home buyer guide

TRANSCRIPT

Coldwell Banker® Homebuyer GuideENTER YOUR

COMPANY DBA

HERE

Buying Your New Home

When using a Coldwell

Banker® Sales Associate,

you can be confident your

search for a new home will

be successful.

Finding and Financing A Home Made Simple

ENTER YOUR

COMPANY DBA

HERE

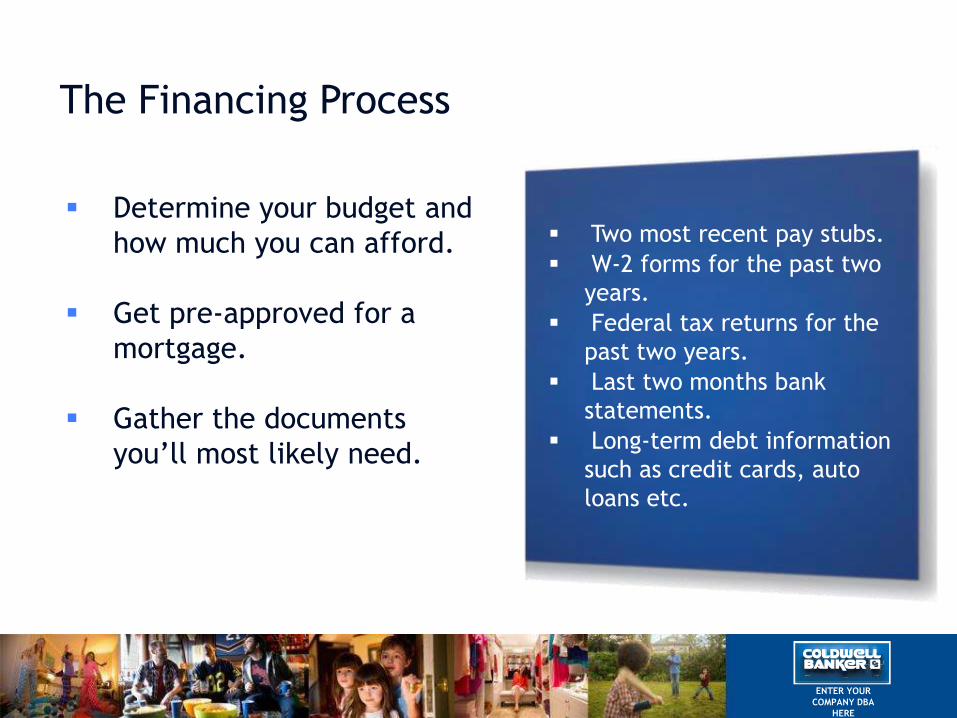

Determine your budget and

how much you can afford.

Get pre-approved for a

mortgage.

Gather the documents

you’ll most likely need.

Two most recent pay stubs.

W-2 forms for the past two

years.

Federal tax returns for the

past two years.

Last two months bank

statements.

Long-term debt information

such as credit cards, auto

loans etc.

The Financing Process

ENTER YOUR

COMPANY DBA

HERE

A lender will check your credit to see if you’re a good candidate for a

loan.

If your credit rating is poor, there are things you can do to improve it.

Make sure the report is correct.

If not, call to fix it.

Begin to pay your bills on time.

Use two to four credit cards so you

can keep track of them.

Keep a separate checking and

savings account.

Keep the same job for a few years

Getting Approved

ENTER YOUR

COMPANY DBA

HERE

Pre-Approved vs. Pre-Qualified

Pre-Approved: confirmation the

lender will give you a commitment

to support your purchase.

Pre-Qualified: an estimate of what

you can afford.

Being pre-approved makes you a

more attractive candidate to the

seller when making an offer.

