important caveats in technical analysisimportant … · important caveats in technical...

TRANSCRIPT

Important Caveats in Technical AnalysisImportant Caveats in Technical AnalysisAn Introduction to Risk-Opportunity Analysis

http://ralphvince comhttp://ralphvince.com

Tampa 2 Day Course, “Risk-Opportunity Analysis”Tampa 2 Day Course, Risk Opportunity Analysis

November 13-14, 2010:

http://rvincetampa201011 eventbrite com/http://rvincetampa201011.eventbrite.com/

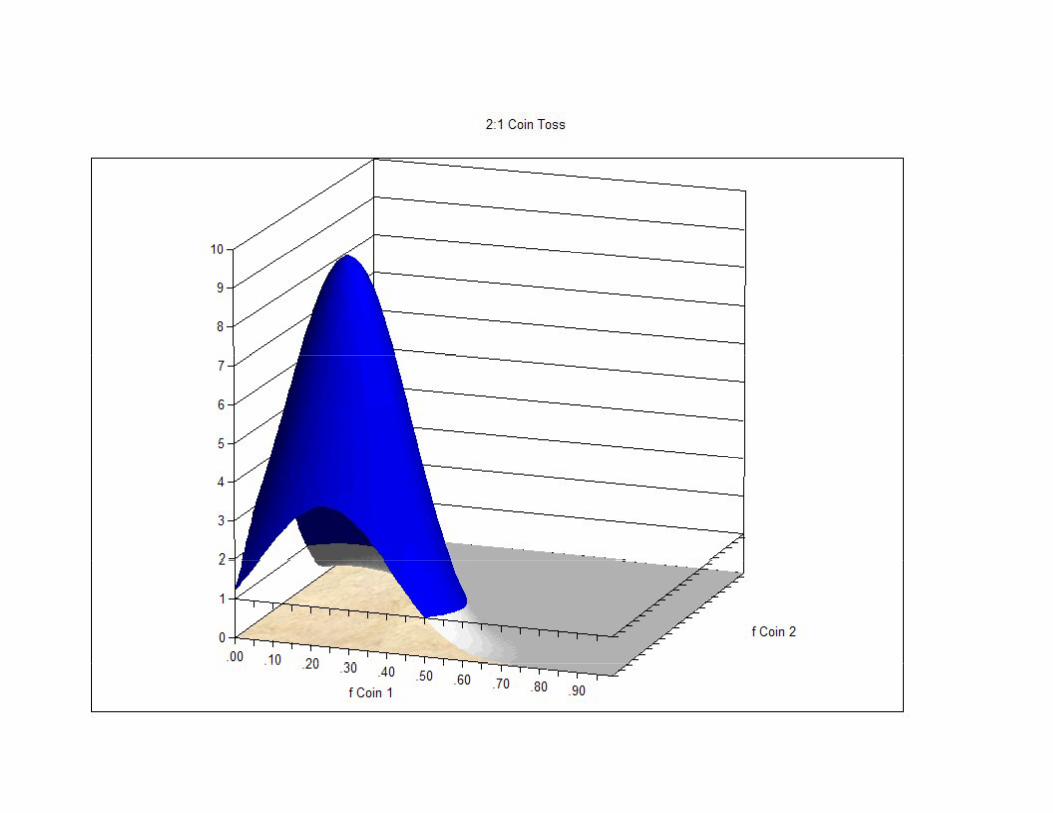

The distribution can be made into bins. A scenario is a bin. It has a probability and An outcome (P/L)

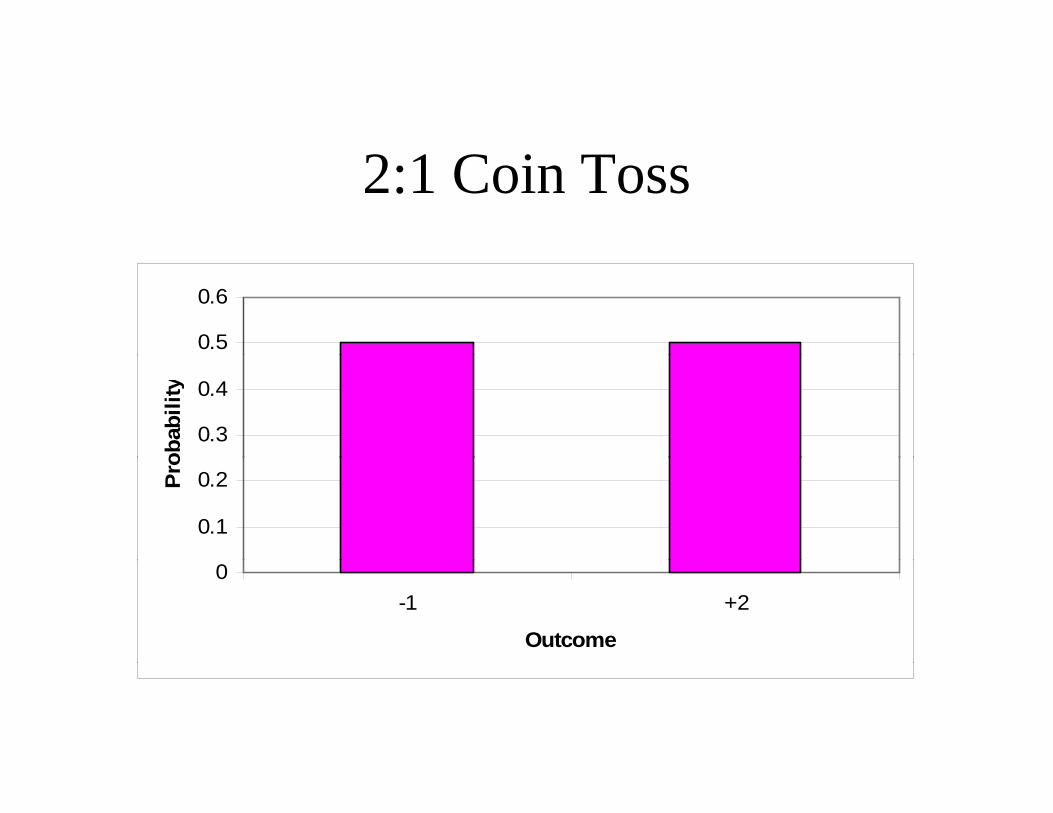

2:1 Coin Toss

0.5

0.6

0.3

0.4

obab

ility

0.1

0.2Pro

0-1 +2

Outcome

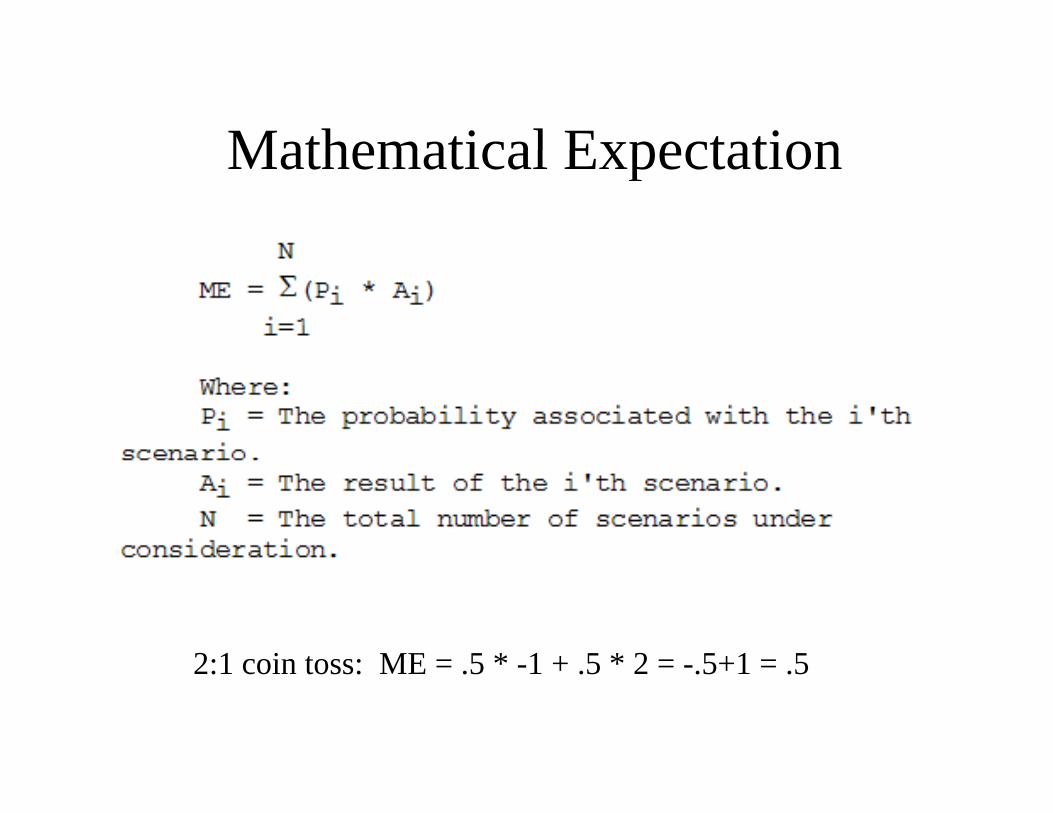

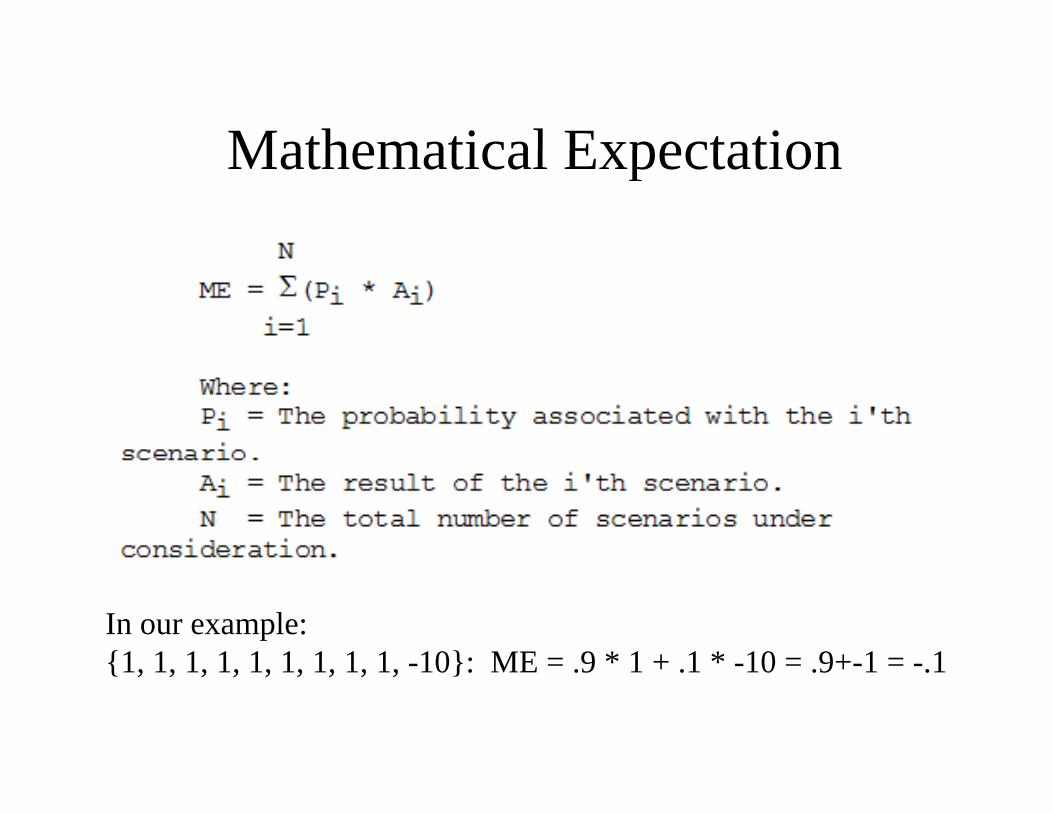

Mathematical ExpectationMathematical Expectation

2:1 coin toss: ME = 5 * 1 + 5 * 2 = 5+1 = 52:1 coin toss: ME = .5 * -1 + .5 * 2 = -.5+1 = .5

