idc marketscape: worldwide enterprise wlan 2015 2016

TRANSCRIPT

December 2015, IDC #US40653915e

IDC MarketScape

IDC MarketScape: Worldwide Enterprise WLAN 2015–2016 Vendor Assessment

Nolan Greene Rohit Mehra

THIS IDC MARKETSCAPE EXCERPT FEATURES: FORTINET-MERU

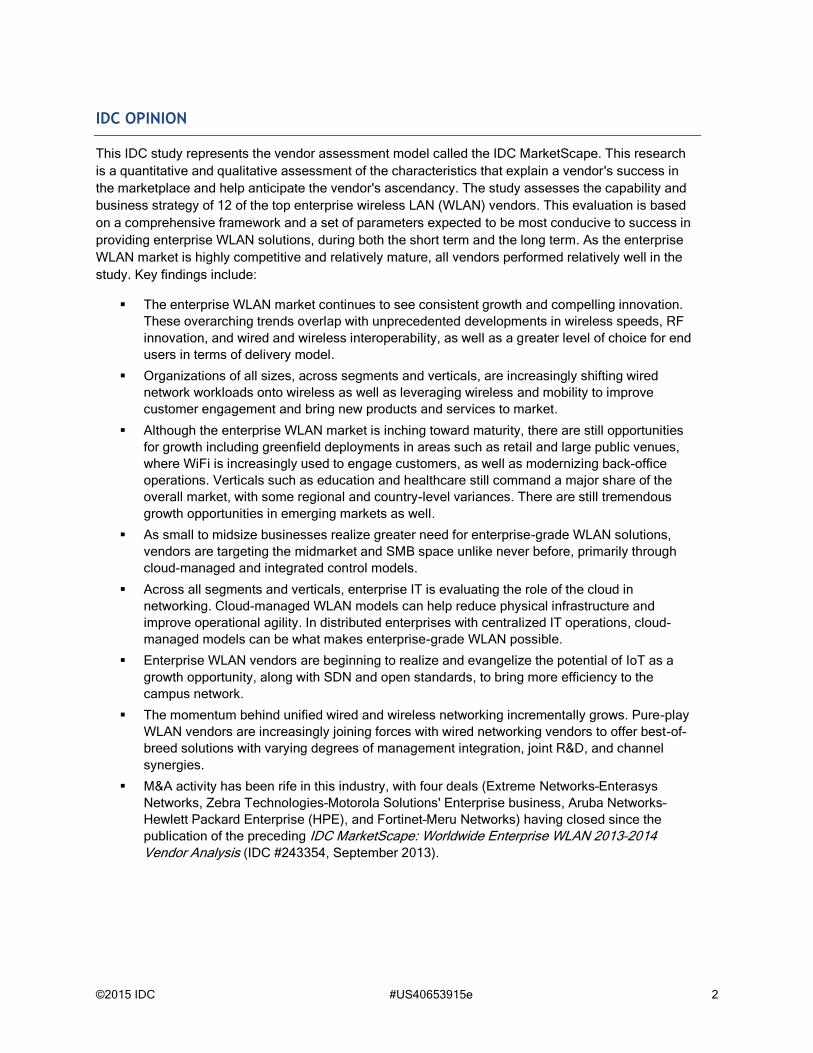

IDC MARKETSCAPE FIGURE

FIGURE 1

IDC MarketScape Worldwide Enterprise WLAN Vendor Assessment

Source: IDC, 2015

Please see the Appendix for detailed methodology, market definition, and scoring criteria.

©2015 IDC #US40653915e 2

IDC OPINION

This IDC study represents the vendor assessment model called the IDC MarketScape. This research

is a quantitative and qualitative assessment of the characteristics that explain a vendor's success in

the marketplace and help anticipate the vendor's ascendancy. The study assesses the capability and

business strategy of 12 of the top enterprise wireless LAN (WLAN) vendors. This evaluation is based

on a comprehensive framework and a set of parameters expected to be most conducive to success in

providing enterprise WLAN solutions, during both the short term and the long term. As the enterprise

WLAN market is highly competitive and relatively mature, all vendors performed relatively well in the

study. Key findings include:

The enterprise WLAN market continues to see consistent growth and compelling innovation.

These overarching trends overlap with unprecedented developments in wireless speeds, RF

innovation, and wired and wireless interoperability, as well as a greater level of choice for end

users in terms of delivery model.

Organizations of all sizes, across segments and verticals, are increasingly shifting wired

network workloads onto wireless as well as leveraging wireless and mobility to improve

customer engagement and bring new products and services to market.

