housing in fingal a market perspective. housing in fingal a market perspective housing supply...

TRANSCRIPT

Housing in Fingal A MARKET PERSPECTIVE

Housing in Fingal A Market Perspective

Housing Supply Capacity Survey recently undertaken by Society of

Chartered Surveyors with FutureAnalytics

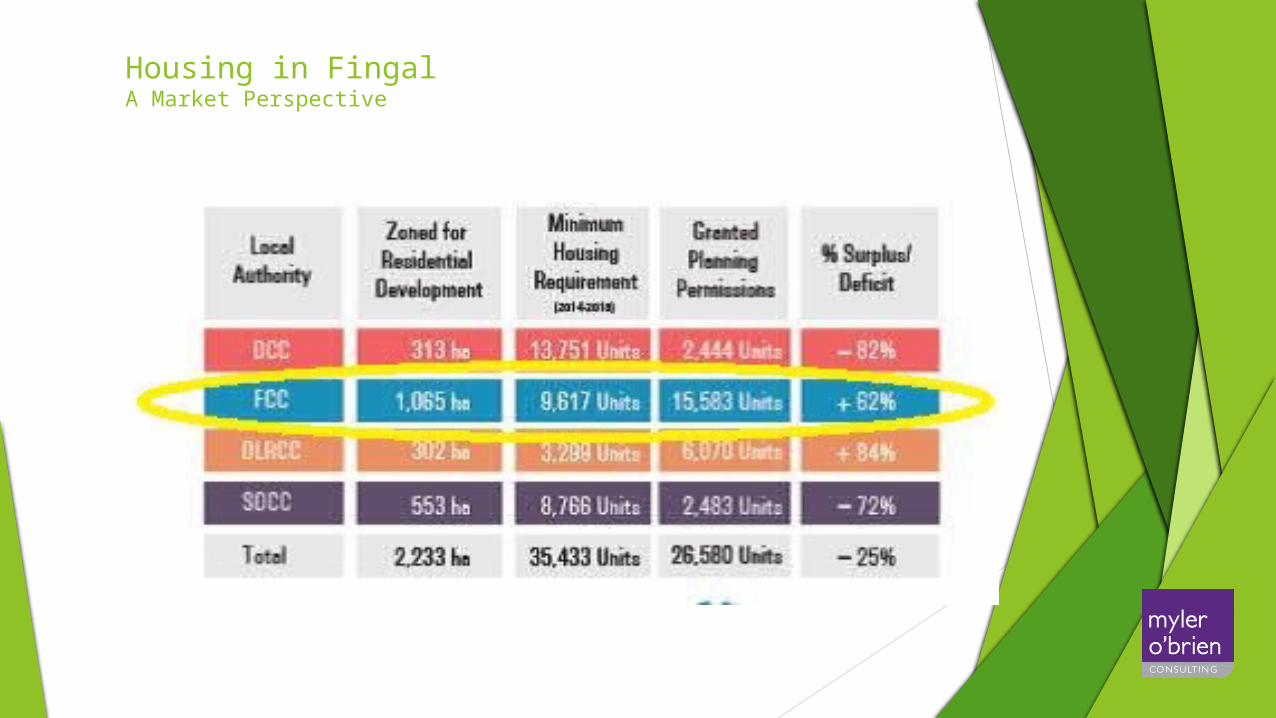

Identified 2,233 hectares of land zoned and potentially available for

residential development, 2.4% of the total land area in the Dublin Region

This zoned land can deliver approximately 102,500 additional

housing units under the minimum recommended density

This would potentially house 269,000 additional persons

There is a minimum requirement for 35,433 units between 2014 – 2018

Planning permission granted for 26,580 units

Housing in FingalA Market Perspective

Housing in FingalA Market Perspective

Existing Fingal stock of 103,295 housing units – 20% of current total Dublin stock – and a population of 273,991 (Census 2011)

Almost 48% of total Dublin land area

Strong population growth of 13.8% 2006 – 2011 (Census 2011)

