hungarian financial supervisory authority

TRANSCRIPT

A publication by the Hungarian Financial Supervisory Authority

1013 Budapest, Krisztina krt. 39.

Phone: (00-36-1) 489-9100

Fax: (00-36-1) 489-9102

Website: www.pszaf.hu

©Hungarian Financial Supervisory Authority

Hungarian Financial supervisory autHority

TABLE OF CONTENTS

THE HFSA’S MISSION ......................................................................................7

PRESIDENT’S FOREWORD ...............................................................................8

ACRONYMS ...................................................................................................14

THE HFSA’S STATUS AND OPERATING ENVIRONMENT .............................18

MAiN ChANgES iN ThE hFSA ACT, ExpANdEd dECrEE-iSSuiNg righTS ... 18

ChANgES TO ThE rEguLATOry ENvirONMENT ......................................... 19

ECONOMiC ENvirONMENT ............................................................................ 19

RISK-BASED SUPERVISION, IMPACT RATING AND SUPERVISION METHODOLOGY ............................................................................................21

iMpACT rATiNg ANd iNSTiTuTiON ASSESSMENT ....................................... 22Individually supervised institutions ................................................................... 24Jointly supervised institutions ........................................................................... 24

rEviSiON OF METhOdOLOgiES ..................................................................... 25On-site inspection manuals ................................................................................ 25

iCAAp-SrEp MANuALS ..................................................................................... 25

KEY TARGET AREAS OF SUPERVISION IN 2012 ..........................................26

KEy TArgET ArEAS OF SupErviSiON iN 2012 .............................................. 26

SUPERVISION OF INSTITUTIONS .................................................................32

OFF-SiTE SupErviSiON .................................................................................... 33Off-site supervision of money market institutions .......................................... 34Off-site supervision of pension, healthcare and voluntary mutual funds .... 35Off-site supervision of capital market institutions .......................................... 36Off-site supervision of insurers .......................................................................... 37

ON-SiTE SupErviSiON ..................................................................................... 38Findings of on-site inspections ........................................................................... 38Measures concluding inspections...................................................................... 40Money market sector inspections ..................................................................... 40On-site supervision of pension, healthcare and voluntary mutual funds .... 43Capital market inspections ................................................................................. 43Findings of on-site supervision of insurers ...................................................... 44IT inspections at supervised institutions........................................................... 45

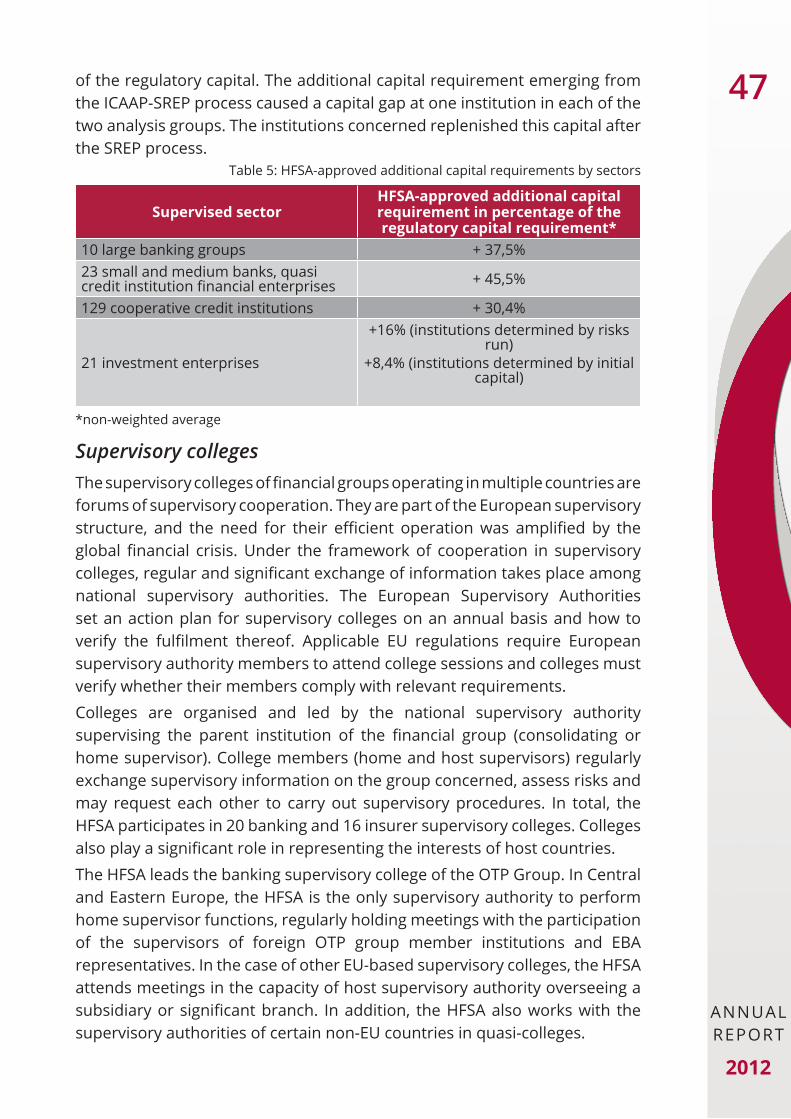

FiNdiNgS OF SrEp ExErCiSES ....................................................................... 46Supervisory colleges ............................................................................................ 47

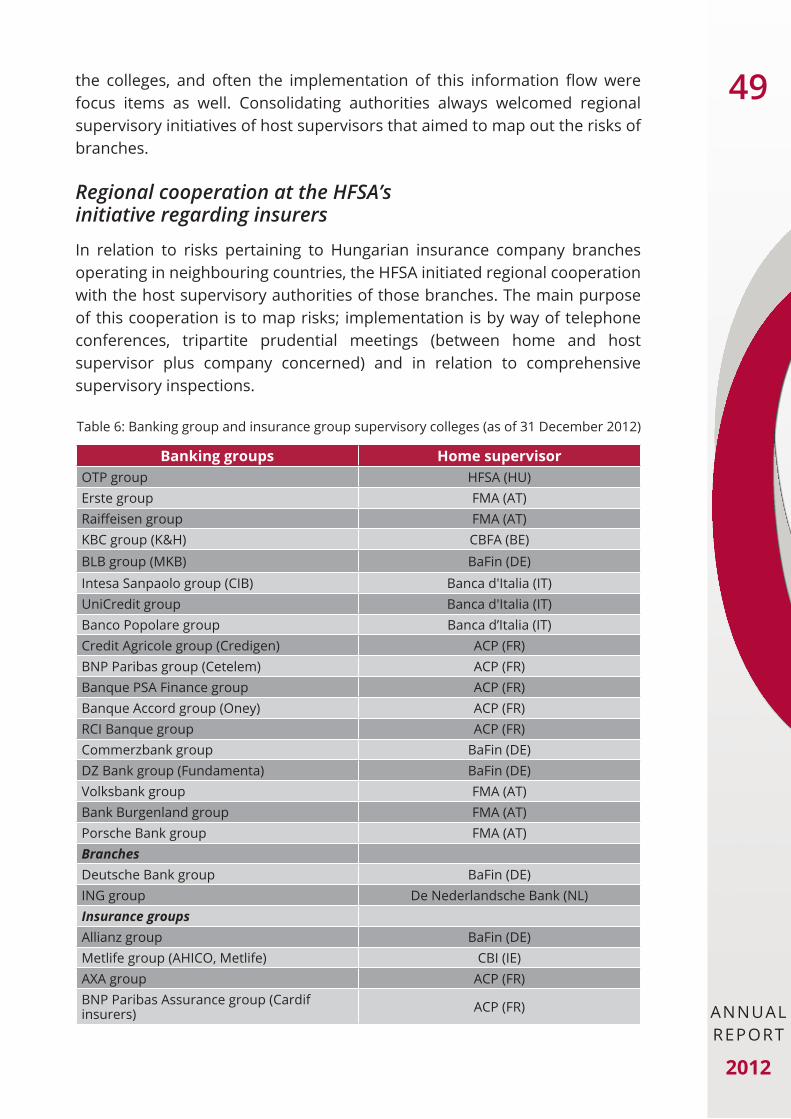

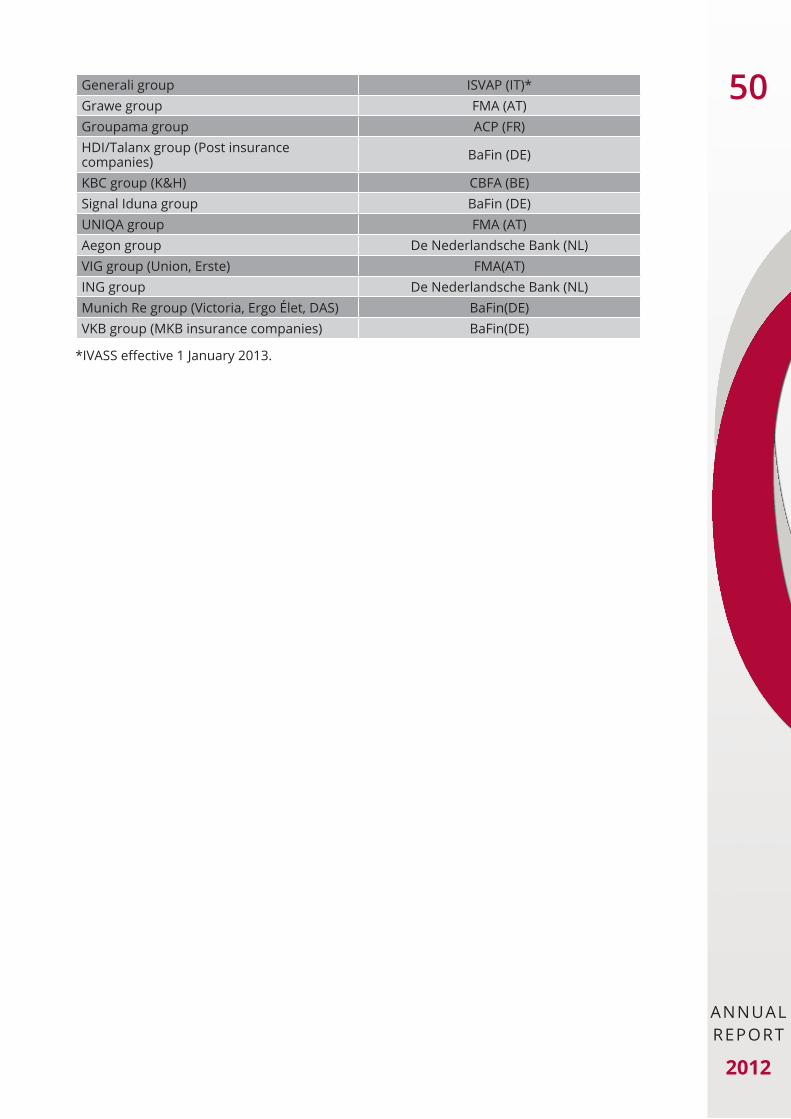

SupErviSOry COLLEgES OF BANKiNg grOupS .......................................... 48Banking group supervision in the capacity of home supervisor.................... 48Banking group supervision in the capacity of host supervisor ...................... 48Insurance colleges ............................................................................................... 48Regional cooperation at the HFSA’s initiative regarding insurers .................. 49

MARKET SUPERVISION .................................................................................51

MArKET SupErviSiON ACTiviTiES ................................................................. 51

MArKET iNSpECTiONS ..................................................................................... 51Short Selling decree ............................................................................................. 51Inspection of unlicensed portfolio management at online FOREX service providers ............................................................................................................... 52Inspection of unlicensed debt purchasing activities ....................................... 53Inspection of unlicensed financial services marketed as bond issuance ..... 54

SupErviSiON CONCErNiNg iSSuErS OF puBLiCLy TrAdEd SECuriTiES . 54

SupErviSOry LiCENSiNg OF SECuriTiES iSSuANCE ................................... 55Verifying compliance of investment funds with new legal requirements .... 55Findings concerning the licensing of the public issuance of securities and introducing them on regulated markets (stock exchange) ............................. 56

CONSUMER PROTECTION ...........................................................................58

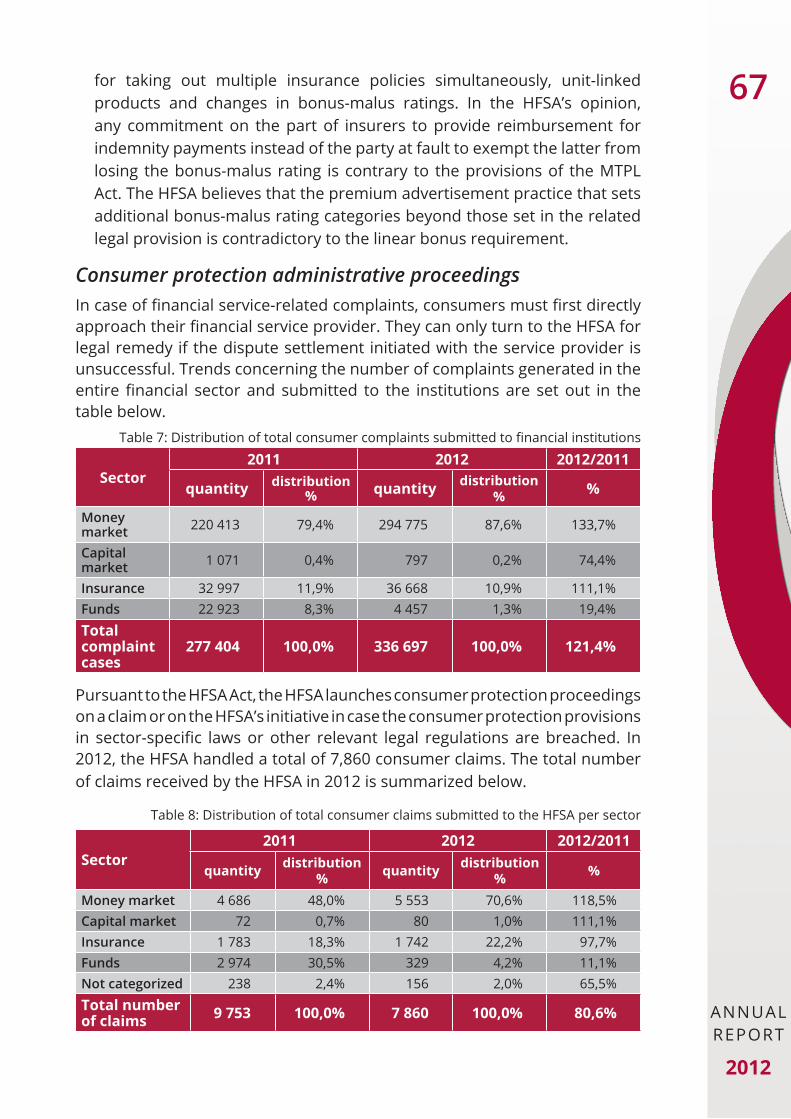

CONSuMEr pOLiCy.......................................................................................... 58

