gek terna – company update - axia ventures · gek terna – company update axia research page 2...

TRANSCRIPT

Gek Terna – Company Update

AXIA Research Page 1

GEK TERNA S.A. Construction / Greece

Reuters/Bloomberg: HMrr.AT / GEKTERNA GA

May 12 , 2017

Rebuilding Greece

Rating Buy vs. previous rating Buy

Gek Terna’s performance in 2016 confirmed the excellent momentum in the group’s construction and

renewable activities but importantly signaled the end of a prolonged period of bottom line losses. The

future looks even more promising. Following a 26% GDP contraction between 2008-16 Greece is now

expected to finally enter into a strong growth cycle supported by infrastructure investments mostly financed

by the EU. With the construction activity in Greece having hit its trough in 2010-16, the next period could be

the start of a multi-year recovery for Greece’s construction in our view. Gek Terna having a healthy balance

sheet and a leading position in the market offers one of the most interesting investment stories among

Greek equities. The launch of a series of long awaited infrastructure investments and strong cash flow

streams form the RES subsidiary will be a key catalyst for the name.

We raise our Target Price to EUR 4.70/sh (vs. EUR 3.40/sh previously), pointing to a 40.3% upside. Note that on

our valuation we assume only a fraction of the projects that the company could book in the coming years (the

Kasteli concession that Gek Terna is the sole bidder, would add about EUR 1.5 per share) and no further RES

expansion after 2018. Our estimates call for a FCF yield of 19-26% for 2018-19 vs. a sector average of 7.0-

8.0%. At current levels the stock trades at 4.4x-4.1x EV/EBITDA for 2017-18 and 7.7x-7.4x P/E, representing a

c50% discount to peers across both metrics.

Rebuilding Greece

Greece has remained underinvested for a long period of timing, effectively undermining its growth potentials.

We calculate the investment gap of about EUR 90bn created since the burst of the crisis. In the effort to

spearhead economic growth, construction activities that carry a multiplier of 1.8x will be a key catalyst. With

EU funds of about EUR 20bn in 2014-20 targeting mainly infrastructure investments in Greece and increasing

construction appetite on the private side, we believe we could be in the dawn of a multi-year recovery in

Greek construction.

Leading the market with solid financials

Gek Terna has grown significantly over the years, navigating through the crisis and booking record high

revenues and EBITDA in 2016. The company has a current backlog of EUR 2.5bn and another EUR 800m of

projects to be signed. At the same time its RES subsidiary (Terna Energy-TP EUR 4.50/sh) is about to hit the

1.0GW mark of wind installed capacity with its EBITDA increasing 12.7% CAGR in 2016-19. Additionally the

company’s EUR 175m investment in concession is going to start paying cash dividends as of early 2H17, which

we estimate at about EUR 15-20m per year. The group sits at net cash position (excluding the project related

net debt of EUR 485m of the RES division) while following the completion of RES investment cycle in 2017 FCF

generation is estimated at about EUR 60-80m per year.

Updated estimates

Following the revision of our estimates for the key divisions of construction and wind parks, we adjust our

group forecasts accordingly. We raise our 2017-18 group EBITDA estimates by 15%-20%, driving our EPS

figures sharply higher (+87% in 2017, +47.9% in 2018). All in all we see 2017 EBITDA at EUR 213.8m and net

income at EUR 43.2m, while for 2018 we forecast an EBITDA and net of EUR 228.1m and EUR 45.1m. Strong

FCF generations should be more than adequate to put leverage a declining trend, while we expect dividend

distribution to start in 2018.

EUR m 2015 2016 2017E 2018F 2019F

Revenues 971.8 1,163.5 1,119.4 1,148.1 1,057.8

EBITDA 145.2 246.1 213.8 228.1 217.1

Net Income (14.5) 34.6 43.2 45.1 38.3

EPS (0.14) 0.34 0.42 0.44 0.37

Net Debt/(Cash) 416.6 403.1 610.4 596.3 517.4

Net Debt/EDITDA (x) 2.9 x 1.6 x 2.9 x 2.6 x 2.4 x

P/E (x) n.m. 6.6 x 7.7 x 7.4 x 8.7 x

EV/EBITDA (x) 3.9 x 2.6 x 4.4 x 4.1 x 3.9 x

P/BV 0.3 x 0.4 x 0.5 x 0.5 x 0.4 x Source: AXIA Research, The Company

Target Price (EUR) 4.70

Previous TP 3.40

Current Share Price* (EUR) 3.35

*11 /05/ 2017

Stock Data

Market Cap (EUR m) 331.7

Free Float 75%

EV (EUR m) 944

Num. of Shares (m) 99m (ex-treasury)

Performance 1m 3m 12m

Absolute (%) 27.9 45.7 86.1

ASE General (Abs) 10.7 23.4 24.5

Day avg. no traded shr (k-12m) 92 Price high-12 m (EUR) 3.39

Price low-12m (EUR) 1.62

GEK TERNA is the parent company of the group that is active in construction, renewable energy, thermal energy, real estate and concessions. The Renewable energy activity falls under Terna Energy (39%). The thermal energy division includes 50% and 25% ownership in the plants HERON I and HERON II. The group holds one of the leading positions in their area of activities in Greece and also has established a strong position in key markets in South East Europe in Energy, real estate and construction

Shareholders: York Global Finance 17.35%, Peristeris Giorgos 14.1%, Kampas Nikolaos 10% Argyrios Gkonis - Analyst [email protected] +30 210 7424462 Constantinos Zouzoulas – Head of Research [email protected] +30 210 7424460

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Daily Volume Traded

GEK TERNA HOLDING, REAL ESTATE, CONSTRUCTION S.A.

ATHEX Composite Index (Rebased)

Gek Terna – Company Update

AXIA Research Page 2

Investment thesis Get Terna’s performance in 2016 confirmed the excellent momentum in the group’s construction

and renewable activities but importantly signaled the end of a prolonged period of bottom line

losses. With the construction activity in Greece having hit its trough in 2015-16, the next period

could be the start of a multi-year recovery in Greece’s construction in our view. With a healthy

balance sheet and a leading position in the market, Gek Terna offers one of the most interesting

investment stories among Greek equities. Improving macro momentum and a series of long

awaited investments are the key catalysts for the name.

We raise our Target Price to EUR 4.70/sh (vs. EUR 3.40/sh previously), pointing to a 40.3% upside.

Our estimates call for a FCF yield of 19-26% for 2018-19 vs. a sector average of 7.0-8.0%.

Greece has remained underinvested for a long period of time affected by the deep recession. Gross

fixed capital formation for the whole economy during the period 2010-16 averaged about EUR 25bn

per year, 44% below the EUR 46bn per year average of the 2000-10 period. As construction projects

carry an economic multiplier of about 1.8x on the economic activity, the rebuilding of the country

will start from construction. The country with the support of EU Cohesion funds and private sector

participation is expected to significantly boost infrastructure investments. According to EU

Commission estimates in 2017-18 fixed capital investments are expected to increase by 17% per

year during this period, driven by a 25% spending increase from the private economy. At the same

time the regional character and the particularities of the Greek market continue to be a hurdle for

the active involvement of international construction companies thus allowing more space for the

few large local players.

The deep recession that brought the country’s GDP down by about 26% since 2008, has taken a

significant toll on Greek contractors. With a number of contractors effectively out of business or

facing significant financial problems, the number of active domestic players has significantly

narrowed. During the period Gek Terna with a focused strategy has managed to take advantage of

the market conditions and drive its construction revenues up 7.0% CAGR during 2008-16 to reach

the historical high of EUR 954m in 2016, while it’s EBITDA touched EUR 150m last year vs. EUR 36m

in 2008 (+19.3% CAGR). With a current signed backlog of EUR 2.5bn and another EUR 800m of

projects pending to be signed, Gek Terna’s construction activity is expected to be the group’s

profitability driver.

Gek’s wind park subsidiary (40%), Terna Energy, the largest RES producer in the country (TENERGY

GA, TP EUR 4.50/sh), is on course to hit the mark of about 1.0GW of wind installed capacity before

the end of 2018. Currently there are 48MW in Greece in advanced construction while another

155MW in the US and 44MW in Greece are under construction. Upon the completion of these parks

(we estimate 2H2018) Terna Energy shall hold a wind installed capacity of 984MW (57% in Greece,

27% in the US and 13.6% in Eastern Europe) and a total installed capacity of 1.01GW. Upon having

met the 1.0GW mark Terna Energy would have the financial capacity to selectively expand taking

advantage of its strong operational cash flows, focusing mainly in the US market. At the same time

sector M&A activity adds scarcity value to the name that is not currently priced in our view. Find

more details on Terna Energy on our dedicated note Approaching Elysium.

Gek Terna has invested about EUR 175m of equity in three highways concession roads in Greece,

with the final payments made in 2016. Gek Terna holds a 56% stake in Ionia Odos and 50% in Central

Greece highway (E-65) and a minority 17% in Olympia Odos. Upon the long awaited completion of

the projects in early 2H17, the concession with be eligible to distribute cash dividends to

shareholders. With a tenor of up to 2038, Gek is estimated to cumulatively collect about EUR 450m

during the lifetime of the concession that translates to about EUR 20m per year in cash streams

starting in late 2017 based on our estimations. Additionally, the company has been the sole bidder

for the 40 year construction and operating concession of a new airport in Kasteli Crete. Gek is

expected to invest EUR 120m upon awarding of the concession, holding a 60% stake in the project

that we estimate can yield a high digit IRR. Note that concession income is consolidated under the

equity method (income from associates).

Rebuilding Greece

Leading position in the sector

Wind park business at 1.0GW mark

Concessions sweetening the deal.

Gek Terna – Company Update

AXIA Research Page 3

Valuation

Following the revision of our assumptions on the key divisions of construction and renewable, we

revise our SOTP valuation for the Group. We raise our target price to EUR 4.70 per share (from

EUR 3.40/sh previously) looking to a 40.3% upside from current levels.

Based on our estimates the stock currently trades at a 50% discount to our selected contractors

peer universe on P/E and EV/EBITDA terms, while we estimate a strong FCF yield of 18%-26% in

2018-19 vs. a sector average of about 7.5%.

Key themes of our valuation exercise include:

Construction: In terms of projects we include the current signed backlog (EUR 2.5bn) and

additional about EUR 300m of wins per annum during 2018-22 (vs. an average win of EUR

750m during the recessionary 2008-16). Profitability is also cautiously reverted to

historical average levels. Our WACC is now set at 12% (vs. 15% previously) following the

significant spreads decline, while we assume an exit EBITDA multiple of 4.5x. We do not

account for Kasteli project that would add another EUR 0.4-05/sh to our division’s

valuation.

Renewables (Terna Energy): Our DCF valuation takes into account the additions in 2017-

18, with the respective capex deployment and a terminal wind capacity of 984MW, while

we make explicit forecasts up to 2026 (10 year) using an exit EV/EBITDA multiple of 5.5x.

Our WACC is now adjusted lower vs. previously to 9.5% (vs. 11% before) accounting for a

lower risk free rate following the GGB’s performance.

