iia/isaca/acfe joint conference - chapters.theiia.org county/iia oc presentation... · page 5. rpa...

TRANSCRIPT

IIA/ISACA/ACFE Joint Conference

March 16, 2018

Page 2

Robotics Process Automation

IIA/ISACA/ACFE Joint Conference

Page 3

… what if it meant 25% to 40%+ sustainable efficiency gains

… and improved accuracy?

Robotic Process Automation (RPA)

Discussion agenda

1. Introduction to RPA2. Key risks associated with

RPA3. How will internal controls

and internal audit evolve with RPA

4. How can internal audit use RPA

IIA/ISACA/ACFE Joint Conference

Page 4

1. Introduction to RPA

IIA/ISACA/ACFE Joint Conference

Page 5

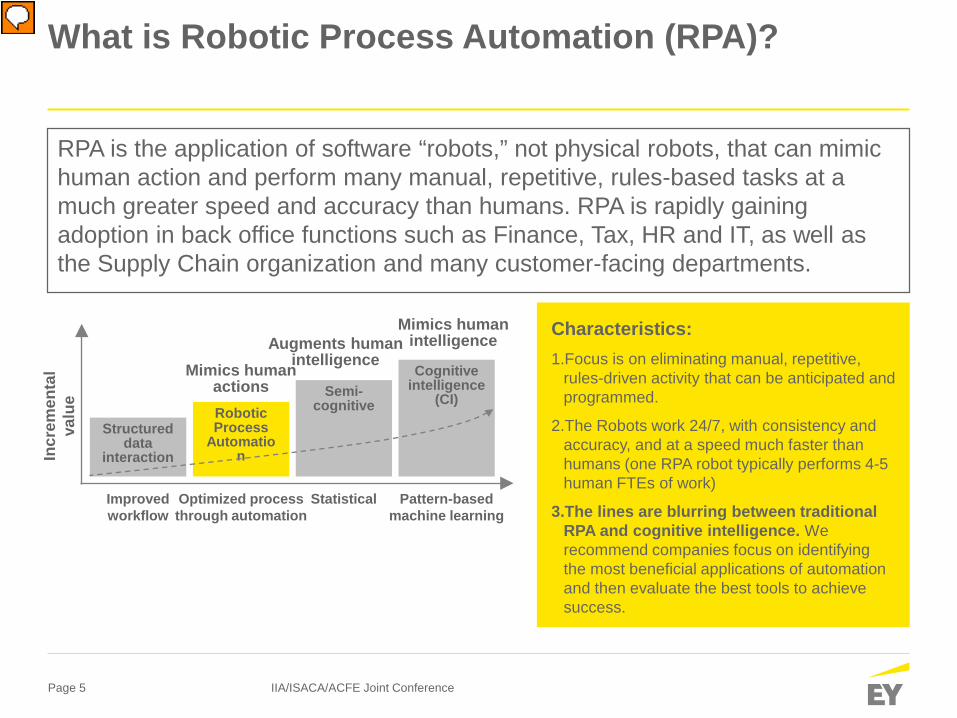

RPA is the application of software “robots,” not physical robots, that can mimic human action and perform many manual, repetitive, rules-based tasks at a much greater speed and accuracy than humans. RPA is rapidly gaining adoption in back office functions such as Finance, Tax, HR and IT, as well as the Supply Chain organization and many customer-facing departments.

Pattern-based machine learning

StatisticalOptimized processthrough automation

Improved workflow

Cognitive intelligence

(CI)Semi-cognitiveRobotic

Process Automatio

n

Structured data

interactionIncr

emen

tal

valu

e

Mimics human actions

Augments human intelligence

Mimics human intelligence

What is Robotic Process Automation (RPA)?

Characteristics:1.Focus is on eliminating manual, repetitive,

rules-driven activity that can be anticipated and programmed.

2.The Robots work 24/7, with consistency and accuracy, and at a speed much faster than humans (one RPA robot typically performs 4-5 human FTEs of work)

3.The lines are blurring between traditional RPA and cognitive intelligence. We recommend companies focus on identifying the most beneficial applications of automation and then evaluate the best tools to achieve success.

IIA/ISACA/ACFE Joint Conference

Page 6

RPA and the “virtual worker”

IIA/ISACA/ACFE Joint Conference

Low-risk, low-cost extension of existing technologyRPA is overlaid on existing systems and integrated with existing data minimizing disruption to IT strategy and architecture.

While most RPA applications will be part of the long-term architecture, some applications provide a cost-effective, medium-term solution until core systems are expanded.

ReliabilityNo sick days, services provided 365 days a year

Audit trailFully maintained logs essential for compliance

ConsistencyIdentical processes and tasks, eliminating output variations

Right shoringGeographical independence reducing need to offshore jobs while still delivering cost savings

RetentionShifts human effort toward more stimulating tasks

ROITypical RPA projects with multiple functional “pilots” but generally completed in 9 to 12 months with a return on investment (ROI) < 1 year

Cost savings or avoidance

Ranging from 20–60% of

baseline FTE cost

Opportunity focusedCan focus RPA on only those areas where significant opportunity exists; does not require enterprise adoption

AccuracyDouble-digit reductions in error ratesRPA often “fills the gaps”

between existing systems

ScalabilityInstant ramp up and down to match demand peaks and troughs

ProductivityFreed up human resources for higher value-added tasks.

