holiday spend analysis - first data spend analysis - mid-season update | december 2017 | ©first...

TRANSCRIPT

HOLIDAY SPEND ANALYSIS - MID-SEASON UPDATE | DECEMBER 2017 | ©FIRST DATA CORPORATION. ALL RIGHTS RESERVED.

1

Holiday Spend Analysis Mid-Season Update

Information and Analytics December 2017

HOLIDAY SPEND ANALYSIS - MID-SEASON UPDATE | DECEMBER 2017 | ©FIRST DATA CORPORATION. ALL RIGHTS RESERVED.

2

Executive Summary – Mid-Season Update

Overall growth for Mid-Season analysis (excluding gasoline) was 6.0%, eclipsing last year’s overall growth of 3.7%

Retail growth was 5.4%, more than doubling last year’s retail growth of 2.0%

Retail eCommerce sales growth continues to out-pace brick and mortar growth, ending at 10.5% vs. 3.9% for Brick & Mortar

eCommerce continues to grow fastest in Specialty Retail, Electronics, and Building Materials.

Electronics and Building Materials have also increased their share of total Brick & Mortar spend, taking most of this share from Clothing and Sporting Goods.

Houston continues to recover from Hurricane Harvey with the strongest Retail growth of the largest US cities at 17.5%. Houston's largest growth was in Building Materials (33%) and Furniture (22.6%)

Southwest and West Regions had the strongest US growth, while Mid-Atlantic had the weakest

Los Angeles (4.8%), San Francisco (7.4%) and Seattle (8.3%) drove overall sales growth for the West region, while Dallas (4.4%), Houston (10.6%), and San Antonio (5.5%) drove the Southwest region

Largest RETAIL average ticket was $89.33 in New York, followed by New Hampshire at $85.48 and Colorado at $85.03. Smallest average RETAIL ticket was $41.99 in Nebraska, followed by Mississippi at $48.29 and West Virginia at $51.63

Biggest average ticket growth was 6.7% in Utah, 6.0% in Maine, and 5.7% in Maryland

Louisiana is the only state that shrunk YOY in average ticket size, losing 1.9%

Total US Level Observations State & MSA Level Observations

HOLIDAY SPEND ANALYSIS - MID-SEASON UPDATE | DECEMBER 2017 | ©FIRST DATA CORPORATION. ALL RIGHTS RESERVED.

3

Spending Growth: Pre-Holiday, Thanksgiving + Black Friday, Thanksgiving to Cyber Monday, Mid-Season We saw an impressive pickup in 2017 across pre-holiday, TH+BF, and through to Cyber Monday

Total Spend YoY Growth

4.9%

2.8% 3.4%

5.7% 5.2%

10.6%

7.8%

11.9%

7.9% 7.5%

5.6%

11.3%

2.7% 2.7% 3.7%

6.0%

0%

5%

10%

15%

2014 2015 2016 2017

Pre-Holiday TH + BF TH to CM MIDSEASON

Note: Figures exclude gasoline stations. Pre-Holiday defined as the approximate 3-week period, starting November 1 and continuing through to the day before Thanksgiving. Source: First Data aggregated data.

Pre-Holiday saw a big increase in 2017 vs. prior years

The TH+BF Holiday period saw the strongest growth rate in several years

The 5 day period of TH to CM saw sustained momentum

The 2017 Mid-Season results are the strongest of the last 4 years

HOLIDAY SPEND ANALYSIS - MID-SEASON UPDATE | DECEMBER 2017 | ©FIRST DATA CORPORATION. ALL RIGHTS RESERVED.

4

3.4%

1.7% 1.6%

5.9%

3.5%

9.4% 9.0% 9.3%

5.3% 6.3%

5.8%

8.0%

1.8% 2.4% 2.0%

5.4%

0%

5%

10%

15%

2014 2015 2016 2017

Pre-Holiday TH + BF TH to CM MIDSEASON

Spending Growth: Pre-Holiday, Thanksgiving + Black Friday, Thanksgiving to Cyber Monday, Mid-Season We saw an impressive pickup in 2017 across pre-holiday, TH+BF, and through to Cyber Monday

Note: Figures exclude gasoline stations. Pre-Holiday defined as the approximate 3-week period, starting November 1 and continuing through to the day before Thanksgiving. Source: First Data aggregated data.