We value concessions at their book value, not including Kasteli project that would add

another EUR 1.0 per share

We account for a 15% holding discount due to group’s structure.

Table 1. Gek Terna SOTP valuation

Division

Method Equity Value

(EUR m) Gek Terna stake

Stake's Equity Value (EUR m)

Value per

Share (€/sh)

Construction DCF 301.1 100% 301.1 3.0

RES DCF 470.5 40.0% 188.2 1.9

Real Estate BV 43.3 100% 43.3 0.4

Industry-Mines BV 27.0 100% 27.0 0.3

Concessions

Ionia BV

57% 109.0 1.1

Olympia BV

17% 34.0 0.3

Central BV

50% 32.0 0.3

Thermal Energy DDM

50% Heron I / 25% Heron II 20.0 0.2

Total 754.6 7.6

(-) Other Net Debt (end-2016)

204.5 -2.1

o/w Concessions

148.5 -1.5

o/w Holding-Mines

56.0 -0.6

NAV 550.1 5.5

Holding Co. Discount

15%

Estimated NAV 467.6

Num of Shares(1)

99.0

Target Price

4.70

Current price 3.35

Upside (%)

40.3%

(1) Excluding treasury shares Source: AXIA Research

Gek Terna – Company Update

AXIA Research Page 4

Table 2. AXIA Research international contractors peers valuation sheet

Company

P/E

EV/EBITDA

P/BV

Div. Yield Net Debt/EBITDA FCF yield

FY2017 FY2018 FY2019 FY2017 FY2018 FY2019 FY2017 FY2018 FY2019 FY2017 FY2018 FY2019 FY2017 FY2018 FY2019 FY2017 FY2018 FY2019

Balfour Beatty plc 22.0 14.0 11.8 12.6 9.0 7.8 2.3 2.1 1.8 1.4% 2.2% 3.1% -0.3 -0.5 -0.9 0.9% 7.4%

Costain Group plc 14.0 13.1 12.6 6.7 6.3 5.9 4.4 3.9 3.5 3.1% 3.4% 3.7% -2.0 -2.0 -1.9 -4.5% 5.5% 5.1%

Sacyr, S.A. 7.0 5.7 4.5 15.1 13.6 13.1 0.6 0.6 1.2% 1.5% 2.5% 8.0 8.0 7.3 5.4% 6.2%

Skanska AB (publ) 16.0 16.7 16.2 9.4 9.5 8.7 3.1 2.9 2.8 3.9% 3.7% 4.3% -0.8 -0.8 -0.7 6.3% 6.8% 3.8%

Eiffage SA 15.9 13.8 12.3 8.0 7.7 7.4 1.8 1.7 1.5 2.2% 2.5% 3.1% 4.4 4.1 3.7 8.9% 11.0% 13.1%

Compagnie de Saint-Gobain S.A. 17.2 15.1 13.6 7.8 7.3 6.8 1.4 1.3 1.3 2.6% 2.7% 3.2% 1.2 0.9 0.7 4.8% 5.3% 5.8%

HOCHTIEF Aktiengesellschaft 25.5 23.4 21.6 9.6 9.0 8.5 5.6 4.8 4.4 1.9% 2.1% 2.4% -1.0 -1.0 -1.1 8.4% 4.6% 5.2%

VINCI SA 16.7 15.5 14.6 9.1 8.8 8.3 2.5 2.3 2.1 3.0% 3.2% 3.4% 2.0 1.6 1.3 7.5% 7.8% 8.8%

Ferrovial, S.A. 32.7 32.2 27.1 20.2 20.2 18.9 2.6 2.5 2.4 3.9% 4.0% 4.1% 4.5 4.6 4.6 2.6% 3.2% 4.7%

ACS 14.1 13.5 12.8 6.5 6.2 6.0 2.7 2.4 2.2 3.5% 3.7% 4.1% 0.4 0.4 8.1% 8.9% 9.9%

Fomento de Construcciones 22.1 19.0 16.7 8.4 8.1 7.9 3.0 2.6 0.0% 0.3% 1.1% 4.2 4.1 3.3 9.3% 5.6% 3.2%

Strabag SE 13.9 13.4 12.6 3.7 3.6 3.7 1.1 1.1 2.9% 3.2% 3.3% -0.8 -1.0 4.7% 7.1% 8.0%

Mota-Engil, SGPS, S.A. 13.4 8.6 8.3 5.6 5.1 5.0 1.3 1.1 3.1% 5.4% 5.1% 3.0 2.6 2.5 16.9% 12.8% 16.4%

Astaldi S.p.A. 5.8 5.3 4.7 5.8 5.9 5.3 0.7 0.7 0.6 3.7% 4.0% 4.1% 2.7 2.8 2.3 22.5% 4.7% 12.0%

Average 16.9 15.0 13.5 9.2 8.6 8.1 2.4 2.1 2.3 2.6% 3.0% 3.4% 1.8 1.7 1.7 7.3% 6.9% 8.0%

Gek Terna S.A. 7.7 7.4 8.7 4.4 4.1 3.9 0.5 0.5 0.4 0.0% 2.4% 2.3% 2.9 2.6 2.4 -48.4% 18.8% 26.2% Source: Capital IQ, AXIA Research

Table 3. AXIA Research global wind sector peers

Mcap

P/E

EV/EBITDA

P/BV

Net Debt/EBITDA

Div. Yield

Company Country (EUR) FY2017 FY2018 FY2019 FY2017 FY2018 FY2019 FY2017 FY2018 FY2019 FY2017 FY2018 FY2019 FY2017 FY2018 FY2019

El.Tech.Anemos* Greece 100.9 10.8 6.7 6.7 7.4 6.0 6.0 0.7 0.6 0.6 4.5 3.2 2.6

Albioma France 536.7 17.0 12.2 12.2 8.6 7.3 7.0 1.4 1.3 1.1 4.8 4.1 4.0 3.3% 4.1% 4.5%

Voltalia SA France 459.3 42.2 20.0 11.3 11.2 7.2 5.0 1.2 1.2 1.1 6.2 6.3 5.1 0.4% 0.9% 2.4%

Falck Renewables S.p.A. Italy 336.9 33.9 29.2 16.0 6.9 6.6 5.9 0.8 0.8 0.8 4.6 4.1 3.8 4.6% 5.0% 5.3%

Saeta Yield, S.A. Spain 745.0 18.3 17.8 17.3 8.8 9.3 9.3 1.4 1.6 1.6 5.1 5.0 4.6 8.5% 9.0% 9.0%

EDP Renováveis, S.A.* Spain 6,125.3 32.1 28.6 23.9 8.4 7.9 7.4 1.1 1.0 0.9 3.0 2.9 2.9 0.9% 1.0% 1.2%

Energiekontor AG Germany 277.3 18.8 18.8 15.2 6.1 5.7 4.9 3.7 3.5 3.2 2.2 2.8 3.9 4.1% 4.2%

CHORUS Clean Energy AG Germany 360.7 15.5 15.1

9.4 9.3

1.3 1.1

4.7 3.8

3.2% 3.3%

Atlantica Yield plc United Kingdom 1,859.3 16.9 22.5 12.1 9.7 9.2 8.7 1.2 1.1 1.0 7.0 6.6 6.7 6.8% 9.4% 10.5%

Arise AB (publ) Sweden 54.2

10.4 9.0 8.4 6.2 5.6 0.5 0.5 0.5 7.3 4.9 3.8

24.6%

NextEra Energy Partners, LP United States 1,679.2 21.9 19.7 13.2 7.3 6.0 5.0 2.4 2.5 2.3 5.3 4.8 4.3 4.9% 5.6% 6.5%

Pattern Energy Group Inc. United States 1,747.3

39.6 29.2 11.7 10.0 8.6 2.1 1.2 1.9 5.4 4.7 4.5 8.5% 9.1% 9.8%

TransAlta Renewables Inc. Canada 2,302.4 17.5 14.5 13.1 10.3 9.6 10.0 1.7 1.6 1.8 2.3 2.1 2.5 8.8% 9.2% 9.5%

Average

22.3 19.6 14.9 8.8 7.7 7.0 1.5 1.4 1.4 4.8 4.3 4.1 4.9% 7.1% 6.5%

Terna Energy S.A. Greece 344.5 12.8 10.0 8.7 7.8 6.6 5.9 0.9 0.8 0.8 5.2 4.4 3.8 4.1% 5.0% 6.9%

*AXIA Research estimates Source: Capital IQ, AXIA Research

Gek Terna – Company Update

AXIA Research Page 5

Estimates Update

Following the revision of our estimates for the key divisions of construction and wind parks, we

adjust our group forecasts accordingly. We raise our 2017-18 group EBITDA estimates by 15%-20%

vs. previous, driving our EPS figures sharply higher (+87% in 2017, +47.9% in 2018).

Key themes driving our revisions include:

Significantly enhanced construction outlook both in terms of projects as well as

profitability. Current signed backlog at EUR 2.5bn, with additional EUR 800m of projects in

the near term pipeline.

Adjustment of RES division estimates to the updated installation pattern, now including

the 155MW wind park in the US and accounting for a terminal wind capacity of 980MW

(total 1.01GW).

Concession dividend streams of about EUR 15-20m per annum following the completion

of the highways projects by early 2H17.

Higher leverage to support RES expansion.

Table 4. Gek Terna estimates revision

EUR m 2016 2017E 2018F

New Old New-vs-old New Old New-vs-old

Group Revenues 1,163.5 1,119.4 862 29.9% 1,148.1 845.5 35.8%

Construction 954.9 900.0 670 34.3% 900.0 650.0 38.5%

RES 151.0 173.6 167.9 3.4% 200.7 168.5 19.1%

Group EBITDA 252.8 213.8 185.4 15.3% 228.1 190.1 20.0%

Construction 149.8 86.0 49.6 73.4% 77.0 53.0 45.3%

RES 109.0 132.8 131 1.4% 156.1 131.5 18.7%

Net 34.6 43.2 23.1 87.1% 45.1 29.6 52.3% Source: AXIA Research, The Company

Overall we are now looking for group revenues of EUR 1,119m in 2017 (-3.8% y-o-y) mainly on a

5.7% y-o-y decline in construction revenues from the historical highs of 2016. On the EBITDA line,

we expect group EBITDA in 2017 to settle at EUR 213.8m (-15.4% y-o-y), following the normalization

on construction profitability vs. the exceptionally strong 2016 that included the accelerated

execution of the Greek highways projects. Note that RES EBITDA contribution to the total rises by

21.8% on increased effective capacity. On the bottom line we call for a 24.8% y-o-y rise in profits to

EUR 43.2m driven by profitability improvements. Note that 2016 EBT included a provision of cEUR

20m for the settlement with the Competition Authority petition (expected to be settled in cash in

2017).

Looking in 2018, we model for a 2.6% y-o-y hike in revenues to EUR 1,148m based on increased RES

output amid stable construction activity contribution. Group EBITDA is seen advancing by 6.7% y-o-y

to EUR 228.1m courtesy of the 17.5% y-o-y increase in RES EBITDA. Below that we expect a

contribution of EUR 15m from highways concessions, to push bottom line at EUR 43.8m (+4.3% y-o-

y), despite the higher depreciation charges due to increased RES assets.

