hsbc global asset management hsbc global macro fund

TRANSCRIPT

HSBC Global Macro Fund HSBC GLOBAL ASSET MANAGEMENT

This presentation is only intended for professional investors

2Non contractual document

Contents

Executive SummaryFirm OverviewThe Case for a Global Macro AllocationHSBC Global Macro CapabilitiesInvestment Philosophy and ProcessPerformance and Characteristics

Appendices BiographiesImportant Information

Section 1

Section 2

Section 3

Section 4

Section 5

Section 6

Appendix I

Appendix II

3Non contractual document

Executive Summary

Source: Halbis - As at December 2008 - Past performance is not a guide of future returns.

►

The HSBC Global Macro Fund is an absolute return fund that seeks

to exploit pricing anomalies using complementary quantitative and qualitative based

strategies.

►

Our global opportunity set of Bonds, Equities, and Currencies is

implemented primarily through liquid exchange-traded futures and exchange-traded options.

►

Over 90 years of collective investment experience is blended with a detailed understanding of economics and asset price valuation. Our fundamental approach

provides maximum opportunities to exploit pricing anomalies within a diversified portfolio.

►

The investment vehicle is a UCITS III Registered Fund which looks to target a Euribor

+600 bps return with an annualised

volatility target of 7.5% and offers daily liquidity.

►

In 2008, the Global Macro Team finished the year up +10.07% with

a realised

monthly volatility of less than 4%.

Firm Overview

5Non contractual document

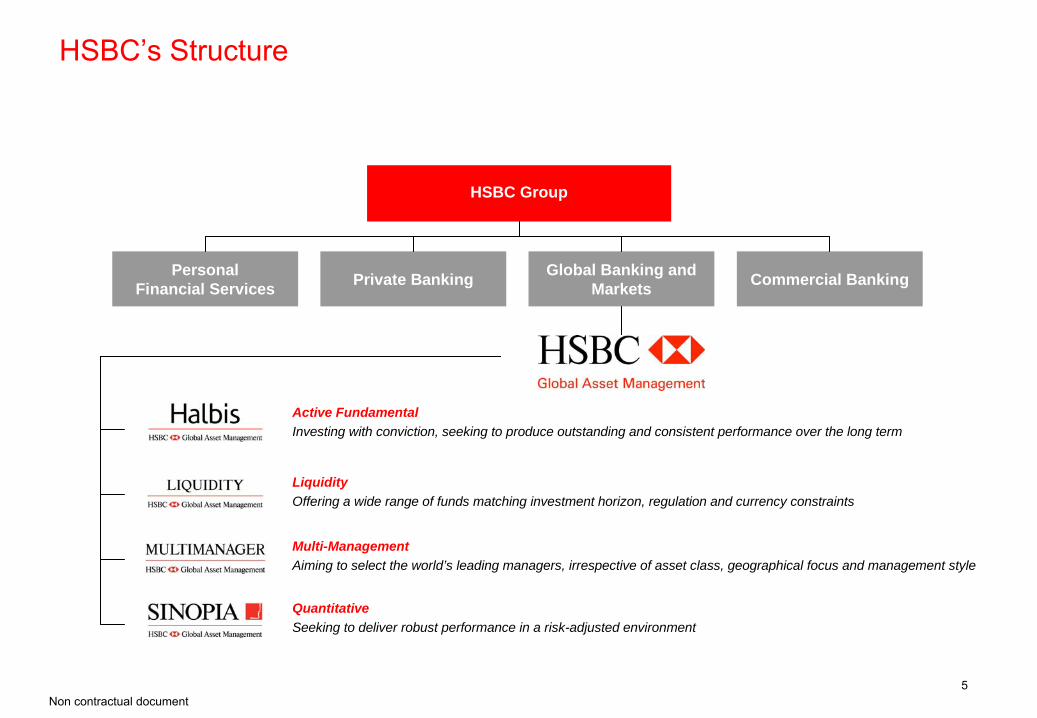

HSBC’s Structure

Active FundamentalInvesting with conviction, seeking to produce outstanding and consistent performance over the long term

QuantitativeSeeking to deliver robust performance in a risk-adjusted environment

Multi-ManagementAiming to select the world’s leading managers, irrespective of asset class, geographical focus and management style

Personal Financial Services Private Banking Global Banking and

Markets Commercial Banking

HSBC Group

LiquidityOffering a wide range of funds matching investment horizon, regulation and currency constraints

6Non contractual document

HSBC Global Asset Management

►

Multi-specialist asset management firm offering broad, highly diverse strategies

►

Aim to achieve long-term competitive performance by delivering sound investment solutions to clients

►

Distinct asset management capabilities EquityFixed IncomeMulti-asset and balancedAlternativesLiquidityStructured and Guaranteed

►

Strong global presence with extensive local knowledge and expertise

►

A leader in emerging markets asset management

7Non contractual document

HSBC Global Asset Management

►

HSBC’s core investment business dedicated to managing institutional and individual assets around the world

►

US$354.6 billion in assets under management*

►

Approximately 2,200 employees in 31 countries and territories*

►

A distinct multi-specialist investment modelHalbis – active fundamental HSBC Liquidity – active cash managementHSBC Multimanager - manager of managers/fund of funds platformSinopia – quantitative

►

Recognised

expertise Emerging MarketsAlternatives, including Fund of Hedge FundsClimate ChangeSocially Responsible InvestmentAmanah (Shariah compliant investments)

*As at 31 March 2009; Including Halbis, Liquidity, Multimanager and Sinopia.

8Non contractual document

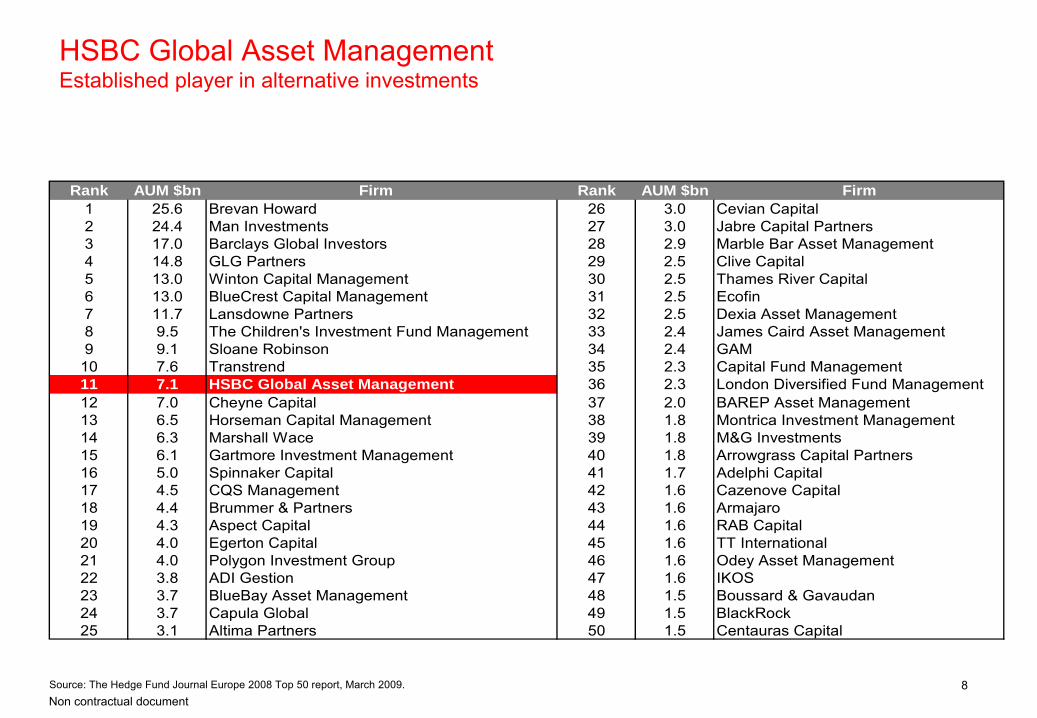

HSBC Global Asset Management Established player in alternative investments

Rank AUM $bn Firm Rank AUM $bn Firm1 25.6 Brevan Howard 26 3.0 Cevian Capital2 24.4 Man Investments 27 3.0 Jabre Capital Partners3 17.0 Barclays Global Investors 28 2.9 Marble Bar Asset Management4 14.8 GLG Partners 29 2.5 Clive Capital5 13.0 Winton Capital Management 30 2.5 Thames River Capital6 13.0 BlueCrest Capital Management 31 2.5 Ecofin7 11.7 Lansdowne Partners 32 2.5 Dexia Asset Management8 9.5 The Children's Investment Fund Management 33 2.4 James Caird Asset Management9 9.1 Sloane Robinson 34 2.4 GAM

10 7.6 Transtrend 35 2.3 Capital Fund Management11 7.1 HSBC Global Asset Management 36 2.3 London Diversified Fund Management12 7.0 Cheyne Capital 37 2.0 BAREP Asset Management13 6.5 Horseman Capital Management 38 1.8 Montrica Investment Management14 6.3 Marshall Wace 39 1.8 M&G Investments15 6.1 Gartmore Investment Management 40 1.8 Arrowgrass Capital Partners16 5.0 Spinnaker Capital 41 1.7 Adelphi Capital17 4.5 CQS Management 42 1.6 Cazenove Capital18 4.4 Brummer & Partners 43 1.6 Armajaro19 4.3 Aspect Capital 44 1.6 RAB Capital20 4.0 Egerton Capital 45 1.6 TT International21 4.0 Polygon Investment Group 46 1.6 Odey Asset Management22 3.8 ADI Gestion 47 1.6 IKOS23 3.7 BlueBay Asset Management 48 1.5 Boussard & Gavaudan24 3.7 Capula Global 49 1.5 BlackRock25 3.1 Altima Partners 50 1.5 Centauras Capital

Source: The Hedge Fund Journal Europe 2008 Top 50 report, March 2009.

The Case for a Global Macro Allocation

10Non contractual document

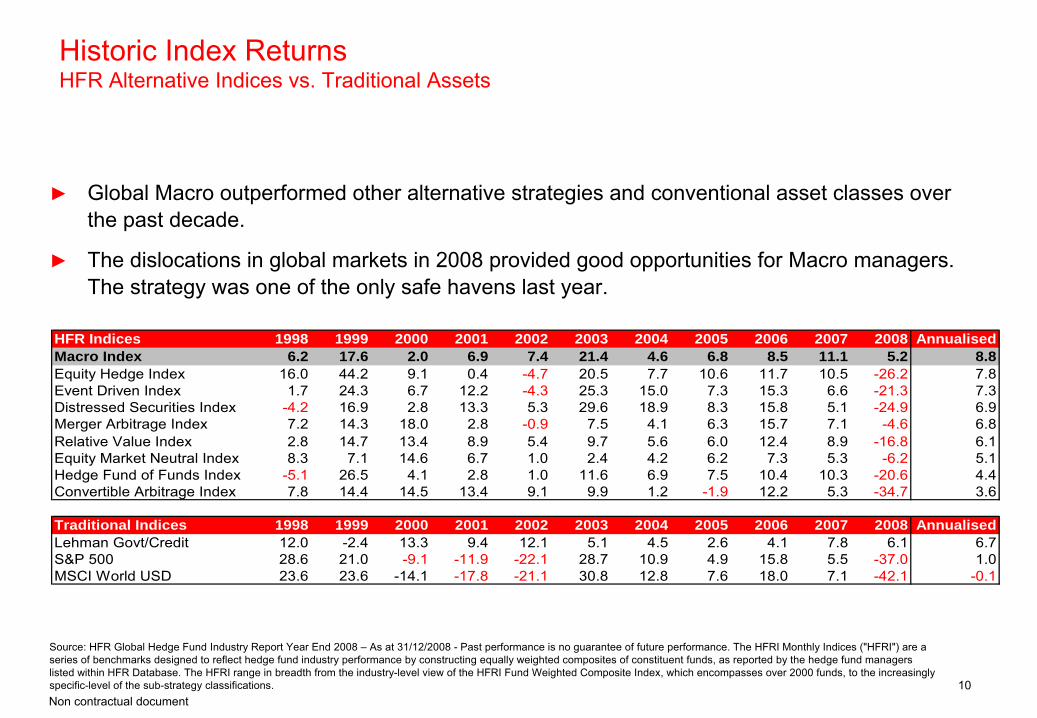

Historic Index Returns HFR Alternative Indices vs. Traditional Assets

HFR Indices 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 AnnualisedMacro Index 6.2 17.6 2.0 6.9 7.4 21.4 4.6 6.8 8.5 11.1 5.2 8.8Equity Hedge Index 16.0 44.2 9.1 0.4 -4.7 20.5 7.7 10.6 11.7 10.5 -26.2 7.8Event Driven Index 1.7 24.3 6.7 12.2 -4.3 25.3 15.0 7.3 15.3 6.6 -21.3 7.3Distressed Securities Index -4.2 16.9 2.8 13.3 5.3 29.6 18.9 8.3 15.8 5.1 -24.9 6.9Merger Arbitrage Index 7.2 14.3 18.0 2.8 -0.9 7.5 4.1 6.3 15.7 7.1 -4.6 6.8Relative Value Index 2.8 14.7 13.4 8.9 5.4 9.7 5.6 6.0 12.4 8.9 -16.8 6.1Equity Market Neutral Index 8.3 7.1 14.6 6.7 1.0 2.4 4.2 6.2 7.3 5.3 -6.2 5.1Hedge Fund of Funds Index -5.1 26.5 4.1 2.8 1.0 11.6 6.9 7.5 10.4 10.3 -20.6 4.4Convertible Arbitrage Index 7.8 14.4 14.5 13.4 9.1 9.9 1.2 -1.9 12.2 5.3 -34.7 3.6

