hexaware technologies adds 9 clients in q2cy15, buy

TRANSCRIPT

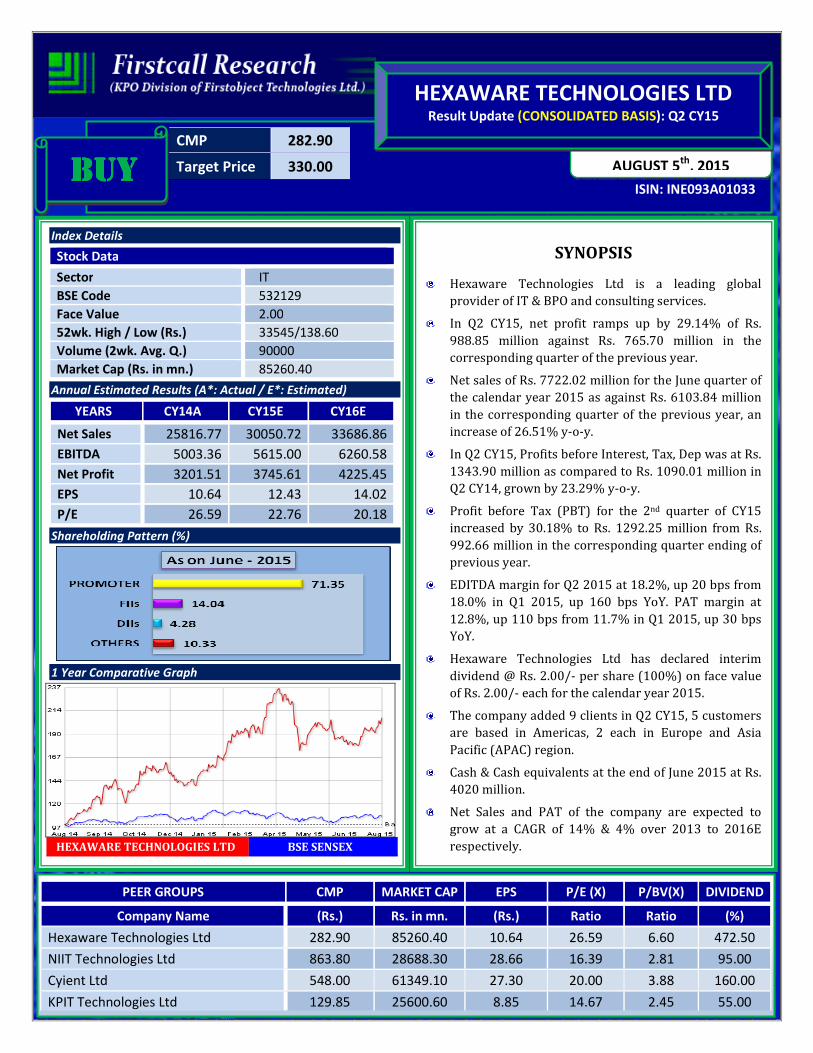

CMP 282.90

Target Price 330.00

ISIN: INE093A01033

AUGUST 5th

, 2015

HEXAWARE TECHNOLOGIES LTD

Result Update (CONSOLIDATED BASIS): Q2 CY15

BUYBUYBUYBUY

Index Details

Stock Data

Sector IT

BSE Code 532129

Face Value 2.00

52wk. High / Low (Rs.) 33545/138.60

Volume (2wk. Avg. Q.) 90000

Market Cap (Rs. in mn.) 85260.40

Annual Estimated Results (A*: Actual / E*: Estimated)

YEARS CY14A CY15E CY16E

Net Sales 25816.77 30050.72 33686.86

EBITDA 5003.36 5615.00 6260.58

Net Profit 3201.51 3745.61 4225.45

EPS 10.64 12.43 14.02

P/E 26.59 22.76 20.18

Shareholding Pattern (%)

1 Year Comparative Graph

HEXAWARE TECHNOLOGIES LTD BSE SENSEX

SYNOPSIS

Hexaware Technologies Ltd is a leading global

provider of IT & BPO and consulting services.

In Q2 CY15, net profit ramps up by 29.14% of Rs.

988.85 million against Rs. 765.70 million in the

corresponding quarter of the previous year.

Net sales of Rs. 7722.02 million for the June quarter of

the calendar year 2015 as against Rs. 6103.84 million

in the corresponding quarter of the previous year, an

increase of 26.51% y-o-y.

