gb 2015 engl - raiffeisen bankengruppe · 2020-05-19 · raiffeisen landesbank oberösterreich...

TRANSCRIPT

Raiffeisen LandesbankOberösterreich

www.rlbooe.at

Raiffeisen LandesbankOberösterreich

www.rlbooe.at

Annual Report 2015Europaplatz 1a, 4020 LinzTel. +43 (0) 732/6596-0Fax +43 (0) 732/6596-22739E-Mail: [email protected]

Annu

al R

epor

t 201

5

The foundation for a successful future.

Annual Report 2015

2 Annual Report 2015

3Raiffeisen Banking Group Upper Austria Raiffeisenlandesbank Oberösterreich Group General information

Contents

General information

Foreword by Heinrich Schaller _____________________________________________________________________________ 5The Managing Board of Raiffeisenlandesbank Oberösterreich Aktiengesellschaft _________________________________ 8Foreword by Jakob Auer __________________________________________________________________________________ 10The Supervisory Board of Raiffeisenlandesbank Oberösterreich Aktiengesellschaft ________________________________ 122015 in retrospect ________________________________________________________________________________________ 26Sustainability management and corporate social responsibility _________________________________________________ 28

Raiffeisenlandesbank Oberösterreich Aktiengesellschaft Group

Group management report ________________________________________________________________________________ 44IFRS consolidated financial statements 2015 _________________________________________________________________ 62

Raiffeisenlandesbank Oberösterreich Aktiengesellschaft

Management Report 2015 of Raiffeisenlandesbank Oberösterreich Aktiengesellschaft ____________________________ 164Annual financial statements 2015 of Raiffeisenlandesbank Oberösterreich Aktiengesellschaft _______________________ 184

Statement of the Managing Board ____________________________________________________________ 206

Report of the Supervisory Board _____________________________________________________________ 207

Raiffeisen Banking Group Upper Austria

Results 2015 (consolidated)________________________________________________________________________________ 208

Glossary _______________________________________________________________________________________________ 213Imprint _________________________________________________________________________________________________ 214

4 Annual Report 2015

General information

Foreword by Heinrich Schaller __________________________________________ 5

The Managing Board of Raiffeisenlandesbank Oberösterreich Aktiengesellschaft 8

Foreword by Jakob Auer _______________________________________________ 10

The Supervisory Board of Raiffeisenlandesbank Oberösterreich Aktiengesellschaft ___________________________________________________ 12

2015 in retrospect ____________________________________________________ 26

Sustainability management and corporate social responsibility _______________ 28

5Raiffeisen Banking Group Upper Austria Raiffeisenlandesbank Oberösterreich Group General information

Foreword by Heinrich Schaller

Successful strategy for strengths and customer focus

Developing through our own strengths

Raiffeisenlandesbank Oberösterreich uses its capacity for change to benefit its customers. A series of strategic mea-sures that have been introduced and implemented since 2012 have shown encouraging results. In particular, they provide a solid foundation for consistent growth in future. Raiffeisen-landesbank Oberösterreich develops these through its own internal strengths and not through external capital increases.

Outperforming our high standards

The European Central Bank (ECB) sets particularly high stan-dards for the leading banks in Europe. In addition to the reg-ulatory capital requirements, these institutions are bound to comply with a SREP ratio and from 2016 they will also be sub-ject to an additional national capital buffer. As the fourth-larg-est bank in Austria, Raiffeisenlandesbank Oberösterreich wants to exceed every high standard placed on it by the Euro-pean Union as a “significant” bank. This will be done in main-taining the overall high quality of service provision.

Creative force through a strong capital position

As a ECB-audited bank with a strong capital position, Raif-feisenlandesbank Oberösterreich is a reliable, safe and strong partner for its customers. A further objective is to continue to increase efficiency and results in order to take our customer focus to the next level and develop and maintain a solid foun-dation for our existing strong independence.

Raiffeisen Oberösterreich and cooperation

Through working together with the Raiffeisen banks in Upper Austria, the Raiffeisenlandesbank Oberösterreich emphasises cooperation instead of consolidation. The new ways of co-operating are already showing excellent results. The aim of this cooperation is to produce efficiency savings in the various departments that should form the basis of Raiffeisen Oberös-terreich maintaining or strengthening its position as a clear market leader.

