igcse business studies revision notes finance … · · 2008-05-26igcse business studies revision...

TRANSCRIPT

IGCSE Business Studies revision notes Finance

IIGGCCSSEE FFIINNAANNCCEE RREEVVIISSIIOONN NNOOTTEESS

Table of contents

Table of contents ................................................................................................................. 2 SOURCES OF FINANCE........................................................................................................ 3 CASH FLOW......................................................................................................................... 5 HOW TO CALCULATE THE CASH BALANCE............................................................... 5 HOW TO WORK OUT THE CASH AVAILABLE TO THE BUSINESS ................................ 8 THE PURPOSE OF ACCOUNTING....................................................................................... 9 THE ACCOUNTANT.......................................................................................................... 11 TRADING ACCOUNTS AND PROFIT AND LOSS ACCOUNTS.................................. 12 BALANCE SHEETS .............................................................................................................. 14 RATIO ANALYSIS ............................................................................................................... 18 Profitability Ratios .............................................................................................................. 18 Liquidity Ratios ................................................................................................................... 18 Break Even Analysis ............................................................................................................ 24

IGCSE Business Studies revision notes Finance

SOURCES OF FINANCE

Companies1 need short-term finance to start up, or to cover day-to-day running costs. This has to be repaid over a short period. It provides a business with working capital. Long-term finance is used to grow or expand and is paid back over a number of years. Sources of finance can be:

• Internal • External

Internal sources of finance are a cheaper way to raise working capital. Obtaining finance externally is usually the last option as interest has to be paid.

Try to remember three ways of raising finance from each source, internal and external: IINNTTEERRNNAALL SSOOUURRCCEESS OOFF FFIINNAANNCCEE The Directors of a Public Limited Company may retain profits for a year rather than share it amongst the owners (Through paying out dividends). The cash could be invested to earn interest. Assets that are no longer required, like an outdated computer or an obsolete piece of machinery, can be sold to raise cash. Stock levels can be reduced (sold) and the money used for other things. EXTERNAL SOURCES OF FINANCE A sole trader or a small business may be able to borrow money from family or friends without paying interest. Shareholders could also put more money into a Limited Company through a rights issue. Loans from a bank or a building society can be expensive. An agreed amount is borrowed and repaid over a fixed period of time with interest. A bank overdraft is also expensive. Grants from central or local government can cost the firm nothing. 1 firm = business = company = organisation.

IGCSE Business Studies revision notes Finance

Firms often lease equipment or machinery to avoid a large outlay of cash. This is useful if a firm needs to upgrade within the medium term as technology advances. Why would it want to do this? Check your understanding of which internal and external sources of finance are available to businesses, and when they are used.

IGCSE Business Studies revision notes Finance

CASH FLOW

A business needs to know how much cash is coming in and going out. Cash is like a river flowing through a business. Cash is like the liquid flowing through the diagram above. Cash is often called a “liquid asset”.

Drawing up a cash flow forecast shows whether there is enough cash (liquidity) available to pay salaries and settle (ie pay) debts on time. It calculates the firm's reserves, which could be invested in expansion projects or new equipment. Accountants can identify when shortfalls are likely to happen, and when surplus funds are likely to become available. This helps them plan for when the firm might need an overdraft, or be able to reinvest its retained profits into the business. Remember Questions on cash flows are fairly common in Business Studies examinations, so you must to be able to:

• calculate the cash balance • spot monthly trends – ie any problems • give solutions to those problems

HOW TO CALCULATE THE CASH BALANCE (it’s easy!) Go Faster Sports is a high-street retail outlet (a shop!) that has only been open six months, but it has already managed to establish itself locally (ie it’s managing to survive). As a result, it is considering whether to invest more money into the business.