In respect of depreciation note that currently the RES subsidiary, Terna Energy uses a 20y average lifetime assumption for its wind parks. Extensive industry studies have allowed major wind park developers over the last couple of years to extend the average estimated lifetime of their wind parks by 5 years. If Terna Energy was to proceed with a similar 5 year extension, we estimate that depreciation charge would decline by about EUR 10m per annum, moving our bottom line assumptions for the group higher by about 5-6%.

Gek Terna – Company Update

AXIA Research Page 6

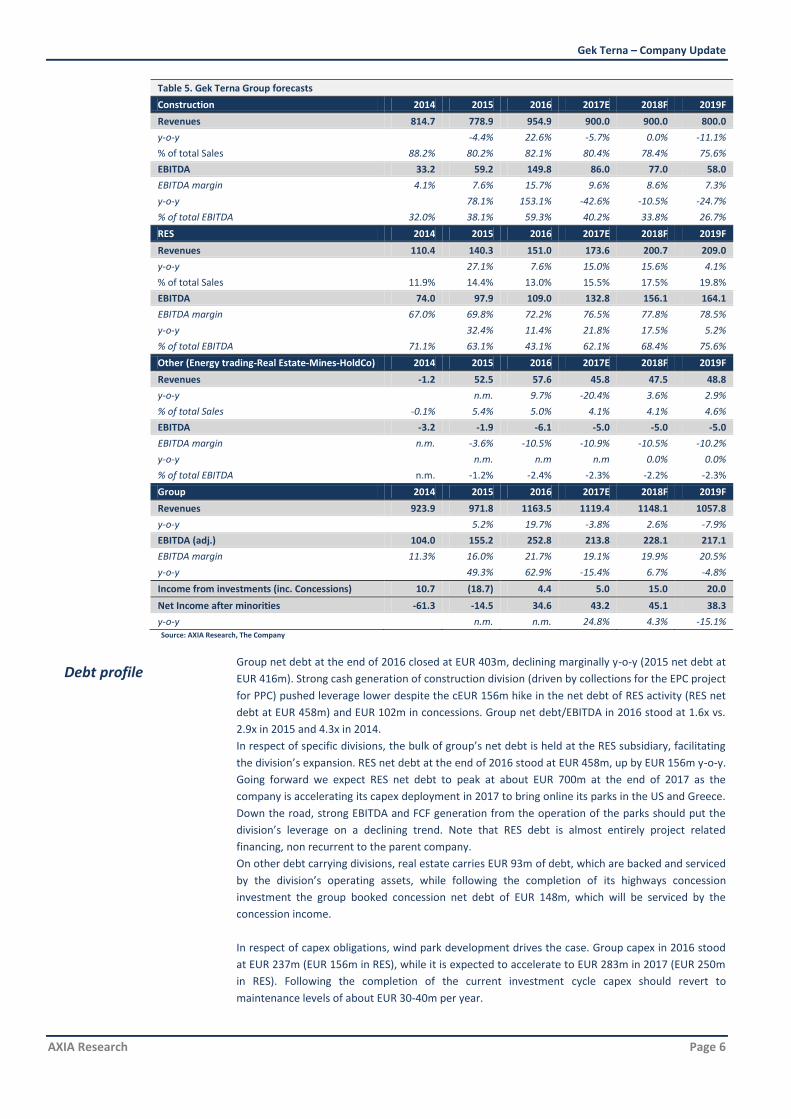

Table 5. Gek Terna Group forecasts

Construction 2014 2015 2016 2017E 2018F 2019F

Revenues 814.7 778.9 954.9 900.0 900.0 800.0

y-o-y -4.4% 22.6% -5.7% 0.0% -11.1%

% of total Sales 88.2% 80.2% 82.1% 80.4% 78.4% 75.6%

EBITDA 33.2 59.2 149.8 86.0 77.0 58.0

EBITDA margin 4.1% 7.6% 15.7% 9.6% 8.6% 7.3%

y-o-y 78.1% 153.1% -42.6% -10.5% -24.7%

% of total EBITDA 32.0% 38.1% 59.3% 40.2% 33.8% 26.7%

RES 2014 2015 2016 2017E 2018F 2019F

Revenues 110.4 140.3 151.0 173.6 200.7 209.0

y-o-y 27.1% 7.6% 15.0% 15.6% 4.1%

% of total Sales 11.9% 14.4% 13.0% 15.5% 17.5% 19.8%

EBITDA 74.0 97.9 109.0 132.8 156.1 164.1

EBITDA margin 67.0% 69.8% 72.2% 76.5% 77.8% 78.5%

y-o-y 32.4% 11.4% 21.8% 17.5% 5.2%

% of total EBITDA 71.1% 63.1% 43.1% 62.1% 68.4% 75.6%

Other (Energy trading-Real Estate-Mines-HoldCo) 2014 2015 2016 2017E 2018F 2019F

Revenues -1.2 52.5 57.6 45.8 47.5 48.8

y-o-y n.m. 9.7% -20.4% 3.6% 2.9%

% of total Sales -0.1% 5.4% 5.0% 4.1% 4.1% 4.6%

EBITDA -3.2 -1.9 -6.1 -5.0 -5.0 -5.0

EBITDA margin n.m. -3.6% -10.5% -10.9% -10.5% -10.2%

y-o-y n.m. n.m n.m 0.0% 0.0%

% of total EBITDA n.m. -1.2% -2.4% -2.3% -2.2% -2.3%

Group 2014 2015 2016 2017E 2018F 2019F

Revenues 923.9 971.8 1163.5 1119.4 1148.1 1057.8

y-o-y 5.2% 19.7% -3.8% 2.6% -7.9%

EBITDA (adj.) 104.0 155.2 252.8 213.8 228.1 217.1

EBITDA margin 11.3% 16.0% 21.7% 19.1% 19.9% 20.5%

y-o-y 49.3% 62.9% -15.4% 6.7% -4.8%

Income from investments (inc. Concessions) 10.7 (18.7) 4.4 5.0 15.0 20.0

Net Income after minorities -61.3 -14.5 34.6 43.2 45.1 38.3

y-o-y n.m. n.m. 24.8% 4.3% -15.1% Source: AXIA Research, The Company

Group net debt at the end of 2016 closed at EUR 403m, declining marginally y-o-y (2015 net debt at

EUR 416m). Strong cash generation of construction division (driven by collections for the EPC project

for PPC) pushed leverage lower despite the cEUR 156m hike in the net debt of RES activity (RES net

debt at EUR 458m) and EUR 102m in concessions. Group net debt/EBITDA in 2016 stood at 1.6x vs.

2.9x in 2015 and 4.3x in 2014.

In respect of specific divisions, the bulk of group’s net debt is held at the RES subsidiary, facilitating

the division’s expansion. RES net debt at the end of 2016 stood at EUR 458m, up by EUR 156m y-o-y.

Going forward we expect RES net debt to peak at about EUR 700m at the end of 2017 as the

company is accelerating its capex deployment in 2017 to bring online its parks in the US and Greece.

Down the road, strong EBITDA and FCF generation from the operation of the parks should put the

division’s leverage on a declining trend. Note that RES debt is almost entirely project related

financing, non recurrent to the parent company.

On other debt carrying divisions, real estate carries EUR 93m of debt, which are backed and serviced

by the division’s operating assets, while following the completion of its highways concession

investment the group booked concession net debt of EUR 148m, which will be serviced by the

concession income.

In respect of capex obligations, wind park development drives the case. Group capex in 2016 stood

at EUR 237m (EUR 156m in RES), while it is expected to accelerate to EUR 283m in 2017 (EUR 250m

in RES). Following the completion of the current investment cycle capex should revert to

maintenance levels of about EUR 30-40m per year.

Debt profile

Gek Terna – Company Update

AXIA Research Page 7

Given the contained debt servicing needs and strong FCF generation after 2017 (we expect FCF of

about EUR 60-80m in 2018-19); we would expect the group to start distributing dividend from 2018

onwards. We model for a total dividend of about EUR 8.0m p.a. starting in 2018.

Table 6. Gek Terna Group net debt breakdown

EUR m 2014 2015 2016 2017E 2018F 2019F

Construction -30.8 -108.3 -380.3 -390.9 -403.3 -423.7

RES 254.5 328.7 485.4 697.8 690.1 626.7

Real Estate 80.8 82.8 93.7 93.8 93.8 93.8

Mine/Industrial 21.4 31.8 38.2 40.3 55.3 70.3

Concessions 41.5 46.5 148.5 150.0 150.0 150.0

Thermal Energy -1.1 -1.3 0.0 0.0 0.0 0.0

Holding 13.3 36.4 17.8 20.0 20.0 20.0

Total 379.7 416.6 403.2 611.0 605.8 537.1

Net Debt/EBITDA (x) 4.3 2.9 1.6 2.9 2.7 2.5

EBIT/Interest expense (x) 0.4 1.5 3.1 2.3 2.4 2.2 Source: AXIA Research, The Company

Gek Terna – Company Update

AXIA Research Page 8

Rebuilding Greece

We believe Greece currently finds itself in what could be the beginning of a multi-year recovery

for its construction activity. With the country lagging both Euro area average and its own recent

historical performance, we calculate that there is an investment gap of about EUR 90bn

accumulated over the last 7 years that should be covered in the medium to longer term. EU

subsidy funds, traditionally geared towards the underdeveloped economies of the union, as well

as private sector participation and the improving State fiscal environment should facilitate the

country’s efforts to bridge the investment gap.

The economic recession that hit the country and striped of 26% of its GDP since 2008 has also taken

a significant toll in the country’s infrastructure. Gross fixed capital formation as % of GDP in Greece

during 2010-16 averaged 13.2% which is almost half of the Euro area (20%) and significantly lower

vs. the 2000-10 average of 23.2% in Greece. This has resulted in a major underinvestment in key

parts of the economy, with Greece currently ranking 26th

among EU countries in terms of

infrastructure quality cording to IMF’s Global Competiveness report.

Chart 1a. Fixed Capital Formation % of GDP (Total Economy) Chart 1b. Quality of infrastructure Index

Source: AMECO, IMF Global Competitiveness report

Chart 2a. Production Index in Industry Chart 2b. Cement consumption in Greece

Source: ELSTAT, Hellenic Cement Industry Association

To this end private sector that accounted for about 80% of the capital investments in Greece in the

last decade, has significantly slowed down its investments that averaged 9.8% of GDP in 2010-16 vs.

18% in 2000-10. In absolute terms fixed capital private sector investments averaged EUR 19m per

year in 2010-16 vs. EUR 35.5bn in 2000-10 (-46%), with the private sector now accounting for c65%

of the capital investments vs. 80% in the last decade and 85% OF THE Euro area average.

Official sector (general government level) investments declined from EUR 10.3bn a year in 2000-10

(5.2% of GDP) by 38.1% to stand at EUR 6.4bn (3.4% of GDP), while they increased their significance

to the economy as they account for 35% of the total investments vs. 25% in the previous decade and

13% of the Euro area. State investments have been significantly supported by EU cohesion funds

(Co-financed projects) that accounted in 2016 for 89% of the total public investment program vs.

