historic rehabilitation tax credits federal incentives for preservation

TRANSCRIPT

Historic Rehabilitation Tax Credits

Federal Incentives for Preservation

Program Benefit

• 20% of qualified rehabilitation costs available as credit (dollar for dollar reduction in tax)

• Credit available to owners of the property at the time project is completed

Building must be depreciable

• Income producing• Not owner-occupied home

Property must be a certified historic building

• Individually listed in the National Register

or• A contributing building in a National

Register historic district or an NPs certified local district

Rehabilitation must be “substantial”

• Cost of work done in a 24-month period must exceed the greater of:– the adjusted basis in the building at the

beginning of the project or – $5,000

Project must be a certified rehabilitation

• Meets the Secretary of the Interior’s Standards for Rehabilitation

• Evaluation and determination by National Park Service

IRS Provisions Affecting Use of the Credit

• At Risk Rules– Credit available to investors who are “at risk” for the

investment.

• Passive Activity Limitation– Credit from “passive” sources may not be used to offset

tax liability from “active:” sources.

• Government and Tax-Exempt Use– No credit with disqualified lease for > 50% of property

Tax Incentives for West Virginians

• West Virginia state income tax credit for the rehabilitation of historic income producing properties.

– Under the provisions of West Virginia State Code §11-21-8a, there is a state income tax credit equal to 10% of the qualified rehabilitation expenditures.

Tax Incentives for West Virginians

• West Virginia state income tax credit for the rehabilitation of historic residential properties

– This credit is equal to 20% of the eligible rehabilitation expenses and is taken directly against the homeowner’s state tax burden.

Expenses that are Not Eligible• Costs of acquiring the building or interest

therein • Enlargement costs which expand the total

volume of the existing building. (Interior remodeling is not considered enlargement.)

• Expenditures attributable to work done to facilities related to a building such as parking lots, sidewalks and landscaping.

• New building construction costs • Appliances & Cabinets • Carpeting (if tacked in place and not glued) • Decks (not part of original building) • Demolition costs (removal of a building on

property site) • Enlargement costs (increase in total volume) • Fencing & landscaping• Feasibility studies

• Financing fees • Furniture• Leasing expenses • Moving (building) costs (if part of

acquisition) • Outdoor lighting remote from building • Parking lot • Paving • Planters • Porches and Porticos (not part of original

building) • Retaining walls • Sidewalks • Signage • Storm sewer construction costs • Window treatments

Eligible Rehabilitation Expenses

Any expenditure for a structural component of a building. • Structural components include:

– walls – partitions – floors – ceilings – Permanent coverings such as paneling

or tiling – windows – doors – components of central air conditioning

or heating systems – plumbing and plumbing fixtures – electrical wiring and lighting fixtures – chimneys

– stairs – escalators – elevators – sprinkling systems – fire escapes – other components related to operation

or maintenance of the building • Construction period interest and taxes • Architect fees • Engineering fees • Construction management costs • Reasonable developer fees • Other fees paid that would normally be

charged to a capital account

Certified Rehabilitation

• IRS code: “certified by the Secretary of the Interior as being consistent with the historic character of the property.”

• NPS regulations: Secretary of the Interior’s Standards for Rehabilitation

• NPS technical guidance publications:Guidelines for Rehabilitating Historic Buildings

