guinness atkinson asia pacific dividend builder fund ... · guinness atkinson asia pacific dividend...

TRANSCRIPT

GuinnessAtkinsonAsiaPacificDividendBuilderFundManagersMonthlyUpdate–January2018

SummaryReview&Outlook

Fund&Market

• ThepastmonthhasseenAsianmarketsrisestronglywiththeMSCIACPacificexJapanIndexrise6.99%inUSdollarterms.

• TheseconditionsdonotsuitthisFund’sparticularstyleandthusitlaggedthemarketby2.51%.• ThebestperformingsectorswereChinaEnergy,KoreaandSingaporeIndustrials,ChinaTechnology

andChinaFinancials.Amongstcountries,Chinawasthestandoutwinnerrisingover12%indollartermsfollowedbyThailandandMalaysia.

• WewouldnotexpecttooutperformintheseconditionsandalthoughtheFundhaslaggedinJanuary,itisstillintouchwithbroadmarket.OnoccasionsofmarketweaknessattheendofthemonththeFunddemonstrateddefensivequalitiesaswewouldhope.

• Inthemonth,allfourofourChinesebankswereoutperformers,beatingthemarketby7%ormoreindollarterms.WealsosawgoodcontributionsfromAustralianretailerJBHi-Fi,ThaienergycompanyPTT,TaiwantechnologycompaniesNovatekandTaiwanSemiconductor,andfromChineseshipbuilderYangzijiang.

• TheMalaysianringgit,ThaibahtandChineseyuanwerethenestperformingcurrencies;theKoreanwonandPhilippinepesoweretheweakest.

• ThepricesofBrentcrudeoilandGoldbothrose3%,whichwasinlinewithdollarweakness.• Twentytwoofthethirty-sixstockslaggedthemarketmostlybecausetheyarelowerbetanamesso

lesssensitivetomarketmovements.Therewereacoupleofstockshoweverthatarefacingheadwinds.LukFookjewelryreporteddeceleratinggrowthinsamestoresalesinChinaandguidednextyear’sgrowthat~8%comparedtoearlierforecastsof~14%,whichdisappointedthemarket.Li&FungwasweakeronmacroconcernsfollowingamoreaggressivetradestancefromtheUSfollowingtheimpositionoftariffsonChinese-madesolarpanelsanddomesticappliances.

Fundperformance

asof1/31/2018

YTD 1YR 3YR 5YR

10YR

AsiaPacificDividendBuilderFund(GAADX) 4.48% 36.82% 13.69% 9.11% 5.90%

MSCIACPacificexJapan 6.99% 39.05% 12.72% 8.60% 6.88%

Allreturnsover1yearannualized.Source:Bloomberg,GuinnessAtkinsonAssetManagement

ExpenseRatio:1.11%(net)*;3.14%(gross)

GuinnessAtkinsonAsiaPacificDividendBuilderFundManagersMonthlyUpdate–January2018

Performancedataquotedrepresentspastperformance;pastperformancedoesnotguaranteefutureresults.Theinvestmentreturnandprincipalvalueofaninvestmentwillfluctuatesothataninvestor’sshares,whenredeemed,maybeworthmoreorlessthantheiroriginalcost.CurrentperformanceoftheFundmaybelowerorhigherthantheperformancequoted.Performancedatacurrenttothemostrecentmonthendmaybeobtainedbycalling800-915-6566and/orvisitingwww.gafunds.com.Performancedatadoesnotreflectthe2%redemptionfeeforsharesheldlessthan30daysand,ifdeductedthefeewouldreducetheperformancenoted.Totalreturnsreflectafeewaiverineffectandintheabsenceofthiswaiver,totalreturnswouldbelower.

EventsinJanuary

• USbondyieldsroseandthedollarweakened.TheUSGovernment10Yearyieldrosefrom2.5%to2.7%andbyFeb2nditreached2.84%.Atthesametimethedollarweakenedontrade-weightedbasisby3.2%(asmeasuredbytheDXYDollarIndexwhichismadeupofEUR57.6%,JPY13.6%,GBP11.9%,CAD9.1%,SEK4.2%andCHF3.6%).

