global events disturb fertilizer makers

TRANSCRIPT

News of the Week

GLOBAL EVENTS DISTURB FERTILIZER MAKERS At the Fertilizer Institute's annual meeting in Chicago, institute members were wondering what was going to happen next. Still trying to come to grips with President Carter's partial embargo on grain shipments to the U.S.S.R., and still trying to figure out why ammonia was in such short supply—when a glut had been predicted—they were then faced with the news that the Commerce Department had, in effect, also suspended exports of phosphates and phosphate derivatives to the U.S.S.R. (see page 7).

Nevertheless, fertilizer producers and dealers were holding up fairly well. FI statistics show a 14% increase in domestic disappearance of fertilizer materials for the first six months of the 1979-80 fertilizer year (beginning July 1), compared to the corresponding 1978-79 period. Production was averaging about 7% higher during the period, so that producer inventories were generally at record low levels.

FI president Edwin M. Wheeler, summing up the "state of the industry" at the Chicago meeting, said that farmers will continue to use large quantities of fertilizer. He predicts that U.S. shipments in the 1979-80 fertilizer year certainly will equal and probably surpass the "near-record" 51 million tons moved in 1978-79.

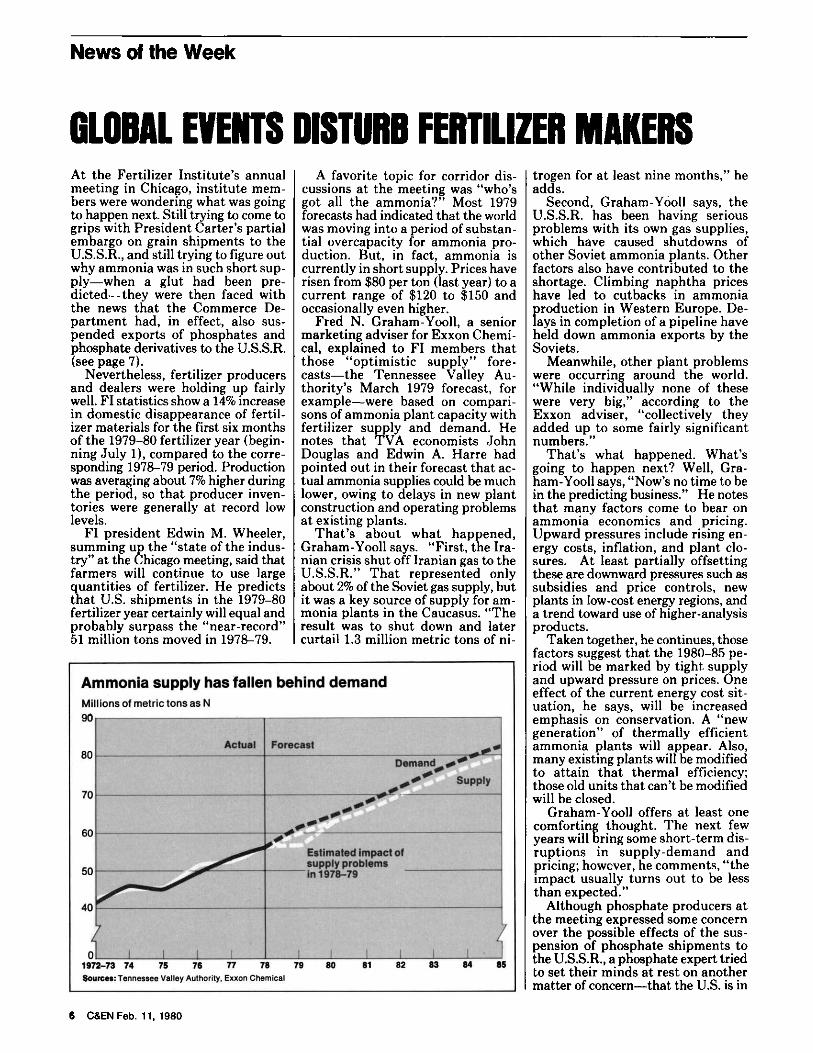

A favorite topic for corridor discussions at the meeting was "who's got all the ammonia?" Most 1979 forecasts had indicated that the world was moving into a period of substantial overcapacity for ammonia production. But, in fact, ammonia is currently in short supply. Prices have risen from $80 per ton (last year) to a current range of $120 to $150 and occasionally even higher.

