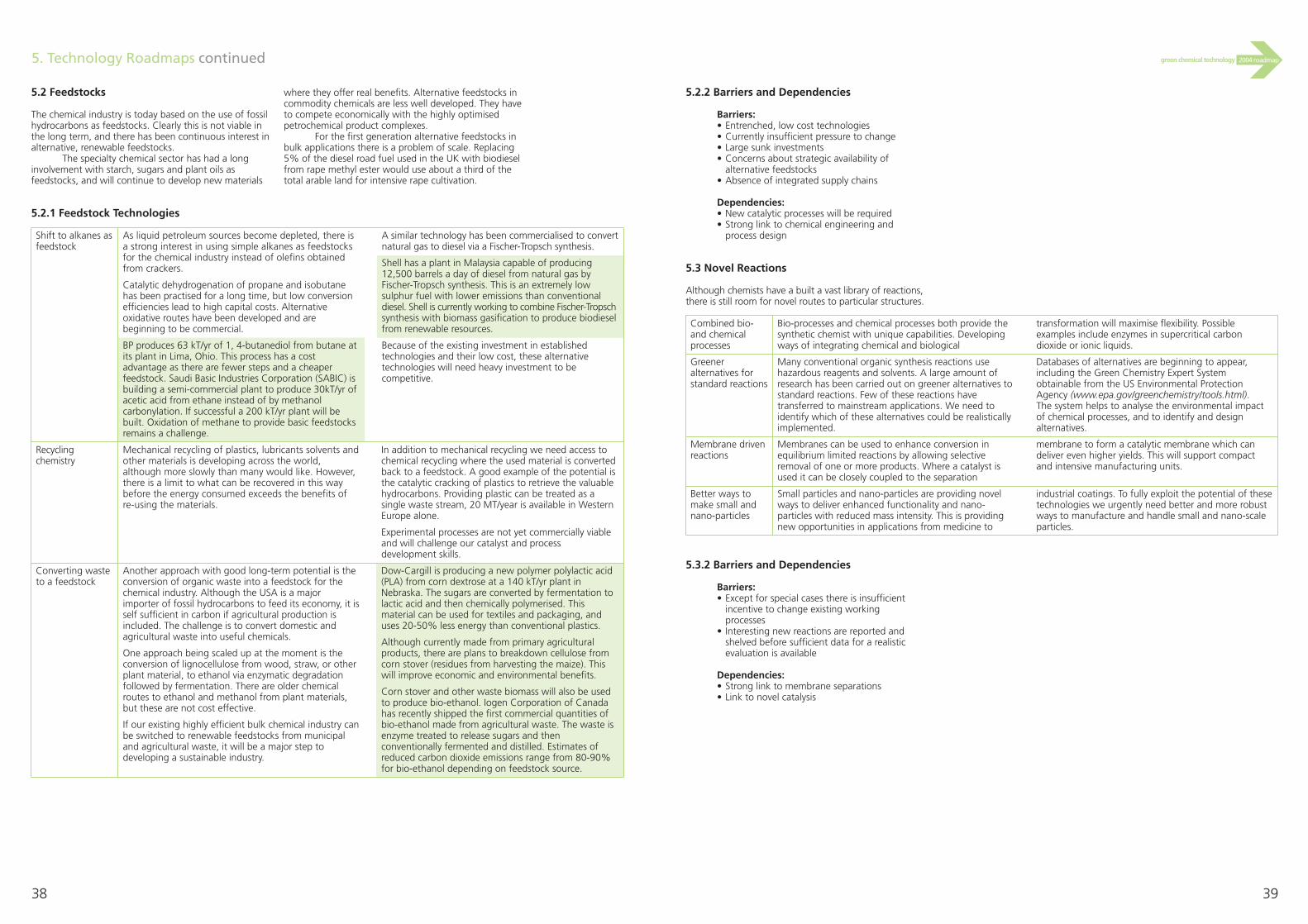

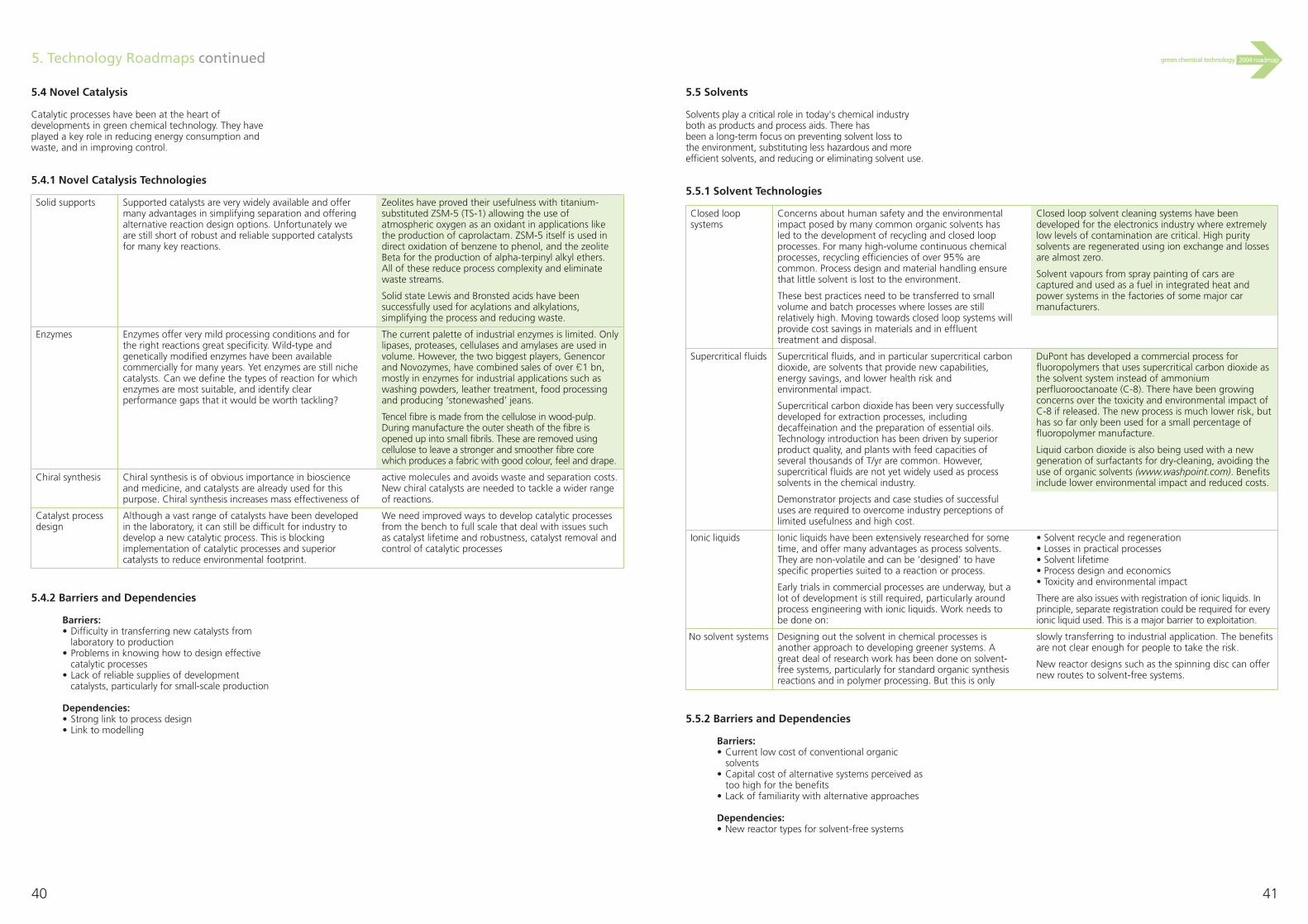

gct roadmap

DESCRIPTION

TRANSCRIPT

�2004 roadmapgreen

chemical technology

3

�2004 roadmapgreen chemical technology

2

The industry’s products pervade our society and are critical to the quality of life currently enjoyed by the public. A thriving andsustainable chemical industry is vital to our future.

The UK chemical industry is a vitalpart of our economy. It accountsfor 2% of UK GDP and 10% ofmanufacturing gross value added.It is UK manufacturing’s largestexporter.

Executive summary 41 Introduction, the purpose of the roadmap 82 Development of the roadmap 122.1 Process steps 123 Trends and drivers 143.1 Social trends and drivers 143.2 Technological trends and drivers 163.3 Economic trends and drivers 183.4 Environmental trends and drivers 203.5 Political trends and drivers 223.5.1 Future legislation 224 Features, attributes and technology

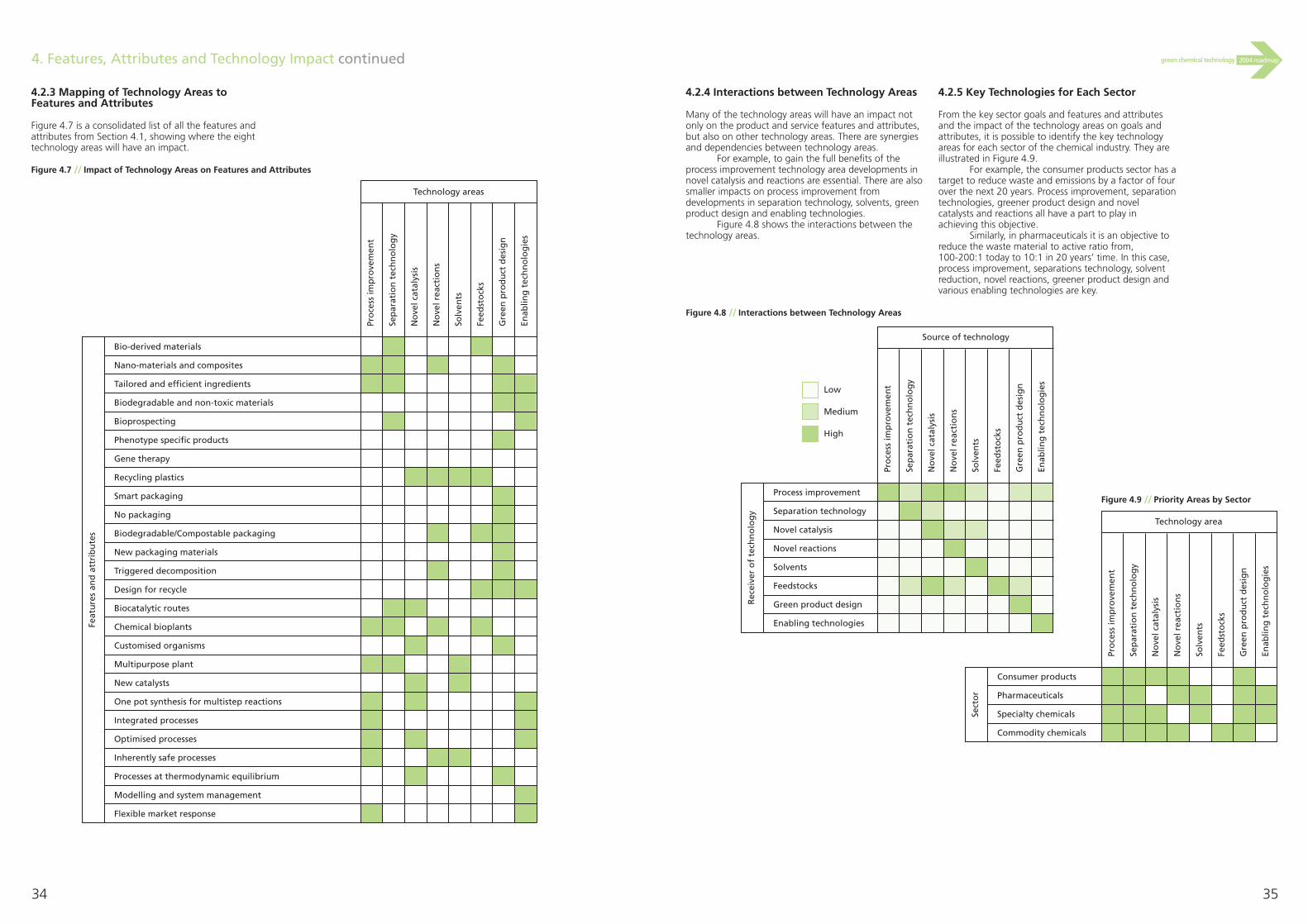

impact 244.1 Features and attributes by sector 244.1.1 Pharmaceuticals 244.1.3 Consumer 264.1.5 Specialties 284.1.7 Commodities 304.2 Grouping of sector goals 324.2.1 Identifying key goals 324.2.2 Mapping of technology areas to key goals 334.2.3 Mapping of technology areas to features

and attributes 344.2.4 Interactions between technology areas 354.2.5 Key technologies for each sector 35

5 Technology roadmaps 365.1 Green product design 365.2 Feedstocks 385.3 Novel reactions 395.4 Novel catalysis 405.5 Solvents 415.6 Process improvement 425.7 Separation technology 435.8 Enabling technologies 446 Priority activity areas 456.1 Exploiting existing technologies 456.2 Developing complete packages

for industry 456.3 Demonstrating the business case 456.4 Green product design for

the chemical industry 457 Key messages for government, industry 46

and academia8 Next steps 479 References 4810 Appendices 49

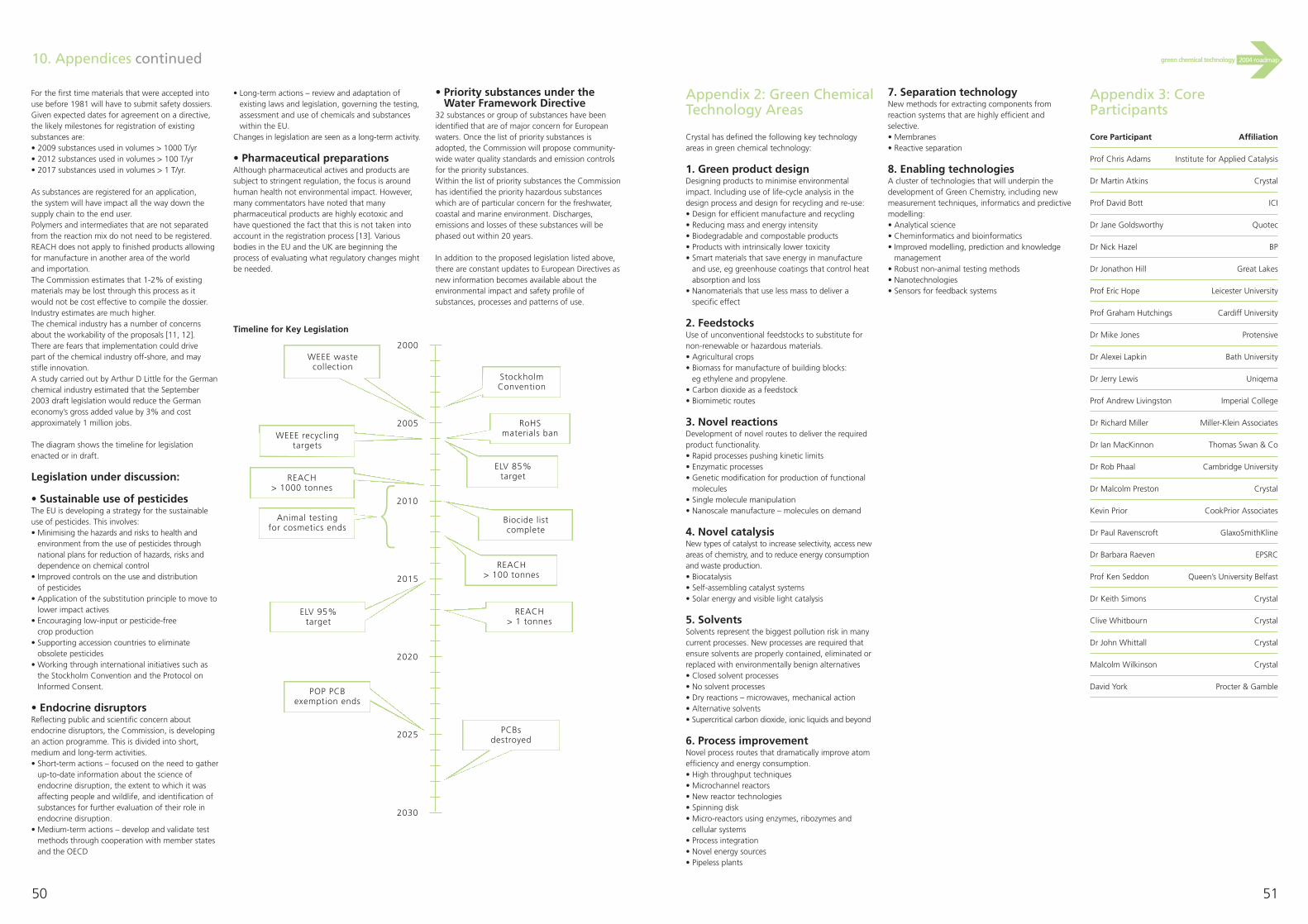

Appendix 1: Future legislation 49Appendix 2: Green Chemical Technology areas 51Appendix 3: Core participants 51

Maps are very useful things. We can try to find our way around the countryside without one, but simply following local signs may be foolhardy. For a trip from A to Z, a map is a must.