ENTER YOUR

COMPANY DBA

HERE

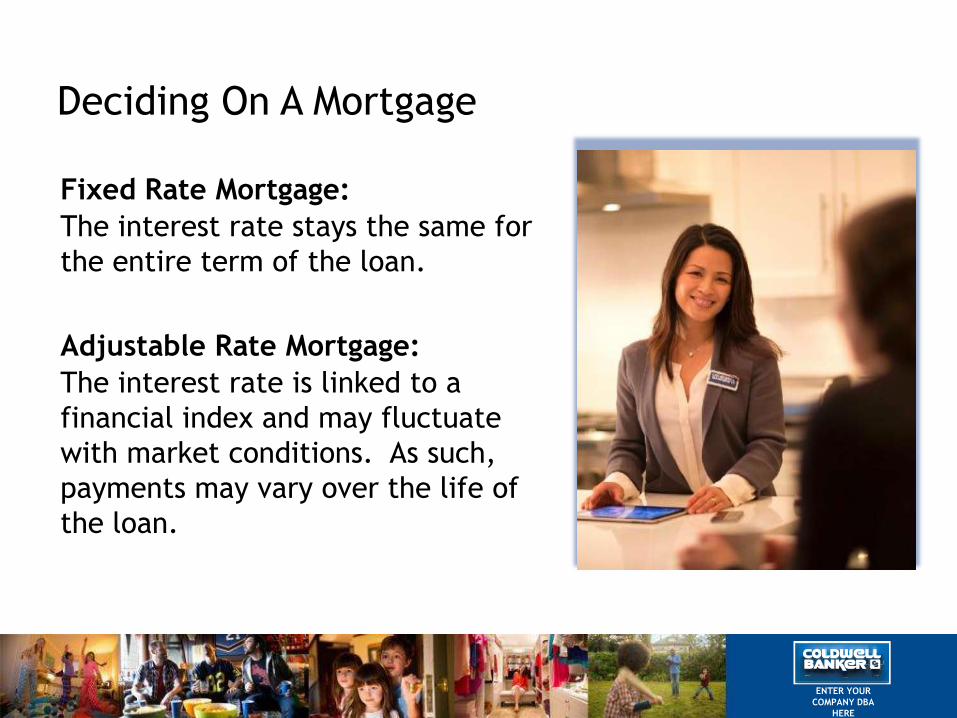

Fixed Rate Mortgage:

The interest rate stays the same for

the entire term of the loan.

Adjustable Rate Mortgage:

The interest rate is linked to a

financial index and may fluctuate

with market conditions. As such,

payments may vary over the life of

the loan.

Deciding On A Mortgage

ENTER YOUR

COMPANY DBA

HERE

Calculating Your Budget

To estimate your budget, add up your

total financial worth and then subtract

all the cost in the purchase.

Some expenses you may carry:

Down payment

Mortgage

Insurance

Taxes

Points

Attorney’s fees

ENTER YOUR

COMPANY DBA

HERE

The Fun Begins

Things to consider:

Size of property

Type of neighborhood you desire

Quality of school system

Nearby public transportation

Urban or suburban

ENTER YOUR

COMPANY DBA

HERE

Multiple Listings, Open Houses & Special

Features

As your Coldwell Banker®

Sales Associate, I can show

you every home available

on the market that meets

your specific needs.

ENTER YOUR

COMPANY DBA

HERE

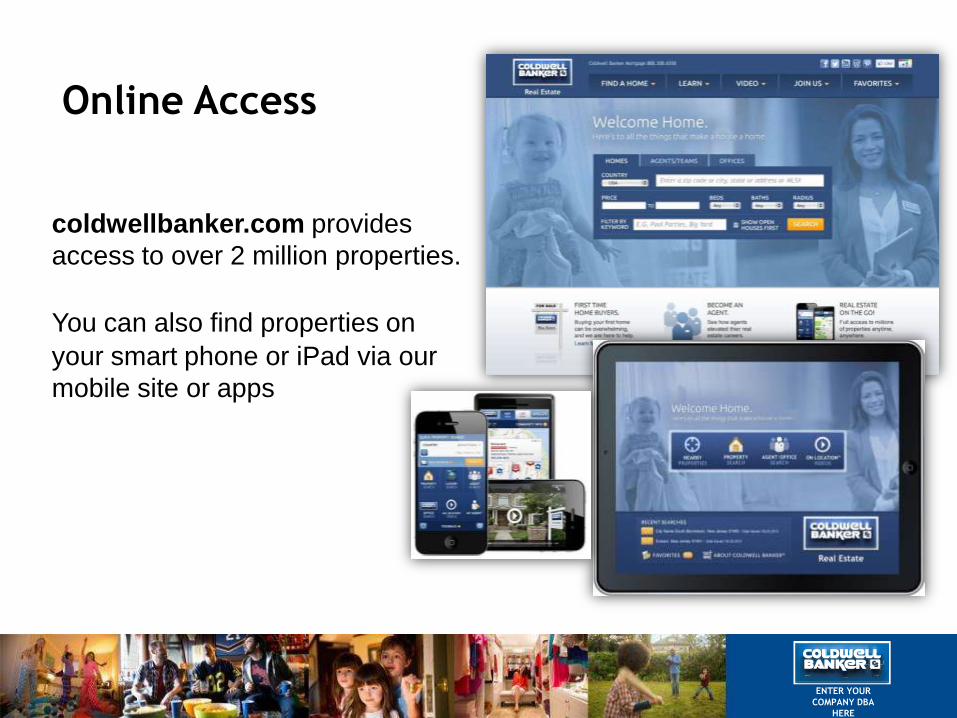

Online Access

coldwellbanker.com provides

access to over 2 million properties.