Retail Spend YoY Growth

Pre-Holiday saw a big increase in 2017 vs. prior years

The TH+BF Holiday period saw continued strong growth vs. tough prior year comps as well

Overall, retail growth during the 5day period of TH to CM was strong (+8.0%)

The 2017 Mid-Season results are the strongest of the last 4 years

HOLIDAY SPEND ANALYSIS - MID-SEASON UPDATE | DECEMBER 2017 | ©FIRST DATA CORPORATION. ALL RIGHTS RESERVED.

5

Transactions, Average Ticket and Sales: Mid-Season Holiday Spending eCommerce spending appears to be trickling down to include more everyday items

Note: Figures exclude gasoline stations. Source: First Data aggregated data.

Retail Sector – Transactions, Average Ticket and Sales Trends YoY Growth

2.2%

13.0%

3.9% 2.0%

-2.3%

1.7% 4.0%

10.5%

5.4%

-10%

-5%

0%

5%

10%

15%

20%

MidSeason 2017Brick & Mortar

MidSeason 2017eCommerce

MidSeason 2017Total

Transactions Average Ticket Sales • As spending cools off, we see the Brick & Mortar growth has settled around 4%. Average ticket and transactions have both grown at comparable pace within Brick & Mortar.

• eCommerce continues to see an explosion of transaction growth, but we also see the average ticket size is decreasing. More evidence that consumers are likely stocking their baskets with more routine replenishment of everyday household items.

Key Takeaways

HOLIDAY SPEND ANALYSIS - MID-SEASON UPDATE | DECEMBER 2017 | ©FIRST DATA CORPORATION. ALL RIGHTS RESERVED.

6

Total Spend Growth by Category: Mid-Season Electronics & Appliances has remained the strongest growth category throughout the holiday season thus far

Note: Figures exclude gasoline stations. Source: First Data aggregated data.

Growth Breakdown by Retail Category

9.3% 6.9%

5.8%

3.2% 2.3% 1.9%

-0.9%

Electronics &Appliances

Building Materials& DIY

SpecialtyRetailers

Furniture &Home Furnishings

Clothing &Accessories

GeneralMerchandise

Sporting Goods/Hobby/Books/Music

YoY Growth

Total Retail 5.4%

HOLIDAY SPEND ANALYSIS - MID-SEASON UPDATE | DECEMBER 2017 | ©FIRST DATA CORPORATION. ALL RIGHTS RESERVED.

7

Average Ticket Size by Category: Mid-Season Building Materials/DIY has steadily drawn larger basket sizes throughout the holiday season, and is heavily influenced by eCommerce average basket size, which is more than twice that of a typical Brick & Mortar basket.

Note: Figures exclude gasoline stations. Source: First Data aggregated data.

4.6%

2.0%

1.0% 0.7% 0.4% 0.1%

-0.9%

BuildingMaterials/DIY

Clothing &Accessories

Furniture/Home Furnishings

GeneralMerchandise

SpecialtyRetailers

Electronics &Appliances

Sporting Goods/Hobby/Books/Music

Ticket Growth by Retail Category YoY Growth

Total Retail 1.7%

HOLIDAY SPEND ANALYSIS - MID-SEASON UPDATE | DECEMBER 2017 | ©FIRST DATA CORPORATION. ALL RIGHTS RESERVED.

8

Average Ticket Size by Category: Mid-Season Building Materials and General Merchandise see the biggest difference between eCommerce and Brick & Mortar average tickets

Note: Figures exclude gasoline stations. Source: First Data aggregated data.

$85.03 $81.49

$233.93

$36.85

$55.57

$154.38

$80.50

$192.08

$111.13

$274.21

$95.20 $103.91

$92.24 $86.75

BuildingMaterials/DIY

Clothing &Accessories

Furniture/Home Furnishings

GeneralMerchandise

SpecialtyRetailers

Electronics &Appliances

Sporting Goods/Hobby/Books/Music

Brick & MortareCommerce

Average Ticket Size by Retail Category

HOLIDAY SPEND ANALYSIS - MID-SEASON UPDATE | DECEMBER 2017 | ©FIRST DATA CORPORATION. ALL RIGHTS RESERVED.