They’ve been around a long time.Maps started off showing just thegeographical world around us – a meansof sharing experience with others andremembering for ourselves. Now mappinghas gone well beyond this. We mapeverything – including technology –without limiting ourselves to thedimensions of physical space. A technologyroadmap seeks to set out how an area oftechnology will develop with time. We canuse it to chart a way ahead. Like itsgeographical forebears, it helps us avoidobvious dangers and dead-ends.

Industry has already used technologyroadmaps extensively to co-ordinate theactivities of the whole supply chain and to

provide detail in focused areas ofdevelopment. This roadmap – of GreenChemical Technology – is a first editionand certainly contains errors. It will getbetter as more people contribute, or asthose who did contribute – at the invitationof the Crystal Faraday Partnership – learnmore. The fact that it exists at all is animportant step for chemistry-basedindustries, as it lays out the current stateof knowledge in a format accessible to all.Its roots are in UK experience but thecontents do not recognise nationalboundaries, so it has global utility.

You can apply this document to yourown strategic objectives and planaccordingly. Equally, the experiencedCrystal team is ready to help you use itcorporately or in a specific technologicalarea. Crystal takes responsibility for thecore document, but is keen to capture allthe options and implications. So why notget in touch?

Foreword

Professor David Bott

Executive summary

4 5

�2004 roadmapgreen chemical technology

The UK chemical industry is a vital partof our economy. It accounts for 2% ofUK GDP and 10% of manufacturinggross value added. It is UKmanufacturing’s largest exporter. The industry’s products pervade oursociety and are critical to the qualityof life currently enjoyed by the public.A thriving and sustainable chemicalindustry is vital to our future.

To secure that future the chemicalindustry needs to reduce its overallenvironmental impact. Public and politicalpressures plus the physical limitations ofthe ecosphere mean that the chemicalindustry must change. It cannot continueat current levels of impact.

Green chemical technology is aroute to a more sustainable chemicalindustry. The OECD defines greenchemistry as:

“the design, manufacture, and use of environmentally benignchemical products and processes that prevent pollution, produce lesshazardous waste and reduceenvironmental and human healthrisks.”

Green chemical technology avoidsthe use of non-renewable resources,reduces energy and material use, reduceswaste and lowers environmental andhuman health impacts.

The Crystal Faraday Partnership hasbeen set up to be the lead organisationfor the research, development, andimplementation of green chemicaltechnology and practices in the UKchemical and allied industries.

Crystal has carried out thistechnology roadmapping study to identifythe future needs of the chemical industryfor green chemical technology and todevelop a strategy for their furtherdevelopment and implementation.

The trends and drivers affecting thechemical industry have been reviewedunder five headings (the STEEP model)[see section 3]:

• Social• Technological• Economic• Environmental• Political

The key messages from the social trendsand drivers are that the reputation of thechemical industry for environmentalresponsibility is low, and that consumerswish to avoid ‘chemicals’. The industrymust be seen to tackle these issues bydeveloping low-risk products and low-impact manufacturing. Failure to do socould lead to the public withdrawing theindustry’s ‘licence to operate’.

At the same time there is a growingskills gap caused by demographics andthe low reputation of the industry.

Technical trends will support themove towards zero-waste and zero-impact manufacturing. Greater recyclingand use of renewable raw materials willreduce unsustainable materialconsumption, and green product designwill reduce the lifetime environmentalimpact and cost of products.Developments in computing capability willplay an important role in creating a moresustainable chemical industry.

Economic trends are pushing theindustry in highly developed countriestowards added value ‘effect’ chemicals asbulk chemical production moves to lessdeveloped countries as part of their ownindustrialisation. In most sectors chemicalcompanies will become smaller, faster andmore flexible focusing on the knowledgecontent of products. As chemicalcompanies are forced to account for thewhole-life costs of a product, businessmodels will change to emphasise greenerproducts and processes, as well as productre-use, re-manufacture and recycling.

Environmental drivers will focus theindustry’s attention on the threat of climatechange, and the need to use resourcesefficiently and to switch to renewableresources. The industry will need to bebetter at understanding the whole life-cycle impact of products, and developingroutes to re-use and recycle materials.

Political trends impact the industryprincipally through legislation. Increasingregulation, both internationally and withinthe European Union, has been a powerfulforce for change in the chemical industryand this will continue. Green chemicaltechnology is essential if the industry is tomeet the demands of society.

There are eight areas of greenchemical technology that can improve thesustainability of the chemical industry andaddress the issues raised by the STEEPanalysis:

• Green product design –minimising environmental impact

• Feedstocks – substitutingrenewable for non-renewable

• Novel reactions• Novel catalysis• Solvents• Process improvement• Separation technology• Enabling technologies

These technology areas can be used todeliver benefits in nine different areasidentified as critical by the chemical industry:

• Reduce product toxicity• Reduce environmental impact of

a product• Reduce materials needed to

deliver a specific level ofperformance

• Reduce materials used tomanufacture the product

• Reduce use of non-renewableresources

• Reduce waste and emissionsduring manufacture

• Reduce energy used tomanufacture the product

• Reduce risk and hazard frommanufacturing processes

• Reduce life-cycle cost of chemical plant

Looking at the desired benefits and thetechnical opportunities we can identifythe key technical developments that willhave the most impact on developing asustainable chemical industry over theshort to medium term [see Section 5].

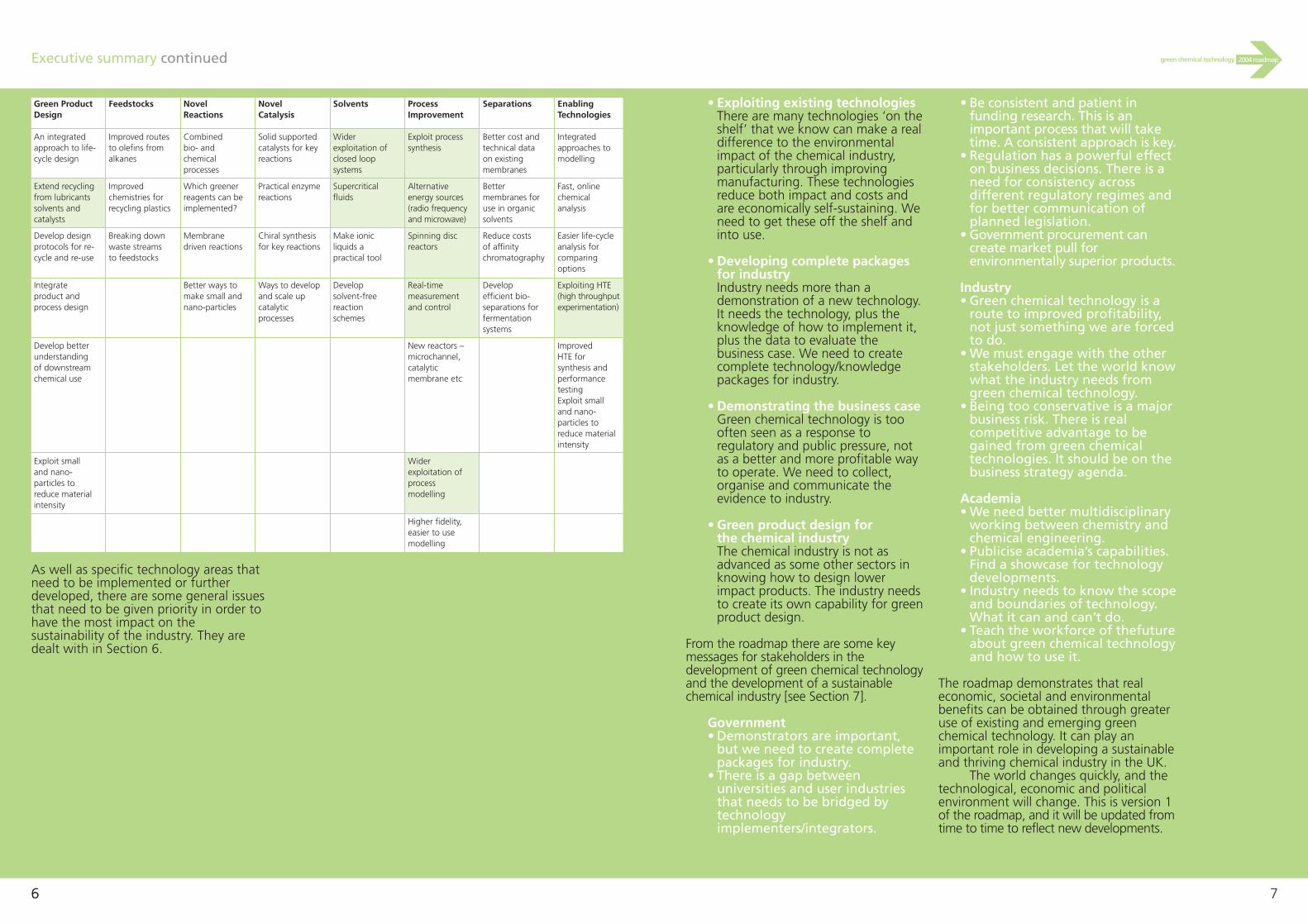

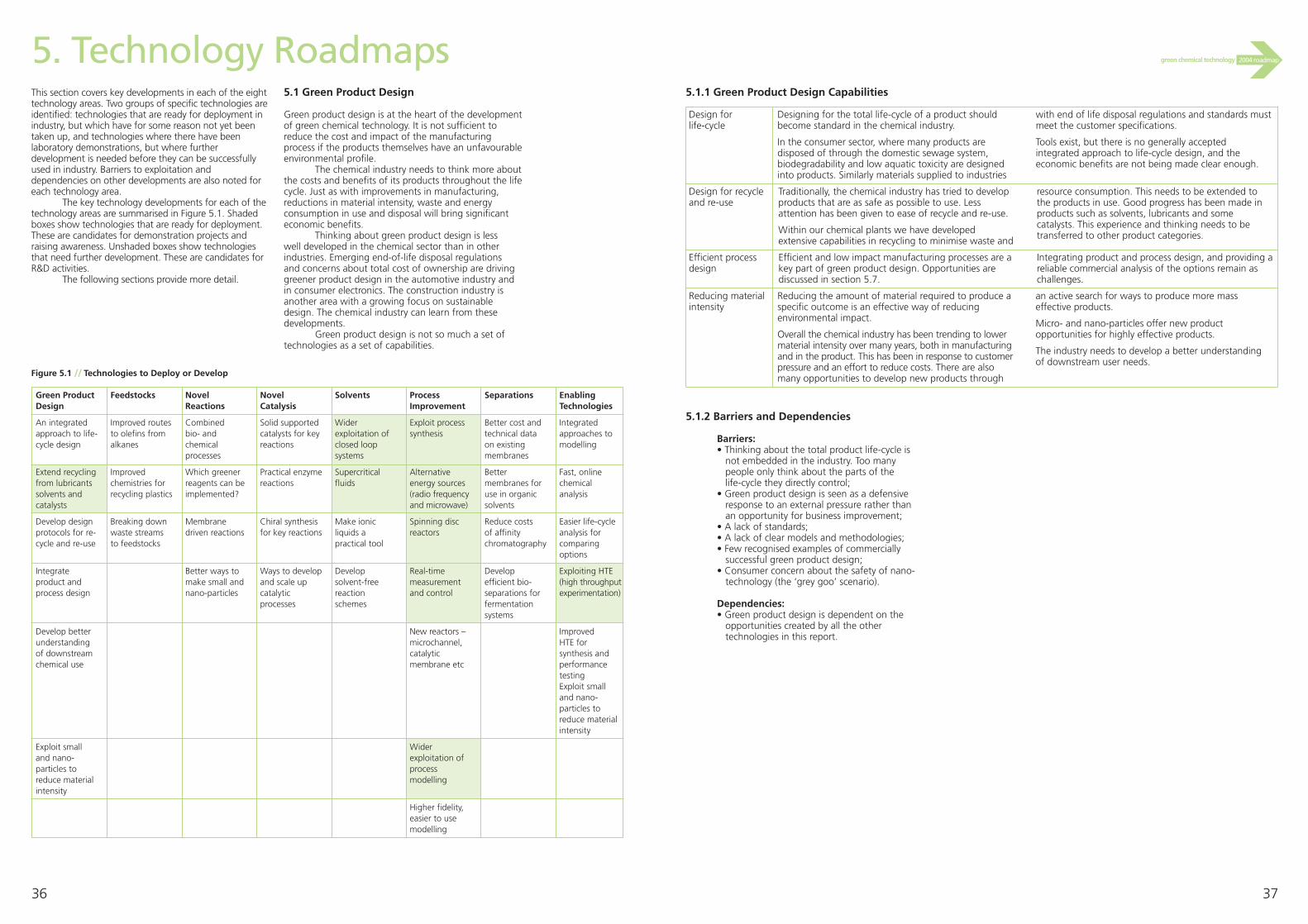

The key opportunities for eachtechnology area are summarised in the tableon page 6 [see also table 5.1, page 36].Shaded boxes are technologies ready forimplementation today that need support tobreakthrough to mainstream application.Unshaded boxes are technologies that needfurther development.

Executive summary continued

66 7

�2004 roadmapgreen chemical technology

As well as specific technology areas thatneed to be implemented or furtherdeveloped, there are some general issuesthat need to be given priority in order tohave the most impact on thesustainability of the industry. They aredealt with in Section 6.

• Exploiting existing technologies There are many technologies ‘on theshelf’ that we know can make a realdifference to the environmentalimpact of the chemical industry,particularly through improvingmanufacturing. These technologiesreduce both impact and costs andare economically self-sustaining. Weneed to get these off the shelf andinto use.

• Developing complete packages for industryIndustry needs more than ademonstration of a new technology.It needs the technology, plus theknowledge of how to implement it,plus the data to evaluate thebusiness case. We need to createcomplete technology/knowledgepackages for industry.

• Demonstrating the business caseGreen chemical technology is toooften seen as a response toregulatory and public pressure, notas a better and more profitable wayto operate. We need to collect,organise and communicate theevidence to industry.

• Green product design for the chemical industryThe chemical industry is not asadvanced as some other sectors inknowing how to design lowerimpact products. The industry needsto create its own capability for greenproduct design.

From the roadmap there are some keymessages for stakeholders in thedevelopment of green chemical technologyand the development of a sustainablechemical industry [see Section 7].

Government• Demonstrators are important,

but we need to create completepackages for industry.

• There is a gap betweenuniversities and user industriesthat needs to be bridged bytechnologyimplementers/integrators.

• Be consistent and patient infunding research. This is animportant process that will taketime. A consistent approach is key.

• Regulation has a powerful effecton business decisions. There is aneed for consistency acrossdifferent regulatory regimes andfor better communication ofplanned legislation.

• Government procurement cancreate market pull forenvironmentally superior products.

Industry• Green chemical technology is a

route to improved profitability,not just something we are forcedto do.

• We must engage with the otherstakeholders. Let the world knowwhat the industry needs fromgreen chemical technology.

• Being too conservative is a majorbusiness risk. There is realcompetitive advantage to begained from green chemicaltechnologies. It should be on thebusiness strategy agenda.

Academia• We need better multidisciplinary

working between chemistry andchemical engineering.