Although the enterprise WLAN market is inching toward maturity, there are still opportunities

for growth including greenfield deployments in areas such as retail and large public venues,

where WiFi is increasingly used to engage customers, as well as modernizing back-office

operations. Verticals such as education and healthcare still command a major share of the

overall market, with some regional and country-level variances. There are still tremendous

growth opportunities in emerging markets as well.

As small to midsize businesses realize greater need for enterprise-grade WLAN solutions,

vendors are targeting the midmarket and SMB space unlike never before, primarily through

cloud-managed and integrated control models.

Across all segments and verticals, enterprise IT is evaluating the role of the cloud in

networking. Cloud-managed WLAN models can help reduce physical infrastructure and

improve operational agility. In distributed enterprises with centralized IT operations, cloud-

managed models can be what makes enterprise-grade WLAN possible.

Enterprise WLAN vendors are beginning to realize and evangelize the potential of IoT as a

growth opportunity, along with SDN and open standards, to bring more efficiency to the

campus network.

The momentum behind unified wired and wireless networking incrementally grows. Pure-play

WLAN vendors are increasingly joining forces with wired networking vendors to offer best-of-

breed solutions with varying degrees of management integration, joint R&D, and channel

synergies.

M&A activity has been rife in this industry, with four deals (Extreme Networks–Enterasys

Networks, Zebra Technologies–Motorola Solutions' Enterprise business, Aruba Networks–

Hewlett Packard Enterprise (HPE), and Fortinet–Meru Networks) having closed since the

publication of the preceding IDC MarketScape: Worldwide Enterprise WLAN 2013–2014

Vendor Analysis (IDC #243354, September 2013).

©2015 IDC #US40653915e 3

IDC MARKETSCAPE VENDOR INCLUSION CRITERIA

This research includes analysis of 12 of the largest enterprise WLAN vendors spanning IDC's research

coverage and with global or regional importance. This assessment is designed to evaluate the

characteristics of each firm — as opposed to its size or the breadth of its services. It is conceivable, and

in fact the case, that specialty firms can compete with multidisciplinary firms on an equal footing. As

such, this evaluation should not be considered a "final judgment" on the firms to consider for a

particular project. An enterprise's specific objectives and requirements will play a significant role in

determining which firms should be considered as potential candidates for an engagement.

In total, 12 firms were evaluated in this IDC MarketScape. They are (in alphabetical order): ADTRAN,

Aerohive Networks, AirTight Networks, Cisco (including Cisco Meraki), D-Link, Extreme, Fortinet-Meru,

Aruba-HPE, Huawei, Ruckus Wireless, Xirrus, and Zebra. For inclusion in this IDC MarketScape,

vendors had to demonstrate two years of general worldwide availability of a standards-based WLAN

portfolio and should have reached a critical mass of shipments and/or revenue.

ESSENTIAL BUYER GUIDANCE

Organizations must consider near- and long-term needs for the 802.11ac standard. Some

vendors have announced their plans to release Wave 2 802.11ac access points (APs), with a

few shipping. Other vendors have yet to announce availability of Wave 2–capable APs. IDC

recommends that organizations evaluating new WLAN infrastructure should consider their

needs for 802.11ac. Organizations for which their current 802.11n deployments are not

meeting business needs should consider an immediate upgrade to 802.11ac. For

organizations with WLAN infrastructures that are meeting today's needs, IDC recommends

waiting until a broader set of Wave 2–capable platforms are available. This time frame will vary

according to vendor but will happen in 2016. In addition, when upgrading to Wave 2,

organizations may need to upgrade their cabling and switching infrastructure; a good reseller

or integrator can guide this process.

Cloud-managed network models continue to become more common and have grown in

capability. Small to midsize organizations and "distributed enterprise" (organizations with a

centralized IT and dispersed remote locations) often find that cloud-managed WLAN allows for

an accessible, enterprise-grade delivery model. Cloud-managed WiFi is generally more opex

oriented than capex oriented and can be a viable option for organizations seeking greater

operational agility and centralized policy controls.

There are a number of architectural options for enterprise WLAN. These include physical

controller based, virtual controller, cloud managed, and APs with integrated control. There are

strong cases to be made for all of these, and final decisions should be made based on

individual business needs. In any case, it may be worthwhile to consider vendors with flexible

architectural models as business needs change.

In choosing an enterprise WLAN solution, organizations must consider the possibilities for

creating additional business value from the technology. New WLAN applications for customer-

facing location-based services (LBS), network analytics, and in-venue WiFi–enabled tools are

leading to new monetization opportunities in retail, hospitality, healthcare, education, and other

verticals.