66% in 2000-10.

-10.0%

0.0%

10.0%

20.0%

30.0%

Greece - GFCF EU - GFCF EU - Net Fixed Capital Formation GR - Net Fixed Capital Formation

6.1 6

5.9 5.7

5.6 5.6

5.5 5.5

5.2 5.2

5.1 5.1

4.7 4.7

4.6 4.5 4.5

4.4 4.4 4.4

4.3 Greece, 4.2 4.2 4.2

3.9 3.4

4.9

Finaland

Denmark Aurtsria

Luxemburg

Spian

Esthonia

Belgium

Ireland

Slovenia

Hungary

Latvia

Italy

Malta

Bulgaria

Average

0

50

100

150

200

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

2008 2009 2010 2011 2012 2013 2014 2015 2016

Private sector investments declined…

…with official sector trying to fill in

Gek Terna – Company Update

AXIA Research Page 9

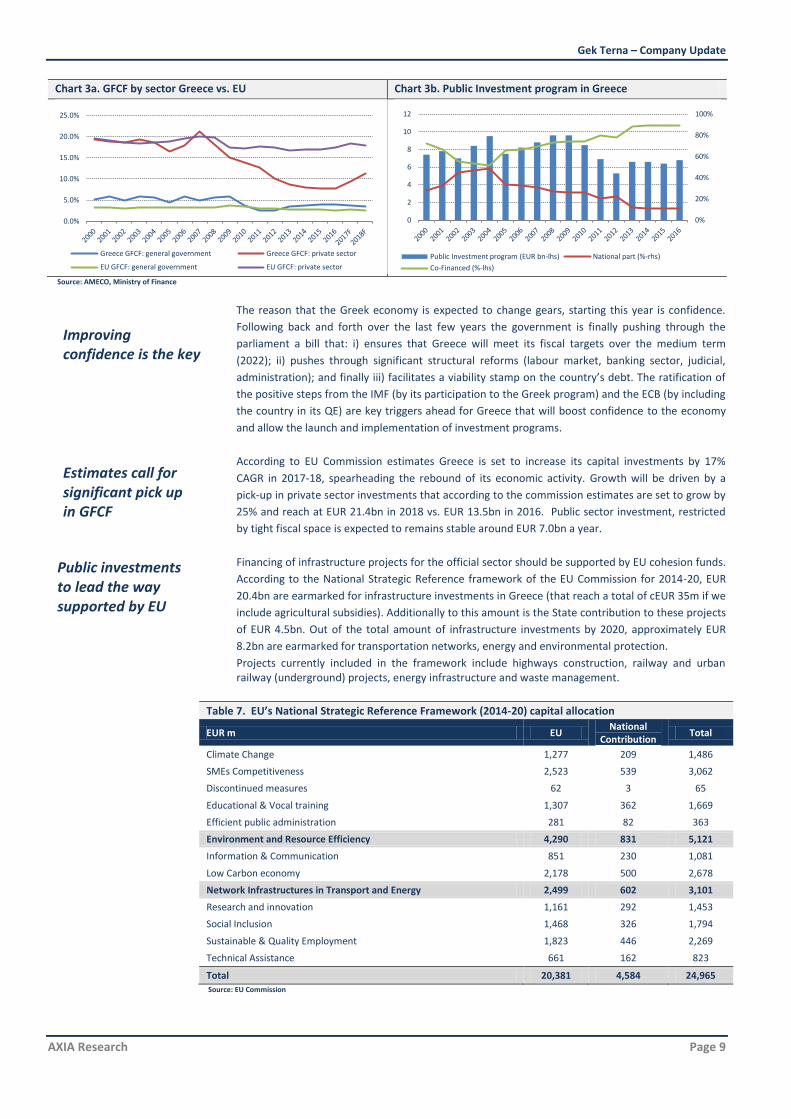

Chart 3a. GFCF by sector Greece vs. EU Chart 3b. Public Investment program in Greece

Source: AMECO, Ministry of Finance

The reason that the Greek economy is expected to change gears, starting this year is confidence.

Following back and forth over the last few years the government is finally pushing through the

parliament a bill that: i) ensures that Greece will meet its fiscal targets over the medium term

(2022); ii) pushes through significant structural reforms (labour market, banking sector, judicial,

administration); and finally iii) facilitates a viability stamp on the country’s debt. The ratification of

the positive steps from the IMF (by its participation to the Greek program) and the ECB (by including

the country in its QE) are key triggers ahead for Greece that will boost confidence to the economy

and allow the launch and implementation of investment programs.

According to EU Commission estimates Greece is set to increase its capital investments by 17%

CAGR in 2017-18, spearheading the rebound of its economic activity. Growth will be driven by a

pick-up in private sector investments that according to the commission estimates are set to grow by

25% and reach at EUR 21.4bn in 2018 vs. EUR 13.5bn in 2016. Public sector investment, restricted

by tight fiscal space is expected to remains stable around EUR 7.0bn a year.

Financing of infrastructure projects for the official sector should be supported by EU cohesion funds.

According to the National Strategic Reference framework of the EU Commission for 2014-20, EUR

20.4bn are earmarked for infrastructure investments in Greece (that reach a total of cEUR 35m if we

include agricultural subsidies). Additionally to this amount is the State contribution to these projects

of EUR 4.5bn. Out of the total amount of infrastructure investments by 2020, approximately EUR

8.2bn are earmarked for transportation networks, energy and environmental protection.

Projects currently included in the framework include highways construction, railway and urban railway (underground) projects, energy infrastructure and waste management.

Table 7. EU’s National Strategic Reference Framework (2014-20) capital allocation

EUR m EU National

Contribution Total

Climate Change 1,277 209 1,486

SMEs Competitiveness 2,523 539 3,062

Discontinued measures 62 3 65

Educational & Vocal training 1,307 362 1,669

Efficient public administration 281 82 363

Environment and Resource Efficiency 4,290 831 5,121

Information & Communication 851 230 1,081

Low Carbon economy 2,178 500 2,678

Network Infrastructures in Transport and Energy 2,499 602 3,101

Research and innovation 1,161 292 1,453

Social Inclusion 1,468 326 1,794

Sustainable & Quality Employment 1,823 446 2,269

Technical Assistance 661 162 823

Total 20,381 4,584 24,965 Source: EU Commission

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Greece GFCF: general government Greece GFCF: private sector

EU GFCF: general government EU GFCF: private sector

0%

20%

40%

60%

80%

100%

0

2

4

6

8

10

12

Public Investment program (EUR bn-lhs) National part (%-rhs)

Co-Financed (%-lhs)

Public investments to lead the way supported by EU

Estimates call for significant pick up in GFCF

Improving confidence is the key

Gek Terna – Company Update

AXIA Research Page 10

On the private side, we would expect significant investments to be realized on the tourism and real

estate sectors that are attracting significant interest as well as on projects related to privatization.

Projects should include both greenfield development following the fast tracking of relevant

framework agreements as well as investments towards improving and upgrading existing facilities.

Hellinikon development, a EUR 8.0bn mega investment project on the location of the former Athens

international airport in Athens seafront course is an illustrative case. We would expect construction

works to start in 2018-19, with a big part of the civil engineering projects completed within the first

five years. The plan foresees the development of residences, mall, hotels as well as an urban

recreation park.

On a similar note there are currently on-going a numerous of greenfield hotel projects around the

country’s hospitality industry as well as long awaited revamps. Greek hoteliers are looking to expand

the momentum of the strong tourism demand by up scaling their supply standards and attracting

higher net-worth travelers while extending the tourism season.

On the real estate sector, we note the interest for the greenfield investments that have been

postponed for a period due to the volatile macro environment. At the same time, with real estate

prices showing stabilization signs after a prolonged period, revamping existing facilities would allow

owners to attract interest.

Finally, a sizable backlog is expected from the country’s ambitious privatization program (apart from

Hellinikon). The concession of regional airports to a Fraport led consortium and the sale of Greece’s

railway company to Italian railways, kick-started an investment cycle that is expected to be followed

by port facilities upgrades, logistics facilities and marinas upgrades.

Private sector to follow

Gek Terna – Company Update

AXIA Research Page 11

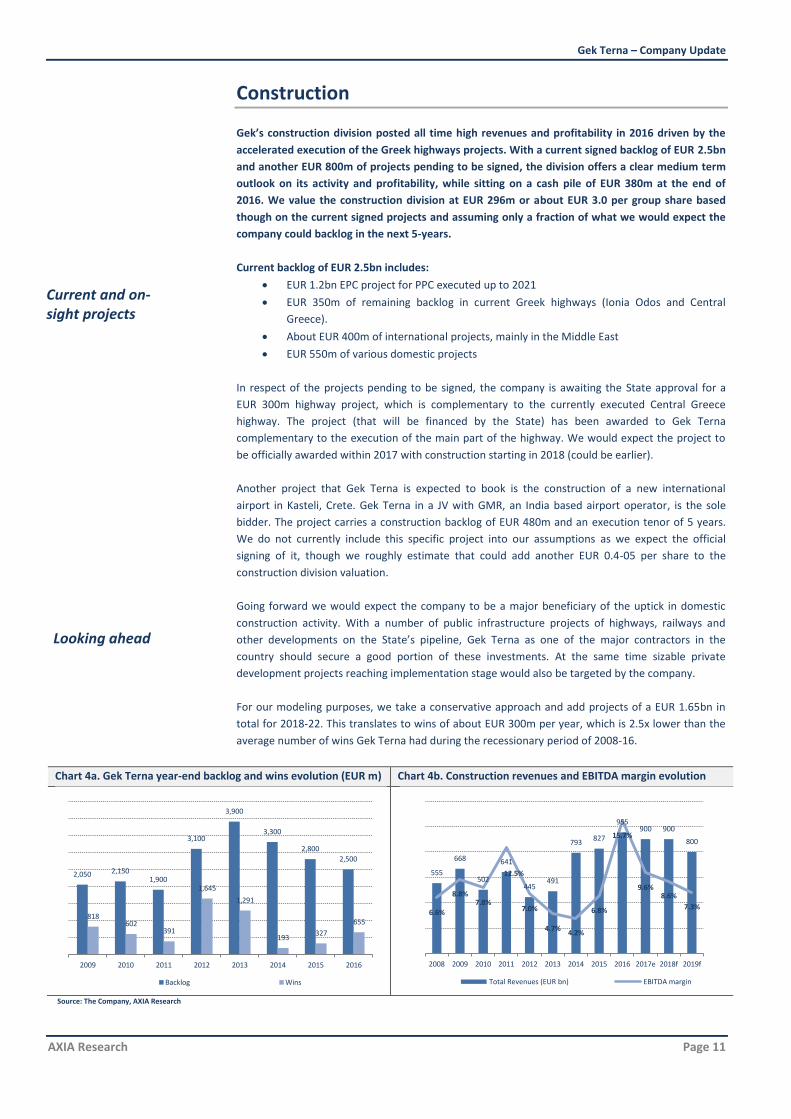

Construction

Gek’s construction division posted all time high revenues and profitability in 2016 driven by the

accelerated execution of the Greek highways projects. With a current signed backlog of EUR 2.5bn

and another EUR 800m of projects pending to be signed, the division offers a clear medium term

outlook on its activity and profitability, while sitting on a cash pile of EUR 380m at the end of

2016. We value the construction division at EUR 296m or about EUR 3.0 per group share based

though on the current signed projects and assuming only a fraction of what we would expect the

company could backlog in the next 5-years.

