icici prudential

DESCRIPTION

Summer Internship projectTRANSCRIPT

1

Table of Contents EXECUTIVE SUMMARY ........................................................................................................................................... 2

I) INTRODUCTION ...................................................................................................................... 3 INDUSTRY PROFILE ................................................................................................................................................. 5 1) Life insurance: .................................................................................................................................................... 6 2) Non-life (general) Insurance: ............................................................................................................................. 7 3) Reinsurance Companies ............................................................................................................................... 8 Contribution to Indian Economy ............................................................................................................................ 8 Roles in the Insurance Industry .............................................................................................................................. 9 COMPANY PROFILE .............................................................................................................................................. 11 FUNCTION OF INSURANCE ................................................................................................................................... 13 WHY WE NEED INSURANCE: ................................................................................................................................ 14 RISK ...................................................................................................................................................................... 15 PRODUCT/SERVICES PROFILE ............................................................................................................................... 16 Type of INSURANCE Product ................................................................................................................................ 17 AWARENESS ......................................................................................................................................................... 19 STATEMENT OF RESEARCH................................................................................................................................... 19 OBJECTIVE OF THE STUDY .................................................................................................................................... 19 SIGNIFICANCE OF THE STUDY............................................................................................................................... 20 LIMITATIONS OF THE STUDY ................................................................................................................................ 20

II) RESEARCH METHODOLOGY ........................................................................................................ 21 RESEARCH DESIGN: .............................................................................................................................................. 22 SAMPLING PLAN: .................................................................................................................................................. 23 ANALYSIS AND INTERPRETATION: ........................................................................................................................ 23 DATA ANALYSIS AND INTERPRETATION ............................................................................................................... 24 AGE ....................................................................................................................................................................... 24 Marital status ....................................................................................................................................................... 26 Occupation VS Annual Income ............................................................................................................................. 27 Dependents .......................................................................................................................................................... 28 Do you have any of these Loans? ......................................................................................................................... 29 Do you have any of these? ................................................................................................................................... 30 How good is your knowledge about Financial & Capital Market? ....................................................................... 31 How long you instead to be investment and what is your purpose .................................................................... 32 FINDINGS .............................................................................................................................................................. 33

III) THEORETICAL BACKGROUND .................................................................................................. 34 Portfolio Construction .......................................................................................................................................... 35 Analysis of constraints ......................................................................................................................................... 37 Determination of objectives ................................................................................................................................ 39 Selection of portfolio ........................................................................................................................................... 40 Risk and return analysis ....................................................................................................................................... 41 Diversification ...................................................................................................................................................... 41 ICICI PRUDENTIAL PRODUCT ................................................................................................................................ 42

MANAGEMENT LESSON: ................................................................................................................. 49

RECOMMENDATIONS TO COMPANY ............................................................................................... 53

IV CONCLUSION ............................................................................................................................. 56 Conclusion ............................................................................................................................................................ 57 BIBLIOGRAPHY ..................................................................................................................................................... 58 ANNEXURE ........................................................................................................................................................... 59

2

EXECUTIVE SUMMARY

ICICI Prudential Life Insurance is one of the largest Insurance networks in the country, and

2nd Life Insurance Company in India. The ICICI Group has been in existence since 1955 when

ICICI Ltd., was created. ICICI Prudential started in 2002 as subsidiary of ICICI Ltd, The

Insurance sector, after the opening up, provides greater opportunities. Several global players have

emerged and the market has changed significantly. In the changed scenario, the expectation is that

the low Insurance premium as a percentage of GDP prevailing in India will improve and will offer

better opportunities to the insurance players.

In the life Insurance segment the Life Insurance Corporation of India (LIC) is the major

player. It is constituted in to seven Zones. Currently there are 5, 60,000 LIC agents in India. General

Insurance is another segment, which has been growing at a faster pace.

3

I) INTRODUCTION

4

Life insurance is a form of insurance that pays monetary proceeds upon the death of the

insured covered in the policy. Essentially, a life insurance policy is a contract between the named

insured and the insurance company wherein the insurance company agrees to pay an agreed upon

sum of money to the insured's named beneficiary so long as the insured's premiums are current.

With a large population and the untapped market area of this population insurance happens to be a

very big opportunity in India. Today it stands as a business growing at the rate of 15-20% annually.

Together with banking services, it adds about 7 %to the country’s GDP. In spite of all this growth

statistics of the penetration of the insurance in the country is very poor. Nearly 80% of Indian

populations are without life insurance cover and the health insurance. This is an indicator that

growth potential for the insurance sector is immense in India.

It was due to this immense growth that the regulations were introduced in the insurance sector and

in continuation “Malhotra Committee” was constituted by the government in 1993 to examine the

various aspects of the industry. The key element of the reform process was participation of overseas

insurance companies with 26% capital.

Since then the insurance industry has gone through many changes. The liberalization of the industry

the insurance industry has never looked back and today stand as one of the most competitive and

exploring industry in India. The entry of the private players and the increased use of the new

distribution are in the limelight today. The use of new distribution techniques and the IT tools has

increased the scope of the industry in the longer run.

Insurance is the method of spreading and transfer of risk. The fortunate many who are exposed to

some or similar risk shares loss of the unfortunate. Insurance does not protect the assets but only

compensates the economic or financial loss.

5

INDUSTRY PROFILE

Insurance in India

The insurance sector in India has come a full circle from being an open competitive market to

nationalization and back to a liberalized market again. Tracing the developments in the Indian

insurance sector reveals the 360 degree turn witnessed over a period of almost two centuries.

A Brief history of the Insurance Sector

The business of life insurance in India in its existing form started in India in the year 1818 with the

establishment of the Oriental Life Insurance Company in Calcutta.

For over 50 years, life insurance in India was defined and driven by only one company- the Life

Insurance Corporation of India (LIC). With the Insurance Regulatory and Development Authority

(IRDA) Bill 1999 paving the way for entry of private companies into both life and general sectors

there was bound to be new-found excitement- and new success stories

The percentage of premium income to GDP which was just 2.3% in 2000-01 rose to 3.3% in 2002-

03; and life insurance has emerged as the dominant contributor to this growth.

The industry presented a huge opportunity. Life insurance penetration, for instance, was at an

abysmal 22% of the insurable population. However, private players have had to rise to many

challenges. They were faced with attitudinal barriers towards the category and the perception that

insurance was only a tax saving tool. Insurance per se had lost it basic rationale: protection. It wasn’t

surprising then that its potential lay frozen and unexploited. The challenge for private insurance

players was to change the established category driver and get customers to evaluate life insurance

as an investment-cum-protection tool.

Classification of insurance

The insurance industry in India can broadly classified in two parts. They are.

1) Life insurance.

2) Non-life (general) insurance.

6

1) Life insurance:

Life insurance can be defined as “life insurance provides a sum of money if the person who is

insured dies while the policy is in effect”.