It is important to consider the security capabilities of any WLAN solution. While all solutions

profiled in this document will meet the minimum security requirements of most organizations,

IT decision makers should look at advanced security needs, support for vertical-specific

©2015 IDC #US40653915e 4

protocols and compliance needs, and level of integration offered with non-WLAN security

tools.

Support and services from vendors, resellers, integrators, and managed service providers

(where applicable) cannot be overlooked in the vendor selection process. Good vendors,

resellers, integrators, and managed service providers will provide competent guidance through

the RFP, installation, and training processes while being accessible for ongoing support

throughout the infrastructure's life cycle. This is especially important for organizations with lean

internal network staff.

The networking industry's move to greater support for open source and multivendor initiatives

like SDN will begin to have impact in enterprise WLAN in the medium term. Organizations

should determine their strategies around SDN and open networking and choose a WLAN

vendor with an aligned strategy.

To assist in the vendor selection process, organizations, IT, and end users are encouraged to

utilize the visual graphic in this IDC MarketScape research (refer back to Figure 1), along with

the vendor text profiles, to help in developing a short list of potential enterprise WLAN vendors

to consider for their WLAN deployment project(s).

VENDOR SUMMARY PROFILES

This section briefly explains IDC's key observations resulting in a vendor's position in the IDC

MarketScape. While every vendor is evaluated against each of the criteria outlined in the Appendix,

the description here provides a summary of each vendor's strengths and challenges.

Fortinet-Meru

Fortinet-Meru is rated as a Major Player in this IDC MarketScape. Meru Networks, one of the oldest

established vendors of 802.11 technology, was acquired in July 2015 by network security vendor

Fortinet. Both vendors offer a range of WLAN APs and controllers. At this time, the combined entity is

selling both portfolios — Meru and FortiAP, as well as applicable controllers. In addition, both portfolios

have offered a cloud-managed option, Meru with XPress Cloud and Fortinet with FortiAP-S.

Meru's greatest differentiation comes from the company's single-channel architecture, where individual

channels are layered into a "super channel." This aims to reduce the complexity of channel planning,

security associations, and application segmentation. Meru is the only vendor in this IDC MarketScape

to offer this type of technology. Historically, Meru has found strength in higher education, healthcare,

and hospitality. Meru has also been an early mover in SDN-enabled WLAN, releasing the first

OpenFlow-ready WLAN controller in 2014.

Fortinet's WLAN products are differentiated through integration of the FortiGate network security

platform (where control resides). FortiAP combines WLAN access, firewall, VPN gateway, WIPS, and

Web filtering and application control, among other capabilities, into a single appliance. FortiAP-S offers

similar security capabilities inside the AP managed via the cloud without the need for a controller.

Fortinet WLAN solutions have typically been targeted to the enterprise branch, K–12 education, and

distributed enterprise (retail, QSR, and consumer finance, among others). Fortinet also has a line of

switching equipment, providing some capabilities with regard to unified wired and wireless access.

Both Fortinet and Meru's control platforms can be deployed on a VM.

Future success of Fortinet-Meru deployments depends on execution of the integration strategy. The

individual portfolios are highly complementary. Meru brings unique a RF architecture, SDN innovation,

©2015 IDC #US40653915e 5

and the knowledge and legacy that come with being one of the oldest pure-play WLAN vendors to

Fortinet's security leadership and tremendous business resources. Integrated security is becoming

more important in enterprise networking, and SDN is gradually garnering more interest for campus

deployments. These are among the factors that can position Fortinet-Meru for success.

Strengths

Integrated security requirements are increasing across enterprises. Fortinet has the ability to

offer a fairly comprehensive set of embedded security capabilities in future iterations of the

combined portfolio.

Fortinet-Meru is in a strong position financially, holding no long-term debt. This bodes well for

future WLAN development.

Historically, Meru has been one of the companies best attuned to the unique issues affecting

individual verticals. If this type of vertical alignment can be extended to Fortinet's targeted

verticals, it should yield great benefits.

Fortinet offers 24 x 7 support in all regions.

Challenges

The ultimate strategy for combining the two portfolios is not completely clear. Fortinet-Meru

will be challenged to support legacy customers during the integration process.

Prior to acquisition, Meru had been struggling with a loss of market share and footprint.

Compared with many vendors, Fortinet-Meru is relatively thin in terms of breadth and depth of

managed service provider and carrier offerings.

APPENDIX

Reading an IDC MarketScape Graph

For the purposes of this analysis, IDC divided potential key measures for success into two primary

categories: capabilities and strategies.