Current backlog of EUR 2.5bn includes:

EUR 1.2bn EPC project for PPC executed up to 2021

EUR 350m of remaining backlog in current Greek highways (Ionia Odos and Central

Greece).

About EUR 400m of international projects, mainly in the Middle East

EUR 550m of various domestic projects

In respect of the projects pending to be signed, the company is awaiting the State approval for a

EUR 300m highway project, which is complementary to the currently executed Central Greece

highway. The project (that will be financed by the State) has been awarded to Gek Terna

complementary to the execution of the main part of the highway. We would expect the project to

be officially awarded within 2017 with construction starting in 2018 (could be earlier).

Another project that Gek Terna is expected to book is the construction of a new international

airport in Kasteli, Crete. Gek Terna in a JV with GMR, an India based airport operator, is the sole

bidder. The project carries a construction backlog of EUR 480m and an execution tenor of 5 years.

We do not currently include this specific project into our assumptions as we expect the official

signing of it, though we roughly estimate that could add another EUR 0.4-05 per share to the

construction division valuation.

Going forward we would expect the company to be a major beneficiary of the uptick in domestic

construction activity. With a number of public infrastructure projects of highways, railways and

other developments on the State’s pipeline, Gek Terna as one of the major contractors in the

country should secure a good portion of these investments. At the same time sizable private

development projects reaching implementation stage would also be targeted by the company.

For our modeling purposes, we take a conservative approach and add projects of a EUR 1.65bn in

total for 2018-22. This translates to wins of about EUR 300m per year, which is 2.5x lower than the

average number of wins Gek Terna had during the recessionary period of 2008-16.

Chart 4a. Gek Terna year-end backlog and wins evolution (EUR m) Chart 4b. Construction revenues and EBITDA margin evolution

Source: The Company, AXIA Research

2,050 2,150 1,900

3,100

3,900

3,300

2,800

2,500

818 602

391

1,645

1,291

193 327

655

2009 2010 2011 2012 2013 2014 2015 2016

Backlog Wins

555

668

502

641

445 491

793 827

955 900 900

800

6.6%

8.8% 7.8%

12.5%

7.0%

4.7% 4.2%

6.8%

15.7%

9.6% 8.6%

7.3%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

0

200

400

600

800

1000

1200

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017e 2018f 2019f

Total Revenues (EUR bn) EBITDA margin

Current and on-sight projects

Looking ahead

Gek Terna – Company Update

AXIA Research Page 12

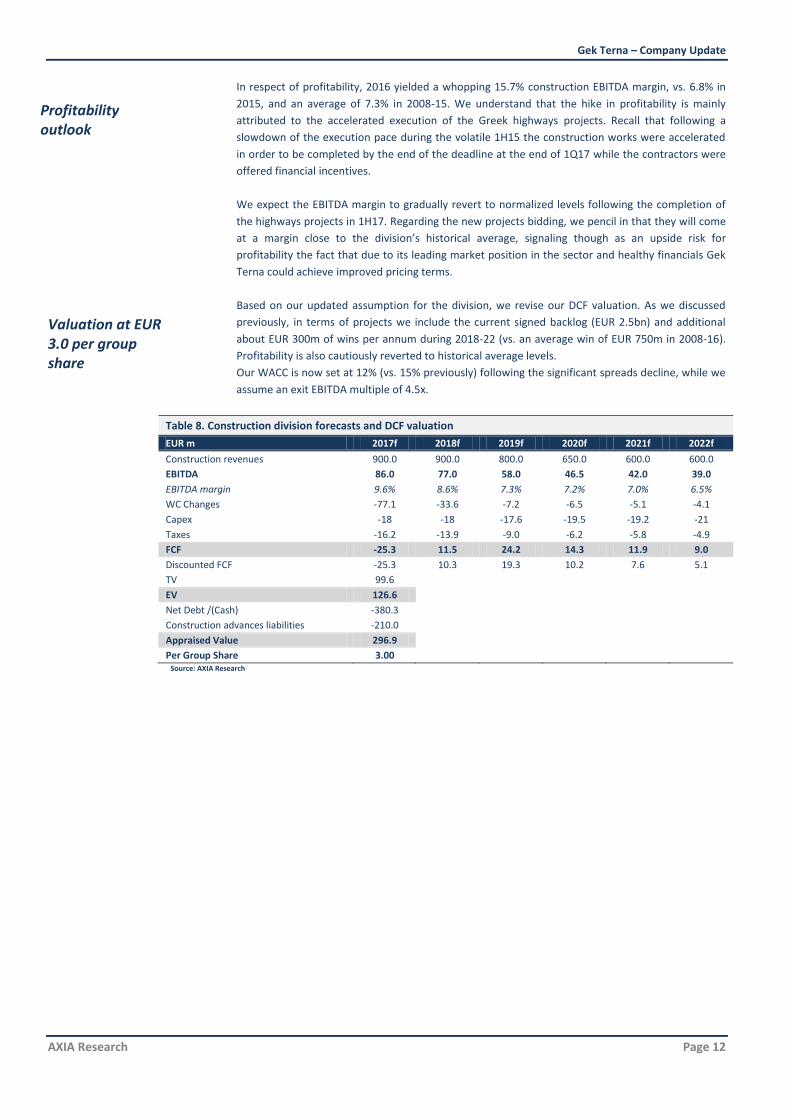

In respect of profitability, 2016 yielded a whopping 15.7% construction EBITDA margin, vs. 6.8% in

2015, and an average of 7.3% in 2008-15. We understand that the hike in profitability is mainly

attributed to the accelerated execution of the Greek highways projects. Recall that following a

slowdown of the execution pace during the volatile 1H15 the construction works were accelerated

in order to be completed by the end of the deadline at the end of 1Q17 while the contractors were

offered financial incentives.

We expect the EBITDA margin to gradually revert to normalized levels following the completion of

the highways projects in 1H17. Regarding the new projects bidding, we pencil in that they will come

at a margin close to the division’s historical average, signaling though as an upside risk for

profitability the fact that due to its leading market position in the sector and healthy financials Gek

Terna could achieve improved pricing terms.

Based on our updated assumption for the division, we revise our DCF valuation. As we discussed

previously, in terms of projects we include the current signed backlog (EUR 2.5bn) and additional

about EUR 300m of wins per annum during 2018-22 (vs. an average win of EUR 750m in 2008-16).

Profitability is also cautiously reverted to historical average levels.

Our WACC is now set at 12% (vs. 15% previously) following the significant spreads decline, while we

assume an exit EBITDA multiple of 4.5x.

Table 8. Construction division forecasts and DCF valuation

EUR m 2017f 2018f 2019f 2020f 2021f 2022f

Construction revenues 900.0 900.0 800.0 650.0 600.0 600.0

EBITDA 86.0 77.0 58.0 46.5 42.0 39.0

EBITDA margin 9.6% 8.6% 7.3% 7.2% 7.0% 6.5%

WC Changes -77.1 -33.6 -7.2 -6.5 -5.1 -4.1

Capex -18 -18 -17.6 -19.5 -19.2 -21

Taxes -16.2 -13.9 -9.0 -6.2 -5.8 -4.9

FCF -25.3 11.5 24.2 14.3 11.9 9.0

Discounted FCF -25.3 10.3 19.3 10.2 7.6 5.1

TV 99.6

EV 126.6

Net Debt /(Cash) -380.3

Construction advances liabilities -210.0

Appraised Value 296.9

Per Group Share 3.00

Source: AXIA Research

Valuation at EUR 3.0 per group share

Profitability outlook

Gek Terna – Company Update

AXIA Research Page 13

Wind parks (Terna Energy)-Approaching Elysium

Gek’s wind park subsidiary (40% owned by the group), Terna Energy, is speeding up its capacity

additions, planning to bring online at least 246MW in 2017-18 (of which 155MW in the US), to

reach a total installed wind capacity of 984MW (total installed 1,010MW including 26.5MW of

operating small hydro and solar). The new additions, accompanied with the full operation of Agios

Georgios hybrid park in Greece (73MW) in 2017, are expected to drive the division’s EBITDA up by

12.7% CAGR in 2016-19 to reach EUR 165m in 2019 from EUR 116m in 2016.

Terna Energy screens attractively vs. peers, trading at EV/MW of 0.83x for end-2017 capacity vs. a

sector average of 1.4x. Based on our profitability assumptions, Terna Energy trades at a 50%

discount to peers on P/E terms and 15% discount on EV/EBITDA.

We update our DCF for Terna Energy now estimating a value of EUR 470m for the total company,

or EUR 1.8 per Gek Terna share.

In respect of installations in Greece, the company is in the last construction stages of 48MW in

Greece’s mainland (Dervenoxoria), while according to management some of this capacity is already

in operation. We model this park to come online in 2H17.

At the same time another park of 44MW has started construction in Northern Greece (Vermio).

According to the management this park should be commissioned in early 2018.

The capex for these parks amounts to approximately EUR 120m and is spilt in 2016-17. In respect of

financing structure, the company’s equity contribution will cover about 30% of the total investment,

with the remaining covered by bank debt on a project basis.

By the end of 2017 Terna Energy is planning to bring online its new 155MW Fluvana I park in the US

in Scurry County, Texas. Note that this is the second park for the company is the US as it operates a

138MW wind park in Elmore County, Idaho as of 2012.

The park upon its operation is expected to generate about EUR 17m of EBITDA per annum, taking

advantage of the very strong wind dynamics in the area (load factor at 45%). The total investment

for the park stands at USD 250m. Part of the designated capex was spent in 2016, with the larger

portion though invested in 2017.

Fluvanna I is owned and will be operated by Terna Energy. Copenhagen Infrastructure Partners (CIP-

PensionDanmark) is investing USD 61m to the project, while subject to satisfaction of certain

conditions precedent Goldman Sachs will make an equity investment in the holding company that

owns the project following the commencement of commercial operations of the project. Financing

during construction will be covered, through loans by a group of banks.

Moreover Terna Energy has acknowledged that CIP has also expressed interest to invest in Fluvanna

II (130MW wind) under a similar financing structure. It is to our understanding that upon the final

decision for the implementation of the project (capex at about USD 250m again), the construction

could be completed in a very short time (6-months). We do not include this project to our model at

this point. We estimate that if the project goes ahead it will generate about EUR 15m of EBITDA per

annum.

Chart 5a. Terna Energy Wind Installed Capacity Evolution (MW) Chart 5b. Financial performance (EUR m)

Source: The Company, AXIA Research

263 394

559 56

102

102

30

30

30 138

293.4

349

664

984.4

2011 2015 2018F

Greece Poland Bulgaria US

46.5

140.3

200.7

32.6

102.8

157.6

70.1%

73.3%

78.5%

64.0%

66.0%

68.0%

70.0%

72.0%

74.0%

76.0%

78.0%

80.0%

0.0

50.0

100.0

150.0

200.0

250.0

2011 2015 2018F

RES Revenues EBITDA EBITDA margin

1.0GW on sight

Focus turning to US

Gek Terna – Company Update

AXIA Research Page 14

Upon having met the 1.0GW mark Terna Energy will have the financial capacity to selectively

expand taking advantage of its strong operational cash flows. Specifically we expect the focus to

remain in US opportunities taking advantage of the organic FCF generation of EUR 90m per annum

that according to our estimates should allow for capacity growth of about 10% per annum in the

medium to longer term.

