guidance on eiti requirements 12 and 13 eiti international secretariat april 2011

TRANSCRIPT

Guidance on EITI Requirements 12 and 13

EITI International SecretariatApril 2011

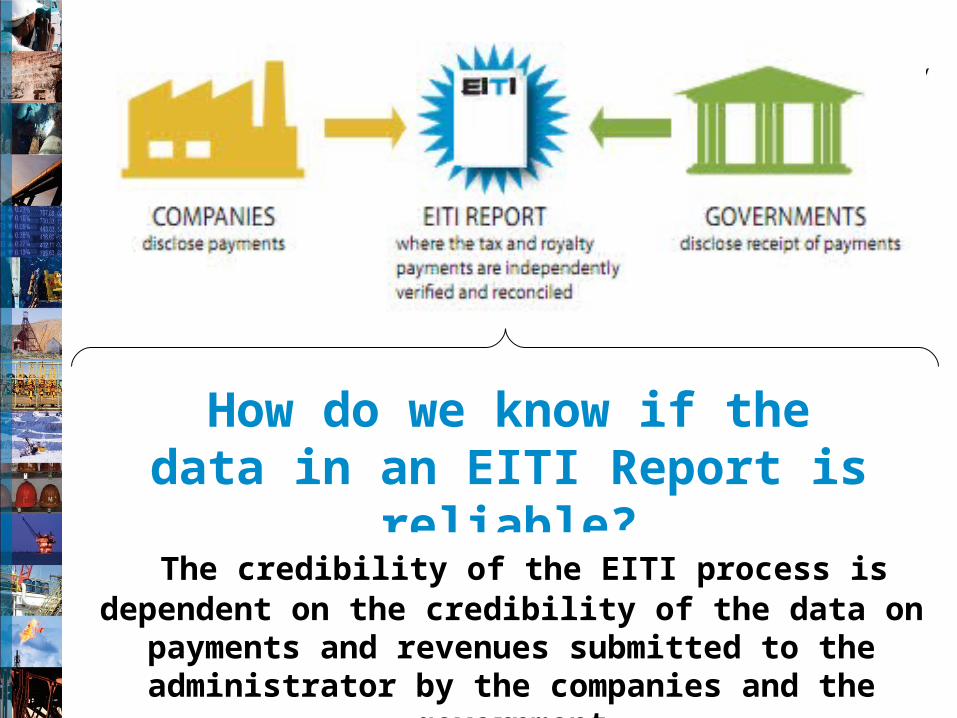

How do we know if the data in an EITI Report is

reliable? The credibility of the EITI process is

dependent on the credibility of the data on payments and revenues submitted to the administrator by the companies and the

government

EITI Criteria #2

“Where such audits do not already exist, payments and revenues are the subject of a credible, independent audit, applying international auditing standards”

• Safeguards the quality of the EITI Report

• Reduces the risk of collusion (government and/or companies fabricating data).