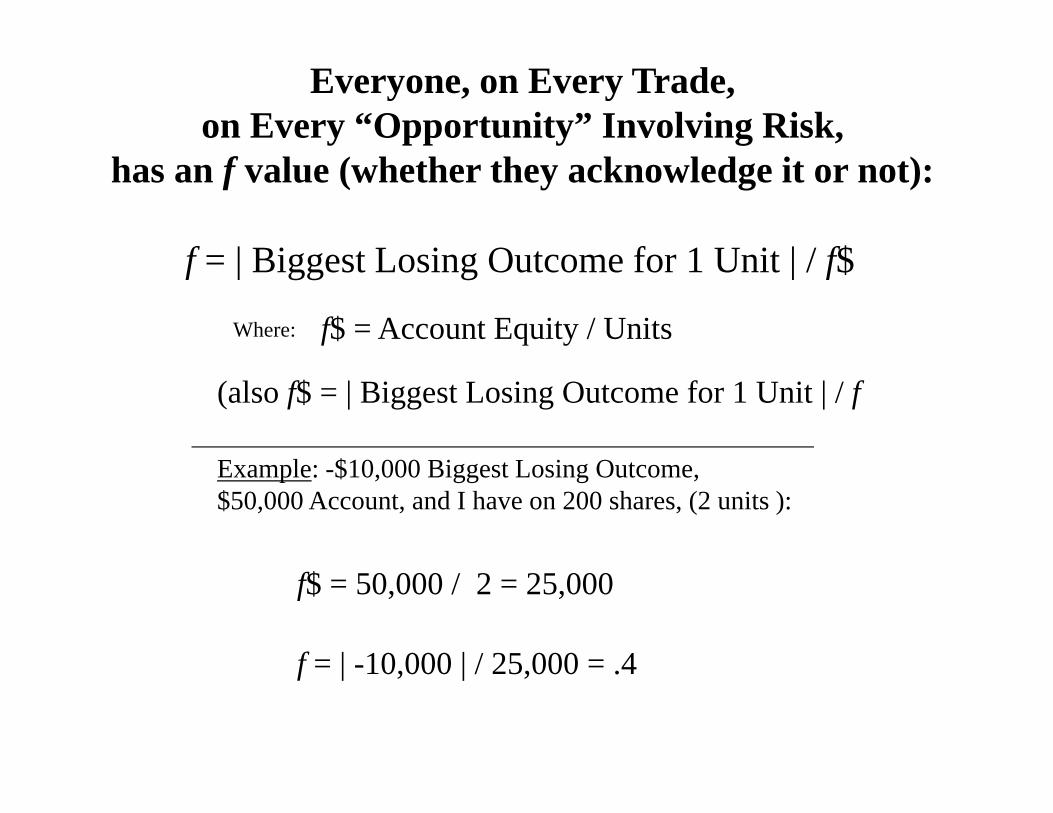

Everyone, on Every Trade, on Every “Opportunity” Involving Risk,

f | Bi t L i O t f 1 U it | / f$

has an f value (whether they acknowledge it or not):

f = | Biggest Losing Outcome for 1 Unit | / f$

f$ = Account Equity / UnitsWhere:

(also f$ = | Biggest Losing Outcome for 1 Unit | / f

Example: -$10,000 Biggest Losing Outcome, $50,000 Account, and I have on 200 shares, (2 units ):

f$ = 50,000 / 2 = 25,000

f = | 10 000 | / 25 000 = 4f = | -10,000 | / 25,000 = .4

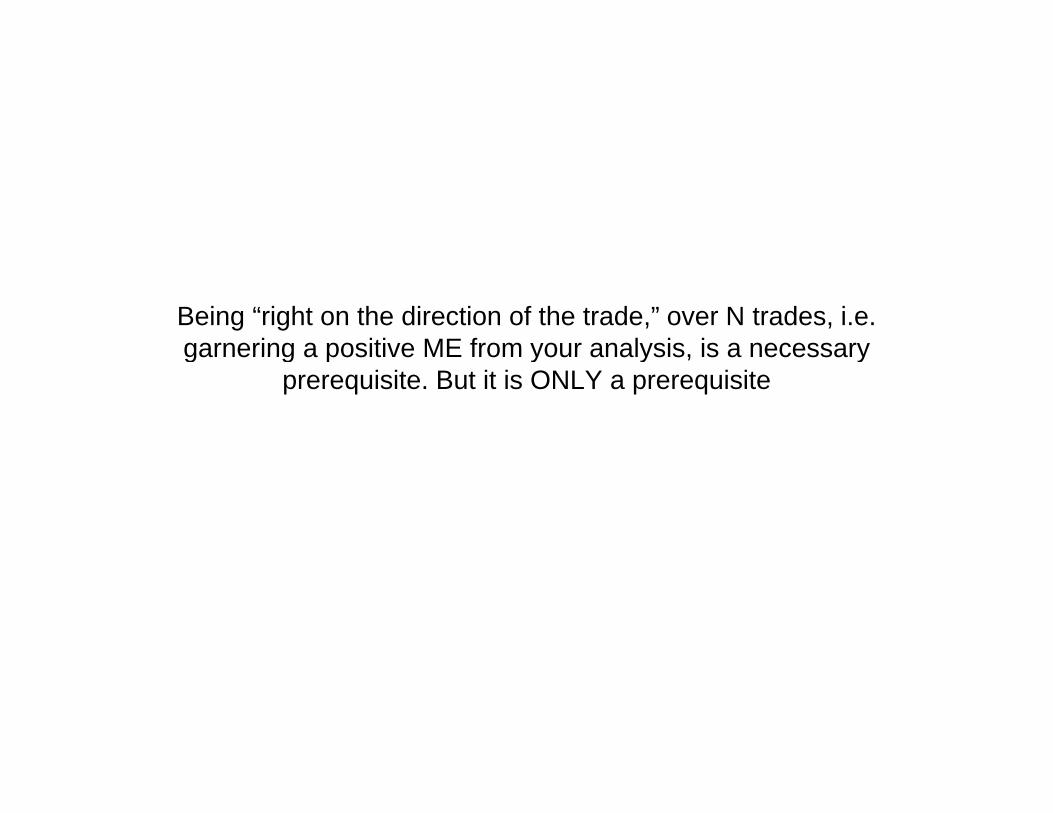

Being “right on the direction of the trade,” over N trades, i.e. garnering a positive ME from your analysis, is a necessarygarnering a positive ME from your analysis, is a necessary

prerequisite. But it is ONLY a prerequisite

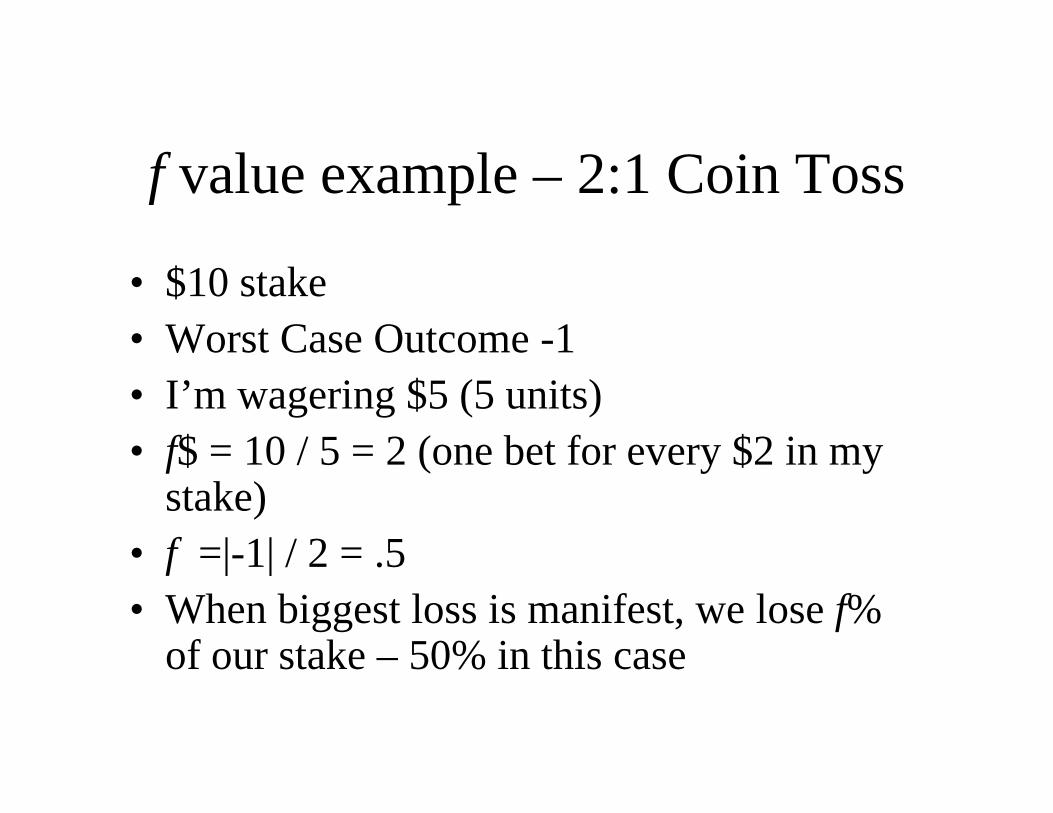

f value example – 2:1 Coin Toss

• $10 stake• Worst Case Outcome -1• I’m wagering $5 (5 units)• f$ = 10 / 5 = 2 (one bet for every $2 in myf$ 10 / 5 2 (one bet for every $2 in my