Average Household Size 2.67 persons (Census 2011)

1,065 hectares of zoned and potentially available land – almost 50% of all Dublin area zoned lands

Positive future development proposition

Housing in FingalA Market Perspective

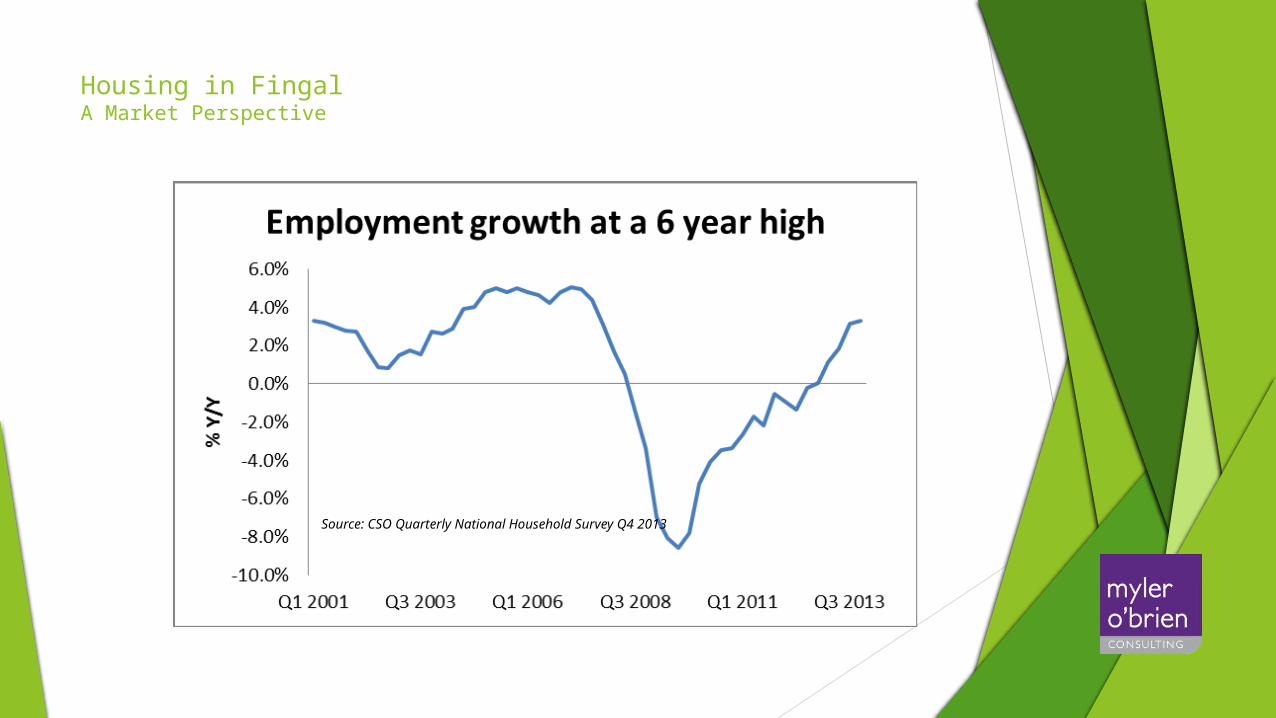

Source: CSO Quarterly National Household Survey Q4 2013

Housing in FingalA Market Perspective

Housing in FingalA Market Perspective

Housing in FingalA Market Perspective

Planning Permissions already granted

Land Area – 231 Hectares