9

Total Spending by Channel: Mid-Season eCommerce continued to grow its share of total commerce in 2017

Note: Figures exclude gasoline stations. Source: First Data aggregated data.

Brick & Mortar vs. eCommerce

84% 82% 75% 76% 71% 72% 71%

16% 18% 25% 24% 29% 28% 29%

2014TH+BF

2015TH+BF

2016TH+BF

2016TH to CM

2017TH+BF

2017TH to CM

2017MIDSEASON

Brick & Mortar eCommerce

Percent of Spending by Channel

HOLIDAY SPEND ANALYSIS - MID-SEASON UPDATE | DECEMBER 2017 | ©FIRST DATA CORPORATION. ALL RIGHTS RESERVED.

10

Spend Growth by Category: Mid-Season

Note: Figures exclude gasoline stations. Source: First Data aggregated data.

Brick & Mortar vs. eCommerce – Selected Categories YoY Growth

Brick & Mortar eCommerce Total

2016 2017 2016 2017 2016 2017

Building Materials & DIY 9.4% 6.1% 13.2% 12.6% 9.8% 6.9%

Clothing & Accessories -1.7% 1.3% 2.5% 6.3% -0.9% 2.3%

Electronics & Appliances 5.6% 8.7% 11.3% 11.8% 7.0% 9.3%

Furniture & Home Furnishings 1.4% 0.9% 8.5% 8.7% 3.2% 3.2%

General Merchandise -5.3% 1.6% 23.5% 9.0% -2.8% 1.9%

Specialty Retailers -1.4% 4.2% 4.9% 10.0% -0.1% 5.8%

Sporting Goods/Hobby/Books/Music -8.2% -1.8% 14.8% 4.1% -0.8% -0.9%

Total Retail 0.1% 4.0% 9.0% 10.5% 2.0% 5.4%

Notable acceleration Notable deceleration

HOLIDAY SPEND ANALYSIS - MID-SEASON UPDATE | DECEMBER 2017 | ©FIRST DATA CORPORATION. ALL RIGHTS RESERVED.

11

Regional Spending

HOLIDAY SPEND ANALYSIS - MID-SEASON UPDATE | DECEMBER 2017 | ©FIRST DATA CORPORATION. ALL RIGHTS RESERVED.