stake)• f =|-1| / 2 = 5f | 1| / 2 .5• When biggest loss is manifest, we lose f%

of our stake – 50% in this caseof our stake 50% in this case

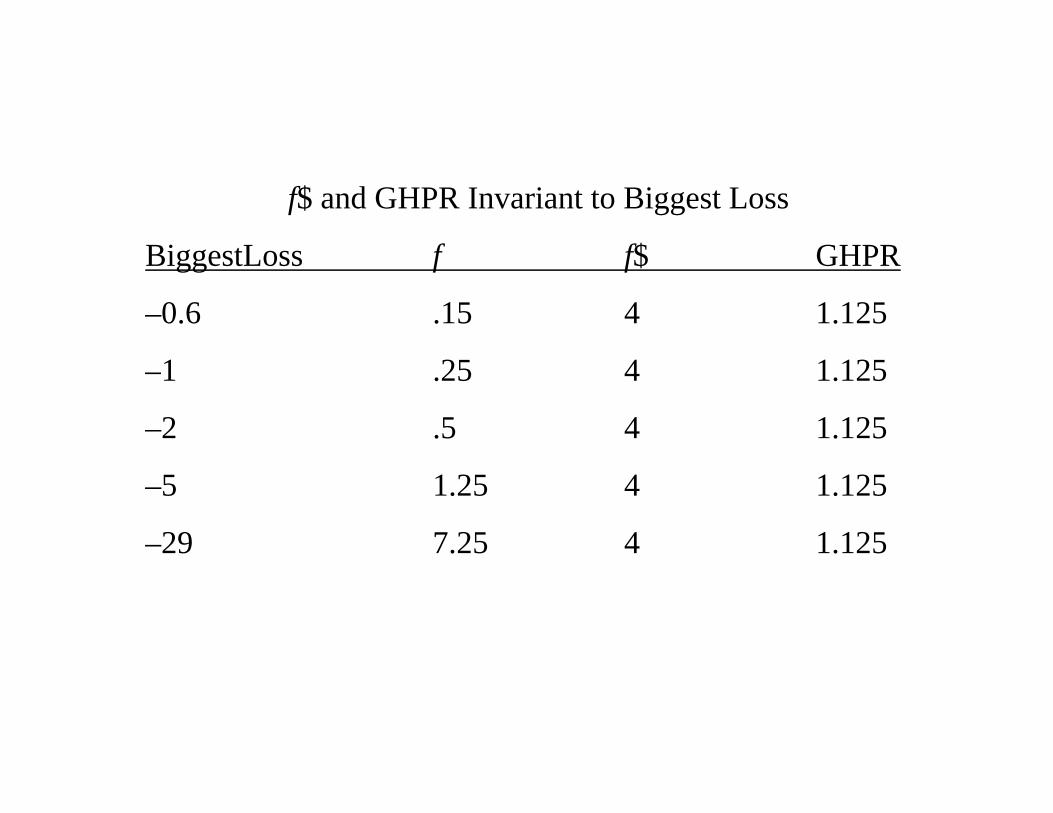

f$ and GHPR Invariant to Biggest Loss

BiggestLoss f f$ GHPRBiggestLoss f f$ GHPR

–0.6 .15 4 1.125

–1 .25 4 1.125

–2 .5 4 1.125

–5 1.25 4 1.125

–29 7.25 4 1.125

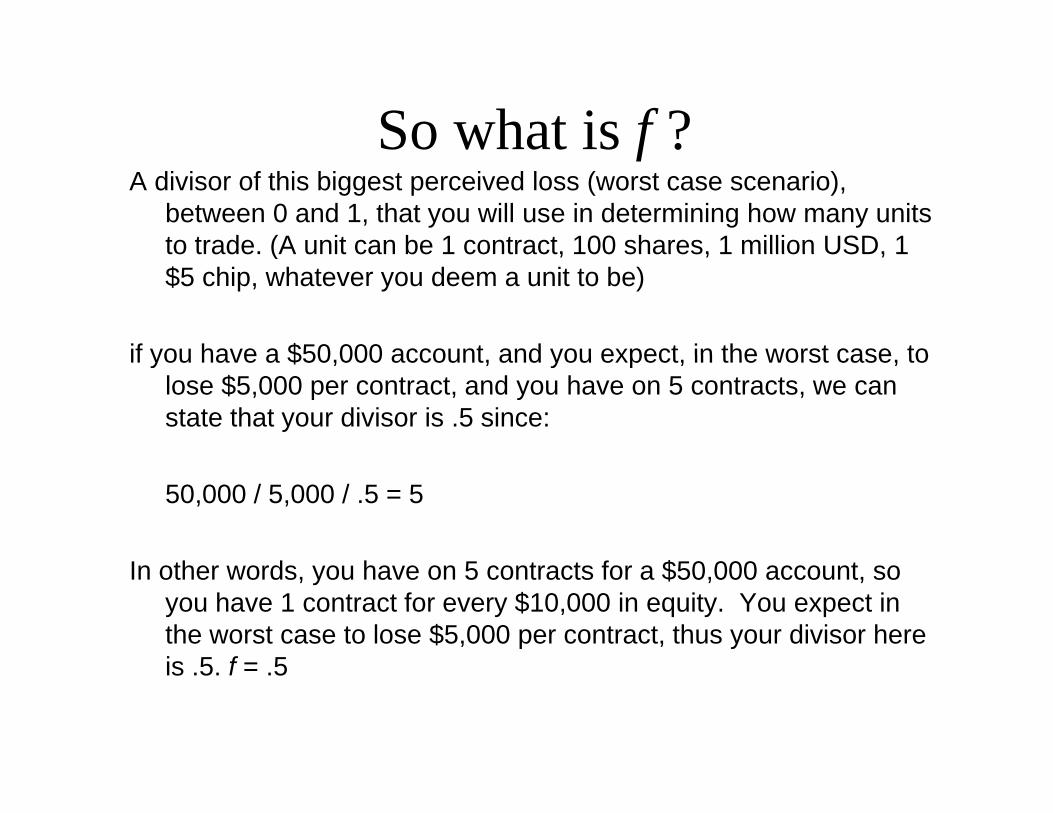

So what is f ?fA divisor of this biggest perceived loss (worst case scenario),

between 0 and 1, that you will use in determining how many units to trade. (A unit can be 1 contract, 100 shares, 1 million USD, 1to trade. (A unit can be 1 contract, 100 shares, 1 million USD, 1 $5 chip, whatever you deem a unit to be)

if you have a $50 000 account and you expect in the worst case toif you have a $50,000 account, and you expect, in the worst case, to lose $5,000 per contract, and you have on 5 contracts, we can state that your divisor is .5 since:

50,000 / 5,000 / .5 = 5

f $ 0 000In other words, you have on 5 contracts for a $50,000 account, so you have 1 contract for every $10,000 in equity. You expect in the worst case to lose $5,000 per contract, thus your divisor here is 5 f = 5is .5. f = .5

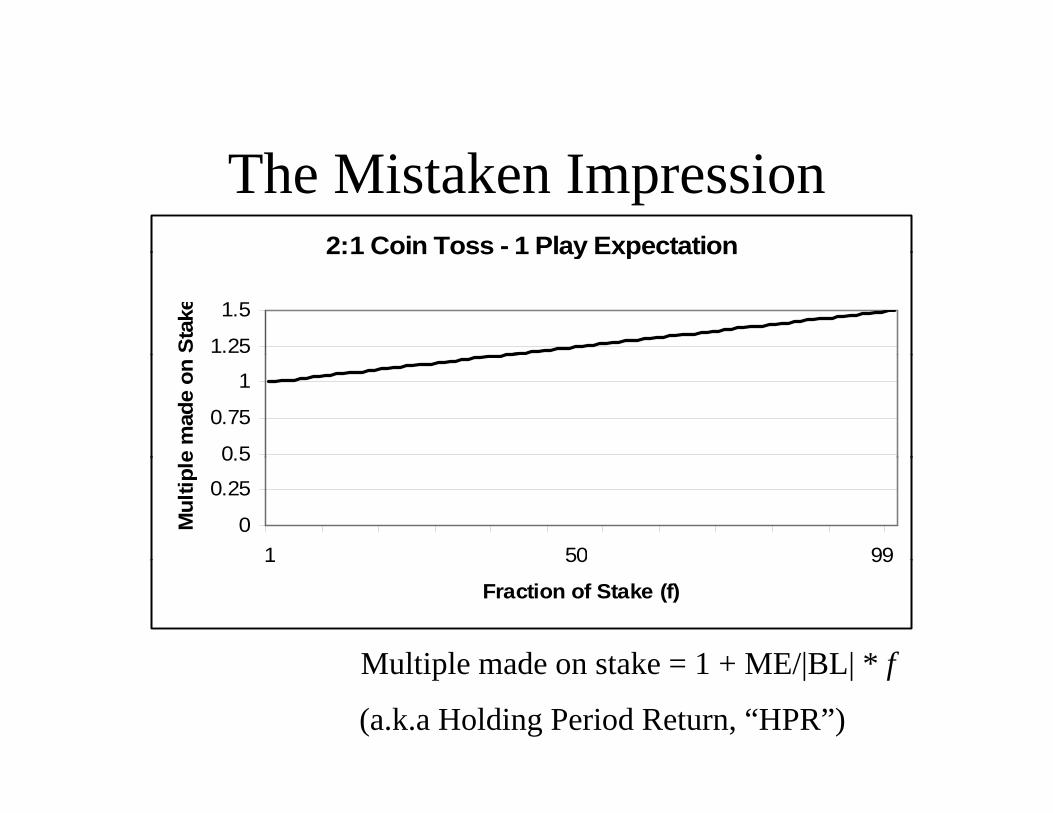

The Mistaken Impression2:1 Coin Toss - 1 Play Expectation2:1 Coin Toss 1 Play Expectation

1.25

1.5

Stak

e

0 5

0.75

1

e m

ade

on

0

0.25

0.5

1 50 99

Mul

tiple

1 50 99

Fraction of Stake (f)

Multiple made on stake = 1 + ME/|BL| * fMultiple made on stake = 1 + ME/|BL| * f

(a.k.a Holding Period Return, “HPR”)