You can also find properties on

your smart phone or iPad via our

mobile site or apps

ENTER YOUR

COMPANY DBA

HERE

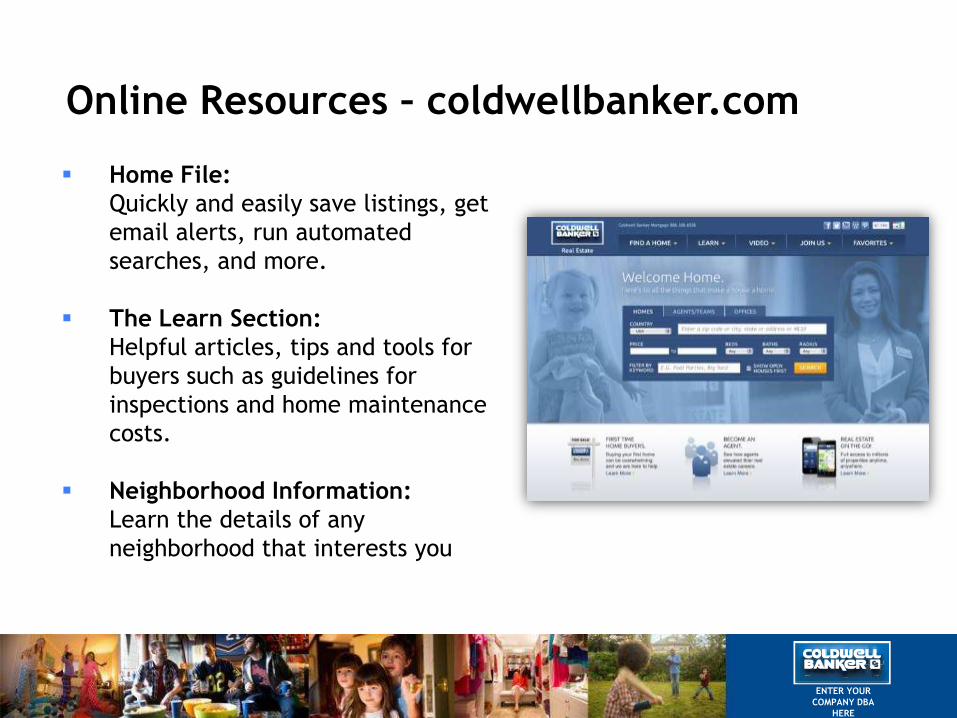

Online Resources – coldwellbanker.com

Home File:

Quickly and easily save listings, get

email alerts, run automated

searches, and more.

The Learn Section:

Helpful articles, tips and tools for

buyers such as guidelines for

inspections and home maintenance

costs.

Neighborhood Information:

Learn the details of any

neighborhood that interests you

ENTER YOUR

COMPANY DBA

HERE

Writing the Offer

Once you’ve found the perfect

home, I will write up the offer

and ensure all paperwork and

activities are completed so you

can close on your property.

ENTER YOUR

COMPANY DBA

HERE

The Closing

This is the meeting where

the transaction is finalized. I

will guide you through all

closing procedures to make

your home officially yours.

ENTER YOUR

COMPANY DBA

HERE

Enjoy Your New Home

ENTER YOUR

COMPANY DBA

HERE

ENTER YOUR

COMPANY DBA

HERE

©2013 Coldwell Banker Real Estate LLC. A Realogy Company. All Rights Reserved. Coldwell Banker Real Estate LLC fully supports the principles of the Fair Housing Act and the Equal Opportunity Act. Each Office is

Independently Owned and Operated. Coldwell Banker® and the Coldwell Banker Logo are registered service marks owned by Coldwell Banker Real Estate LLC. Each agent and broker is responsible for complying with

any consumer disclosure laws or regulations.