govind dissertation

TRANSCRIPT

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 1/52

Synopsis

“A STUDY ON EFFECT OF BRAND IMAGE

ON CONSUMER’S TASTE AND

PREFERENCES IN CONSUMER DURABLE

SECTOR ”

In Partial Fulfillment for the award of the degree

PGDM

(2010-12)

Institute of Management Studies,

Lal Quan, Ghaziabad

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 2/52

“A STUDY ON EFFECT OF BRAND IMAGE

ON CONSUMER’S TASTE AND

PREFERENCES IN CONSUMER DURABLE

SECTOR ”

Under the supervision of

Of

Prof. Vijendra dhyani

Submitted By: Submitted to:

Govind Gupta Prof. Vijendra dhyani

PGDM

BM-010059

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 3/52

DECLARATION

I student of Institute of Management

Studies Batch (20010-12) declare that every part of the Project Report “A

Study on effect of brand image on Consumer’s taste

and preferences in Consumer Durable Sector” that I have

submitted is original.

Date of Project Submission:

Signature of the Student:

Faculty’s Comments:

Signature of the Faculty:

Name:

Signature of the Research Methodology: ………………………………

Name: …………………………………………………………………..

ACKNOWLEDGEMENT

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 4/52

The making of any report calls for contribution and cooperation from many

others, besides the individual alone. It is the result of meticulous efforts put

in by the many minds that contribute to the final report formation. I duly

acknowledge my gratitude to each one of them.

During the perseverance of this project, I was supported by different people,

whose names if not mentioned would be inconsiderate on my part.

I would like to extend my sincere gratitude and appreciation to my project

guide and faculty Prof. Vijendra dhyani, for extending valuable guidance

and encouragement from time to time, without which it would not have been

possible to undertake and complete this project. The Project was an

enriching experience and taught me various critical factors that influence

Consumer Durable Industry. Additionally, this project helped me in

understanding that how actual research is conducted and the various

challenges that researches face while conducting a research.

I would also like to thank my friends and different people for their support

and patience in filling up the questionnaires and hence in the successful

completion of the project.

Above all I would like to thank the divine intervention who backed me at all

the time and provided me enough motivation to accomplish this voyage.

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 5/52

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 6/52

Preface

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 7/52

Before the liberalization of the Indian economy, only a few companies likeKelvinator, Godrej, Alwyn, and Voltas were the major players in theconsumer durables market, accounting for no less than 90% of the market.Then, after the liberalization, foreign players like LG, Sony, Samsung,Whirlpool, Daewoo, and Aiwa came into the picture. Today, these playerscontrol the major share of the consumer durables market. Consumer durablesmarket is expected to grow at 10-15% in 2007-2008. It is growing very fast

because of rise in living standards, easy access to consumer finance, andwide range of choice, as many foreign players were entering in the marketwith the increase in income levels, easy availability of finance, increase inconsumer awareness, and introduction of new models, the demand for consumer durables has increased significantly. Products like washingmachines, air conditioners, microwave ovens, color televisions (C-TV) wereno longer considered luxury items. However, there were still very few

players in categories like vacuum cleaners, and dishwashers Consumer durables sector is characterized by the emergence of MNCs, exchangeoffers, discounts, and intense competition. The market share of MNCs inconsumer durables sector is 65%. MNC's major target is the growing middleclass of India. MNCs offer superior technology to the Consumers whereasthe Indian companies compete on the basis of firm grasp of the localmarket, their well acknowledged brands, and hold over wide distributionnetwork. However, the penetration Level of the consumer durables is stilllow in India. Indian Consumer durables market used to be dominated by fewdomestic players like Godrej, Voltas, Allwyn and Kelvinator. But postliberalization many foreign companies have entered into Indian marketdethroning the Indian players and dominating Indian market the major categories being CTV, REFRIGRATOR, MICROWAVE OVEN andWASHING MACHINES. India being the second largest growing economywith huge consumer class has resulted in consumer durables as the fastestgrowing industries in India. LG, SAMSUNG the two Korean companieshave been maintaining the lead in the market with LG being leader in almostall the categories. The rural market is growing faster than the urban market,although the penetration level is much lower .The CTV segment is expected

to the largest contributing segment to the overall growth of the industry. Therising income levels double-income families and consumer awareness werethe main growth drivers of the industries.

EXECUTIVE SUMMARY

The goal of marketing research is to provide the facts and direction that

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 8/52

managers need to make their more important marketing decisions.Marketing research covers a wider range of activities. Marketing research ishaving following steps

Determine research design,

Identify data types and sources,

Design data collection forms and questionnaires,

Determine sample plan and size,

Collect the data,

Analyze and interpret the data,

Prepare the research report

In this report, we have done a market research on consumer durables, andcome with some suggestion, limitation, and conclusion on the basis of marketing research work As far is summary part is concern, in research project we have selectedmarket survey on

Consumer durables. Consumer durable industry, we have to do marketsurvey for electronic products preference toward, so we were collected

primary and secondary data for research methodology and follow up withthe analysis part.

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 9/52

Literature

Review &Research

Methodology

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 10/52

Literature review:

The Indian retail market, which is the fifth largest retail destination globally,has been ranked as the most attractive emerging market for investment in theretail sector by AT Kearney's eighth annual Global Retail DevelopmentIndex (GRDI), in 2009. As per a study conducted by the Indian Council for Research on International Economic Relations (ICRIER), the retail sector isexpected to contribute to 22 per cent of India's GDP by 2010.

With rising consumer demand and greater disposable income, the US$ 400 billion Indian retail sector is clocking an annual growth rate of 30 per cent. Itis projected to grow to US$ 700 billion by 2010, according to a report by

global consultancy Northbridge Capital. The organized business is expectedto be 20 per cent of the total market by then. In 2008, the share of organizedretail was 7.5 per cent or US$ 300 million of the total retail market.

A McKinsey report, 'The rise of Indian Consumer Market', estimates that theIndian consumer market is likely to grow four times by 2025. Commercialreal estate services company, CB Richard Ellis' findings state that India'sretail market has moved up to the 39th most preferred retail destination inthe world in 2009, up from 44 last year.

India continues to be among the most attractive countries for global retailers.Foreign direct investment (FDI) inflows as on September 2009, in single-

brand retail trading, stood at approximately US$ 47.43 million, according tothe Department of Industrial Policy and Promotion (DIPP).

India's overall retail sector is expected to rise to US$ 833 billion by 2013and to US$ 1.3 trillion by 2018, at a compound annual growth rate (CAGR)of 10 per cent. As a democratic country with high growth rates, consumer spending has risen sharply as the youth population (more than 33 percent of

the country is below the age of 15) has seen a significant increase in itsdisposable income. Consumer spending rose an impressive 75 per cent in the

past four years alone. Also, organized retail, which is pegged at around US$8.14 billion, is expected to grow at a CAGR of 40 per cent to touch US$ 107

billion by 2013.

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 11/52

The organized retail sector, which currently accounts for around 5 per centof the Indian retail market, is all set to witness maximum number of largeformat malls and branded retail stores in South India, followed by North,West and the East in the next two years. Tier II cities like Noida, Amritsar,Kochi and Gurgaon, are emerging as the favored destinations for the retailSector with their huge growth potential.

Further, this sector is expected to invest around US$ 503.2 million in retailtechnology service solutions in the current financial year. This could gofurther up to US$ 1.26 billion in the next four to five years, at a CAGR of 40

per cent.

Moreover, many new apparel brands such as Zara, the fashion label owned by Inditex SA of Spain, UK garment chain Topshop, the Marc Ecko clothing

line promoted by the US entrepreneur of the same name and the Japanesecasual wear brand Uniqlo are preparing to open outlets in India.

Buoyed by improved consumer spending, sales of listed retailers increased by 12 per cent in the September 2009 quarter compared with the same periodin 2008.

Australia's Retail Food Group is planning to enter the Indian market in2010. It has ambitious investment plans which aim to clock revenue of

US$ 87 million from the country within five years from start of operations.

British retail major Marks & Spencer (M&S) is looking at scaling upits India operations and plans to open at least 50 more outlets in thecountry over the next few years.

Koutons Retail India plans to open 200 stores in FY11 in addition toits existing 1,400. Of the 200 stores, 100 would be family conceptstores, which would include women and children's wear.

Reliance Footprint, part of Reliance Retail, plans to spend US$ 86.62million to add 100 outlets across the country in two years to sell

branded footwear. It currently has 16 outlets.

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 12/52

Retail chain Suvidhaa Infoserve plans to open 1,000-1,200 newoutlets every month across the country and is eyeing a 100,000 strongnetwork in the next two to three years. At present, the Mumbai-based

firm has 18,000 convenient neighbourhood stores called 'SuvidhaaPoint' across the country in over 20 states and over 400 cities.

Lifestyle International, part of the Dubai-based US$ 1.5 billionLandmark Group, plans to have over 50 stores across India by 2012– 13. These will include 35 Lifestyle stores for retailing apparel,cosmetics and footwear, besides 15 Home Centres that sell homefurnishing goods.

Wills Lifestyle plans to expand its operations by opening 100 new

stores in the next three years. It also plans to concentrate on online buyers.

Pantaloon Retail India (PRIL) is planning to invest US$ 77.88 millionthis fiscal to add up to 2.4 million sq ft retail space at its existingoperations. Pantaloon Retail is also looking to hive off its value retailchain, Big Bazaar, into a separate subsidiary, which may eventuallygo for an initial public offer (IPO). PRIL proposes to open 155 BigBazaar stores by 2014, increasing its total network to 275 stores.

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 13/52

Objectives:

The research was aimed at studying the purchase pattern of consumers for consumer durable.

To study the factors affecting purchase of consumer durables

To study brand preference of consumers for consumer durable goods

To study brand preference of consumers towards organized &

unorganized outlet for the consumer durable goods.

