ifc jd power cologne global outlook 29 apr 10 10 04 26 ep

TRANSCRIPT

Financing the Automotive Sector in Emerging Markets …

… in an incredibly fast changing world !

Emmanuel POULIQUEN

Principal Industry Specialist, Energy Efficient Machinery

JD Power Automotive Forecasting Global Outlook Conference

Köln – 29 Apr 2010

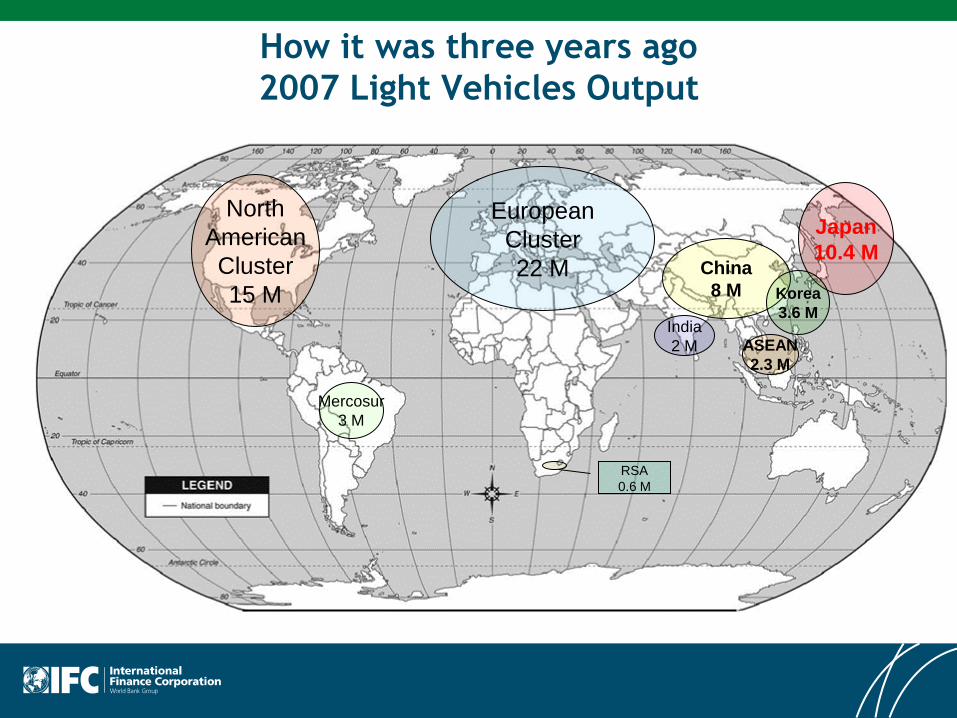

How it was three years ago

2007 Light Vehicles Output

2

Page 2

North

American

Cluster

15 M

European

Cluster

22 M

Mercosur

3 M

China

8 M

Japan

10.4 M

India

2 M ASEAN

2.3 M

Korea

3.6 M

RSA

0.6 M

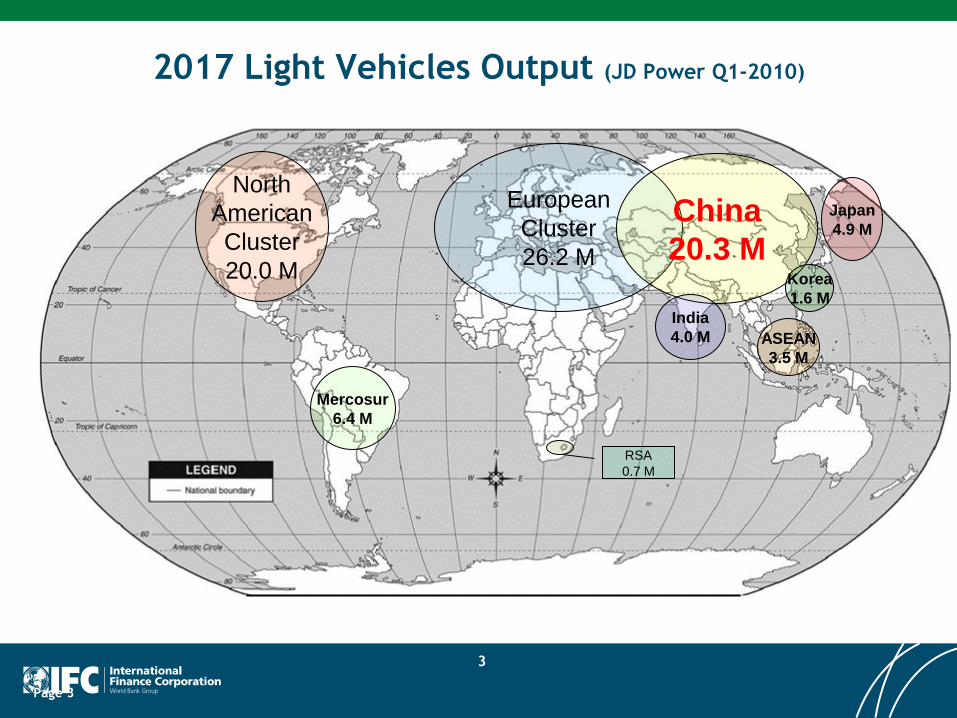

2017 Light Vehicles Output (JD Power Q1-2010)

3

Page 3

North

American

Cluster

20.0 M

European

Cluster

26.2 M

Mercosur

6.4 M

China

20.3 M

Japan

4.9 M

India

4.0 M ASEAN

3.5 M

Korea

1.6 M

RSA

0.7 M

How fast things go !

• JD Power Paris Round table – September 2006

“Is Asia a global threat ?”

“… The end of the Old Auto World ???”

“Leverage your continent”

• 2008-2009

Largest global financial crisis since the Great Depression

• GM & Chrysler saved from the grave – are they still Zombie ?

• US Market sales fall from 16.1 M in 2007 to 10.4 M Light Vehicles in

2009

While the developed countries car businesses collapse, governments

inject massive amounts of deficit financed cash to save (or resuscitate)

the Industry

Fearing to go below 6% GDP growth, China pumps money in its own

Industry … so much that 2009 becomes a boom year with sales of nearly

13M light Vehicles !

4

Well, you know …

• “… Chinese cars are not American cars ! (and even less

European or Japanese ones !)”

Crash test !

Emissions !

Quality !

Bells and whistles (?)

Efficiency (!?)