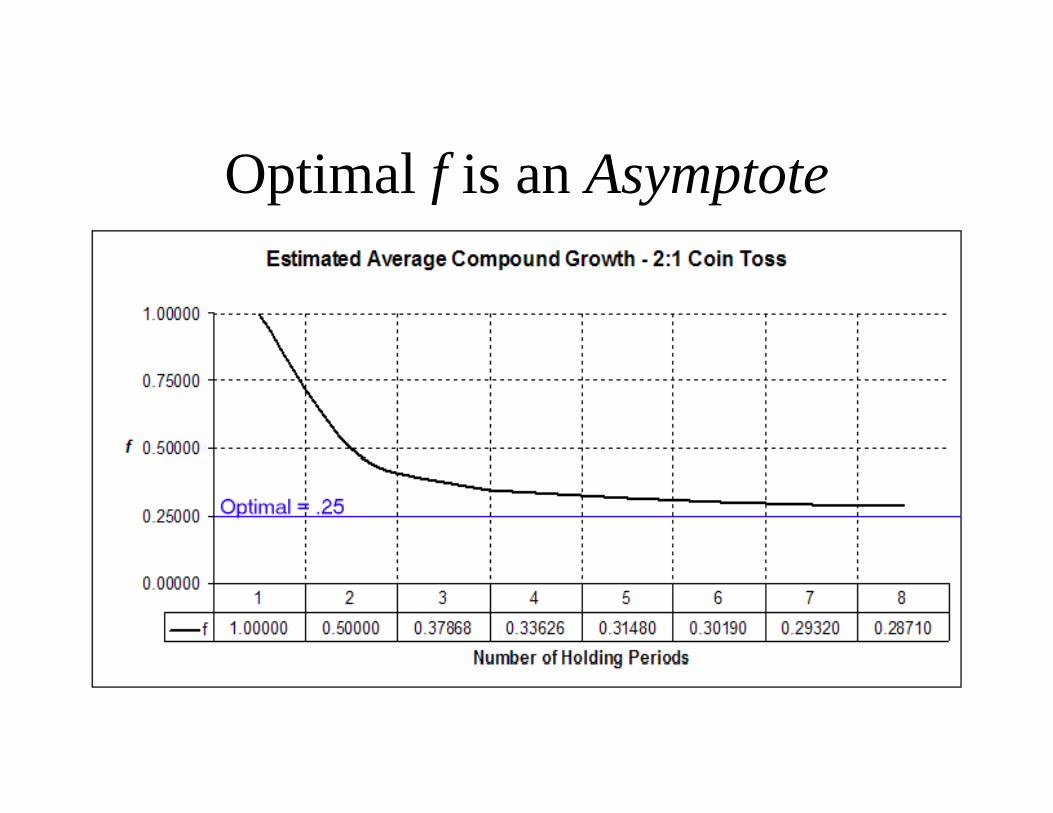

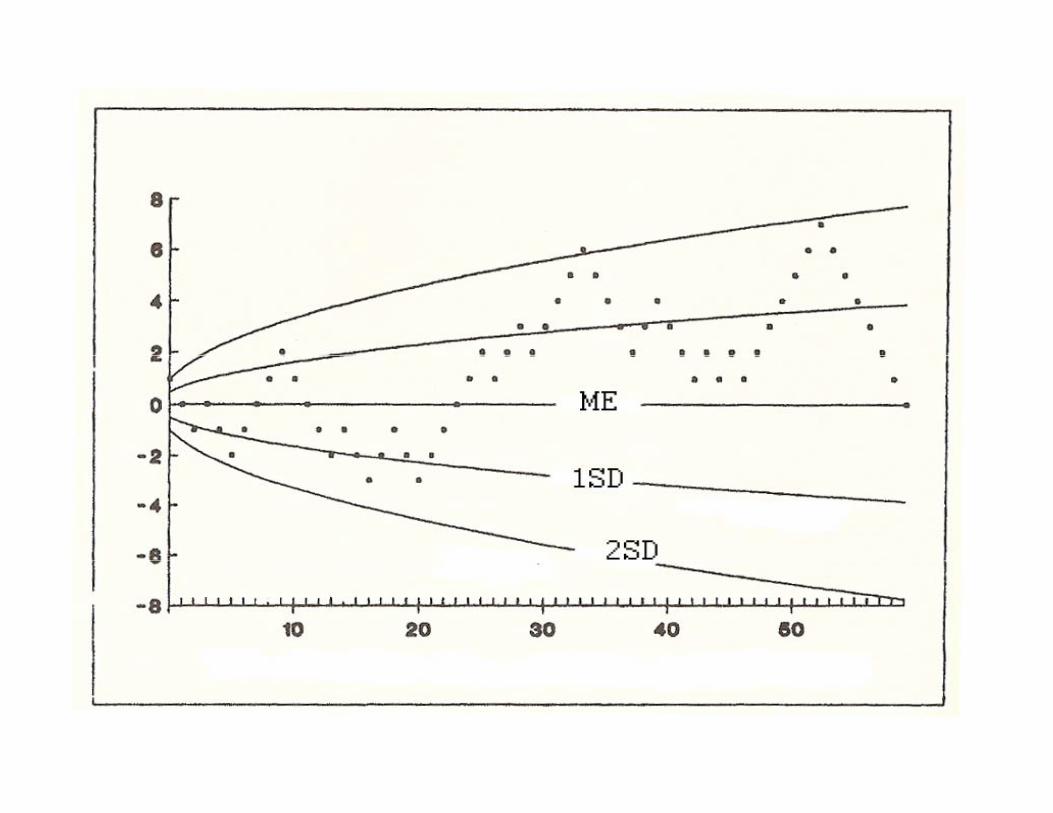

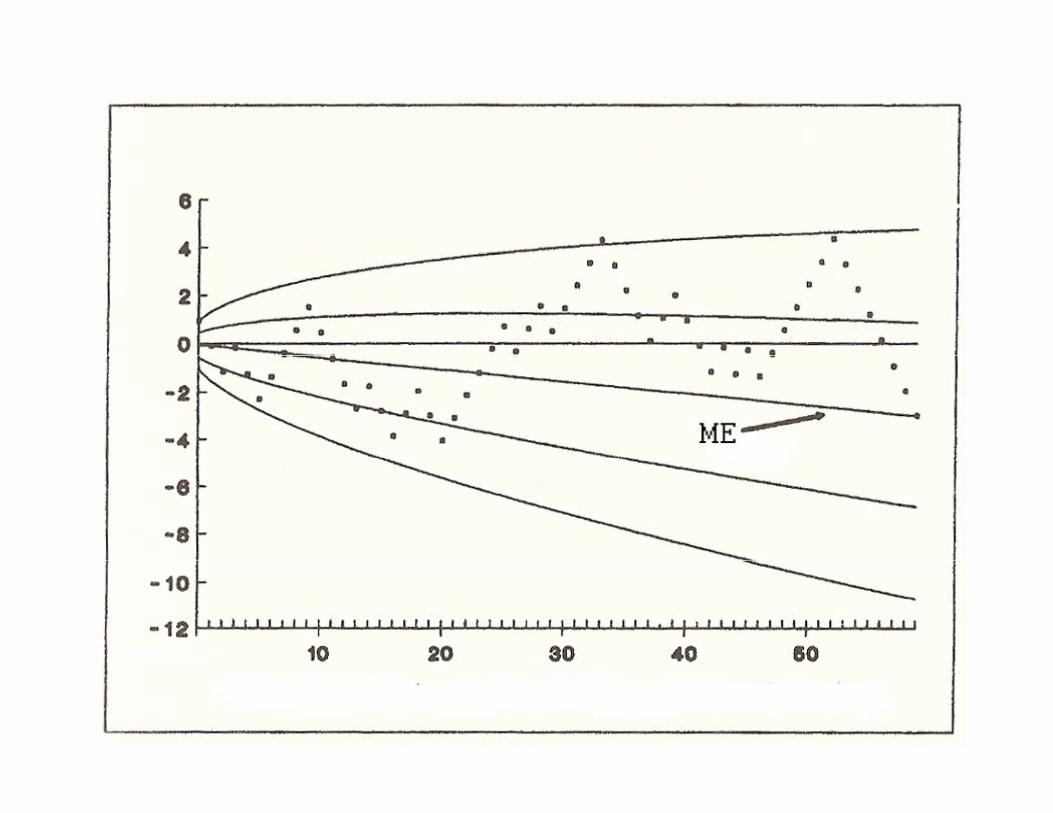

Optimal f is an Asymptote

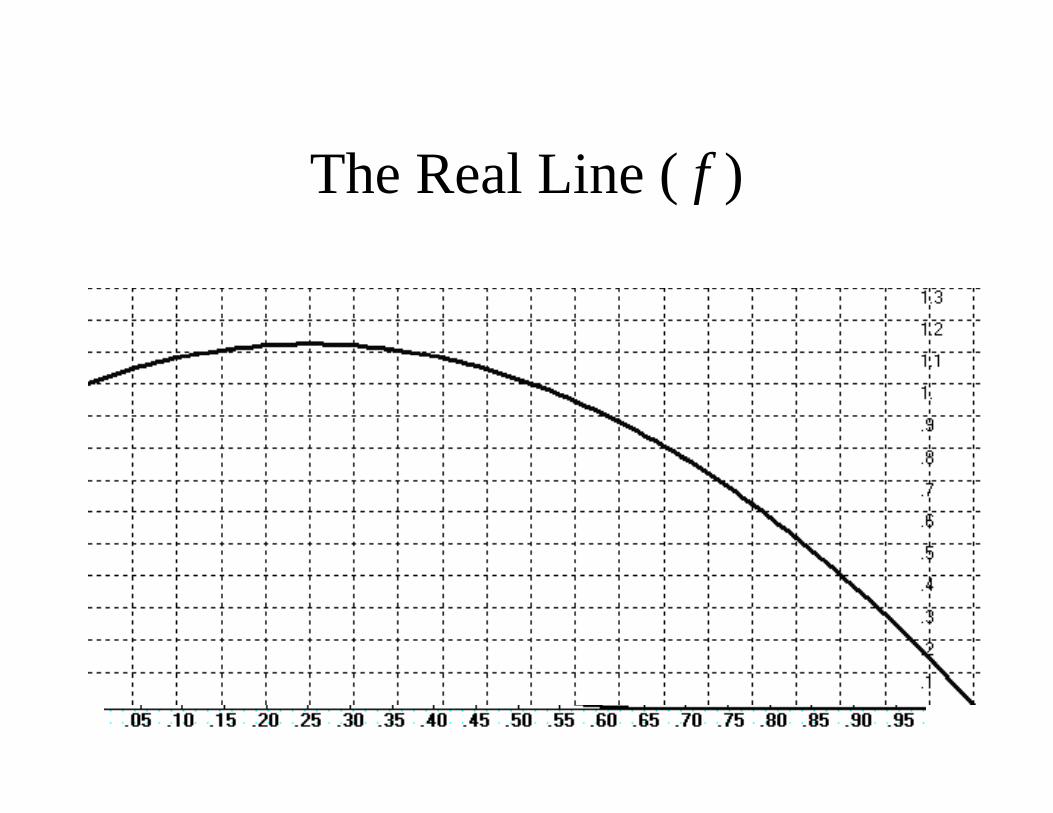

The Real Line ( f )