• TheUSannouncedpunitivetariffsonChinese-madesolarpanelsanddomesticappliances.ThisfollowsagenerallymoreactivestanceontradematterswithrespecttoNAFTA.TheChineseresponsesofarhasbeennoticeablymuted.

• InlightoftheweakerdollartheChinesecurrencyhasbeenallowedtoappreciatebrisklyagainstthedollarby3.4%,toitsstrongestlevelsinceJuly2015.Onatradeweightedbasis,theChinesecurrencyiseffectivelyunchangedoverthemonth.

• Inthetechnologysector,thesmartphonerelatedcompaniesareseeingsharepricepressureonweakerdemandinbothChinesesmartphoneandiPhoneXdemand.ChannelcheckssuggestthatAppleisexpectingmoremoderatedemandandisthusscalingbackordersforcomponents.ThisisnotnewnewsandmanyofthesestockshavebeenpricingthisinsinceNovember.

Outlook

• Asianstockmarketsarewellsupportedbyearning’sgrowthandmacro-economicmomentumsupportedbydomesticactivity(particularlyinChina,SingaporeandThailand)andbyglobalgrowthwhichislookingbrighterthanithasformanyyears.

• Wemustexpectthatreportedearningsgrowthwilldecelerateincomingmonths.Thisisamathematicalcertaintyasthecomparisonswillbemadeagainstahigherbase.

• ValuationsinAsiaforthemostpartremainsupportive,especiallyforthosebusinesseswithaprofileofconsistentprofitability.Wearecautiousonthosestocksinthecyclicalsectorsdrivenbymacro-factorsespeciallythoseexposedtoindustrialcommodityprices,likethesteelmakers.

• WeexpecttoseeUSinterestratesmovetowardnormalizationandwearealreadyseeingthebondmarketmovemorequickly.ThismayremovetheneedfortheFederalReservetomovefasterbuttheeffectswillalmostcertainlybefeltintheequitymarkets.

• Thebestdefenses:focus,aswedo,onthosecompanieswhosereturnoncapitalhasbeensustainedabovethecostofcapitalbecauselessoftheirinvestmentvaluewillbeerodedbyahigher

GuinnessAtkinsonAsiaPacificDividendBuilderFundManagersMonthlyUpdate–January2018

discountrate;focus,aswedo,oncompanieswithonlymoderatedebtlevelswiththeratioofdebttoequitynogreaterthan1.

Discussion

Asianearningsconsensusforecastswereupgradedafurther2.2%for2018and2019fortheMSCIAsiaPacificexJapanindex.ChineseandSingaporeanmarketssawthebiggestmoves,up3%and2%respectively.Overthepasttwelvemonthsamountstoa16%upgradetoChinaestimatesand5%upgradetoSingapore.DowngradestoforecastsinJanuarywereforTaiwan,PhilippinesandIndia.AustralianandKoreaearningsestimateswereunchangedfor2018andupslightlyfor2019.

WethinkthatAsianmarketswillnowbemuchmorefocusedontheoutlookforearnings.InthepasteighteenmonthsitisouropinionthatmarketmoveshavebeendrivenprimarilybyanexcessivelylowvaluationrelativetobothAsia’shistoryandtodevelopedmarkets.Reportedearningsgrowthhasbeenstronginthepastyearandthishasprovidedsupporttotherallybutnowwethinkinvestorsarelookingaheadforreasonstocontinuetobuy.

UpgradestoChinahavebeensignificantashasChina’sequitymarketperformance.WecontinuetoremindreadersthatAshare(ShanghaiandShenzhen)marketperformanceisnotthebestguidetoassessingChina’seconomicwell-being.Instead,thesemarketstendtobemoreresponsivetoshorttermliquidityconditionsandthisisespeciallytrueoftheShenzhenstockexchange.ButChinaisdoingwell:

• Economicgrowthmomentumisevidentwithoverallgrowthof6.9%in2017vs6.7%in2016.• RisingcommoditypricesareabenefitforChinabecauseitallowsmaterialsproducerstoraise

prices• Pricingpowerforheavyindustryand16%growthinindustrialprofitsimprovesthedebtservicing

capacityofthemoreheavilyindebtedsectors• Higherdebtservicingcapacityhasalsobeenevidentinslowingnon-performingloanformationin

thebankingsector• Thereisnowevidencethatintensifiedeffortsatfinancialreformareprovingeffectiveandnot

destabilizingassomefeared;creditgrowthhasslowedthisyearanddeleveraginginthebankingsectorisbeingenforced.