ThE FOuNdATiON OF ThE hFSA’S CONSuMEr prOTECTiON ACTiviTiES ANd ThE TOOLS AT iTS diSpOSAL ................................................................. 60Effective consumer protection regulation ........................................................ 60The HFSA’s own consumer protection tools ..................................................... 62Consumer protection administrative proceedings .......................................... 67Consumer protection inspections ..................................................................... 68Major consumer protection administrative proceedings launched at the HFSA’s initiative in 2012 ........................................................................... 70Major consumer protection administrative proceedings launched on consumer claims in 2012 .............................................................................. 73Resolutions arising from cooperation with the Financial Arbitration board .......................................................................... 75Public actions and enforcing claims of public interest .................................... 76Consumer protection monitoring ...................................................................... 78Regular and proactive supervisory communication – informing customers via contemporary channels ............................................................................... 78Informing consumers via the HFSA’s customer service ................................. 81Informing consumers via the civil consumer protection network ................. 83

LICENSING ....................................................................................................85

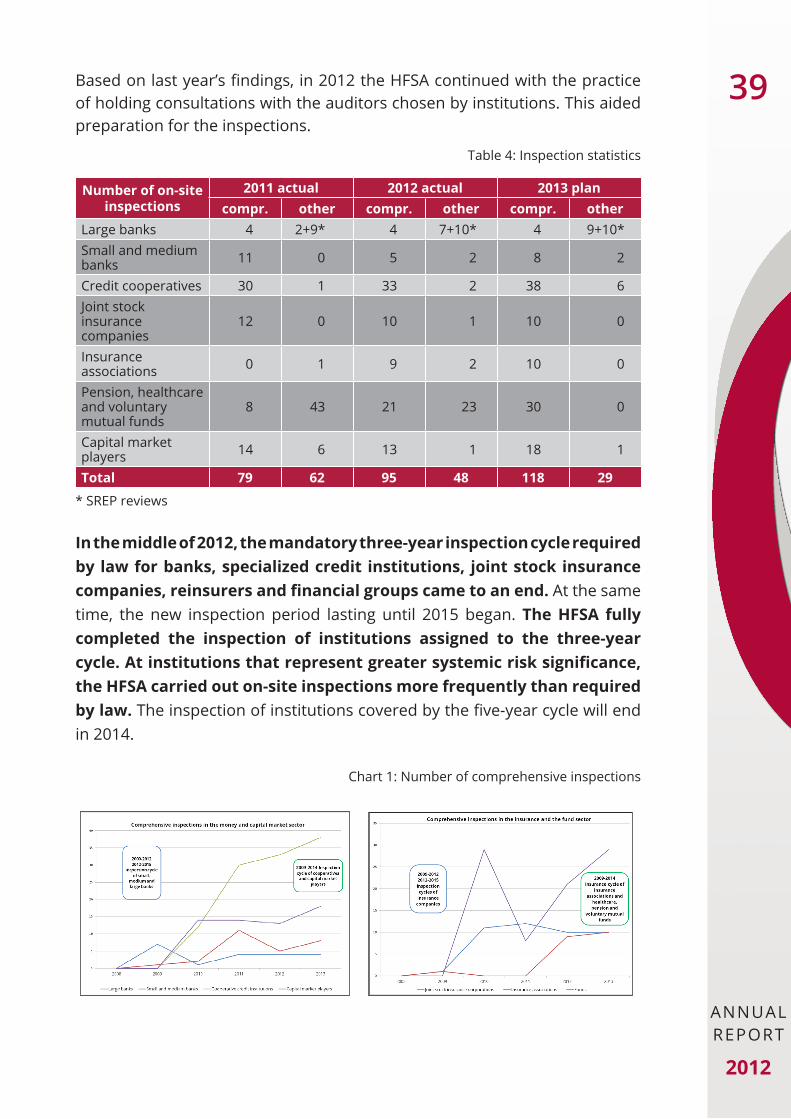

MONEy MArKET LiCENSiNg ........................................................................... 85Credit institution licensing .................................................................................. 85

Licensing financial enterprises and independent intermediaries ................. 86

CApiTAL MArKET LiCENSiNg .......................................................................... 87

iNSurANCE LiCENSiNg ................................................................................... 88

LiCENSiNg iN ThE pENSiON, hEALThCArE ANd vOLuNTAry MuTuAL FuNdS SECTOr .......................................................... 89Licensing authority examinations for intermediaries ..................................... 90

PRUDENTIAL LEGAL ENFORCEMENT ..........................................................91

rELEASE OF ruLiNgS ...................................................................................... 91

MONEy ANd CApiTAL MArKET LEgAL ENFOrCEMENT ............................... 92Money market ...................................................................................................... 92Capital market ..................................................................................................... 96Insurance legal enforcement.............................................................................. 97Legal enforcement regarding pension funds ................................................... 99Legal enforcement concerning authority examinations for intermediaries .............................................................................................. 101

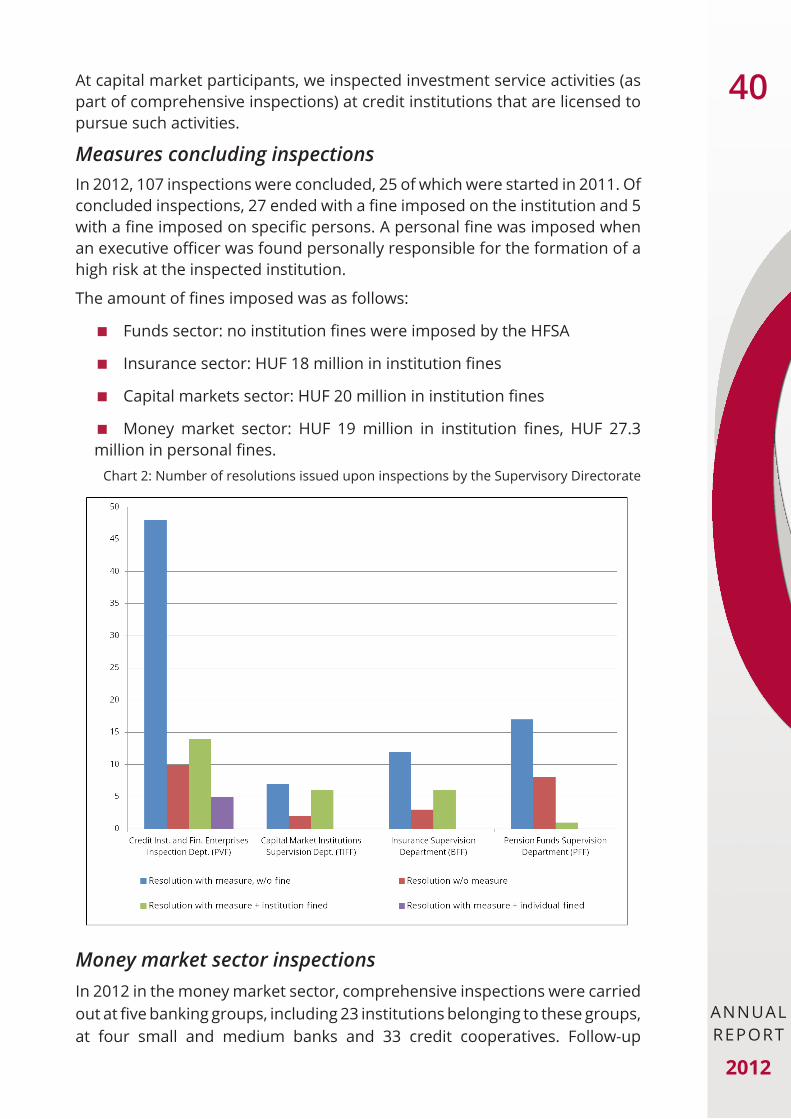

DOMESTIC COOPERATION .........................................................................103

COOpErATiON AgrEEMENTS ....................................................................... 103

CONFErENCES, EvENTS ................................................................................. 103

REGULATORY TOOLS .................................................................................105

hFSA dECrEES ................................................................................................ 105

rECOMMENdATiONS .................................................................................... 107CEO letters .......................................................................................................... 109

METhOdOLOgy guidELiNES ....................................................................... 110

INTERNATIONAL COOPERATION .............................................................112

COOpErATiON AT EurOpEAN LEvEL ........................................................... 112The European financial supervisory structure ............................................... 112

ThE hFSA’S pArTiCipATiON iN ThE EurOpEAN FiNANCiAL SupErviSOry STruCTurE ..................................................................................................... 113The European supervisory authorities and the ESRB ................................... 113

iNTErNATiONAL COOpErATiON OuTSidE ThE EurOpEAN uNiON ........ 116

MANAGEMENT OF THE HFSA’S RESOURCES ............................................122

hr pOLiCy, hr MANAgEMENT ..................................................................... 122HR policy ............................................................................................................. 122HR management ................................................................................................ 122Training, development ...................................................................................... 123

Distribution of resources .................................................................................. 125

iNTErNAL rEguLATiON ANd OrgANizATiON dEvELOpMENT ............... 126Internal regulation ............................................................................................. 126Internal control system ..................................................................................... 126Internal audit ...................................................................................................... 127Organization development ............................................................................... 129

COMMuNiCATiON: hFSA wEBSiTE, CONSuMEr iNFOrMiNg, prESS ..... 130Communication, website, informing of consumers ...................................... 130Press .................................................................................................................... 131IT priorities .......................................................................................................... 132

prEpArATiON OF LAwS ................................................................................ 133Participation in the preparation of laws ......................................................... 133Lower level legal provisions (government decrees, ministerial decrees) ... 134

ThE hFSA’S ACTiviTiES iN dATA prOviSiON, dATA puBLiCATiON ANd riSK MONiTOriNg ................................................................................ 135

ThE hFSA’S ANALySiNg ACTiviTiES ............................................................. 138

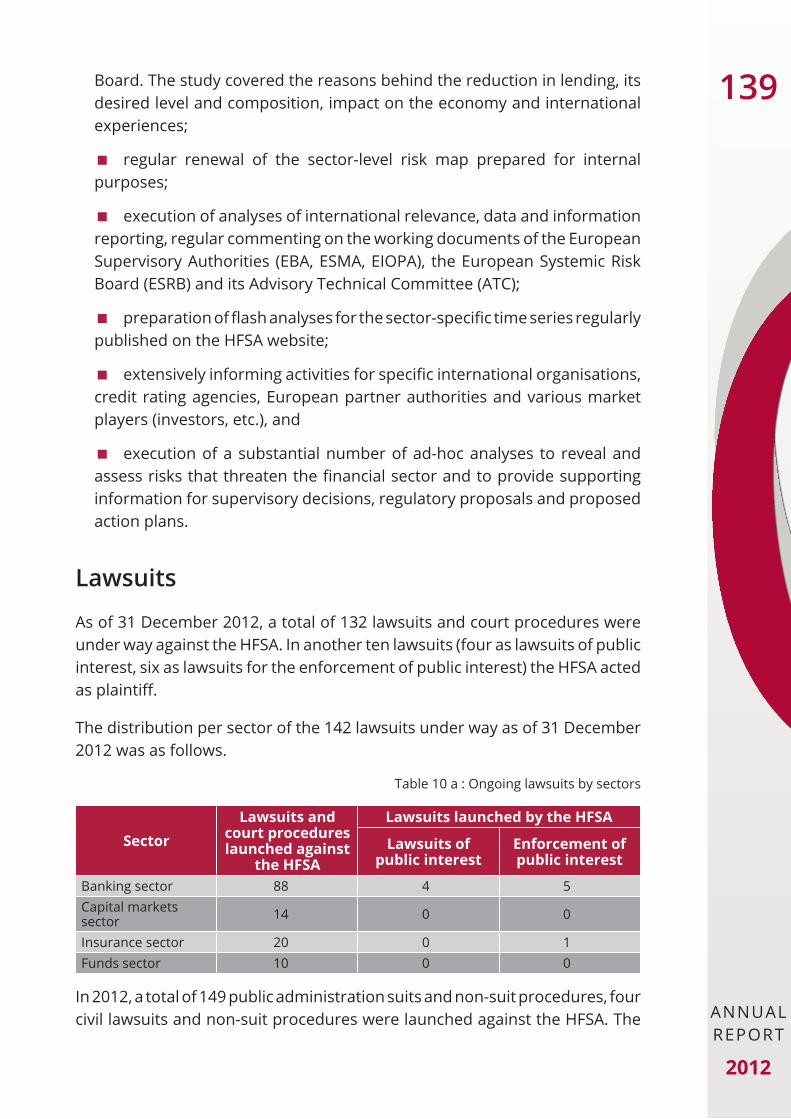

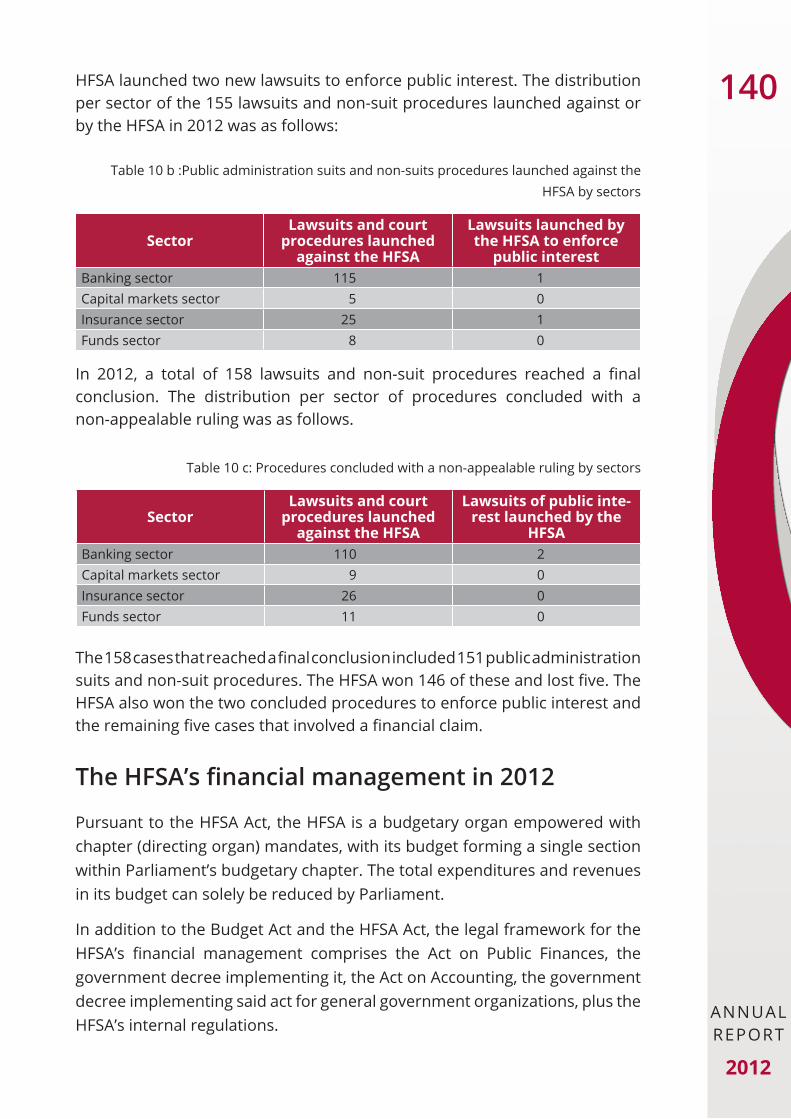

LAwSuiTS ........................................................................................................ 139