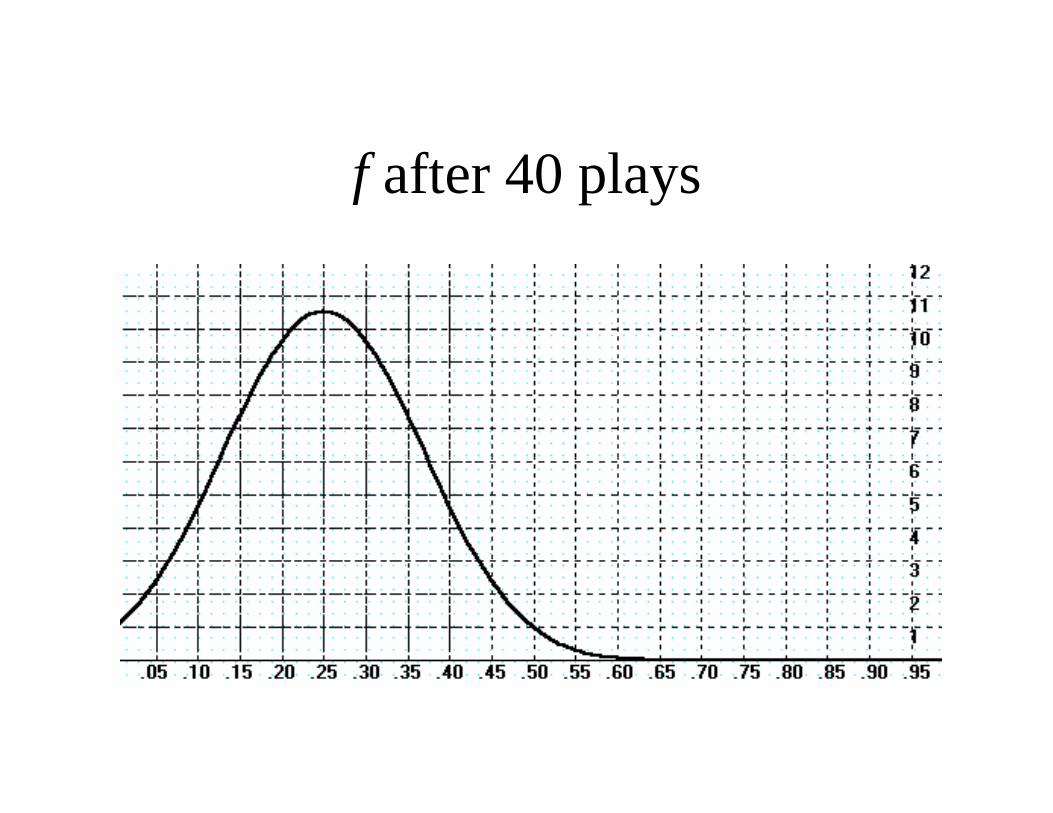

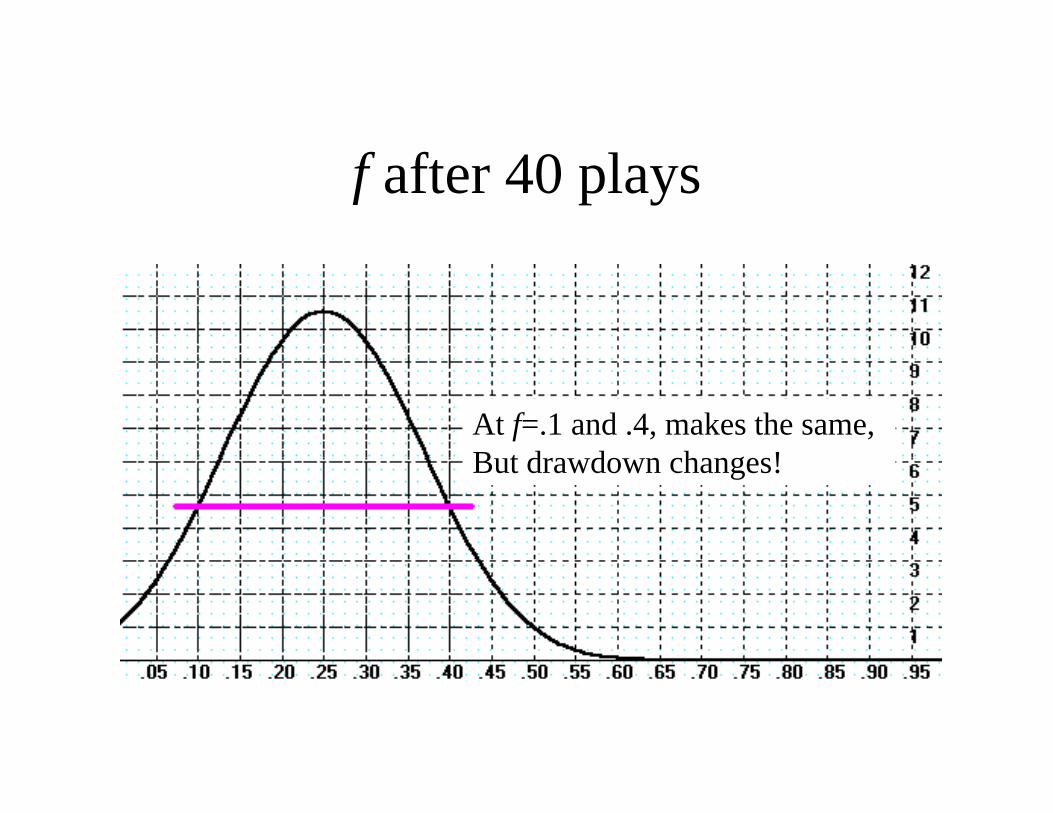

f after 40 plays

f after 40 plays

40 Plays

1 Play1 Play

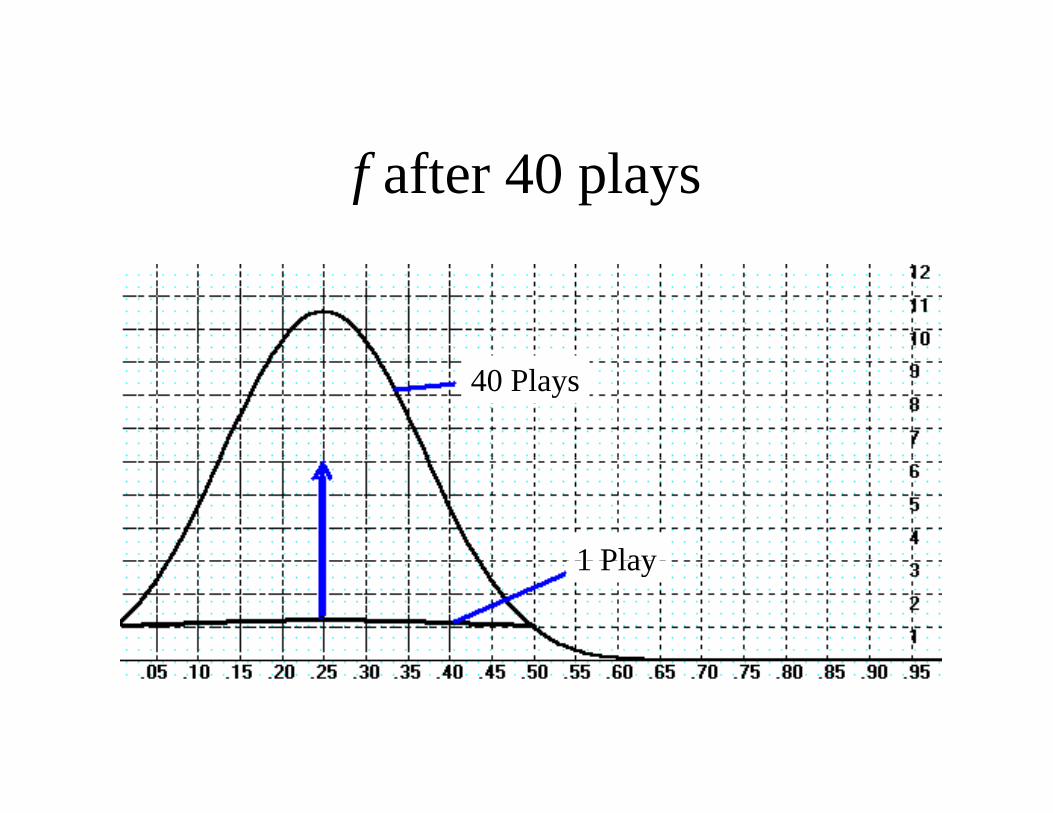

f after 40 plays

At .15 and .40, makes the same, but drawdown changesAt f=.1 and .4, makes the same,B t d d h !But drawdown changes!

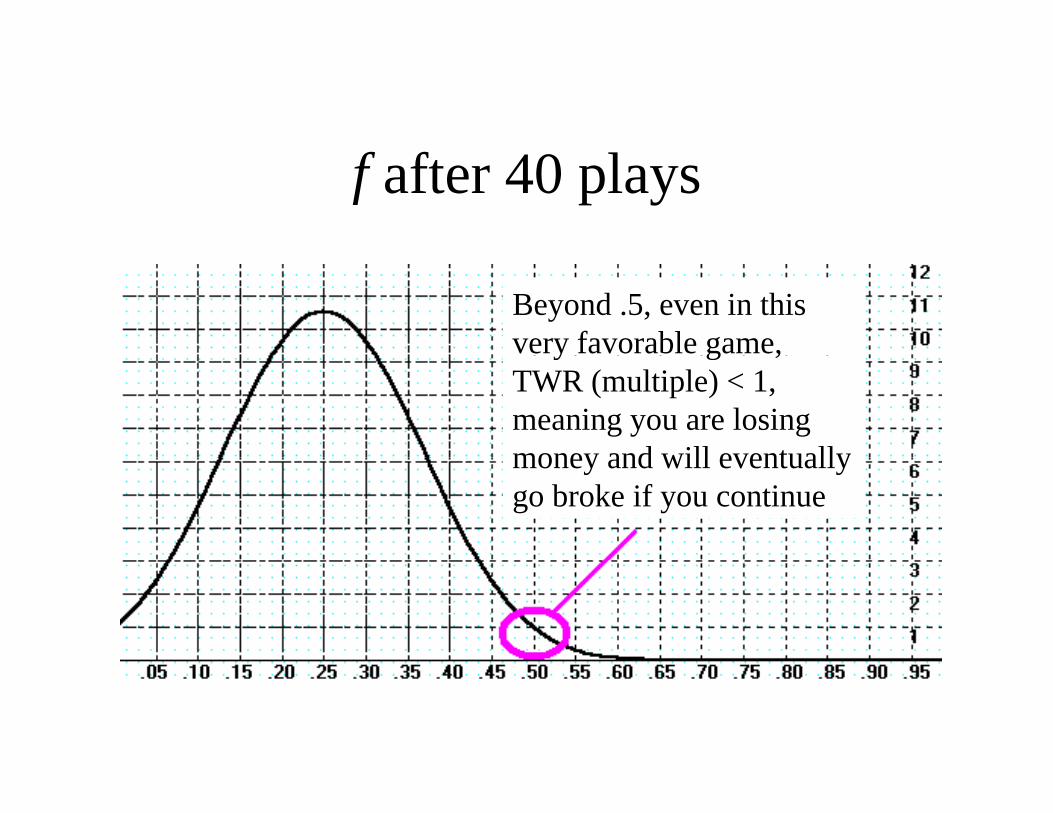

f after 40 plays

Beyond .5, even in thisvery favorable game, y g ,TWR (multiple) < 1,meaning you are losing money and will eventuallymoney and will eventuallygo broke if you continue