IGCSE Business Studies revision notes Finance

Apart from the manager, there are two full-time members of staff. This is its cash flow for the past three months – in other words, they are looking back in time:

You can see that the total flow of cash into the business (income) for January was £15,500, and that the total outflow from the business (expenditure) was £15,000. You can find the cash balance by subtracting the expenditure from the income, shown as a net surplus (profit) or a net deficit (loss). Income - Expenditure = Balance £15,500 - £15,000 = £500 (a surplus) Compare this with February's results: Income - Expenditure = Balance £16,100 - £17,200 = -£1,100 (a deficit) February’s deficit could also be written like this: (£1,100) with a bracket, or in red: £1,100 You will also (probably) need to work out WHEN the CASH comes in to the business. You will need to work out a cash part of the sales. This money will come into the business when the goods are sold

IGCSE Business Studies revision notes Finance

There will always (?) be a CREDIT part of sales. The CASH from this will arrive in one or two months time, so that is where you enter it into the cashflow forecast. So, stuff sold in January on two months credit will not appear in the cash flow forecast until March. This is often one of the main reasons for cash flow problems.

IGCSE Business Studies revision notes Finance

HOW TO WORK OUT THE CASH AVAILABLE TO THE BUSINESS

The cash balances you have just calculated are only monthly results. To assess the cash available to the business, you have to add existing profits or deficits to the cash balance of the following month. This amount is the cash balance to carry forward, and in the next month's results is referred to as the cash balance brought forward. You will see that they are the same amount. For example, in January, the cash balance to carry forward was £2,150, the same figure as the cash balance brought forward for February. Similarly, you can tell that the cash balance to carry forward for the previous December was £1,650. This type of record helps managers to spot trends, and to plan the following months. Now look at the layout below. It’s different! This is a cash flow projection. In other words, they are looking a year ahead. It’s a guessing game! Remember In an examination you can never be 100% sure if the layout for cash flow, Trading, Profit and Loss accounts or Balance Sheets are going to be exactly the same as you have studied in class. But don’t panic! The basic principles are exactly the same. Just read it carefully, and it will all fall into place!

ASHLEY’S SHOES Cash Flow Projection for 2006 JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC

$ $ $ $ $ $ $ $ $ $ $ $

OPENING BALANCE 0 450 1150 2300 3150 3050 5100 8200 9050 11850 12500 16300

Cash Inflows

Customer Sales 11000 12000 13000 13500 12000 14000 14200 12000 13000 12000 14500 15000

Total Cash Inflow 11000 12000 13000 13500 12000 14000 14200 12000 13000 12000 14500 15000

Cash Outflow

Cost of shoes purchased 5000 5500 5500 6500 6000 6000 5000 5000 4500 5400 4900 6000

Wages 1900 1900 1950 1950 2000 2000 2000 2000 2000 2000 2000 2000

Electricity 1150 1200 1400 1100 1100 1000 1100 1000 900 1100 1200 1150

Rent 1000 1000 1000 1000 1000 1000 1000 1000 1000 1000 1000 1000

Other Expenses 1500 1700 2000 2100 2000 1950 2000 2150 1800 1850 1600 1900

Total Cash outflow 10550 11300 11850 12650 12100 11950 11100 11150 10200 11350 10700 12050

Net Cash Flow 450 700 1150 850 -100 2050 3100 850 2800 650 3800 2950

CLOSING BALANCE 450 1150 2300 3150 3050 5100 8200 9050 11850 12500 16300 19250

IGCSE Business Studies revision notes Finance

THE PURPOSE OF ACCOUNTING

The main aim of any business is to survive! Isn't it? Then it wants to make a profit! Doesn’t it? If it is in the private sector it will want to make a profit. If it is in the public sector it may want to improve or expand the services it provides. Whether public or private, it will need to control its finances. Imagine running a business where nobody cares how much is spent! Do you think it would last long? By collecting all the available financial information and writing it down in various accounts a business can assess how well it is performing. This is important both for a business internally as well as externally. INTERNALLY, managers want to know 3 things:

1. how much they are selling

2. how much they are spending (the level of their costs)

3. the amount of profit they are making From this information they can set budgets and performance targets to plan for the next trading year. An accountant can show managers where financial problems might be occurring within their company. Budgets allow managers to

• Delegate, but still keep control. They control the limits in which the juniors can work. • Can monitor performance. i.e. have you reached your targets. • Motivate: If you reach your targets, then you get a bonus.

