guide to buying an investment property - … guides/guide-to... · • jargon buster p 15 ......

TRANSCRIPT

Guide to buyingan investment property

The Ultimate Guide To Buying an Investment

Property

P 1Guide to buying an investment property

CONTENTS

• Why get your investment loan with loans.com.au P 2

• Breakout: The onTrack Advantage P 3

• The property investment process P 4

1. Decide what you want to buy P 5

2. How much can you afford? P 6

3. Other costs to consider P 7

4. Getting pre-qualified P 8

5. Making an offer P 9

6. Our investment property loan process to settlement P 10

7. Repaying your loan P 13

• Documents to get a loan P 14

• Jargon Buster P 15

• About loans.com.au P 16

• Contact P 17

P 2Guide to buying an investment property

WHY GET YOUR INVESTMENT LOAN WITH LOANS.COM.AU

The simple process at loans.com.au

1. Apply online

2. Talk to a specialist lender in our Australian-based call centre

3. Upload your documents and track the progress of your loan using the onTrack website plus mobile app

4. Access your account online, VISA, ATM

This is an exciting time to get an investment property loan with loans.com.au.

At loans.com.au we are proud to offer one of the most competitive interest rates in Australia for customers who want to invest in property.

You can save thousands of dollars on your loan and pay it off sooner with loans.com.au.

Benefits include:

• Award-winning investment loans packed with features

• A game-changing online model which means we can pass on ultra-low interest rates to our customers

• Simple online application process with our innovative onTrack system

• Borrow safe in the knowledge that we are secure, powered by Firstmac, which has been in business for over 38 years

To find out how much you can borrow, just use our handy borrowing power calculator.

If you are ready to apply for a loan, you can get started now by filling out one of our easy online applications here. It only takes a few minutes.

Otherwise, keep reading to learn more about the journey to buying an investment property.

P 3Guide to buying an investment property

Canstar 5 star award for 2017

outstanding value

BREAKOUT: THE onTrack ADVANTAGE

onTrack is our innovative online portal which allows you to complete your loan application entirely on your handheld device or computer from initial contact through to settlement and beyond.

Using onTrack means that you are able to complete your loan application in your own time. You don’t have to wait for a bank branch to open to complete your investment property loan!

onTrack allows you to download all required forms and documents as well as allowing you to book an

appointment with one of our loan specialists at a time that suits you. You can securely submit your forms and supporting documents.

You can also:

• track the status of your loan,including what you havesubmitted, what we aredoing, and what you need todo next

• communicate with your loansupport officer through areal-time messaging system

onTrack is an end-to-end system, making your switch to loans.com.au hassle free and fast

onTrack gives you more control to fast track your investment property loan and more knowledge than traditional lending processes

P 4Guide to buying an investment property

THE PROPERTY INVESTMENT PROCESS

Buying an investment property is an exciting time but it can also be daunting. There are so many different challenges to overcome including finding an investment property, buying it and getting the best value loan.

• Buying by yourself

• Buying with somebody else

• Your deposit saved

• Your income

• Your expenses

• Home equity

• Negative gearing

• Repayment type

2. How much can you afford?

• Get pre-qualified

• Apply online

• Know what you can offer to purchase

4. Getting pre-qualified

• Apply

• Speak to a specialist

• Upload documents

• Property valuation completed

• Loan approved

• Loan documentation delivered

• Property settlement

6 .Our investment property loan process to settlement

03

01

02

04

05

06

07

1. Decide what you want to buy

• Location/suburb of property

• Buy a house or unit

• Do you want to build a new dwelling

• Stamp duty

• Lenders Mortgage insurance (LMI)

• Property valuation

• Conveyancing

3. Other costs to consider

• Private sale

• Auction

5. Making an offer

• Access your account online

7. Repaying your loan

P 5Guide to buying an investment property

To help you succeed we have created this step by step guide to the process.

many advantages. They are significantly cheaper, low maintenance, and much less expensive to refurbish. Whichever way you jump, you will need to decide between house and apartment before you start looking.

Do you want to build a new dwelling – Building a new house or buying an apartment off the plan is an option for investment. If you decide to build, you will want to consider a Construction Loan which is designed specifically for people building a house or unit.

1. Decide what you want to buy

Before you start searching for a property you need to narrow down your criteria. Questions include:

Location – Where do you want to buy? Ideally you’ll want to buy in an area that suits the needs of potential tenants and their lifestyle. Close to centres of work, public transport, schools and shops.