Scope of the study:

The research is conducted in Ahmedabad city to study purchase pattern of consumer durables that includes major factors affecting the decision, brand

preference and preference towards organized and unorganized formats to purchase the same.

Research design:

Research design is descriptive in nature. Preference of people is analyzedand quantified to know the factors responsible for their preference. Further

preference is quantified in terms of organized and unorganized retailformats.

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 14/52

Data Collection Sources:

Primary Data:

These data was collected through survey of consumers with the help of questionnaire.

Secondary Data:

Information regarding the project, secondary data was also required. Thesedata were collected from various past studies and other sources like

magazines, newspapers, and websites that qualified as reliable.

Research instrument:

Structured questionnaire

Sampling plan:

Target population: Households of Ghaziabad

Sampling unit: Households & People purchasing consumer durables fromstores at the time of research

Sampling method: convenience and Step out sampling

Sample size: 100

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 15/52

Analytical tools:

Graphical presentation

Hypothesis

Weighted average

Contribution of the study

The study reveals preferential criteria for the purchase of consumer durables.it also gives insights into the preference towards organized and unorganizedstore along with reasons which may become helpful to the marketers toredesign strategies

Limitation of the Study:

As the time given to complete the project is lesser than actual time requiredcompleting similar studies, the quality of findings may get affected. Thesample size s 200 (hundred), thus the findings from the same may not berepresentative of the actual population.

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 16/52

Industry

Profile

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 17/52

Definition of the Consumer Durable Industry:

Consumer goods like washing machines, motorcars, TV sets, audio-videosystems etc, which yield services or utility over time rather than beingcompletely used up at the moment of consumption can be termed as theconsumer durables. Most consumer goods are durables to some degree, andthe term is often used in a more restricted sense to denote relativelyexpensive, technologically sophisticated goods ‗consumer durables‘ such asthe examples given above which implies high involvement at the time of

purchase.

The consumer durables segment can be segregated into consumer electronics(TVs, VCRs/VCPs and audio systems) and consumer appliances (alsoknown as white goods) like refrigerators, washing machines, air conditioners(ACs), microwave ovens, vacuum cleaners and dishwashers.

Over the years demand for consumer durables has increased with the risinglevel of incomes, double income families, changing lifestyles, availability of credit, increasing consumer awareness and the introduction of new models

by the Indian as well as multinational companies. Consumer durableindustry was once considered to be luxury item with targeting the upper-middle class for consumption. With increasing competition, price wars,

branding and promotional strategies, the concept has melted down to themasses and has become a part of the household‘s necessities even in thelower-middle class and rural part of the countries.

Most of the segments in this sector are characterized by intense competition,emergence of new companies (especially MNCs), and introduction of state-of-the-art models, price discounts and exchange schemes. Despite of thatMNCs are entering in to Indian market because growing Indian middle class

of around 250 millions. Also it is widely accepted that consumer durable penetration increases rapidly after per capita income (PCI) crosses athreshold limit of $2000. In India, the PCI is low at $370, though it isequivalent to $600 on PPP (Purchasing Power Parity) basis and expected tosee a consistent growth of over 6% over the next years to come.

According to NCEAR survey estimates, the number of households in the

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 18/52

higher and middle income categories will rise rapidly. There will alsoabsolute reduction in the number of households in the low incomes. Thiswill lift large number of households to income levels atwhich they can

become purchasers of consumer durable products. Continuous economicgrowth and higher income levels will drive growth in volumes, anyreduction in the duties will leads to lower down of the values and this will

bring more customers for the durable products.

The biggest attraction for MNCs is the growing Indian middle class (approx.250 m). This market is characterized with low penetration levels. MNCshold an edge over their Indian counterparts in terms of superior technologycombined with a steady flow of capital, while domestic companies competeon the basis of their well-acknowledged brands, an extensive distributionnetwork and an insight in local market conditions.

The Indian middle class market of 250 million is the biggest attraction for the MNCs along with the level of the penetration of consumer durables inthe India has more attracted Multinationals to the India, in the case of consumer durables penetration levels of TV is believed to the highest, andafter that the penetration of the refrigerator comes.

In the future, earnings will be driven by rising demand for consumer durables in general. As per the National Sample Survey Organization reportof "Use of durable goods by Indian households", the per capita totalexpenditure on durable goods increased from Rs112.89 in 1987-88 toRs148.02 in 1993-94. Similarly, NCAER estimates point to the fact that thenumber of households with monthly incomes above Rs 10,000 in metros andRs 5,000 in non-metros is expected to rise from 22.7 million in 1995-96 to ahuge 57.2 million in 2005-06. This will mean that firstly, there will be a

perceptible shift towards branded products and secondly, the level of aspiration buying will increase.

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 19/52

Size of The Market:

The total Rs. 15500 crore consumer durables industry consists of Colour Televisions, Black and White Televisions, Refrigerators, WashingMachines, Air-conditioners, Microwave Ovens, Vacuum Cleaners, AudioSystems, Electronic Appliances and Water Purifiers. The table below showsthe Estimated industry size‘ and the competition in the various segments.

Now considering consumer durables industry in general, the drivers that willleads to the growth of the industry in general will be:

The degree of distribution network in the market.

The advertising and marketing strategy adopted by the players in theindustry.

The brand image of the product as perceived by the consumer.

The technology used by the company viz. state-of-the art technology

or and older version.

The ability of the company to introduce newer products and newer product features.

The capability of the company to service its products.

The discount schemes and consumer finance facility available.

The market positioning of the product.

The cost competitiveness and pricing strategy of the company.

The financial strength of the players.

The competition in the industry has intensified after the liberalization and

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 20/52

more and more MNC are coming to India to target the huge middle class of the country. The competition is dependent upon the brand strength anddistribution network. In other words, the advertising and marketing expenses

play a vital role in competition. As a result of the increased competitiveactivity, the advertising and marketing costs as a percentage of operatingincome 10have increased over the years. This ratio for the industry hasincreased from 4.4 percent in 1993 to 6.7 percentage in 2000.However, the export prospects are least or minimal because indigenousmanufacturers do not possess adequate brand equity or excellent productquality. There are even constraints like transportation due to poor infrastructure and relatively under developed markets in the neighboringcountries.

Changes In The Strategies:

There is a shift in trend as the emphasis has moved from the manufacturing process to marketing and advertising strategies. In other words, themarketing game has become a vital factor for driving sales as against themanufacturing process of the products in the past. Players are nowconcentrating on the creation of brand image in order to economize their scale of operations and to increase their brand strength. The advertisingexpenses of the companies operating in this segment are going high everyyear and the returns are diminishing still the brand will play a major role inselling of the product.

Because of this, most of the manufacturers like, Videocon and Electrolux areacting as OEM manufacturers for manufacturing refrigerators of Samsungand LG. Even, players have increased the percentage of their advertising andmarketing costs as a percentage to operating income over the years; the ratiofor the industry has increased from 4.6% in 1993 to around 7% in 2000. The

brand building is very critical in the industry and constant advertising isnecessary.

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 21/52

Introduction:

The Consumer Durables industry consists of durable goods and appliancesfor domestic use such as televisions, refrigerators, air conditioners andwashing machines. Instruments such as cell phones and kitchen applianceslike microwave ovens were also included in this category.

The sector has been witnessing significant growth in recent years, helped byseveral drivers such as the emerging retail boom, real estate and housingdemand, greater disposable income and an overall increase in the level of affluence of a significant section of the population.

Major international and local players such as BPL, Videocon, Voltas, BlueStar, MIRC Electronics, Titan, Whirlpool, etc. represent the industry. Theconsumer durables industry can be broadly classified into two segments:Consumer Electronics and Consumer Appliances. Consumer Appliances can

be further categorized into Brown Goods and White Goods. The key productlines under each segment were as follows.

Industry Size, Growth, Trends:

The consumer durables market in India was estimated to be around US$ 5 billion in 2007-08. More than 7 million units of consumer durableappliances have been sold in the year 2006-07 with colour televisions (CTV)forming the bulk of the sales with 30 percent share of volumes. CTV,refrigerators and Air-conditioners together constitute more than 60 per centof the sales in terms of the number of units sold. In the refrigerators market,the frost-free category has grown by 8.3 per cent while direct cool segmenthas grown by 9 per cent. Companies like LG, Whirlpool and Samsung have

registered double-digit growth in the direct cool refrigerator market. In thecase of washing machines, the semi-automatic category with a higher baseand fully-automatic categories have grown by 4 per cent to 526,000 unitsand by 8 per cent to 229,000 units, respectively. In the air-conditionerssegment, the sales of window ACs have grown by 32 per cent and that of split ACs by 97 per cent. Since the penetration in the urban areas for these

products is already quite high, the markets for both C-TV and refrigerators

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 22/52

were shifting to the semi-urban and rural areas. The growth across productcategories in different segments is assessed in the following sections.

Consumer Electronics:

The CTV production was 15.10 million units in 2007-08 and is expected togrow by at least 25 per cent. At the disaggregated level, conventional CTVvolumes have been falling while flat TVs have grown strongly. Marketsources indicate that most CTV majors have phased out conventional TVsand have been instead focusing more on flat TVs. The flat segment of 12CTVs now account for over60 per cent of the total domestic TV

production and is likely to be around 65 per cent in 2007-08.High-end products such a s liquid crystal display (LCD)and plasma display CTV grew by 400 per cent and 150 percent respectively in 2009–10 following a sharpdecline in prices of these products and this trend is expected to continue. Theaudio/video player market has seen significant growth rates in the domesticmarket as prices have dropped. This trend is expected to continue through2009- 2010, as competition is likely to intensify to scale and capture themass market.

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 23/52

Changing

behavior of Consumers

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 24/52

Changing attitudes of Today’s customers:

Today customer likes to indulge in buying spree. No more the customers buyonly to fulfill their basic needs and emphasise on savings itself.

