guidelines for preparing capital expenditure program 2015

DESCRIPTION

This is a useful document for preparing capex in network planningTRANSCRIPT

1

Guidelines for Preparing Capital Expenditure Program 2015

Issued by : Budgetary Control Wing, PTCL H/Qs, Islamabad

2

ContentsDEFINITIONS..................................................................................................................................................3

Assets ....................................................................................................................................................3

Capital ...................................................................................................................................................3

Capital Expenditure...............................................................................................................................3

Capital Expenditure Program................................................................................................................ 3

Current Assets .......................................................................................................................................4

Financial Feasibility ...............................................................................................................................4

Fixed Assets/ Non-Current Assets.........................................................................................................4

Overheads .............................................................................................................................................4

Project ...................................................................................................................................................4

Project Implementation Plan (PIP)........................................................................................................4

BUDGETING & PLANNING PROCESS OVERVIEW...........................................................................................5

PURPOSE .......................................................................................................................................................7

NON-PERMISSIBLE EXPENSES WITHIN A CAPITAL PROJECT .........................................................................8

SCOPE............................................................................................................................................................ 9

PRELIMINARY APPRAISAL BY PROJECT INITIATOR/ END USER ...........................................................10

POST PRELIMINARY APPRAISAL BY PLANNING WING:........................................................................11

DETAILED APPRAISAL BY FINANCE WING ...........................................................................................12

REVENUE PARAMETERS ..............................................................................................................................13

OPERATING EXPENDITURE PARAMETERS (OPEX).......................................................................................16

SCENARIO/ SENSITIVITY ANALYSIS..............................................................................................................16

APPRAISAL OF NON-COMMERCIAL PROJECTS............................................................................................16

REVIEW USING TENDER/ CONTRACT PRICES..............................................................................................18

DELAY IN PROJECT IMPLEMENTATION .......................................................................................................18

3

DEFINITIONS

AssetsAnything of material value or usefulness that is owned by a person or company for generating revenues for business is called as an Asset.

Capital1. Capital is the money that is used to generate income or to make an investment.2. Cash or goods used to generate income by investing in the business.

Capital ExpenditureCapital expenditures (CAPEX) are incurred to have future benefits. A capital expenditure is incurred when a business spends money either to buy fixed assets or to add to the value ofan existing fixed asset resulting in extension in the useful life of that asset beyond one accounting year. Capital expenditure is incurred on:

a. Acquiring fixed assets.b. Fixing problems with an asset that existed prior to acquisition.c. Preparing an asset to be used in business.d. Legal costs of establishing or maintaining one's right of ownership in a piece of

property.e. Restoring property, plant and equipment or adapting it to a new or different use.f. Enhancement of capacity or increase in useful life of existing asset.g. Starting a new business.

In accounting, normally a capital expenditure is added to an asset account i.e. capital work in progress account and on completion of the asset, this account is closed which is called as capitalization thus resulting in increase of asset's base. In some cases the assets are directly charged to Fixed assets acquired through direct purchases e.g. land, building, vehicles etc.(Admn CAPEX).

Capital Expenditure ProgramThe Capital Expenditure Program explains the proposed financial commitment of planned capital projects and its respective cash out flow during a year and its phasing as the project life can be more than one year.

4

Current AssetsA current asset is an asset which is expected to be sold or otherwise used up in the near future, usually within one year, or one business cycle whichever is longer. Typical current assets include cash, cash equivalents, accounts receivable, inventory, the portion of prepaid accounts which will be used within a year, and short-term investments.

Financial FeasibilityFinancial feasibility is a study to check that the proposed project is giving higher rate than expected rate of return after taking into consideration its total cost and probable revenues over a period of its useful life. In other words, it is the decision whether to go for the project or not.

Fixed Assets/ Non-Current AssetsA long-term tangible piece of property that a company owns and uses in the production of its income and is not expected to be consumed or converted into cash any sooner than at least one year's time.

Overheads1. Overhead or overhead expense refers to an ongoing expenses on the projects that

cannot be directly identified to a specific project/sub project.2. Resource consumed or lost in completing a process that does not contribute directly

to the end product.3. Overhead (OH) expenses are all costs except for direct labour, direct materials, and

direct expenses. Overhead expenses include accounting fees, advertising, insurance, interest, legal fees, labor burden, rent, repairs, supplies, taxes, travel expendituresand utilities, etc.

ProjectProposals for capital investment/ expenditure that are required by the company for expansion of networks, increase in capacity and diversity, to improve quality, efficiency, rehabilitation of existing networks, introduction of new services and to acquire new technology that would result in operational cost savings etc. are called projects.

Project Implementation Plan (PIP)A Project Implementation Plan is used to identify activities associated with an implementation to ensure adequate preparation has taken place and adequate contingencies are in place.

5

BUDGETING & PLANNING PROCESS OVERVIEW

As per Finance and Accounting Manual, the budgeting activities of the company are broadly divided into two categories, which are:

1. Long term planning in the form of Business plan which covers period of five years, and 2. Short term planning in the form of Annual Corporate Budget.

The business plan is updated and revised every year along with annual corporate budget. The company’s short term planning process is a part of annual budgeting process which should be in line with the business plan.

The planning and budgeting process result in series of related budgets. The budgeting process at the Regions/ Zones/ Headquarters is initiated once the strategic plan within business plan has been finalized. Due to interdependencies between the budgets and to enable the effective and efficient preparation of annual corporate budget, the sequence of preparation of the budgets is as follows:

1. Revenue budget.2. Capital Expenditure budget.3. Human Resource budget.4. Non Project Capital budget, and5. Operating budget.

Each owner/ budgeting unit is responsible for preparation of its budget but it is the responsibility of Finance wing to consolidate all budgets received from appropriate controlling departments to prepare Annual Corporate Budget.