Fred N. Graham-Yooll, a senior marketing adviser for Exxon Chemical, explained to FI members that those "optimistic supply" forecasts—the Tennessee Valley Authority's March 1979 forecast, for example—were based on comparisons of ammonia plant capacity with fertilizer supply and demand. He notes that TVA economists John Douglas and Edwin A. Harre had pointed out in their forecast that actual ammonia supplies could be much lower, owing to delays in new plant construction and operating problems at existing plants.

That's about what happened, Graham-Yooll says. "First, the Iranian crisis shut off Iranian gas to the U.S.S.R." That represented only about 2% of the Soviet gas supply, but it was a key source of supply for ammonia plants in the Caucasus. "The result was to shut down and later curtail 1.3 million metric tons of ni-

Ammonia supply has fallen behind demand Millions of metric tons as Ν 90 r

80

70

60

50

40

; i

Actual )

\\

\

)1 ι !

Forecast _ J Demand ^ ^ ^ ++* Supply

- " " Estimated impact of supply problems in 1978-79

I I Ι Ι Ι Ι Ί 1972-73 74 75 76 77 78 79 Sources: Tennessee Valley Authority, Exxon Chemical

81 82 83 84 85

trogen for at least nine months," he adds.

Second, Graham-Yooll says, the U.S.S.R. has been having serious problems with its own gas supplies, which have caused shutdowns of other Soviet ammonia plants. Other factors also have contributed to the shortage. Climbing naphtha prices have led to cutbacks in ammonia

[>roduction in Western Europe. De-ays in completion of a pipeline have

held down ammonia exports by the Soviets.

Meanwhile, other plant problems were occurring around the world. "While individually none of these were very big," according to the Exxon adviser, "collectively they added up to some fairly significant numbers."

That's what happened. What's going to happen next? Well, Graham-Yooll says, "Now's no time to be in the predicting business." He notes that many factors come to bear on ammonia economics and pricing. Upward pressures include rising energy costs, inflation, and plant closures. At least partially offsetting these are downward pressures such as subsidies and price controls, new plants in low-cost energy regions, and a trend toward use of higher-analysis products.

Taken together, he continues, those factors suggest that the 1980-85 period will be marked by tight supply and upward pressure on prices. One effect of the current energy cost situation, he says, will be increased emphasis on conservation. A "new generation" of thermally efficient ammonia plants will appear. Also, many existing plants will be modified to attain that thermal efficiency; those old units that can't be modified will be closed.

Graham-Yooll offers at least one comforting thought. The next few years will bring some short-term disruptions in supply-demand and pricing; however, he comments, "the impact usually turns out to be less than expected."

Although phosphate producers at the meeting expressed some concern over the possible effects of the suspension of phosphate shipments to the U.S.S.R., a phosphate expert tried to set their minds at rest on another matter of concern—that the U.S. is in

6 C&ENFeb. 11, 1980

danger of running out of phosphate rock.

Judson H. Drewry, president of International Minerals & Chemical's fertilizer group, cited a recent General Accounting Office study that concludes that U.S. phosphate reserves amount to about 2.2 billion metric tons, adequate only for the next 20 years or so. The study predicts that phosphate rock production will start to decline around 1985, and that the U.S. will be increasingly dependent on imports.

The GAO study is flawed, Drewry says, because it "used U.S. Bureau of Mines data that limit reserves to deposits that can be produced for $15 per ton or less, and discounts future price or technological improvements." He concedes that the rich "Bone Valley" deposits in Florida may be depleted in about 25 years.. However, he says, another large phosphate resource, the Hawthorn formation, stretches over parts of Florida, Georgia, and North and South Carolina.

"This formation will be the prime source of future mines, some within three or four years," Drewry says. Florida alone, he notes, has some 25 billion tons of phosphate resources, according to U.S. Geological Survey estimates; on that basis, Florida will continue to be a phosphate source for several hundred more years. IMC is convinced, Drewry says, that U.S. phosphate resources are adequate for all reasonable future projections and that exhaustion of resources cannot now be predicted realistically. D

Phosphate exports to Soviets suspended Until the government completes a review of its export control policy, which could take two to four weeks, the Department of Commerce will require validated export licenses for "phosphate" shipments to the U.S.S.R.