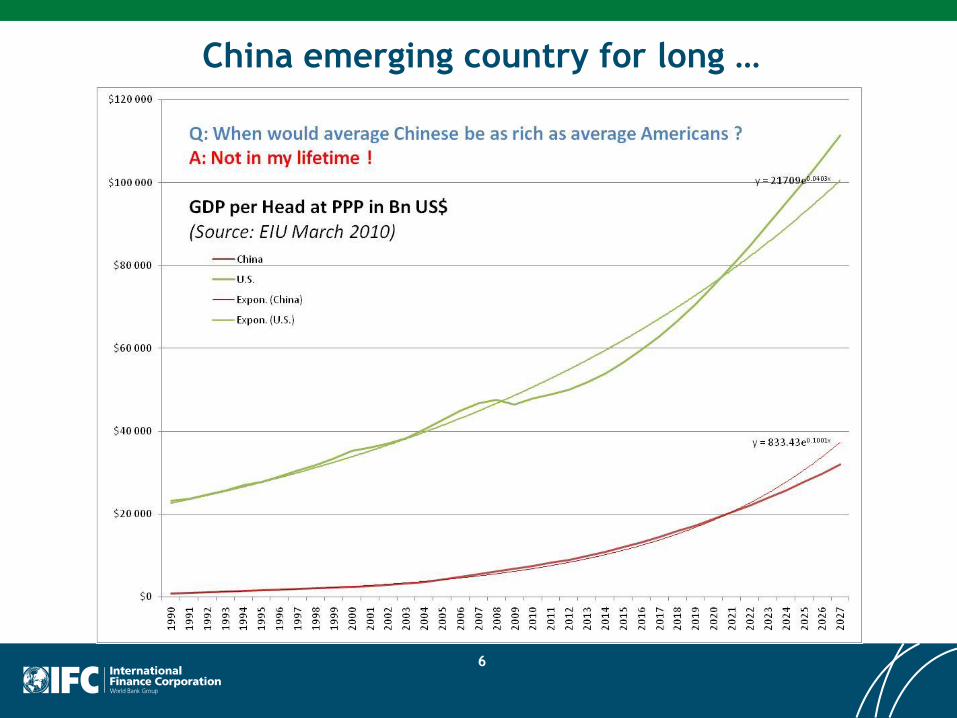

• “Anyway, China is still an emerging country for long and they

only make cheap cars for lower income people !”

• … but, well, perhaps we should pay attention a bit more ?

BYD ?

Tibet ?

Africa ?

5

China emerging country for long …

6

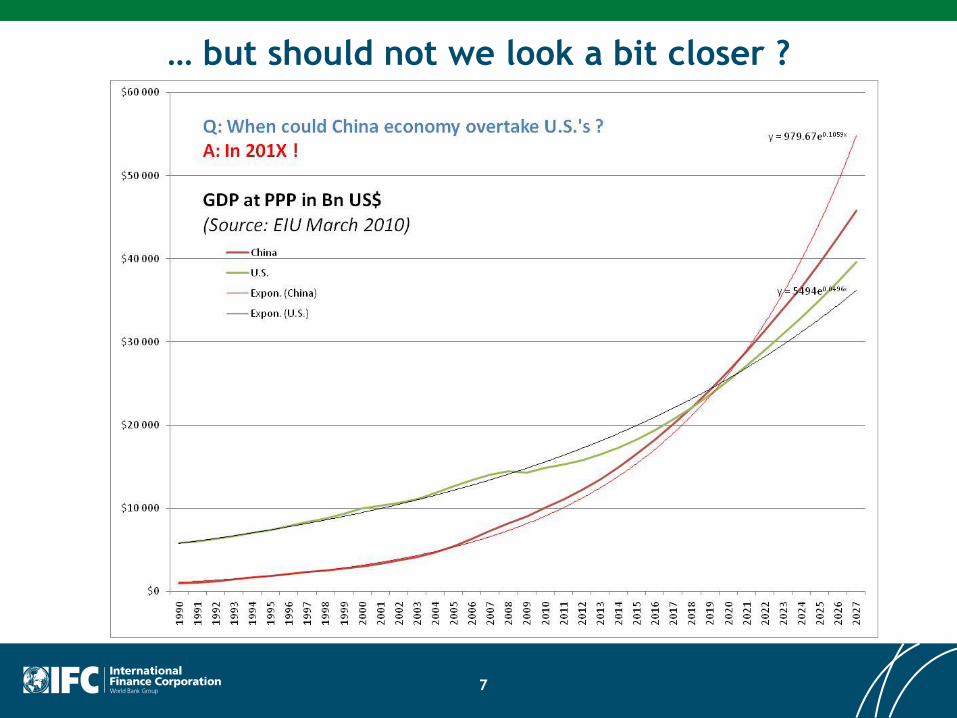

… but should not we look a bit closer ?

7

The path to 50 M Chinese Cars per year

• How many cars per year in China in the end ?

• In 2010:

Japanese model: 128.3 M People – 60 M Car Parc – 5 M Light Vehicles Sold

Car Sales = Car Parc (U.S. model: Car Sales = Car Parc / 20)

12

China: 1 331.4 M People – 40 M Car Parc

• The Japanese model would give 622 M Car Parc in China 50 M Light

Vehicles Market (U.S. model: 30 M Light Vehicles Market)

• How long will the growth last ?

2003: 2.36 M Cars Sold 2010: 9.6 M Cars Sold CAGR = 22.1% !

At 22.1% growth per year, 50 M Cars yearly sales would be reached in less

than 9 years

… 600 M cars on the Chinese roads by the end of next decade ???