Positioning on the y-axis reflects the vendor's current capabilities and menu of services and how well

aligned the vendor is to customer needs. The capabilities category focuses on the capabilities of the

company and product today, here and now. Under this category, IDC analysts will look at how well a

vendor is building/delivering capabilities that enable it to execute its chosen strategy in the market.

Positioning on the x-axis, or strategies axis, indicates how well the vendor's future strategy aligns with

what customers will require in three to five years. The strategies category focuses on high-level

decisions and underlying assumptions about offerings, customer segments, and business and go-to-

market plans for the next three to five years.

The size of the individual vendor markers in the IDC MarketScape represents the market share of each

individual vendor within the specific market segment being assessed.

IDC MarketScape Methodology

IDC MarketScape criteria selection, weightings, and vendor scores represent well-researched IDC

judgment about the market and specific vendors. IDC analysts tailor the range of standard

characteristics by which vendors are measured through structured discussions, surveys, and

interviews with market leaders, participants, and end users. Market weightings are based on user

©2015 IDC #US40653915e 6

interviews, buyer surveys, and the input of a review board of IDC experts in each market. IDC analysts

base individual vendor scores, and ultimately vendor positions on the IDC MarketScape, on detailed

surveys and interviews with the vendors, publicly available information, and end-user experiences in

an effort to provide an accurate and consistent assessment of each vendor's characteristics, behavior,

and capability.

Market Definition

Enterprise WLAN

IDC breaks wireless LAN (WLAN) infrastructure into three segments: WLAN equipment, WLAN

connectivity, and WLAN IT services. This IDC MarketScape competitive analysis is primarily focused

on the WLAN equipment category but looks at other segments to deliver complete enterprise wireless

solutions.

Product Class

The WLAN equipment category is segmented into enterprise and consumer infrastructure:

Enterprise: Enterprise-grade access devices are WLAN access devices designed for use in

multiaccess point systems or for standalone deployments and typically have a rich and

upgradeable feature set. There are two types of enterprise-class access point (AP) devices:

independent (traditional) and dependent. Deployments are in building or outdoor.

Consumer: Consumer-grade access devices are products designed for small-office/home

office (SOHO) and consumer (residential) deployments. Access points and gateways/routers

with WLAN functionality that sell for under $200 are typically included in this category.

Product Category

Controller/switch: Access point controllers typically manage access to the network, load

balance users, enforce security policies, and provide a number of higher-level network

services. This functionality is typically packaged in a Layer 2 or 3 edge or core controller,

integrated in an Ethernet LAN switch, or an appliance. These are products designed to

integrate a WLAN infrastructure with a wired Ethernet network through automating WLAN

access point configuration and RF management.

Access points: This category includes equipment that acts as an intermediary between the

wired and wireless part of the network by receiving and transmitting 802.11 packets. The

packets are sent over a set of predefined bands in the 2.4GHz and 5GHz radio spectrums to

and from associated wireless client devices. Access devices are connected to the wired

network either directly through Ethernet cables or via wireless connections to other access

devices. WLAN may also be used for establishing LAN-to-LAN bridges that usually involve

providing connectivity between buildings without the use of cabling. The current generation of

APs have one or more (typically two) radios with the 802.11n standard but are backward

compatible to support legacy 802.11a/b/g protocols. Increasingly, WLAN vendors are

introducing APs that support the emerging 802.11ac standard.

Independent (traditional) AP: Independent (in-building, standalone) access points, or

traditional access points, include network processing hardware, are set up and configured with

standalone configuration tools, and have a full feature set that allows them to operate as

independent endpoints on the wired network.

Dependent AP: Dependent access points ("thin" or "light" or "managed" or "in-building-thin"

access points) rely on a centralized controller or alternate management and control platform

(integrated, cloud based, or virtualized) for operation and management. They may be lighter in

©2015 IDC #US40653915e 7

terms of onboard network processing hardware, although that difference has started to erode

recently as controller-based architectures are also being deployed using alternate centralized

or decentralized solutions for provisioning and managing network parameters and policies.

Gateways/routers: Gateway/routers are networking devices that connect local area networks

(LANs) at home or SOHO environments to wide area networks (WANs) or other LANs. The

WAN connectivity can be provided through cable modems, DSL modems, or a cellular/mobile

network.