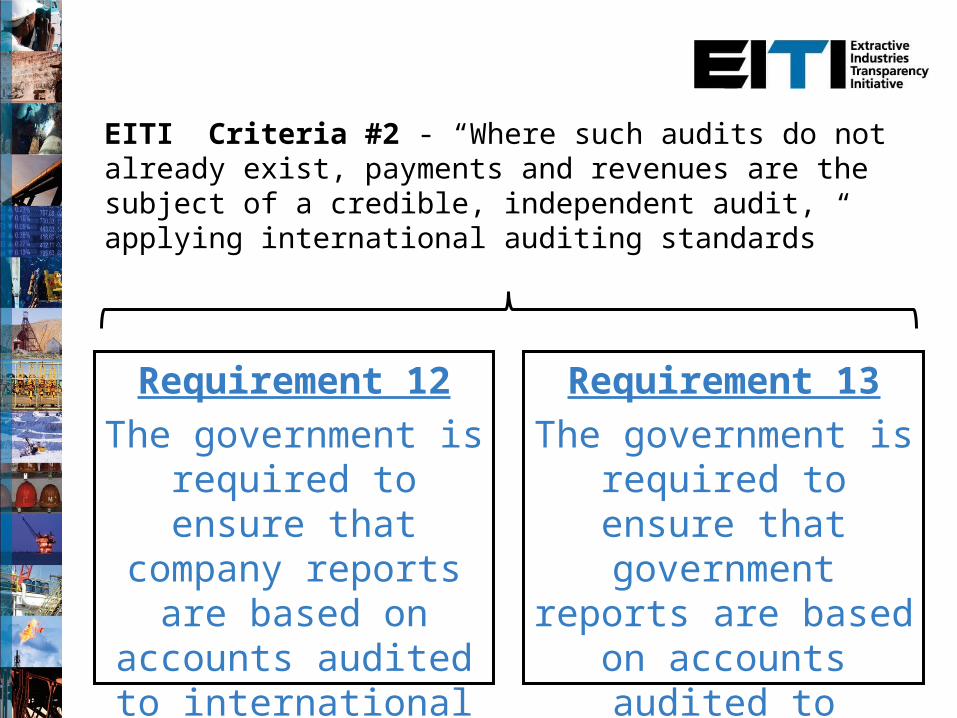

EITI Criteria #2 - “Where such audits do not already exist, payments and revenues are the subject of a credible, independent audit, applying international auditing standards”

Requirement 12The government is required to ensure

that company reports are based

on accounts audited to international

standards.

Requirement 13The government is required to ensure that government reports are based

on accounts audited to international

standards.

Requirement 12 & 13

If company and government auditing is sound, an EITI reconciliation process is viable. Where such audits have not been done – or the audits are not regarded as credible – the MSG should consider an EITI Audit.

Requirement 12

All payments and revenues reported under EITI should have been the subject of credible, independent audit. •When companies submit payments data that has been verified by their own independent auditor, no other audit will normally be required. •Where such audits have not been done – or the audit is not regarded as credible – then an audit should be considered•It is recommended that the process relies as much as possible on existing procedures and institutions, and on international standards.

Requirement 13

All payments and revenues reported under EITI should have been the subject of credible, independent audit. •When government revenue data has been verified by an independent auditor, no other audit will normally be required. •Where such audits have not been done (or the audit is not regarded as credible) then an audit should be considered.•It is recommended that the process relies as much as possible on existing procedures and institutions, and on international standards.

(1)MSGs should examine the auditing processes for government agencies

– How is government data audited? – Which institutions are involved? – Are reforms to the government’s

auditing processes underway? (if so, what is the status)?

(2)Is government auditing consistent with international best practice (e.g., INTOSAI)?

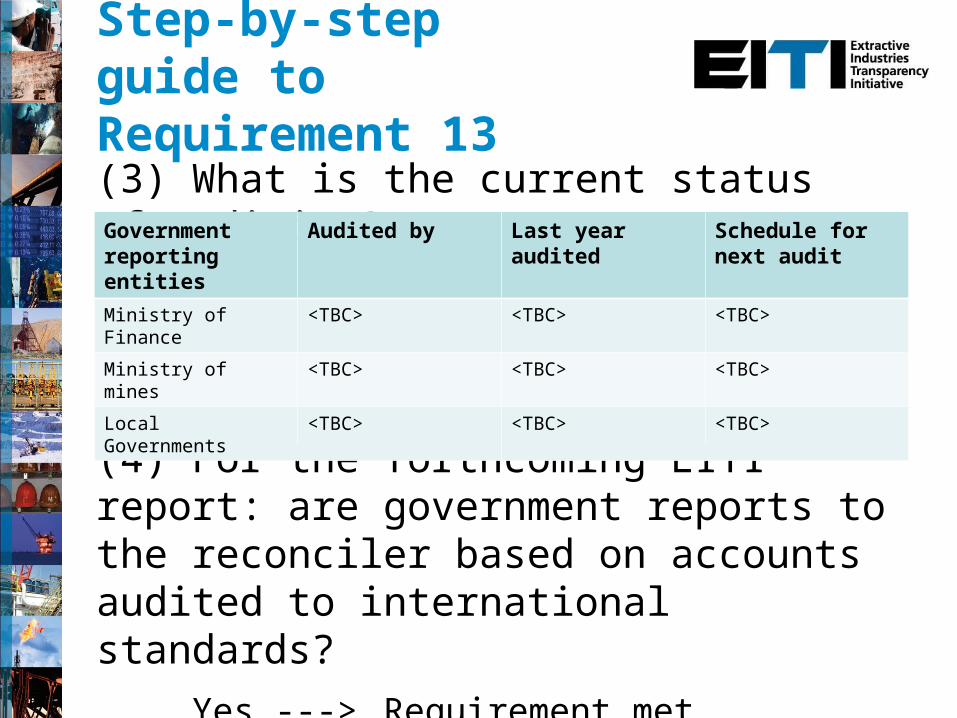

Step-by-step guide to Requirement 13

(4) For the forthcoming EITI report: are government reports to the reconciler based on accounts audited to international standards?