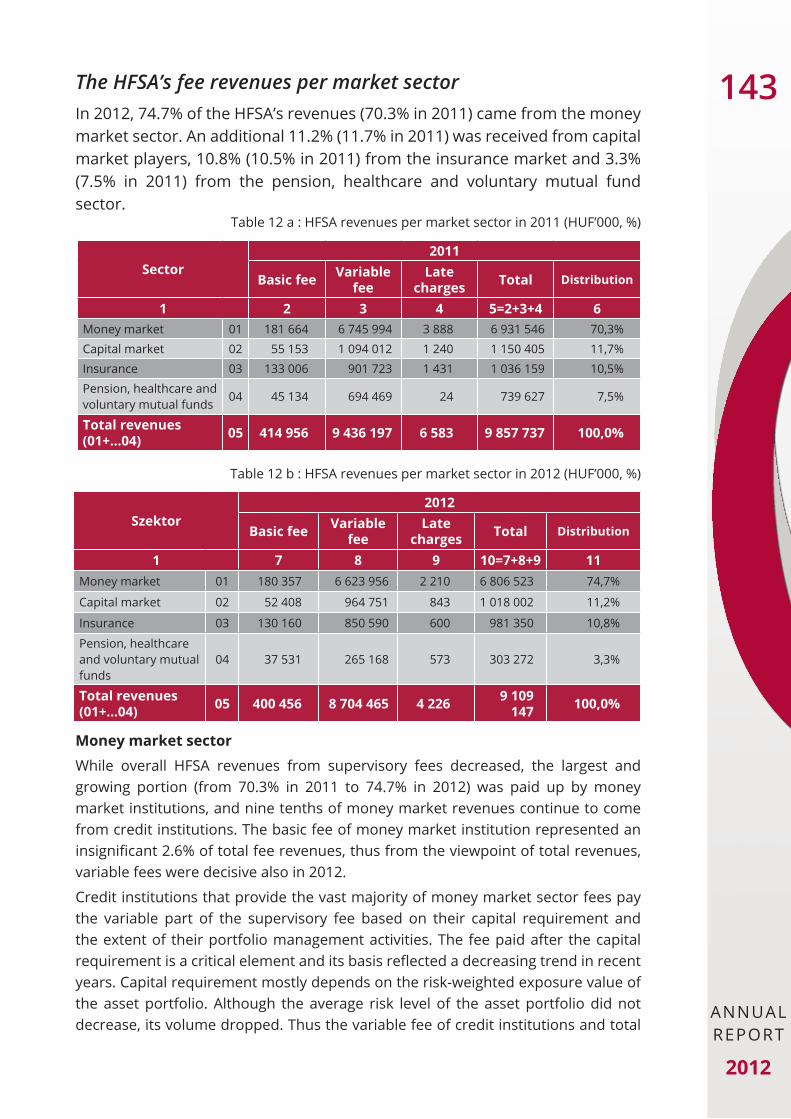

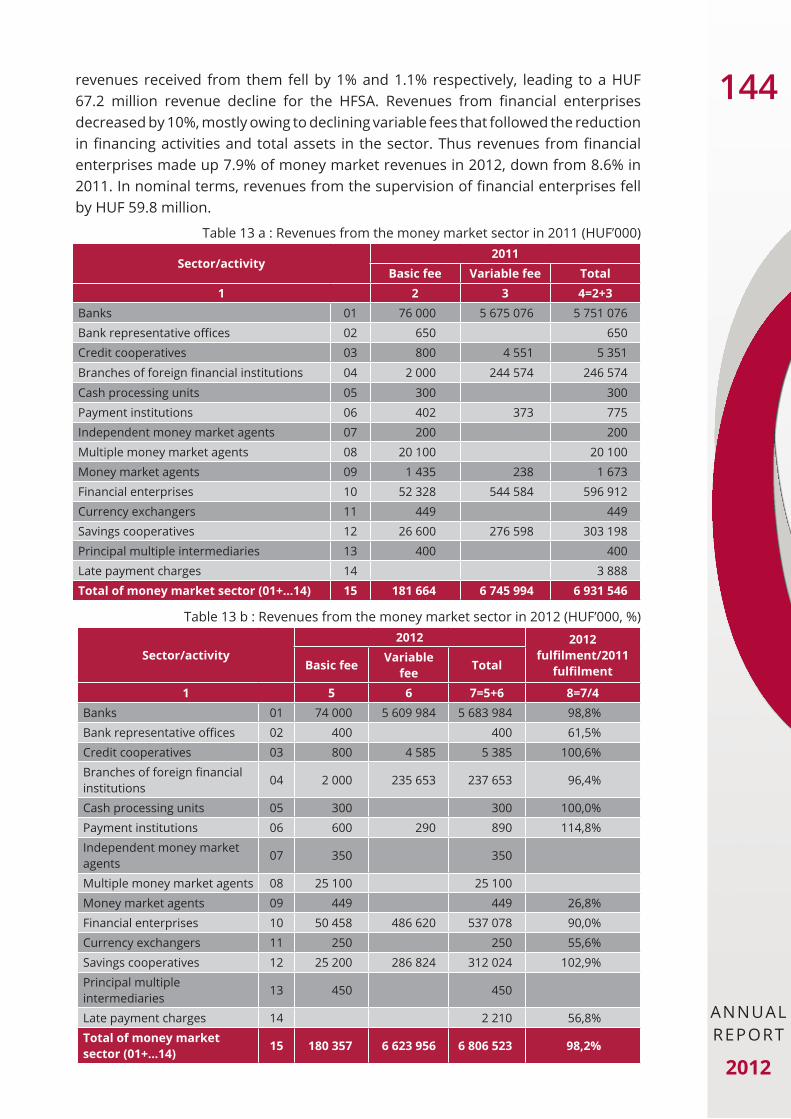

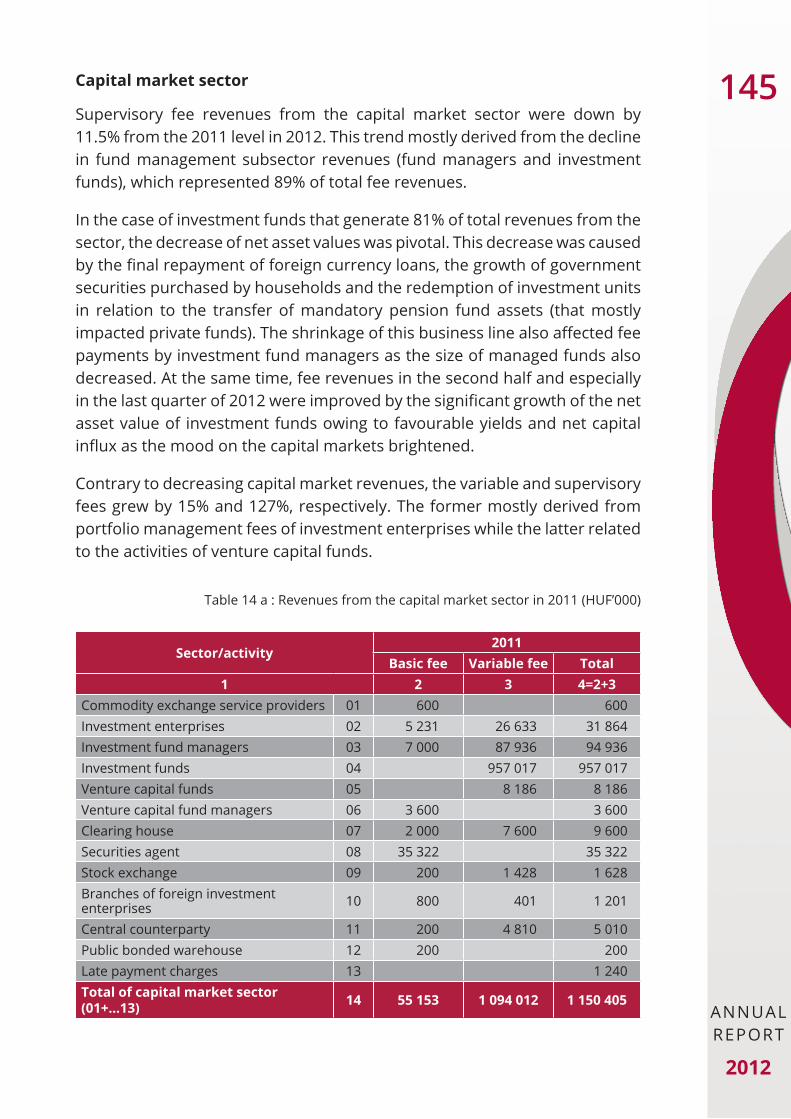

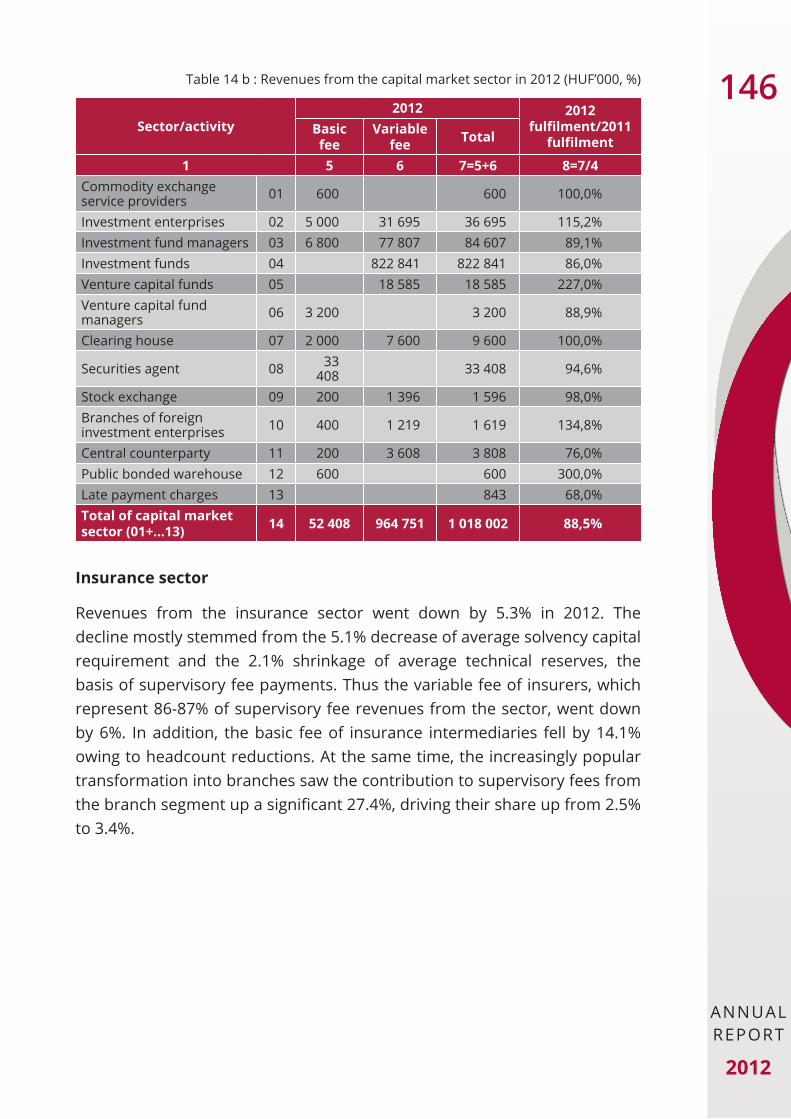

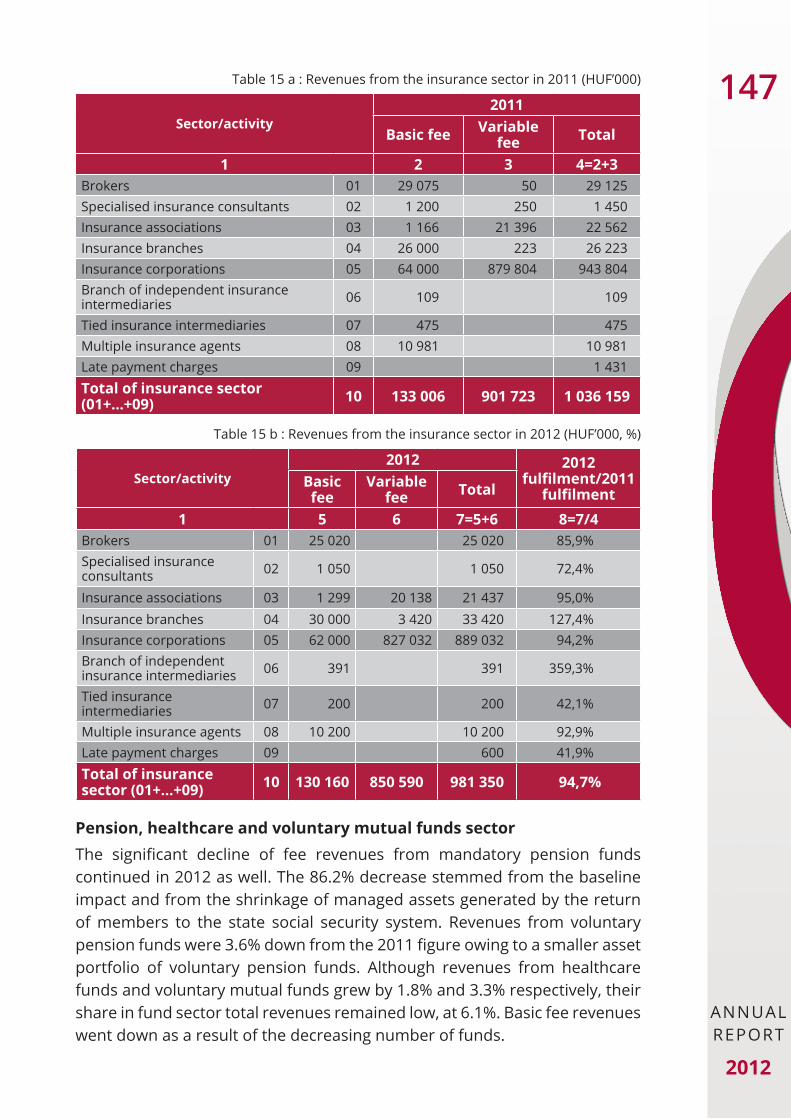

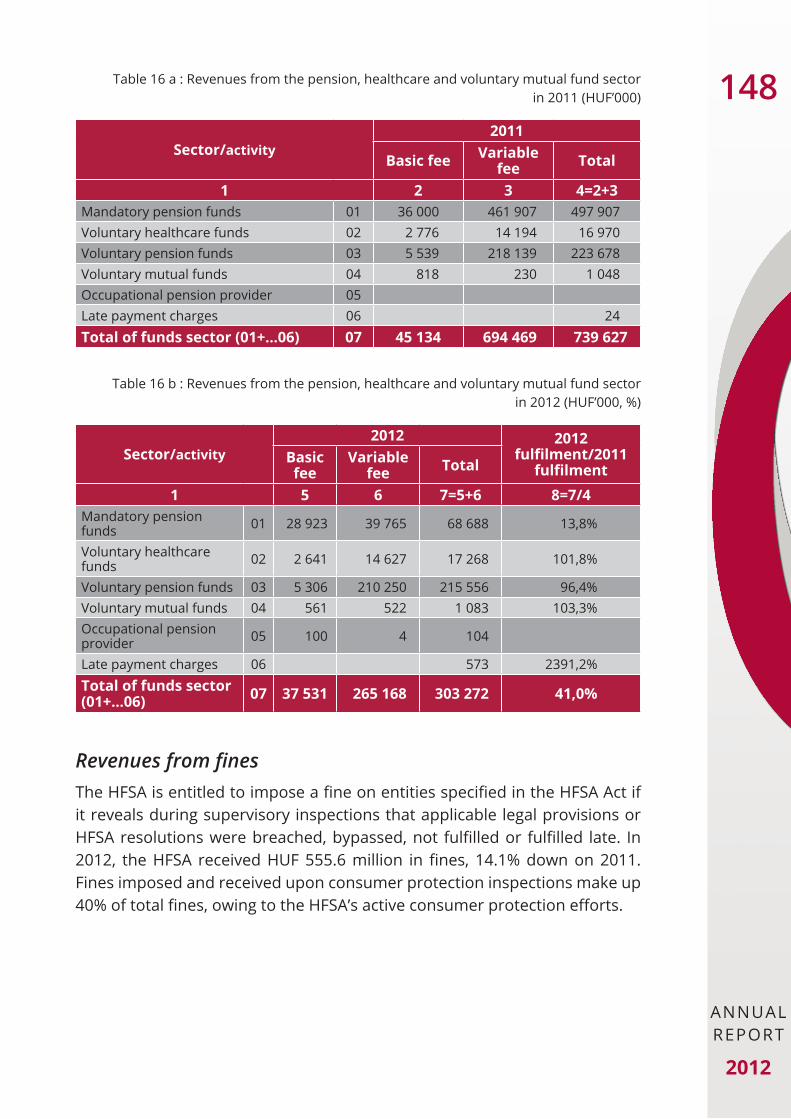

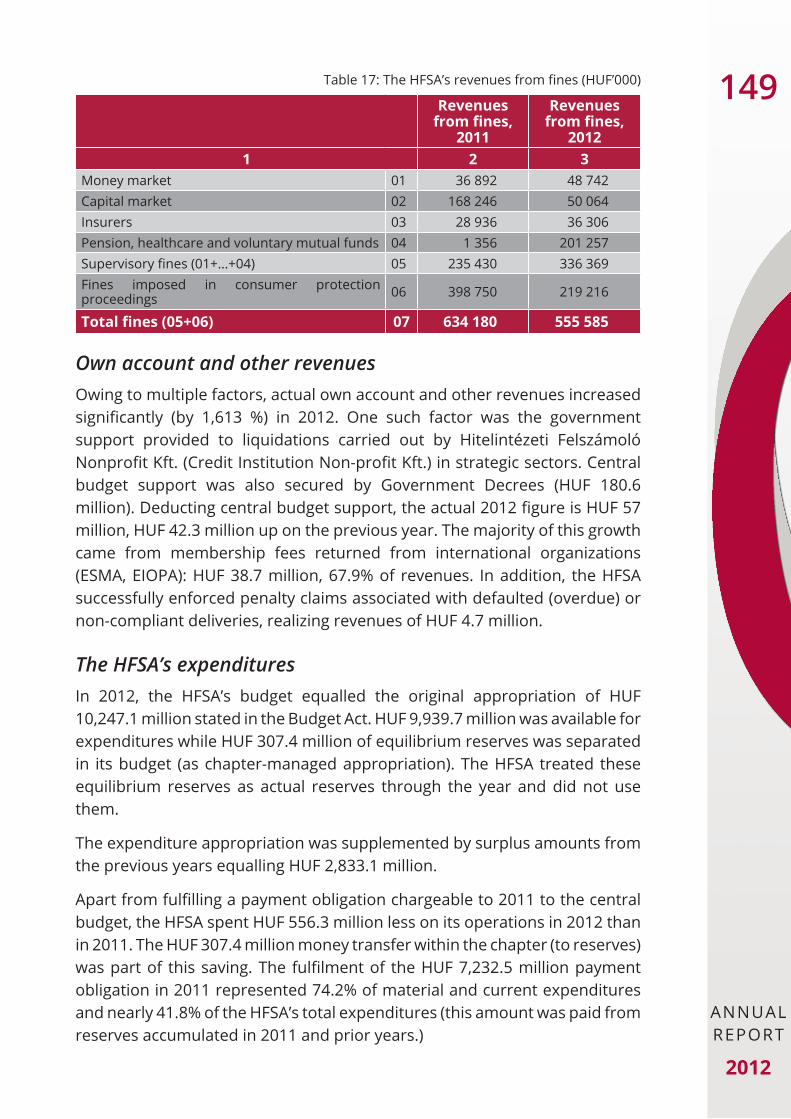

ThE hFSA’S FiNANCiAL MANAgEMENT iN 2012 ......................................... 140Revenues of the HFSA ....................................................................................... 141The HFSA’s fee revenues per market sector ................................................... 143Revenues from fines .......................................................................................... 148Own account and other revenues ................................................................... 149The HFSA’s expenditures .................................................................................. 149