Indian consumers have become value sensitive and are not much pricesensitive as was the case earlier. If they feel that a particular product offers

them more value and its price is high, even then they are willing to buy the product.

The Indian consumers strictly follow their culture, tradition and values, as aresult of which foreign companies were forced to give an Indian touch tothem in order to succeed in India. McDonalds, MTV, Pepsi, Star TV, CocaCola India and many more had to Indianise themselves to flourish in India.Karva Chauth is celebrated with more zeal and enthusiasm than theValentine Day. The Indian consumer of today gives preference to features of a product rather than its brand name. The trend that higher segmentconsumers only buy the top brands has also come to an end.

Even after liberalization Indian companies and brands are doing very well. Itis clearly evident from the fact that despite many foreign brands being soldin India, Raymond is still India‘s largest textile company and Haldiram isdoing well despite the presence of McDonalds and Pizza Hut. Theconsumers today are not confined to a single brand and prefer change rather than sticking to the same brand. Not often do we see any home with cars of the same brand or household products of the same brand. The use of credit

card for shopping is a new emerging trend in India. Also consumers areavailing credit or loan from banks and other financial institutions to fulfilltheir needs and wants.

The Indian consumers are spending thick and fast on premium and luxury products. The Indian consumers have shown another major change in their buying behavior. They just don‘t want availability of products, they also

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 25/52

want better experience, services and ambience. This has led to the growth of shopping malls where shopping, entertainment and better facilities are allavailable under one roof. To a great extent the presence of heavy weightsuch as the pantaloons, big bazaar, croma , nilgiris etc has given a huge fillipto the growing market by not only selling products but also the experience.The Indian consumer are much more inclined to the organized sector.The rural Indian consumers are also showing signs of change. They have allthe modern amenities at their home and their standard of living is fastimproving. The rural households have earned huge money due to price risein real estate. They are also shifting towards industrial and services sector,hence their purchasing power is increasing. It is reflected in their livingstandard and possession of all electronic gadgets and luxury cars. There is astiff competition in the Indian market today and it has become a buyer‘smarket from seller‘s market. Customers are the ultimate beneficiary of the

fierce competition in the market. Competition has reduced prices to a greatextent and has forced the manufacturer to maintain product quality to sustainin the highly competitive market.

Though in a small way internet and telemarketing have also caught theattention of the Indian customers. Dell. Amazon .com, etc have carved agood niche for them in the sector. The consumers today do not mind availingcredit as when needed. So credit availability has become a key factor for determination of a buying a good. Consumers are also availing theinformation available on net through various forums and websites.

Marketer’s response to Consumer attitude:

With change in consumer buying behavior the companies also madenecessary changes in their marketing strategies. The changes include:

1) Launching of premium products by companies to fulfill requirements

of high class consumers.

2) Since purchasing power of rural India has increased, the companieshave started shifting their focus towards rural India to captureuntapped rural market. This has reaped huge benefits for companieslike in cases of PepsiCo, Coca Cola India and other FMCGcompanies.

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 26/52

3) Companies not only aim to sell their products but also aim to provide better after sales services to its consumers. For example companieshave provisions to send their technicians to repair the cars struck athighways or other outer locations due to technical failure or in case of a mishap. This improves the company‘s credibility and helps to buildits customer base.

4) Companies design their products on the basis of market segmentationso that they have products to suit every pocket and requirement.

5) Due to sharp growth in the communication sector, companies are providing many schemes and plan to attract customers. For example

mobile service providers provide lifetime option and free calls to other mobile users under a specific plan of the company.

6) Due to fierce competition in the electronics market and people‘swillingness to purchase hi-tech products the rates of LCD and plasmaTVs have been slashed by 25%-30%. Through this strategy electroniccompanies received very good response from the consumers in therecent past and were able to build a considerable market for their

products.

7) Indian consumers have developed a liking for foreign tours andholidays. This has led to development of many travel agencies that

provide a planned foreign tour at a reasonable price. What is evenmore interesting is that the customer does not have to pay the amountin lump sum; instead, he has the facility to make the payment inmonthly installments according to his convenience.

8) Consumers of India have developed a tendency to save travel time.For such consumers low fare or low cost carriers are available that

provide air travel facility at a very affordable price.

9) Consumers of India want better housing facilities. The constructioncompanies are fulfilling this requirement of consumers by providingthem luxurious houses, exquisite interiors, round the clock water andelectricity supply, full time security, club house, gymnasium, etc.within the premises.

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 27/52

10) Indian consumers are increasingly becoming aware of theimportance of health and hygiene. Hence companies are making

products to suit their health like low calorie, low fat food. As far ashygiene is concerned companies have fully mechanized their plants tomaintain hygiene and pack the food in such a way that it remains freshfor longer period of time and does not lose its nutritive value beforeconsumption.

11) The need for Internet is fast growing. To fulfill this need of consumers, mobile manufacturing companies are providing Internetaccess facility on mobile phones.

12) This has revolutionized the communication sector and

provided a means of communication that was never ever in anybody‘sdreams till a few year back.

13) Indian consumer‘s liking for credit is also increasing rapidly.Hence many financial institutions have come into existence in Indiaand are flourishing. Banks have also become liberal in their loan andcredit policies.

The road ahead:

The rising rate of growth of GDP, rising purchasing power of people withhigher propensity to consume with preference for sophisticated brandswould provide constant impetus to growth of white goods industry segment.

Penetration of consumer durables would be deeper in rural India if banksand financial institutions come out with liberal incentive schemes for thewhite goods industry segment, growth in disposable income, improving

lifestyles, power availability, low running cost, and rise in temperatures.

While the consumer durables market is facing a slowdown due to saturationin the urban market, rural consumers should be provided with easily payableconsumer finance schemes and basic services, after sales services to suit theinfrastructure and the existing amenities like electricity, voltage etc.

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 28/52

Currently, rural consumers purchase their durables from the nearest towns,leading to increased expenses due to transportation. Purchase necessarilydone only during the harvest, festive and wedding seasons — April to Juneand October to November in North India and October to February in theSouth, believed to be months `good for buying‘, should be converted toroutine regular feature from the seasonal character.

Rural India that accounts for nearly 70% of the total number of households,has a 2% penetration in case of refrigerators and 0.5% for washingmachines, offers plenty of scope and opportunities for the white goodsindustry.

The urban consumer durable market for products including TV is growingannually by 7 to 10 % whereas the rural market is zooming ahead at around

25 % annually. According to survey made by industry, the rural market isgrowing faster than the urban India now. The urban market is a replacementand up gradation market now.

The other factor for surging demand for consumer goods is the phenomenalgrowth of media in India. The flurry of television channels and the rising

penetration of cinemas will continue to spread awareness of products in theremotest of markets.

The vigorous marketing efforts being made by the domestic majors will helpthe industry. The Internet being now used by the market functionaries thatwill lead to intelligence sales of the products. It will help to sustain thedemand boom witnessed recently in this sector.

The ability of imports to compete is set to rise. However, the effective duty protection is still quite high at about 35-40 per cent. So, a flood of imports isunlikely and would be rather need based.

Reduction in import duties may significantly lower prices of products such

as microwave ovens, whose market size is quite small in India. Otherwise,local manufacturing will continue to stay competitive. At the same time,there will be some positive benefits in the form of reduction in input costs.Washing machines and refrigerators will also benefit from lower input costs.

According to a study by the McKinsey Global Institute (MGI), Indianincomes are likely to grow three-fold over the next two decades and India

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 29/52

will become the world's fifth-largest consumer market by 2025. In the givenscenario, urban markets will continue to fuel the Indian economy for quitesome time to come. Moreover, expenditure by the middle class accounts for the bulk of India‘s urban consumer expenditure. About 61 per cent of totalurban income comes from households that can be classified as middle class

—earning between US$ 1,493 and US$ 9,955 a year.

Further, India is likely to see rapid urbanization, with around 45 per cent of Indians living in urban areas by 2050, up from 30 per cent in 2007-08,according to a study co-authored by National Council of Applied EconomicResearch's (NCAER) Rajesh Shukla and Future Capital Research's RoopaPurushothaman.

According to a report by McKinsey, India's overall retail sector is likely to

grow to US$ 419.93 billion by 2015.

According to global real estate consultant, CB Richard Ellis, India hasmoved up to the 39th most preferred retail destination in the world in 2009,up from 44 last year. The turnover of the organized retail segment in India is

pegged at around US$ 8.1 billion. It is expected to reach US$ 51 billion by2010.

Retail opportunity is slated to rise by about US$ 160 billion in India in fiveyears. In urban India, modern retail is likely to grow from the current 9.6 per cent of total retail to 26 per cent in the next five years, as per Technopak Advisors

The Indian consumer durables market seems to be relatively untouched bythe economic slowdown. The consumer durable goods output witnessed a2.5 per cent rise in durables output in the first quarter of 2009, according to areport by the Development Bank of Singapore (DBS). Colour televisionshave seen an increase in sales, growing 2 per cent to 2.8 million units inJanuary-March 2009, according to the figures released by ORG-GFK.

Whirlpool is on the expansion mode and is targeting a 22 per cent share of the US$ 423.28 million washing machine market in India by the end of 2009, and is launching a range of new products with an investment of US$ 4million for the same.

Moreover, a large number of hi-technology durables are expected to floodthe US$ 4.03 billion Indian durables market in 2009. Samsung, LG, Haier

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 30/52

and Videocon are among companies planning new product launches in thecoming months

Major Organized &Unorganized Players

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 31/52

Major players:The major players in the consumer durables industry, operating in differentsectors such as air conditioners, washing machines, refrigerators &television include:

Samsung India:Acquired digital leadership in India by introducing its digital readytelevisions like the 40" LCD Projection TV, 43"Projection TV and the Planoseries of Flat Colour televisions.