Traditional Indices 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 AnnualisedLehman Govt/Credit 12.0 -2.4 13.3 9.4 12.1 5.1 4.5 2.6 4.1 7.8 6.1 6.7S&P 500 28.6 21.0 -9.1 -11.9 -22.1 28.7 10.9 4.9 15.8 5.5 -37.0 1.0MSCI World USD 23.6 23.6 -14.1 -17.8 -21.1 30.8 12.8 7.6 18.0 7.1 -42.1 -0.1

►

Global Macro outperformed other alternative strategies and conventional asset classes over the past decade.

►

The dislocations in global markets in 2008 provided good opportunities for Macro managers. The strategy was one of the only safe havens last year.

Source: HFR Global Hedge Fund Industry Report Year End 2008 –

As at 31/12/2008 -

Past performance is no guarantee of future performance. The HFRI Monthly Indices ("HFRI") are a series of benchmarks designed to reflect hedge fund industry performance by constructing equally weighted composites of constituent funds, as reported by the hedge fund managers listed within HFR Database. The HFRI range in breadth from the industry-level view of the HFRI Fund Weighted Composite Index, which encompasses over 2000 funds, to the increasingly specific-level of the sub-strategy classifications.

11Non contractual document

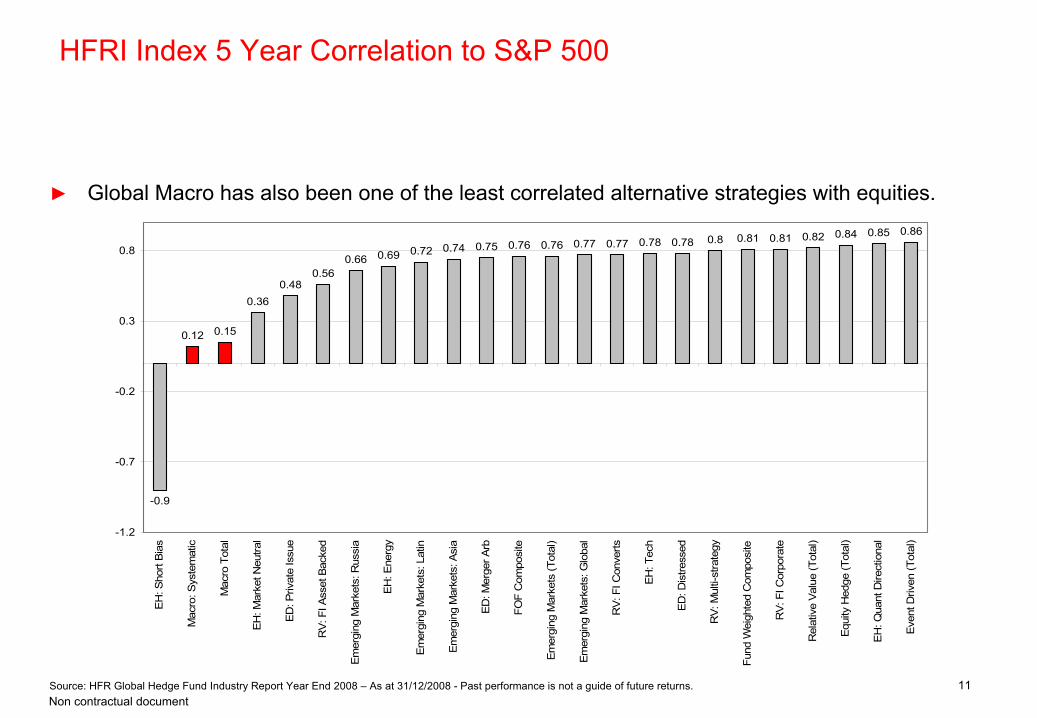

HFRI Index 5 Year Correlation to S&P 500

-0.9

0.12 0.15

0.360.48

0.560.66 0.69 0.72 0.74 0.75 0.76 0.76 0.77 0.77 0.78 0.78 0.8 0.81 0.81 0.82 0.84 0.85 0.86

-1.2

-0.7

-0.2

0.3

0.8

EH: S

hort

Bias

Mac

ro: S

yste

mat

ic

Mac

ro T

otal

EH: M

arke

t Neu

tral

ED: P

rivat

e Is

sue

RV:

FI A

sset

Bac

ked

Emer

ging

Mar

kets

: Rus

sia

EH: E

nerg

y

Emer

ging

Mar

kets

: Lat

in

Emer

ging

Mar

kets

: Asi

a

ED: M

erge

r Arb

FOF

Com

posi

te

Emer

ging

Mar

kets

(Tot

al)

Emer

ging

Mar

kets

: Glo

bal

RV:

FI C

onve

rts

EH: T

ech

ED: D

istre

ssed

RV:

Mul

ti-st

rate

gy

Fund

Wei

ghte

d C

ompo

site

RV:

FI C

orpo

rate

Rel

ativ

e Va

lue

(Tot

al)

Equi

ty H

edge

(Tot

al)

EH: Q

uant

Dire

ctio

nal

Even

t Driv

en (T

otal

)

►

Global Macro has also been one of the least correlated alternative strategies with equities.

Source: HFR Global Hedge Fund Industry Report Year End 2008 –

As at 31/12/2008 -

Past performance is not a guide of future returns.

12Non contractual document

HFRI Index 5 Year Risk Return Comparison

EH

Energy

TechE-D

Macro

Macro: Sys Div

ConvArb

FI-Corp

EM: LatAm

EM: Russia

S&P 500

EqMrktNtrl

QuantDrctnl

Short

Distressed

MergArb RegD

RV

Asset-Bcked

RV: Multi

Yield Alts

FWC

FOF

Emrgng MrktsEM: Asia ex-Japan

EM: Global

Lehman Govt/Credit

(10.00)

(5.00)

0.00

5.00

10.00

15.00

0.00 5.00 10.00 15.00 20.00 25.00

Standard Deviation %

Rat

e of

Ret

urn

%

►

Global Macro has been compelling from a risk / return standpoint

vs. other alternatives.

Source: HFR Global Hedge Fund Industry Report Year End 2008 –

As at 31/12/2008 -

Past performance is not a guide of future returns.

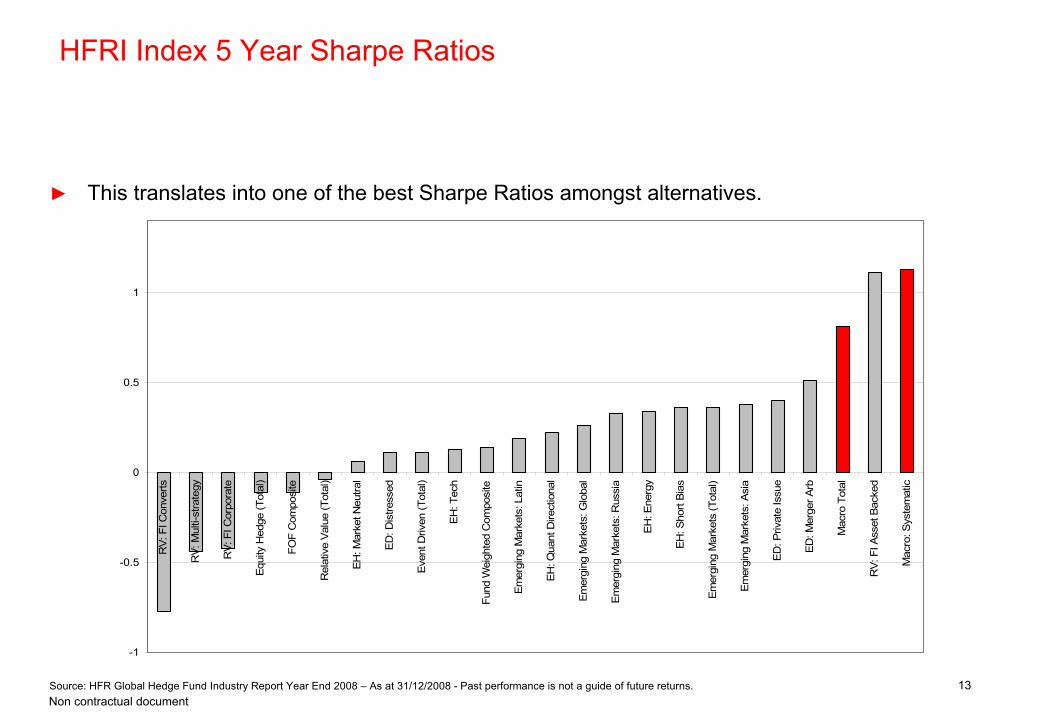

13Non contractual document

HFRI Index 5 Year Sharpe Ratios

-1

-0.5

0

0.5

1

RV:

FI C

onve

rts

RV

: Mul

ti-st

rate

gy

RV:

FI C

orpo

rate

Equi

ty H

edge

(Tot

al)

FOF

Com

posi

te

Rel

ativ

e Va

lue

(Tot

al)

EH: M

arke

t Neu

tral

ED: D

istre

ssed

Even

t Driv

en (T

otal

)

EH: T

ech

Fund

Wei

ghte

d C

ompo

site

Emer

ging

Mar

kets

: Lat

in

EH: Q

uant

Dire

ctio

nal

Emer

ging

Mar

kets

: Glo

bal

Emer

ging

Mar

kets

: Rus

sia

EH: E

nerg

y

EH: S

hort

Bias

Emer

ging

Mar

kets

(Tot

al)

Emer

ging

Mar

kets

: Asi

a

ED: P

rivat

e Is

sue

ED: M

erge

r Arb

Mac

ro T

otal

RV:

FI A

sset

Bac

ked

Mac

ro: S

yste

mat

ic

►

This translates into one of the best Sharpe Ratios amongst alternatives.

Source: HFR Global Hedge Fund Industry Report Year End 2008 –

As at 31/12/2008 -

Past performance is not a guide of future returns.

HSBC Global Macro Investment Capabilities

15Non contractual document

Core investment team has been together since 2005 and has extensive industry expertise.

Experienced Team

Greater transparency for investors and daily liquidity via our UCITS III structure.

Transparency & Liquidity

Multi-Strategy Approach: Combining quantitative analysis with macro-economic research.

Innovative “Best of Both”

Approach

Aim for consistent absolute performance within a conservative risk budget.

Performance Orientation

Experience of a wide variety of techniques to capture returns across asset classes.