8

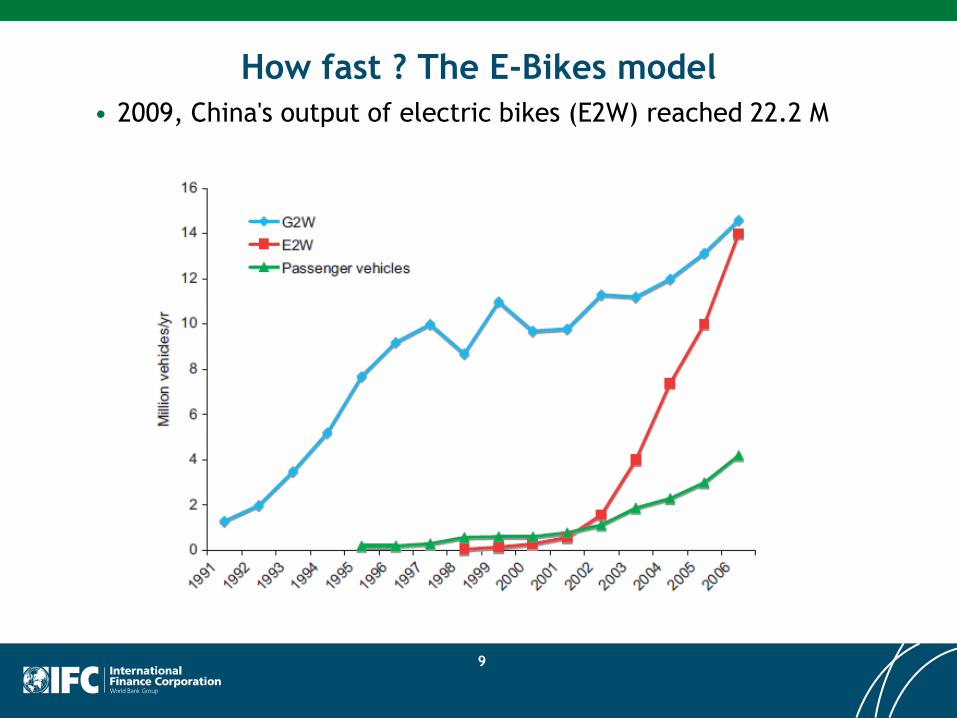

How fast ? The E-Bikes model

• 2009, China's output of electric bikes (E2W) reached 22.2 M

9

Not a Chinese Tsunami ! (but …)

• 中国 = Country in the Middle = Self Centric – and pragmatic !

• Not a Japanese or Korean export model

Largest internal market in history

No former American protectorate

• 1980-2000: Get hard currencies to pay for technology

Export whatever you can (From Barbie dolls to TV sets and PCs)

Import technology and business know-how

• 2000-2010: Prime the internal demand era

Grow the industry and expand technical know-how towards hi-tech

• 2011 and later: Internal demand attractiveness beats all markets

Similar to the U.S. from 1900 to 1929 … but 15 times larger

Exports still needed for offsetting raw materials/energy imports

Flows of exports accelerate with Africa and South-America in line with imports

Yuan becomes the reference trade currency for Africans … and others (?)

11

In the mean time …

• Confederate Europe expands its cluster to Middle east (500 M consumers

with Oil, Gas, Solar and Nuclear Energy)

North Africa and Turkey complement Eastern Europe as growth centers

Cluster stability around the Euro

Internal cluster industrial exchanges most important

• Astonished America is no more number one and must turn to frugality

The Illness:

• Hardest hit by inflation of oil and raw materials

• Hardest hit by the diminishing power of the Dollar

• Hardest hit by its national deficit

A Cure: Considers “the confederation of NAFTA” - Strengthened Cluster

• South-America (Brazil cluster) grows well and learns to love China

• Japan and Korea become China economic protectorates

• India continues a difficult adolescence and re-explores links with Russia

12

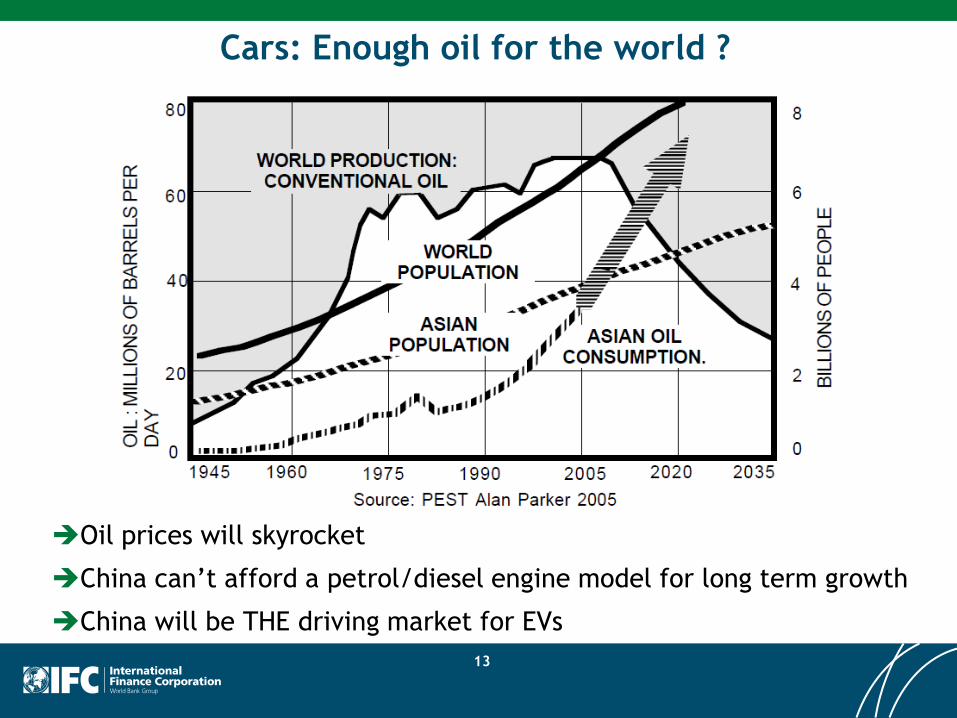

Cars: Enough oil for the world ?

Oil prices will skyrocket

China can’t afford a petrol/diesel engine model for long term growth

China will be THE driving market for EVs

13

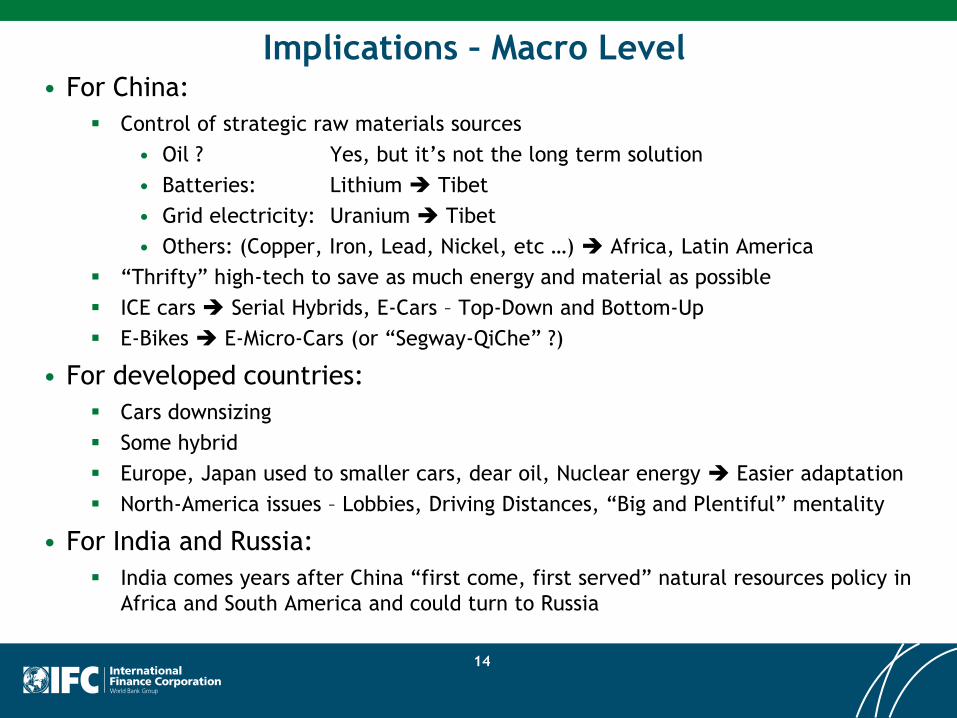

Implications – Macro Level • For China:

Control of strategic raw materials sources

• Oil ? Yes, but it’s not the long term solution

• Batteries: Lithium Tibet

• Grid electricity: Uranium Tibet

• Others: (Copper, Iron, Lead, Nickel, etc …) Africa, Latin America

“Thrifty” high-tech to save as much energy and material as possible

ICE cars Serial Hybrids, E-Cars – Top-Down and Bottom-Up

E-Bikes E-Micro-Cars (or “Segway-QiChe” ?)

• For developed countries:

Cars downsizing

Some hybrid

Europe, Japan used to smaller cars, dear oil, Nuclear energy Easier adaptation

North-America issues – Lobbies, Driving Distances, “Big and Plentiful” mentality

• For India and Russia:

India comes years after China “first come, first served” natural resources policy in

Africa and South America and could turn to Russia

14

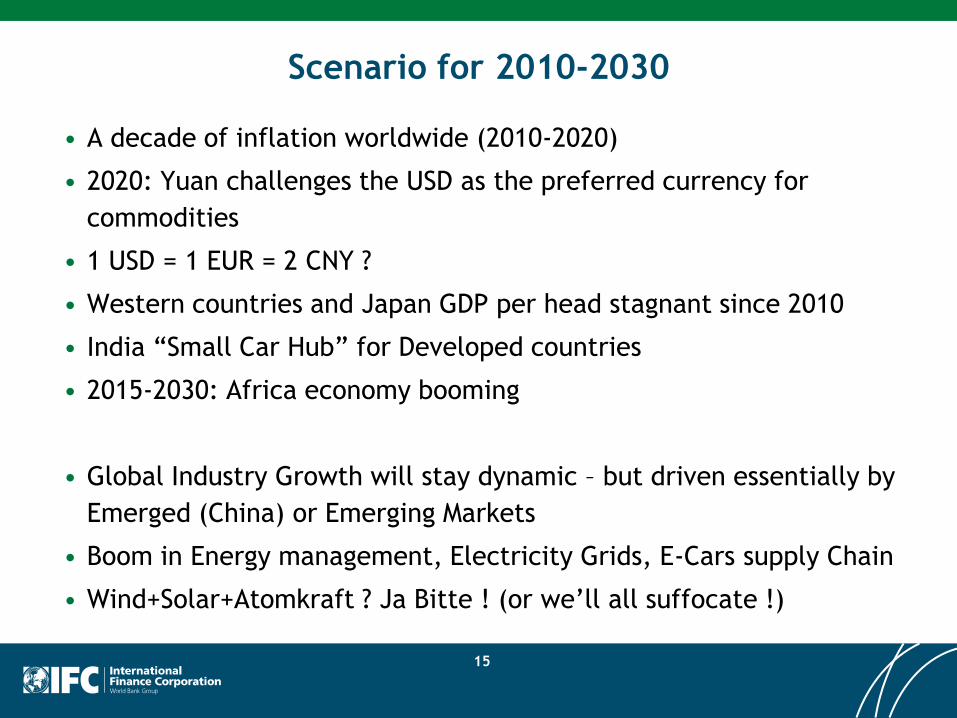

Scenario for 2010-2030

• A decade of inflation worldwide (2010-2020)

• 2020: Yuan challenges the USD as the preferred currency for

commodities

• 1 USD = 1 EUR = 2 CNY ?

• Western countries and Japan GDP per head stagnant since 2010

• India “Small Car Hub” for Developed countries

• 2015-2030: Africa economy booming

• Global Industry Growth will stay dynamic – but driven essentially by

Emerged (China) or Emerging Markets

• Boom in Energy management, Electricity Grids, E-Cars supply Chain

• Wind+Solar+Atomkraft ? Ja Bitte ! (or we’ll all suffocate !)

15

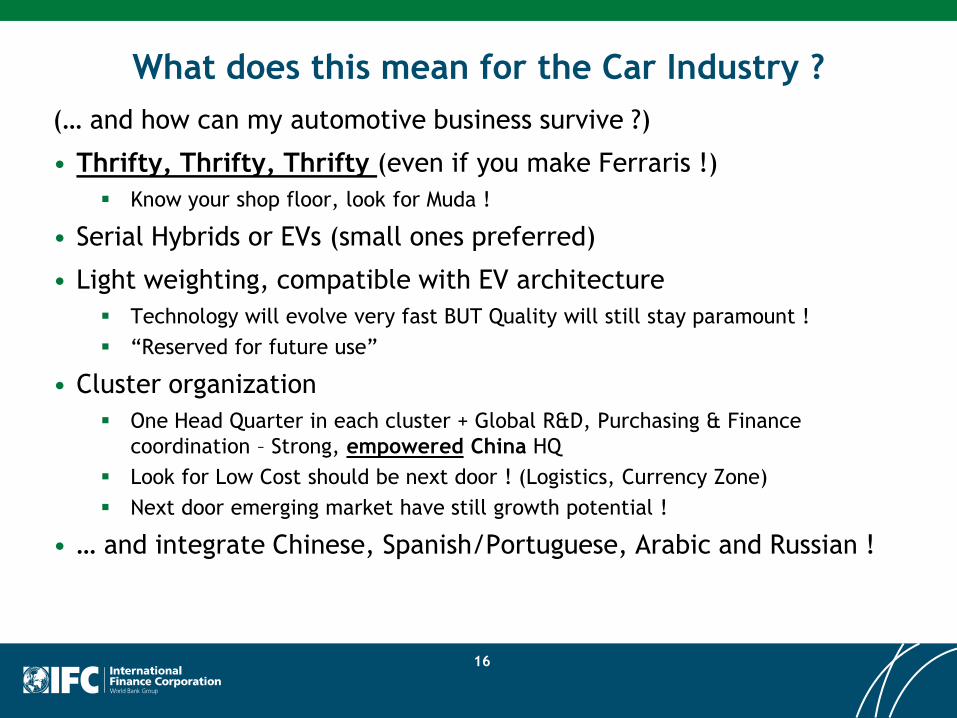

What does this mean for the Car Industry ?

(… and how can my automotive business survive ?)