Control through Variance analysis Once we have a budget, we can check how well we are actually doing in relation to how we thought we would do. The difference between the two is the variance. Care! Those differences in that are ‘good’ for the business are positive. No matter if they are more than budget (Sales for example.), or less than the budget (costs, for example). It is their ‘goodness’ that makes them positive. In the same way negative variances BAD for the business, no matter whether they are more or less than budgeted amount. EXTERNALLY, all businesses are legally required to keep records of their finances. In the UK a business has to make its accounts available to the Inland Revenue (Corporation Tax), and Customs and Excise (VAT). The larger the business, the stricter the rules on what accounts it has to prepare. Most business have to prepare a:

1. Trading account

2. Profit and loss account

3. Balance sheet

IGCSE Business Studies revision notes Finance

Limited companies also have to publish an annual report and final accounts because they have a separate legal identity. These accounts have to be checked by an independent person - an auditor - to ensure that they give a 'true and fair view' of what has happened to the business during the previous year. Potential investors or shareholders, for example, will want to know if a business is worth investing in. Potential creditors will also want to know whether the company will be able to repay any credit they give them. These assessments are based on two key accounting ideaS, which you need to be able to explain:

1. liquidity

2. profitability

IGCSE Business Studies revision notes Finance

THE ACCOUNTANT

An accountant has three main responsibilities. These are to:

1. Collect a firm's financial records e.g. receipts, invoices, cheques and statements

2. Maintain the book-keeping and construct accounts

3. Analyse and interpret the information. Once all the individual departments' financial records have been collected, the accountant can construct the company's accounts. These accounts are often known as a ledger and includes a sales ledger, bought ledger and cash book amongst others. Usually they are computerised. You don’t have to know exactly how they work. The accountant then analyses the information using various accounting ratios and formulae. The purpose of this is to identify any trends by comparing the results with previous results. Any trend, whether positive or negative, could affect the planning for the next year. Accountancy is a specialist area with its own technical language. As a result, the accountant will have to interpret his/her findings into a meaningful format. Other managers can then understand the information and will then be able to work together to plan and set budgets for the next year.

Check your understanding of accounting principles. Try answering these questions, T(rue) or F(alse). 1. An auditor must be an independent person. 2. Business Studies teachers are amazingly cool. 3. Profitability is a measure of a firm's gross profits. 4. One function of accounting is to compare results and identify trends. 5. Only limited companies have to keep financial records. 6. A firm's liquidity is its ability to meet short-term debts as they arise.