House or unit – What do you want to buy? Most people ultimately want to live in a free-standing house but as investment properties, apartments have

P 6Guide to buying an investment property

2. How much can you afford?

Before you start looking for an investment property you need to work out how much you can afford to pay so you don’t waste time on properties in the wrong price range. This will be determined by a number of factors.

Buying by yourself – if you are buying by yourself the amount you can borrow will be determined by your finances alone.

Buying with somebody else – if you are buying with somebody else, be it a spouse, partner or family member, the amount you can afford to borrow will be determined by both of your finances.

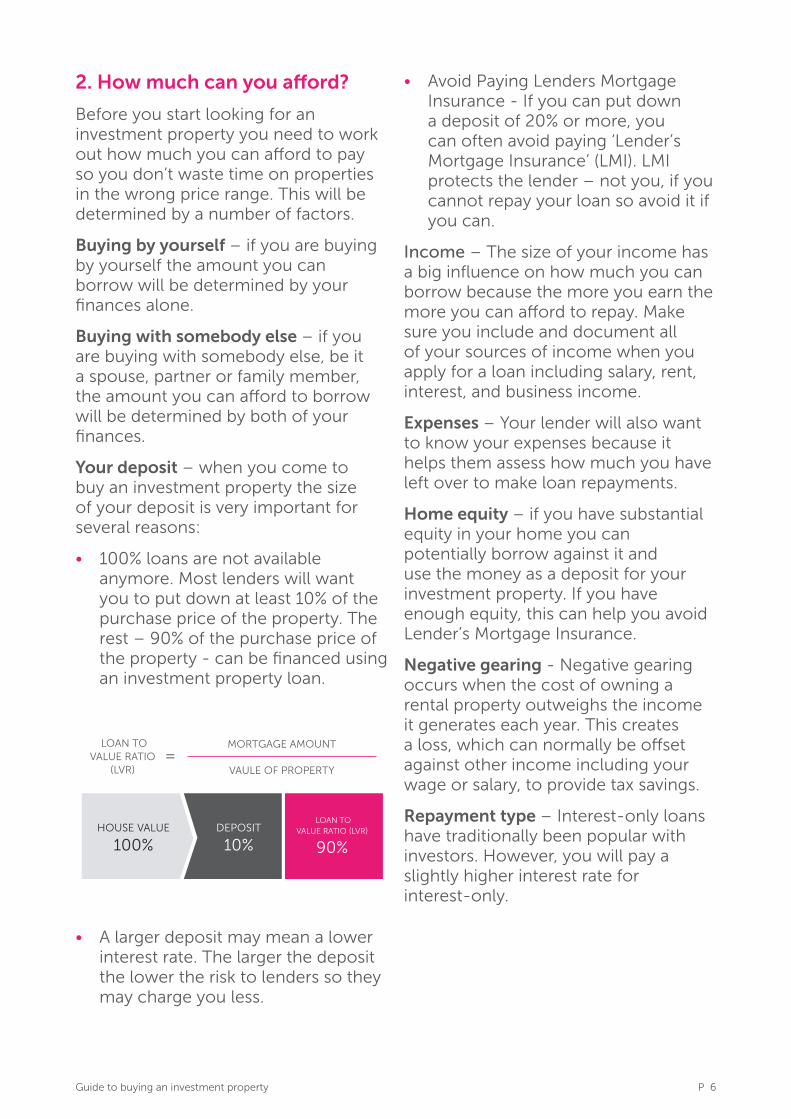

Your deposit – when you come to buy an investment property the size of your deposit is very important for several reasons:

• 100% loans are not available anymore. Most lenders will want you to put down at least 10% of the purchase price of the property. The rest – 90% of the purchase price of the property - can be financed using an investment property loan.

• A larger deposit may mean a lower interest rate. The larger the deposit the lower the risk to lenders so they may charge you less.

HOUSE VALUE

100%DEPOSIT

10%

LOAN TOVALUE RATIO (LVR)

90%

LOAN TOVALUE RATIO

(LVR)=

MORTGAGE AMOUNT

VAULE OF PROPERTY

• Avoid Paying Lenders Mortgage Insurance - If you can put down a deposit of 20% or more, you can often avoid paying ‘Lender’s Mortgage Insurance’ (LMI). LMI protects the lender – not you, if you cannot repay your loan so avoid it if you can.