KEY EVENTS OF 2012 IN CHRONOLOGICAL ORDER ................................160

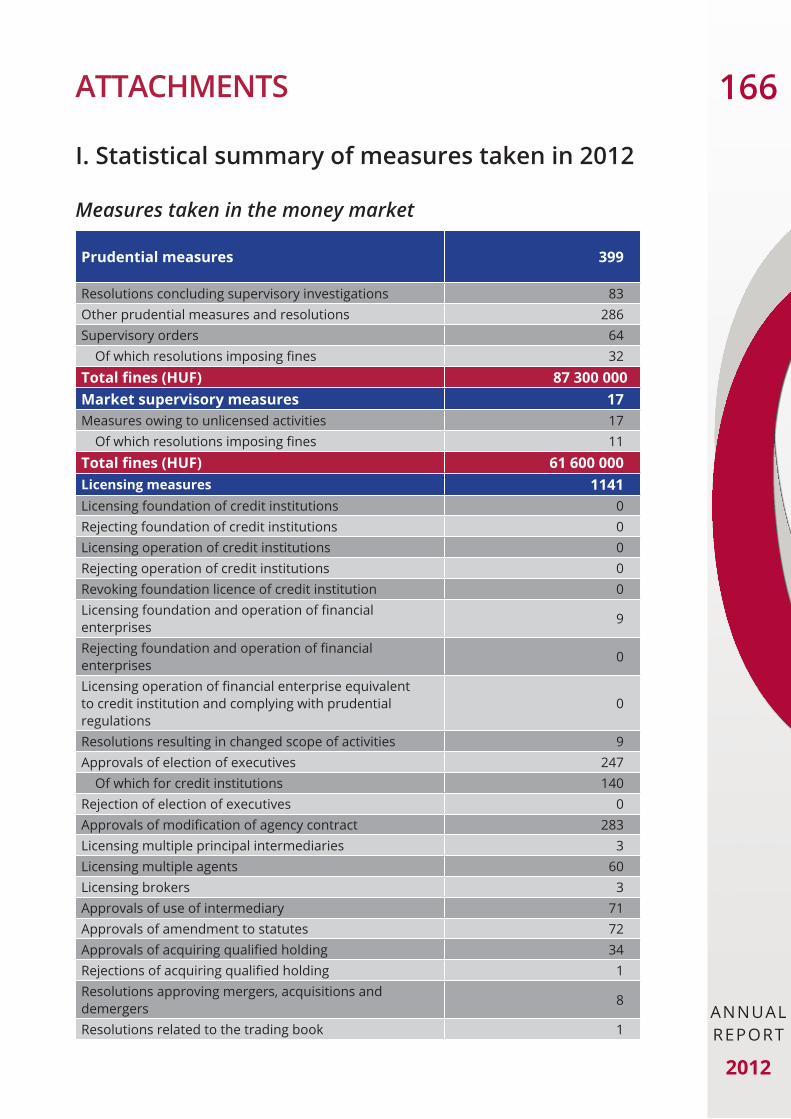

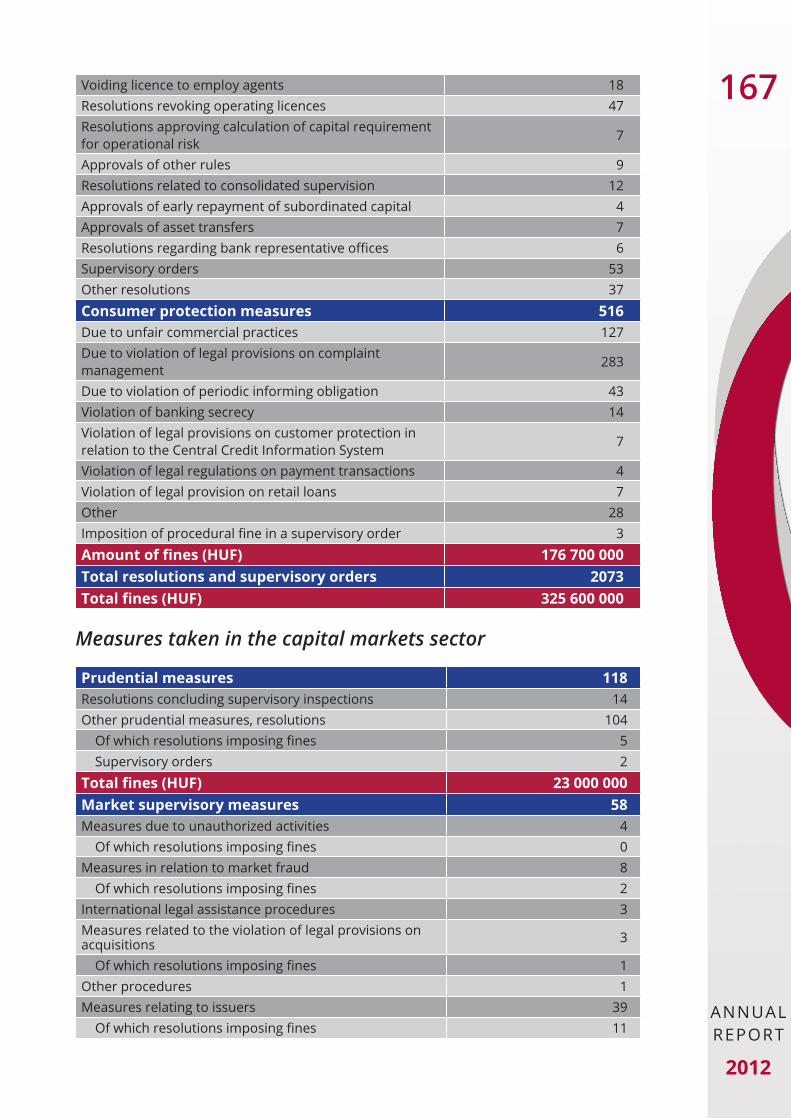

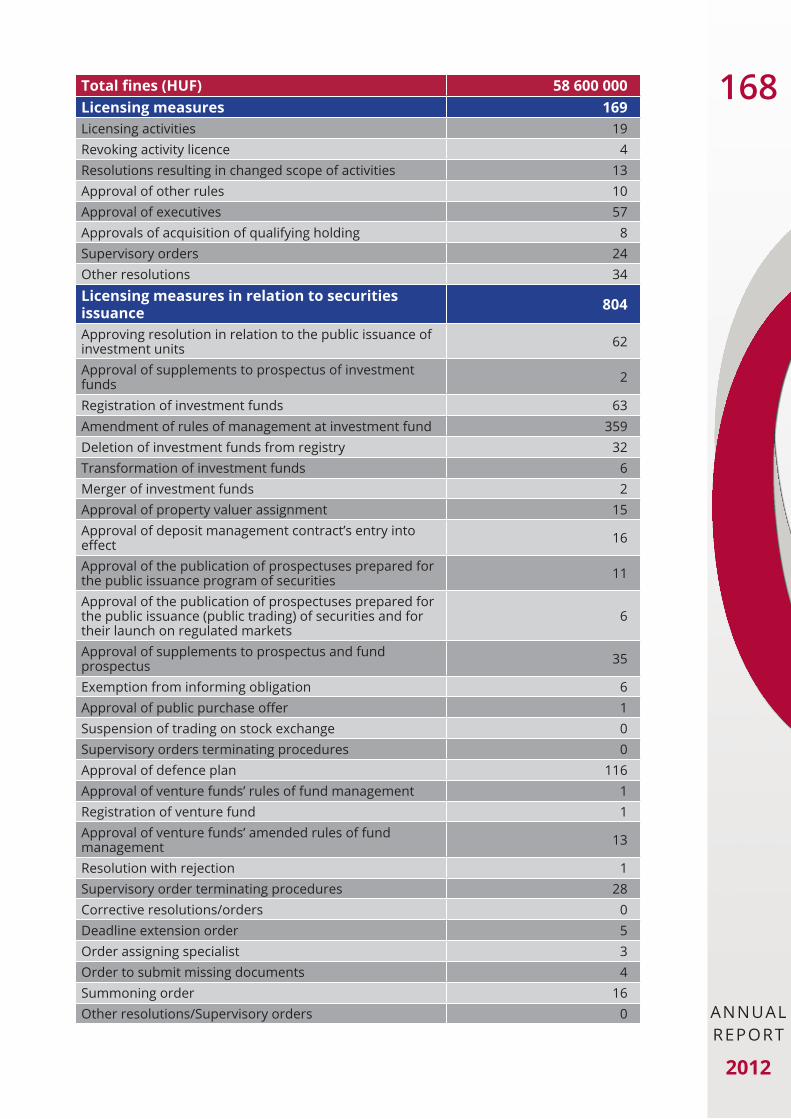

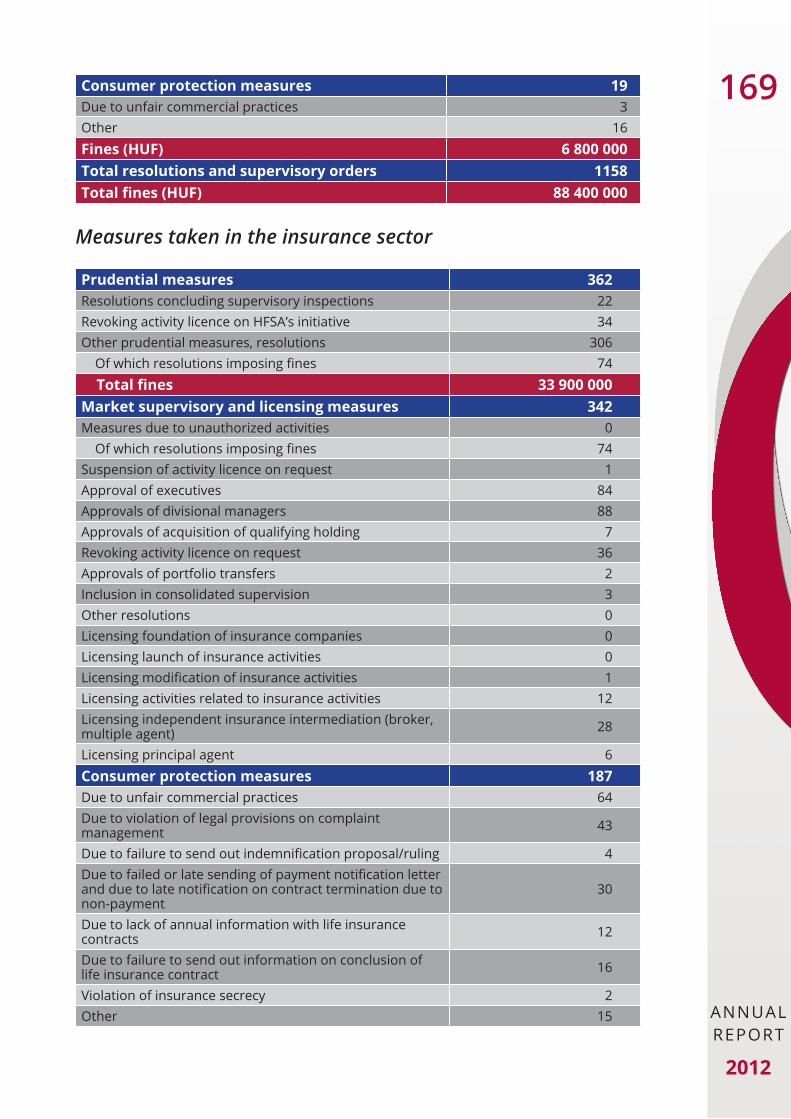

ATTACHMENTS ............................................................................................166

7

AnnuAL REPORT

2012

ThE hFSA’S MiSSiONThe Hungarian Financial Supervisory Authority is an autonomous regulatory organ responsible for the supervision, control and regulation of the financial intermediary system of Hungary. It is only subordinated to the power of law.

The fundamental mission of the Supervisory Authority is as follows:

to ensure, and when necessary, to enforce � the solid, transparent and efficient operation of the financial intermediary system, as well as the prudent activities of its constituent persons and organizations,

to create � stable and orderly operating financial markets, as well as secure and competitive development frameworks, which are compliant with the laws of the European union, through its decrees and other regulatory proposals,

to identify � and efficiently prevent the risks jeopardizing the individual financial institutions and sectors, through its preventive measures, as well as to reduce or eliminate the already existing risks,

to protect the rights and interests of the customers � who use the services provided by financial institutions in a consistent and proactive manner, to establish a forum for consumer dispute-settlement, and to increase consumers’ financial awareness,

to strengthen public trust in the financial intermediary system � ,

with a view to facilitate European-level financial supervision, � as a member of the European System of Financial Supervisors, to represent Hungarian interests and to cooperate with the European and other supervisory authorities.

8

AnnuAL REPORT

2012

prESidENT’S FOrEwOrdThe President of the Hungarian Financial Supervisory Authority reports to Parliament on the HFSA’s activities annually. The 2012 Annual Report outlines the HFSA’s activities last year, the changes in organizational and operating conditions, the developments of the international supervisory environment, and summarizes the experiences learned during that year. The Annual Report, however, is not merely a report to Parliament; it is also intended to inform industry professionals, the wider public and financial organizations on how the HFSA carried out the duties assigned to it by law, how it performed and how it managed its assigned resources.

***

The economic crisis that began in 2008 is now taking new turns. Consolidated mostly with help from governments, the European banking system continues to rest on fragile foundations and the financial system seeks additional support, mainly in the Southern European countries. One lesson from the crisis is that a new approach and new tools are needed in supervision: First, greater attention must be paid to phenomena and innovations emerging in areas of the financial system outside the banking sector. Second, the interactions between banks and the real economy must also be scrutinized with a different approach. In addition, the capital level of the banking system must be raised and its liquidity must be improved so that it becomes more risk tolerant in bearing former burdens and resisting future shocks. Further, it became clear that the actual condition of the financial intermediation system is inseparable from its sovereign environment. The condition of the banking system is closely dependent upon the macroeconomic conditions that constitute its framework and vice versa: the operation of the banking system and its problems also impact the macroeconomic environment.

Today, the eradication of the lingering defects in the system requires more than just improving the capital position of banks. These capital raises and recapitalization steps must be carried out in a market conform manners, i.e. without spending taxpayer money. new solutions and mechanisms are needed that will either replace or reduce the burdens of any underlying government contribution during future crises while improving the efficiency of supervision. Action items coordinated at European union level can only be implemented successfully if deposit insurance and the crisis management efforts of institutions become, like a safety net, an integral part of harmonized European frameworks. These elements altogether constitute the banking union.

9

AnnuAL REPORT

2012

One new challenge for the European integration process is that the single supervisory mechanism will already be in place in 2014 (primarily in the Eurozone) while certain elements of the banking union (e.g. the European level resolution mechanism and the joint deposit insurance system) will not have been implemented. Although Hungary is not required to join the banking union but has the option to do so, it impacts us fundamentally as the Hungarian market is part of the European union’s single market. Further, a large number of financial institutions operating in Hungary are subsidiaries and branches of Western European or global financial service providers that are directly impacted by these changes and Hungarian financial institutions are also present in other Eu member states. However, institutions with no international background cannot stay out of the process, otherwise they may suffer regulatory or competition disadvantages.

The specific method of implementation calls for some major decisions on the part of the European union to which we must contribute in a manner that harmonizes with our national interests. While these are one-off decisions, their consequences will determine financial development for decades in Europe and Hungary. Thorough and careful preparations are required: the effects of any possible wrong decision are far too costly, not only in a material sense but also for society. Therefore, responsible, timely decisions must be taken, applying calm assessment and wisdom.

In line with international trends set by the G20, the European union is currently implementing a comprehensive financial regulatory reform, aiming to make the financial system more resistant and secure, and to deepen integration and thereby also improve the EU’s competitiveness in financial services. The new regulation philosophy calls for a new approach and contemporary regulatory tools. In more and more areas, minimum harmonization is replaced with full or maximum harmonization. To this end, directives are gradually replaced by regulations that are directly effective in the entire EU, and by regulatory and implementing technical standards. This revaluates Hungary’s participation in the preparatory efforts directed by the European supervisory authorities, as this is where national considerations can be best enforced.

Thanks to the new approach, the European mapping and implementation of the Basel III international regulatory package (the prudential regulation of credit institutions and investment enterprises) is carried out via an Eu-level regulation (CRR) and directive (CDR IV) and will be supplemented with a series of technical standards (e.g. standardized and joint data reporting on capital: COREP). The final text of the CRD has been approved and member states will have very limited time for implementation. The intention of legislators is that the new prudential regulatory system will enter into effect on 1 January 2014. The CRR will be in effect directly in EU member states.

10

AnnuAL REPORT

2012

Thus there is no implementation obligation here either, but special attention must be paid to the implementation of both legal provisions.