IGCSE Business Studies revision notes Finance

TRADING ACCOUNTS AND PROFIT AND LOSS ACCOUNTS

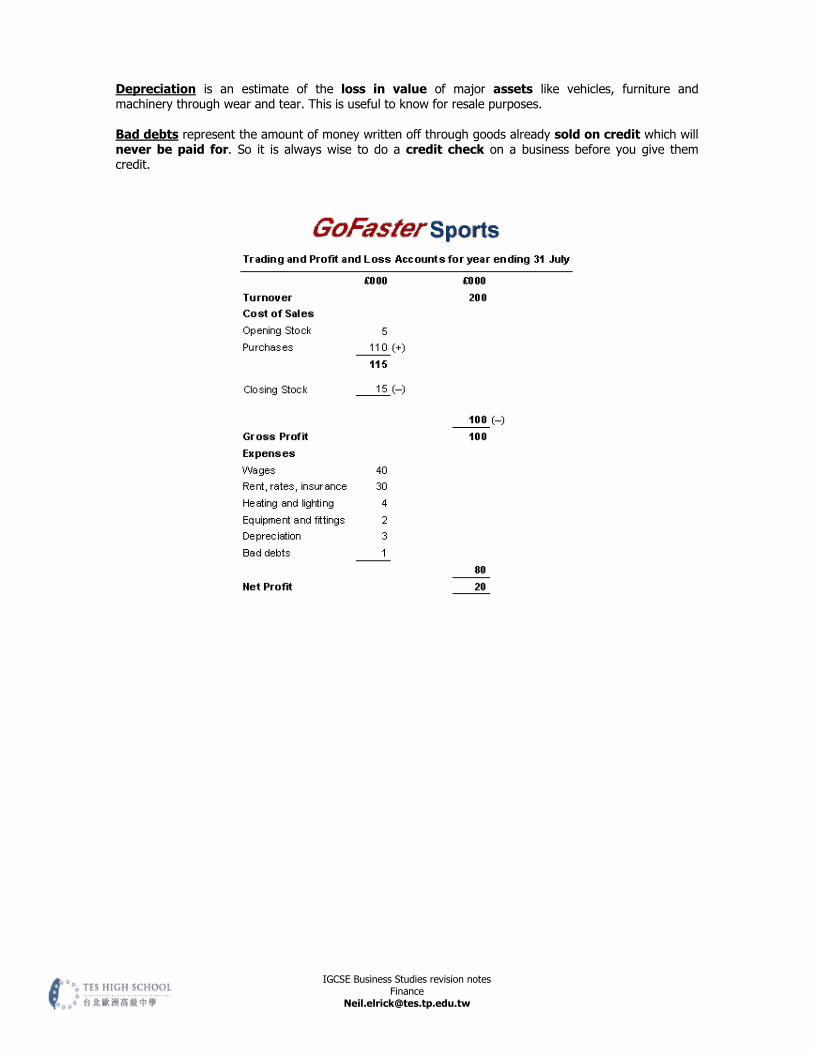

At the end of every trading year a business prepares final accounts. These provide a financial summary of all their trading activity during the year. The trading account shows the GROSS profit (or loss!) that the company has made.

Profit = income - expenses The profit and loss account shows the NET profit (or loss!) made. The trading account and profit and loss account are often combined into one, so that both the gross and net profit can be displayed in the same set of accounts. Look at the accounts below of a company called Go Faster Sports, a high-street retail outlet. The first part of the accounts is the trading account. Make sure you understand all the business terms which are underlined: Turnover shows the amount of revenue earned by the firm through the sale of goods at the marked up price (what is a mark-up?) Cost of sales shows how much they have spent on buying the goods at cost price before the firm has added its own profit margin (what is a profit margin?) The cost of sales is divided into three sections2:

1. Opening stock is the value of stock remaining unsold from the previous year.

2. Purchases are the amount spent on new stock during the current year.

3. Closing stock is the value of stock left unsold this year to be carried forward. The opening stock and purchases are added together. Then the closing stock is subtracted to give the cost of sales total of £100,000. (Make sure you understand how to work out the Cost of Sales! If you can’t do this, then you have to just stop there, and can’t get any further marks). This amount, the cost of sales total, is then subtracted from the turnover of £200,000 to give a gross profit of £100 000. The accounts then continue with the profit and loss account. They show the rest of the annual expenditure, which is the normal cost of running a business, plus depreciation and bad debts. These are deducted from the gross profit to give the true profit: the net profit.

2 you really must understand how to do this! In the end you’ll find it’s very easy! But it takes everybody a few times to go through it. If you can’t understand it in class, which is not at all unusual, then you must tell me so until you do. If you can’t work out the Gross Profit your marks stop there!