Income – The size of your income has a big influence on how much you can borrow because the more you earn the more you can afford to repay. Make sure you include and document all of your sources of income when you apply for a loan including salary, rent, interest, and business income.

Expenses – Your lender will also want to know your expenses because it helps them assess how much you have left over to make loan repayments.

Home equity – if you have substantial equity in your home you can potentially borrow against it and use the money as a deposit for your investment property. If you have enough equity, this can help you avoid Lender’s Mortgage Insurance.

Negative gearing - Negative gearing occurs when the cost of owning a rental property outweighs the income it generates each year. This creates a loss, which can normally be offset against other income including your wage or salary, to provide tax savings.

Repayment type – Interest-only loans have traditionally been popular with investors. However, you will pay a slightly higher interest rate for interest-only.

P 7Guide to buying an investment property

3. Other costs to consider

Buying an investment property isn’t just about paying the price of the property. There are some extra costs all buyers should be aware of.

Stamp duty – When you by a property you have to pay a state tax called stamp duty within 30 days of the property settlement. Stamp duty is decided by separate state and territory governments, rather than the Federal Government, so rates vary.

Lenders Mortgage Insurance - Lender’s Mortgage Insurance is an insurance policy that protects the lender from financial loss in the event that the borrower can’t afford to keep up their mortgage repayments. Most lenders make it a condition of borrowing that you pay for a lender’s mortgage insurance policy if you have less than 20% deposit.

Valuation – Most lenders will require you to pay for a valuation of the property you are using as security when you apply for a loan.

Conveyancing - Conveyancing is the process of transferring ownership of a legal title of land (property) from one person or entity to another. When you buy a property you should appoint a conveyancer or solicitor to handle the conveyancing for you.

>20%DEPOSIT

$

P 8Guide to buying an investment property

4. Getting pre-qualified

You can save yourself a lot of time and heartache if you pre-qualify for a loan before bidding on a property.

What is pre-qualification - Also known as conditional approval or preliminary approval, pre-qualification is an offer from us to lend you an agreed amount, subject to full approval. Pre-qualification remains valid for four months. To gain full approval you will need to supply more supporting documents and updated information.

Apply online - You can apply to pre-qualify with loans.com.au in just a few minutes by visiting our website.

Know what you can offer – Once you have pre-qualified you will know what you can offer a seller or what you can bid at auction. This means you can avoid wasting time looking at properties in the wrong price range and that you can bid with confidence.

4 MONTHS

P 9Guide to buying an investment property

5. Making an offer

There are two ways to buy a property in Australia. You can make an offer to purchase via a contract, or by bidding at an auction.

Private sale - Most residential properties in Australia are sold by making a private offer via a contract to purchase. Using this method, the owner sets the price they would like to get for their property. You put in an offer, which is usually below the asking price and negotiate as necessary with the seller from there by writing your offer on the contract and giving it to their agent. Offers pass back and forth until you and the buyer agree on price and terms and exchange contracts. You pay a deposit, typically 10 per cent of the selling price, and there is a cooling-off period. The cooling-off period allows you to complete final legal, building and financial checks but if you do back out of the sale you will most likely forfeit a small part of you deposit. When you buy via a contract offer you will typically also include clauses in the contract for finance and a building-

and-pest inspection. These allow you to cancel the purchase without penalty if you cannot get acceptable finance or if the building and pest report has serious faults.

Auction – A property auction is a public sale usually conducted by an agent acting as an auctioneer. It is governed by strict rules. The auction is advertised for a specific place, time and date. Prospective buyers bid and the property is offered to the highest bidder. There is an advertising campaign with open house inspections for several weeks leading up to the auction date. When a property is sold at auction, the owner sets a reserve price – the minimum for which they will sell the property – and prospective buyers make their bids, with the property going to the highest bidder over the reserve price. The most important thing to remember is that there is no cooling-off period. You will also need to provide a substantial deposit on the day of the auction if you are the winning bidder. This is usually paid by cheque.