The regulation to be introduced in the insurance sector will be similar to that in the banking system. The new regulations known as Solvency II also put the emphasis on the following items: more accurate measurement of risks; strengthening capital coverage; model-based calculation of capital requirement; assessment and approval of these by supervisory authorities; and strengthening disclosure requirements. However, insurers have several peculiarities, mostly because of the long time horizon typical to the life sector that presents quite a challenge to institutions regarding investments. Bringing assets and liabilities into harmony requires careful and diligent, i.e. prudent behaviour on the part of insurers. However, this is not always simple in an era of low interest rates and investments with poor profitability, and spurs intensified risk assumption. While the low interest rate environment that took shape in recent years brings great help for debtors by reducing repayment interest rates, the same phenomenon poses several challenges to insurance companies because it is difficult to achieve promised returns in such circumstances.

Concerning the capital market, the European capital market infrastructure and short selling are regulated in regulations already (and in technical standards), but regulations are under preparation on reducing market fraud and selling capital market assets. Sometimes these efforts are accompanied by the review of supporting directives.

***

Since early April 2000 (pursuant to an act passed under the first Orbán government), the HFSA has been an integrated supervisory authority. Thus it is supervising all sectors (banking, insurance, capital markets, funds) simultaneously and in a standardized manner in an economic environment characterized by specialization, diversity of complexity and a closely interlocking and complementary array of competing financial products and financial institutions. The relations of owners, the opportunity to transfer risks between institutions and sectors, short transactions times enabled by technological development and the management of all these factors from the regulatory side all suggest that the financial system can only be kept under control efficiently in integrated form along standardized supervision rules. Prudential supervision, consumer protection inspections and capital market inspections are means that are built on each other and complement each other. All are necessary if we seek to paint a true picture of risks present in the sector. Therefore, effective supervision today is only possible with full utilization of these synergies.

11

AnnuAL REPORT

2012

Risk-taking is an attribute of the financial sector’s operation, but it must be kept within reasonable limits. Thus one key task of the HFSA is to monitor developments in the financial sector and to intervene before risks become hazards to stability and confidence. Licensing, continual supervision and consumer protection all have a risk management and risk mitigation role. The prudential supervision of institutions can only be efficient if it is risk-based. However, risk-based supervision cannot be effective if it lacks the means of early intervention, i.e. if the supervisory authority can act only after a negative-impact event occurs instead of taking measures before, or as, the threat emerges (i.e. in due time). Therefore, the HFSA consistently represents the opinion that supervisory toolsets must be extended also to enable prevention.

With the introduction of risk-based supervision, the HFSA’s supervisory methodology was renewed. In addition to risk-based supervision gaining ground, the crisis also highlighted the indispensability of comprehensive on-site inspections. One significant accomplishment of 2012 was that the first three-year cycle was completed, during which the HFSA carried out the comprehensive, on-site inspection of all banks, specialized credit institutions, financial groups and joint stock insurance corporations. At institutions representing the greatest significance from a systemic risk viewpoint, the HFSA performed on-site inspections more frequently than required by law, paying special attention to its home supervisor status where applicable.

In additional to prudential considerations, the HFSA is also committed to financial consumer protection, as we believe that prudential and consumer protection considerations can only be interpreted [in conjunction and] in harmony with each other. The prudential position of financial institutions must be built on consumer confidence, and vice versa: consumer confidence requires a strong system of financial institutions. The equation works both ways: one cannot build a strong financial institution by deceiving consumers, and such deception may lead to the erosion of trust in the entire intermediary system.

Financial consumer protection and supervisory actions that support it are becoming stronger and stronger worldwide and also in Hungary. The HFSA handles almost ten thousand consumer claims annually, and launches targeted and thematic inspections at its own initiative at financial organizations to reveal and correct high-risk practices that impact a wide range of consumers. In 2012, the HFSA had institutions pay back more than HuF 5.3 billion in incorrectly collected revenues to mandatory pension fund members and customers of banks. While the HFSA’s consumer protection activities aiming to resolve systemic consumer-related problems represent a significant step forward, they are not always suitable to resolve unique consumer complaints.

12

AnnuAL REPORT

2012

Therefore, the transformation of financial arbitration in Hungary on the HFSA’s initiative constituted outstanding progress regarding the resolution of unique financial disputes. Effective July 2011, the Financial Arbitration Board (FAB) began operations as a professionally independent body within the HFSA organization. The FAB makes decisions quickly, effectively and free of charge concerning disputes arising from contracts made between consumers and financial service providers.

The establishment and operation of a financial consulting network of national coverage with professional and financial support from the HFSA is a significant accomplishment in serving financial consumers. The HFSA’s goal in setting up the consulting network was to take independent and proficient financial consumer informing services beyond the Budapest-based HFSA customer service, and to make sure that professional consultation offices that meet HFSA expectations are in place in each region.

In the HFSA’s opinion, publicity is the best and strongest tool in expanding the coverage of consumer protection. The media is the most effective way of calling the attention of consumers to the accomplishments of consumer protection activities, identified risks, potential market anomalies and players that pursue unfair practices.

The issue of foreign currency-denominated lending impacts a significant section of Hungarian society. Under the final mortgage repayment option closed at the end of February 2012, 170,000 foreign currency loans were repaid in a total amount of HuF 1,354 billion. Debtors unable to opt in to final repayment had the option to convert their foreign exchange loans to forint loans at a preferential exchange rate between April and end August 2012. Another debt repayment facilitation step in 2012 was the extension of the exchange rate barrier program, also aimed to assist foreign currency loan debtors. Debtors choosing to opt in the program are freed from currency exchange rate fluctuation risks for years; by the end of 2012, more than 110,000 pool accounts were opened by foreign currency loan holders participating in the program.

Receivables management is another problem that impacts a wide range of consumers. using the tools available to it, the HFSA took steps, issued a recommendation and proposed new regulation. The regulatory proposal was prepared by March 2012 and defined the concepts of debt purchasing and receivables management as business activities. The proposal initiated that the market entry and operation of receivables management firms should be made subject to a licence and stricter operating requirements and recommended strict rules of conduct to receivables management firms in order to eliminate misdemeanours.