Deep Capabilities

Performance fees with a hurdle and management compensation align client and manager interest.

Alignment of Interest

HSBC Global Macro Fund Key Strengths

16Non contractual document

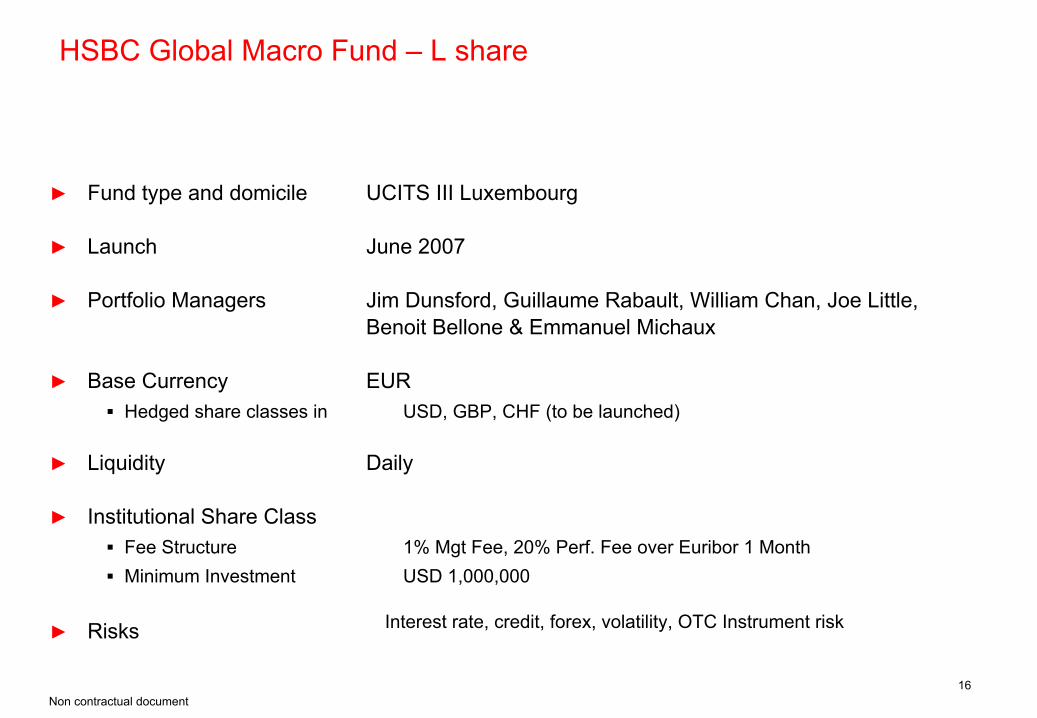

HSBC Global Macro Fund –

L share

►

Fund type and domicile

►

Launch

►

Portfolio Managers

►

Base Currency Hedged share classes in

►

Liquidity

►

Institutional Share ClassFee Structure Minimum Investment

►

Risks

UCITS III Luxembourg

June

2007

Jim Dunsford, Guillaume Rabault, William Chan, Joe Little, Benoit Bellone & Emmanuel Michaux

EURUSD, GBP, CHF (to be

launched)

Daily

1% Mgt

Fee, 20% Perf. Fee

over Euribor

1 MonthUSD 1,000,000

Interest

rate, credit, forex, volatility, OTC Instrument risk

Investment Philosophy and Process

18Non contractual document

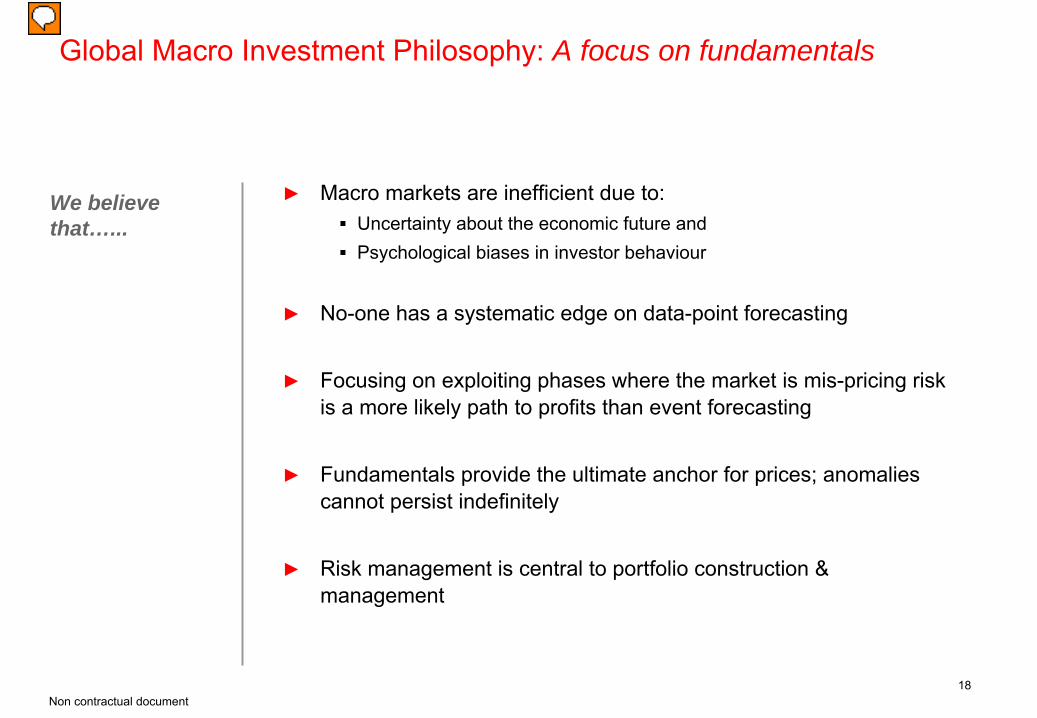

Global Macro Investment Philosophy: A focus on fundamentals

We believe that…...

►

Macro markets

are inefficient due to:Uncertainty about the economic future andPsychological biases in investor behaviour

►

No-one has a systematic

edge

on data-point forecasting

►

Focusing

on exploiting

phases where

the market

is

mis-pricing

risk

is

a more likely

path

to profits than

event

forecasting

►

Fundamentals provide

the ultimate

anchor

for prices; anomalies cannot

persist

indefinitely

►

Risk

management is

central to portfolio construction & management

19Non contractual document

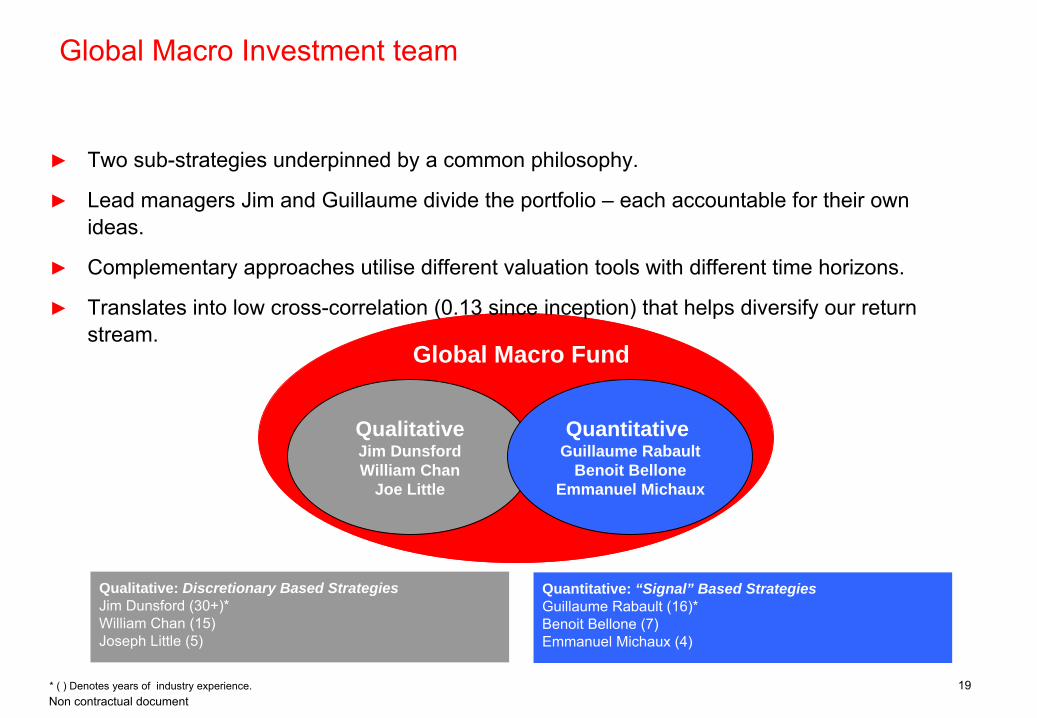

Global Macro Investment team

Qualitative: Discretionary Based StrategiesJim Dunsford (30+)*William Chan (15)Joseph Little (5)

QualitativeJim DunsfordWilliam Chan

Joe Little

Global Macro Fund

Quantitative Guillaume Rabault

Benoit BelloneEmmanuel Michaux

Quantitative: “Signal” Based StrategiesGuillaume Rabault (16)*Benoit Bellone

(7)Emmanuel Michaux

(4)

►

Two sub-strategies underpinned by a common philosophy.

►

Lead managers Jim and Guillaume divide the portfolio –

each accountable for their own ideas.

►

Complementary approaches utilise

different valuation tools with different time horizons.

►

Translates into low cross-correlation (0.13 since inception) that helps diversify our return stream.

* ( ) Denotes years of industry experience.

20Non contractual document

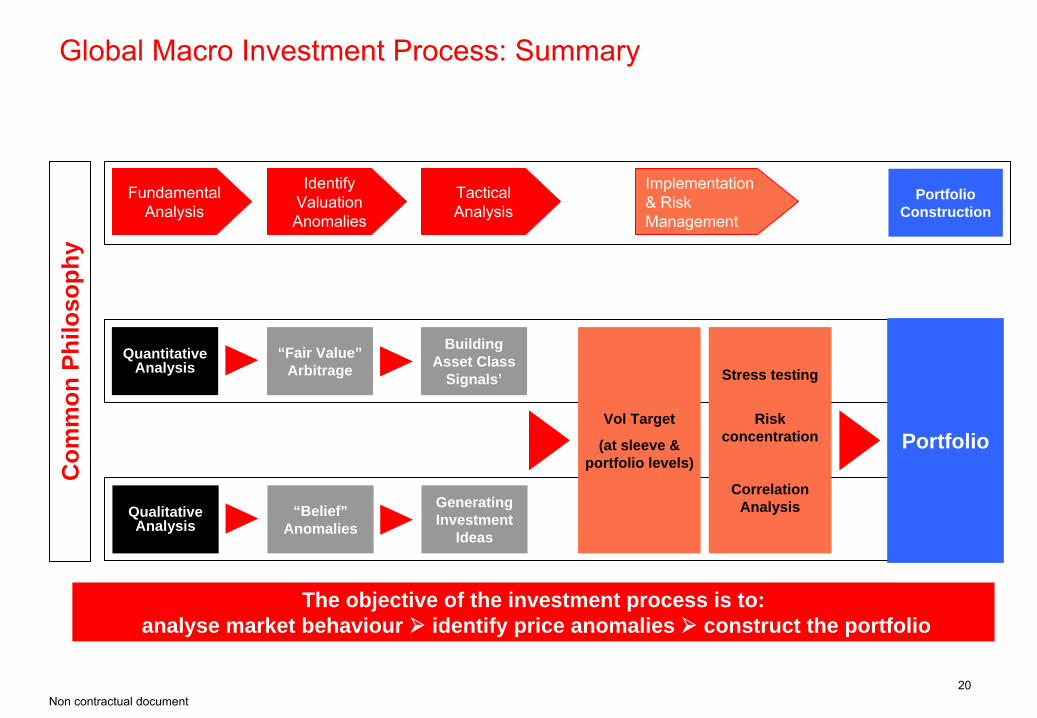

Portfolio

Global Macro Investment Process: Summary

The objective of the investment process is to:analyse market behaviour identify price anomalies construct the portfolio