Constantly working on efficiency savings

Raiffeisenlandesbank Oberösterreich has also put in place a number of measures over the past year aimed at continuously increasing efficiency. For example, in 2015, PRIVAT BANK and bankdirekt.at were integrated into Raiffeisenlandesbank Oberösterreich and since then have been managed as their own business areas. This way, it is possible to avoid unnec-essary duplication while maintaining high levels of service. Working on improving efforts, organisation and processes is not a one-off at Raiffeisenlandesbank Oberösterreich but a constant.

Further strengthening Tier 1 capital ratio

Sustainable customer relationships and responsible handling of resources helped produce excellent annual results for Raif-feisenlandesbank Oberösterreich in 2015. As was the case in previous years, operational business development remained positive and stable.

6 Annual Report 2015

Raiffeisenlandesbank Oberösterreich proved itself to be strong, resilient and healthy during the bank check of the most important financial institutions in the euro zone. It is committed to showing its strength and stability in the future, meeting the highest international standards and, in particular, intensively supporting and advising clients.

Heinrich Schaller

7Raiffeisen Banking Group Upper Austria Raiffeisenlandesbank Oberösterreich Group General information

The key results in 2015 in summary

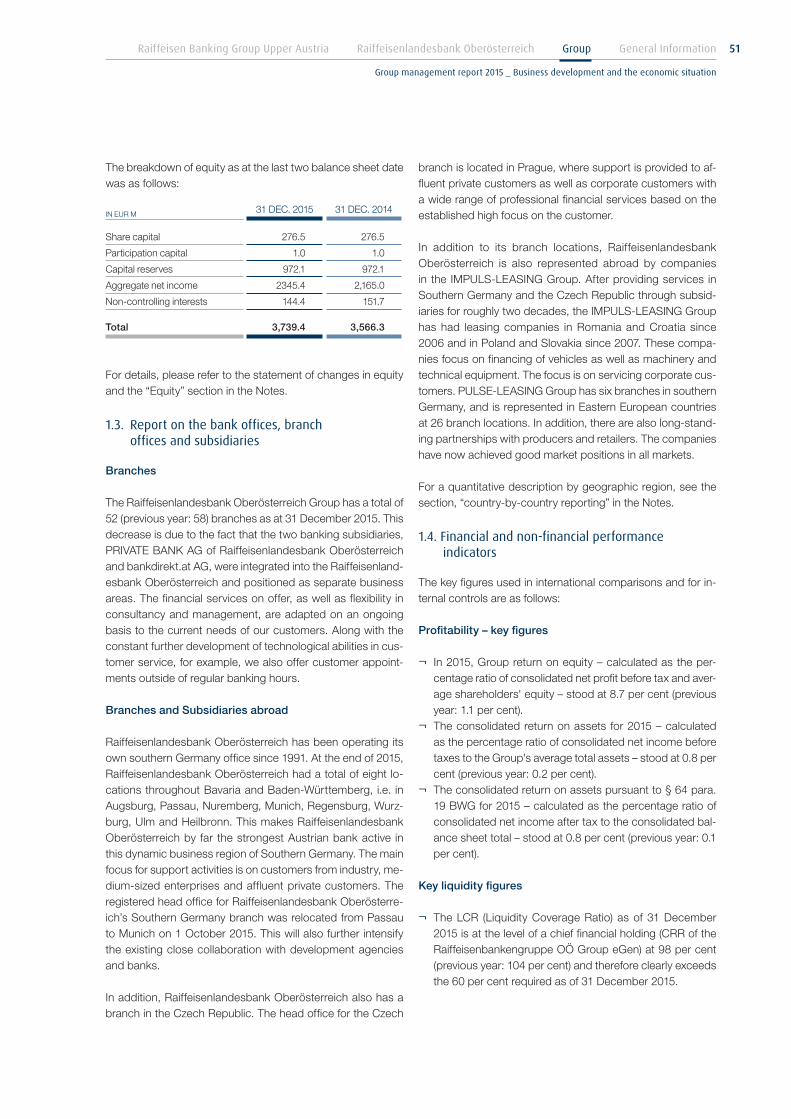

The Group's Tier 1 capital ratio increased to 13.8 per cent (+ 2.6 percentage points)Raiffeisenlandesbank Oberösterreich significantly improved its equity capital base in 2015.