• Publicise academia’s capabilities.Find a showcase for technologydevelopments.

• Industry needs to know the scopeand boundaries of technology.What it can and can’t do.

• Teach the workforce of thefutureabout green chemical technologyand how to use it.

The roadmap demonstrates that realeconomic, societal and environmentalbenefits can be obtained through greateruse of existing and emerging greenchemical technology. It can play animportant role in developing a sustainableand thriving chemical industry in the UK.

The world changes quickly, and thetechnological, economic and politicalenvironment will change. This is version 1of the roadmap, and it will be updated fromtime to time to reflect new developments.

Green ProductDesign

An integratedapproach to life-cycle design

Extend recyclingfrom lubricantssolvents andcatalysts

Develop designprotocols for re-cycle and re-use

Integrateproduct andprocess design

Develop betterunderstandingof downstreamchemical use

Exploit smalland nano-particles toreduce materialintensity

Feedstocks

Improved routesto olefins fromalkanes

Improvedchemistries forrecycling plastics

Breaking downwaste streamsto feedstocks

NovelReactions

Combined bio- andchemicalprocesses

Which greenerreagents can beimplemented?

Membranedriven reactions

Better ways tomake small andnano-particles

NovelCatalysis

Solid supportedcatalysts for keyreactions

Practical enzymereactions

Chiral synthesisfor key reactions

Ways to developand scale upcatalyticprocesses

Solvents

Widerexploitation ofclosed loopsystems

Supercriticalfluids

Make ionicliquids apractical tool

Develop solvent-freereactionschemes

ProcessImprovement

Exploit processsynthesis

Alternativeenergy sources(radio frequencyand microwave)

Spinning discreactors

Real-timemeasurementand control

New reactors –microchannel,catalyticmembrane etc

Widerexploitation ofprocessmodelling

Higher fidelity,easier to usemodelling

Separations

Better cost andtechnical dataon existingmembranes

Bettermembranes foruse in organicsolvents

Reduce costs of affinitychromatography

Developefficient bio-separations forfermentationsystems

EnablingTechnologies

Integratedapproaches tomodelling

Fast, onlinechemicalanalysis

Easier life-cycleanalysis forcomparingoptions

Exploiting HTE(high throughputexperimentation)

Improved HTE forsynthesis andperformancetestingExploit smalland nano-particles toreduce materialintensity

9

�2004 roadmapgreen chemical technology

99

1. Introduction

8

The Crystal Faraday Partnership has been set up to bethe lead organisation for the research, development,and implementation of green chemical technology andpractices in the UK chemical and allied industries.

Crystal is a knowledge transfer company forgreen chemical technology accessing the considerableresources of its industrial and academic participants topromote lower-cost, sustainable manufacturing, for thechemical industry. The importance of green chemicaltechnology to the UK chemical industry was emphasisedby the Foresight programme. The chemical industry isfacing increasing competition and pressure on costs fromenvironmental legislation. Crystal is helping industry tomeet these challenges, and at the same time to build aresearch base of world-class quality in green technology.

Crystal has six key objectives:

• To be a single point of contact for greenchemical technology in the UK;

• To transfer new, green technology and bestpractice into real application;

• To identify core research prioritiesmatching industry's needs with innovationin universities;

• To stimulate new research or practicalapplications where they are needed;

• To increase awareness of best practice forsustainable products and processes;

• To train all those involved for the culturechange required.

1.1 Purpose of the Roadmap

Crystal has undertaken this technology roadmappingstudy to develop a strategy for green chemical technologyresearch and development based on the future needs ofindustry. The study has looked at the key needs of theindustry out to 2025.

The technology strategy will provide keydecision-makers in industry, academia and the UKgovernment with a clear picture of the role that greenchemical technology can play in developing a vibrantand sustainable chemical industry in the UK. It willidentify the opportunities, the gaps and the key actionsthat need to be taken to make sure that the potential ofgreen chemical technology is delivered.

The roadmap and technology strategy are livingdocuments and will be kept constantly under review. Inaddition to this report a website is planned to enable allstakeholders to explore and comment on the roadmapand strategy.

1.2 The Chemical Industry

The UK chemical industry brings enormous value to theUK economy and to society at large. The products of theindustry pervade all aspects of modern life, and thequality of life currently enjoyed by the public would beimpossible without a thriving chemical industry. Over many years it has provided a stream of innovationsthat are not only in direct use by consumers, but alsounderpin innovation right across the rest of industry, fromengineering and electronics to food and healthcare.

The chemical industry is a large and important partof the UK manufacturing sector. Domestic production ofchemicals was £34 billion in 2001. This accounts for 2%of UK GDP and 10% of manufacturing industry’s grossvalue added. The industry is UK manufacturing’s largestexporter with a trade surplus in 2001 of £5.5 billion. In addition, the industry earned £885 million in royaltypayments for exploitation of its intellectual property inother markets. Average growth rate over the period 1991-2001 was 3.1%, about the same as GDP growth andsecond in the manufacturing sector behind electrical andoptical equipment.

Approximately 230,000 skilled people areemployed in 3500 companies that range in size fromfewer than 10 employees to many thousands. Theindustry invests £400 million per annum in training,enriching the skill base of the country, and £3.5 billionper annum on R&D activities supporting innovation ofall types [1, 2].

The chemical industry was one of the first in theUK to come under the scrutiny of environmentalcampaigners, and has experienced progressive pressurefrom public opinion and government regulation. In response it has made great strides in reducing itsenvironmental footprint and its potential impact onhuman health. Waste and emissions of all types havebeen sharply reduced as the industry has taken steps toclean itself up.

However, despite all this good work, thechemical industry finds itself with a very poor publicreputation. A recent MORI survey found that onlyaround 20% of the public viewed the industryfavourably [2]. The main reason for the low reputationwas concern about the environmental and healthimpact of the chemical industry. A poor publicreputation can have a devastating impact on anindustry. It can mean:

• difficulties in raising finance;• problems with recruiting and retaining talent;• loss of its licence to operate – either nationally

or locally;• consumers aggressively reject the industry’s

products;• a weak position in negotiations with

government about the regulatory, economicand fiscal environment.

Developing a sustainable future for the UKrequires the products of a strong and successful chemicalindustry. That industry can be in the UK or elsewhere,but it must exist. Many of the dilemmas of sustainabledevelopment can only be solved with the expertise andknow-how of chemists, chemical engineers and thechemical industry. Since the chemical industry alreadycontributes so much to the UK economy and society, it is desirable to continue to develop the chemicalindustry in the UK rather than simply importing ourrequirements from other countries.

To be able to take advantage of the economicprosperity and technical innovation of the chemicalindustry in the UK we need to develop and communicatea vision of a sustainable chemical industry: an industrywhich is valued by the public and not viewed withconstant suspicion. Green chemical technology can playan important part in this transformation, continuing thework of reducing the environmental impact of theexisting business, but also unleashing innovation throughthe application of new technologies.

For the purpose of this report the UK chemicalindustry is divided into four sectors each of which raisesdifferent issues of sustainability. Each will exploit greenchemical technology in different ways.

• Pharmaceuticals

Chemicals and formulated products to preventor treat disease conditions and to promotehealth. This is a large part of the UK chemicalindustry and dominates the total R&Dinvestment. This is a highly innovative sector,with a constant need to find novel activeingredients and new ways to deliver drugs.There is a strong interest in reducing toxicity of actives and increasing their efficiency.

• Consumer products

Products sold directly to consumers, includingcosmetics, cleaning products, paints andadhesives, but excluding foods and fuels. These products are sold on performance andbrand. These chemical products are usuallydesigned to be released directly into theenvironment, and so there is considerableinterest in reducing their toxicity and overallenvironmental impact.

• Specialty chemicals

Specialty chemicals are sold on what they do,rather than what they are and what they cost.Performance is the important issue. Specialtychemicals are sold in lower volumes and athigher value than commodity chemicals.Innovation is key and the attraction for thissector is the potential of green chemicaltechnologies to open up new areas of chemistrywhilst continuing to drive down toxicity andenvironmental impact.

• Commodity chemicals

Chemicals produced in high volumes and sold onthe basis of specification and price. The area ofgreen chemical technology of most interest to thissector is improving atom efficiency by minimisingresource and energy consumption, and waste.

1.3 Green Chemistry and Green Chemical Technology

The concept of Green Chemistry has been defined in anumber of ways. The OECD [3] describes it as:

“the design, manufacture, and use ofenvironmentally benign chemical products and processesthat prevent pollution, produce less hazardous waste andreduce environmental and human health risks.”

Green Chemistry seeks to avoid the use ofdepleting and non-renewable resources, reduce thematter and energy required to deliver a particular effect,reduce human health and safety issues and reduce theenvironmental impact of products in manufacture and use.

Some of the main themes in Green Chemistry are [4, 5]:

• atom efficiency – designing processes to maximise the amount of raw materialthat is converted into product;

• energy conservation – designing moreenergy efficient processes;

• waste minimisation – recognising that thebest form of waste disposal is not to createwaste in the first place;

• substitution – using safer, moreenvironmentally benign raw materialsand solvents or solvent-free processes;

• designing safer products – using moleculardesign and the principles of toxicity andmechanism of action to minimise theintrinsic toxicity of the product whilemaintaining its efficacy of function;

• developing alternative reaction conditions– designing reaction conditions thatincrease selectivity for the product andallow for dematerialization of the productseparation process;

• use of alternative feedstocks – usingfeedstocks that are renewable and less toxic to human health and theenvironment;

• employing natural processes – usingbiosynthesis, biocatalysis and biotech-based chemical transformations forefficiency and selectivity.

Introduction continued

10 11

�2004 roadmapgreen chemical technology

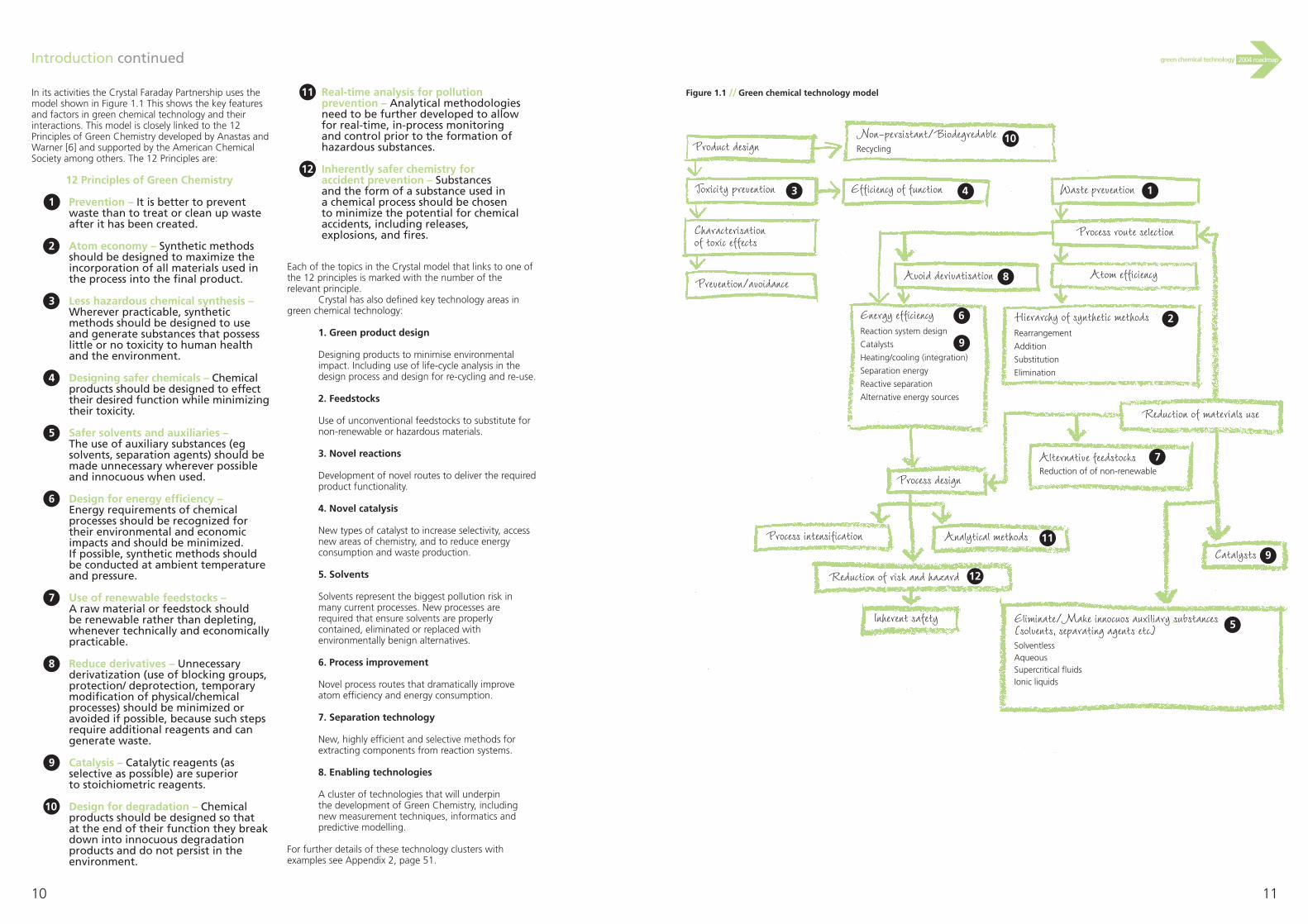

In its activities the Crystal Faraday Partnership uses themodel shown in Figure 1.1 This shows the key featuresand factors in green chemical technology and theirinteractions. This model is closely linked to the 12Principles of Green Chemistry developed by Anastas andWarner [6] and supported by the American ChemicalSociety among others. The 12 Principles are:

11 Real-time analysis for pollutionprevention – Analytical methodologiesneed to be further developed to allowfor real-time, in-process monitoringand control prior to the formation ofhazardous substances.

12 Inherently safer chemistry for accident prevention – Substances and the form of a substance used in a chemical process should be chosen to minimize the potential for chemicalaccidents, including releases,explosions, and fires.

12 Principles of Green Chemistry

1 Prevention – It is better to preventwaste than to treat or clean up wasteafter it has been created.

2 Atom economy – Synthetic methodsshould be designed to maximize theincorporation of all materials used inthe process into the final product.

3 Less hazardous chemical synthesis –Wherever practicable, syntheticmethods should be designed to useand generate substances that possesslittle or no toxicity to human healthand the environment.

4 Designing safer chemicals – Chemicalproducts should be designed to effecttheir desired function while minimizingtheir toxicity.

5 Safer solvents and auxiliaries –The use of auxiliary substances (egsolvents, separation agents) should bemade unnecessary wherever possibleand innocuous when used.

6 Design for energy efficiency –Energy requirements of chemicalprocesses should be recognized fortheir environmental and economicimpacts and should be minimized. If possible, synthetic methods shouldbe conducted at ambient temperatureand pressure.

7 Use of renewable feedstocks –A raw material or feedstock should be renewable rather than depleting,whenever technically and economicallypracticable.

8 Reduce derivatives – Unnecessaryderivatization (use of blocking groups,protection/ deprotection, temporarymodification of physical/chemicalprocesses) should be minimized oravoided if possible, because such stepsrequire additional reagents and cangenerate waste.

9 Catalysis – Catalytic reagents (asselective as possible) are superior to stoichiometric reagents.

Design for degradation – Chemicalproducts should be designed so that at the end of their function they breakdown into innocuous degradationproducts and do not persist in theenvironment.

Each of the topics in the Crystal model that links to one ofthe 12 principles is marked with the number of therelevant principle.

Crystal has also defined key technology areas ingreen chemical technology:

1. Green product design

Designing products to minimise environmentalimpact. Including use of life-cycle analysis in thedesign process and design for re-cycling and re-use.

2. Feedstocks

Use of unconventional feedstocks to substitute fornon-renewable or hazardous materials.

3. Novel reactions

Development of novel routes to deliver the requiredproduct functionality.

4. Novel catalysis

New types of catalyst to increase selectivity, accessnew areas of chemistry, and to reduce energyconsumption and waste production.