Com

mon

Phi

loso

phy

FundamentalAnalysis

IdentifyValuationAnomalies

TacticalAnalysis

Implementation& Risk Management

“Fair Value” Arbitrage

Quantitative Analysis

Building Asset Class

Signals’

“Belief” Anomalies

Qualitative Analysis

Generating Investment

Ideas

Portfolio Construction

Vol Target

(at sleeve & portfolio levels)

Stress testing

Risk concentration

Correlation Analysis

21Non contractual document

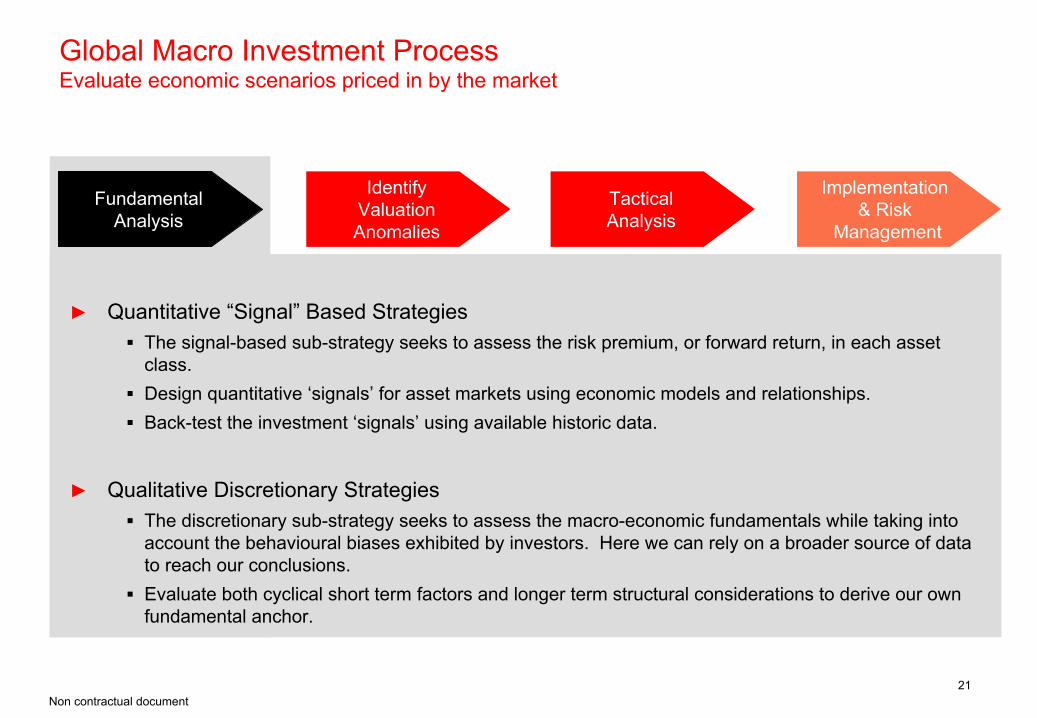

Global Macro Investment Process Evaluate economic scenarios priced in by the market

►

Quantitative “Signal”

Based StrategiesThe signal-based sub-strategy seeks to assess the risk premium, or forward return, in each asset class.Design quantitative ‘signals’ for asset markets using economic models and relationships.Back-test the investment ‘signals’ using available historic data.

►

Qualitative Discretionary StrategiesThe discretionary sub-strategy seeks to assess the macro-economic fundamentals while taking into account the behavioural biases exhibited by investors. Here we can rely on a broader source of data to reach our conclusions.Evaluate both cyclical short term factors and longer term structural considerations to derive our own fundamental anchor.

FundamentalAnalysis

IdentifyValuationAnomalies

TacticalAnalysis

Implementation & Risk

Management

22Non contractual document

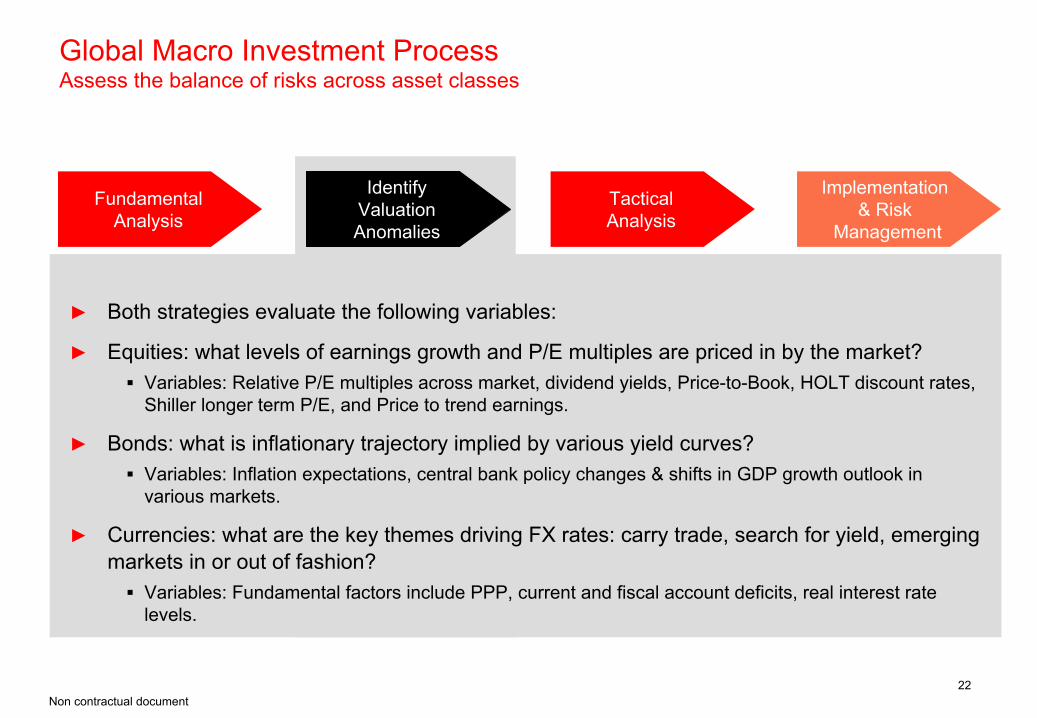

Global Macro Investment Process Assess the balance of risks across asset classes

►

Both strategies evaluate the following variables:

►

Equities: what levels of earnings growth and P/E multiples are priced in by the market?Variables: Relative P/E multiples across market, dividend yields, Price-to-Book, HOLT discount rates, Shiller longer term P/E, and Price to trend earnings.

►

Bonds: what is inflationary trajectory implied by various yield curves?Variables: Inflation expectations, central bank policy changes & shifts in GDP growth outlook in various markets.

►

Currencies: what are the key themes driving FX rates: carry trade, search for yield, emerging markets in or out of fashion?

Variables: Fundamental factors include PPP, current and fiscal account deficits, real interest rate levels.

FundamentalAnalysis

IdentifyValuationAnomalies

TacticalAnalysis

Implementation & Risk

Management

23Non contractual document

Global Macro Investment Process Focus where risk is mis-priced & consensus deviates from our views

FundamentalAnalysis

IdentifyValuationAnomalies

TacticalAnalysis

Implementation & Risk

Management

►

The Qualitative Strategy in particular considers additional factors to determine entry and exit points:

Sentiment surveys like the AAII Bull-Bear RatioPut / Call ratios to assess bullish or bearish sentimentIMM Index of Speculative Positions for consensus on currenciesRSI indicators

24Non contractual document

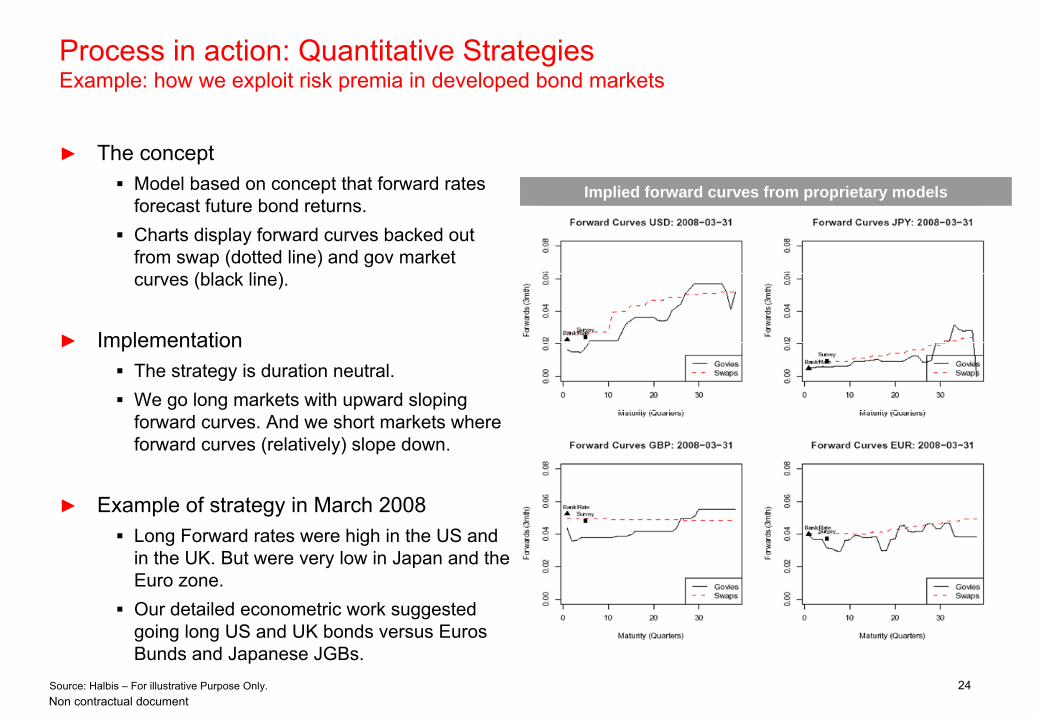

Process in action: Quantitative Strategies Example: how we exploit risk premia

in developed bond markets

Implied forward curves from proprietary models

►

The conceptModel based on concept that forward rates forecast future bond returns.Charts display forward curves backed out from swap (dotted line) and gov market curves (black line).

►

ImplementationThe strategy is duration neutral.We go long markets with upward sloping forward curves. And we short markets where forward curves (relatively) slope down.

►

Example of strategy in March 2008Long Forward rates were high in the US and in the UK. But were very low in Japan and the Euro zone.Our detailed econometric work suggested going long US and UK bonds versus Euros Bunds and Japanese JGBs.

Implied forward curves from proprietary models

Source: Halbis –

For illustrative Purpose Only.