• Domesticconfidenceishigherasevidencednotonlyinretailsalesandtherealestatesectorbutalsointhereductionincapitaloutflowswhichhasbeenaccompaniedbyrenminbistrengthagainstthedollarto2015levels.

Singaporeupgradesarelesssignificanttotheworldbutareinterestingnevertheless.Thecountryisdevelopedmarketandhasbeenintheeconomicdoldrumsforanumberofyears.Productioncostsarehigherthereandsothegoalhasbeentofindareplacementfortheelectronicmanufacturingsegmentthatdrovegrowthintheyearsbeforethefinancialcrisis.Policymissteps,possiblythegreatestbeingthecontrolsonimmigration,forcedwagecostssharplyhigherandfurthererodedcompetitiveness.Italsohadanimpactonthepropertymarketwhicherodeddomesticconfidencethroughanegativewealtheffect.

GuinnessAtkinsonAsiaPacificDividendBuilderFundManagersMonthlyUpdate–January2018

TheSingaporedollardeclinedagainsttheUSdollarfrommid-2014totheendof2016afterstrengtheningfairlysteadilyovertheprevious13years.

However,conditionshavebeguntochangeforthebetter.Theshiftintohealthcare(biotechandpharmaceuticals)isnowpayingoff.Singapore’sfinancialservices,especiallyinassetmanagementandwealthmanagementhavegainedcriticalmass.Macro-economicdatashowarecoveryinindustrialproductionandnon-oilexports.ConsumerconfidencewhichhasbeenfragileisnowshowingsignsoffirmingandtheSingaporedollarstrengthened8.5%in2017andhasrisenafurther1%inJanuary.

Portfolioactivity

WehavekepttheportfoliocompositionunchangedinJanuarybutwithflowsintotheFundwehavebeenabletoeffectrebalancing.ExamplebeneficiariesofthishavebeenLukFook,KT&GandLi&Fung.Thesestockshaveallbeenunderperformersthismonthasmarketattentionhasbeenelsewherewhichrepresentsagoodopportunitytotopupassumingwearecorrectinourtwobaseassumptionswhicharefirstly,thesebusinessesarelikelytosustaintheir8%-orbettercashflowreturnoninvestment(CFROI)andsecondly,thatthemarketundervaluesthatlikelypersistence.

LukFook,aswementionedearlier,hasunderperformedbecausesamestoresalesgrowthinitsChinajewelrystoreshasslowedbymorethaninvestorshadexpected.Thisgrowthslowdownhasbeenintheirsalesofgemsetswhicharehighermargin,butweregardedthisasalmostinevitablegiventhepreviousgrowthratewasunsustainable.Theconcernnowisthatwithmoregrowthcomingfromlowermargingoldproductswewillseeanoverallreductioninprofitability.However,itisourviewthatmargindeclineexpectationshavebeenoverdoneandsecond,ifinflationbecomesanissueweexpecttoseegoldpricespickupwhichwillbenefitLukFook.Wehavealreadya3%riseinthegoldpricethismonthandsoweconsiderLukFook’ssharepricedroptoabeknee-jerkreactionandwearebuyers.

KT&GisaKoreantobacconamewelikethatcomesinandoutoffavor,butitsprofitabilityhasbeenconsistent.Inrecentmonthsthesharepricewasboostedbythelaunchofits“heatnotburn”tobaccoproductbutsomearenowsayingthiswillstillresultinmarketsharelossforKT&G,margincompressionduetohigherproductioncostsandmarketingexpensesandthatitwilltakelongertoachievescaleeconomies.Theseviewshavecontributedtothe16%dropinthesharepricesinceitsmid-Novemberpeak.Wetakeheartfromrecentmanagementguidanceofafasternationalroll-outthisyear,fromsignsoffasterconsumeracceptanceoftheproductsandadditionallyfrommanagementsimproveddividendpolicywhich(let’snotoverstateit)ismoreshareholderfriendlybyensuringaminimum40%ofprofitswillbepaidoutasdividends.