In 1818 British introduced to India, with the establishment of the oriental life insurance company

in Calcutta. The first Indian owned Life Insurance Company; the Bombay mutual life assurance

society was set up in 1870.The union government had opened the insurance sector for private

participation in 1999, also allowing the private companies to have foreign equity up to 26%.

Budget 2014 government have given permission up to 49% of shares of overseas insurance

company.

Benefits of life insurance

1) Life insurance encourages saving and forces thrift.

2) It is superior to a traditional savings vehicle.

3) It helps to achieve the purpose of life assured.

4) It can be enchased and facilitates quick borrowing.

5) It provides valuable tax relief.

Fundamental principles of life insurance contract;

1) Principle of almost good faith:

“A positive duty to voluntary disclose, accurately and fully, all facts, material to the risk being

proposed whether requested or not”.

2) Principle of insurable interest:

“Relationships with the subject matter (a person) which is recognized in law and gives legal right

to insure that person”.

7

2) Non-life (general) Insurance:

Non-life insurance companies generally cover risks other than those relating to human lives. The

exceptions to this are personal accident and health insurance, which are provided by non-life

insurance companies. Any asset either gives a monetary return (e.g. a house given on rent), or offers

convenience (e.g. a car which can be used to travel from one place to another) can be insured. All

assets are exposed to various risks: they can be damaged or destroyed by fire, earthquake, riot, theft,

flooding, cyclones etc. If the asset is damaged by any of these risks, the owner will be at a

disadvantage and they will lose the income or the convenience the asset provided. Non-life

insurance companies offer products that cover these risks and compensate the owner should the

asset be damaged by one of them. It is a product from this type of company that an individual would

buy to protect their assets, for example, their home against fire etc.

8

3) Reinsurance Companies

We know that insurance is a risk transfer mechanism. Risk is transferred from those who are unable

to bear it to those who can. However, insurance companies can only take on so much risk. Once

that limit is reached, the insurer itself is exposed to the risk of loss. When this happens insurers look

to transfer some of their risks to someone else to shield themselves from overexposure. This is

where reinsurance companies come into use. A reinsurance company is an insurer for the insurance

company. Reinsurance companies take on a certain percentage of the risks on the insurance

company’s books, in return for the payment of a consideration.

Contribution to Indian Economy

Life Insurance is the only sector which garners long term savings.

Spread of financial services in rural areas and amongst socially less privileged.

Long term funds for infrastructure.

Strong positive correlation between development of capital markets and insurance/pension

structure.

Employment generation.

9

Roles in the Insurance Industry

Chart-1.1

Agents

Corporate Agents

Intermediaries

Underwriters

Actuaries

TPAs

Sureyors/

Loss Adjusters

Training Institutes

NGO Protecting the

Customer Rights

10

Agents These contribute the major percentage of insurance sales in India. It is the

agent’s primary responsibility to meet the prospective client, understand

their needs, and accordingly recommend suitable products. We shall discuss

the role of agents in more detail in section H.

Corporate

agents

These include banks and brokers. More details about these are included in

section F2

Intermediaries These can be individuals as well as organisations, like firms, banks and

composite brokers. Intermediaries solicit and procure business from

prospective clients for the insurance company.

Underwriters These decide whether to accept or reject the insurance proposal. If the

proposal is to be accepted, then the underwriter decides at what price it

should be accepted

Actuaries These calculate the standard price of products. They take into account

statistical data and the past claims experience of the company. Apart from

pricing individual products, they also do an overall financial assessment of

the insurance company from time to time to make sure that the company has

sufficient reserves to pay for future liabilities.

Third party

administrators

(TPAs)

These do the work of building hospital networks. They also help with

approvals at the time of cashless admission to a hospital and with settling

the bill with the insurer on discharge

Loss

adjusters/

surveyors

These do the work of assessing and certifying a loss when a claim is made

on the insurance company. They have a major role to play in non-life

insurance business.

The Regulator The Insurance Regulatory and Development Authority (IRDA) is the

insurance Regulator in India. The IRDA grants licences to insurance

companies and makes sure all insurance companies are in compliance with

the regulations at all times.

Training

institutes

These have the responsibility of supplying trained manpower to meet the

ever growing need for skilled labour in the insurance industry.

NGOs –

Protecting the

customers’

rights

Non-Governmental Organisations (NGOs) play an important role in

spreading awareness about insurance products and protecting the rights of

the customers. The role of NGOs is more important in the rural areas where

they work with Self Help Groups (SHGs) and insurance companies on

deeper penetration of micro-insurance products at the grassroots level.

Table 1.1

11

COMPANY PROFILE

ICICI Prudential Life Insurance Company limited (‘the Company’) a joint venture

Between ICICI Bank Limited and Prudential plc. Of UK was incorporated on July

20, 2000 as a company under the Companies Act, 1956 (‘the Act’). The Company

Is licensed by the Insurance Regulatory and Development Authority (‘IRDA’) for carrying life

insurance business in India.

The company brings together the local market expertise and financial strength of ICICI Bank and

Prudential’s International life insurance experience. The company was granted a certificate of

Registration by the IRDA on November 24, 2000 and eighteen days later, issued its first policy on

December 12. ICICI Prudential was amongst the first private sector insurance companies to begin

operations in December 2000 after receiving approval from Insurance Regulatory Development

Authority (IRDA).

ICICI Prudential’s equity base stands at Rs. 1185 crore with ICICI Bank and Prudential plc holding

74% and 26% stake respectively. For the year ended March 31, 2006, the company garnered Rs.2,

412 crore of weighted new business premium and wrote 837,963 policies. The sum assured in force

stands at Rs.45, 888 crore. The company has a network of over 72,000 advisors; as well as 9

bancasurance partners and over 200 corporate agent and broker tie-ups.

ICICI Prudential is also the only private life insurer in India to receive a National Insurer Financial

Strength rating of AAA (Ind) from Fitch ratings. The AAA rating is the highest credit rating, and is

a clear assurance of ICICI Prudential’s ability to meet its obligations to customers at the time of

maturity or claims.

For the past five years, ICICI Prudential has retained its position as the No.1 private insurer in the

country, with a wide range of flexible products that meet the needs of the Indian customer at every

step in life.

ICICI Prudential closed the financial year ended march 31, 2004 with a total received premium

income of Rs. 9.9 billion; up 135% last years total premium income of Rs.4.20 billion. New business

premium income shows a 106% growth at Rs. 7.5 billion, driven mainly by the company’s range of

unique unit-linked policies and pension plans. The company’s retail market share amongst private

companies stood at 36%, making it clear leader in the segment. To add to its achievements, in the

year 2003/04 it was adjudged Most Trusted Private Life Insurer (Economic Times ‘Most Trusted

12

Brand Survey’ by AC Nielsen ORG-MARG). It was also conferred the ‘Outlook Money-Best Life

Insurer’ award for the second year running. The company is also proud to have won Silver at

EFFIES 2003 for its ‘Retire from work, not life’ campaign. Notably, ICICI Prudential was also

short-listed to the final round for its ‘Sindoor campaign in EFFIES 2002.