No. of Units – 15,583 Units

Breakdown –

- 1,005 One Bed Units

- 6,502 Two Bed Units

- 4,765 Three Bed Units

- 2,365 Four Bed Units

- 684 Five Bed Units

Housing in FingalA Market Perspective

Housing in FingalA Market Perspective

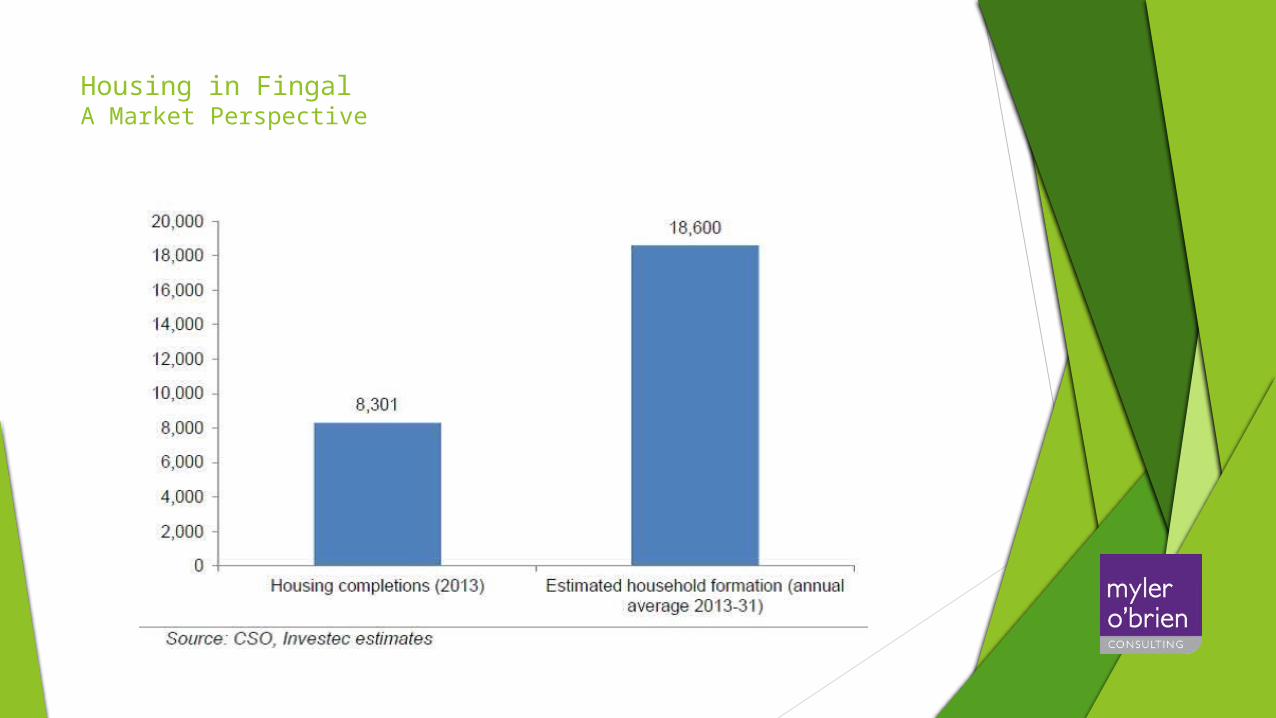

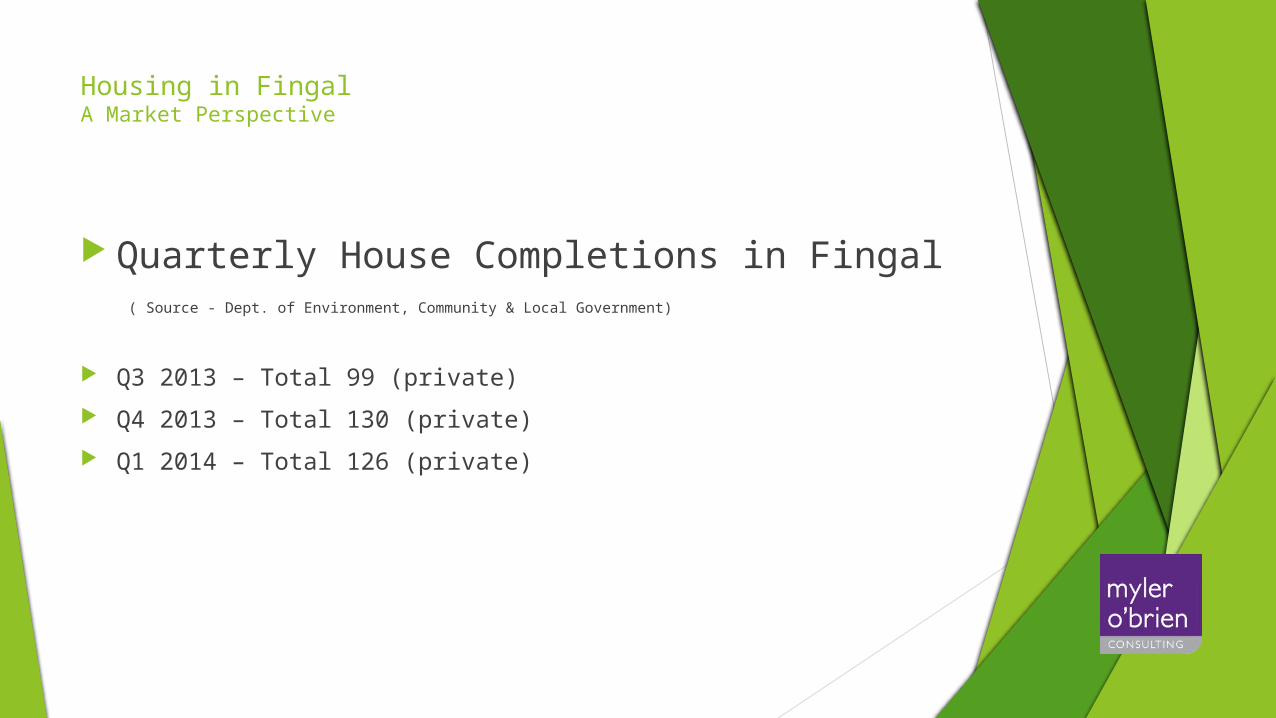

Quarterly House Completions in Fingal ( Source - Dept. of Environment, Community & Local Government)

Q3 2013 – Total 99 (private)

Q4 2013 – Total 130 (private)

Q1 2014 – Total 126 (private)