P 10Guide to buying an investment property

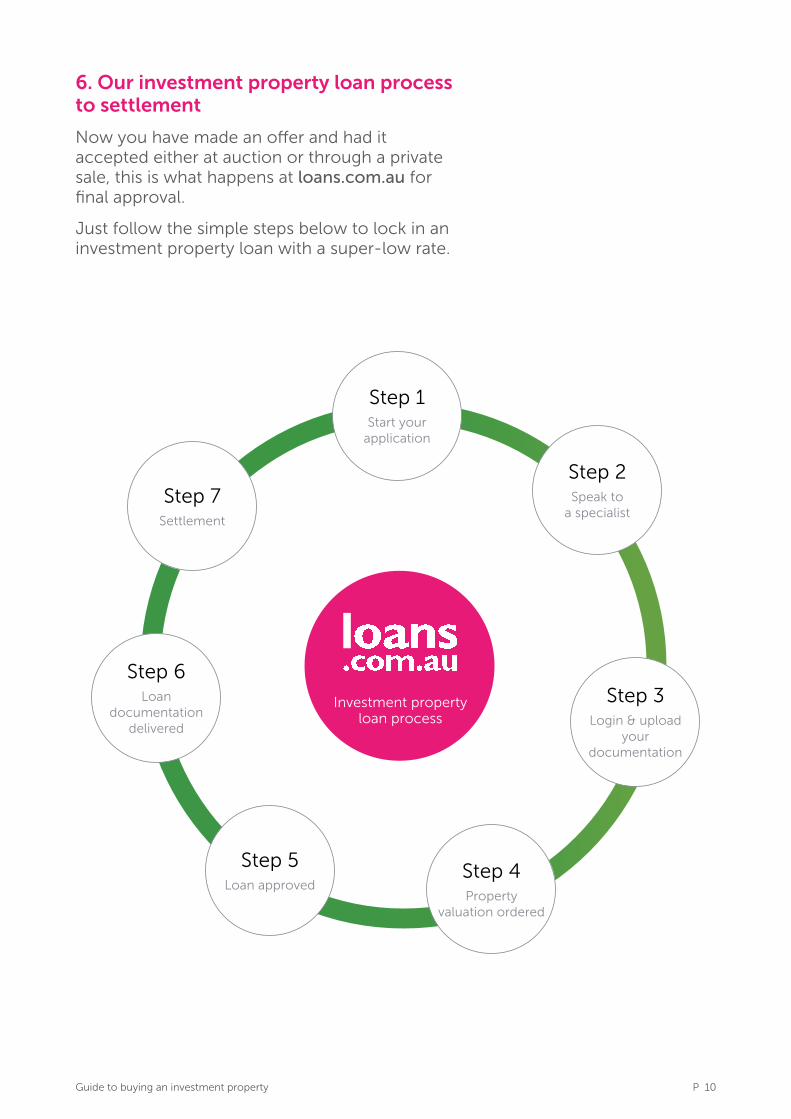

Step 1Start your

application

Step 2Speak to

a specialist

Step 3Login & upload

your documentation

Step 4Property

valuation ordered

Step 5Loan approved

Step 6Loan

documentationdelivered

Step 7Settlement

Investment propertyloan process

6. Our investment property loan process to settlement

Now you have made an offer and had it accepted either at auction or through a private sale, this is what happens at loans.com.au for final approval.

Just follow the simple steps below to lock in an investment property loan with a super-low rate.

P 11Guide to buying an investment property

6. Our investment property loan process to settlement

Now you have made an offer and had it accepted either at auction or through a private sale, this is what happens at loans.com.au for final approval.

Just follow the simple steps below to lock in an investment property loan with a super-low rate.

1. Start your application

Visit loans.com.au and fill out an online application. It only takes a few minutes to complete. You will then be prompted to book a quick phone appointment with one of our online loan specialists to review your application and lodge it. You will also receive login credentials for onTrack, our easy-to-use online portal. You can use onTrack on any computer or mobile device including your mobile phone.

What you do What we do• Fill out an application online

• Book an appointment with a loan specialist

• Contact you at the requestedtime to discuss the informationyou provided

2. Speak to a specialist

Talk with one of our loan specialists. They will review your application and help you choose the most appropriate loan for your needs.

What you do What we do• Be prepared with your financial

information such as incomeand expenses

• Tell us your key financial goals

• Verify the information you provided

• Tailor a loan product to achieveyour goals

• Provide access to our onTrackapplication portal

3. Login and upload your documentation

Once you have applied, you will need to supply some supporting documents such as pay slips and bank statements. You can do this using onTrack.