Strategies and Capabilities Criteria

The importance of a vendor's characteristics to project success and relevance of the particular issue

combined with IDC's opinion about the impact those elements have on the selection of firms implies a

unique weighting of these elements when evaluating a vendor's overall strategy and capability to

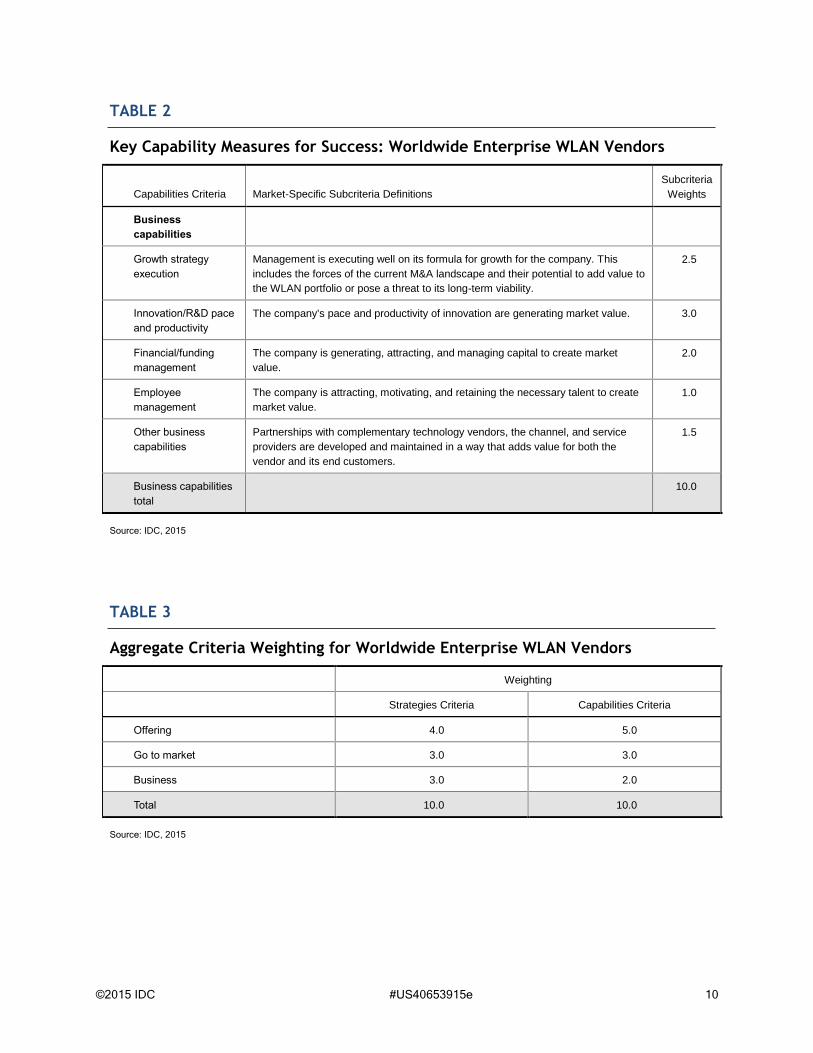

address market opportunity and realizing market success (see Tables 1 and 2).

In addition to the criteria for success having varying weights, IDC believes the aggregate criteria

(offering, go to market, and business) should also be weighted. Table 3 illustrates the relative weights

used in this analysis.

TABLE 1

Key Strategy Measures for Success: Worldwide Enterprise WLAN Vendors

Strategies Criteria Market-Specific Subcriteria Definitions

Subcriteria

Weights

Offering strategy

Functionality or

offering road map

Future plans for offering functionality are well aligned with current and future

customer needs and with priority customer segments.

2.5

Delivery model Plans are in place for support of offering delivery model(s) that will match the

shifting preferences of customers for adoption/consumption in the next five years

and allow them to successfully capture revenue flow as it shifts among different

delivery models (e.g., packaged software versus SaaS).

2.0

Cost management

strategy

Strategies for developing and producing the supplier's offering lead to competitive

offering costs and support competitive pricing, customer engagement, and future

opportunities.

1.0

Portfolio strategy The offering is well supported and enhanced by a portfolio of complementary

offerings offered by the company or its ecosystem of partners.

2.0

Range of services

strategies

Vendors may be rated on adoption and plans for contract terms, licensing, and

pricing arrangements that customers want to see in the future as well as the level

and range of support and tools that will be provided by the vendor to support the

demands of clients in the near future.

1.0

Future integration

strategy

In the enterprise WLAN market, integration primarily refers to how the WLAN

portfolio interoperates with the wired switching element of the network

infrastructure. In particular, this refers to the unified management of wired and

wireless in a single vendor or multivendor infrastructure. This also can refer to

support for SDN open networking standards.