13

AnnuAL REPORT

2012

Mandatory pension fund members could report their intention to return to the social security pension system by 31 March 2012: accordingly, a total of 25,305 mandatory pension fund members returned to the state pension system, with their mandatory pension fund membership terminated on 31 May 2012. At the end of the year, the aggregate membership in the mandatory pension fund sector was slightly below 100.000.

***

The HFSA’s role is to provide for the continual and stable operation of the Hungarian financial system also amidst the financial crisis, thereby contributing to the public good. The HFSA has entirely fulfilled this role: while financial turbulence and crises evolved in a number of EU member states, in Hungary there was no need to spend public funds on stabilizing the financial sector. Owing to timely measures taken by the HFSA, the parent institutions made available sufficient capital to their daughter companies. Where the HFSA deemed that there was no realistic opportunity to restore capital position either by internal capital accumulation or by an equity raise, it exercised its right to revoke the institution’s operating licence. In the case of the Soltvadkert és Vidéke Savings Cooperative, the insolvency of the financial institution was a realistic threat, thus the only adequate tool remaining at the HFSA’s disposal to settle the situation was to revoke the cooperative’s operating licence.

The continuing crisis severely impacted Hungarian banks, insurance companies and the Hungarian capital market alike. Sector participants are still struggling with these impacts and the HFSA has had to face the negative consequence of the lengthy crisis for several years. At the same time, owing to regular and thorough supervisory efforts, the Hungarian financial intermediary system has withstood the storm unleashed by the crisis, demonstrating an extraordinary resistance to shocks. A key element of this resistance is the capital adequacy of banks, which the HFSA examines on an ongoing basis.

The HFSA operates with a view to the tasks and objectives set out in its mission statement. Significant progress and development was achieved in each area last year and the HFSA was able to accomplish targets along strategic objectives in a swiftly changing environment full of challenges. Existing supervisory values, accomplishments in supervision, accumulated supervisory knowledge and experience, together with the organic relations between professional areas and the embedding of the HFSA into the European supervision system all constitute a solid basis for optimism regarding serious future challenges to the financial system.

May 2013, Budapest

Dr. Károly SzászPresident

14

AnnuAL REPORT

2012

ACrONyMSACI (Hpt.) � – Act CXII of 1996 on Credit Institutions and Financial

Enterprises

ACM (Tpt.) � – Act CXX of 2001 on the Capital Market

ACP � – Autorité de contrôle prudentiel (Prudential Supervisory Authority, France)

AIMFD � – Alternative Investment Fund Managers Directive

AFPSSS (Tvt.) � – Act XXIII of 2003 on Finality in payment and securities settlement systems

AIFCD (Bszt.) � – Act CXXXVIII of 2007 on Investment Firms and Commodity Dealers, and on the Regulations Governing their Activities

AIFMC (Batv.) � – Act CXCIII of 2011 on investment fund managers and collective investment forms on 1 January 2011

APR � – Annual percentage rate

ASC � – Advisory Scientific Committee (ESRB)

ATC � – Advisory Technical Committee (ESRB)

BaFin � – Bundesanstalt für Finanzdienstleistungsaufsicht (Federal Supervision of Financial Services, Germany)

BIS � – Bank for International Settlements

BSE (BÉT) � – Budapest Stock Exchange

BUBOR � – Budapest Interbank Forint Credit Interest Rate

CAR (TMM) � – Capital Adequacy Ratio

CCP � – Central Counterparty

CDS � – Credit Default Swap

CIRC � – China Insurance Regulatory Commission

COREP � – Common Reporting (tables for reporting on capital adequacy)

CRD � – Capital Requirements Directives (European directives 2006/48/EC and 2006/49/EC on the capital requirements of credit institutions and investment enterprises)

CRR � – Capital Requirements Regulation (draft regulation on prudential capital requirements of credit institutions and investment enterprises)

15

AnnuAL REPORT

2012

EBA � – European Banking Authority

ECB � – European Central Bank

Ecofin � – Council of Economic and Finance Ministers of the Eu

EIOPA � – European Insurance and Occupational Pensions Authority

EMIR � – European Market Infrastructure Regulation (regulation on trading repositories)

ERA � – HFSA’s electronic system for receiving authenticated data

ESA � – European Supervisory Authority

ESFS � – European System of Financial Supervisors

ESMA � – European Securities and Markets Authority

ESRB � – European Systemic Risk Board

FAB (PBT) � – Financial Arbitration Board

FIN-NET � – A financial dispute resolution network of national out-of-court complaint schemes in the European Economic Area countries

FINREP � – Financial Reporting (general financial data reporting to the supervisory authority)

FMA � – Österreichische Finanzmarktaufsicht (Financial Market Authority of Austria)

FMC (FEUVE) � – Financial management control

FSB (PST) � – Financial Stability Board

FSI � – Financial Stability Institute

HAS � – Hungarian Accounting Standards

HBA � – First Domestic Voluntary Deposit Insurance and Institution Protection Fund of Credit Institutions

HFSA (PSZÁF) � – Hungarian Financial Supervisory Authority

HFSA Act (Psztv.) � – Act CLVIII on the Hungarian Financial Supervisory Authority

IAIS � – International Association of Insurance Supervisors

ICAAP � – Internal Capital Adequacy Assessment Process

ICP � – Insurance Core Principles

IFRS � – International Financial Reporting Standards

16

AnnuAL REPORT

2012

IIF � – Institute of International Finance

IMF � – International Monetary Fund

Insurance Act (Bit.) � – Act LX of 2003 on Insurance Institutions and the Insurance Business

IOPS � – International Organisation of Pension Supervisors

IOSCO � – International Organization of Securities Commissions

KEF � – Public Procurement and Supply Directorate General

KELER � – Central Counterparty and Depository of Hungary Co. Ltd.

KHR � – Centralized Credit Information System

KIID � – Key Investor Information Document

KOMÓD � – The HFSA’s risk-based supervision methodology

MABISZ � – Association of Hungarian Insurance Companies

MANBESZ � – Association of Hungarian Non-profit Insurance Unions

MfNE (NGM) � – Ministry for national Economy

MiFID � – Markets in Financial Instruments Directive, 2004/39/EC

MNB � – Magyar nemzeti Bank (national Bank of Hungary)

MTF � – Multilateral Trading Facility

MTPL (Kgfb) � – Motor third-party liability insurance

NSAs � – national Supervisory Authorities

OECD � – Organisation for Economic Co-operation and Development

OTIVA � – national Fund for Safeguarding Savings Cooperatives

PD � – Prospectus Directive (on the prospectus to be published when securities are offered to the public or admitted to trading) 2003/71/EC

PKN � – Central Registry of Pension, Healthcare and Voluntary Mutual Funds

PP Act (Mpt.) � – Act LXXXII of 1997 on Private Pensions and Private Pension Funds

PSA (NYESZ) � – Pension savings account

REPIVA � – Institution Protection Fund of Regional Financial Institutions

ROO (SZMSZ) � – Rules of Organization and Operation

17

AnnuAL REPORT

2012

RTS � – Regulatory Technical Standard

SAO (ÁSZ) � – State Audit Office

SEPA � – Single Euro Payments Area

SREP � – Supervisory Review and Evaluation Process

SSM � – Single Supervisory Mechanism

T2S � – (real time gross securities settlement system)

TAKIVA � – Institution Protection Fund for Savings Cooperatives

UCITS � – undertakings for Collective Investments in Transferable Securities

UL � – unit-linked (unit-linked life insurance)

XETRA � – Exchange Electronic Trading (electronic securities trading platform)

18

AnnuAL REPORT

2012

ThE hFSA’S STATuS ANd OpErATiNg ENvirONMENT

’One strategic objective of the HFSA is the improvement of its efficiency, performing its tasks as an independent, strong and integrated supervisory authority.’1

Main changes in the hFSA Act, expanded decree-issuing rightsParagraph (1) in Article 23 of the Fundamental Law of Hungary authorized Parliament to establish, in cardinal Acts, independent regulatory organs for fulfilling specific tasks and mandates of the executive power. Accordingly, pursuant to Article 1 of Act CLVIII of 2010 on the Hungarian Financial Supervisory Authority (HFSA Act), the Hungarian Financial Supervisory Authority (HFSA) is the autonomous regulatory organ responsible for the supervision, control and regulation of the financial intermediary system of Hungary. It is only subordinated to the power of law.

Pursuant to Paragraph (2) in Article 23 of the Fundamental Law, the leaders of independent organs are appointed by the Prime Minister or, on the Prime Minister’s proposal, by the President of the Republic for a period specified in a cardinal Act. The leader of an autonomous regulatory organ shall appoint one or more deputies. In accordance with Paragraph (2) in Article 23 of the Fundamental Act, the President of the HFSA shall report to Parliament on the HFSA’s activities on an annual basis.

Rules pertaining to the HFSA’s legislatory mandate are specified in Article T) and Paragraph (4) in Article 23 of the Fundamental Law. Pursuant to Article T) of the Fundamental Law, legislation includes Acts of Parliament, government decrees, orders by the Governor of the national Bank of Hungary, orders by the Prime Minister, ministerial decrees, orders by autonomous regulatory bodies and local governments.

Pursuant to Paragraph (4) in Article 23 of the Fundamental Law and acting within his competence specified in a cardinal Act, the President of the HFSA shall issue decrees by statutory authorisation, which may not conflict with any Act, government decree, any decree of the Prime Minister, ministerial decree or with any order of the Governor of the national Bank of Hungary. Decree designated deputies of the President of the HFSA may issue decrees on behalf of the President.1 Mottos are taken from the document, “Strategy of the Hungarian Financial Supervisory Authority”.

19

AnnuAL REPORT

2012

Changes to the regulatory environment

Effective 28 October 2012, Act CLI of 2012 on amending certain financial laws assigned to the president of the HFSA three new rights to issue decrees:

Definition of detailed rules for reports related to severe IT system 1. problems occurring during data reporting;

Creating detailed rules for setting, collecting, managing, recording and 2. refunding the administrative services fee in the case of financial, capital and insurance market organizations, voluntary mutual funds, private pension funds and occupational pension service providers in respect of procedures within the HFSA’s purview:

licensing foundation or establishment; �

licensing mergers and separations; �

registration; �

issuing operating licences; �

reporting cross-border activities; �

establishing a branch; �

approving or amending rules; �

licensing qualifying participation; �

licensing or registration necessary for using an independent or tied �intermediary.

For setting detailed rules regarding the content, form and submission 3. of licensing and reporting forms and electronic templates to be used pursuant to Paragraph (3) of Article 50 of the HFSA Act.

Economic environment

The economic crisis that began in 2008 severely impacted the Hungarian capital market and the country’s banks and insurance companies. Financial sector participants are still struggling with its effects, and the HFSA will be dealing with the negative fall out of the prolonged crisis for years to come. As markets stagnate or shrink owing to declining demand, the risk appetite of institutions decreases, as does turnover and the size of managed portfolios. The HFSA’s operation is funded from fees paid by supervised institutions, with the major part based on capital requirements that relate to assumed risks, while the lesser part reflects managed assets and turnover. Therefore, in addition to posing prudential, market supervision and consumer protection

20

AnnuAL REPORT

2012

risks, the crisis has also caused the HFSA’s fee revenues to fall year by year, precisely at the moment when its responsibilities and international financial obligations expanded.

These circumstances fundamentally changed the economic environment of the HFSA’s operations, presenting new challenges to the entire organization. The HFSA is not publically funded in any form at all; supervisory fees paid by industry participants are its sole source of revenue. In 2012, the HFSA’s revenues were 7.6% lower nominally than in the previous year. The biggest fee decline was suffered at the funds sector, where revenues fell by 59% from the 2011 level. Supervisory fee revenues in the capital markets sector were 11.5% lower in 2012 than in 2011. The insurance sector has also been shrinking for years, with supervisory fee revenues from this sector down by 5.3% in 2012. The largest fee revenue generator is the financial market sector, but even that sector failed to grow, with supervisory fee revenues in 2012 down 1.8% on 2011.

The effects of the crisis are lingering, which might generate an increasing number of problems in supervised sectors and may yet bring new issues to the surface. The HFSA must tackle all this with a shrinking budget, and in order to manage future challenges effectively must apply the most efficient supervisory methodology in all of its work.

21

AnnuAL REPORT

2012

riSK-BASEd SupErviSiON, iMpACT rATiNg ANd SupErviSiON METhOdOLOgy

‘The HFSA’s objective is to develop and apply risk-based methodologies that regulate the operation of financial markets and render a high degree of flexibility, quick response capability and an adequate toolset for exercising supervision.’

Pursuant to Article 38 of the HFSA Act, the HFSA exercises ongoing supervision over organisations and persons subject to the laws specific to the financial sector. Licensing, institution supervision (prudential), consumer protection and market supervision procedures are all part of this. Ongoing supervision encompasses on-site inspections along with the verification and analysis of data derived from regular and ad-hoc provision, documents submitted to the HFSA and officially available information.

In line with European practice, the HFSA strives to utilize available resources with a view to the risk level represented by individual institutions. For many years the HFSA has followed a risk-based supervision methodology (KOMÓD) when supervising institutions. In this approach, optimum supervisory effectiveness is sought by efficiently distributing resources based on the actual legality and prudential supervision tasks.

Risk-based supervision aligns the supervision process to actual risks. In the real-life application of risk-based supervision, the supervisory resources assigned by the HFSA to the supervision of each institution or phenomenon that conveys observed and detected financial market risks are proportionate to their impact on the financial system. Proportionate supervision also means that the HFSA employs different tools for supervising institutions that may threaten the financial system in different ways. This differentiation equally entails the applied supervision methodologies and the depth, scope and intensity of supervision.