What you do What we do• Log in to onTrack

• Start uploading supportingdocuments to yourapplication checklist

• Verify the information you provide

• Contact you to assist with theapplication process

P 12Guide to buying an investment property

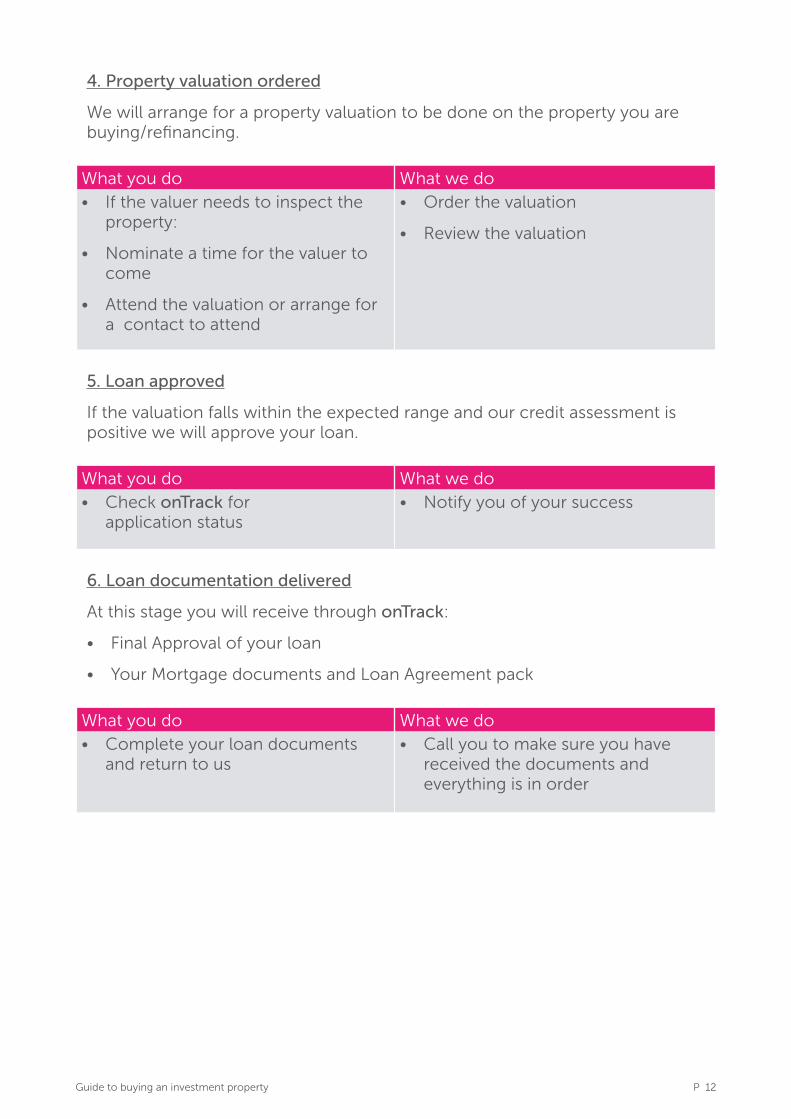

4. Property valuation ordered

We will arrange for a property valuation to be done on the property you are buying/refinancing.

What you do What we do• If the valuer needs to inspect the

property:

• Nominate a time for the valuer to come

• Attend the valuation or arrange for a contact to attend

• Order the valuation

• Review the valuation

5. Loan approved

If the valuation falls within the expected range and our credit assessment is positive we will approve your loan.

What you do What we do• Check onTrack for

application status• Notify you of your success

6. Loan documentation delivered

At this stage you will receive through onTrack:

• Final Approval of your loan

• Your Mortgage documents and Loan Agreement pack

What you do What we do• Complete your loan documents

and return to us• Call you to make sure you have

received the documents and everything is in order

P 13Guide to buying an investment property

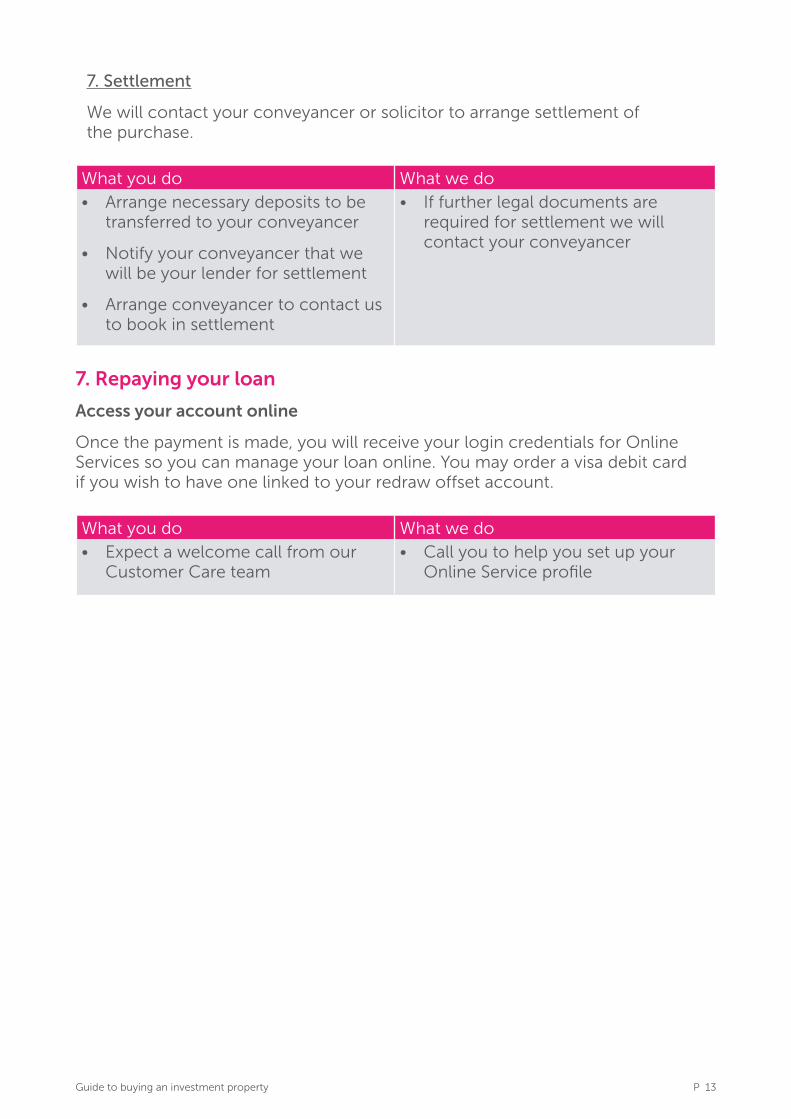

7. Settlement

We will contact your conveyancer or solicitor to arrange settlement of the purchase.

What you do What we do• Arrange necessary deposits to be

transferred to your conveyancer

• Notify your conveyancer that wewill be your lender for settlement

• Arrange conveyancer to contact usto book in settlement

• If further legal documents arerequired for settlement we willcontact your conveyancer

7. Repaying your loan

Access your account online

Once the payment is made, you will receive your login credentials for Online Services so you can manage your loan online. You may order a visa debit card if you wish to have one linked to your redraw offset account.