The business plan and annual corporate budget is submitted to PTCL BoD for review and approval in October every year.

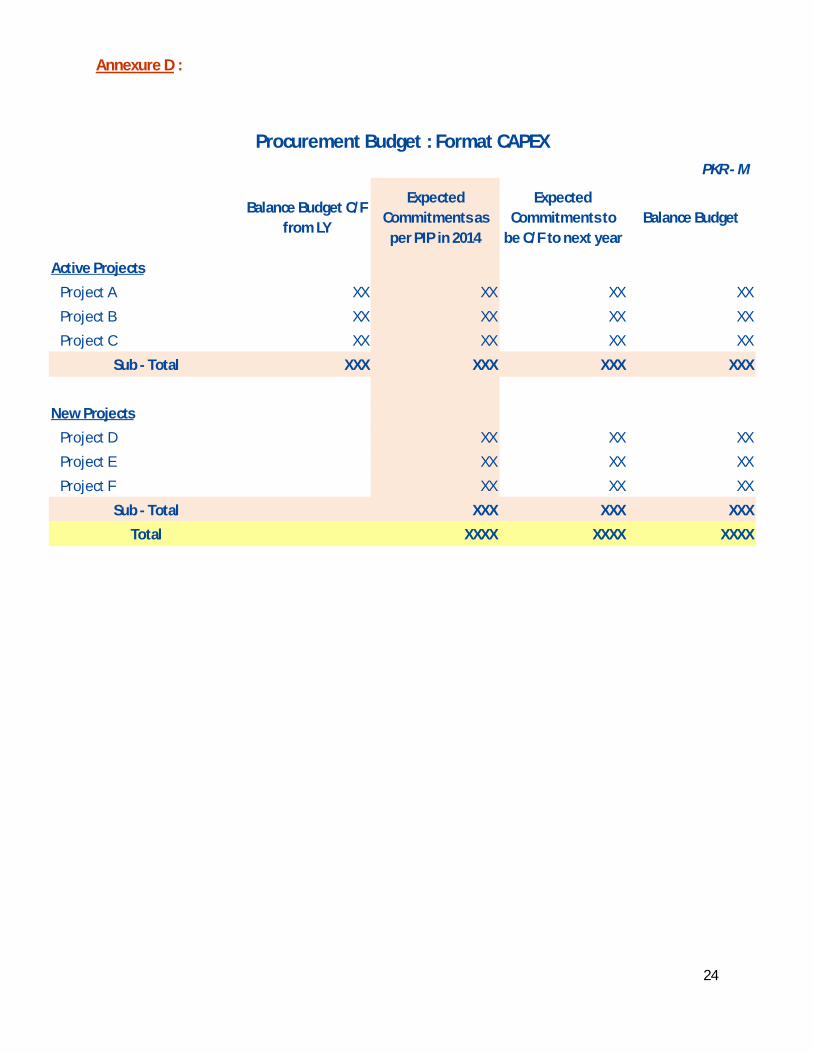

In order to monitor and smooth management of CAPEX for the year, it is essentially required to have an insight of expected CAPEX and commitment of the Company against all projects of CAPEX 2015. In this regard, a concept of Procurement budget has been introduced. This Procurement budget would give the details of actual CAPEX, actual and expected commitmentsagainst all projects, commitment for the year 2015, CAPEX and capitalization outlook for year2015, etc. Format of procurement budget is placed at Annexure D.

Further, to capture information for procurement budget, it is required that Project Implementation Plan (PIP) for every planned investment is made part of planning and financial appraisal process. The information provided in PIP would be used as input for preparation and reporting of Company vide Procurement budget.

Procurement wing will provide a monthly report of commitments issued/ finalized against all projects against prescribed format placed at Annexure E to Budgetary Control wing.

6

Process flow for budgeting, planning and execution of projects relating to Corporate Sector is under process and will be made part of these guidelines as and when finalized.

7

PURPOSE

The purpose of these guidelines is to ensure that before entering into major infrastructure expenditures, it is essential to undertake a detailed review of this expenditure in order to gauge its feasibility. A more thorough and disciplined approach is required so that capital expenditure proposals are adequate at time of approval and to ensure that PTCL does not find itself in an adverse financial position afterwards. Therefore, these guidelines have been revised to:

Have systematic appraisal of all capital projects in order to ensure that the best choices have been opted so that better returns can be obtained.

Introduce greater consistency in project appraisal while maintaining a meticulous approach.

Reflect changes in financial evaluation, project appraisal, Provide more clarity and greater understanding in relation to the roles of all those

involved in approving capital expenditure.

PTCL has entered into ERP-SAP environment, so it is required that investment proposals are generated in SAP-Investment Management (IM) module. The IM module provides functions to support planning, investment and financing processes, so the integrated planning process allows rolling up planned values (budget) from appropriation requests. It also measures the investment program (project) to which they are assigned i.e. SAP is an integrated system so the budgetary control on capital projects will be established from SAP IM module as soon as any business proposal is finalized.

Release Strategy (RS) mechanism has been implemented in ERP-SAP for strengthening of budgetary controls on CAPEX processes. This process flow is applicable to Capital Expenditures like Business CAPEX, Deposit Works, USF Projects etc. however it is not applicable to Admin CAPEX. Release strategy comprises of following two stages:

1. After approval of project by relevant authority as per Authority Matrix and creation of Project structure in SAP by Project Planning & Capitalization (PP&C) wing, project structure will be released by Budgetary Control Wing.

2. After release of project structure, PP&C will allocate budget at WBSE level in SAP. Budget for projects will be released by Budgetary Control wing on the basis of actual BOQ and relevant information as and when required.