1.5

Offering strategy total 10.0

©2015 IDC #US40653915e 8

TABLE 1

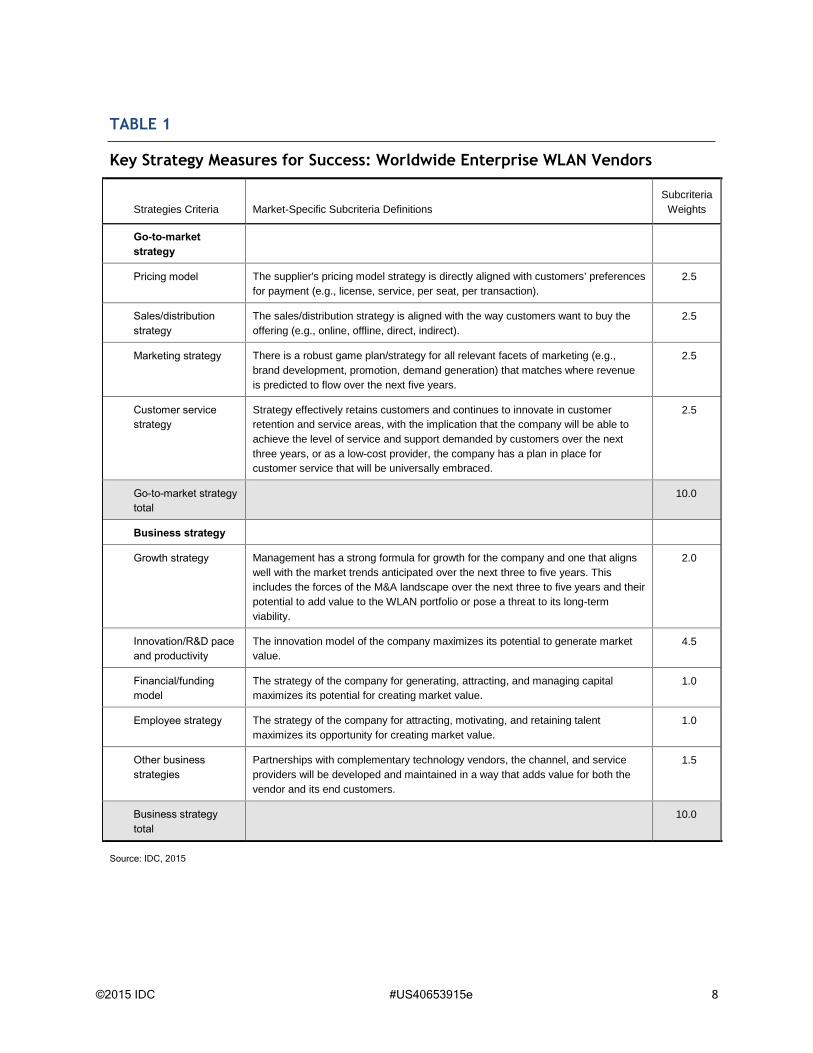

Key Strategy Measures for Success: Worldwide Enterprise WLAN Vendors

Strategies Criteria Market-Specific Subcriteria Definitions

Subcriteria

Weights

Go-to-market

strategy

Pricing model The supplier's pricing model strategy is directly aligned with customers' preferences

for payment (e.g., license, service, per seat, per transaction).

2.5

Sales/distribution

strategy

The sales/distribution strategy is aligned with the way customers want to buy the

offering (e.g., online, offline, direct, indirect).

2.5

Marketing strategy There is a robust game plan/strategy for all relevant facets of marketing (e.g.,

brand development, promotion, demand generation) that matches where revenue

is predicted to flow over the next five years.

2.5

Customer service

strategy

Strategy effectively retains customers and continues to innovate in customer

retention and service areas, with the implication that the company will be able to

achieve the level of service and support demanded by customers over the next

three years, or as a low-cost provider, the company has a plan in place for

customer service that will be universally embraced.

2.5

Go-to-market strategy

total

10.0

Business strategy

Growth strategy Management has a strong formula for growth for the company and one that aligns

well with the market trends anticipated over the next three to five years. This

includes the forces of the M&A landscape over the next three to five years and their

potential to add value to the WLAN portfolio or pose a threat to its long-term

viability.

2.0

Innovation/R&D pace

and productivity

The innovation model of the company maximizes its potential to generate market

value.

4.5

Financial/funding

model

The strategy of the company for generating, attracting, and managing capital

maximizes its potential for creating market value.

1.0

Employee strategy The strategy of the company for attracting, motivating, and retaining talent

maximizes its opportunity for creating market value.