LG India (CURRENT MARKET SHARE-23%):

LG Electronics rightly understood the consumer motivations to createmagnetic products, price them strategically, position them sharply and keepmaking the magnetism more potent. Having understood the finer differencesin consumer motivations, it opted for sharp-arrow reasons-to buy‘̳ differentiation over the blanket-all approach‘ taken by most of the other ̳

players. It is an aggressive marketer. It focuses on low and medium price

products.

Toshiba India:

Toshiba India Private Limited (TIPL) is the wholly owned subsidiary of Japanese Electronics giant Toshiba Corporation and was incorporated inIndia on September 2001. Toshiba had a presence in India since 1985 andwas represented in India through their Liaison Office.

Sony India (CURRENT MARKET SHARE-21-22%):

Sony Corporation, Japan, established its India operations in November 1994.In India, Sony has its distribution network comprising of over 7000 channel

partners, 215 Sony World and Sony Exclusive outlets and 21 direct branchlocations. The company also has presence across the country with 21

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 32/52

company owned and 172 authorized service centres.

Sharp India Ltd:

Sharp India ltd was incorporated in 1985 as Kalyani Telecommunicationsand Electronics Pvt Ltd, the company was converted into a public limitedcompany in the same year. The name was changed to Kalyani Sharp India in1986. The company was entered into a joint venture with Sharp Corporation,Japan - a leading manufacturer of consumer electronic products tomanufacture VCRs/VCPs/VTDMs. The company manufactures consumer electronic goods such as TVs, VCRs, VCPs and audio products. The

products were sold under the Optonica brand name. Sharp has a production base in 26 countries with 33 plants, and its products are used in 133countries. The company was accredited with the ISO-9001 certification in

the month of February, 2001.

Hitachi India:

Hitachi India Ltd (HIL) was established in June 1998 and engaged inmarketing and sells a wide range of products ranging from Power andIndustrial Systems, Industrial \Components & Equipment, Air Conditioning& Refrigeration Equipment to International Procurement of software,materials and components. Some of HIL‘s product range includes

Semiconductors and Display Components. It also supports the sale of Plasma TVs, LCD TVs, LCD Projectors, Smart Boards and DVDCamcorders.

Mirc Electronics (ONIDA):

The company commands strong brand equity among consumers largelyowing to the success of its Onida brand. High-quality designs have made thecompany a leading player in the electronics and entertainment business. Its

popular devil ad although had engendered a strong emotional pull towardsthe brand, Technologically it represented no advancement. The company

plugged the gap by touting its digital technology. Like Videocon, it has also been able to hold its market share. The world-class quality of Onida hasenabled the company to make a breakthrough on the export front. Onida is aleading brand in Gulf market and also exports its models to Africa,Bangladesh, Sri Lanka and Nepal. It has technical tie-up with the Japan

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 33/52

Victor Company, better known as JVC. So focused is Onida on positioningitself on the premium, high-tech plank that it is even planning to push itsown envelope on obsolescence, much like Intel has been doing in its ownindustry. The strategy is aimed at further broad basing the product offeringof the company, which has largely dominated the top-end of the televisionmarket, across multiple market segments. Besides understanding the strategyadopted by different players, several other factors- industry growth,concentration and balance, corporate stakes, fixed cost, and productdifferences need to be analyzed to determine the extent of rivalry betweenthe existing players.

Videocon (CURRENT MARKET SHARE-12%):

It is the market leader in the consumer electronics and home appliances

segments in India; the company manufactures home appliances such asrefrigerators, microwave ovens, compressors, air conditioners and washingmachines.It has plans to acquire Daewoo‘s consumer electronics businesses worldwideto bring LCD TVs, plasma TVs and components into its fold; the movewould also help it acquire a consuming partner for the recently acquiredThomson‘s picture tube business. Videocon has always been a price player and has an image of a low price brand. This entails providing more featuresat a given price vis-à-vis competitors. It has taken over multinational brands

to cater to un served segments, like Sansui- to flank the flagship brandVideocon in the low to mid priced segment, essentially to fight against

brands like BPL, Philips, and Onida and taken over Akai- tail end brand or brands like Aiwa. Videocon is one of the largest manufacturers of televisionand its components in India and thus has advantages of economies of scaleand low cost due to indigenization. It has the widest distribution network inIndia with more than 5000 dealers in the major cities .It also has a strong

base in the semi- urban and rural markets. Due to its multi-brand strategy, ithas at present multiple brands at the same price point. This has led to a stateof diffused positioning for its brands. It has also led to a cannibalization of sales among these brands. The flagship brand Videocon has lost marketshare due to the presence of Sansui in the same segment. Because of reduction in import duties on CPT the cost advantage of Videocon is also onthe decline. Hence it is facing rough weather and also trying to boostexports.

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 34/52

Panasonic India (CURRENT MARKET SHARE-6%):

Panasonic Corporation based in Osaka, Japan is a worldwide leader in thedevelopment and Manufacture of electronic products for a wide range of consumer, business, and industrial needs. Panasonic Electric Works Co.,Ltd. traces its roots to the company started in 1918 by Konosuke Matsushita.Panasonic India plans to invest USD 100 million in its new plasma TV

production facility in 2011.The company currently has five production units in the country, at Noida,Gurgaon, Vadodara, Chennai and Delhi. It also launched the worlds

slimmest, 1-inch plasma TV called Vierra PDP Z1.According to PanasonicThe market potential for plasma TV was much greater in India than China,The demand for such high-end sets was increasing at a rate of 4- 10 per centin the country. The company has priced its plasma TV between Rs 24,000and Rs 30 lakh (for a 103-inch screen). It has already sold ten such units thismonth.

Agrawal Group - Manufactures consumer electronic products; radios,

tape-recorders, car stereos and CD systems.

Anchor - Manufactures electrical switches, accessories, lighting

luminaries, and PVC wires, domestic appliances like electrical irons, mixers,grinders, toasters and fans.

Bajaj International - Exporters of electrical fans, household appliances,lamps, fluorescent tube lights, light fittings, hoists etc. Imports steel andengineering items.

BOSS Portable Blenders - Manufacturer and exporter of portable

blender and home appliances includes hand held mixers, juice makers,stainless steel blender and more.

E.P.C Industrial Fans & Motors - Manufacturers & Exporters of industrial fans, domestic fans, instrument cooling fans, cabin fans, electricfans & electric motors.

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 35/52

Eureka Forbes - Details on consumer products include vacuum cleaners,

floor care equipment, high-pressure water jet cleaners and electronic securitysystems.

Global Wonders - The fastest search engine, directory, map and webguide for information on the most popular websites. Features list of wholesaler, retailer along with

products list, consumer durable and more.

Hot shine Appliances - U.P - Manufacturers of gas cookers & stoves &

electrical appliances, product range includes cooking ranges, steam irons,oven toaster and grillers.

Kelvin Systems - Dealers for Carrier Aircon Ltd (air-conditioningequipment), Honda (Siel) Power Products Ltd (portable electric generators),and Eureka Forbes Ltd (vacuum cleaners).

Mangal Singh & Sons - Dealers in home appliances, consumer goods

and electrical appliances, includes television, refrigerator, audio products,washing machines, vacuum flask, cooking range, oven and dining sets.

Moniba - Manufactures chemical pump, air operated pump, water purifier,health care product, and bacteria free water, home appliances and chemical

plant machinery.

Nadi Industrial Fans - Manufacturers of fans; product range includes

axial fans, centrifugal fans and special fans.

Onida - Provide an online showroom to purchase the entire range of Onida

products. Offers free delivery.

Orient Fan - Specialized in manufacturing mini motors, deluxe decorative

ceiling fans, shaded pole motors, box fans, food blender, food mixer, fruit juicer, vacuum cleaner etc.

Padmini Appliances - Manufacturers of gas stoves, oven-toaster-griller, juicer- mixer-grinder, electric hot plates, washing machines, ceiling fans,water heaters, irons etc.

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 36/52

Philips - Details for consumer electronics, lighting, domestic appliances,

semi conductors, components, enabling technologies, multi media projectorsetc.

PICASSO Home Products - Manufacturer and Exporter of varioushome appliances like roti maker, mixer grinder, sandwich maker, oventoaster griller, Non Stick Appliances and more.

Salora - Manufactures black-and-white & color television sets, Panasonic

fax machines, printers, and digital cameras; color monitors and cordless phones.

Sansui India - Manufacturer of electronic products, audio systems, hometheatres, projection TVs, video CDs and home appliances.

Singer - Manufacturers of sewing machines, food processors, refrigerators,televisions, oven, toasters, washing machines, electric irons etc.

Sony India - Details of product ranges from color TVs, hi-fi musicsystems, video CDs, home theatre systems, DVDs, portable audio systems,digital cameras, RMEG products, Wega T.V etc.

Sony World - Features wide ranges of products: car audios, handy cams,

digital cameras, VCD, LD, DVD players, cordless phones, Walkman, anddisc mans, and Televisions.

Sumeet - Manufacturers of mixer-grinders. Offers details about themachines, recipes, Sumeet outlets and more.

Sunflame Appliances - Manufacturers of kitchen appliances, home

appliances and electrical appliances in India.

Usha International - Manufacturer of sewing machines, fans, air

conditioners, water coolers, home appliances, agricultural and domestic pump sets, and auto products.

Usha Lexus - Makers of home appliances like sandwich toasters, juicer,

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 37/52

mixer grinders, ovens, ventilating fans, irons and room coolers.

Videocon - Suppliers of home appliances, TVs, refrigerators, ACs, air conditioners, audios, tape recorder, colour monitors, digital organizers,

Kenwood digital hi-fi systems, television sets etc.

Vijay Sales - Dealers in consumer durables includes details for their

product, customer care, schemes, consumer finance, and more.

Voltas Limited - Makers of room air conditioners and refrigeration

equipment, water coolers, cranes, pumps and office furniture; includesmachine tools, industrial chemicals etc.