ICICI Prudential’s success is rooted in its philosophy to always offer the customer a choice. This

has been the driving force behind its multi-channel distribution strategy, which includes advisors,

banks, direct marketing and corporate agents. In fact, ICICI Prudential was the first life insurer to

invest in multiple channels and offer the customer choice and access; thus reducing dependency on

any one channel, great strides in the retirement solutions and pensions market.

The company has 9 bank partnerships for distribution, having agreements with ICICI Bank, Bank

of India, Federal Bank, South Indian Bank, Lord Krishna Bank, and some co-operative banks, as

well as over 200 corporate agents and brokers, it has also tied up with NGOs, MFIs and corporates

for the distribution of rural policies.

ICICI Prudential has recruited and trained more than 72,000 insurance advisors to interface with

and advise customers. Further, it leverages its state-of-the-art IT infrastructure to provide superior

quality of service to customers.

The joint strengths

A powerful joint venture partnership with each carrying a set of strengths

complementing each others

Reputation

Insurance

expertise

Product

Distribution

Operations

Brand strength

Infrastructure

Customer base

Local knowledge

Market Innovators

PRUDENTIALICICI

Chart 1.2

13

FUNCTION OF INSURANCE

Provide protection: The primary function of insurance is to provide protection against

future risk, accidents and uncertainty. Insurance cannot prevent the happening of the risk, it

can only provide compensation (sum assured) for the loss that comes as a result of the certain

event happening.

Collective bearing of risk: Insurance is an instrument to share the financial loss of few

among many others. Insurance is a mean by which few losses are shared among larger

number of people. All the insured contribute the premiums towards a fund and out of which

the persons exposed to a particular risk is paid.

Assessment of risk: Insurance determines the probable volume of risk by evaluating various

factors that give rise to risk. Risk is the basis for determining the premium rate also.

Small capital to cover larger risk: Insurance relieves the businessmen/ employee from

security investments, by paying small amount of premium against larger risks and

uncertainty.

Means of savings and investment: Insurance serves as savings and investment, insurance

provide option to invest in unit linked plans as well as traditional plans such as money back,

endowment etc. For the purpose of availing income-tax exemptions also, people invest in

insurance.

14

WHY WE NEED INSURANCE:

Dying Too Soon (premature death): Insurance provides protection against the premature death

because we all know our Date of Birth, but we don’t know our Date of expiry. Life is uncertain so

we have to insured our life for securing our family future need.

Living death: This term refers to those who have contracted a serious illness or met an accident

that disables the person and renders him or her unable to work for an income to support the family,

besides having endures the terrible pain that goeswith the condition.

Saving for old age: - After retirement the earning capacity of a person reduces. Life insurance

enables a person to enjoy peace of mind and a sense of security in his/her old age.

Children’s future: for the tackle with the financial need of children big event such as education,

marriage etc. we need insurance because we don’t know about life because it uncertain so we need

proper arrangement for this & insurance is a better option for this.

Initiates investments: - Life Insurance Corporation encourages and mobilizes the public savings

and canalizes the same in various investments for the economic development of the country. Life

insurance is an important tool for the mobilization and investment of small savings.

Tax Benefit: - Under the Income Tax Act, premium paid is allowed as a deduction from the total

income under section 80C.

15

RISK

Chart 1.3

Premature death – Individual job profile is quite stressful and may involves intense travelling.

He is exposed to the risk of early death which could occur due to an accident or illness caused by

stress. A life insurance plan can protect his family against the risk of individual early death.

Accident – Due to the frequent travelling that individual has to do, he is prone to the risk of

accidents that can result in either permanent or temporary disability. A life insurance plan with a

disability benefit rider or a separate accidental death policy can protect his family against the risk

of becoming disabled.

Illness – Due to the stressful nature of his job, individual is exposed to the risk of suffering from

critical illnesses. A life insurance plan with a critical illness rider, or a health insurance policy, can

help meet the hospitalization expenses should individual suffer from any critical illness.

Unemployment – If individual has an accident and becomes disabled, he risks losing his job and

becoming unemployed.

Living too long –Individual may be exposed to the risk of living too long beyond retirement. He

is working for a private company that does not provide a monthly pension after retirement as part

of his employee benefits. Hence he needs to work towards building a retirement fund during his

working life by investing in a retirement pension plan.

Risk

Premature

Death

Illness

Accedent

Living to long

16

PRODUCT/SERVICES PROFILE

ICICI Prudential’s product range has been developed on the understanding that different

people have their own sets of needs at various stages of their lives. It has thus built a flexible

portfolio of products that can be customized to cater to varying needs of people at each stage, and

thus ensure protection in every step of life. The company’s philosophy has been to help customers

understand their financial needs and work closely with them to customize a product that would

meet. Advisors can offer a complete range of products –Savings plans, Child plans, Market-linked

plans, Protection plans, and Retirement plans – and tailor a flexible solution to meet customers’

changing needs at every stage of life. In fact, ICICI Prudential was the first to un-bundle product

benefits, pioneering the concept of ‘riders’ and soon after introduce comprehensive market-linked

and retirement plans.

ICICI Prudential has launched a handful of products that are analyzed below:

ICICI Prudential's life insurance products may be loosely categorized under three forms: pure life

insurance products without an investment angle to them; a product that is a mix of a cumulative

investment scheme and an insurance product; and, finally, standard products such as money-back

and endowment policies.

1. Accident and disability benefit: If death occurs as the result of an accident during the

term of the policy, the beneficiary receives an additional amount equal to the rider sum

assured under the policy. If the death occurs while traveling in an authorized mass

transport vehicle, the beneficiary will be entitled to twice the sum assured as additional

benefit.

2. Accident Benefit: This rider option pays the sum assured under the rider on death due

to accident.

3. Critical Illness Benefit: Protects the insured against financial loss in the event of 9

specified critical illnesses. Benefits are payable to the insured for medical expenses prior

to death

4. Income Benefit: This rider pays the 10% of the sum assured to the nominee every year,

till maturity, in the event of the death of the life assured. It is available in SmartKid,

SecurePlus, and CashPlus.

5. Waiver of Premium: In case of total and permanent disability due to an accident, the

premiums are waived till maturity. This rider is available with SecurePlus and CashPlus.

17

Type of INSURANCE Product

The entire Insurance sector is divided into 2 broad categories:

General Insurance

Life Insurance

Further Life Insurance is sub-divided into two categories:

TRADITIONAL INSURANCE PLANS

ULIPS (Unit Linked Insurance Plans)

Chart 1.4

Traditional products are basically the term plans and the whole life plans, in which risk cover is

the foremost objective of the customers. In case of term plans the sum assured is given to the

nominee of the life to be insured in case of his death, there is no maturity claim, whereas in case of

whole life some amount is paid after a certain period of time.

Main Life Insurance product

Term plan Endowment plan Whole Life

Insurance plans

Unit Linked Insurance Plan

Pension

& Savings Plans

18

ULIPS were introduced couple of years back in the Indian market. These include the endowment

policies and money back policies that have the investment benefit along with the risk cover i.e. the

certain portion of the premium paid by the customer is used for the risk cover and rest is further

invested in the funds offered by the company.