f after 40 plays

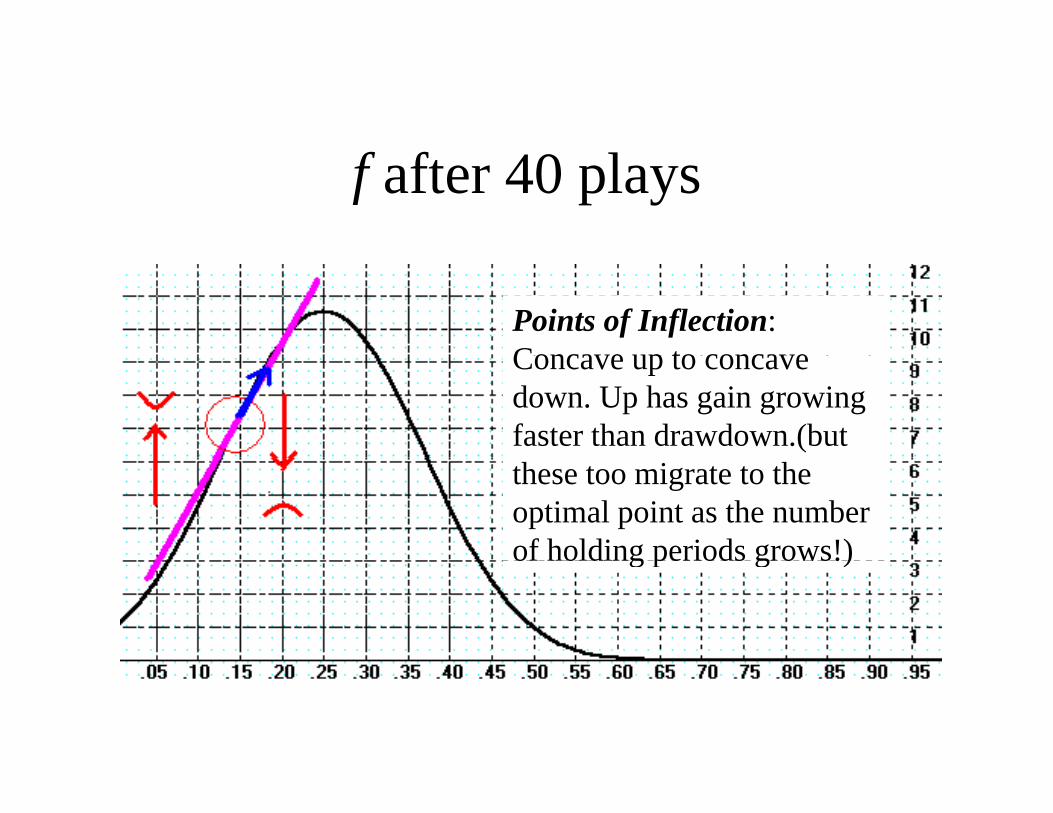

Points of Inflection:Concave up to concaveConcave up to concave down. Up has gain growing faster than drawdown.(but these too migrate to the optimal point as the number of holding periods grows!)of holding periods grows!)

f after 40 plays

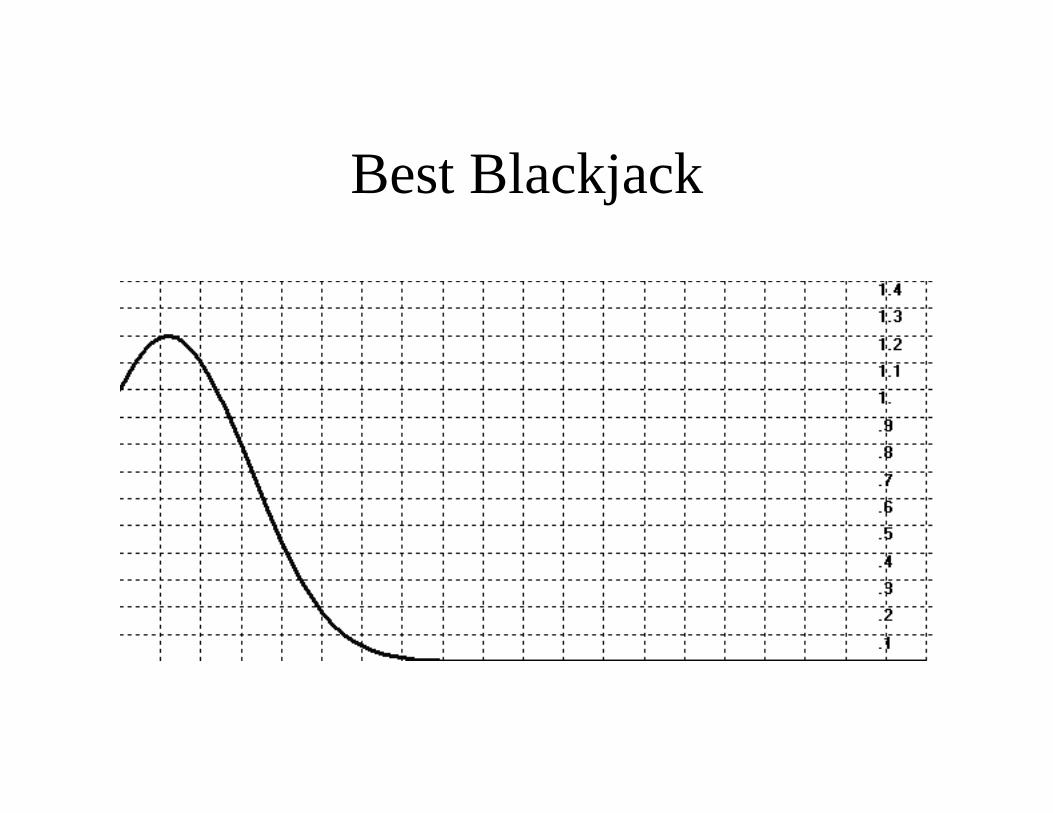

Best Blackjack

Leverage has 2 Axes – 2 FacetsThe instant caseThe instant case of how much I amlevered up

f

How I progress myquantity with respect

f

quantity with respectto time / equity changes

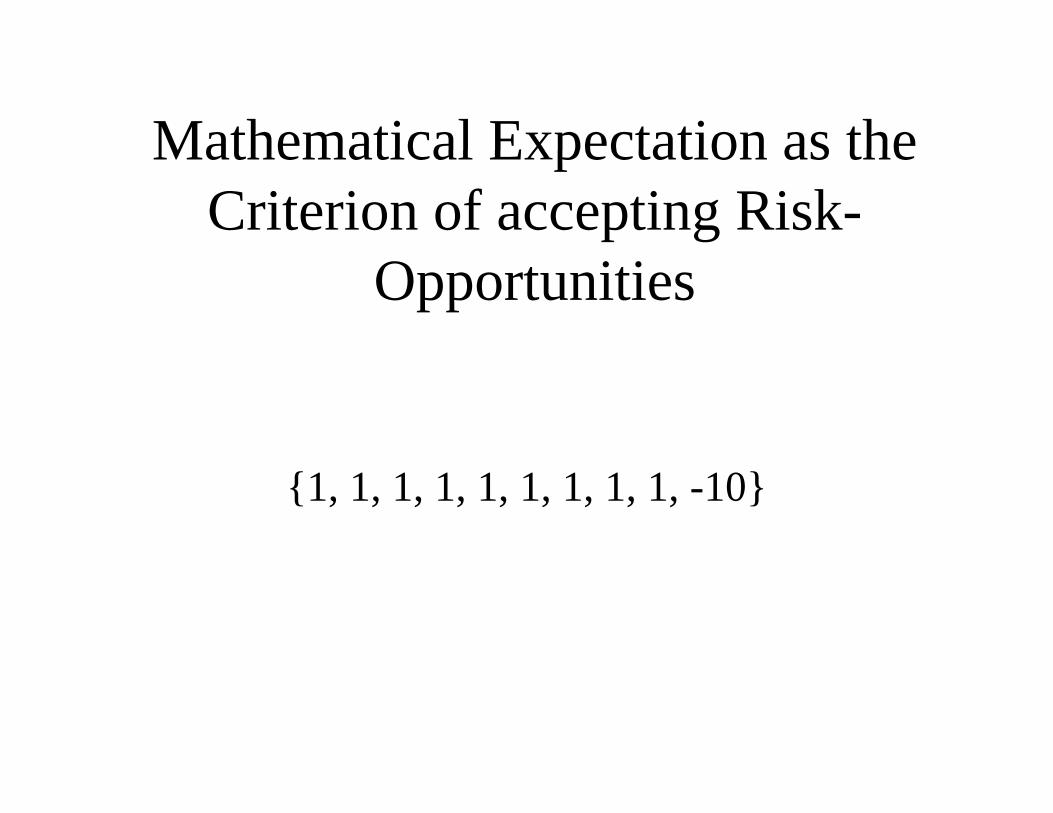

Mathematical Expectation as theMathematical Expectation as the Criterion of accepting Risk-

Opportunities

{1, 1, 1, 1, 1, 1, 1, 1, 1, -10}

Mathematical ExpectationMathematical Expectation

In our example:{1 1 1 1 1 1 1 1 1 10}: ME = 9 * 1 + 1 * 10 = 9+ 1 = 1{1, 1, 1, 1, 1, 1, 1, 1, 1, -10}: ME = .9 * 1 + .1 * -10 = .9+-1 = -.1