IGCSE Business Studies revision notes Finance

Depreciation is an estimate of the loss in value of major assets like vehicles, furniture and machinery through wear and tear. This is useful to know for resale purposes. Bad debts represent the amount of money written off through goods already sold on credit which will never be paid for. So it is always wise to do a credit check on a business before you give them credit.

IGCSE Business Studies revision notes Finance

BALANCE SHEETS

A balance sheet shows the value of a business. It shows what the business is worth. It shows what it owns and what it owes, in other words, its assets and its liabilities on a particular date. It is a “snapshot” of the business, and you can draw up a balance sheet at any time. (But the Trading and Profit and Loss account tells you how profitable the business has been over the past year). AASSSSEETTSS AANNDD LLIIAABBIILLIITTIIEESS An asset is something the business owns, such as machinery, land, buildings or money (eg cash in bank, or creditors invoices yet to be paid). There are two main types of asset –

1. fixed assets 2. current assets

FFIIXXEEDD AASSSSEETTSS A fixed asset is something the business owns and intends to keep for more than 12 months. There are three types of fixed assets:

1. Tangible fixed assets (physical items such as land, buildings, machinery, and vehicles, the purchase of which is known as ‘capital expenditure’).

2. Intangible fixed assets (non-physical items, which are very difficult to place a value on, such as brand names, and patents).

3. Financial fixed assets (investments that a business might have, such as shares in other companies)

CCUURRRREENNTT AASSSSEETTSS A current asset is also something the company owns, but it will probably be disposed of within 12 months. There are five types of current assets:

1. Cash in the bank. 2. Cash on the premises ("petty cash"). 3. Debtors (customers who have bought goods from the business on credit, and have not yet paid). They are called debtors because they owe you a debt. 4. Stock (raw materials, work-in-progress and unsold finished goods). 5. Prepayments (where the business has paid in advance for the use of something - rent for an

office, for example). LLAABBIILLIITTIIEESS A liability is money that the business owes to someone else or another business, and it has to be paid back.

IGCSE Business Studies revision notes Finance

There are two main types of liabilities: 1. long-term liabilities 2. current liabilities LLOONNGG TTEERRMM LLIIAABBIILLIITTIIEESS A long-term liability is something borrowed by the business for more than 12 months, but which still has to be paid back. There are three types of long-term liability that a company might have: 1. Bank loans. 2. Mortgages (a long-term loan to purchase land and buildings). 3. Debentures CCUURRRREENNTT LLIIAABBIILLIITTIIEESS A current liability is money the business owes to someone else, or another business, which will be paid back in less than 12 months. There are four main types of current liability. 1. Bank overdraft 2. Creditors (suppliers who the business has not yet paid). 3. Corporation tax (owed to the Government). 4. Dividends payable to shareholders in the business OOWWNNEERRSS FFUUNNDDSS TThhee ffiinnaall bbaallaanncciinngg iitteemm iiss tthhee mmoonneeyy tthhaatt tthhee oowwnneerrss ooff tthhee bbuussiinneessss iinnvveesstteedd.. TThhee bbuussiinneessss ssttiillll oowweess tthheemm tthhee mmoonneeyy,, ssoo iitt mmuusstt bbee sshhoowwnn.. TThheerree aarree ttwwoo mmaaiinn iitteemmss hheerree..

11.. OOwwnneerrss ccaappiittaall:: TThhee mmoonneeyy tthhaatt wwaass iinniittiiaallllyy iinnvveesstteedd iinn tthhee ffiirrmm.. 22.. RReettaaiinneedd pprrooffiitt ((RReesseerrvveess)):: TThhee ttoottaall ooff aallll ooff tthhee pprreevviioouuss yyeeaarrss rreettaaiinneedd pprrooffiittss ffrroomm tthhee

pprrooffiitt aanndd lloossss aaccccoouunntt.. Look at the balance sheet below for Go Faster Sports.