L.G India - Details of product ranges from colour TVs, hi-fi musicsystems, video CDs, home theatre systems, DVDs, portable audio systems,digital cameras, RMEG products, T.V etc. Features wide ranges of products:car audios, handy cams, digital cameras, VCD, LD, DVD players, Cdmamobiles, walkman, and disc mans, and Televisions.

Samsung Electronics India Ltd - Details of product ranges fromcolour TVs, hi-fi music systems, video CDs, home theatre systems, DVDs,

portable audio systems, digital cameras, RMEG products, T.V etc. Featureswide ranges of products: car audios, handy cams, digital cameras, VCD, LD,

DVD players, mobiles, Walkman, and disc mans, and Televisions. There has been strong competition between the major MNCs like Samsung, LG, andSony.

LG Electronics India Ltd has announced its extension plan in 2006. Thecompany is going to invest $250 million in India by 2011 and is planning toestablish a manufacturingfacility in Pune.

TCL Corporation is also planning to establish a $22 million manufacturingfacility in India. The Indian companies like Videocon Industries and Onidaare also planning to expand. Videocon has acquired Electrolux brand in ndia.Also, with the acquisition of Thomson Displays by Videocon in Poland,China, and Mexico, the company is marking its international presence.According to supply Corporation (Applied Market Intelligence), country'sfiscal policy has encouraged Indian consumer electronic industry. The

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 38/52

reduction on import duty in the year 2005-06 has benefited many companies,such as Samsung, LG, and Sony. These companies import their premiumend products from manufacturing facilities that are located outside India.Indian consumers are now replacing their existing appliances with frost-freerefrigerators, split air conditioners, fully automatic washing machines, andcolor televisions (CTVs), which are boosting the sales in these categories.Some companies like Samsung Electronics Co. Ltd. and LG ElectronicsIndia Ltd. are now focusing on rural areas also. These companies areintroducing gift schemes and providing easy finance to capture the consumer

base in rural areas.

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 39/52

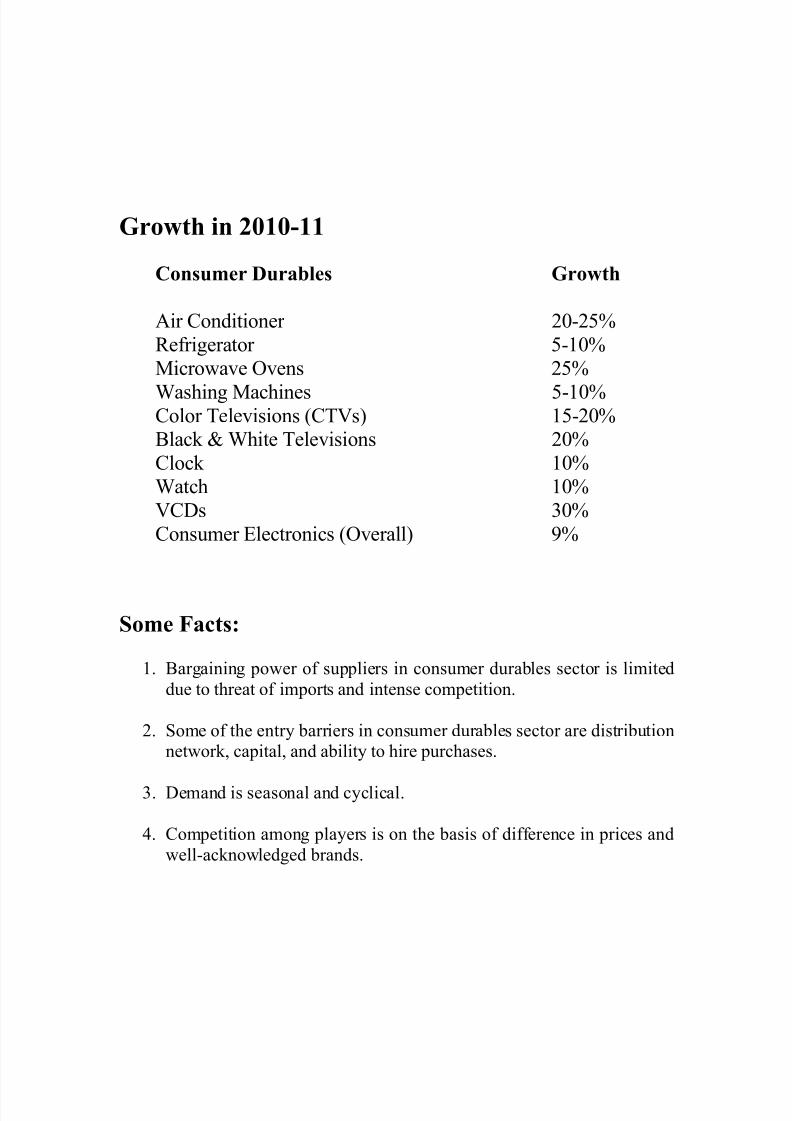

Growth in 2010-11

Consumer Durables Growth

Air Conditioner 20-25%Refrigerator 5-10%Microwave Ovens 25%

Washing Machines 5-10%Color Televisions (CTVs) 15-20%Black & White Televisions 20%Clock 10%Watch 10%VCDs 30%Consumer Electronics (Overall) 9%

Some Facts:

1. Bargaining power of suppliers in consumer durables sector is limiteddue to threat of imports and intense competition.

2. Some of the entry barriers in consumer durables sector are distributionnetwork, capital, and ability to hire purchases.

3. Demand is seasonal and cyclical.

4. Competition among players is on the basis of difference in prices andwell-acknowledged brands.

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 40/52

Marketing Strategies:

They studied closely and picked up the salient features of the Japanesemanufacturing and made themselves an expert in that.

Their planning is very meticulous on the execution of the job in hand.

The Koreans never shown any bias against India. The Americans andJapanese took their brand equity for granted. The Koreans did not. Asa result of this they didn‘t make any value judgments of the Indian

customers and introduced contemporary products. This way they gottheir brand noticed.

Both L.G and Samsung have consistently launched contemporarymodels-be it fuzzilogic washing machines, flat screen TVs or microwave ovens-in step with their launchglobally.

Further power was added to this strategy of dazzling Indians withglobal products was their high advertising spends. L.G spent Rs 110crores in advertising while Samsung spent Rs 80 crore in 2001. In2003 L.G spent Rs 225 crores and Samsung Rs 100 Crores. Such highvoltage advertising has made the Koreans the biggest spenders in their

businesses, and they outspend competition by a factor of at least two.These spends have placed the Koreans in the class of some of thehighest spenders in India such as Colgate, ITC, Dabur and HindustanLever.

They are huge buyers of advertising so they exude through a lot of visible brand building.

The Koreans have also started making a name for their ability tounderstand what customers want. They practice this shibboleth withunusual vigor.

They figure out quickly and very well what the consumer wants. Butthe important part is they quickly adapt their strategies accordingly.

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 41/52

Unlike U.S companies following the office marketing strategy theKoreans follow the principle of Feet marketing‘. That means even the̳ higher officials roam about the market to give boost to dealers andalso to gather the first hand information on the current marketconditions. This helps in knowing the ground realities better whichresults in a better strategy.

The Koreans always think big and take risks. That‘s why they haveinfused so investment, which is now bearing the fruits.

Players like Whirlpool and Electrolux that made a foray into consumer electronics around the same time that L.G and Samsung did. Theyhedged bets by buying existing brands and capacities here

(Kelvinator, Maharaja, Allwyn, and the like) while the Koreans builtcapacity from scratch and gives them an edge over the competitors.

The Koreans want to outdo the Japanese. They don‘t start on a hunch.Their planning is meticulous. When they take up a job they take itvery seriously.

All Korean managers bring on board a monk like devotion to their task at hand. This ensures quick execution of the work.

The Koreans believe that manufacturing is a key strength and that‘swhy they eschew contract manufacturing and invest in their ownmanufacturing facilities around the globe.

They have culture sensitive workshops to ensure that the Koreans andIndians work well together.

They bundle one product with another so as to promote the weaker one backed by the established product.

They have well-entrenched the consumers in India by sponsoring anumber of premier events like cricket matches and others with a highTRP ratings.

According to prof. R.R.Krishnan at center for East Asian Studies of

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 42/52

Jawaharlal Nehru University the insecurity element in the history of Korean comprising colonization, acquisition of their country in the

past tends them to form a marketing strategy that requires best of them.

Though the Koreans are making huge profits in India they have notfully presented themselves in India. Many business like chipmanufacturing, humungous chemicals, energy business etc. whichthey are operating in other countries has not found its way to India.The reason being the instability and lack of infrastructure of India tosupport these businesses. This shows their marketing tactics and their inclination towards the prelaunch test that they conduct beforeinduction of each product in India.

The Koreans always do a prelaunch market survey unlike its Japaneseor U.S counterparts who take their brand equity for granted. Thisresearch gives useful inputs to the Korean players and also times toadapt them for the new situation.

BACKGROUND:

Prior to liberalization, the Consumer Durables sector in India was restrictedto a handful of domestic players like Godrej, Allwyn, Kelvinator and Voltas.

Together, they controlled nearly 90% of the market. Players like BPL andVideocon first super ceded them in the early 1990s, who invested in brand

building and in enhancing distribution and service channels. Then, withliberalization came a spate of foreign players from LG Electronics to Sonyto Aiwa. Both rising living standards, especially in urban India, and easyaccess to consumer finance have fuelled the demand for consumer durablesin the country. Also, the entry of a large number of foreign players meansthe consumer is no longer starved for choice. But this has also resulted in anover-supply situation in recent times as growth levels have tapered off.