1.0

Other business

strategies

Partnerships with complementary technology vendors, the channel, and service

providers will be developed and maintained in a way that adds value for both the

vendor and its end customers.

1.5

Business strategy

total

10.0

Source: IDC, 2015

©2015 IDC #US40653915e 9

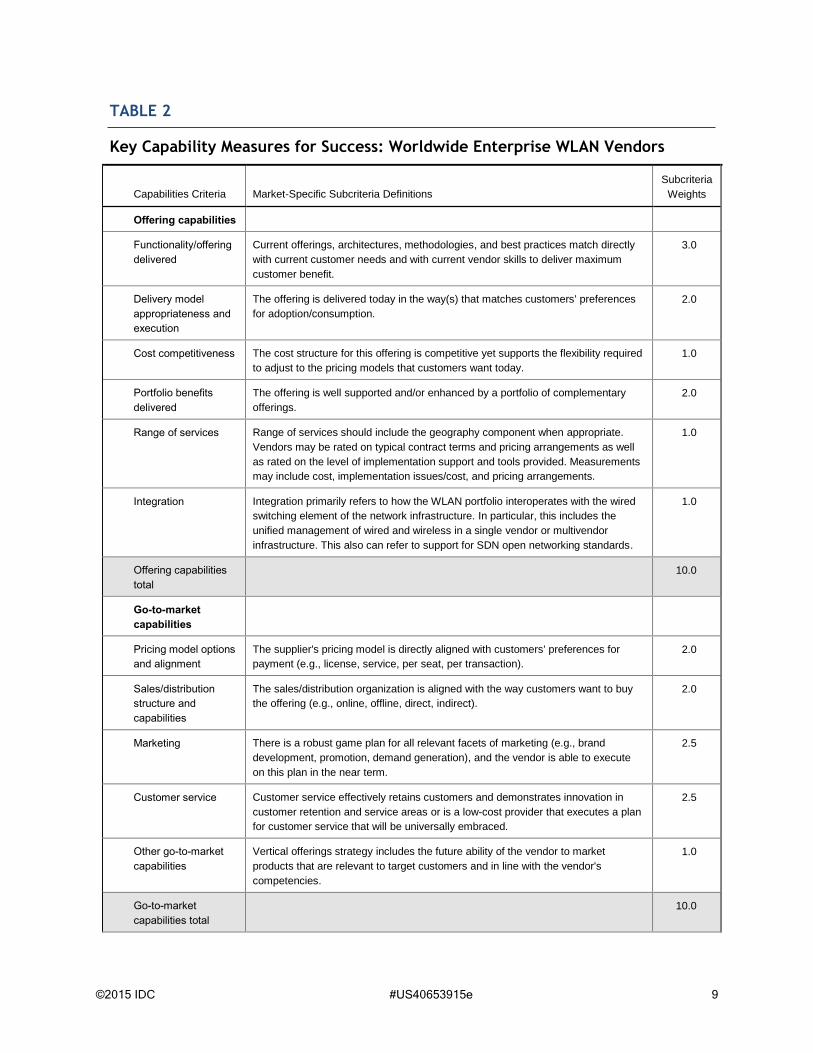

TABLE 2

Key Capability Measures for Success: Worldwide Enterprise WLAN Vendors

Capabilities Criteria Market-Specific Subcriteria Definitions

Subcriteria

Weights

Offering capabilities

Functionality/offering

delivered

Current offerings, architectures, methodologies, and best practices match directly

with current customer needs and with current vendor skills to deliver maximum

customer benefit.

3.0

Delivery model

appropriateness and

execution

The offering is delivered today in the way(s) that matches customers' preferences

for adoption/consumption.

2.0

Cost competitiveness The cost structure for this offering is competitive yet supports the flexibility required

to adjust to the pricing models that customers want today.

1.0

Portfolio benefits

delivered

The offering is well supported and/or enhanced by a portfolio of complementary

offerings.

2.0

Range of services Range of services should include the geography component when appropriate.

Vendors may be rated on typical contract terms and pricing arrangements as well

as rated on the level of implementation support and tools provided. Measurements

may include cost, implementation issues/cost, and pricing arrangements.

1.0

Integration Integration primarily refers to how the WLAN portfolio interoperates with the wired

switching element of the network infrastructure. In particular, this includes the

unified management of wired and wireless in a single vendor or multivendor

infrastructure. This also can refer to support for SDN open networking standards.

1.0

Offering capabilities

total

10.0

Go-to-market

capabilities

Pricing model options

and alignment

The supplier's pricing model is directly aligned with customers' preferences for

payment (e.g., license, service, per seat, per transaction).