• Thrifty, Thrifty, Thrifty (even if you make Ferraris !)

Know your shop floor, look for Muda !

• Serial Hybrids or EVs (small ones preferred)

• Light weighting, compatible with EV architecture

Technology will evolve very fast BUT Quality will still stay paramount !

“Reserved for future use”

• Cluster organization

One Head Quarter in each cluster + Global R&D, Purchasing & Finance

coordination – Strong, empowered China HQ

Look for Low Cost should be next door ! (Logistics, Currency Zone)

Next door emerging market have still growth potential !

• … and integrate Chinese, Spanish/Portuguese, Arabic and Russian !

16

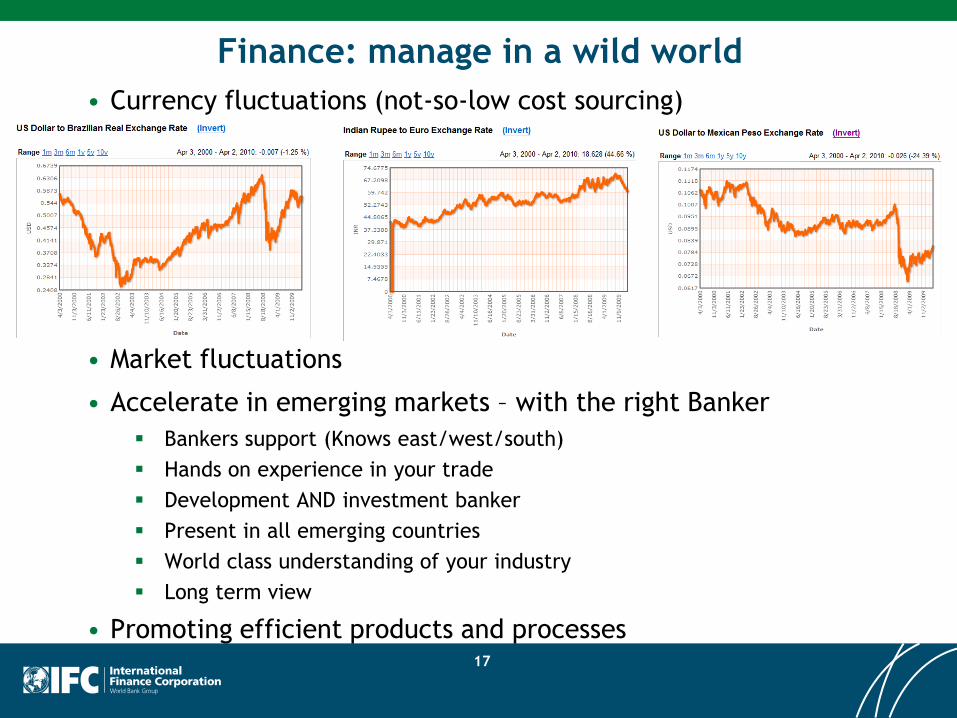

Finance: manage in a wild world

17

• Currency fluctuations (not-so-low cost sourcing)

• Market fluctuations

• Accelerate in emerging markets – with the right Banker

Bankers support (Knows east/west/south)

Hands on experience in your trade

Development AND investment banker

Present in all emerging countries

World class understanding of your industry

Long term view

• Promoting efficient products and processes

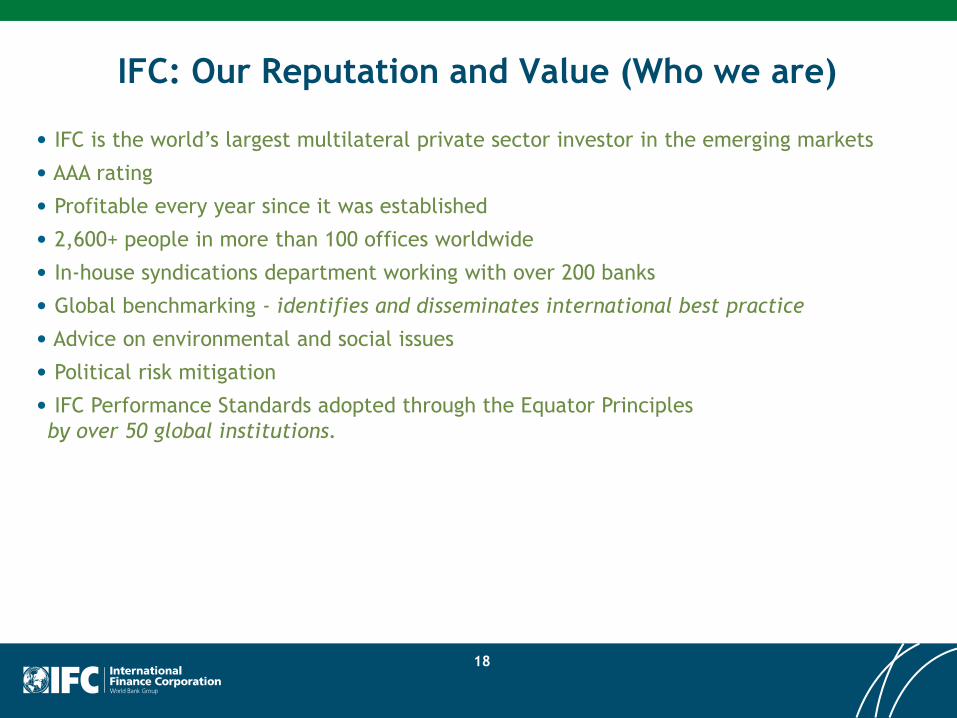

• IFC is the world’s largest multilateral private sector investor in the emerging markets

• AAA rating

• Profitable every year since it was established

• 2,600+ people in more than 100 offices worldwide

• In-house syndications department working with over 200 banks

• Global benchmarking - identifies and disseminates international best practice

• Advice on environmental and social issues

• Political risk mitigation

• IFC Performance Standards adopted through the Equator Principles

by over 50 global institutions.