It is mentioned that no transaction/ financial activity in SAP would take place without release of project structure and budget.

8

NON-PERMISSIBLE EXPENSES WITHIN A CAPITAL PROJECT

Expenses of following items should not be included in Projects as capital expenditure:

a) POLb) Stationery and Printingc) Wages of daily paid staffd) Purchase of furniture and fittingse) Purchase of Vehiclesf) Repair and Maintenance of Vehicles/ Buildingsg) Purchase of Office Equipmenth) TA/DA, etc.

9

SCOPE

These guidelines are limited to capital projects only and explain the process flow for formulating capital projects as follows:

1. Preliminary appraisal by project initiator/ end user.2. Post preliminary appraisal by Planning Wing.3. Detailed financial appraisal/cost vetting by Finance Wing.

The abovementioned three stages are elaborated in following paragraphs:

10

PRELIMINARY APPRAISAL BY PROJECT INITIATOR/ END USERPreliminary appraisal will be carried over by the project initiator/ department/ region before sending official capital investment proposal to Project Planning Wing. This aims to assess that the project proposal has sufficient merit to justify a full detailed appraisal.

a. Concept/ Initial PlanPreliminary work on potential projects will be undertaken by regions/end user or relevant department

b. Need AnalysisIt is important to demonstrate a clear need for a particular project proposal. The need analysis should be aligned to Company’s strategic objectives, highlighting how a proposed project helps to achieve these goals. The analysis should describe clearly:

The reasons for incurrence of Capital expenditure along with the extent and urgency of the project.

Supporting with statistical data and baseline information justifying the need for capital expenditure at that point of time.

The trade off results if the project is not undertaken

c. Risks AssociatedRegions/End User must assess the main areas of risk that might prevent a project from delivering anticipated results/outputs.

Cost overruns, including those resulting from inflation or foreign exchange ratefluctuations

Any Regulatory difficulties Chances of delays in project implementation due to any other reason.

11

POST PRELIMINARY APPRAISAL BY PLANNING WING:After the investment has been analyzed in accordance with above mentioned criterion, a formal CIP should be initiated in Project Planning and Capitalization (P P & C) Department. The capital investment proposal (CIP), when forwarded to Finance wing must contain the followinginformation complete in all respect:

1. Name, Type of the Project and Location/Sites.2. Project description.3. Budget provision and cash flows in Annual capital expenditure program 2015 along

with yearly breakdown of expenditure.4. Category/sector under which the project falls.5. Verification of allied services likely to be provided with the major element of CIP.6. Relevance/ benefit of the project with regard to the existing capital projects/ future

projects. 7. Explore all the alternatives, in case the project does not become viable/ not approved.8. Project Implementation Plan (PIP) highlighting critical activities, costs, expected

difficulties and schedules that are required to achieve the objectives of the investment proposal.

9. Estimated capital costs with detailed BOQ mentioning separately cost of each and every cash and store item along with the break-up under major asset heads of expenditure and aggregation of the same on site level.

10. Pending/ projected demand for services covered under the capital expenditure project. Projects of additional capacities of fixed line, WLL, DSL, DXX, DRS etc should mention the capacities separately which should be given by the concerned head/ project owneralong with yearly physical phasing.

11. For expansion projects, where services are already provided, the existing ARPUs for all the services covered for respective region/ exchange should be provided separately by the project owner.

12. For any project proposal prepared for new service, approved tariffs verified from commercial department should be annexed with the proposal.

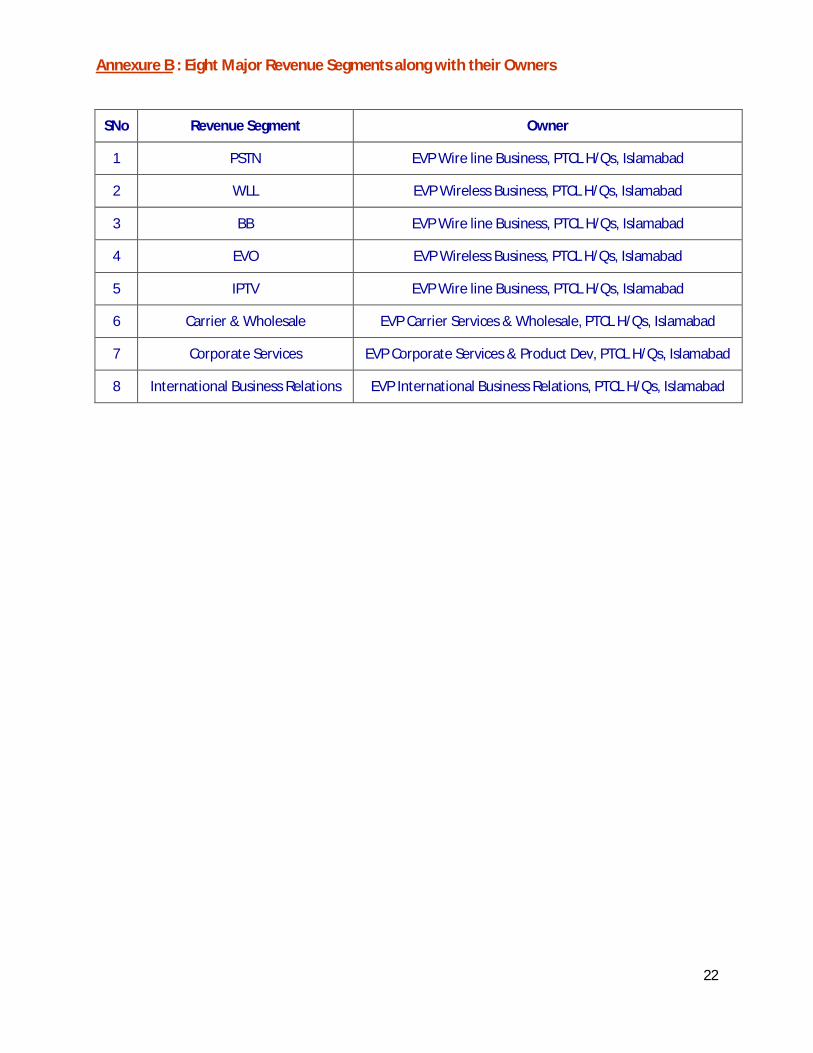

13. Number of yearly active customers, tariffs, etc should be verified by Commercial department. At present, there are eight major revenue segments and these segments along with their owners are attached as Annexure B.