In Q2 CY15, Profits before Interest, Tax, Dep was at Rs.

1343.90 million as compared to Rs. 1090.01 million in

Q2 CY14, grown by 23.29% y-o-y.

Profit before Tax (PBT) for the 2nd quarter of CY15

increased by 30.18% to Rs. 1292.25 million from Rs.

992.66 million in the corresponding quarter ending of

previous year.

EDITDA margin for Q2 2015 at 18.2%, up 20 bps from

18.0% in Q1 2015, up 160 bps YoY. PAT margin at

12.8%, up 110 bps from 11.7% in Q1 2015, up 30 bps

YoY.

Hexaware Technologies Ltd has declared interim

dividend @ Rs. 2.00/- per share (100%) on face value

of Rs. 2.00/- each for the calendar year 2015.

The company added 9 clients in Q2 CY15, 5 customers

are based in Americas, 2 each in Europe and Asia

Pacific (APAC) region.

Cash & Cash equivalents at the end of June 2015 at Rs.

4020 million.

Net Sales and PAT of the company are expected to

grow at a CAGR of 14% & 4% over 2013 to 2016E

respectively.

PEER GROUPS CMP MARKET CAP EPS P/E (X) P/BV(X) DIVIDEND

Company Name (Rs.) Rs. in mn. (Rs.) Ratio Ratio (%)

Hexaware Technologies Ltd 282.90 85260.40 10.64 26.59 6.60 472.50

NIIT Technologies Ltd 863.80 28688.30 28.66 16.39 2.81 95.00

Cyient Ltd 548.00 61349.10 27.30 20.00 3.88 160.00

KPIT Technologies Ltd 129.85 25600.60 8.85 14.67 2.45 55.00

Analysis & Recommendation - ‘BUY’

Hexaware reported healthy broad based net sales growth of 26.14% y-o-y and an improvement in margins.

These investments enable the Company to drive healthy revenue growth consistently over the long term. For Q2

CY15, Net sales of the company were at Rs. 7722.02 million from Rs. 6103.84 million in Q2 CY14. In Q2 CY15, Net

profit of the company at Rs. 988.85 million, an increase of 29.14% y-o-y against Rs. 765.70 million in the

corresponding quarter of the previous year.

For Q2 CY15, the Company added 9 new clients across all its key focus areas. The company added 3 clients each

in the Manufacturing and Consumer Vertical and Travel and Transportation Segment. 2 clients were added in

Healthcare & Insurance and 1 client was added in Banking and Financial Services Segment. Of the 9 clients added

in Q2 2015, 5 customers are based in Americas, 2 each in Europe and Asia Pacific (APAC) region. This 2nd Quarter

the company witnessed significant revenue growth with Europe leading among geographies with 8% QoQ

growth. The robust customer acquisitions during the quarter are early results of its investments in creating

differentiated solutions. These will help improving sustainability of its revenue growth in the future. Hexaware’s

focused customer mining strategies and investments in digital technologies have also started yielding results.

Hexaware has delivered a modest revenue growth in a seasonally difficult quarter. The company remains

confident in future and continues to invest in its growth. Cash & Cash equivalents at the end of June 2015 at Rs.

4020 million. Hence, we recommend ‘BUY’ for ‘HEXAWARE TECHNOLOGIES LTD’ with a target price of Rs.

330.00 on the stock.

QUARTERLY HIGHLIGHTS (CONSOLIDATED)

Results updates- Q2 CY15,

Hexaware Technologies Ltd is a global provider of IT,

BPO and consulting services that caters to industries

spanning across Banking and Financial Services, Travel

and Transportation, Manufacturing and Services,

Healthcare and Insurance with revenue over USD 400

million. Reported its financial results for the quarter

ended 30th June, 2015.

The company has achieved a turnover of Rs. 7722.02 million for the June quarter of the calendar year 2015 as

against Rs. 6103.84 million in the corresponding quarter of the previous year, an increase of 26.51% y-o-y.

EBITDA stood at Rs. 1343.90 million in Q2 CY15 when compared to Rs. 1090.01 million in Q2 F14, grown by

23.29% y-o-y. In the same period, net profit ramps up by 29.14% of Rs. 988.85 million against Rs. 765.70 million

in the corresponding quarter of the previous year. The company has reported an EPS of Rs. 3.28 for the 2nd

quarter as against an EPS of Rs. 2.55 in the corresponding quarter of the previous year.