Commerce's action, although not an embargo on phosphate rock, phosphoric acid concentrates, and superphosphoric acid fertilizer, effectively suspends shipments of these commodities to the U.S.S.R. until the export policy review is completed. If these phosphate commodities are not embargoed at the study's completion, future shipments nevertheless will require prior Commerce approval. Before Commerce Secretary Philip M. Klutznick announced this latest retaliatory action against the Soviet Union, such exports were permitted under "general" export licenses, which required no review.

The fate of Occidental Petroleum's 20-year agreement with the Soviet Union hangs in the balance. Under the long-term contract, Occidental exports superphosphoric acid fertilizer to the U.S.S.R. and imports anhydrous ammonia fertilizer.

An Occidental spokesman says the company is certain that the export policy review will be completed expeditiously. Further, the company contends that its fertilizer agreement with the U.S.S.R. is in the "national interest." Halting phosphate exports, Occidental says, will not hurt the Soviets since other countries have additional phosphate available for export. These other countries include Jordan, Morocco, and South Africa.

Occidental feels certain that

Ehosphate exports will not be em-argoed in the future. However, if

such an embargo is imposed, Occidental says it can sell 80% of its phosphates elsewhere.

This latest government action follows on the heels of the embargo on 17 million metric tons of grain to the U.S.S.R., and the reduction from 1.5 million to 1.0 million metric tons of anhydrous ammonia fertilizer from the U.S.S.R. D

New weather-resistant plastic introduced A resin formulation designed to bridge the cost-performance gap between acrylonitrile-butadiene-sty-rene (ABS) on the one hand and polycarbonates and polyphenylene oxides on the other has been introduced by Uniroyal Chemical Co., Naugatuck, Conn., a division of Uniroyal.

Tradenamed Rovel, the resin formulation can be molded, extruded, or vacuum-formed alone or coextruded as a protective outer skin over such nonweatherable plastics as ABS.

Uniroyal spokesmen describe the product as a styrene-acrylonitrile resin compounded with an olefinic rubber. Rovel 501 for profile extrusion and Rovel 701 for injection molding will sell for $1.15 per lb. With their specific gravities of 1.02, the cost will be 4.3 cents per cu in, compared to 6.2 cents per cu in for extrusion and 5.8 cents per cu in for injection-molding grades of polycarbonate. Rovel 401 for sheet and coextrusion is priced at $1.05 per lb.

Uniroyal will sell Rovels in black, white, and natural opaque. Color concentrates are available from Americhem, Cuyahoga Falls, Ohio.

Tensile strengths of Rovel formulations are 5600 to 6000 psi, whereas that of polycarbonate is 8700 psi and

Rovel Is used as protective outer skin for ABS In Brahma minl-plckup toppers

of high-impact ABS 6000 psi. Flex-ural strengths of the new plastic are 7700 to 8900 psi, whereas polycarbonate has 13,500 psi and ABS 9000 psi. Heat-deflection temperatures of Rovels are intermediate between those of polycarbonate and ABS. Uniroyal claims stress-cracking resistance of Rovels is equal to or superior to that of polycarbonate.

The saturated character of the olefin rubber compound enables molders to process Rovel at temperatures as high as 525° F without thermal degradation. Reground Rovel can be used at 20% levels in virgin resin, and regrind from Rovel-topped ABS can be used in fabricating ABS substrate for coextrusion with Rovel.

Applications tested include camping units for pickup trucks, vacuum-formed from ABS sheet coextruded with Rovel. Solid-molded Rovel has been used to form casings for solar electricity and solar-heating cells from two other firms. Other potential uses include motorcycle accessories, outdoor signs, marine hardware, motorboat engine shrouds, and farm animal shelters and feeding troughs. For the future, Fisher Body division of General Motors has assigned Rovel a specification number, which means the resin may be used for parts in 1981 GM car models. D

Stagnation of academic research forecast The health and vitality of scientific research at U.S. universities is being sapped by the "graying" of their faculties and the shortage of openings for new researchers, concludes a National Research Council study committee.

The NRC committee's principal solution: Support outstanding new

Feb. 11, 1980C&EN 7