We would expect the company to keep its radar open for greenfield investment opportunities in the

US market building upon its existing presence and know how. Although the major renewable energy

producers in the US have accumulated a significant part of the capacity, Terna Energy could focus on

regional medium and small sized projects building upon its presence in the country. As the

management has indicated the company would be looking into projects in the US market with an

IRR of about 13%.

In respect of the RES market in Greece, following the completion of the current under construction

wind parks in 2017-18, we would not expect any other additions in the short term. Following the

framework change (we discuss this in the following section of the report), that effectively calls for

tenders for new capacity based on a feed in premium Terna Energy as the largest player in the

market could selectively target attractive projects, having the financial capacity to proceed to their

implementation.

Taking a more quantitative look on the company’s financial capacity to go after new investments in

Greece and abroad, based on our estimates for the company’s organic FCF in the medium term we

believe Terna Energy could be able to invest about EUR 30-40m of equity per annum into new

projects. This amount, leveraged with the customary terms would allow the company to finance

investments of about 80-100MW per annum, while safely meeting its debt service needs and

allowing for a solid return to the shareholders.

Chart 6. FCF* (EUR m)

*FCF excluding expansion capex Source: AXIA Research, The Company

Wind installed capacity in the country at the end of 2016 reached 2.37GW, increased by 219MW y-

o-y, with the bulk of the new installation located in the mainland. Wind parks in 2016 generated

5.1GWh (+6.5% y-o-y), covering 8.7% of the total demand of the country and accounting for 51% of

the total RES production. The higher output was driven mainly by the new capacity that came online

as stable wind dynamics kept load factor practically unchanged y-o-y at 25.5%.

In respect of market participants, Terna Energy remains the largest producer with wind installed

capacity in the country reaching 460MW (20% of total), followed by Iberdrola (250.8MW), El.Tech.

Anemos (238.6MW) and EDF (238.2MW). It is worth noting that the five biggest wind producers

account for just 50% of the total wind installed capacity in the country.

(40.0)

(20.0)

-

20.0

40.0

60.0

80.0

100.0

120.0

2014 2015 2016 2017e 2018f 2019f 2020f

Looking ahead…

Greek wind market overview

Gek Terna – Company Update

AXIA Research Page 15

4,139 3,688

4,620 5,145

26.77% 22.62%

25.79% 25.47%

6.9% 6.5% 7.9% 8.7%

48.1% 44.3%

49.4% 51.6%

5.00%

25.00%

45.00%

65.00%

-

2,000

4,000

6,000

2013 2014 2015 2016

Output (GWh) Load factor % of total demand % of RES Production

Chart 7a. Wind producers installed capacity (MW) Chart 7b. Wind park generation dynamics

Source: LAGIE, Eletaen, AXIA Research

In respect of market economics, the deficit of the dedicated account for renewable producers at the

end of 2016 stood at about EUR 200m, vs. EUR 84.28m at the end of 2015 and EUR 200m at the end

of 2014. This resulted in a cash conversion cycle of about 7-8 months for RES producers (vs. 5-6

months before). Key factors that drove the deficit higher were the increased RES output and the

decline in SMP that were not followed by increases in the fee paid by the consumers (ETMEAR) by

the Ministry of Energy to bridge the gap. That resulted in delays in the payment of RES producers

that are currently being paid by a delay of about 6-7 months vs. 4-5 months approximately in 2014-

15.

During 2016 the government, following MoU guidelines, drafted and legislated a framework to

balance the RES account within 2017 and automatically monitor its performance going forward.

According to the introduced methodology, electricity suppliers will take up a charge to cover the

deficit (RES fee). The relevant charge will be calculated by the regulator (RAE) for each year based

on the projected deficit and will be paid by the suppliers based on their market share. This,

alongside with the contribution of the “ETMEAR” fee paid by the consumers are expected to balance

the RES account by the end of 2017.

Chart 8. RES account deficit bridge estimates

Source: LAGIE, AXIA Research

Based on our updated capacity expansion plan, we adjust our estimates for Terna Energy and the

RES division accordingly, accounting now for a terminal wind capacity of 980MW in 2018 vs.

880MW previously.

We expect a 15% y-o-y hike in RES sales in 2017 that are seen at EUR 173.6m. The hike is attributed

to the operation of Agios Georgios 73MW hybrid park for the entire year as well as the operation of

48 additional MW that are expected to be operational in 2H17. A further hike of 16% y-o-y is

expected in 2018 courtesy of the operation of the 155MW Fluvana I park the US in 1H18 and the

44MW in Greece later in the year. In respect of group revenues we model for a stable stream on

trading related income (an activity with minimal profitability), while we pencil in construction

0

100

200

300

400

500

600

Terna Energy

Iberdrola Anemos EDF ENEL Green Power

Europe Energy

EREN Group

Protergia PPC RES Other

2016 2015

1,865 1,806

470 367.5

920 949.8

374

66

101

200

200

Total RES compensation Total acount inflows Total RES compensation Total acount inflows

2017e 2016

Market pool ETMEAR RES fee Other Deficit

Greek RES account to balance in 2017 removing a significant concern

Updating estimates

Gek Terna – Company Update

AXIA Research Page 16

revenues for third parties of about EUR 25m per annum (on minimal profitability). Note that at the

end of 2016 construction activity backlog stood at EUR 52.6m.

On profitability, group EBIBTDA is driven by the new additions that also yield economies of scale,

thus improving margins. For 2016 we estimate a group EBITDA of EUR 134.1m (+16.1% y-o-y), while

we estimate a similar hike in 2018, with group EBITDA seen at EUR 157.6m.

Capex in 2017 is expected to hike to EUR 250m vs. EUR 145m in 2016 and EUR 86m in 2014. The

capex should account for the bulk of the investment in Fluvana I park plus a big part of the 44MW in

Greece coming online in 2018.

Our DCF valuation takes into account the additions in 2017-18, with the respective capex

deployment, while we make explicit forecasts up to 2026 (10 year) using an exit EV/EBITDA multiple

of 5.5x. Our WACC is now adjusted lower vs. previously to 9.5% (vs. 11% before) accounting for a

lower risk free rate following the GGB’s performance. Note we also account for the return of the

EUR 87m of cash grants the company is due in the next two years.

Table 9. Terna Energy DCF Valuation

EUR m 2017 2018 2018 2020 2021 2022 2023 2024 2025 2026 2026 EBITDA 134.3 157.6 165.5 166.6 166.7 166.8 166.9 167.0 167.1 167.2 167.3

Income tax (14.8) (19.6) (22.8) (23.6) (25.9) (26.9) (27.9) (29.2) (29.5) (30.1) (30.7) Capex (251.0) (20.9) (10.0) (10.0) (10.0) (10.0) (10.0) (10.0) (10.0) (10.0) (10.0) WC changes 32.1 (1.0) (3.6) (0.4) (0.1) (0.1) (0.1) (0.1) (0.1) (0.1) (0.1)

FCF (99.3) 116.0 129.0 132.6 130.7 129.8 128.9 127.7 127.5 127.0 126.5

NPV of FCF (99.3) 106.0 107.6 101.0 90.9 82.5 74.8 67.7 61.7 56.1 51.1 Sum of NPVs 699.9

Terminal Value 361.2

EV 1,061.1

Net Debt (end-2016) 503.5

Grant liabilities 87.1

NAV 470.5

Gek Terna stake 40%

Per Gek Group Share

1.80

Source: AXIA Research

Table 10a. Targeted valuation metrics

Table 10b. WACC

2017 2018 2019 Assumptions

P/E (x) 17.5 13.7 11.9 Risk free 6.50%

EV/EBITDA (x) 7.9 6.7 6.4 Market risk 6.50%

EV/MW (x) 1.10 1.05 1.05 Beta 1.6

organic FCF yield* 14.7% 9.7% 20.6% Cost of debt (pre tax) 6.5%

Div. yield 3.0% 3.7% 5.0% Debt/Capital 60% *exc. expansion capex Source: AXIA Research

In respect of trading multiples, on P/E terms Terna Energy trades at 12.8x-10.0x in 2017-18, standing

at about 50% discount to peers (22.3x-19.6x respectively). On EV/EBITDA terms, the company trades

at 7.8x-6.6x for 2017-18, down by about 15% to the industry that trades at 8.8x-7.7x for the same

period.

Valuing RES division at EUR 1.8 per group share

Gek Terna – Company Update

AXIA Research Page 17

Concession portfolio

Following the completion of the Greek highways, Gek Terna will start receiving cash dividend

streams from its EUR 165m equity investment. Beyond that, the prospect of engaging and

completing the Kasteli airport concession, an EUR 120m investment, would significantly enhance

the company’s concession portfolio securing long term, stable and predictable cash streams to the

group that can total up to EUR 40m per year.

We currently do not include Kasteli concession on our estimates and value highways concession

participation at their book value of EUR 175m (EUR 1.8/sh). Kasteli would add another cEUR 1.0 per

share on concession activity valuation.

Table 11. Gek Terna Concession portfolio

Project Status Stake Equity Invested

(EUR m) IRR

Ionian Road Under Construction c56% 109 7.8%

Central Greece Motorway Under Construction c50% 32 7.5%

Olympia Odos Motorway Under Construction 17.0% 34 11.8%

Kasteli Airport Sole bidder 60.0% 120 high single digit(1)

(1) AXIA Research estimates Source: AXIA Research, The Company

Highways concessions were tendered in 2006-07 for the construction and operation of highways in

the mainland of Greece with a total budget at the time of EUR 8.5bn. At that time consortiums of

both Greek and international companies participated in the tenders securing various projects.

Projects would be financed by equity contribution of the concessionaires (c10% of total), Greek and

foreign banks loans (40-50%) and State participation utilizing EU funds.

Following the burst of the crisis projects were halted in early 2010, as the lower revision of traffic

volume projections raised questions over the viability of the projects under the current framework by

the lending banks and concessionaires. Following extensive negotiations in late 2013 the State came

into an agreement with all interested parties on a new framework that should allow the completion

of the projects. Among other cost revisions and cuts in the overall projects to be executed that

brought total const down to EUR 5.5bn and revised the IRR of the projects from 9-10% to c7.0%, a

key element to the revision was the decision of the State to concede the priority in cash payment to

the banks and the concessionaires. More specifically In the initial signed agreements the State was

first in the cash flow chain, so the operator had to pay the State, then opex etc and finally pay

dividend to the other shareholders and the respective obligations to creditors. With the new

agreement, the creditors have moved to the top of the cash flow chain, leaving the Greek State at

the bottom. This secures the self funding of the projects and assumes lower traffic volume risk than

the previous structure.