25Non contractual document

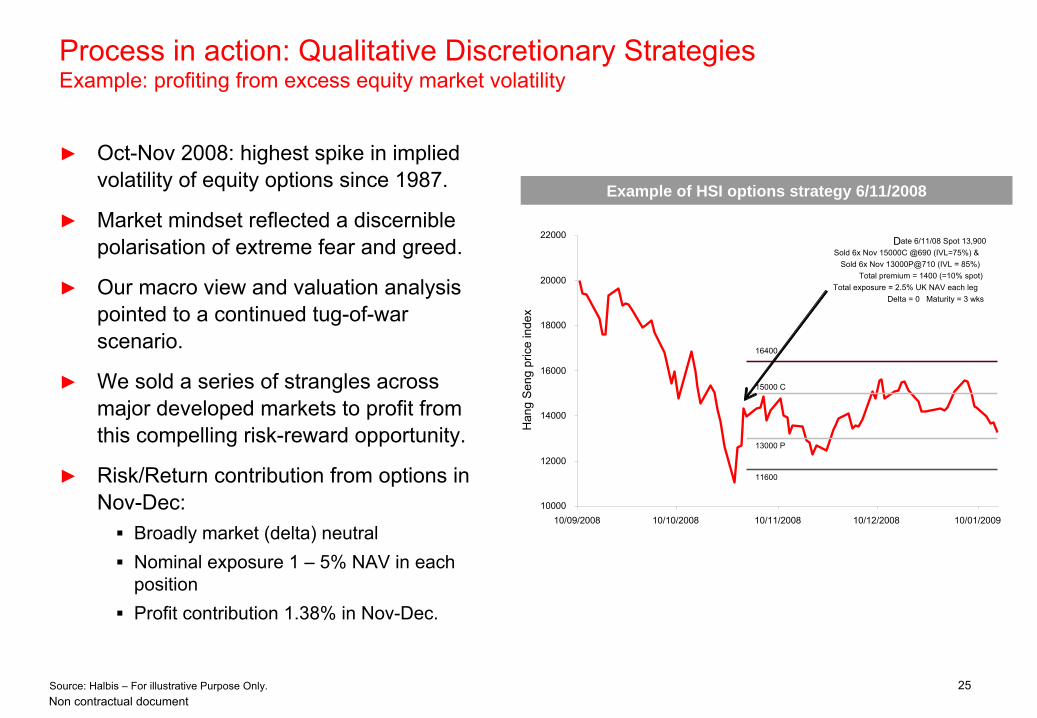

Process in action: Qualitative Discretionary Strategies Example: profiting from excess equity market volatility

Example of HSI options strategy 6/11/2008

10000

12000

14000

16000

18000

20000

22000

10/09/2008 10/10/2008 10/11/2008 10/12/2008 10/01/2009H

ang

Seng

pric

e in

dex

11600

13000 P

15000 C

16400

Date 6/11/08 Spot 13,900Sold 6x Nov 15000C @690 (IVL=75%) &

Sold 6x Nov 13000P@710 (IVL = 85%)Total premium = 1400 (=10% spot)

Total exposure = 2.5% UK NAV each legDelta = 0 Maturity = 3 wks

►

Oct-Nov 2008: highest spike in implied volatility of equity options since 1987.

►

Market mindset reflected a discernible polarisation

of extreme fear and greed.

►

Our macro view and valuation analysis pointed to a continued tug-of-war scenario.

►

We sold a series of strangles across major developed markets to profit from this compelling risk-reward opportunity.

►

Risk/Return contribution from options in Nov-Dec:

Broadly market (delta) neutralNominal exposure 1 – 5% NAV in each positionProfit contribution 1.38% in Nov-Dec.

Source: Halbis –

For illustrative Purpose Only.

26Non contractual document

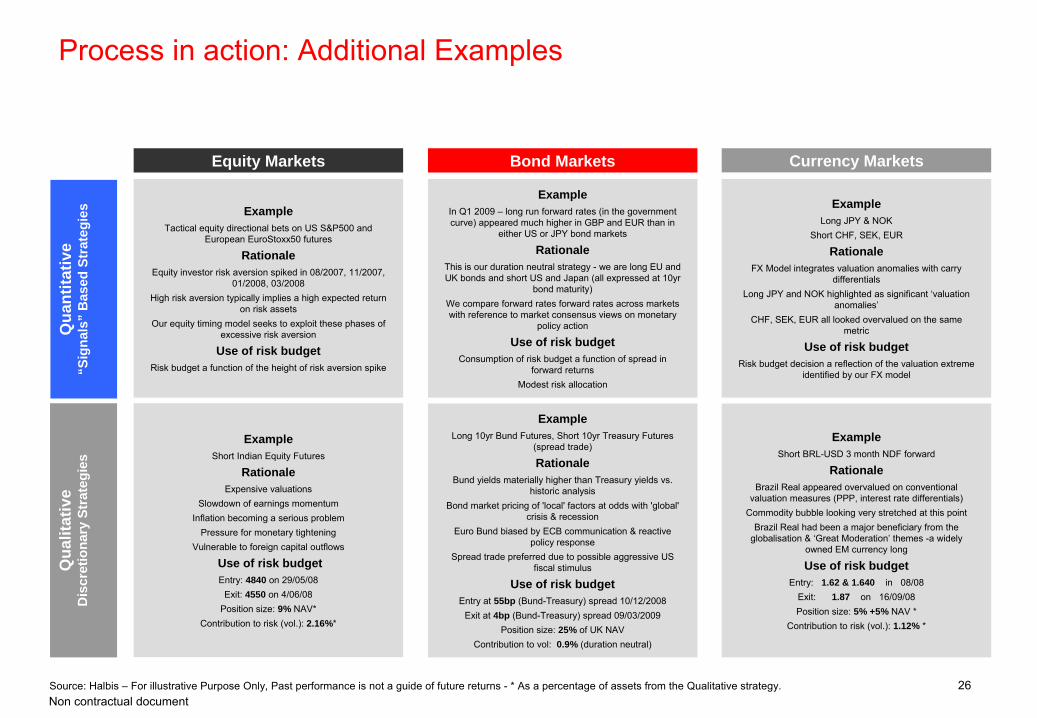

Process in action: Additional Examples

ExampleTactical equity directional bets on US S&P500 and

European EuroStoxx50 futures

RationaleEquity investor risk aversion spiked in 08/2007, 11/2007,

01/2008, 03/2008 High risk aversion typically implies a high expected return

on risk assetsOur equity timing model seeks to exploit these phases of

excessive risk aversion

Use of risk budgetRisk budget a function of the height of risk aversion spike

Equity Markets

ExampleIn Q1 2009 –

long run forward rates (in the government curve) appeared much higher in GBP and EUR than in

either US or JPY bond markets

RationaleThis is our duration neutral strategy -

we are long EU and UK bonds and short US and Japan (all expressed at 10yr

bond maturity)We compare forward rates forward rates across markets with reference to market consensus views on monetary

policy action

Use of risk budgetConsumption of risk budget a function of spread in

forward returnsModest risk allocation

Bond Markets

ExampleLong JPY & NOK

Short CHF, SEK, EUR

RationaleFX Model integrates valuation anomalies with carry

differentialsLong JPY and NOK highlighted as significant ‘valuation

anomalies’CHF, SEK, EUR all looked overvalued on the same

metric

Use of risk budgetRisk budget decision a reflection of the valuation extreme

identified by our FX model

Currency Markets

ExampleShort Indian Equity Futures

RationaleExpensive valuations

Slowdown of earnings momentumInflation becoming a serious problem

Pressure for monetary tighteningVulnerable to foreign capital outflows

Use of risk budgetEntry: 4840 on 29/05/08

Exit: 4550 on 4/06/08Position size: 9% NAV*

Contribution to risk (vol.): 2.16%*

ExampleLong 10yr Bund Futures, Short 10yr Treasury Futures

(spread trade)

RationaleBund yields materially higher than Treasury yields vs.

historic analysisBond market pricing of 'local' factors at odds with 'global'

crisis & recessionEuro Bund biased by ECB communication & reactive

policy responseSpread trade preferred due to possible aggressive US

fiscal stimulus

Use of risk budgetEntry at 55bp (Bund-Treasury) spread 10/12/2008

Exit at 4bp (Bund-Treasury) spread 09/03/2009Position size: 25% of UK NAV

Contribution to vol: 0.9% (duration neutral)

ExampleShort BRL-USD 3 month NDF forward

RationaleBrazil Real appeared overvalued on conventional

valuation measures (PPP, interest rate differentials)Commodity bubble looking very stretched at this point

Brazil Real had been a major beneficiary from the globalisation & ‘Great Moderation’

themes -a widely owned EM currency long

Use of risk budgetEntry: 1.62 & 1.640 in 08/08

Exit: 1.87 on 16/09/08Position size: 5% +5% NAV *

Contribution to risk (vol.): 1.12% *

Qua

litat

ive

Dis

cret

iona

ry S

trat

egie

sQ

uant

itativ

e“S

igna

ls”

Bas

ed S

trat

egie

s

Source: Halbis –

For illustrative Purpose Only, Past performance is not a guide of future returns -

* As a percentage of assets from the Qualitative strategy.

27Non contractual document

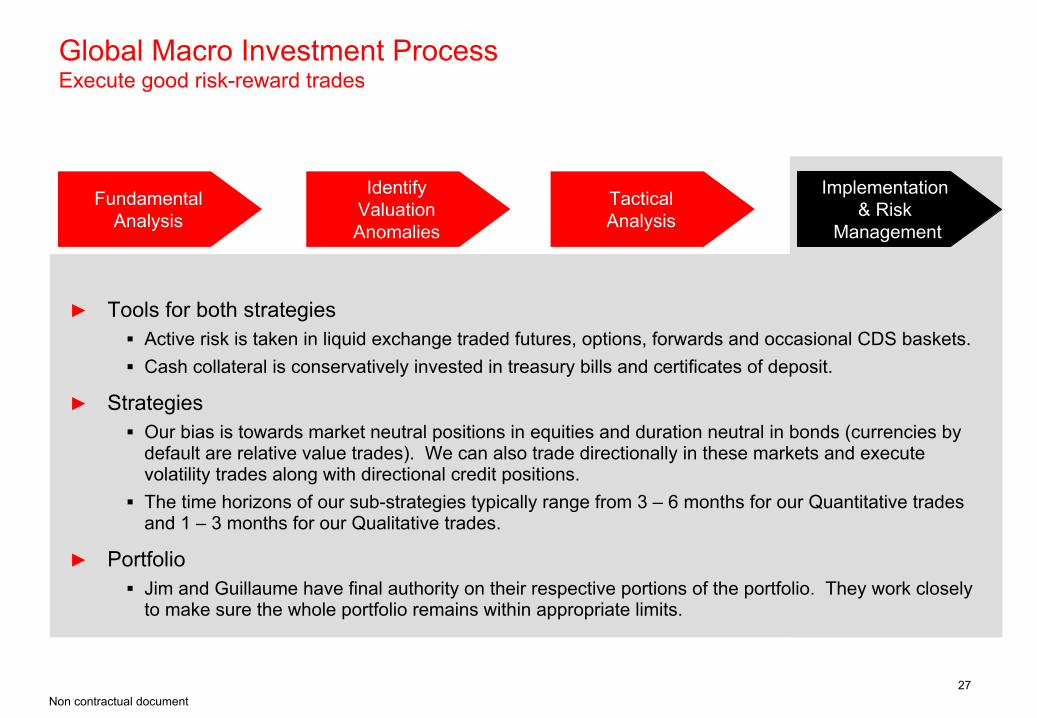

Global Macro Investment Process Execute good risk-reward trades

FundamentalAnalysis

IdentifyValuationAnomalies

TacticalAnalysis

Implementation & Risk

Management

►

Tools for both strategiesActive risk is taken in liquid exchange traded futures, options, forwards and occasional CDS baskets.Cash collateral is conservatively invested in treasury bills and certificates of deposit.

►

StrategiesOur bias is towards market neutral positions in equities and duration neutral in bonds (currencies by default are relative value trades). We can also trade directionally in these markets and execute volatility trades along with directional credit positions. The time horizons of our sub-strategies typically range from 3 – 6 months for our Quantitative trades and 1 – 3 months for our Qualitative trades.

►

PortfolioJim and Guillaume have final authority on their respective portions of the portfolio. They work closely to make sure the whole portfolio remains within appropriate limits.