5. Solvents

Solvents represent the biggest pollution risk inmany current processes. New processes arerequired that ensure solvents are properlycontained, eliminated or replaced withenvironmentally benign alternatives.

6. Process improvement

Novel process routes that dramatically improveatom efficiency and energy consumption.

7. Separation technology

New, highly efficient and selective methods forextracting components from reaction systems.

8. Enabling technologies

A cluster of technologies that will underpin the development of Green Chemistry, includingnew measurement techniques, informatics andpredictive modelling.

For further details of these technology clusters withexamples see Appendix 2, page 51.

Product design

Characterisation of toxic effects

Prevention/avoidance

Waste prevention

Process route selection

Avoid derivatisation

Hierarchy of synthetic methods

Rearrangement

Addition

Substitution

Elimination

Energy efficiency

Reaction system design

Catalysts

Heating/cooling (integration)

Separation energy

Reactive separation

Alternative energy sources

Atom efficiency

Process design

Analytical methodsProcess intensification

Reduction of risk and hazard

Catalysts

Inherent safety Eliminate/Make innocuos auxiliary substances (solvents, separating agents etc)

SolventlessAqueousSupercritical fluidsIonic liquids

Figure 1.1 // Green chemical technology model

Reduction of materials use

Alternative feedstocksReduction of of non-renewable

Toxicity prevention Efficiency of function

Non-persistant/Biodegredable

Recycling10

1

8

6

9

43

2

5

9

11

10

7

12

1

13

�2004 roadmapgreen chemical technology2. Development of the Roadmap

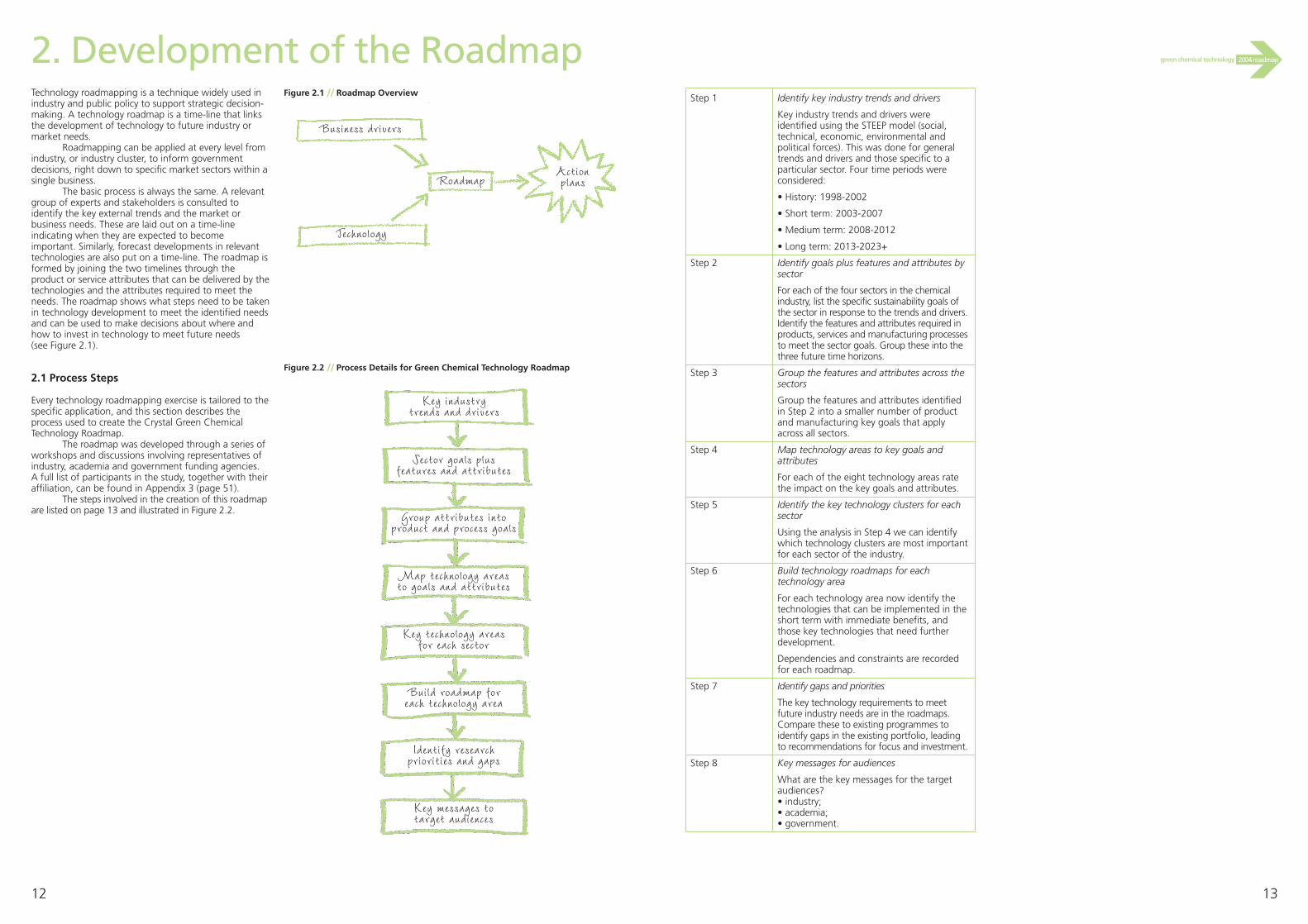

12

Technology roadmapping is a technique widely used inindustry and public policy to support strategic decision-making. A technology roadmap is a time-line that linksthe development of technology to future industry ormarket needs.

Roadmapping can be applied at every level fromindustry, or industry cluster, to inform governmentdecisions, right down to specific market sectors within asingle business.

The basic process is always the same. A relevantgroup of experts and stakeholders is consulted toidentify the key external trends and the market orbusiness needs. These are laid out on a time-lineindicating when they are expected to becomeimportant. Similarly, forecast developments in relevanttechnologies are also put on a time-line. The roadmap isformed by joining the two timelines through theproduct or service attributes that can be delivered by thetechnologies and the attributes required to meet theneeds. The roadmap shows what steps need to be takenin technology development to meet the identified needsand can be used to make decisions about where andhow to invest in technology to meet future needs (see Figure 2.1).

2.1 Process Steps

Every technology roadmapping exercise is tailored to thespecific application, and this section describes theprocess used to create the Crystal Green ChemicalTechnology Roadmap.

The roadmap was developed through a series ofworkshops and discussions involving representatives ofindustry, academia and government funding agencies. A full list of participants in the study, together with theiraffiliation, can be found in Appendix 3 (page 51).

The steps involved in the creation of this roadmapare listed on page 13 and illustrated in Figure 2.2.

Step 1

Step 2

Step 3

Step 4

Step 5

Step 6

Step 7

Step 8

Figure 2.1 // Roadmap Overview

Figure 2.2 // Process Details for Green Chemical Technology Roadmap

Business drivers

Technology

RoadmapActionplans

Key industry trends and drivers

Sector goals plus features and attributes

Group attributes into product and process goals

Map technology areas to goals and attributes

Key technology areas for each sector

Build roadmap for each technology area

Identify research priorities and gaps

Key messages totarget audiences

Identify key industry trends and drivers

Key industry trends and drivers wereidentified using the STEEP model (social,technical, economic, environmental andpolitical forces). This was done for generaltrends and drivers and those specific to aparticular sector. Four time periods wereconsidered:

• History: 1998-2002

• Short term: 2003-2007

• Medium term: 2008-2012

• Long term: 2013-2023+

Identify goals plus features and attributes bysector

For each of the four sectors in the chemicalindustry, list the specific sustainability goals ofthe sector in response to the trends and drivers.Identify the features and attributes required inproducts, services and manufacturing processesto meet the sector goals. Group these into thethree future time horizons.

Group the features and attributes across thesectors

Group the features and attributes identifiedin Step 2 into a smaller number of productand manufacturing key goals that applyacross all sectors.

Map technology areas to key goals andattributes

For each of the eight technology areas ratethe impact on the key goals and attributes.

Identify the key technology clusters for eachsector

Using the analysis in Step 4 we can identifywhich technology clusters are most importantfor each sector of the industry.

Build technology roadmaps for eachtechnology area

For each technology area now identify thetechnologies that can be implemented in theshort term with immediate benefits, andthose key technologies that need furtherdevelopment.

Dependencies and constraints are recordedfor each roadmap.

Identify gaps and priorities

The key technology requirements to meetfuture industry needs are in the roadmaps.Compare these to existing programmes toidentify gaps in the existing portfolio, leadingto recommendations for focus and investment.

Key messages for audiences

What are the key messages for the targetaudiences?• industry;• academia;• government.

Industry is seen as theprovider

of solutions,not as the problem

15

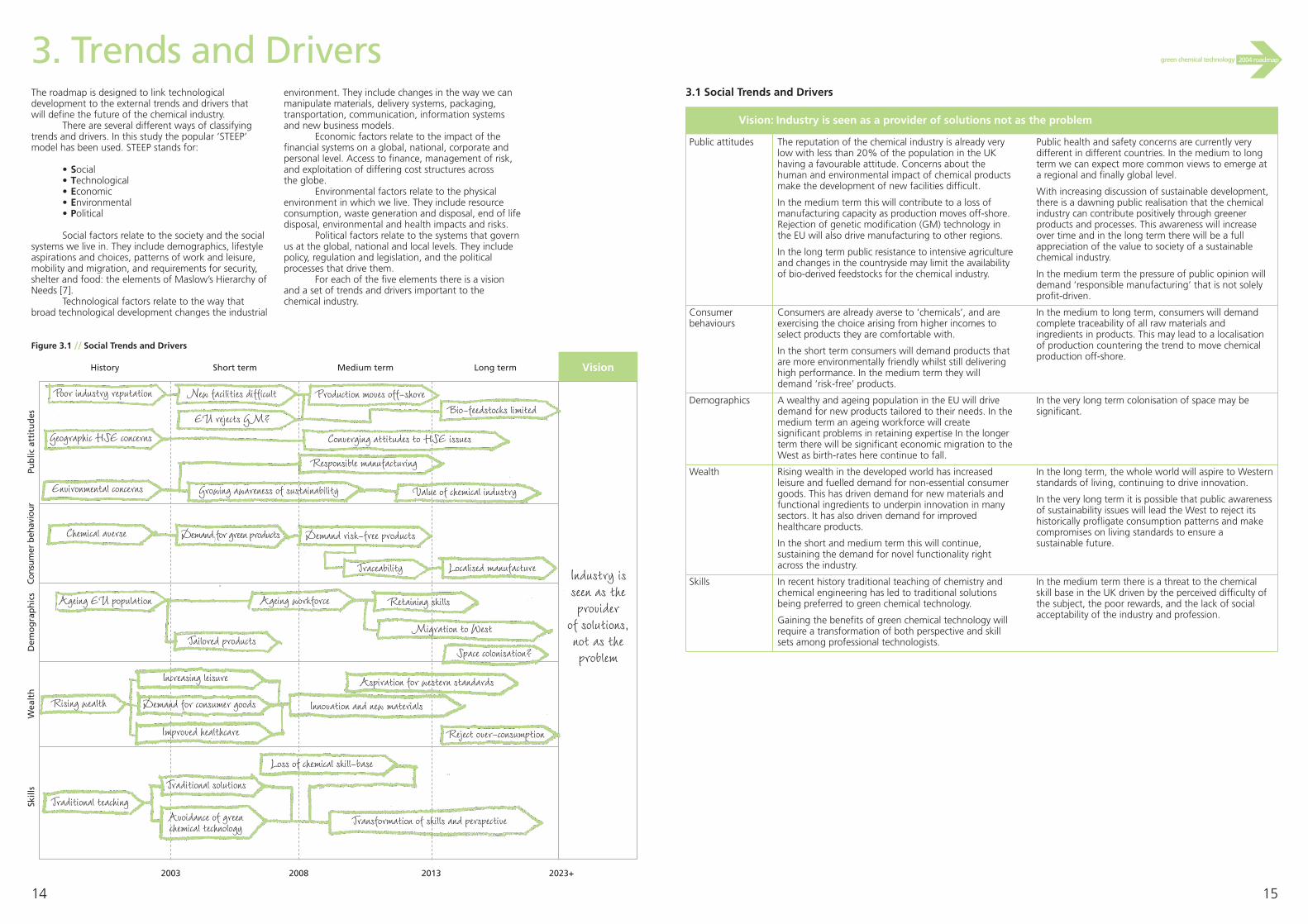

�2004 roadmapgreen chemical technology3. Trends and Drivers

14

The roadmap is designed to link technologicaldevelopment to the external trends and drivers that will define the future of the chemical industry.

There are several different ways of classifyingtrends and drivers. In this study the popular ‘STEEP’model has been used. STEEP stands for:

• Social• Technological• Economic• Environmental• Political

Social factors relate to the society and the socialsystems we live in. They include demographics, lifestyleaspirations and choices, patterns of work and leisure,mobility and migration, and requirements for security,shelter and food: the elements of Maslow’s Hierarchy ofNeeds [7].

Technological factors relate to the way thatbroad technological development changes the industrial

environment. They include changes in the way we canmanipulate materials, delivery systems, packaging,transportation, communication, information systemsand new business models.

Economic factors relate to the impact of thefinancial systems on a global, national, corporate andpersonal level. Access to finance, management of risk,and exploitation of differing cost structures across the globe.

Environmental factors relate to the physicalenvironment in which we live. They include resourceconsumption, waste generation and disposal, end of lifedisposal, environmental and health impacts and risks.

Political factors relate to the systems that governus at the global, national and local levels. They includepolicy, regulation and legislation, and the politicalprocesses that drive them.

For each of the five elements there is a visionand a set of trends and drivers important to thechemical industry.

Poor industry reputation New facilities difficult Production moves off-shore

Geographic HSE concerns

EU rejects GM?Bio-feedstocks limited

Converging attitudes to HSE issues

Environmental concerns

Chemical averse

Ageing EU population

Value of chemical industry

Responsible manufacturing

Demand risk-free products

Ageing workforce

Traceability Localised manufacture

Retaining skills

Migration to WestTailored products

Space colonisation?

Rising wealth

Increasing leisure

Demand for consumer goods

Improved healthcare

Innovation and new materials

Reject over-consumption

Loss of chemical skill-base

Traditional solutions

Traditional teaching

Avoidance of greenchemical technology

Transformation of skills and perspective

Aspiration for western standards

Demand for green products

Growing awareness of sustainability

Figure 3.1 // Social Trends and Drivers

Public attitudes

Consumer behaviours

Demographics

Wealth

Skills

The reputation of the chemical industry is already verylow with less than 20% of the population in the UKhaving a favourable attitude. Concerns about thehuman and environmental impact of chemical productsmake the development of new facilities difficult.

In the medium term this will contribute to a loss ofmanufacturing capacity as production moves off-shore.Rejection of genetic modification (GM) technology inthe EU will also drive manufacturing to other regions.

In the long term public resistance to intensive agricultureand changes in the countryside may limit the availabilityof bio-derived feedstocks for the chemical industry.

Public health and safety concerns are currently verydifferent in different countries. In the medium to longterm we can expect more common views to emerge ata regional and finally global level.

With increasing discussion of sustainable development,there is a dawning public realisation that the chemicalindustry can contribute positively through greenerproducts and processes. This awareness will increaseover time and in the long term there will be a fullappreciation of the value to society of a sustainablechemical industry.

In the medium term the pressure of public opinion willdemand ‘responsible manufacturing’ that is not solelyprofit-driven.

Consumers are already averse to ‘chemicals’, and areexercising the choice arising from higher incomes toselect products they are comfortable with.

In the short term consumers will demand products thatare more environmentally friendly whilst still deliveringhigh performance. In the medium term they willdemand ‘risk-free’ products.

In the medium to long term, consumers will demandcomplete traceability of all raw materials andingredients in products. This may lead to a localisationof production countering the trend to move chemicalproduction off-shore.

A wealthy and ageing population in the EU will drivedemand for new products tailored to their needs. In themedium term an ageing workforce will createsignificant problems in retaining expertise In the longerterm there will be significant economic migration to theWest as birth-rates here continue to fall.

In the very long term colonisation of space may besignificant.