2.0

Sales/distribution

structure and

capabilities

The sales/distribution organization is aligned with the way customers want to buy

the offering (e.g., online, offline, direct, indirect).

2.0

Marketing There is a robust game plan for all relevant facets of marketing (e.g., brand

development, promotion, demand generation), and the vendor is able to execute

on this plan in the near term.

2.5

Customer service Customer service effectively retains customers and demonstrates innovation in

customer retention and service areas or is a low-cost provider that executes a plan

for customer service that will be universally embraced.

2.5

Other go-to-market

capabilities

Vertical offerings strategy includes the future ability of the vendor to market

products that are relevant to target customers and in line with the vendor's

competencies.

1.0

Go-to-market

capabilities total

10.0

©2015 IDC #US40653915e 10

TABLE 2

Key Capability Measures for Success: Worldwide Enterprise WLAN Vendors

Capabilities Criteria Market-Specific Subcriteria Definitions

Subcriteria

Weights

Business

capabilities

Growth strategy

execution

Management is executing well on its formula for growth for the company. This

includes the forces of the current M&A landscape and their potential to add value to

the WLAN portfolio or pose a threat to its long-term viability.

2.5

Innovation/R&D pace

and productivity

The company's pace and productivity of innovation are generating market value. 3.0

Financial/funding

management

The company is generating, attracting, and managing capital to create market

value.

2.0

Employee

management

The company is attracting, motivating, and retaining the necessary talent to create

market value.

1.0

Other business

capabilities

Partnerships with complementary technology vendors, the channel, and service

providers are developed and maintained in a way that adds value for both the

vendor and its end customers.

1.5

Business capabilities

total

10.0

Source: IDC, 2015

TABLE 3

Aggregate Criteria Weighting for Worldwide Enterprise WLAN Vendors

Weighting

Strategies Criteria Capabilities Criteria

Offering 4.0 5.0

Go to market 3.0 3.0

Business 3.0 2.0

Total 10.0 10.0

Source: IDC, 2015

©2015 IDC #US40653915e 11

LEARN MORE

Related Research

IDC MaturityScape: Enterprise WLAN (IDC #US40211115, December 2015)

IT's 3rd Platform Drives Need for Network Innovation (IDC #259317, September 2015)

Market Analysis Perspective: Worldwide Enterprise Communications Infrastructure, 2015 (IDC

#259364, September 2015)

Worldwide WLAN 2Q15 Market Share Update (IDC #259193, September 2015)

The Next Wave of 802.11ac WiFi Is Coming: What Enterprise IT Needs to Know (IDC

#256787, June 2015)

Worldwide Enterprise WLAN 2014–2018 Forecast (IDC #252694, December 2014)

Synopsis

This IDC study provides an assessment of the capabilities and business strategies of 12 vendors in the

worldwide enterprise WLAN market for 2015–2016.

"There is a vast range of enterprise WLAN options speaking to the many needs of the market," says

Nolan Greene, research analyst, Enterprise Network Infrastructure. "The 802.11ac standard, cloud-

based delivery models, network analytics and value-added services, and technology partnerships are

bringing about new possibilities for organizations to fulfill business objectives through the WiFi

network. This IDC MarketScape can be helpful to organizations that are considering a move to a new

enterprise WLAN solution, including new deployment options."

About IDC

International Data Corporation (IDC) is the premier global provider of market intelligence, advisory

services, and events for the information technology, telecommunications and consumer technology

markets. IDC helps IT professionals, business executives, and the investment community make fact-

based decisions on technology purchases and business strategy. More than 1,100 IDC analysts

provide global, regional, and local expertise on technology and industry opportunities and trends in

over 110 countries worldwide. For 50 years, IDC has provided strategic insights to help our clients

achieve their key business objectives. IDC is a subsidiary of IDG, the world's leading technology

media, research, and events company.

Global Headquarters

5 Speen Street

Framingham, MA 01701

USA

508.872.8200

Twitter: @IDC

idc-insights-community.com

www.idc.com

Copyright Notice

This IDC research document was published as part of an IDC continuous intelligence service, providing written

research, analyst interactions, telebriefings, and conferences. Visit www.idc.com to learn more about IDC

subscription and consulting services. To view a list of IDC offices worldwide, visit www.idc.com/offices. Please

contact the IDC Hotline at 800.343.4952, ext. 7988 (or +1.508.988.7988) or [email protected] for information on

applying the price of this document toward the purchase of an IDC service or for information on additional copies

or Web rights.

Copyright 2015 IDC. Reproduction is forbidden unless authorized. All rights reserved.