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 43/52

Micro Level Analysis

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 44/52

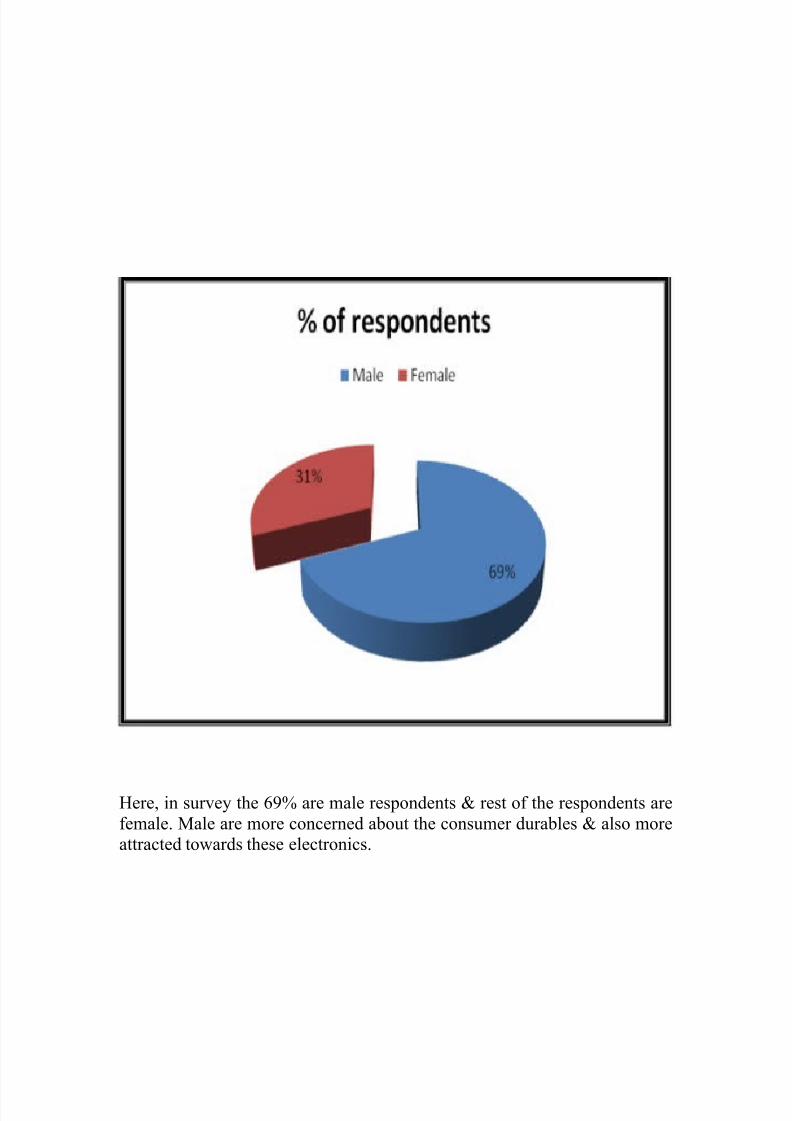

Here, in survey the 69% are male respondents & rest of the respondents arefemale. Male are more concerned about the consumer durables & also moreattracted towards these electronics.

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 45/52

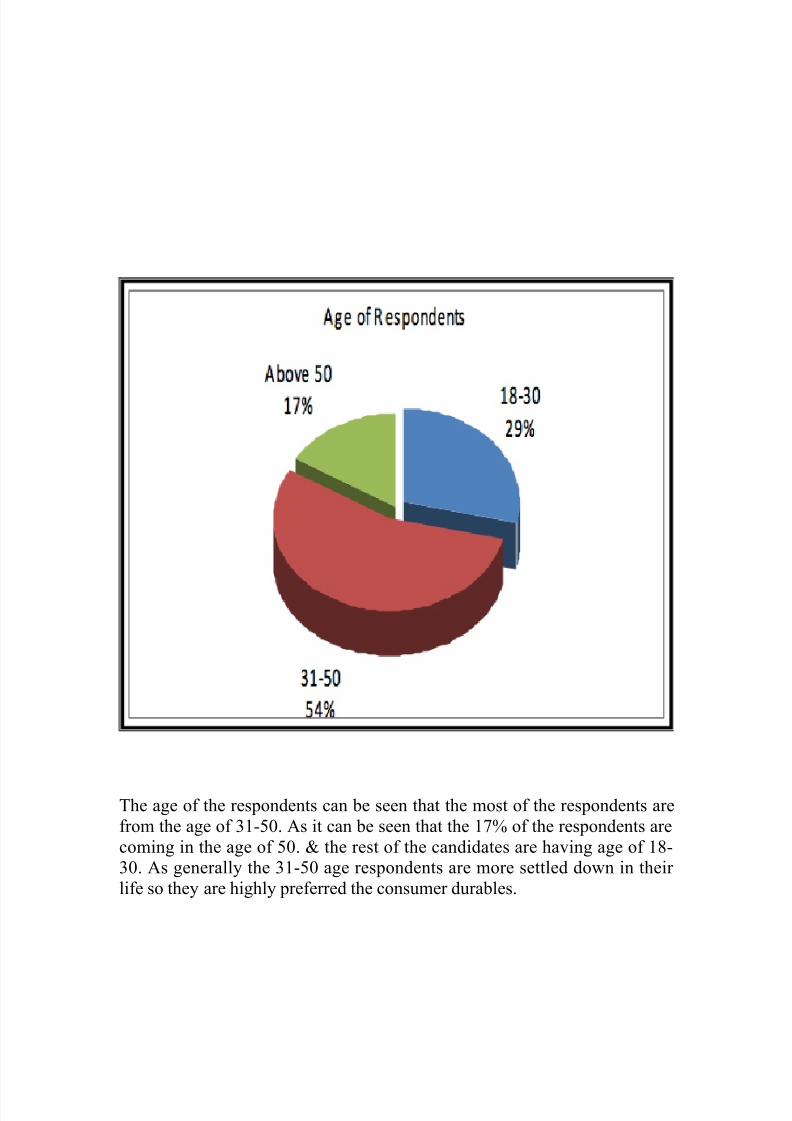

The age of the respondents can be seen that the most of the respondents arefrom the age of 31-50. As it can be seen that the 17% of the respondents arecoming in the age of 50. & the rest of the candidates are having age of 18-30. As generally the 31-50 age respondents are more settled down in their life so they are highly preferred the consumer durables.

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 46/52

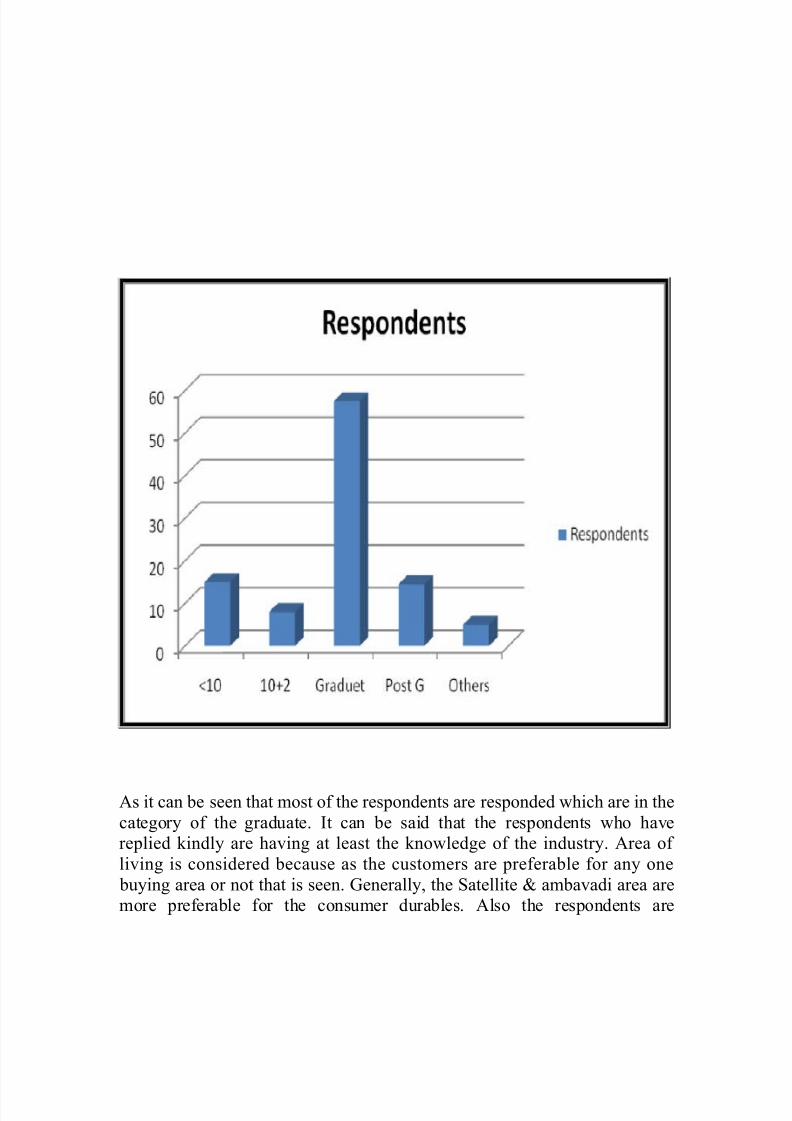

As it can be seen that most of the respondents are responded which are in thecategory of the graduate. It can be said that the respondents who havereplied kindly are having at least the knowledge of the industry. Area of living is considered because as the customers are preferable for any one

buying area or not that is seen. Generally, the Satellite & ambavadi area aremore preferable for the consumer durables. Also the respondents are

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 47/52

generally belongs to these particular areas from Ahmedabad.