IFC: Our Reputation and Value (Who we are)

18

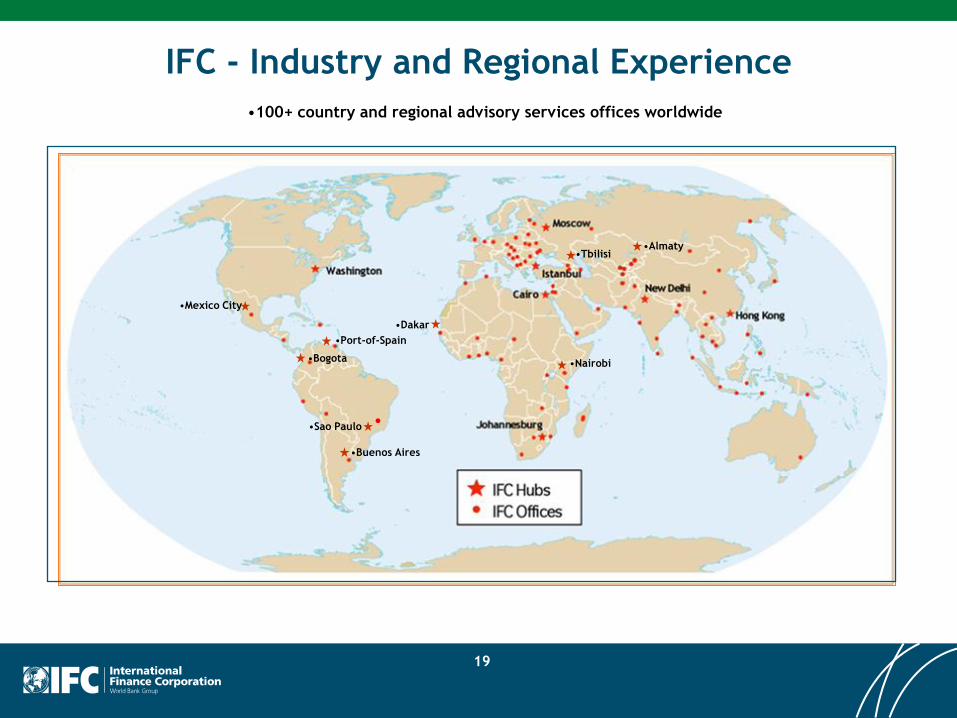

•100+ country and regional advisory services offices worldwide

•Port-of-Spain

•Bogota

•Buenos Aires

•Sao Paulo

•Mexico City

•Dakar

•Nairobi

•Tbilisi •Almaty

IFC - Industry and Regional Experience

19

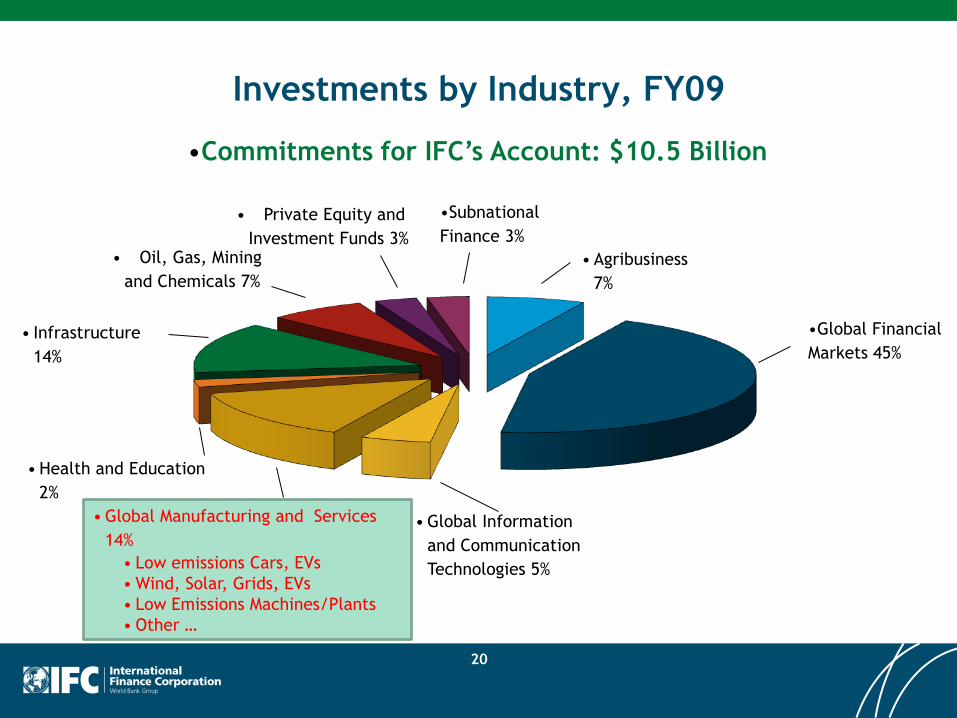

Investments by Industry, FY09

20

•Global Financial

Markets 45%

•Commitments for IFC’s Account: $10.5 Billion

• Global Information

and Communication

Technologies 5%

• Global Manufacturing and Services

14%

• Low emissions Cars, EVs

• Wind, Solar, Grids, EVs

• Low Emissions Machines/Plants

• Other …

• Infrastructure

14%

•Subnational

Finance 3%

• Health and Education

2%

• Oil, Gas, Mining

and Chemicals 7%

• Private Equity and

Investment Funds 3%

• Agribusiness

7%

IFC Strategic Priorities

• Strengthening the focus on frontier markets – IDA countries,

poorer regions of middle-income countries, conflict affected

and fragile states, and industries with the broadest potential

for development impact

• Building enduring partnerships with emerging market players

• Addressing climate change and ensuring environmental and

social sustainability

• Promoting private sector growth in infrastructure, health,

education, and the food supply chain

• Developing local financial markets

21

IFC’s Business (What we do) Investment Services

• Loans and intermediary services

• Equity and quasi-equity

• Syndications

• Structured and securitized products

• Risk management products

• Trade finance

• Subnational finance

• Treasury operations

• CleanTech Venture Capital

22

IFC Offers to Clients (What we bring) Unparalleled Expertise

• Knowledge of global industries and local markets

• Financial sector influence

• Long-term partnerships; countercyclical role

• Sustainable investments

• Leadership on corporate governance

• Value-adding expertise

23

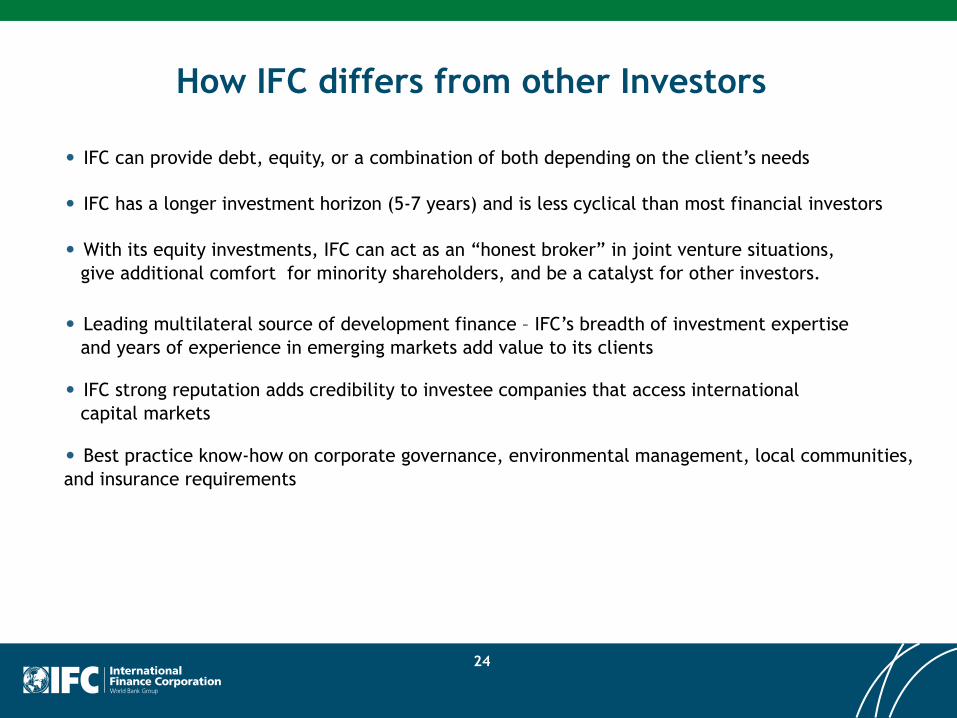

• IFC can provide debt, equity, or a combination of both depending on the client’s needs

• IFC has a longer investment horizon (5-7 years) and is less cyclical than most financial investors

• With its equity investments, IFC can act as an “honest broker” in joint venture situations,

give additional comfort for minority shareholders, and be a catalyst for other investors.

• Leading multilateral source of development finance – IFC’s breadth of investment expertise

and years of experience in emerging markets add value to its clients

• IFC strong reputation adds credibility to investee companies that access international

capital markets

• Best practice know-how on corporate governance, environmental management, local communities,

and insurance requirements

How IFC differs from other Investors

24

Questions ?

Mr. Emmanuel POULIQUEN (普迈新)

Principal Industry Specialist

IFC - Global Manufacturing & Services – Energy Efficient Machinery

Financing production and deployment of equipment that

efficiently generate, store, transport or transform energy

http://www.ifc.org/ifcext/gms.nsf/Content/EEM_Overview

2121 Pennsylvania Ave., NW

Washington, DC 20433

Tel: +1 (202) 473-9114 Fax: +1 (202) 974-4394

Email: [email protected]