Months June -15 June -14 % Change

Net Sales 7722.02 6103.84 26.51

PAT 988.85 765.70 29.14

EPS 3.28 2.55 28.69

EBITDA 1343.90 1090.01 23.29

Break up of Expenditure

Segment Revenue

Latest Updates

� EDITDA margin for Q2 2015 at 18.2%, up 20 bps from 18.0% in Q1 2015, up 160 bps YoY. PAT margin at

12.8%, up 110 bps from 11.7% in Q1 2015, up 30 bps YoY.

� Return on Equity (RoE) at 30.9 % at the end of Q2 2015 up from 26.9% last quarter.

� Gross margin for Q2 2015 at 36.0%, up 30 bps QoQ.

� Hexaware and Riversand enter into a global partnership to Transform Data Management for Digital

Businesses.

� The Company has hedges worth $ 177.00 mn at an effective rate of Rs. 67.73 and € 6.68 mn at an effective

exchange rate of Rs. 75.68 maturing over the course of the next eight quarters (from July 2015 to April 2017).

Break up of Expenditure (Rs. in millions)

Q2 CY15 Q2 CY14 Chng %

Employee Benefit Exp 4307.87 3390.19 27%

Operating & Other Exp 1316.21 1054.65 25%

Dep & Amortin Exp 114.87 107.64 7%

Software and other Exp 1316.21 1054.65 25%

� For Q2 CY15, the Company added 9 new clients across all its key focus areas. The company added 3

clients each in the Manufacturing and Consumer Vertical and Travel and Transportation Segment. 2

clients were added in Healthcare & Insurance and 1 client was added in Banking and Financial

Services Segment. Of the 9 clients added in Q2 2015, 5 customers are based in Americas, 2 each in

Europe and Asia Pacific (APAC) region.

� From a horizontal service line perspective, 3 clients were added in Infrastructure Management Services

(IMS), 2 clients each in Business Intelligence (BI) and Enterprise Solutions (ES), 1 client each in Applications

Development & Maintenance (ADM) and Quality Assurance and Testing Services (QATS).

COMPANY PROFILE

The Company founded in 1990, and focuses on key domains such as Banking, Financial Services, Insurance,

Travel, Transportation, Logistics, Life Sciences and Healthcare. Hexaware focuses on delivering business results

and leveraging technology solutions by specializing in Business Intelligence & Analytics, Enterprise Solutions,

Quality Assurance and Testing Services, Remote Infrastructure Management Services and Legacy Modernization.

Hexaware has a well-established global delivery model armed with proven proprietary tools and methodologies,

skilled human capital.

Hexaware Technologies, reported that it will work with Oracle to launch Oracle’s PeopleSoft Test Framework

(PTF) services, which will allow users to install, configure, implement and maintain PTF automation. As a

Platinum member of Oracle’s Partner Network (OPN), Hexaware’s PTF services allow customers to execute more

tests with greater accuracy in a shorter time, and enable significantly reduced operational costs. “By unveiling

Hexaware PTF service offerings, we’re not only saving money for its clients by helping to eliminate unnecessary

and redundant processes, but also enabling an enhanced time-to-market solution with ROI within just two test

cycles. PTF is an excellent option because it comes packaged with People Tools, and there is no additional

licensing fee involved for using PTF as the test automation tool.” Hexaware has been featured in the GS100 -

2013 List, which includes companies that define leadership in the global services business.

The company’s onsite/offshore delivery model provides significant cost savings development centers are

assessed at SEI CMMI-Level 5, and are also ISO 9001:2000 and TickIT certified. These help to continually provide

high value, high quality deliverables to their clients.

Business Area

Global Operations

Hexaware’s global operations are located in North America, Europe and Asia Pacific. The Texas centre joins the

two New Jersey centres to service North America based customers. In addition, Hexaware has Global Delivery

Centres located in Mumbai, Chennai, Pune, Nagpur and Bengaluru in India and three Nearshore Delivery Centres

at Saltillo in Mexico.

Technology Services

Industry Solutions

The Company focuses on key domains such as Banking, Financial Services, Insurance, Travel, Transportation,

Logistics, Life Sciences and Healthcare.