ERP EPM

CRM

SCM HRIS

Page 7

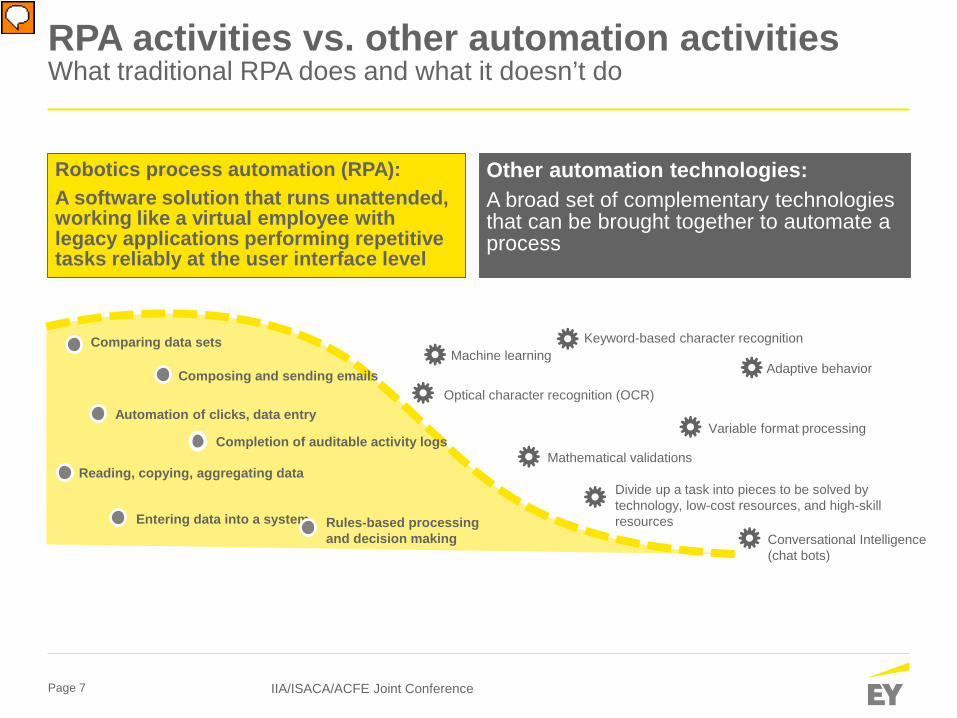

RPA activities vs. other automation activities What traditional RPA does and what it doesn’t do

Robotics process automation (RPA):A software solution that runs unattended, working like a virtual employee with legacy applications performing repetitive tasks reliably at the user interface level

Other automation technologies:A broad set of complementary technologies that can be brought together to automate a process

Divide up a task into pieces to be solved by technology, low-cost resources, and high-skill resources

Keyword-based character recognition

Optical character recognition (OCR)

Completion of auditable activity logs

Entering data into a system

Composing and sending emails

Rules-based processing and decision making

Comparing data sets

Reading, copying, aggregating data

Automation of clicks, data entry

Machine learning

Variable format processing

Adaptive behavior

Mathematical validations

Conversational Intelligence(chat bots)

IIA/ISACA/ACFE Joint Conference

Page 8

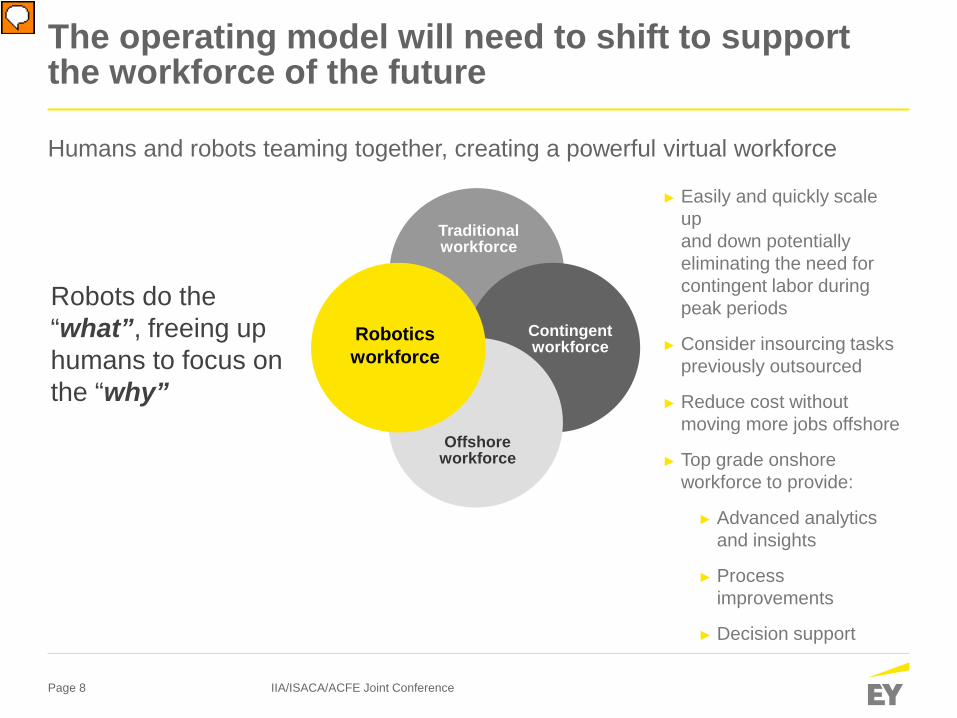

The operating model will need to shift to support the workforce of the future

Robots do the “what”, freeing up humans to focus on the “why”