28Non contractual document

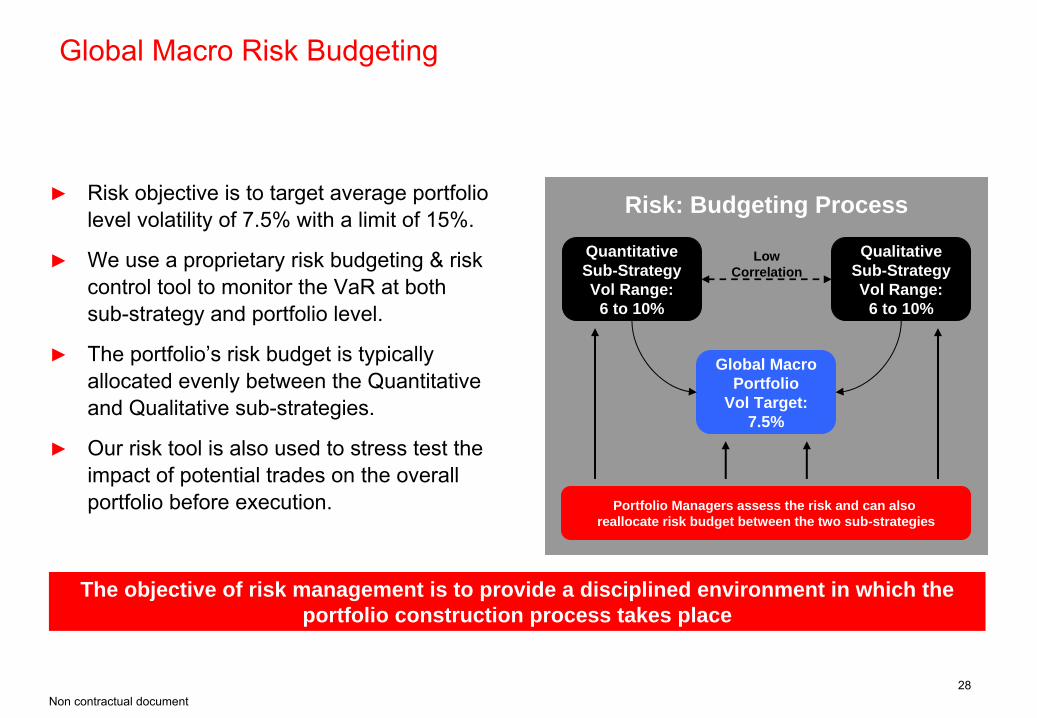

Global Macro Risk Budgeting

The objective of risk management is to provide a disciplined environment in which the portfolio construction process takes place

QuantitativeSub-StrategyVol Range:

6 to 10%

QualitativeSub-StrategyVol Range:

6 to 10%

Low Correlation

Global MacroPortfolio

Vol Target:7.5%

Portfolio Managers assess the risk and can also reallocate risk budget between the two sub-strategies

Risk: Budgeting Process►

Risk objective is to target average portfolio level volatility of 7.5% with a limit of 15%.

►

We use a proprietary risk budgeting & risk control tool to monitor the VaR at both sub-strategy and portfolio level.

►

The portfolio’s risk budget is typically allocated evenly between the Quantitative and Qualitative sub-strategies.

►

Our risk tool is also used to stress test the impact of potential trades on the overall portfolio before execution.

29Non contractual document

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

Mar-08 Jun-08 Sep-08 Dec-08 Mar-09 Jun-09-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

Jul-08 Oct-08 Jan-09 Apr-09 Jul-09

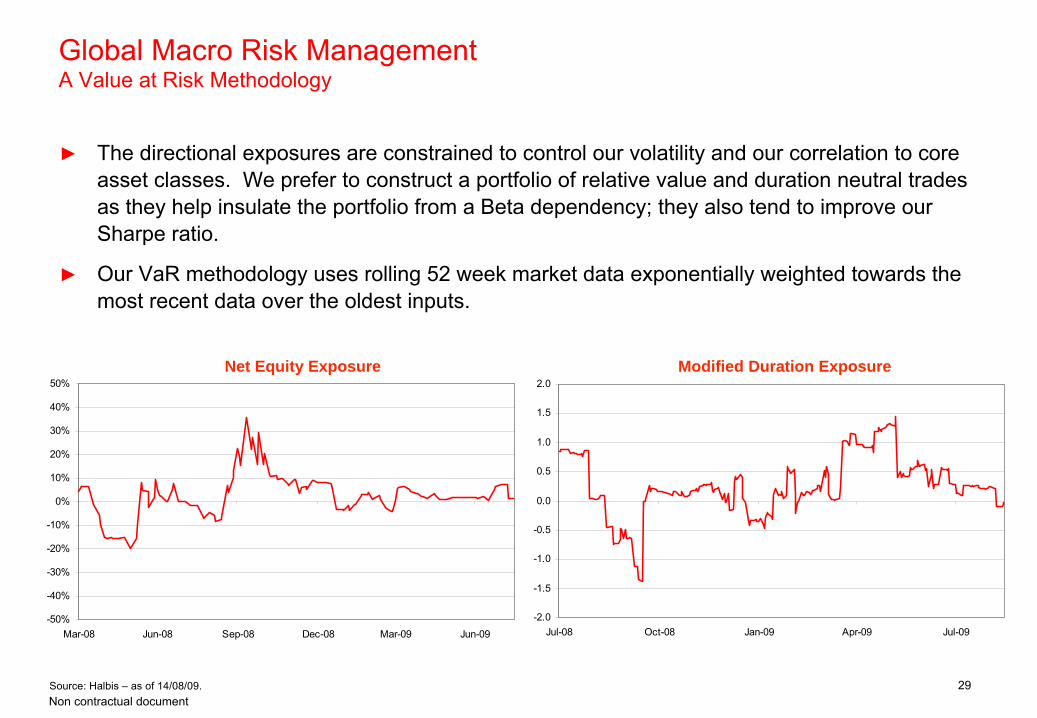

Global Macro Risk Management A Value at Risk Methodology

Net Equity Exposure Modified Duration Exposure

►

The directional exposures are constrained to control our volatility and our correlation to core asset classes. We prefer to construct a portfolio of relative value and duration neutral trades as they help insulate the portfolio from a Beta dependency; they

also tend to improve our Sharpe ratio.

►

Our VaR methodology uses rolling 52 week market data exponentially weighted towards the most recent data over the oldest inputs.

Source: Halbis –

as of 14/08/09.

30Non contractual document

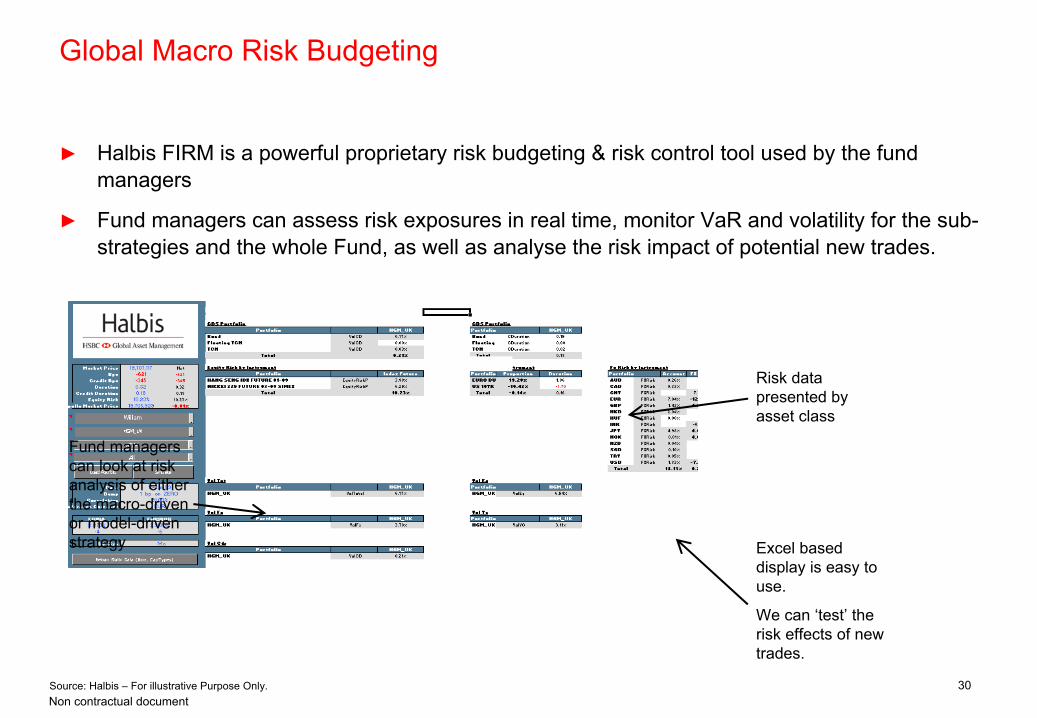

Global Macro Risk Budgeting

►

Halbis FIRM is a powerful proprietary risk budgeting & risk control tool used by the fund managers

►

Fund managers can assess risk exposures in real time, monitor VaR and volatility for the sub-

strategies and the whole Fund, as well as analyse the risk impact of potential new trades.

Fund managers can look at risk analysis of either the macro-driven or model-driven strategy

Risk data presented by asset class

Excel based display is easy to use.

We can ‘test’

the risk effects of new trades.

Source: Halbis –

For illustrative Purpose Only.

31Non contractual document

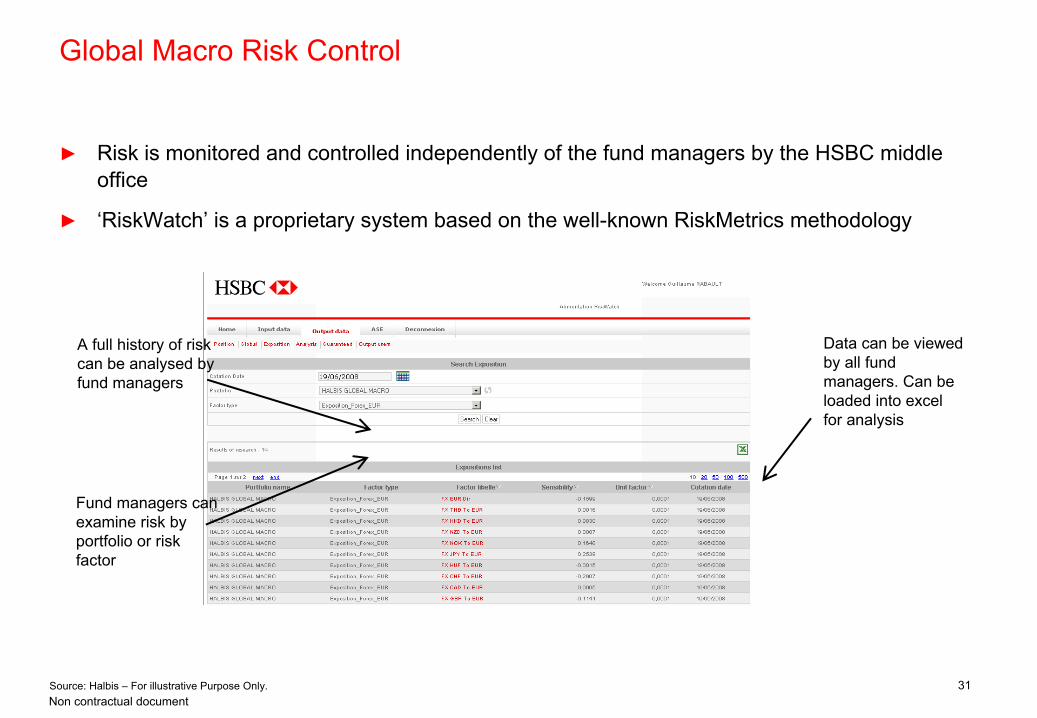

Global Macro Risk Control

►

Risk is monitored and controlled independently of the fund managers by the HSBC middle office

►

‘RiskWatch’

is a proprietary system based on the well-known RiskMetrics

methodology

Fund managers can examine risk by portfolio or risk factor

Data can be viewed by all fund managers. Can be loaded into excel for analysis

A full history of risk can be analysed by fund managers

Source: Halbis –

For illustrative Purpose Only.

32Non contractual document

Portfolio Construction Bringing the sub-strategies together

►

Autonomous sub-strategy sleeves are united by a philosophy based upon fundamentals and a regular communication process.

►

Weekly meetings to review the entire portfolio and debate the macro-economic backdrop.

►

The teams carefully calibrate the portfolio exposures when exposures overlap as they did directionally in October 2008.

►

The sub-strategies theoretically could trade against one another but the

common commitment to valuation anchors mitigates the likelihood of this occurring.

►

Shared systems further mitigate this and other risks. The PMs stress test trade ideas’

impact on the whole portfolio prior to execution.