IGCSE Business Studies revision notes Finance

Make sure you thoroughly understand these (underlined) important business terms: Fixed assets shows the current value of major purchases that help in the running of the business, like delivery vans or PCs. In this case it is £40,000. This amount should be subtracted on the balance sheet. Current assets shows the cash or near-cash available to the firm. This includes stock ready to sell, money owed to them by debtors, and cash in the bank. Here the amount comes to £30,000. Current liabilities shows the short-term amounts that the firm owes. In this case they may have a short-term loan for £5,000. To calculate the net current assets, the current liabilities are subtracted from the current assets:

Net current assets = current assets – current liabilities

£30 000 - £5,000 = £25,000 This amount is added to the fixed assets value to give the net assets total: £40,000 + £25 000 = £65,000 Business finance: all businesses have to be financed. Initially this comes from the owners through the capital they invest, or from taking out long-term loans. All the financing has to be shown in this section of the accounts, and is added together to give the value of the business. In this case, the only financing is the capital and the net profit for the year:

IGCSE Business Studies revision notes Finance

£45,000 + £20,000 = £65,000 Remember The net assets total and the financing total must balance (in other words they must be the same). Capital and profits are also liabilities, because the firm owes this money to the owners. In other words: WHATEVER A FIRM OWNS, IT ALWAYS OWES IT TO SOMEONE! So the balance sheet must… balance!

IGCSE Business Studies revision notes Finance

RATIO ANALYSIS

RATIO CHECK SHEET Profitability Ratios 1 The gross profit margin 2 The net profit margin 3 Return on Capital Employed (R.O.C.E) Liquidity Ratios 4 The current ratio 5 The ‘acid-test’ ratio

When an exam question asks you to analyse the performance of a business over the last year, then this is what they want: RATIOS! They do not want a simple “The profit has gone up so that must be good.” Ratio analysis is used to measure a company’s

• profitability and

• solvency ( also known as liquidity) It does this by analysing its financial accounts (the balance sheet and the profit and loss account). Ratios are very easy to calculate! They enable a business to see which areas of its finances are weak and therefore require immediate attention. There are TWO main types of accounting ratio you need to know about:

1) PROFITABILITY (or “PERFORMANCE”) ratios. These analyse the profit made over the

last year.

2) SOLVENCY ( or “LIQUIDITY”) ratios. These measure the solvency of the business – in other words, its ability to meet short-term debts with cash it can find quickly.

PPRROOFFIITTAABBIILLIITTYY RRAATTIIOOSS We said before that he aim of businesses in the private sector is to make a profit. Profit is important in three ways:

1. It rewards the business people who have taken risks to run it

2. It provides the funds to develop the business further

3. It is a source of cash, which allows the business to meet its debts The purposes of a firm's Trading account and Profit and Loss account are to calculate and show the gross and net profits.

IGCSE Business Studies revision notes Finance

Ratios make it easier to compare one set of results with those of a previous year, or those of a competitor. You may have to answer questions in an exam about information given in a Trading account and Profit and Loss account, like Go Faster Sports below, and you may have to calculate

• The gross profit margin,

• The net profit margin

• The Return on Capital Employed (ROCE). The next section tells you exactly how to do it. It’s easy! GGRROOSSSS PPRROOFFIITT MMAARRGGIINN Question Calculate Go Faster Sports' gross profit margin. To calculate the gross profit margin, use the following equation: Gross Profit Margin = gross profit/turnover x 100 Answer Go Faster's Gross Profit Margin would therefore be: £100,000/£200,000 x 100 = 50%

NNEETT PPRROOFFIITT MMAARRGGIINN Question Calculate Go Faster Sports' net profit margin. Calculate the net profit margin, in the same way: Net Profit Margin = net profit/turnover x 100 Answer Go Faster's Net Profit Margin would therefore be:

£20,000/£200,000X 100 = 10% If you were asked in the exam to comment on Go Faster's profitability, you could say their gross profit margin of 50% is fairly healthy, but the net profit margin of only 10% is not very good. It suggests that Go-Faster's expenditure relative to income is higher than they might want. The management might look for ways to cut costs, for example by reducing their wage bill, which is quite high.