So when the private players entered the market they decided to introduce market driven plans named

ULIP which promised a very attractive return to the consumers. Birla Sun Life was the first

company to establish the concept of ULIP. Though this concept was very attractive but still a

number of policies got lapsed, then the private players came up with an idea of 3 years lock in

period, so that number of policies lapsing could be reduced, which worked well.

Now since the expectations of investors have increased who are investing their money, so the money

flow in mutual funds and stock market has increased gradually because the returns are as high as

25- 30% despite of that Life Insurance is Safe Avenue while promising you good returns, this would

be clear from the following points:

Returns in ULIPs are also as high as 25% - 30%, while it also gives life cover in case of

happening such as death, disability, etc.

Risk in ULIPs is less as compared to mutual funds and stock market, as ULIPs offer different

funds with different combinations of debt and equity.

Fund management fee in ULIPs is 1.25% as compared to the fee in mutual funds 2.5%.

The entire fund of the investor can be eroded under mutual fund if market crashes, but under

ULIPs at least principle amount plus bank rate is guaranteed.

ULIPs provide insurance cover as well as good returns.

Capital gains are not taxable under ULIPs.

Most companies offering ULIPs provide a number of free switches to its investors, if they

would like to switch their funds, but these switches are chargeable under mutual funds.

Most of the investors in the Indian market are not aware of these benefits of Life Insurance, but as

the awareness is increasing more and more investors are joining this sector, resulting in increased

turnover year over year.

19

AWARENESS

If you take example of US the percentage of insured person for life & Health insurance is

75% but unfortunately in India people are less interested in the insurance. They are only 6 -8 % in

the number those who taken insurance. So here insurance company have to make aware about the

benefit of the insurance & provide better solution to increase the customer base.

STATEMENT OF RESEARCH

“Study Of Equity Fund Performance & Consumer Financial Need Analysis Of ICICI Prudential

Life Insurance Products”.

OBJECTIVE OF THE STUDY

For every problem there is a research. As all the researches are based on some and my

study is also based upon some objective and these are as follows.

1. To understand the customer risk and return

2. To understand the insurance products and there Fund performance of ICICI Prudential life

insurance co ltd.

3. To understand Equity and Debt fund

20

SIGNIFICANCE OF THE STUDY

The project is concerned with the “STUDY ON CONSUMER RISK & RETURN AND FUND

PERFORMANCE ICICI PRUDENTIAL LIFE INSURANCE”. This study is very useful as the

financial market become more sophisticated and complex, investor needs a financial intermediary

who provides the required knowledge and professional expertise on successful investing and Life

insurance is a form of insurance that pays monetary proceeds upon the death of the insured covered

in the policy. Essentially, a life insurance policy is a contract between the named insured and the

insurance company wherein the insurance company agrees to pay an agreed upon sum of money to

the insured's named beneficiary so long as the insured's premiums are current

LIMITATIONS OF THE STUDY

By working on this project, a lot of knowledge about the insurance sector in INDIA has been gained.

However, there were many limitations or problems that I faced while working on this project. The

following are the limitations:

Small Sample Size: The study was relied more on the primary data and the data was

collected from a small population of 200, therefore, the findings may not be applicable in

their true sense when it is applied in general.

Time Constraint: As the duration of internship was only 8 weeks, therefore, it was very

difficult to conduct the entire study about the vast insurance sector.

Small area: - This research done only in Jamnagar area including some targeted population.

Respondent’s error: - There is possibility to respondent errors. People generally do not

feel right to discuss their savings and investments.

21

II) RESEARCH

METHODOLOGY

22

Introduction

Research in common parlance refers to a search for knowledge. One can also define

research as a scientific and systematic search for pertinent information on a specific topic.

Research is the solution of the problem, whether created or already generated. When

research is done, some new outcome, so that the problem (created or generated) to be solved.

RESEARCH DESIGN:

Research Design is the conceptual structure within which research is conducted. It

constitutes the blueprint for collection, measurement and analysis of data. The design used

for carrying out this research is Descriptive.

Descriptive Research

This study is based on a descriptive research design wherein the financial needs and

investment associated with the various asset classes have been studied and the reasons for

customer perception regarding these asset classes have been found out

DATA TYPE: In this research the type of data collection is

Primary data

Secondary data

DATA SOURCE: The sources of collection of secondary data are:

Questionnaire

Books

Websites

Brochure

23

SAMPLING PLAN:

It is very difficult to collect information from every member of a population .As time and

costs are the major limitation that the researcher faces.

A sample of 100 was taken the sample size of 100 individuals were selected on the basis of

convenient sampling technique. The individuals were selected in the random manner to

form sample and data were collected from them for the research study.

ANALYSIS AND INTERPRETATION:

Data collection through questionnaire and personnel interview resulted in availability of the

desired information but these were useless until there were analyzed. Various steps required

for this purpose were editing, coding and tabulating. Tabulating refers to bringing together

similar data and compiling them in an accurate and meaningful manner. The data collected

by questionnaire was analyzed, interpreted with the help of table, bar chart and pie chart.

24

DATA ANALYSIS AND INTERPRETATION

AGE

Row Labels Count of AGE

Below 30 71

30-40 13

40-50 10

Above 50 6

Grand Total 100

Table 2.1

Graph 2.1

So above table show there are more respondent age below 30, so here we can conclude

that there are more number of young respondent so there lives are more important as there are

many responsibility on today’s youth. So product like insurance is most important for them but in

India only 6-8 % population are avail with Insurance.

71

13 106

0

10

20

30

40

50

60

70

80

Below 30 30-40 40-50 Above 50

AG

E

Count of AGE

25

The group of people who all are above 50 don’t actually get the benefit from insurance as they

have to pay more premium if they want insurance policy or may be company may reject the

proposal of the one who are suffering from deadly disease.

26

Marital status

Marital Status / Age group 30 or less 30-40 40-50 Above 50 Grand Total

Married 3 12 11 4 30

Unmarried 66 4 70

Grand Total 69 16 11 4 100

Table 2.2

Graph 2.2

From the above diagram we can observe that almost 66 % of respondent are unmarried at the age

of 30 or less so they don’t have much responsibility so there should have more saving and

investment and their investment can be more risky.