Table 11a. Highways budget Table 11b. Funding structure of projects

Highway Budget (EUR m) Length (Km)

Ionia 1,057 379

Aegean 943 229

Olympia 2,092 311

Central Greece 1,370 231

Amount (EUR bn) % of total

Private Equity 0.675 12.5%

Debt 1.595 29.4%

EU & EIB 1.65 30.4%

State 1.5 27.7%

Source: AXIA Research, press

Highways concessions were tendered in 2006-07 for the construction and operation of highways in

the mainland of Greece with a total budget at the time of EUR 8.5bn that was split amongst 4

consortiums with the participation of German, French and Spanish companies along with Greek

contractors.

Gek Terna initially participated in Ionia Odos and Central Greece with a 33% stake along with

Ferrovial and ACS, while it held a 17% stake in Olympia Odos. Following the relaunch of the projects

in 2013 the company increased its stake in Ionia and Central Greece taking upon the stakes of its

Spanish partners, currently holding a c56% stake in Ionia and c50% in Central Greece, while it

Greek highways concessions background

Gek Terna investment in highways…

Gek Terna – Company Update

AXIA Research Page 18

maintained stable its stake in Olympia Odos at 17%. The company has currently invested in total

EUR 165m up till now and upon the full completion in early 2H17 total investment should reach EUR

175m.

Upon the completion of the construction works the concession will be enabled to start paying cash

dividends to its shareholders. Note that the 40 year concession period started officially in about

2009 and has a 40 year tenor. According to the date submitted to the parliament with the

restructuring deal, Ionia Odos carries an IRR of 7.76%, Central Greece of 7.49% and Olympia 11.8%.

Taking into account as well the delayed cash payments for the previous years, we estimate that Gek

Terna will receive about EUR 15-20m per year as cash dividends up to 2039. Concessions are

consolidated under the equity method as per by the bylaws the decisions request increased majority

and the income is reported as (income from associates). Note that part of these dividends will be

used to service the cEUR 148m of debt under Gek’s concession division.

In respect of the Kasteli airport concession, Gek Terna has been the sole bidder for the project in a

JV with India based airport operator JMR. The project concerns the greenfield development and 40-

year operating concession of a new international airport in Kasteli, Crete.

According to the bid Gek Terna will hold a 60% stake in the operating concession, while the

company’s construction arm will undertake the development of the project for a budget of EUR

480m. In terms of financing, EUR 200m will come from the concessionaires (Gek to contribute EUR

120m), with the State adding the remaining amount utilizing public investment funds as well as the

State fees from the current nearby operating airport in Heraklio, Crete that will be eventually

decommissioned.

Currently the technical file of the offer has been cleared by the relevant Ministry and the financial

terms are being examined. We would expect relevant in the close period. Note that the project has

a 5 year construction period.

In respect of prospects for the project, although we do not include it at this point in our estimates

we calculate that the airport concession could yield a high single digit IRR for the project. Assuming

the Equity investment of EUR 120m, we would add another cEUR 1.0 per share to the concession

division estimates. Recall that we roughly estimate about another EUR 0.4-0.5 per share for the

construction division from the project.

Crete is the biggest island in the country and a major tourism destination in the Mediterranean. The

two currently operating international airports in Crete host about 20% of the total international

arrivals in the country, with Athens International airport accounting for another c45%. International

air traffic volumes in the island have been outperforming the overall country’s growth rates for a

long time. Yet the relevant infrastructure remained underinvested, with demand urging for

significant upgrade projects.

Chart 9a. Heraklio airport traffic volumes (m passengers) Chart 9b. Heraklio airport traffic volumes % growth

Source: AXIA Research, HCAA

4.0

3.6 3.4

3.9 4.0

5.0 5.2 5.0

4.8 4.8 4.7 4.9

5.3 5.4 5.4 5.1 4.9

5.2 5.1

5.8 6.0 6.1

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Domestic International Total

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

Heracleio Airport Total GR airports

…to generate cumulative cash of about EUR 450m

Kasteli airport concession

Gek Terna – Company Update

AXIA Research Page 19

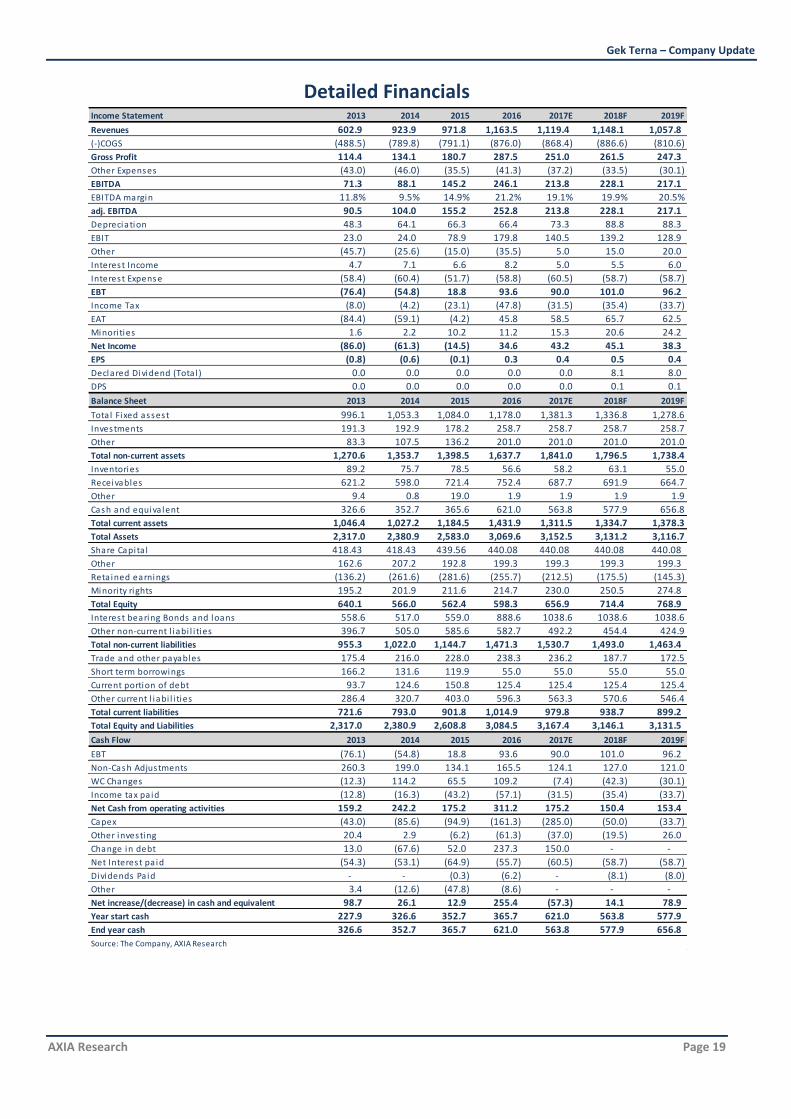

Detailed Financials

Income Statement 2013 2014 2015 2016 2017E 2018F 2019F

Revenues 602.9 923.9 971.8 1,163.5 1,119.4 1,148.1 1,057.8

(-)COGS (488.5) (789.8) (791.1) (876.0) (868.4) (886.6) (810.6)

Gross Profit 114.4 134.1 180.7 287.5 251.0 261.5 247.3

Other Expenses (43.0) (46.0) (35.5) (41.3) (37.2) (33.5) (30.1)

EBITDA 71.3 88.1 145.2 246.1 213.8 228.1 217.1

EBITDA margin 11.8% 9.5% 14.9% 21.2% 19.1% 19.9% 20.5%

adj. EBITDA 90.5 104.0 155.2 252.8 213.8 228.1 217.1

Depreciation 48.3 64.1 66.3 66.4 73.3 88.8 88.3

EBIT 23.0 24.0 78.9 179.8 140.5 139.2 128.9

Other (45.7) (25.6) (15.0) (35.5) 5.0 15.0 20.0

Interest Income 4.7 7.1 6.6 8.2 5.0 5.5 6.0

Interest Expense (58.4) (60.4) (51.7) (58.8) (60.5) (58.7) (58.7)

EBT (76.4) (54.8) 18.8 93.6 90.0 101.0 96.2

Income Tax (8.0) (4.2) (23.1) (47.8) (31.5) (35.4) (33.7)

EAT (84.4) (59.1) (4.2) 45.8 58.5 65.7 62.5

Minori ties 1.6 2.2 10.2 11.2 15.3 20.6 24.2

Net Income (86.0) (61.3) (14.5) 34.6 43.2 45.1 38.3

EPS (0.8) (0.6) (0.1) 0.3 0.4 0.5 0.4

Declared Dividend (Tota l ) 0.0 0.0 0.0 0.0 0.0 8.1 8.0

DPS 0.0 0.0 0.0 0.0 0.0 0.1 0.1

Balance Sheet 2013 2014 2015 2016 2017E 2018F 2019F

Total Fixed assest 996.1 1,053.3 1,084.0 1,178.0 1,381.3 1,336.8 1,278.6

Investments 191.3 192.9 178.2 258.7 258.7 258.7 258.7

Other 83.3 107.5 136.2 201.0 201.0 201.0 201.0

Total non-current assets 1,270.6 1,353.7 1,398.5 1,637.7 1,841.0 1,796.5 1,738.4

Inventories 89.2 75.7 78.5 56.6 58.2 63.1 55.0

Receivables 621.2 598.0 721.4 752.4 687.7 691.9 664.7

Other 9.4 0.8 19.0 1.9 1.9 1.9 1.9

Cash and equiva lent 326.6 352.7 365.6 621.0 563.8 577.9 656.8

Total current assets 1,046.4 1,027.2 1,184.5 1,431.9 1,311.5 1,334.7 1,378.3

Total Assets 2,317.0 2,380.9 2,583.0 3,069.6 3,152.5 3,131.2 3,116.7

Share Capita l 418.43 418.43 439.56 440.08 440.08 440.08 440.08

Other 162.6 207.2 192.8 199.3 199.3 199.3 199.3

Retained earnings (136.2) (261.6) (281.6) (255.7) (212.5) (175.5) (145.3)

Minori ty rights 195.2 201.9 211.6 214.7 230.0 250.5 274.8

Total Equity 640.1 566.0 562.4 598.3 656.9 714.4 768.9

Interest bearing Bonds and loans 558.6 517.0 559.0 888.6 1038.6 1038.6 1038.6

Other non-current l iabi l i ties 396.7 505.0 585.6 582.7 492.2 454.4 424.9

Total non-current liabilities 955.3 1,022.0 1,144.7 1,471.3 1,530.7 1,493.0 1,463.4

Trade and other payables 175.4 216.0 228.0 238.3 236.2 187.7 172.5

Short term borrowings 166.2 131.6 119.9 55.0 55.0 55.0 55.0

Current portion of debt 93.7 124.6 150.8 125.4 125.4 125.4 125.4

Other current l iabi l i ties 286.4 320.7 403.0 596.3 563.3 570.6 546.4

Total current liabilities 721.6 793.0 901.8 1,014.9 979.8 938.7 899.2

Total Equity and Liabilities 2,317.0 2,380.9 2,608.8 3,084.5 3,167.4 3,146.1 3,131.5