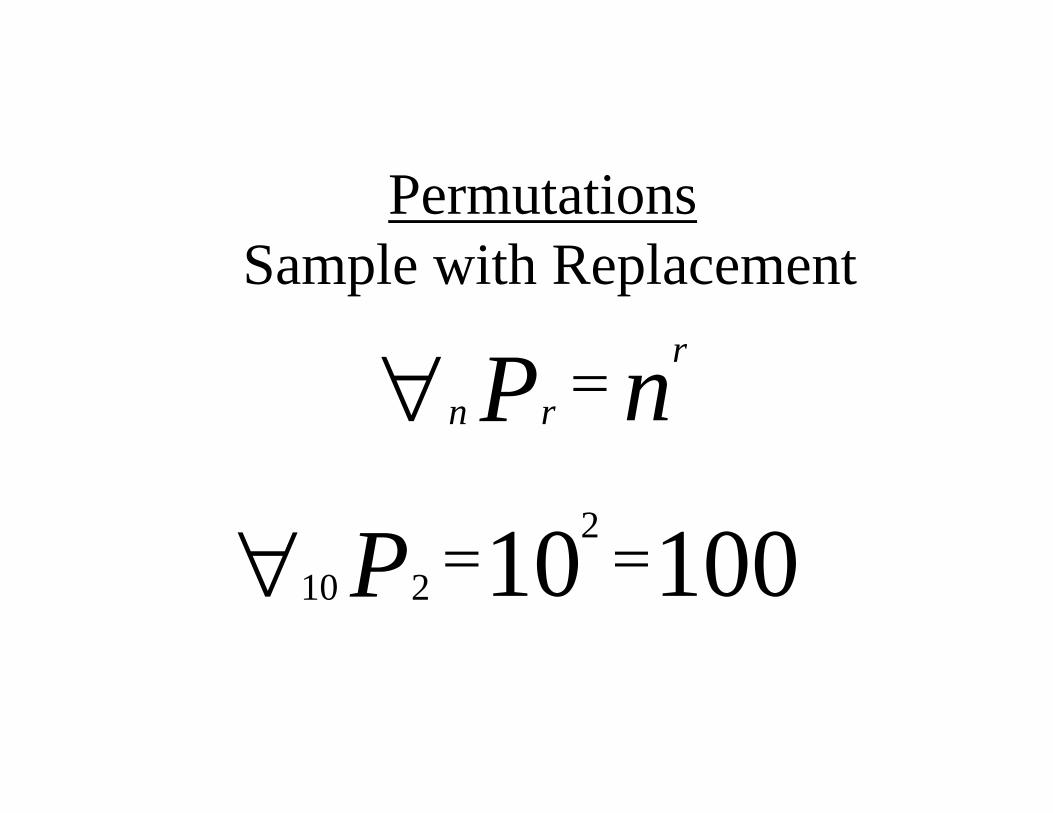

Permutations S l ith R l tSample with Replacement

rnP r

rn

100102 P 10010210 P

{A, B, C, D}

{A, B, C, D}

At Our Terminal Horizon (T=2)At Our Terminal Horizon (T 2)

{1/.1, 1/.1, 1/.1, 1/.1, 1/.1, 1/.1, 1/.1, 1/.1, 1/.1, -10/.1}

{2/.81, -9/.18, -20/.01}

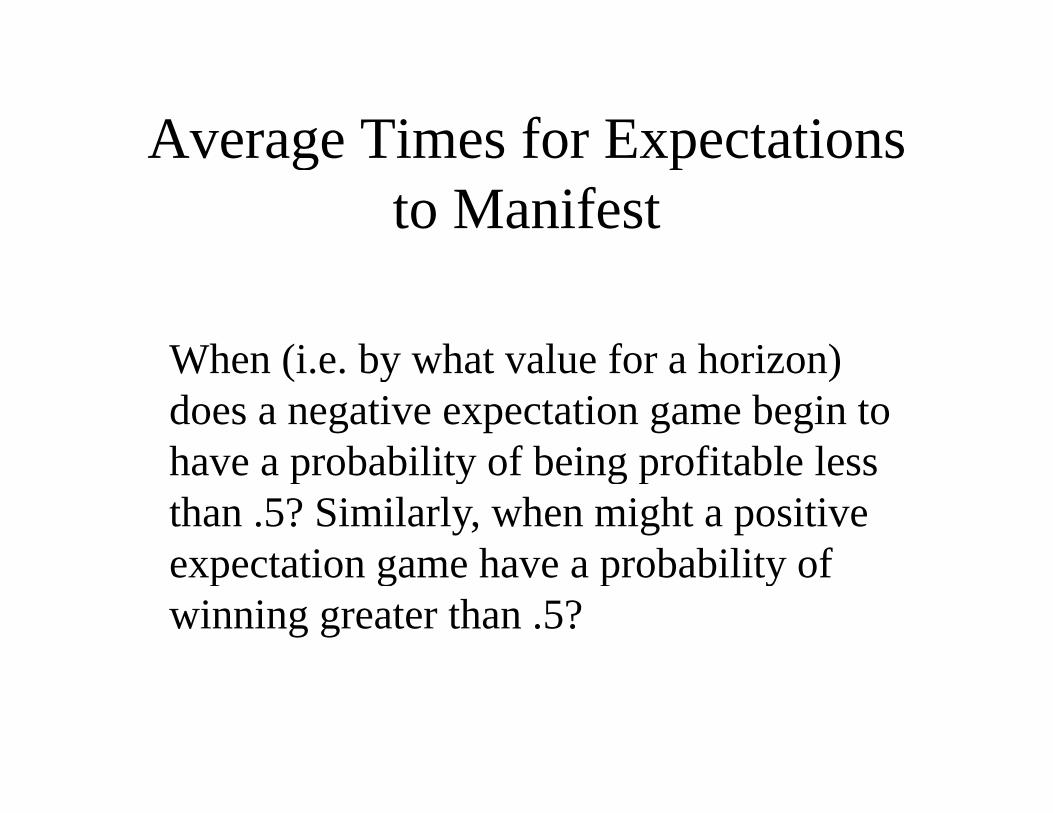

Average Times for ExpectationsAverage Times for Expectations to Manifest

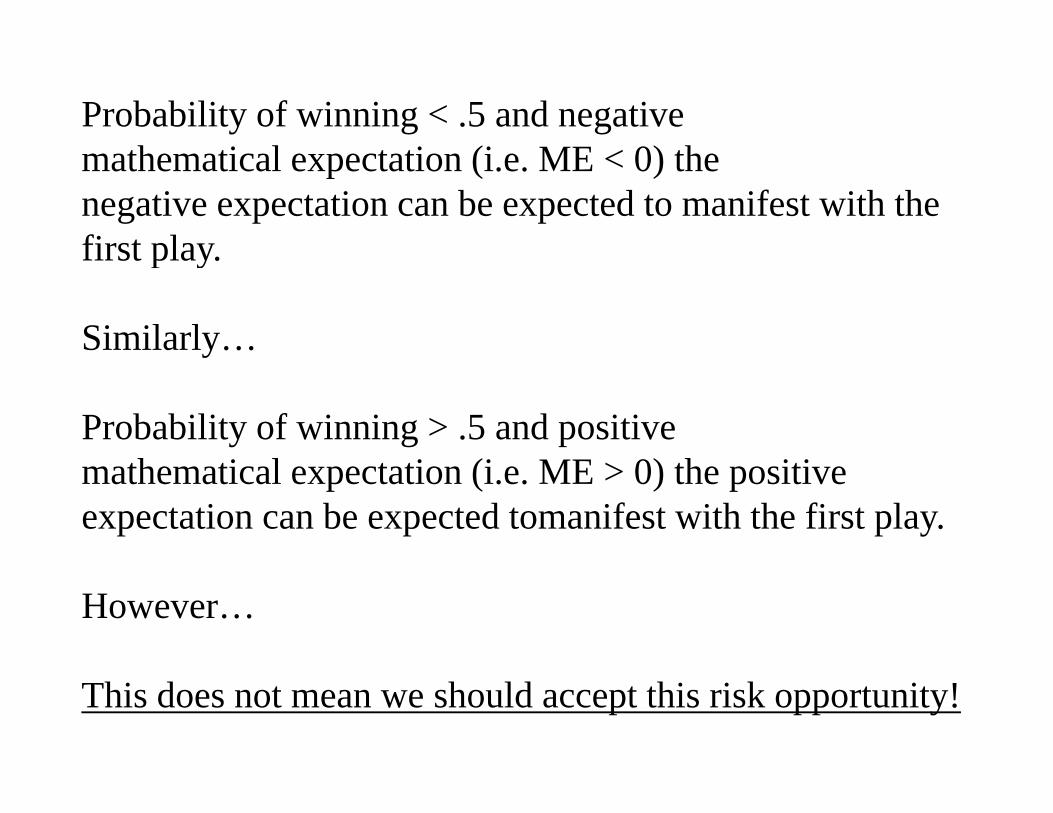

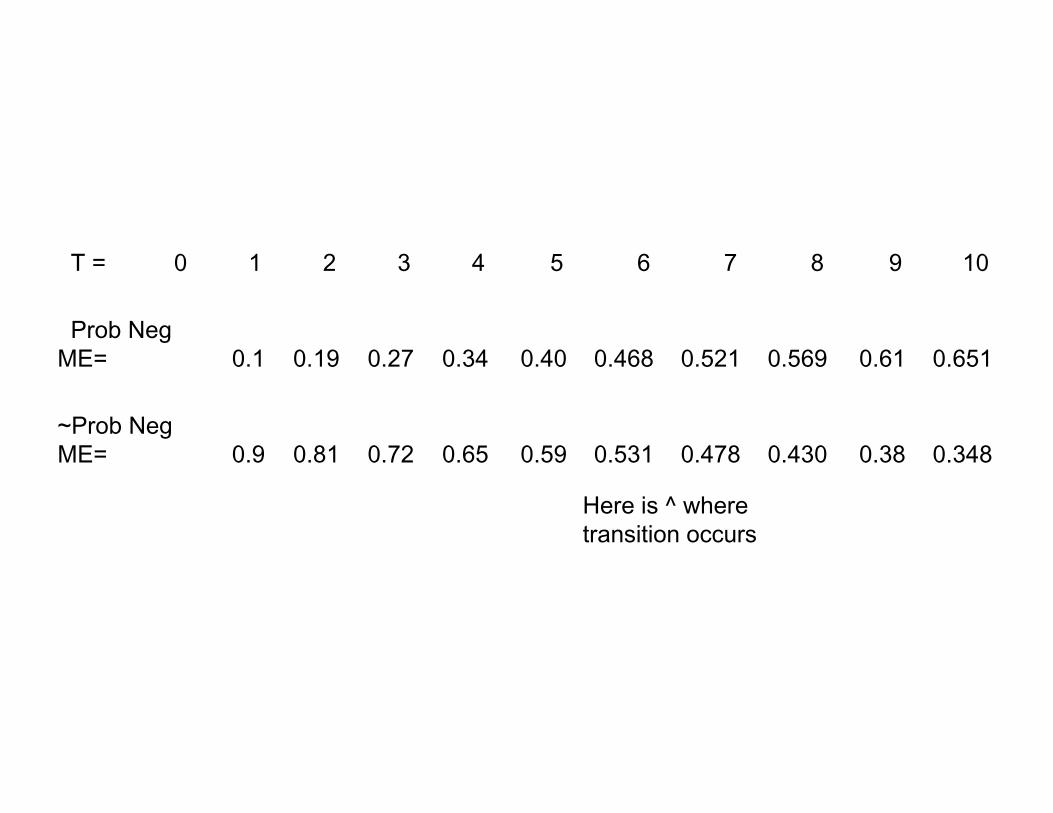

When (i e by what value for a horizon)When (i.e. by what value for a horizon) does a negative expectation game begin to have a probability of being profitable lesshave a probability of being profitable less than .5? Similarly, when might a positive expectation game have a probability ofexpectation game have a probability of winning greater than .5?