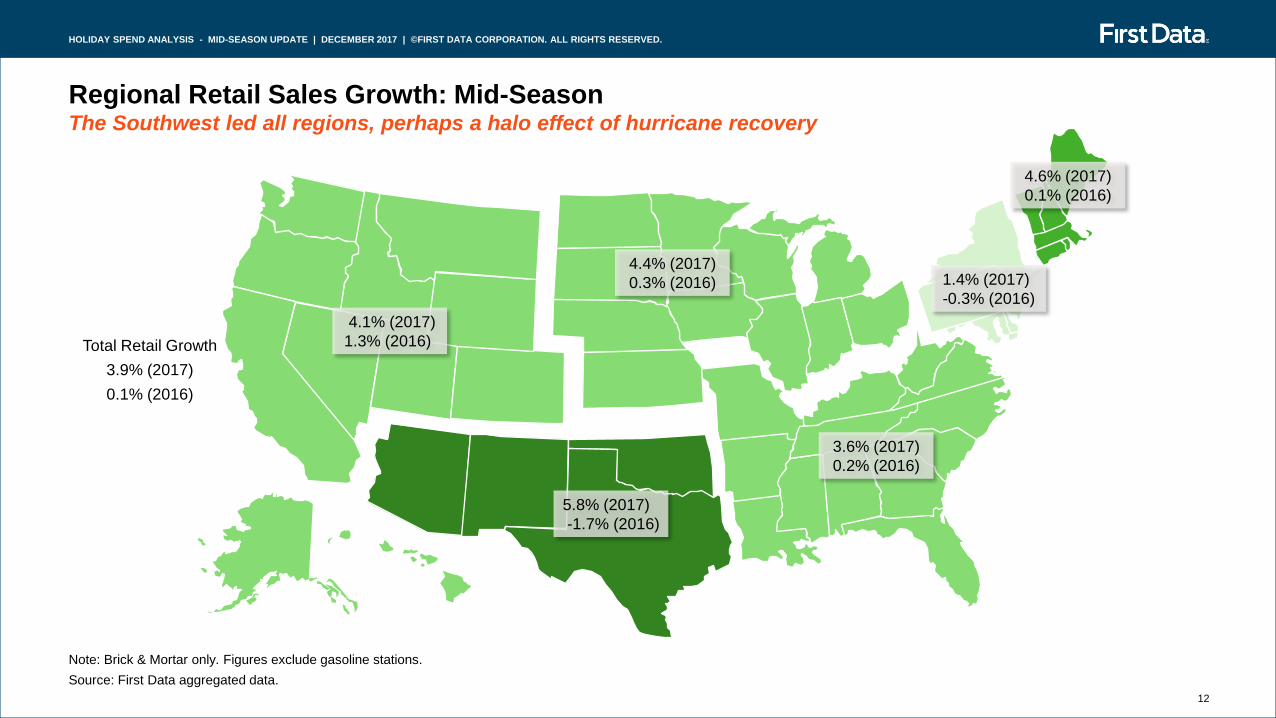

12

Regional Retail Sales Growth: Mid-Season The Southwest led all regions, perhaps a halo effect of hurricane recovery

Note: Brick & Mortar only. Figures exclude gasoline stations. Source: First Data aggregated data.

Total Retail Growth 3.9% (2017) 0.1% (2016)

4.4% (2017) 0.3% (2016)

3.6% (2017) 0.2% (2016)

5.8% (2017) -1.7% (2016)

4.1% (2017) 1.3% (2016)

4.6% (2017) 0.1% (2016)

1.4% (2017) -0.3% (2016)

HOLIDAY SPEND ANALYSIS - MID-SEASON UPDATE | DECEMBER 2017 | ©FIRST DATA CORPORATION. ALL RIGHTS RESERVED.

13

Top MSA Retail Sales Growth: Mid-Season Among the largest US cities, Houston and Miami lead in brick & mortar retail sales growth

Note: Brick & Mortar only. Figures exclude gasoline stations. Source: First Data aggregated data.

Total Retail Growth 3.9% (2017) 0.1% (2016)

Ttl Midwest: 4.4% Chicago: 0.1%

Ttl South: 3.6% Atlanta: 1.5% Miami: 7.5%

Ttl Southwest: 5.8% Houston: 17.5% Dallas: 1.0%

Ttl West: 4.1% LA: 3.7% SF: 5.2%

Ttl New England: 4.6% Boston: 4.4%

Ttl Mid Atlantic: 1.4% New York: 2.7% Philadelphia: 3.8% Washington DC: 1.4%

HOLIDAY SPEND ANALYSIS - MID-SEASON UPDATE | DECEMBER 2017 | ©FIRST DATA CORPORATION. ALL RIGHTS RESERVED.

14

Methodology

All data is proprietary transaction data from First Data’s systems

Our analysis includes all card-based forms of payment and is based on actual, same-store sales activity

We have selected 1.3MM merchants’ POS activity as a representative sample:

― 1.1MM Brick & Mortar

― 200K eCommerce

Selection criteria included all merchants with 13 months of consecutive activity since October 2016

Additional filtering parameters were applied to exclude merchants disproportionately impacted by non-economic activities (i.e. natural disaster)

All growth rates reflect a year-over-year basis

Pre-Holiday dates include 11/02–11/23/2016 (prior year) and 11/01–11/22/2017 (current year)

Thanksgiving and Black Friday comparisons covered 11/24–11/25/2016 (prior year) and 11/23–11/24/2017 (current year)

Thanksgiving to Cyber Monday comparisons covered 11/24-11/28/2016 (prior year) and 11/23-11/27/2017 (current year)

Mid-Season comparisons covered 10/29-12/12/2016 (prior year) and 10/28-12/11/2017 (current year)

HOLIDAY SPEND ANALYSIS - MID-SEASON UPDATE | DECEMBER 2017 | ©FIRST DATA CORPORATION. ALL RIGHTS RESERVED.

15