IGCSE Business Studies revision notes Finance

RREETTUURRNN OONN CCAAPPIITTAALL EEMMPPLLOOYYEEDD ((RROOCCEE)) RRAATTIIOO Investors want to know how much profit their capital investment is making for them. This also applies to prospective shareholders. The ROCE is an important indicator of how efficiently a business is being managed. To get a meaningful picture, Go Faster Sports results this year would have to be compared with those of previous years, and with those of their competitors. The equation for calculating the Return on Capital Employed is: ROCE = net profit/capital employed x 100 Question Look at Go Faster Sports' Trading and Profit and Loss accounts. It gives information for the year ending 31 July. Try and work out the Return on Capital Employed before checking the answer. Trading and Profit and Loss Accounts for the year ending 31 July

To calculate the ROCE use the equation: ROCE = net profit/capital employed x 100 Answer This makes Go Faster's ROCE: £20,000/£65,000 x 100 = 30.77%

IGCSE Business Studies revision notes Finance

This represents a good investment. The amount being earned per pound (£0.31 rounded up) is much higher than most alternative investments would offer, such as a building society savings account. Remember The results in themselves, however, mean little, unless they are compared with previous company results or those of their competitors.

SSOOLLVVEENNCCYY RRAATTIIOOSS All businesses need to know how well or how badly they are performing. This next section uses simple calculations to assess solvency. It covers:

• Working capital • Current ratio • Acid test / liquid assets ratio

Remember There are many groups of people who are interested in the published accounts of a company. The information these accounts provide may influence future decisions. For example, lenders will always be looking at the solvency of a business. Why? A business is solvent if it can meet its short-term debts when they are due for payment. To do this it needs adequate working capital. There are 3 main reasons why a business needs adequate working capital. It must:

1. pay staff wages and salaries

2. settle debts and therefore avoid legal action by creditors

3. benefit from cash discounts offered in return for prompt payment You can calculate a firm's working capital by using the following equation: Working capital = current assets - current liabilities Question Go-Faster Sports is a high street retailer dealing in sports equipment. Look at its balance sheet below and calculate its working capital.

IGCSE Business Studies revision notes Finance

You can see that: current assets amount to £30,000 current liabilities amount to £5,000 Answer The result is £30,000 - £5,000 = £25,000 working capital. Notice this is the same amount as the net current assets.

CCUURRRREENNTT RRAATTIIOO Lenders need to know that Go Faster will be able to repay any credit they are given in the short-term. It provides information on its ability to meet its short-term debts by publishing its current ratio. This assesses how many times it could afford to pay its current liabilities out of its current assets. Here is the equation you should learn: current ratio = current assets/current liabilities Simple, isn’t it? Now look at Go Faster Sports Balance sheet and calculate its current ratio using this formula.

IGCSE Business Studies revision notes Finance

You will see that it is:

£30,000/£5,000 = 6/1 = 6:1 This ratio shows us that it could afford to pay its liabilities six times from its current assets.

AACCIIDD TTEESSTT // LLIIQQUUIIDD AASSSSEETTSS RRAATTIIOO Another measure of liquidity is the acid test/liquid assets ratio. This deducts the value of currently held stock to find the company's ability to meet (pay) its liabilities immediately. Stock is the least liquid current asset so it is deducted to give a more realistic view of the company's liquidity. Learn this equation. You may be asked to calculate the acid test ratio in an exam. acid test = current assets - closing stock/current liabilities Now look at Go Faster Sport's balance sheet and calculate the acid test / liquid assets ratio. You will see it is:

£30,000 - £15,000/£5,000 = £15,000/£5,000 = 3/1 = 3:1 This shows us that Go Faster can afford to pay their short-term debts three times over immediately without selling any stock.