3

12 11

4

66

4

0

10

20

30

40

50

60

70

30 or less 30-40 40-50 Above 50

No

. of

resp

on

den

ce

Martial Status VS Age Group

Married Unmarried

27

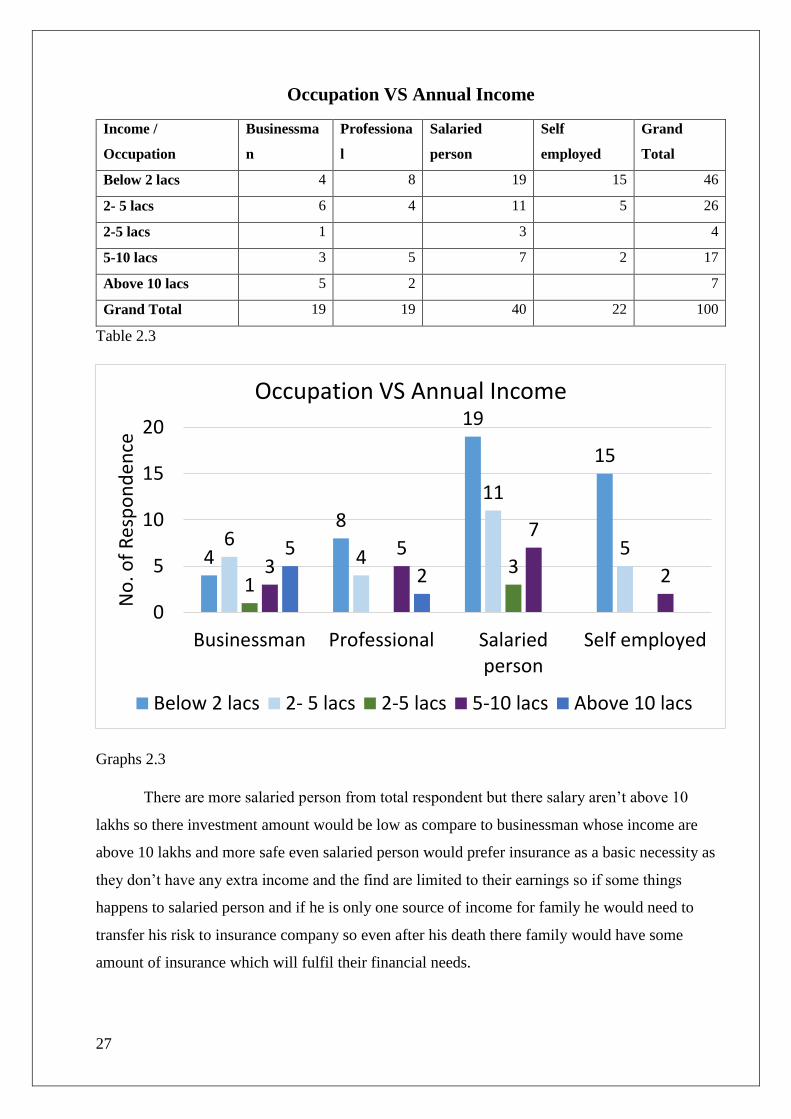

Occupation VS Annual Income

Income /

Occupation

Businessma

n

Professiona

l

Salaried

person

Self

employed

Grand

Total

Below 2 lacs 4 8 19 15 46

2- 5 lacs 6 4 11 5 26

2-5 lacs 1 3 4

5-10 lacs 3 5 7 2 17

Above 10 lacs 5 2 7

Grand Total 19 19 40 22 100

Table 2.3

Graphs 2.3

There are more salaried person from total respondent but there salary aren’t above 10

lakhs so there investment amount would be low as compare to businessman whose income are

above 10 lakhs and more safe even salaried person would prefer insurance as a basic necessity as

they don’t have any extra income and the find are limited to their earnings so if some things

happens to salaried person and if he is only one source of income for family he would need to

transfer his risk to insurance company so even after his death there family would have some

amount of insurance which will fulfil their financial needs.

4

8

19

15

64

11

5

133

57

2

5

2

0

5

10

15

20

Businessman Professional Salariedperson

Self employed

No

. of

Res

po

nd

ence

Occupation VS Annual Income

Below 2 lacs 2- 5 lacs 2-5 lacs 5-10 lacs Above 10 lacs

28

Dependents

Dependents Count

Parents 63

Spouse 11

Children 8

Others 18

Grand Total 100

Table 2.4

Graphs 2.4

Most of the respondent have responsibility of their parents spouse children and others but 63

dependents have responsibility of only parents.

63

11 8

18

0

10

20

30

40

50

60

70

Parents Spouse Children Others

No

. Of

Dep

end

ents

Dependents

29

Do you have any of these Loans?

Loans No. of Respondents having loan

Business loan 2

Car loan 10

House loan 15

Personal loan 19

Other loan 15

Grand Total 61

Table 2.5

Graph 2.5

There are 19 respondent who have personal loan also there are only 2 respondent who have taken

business so there are very few businessman as observed in previous chart of occupation.

210

15

19

15

No. of Respondents having loan

Business loan Car loan House loan

Personal loan Other loan

30

Do you have any of these?

Insurance Count

Property Insurance 6

Medical Claim 4

Pure Life Insurance 73

disability/Physical impairment/Trauma benefits 16

Total 100

Table 2.6

Graphs 2.6

From above chart we can observe that almost 73 have pure insurance but there very few who have

medical claim which means they might not be aware about medical claim or they must not feel

medical as importance as life insurance. Instead medical claim is also most important because

many times you suddenly might fall sick which result in some surgery which will cost a lot for a

middle class family so to be get protection from the uncertain health Medical claim is most

important.

Property …

Medical Claim5%

Pure Life Insurance

73%

disability/Physical impairment/Trauma

benefits…

31

How good is your knowledge about Financial & Capital Market?

Knowledge about Financial Market

Bank savings &

FD Equity

Mutual

Funds ULIP

Grand

Total

Expert of Finance & Capital market 2 16 12 4 34

Knowledge of Bank FD/Post

office/NSC 12 5 17

Knowledge of Mutual Fund / Share

Market 3 8 15 3 29

No Knowledge 7 8 5 20

Grand Total 24 24 40 12 100

Table 2.7

Graph 2.7

From above chart there are 16 respondent who invest in Equity and are expert of financial and

capital market so they can get reasonable return but there are 8 respondent who invest in Equity but

they have some knowledge of MF/ share market.

But there are very few who invest in UIP an insurance plan, as most of respondent is actually not

aware about ULIP plan there return and risk so the customer mostly don’t invest in ULIP plan.

2

16

12

4

12

5

3

8

15

3

78

5

0

2

4

6

8

10

12

14

16

18

Bank savings & FD Equity Mutual Funds ULIP

No

. Of

Res

po

nd

ent

Investment Pattern

Konwlege of Investment VS. Investment Pattern

Expert of Finance & Capital market Knowledge of Bank FD/Post office/NSC

Knowledge of Mutual Fund / Share Market No Knowledge

32

How long you instead to be investment and what is your purpose

Purpose of Investment / Time Period

Less than

5 years

Between

5-7 years

Between

7-10 years

Above

10 years

Grand

Total

Generate current income & also grow

the value of investment somewhat

overtime by taking little risk 15 8 3 6 32

Grow the value of investment

moderately over time by taking a fair

level of risk 6 9 5 5 25

Grow the value of investment

substantially over time by taking a

considerable amount of risk 9 3 1 2 15

Preserve the value of my investment &

minimize the risk of my wealth losing

value 6 12 6 4 28

Grand Total 36 32 15 17 100

Table 2.8

Graph 2.8

Analysis

From above table and diagram there are more respondent who all are interested to get

current income also grow the value of investment it is possible in term of buying value stocks in

which there are high dividend yield also stock price may rise in future. Also individual can invest

in pension fund.

