h1 2017 trading update - amazon web services · pdf filecarillion plc h1 2017 trading update -...

TRANSCRIPT

CARILLION PLC H1 2017 TRADING UPDATE - JULY 2017 1

H1 2017 Trading Update10 July 2017

CARILLION PLC H1 2017 TRADING UPDATE - JULY 2017 2

Disclaimer

This presentation has been prepared by Carillion plc (the “Company”) contains certainforward-looking statements with respect to certain of the Company’s current expectationsand projections about future performance, anticipated events or trends and other mattersthat are not historical facts. These forward-looking statements, which sometimes use wordssuch as "aim", "anticipate", "believe", "intend", "plan", "estimate", "expect" and words ofsimilar meaning, include all matters that are not historical facts and reflect the directors'beliefs and expectations and involve a number of risks, uncertainties and assumptions thatcould cause actual results and performance to differ materially from any expected futureresults or performance expressed or implied by the forward-looking statements. Thesestatements are subject to unknown risks, uncertainties and other factors that could causeactual results to differ materially from those expressed or implied by such forward-lookingstatements. Statements contained in this presentation regarding past trends or activitiesshould not be taken as a representation that such trends or activities will continue in thefuture.

The Company obtained certain industry and market data used in this presentation frompublications and studies conducted by third parties and estimates prepared by the Companybased on certain assumptions. While the Company believes that the industry and marketdata from external sources is accurate and correct, the Company has not independentlyverified such data or sought to verify that the information remains accurate as of the date ofthis presentation and the Company does not make any representation as to the accuracy ofsuch information. Similarly, the Company believes that its internal estimates are reliable, butthese estimates have not been verified by any independent sources.

CARILLION PLC H1 2017 TRADING UPDATE - JULY 2017 3

Agenda

Introduction Philip Green,

Non-Executive Chairman

Keith Cochrane,

Interim Group Chief Executive

Zafar Khan,

Group Finance Director

Keith Cochrane,

Interim Group Chief Executive

Q&A

Overview

and Strategy

Financial

Review

Conclusions

Overview & strategy

Keith Cochrane Interim Group Chief Executive

CARILLION PLC H1 2017 TRADING UPDATE - JULY 2017 5

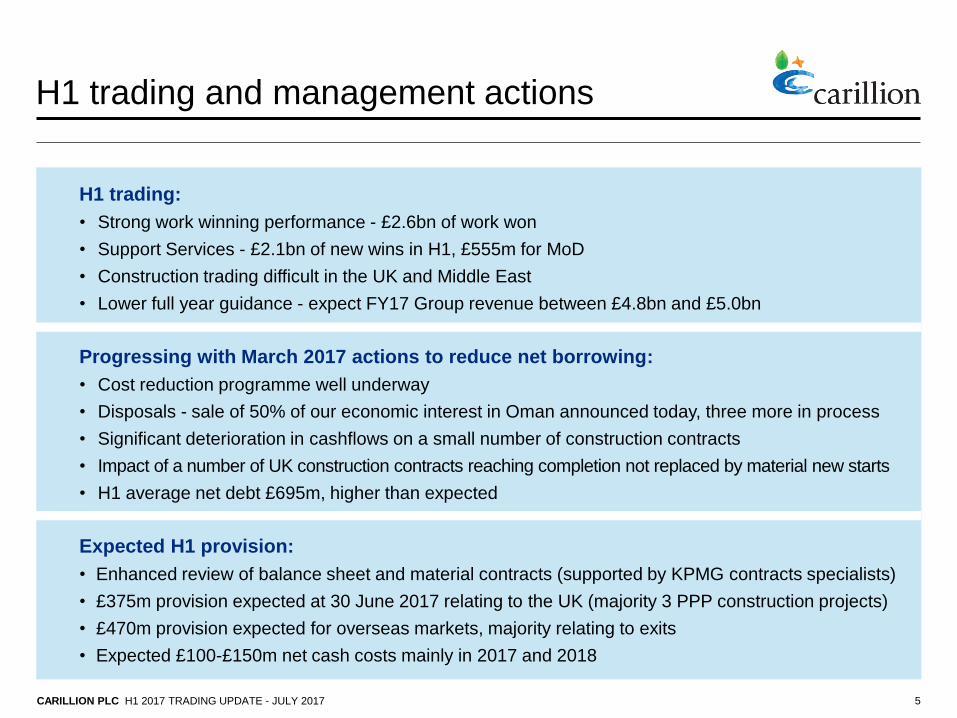

H1 trading and management actions

H1 trading:

• Strong work winning performance - £2.6bn of work won

• Support Services - £2.1bn of new wins in H1, £555m for MoD

• Construction trading difficult in the UK and Middle East

• Lower full year guidance - expect FY17 Group revenue between £4.8bn and £5.0bn

Progressing with March 2017 actions to reduce net borrowing:

• Cost reduction programme well underway

• Disposals - sale of 50% of our economic interest in Oman announced today, three more in process

• Significant deterioration in cashflows on a small number of construction contracts

• Impact of a number of UK construction contracts reaching completion not replaced by material new starts

• H1 average net debt £695m, higher than expected

Expected H1 provision:

• Enhanced review of balance sheet and material contracts (supported by KPMG contracts specialists)

• £375m provision expected at 30 June 2017 relating to the UK (majority 3 PPP construction projects)

• £470m provision expected for overseas markets, majority relating to exits

• Expected £100-£150m net cash costs mainly in 2017 and 2018

CARILLION PLC H1 2017 TRADING UPDATE - JULY 2017 6

Strategic and operational review

Decisions already taken

• Exit PPP construction

• Exit Egypt, Saudi Arabia and Qatar construction

• Sale of 50% of Oman business for up to £42m (£12m upfront)

• Bid only lower risk procurement routes on construction contracts

Leadership and management changes

Strategic and operational review:

A thorough review of the

business and its capital

structure with all options

being given appropriate

consideration

CARILLION PLC H1 2017 TRADING UPDATE - JULY 2017 7

Actions to reduce net debt

• Substantial programme of action to reduce net debt also underway:

– Scope for significant further cost efficiencies – to be quantified as part of the strategic and operational review

– Non-core disposals targeting proceeds of £125m(1)

within 12 months

– Targeting significant receivable recoveries

– Improved contract execution

• 2017 dividends suspended (saving c£80m pa), Board to review dividend policy in 2018

(1) Includes £12.8m upfront consideration from sale of Carillion Alawi but not the deferred consideration

CARILLION PLC H1 2017 TRADING UPDATE - JULY 2017 8

Enhanced balance sheet and contracts review

• Anticipated total net cash outflow £100-150m mainly in 2017 and 2018

• Four large contracts (3 in UK, 1 in Middle East) account for around half the provision

• All four complete within the next 18 months

Since March 2017 Impairment

UK: • Majority 3 PPP construction contracts

£375m

Overseas:• Majority related to exits (Canada & Middle East)

£470m

TOTAL EXPECTED H1 PROVISION £845m

CARILLION PLC H1 2017 TRADING UPDATE - JULY 2017 9

Lessons learned and actions

• Acceptance of a high degree of uncertainty around key assumptions

• Success contingent on performance of others not under our control

• Design changes agreed without agreeing incremental cost and value

• Geographic risk

• Exit non-core countries and markets

• Strengthen governance

• Leadership & management changes:

– New CEO

– UK Building MD exited

– Construction Services team strengthened and refreshed

– Changed 3 BU FDs

– Incentives to be linked to de-leveraging

Two clear root causes are international construction and

PPP construction which we have addressed

Key Issues Key Actions

CARILLION PLC H1 2017 TRADING UPDATE - JULY 2017 10

Why we believe in this business

We are a market leading Support

Services business

• Focused on infrastructure and property

services

• A strong reputation for service excellence

• Outlook underpinned by more than 90% of

work won in H1 for repeat customers with

long-term contracts

• High revenue visibility in Support Services –

94% for 2017, 58% for 2018 and 44% for 2019

• No significant renewals until end 2019

• Selected on frameworks worth £23bn in total

Key differentiators

• Our People and Culture

• Use of Technology

• Health & Safety Excellence

• Approach to Sustainability

CARILLION PLC H1 2017 TRADING UPDATE - JULY 2017 11

Leading positions in growth markets

INFRASTRUCTURESERVICES

Rail

Highways

Transmission

Telecoms

Oil & Gas

No. 2 in UK

No. 2 in Framework

No. 3 in Canada

No.1 in Broadband

MarketGrowth

PROPERTYSERVICES

Defence

Communities

Corporate

Central Gov

Health

No. 1 in UK

LA Partnerships

CCS Framework

MarketGrowth

CARILLION PLC H1 2017 TRADING UPDATE - JULY 2017 12

Only Lower Risk

Procurement Routes

A lower risk Construction business

Construction Positioning

• Change in approach to Construction

• Exit PPP construction

• Reduced Middle East exposure

• Only bidding under lower risk forms of procurement

• Going forward:

– Highly selective approach

– Small number of customers

– Targeted at Support Services customers

– Focusing on the UK

• In H1 c70% of construction work won in the UK was for repeat customers and all is under lower risk procurement routes