What you do What we do• Expect a welcome call from our

Customer Care team• Call you to help you set up your

Online Service profile

P 14Guide to buying an investment property

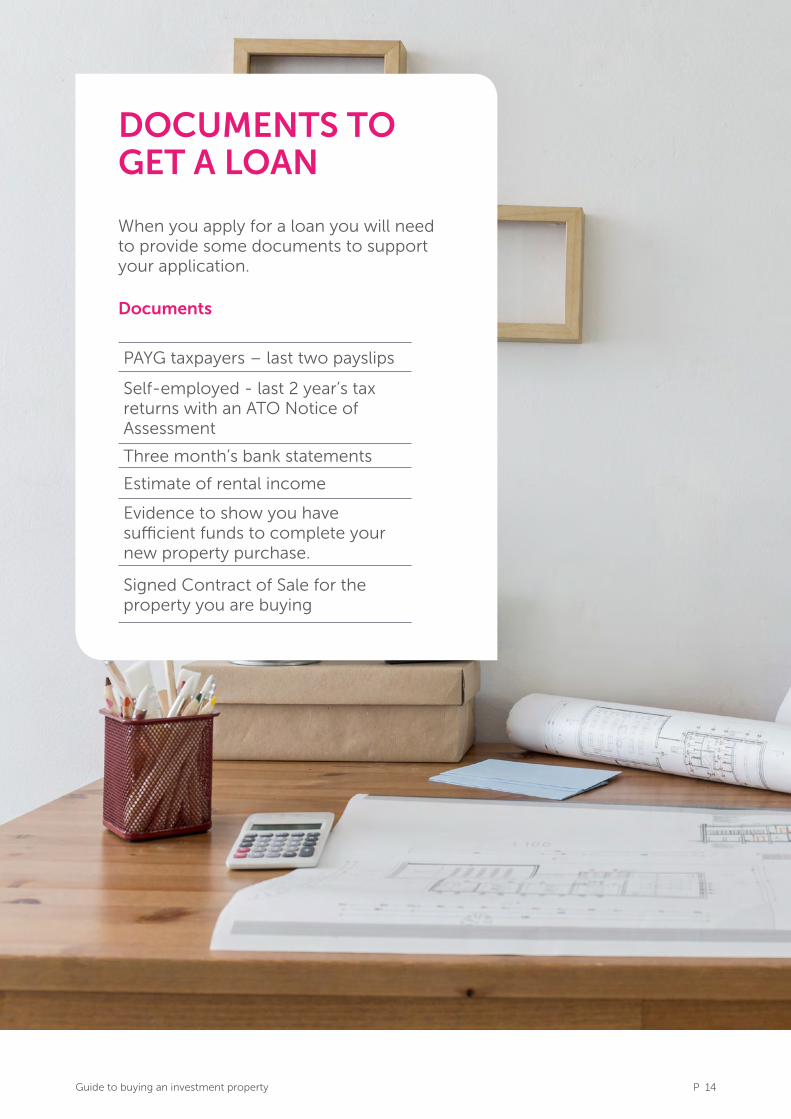

DOCUMENTS TO GET A LOAN

When you apply for a loan you will need to provide some documents to support your application.

Documents

PAYG taxpayers – last two payslips

Self-employed - last 2 year’s tax returns with an ATO Notice of Assessment

Three month’s bank statements

Estimate of rental income

Evidence to show you have sufficient funds to complete your new property purchase.