158

366

95 5

93 1 2

612

6 4

0

10

20

Less than 5 years Between 5-7 years Between 7-10 years Above 10 years

Purpose of Investmnet VS. Time Period

Generate current income & also grow the value of investment somewhat overtime by takinglittle risk

Grow the value of investment moderately over time by taking a fair level of risk

Grow the value of investment substantially over time by taking a considerable amount ofrisk

Preserve the value of my investment & minimize the risk of my wealth losing value

33

FINDINGS

Age: influences the needs of an individual in several ways. When an individual starts earning in

their early twenties they are more concerned with self-protection and the protection of income.

Going forward, the responsibility of an individual increases when they get married, acquire assets

like a home and a retirement fund, and they start to need to take care of their parents. Age also

affects the cost of buying protection. Insurance premiums for a person in the 20-25 year age group

are much less than the premiums for a person in the 30-35 year age group. So it is wise to buy

insurance protection as early as possible.

Dependents: When an individual gets married, they will extend their family and have the

responsibility of providing for their spouse and children. At a later stage in life when the

individual’s parents retire, they may also become dependent, thereby increasing the individual’s

number of dependents. Hence the greater the number of dependents, and the greater the need for a

higher insurance protection cover.

Income: The income of an individual has a larger role to play in meeting their financial

responsibilities, like planning for their children’s education, children’s marriage, buying a home

and building a retirement fund. When an individual starts earning their income is generally low.

At that stage the income cannot take care of requirements like buying a house and/or a car. Loans

bridge this gap. Insurance protection against these loans is important in the event of anything

happening to the family’s main income provider. For responsibilities such as investing for a

child’s education and marriage and their own retirement, the individual can start with a small

amount and increase their investments as their income grows.

Assets and liabilities Assets and liabilities have a considerable effect on an individual’s

protection needs. Assets like a house are mainly financed through loans. Income protection will

enable the repayment of such loans in the event of long-term disability or the untimely death of

the family income provider. Liabilities, such as loans taken to buy a car or for vacations, can be a

burden on the family members in the event of the income provider’s death. It may force the family

to sell other assets or dip into investments to clear these loans which can be detrimental to the

interests of the family

34

III) THEORETICAL

BACKGROUND

35

Portfolio Construction

Constructing a portfolio depends, to a significant degree, on the nature of the investor. Portfolio

refers to a combination of securities such as stocks, bonds and money market instruments. Portfolio

construction is the process of combining the broad assets classes to yield optimum return with

minimum risk.

Approaches in portfolio construction

1. Traditional approach

2. Markowitz efficient frontier approaches

Traditional approach

The traditional approaches deals with two crucial decisions

1. Determining the objectives of the portfolio

2. Selecting the securities to be included in the portfolio.

This is carried out in 4 to 6 steps. The constraints of the investor should be analysed before

formulating the objectives. Then based on objectives the securities are selected. There after the risk

and return of the securities should be studied. The investor must determine the main risk categories

that he or she is trying to minimize. A compromise between risk and no-risk factors is then made.

Finally relative portfolio is then assigned to securities like bonds, stocks, and debentures and

diversification is carried out.

Following is the flow chart depicting the above steps.

36

Chart 3.1

37

Analysis of constraints

These are some of the most common constraints: -

Income needs / financial need

The income needs depend on the need for income in constant rupees and current rupees.

Need for current income:

The investor should establish t income which the portfolio should make. The current income

needs depend on the total current financial plan of the investor. The expenditure required to maintain

a certain standard of living and all the other income generating sources should be determined. Then

it is possible to determine how much income must be provided for the portfolio of securities.

Need for constant income:

Inflation reduces the purchasing power of money. Hence the investor estimates the impact

of inflation on his estimated stream of income and tries to create a portfolio which could offset the

impact of inflation.

Liquidity

The liquidity requirement of an investor are highly subjective. If the investor prefers to maintain

high liquidity, then funds should be invested in high quality short term debts such as money market

funds, commercial papers and shares that are widely traded. The investor should plan his cash drain

and the need for net cash inflows during the investment period.

Safety of principal

Investment in bonds and debentures is safer than investment in stocks. Even among stocks, the

money should be invested in regularly traded companies of long standing. Investing money in

unregistered finance companies may not provide adequate protection.

Time horizon

Time horizon refers to the investment timeframe under consideration. An individual’s risk and

return preferences are often described in terms of his life cycle.

The first stage of early career days assets are few than liabilities. He has long horizon of life

expectancy with possibilities of growth in income. He may take high risk and growth oriented

investments.

At midcareer stage he wants to protect his capital investment due to less time horizon and more

assets than liabilities. He may take moderate risk and reduce some high risk investments.

At final stage or retirement age time horizon is limited, he needs steady income. He shifts his

investment to the lower return and low risk category, as now safety of principal is at top priority.

38

Tax consideration

Investors in the income tax paying group consider the tax consideration they could get from their

investments. They would always like to reduce taxes. Investing in government bond and NSCs

can help avoid taxes. This constraint makes the investor include those assets in his portfolio that

will reduce taxes.

Temperament.

Some investors are risk lovers who like to take on higher risk even for low returns. Others are risk

averse, who may not be willing to take high risk even for high returns. The other category may be

risk-neutral investors who balance returns and risk.

39

Determination of objectives

Portfolios have common objective of financing present and future expenditures from a large pool

of assets. The return that investor wants and the degree of risk that he is willing to take depends

on the constraints.

The common objectives are: -

1. Current income

2. Growth in income

3. Capital appreciation

4. Preservation of capital.

The investor in general would like to achieve all the four objectives; nobody would like to lose his

investment. It is not possible to achieve all 4 objectives simultaneously. If the investor aims at

capital appreciation, he should include securities where there is equal chance of losing the capital.

Thus there is conflict among the objectives.

40

Selection of portfolio

Objectives and asset mix

If the main goal is ensuring adequate current income, then 60% of the investment is on debt

instruments and 40% on equities. The proportion changes on individual preferences. Here growth

of income becomes secondary and stability of the principal ranks third.

Growth of income and asset mix

Here the investor looks in certain percentage of growth in income from his investment. The

investor’s portfolio may consist of 60-100 % in equities and 0-40% in debt instruments. The debt

portion of portfolio may consist of investments are entitled to tax exemptions.

Capital appreciation and asset mix

Capital appreciation means that the value of original investment increase over the years. Investment

in real estate may provide a faster rate of capital appreciation, but it lacks liquidity. In the capital

market, values of shares are much higher than the original issue prices. Next to real estates, the

stock market offer the best opportunity for capital appreciation. Here he invest. 90-100% of his

portfolio in equities and 0-10% in debt.

Safety of principal and asset mix

Usually risk averse investors are highly particular about the stability of the principal. The investor’s

portfolio may comprise more debt instruments, and within the debt portfolio, there would be more

of short term debts.