14. Estimates of any incremental operating costs associated with the project.15. Cost benefit analysis of those projects which have no direct revenues, must be

mentioned clearly by taking assumptions of e.g. saving in operating cost, improvement in the efficiency of system, personnel, reduction in churn/ bad debts etc. However, these assumptions should have solid justification and vetting by respective department.

16. Useful life of each capital project.

12

DETAILED APPRAISAL BY FINANCE WINGDetailed appraisal will be carried out when the project is forwarded to Finance Department after furnishing all the above mentioned requisite information. In case any vital information is not provided the case will be returned to GM (PP&C) without financial vetting/feasibility. This appraisal will facilitate to arrive at a decision by considering the financial results.

I. Cost VettingProject’s proposed costs will be checked by Finance Department in the following perspectives;

The project is identified in Annual Capital expenditure Program for the year 2015. That budgeted costs are complete and realistic.

Apart from cost vetting, Finance wing will also allocate provision of Overheads charges (OH) to every capital project @ 9% (inclusive of disallowed GST) of total capital cost of eachproject. This rate may vary on the basis of CAPEX Budget approved by BOD.

II. Financial AppraisalIn order to carry out the financial appraisal, following techniques will be applied to assess the financial feasibility of the project keeping in view the life of the project:

Cash Flow Analysis Profit and Loss Account Projections Net Present Value (NPV) @ 16% discount rate Internal Rate of Return (IRR) Payback Period

III. Commitment Certificate Before finalizing financial feasibility of projects where revenue/ cost savings is forecasted by respective revenue owner/ project owner against new/ additional capacities deployed, the respective revenue owner/ project owner and EVP NP&S will provide a certificate as in Annexure C. This will be the certification of planned installed capacity, sale of services/ loading of lines, ARPU, etc. upon which yearly inflows/ benefits to the company are estimated and feasibility is based.

13

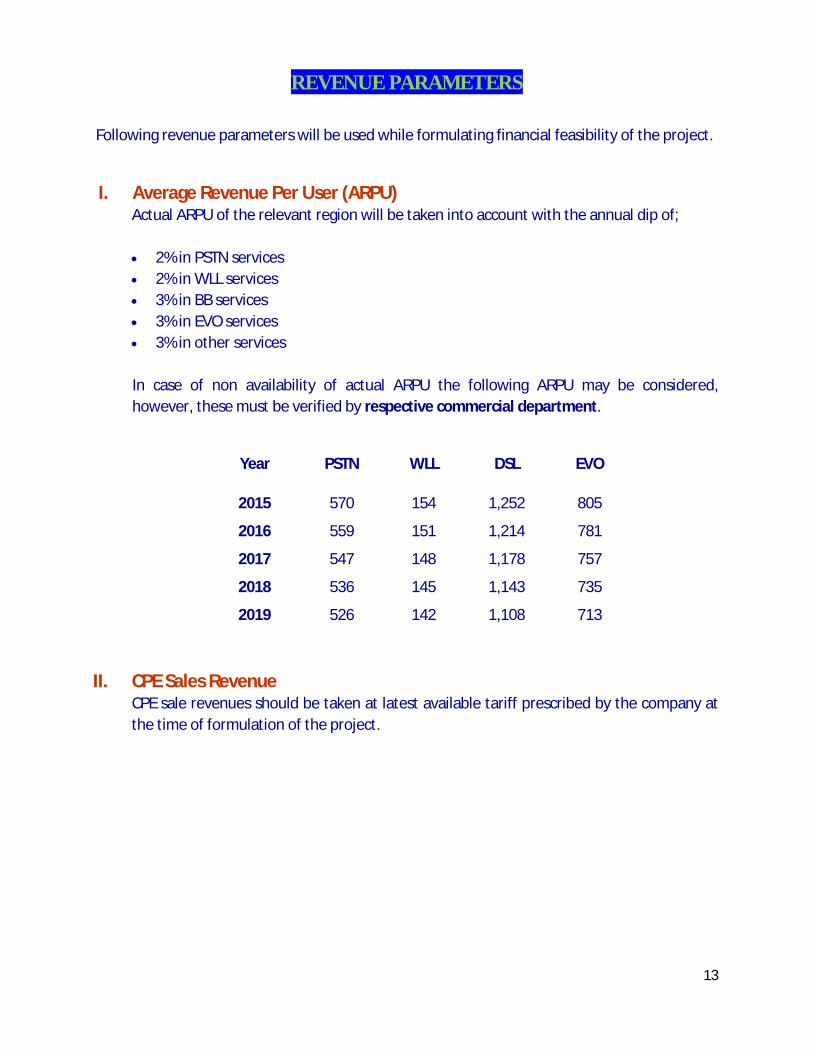

REVENUE PARAMETERS

Following revenue parameters will be used while formulating financial feasibility of the project.

I. Average Revenue Per User (ARPU)Actual ARPU of the relevant region will be taken into account with the annual dip of;

2% in PSTN services 2% in WLL services 3% in BB services 3% in EVO services 3% in other services

In case of non availability of actual ARPU the following ARPU may be considered, however, these must be verified by respective commercial department.