► Easily and quickly scale upand down potentially eliminating the need for contingent labor during peak periods

► Consider insourcing tasks previously outsourced

► Reduce cost without moving more jobs offshore

► Top grade onshore workforce to provide:

► Advanced analytics and insights

► Process improvements

► Decision support

Traditional workforce

Contingent workforce

Offshoreworkforce

Roboticsworkforce

Humans and robots teaming together, creating a powerful virtual workforce

IIA/ISACA/ACFE Joint Conference

Page 9

2. Key risks associated with RPA

IIA/ISACA/ACFE Joint Conference

Page 10

Key RPA Risks

Policy and governance

Logical user access

System change

management

Timely system

outage/issue detection

Vendor/3rd party

management

Completeness/accuracy of

RPA processing

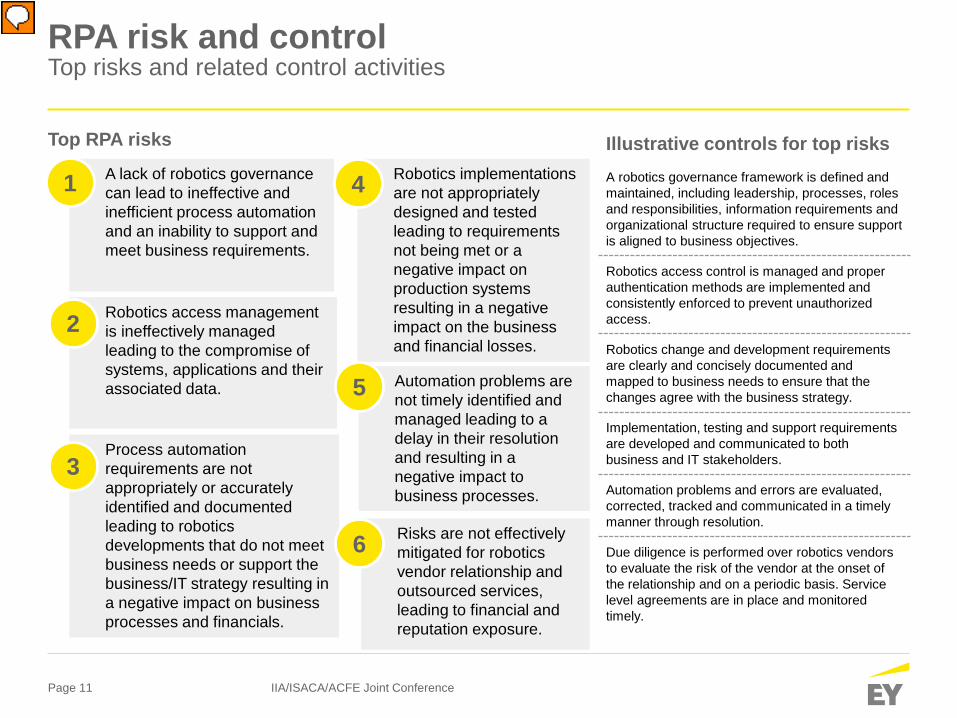

A lack of robotics governance can lead to ineffective and inefficient process automation and an inability to support and meet business requirements.

Key risks in RPA

Robotics access management is ineffectively managed leading to the compromise of systems, applications and their associated data.

Automation problems are not timely identified and managed leading to a delay in their resolution and resulting in a negative impact to business processes.

Risks are not effectively mitigated for robotics vendor relationship and outsourced services, leading to financial and reputation exposure.

Input/upstream data is not completely/accurately received by the robot, or the robot may fail to completely/accurately process and calculate data to hand off downstream.

Process automation requirements are not appropriately or accurately identified and documented leading to robotics developments that do not meet business needs or support the business/IT strategy resulting in a negative impact on business processes and financials.

IIA/ISACA/ACFE Joint Conference

Page 11

RPA risk and controlTop risks and related control activities

A lack of robotics governance can lead to ineffective and inefficient process automation and an inability to support and meet business requirements.

Top RPA risks Illustrative controls for top risksA robotics governance framework is defined and maintained, including leadership, processes, roles and responsibilities, information requirements and organizational structure required to ensure support is aligned to business objectives.

Robotics access control is managed and proper authentication methods are implemented and consistently enforced to prevent unauthorized access.

Robotics change and development requirements are clearly and concisely documented and mapped to business needs to ensure that the changes agree with the business strategy.

Implementation, testing and support requirements are developed and communicated to both business and IT stakeholders.