Li&Fungisastockwehavewrittenaboutmanytimesbefore.Thecompanyactsasamiddle-manbetweenmanufacturersinAsiaandretailersintheUSandEurope.Inrecentyearsit'sbusinesshasbeensqueezedbyslowerdevelopedmarketdemandandbythedisintermediatingeffectsoftechnology.Li&Fungthereforehastoreinventitselftosomedegreeandre-focusontheserviceelementofitsbusinessandtodivestitselfofdirectproductionactivity.Theiraimistoprovideaproductdesign,sourcing,productionandshippingservicethatwillreducethetimebetweenproductconceptandfinaldeliveryfromaround40weeksto20.Theyaremakinggoodprogressandthesharepriceralliedlastyear.ItfellbackonPresident

GuinnessAtkinsonAsiaPacificDividendBuilderFundManagersMonthlyUpdate–January2018

Trump’simpositionoftariffsonsolarpanelsandwhitegoods;investorsworrywhetherbroadtraderelationsareabouttodeteriorate.Webelievenotandthatthesharepriceweaknessisanopportunity.

Summaryandconclusion

Theportfolioistradingonaprice/earningsmultiplebasis,ata10%discounttothemarketasmeasuredbytheMSCIACPacificexJapanIndex.Thisindexisinturntradingatawiderdiscounttodevelopedmarketsthanitsten-yearaverage.Acombinationofaboveaveragecompaniesinouropinion,payingaboveaveragedividendsandtradingonabelow-averagevaluationseemstoustobeanattractiveone.

EdmundHarrissandMarkHammonds(portfoliomanagers)SharukhMalik(analyst)

TheFund’sinvestmentobjectives,risks,chargesandexpensesmustbeconsideredcarefullybeforeinvesting.Thestatutoryandsummaryprospectuscontainsthisandotherimportantinformationabouttheinvestmentcompany,anditmaybeobtainedbycalling800-915-6566orvisitinggafunds.com.Readitcarefullybeforeinvesting.

Investmentsinforeignsecuritiesinvolvegreatervolatility,political,economicandcurrencyrisksanddifferencesinaccountingmethods.Theserisksaregreaterforemergingmarketscountries.Non-diversifiedfundsconcentrateassetsinfewerholdingsthandiversifiedfunds.Therefore,non-diversifiedfundsaremoreexposedtoindividualstockvolatilitythandiversifiedfunds.Investmentsindebtsecuritiestypicallydecreaseinvaluewheninterestratesrise,whichcanbegreaterforlonger-termdebtsecurities.Investmentsinderivativesinvolverisksdifferentfrom,andincertaincases,greaterthantheriskspresentedbytraditionalinvestments.Investmentsinsmallercompaniesinvolveadditionalriskssuchaslimitedliquidityandgreatervolatility.Fundsconcentratedinaspecificsectororgeographicregionmaybesubjecttomorevolatilitythanamorediversifiedinvestment.Investmentsfocusedinasinglegeographicregionmaybeexposedtogreaterriskthaninvestmentsdiversifiedamongvariousgeographies.Investmentsfocusedontheenergysectormaybeexposedtogreaterriskthaninvestmentsdiversifiedamongvarioussectors.

MSCIACPacificEx-JapanIndexisamarketcapitalizationweightedindexthatmonitorstheperformanceofstocksfromthePacificregion,excludingJapanconsistingofAustralia,China,HongKong,Indonesia,Korea,Malaysia,NewZealand,Philippines,Singapore,Taiwan,andThailand.

DXYistheUSDollarIndexandindicatesthegeneralinternationalvalueoftheUSDollar.ItdoesthisbyaveragingtheexchangeratesbetweentheUSDandmajorworldcurrencies.TheIntercontinentalExchangeInc(ICE,whichoperatesglobalcommodityandfinancialproductsmarketplaces)computesthisbyusingtheratessuppliedbysome500banks.