Benefit: independent quantitative and qualitative sub-strategies operating within a common risk and valuation framework with low cross correlation

33Non contractual document

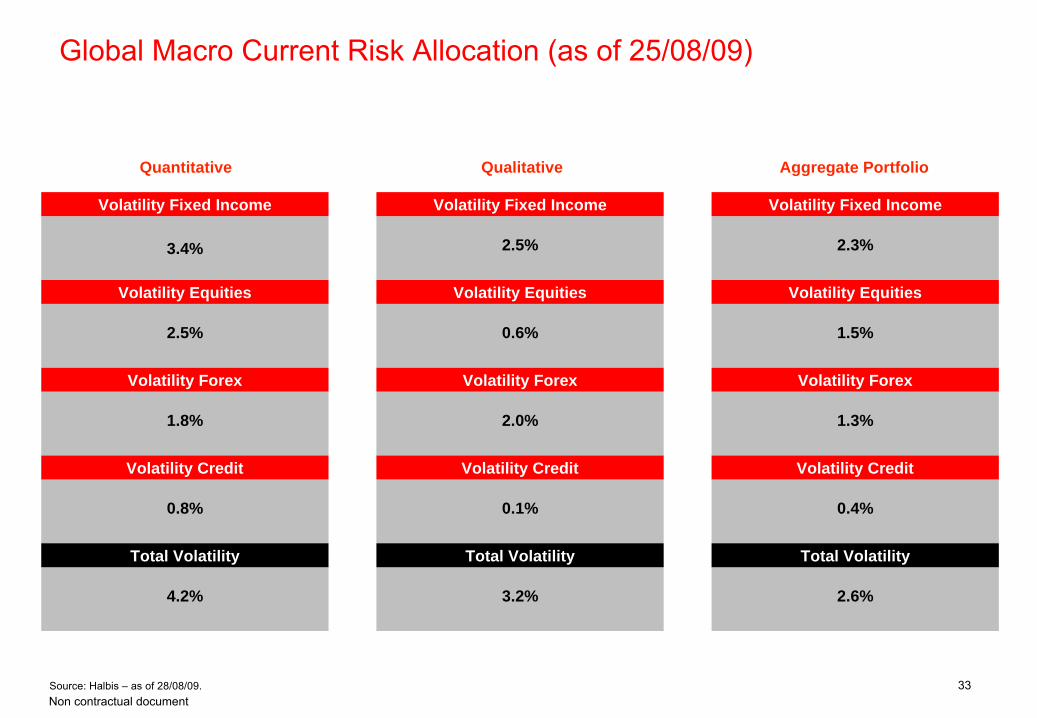

2.5%

0.6%

2.0%

0.1%

3.2%

2.3%

1.5%

1.3%

0.4%

2.6%

3.4%

2.5%

1.8%

0.8%

4.2%

Volatility Fixed Income

Volatility Equities

Volatility Credit

Total Volatility

Volatility Forex

Volatility Fixed Income Volatility Fixed Income

Volatility Equities Volatility Equities

Volatility Forex Volatility Forex

Volatility Credit Volatility Credit

Total Volatility Total Volatility

Quantitative Qualitative Aggregate Portfolio

Global Macro Current Risk Allocation (as of 25/08/09)

Source: Halbis –

as of 28/08/09.

Performance and Characteristics

35Non contractual document

HSBC Global Macro Performance

Sources: Bloomberg, Halbis –

As at 31-07-2009 -

Past performance is not a guide of future returns.

-0.46%

0.45%0.35%0.59%0.11%

-2.51%

1.53%1.59% 1.58%

-0.08%

0.82%1.27%1.22%

2.26%2.58%

-0.77%

1.05%0.66%

0.36%

1.20%

-0.30%

0.22%0.79%

-1.00%

0.07%0.16%

-4%

-2%

0%

2%

4%

Jun-07 Sep-07 Dec-07 Mar-08 Jun-08 Sep-08 Dec-08 Mar-09 Jun-0980

90

100

110

120

Fund Return (%) Euribor 1 Month Halbis Global Macro - NAV

Year Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Year2007 -0.46% 0.45% 0.35% 0.59% 0.11% -2.51% 1.53% 0.00%2008 1.59% 0.16% -1.00% 1.58% 0.07% -0.08% 0.82% 1.27% 1.22% 2.26% 2.58% -0.77% 10.07%2009 1.05% 0.66% 0.36% 1.20% -0.30% 0.22% 0.79% 4.04%

Return Risk CorrelationsAnnualised Return 6.46% Volatility 3.69% MSCI World TR (€) -0.01Cumulative Return 14.52% Sharpe Ratio 0.83 Tremont Index (€) -0.35 (as of Jun 09)

Best month 2.58% Max drawdown -2.51% Tremont Global Macro (€) -0.15 (as of Jun 09)

Worst month -2.51% Months to recover 2% Positive month 77%

Monthly performance (%, net of fees)

Statistical analysis

36Non contractual document

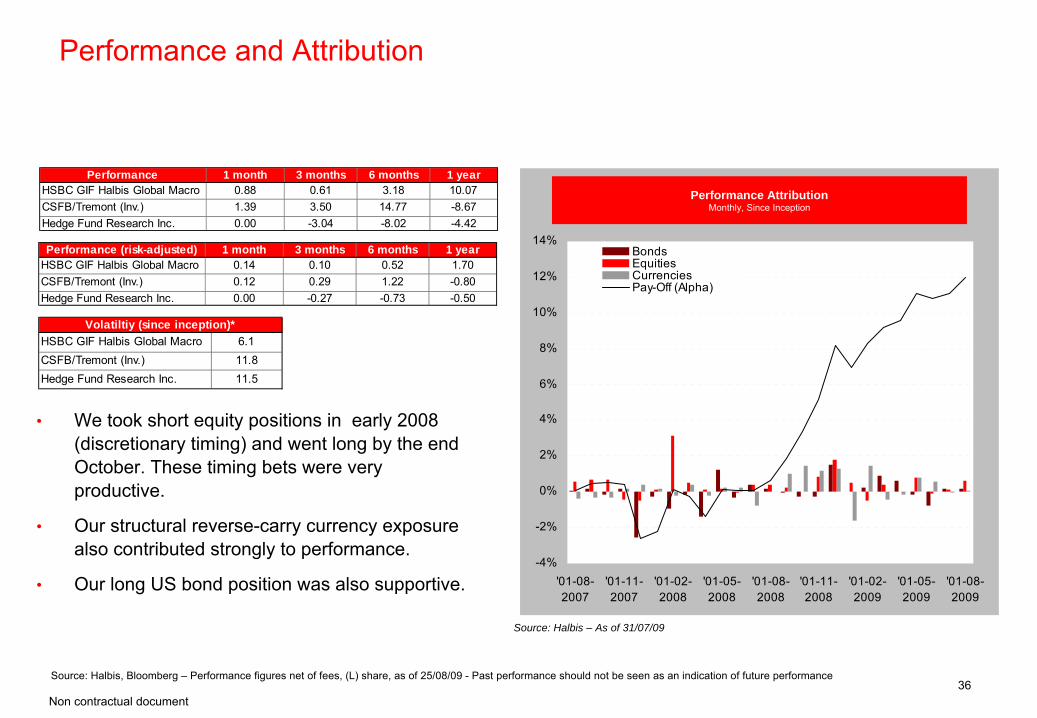

Performance and Attribution

•

We took short equity positions in early 2008 (discretionary timing) and went long by the end October. These timing bets were very productive.

•

Our structural reverse-carry currency exposure also contributed strongly to performance.

•

Our long US bond position was also supportive.

Source: Halbis, Bloomberg –

Performance figures net of fees, (L) share, as of 25/08/09 -

Past performance should not be seen as an indication of future performance

Source: Halbis – As of 31/07/09

Performance AttributionMonthly, Since Inception

Performance (risk-adjusted) 1 month 3 months 6 months 1 yearHSBC GIF Halbis Global Macro 0.14 0.10 0.52 1.70CSFB/Tremont (Inv.) 0.12 0.29 1.22 -0.80Hedge Fund Research Inc. 0.00 -0.27 -0.73 -0.50

Performance 1 month 3 months 6 months 1 yearHSBC GIF Halbis Global Macro 0.88 0.61 3.18 10.07CSFB/Tremont (Inv.) 1.39 3.50 14.77 -8.67Hedge Fund Research Inc. 0.00 -3.04 -8.02 -4.42

HSBC GIF Halbis Global Macro 6.1CSFB/Tremont (Inv.) 11.8Hedge Fund Research Inc. 11.5

Volatiltiy (since inception)*

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

'01-08-2007

'01-11-2007

'01-02-2008

'01-05-2008

'01-08-2008

'01-11-2008

'01-02-2009

'01-05-2009

'01-08-2009

BondsEquitiesCurrenciesPay-Off (Alpha)

37Non contractual document

Source: Halbis –

As of 31/07/09 -

Past performance should not be seen as an indication of future performance

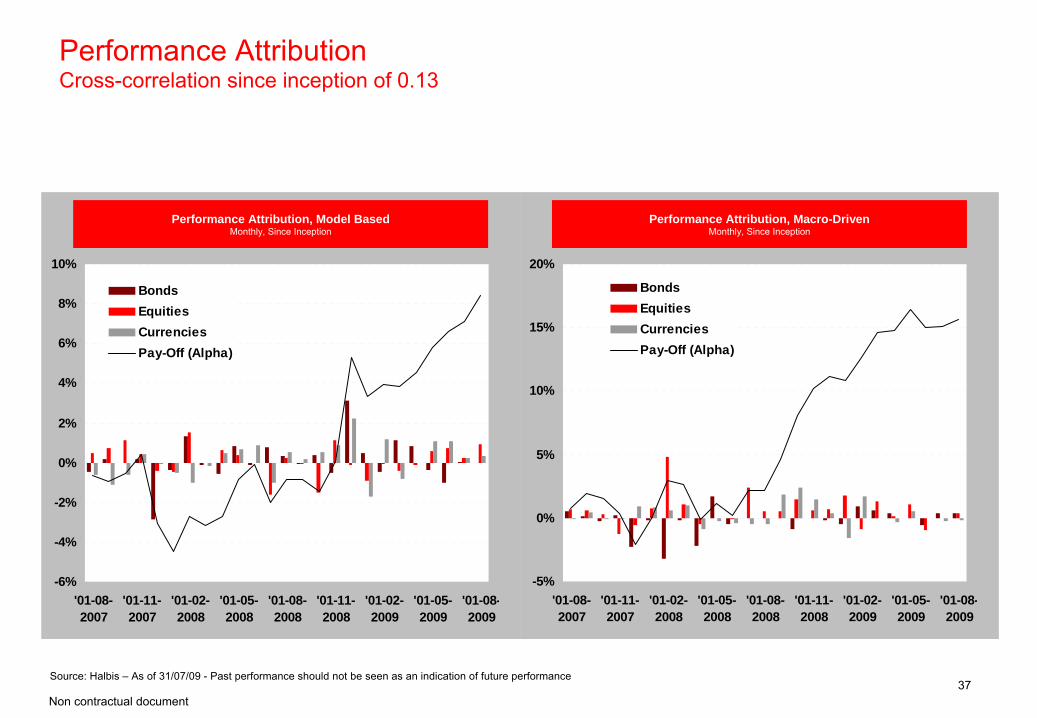

Performance Attribution, Model BasedMonthly, Since Inception

Performance Attribution, Macro-DrivenMonthly, Since Inception

Performance Attribution Cross-correlation since inception of 0.13

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

'01-08-2007

'01-11-2007

'01-02-2008

'01-05-2008

'01-08-2008

'01-11-2008

'01-02-2009

'01-05-2009

'01-08-2009

BondsEquitiesCurrenciesPay-Off (Alpha)

-5%

0%

5%

10%

15%

20%

'01-08-2007

'01-11-2007

'01-02-2008

'01-05-2008

'01-08-2008

'01-11-2008

'01-02-2009

'01-05-2009

'01-08-2009

BondsEquitiesCurrenciesPay-Off (Alpha)