41

Risk and return analysis

The traditional approach to portfolio is based on some basic assumptions.

First, an individual prefers larger to smaller returns form securities. An investor has to take risk to

achieve his goal. The ability to achieve higher returns depends on his ability to assess risk and take

risk. These risk are interest rate risk, purchasing power risk, financial risk and market risk. The

investor analyses the varying degrees of risk and construct his portfolio. At first, he establishes the

minimum income that he must have to avoid hardships under the most adverse economic conditions

and then decides what loss of income can be tolerated. The investors make a series of compromises

on risk and no-risk factors such as taxation and marketability after assessing and minimizing the

main risk.

Diversification

Once the asset mix is determined, and the risk and return are analysed, the final step is the

diversification of the portfolio. Good quality convertibles may balance financial risk and purchasing

power risk. The portfolio is diversified according to investor’s need for income and his risk

tolerance level.

Steps in portfolio diversification

Chart 3.2

The investor must select the industries appropriate to his investment objectives. Each industry meets

the goals of the investor. Likewise, the investor should select one or two companies from each

industry. The selection depends on its growth, yield, expected earnings, past earnings, PE ratio,

dividend and the amount spent on research and development. The final step is to determine the

number of shares of each stock to be purchased.

Selection of Industries

Selection of Compnies in Industry

Determining the Size of Participation.

42

ICICI PRUDENTIAL PRODUCT

ICICI Prudential have different plan are as follows

TERM

PLAN

WEALTH

PLAN

RETIREME

NT PALN GROUP PLAN

RURAL

PLAN

1 ICARE II

GAURENTEED

WEALTH

EASY

RETIREMENT

GROUP TERM LIFE

SOLUTION

SARV JANA

SURAKSHA

2

CASH

ADVANTAGE

EASY

RETIREMENT SP GROUP GRATUITY

3

SAVING

SURAKSHA

IMMEDIATE

ANNUITY

GROUP

SUPERANNUATION

4 ELITE LIFE II

GROUP LEAVE

ENCASHMENT

5

ELITE

WEALTH II

GROUP IMMEDIATE

ANNUITY PLAN

6

WEALTH

BUILDER II

Table 3.1

From the above table we can observe different product and each product have different benefit.

There are some ULIP plan in which many customer invest heavily as there are reasonable return as

they are connected with equity and debt market.

So for customer who have invested in ULIP plan are more in worried about their NAV (Net Asset

Value).

So fund performance is important to know the growth of fund so as to increase NAV.

As I have selected some of the Equity base Fund.

1) Maximizer fund

2) Multicap growth fund

3) Bluechip fund

4) Rich fund

5) Opportunity fund

43

Blue chip fund

Objective: To provide long term capital appreciation from equity portfolio predominantly

invested in large cap stocks.

Asset Mix Asset Mix Asset Mix

Equity & Equity related securities MAX 100% & MINI 80% 97%

Debt, Money Market & Cash MAX 20% & MINI 0% 3%

Table 3.2

Graph 3.1

44

Maximiser V

Objective: the objective of the fund is to provide long term capital appreciation through

investment primarily in equity & equity related instruments.

Asset Mix Asset Mix Asset Mix

Equity & Equity related securities MAX 100% 94%

Debt, Money Market & Cash MAX 25% 6%

Table 3.3

Graph 3.2

45

Multi Cap Growth Fund

Objective: To generate Superior Long-term Returns from diversified Portfolio of equity &

equity related instrument of large, mid & small cap companies.

Asset Mix Asset Mix Asset Mix

Equity & Equity related securities MAX 100% & MINI 80% 93%

Debt, Money Market & Cash MAX 20% & MINI 0% 7%

Table 3.4

Graph 3.3

46

Opportunity Fund

Objective: To generate superior long-term returns from a diversified portfolio of equity

and equity related instruments of companies operating in four important types of industries viz.,

Resources, Investment-related, Consumption-related and Human Capital leveraged industries

Asset Mix Asset Mix Asset Mix

Equity & Equity related securities MAX 100% & MINI 80% 90%

Debt, Money Market & Cash MAX 20% & MINI 0% 10%

Table 3.5

47

R.I.C.H Fund

Objective: The objective of the fund is to generate superior long-term returns from a diversified

portfolio of equity and equity related instruments of companies operating in four important types

of industries viz., Resources, Investment-related, Consumption-related and Human Capital

leveraged industries.

Asset Mix Asset Mix Asset Mix

Equity & Equity related securities MINI 80% 98%

Debt, Money Market & Cash MAX 20% 2%

Table 3.6

Graph 3.5

48

Proportion

Inception

date Fund

Equity

%

Debt

%

Return

% Bench mark

Bench mark

return %

29-Aug-11 Maximizer 94 6 19.57

S&P BSE

100 19.49

24-Nov-09 Opportunity 90 10 9.56

S&P BSE

200 9.68

24-Nov-09

Multi-cap growth

fund 93 7 10.13 CNX 500 13.54

24-Nov-09 Bluechip fund 97 3 7.4 CNX nifty 20.19

11-Apr-08 RICH fund 97 3 8.93

S&P BSE

200 22.82

Table 3.7

From above table we can observe that the return of fund are almost same in Maximizer &

opportunity as compare to Bench Mark return. But Rich Fund has given very low return i.e. 8.93 as

S&P BSE 200 has given around 22.82 so the fund manager might have not selected proper stock.

-

49

MANAGEMENT LESSON:

50

1. Focus on the goal: I learn here to go for your goal don’t diversify whatever the matter

always go straight and achieve goal.

2. Time management: This is the curtail thing I learn time management because if you a not

capable to manage your time maybe you lose lots of opportunity in your life.

3. Decision making skill: I learn about the decision making ability because I take a training

of financial advisor so my job is to analyze the risk and need and give suggestion to the

other. So I have to make decision after using need analysis tool.

4. Know your capability: This is about knows your capability when person know his/her

capability so he/she is able to provide better performance.

5. Identify the problem: If person identify the problem then he able to tackle with that

problem & in insurance we try to identify the problem of the person.

6. Determine the risk: This is the base in insurance sector which I learn determine the risk

because if you able to do this & if it is certain then also you save at least rather than losing

everything.

7. Transfer the risk:. In insurance sector we learn this thing to transfer your risk to the others

because it less impact on your financial status. Insurance bearing the risk of others so it

obvious thing which I learn.

8. Divide the task in sub-task: If you try to divide your work in different part so it easy to

handle that task and complete in efficient way.

9. Generate creative idea: when you think this is the problem then you think how it can be

handle & come out with creative idea.

51

10. Take your responsibility: don’t try to put your work to the other you should take your

responsibility & complete work by own.

11. Co-ordination: don’t go individually in the organization. You should support your

colleague or staff.

12. Be flexible: Don’t follow always a routine make your time table flexible as per

requirement of the organization.

13. Make contacts: Make friends in organization you don’t know who is came as your support

in bad times.