Rising wealth in the developed world has increasedleisure and fuelled demand for non-essential consumergoods. This has driven demand for new materials andfunctional ingredients to underpin innovation in manysectors. It has also driven demand for improvedhealthcare products.

In the short and medium term this will continue,sustaining the demand for novel functionality rightacross the industry.

In the long term, the whole world will aspire to Westernstandards of living, continuing to drive innovation.

In the very long term it is possible that public awarenessof sustainability issues will lead the West to reject itshistorically profligate consumption patterns and makecompromises on living standards to ensure a sustainable future.

In recent history traditional teaching of chemistry andchemical engineering has led to traditional solutionsbeing preferred to green chemical technology.

Gaining the benefits of green chemical technology willrequire a transformation of both perspective and skillsets among professional technologists.

In the medium term there is a threat to the chemicalskill base in the UK driven by the perceived difficulty ofthe subject, the poor rewards, and the lack of socialacceptability of the industry and profession.

History Short term Medium term Long term

Skill

sW

ealt

hD

emo

gra

ph

ics

Cons

umer

beh

avio

ur

2003 2008 2013

Pub

lic a

ttit

ud

es

2023+

Vision: Industry is seen as a provider of solutions not as the problem

3.1 Social Trends and Drivers

Vision

17

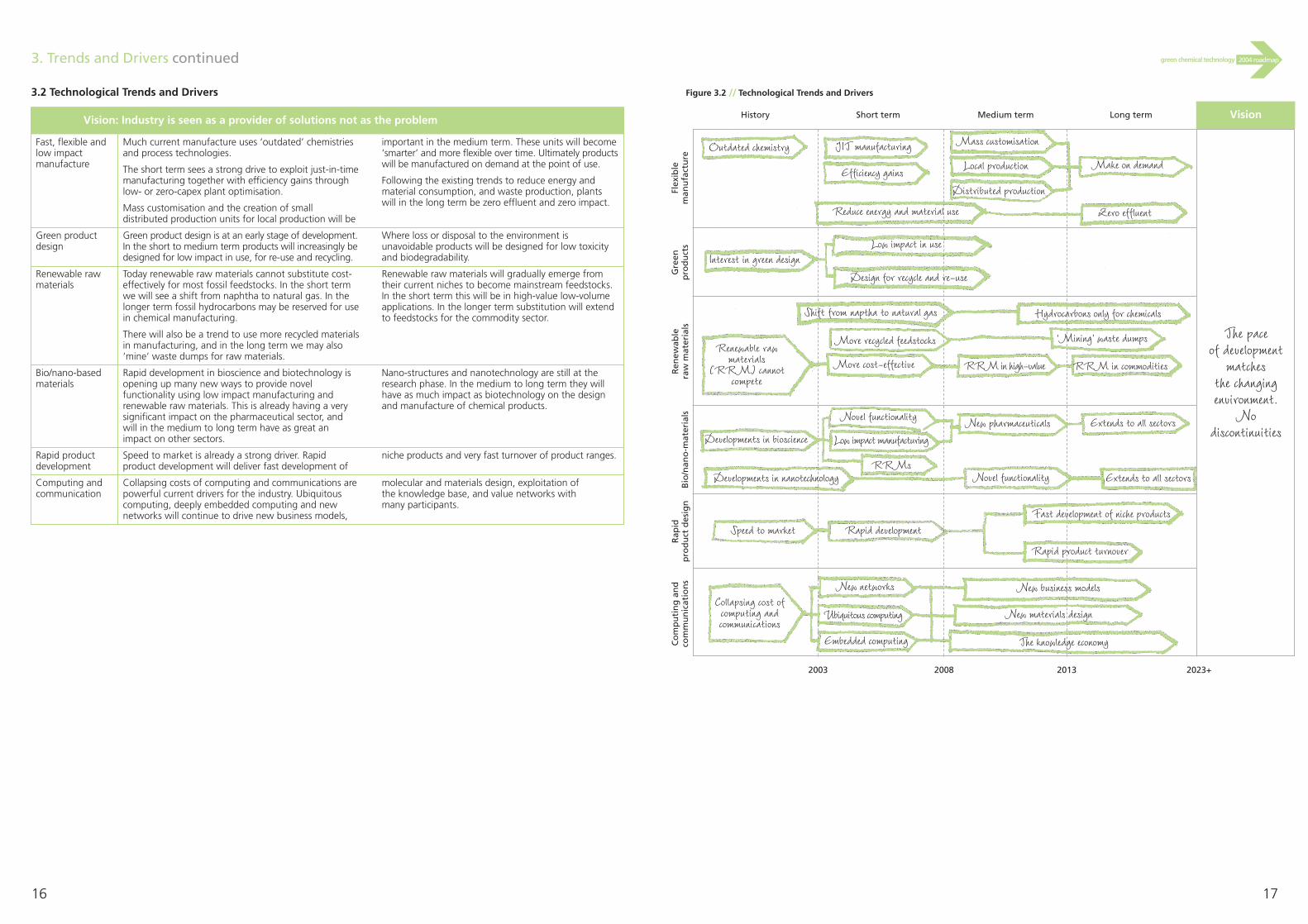

�2004 roadmapgreen chemical technology3. Trends and Drivers continued

16

Fast, flexible and low impact manufacture

Green productdesign

Renewable rawmaterials

Bio/nano-basedmaterials

Rapid productdevelopment

Computing andcommunication

Figure 3.2 // Technological Trends and Drivers

Outdated chemistry JIT manufacturing

Efficiency gains

Mass customisation

Local production

Distributed production

Make on demand

Zero effluent

Interest in green design

Reduce energy and material use

Low impact in use

Design for recycle and re-use

Shift from naptha to natural gas

More recycled feedstocks

Hydrocarbons only for chemicals

‘Mining’ waste dumpsRenewable raw

materials(RRM) cannot

compete

More cost-effective RRM in high-value RRM in commodities

Developments in bioscience

Novel functionality

Low impact manufacturing

New pharmaceuticals Extends to all sectors

Developments in nanotechnologyRRMs

Extends to all sectorsNovel functionality

Speed to market Rapid development

Rapid product turnover

History Short term Medium term Long term

2003 2008 2013 2023+Fl

exib

le

man

ufa

ctu

reG

reen

p

rod

uct

sR

enew

able

ra

w m

ater

ials

B

io/n

ano

-mat

eria

lsR

apid

p

rod

uct

des

ign

Much current manufacture uses ‘outdated’ chemistriesand process technologies.

The short term sees a strong drive to exploit just-in-timemanufacturing together with efficiency gains throughlow- or zero-capex plant optimisation.

Mass customisation and the creation of smalldistributed production units for local production will be

important in the medium term. These units will become‘smarter’ and more flexible over time. Ultimately productswill be manufactured on demand at the point of use.

Following the existing trends to reduce energy andmaterial consumption, and waste production, plantswill in the long term be zero effluent and zero impact.

Green product design is at an early stage of development.In the short to medium term products will increasingly bedesigned for low impact in use, for re-use and recycling.

Where loss or disposal to the environment isunavoidable products will be designed for low toxicityand biodegradability.

Today renewable raw materials cannot substitute cost-effectively for most fossil feedstocks. In the short termwe will see a shift from naphtha to natural gas. In thelonger term fossil hydrocarbons may be reserved for usein chemical manufacturing.

There will also be a trend to use more recycled materialsin manufacturing, and in the long term we may also‘mine’ waste dumps for raw materials.

Renewable raw materials will gradually emerge fromtheir current niches to become mainstream feedstocks.In the short term this will be in high-value low-volumeapplications. In the longer term substitution will extendto feedstocks for the commodity sector.

Rapid development in bioscience and biotechnology isopening up many new ways to provide novelfunctionality using low impact manufacturing andrenewable raw materials. This is already having a verysignificant impact on the pharmaceutical sector, andwill in the medium to long term have as great animpact on other sectors.

Nano-structures and nanotechnology are still at theresearch phase. In the medium to long term they willhave as much impact as biotechnology on the designand manufacture of chemical products.

Speed to market is already a strong driver. Rapidproduct development will deliver fast development of

niche products and very fast turnover of product ranges.

Collapsing costs of computing and communications arepowerful current drivers for the industry. Ubiquitouscomputing, deeply embedded computing and newnetworks will continue to drive new business models,

molecular and materials design, exploitation of the knowledge base, and value networks with many participants.

3.2 Technological Trends and Drivers

Vision: Industry is seen as a provider of solutions not as the problem

Collapsing cost ofcomputing and communications

New networks

Ubiquitous computing

Embedded computing

New business models

New materials design

The knowledge economyCo

mp

uti

ng

an

d

com

mu

nic

atio

ns

Vision

The pace of development

matches the changing environment.

No discontinuities

Fast development of niche products

A successful

and sustainable

chemical industry

19

�2004 roadmapgreen chemical technology3. Trends and Drivers continued

18

2003 2008 2013 2023+

Figure 3.3 // Economic Trends and Drivers

Long termHistory Short term Medium term

Effe

cts

chem

ical

sIn

telle

ctu

alp

rop

erty

Ch

ang

ing

b

usi

nes

s m

od

els

‘Res

po

nsi

ble

’m

anu

fact

uri

ng

Res

tru

ctu

re

Commodity manufacturing declines Commodity manufacturing vanishes from EU

UK focuses on ‘solutions’

Added value ingredients

Other sectors leave EU

Added value productionmoves off-shore

UK manufacturing declines

Knowledge intensive products

Shortage of skills Localised manufacture

Positive trade balance in licence fees Increasing revenue from licensing

Selling physical products

Selling services

Distributed manufactureInnovation and knowledge separate from manufacturing

Manufacture on demand

Green accounting Greener products and services

Demand for compliance with international standards

Globalisation

Commoditisation

Restructuring

Only ‘responsible’ manufacturers survive

Pharma companies get bigger

Specialties spin-out

Commodity companies get bigger Vertical integration disappears

Commodity over-capacity blocks green chemical technology

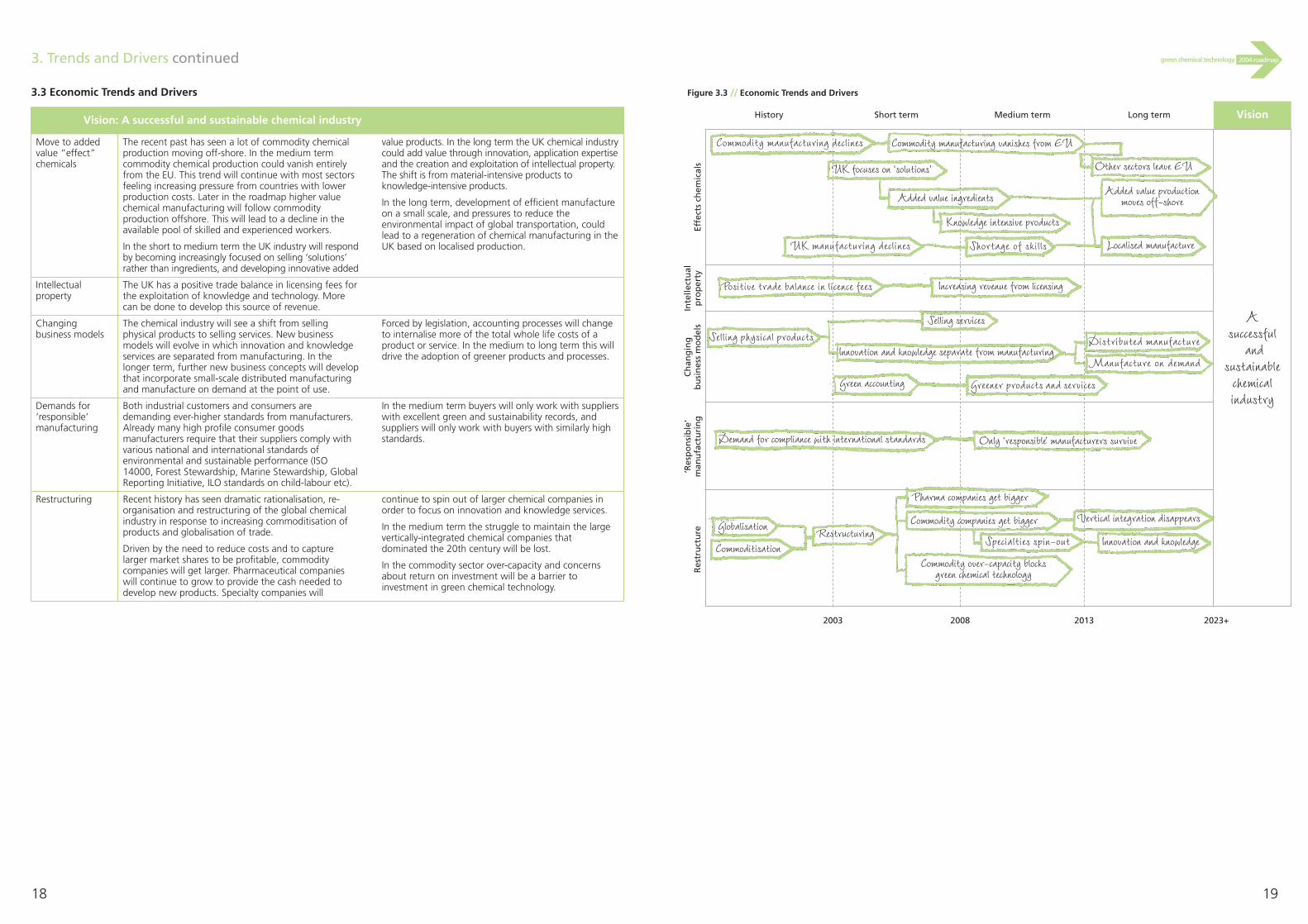

Move to addedvalue “effect”chemicals

Intellectualproperty

Changingbusiness models

Demands for‘responsible’manufacturing

Restructuring

The recent past has seen a lot of commodity chemicalproduction moving off-shore. In the medium termcommodity chemical production could vanish entirelyfrom the EU. This trend will continue with most sectorsfeeling increasing pressure from countries with lowerproduction costs. Later in the roadmap higher valuechemical manufacturing will follow commodityproduction offshore. This will lead to a decline in theavailable pool of skilled and experienced workers.

In the short to medium term the UK industry will respondby becoming increasingly focused on selling ‘solutions’rather than ingredients, and developing innovative added

value products. In the long term the UK chemical industrycould add value through innovation, application expertiseand the creation and exploitation of intellectual property.The shift is from material-intensive products toknowledge-intensive products.

In the long term, development of efficient manufactureon a small scale, and pressures to reduce theenvironmental impact of global transportation, couldlead to a regeneration of chemical manufacturing in theUK based on localised production.

The UK has a positive trade balance in licensing fees forthe exploitation of knowledge and technology. Morecan be done to develop this source of revenue.

The chemical industry will see a shift from sellingphysical products to selling services. New businessmodels will evolve in which innovation and knowledgeservices are separated from manufacturing. In thelonger term, further new business concepts will developthat incorporate small-scale distributed manufacturingand manufacture on demand at the point of use.

Forced by legislation, accounting processes will changeto internalise more of the total whole life costs of aproduct or service. In the medium to long term this willdrive the adoption of greener products and processes.

Both industrial customers and consumers aredemanding ever-higher standards from manufacturers.Already many high profile consumer goodsmanufacturers require that their suppliers comply withvarious national and international standards ofenvironmental and sustainable performance (ISO14000, Forest Stewardship, Marine Stewardship, GlobalReporting Initiative, ILO standards on child-labour etc).

In the medium term buyers will only work with supplierswith excellent green and sustainability records, andsuppliers will only work with buyers with similarly highstandards.

Recent history has seen dramatic rationalisation, re-organisation and restructuring of the global chemicalindustry in response to increasing commoditisation ofproducts and globalisation of trade.

Driven by the need to reduce costs and to capturelarger market shares to be profitable, commoditycompanies will get larger. Pharmaceutical companieswill continue to grow to provide the cash needed todevelop new products. Specialty companies will

continue to spin out of larger chemical companies inorder to focus on innovation and knowledge services.

In the medium term the struggle to maintain the largevertically-integrated chemical companies thatdominated the 20th century will be lost.

In the commodity sector over-capacity and concernsabout return on investment will be a barrier toinvestment in green chemical technology.