Year PSTN WLL DSL EVO

2015 570 154 1,252 805

2016 559 151 1,214 781

2017 547 148 1,178 757

2018 536 145 1,143 735

2019 526 142 1,108 713

II. CPE Sales RevenueCPE sale revenues should be taken at latest available tariff prescribed by the company at the time of formulation of the project.

14

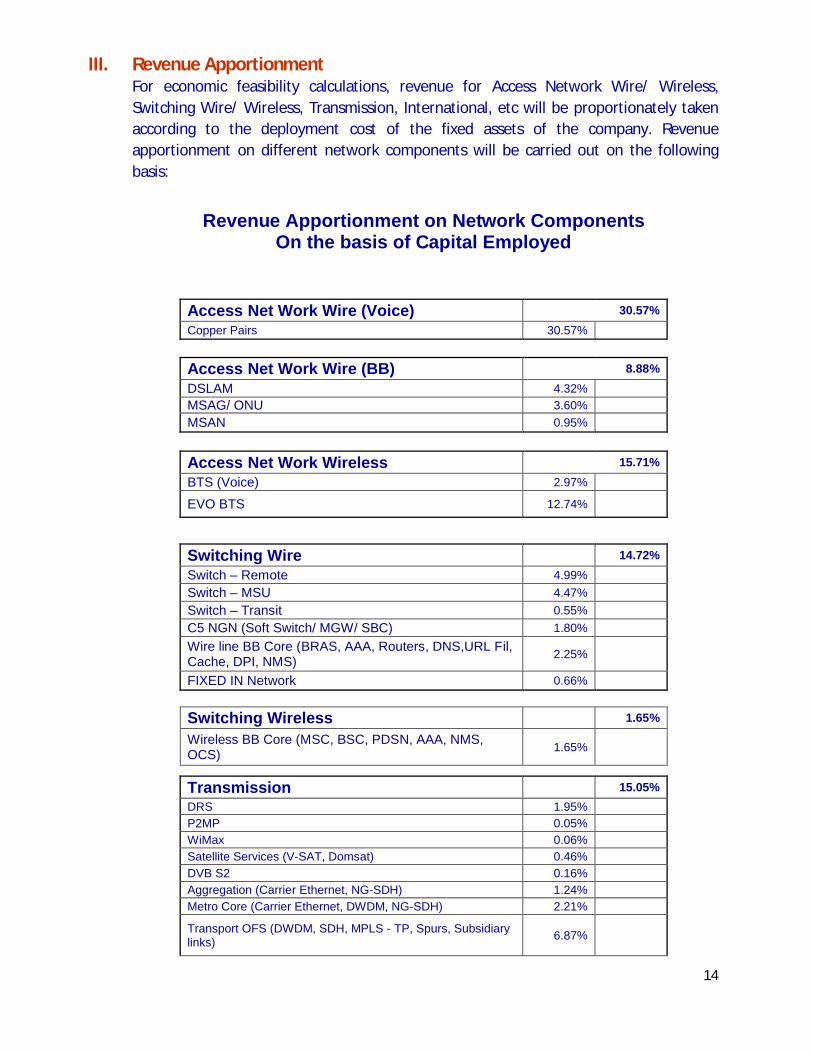

III. Revenue ApportionmentFor economic feasibility calculations, revenue for Access Network Wire/ Wireless, Switching Wire/ Wireless, Transmission, International, etc will be proportionately taken according to the deployment cost of the fixed assets of the company. Revenue apportionment on different network components will be carried out on the following basis:

Revenue Apportionment on Network Components On the basis of Capital Employed

Access Net Work Wire (Voice) 30.57%

Copper Pairs 30.57%

Access Net Work Wire (BB) 8.88%

DSLAM 4.32%

MSAG/ ONU 3.60%

MSAN 0.95%

Access Net Work Wireless 15.71%

BTS (Voice) 2.97%

EVO BTS 12.74%

Switching Wire 14.72%

Switch – Remote 4.99%

Switch – MSU 4.47%

Switch – Transit 0.55%

C5 NGN (Soft Switch/ MGW/ SBC) 1.80%

Wire line BB Core (BRAS, AAA, Routers, DNS,URL Fil, Cache, DPI, NMS)

2.25%

FIXED IN Network 0.66%

Switching Wireless 1.65%

Wireless BB Core (MSC, BSC, PDSN, AAA, NMS, OCS)

1.65%

Transmission 15.05%

DRS 1.95%P2MP 0.05%WiMax 0.06%Satellite Services (V-SAT, Domsat) 0.46%

DVB S2 0.16%Aggregation (Carrier Ethernet, NG-SDH) 1.24%Metro Core (Carrier Ethernet, DWDM, NG-SDH) 2.21%

Transport OFS (DWDM, SDH, MPLS - TP, Spurs, Subsidiary links)