Technology solutions

Hexaware focuses on delivering business results and leveraging technology solutions by specializing in

• Enterprise Solutions(applications)

• Quality assurance and Testing Services

• Business intelligence & Analytics

• Microsoft Technology Services

• Legacy Management and technology

• Product Engineering

• Specialized Services

• Infrastructure management Services

• Java Technology Services

• Mobility Services

Partners

Hexaware partnerships are aimed at delivering real business value to clients. Each partnership helps their clients

leverage and enable strong competency and delivery capabilities with the comprehensiveness and strengths of

partner solutions and platforms. Some of these partners are

Oracle

Sap

HP

Microsoft

Lufthansa Systems

Informatica

Unisys

Alaric

eBaoTech

Herald Logic

EiQ Networks

Jamo Solutions

GreenLine

ZAP Technologies

Information Builders

Net APP(service provider)

MicroStrategy

Liferay

IBM

I create software

Checkmarx

Experitest

Cloudera

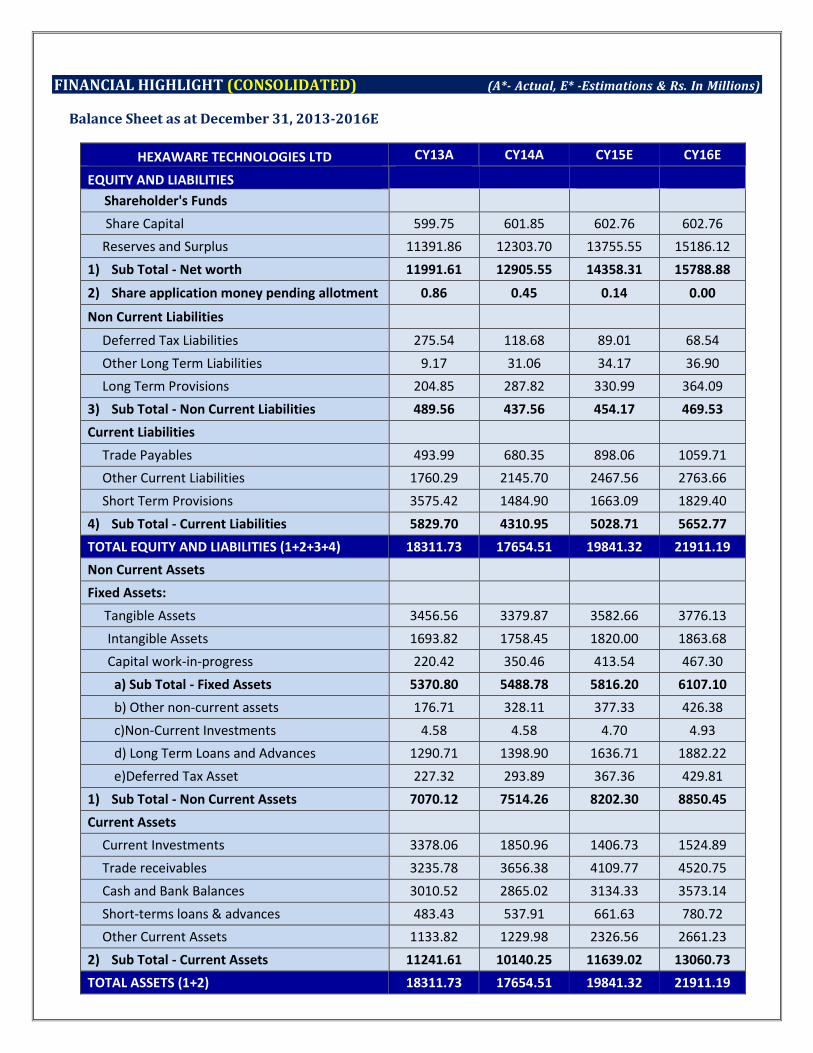

FINANCIAL HIGHLIGHT (CONSOLIDATED) (A*- Actual, E* -Estimations & Rs. In Millions)

Balance Sheet as at December 31, 2013-2016E

HEXAWARE TECHNOLOGIES LTD CY13A CY14A CY15E CY16E

EQUITY AND LIABILITIES

Shareholder's Funds

Share Capital 599.75 601.85 602.76 602.76

Reserves and Surplus 11391.86 12303.70 13755.55 15186.12

1) Sub Total - Net worth 11991.61 12905.55 14358.31 15788.88

2) Share application money pending allotment 0.86 0.45 0.14 0.00

Non Current Liabilities

Deferred Tax Liabilities 275.54 118.68 89.01 68.54

Other Long Term Liabilities 9.17 31.06 34.17 36.90

Long Term Provisions 204.85 287.82 330.99 364.09

3) Sub Total - Non Current Liabilities 489.56 437.56 454.17 469.53

Current Liabilities

Trade Payables 493.99 680.35 898.06 1059.71

Other Current Liabilities 1760.29 2145.70 2467.56 2763.66

Short Term Provisions 3575.42 1484.90 1663.09 1829.40

4) Sub Total - Current Liabilities 5829.70 4310.95 5028.71 5652.77

TOTAL EQUITY AND LIABILITIES (1+2+3+4) 18311.73 17654.51 19841.32 21911.19

Non Current Assets

Fixed Assets:

Tangible Assets 3456.56 3379.87 3582.66 3776.13

Intangible Assets 1693.82 1758.45 1820.00 1863.68

Capital work-in-progress 220.42 350.46 413.54 467.30

a) Sub Total - Fixed Assets 5370.80 5488.78 5816.20 6107.10

b) Other non-current assets 176.71 328.11 377.33 426.38

c)Non-Current Investments 4.58 4.58 4.70 4.93

d) Long Term Loans and Advances 1290.71 1398.90 1636.71 1882.22

e)Deferred Tax Asset 227.32 293.89 367.36 429.81

1) Sub Total - Non Current Assets 7070.12 7514.26 8202.30 8850.45

Current Assets

Current Investments 3378.06 1850.96 1406.73 1524.89

Trade receivables 3235.78 3656.38 4109.77 4520.75

Cash and Bank Balances 3010.52 2865.02 3134.33 3573.14

Short-terms loans & advances 483.43 537.91 661.63 780.72

Other Current Assets 1133.82 1229.98 2326.56 2661.23

2) Sub Total - Current Assets 11241.61 10140.25 11639.02 13060.73

TOTAL ASSETS (1+2) 18311.73 17654.51 19841.32 21911.19

Annual Profit & Loss Statement for the period of 2013 to 2016E

Value(Rs.in.mn) CY13A CY14A CY15E CY16E

Description 12m 12m 12m 12m

Net Sales 22853.48 25816.77 30050.72 33686.86

Other Income 372.73 227.76 145.77 163.26

Total Income 23226.21 26044.53 30196.49 33850.12

Expenditure -17731.19 -21041.17 -24581.49 -27589.54

Operating Profit 5495.02 5003.36 5615.00 6260.58

Interest -2.04 -8.98 -5.21 -5.73

Gross profit 5492.98 4994.38 5609.79 6254.85

Depreciation -386.04 -439.72 -470.50 -510.49

Exceptional Items -311.99 -373.47 -306.25 -321.56

Profit Before Tax 4794.95 4181.19 4833.04 5422.80

Tax -1003.61 -979.68 -1087.43 -1197.35

Net Profit 3791.34 3201.51 3745.61 4225.45

Equity capital 599.75 601.85 602.76 602.76

Reserves 11391.86 12303.71 13755.55 15186.12

Face value 2.00 2.00 2.00 2.00

EPS 12.64 10.64 12.43 14.02

Quarterly Profit & Loss Statement for the period of 31st Dec, 2014 to 30th Sept, 2015E