Innovation and knowledge

3.3 Economic Trends and Drivers

Vision: A successful and sustainable chemical industry Vision

21

�2004 roadmapgreen chemical technology

3. Trends and Drivers continued

20

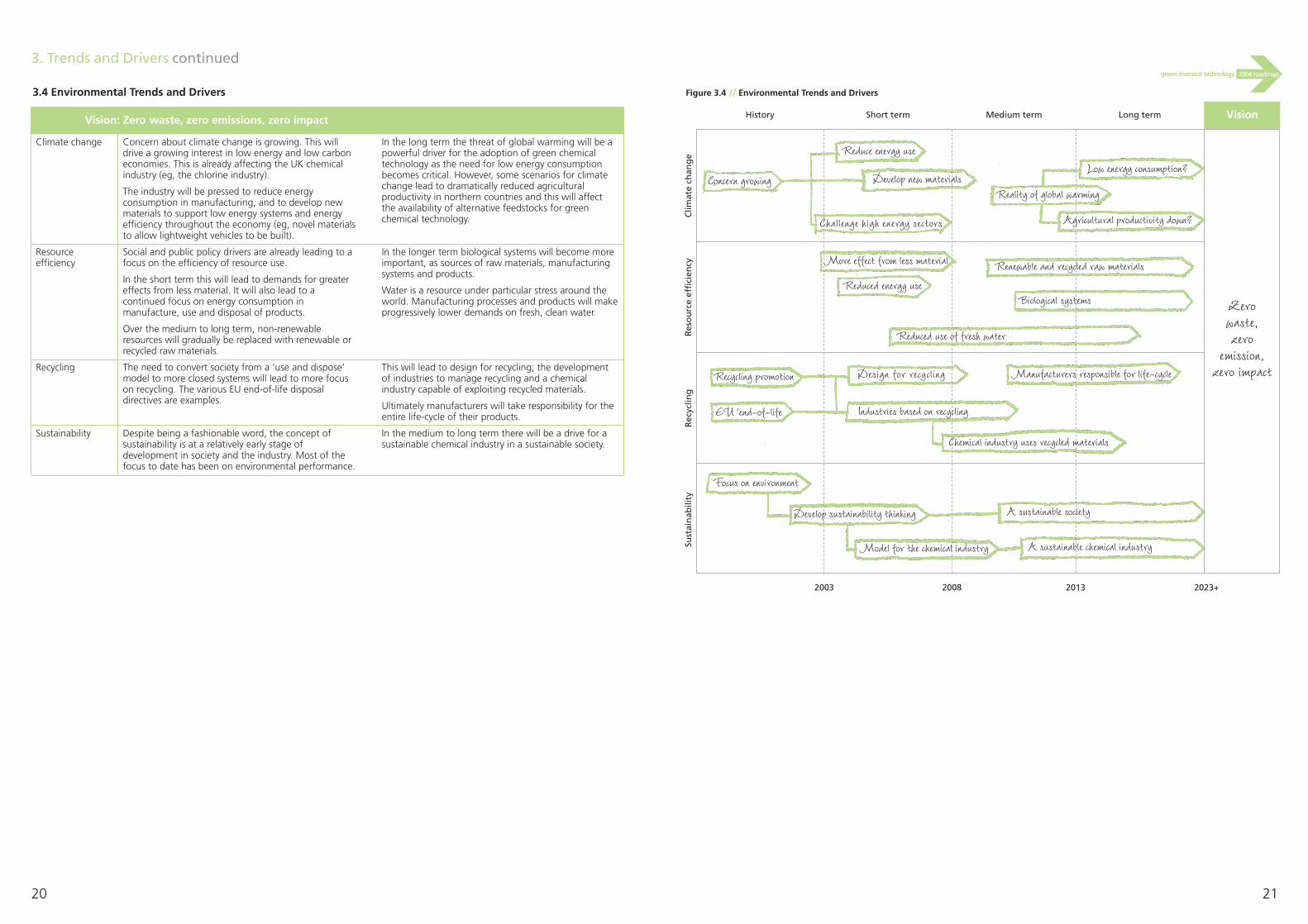

3.4 Environmental Trends and Drivers

Vision: Zero waste, zero emissions, zero impact

Figure 3.4 // Environmental Trends and Drivers

History Long termShort term Medium term

Concern growing

Reduce energy use

Develop new materials

Challenge high energy sectors

Reality of global warming

Low energy consumption?

Agricultural productivity down?

More effect from less material

Reduced energy use

Renewable and recycled raw materials

Reduced use of fresh water

Biological systems

Recycling promotion

EU ‘end-of-life

Design for recycling

Industries based on recycling

Chemical industry uses recycled materials

Manufacturers responsible for life-cycle

Focus on environment

Develop sustainability thinking

Model for the chemical industry

A sustainable society

A sustainable chemical industry

Rec

yclin

gSu

stai

nab

ility

Clim

ate

chan

ge

Res

ou

rce

effi

cien

cy

2003 2008 2013 2023+

Concern about climate change is growing. This willdrive a growing interest in low energy and low carboneconomies. This is already affecting the UK chemicalindustry (eg, the chlorine industry).

The industry will be pressed to reduce energyconsumption in manufacturing, and to develop newmaterials to support low energy systems and energyefficiency throughout the economy (eg, novel materialsto allow lightweight vehicles to be built).

In the long term the threat of global warming will be apowerful driver for the adoption of green chemicaltechnology as the need for low energy consumptionbecomes critical. However, some scenarios for climatechange lead to dramatically reduced agriculturalproductivity in northern countries and this will affectthe availability of alternative feedstocks for greenchemical technology.

Social and public policy drivers are already leading to afocus on the efficiency of resource use.

In the short term this will lead to demands for greatereffects from less material. It will also lead to acontinued focus on energy consumption inmanufacture, use and disposal of products.

Over the medium to long term, non-renewableresources will gradually be replaced with renewable orrecycled raw materials.

In the longer term biological systems will become moreimportant, as sources of raw materials, manufacturingsystems and products.

Water is a resource under particular stress around theworld. Manufacturing processes and products will makeprogressively lower demands on fresh, clean water.

The need to convert society from a ‘use and dispose’model to more closed systems will lead to more focuson recycling. The various EU end-of-life disposaldirectives are examples.

This will lead to design for recycling; the developmentof industries to manage recycling and a chemicalindustry capable of exploiting recycled materials.

Ultimately manufacturers will take responsibility for theentire life-cycle of their products.

Despite being a fashionable word, the concept ofsustainability is at a relatively early stage ofdevelopment in society and the industry. Most of thefocus to date has been on environmental performance.

In the medium to long term there will be a drive for asustainable chemical industry in a sustainable society.

Climate change

Resourceefficiency

Recycling

Sustainability

Zero waste,zero

emission,zero impact

Vision

Legislation

Globalisation ofenvironmentalstandards

The ‘knowledgeeconomy’

23

�2004 roadmapgreen chemical technology3. Trends and Drivers continued

22

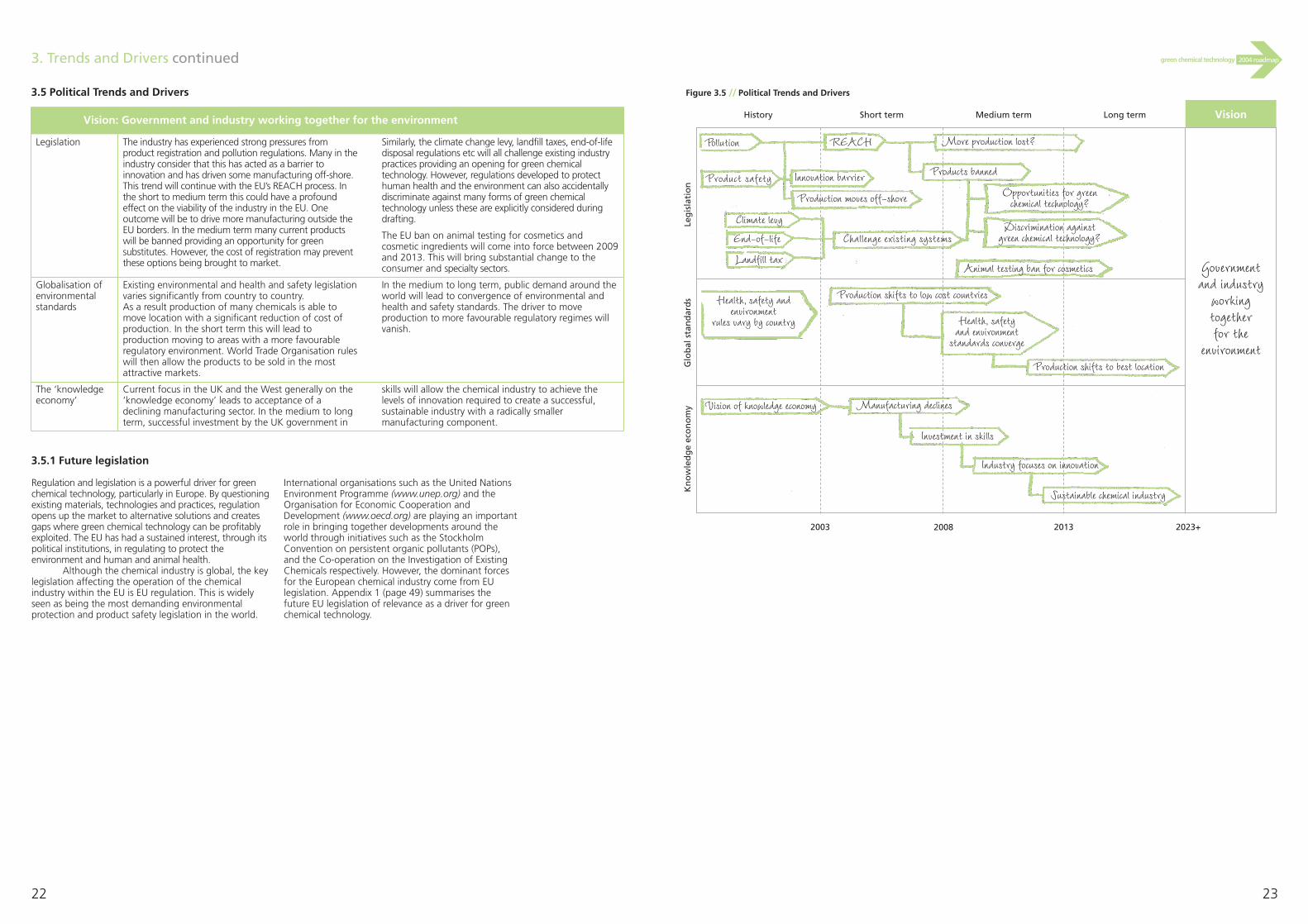

3.5 Political Trends and Drivers

Vision: Government and industry working together for the environment

Figure 3.5 // Political Trends and Drivers

History Long termShort term Medium term

Leg

isla

tio

nG

lob

al s

tan

dar

ds

Kn

ow

led

ge

eco

no

my

Pollution

Product safety

REACH

Innovation barrier

Production moves off-shore

More production lost?

Products banned

Climate levy

End-of-life

Landfill tax

Challenge existing systems

Opportunities for greenchemical technology?

Discrimination againstgreen chemical technology?

Animal testing ban for cosmetics

Health, safety andenvironment

rules vary by country

Production shifts to low cost countries

Health, safety and environment

standards converge

Production shifts to best location

Vision of knowledge economy Manufacturing declines

Investment in skills

Industry focuses on innovation

2003 2008 2013 2023+

Sustainable chemical industry

The industry has experienced strong pressures fromproduct registration and pollution regulations. Many in theindustry consider that this has acted as a barrier toinnovation and has driven some manufacturing off-shore.This trend will continue with the EU’s REACH process. Inthe short to medium term this could have a profoundeffect on the viability of the industry in the EU. Oneoutcome will be to drive more manufacturing outside theEU borders. In the medium term many current productswill be banned providing an opportunity for greensubstitutes. However, the cost of registration may preventthese options being brought to market.

Similarly, the climate change levy, landfill taxes, end-of-lifedisposal regulations etc will all challenge existing industrypractices providing an opening for green chemicaltechnology. However, regulations developed to protecthuman health and the environment can also accidentallydiscriminate against many forms of green chemicaltechnology unless these are explicitly considered duringdrafting.

The EU ban on animal testing for cosmetics andcosmetic ingredients will come into force between 2009and 2013. This will bring substantial change to theconsumer and specialty sectors.

Existing environmental and health and safety legislationvaries significantly from country to country.As a result production of many chemicals is able tomove location with a significant reduction of cost ofproduction. In the short term this will lead toproduction moving to areas with a more favourableregulatory environment. World Trade Organisation ruleswill then allow the products to be sold in the mostattractive markets.

In the medium to long term, public demand around theworld will lead to convergence of environmental andhealth and safety standards. The driver to moveproduction to more favourable regulatory regimes willvanish.

Current focus in the UK and the West generally on the‘knowledge economy’ leads to acceptance of adeclining manufacturing sector. In the medium to longterm, successful investment by the UK government in

skills will allow the chemical industry to achieve thelevels of innovation required to create a successful,sustainable industry with a radically smallermanufacturing component.

Regulation and legislation is a powerful driver for greenchemical technology, particularly in Europe. By questioningexisting materials, technologies and practices, regulationopens up the market to alternative solutions and createsgaps where green chemical technology can be profitablyexploited. The EU has had a sustained interest, through itspolitical institutions, in regulating to protect theenvironment and human and animal health.

Although the chemical industry is global, the keylegislation affecting the operation of the chemicalindustry within the EU is EU regulation. This is widelyseen as being the most demanding environmentalprotection and product safety legislation in the world.

International organisations such as the United NationsEnvironment Programme (www.unep.org) and theOrganisation for Economic Cooperation andDevelopment (www.oecd.org) are playing an importantrole in bringing together developments around theworld through initiatives such as the StockholmConvention on persistent organic pollutants (POPs),and the Co-operation on the Investigation of ExistingChemicals respectively. However, the dominant forcesfor the European chemical industry come from EUlegislation. Appendix 1 (page 49) summarises thefuture EU legislation of relevance as a driver for greenchemical technology.

3.5.1 Future legislation

Government and industry

working together for the

environment

Vision

4. Features, Attributes and Technology Impact

24

New therapies

Manufacturing

Information technology

25

�2004 roadmapgreen chemical technology

In this section the specific sustainability goals inresponse to the trends and drivers are described for each of the four sectors in the chemical industry.These are coupled with the features and attributes inproducts, services and manufacturing processes requiredto meet the sector goals.