Automation problems and errors are evaluated, corrected, tracked and communicated in a timely manner through resolution.

Due diligence is performed over robotics vendors to evaluate the risk of the vendor at the onset of the relationship and on a periodic basis. Service level agreements are in place and monitoredtimely.

1

Robotics access management is ineffectively managed leading to the compromise of systems, applications and their associated data.

2

Process automation requirements are not appropriately or accurately identified and documented leading to robotics developments that do not meet business needs or support the business/IT strategy resulting in a negative impact on business processes and financials.

3

Robotics implementations are not appropriately designed and tested leading to requirements not being met or a negative impact on production systems resulting in a negative impact on the business and financial losses.

4

Automation problems are not timely identified and managed leading to a delay in their resolution and resulting in a negative impact to business processes.

5

Risks are not effectively mitigated for robotics vendor relationship and outsourced services, leading to financial and reputation exposure.

6

IIA/ISACA/ACFE Joint Conference

Page 12

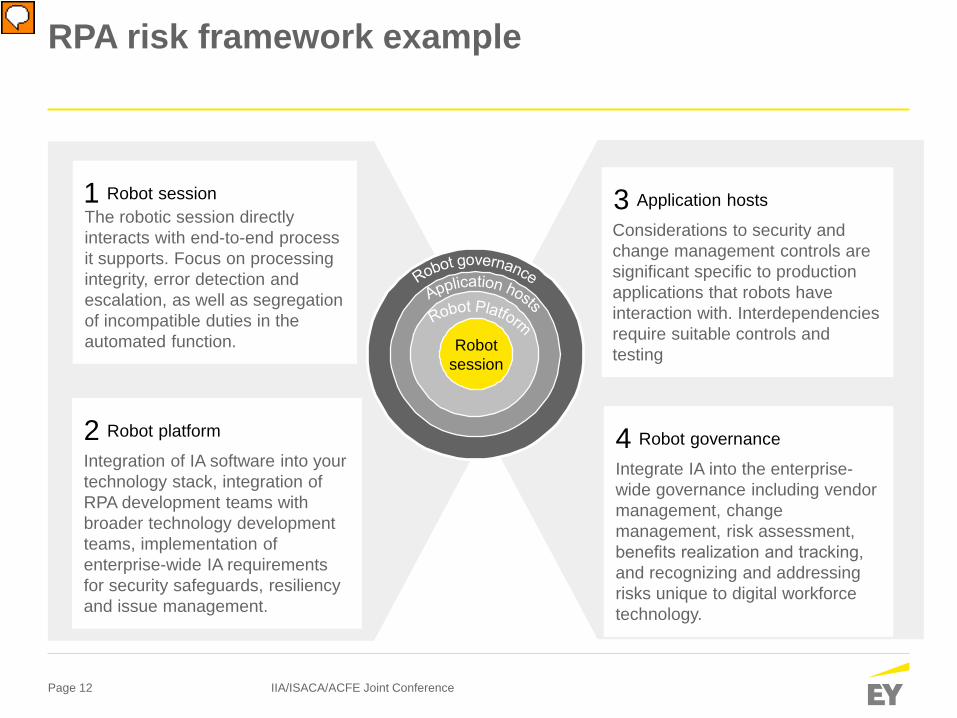

RPA risk framework example

1 Robot sessionThe robotic session directly interacts with end-to-end process it supports. Focus on processing integrity, error detection and escalation, as well as segregation of incompatible duties in the automated function.

2 Robot platform

Integration of IA software into your technology stack, integration of RPA development teams with broader technology development teams, implementation of enterprise-wide IA requirements for security safeguards, resiliency and issue management.

3 Application hosts

Considerations to security and change management controls are significant specific to production applications that robots have interaction with. Interdependencies require suitable controls and testing

4 Robot governance

Integrate IA into the enterprise-wide governance including vendor management, change management, risk assessment, benefits realization and tracking, and recognizing and addressing risks unique to digital workforce technology.