Housing in FingalA Market Perspective

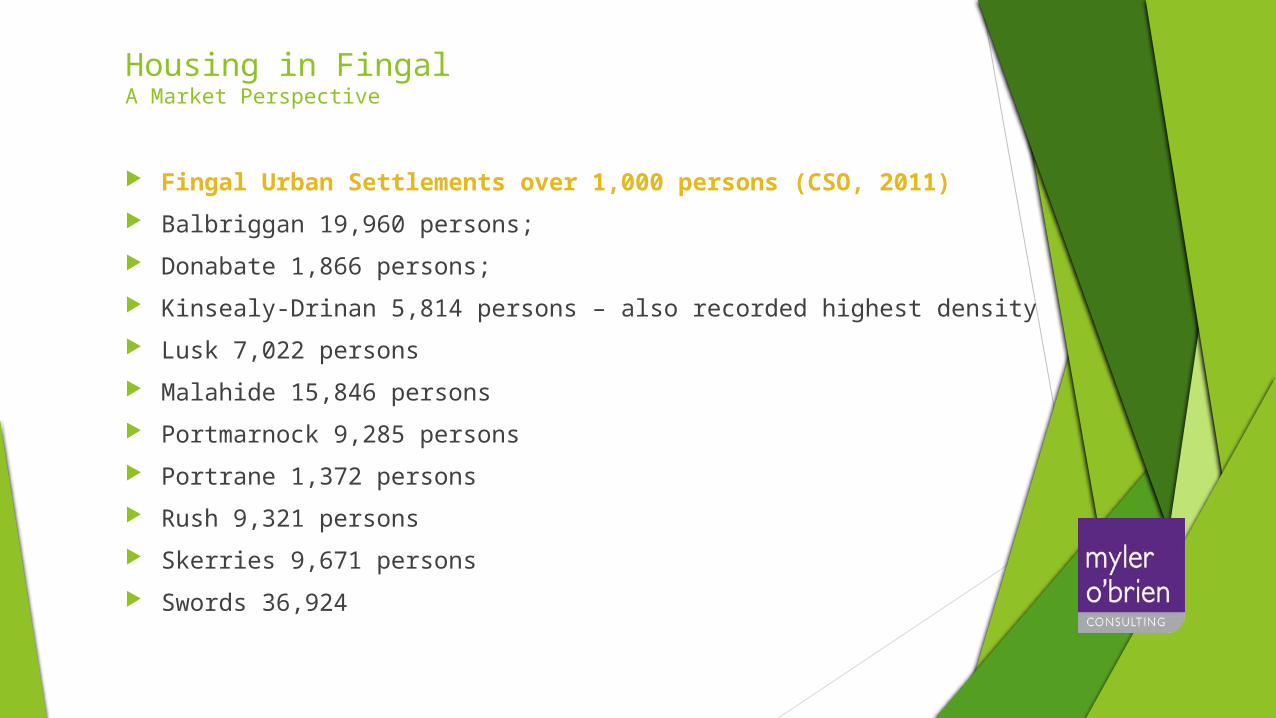

Fingal Urban Settlements over 1,000 persons (CSO, 2011)

Balbriggan 19,960 persons;

Donabate 1,866 persons;

Kinsealy-Drinan 5,814 persons – also recorded highest density

Lusk 7,022 persons

Malahide 15,846 persons

Portmarnock 9,285 persons

Portrane 1,372 persons

Rush 9,321 persons

Skerries 9,671 persons

Swords 36,924

Housing in FingalA Market Perspective

What attracts occupiers to Fingal – Fluirse Talaimh is Mara (Abundance of Land & Sea)

Infrastructure leads development

Dublin Airport, M1, M2, M3, M50, direct Link to Port Tunnel, Dart, mainline train links, QBCs

Metro North Project?

Broad spectrum of housing type from heavily populated areas to network of small villages to individual rural houses

Good local road network to support car-commuting population

Pressure on agricultural hinterland for development in future

Housing in FingalA Market Perspective

Housing in FingalA Market Perspective

Supply of new housing is affected by the availability and cost of

Land

Credit (both Acquisition & Development Finance)

Skilled labour and cost of materials

Infrastructure provision

Planning Constraints and Building Regulations

Council’s ability to influence some of these factors in order to encourage efficient and timely delivery of new housing units

Housing in FingalA Market Perspective

EXAMPLE

Build Cost for 3 Bed Semi-Detached House – €145,000 total

Local Authority Levies – c. €21,000* - 15% of build cost

Average Price - €189,000

Developer’s Profit @ 15% - €22,000

VAT @ 13.5% of sale price - €23,000

€43,000 / 23% of House Price in Tax/Levies