OnecannotinvestdirectlyinanIndex.

GuinnessAtkinsonAsiaPacificDividendBuilderFundManagersMonthlyUpdate–January2018

Price/EarningsRatio(P/E)isanequityvaluationmultiple.Itisdefinedasmarketpricepersharedividedbyannualearningspershare.

Opinionsexpressedaresubjecttochange,arenotaguaranteeandshouldnotbeconsideredinvestmentadvice.Pastperformanceisnotindicativeoffutureresults.

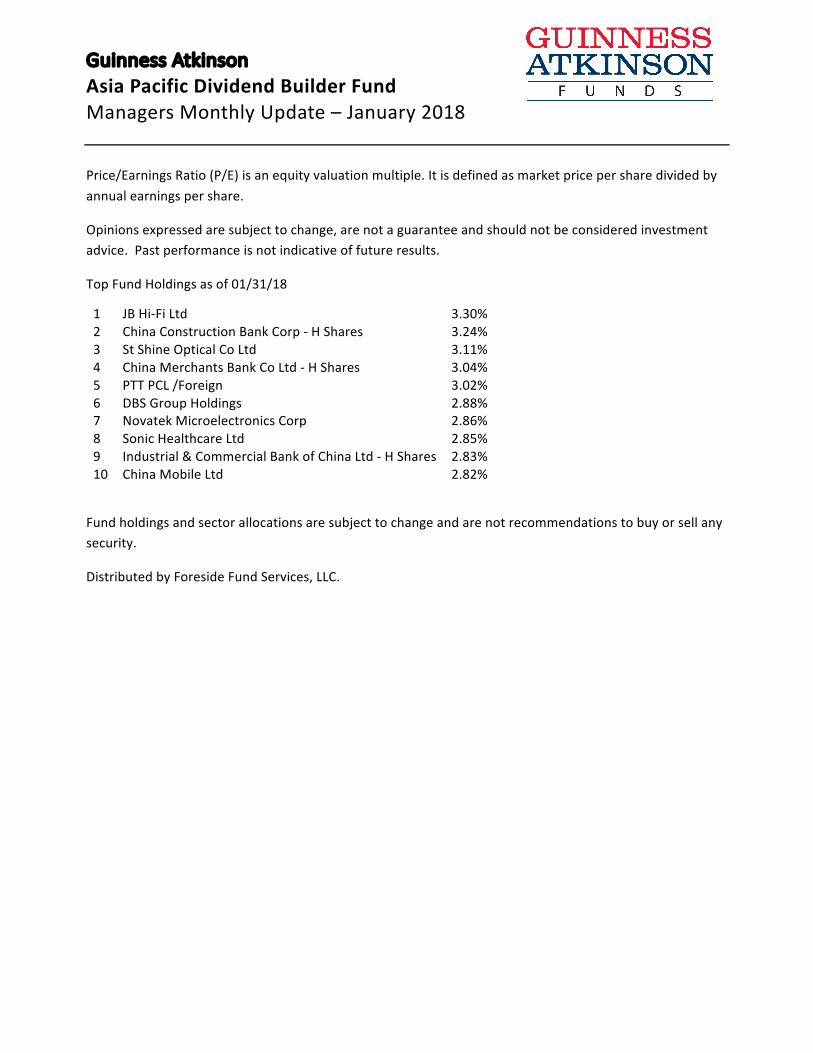

TopFundHoldingsasof01/31/18

1 JBHi-FiLtd 3.30%2 ChinaConstructionBankCorp-HShares 3.24%3 StShineOpticalCoLtd 3.11%4 ChinaMerchantsBankCoLtd-HShares 3.04%5 PTTPCL/Foreign 3.02%6 DBSGroupHoldings 2.88%7 NovatekMicroelectronicsCorp 2.86%8 SonicHealthcareLtd 2.85%9 Industrial&CommercialBankofChinaLtd-HShares 2.83%10 ChinaMobileLtd 2.82%

Fundholdingsandsectorallocationsaresubjecttochangeandarenotrecommendationstobuyorsellanysecurity.

DistributedbyForesideFundServices,LLC.