Yes ---> Requirement met

No ---> MSG should agree a response

(3) What is the current status of auditing?Government reporting entities

Audited by Last year audited

Schedule for next audit

Ministry of Finance

<TBC> <TBC> <TBC>

Ministry of mines

<TBC> <TBC> <TBC>

Local Governments

<TBC> <TBC> <TBC>

Step-by-step guide to Requirement 13

Guidance•Consider Public Expenditure and Financial Accountability assessments (www.pefa.org) •Examines compliance with INTOSAI Auditing Standards for most EITI countries, and related capacity building•PEFA indicator 26 deals with audits of government accounts.

Step-by-step guide to Requirement 13

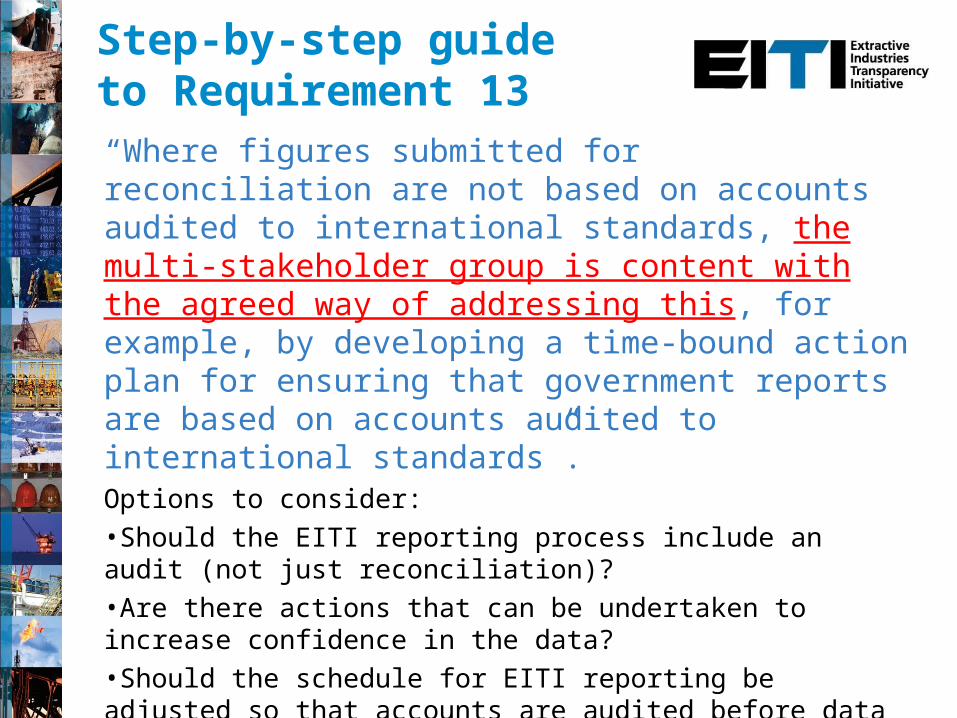

“Where figures submitted for reconciliation are not based on accounts audited to international standards, the multi-stakeholder group is content with the agreed way of addressing this, for example, by developing a time-bound action plan for ensuring that government reports are based on accounts audited to international standards”. Options to consider:•Should the EITI reporting process include an audit (not just reconciliation)?•Are there actions that can be undertaken to increase confidence in the data? •Should the schedule for EITI reporting be adjusted so that accounts are audited before data is disclosed to the validator (note the trade off here, timeliness vs reliability)?•Are reforms to the government’s auditing processes needed? (If so, which agencies are responsible and what is the timeframe).