6.87%

15

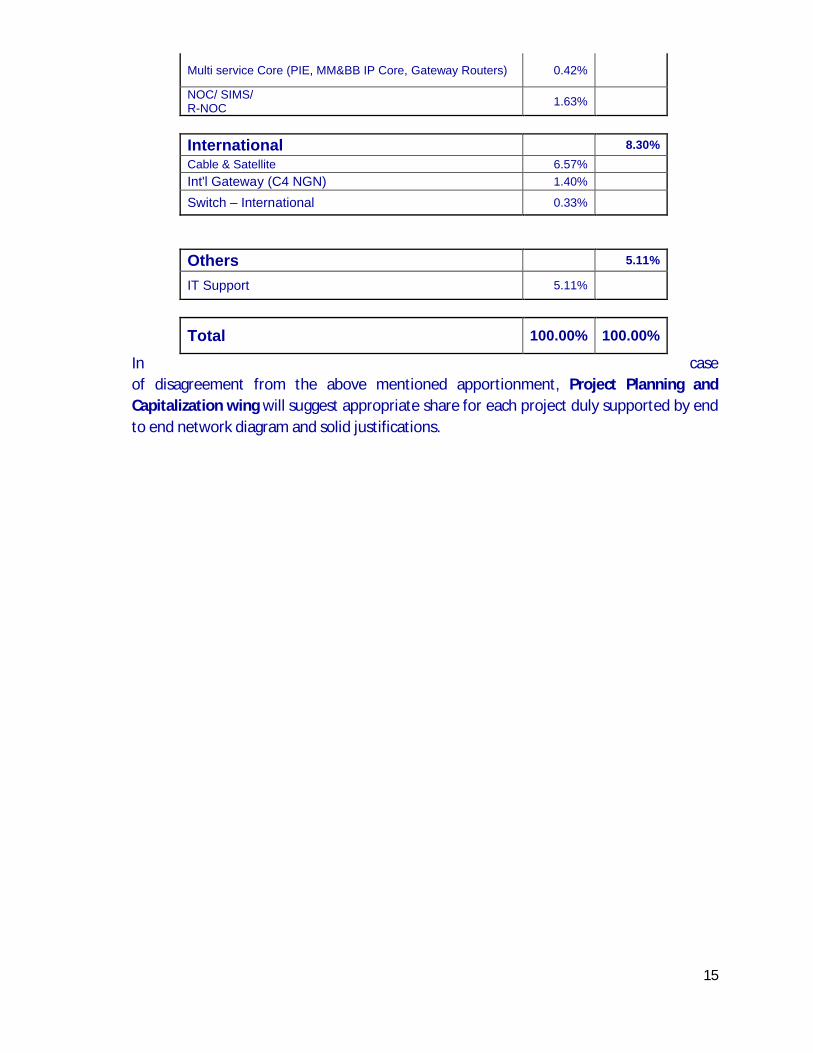

In case of disagreement from the above mentioned apportionment, Project Planning and Capitalization wing will suggest appropriate share for each project duly supported by end to end network diagram and solid justifications.

Multi service Core (PIE, MM&BB IP Core, Gateway Routers) 0.42%

NOC/ SIMS/R-NOC

1.63%

International 8.30%

Cable & Satellite 6.57%

Int'l Gateway (C4 NGN) 1.40%

Switch – International 0.33%

Others 5.11%

IT Support 5.11%

Total 100.00% 100.00%

16

OPERATING EXPENDITURE PARAMETERS (OPEX)

Following major expenses are to be considered separately while formulating a capital investment project.

General OPEX

o Marketing expense o Miscellaneous expenseso R & D , Annual licenses fee, TSA and USF o Repair and maintenance o Fuel and powero Depreciationo Employment cost o Interconnect cost

Specific as per project’s nature

o Bad debts expenseso Dealer Commissiono Customer Retention Costo Cost of Customer Premises Equipment o RUIM/ CPE chargeso Foreign Operator’s Costo Bandwidth Costo Any other than the above

The rates of different OPEX components are attached as Annexure A respectively.

SCENARIO/ SENSITIVITY ANALYSIS

The cost of large and mega projects will be adjusted to reflect different scenarios based upon variations in key assumptions. Sensitivity analysis of the project will also be undertaken byexamining the effect on the key financial elements on varying the main assumptions of the project (including the discount rate).

APPRAISAL OF NON-COMMERCIAL PROJECTS

17

In the case of non-commercial projects, cost benefit analysis will be carried out to assesswhether the costs benefits associated with a project are greater than its capital costs?

18

REVIEW USING TENDER/ CONTRACT PRICES

When a tender price becomes available, the case for proceeding with the proposal should again be reviewed. If tenders are over the approved limit re-appraisal may be required to determine whether the project should be abandoned or proceeded with.

DELAY IN PROJECT IMPLEMENTATION

If a decision is taken to defer a project, then it should be resent to finance department for full re-evaluation before being started again.