14. Resolve dispute: If there is some conflict between you and your colleague. So resolve this

dispute and be friend. This is good for peaceful working environment.

15. Get deep knowledge about your Industry: Whenever you work get deep knowledge about

that industry to increase your position as well as status.

16. Keep high your patience: Sometimes you face some person those try to irritates you by

asking stupid question that time don’t lose your patience and give answer with smile on

your face.

17. Be energetic: Don’t behave like lazy shows your energetic face to the other it make good

impact on your personality.

18. Self-confidence: Always keep confidence on you don’t lose it because confidence is the

key of success.

19. Self-motivation: Always motivate yourself using such types of word you can do it nothing

is impossible for you.

52

20. Trust yourself: Keep trust on yourself because if you are not having trust on you then how

other persons trust on you.

21. Customer is god: Always respect your customer because you are getting this job to serve

these customers.

22. Tolerate others: Don’t lose your temperament tolerate others & keep going ahead.

23. Be good listener: Before taking a decision you should listen the entire things whatever

they want to speak then reply.

24. Accept mistake: If you are making some mistake then accept because we all are human life

and we can make mistake.

25. Positive attitude: Always think positively because when you start thinking positively then

almost half of the work done that point of time.

26. Do work honestly: Always be honest with your work because this is the bread & butter of

53

RECOMMENDATIONS TO

COMPANY

54

RECOMMENDATIONS TO COMPANY

Since ICICI Prudential Life Insurance co. ltd is the largest in terms of FDI invested, work

force, market share, no. of customers. All these positive stands of the company place at the

number one position. On second aspect whatever amount of money ICICI Prudential save, can be

used to increase the no. of policies, which will helpful to increase the market share of the

company. Since the customers think about the companies in the industry, when they invest money

in the life insurance industry. So it’s necessary to increase the market share of the company. There

are some recommendations.

Open some more branches in semi urban and rural area.

ICICI Prudential has almost its branches in urban area or metros. So in order to

increase the no. of customer, ICICI Prudential should increase the approach towards

potential customers. For that it has to increase the branches in the semi urban cities like C,

D grade cities. And the rural marketing is the best option for ICICI Prudential to increase

its base in the market

Improve customer services.

In order to take the advantage of being industry leader in private sector, ICICI

Prudential has to improve its customer services. According to my experience in the

company, a good number of customers forget to pay their premium at time so it causes a

big loss to the company. ICICI Prudential has already collaborated with the ICICI bank for

its Bancassurance facility and then can include another feature in it. ICICI bank can offer a

bank account with the life insurance policy in which an ATM card will be provided. This

card will have all the information regarding the policy as like future premium payment

dates, payment made, money value of the policy at that date, value of the unit linked plan

and all other information what the customer want. This will help the customer to pay

premium on time and save their losses. This will be mutually helpful for both sister

companies, ICICI bank will get new account and ICICI prudential will be able to more

efficient services to their customers.

55

Bring some unit linked life insurance plans in the market.

Being a market leader doesn’t ensure the leadership in the future. Since after

increment in FDI from 26% to 49% all player will have the opportunity to capture the

market share. So in order to maintain its position ICICI Prudential should

-Introduce some new market linked insurance plan, which will give a competitive

advantage to the ICICI Prudential against its competitors.

Trained the financial advisors more efficiently.

In the changed scenario, more efficient training will be needed, so ICICI Prudential

should provide good and efficient training to their financial advisors. Because they are the

one who interact directly with the customers. So good training will give them the right

way to deal with the potential customers.

56

IV CONCLUSION

57

Conclusion

After the doing this entire project I get a shocking result with the people are giving more importance

to their financial assets such as car, property etc. than their own life. They are not able to identify

the value of life. They should understand the life is also as a generating assets which is facilitates

all these things because you can make a prediction about your valuable assets but you can’t make

prediction about your life.

Earlier Life Insurance was taken as an option for risk cover or a tax saving by people. But in the

present scenario the mind set and outlook of people has changed a lot. They now consider Life

insurance as an investment opportunity in long run. Clients have also shifted a lot from traditional

plans to Unit linked insurance plan (ULIP). ULIP provide the investor with benefits like Potential

for better returns.

They should provide this facility insurance:

1. Flexibility to invest the money the way customer wants: Unlike traditional plans, Ulips allow

customer to full discretion to choose the fund option most appropriate to their risk appetite.

2. Flexibility to change the fund allocation: Ulips also give the customer an option to change the

fund allocation at a later stage through fund switching facility.

3. Focus on need based selling of insurance plan rather than increasing number of policies.

4. Company should focus on only financial advice rather than forcing to purchase policy.

5. Financial advisor/agent should give proper disclosure about the rider facilities because lots of

people are not aware about these facilities. So they can save money to invest in other policy to

secure their need.

6. Financial advisor should focus on customer need rather than his/her commission.

58

BIBLIOGRAPHY

Internet resources:

Search engine : www.google.co.in ,

Websites of the organization : www.iciciprulife.com

Other websites : www.yahooanswer.com

www.irda.gov.in

www.Investopedia.com

Company resources:

Inputs from company team and trainer.

Product Brochures of ICICI Prudential Life Insurance co. ltd

IC33 book for Financial Advisors by IRDA

59

ANNEXURE

QUESTIONNAIRE

Personal information

1. Name of the proposer/customer. ____________

2. Age

o Below 30

o 30-40

o 40-50

o Above 50

3. Marital status

o Married

o Unmarried

4. Qualification ___________

5. Occupation

o Salaried person

o Self employed

6. Annual income

o Below 2L

o 2-5 L

o 5-10 L

o Above 10 L

7. Dependents

Name Relation Age/DOB

Household expenses

8. What are your current responsibilities?

o Loan

o Other liabilities (family commitment)

o Sundry Creditors.

o Bank CC/ OD

60

9. Do you have any of these?

o Health insurance. YES / NO

o Pure Insurance YES/ NO

o Disability/ physical impairment/ trauma benefits. YES/ NO

INVESTMENTS

10. How long do you intent to remain invested?

o Less than 5 years

o Between 5- 7 years

o Between 7-10 years

o Above 10 years.

11. How good is your knowledge about Finance and Capital Market?

o No knowledge

o Knowledge of Bank FD/Post Office/ NSC

o Knowledge of Post office/ Mutual Fund/ Share Market.

o Expert on Finance and capital market.

12. When you invest money your primary goal is to :

o Preserve the value of my investment and minimize the risk of my wealth losing

value

o Generate current income and also grow the value of investments somewhat

overtime by taking little risk.

o Grow the value of investment moderately over time by taking a fair level of risk

o Grow the value of investment substantially over time by taking a considerable

amount of risk

13. Have you invested in any of the following

o Bank savings & FD

o ULIP

o Traditional insurance product

o Direct equity

o Government bond

o Mutual fund

o Property portfolio (real estate)

o Retirement fund

o PPF/ EPF/ VPF

14. Give your preference on the following investment plans.

o ULIP

o Mutual funds

o Equity

o Pension fund

o PPF

o Government bonds.