22

AnnuAL REPORT

2012

impact rating and institution assessment

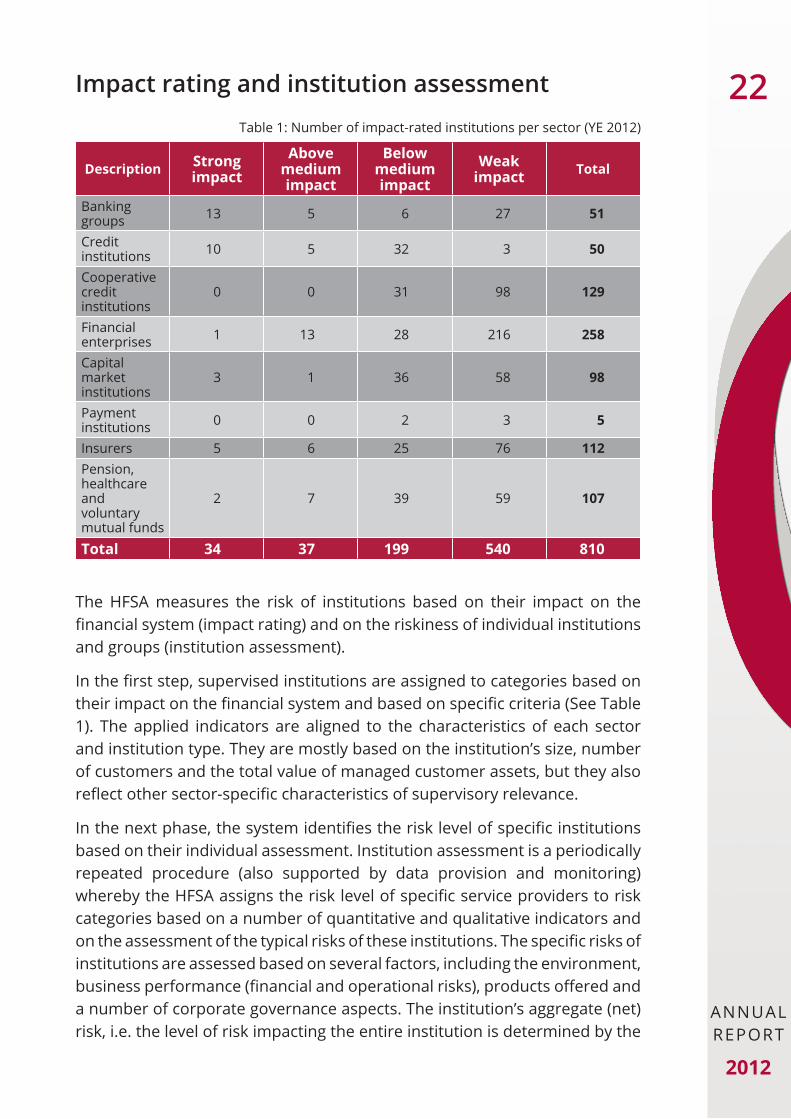

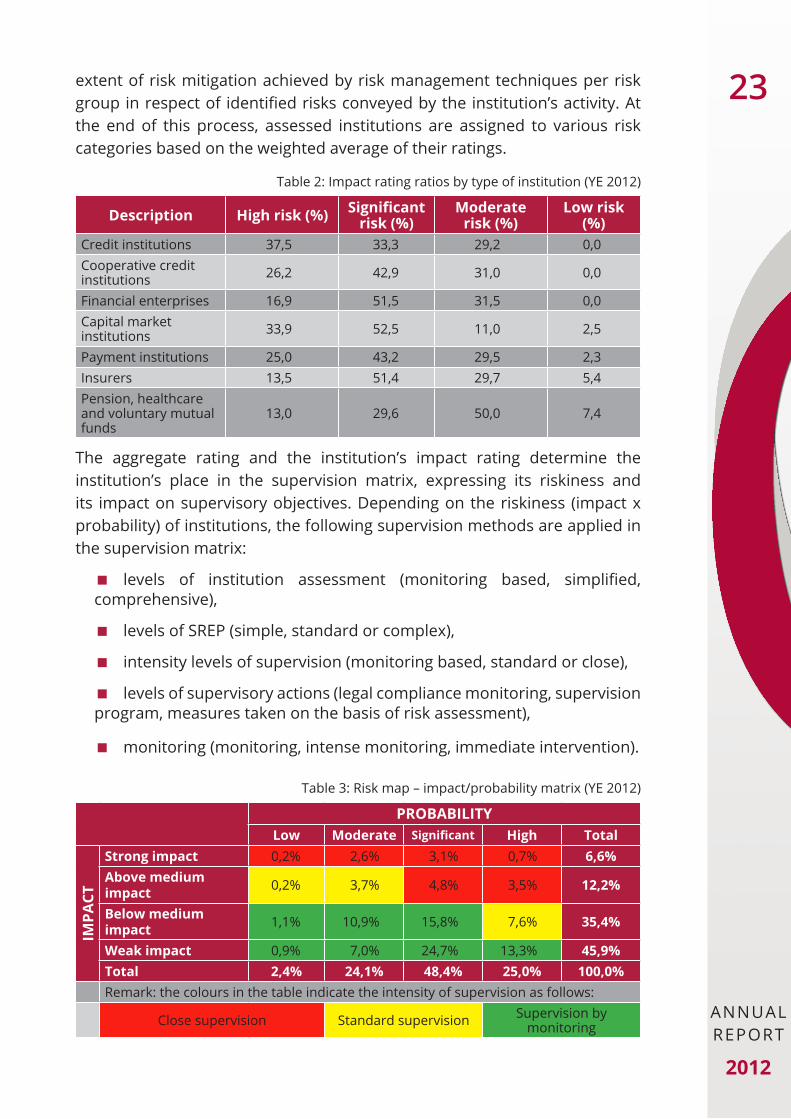

Table 1: number of impact-rated institutions per sector (YE 2012)

Description Strong impact

Above medium impact

Below medium impact

Weak impact Total

Banking groups 13 5 6 27 51

Credit institutions 10 5 32 3 50

Cooperative credit institutions

0 0 31 98 129

Financial enterprises 1 13 28 216 258

Capital market institutions

3 1 36 58 98

Payment institutions 0 0 2 3 5

Insurers 5 6 25 76 112Pension, healthcare and voluntary mutual funds

2 7 39 59 107

Total 34 37 199 540 810

The HFSA measures the risk of institutions based on their impact on the financial system (impact rating) and on the riskiness of individual institutions and groups (institution assessment).

In the first step, supervised institutions are assigned to categories based on their impact on the financial system and based on specific criteria (See Table 1). The applied indicators are aligned to the characteristics of each sector and institution type. They are mostly based on the institution’s size, number of customers and the total value of managed customer assets, but they also reflect other sector-specific characteristics of supervisory relevance.

In the next phase, the system identifies the risk level of specific institutions based on their individual assessment. Institution assessment is a periodically repeated procedure (also supported by data provision and monitoring) whereby the HFSA assigns the risk level of specific service providers to risk categories based on a number of quantitative and qualitative indicators and on the assessment of the typical risks of these institutions. The specific risks of institutions are assessed based on several factors, including the environment, business performance (financial and operational risks), products offered and a number of corporate governance aspects. The institution’s aggregate (net) risk, i.e. the level of risk impacting the entire institution is determined by the

23

AnnuAL REPORT

2012

extent of risk mitigation achieved by risk management techniques per risk group in respect of identified risks conveyed by the institution’s activity. At the end of this process, assessed institutions are assigned to various risk categories based on the weighted average of their ratings.

Table 2: Impact rating ratios by type of institution (YE 2012)

Description High risk (%) Significant risk (%)

Moderate risk (%)

Low risk (%)

Credit institutions 37,5 33,3 29,2 0,0Cooperative credit institutions 26,2 42,9 31,0 0,0

Financial enterprises 16,9 51,5 31,5 0,0Capital market institutions 33,9 52,5 11,0 2,5

Payment institutions 25,0 43,2 29,5 2,3Insurers 13,5 51,4 29,7 5,4Pension, healthcare and voluntary mutual funds

13,0 29,6 50,0 7,4

The aggregate rating and the institution’s impact rating determine the institution’s place in the supervision matrix, expressing its riskiness and its impact on supervisory objectives. Depending on the riskiness (impact x probability) of institutions, the following supervision methods are applied in the supervision matrix:

levels of institution assessment (monitoring based, simplified, �comprehensive),

levels of SREP (simple, standard or complex), �

intensity levels of supervision (monitoring based, standard or close), �

levels of supervisory actions (legal compliance monitoring, supervision �program, measures taken on the basis of risk assessment),

monitoring (monitoring, intense monitoring, immediate intervention) � .

Table 3: Risk map – impact/probability matrix (YE 2012)

PROBABILITYLow Moderate Significant High Total

IMPA

CT

Strong impact 0,2% 2,6% 3,1% 0,7% 6,6%Above medium impact 0,2% 3,7% 4,8% 3,5% 12,2%

Below medium impact 1,1% 10,9% 15,8% 7,6% 35,4%

Weak impact 0,9% 7,0% 24,7% 13,3% 45,9%Total 2,4% 24,1% 48,4% 25,0% 100,0%Remark: the colours in the table indicate the intensity of supervision as follows:

Close supervision Standard supervision Supervision by monitoring

24

AnnuAL REPORT

2012

The figures of the supervision matrix show the ratio of all supervised institutions in all supervised sectors belonging to close, standard or monitoring-based supervision. Based on their position in the matrix, institutions can be supervised individually or jointly.

Individually supervised institutionsInstitutions qualifying as strong-impact entities owing to their size, activity, role in sustaining financial system stability or impact on consumers are monitored by the HFSA by way of individual supervision (whereby the risks of a specific institution or group of institutions are assessed individually). Here the HFSA assigns a supervisor to the institution or group who is responsible for identifying and managing the risks of these entities.

Depending on the institution’s risk and impact rating, the intensity of individual institution supervision can be standard or close.

Standard supervision complements monitoring activities with the findings of comprehensive inspections, also involves the collection of other information about the institution and the quarterly review of simplified institution assessment tables. Standard supervision is typically applied for institutions with above average impact.

In terms of intensity, close supervision exceeds standard supervision as it also involves permanent contact keeping and the ongoing updating of the detailed institution assessment table. Close monitoring is mostly applied to strong-impact institutions. In other cases, it may be necessary owing to the risk rating of the institution.

Jointly supervised institutions The jointly supervised category includes a large number of institutions with low individual impact on the entire financial system. In respect of these institutions, the HFSA’s task is to ensure that no significant risks to the proper operation of the financial system risks can appear and accumulate in this market segment.

In the course of joint supervision, risks are screened on the basis of the combined examination institution groups with similar characteristics and risks. The primary objective of this exercise is to identify, measure and mitigate the common risks of the group. While risk-mitigating measures are set for individual institutions, their impact is aggregated through the reduced risk levels of institutions. Second, if the HFSA detects risks or exposures at several institutions but believes it may be important to manage them at the individual institution level, it publishes supervisory requirements in a recommendation or CEO letter.

25

AnnuAL REPORT

2012

revision of methodologies

On-site inspection manualsInspection manuals collect, per main risk type, information and considerations that are fundamental for the comprehensive on-site inspection of institutions and groups belonging to a specific sector. Another purpose of these manuals is to aid standardization of supervisory inspection.

In 2012, inspection manuals compliant with current legal provisions were drafted for the on-site inspection of insurance companies, investment fund managers and healthcare, pension and voluntary mutual funds. Further, a review was performed on the inspection manuals prepared in 2011 for cooperative credit institutions, investment enterprises, banks and banking groups and for the performance of the public law tasks assigned by law to the Association of Hungarian Insurance Companies (MABISZ). upon the reviews, changes were made to the manuals based on real-life experiences with the inspection methods and work sheets set forth therein, and with a view to amended Eu and domestic laws and data reporting requirements.

iCAAp-SrEp manuals

2012 also saw the review of the internal capital adequacy assessment manuals of institutions (e.g. banks, specialised credit institutions, credit cooperatives, investment enterprises) subject to the European Capital Requirements Directive (CRD). The review covered the methodology guides to the capital requirement calculations of institutions (Internal Capital Adequacy Assessment = ICAAP) and to the related supervisory review process (SREP), encompassing the modification thereof. In the course of the review, the methodology guides were supplemented with new Eu principles and guidelines that both the supervised institutions and the HFSA had to implement. The ICAAP and SREP methodologies are also published on the HFSA website.

As a new element in the SREP methodology in 2012, the HFSA prepared an assessment methodology for institution protection systems. The assessments place institutions in strong, medium or weak protection capability categories. Recent experiences highlight the importance of institution protection systems in the credit institution sector. Today several institution protection systems are present in the sector (OTIVA, TAKIVA, REPIVA, HBA), however, their size, available safety reserves, by-laws, etc. all differ. These integration organizations have an expanding role in preventing members from sliding into a crisis or near-crisis situation and in helping the management of such situations once they occur. In the SREP exercise, the HFSA checks the institution’s membership in an integration organization and assesses the

26

AnnuAL REPORT

2012

protective capability of the institution protection system. The HFSA is entitled to set various additional capital requirements at member institutions for specific protective capability categories upon the SREP.

KEy TArgET ArEAS OF SupErviSiON iN 2012 Pursuant to point e) in Article 21 of the HFSA Act, the HFSA president specifies the key target areas of supervisory inspections every six months. When setting the target areas, the experiences of on-site and off-site inspections must be a starting point, and consideration must be given to HFSA strategy; to the risks identified in the semi-annual HFSA risk and financial consumer protection risk reports; to the topics raised at Financial Stability Board sessions; and the work plans of Eu supervisory authorities (EBA, ESMA, EIOPA). Key inspection target areas are identified on the basis of supervisory knowledge and information available at a specific point in time. However, emphases may be shifted in the light of subsequent events and developments.

In the reporting period, key inspection target areas serve as points of reference for:

comprehensive, target and thematic inspections, �

the elaboration of methodologies, �

analyses and the elaboration of amendments to legal provisions, HFSA �recommendations and decrees, and

how to improve HFSA staff knowledge of specific topics. �

The key target areas of inspection set for the first six months of 2012 were reviewed at mid-year. After careful evaluation, the president of the HFSA mostly designated the same risks and threats as key areas for the second half of the year.

Key target areas of supervision in 2012

MOnEY MARKET SECTOR

Capital1.

The lingering effects of the crisis have had a significant impact on the capital position of financial institutions. Therefore, owing to low internal capital accumulation rates caused by low profitability and the need for equity raises at certain institutions, the HFSA has been paying special

27

AnnuAL REPORT

2012

attention to the capital position of institutions and the quality of capital elements. The purpose of this special treatment at institution, group and sector level is to identify operational risks that relate to capital position i.e. to detect unfavourable trends in a timely manner, and to deal with them swiftly and correctly. The HFSA’s approach and response in this area made a significant contribution to the solid capital adequacy of Hungarian institutions, which is considered secure even in international comparison.

Liquidity2.

The experiences gained during the crisis highlighted the key importance of liquidity. Recognizing this, deposit and balance sheet coverage indicators were launched at the HFSA’s initiative from the middle of January 2012.

Adequate liquidity is a priority also at Eu level. Adherence to the Basel III regime is tighter now and new mandatory liquidity indicators will be introduced: the liquidity coverage ratio (LCR) effective 1 January 2015, and the net stable funding ratio effective 1 January 2018 (NFSR). In this respect, Hungarian legislation is ahead of European, as the HFSA already required financial institutions operating in Hungary to apply the new indicators.

Credit risk3.