4.1. Features and Attributes by Sector

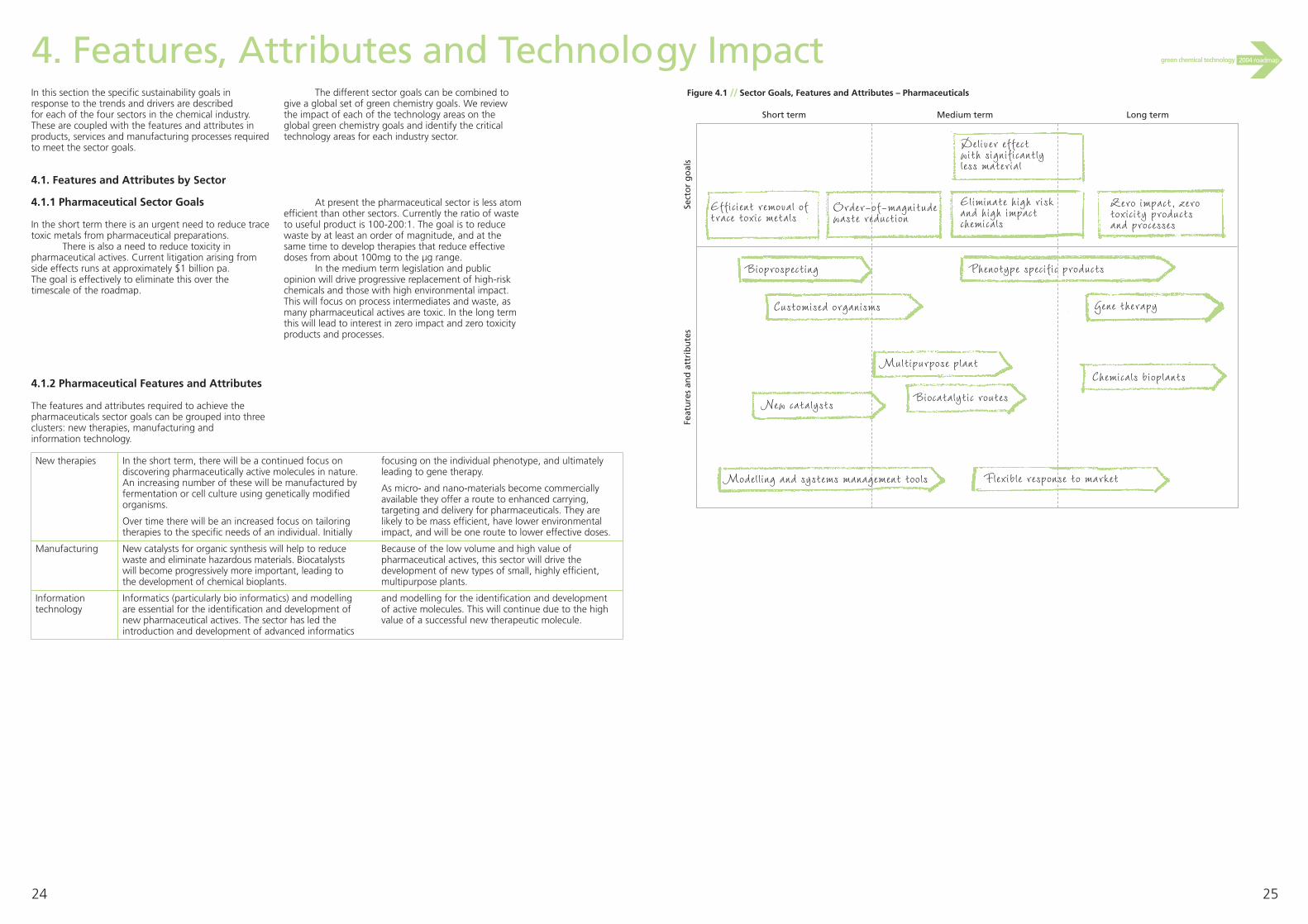

4.1.1 Pharmaceutical Sector Goals

In the short term there is an urgent need to reduce tracetoxic metals from pharmaceutical preparations.

There is also a need to reduce toxicity inpharmaceutical actives. Current litigation arising fromside effects runs at approximately $1 billion pa. The goal is effectively to eliminate this over thetimescale of the roadmap.

Figure 4.1 // Sector Goals, Features and Attributes – Pharmaceuticals

Long termShort term Medium term

Sect

or

go

als

Feat

ure

s an

d a

ttri

bu

tes

Efficient removal oftrace toxic metals

Order-of-magnitudewaste reduction

Deliver effect with significantly less material

Eliminate high riskand high impactchemicals

Zero impact, zerotoxicity productsand processes

Bioprospecting

Gene therapy

Phenotype specific products

Customised organisms

New catalysts

Multipurpose plant

Biocatalytic routes

Chemicals bioplants

In the short term, there will be a continued focus ondiscovering pharmaceutically active molecules in nature.An increasing number of these will be manufactured byfermentation or cell culture using genetically modifiedorganisms.

Over time there will be an increased focus on tailoringtherapies to the specific needs of an individual. Initially

focusing on the individual phenotype, and ultimatelyleading to gene therapy.

As micro- and nano-materials become commerciallyavailable they offer a route to enhanced carrying,targeting and delivery for pharmaceuticals. They arelikely to be mass efficient, have lower environmentalimpact, and will be one route to lower effective doses.

New catalysts for organic synthesis will help to reducewaste and eliminate hazardous materials. Biocatalystswill become progressively more important, leading tothe development of chemical bioplants.

Because of the low volume and high value ofpharmaceutical actives, this sector will drive thedevelopment of new types of small, highly efficient,multipurpose plants.

Informatics (particularly bio informatics) and modellingare essential for the identification and development ofnew pharmaceutical actives. The sector has led theintroduction and development of advanced informatics

and modelling for the identification and developmentof active molecules. This will continue due to the highvalue of a successful new therapeutic molecule.

Modelling and systems management tools Flexible response to market

4.1.2 Pharmaceutical Features and Attributes

The features and attributes required to achieve thepharmaceuticals sector goals can be grouped into threeclusters: new therapies, manufacturing and information technology.

The different sector goals can be combined togive a global set of green chemistry goals. We reviewthe impact of each of the technology areas on theglobal green chemistry goals and identify the criticaltechnology areas for each industry sector.

At present the pharmaceutical sector is less atomefficient than other sectors. Currently the ratio of wasteto useful product is 100-200:1. The goal is to reducewaste by at least an order of magnitude, and at thesame time to develop therapies that reduce effectivedoses from about 100mg to the µg range.

In the medium term legislation and publicopinion will drive progressive replacement of high-riskchemicals and those with high environmental impact.This will focus on process intermediates and waste, asmany pharmaceutical actives are toxic. In the long termthis will lead to interest in zero impact and zero toxicityproducts and processes.

4. Features, Attributes and Technology Impact continued

26 27

�2004 roadmapgreen chemical technology

Figure 4.2 // Sector Goals, Features and Attributes – Consumer

Novel functionality

Effectthroughstructure

Products for a healthy life

Eliminate high riskand high impactchemicals

Bio-derived materials

Zero impact,zero toxicity products and processes

Renewablefeedstocks

Nano-materials and composites

Tailored and efficient ingredients

Phenotype specific products

Biodegradable and non-toxic materials

Modelling and systems management tools

Biocatalytic routes Chemicals bioplants

Flexible response to market

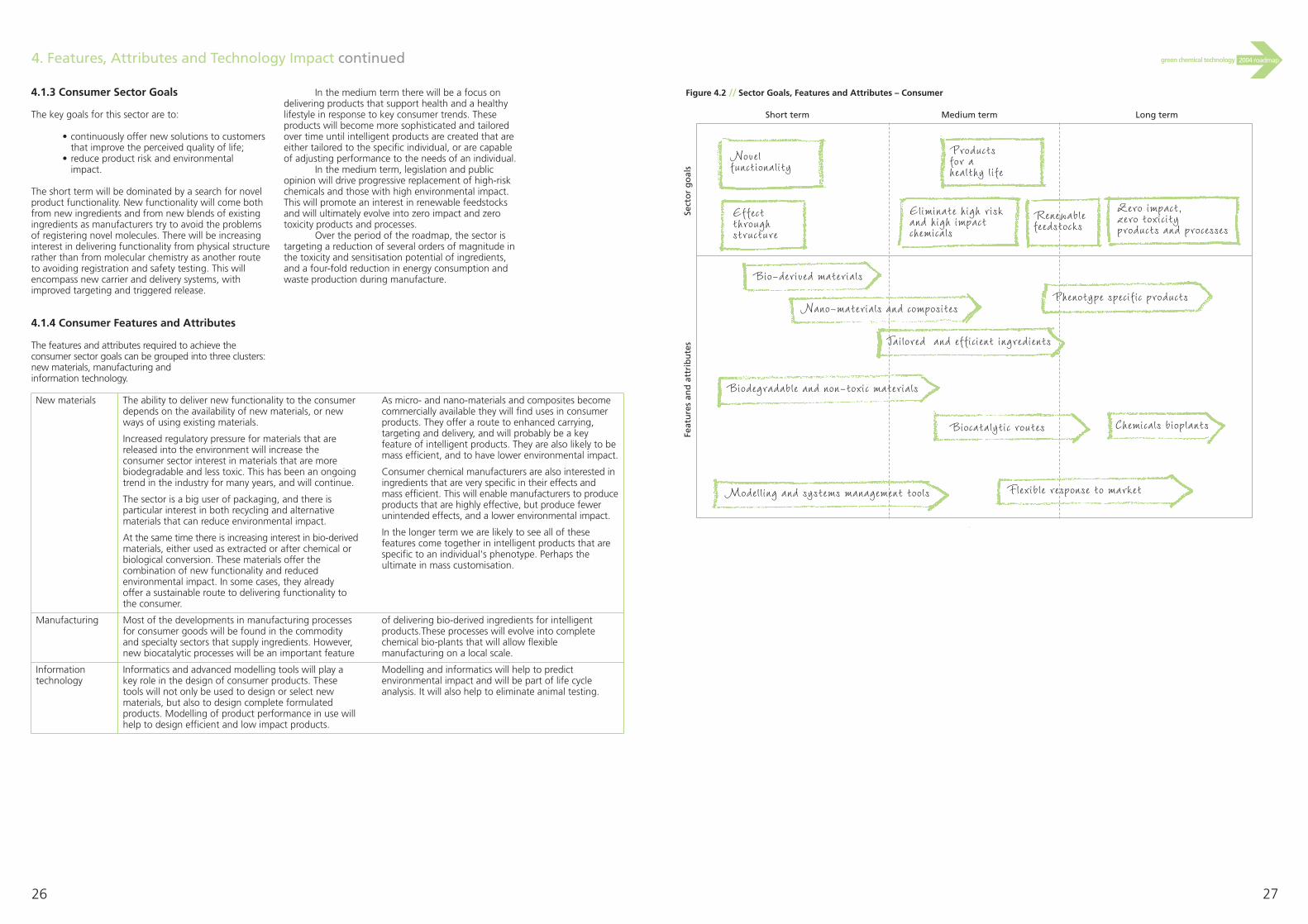

4.1.3 Consumer Sector Goals

The key goals for this sector are to:

• continuously offer new solutions to customers that improve the perceived quality of life;

• reduce product risk and environmental impact.

The short term will be dominated by a search for novelproduct functionality. New functionality will come bothfrom new ingredients and from new blends of existingingredients as manufacturers try to avoid the problemsof registering novel molecules. There will be increasinginterest in delivering functionality from physical structurerather than from molecular chemistry as another routeto avoiding registration and safety testing. This willencompass new carrier and delivery systems, withimproved targeting and triggered release.

In the medium term there will be a focus ondelivering products that support health and a healthylifestyle in response to key consumer trends. Theseproducts will become more sophisticated and tailoredover time until intelligent products are created that areeither tailored to the specific individual, or are capableof adjusting performance to the needs of an individual.

In the medium term, legislation and publicopinion will drive progressive replacement of high-riskchemicals and those with high environmental impact.This will promote an interest in renewable feedstocksand will ultimately evolve into zero impact and zerotoxicity products and processes.

Over the period of the roadmap, the sector istargeting a reduction of several orders of magnitude inthe toxicity and sensitisation potential of ingredients,and a four-fold reduction in energy consumption andwaste production during manufacture.

New materials

Manufacturing

Informationtechnology

The ability to deliver new functionality to the consumerdepends on the availability of new materials, or newways of using existing materials.

Increased regulatory pressure for materials that arereleased into the environment will increase theconsumer sector interest in materials that are morebiodegradable and less toxic. This has been an ongoingtrend in the industry for many years, and will continue.

The sector is a big user of packaging, and there isparticular interest in both recycling and alternativematerials that can reduce environmental impact.

At the same time there is increasing interest in bio-derivedmaterials, either used as extracted or after chemical orbiological conversion. These materials offer thecombination of new functionality and reducedenvironmental impact. In some cases, they already offer a sustainable route to delivering functionality tothe consumer.

As micro- and nano-materials and composites becomecommercially available they will find uses in consumerproducts. They offer a route to enhanced carrying,targeting and delivery, and will probably be a keyfeature of intelligent products. They are also likely to bemass efficient, and to have lower environmental impact.

Consumer chemical manufacturers are also interested iningredients that are very specific in their effects andmass efficient. This will enable manufacturers to produceproducts that are highly effective, but produce fewerunintended effects, and a lower environmental impact.

In the longer term we are likely to see all of thesefeatures come together in intelligent products that arespecific to an individual's phenotype. Perhaps theultimate in mass customisation.

Most of the developments in manufacturing processesfor consumer goods will be found in the commodityand specialty sectors that supply ingredients. However,new biocatalytic processes will be an important feature

of delivering bio-derived ingredients for intelligentproducts.These processes will evolve into completechemical bio-plants that will allow flexiblemanufacturing on a local scale.

Informatics and advanced modelling tools will play akey role in the design of consumer products. Thesetools will not only be used to design or select newmaterials, but also to design complete formulatedproducts. Modelling of product performance in use willhelp to design efficient and low impact products.

Modelling and informatics will help to predictenvironmental impact and will be part of life cycleanalysis. It will also help to eliminate animal testing.

4.1.4 Consumer Features and Attributes

The features and attributes required to achieve theconsumer sector goals can be grouped into three clusters: new materials, manufacturing and information technology.

Long termShort term Medium term

Sect

or

go

als

Feat

ure

s an

d a

ttri

bu

tes

4. Features, Attributes and Technology Impact continued

28 29

�2004 roadmapgreen chemical technology

Figure 4.3 // Sector Goals, Features and Attributes – Specialties

Effectthroughstructure

Eliminate high risk and highimpact chemicals

Deliver effect with significantly less material

Zero impact,zero toxicity products and processes

Bio-derived materials

Nano-materials and composites

Tailored and efficient ingredients

Biodegradable and non-toxic materials

Customised organisms

Integrated processes

New catalysts

Modelling and systems management tools

Inherently safe processes

Biocatalytic routes

Multipurpose plant One pot synthesis for multistep reactions

Thermodynamic minimum

Chemicals bioplants

Flexible response to market

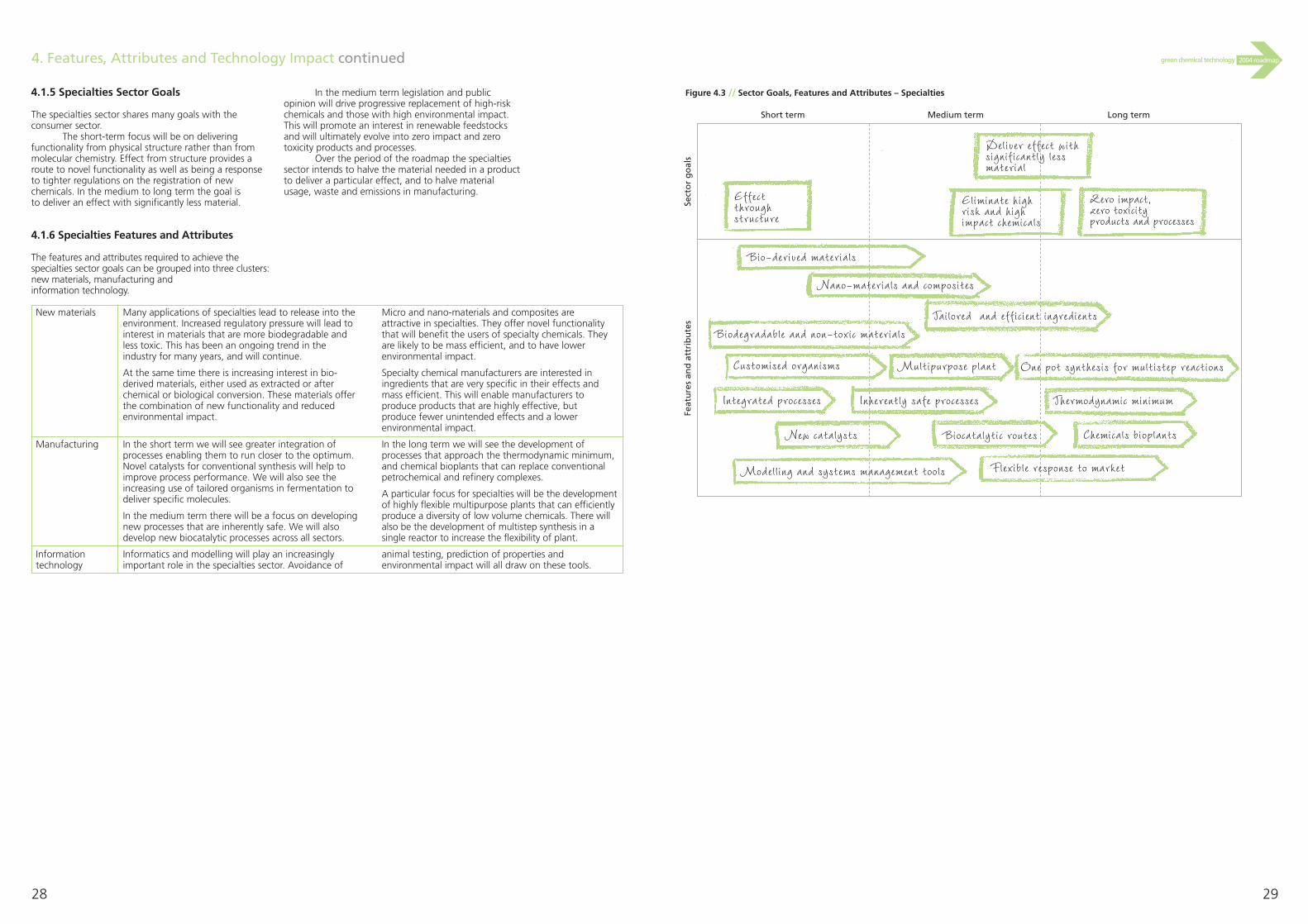

4.1.5 Specialties Sector Goals

The specialties sector shares many goals with theconsumer sector.