Robotsession

IIA/ISACA/ACFE Joint Conference

Page 13

3. How will internal audit and internal controls change

IIA/ISACA/ACFE Joint Conference

Page 14

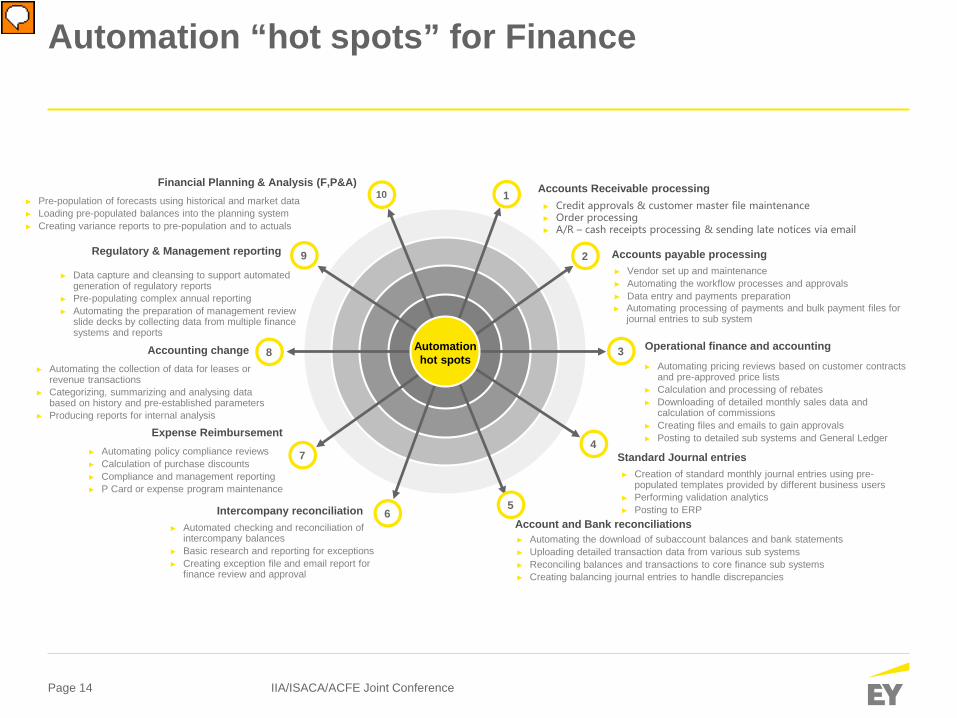

Automation “hot spots” for Finance

1

2

3

4

6

7

8

9

10

5

Operational finance and accounting

► Automating pricing reviews based on customer contracts and pre-approved price lists

► Calculation and processing of rebates► Downloading of detailed monthly sales data and

calculation of commissions► Creating files and emails to gain approvals ► Posting to detailed sub systems and General Ledger

Standard Journal entries► Creation of standard monthly journal entries using pre-

populated templates provided by different business users► Performing validation analytics► Posting to ERP

Accounts payable processing► Vendor set up and maintenance► Automating the workflow processes and approvals► Data entry and payments preparation

Expense Reimbursement► Automating policy compliance reviews► Calculation of purchase discounts► Compliance and management reporting► P Card or expense program maintenance

Intercompany reconciliation

Regulatory & Management reporting

► Automated checking and reconciliation of intercompany balances

► Basic research and reporting for exceptions► Creating exception file and email report for

finance review and approval

Accounts Receivable processing

► Automating processing of payments and bulk payment files for journal entries to sub system

► Data capture and cleansing to support automated generation of regulatory reports

► Pre-populating complex annual reporting ► Automating the preparation of management review

slide decks by collecting data from multiple finance systems and reports

Automation hot spots

► Credit approvals & customer master file maintenance► Order processing► A/R – cash receipts processing & sending late notices via email

Account and Bank reconciliations► Automating the download of subaccount balances and bank statements► Uploading detailed transaction data from various sub systems► Reconciling balances and transactions to core finance sub systems► Creating balancing journal entries to handle discrepancies

Accounting change► Automating the collection of data for leases or

revenue transactions► Categorizing, summarizing and analysing data

based on history and pre-established parameters► Producing reports for internal analysis

► Pre-population of forecasts using historical and market data► Loading pre-populated balances into the planning system► Creating variance reports to pre-population and to actuals

Financial Planning & Analysis (F,P&A)