Cash Flow 2013 2014 2015 2016 2017E 2018F 2019F

EBT (76.1) (54.8) 18.8 93.6 90.0 101.0 96.2

Non-Cash Adjustments 260.3 199.0 134.1 165.5 124.1 127.0 121.0

WC Changes (12.3) 114.2 65.5 109.2 (7.4) (42.3) (30.1)

Income tax pa id (12.8) (16.3) (43.2) (57.1) (31.5) (35.4) (33.7)

Net Cash from operating activities 159.2 242.2 175.2 311.2 175.2 150.4 153.4

Capex (43.0) (85.6) (94.9) (161.3) (285.0) (50.0) (33.7)

Other investing 20.4 2.9 (6.2) (61.3) (37.0) (19.5) 26.0

Change in debt 13.0 (67.6) 52.0 237.3 150.0 - -

Net Interest pa id (54.3) (53.1) (64.9) (55.7) (60.5) (58.7) (58.7)

Dividends Pa id - - (0.3) (6.2) - (8.1) (8.0)

Other 3.4 (12.6) (47.8) (8.6) - - -

Net increase/(decrease) in cash and equivalent 98.7 26.1 12.9 255.4 (57.3) 14.1 78.9

Year start cash 227.9 326.6 352.7 365.7 621.0 563.8 577.9

End year cash 326.6 352.7 365.7 621.0 563.8 577.9 656.8

Source: The Company, AXIA Research

Gek Terna – Company Update

AXIA Research Page 20

Per share data 2013 2014 2015 2016 2017E 2018F 2019F

EPS (0.84) (0.59) (0.14) 0.34 0.42 0.44 0.37

BVPS 6.21 5.49 5.46 5.81 6.38 6.94 7.46

DPS 0.00 0.00 0.00 0.00 0.00 0.08 0.08

Valuation ratios 2013 2014 2015 2016 2017E 2018F 2019F

P/E n.m. n.m. -10.4 x 6.6 x 7.7 x 7.4 x 8.7 x

EV/EBITDA 11.2 x 6.5 x 3.9 x 2.6 x 4.4 x 4.1 x 3.9 x

EV/EBIT 34.7 x 23.8 x 7.2 x 3.5 x 6.7 x 6.7 x 6.6 x

EV/Sales 1.3 x 0.6 x 0.6 x 0.5 x 0.8 x 0.8 x 0.8 x

P/BV 0.5 x 0.3 x 0.3 x 0.4 x 0.5 x 0.5 x 0.4 x

Div. yield 0.0% 0.0% 0.0% 0.0% 0.0% 2.4% 2.3%

FCF yield 39.9% 83.1% 49.5% 38.8% -44.3% 24.4% 43.9%

ROA -2.6% -0.6% 1.2% 1.4% 1.4% 1.2%

ROE -10.2% -2.6% 6.0% 6.9% 6.6% 5.2%

ROIC -3.3% -0.8% 1.6% 1.9% 1.9% 1.6%

Growth rates 2013 2014 2015 2016 2017E 2018F 2019F

Revenues n.m. 53.2% 5.2% 19.7% -3.8% 2.6% -7.9%

EBITDA n.m. 23.5% 64.8% 69.5% -13.1% 6.7% -4.8%

EBIT n.m. 4.4% 228.2% 127.9% -21.9% -0.9% -7.4%

EBT n.m. n.m. n.m. 397.2% -3.8% 12.2% -4.8%

Net Income n.m. n.m. n.m. -339.6% 24.8% 4.3% -15.1%

Profitability ratios 2013 2014 2015 2016 2017E 2018F 2019F

Gross margin 19.0% 14.5% 18.6% 24.7% 22.4% 22.8% 23.4%

EBITDA margin 11.8% 9.5% 14.9% 21.2% 19.1% 19.9% 20.5%

EBIT margin 3.8% 2.6% 8.1% 15.5% 12.5% 12.1% 12.2%

Net Income margin n.m. n.m. -1.5% 3.0% 3.9% 3.9% 3.6%

Leverage Ratios 2013 2014 2015 2016 2017E 2018F 2019F

LT Debt / Tota l Capita l i ztion 1.53 x 2.48 x 3.42 x 3.70 x 3.00 x 3.00 x 3.00 x

Total Debt / Tota l Capita l i zation 2.29 x 3.82 x 5.23 x 4.49 x 3.54 x 3.54 x 3.54 x

Net Debt/EBITDA 6.40 x 4.31 x 2.87 x 1.64 x 2.85 x 2.61 x 2.38 x

FFO / Tota l Debt n.m. 0.00 x 0.07 x 0.10 x 0.10 x 0.11 x 0.11 x

Gearnig (Tota l debt / Debt+Equity) 0.55 x 0.56 x 0.58 x 0.63 x 0.64 x 0.62 x 0.60 x

Net Debt / Equity 0.71 x 0.67 x 0.74 x 0.67 x 0.93 x 0.83 x 0.67 x

Coverage Ratios 2013 2014 2015 2016 2017E 2018F 2019F

FFO Interest Coverage ((FFO + Int.) / Int.) 47.3% 131.9% 244.6% 331.8% 328.2% 372.4% 362.8%

Pretax Interest Coverage (EBIT / Int.) 42.9% 45.1% 175.0% 355.2% 253.3% 261.7% 244.5%

Source: The Company, AXIA Research

Gek Terna – Company Update

AXIA Research Page 21

Disclosures

General information This research report was prepared by AXIA Ventures Group Limited, a company incorporated under the laws of Cyprus (referred to herein, together with its subsidiary companies and affiliates, collectively, as “AXIA”) which is authorised and regulated by the Cyprus Securities and Exchange Commission (authorisation number 086/07). AXIA is authorized to provide investment services in the United Kingdom, Cyprus, Greece and in Portugal pursuant to its permissions under the Markets in Financial Instruments Directive and may also provide similar services in other countries, inside or outside of the European Union, subject to the applicable provisions. AXIA Ventures Group Limited is not a registered broker-dealer in the United States (U.S.), and, therefore, is not subject to U.S. rules regarding the preparation of research reports and the independence of research analysts. In the U.S., this research report is intended solely for persons who meet the definition of “major U.S. institutional investors” in Rule 15a-6 under the U.S. Securities and Exchange Act, as amended, or persons listed under Rule 15a-6(4)) and is meant to be disseminated only through “Axia Capital Markets LLC”, a wholly owned subsidiary of AXIA Ventures Group Limited and associated US registered broker-dealer in accordance with Rule 15a-6 of the US Securities and Exchange Act. Content of the report The persons in charge of the preparation of this report, the names of whom are disclosed below, certify that the views and opinions expressed on the subject security, issuer, companies or businesses covered by this research report (each a “Subject Company” and, collectively, the “Subject Companies”) are their personal opinions and that no part of their compensation was, is or will be directly or indirectly related to the specific recommendations or views contained in this research report. Whilst all substantial sources of information for the research are indicated in this report, including, without limitation, bases of valuation applied to any security or derivative security, such information has not been disclosed to the Subject Companies for their comments and no such information is hereby certified. All information contained herein is subject to change at any time without notice. No member of AXIA has an obligation to update, modify or amend this research report or to otherwise notify a reader thereof in the event that any matter stated herein, or any opinion, projection, forecast or estimate set forth herein, changes or subsequently becomes inaccurate, or if research on the Subject Company is withdrawn. Further, past performance is not indicative of future results. Persons responsible for this report: Argyrios Gkonis (Analyst), Constantinos Zouzoulas (Head of research). Key Definitions

AXIA Research 12-month rating*

Buy The stock to generate total return** of and above 10% within the next 12-months

Neutral The stock to generate total return**between -10% and 10% within the next 12-months

Sell The stock to generate total return** of and below -10% within the next 12 months

Under Review Stock’s target price or rating is subject to possible change

Restricted Applicable Laws / Regulation and AXIA Ventures Group Limited policies might restrict certain types of communication and investment recommendations

Not Rated There is no rating for the company by AXIA Ventures Group Limited

* Exceptions to the bands may be granted by the Investment Review Committee of AXIA taking into account specific characteristics of the Subject Company **Total return: % price appreciation equals percentage change in share price from current price to projected target price plus projected dividend yield.

Rating history for Gek Terna S.A.

Date Rating Share Price (EUR) Target Price (EUR)

11/03/2014 Buy 3.84 7.00

18/06/2015 Buy 1.46 3.80

19/04/2016 Buy 1.71 3.40

12/05/2017 Buy 3.35 4.70

Gek Terna – Company Update

AXIA Research Page 22

AXIA Ventures Group Limited Rating Distribution as of today

Coverage Universe Count Percent Of which Investment

Banking Relationships Count Percent

Buy 11 61% 1 1 6%

Neutral 2 11%

Sell

Restricted

Not Rated

Under Review 5 28%

Independence and objectivity, conflicts of interest management None of the analysts in charge of this report are involved in activities within AXIA where such involvement is inconsistent with the maintenance of that analyst’s independence or objectivity. None of them has received or purchased shares in any Subject Company prior to any private or public offering of those shares. However, the analysts responsible for the preparation of this report may interact with trading desks or sales personnel for the purpose of gathering and interpreting market information with regard to the Subject Companies. As an investment services provider engaging in a wide range of businesses, AXIA is active in the field of activities which may include the provision of services to issuers of securities, with respect to underwriting or placing of financial instruments or with respect to advice on capital structure, industrial strategy and related matters (“investment banking services”). The nature of such activities, in conjunction with the activity of production and issuance of research reports, may be considered as leading to situations of conflict of interests when the research reports cover an issuer with whom AXIA has an ongoing or has recently had a business relationship for the provision of investment banking services. AXIA has all the necessary internal structures and arrangements in order to identify and avoid or, should avoidance be impossible, to manage such situations in a manner consistent with the highest standards, in accordance with its internal conflicts of interest policy. In compliance with such arrangements, analysts and other staff who are involved in the preparation and dissemination of research (including, without limitation, this report) operate independently of management and the reporting line is separate from AXIA’s investment banking business. “Chinese Wall” procedures (procedures separating the availability of information of any Subject Company) are in place between the investment banking and research businesses to ensure that any confidential and/or price sensitive information is handled appropriately. In all cases when, at the time of preparation or issuance of a report, an issuer covered by such report is in a business relationship with AXIA for the provision of investment banking services, Axia includes a note in the report, drawing the attention of the recipients to such fact. The same note is included when such business relationship has been terminated less than 12 months before the issuance of the report. However, it cannot be fully precluded that issuers covered by a report may be in discussions with AXIA’s investment banking department for a potential future cooperation in investment banking matters, even though a business relationship does not already exist. In such cases AXIA may not be able to announce the fact of such discussions in the reports even if such reports cover the specific issuer. Therefore, even if this research report does not mention any existing or recent business relationship with an issuer whose securities are covered by the report, such issuer may be a potential future customer of AXIA in the field of investment banking services. It is noted that, even in such case, the persons in charge of this report do not participate in any such discussion and their remuneration is not determined based on the proceeds of the department providing investment banking services and that such situation is not reasonably expected to impair the independence or objectivity of AXIA’s reports.