The short-term focus will be on deliveringfunctionality from physical structure rather than frommolecular chemistry. Effect from structure provides aroute to novel functionality as well as being a responseto tighter regulations on the registration of newchemicals. In the medium to long term the goal is to deliver an effect with significantly less material.

In the medium term legislation and publicopinion will drive progressive replacement of high-riskchemicals and those with high environmental impact.This will promote an interest in renewable feedstocksand will ultimately evolve into zero impact and zerotoxicity products and processes.

Over the period of the roadmap the specialtiessector intends to halve the material needed in a productto deliver a particular effect, and to halve materialusage, waste and emissions in manufacturing.

4.1.6 Specialties Features and Attributes

The features and attributes required to achieve thespecialties sector goals can be grouped into three clusters: new materials, manufacturing and information technology.

Many applications of specialties lead to release into theenvironment. Increased regulatory pressure will lead tointerest in materials that are more biodegradable andless toxic. This has been an ongoing trend in theindustry for many years, and will continue.

At the same time there is increasing interest in bio-derived materials, either used as extracted or afterchemical or biological conversion. These materials offerthe combination of new functionality and reducedenvironmental impact.

Micro and nano-materials and composites are attractive in specialties. They offer novel functionalitythat will benefit the users of specialty chemicals. Theyare likely to be mass efficient, and to have lowerenvironmental impact.

Specialty chemical manufacturers are interested iningredients that are very specific in their effects andmass efficient. This will enable manufacturers toproduce products that are highly effective, but produce fewer unintended effects and a lowerenvironmental impact.

In the short term we will see greater integration ofprocesses enabling them to run closer to the optimum.Novel catalysts for conventional synthesis will help toimprove process performance. We will also see theincreasing use of tailored organisms in fermentation todeliver specific molecules.

In the medium term there will be a focus on developingnew processes that are inherently safe. We will alsodevelop new biocatalytic processes across all sectors.

In the long term we will see the development ofprocesses that approach the thermodynamic minimum,and chemical bioplants that can replace conventionalpetrochemical and refinery complexes.

A particular focus for specialties will be the developmentof highly flexible multipurpose plants that can efficientlyproduce a diversity of low volume chemicals. There willalso be the development of multistep synthesis in asingle reactor to increase the flexibility of plant.

Informatics and modelling will play an increasinglyimportant role in the specialties sector. Avoidance of

animal testing, prediction of properties andenvironmental impact will all draw on these tools.

New materials

Manufacturing

Informationtechnology

Long termShort term Medium term

Sect

or

go

als

Feat

ure

s an

d a

ttri

bu

tes

4. Features, Attributes and Technology Impact continued

30

Recycling

Packaging

Process improvement

Information technology

31

�2004 roadmapgreen chemical technology

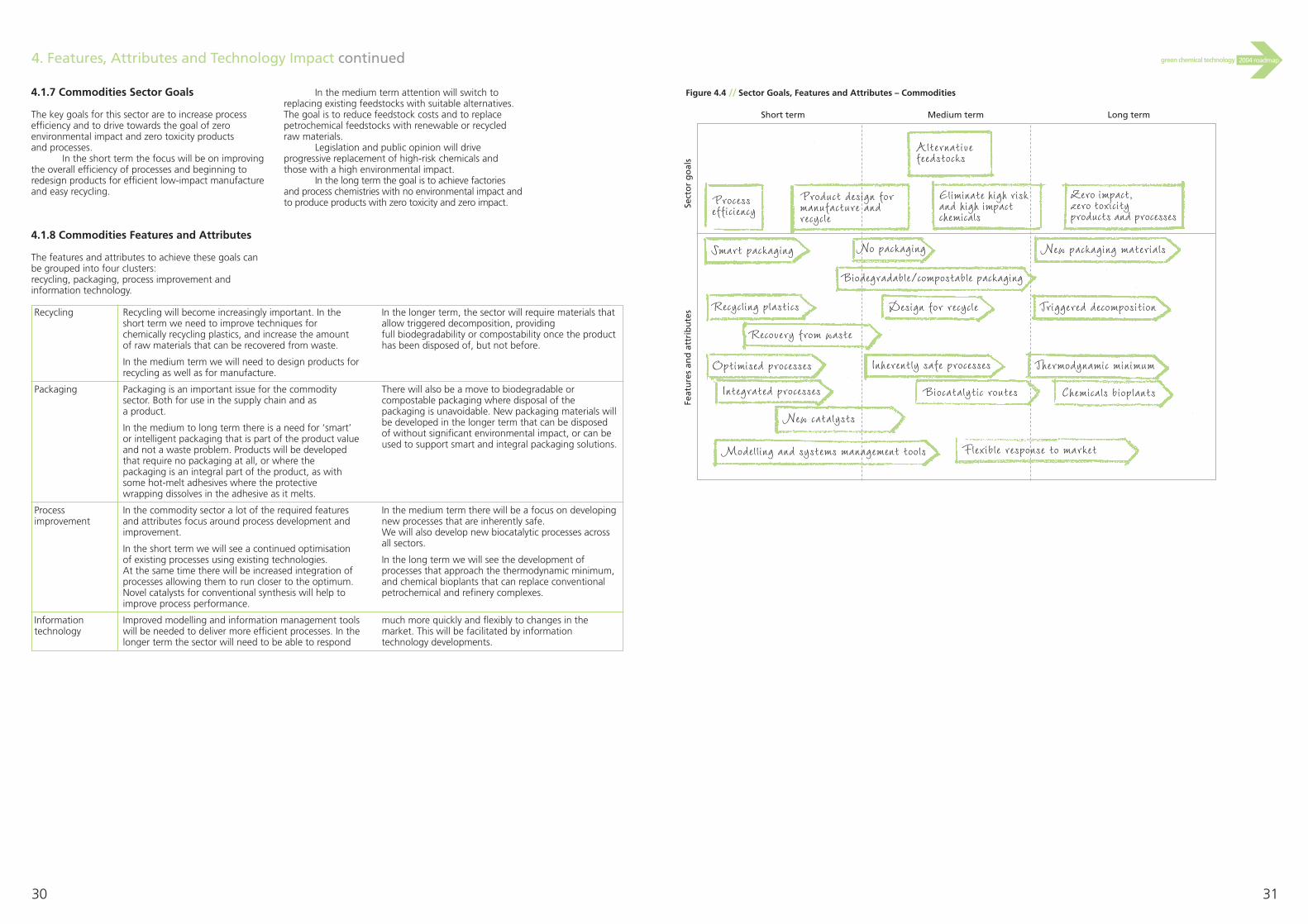

4.1.7 Commodities Sector Goals

The key goals for this sector are to increase processefficiency and to drive towards the goal of zeroenvironmental impact and zero toxicity products and processes.

In the short term the focus will be on improvingthe overall efficiency of processes and beginning toredesign products for efficient low-impact manufactureand easy recycling.

In the medium term attention will switch toreplacing existing feedstocks with suitable alternatives. The goal is to reduce feedstock costs and to replacepetrochemical feedstocks with renewable or recycledraw materials.

Legislation and public opinion will driveprogressive replacement of high-risk chemicals andthose with a high environmental impact.

In the long term the goal is to achieve factoriesand process chemistries with no environmental impact andto produce products with zero toxicity and zero impact.

4.1.8 Commodities Features and Attributes

The features and attributes to achieve these goals canbe grouped into four clusters: recycling, packaging, process improvement andinformation technology.

Figure 4.4 // Sector Goals, Features and Attributes – Commodities

Alternativefeedstocks

Processefficiency

Product design for manufacture andrecycle

Eliminate high riskand high impactchemicals

Zero impact,zero toxicity products and processes

Smart packaging

Recycling plastics

No packaging

Biodegradable/compostable packaging

New packaging materials

Recovery from waste

Design for recycle Triggered decomposition

Optimised processes

Integrated processes

Inherently safe processes

Biocatalytic routes

New catalysts

Thermodynamic minimum

Chemicals bioplants

Modelling and systems management tools Flexible response to market

Recycling will become increasingly important. In theshort term we need to improve techniques forchemically recycling plastics, and increase the amountof raw materials that can be recovered from waste.

In the medium term we will need to design products forrecycling as well as for manufacture.

In the longer term, the sector will require materials thatallow triggered decomposition, providing full biodegradability or compostability once the producthas been disposed of, but not before.

Packaging is an important issue for the commoditysector. Both for use in the supply chain and as a product.

In the medium to long term there is a need for ‘smart’or intelligent packaging that is part of the product valueand not a waste problem. Products will be developedthat require no packaging at all, or where thepackaging is an integral part of the product, as withsome hot-melt adhesives where the protectivewrapping dissolves in the adhesive as it melts.

There will also be a move to biodegradable orcompostable packaging where disposal of thepackaging is unavoidable. New packaging materials willbe developed in the longer term that can be disposedof without significant environmental impact, or can beused to support smart and integral packaging solutions.

In the commodity sector a lot of the required featuresand attributes focus around process development andimprovement.

In the short term we will see a continued optimisationof existing processes using existing technologies. At the same time there will be increased integration ofprocesses allowing them to run closer to the optimum.Novel catalysts for conventional synthesis will help toimprove process performance.

In the medium term there will be a focus on developingnew processes that are inherently safe. We will also develop new biocatalytic processes acrossall sectors.

In the long term we will see the development ofprocesses that approach the thermodynamic minimum,and chemical bioplants that can replace conventionalpetrochemical and refinery complexes.

Improved modelling and information management toolswill be needed to deliver more efficient processes. In thelonger term the sector will need to be able to respond

much more quickly and flexibly to changes in themarket. This will be facilitated by informationtechnology developments.

Long termShort term Medium term

Sect

or

go

als

Feat

ure

s an

d a

ttri

bu

tes

4. Features, Attributes and Technology Impact continued

32 33

�2004 roadmapgreen chemical technology

4.2 Grouping of Sector Goals

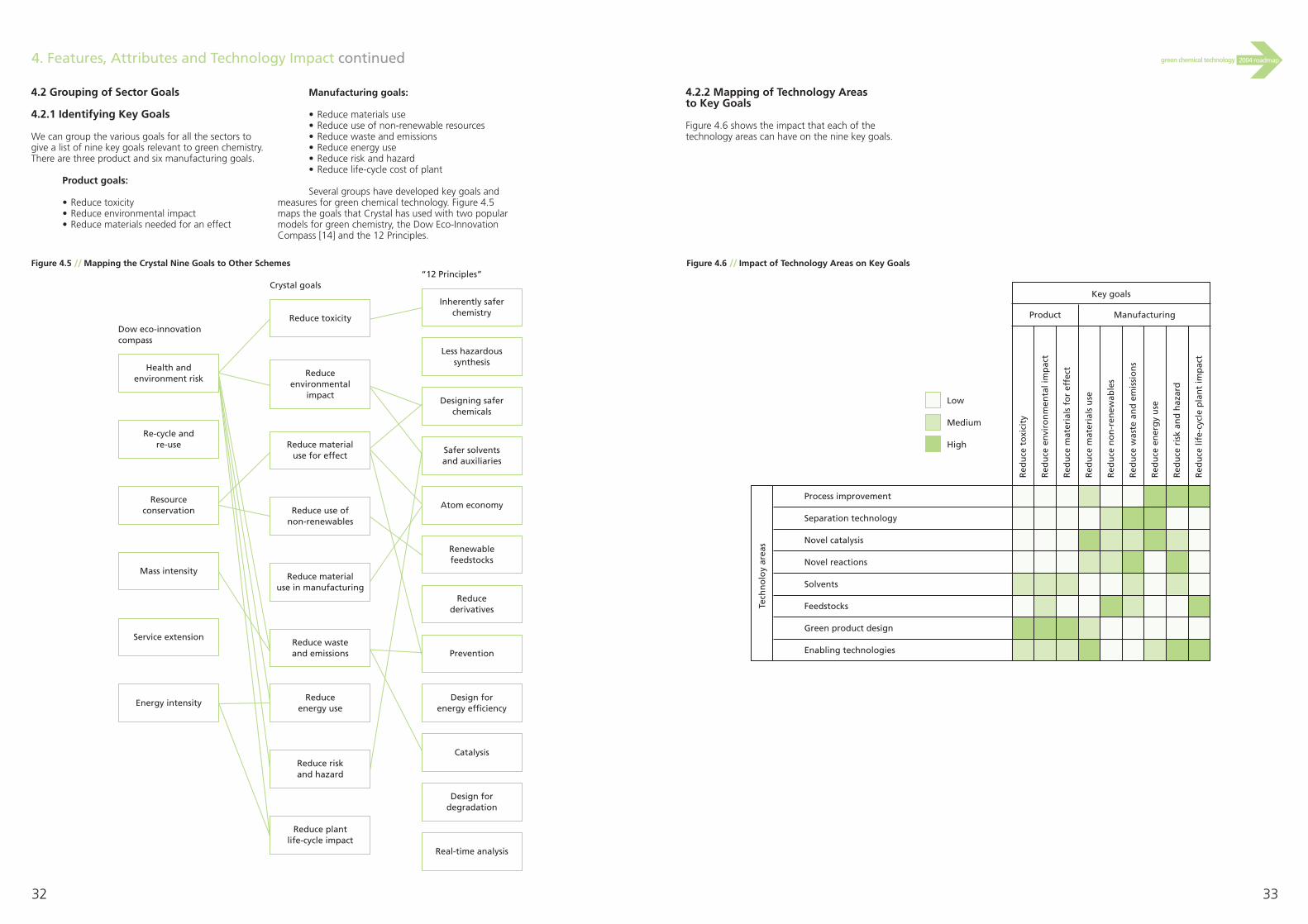

4.2.1 Identifying Key Goals

We can group the various goals for all the sectors togive a list of nine key goals relevant to green chemistry.There are three product and six manufacturing goals.

Product goals:

• Reduce toxicity• Reduce environmental impact• Reduce materials needed for an effect

Manufacturing goals:

• Reduce materials use• Reduce use of non-renewable resources• Reduce waste and emissions• Reduce energy use• Reduce risk and hazard• Reduce life-cycle cost of plant

Several groups have developed key goals andmeasures for green chemical technology. Figure 4.5maps the goals that Crystal has used with two popularmodels for green chemistry, the Dow Eco-InnovationCompass [14] and the 12 Principles.

4.2.2 Mapping of Technology Areas to Key Goals

Figure 4.6 shows the impact that each of thetechnology areas can have on the nine key goals.

Figure 4.5 // Mapping the Crystal Nine Goals to Other Schemes Figure 4.6 // Impact of Technology Areas on Key Goals

Dow eco-innovationcompass

Crystal goals“12 Principles”

Health andenvironment risk

Re-cycle andre-use

Resourceconservation

Service extension

Energy intensity

Reduce toxicity

Reduceenvironmental

impact

Reduce materialuse for effect

Reduce use ofnon-renewables

Reduce material use in manufacturing

Reduce wasteand emissions

Reduceenergy use

Reduce riskand hazard