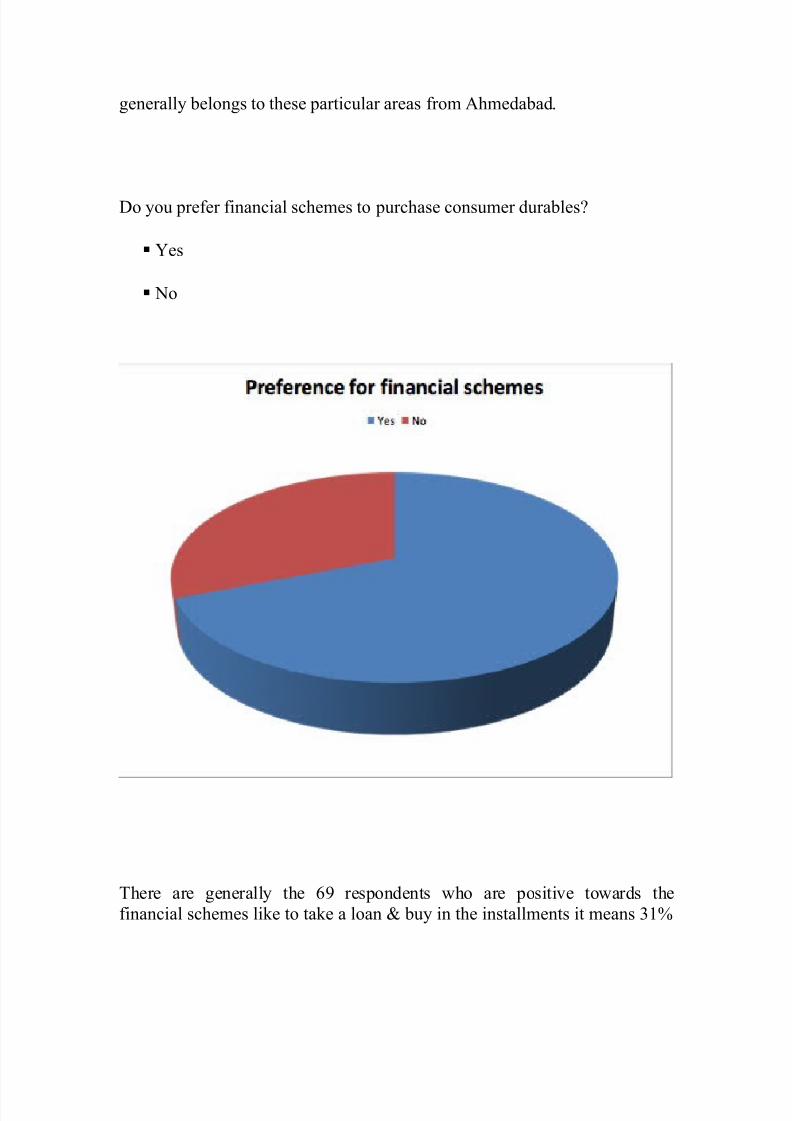

Do you prefer financial schemes to purchase consumer durables?

Yes

No

There are generally the 69 respondents who are positive towards thefinancial schemes like to take a loan & buy in the installments it means 31%

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 48/52

of the respondents are not interested to take a loan.

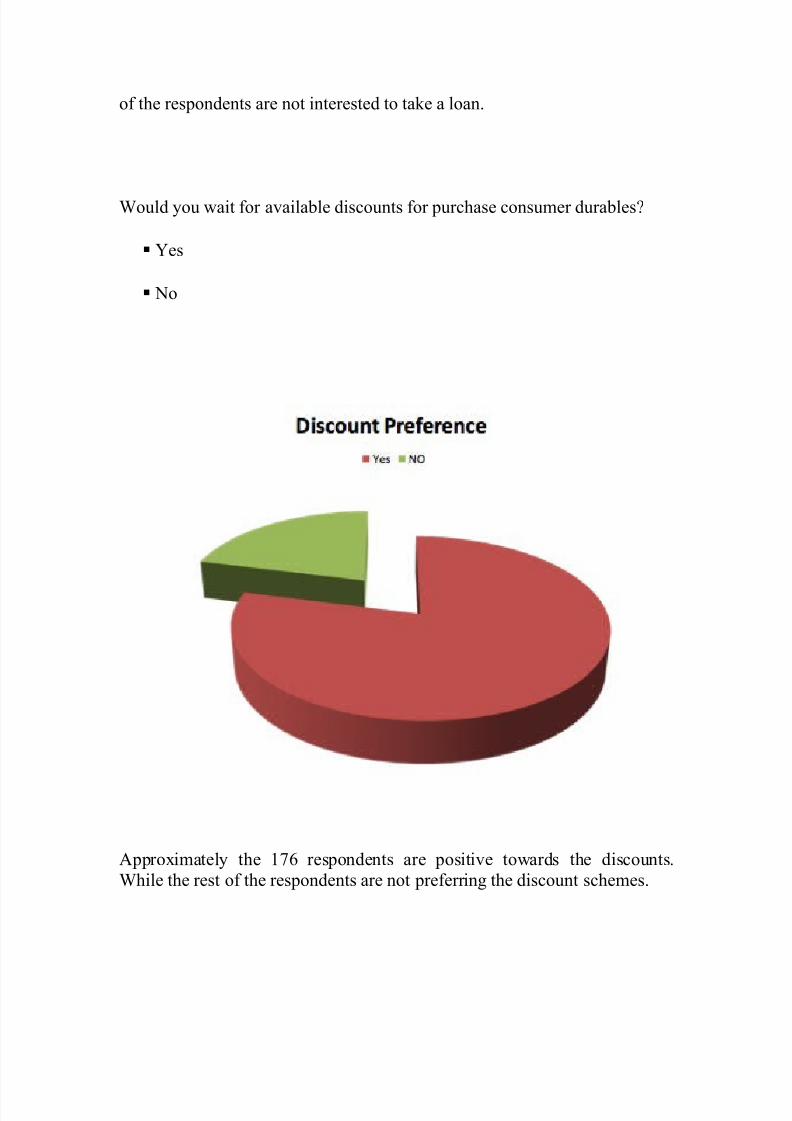

Would you wait for available discounts for purchase consumer durables?

Yes

No

Approximately the 176 respondents are positive towards the discounts.While the rest of the respondents are not preferring the discount schemes.

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 49/52

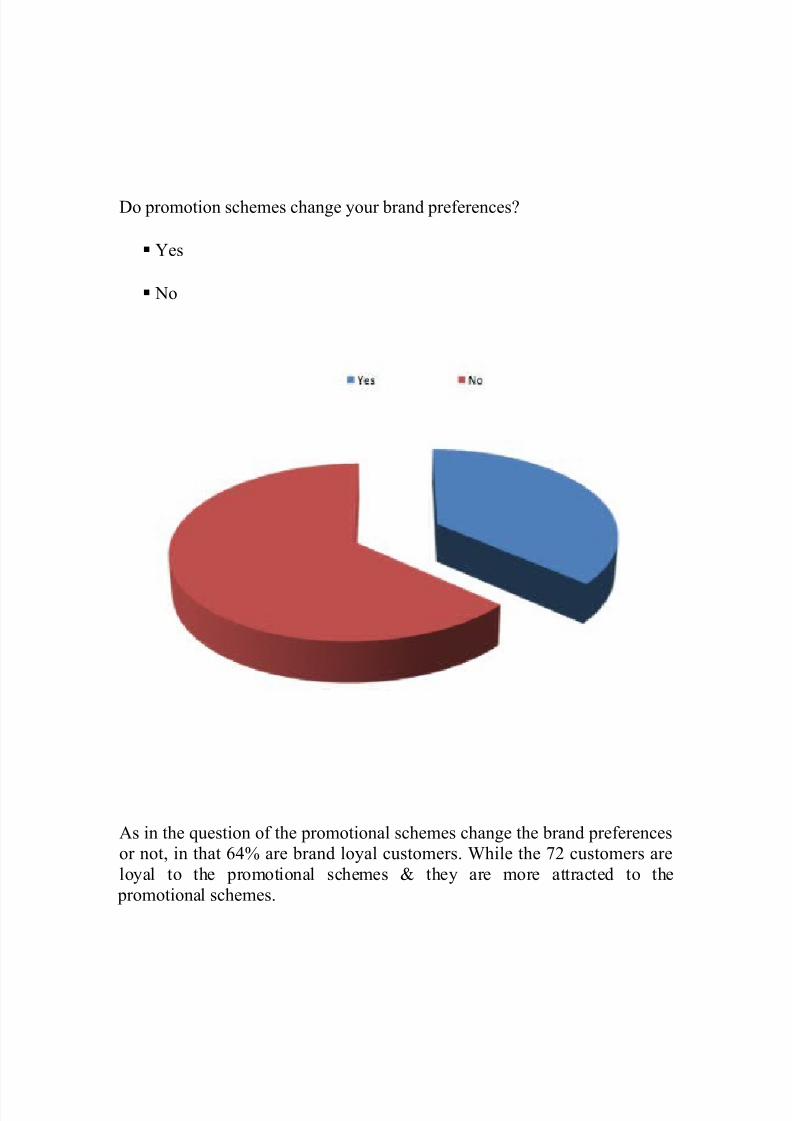

Do promotion schemes change your brand preferences?

Yes

No

As in the question of the promotional schemes change the brand preferencesor not, in that 64% are brand loyal customers. While the 72 customers areloyal to the promotional schemes & they are more attracted to the

promotional schemes.