25

Appendixes

26

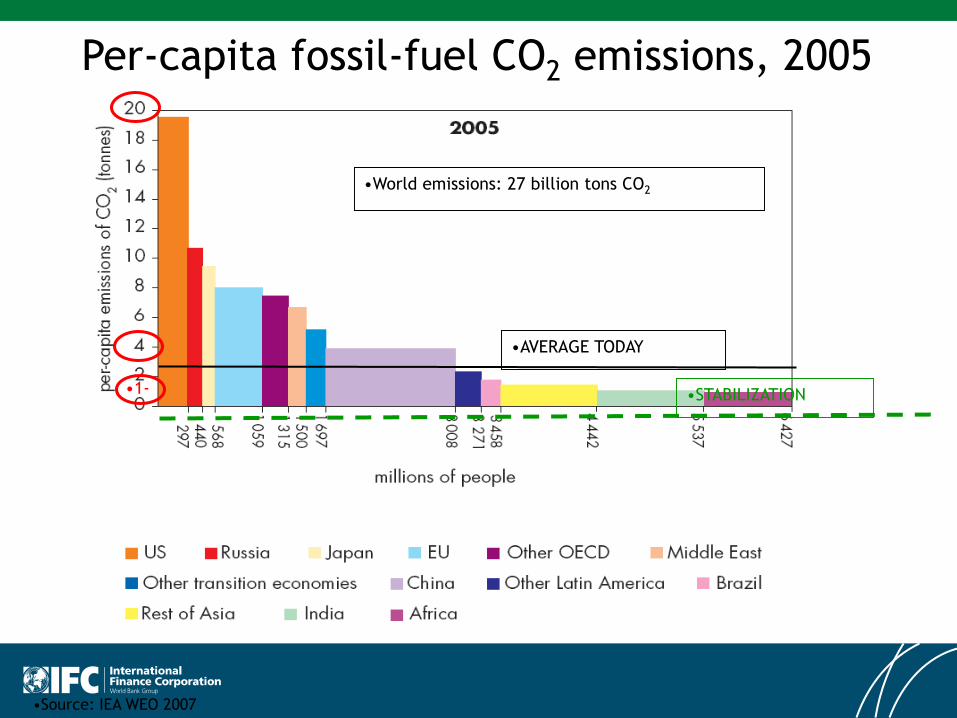

•Source: IEA WEO 2007

Per-capita fossil-fuel CO2 emissions, 2005

•1-

•World emissions: 27 billion tons CO2

•STABILIZATION

•AVERAGE TODAY

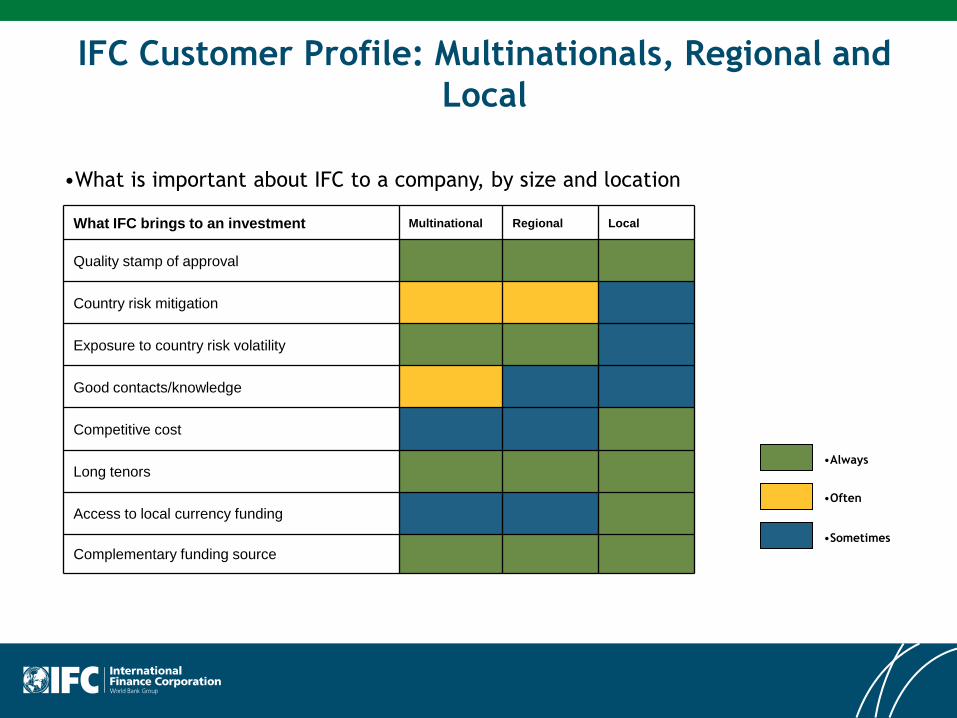

What IFC brings to an investment Multinational Regional Local

Quality stamp of approval

Country risk mitigation

Exposure to country risk volatility

Good contacts/knowledge

Competitive cost

Long tenors

Access to local currency funding

Complementary funding source

•What is important about IFC to a company, by size and location

•Always

•Often

•Sometimes

IFC Customer Profile: Multinationals, Regional and

Local

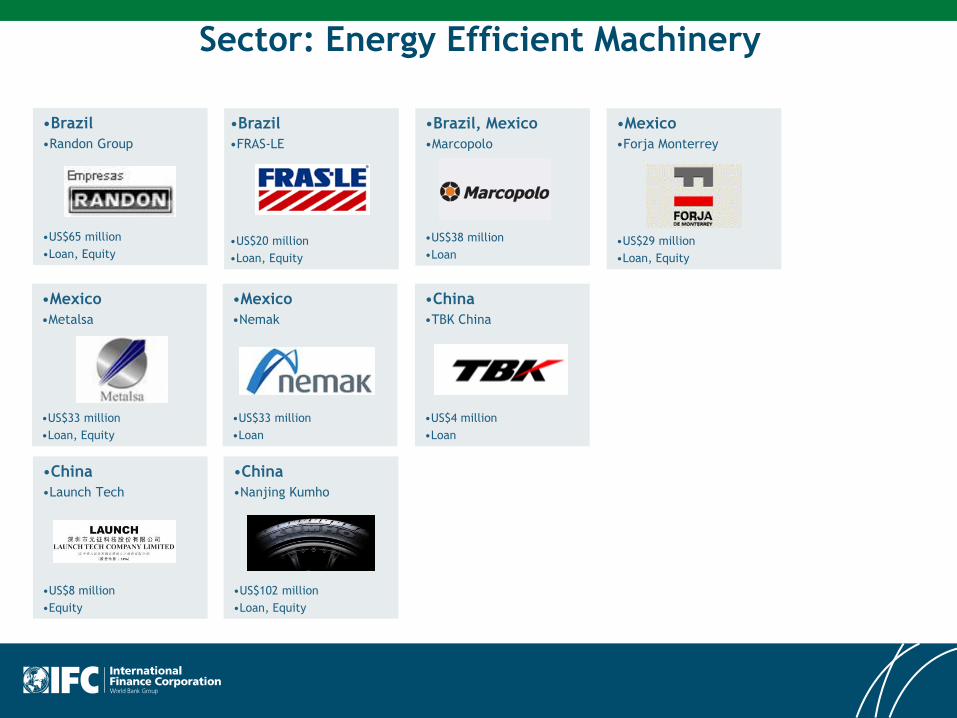

•Brazil

•Randon Group

•US$65 million

•Loan, Equity

•Brazil

•FRAS-LE

•US$20 million

•Loan, Equity

•Brazil, Mexico

•Marcopolo

•US$38 million