Step-by-step guide to Requirement 13

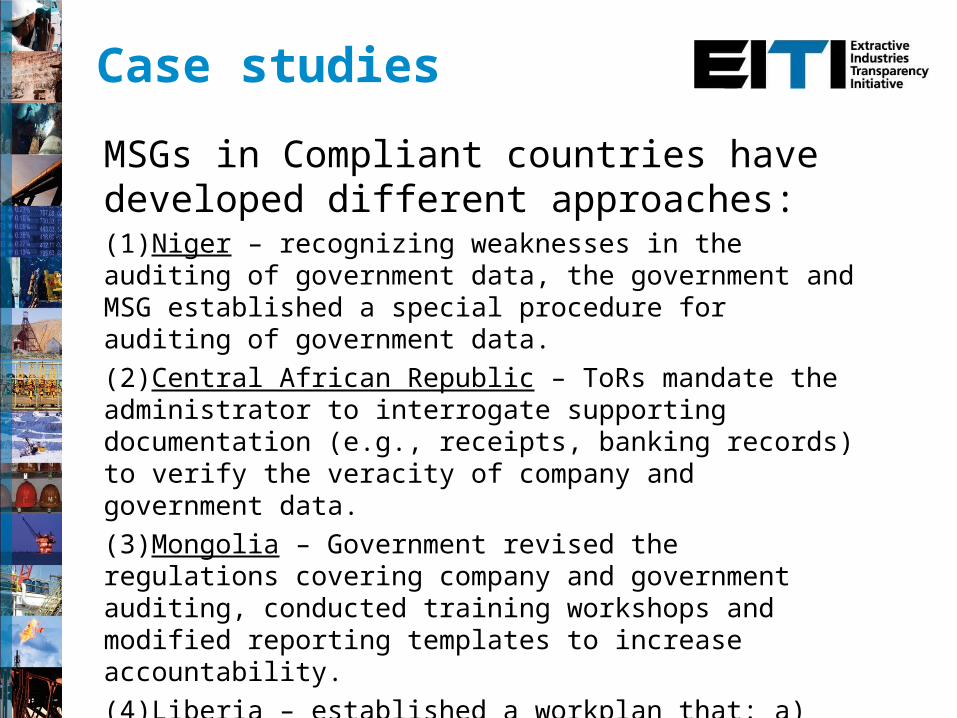

Case studies

MSGs in Compliant countries have developed different approaches: (1)Niger – recognizing weaknesses in the auditing of government data, the government and MSG established a special procedure for auditing of government data. (2)Central African Republic – ToRs mandate the administrator to interrogate supporting documentation (e.g., receipts, banking records) to verify the veracity of company and government data.(3)Mongolia – Government revised the regulations covering company and government auditing, conducted training workshops and modified reporting templates to increase accountability. (4)Liberia – established a workplan that: a) diagnosed the weaknesses in government auditing practice and b) proposed an action plan to bring practices into line with international standards.

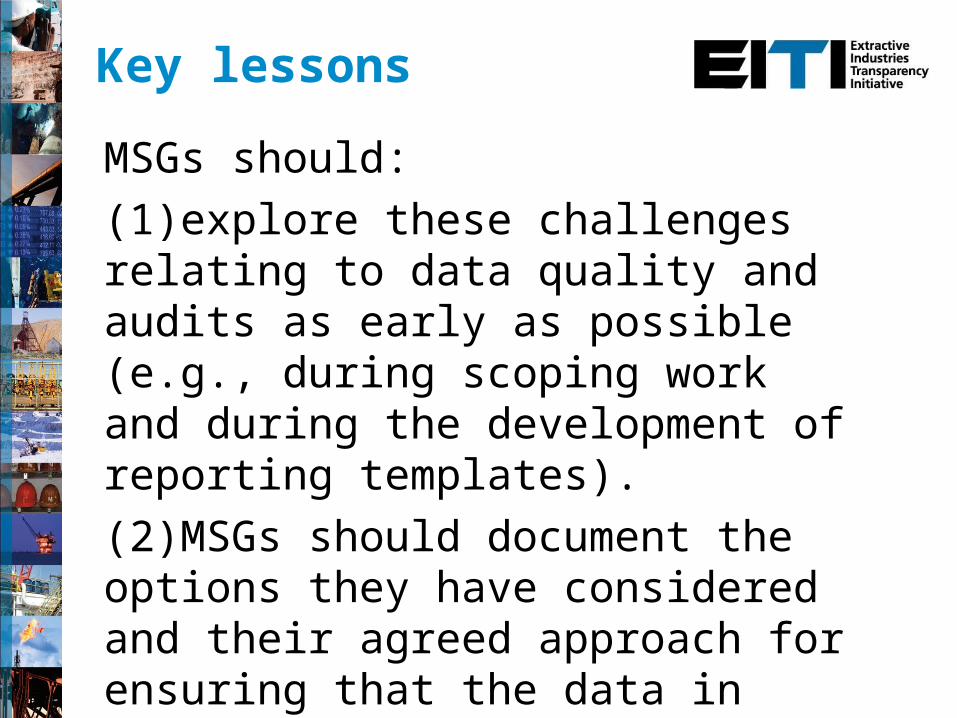

Key lessons

MSGs should: (1)explore these challenges relating to data quality and audits as early as possible (e.g., during scoping work and during the development of reporting templates).(2)MSGs should document the options they have considered and their agreed approach for ensuring that the data in EITI reports are reliable.