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 50/52

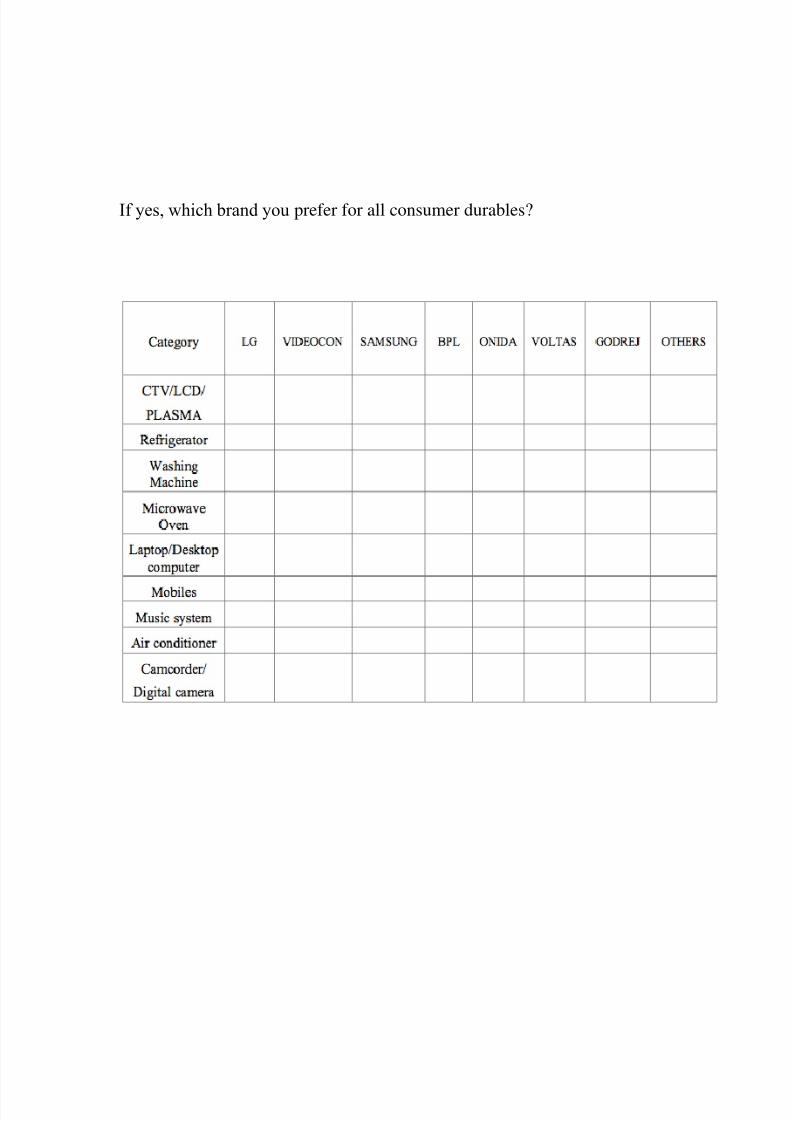

If yes, which brand you prefer for all consumer durables?

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 51/52

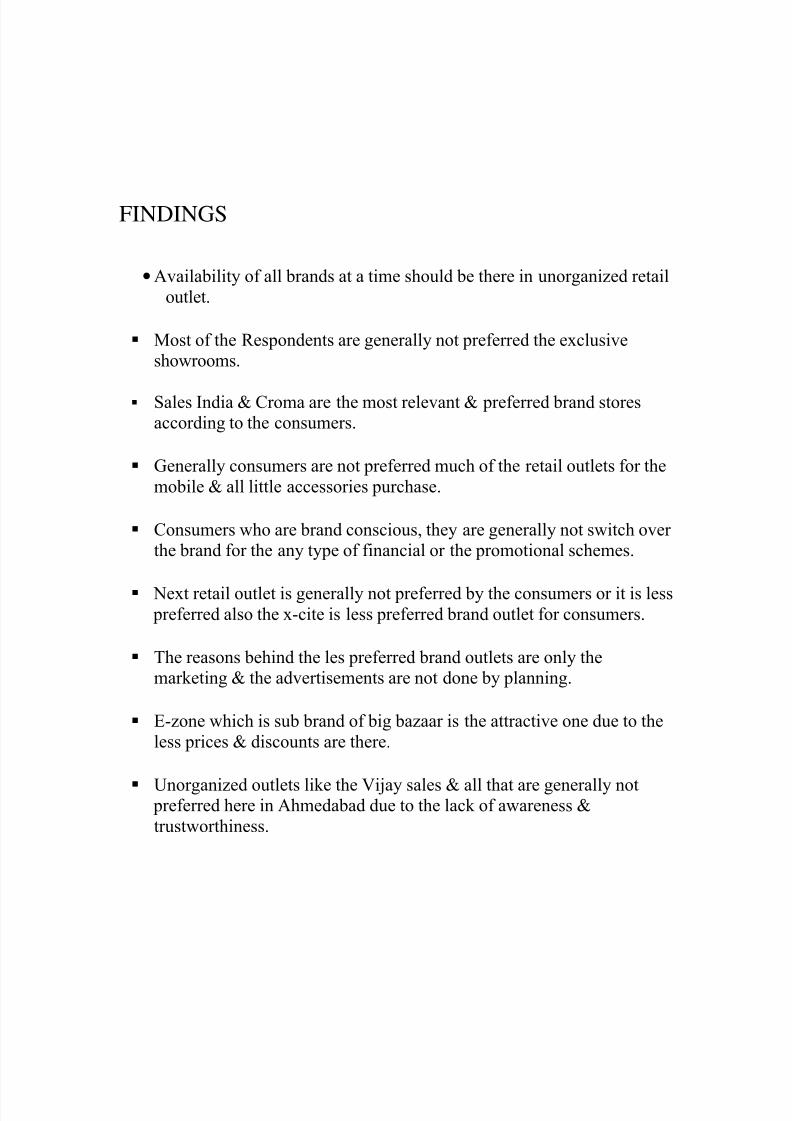

FINDINGS

•Availability of all brands at a time should be there in unorganized retailoutlet.

Most of the Respondents are generally not preferred the exclusiveshowrooms.

Sales India & Croma are the most relevant & preferred brand storesaccording to the consumers.

Generally consumers are not preferred much of the retail outlets for themobile & all little accessories purchase.

Consumers who are brand conscious, they are generally not switch over the brand for the any type of financial or the promotional schemes.

Next retail outlet is generally not preferred by the consumers or it is less preferred also the x-cite is less preferred brand outlet for consumers.

The reasons behind the les preferred brand outlets are only themarketing & the advertisements are not done by planning.

E-zone which is sub brand of big bazaar is the attractive one due to theless prices & discounts are there.

Unorganized outlets like the Vijay sales & all that are generally not preferred here in Ahmedabad due to the lack of awareness &trustworthiness.

8/3/2019 Govind Dissertation

http://slidepdf.com/reader/full/govind-dissertation 52/52

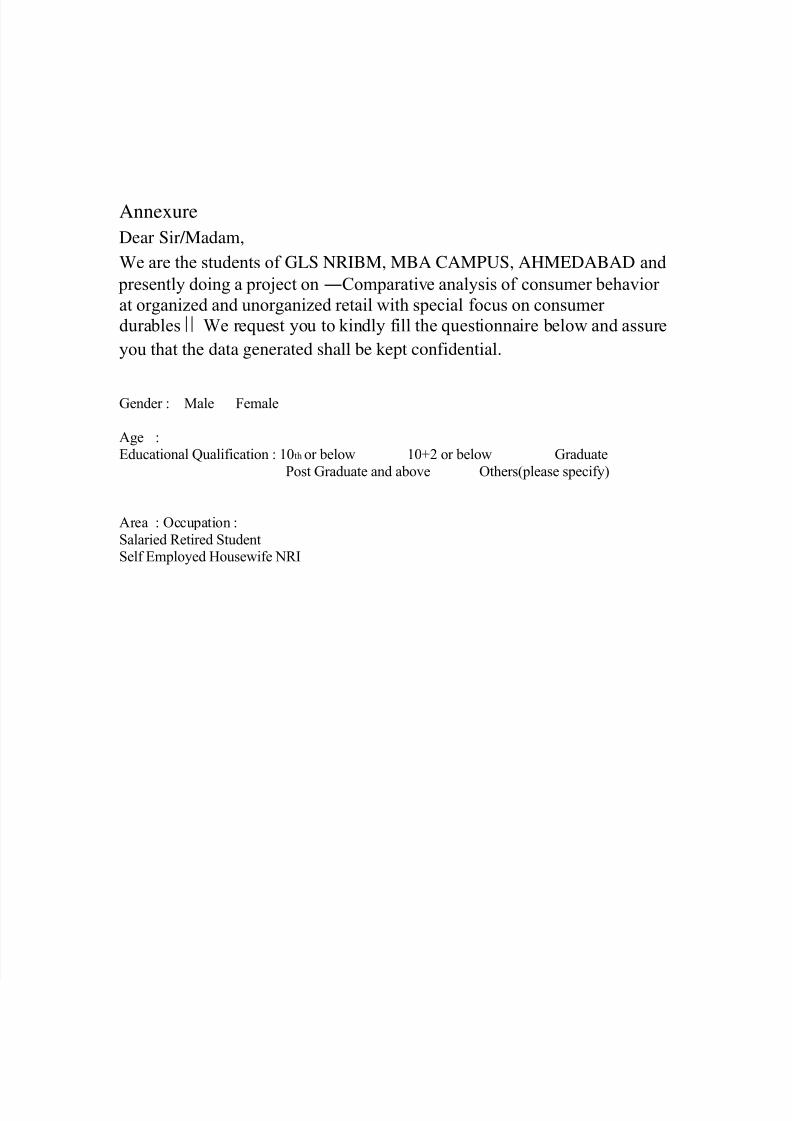

Annexure

Dear Sir/Madam,

We are the students of GLS NRIBM, MBA CAMPUS, AHMEDABAD and

presently doing a project on ―Comparative analysis of consumer behavior at organized and unorganized retail with special focus on consumer durables We request you to kindly fill the questionnaire below and assure‖

you that the data generated shall be kept confidential.

Gender : Male Female

Age :Educational Qualification : 10th or below 10+2 or below Graduate

Post Graduate and above Others(please specify)

Area : Occupation :Salaried Retired StudentSelf Employed Housewife NRI