•Loan

•Mexico

•Forja Monterrey

•US$29 million

•Loan, Equity

•China

•Launch Tech

•US$8 million

•Equity

•China

•Nanjing Kumho

•US$102 million

•Loan, Equity

•Mexico

•Metalsa

•US$33 million

•Loan, Equity

•Mexico

•Nemak

•US$33 million

•Loan

•China

•TBK China

•US$4 million

•Loan

Sector: Energy Efficient Machinery

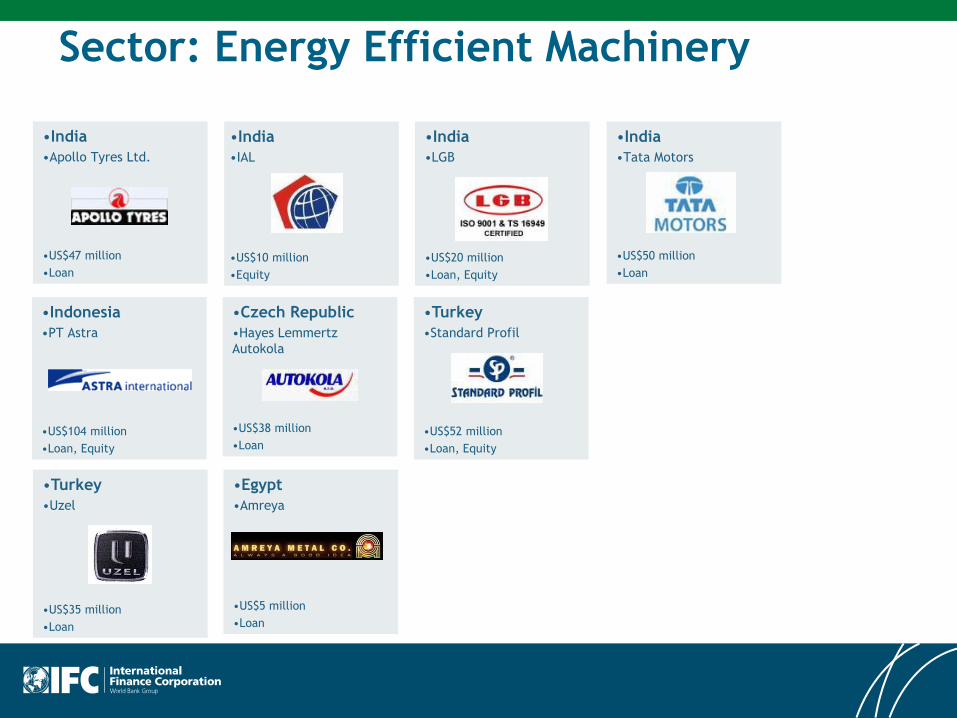

•India

•Apollo Tyres Ltd.

•US$47 million

•Loan

•India

•IAL

•US$10 million

•Equity

•India

•LGB

•US$20 million

•Loan, Equity

•India

•Tata Motors

•US$50 million

•Loan

•Turkey

•Uzel

•US$35 million

•Loan

•Egypt

•Amreya

•US$5 million

•Loan

•Indonesia

•PT Astra

•US$104 million

•Loan, Equity

•Czech Republic

•Hayes Lemmertz

Autokola

•US$38 million

•Loan

•Turkey

•Standard Profil

•US$52 million

•Loan, Equity

Sector: Energy Efficient Machinery