Rehabilitation process

• Returns a property to a state of utility through repair or alteration

• Makes possible a contemporary use• Preserves portions and features that are

significant to property’s historic, architectural and cultural values

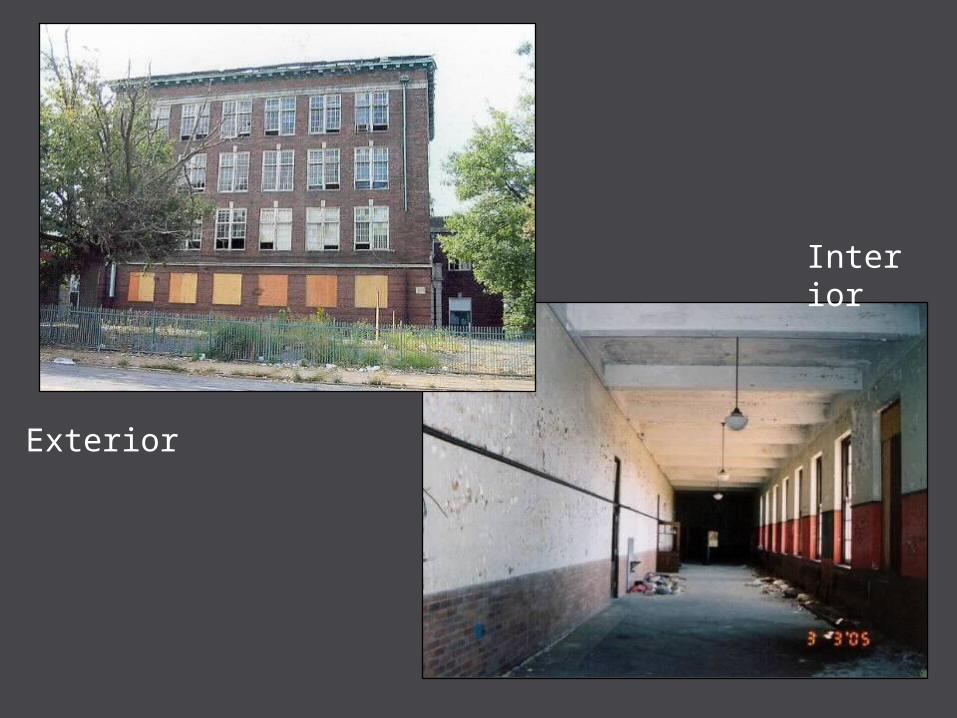

Exterior

Interior

Features

Spaces

Restoration not required

Fundamental Character

Fundamental Character

Additions

Removal

Replacement

Treatments

Secretary of the Interior’sGuidelines

Applying the Standards

• Hierarchy • Condition/Integrity• Cumulative whole

2. “ . . .features and spaces that characterize a property. . .”5. & 9. also use “characterize the property”6. “. . . replacement of a distinctive feature . . .”

Hierarchy: location, visibility, architectural treatment

Integrity

Condition

Cumulative effect

Small change in important space

Substantial change to primary space

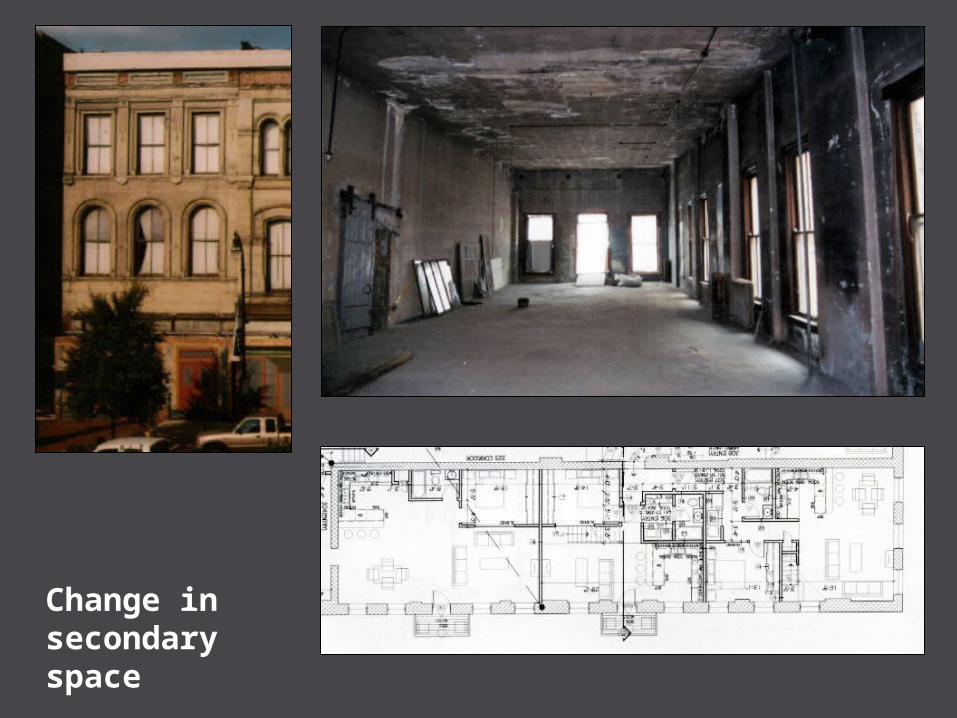

Change in secondary space

Substantial change to secondary elevation

Make additions compatible

Repair rather than replace

Document deterioration

Replace to match

Acquired significance

Replacement of non-historic materials

Certification Process

• Three-part application• Submission made through SHPO• Thirty-day review clock at both SHPO and

NPS• Fee for review of Part 2 and Final

Certification

Part 1- Evaluation of Significance

Needed for:• Contributing building within a district• Multiple buildings in an individual listing• Preliminary determination of eligibility:

individual or district

• Not required for individually listed building

Covered facade

Part 2 - Description of Rehabilitation

• Should be submitted prior to beginning work

• May be amended • Phasing must be determined before work

begins

Submission - Part 2

• Description of work– Written description

governs, supplement with drawings

– Cover all work but focus on significant changes

• True before condition photos– Keyed to a drawing or descriptively labeled

• Supplemental information when needed– Mock-ups, samples, specifications, sight-line studies

Request for Certification of Completed Work

• All proposed work must be completed• Photographs showing all aspects of project• Evaluation but not certification of individual

phases