Cost

reimbursable

Early Contractor

Involvement

– Target Cost

Two Stage

- Design & Build

Frameworks

CARILLION PLC H1 2017 TRADING UPDATE - JULY 2017 13

Short-term priorities

2017 actions

• Leadership and management changes

• Non-core disposals - 50% of Oman sold, three more in process

• Enhanced contract review completed and lessons learnt

• Canada construction exited

• Strategic review - progress update with interims in September

2018 actions

• Non-core disposals substantially completed (£125m)

(1)

• Qatar/KSA/Egypt construction exits completed

• Challenging contracts completed

• Cost out programme

• Receivables recoveries well progressed

(1) Includes £12.8m upfront consideration from sale of Carillion Alawi but not the deferred consideration

Financial review

Zafar KhanGroup Finance Director

CARILLION PLC H1 2017 TRADING UPDATE - JULY 2017 15

Background

• Took over in January 2017 with key priorities of:

– reducing net debt

– increasing financial reporting transparency

• Subsequent adverse developments in H1 have increased net debt despite progress against actions outlined in March

• H1 average net debt £695m

– actions to reduce net debt already underway

− 50% of Oman business sold, raising up to £42m (£13m upfront)

− cost savings programme stepped up

− 2017 dividends suspended

– planning to raise approximately £125m(1)

from disposals in next twelve months – three more businesses currently in a sale process

• Enhanced contracts review:

– as part of wider balance sheet review

– supported by KPMG contracts specialists

(1) Includes £12.8m upfront consideration from sale of Carillion Alawi but not the deferred consideration

CARILLION PLC H1 2017 TRADING UPDATE - JULY 2017 16

Enhanced contracts review - selection and scope

• Contracts in the UK where there has been notable deterioration during 2017 that would indicate potential risk of impairment

• Contracts impacted by decision to exit construction in Canada and certain territories in the Middle East

• Any contracts with material contentious receivables

• All continuing contracts with revenues greater than £20m in the period to 31 May 2017

• All contracts with receivable balances in excess of £20m as at 31 May 2017

• Agreed scope with KPMG contracts specialists

Selection process

• Selection process identified 58 contracts for enhanced review:

– 20 completed contracts

– 38 continuing contracts comprising:

– 13 Support Services contracts

– 25 construction contracts (of a total of 83 continuing construction contracts)

• 38 continuing contracts account for 46%of total Group revenue at 31 May 2017

• 58 reviewed contracts accounted for £1.58bn or 73% of total receivables on the balance sheet as at 31 May 2017

Scope of review

Review covered all completed and ongoing services and construction contracts

CARILLION PLC H1 2017 TRADING UPDATE - JULY 2017 17

Enhanced contracts review - outcomes and financial impacts

Outcomes

• Review identified a number of contracts with potential issues, relating to construction contracts (continuing and completed)

• Expected provision of £845m to be taken as an exceptional at 30 June 2017

• Net cash outflow of £100-£150m expected in relation to underperforming contracts, mainly in 2017 and 2018

• No prior year adjustment

• The four most challenging contracts represent around half the total provision

– All four expected to complete in the next 18 months

– All other contracts identified will complete within 12 months

• Additional cash benefit of £110m relating to further tax losses

£845mTOTAL EXPECTED PROVISION

UK

Canada

Middle East

375

145

325

845

Expected provision£m

Receivables

Payables

Remaining cash flow

328

(443)

(115)*

Revisedposition

(net)£m

(599)

(246)

(845)

927

(197)

730

Currentposition

Impairmentprovision

* Range of £100-£150m

CARILLION PLC H1 2017 TRADING UPDATE - JULY 2017 18

Contracts portfolio

• Average contract period nine years

• No major contract renewals until end 2019

• Approximately 90% for public and regulated sectors

• New work focused on lower risk procurement routes

• Reducing exposure to PPP construction –15% of construction revenue and tracking towards zero by 2018

• Overseas exposure reducing as focused only on contracts supported by UK Export Finance

• PPP investment portfolio performing well

80%

£12.8bn

SUPPORT SERVICES

16%

£2.5bn

CONSTRUCTION

4%

£0.7bnPPP

CARILLION PLC H1 2017 TRADING UPDATE - JULY 2017 19

Actions to reduce average net borrowing

Disposal of non-core businesses

• Approximately £125m(1)

over next 12 months

Increased focus on managing working capital

• Cash collection remains key focus including for problem contracts

• Aim to reduce monthly swings in working capital

Further cost efficiencies

• Significant additional cost savings to be quantified as part of the operational review