19

20

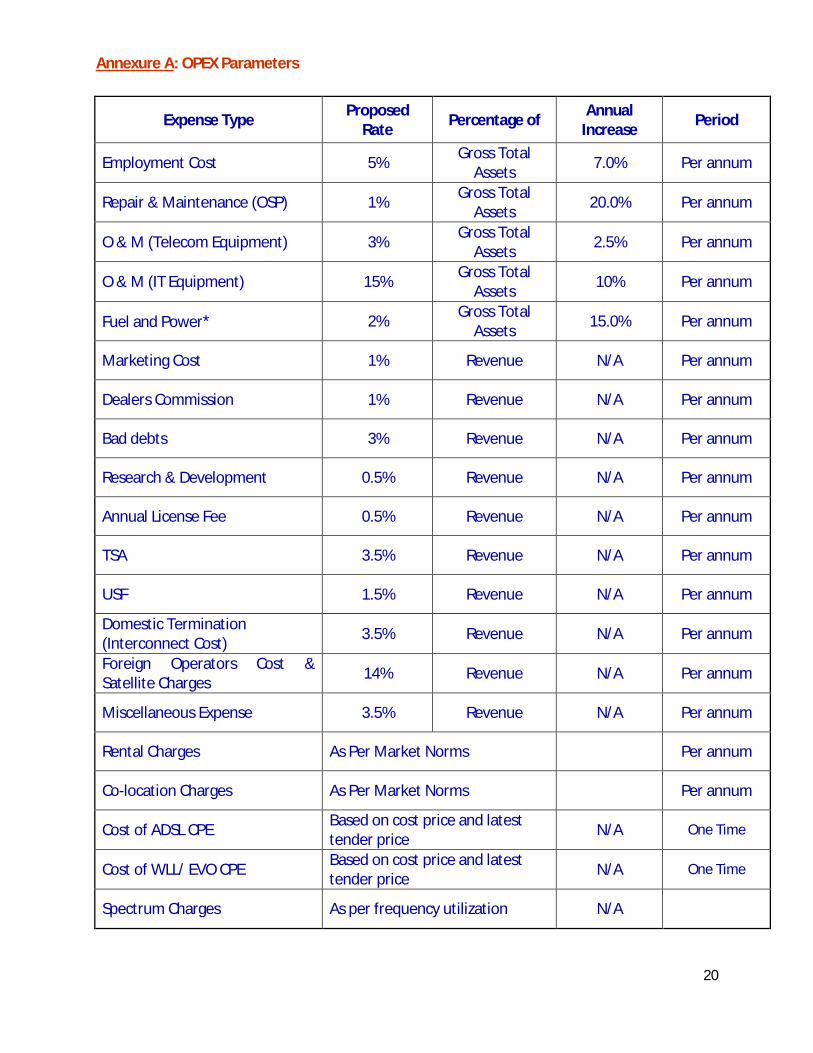

Annexure A: OPEX Parameters

Expense Type Proposed Rate Percentage of Annual

Increase Period

Employment Cost 5% Gross Total Assets 7.0% Per annum

Repair & Maintenance (OSP) 1% Gross Total Assets 20.0% Per annum

O & M (Telecom Equipment) 3% Gross Total Assets 2.5% Per annum

O & M (IT Equipment) 15% Gross Total Assets 10% Per annum

Fuel and Power* 2% Gross Total Assets 15.0% Per annum

Marketing Cost 1% Revenue N/A Per annum

Dealers Commission 1% Revenue N/A Per annum

Bad debts 3% Revenue N/A Per annum

Research & Development 0.5% Revenue N/A Per annum

Annual License Fee 0.5% Revenue N/A Per annum

TSA 3.5% Revenue N/A Per annum

USF 1.5% Revenue N/A Per annum

Domestic Termination(Interconnect Cost) 3.5% Revenue N/A Per annum

Foreign Operators Cost & Satellite Charges 14% Revenue N/A Per annum

Miscellaneous Expense 3.5% Revenue N/A Per annum

Rental Charges As Per Market Norms Per annum

Co-location Charges As Per Market Norms Per annum

Cost of ADSL CPE Based on cost price and latest tender price N/A One Time

Cost of WLL/ EVO CPE Based on cost price and latest tender price N/A One Time

Spectrum Charges As per frequency utilization N/A

21

*It should be calculated on the basis of projected consumption, capacity and usage of the

project as per requirements, however, in the absence of these details above mentioned rate

would be taken.

The above-mentioned rates are based on the averages of actual data; however these rates can be changed depending on the nature of project.

22

Annexure B : Eight Major Revenue Segments along with their Owners

SNo Revenue Segment Owner

1 PSTN EVP Wire line Business, PTCL H/Qs, Islamabad

2 WLL EVP Wireless Business, PTCL H/Qs, Islamabad

3 BB EVP Wire line Business, PTCL H/Qs, Islamabad

4 EVO EVP Wireless Business, PTCL H/Qs, Islamabad

5 IPTV EVP Wire line Business, PTCL H/Qs, Islamabad

6 Carrier & Wholesale EVP Carrier Services & Wholesale, PTCL H/Qs, Islamabad

7 Corporate Services EVP Corporate Services & Product Dev, PTCL H/Qs, Islamabad

8 International Business Relations EVP International Business Relations, PTCL H/Qs, Islamabad

23

Annexure C

Year Installed Capacity/

Drivers of Cost SavingsLoading ARPU

Total Revenue/ Cost Savings

2014

2015

2016

2017

2018

2019

Certified that the above customers and revenue/ cost savings projections taken in feasibility are correct and acceptable for additional revenue in my revenue targets for the respective years Respective Revenue Owner

Certified that the additional/ new capacities taken in feasibility are correct and willenhance the existing capacities in the respective years as mentioned above EVP NP&S

COMMITTED REVENUE/ COST SAVINGS for______________

Project Name

24

Annexure D :