Value(Rs.in.mn) 31-Dec-14 31-Mar-15 30-Jun-15 30-Sep-15E

Description 3m 3m 3m 3m

Net sales 7117.98 7134.26 7722.02 8084.95

Other income 38.17 36.64 20.66 16.94

Total Income 7156.15 7170.90 7742.68 8101.90

Expenditure -5700.06 -5863.16 -6398.78 -6621.58

Operating profit 1456.09 1307.74 1343.90 1480.32

Interest -2.06 -0.16 -0.02 -2.75

Gross profit 1454.03 1307.58 1343.88 1477.57

Depreciation -113.43 -115.43 -114.87 -117.17

Exceptional Items -214.12 -134.08 63.24 -11.05

Profit Before Tax 1126.48 1058.07 1292.25 1349.35

Tax -253.89 -224.58 -303.40 -296.86

Net Profit 872.59 833.49 988.85 1052.50

Equity capital 600.65 602.25 602.76 602.76

Face value 2.00 2.00 2.00 2.00

EPS 2.91 2.77 3.28 3.49

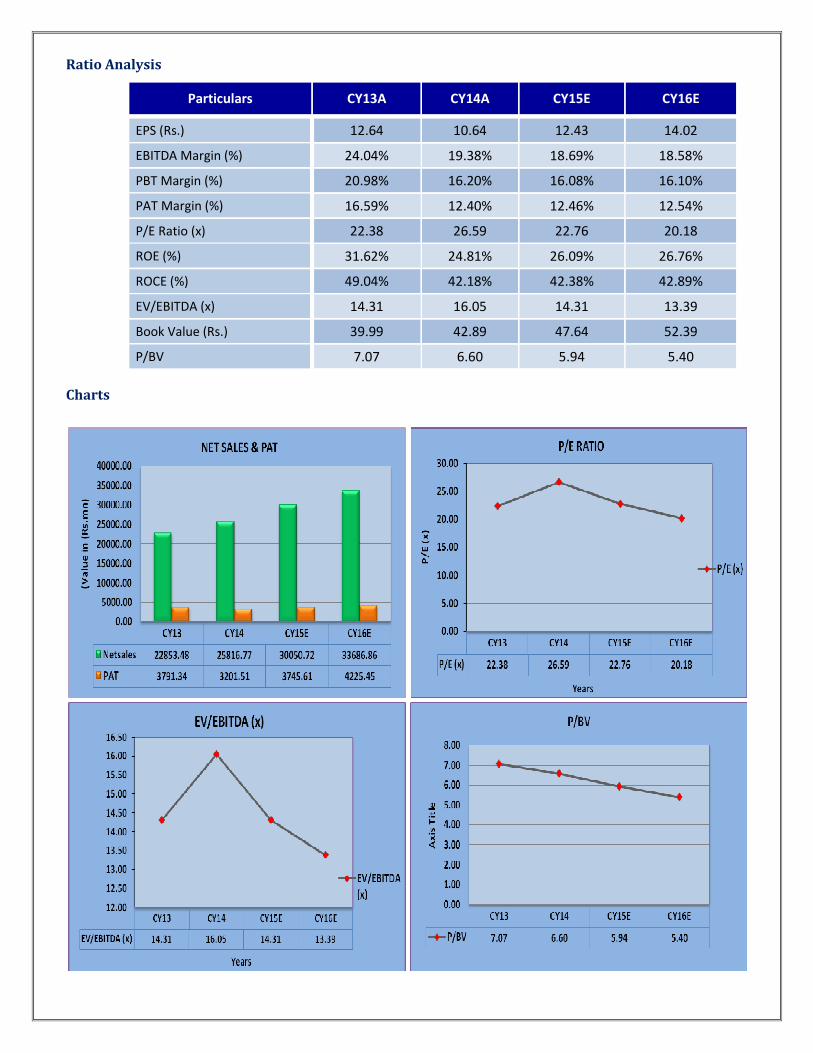

Ratio Analysis

Particulars CY13A CY14A CY15E CY16E

EPS (Rs.) 12.64 10.64 12.43 14.02

EBITDA Margin (%) 24.04% 19.38% 18.69% 18.58%

PBT Margin (%) 20.98% 16.20% 16.08% 16.10%

PAT Margin (%) 16.59% 12.40% 12.46% 12.54%

P/E Ratio (x) 22.38 26.59 22.76 20.18

ROE (%) 31.62% 24.81% 26.09% 26.76%

ROCE (%) 49.04% 42.18% 42.38% 42.89%

EV/EBITDA (x) 14.31 16.05 14.31 13.39

Book Value (Rs.) 39.99 42.89 47.64 52.39

P/BV 7.07 6.60 5.94 5.40

Charts

OUTLOOK AND CONCLUSION

� At the current market price of Rs. 282.90, the stock P/E ratio is at 22.76 x CY15E and 20.18 x CY16E

respectively.

� Earning per share (EPS) of the company for the earnings for CY15E and CY16E is seen at Rs. 12.43and Rs.

14.02 respectively.

� Net Sales and PAT of the company are expected to grow at a CAGR of 14% & 4% over 2013 to 2016E

respectively.

� On the basis of EV/EBITDA, the stock trades at 14.31 x for CY15E and 13.39 x for CY16E.

� Price to Book Value of the stock is expected to be 5.94 x and 5.40 x respectively for CY15E and CY16E.

� We recommend ‘BUY’ in this particular scrip with a target price of Rs. 330.00 for Medium to Long term

investment.