Signed Contract of Sale for the property you are buying

P 15Guide to buying an investment property

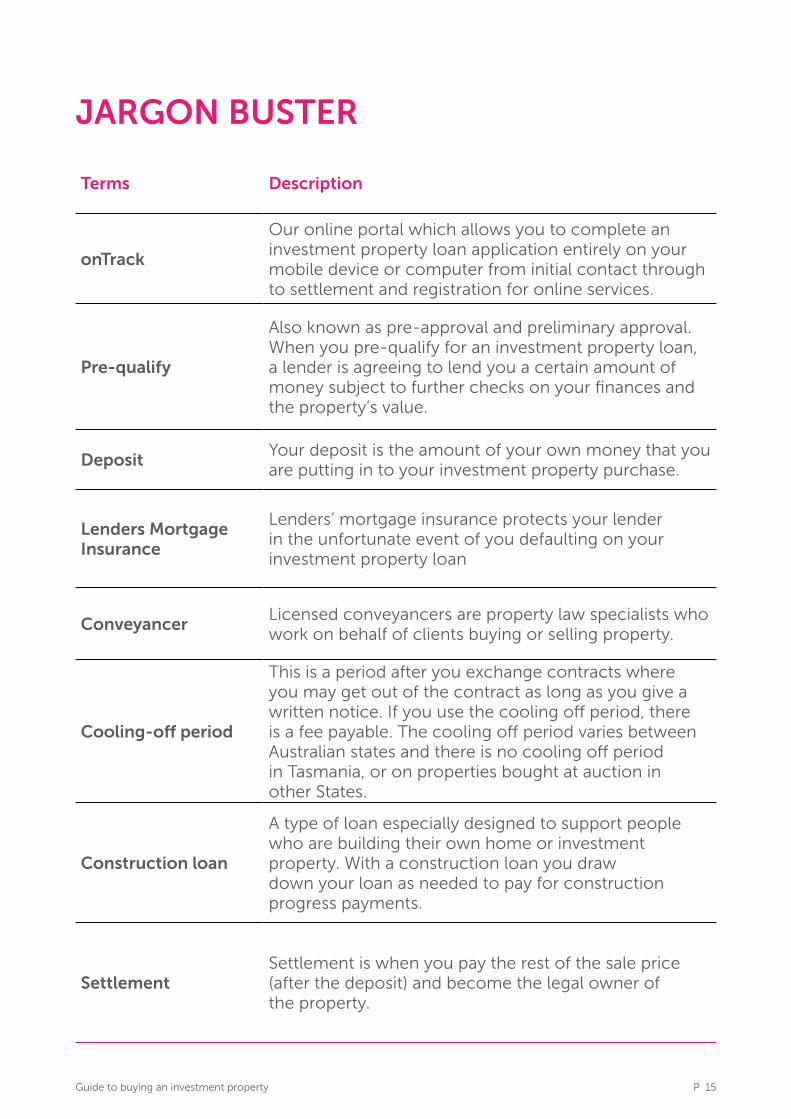

JARGON BUSTER

Terms Description

onTrack

Our online portal which allows you to complete an investment property loan application entirely on your mobile device or computer from initial contact through to settlement and registration for online services.

Pre-qualify

Also known as pre-approval and preliminary approval. When you pre-qualify for an investment property loan, a lender is agreeing to lend you a certain amount of money subject to further checks on your finances and the property’s value.

DepositYour deposit is the amount of your own money that you are putting in to your investment property purchase.

Lenders Mortgage Insurance

Lenders’ mortgage insurance protects your lender in the unfortunate event of you defaulting on your investment property loan

ConveyancerLicensed conveyancers are property law specialists who work on behalf of clients buying or selling property.

Cooling-off period

This is a period after you exchange contracts where you may get out of the contract as long as you give a written notice. If you use the cooling off period, there is a fee payable. The cooling off period varies between Australian states and there is no cooling off period in Tasmania, or on properties bought at auction in other States.

Construction loan

A type of loan especially designed to support people who are building their own home or investment property. With a construction loan you draw down your loan as needed to pay for construction progress payments.

SettlementSettlement is when you pay the rest of the sale price (after the deposit) and become the legal owner of the property.

P 16Guide to buying an investment property

ABOUT LOANS.COM.AULoans.com.au is an award-winning online lender that is proudly Australian and based in the heart of Brisbane, with offices in other capital cities.

Since we were founded in 2011, we have grown to become an industry leader with thousands of happy customers in every state and territory.

From our local call centre, our service team helps hundreds of customers around the country apply for and manage their loans, every day.

Property buyers are choosing us because we don’t have expensive bricks-and-mortar branches and we pass the savings on to them through super-low interest rates.

But we are more than just a great low rate.

We have taken the hassle out of getting an investment property loan by cutting through the old-fashioned processes of traditional lenders to put you in control.

With the support of our local service team you can move through your online application at your own pace and with full knowledge of what is happening at each stage.

You can borrow from loans.com.au secure in the knowledge that we are regulated by the Australian government.

Our operations are covered by the National Credit Code which is enforced by the financial services watchdog, the Australian Securities and Investments Commission.

We are powered by the financial

strength of our parent company Firstmac, which is Australia’s largest non-bank lender. Firstmac has been operating successfully for 38 years and it has more than $8 billion in mortgages under management.

If you follow rugby league you may have heard of Firstmac because it is a Premier sponsor of NRL team, the Brisbane Broncos.

Loans.com.au is Australian-owned-and-run, has a long track record of success, and has super-low rates that can save you thousands of dollars. That’s why we are the Home of Smart Money.

P 17Guide to buying an investment property

CONTACT

Call us on 13 10 90 7am - 7pm, Monday to Friday. AEST Alternatively (+61 7 3017 8899)

Email: [email protected]

Or visit our website at loans.com.au to chat online.

P 18Guide to buying an investment property

7-7am-pm

MON- FRI phone support MORE THAN

$8 BILLION IN MORTGAGES

secure

interest ratesSuper low

FAST TRACKAPPLICATION

thousands of ^

Great value

HAPPY CUSTOMERS

Hassle FREE

Apply online in just five steps

256 SSL encryption AND

a firewall mechanism

The home with

SMART MONEY

1

AWARDED*2015 Home Lender of the year in Mozo's Expert Choice Award

*5 star ratings for our variable rate home loans from Canstar plus many others

FirstmacPowered by

ALL CLICKSNO BRICKS

AEST

save on the cost of branches, we pass on in the form of lower interest rates for our customers.

P 19Guide to buying an investment property

We hope you find this guide valuable. For more info visit www.loans.com.au

ACN 082 587 095

Australian Credit Licence 395219

© 2017 copyright of loans.com.au Pty Ltd