IIA/ISACA/ACFE Joint Conference

Page 15

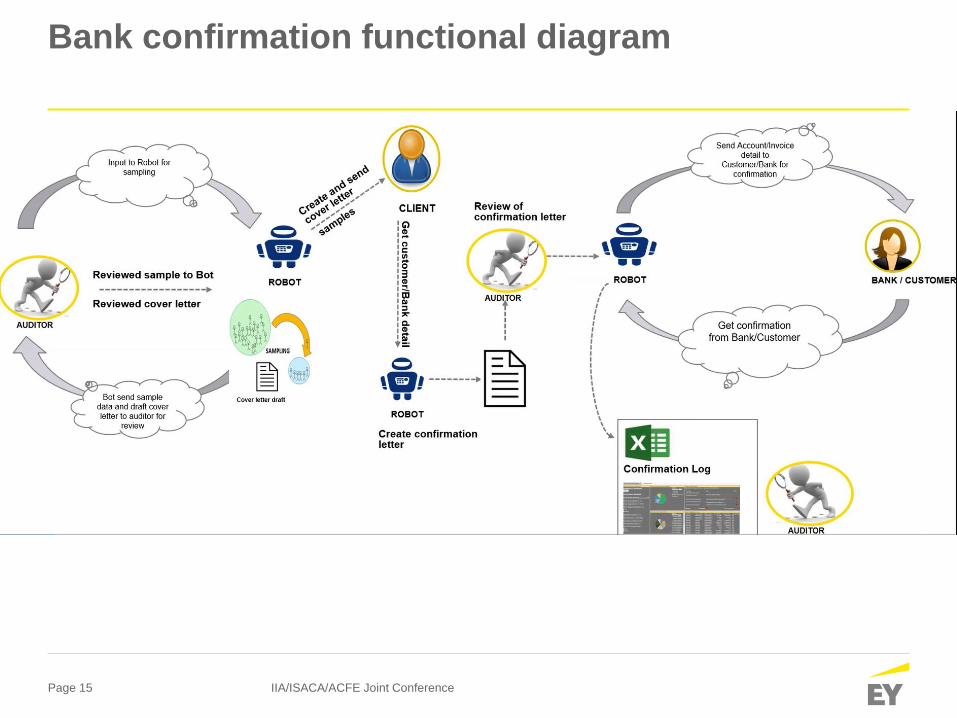

Bank confirmation functional diagram

IIA/ISACA/ACFE Joint Conference

Page 16

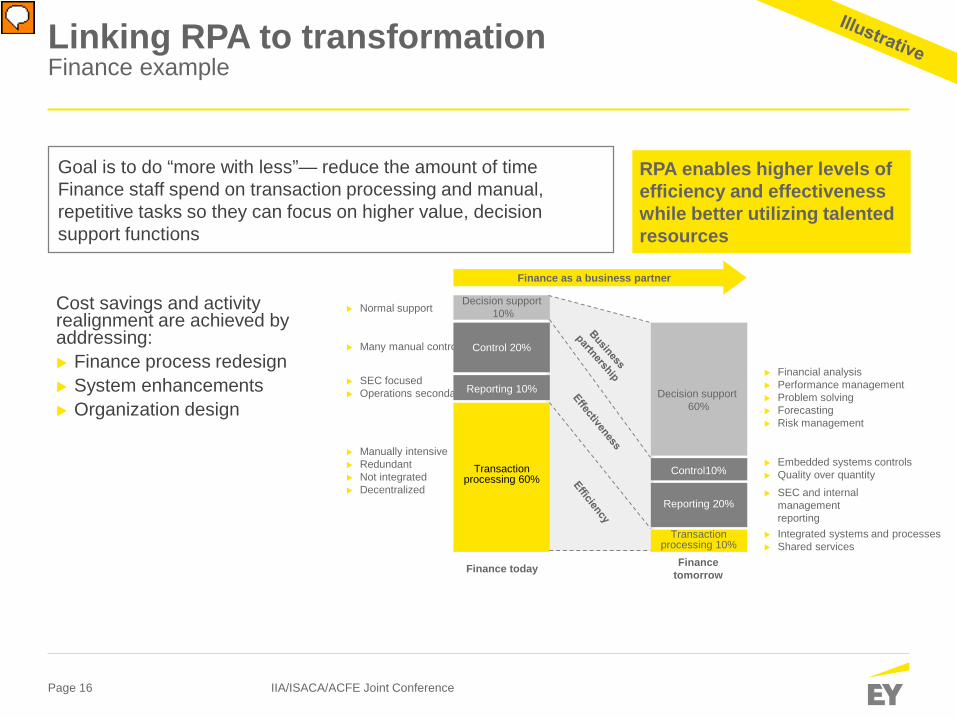

RPA enables higher levels of efficiency and effectiveness while better utilizing talented resources

Cost savings and activity realignment are achieved by addressing: Finance process redesign System enhancements Organization design

Linking RPA to transformation Finance example

IIA/ISACA/ACFE Joint Conference

Goal is to do “more with less”— reduce the amount of time Finance staff spend on transaction processing and manual, repetitive tasks so they can focus on higher value, decision support functions

Normal support

Many manual controls

SEC focused Operations secondary

Manually intensive Redundant Not integrated Decentralized

Financial analysis Performance management Problem solving Forecasting Risk management