38Non contractual document

-8.00%

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

Jan-

08

Feb-

08

Mar

-08

Apr-

08

May

-08

Jun-

08

Jul-0

8

Aug-

08

Sep-

08

Oct

-08

Nov

-08

Dec

-08

HSBC Global Macro Credit Suisse Tremont Macro EUR Euribor 1 Month

90.00

95.00

100.00

105.00

110.00

Dec

-07

Jan-

08

Feb-

08

Mar

-08

Apr-

08

May

-08

Jun-

08

Jul-0

8

Aug

-08

Sep

-08

Oct

-08

Nov

-08

Dec

-08

HSBC Global Macro Credit Suisse Tremont Macro EUR Euribor 1 Month

2008 Monthly Return 2008 Cumulative Return

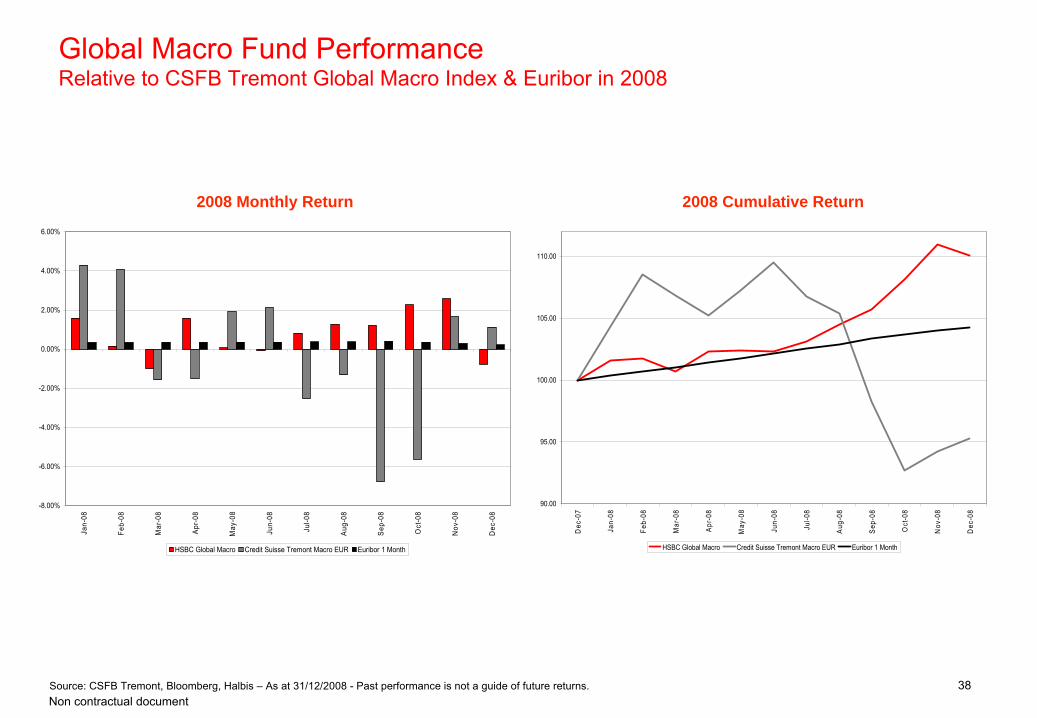

Global Macro Fund Performance Relative to CSFB Tremont Global Macro Index & Euribor

in 2008

Source: CSFB Tremont, Bloomberg, Halbis –

As at 31/12/2008 -

Past performance is not a guide of future returns.

39Non contractual document

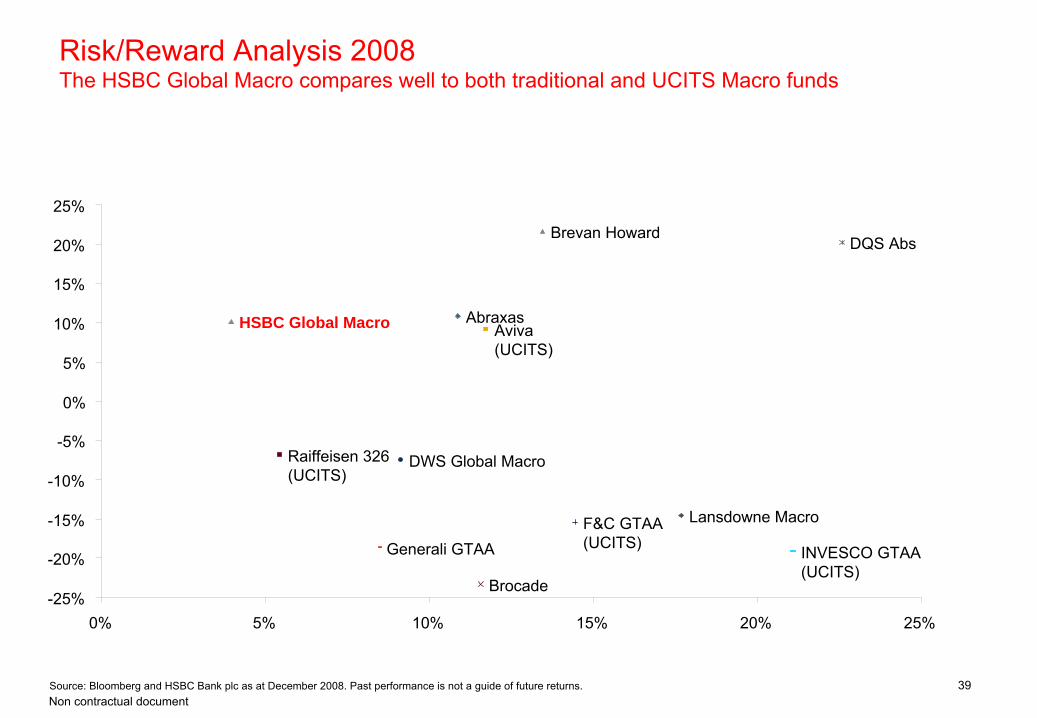

Risk/Reward Analysis 2008 The HSBC Global Macro compares well to both traditional and UCITS Macro funds

AbraxasAviva(UCITS)

Brevan

Howard

Brocade

DQS Abs

DWS Global Macro

F&C GTAA(UCITS)Generali

GTAA INVESCO GTAA(UCITS)

Lansdowne Macro

Raiffeisen

326 (UCITS)

HSBC Global Macro

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

0% 5% 10% 15% 20% 25%

Source: Bloomberg and HSBC Bank plc as at December 2008. Past performance is not a guide of future returns.

Appendix

41Non contractual document

Jim Dunsford, Co-Fund Manager

Jim Dunsford began his investment career in 1972 at Grieveson

Grant before joining the HSBC Group in 1978. He held a number of

positions before being promoted to global head of fixed income in 1994. He holds a Master’s degree from Cambridge University in Natural Sciences and carried out postgraduate research in

Management Development at Birkbeck

College, London University. He also holds a Certified Diploma in Accounting and Finance.

Guillaume Rabault, Co-Fund Manager

Guillaume Rabault began his investment career in 1991. Prior to joining HBSC Group in 2000, Guillaume worked for the French Ministry of Finance for nine years as an economist, researcher and head of the French National Quarterly Account. Guillaume holds a Master's degree from the engineering school Polytechnique

(France), a Master's degree in Economics and Statistics from the

business school ENSAE (France), and a Master's degree (DEA) in Economics and Politics from Ecole

Normale

Supérieure

(France).

Management Team Over 90 years

collective investment

experience

42Non contractual document

Benoit BelloneBenoit Bellone

is a senior economist in the strategy and quantitative analysis

team and has been working in the industry since 2001. Prior to joining Halbis in 2007, Benoit worked as an economist for OECD (France) and for the French Ministry of Finance Treasury

department. He holds a Master's degree in Economics and statistics from ENSAE (France), a Master's degree in Mathematics (DEA) from the University Paris IX -

Dauphine (France) and a BA in Economics from Ecole

Normale

Superieure

de Cachan

(France).

William Chan CFA William Chan is a Senior Fund Manager in the Global Macro team and has been working in the financial industry since 1990. He worked for the Mitsubishi Banking Corporation before joining the

HSBC Group in 1992. William has held a number of investment positions, primarily in TAA (tactical asset allocation) and FX risk management, before being promoted to Head of FX in 1998. He holds an MSc in Economics from the London School of Economics. A

CFA charter-holder, he is also a certified Financial Risk Manager (FRM).

Joe Little CFAJoe Little joined Halbis in 2007 and is a Fund Manager in the Global Macro team. He has been working in the industry since 2003 and previously worked for Cazenove

as a strategist focussing on equity markets and macro. He holds

a First in Economics from Bristol University, an MSc in Economics from Warwick University,

and is a CFA charterholder.

Emmanuel MichauxEmmanuel Michaux

is a fixed income and money market strategist in the strategy and quantitative analysis team and has been working in the industry since 2002. Prior to joining Halbis in 2006, Emmanuel worked as an economist and applied research fellow

for the French Ministry of Finance Treasury department in charge

of economic analysis and forecasts for France. He published his

work in academic journals. Emmanuel holds a Master's degree in Statistics and Economics from the engineering school ENSAE (France) and has a Master's degree in Econometrics (France).

Management Team Over 90 years

collective investment

experience

43Non contractual document

Important Information

The HSBC Global Investment Fund (‘GIF’) range is a Luxembourg domiciled SICAV and is regulated by the CSSF. The funds mentioned in this document may not be registered for sale or available in all jurisdictions. For available funds please contact your local HSBC office. HSBC Global Investment Funds range cannot be sold by anyone in any jurisdiction in which such offer or solicitation is not lawful or in which the person making such an offer or solicitation is not qualified to do so or to anyone to whom it is unlawful to make such offer or solicitation. All applications are made on the basis of the current HSBC Global Investment Funds Prospectus, simplified prospectus and most recent annual and semi-annual reports. These can be obtained on request and free of charge from HSBC Global Asset Management (UK) Limited or the local distributors. The value of investments may go down as well as up and you may not get back the full amount you invested. Where overseas investments are held the rate of exchange may cause the value of investments to go down as well as up. Markets in some countries can be described as ‘emerging markets’. Some of these may involve a higher risk than where an investment is within a more established market. Where a sub-fund invests predominately in one geographical area, any decline

in economic conditions may affect prices and the value of underlying investments. The securities representing interests in the HSBC Global Investment Funds range have not been and will not be registered under the US Securities Act of 1933 and will not be offered for sale or sold in the United States of

America, its territories or possessions and all areas subject to its jurisdiction, or United States person, except in a transaction which does not violate the Securities Law of the United States of America.This document is issued by HSBC Global Asset Management (UK) Limited, 8 Canada Square, Canary Wharf, London, E14 5HQ, UK. Authorised and regulated by the Financial Services Authority and registered as number 122335. ©

Copyright. HSBC Global Asset Management 2009. All Rights Reserved.This product is marketed in a sub-distributing capacity on a principal –

to –

principal basis by the HSBC Global Asset Management MENA, a unit that is part of HSBC Bank Middle East Limited, PO Box 66, Dubai, UAE, which is incorporated and regulated by the Jersey Financial Services Commission. Services are subject to the Bank’s terms and conditions. HSBC Bank Middle East Limited is a member of the HSBC Group. The information provided has not been prepared taking into account the particular investment objectives, financial situation and

needs of any particular investor. As a result, investors using this information should assess whether it is appropriate in the light of their own individual circumstances before acting on it. The information in this document is derived from sources believed to

be reliable, but which have not been independently verified. However, HSBC Bank Middle East Limited makes no guarantee of its accuracy and completeness and is not responsible for errors of transmission of factual or analytical data, nor shall HSBC Bank Middle East Limited be liable for damages arising out of any person’s reliance upon this information. All charts and graphs are from publicly available sources or proprietary data. The opinions in this document constitute the present judgment of the issuer, which is subject to change without notice.This document is neither an offer to sell, purchase or subscribe

for any investment nor a solicitation of such an offer. This document is intended for the use of institutional and professional customers and is not intended for

the use of private customers. This document is intended to be distributed in its entirety. No consideration has been given to the particular investment objectives, financial situation or particular needs of any recipient. Any transaction will be subject to HSBC Bank’s Terms of Business.17285/ME/0909