PKR - M

Balance Budget C/F from LY

Expected Commitments as

per PIP in 2014

Expected Commitments to

be C/F to next yearBalance Budget

Active Projects

Project A XX XX XX XX

Project B XX XX XX XX

Project C XX XX XX XX

Sub - Total XXX XXX XXX XXX

New Projects

Project D XX XX XX

Project E XX XX XX

Project F XX XX XX

Sub - Total XXX XXX XXX

Total XXXX XXXX XXXX

Procurement Budget : Format CAPEX

25

Annexure E

PO Ref SAP #Foreign Portion

CFR USDLocal Portion

PKRTotal Amount

PKR

1

2

3

4

5

- - -

Amount

Total

Statement of Contracts Signed during xxxx

As On <Date>

SNoProject

#

Contract No.Title of Contract

Vendor Name

Date Of Signing

Delivery Period

26

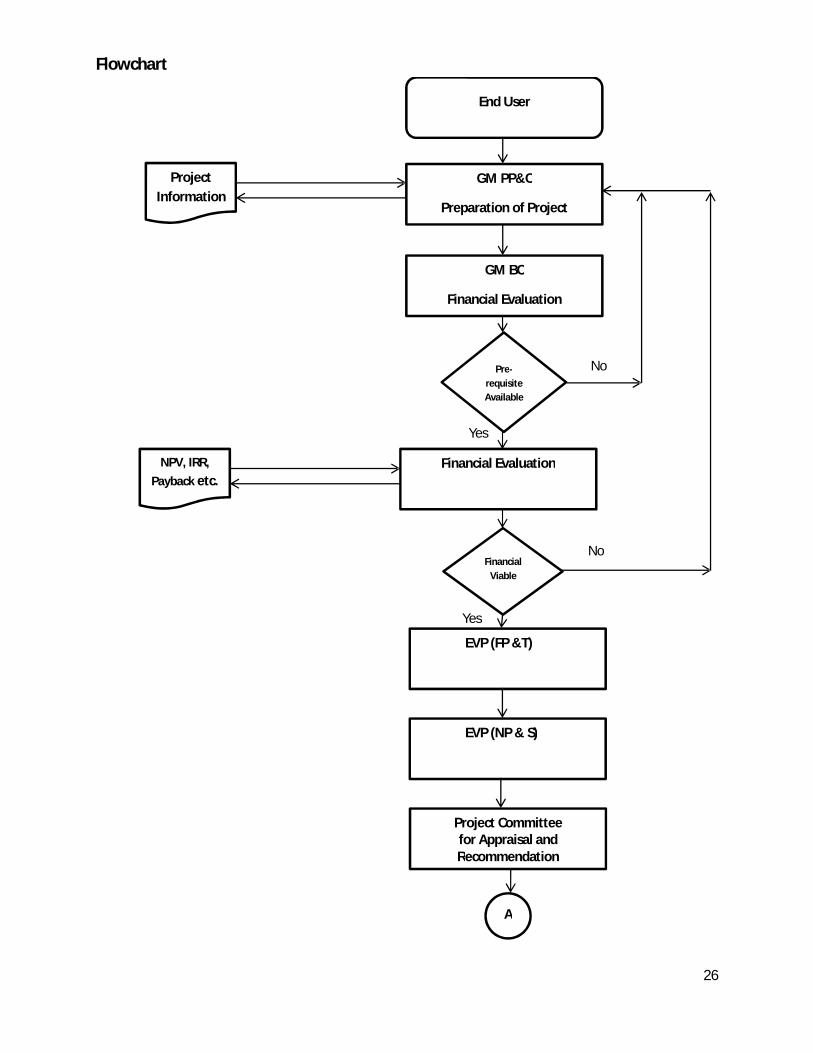

Flowchart

No

Yes

No

Yes

End User

Project Information

GM PP&C

Preparation of Project

GM BC

Financial Evaluation

Pre-requisiteAvailable

NPV, IRR, Payback etc.

Financial Evaluation

Financial Viable

Project Committee for Appraisal and Recommendation

EVP (NP & S)

EVP (FP &T)

A

27

No

Yes

No

Yes

No

Yes

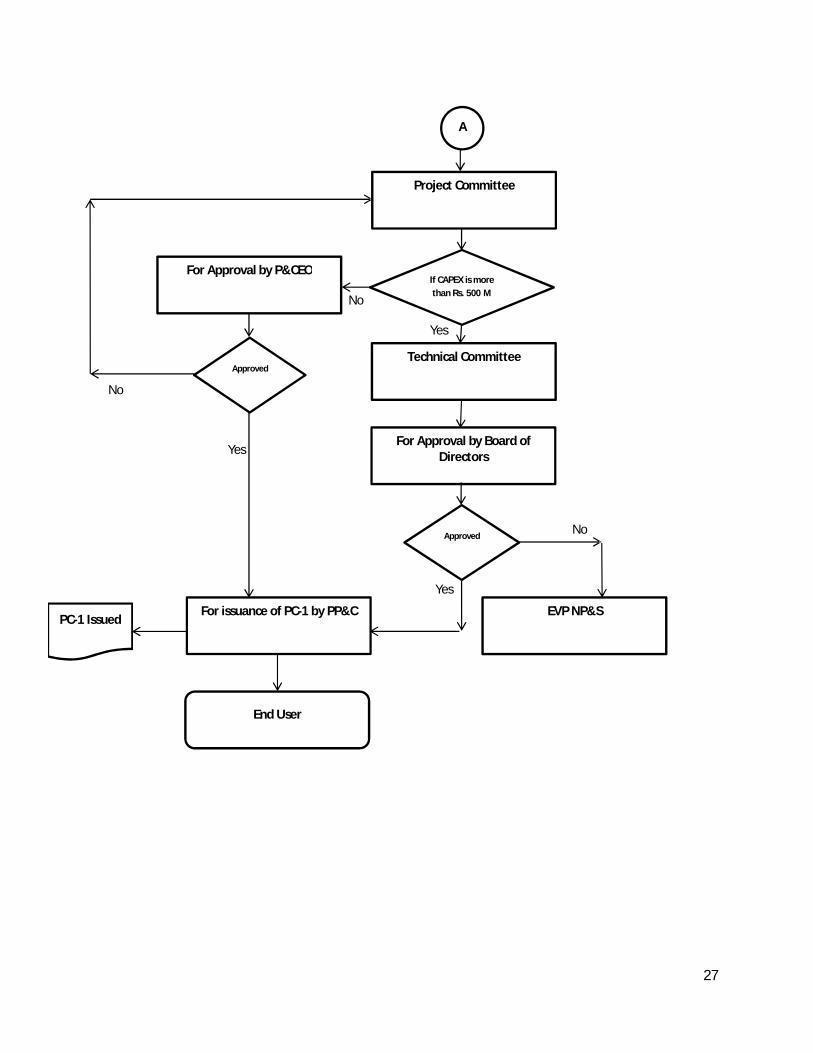

A

Project Committee

If CAPEX is more than Rs. 500 M

Technical Committee

For Approval by P&CEO

For issuance of PC-1 by PP&C

For Approval by Board of Directors

Approved

Approved

PC-1 Issued

End User

EVP NP&S