Embedded systems controls Quality over quantity SEC and internal

management reporting

Integrated systems and processes Shared services

Decision support10%

Decision support 60%

Control 20%

Control10%

Reporting 10%

Reporting 20%

Transactionprocessing 60%

Transaction processing 10%

Finance today Finance tomorrow

Finance as a business partner

Page 17

4. How can internal audit use RPA

IIA/ISACA/ACFE Joint Conference

Page 18

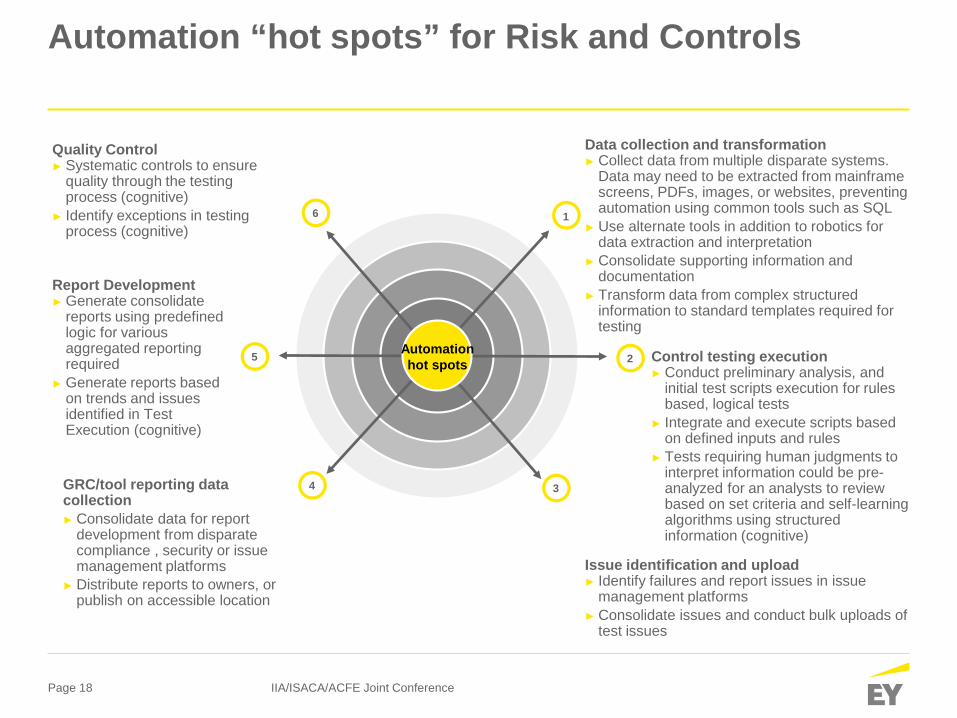

Automation “hot spots” for Risk and Controls

Automation hot spots

1

2

34

6

5

Data collection and transformation► Collect data from multiple disparate systems.

Data may need to be extracted from mainframe screens, PDFs, images, or websites, preventing automation using common tools such as SQL

► Use alternate tools in addition to robotics for data extraction and interpretation

► Consolidate supporting information and documentation

► Transform data from complex structured information to standard templates required for testing

Issue identification and upload► Identify failures and report issues in issue

management platforms► Consolidate issues and conduct bulk uploads of

test issues

Control testing execution► Conduct preliminary analysis, and

initial test scripts execution for rules based, logical tests

► Integrate and execute scripts based on defined inputs and rules

► Tests requiring human judgments to interpret information could be pre-analyzed for an analysts to review based on set criteria and self-learning algorithms using structured information (cognitive)

Quality Control► Systematic controls to ensure

quality through the testing process (cognitive)

► Identify exceptions in testing process (cognitive)

Report Development► Generate consolidate

reports using predefined logic for various aggregated reporting required

► Generate reports based on trends and issues identified in Test Execution (cognitive)

IIA/ISACA/ACFE Joint Conference

GRC/tool reporting data collection► Consolidate data for report

development from disparate compliance , security or issue management platforms

► Distribute reports to owners, or publish on accessible location

Page 19

SAP transport testing bot video

IIA/ISACA/ACFE Joint Conference

Page 20

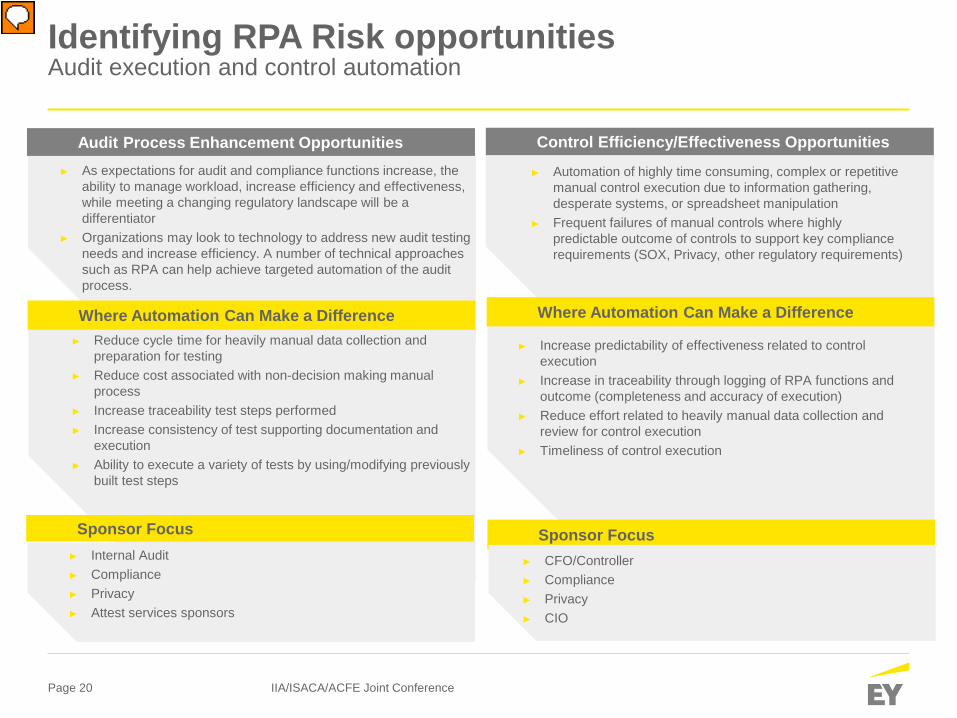

Identifying RPA Risk opportunitiesAudit execution and control automation

Audit Process Enhancement Opportunities► As expectations for audit and compliance functions increase, the

ability to manage workload, increase efficiency and effectiveness, while meeting a changing regulatory landscape will be a differentiator

► Organizations may look to technology to address new audit testing needs and increase efficiency. A number of technical approaches such as RPA can help achieve targeted automation of the audit process.