INDUSTRY OVERVIEW

The International Monetary Fund expects world economy to grow at 3.5 and 3.7 percent in 2015-16, downward

revisions of 0.3 percent relative to the October 2014 World Economic Outlook (WEO). The lower estimates

mirrors the reappraise of forecasts in China, Russia, the euro area, and Japan besides weaker activity in some

major oil exporters due to the sharp drop in oil prices. The economic growth in the United States is expected to

transcend 3% during 2015-16 and has been revised to 3.6% aided by domestic demand that will be driven by the

sharp fall in oil prices, moderate fiscal adjustment, and an accommodative monetary policy stance, despite the

projected gradual rise in interest rates. However, the dollar surge is projected to reduce net exports. Although

lower oil prices and quantitative easing support the Euro zone prospects, the IMF has lowered the economic

growth to 1.2% for 2015 weighed by stagnation and inflation. The impact of Abenomics is yet to translate into

positive economic growth prospect for Japan as it witnessed a technical recession in the third quarter of 2014.

The IMF has revised downward the economic growth to 0.6% in 2015 however; it has indicated lower oil prices

and yen depreciation to aid growth in 2015-16. For emerging market and developing economies, the IMF

forecasts economic growth to remain broadly stable at 4.3% in 2015 and to rise to 4.7% in 2016-a weaker pace

than forecast in the October 2014 WEO.

IT INDUSTRY OVERVIEW

Global it industry

Gartner in its IT Spending Forecast Summary, Q4 2014 Update estimates the US-dollar-valued worldwide IT

spending in 2015 is forecast to grow by 2.4%, down from the 3.9% forecast in last quarter's update. Stripping out

the impact of exchange rate movements, the corresponding constant-currency growth figure is 3.7%.The

worldwide IT services market will exceed USD 980 billion in 2015, growing 3.9% in constant currency in 2015,

or 2.5% in U.S. dollars. With outsourcing contributing more than half of market growth, the market will reach

USD 1.1 trillion in 2018.

Growth trends in the it industry

• Emerging geographies and verticals, non-linear growth due to platforms, products and automation.

• Revival in demand for IT services from US and Europe.

• Increasing adoption of technology and telecom by consumers and focused government initiatives –

leading to increased ICT adoption.

• High value client additions bigger than USD 1 million – the highest in the last 5 years, registering 13.5%

growth.

• Emerging verticals (retail, healthcare, utilities) are driving growth above 14%.

• The SMAC (social, mobility, analytics, cloud) market is expected to grow to USD 225 billion by 2020.

• USD 1.6 billion is spent annually on training workforce and growing R&D spend.

• The National Optical Fibre Network (NOFN) is being laid down in phases to connect all the 250,000 gram

panchayats in the country.

INDIAN IT INDUSTRY SCENARIO

o The Indian IT Services industry is expected to report a 12.6% export revenue growth in FY15E highlights

Nasscom. The revival in demand for IT Services from the US and Europe to be the growth driver for the

Indian IT Services industry in FY2015.

o The Indian IT-BPM industry is expected to maintain its positive momentum following the thrust provided

by the Indian government in the form of Digital India and Smart Cities projects. The industry is likely to

register 12.3% growth in FY 2015 in terms of export revenues led by renewal in demand from the US

reckons Nasscom.

o The Indian IT-BPM industry is expected to maintain its positive momentum following the thrust provided

by the Indian government in the form of Digital India and Smart Cities projects. The industry is likely to

register 12.3% growth in FY2015 in terms of export revenues led by renewal in demand from the US as

per Nasscom.

Disclaimer:

This document is prepared by our research analysts and it does not constitute an offer or solicitation for the

purchase or sale of any financial instrument or as an official confirmation of any transaction. The information

contained herein is from publicly available data or other sources believed to be reliable but we do not represent that

it is accurate or complete and it should not be relied on as such. Firstcall Research or any of its affiliates shall not be

in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the

information contained in this report. Firstcall Research and/ or its affiliates and/or employees will not be liable for

the recipients’ investment decision based on this document.

Firstcall India Equity Research: Email – [email protected]

C.V.S.L.Kameswari Pharma & Diversified

U. Janaki Rao Capital Goods

B. Anil Kumar Auto, IT & FMCG

M. Vinayak Rao Diversified

G. Amarender Diversified

Firstcall Research Provides

Industry Research on all the Sectors and Equity Research on Major Companies

forming part of Listed and Unlisted Segments

For Further Details Contact:

Tel.: 022-2527 2510/2527 6077 / 25276089 Telefax: 022-25276089

040-20000235 /20000233

E-mail: [email protected]

www.firstcallresearch.com