The crisis also had a significant impact on credit institution customers. Credit portfolios deteriorated significantly in recent years, thus the HFSA paid special attention to credit risk trends, focusing on restructured receivables and work-out activities during inspections. The prudential management of credit risk, in particular the adequacy of provisioning in the light of deteriorating portfolios, growing non-performing loan ratios and the related capital requirement of credit risk was scrutinized during both comprehensive inspections and regular (annual) SREP reviews.

The management of credit risk was also a focus item for consumer protection. In H1 2012, the HFSA scrutinized the compliance of final repayment plans offered by credit institutions for retail foreign exchange-based mortgages. Further, through 2012, the HFSA closely inspected the forced collection and receivables management activities of financial enterprises, their compliance with the requirements for transparent pricing set out in the ACI and with the statutory APR cap, and the practices of institutions regarding the new KHR inventory system.

Business strategy4.

Recent changes in the international, Eu and domestic economic environment had a significant impact on Hungarian credit institutions. Owners revised existing medium and long-term business strategies and were compelled to specify the changes to the HFSA. This re-drafting of former business models

28

AnnuAL REPORT

2012

can be regarded as one of the responses of financial market participants to the crisis. Thus the HFSA must know these responses in detail as they may convey risks.

Supervisory inspections and prudential meetings held with the senior managers of supervised institutions indicated significant strategy uncertainties; credit institutions did, or will, reshape and rethink their approach. Therefore, the HFSA monitored changes to credit institution strategies in 2012, via on-site and off-site supervision.

Payments5.

In February 2012, frequent hacker attacks and frauds, and the bankruptcy of Malév Hungarian Airlines called for consumer protection inspections of service provider conduct concerning banking cards. In addition, customer informing prior to payment service contract signing also became an inspection focus. Further, compliance with the new four-hour limit for electronic transfers that entered into effect on 2 July 2012 was also subjected to intensified supervisory scrutiny.

CAPITAL MARKET SECTOR

MiFID1. 2 compliance

Promoting compliance with the Eu Markets in Financial Instruments Directive (MiFID) was set as a key supervisory inspection area for 2012. The HFSA closely examined the standardized application and control of MiFID regulations and MiFID-related recommendations.

Inspection of the operation of key institutions2.

In order to provide for the uninterrupted operation of the capital market and to sustain and strengthen trust, the HFSA paid particular attention to strategic issues pertaining to the operation of the BSE and the KELER group in 2012. As part of this approach, the HFSA closely cooperated with partner authorities, partner supervisory authorities and performed in-depth analysis.

Application of the KIID3. 3 (Key Investor Information Documentum) in domestic practice

The KIID was elaborated by the European Securities and Markets Authority (ESMA) to help uCITS4 directive implementation. Its application in domestic practice, i.e. proper investor informing, received special supervisory attention from a consumer protection viewpoint.

2 Markets in Financial Instruments Directive (MiFID), encompassing the following topics: obligation to obtain preliminary information on customers; order fulfilment in the most favourable way for the customer; conflict of interest, incentives.3 KIID (Key Investor Information Document): A brief, standardized pre-contract information document used in Eu Member States.

29

AnnuAL REPORT

2012

Online sales channels for investment products and other retail 4. savings products

Mapping and inspecting online sales channels for investment products and other retail savings offerings was also a key target area of consumer protection inspections in 2012 as this area conveys special risks compared to traditional sales channels. The HFSA inspected advertising activities at the institutions concerned and sought to uncover potentially deceptive and aggressive commercial practices.

Inspection of issuance activities5.

Of the mandatory information elements that public issuers must provide customers with on a regular basis, the annual report is key (encompassing the audited financial statements, the auditor’s report, the management’s liability acceptance statement, and the presentation of the company’s business environment and future prospects). The HFSA’s objective is to ensure that the required reports are published in due time and that they comply with all content-related and accounting framework requirements. On multiple occasions, our inspections found issuers failed to publish their annual reports by the statutory deadline or with contents required by law. As part of its market supervision activities, the HFSA paid special attention to the compliance of extraordinary information provision.

InSuRAnCE SECTOR

Capital position and profitability1.

In the insurance sector, capital position and profitability were focus items for the HFSA in 2012. The main reason was the consistent erosion of profitability at insurance companies that may have an adverse impact on the institutions’ capital position through balance sheet earnings. Owing to rising capital and revenue risk levels at institutions, special attention was paid to these items during on-site and off-site inspections.

Motor third party liability (MTPL) insurance and the related 2. activities of MABISZ

Motor third party liability insurance offerings have been a key inspection target area for the HFSA for many years. MABISZ, the Association of Hungarian Insurance Companies, is an institution with a public role. However, its activities are not regulated properly in laws, thus the HFSA considers the supervision of MABISZ a priority. In 2012, the HFSA applied a new methodology for inspecting key areas such as the Indemnification Account, the Indemnification Fund and claim history management and maintenance. The methodology was developed for inspecting the MTPL-related activities of MABISZ and is a new prudential approach tool.

30

AnnuAL REPORT

2012

Consumer protection inspections focused on payment notices sent out to customers and on cancellation notification practices. Additional focus items included the MTPL rate advertisements and problems in relation to change of insurance companies.

Unit-linked life insurance products, life insurance packaged with 3. loan products

The management of life insurance offerings linked to an investment unit (unit-linked products, uL), the analysis of the related investment policies and the investigation of life insurance packaged with loan products regarding the potential impact of final mortgage repayment were selected as key inspection target areas by the HFSA. The reason is that prior inspections found the investment policies of unit-linked asset funds to be cause for concern from a prudential and a consumer protection viewpoint.

Insurance branches4. 4

Insurance branches called for special attention owing to the size of the portfolios they manage in certain sectors and the significant role of certain insurance branches in specific sub-markets.

Accident tax5.

With a view to consumer protection considerations, the HFSA closely monitored the compliance of information provided to customers regarding the accident tax introduced effective 1 January 2012, its extent and levying, i.e. the HFSA examined if customers were informed appropriately and in due time about the new obligation, the amount payable and applicable conditions.

PEnSIOn, HEALTHCARE AnD VOLunTARY MuTuAL FunDS SECTOR

Use of technical and operational reserves1.

In the funds sector, on inspection focus for the HFSA in 2012 was the use of technical and operational reserves as part of liquidity management. Operating expenditures of funds could only be financed from operating revenues, and the latter are decreasing consistently owing to the changing market and regulatory environment.

Investment activities2.

The HFSA considered the inspection of funds sector investment activities a key priority in 2012, as the objective of funds is to make the highest possible service payments while they can only finance those from effective investment activities. A key focus of these inspections is to keep compliance with legal and prudential requirements under ongoing supervision.

4 An insurance company or reinsurer seated in another country that pursues activities in Hungary via a branch. The Hungarian branch of an insurer or reinsurer based in the EEC is supervised by the home country supervisory authority.

31

AnnuAL REPORT

2012

Balance and membership fee statements3.

As part of the comprehensive inspection of funds in 2012, the HFSA paid special attention to balance and membership fee statements in relation to services, the legal compliance of payments and the use of fund savings.

TARGET AREAS OVERARCHInG MuLTIPLE SECTORS – SERVICES TO PEOPLE WITH DISABILITIES

Through 2012, the HFSA considered it a key focus area to scrutinize the conduct of financial organizations when providing service to people with disabilities. The protection of the interests of people with disabilities is a basic responsibility of the HFSA assigned to it by the HFSA act. The verification of compliance with all legal provisions pertaining to consumer rights set out in financial sector laws and implementation decrees is part of this consumer protection mandate. The purpose here is to eliminate any potential disadvantages deriving from a person’s disabilities and to ensure equal treatment and equal opportunities. It is not sufficient to apply equal treatment when providing service to people with disabilities. Actual equal opportunities can only be ensured if additional services are also provided. An HFSA recommendation was issued on this topic in 2012, aiming to enforce the rights of people with disabilities in the widest possible context, encompassing a high level of access to services and the provision of additional services that actually ensure equal opportunity and to remove barriers as soon as possible in a targeted manner.

32

AnnuAL REPORT

2012

SupErviSiON OF iNSTiTuTiONS‘Strengthening the role of proactive, risk-based supervision; monitoring the risks, risk management and stress resistance of supervised institutions in addition to compliance are strategic objectives of the HFSA.’

The HFSA carries out continual supervision of organizations and persons subject to laws specific to the financial sector. As part of this continual supervision, the HFSA performs prudential supervision, market supervision, and employs the toolsets of consumer protection (off-site and on-site) to monitor the activities and processes of money and capital market institutions, pension, healthcare and voluntary mutual funds, insurers (financial organizations), and the so-called financial infrastructure institutions (regulated market, central counterparty, central repository). The purpose of continual supervision is to detect risks in a timely manner and to manage them appropriately.

In the case of off-site inspections, the means of continual supervision include the monitoring, processing and analysis of available information, ongoing contact keeping with the institution, harmonization and other communication related to applications and announcements. On-site supervision comprises the execution of inspections. Information obtained in the course of continual supervision is incorporated into risk assessment, and risk assessment and institution assessment provide feedback to continual supervision. All this determines the method and intensity of the institution’s treatment by the HFSA, along with the inspection schedule and the areas of focus of individual inspections.

In recent years, the HFSA’s method and practice of the supervision of institutions transformed markedly, involving the organizational separation of on-site and off-site supervision. Subsequent experiences and accomplishments proved organizational separation to be the right professional decision.

Further, methodology developments were carried out regarding both on-site and off-site supervision in recent years and changes were made to the organization of work. The purpose of these changes was to exploit additional benefits of transformation, to establish sound cooperation between the two areas, and to improve the efficiency of supervision.

When carrying out comprehensive on-site inspections at financial institutions in various sectors, the HFSA always examines the compliance of activities aimed at preventing terrorism financing and money laundering. Such examination is performed using sector-specific methodologies that are revised on an annual basis. In cases when immediate action is required, the HFSA launches

33

AnnuAL REPORT

2012

targeted inspections. When more than one sector or institution is involved, the HFSA initiates a thematic inspection.

Off-site supervision

The main objective of off-site supervision is to enable the HFSA to monitor on an ongoing basis the risks of supervised institutions and to take proactive action if needed to ensure their secure operation. This monitoring is based on data provision by institutions, prudential meetings with the managers of supervised institutions, expert meetings and other information.

In order to monitor the activities and risks of supervised institutions continually, a thorough analysis is drafted at regular intervals in which supervisory areas assess, in a defined framework, the individual sectors, activities and the typical key risks of strong-impact institutions along with the extent and trends of these risks, other related information, market news and information received from the sector.

Considering that in a quickly changing market environment, day-to-day monitoring and risk assessment based on data provision from supervised institutions is of increased importance, the HFSA pays special attention to the structure of supervisory reports, to updating their content and to the accuracy and quality of submitted data reports. In its consolidated supervision work, the HFSA made significant efforts to have supervised institutions convert to IFRS-compliant reporting instead of applying Hungarian accounting standards (HAS) when completing capital adequacy reporting (COREP) tables.

Harmonization with the representatives of new market entrants waiting licensing continues to be an integral part of off-site supervision, as are the various forms of contact with already operating institutions that are either strong-impact entities or convey risks of some sort. Regular and ad-hoc prudential meetings, discussions with top management, legal representatives and auditors also belong here. In addition to enabling the review of the current processes, risks, revenue and capital position of the financial institution concerned, prudential meetings also provide an opportunity to discuss current issues (e.g. the participation of banks and credit institutions in the home protection program).

An important and recurring element of the supervision of institutions is the assessment of rules, strategies, procedures and methodologies pertaining to the internal governance, risk management and capital adequacy of financial sector institutions. The purpose of this assessment is to decide whether the institution’s own funds provides sufficient coverage for the risks run and whether it enables the reliable management of these risks.

34

AnnuAL REPORT

2012

In the course of continual supervision, several questions were again raised in 2012 about the interpretation of legal provisions. These questions formed the basis of the HFSA’s proposed amendments to laws, recommendations, official rulings and methodology.

Supervisory duties are becoming increasingly international. Tasks deriving from Eu and other international cooperation are all part of this trend. They include supervision of institutions with a Hungarian parent company and international subsidiaries; supervision of subsidiaries subject to consolidated supervision by a foreign authority along Hungarian regulations; supervision of the Hungarian branch office of foreign institutions and that of cross-border activities; regular contact keeping with partner authorities as part of home-host supervisory cooperation and in line with applicable Eu regulation. Concerning the latter, personal meetings, information exchange and professional consultations take place in supervisory college sessions.5

Off-site supervision of money market institutions

In addition to monitoring continually the actual capital position of banking groups, the HFSA regularly analysed the changes of banking portfolios and profitability, and elements of strategy change by foreign owners. In 2012, so-called prudential meetings were held with the leaders of large banks on two occasions. Based on those meetings, the HFSA gained a comprehensive picture of the current position, measures and future expectations of banks.

In order to provide for an appropriate level of liquidity at banks in relation to the significant weakening of the forint, the HFSA scrutinized the liquidity position of banks on a daily basis. When risks were identified, the HFSA called the attention of the bank’s leaders to take action to sustain a secure liquidity position. With a few exceptions, all small and medium banks fulfilled the minimum requirement (65%) set for the FX Financing Adequacy Indicator (DMM) introduced on 1 July 2012. The HFSA took measures against institutions that failed to comply with the decree and required them to report data on a daily basis.

Monitoring of the usage of the “Home protection” package was also a key task in 2012, along with the impact analysis of measures such as the exchange rate barrier, the application of forced sales quotas for housing properties, etc. The HFSA analysed in detail the impact of final mortgage repayment on the capital, liquidity and profitability position of credit institutions, in particular that of banking groups.

5 Supervisory colleges of financial groups operating in multiple countries are institutions of cooperation between national supervisory authorities. Their purpose is to promote the efficient supervision of institutions operating in several countries.

35

AnnuAL REPORT

2012

In 2012, the HFSA paid special attention to strengthening the institution protection and integration cooperation that evolved among credit cooperatives. At the middle of the year, the HFSA published its non-binding requirements regarding institution protection systems, then evaluated institution protection funds. The results of this evaluation were published on the HFSA website then presented to all stakeholders at consultation sessions. Finally the HFSA began to enforce rating-based capital requirements on the member institutions of these funds.

The experiences gained through the inspection of credit cooperatives were shared by the HFSA at regular conferences for institutions and in professional circular emails. With these efforts, the HFSA’s objective was to prevent the formation of risks and to disseminate best practices.

Off-site supervision of pension, healthcare and voluntary mutual fundsOf the tasks carried out under the supervision of the funds sector in 2012, items that deserve special mention include the assessment of quarterly reports, the analysis of time deposits of healthcare funds and the examination of compliance with HFSA resolutions issued after the inspection of the direct and indirect costs of private pension fund investments into investment units.