* Varies depending on Local Authority levy rates & Part V contribution

Housing in FingalA Market Perspective

EXAMPLE

Apartment Development not viable based on current prices

NAMA’s Impact on Housing Costs – January 2014

Per Unit Development Cost

- €216,302 (Block of 30)

- €241,659 (Block of 90)

- Sales Prices in Dublin (MyHome.ie Q2 2014)

- 1 Bed Apartment - €139,000

- 2 Bed Apartment - €200,000

Housing in FingalA Market Perspective

Who will build the new housing stock?

Are there any roadblocks to development?

Influence of other stakeholders in the market – NAMA, non-NAMA Banks, Receivers

Vacant site levy to discourage land-banking/hoarding?

New approaches to ensure completion of schemes?

New Part V arrangements

Housing in FingalA Market Perspective

New players in the markets – Property Funds and REITS

Medium to long term Build to Rent investment strategy with professional management

Different design requirements to standard apartment development

Dual orientation, size, central cores, utility and storage areas, retail use at ground floor level, parking – Build to Rent represents new unit type to market

Strong emphasis on finish for durability and quality offering to end user

Revised Tenure – Long Term Rental Agreements with focus on rights and responsibilities of both parties

Housing in FingalA Market Perspective

Post Priory Hall – Buyers need confidence

in Regulatory system

Unfinished Estates/Pyrite/Flood Risk

Recent legislation (Multi-Unit Dwellings act) has provided more control to owners of the management of scheme

Work still needs to be done to convince people to live in high density schemes

Role for Local Authority in developing communities once construction completed?