Suspension of 2017 dividends

• The Board will review the dividend policy in 2018

Pension deficit payments

• c£50m deficit recovery payment in 2017

Recoveries• Provision supported by dedicated team to facilitate cash

settlements on key contracts

(1) Includes £12.8m upfront consideration from sale of Carillion Alawi but not the deferred consideration

CARILLION PLC H1 2017 TRADING UPDATE - JULY 2017 20

H1 Summary financials

Group

• Healthy work winning and order book

• Net debt increase due to working capital outflows, mainly on onerous construction contracts

• Expected exceptional provision of £845m related to Middle East, exiting construction market in Canada and certain construction contracts in the UK

Support Services

• Good H1 work winning

Construction

• Difficult H1 trading in construction, particularly in the UK with a deferral of a number of contract starts

New & probable orders(1)

Order book plus probable orders(1)

Total revenue(1)

Average net debt(1)

Adjusted spot net debt(1) (3)

Average EPF utilisation

Pension deficit (net of tax)(1)

Carried forward tax losses(1)

Net derivative asset(1)

£2.6bn

£16.0bn

£2.5bn

£695m

£536m

£412m

£587m

£810m

£39m

H1 2017

£2.5bn

£16.0bn(2)

£2.5bn

£587m(2)

£183m(2)

£400m(2)

£663m(2)

£186m(2)

£36m(2)

H1 2016

+4%

-

-

-18%

-193%

-3%

+11%

+335%

+8%

Change (%)

(1) Estimated

(2) Vs. 31 December 2016

(3) Adjusted for net derivative asset

CARILLION PLC H1 2017 TRADING UPDATE - JULY 2017 21

Revised guidance

Reduced performance against management expectations for 2017

• Group revenue (including joint ventures) between £4.8bn and £5.0bn

• Support Services revenue of £2.6bn to £2.8bn

• PPP revenue of £225m to £275m with underlying operating profit around 15-20% lower vs. previous year

• Middle East construction services revenue between £520m and £570m and maintained operating margin at around 4 per cent

• Construction services (ex Middle East) revenue of £1.2bn to £1.4bn and margins lower vs. 2016

• Net debt (excluding disposal proceeds)

– YE slightly below 30 June level

– FY average between £775m and £800m

• IFRS 15 review underway – expect to provide an update with our H1 results

CARILLION PLC H1 2017 TRADING UPDATE - JULY 2017 22

My philosophy

• Transparency a priority

• New key performance indicators

– Redefine cash conversion to exclude cash from PPP equity sales

– Analysis and commentary on total Days Sales Outstanding

– ROCE to be included in Group KPIs

• Focus on underlying cash generation and profitability

– Increased disclosure on movements in working capital and net debt

CARILLION PLC H1 2017 TRADING UPDATE - JULY 2017 23

Summary

• Poor first-half cash performance reflects outflows on challenging contracts and phasing of new contract starts

• Enhanced contracts review addressed issues associated with ongoing and legacy contracts

• The actions we are taking should improve future cash generation and reduce contract risks

• Substantial liquidity with no short-term loan maturities

• No covenant issues

– Well within our 3.5x net debt to EBITDA covenant at the half year

• Ongoing de-leveraging supported by:

– Disposals

– Cost reduction

– Collection of legacy receivables and

– A greater focus on underlying working capital

• Increased financial reporting transparency

Conclusions

Keith CochraneInterim Group Chief Executive

CARILLION PLC H1 2017 TRADING UPDATE - JULY 2017 25

A leading Support Services business

• Very difficult H1

• Strengths in underlying business:

– Good positions in growth Support Services markets

– Excellent people, great capabilities

• Key priorities:

– Look afresh at how we operate

– Learn the lessons of recent challenges

– Simplify the business

• Ensure we deliver value to our shareholders

Appendix

Additional Financial Information

CARILLION PLC H1 2017 TRADING UPDATE - JULY 2017 27

Pensions

• Deficit very sensitive to movements in AA bond yield – 10bps movement changes deficit by £60m

• Current contributions plus asset returns of 3% to 5% would be sufficient to cover liabilities

• Main schemes closed to future accrual and c.40% of mortality risk hedged by a longevity swap

• Triennial valuation date 31 December 2016

• c£50m deficit recovery payment in 2017

H1 2017 Dec 2016

Assets

Liabilities

Deficit

Deferred tax

Net pension deficit

2,618

(3,329)

(711)

124

(587)

£m

2,573

(3,378)

(805)

142

(663)

CARILLION PLC H1 2017 TRADING UPDATE - JULY 2017 28

c.£1.5bn of available funding

34 49

249

844

51

227

0 27

2017 2018 2019 2020 2021 2022 2023 2024

Year of maturity

UK borrowing facilities maturity profile (£m)