Probability of winning < .5 and negative th ti l t ti (i ME < 0) thmathematical expectation (i.e. ME < 0) the

negative expectation can be expected to manifest with the first playfirst play.

Similarly…y

Probability of winning > .5 and positive h i l i (i ) h i imathematical expectation (i.e. ME > 0) the positive

expectation can be expected tomanifest with the first play.

However…

This does not mean we should accept this risk opportunity!

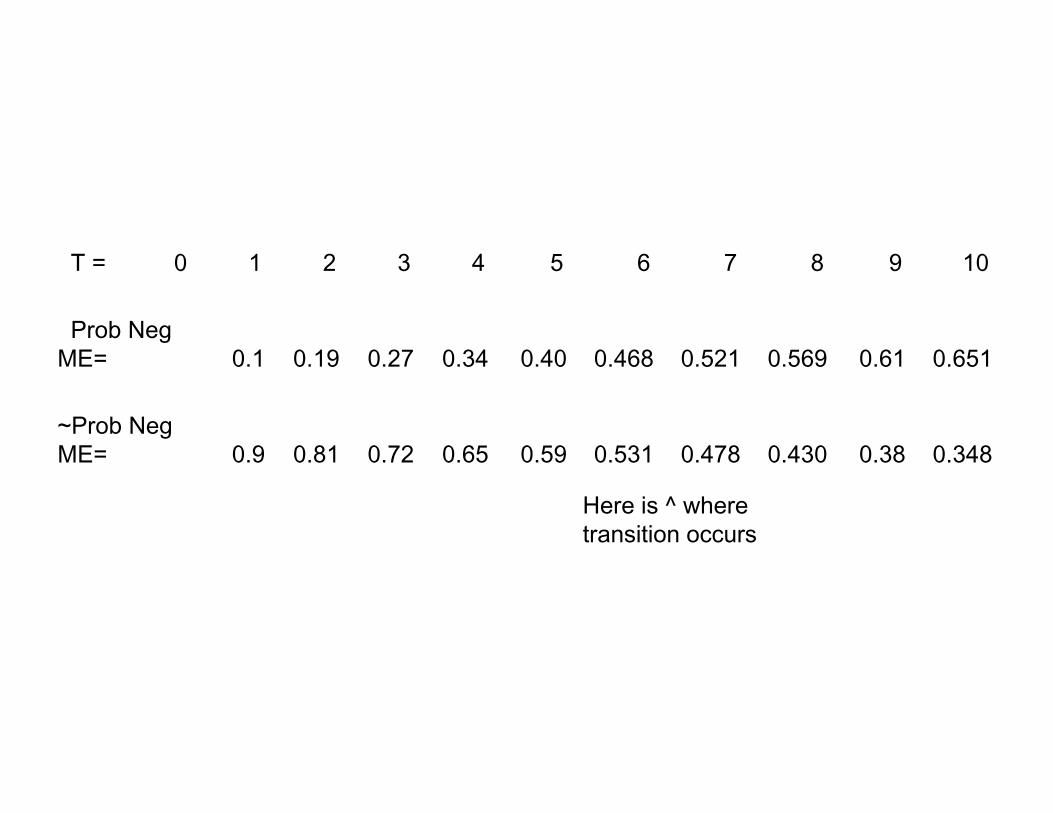

T = 0 1 2 3 4 5 6 7 8 9 10

Prob Neg ME= 0 1 0 19 0 27 0 34 0 40 0 468 0 521 0 569 0 61 0 651ME= 0.1 0.19 0.27 0.34 0.40 0.468 0.521 0.569 0.61 0.651

~Prob Neg ME= 0 9 0 81 0 72 0 65 0 59 0 531 0 478 0 430 0 38 0 348ME 0.9 0.81 0.72 0.65 0.59 0.531 0.478 0.430 0.38 0.348

Here is ^ where transition occurs

The Real Criteria

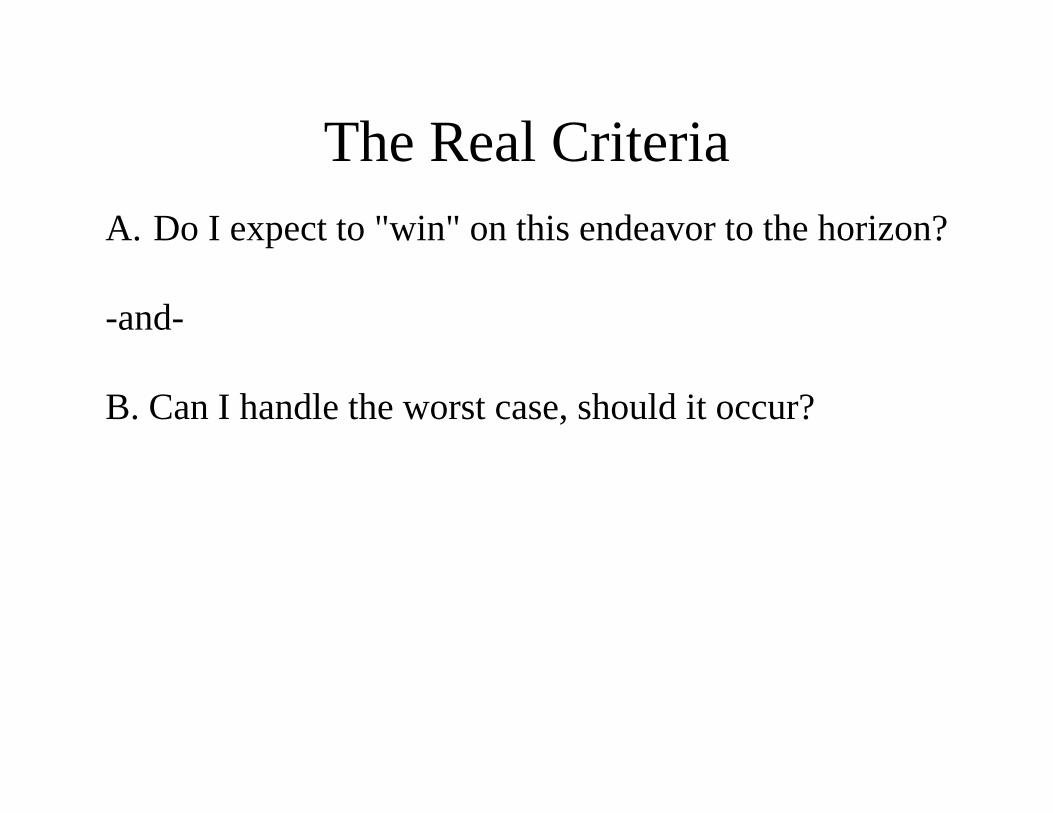

The Real CriteriaThe Real CriteriaA. Do I expect to "win" on this endeavor to the horizon?

-and-

B. Can I handle the worst case, should it occur?

The Real CriteriaThe Real CriteriaA. Do I expect to "win" on this endeavor to the horizon?

-and-

B. Can I handle the worst case, should it occur?

If the gambler can answer affirmatively to both, it’s a risk opportunity worth taking (provided that when the gambler’sopportunity worth taking (provided that when the gambler s horizon is met, the gambler terminates the game entirely and never comes back, i.e. it is the gambler’s terminal horizon, be i b h bl ’ li i h i )it by the gambler’s own volition or otherwise)

The Real CriteriaThe Real CriteriaA. Do I expect to "win" on this endeavor to the horizon?

-and-

B. Can I handle the worst case, should it occur?

A is what the gambler expects to happen. B is what can happen

The Real CriteriaThe Real CriteriaA. Do I expect to "win" on this endeavor to the horizon?

-and-

B. Can I handle the worst case, should it occur?

So the answer to A is a function of both:1. What is the probability I will see my horizon and be profitable -and–2 For a negative expectation game is the horizon sufficiently short2. For a negative expectation game, is the horizon sufficiently short such that the manifestation of the expectation of losing in the run to thehorizon occurs after the horizon? Similarly, for a positive expectation

i th h i ffi i tl l h h th t thgame, is the horizon sufficiently long enough such that the manifestation of the expectation of winning in the run to the horizon occurs before the horizon?

T = 0 1 2 3 4 5 6 7 8 9 10

Prob Neg ME= 0 1 0 19 0 27 0 34 0 40 0 468 0 521 0 569 0 61 0 651ME= 0.1 0.19 0.27 0.34 0.40 0.468 0.521 0.569 0.61 0.651

~Prob Neg ME= 0 9 0 81 0 72 0 65 0 59 0 531 0 478 0 430 0 38 0 348ME 0.9 0.81 0.72 0.65 0.59 0.531 0.478 0.430 0.38 0.348

Here is ^ where transition occurs

Examples

LTCM – Violated B

Quitting a Winning System Too Soon – Violates A

Red/Black Roulette – Violates A (possibly B also!)

Examples

Technical Analysis – All-too-often focuses only on the next trade solely. As a result, we often do not even get to the kind of critical risk opportunity analysis such as this, or to the all-important allocation question such as we have seenall important allocation question such as we have seenpreviously in this discussion.

The 4 Main CaveatsThe 4 Main Caveats

• The technicals dictate what I can make or lose.• You always are using leverage – it is always at

k ( i h f )work on you. (Because it has two facets).• Diversification does not mitigate risk (it increases

it especially in violent markets)it, especially in violent markets).• The mean (expectation) or mode (singlemost

likely outcome) of this distribution of possible y ) poutcomes are not what we should determine in accepting a risk-opportunity prospect. Instead we h d l it i f di d thave a dual criteria of median and worst-case outcomes.

Tamp 2 Day Course,

“Risk-Opportunity Analysis”

November 13-14, 2010:

http://ralphvince.com