Engage with industry for opinion and feedback?

Housing in FingalA Market Perspective

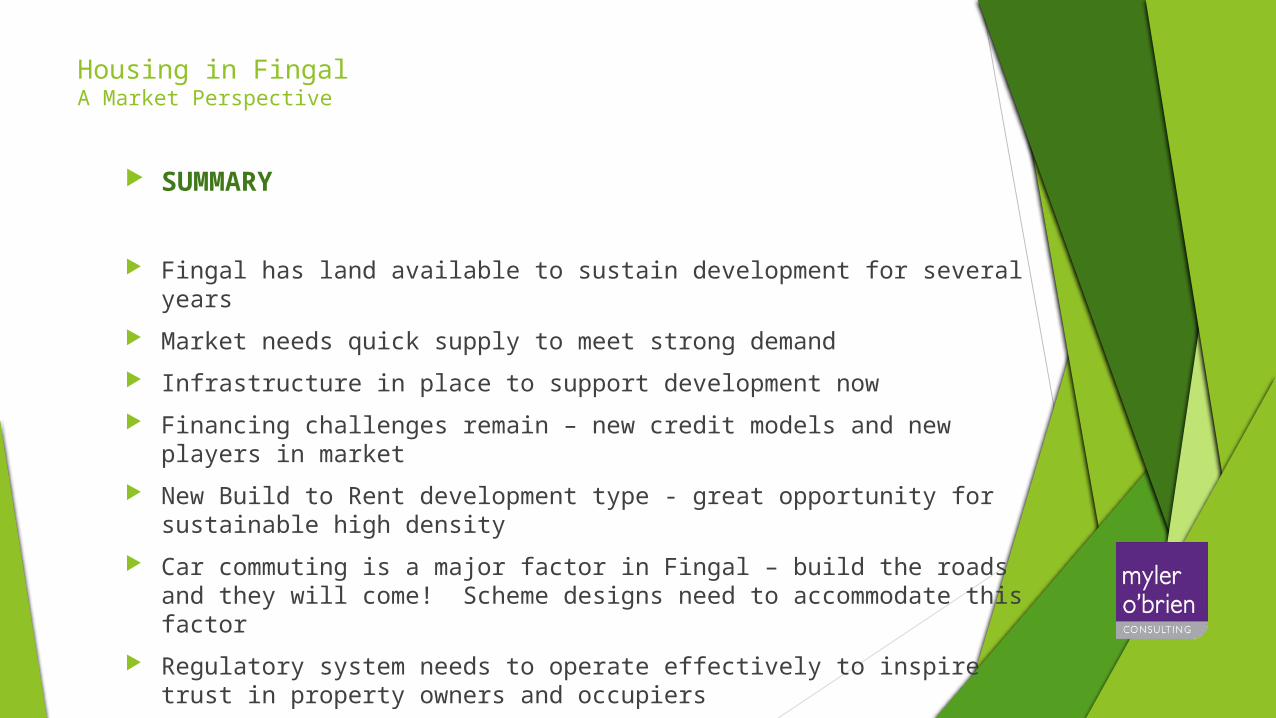

SUMMARY

Fingal has land available to sustain development for several years

Market needs quick supply to meet strong demand

Infrastructure in place to support development now

Financing challenges remain – new credit models and new players in market

New Build to Rent development type - great opportunity for sustainable high density

Car commuting is a major factor in Fingal – build the roads and they will come! Scheme designs need to accommodate this factor

Regulatory system needs to operate effectively to inspire trust in property owners and occupiers

Housing in FingalA Market Perspective

THANK YOU

ANY QUESTIONS?