Where Automation Can Make a Difference► Reduce cycle time for heavily manual data collection and

preparation for testing► Reduce cost associated with non-decision making manual

process► Increase traceability test steps performed► Increase consistency of test supporting documentation and

execution► Ability to execute a variety of tests by using/modifying previously

built test steps

Sponsor Focus► Internal Audit► Compliance► Privacy► Attest services sponsors

Control Efficiency/Effectiveness Opportunities

► Automation of highly time consuming, complex or repetitive manual control execution due to information gathering, desperate systems, or spreadsheet manipulation

► Frequent failures of manual controls where highly predictable outcome of controls to support key compliance requirements (SOX, Privacy, other regulatory requirements)

Where Automation Can Make a Difference

► Increase predictability of effectiveness related to control execution

► Increase in traceability through logging of RPA functions and outcome (completeness and accuracy of execution)

► Reduce effort related to heavily manual data collection and review for control execution

► Timeliness of control execution

Sponsor Focus► CFO/Controller► Compliance► Privacy► CIO

IIA/ISACA/ACFE Joint Conference

Page 21

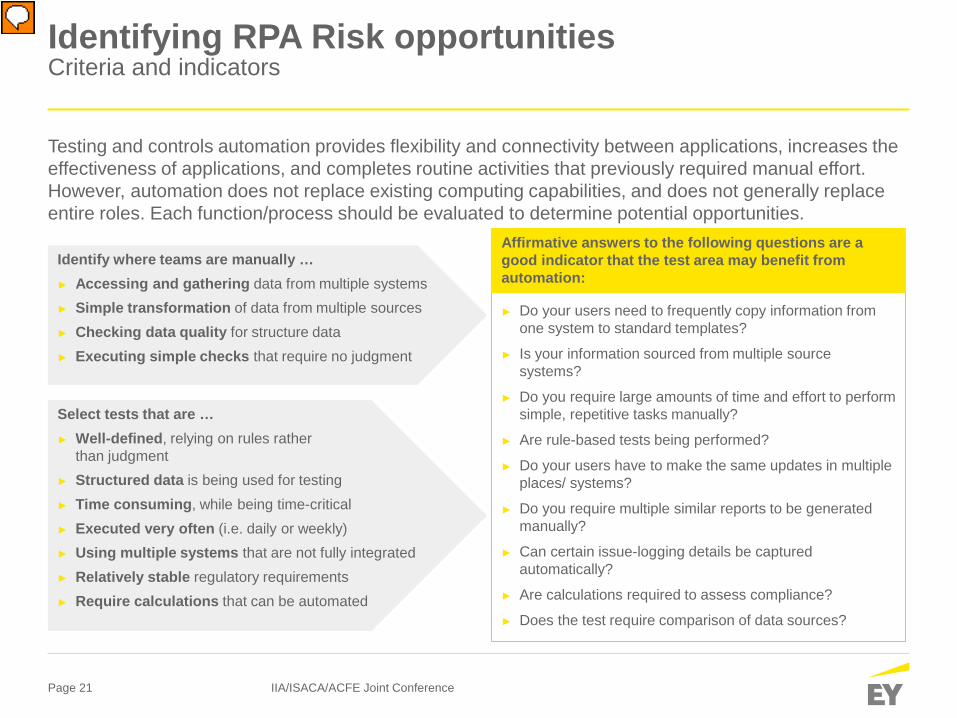

► Do your users need to frequently copy information from one system to standard templates?

► Is your information sourced from multiple source systems?

► Do you require large amounts of time and effort to perform simple, repetitive tasks manually?

► Are rule-based tests being performed?

► Do your users have to make the same updates in multiple places/ systems?

► Do you require multiple similar reports to be generated manually?

► Can certain issue-logging details be captured automatically?

► Are calculations required to assess compliance?

► Does the test require comparison of data sources?

Identifying RPA Risk opportunitiesCriteria and indicators

Testing and controls automation provides flexibility and connectivity between applications, increases the effectiveness of applications, and completes routine activities that previously required manual effort. However, automation does not replace existing computing capabilities, and does not generally replace entire roles. Each function/process should be evaluated to determine potential opportunities.

Identify where teams are manually … ► Accessing and gathering data from multiple systems ► Simple transformation of data from multiple sources ► Checking data quality for structure data ► Executing simple checks that require no judgment

Select tests that are … ► Well-defined, relying on rules rather

than judgment ► Structured data is being used for testing ► Time consuming, while being time-critical ► Executed very often (i.e. daily or weekly) ► Using multiple systems that are not fully integrated ► Relatively stable regulatory requirements ► Require calculations that can be automated

Affirmative answers to the following questions are a good indicator that the test area may benefit from automation:

IIA/ISACA/ACFE Joint Conference

EY | Assurance | Tax | Transactions | Advisory

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

Ernst & Young LLP is a client-serving member firm ofErnst & Young Global Limited operating in the US.

© 2018 Ernst & Young LLP.All Rights Reserved.

1708-2382611ED None

This material has been prepared for general informational purposesonly and is not intended to be relied upon as accounting, tax or otherprofessional advice. Please refer to your advisors for specific advice.

ey.com