IGCSE Business Studies revision notes Finance

Break Even Analysis

This is a way of investigating ‘What if…’ scenarios. E.g. “What if we put our prices up? What if we increase sales by 10%? It looks at how much profit (or loss) a firm will make at a certain level of output. IT DOES NOT

MEAN THIS WILL ACTUALLY HAPPEN. JUST, IF IT DOES HAPPEN, WHAT THE CONSEQUENCES WILL BE.

COSTS One way of dividing up the costs (The money that a business spends on keeping the business going, it does not include the buying of things (assets) that a business will keep.) of a business is into … FIXED COSTS: Those that do not change in PROPORTION to levels of output. For example, rent, insurance, lighting. This is similar to indirect costs. They are not normally directly linked to making the product. And are measured per time (month; year; etc.). It is

really important that you NEVER say that they cannot change. For example, your rent could go up, but not because you are producing more, just because your landlord has put the rent up. VARIABLE COSTS: Those that change in PROPORTION to levels of output. For example, raw materials, direct labour etc. This is similar to direct costs, they are needed to make the product. And are per unit, so you can easily spot them. To calculate the TOTAL COSTS of a business the following formula is used.

= Fixed costs + (variable costs * output) Set against this is the organisation’s income. This is calculated by the following formula,

= Price * Quantity sold

Many organisations are interested in their BREAK EVEN POINT. This is where profit = 0. If an organisation sells more than this it will make a profit. If it sells less then it will make a loss. There are two ways of working out the break-even point. (How many we need to sell to make a profit of 0. BY FORMULA

Fixed costs Price – Variable cost

This can also be used for calculating the output needed to gain a certain amount of profit (π). This is a popular exam question

Output needed = Fixed costs + π Price – variable cost

It can also be calculated and shown graphically… (see 10 steps to Break even)

1. Draw and label axis, x is output, y is money. If you are unsure what to go up to, look in the

question for ‘How much profit & loss is made when x are made?’, and use that for the x axis, for the y axis, multiply this by the price. Do not be afraid to redraw your graph if you need to, it will take seconds.

2. Add up all the fixed costs and draw a HORIZONTAL line from this point on the y axis. And label it fixed costs

3. Add up all the variable costs to give us the variable cost per unit. Find a handy number on the x axis (like 100 or 1000 or something), and multiply this number by the variable cost per unit. Plot this point, join it up to the origin, and extend it rightwards too. And label it variable costs

4. Draw a line parallel to the variable cost line, but starting where the fixed cost line cuts the y axis. Label this one total costs.

IGCSE Business Studies revision notes Finance

5. Next add in the revenue. Repeat step 3, but this time use price rather than variable cost. Label this line revenue.

6. The break even point is where the total cost and revenue lines cross. MEASURE DOWN TO FIND THE BREAK EVEN QUANTITY.

7. Check this is correct by using the formula. 8. Take a deep breath, and now think! Usually, an exam question will ask you to find how much

profit (or loss) (they always put (loss) in brackets) the firm will make if they sell so many. This is easy! Profit is, as we all know, the difference between what we spend (total cost), and what we get in (revenue). Find the right amount on the x axis, and draw a dotted line straight up to where it crosses the highest line on graph (Hopefully the revenue line). Measure across from this point. Now, follow the dotted line down until it crosses the total cost line, again measure across horizontally. The VERTICAL difference between these two points is the profit (or loss).

9. Double check you have done step 8 right by using the formula. 10. To complete your graph, draw on the margin of safety. The question will tell you how much they

are making. It is the distance along the x axis from this amount to the break even point. Easy peasy. So don’t slip up!

We need to remember that increasing the price will lower the break even point (and increase profits. But only if we can sell at this higher price. (It will depend upon price elasticity of demand, and the rest of the marketing mix for loads of bonus points). Break even assumes:

1. No economies of scale 2. We sell all that we make. 3. Don’t have to lower the price to sell more.