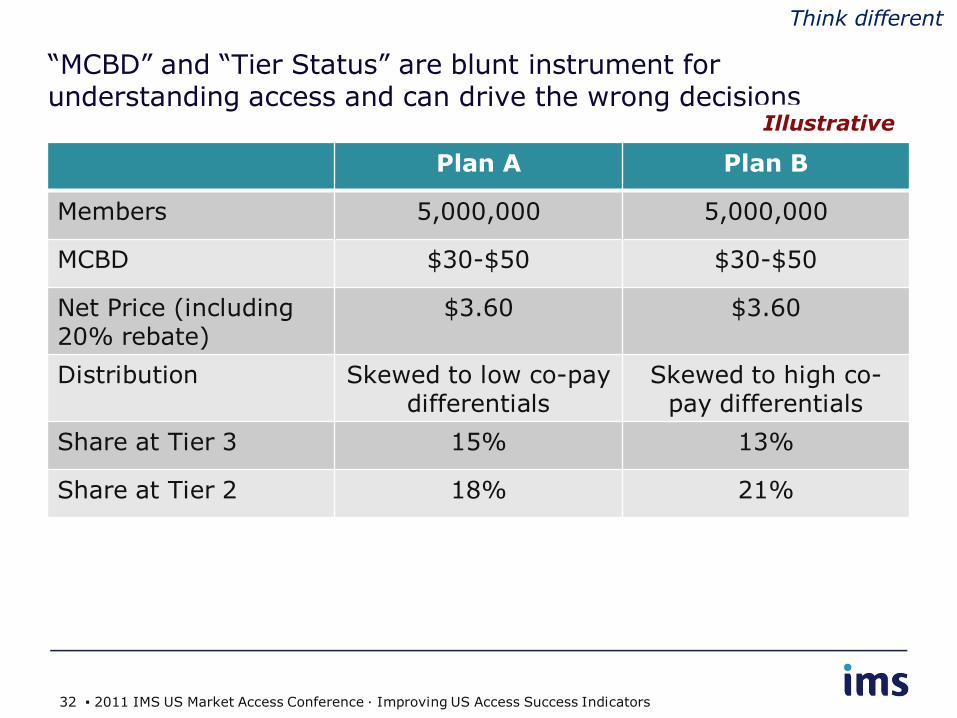

“MCBD” and “Tier Status” are blunt instrument for understanding access and can drive the wrong decisions

Plan A Plan B

Members 5,000,000 5,000,000

MCBD $30-$50 $30-$50

Net Price (including 20% rebate)

$3.60 $3.60

Distribution Skewed to low co-pay differentials

Skewed to high co-pay differentials

Share at Tier 3 15% 13%

Share at Tier 2 18% 21%

Illustrative

Think different

32 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators

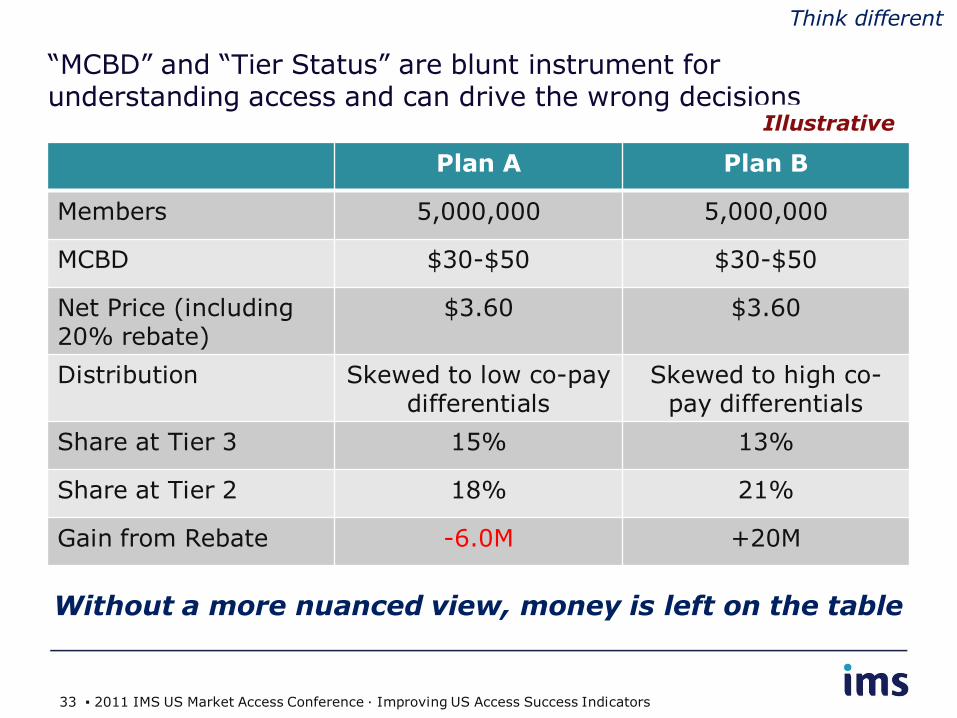

“MCBD” and “Tier Status” are blunt instrument for understanding access and can drive the wrong decisions

Plan A Plan B

Members 5,000,000 5,000,000

MCBD $30-$50 $30-$50

Net Price (including 20% rebate)

$3.60 $3.60

Distribution Skewed to low co-pay differentials

Skewed to high co-pay differentials

Share at Tier 3 15% 13%

Share at Tier 2 18% 21%

Gain from Rebate -6.0M +20M

Without a more nuanced view, money is left on the table

Illustrative

Think different

33 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators

Set & Communicate Access Objectives Differently

• Have you set thresholds for Tier 2?

• Is your threshold appropriate for your product?

− Absolute co-pay level

− Co-pay differential

− Tailored to geography

• Are you effectively applying other co-pay

levers?

Do not contract

Co-pay Differential

Ab

solu

te

Tie

r 2

Co-

pay

Move from “Tier 2 or Bust”

To “Strategic Investment in T2”

Low High

Low

High

1

Act different

34 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators

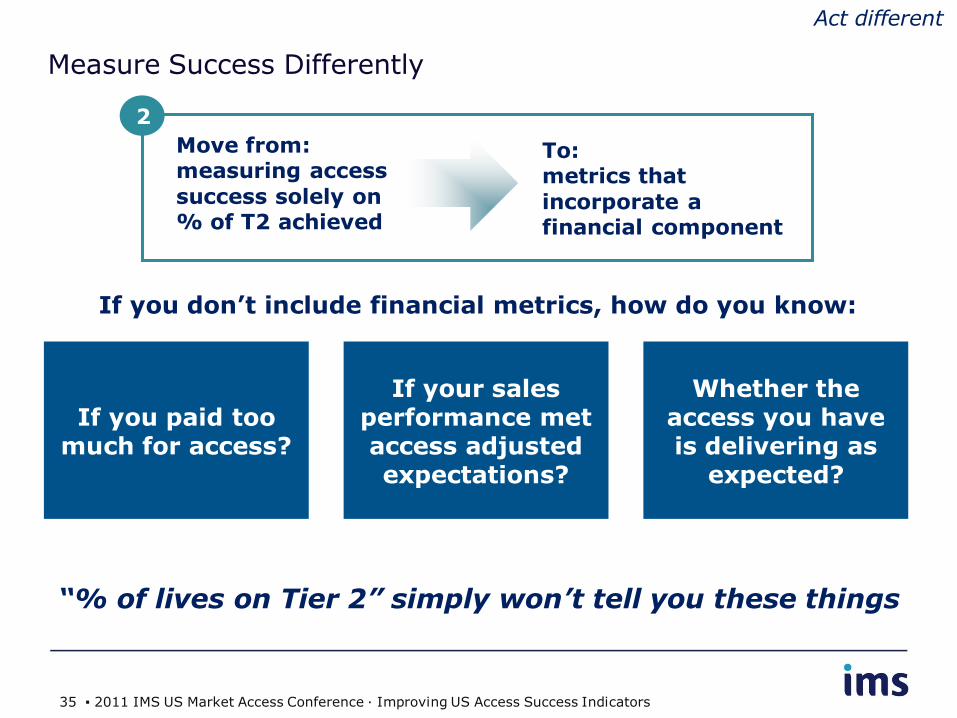

Measure Success Differently

“% of lives on Tier 2” simply won’t tell you these things

If you don’t include financial metrics, how do you know:

If you paid too much for access?

If your sales performance met access adjusted expectations?

Whether the access you have is delivering as

expected?

2

Move from: measuring access

success solely on % of T2 achieved

To: metrics that

incorporate a financial component

Act different

35 ▪ 2011 IMS US Market Access Conference ∙ Improving US Access Success Indicators