¬ In the regulatory-relevant CRR group (banking group), we achieved a CET1 ratio (Common Equity Tier 1 = core Tier 1 capital) of 13.8 per cent (+ 2.6 percentage points) with Tier 1 capital of EUR 3.2 billion.

¬ In terms of the Austrian Commercial Code, Raiffeisenlandes- bank Oberösterreich had, with Tier 1 capital of EUR 2.6 billion, a CET1 ratio of 12.9 per cent. This represents an increase of 1.3%.

¬ As such, both Raiffeisenlandesbank Oberösterreich AG, in accordance with the Austrian Commercial Code, as well as CRR (banking group), in accordance with IFRS, were clearly over the 8.5 per cent Tier 1 capital ratios required starting in 2019 under Basel III capital requirements. They were also clearly over the ratio calculated using the required SREP ratio and the additional capital buffer (from 2016).

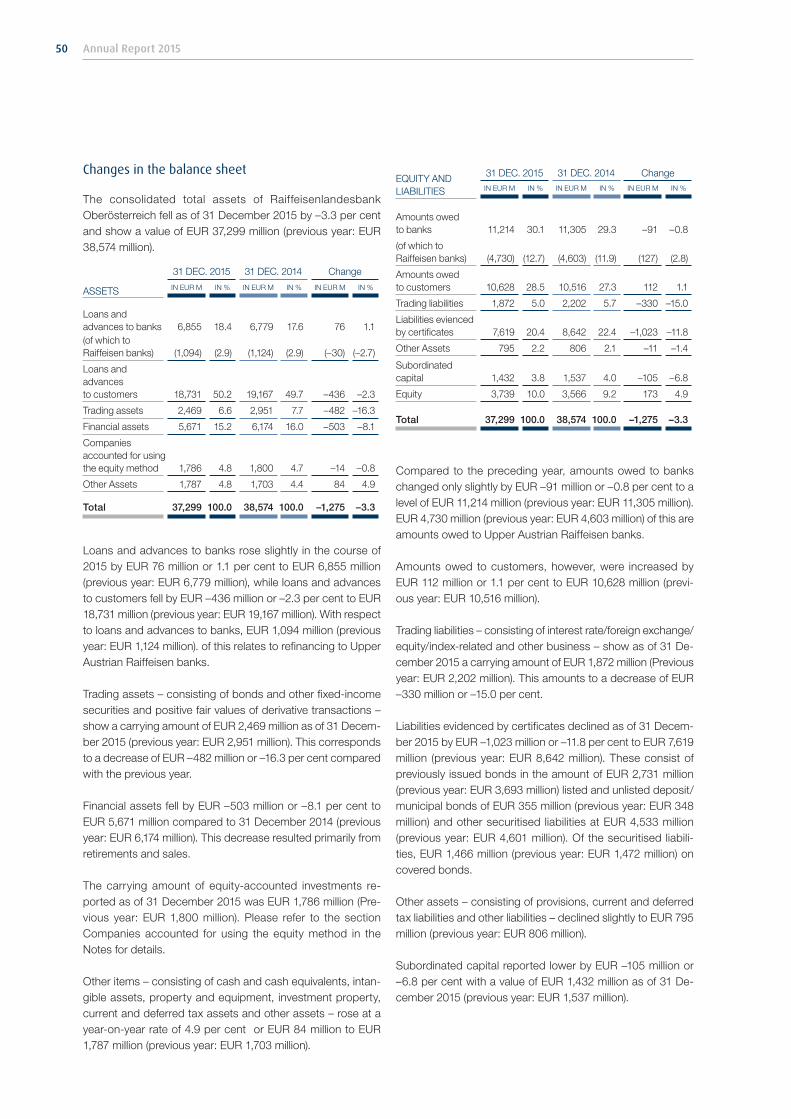

Total assets of EUR 37.3 billion ¬ The Raiffeisenlandesbank Oberösterreich Group’s total

assets fell to EUR 37.3 billion from the figure of EUR 38.6 billion recorded in 2014. This can be traced particularly to a fall in money market financing. This refers to short-term, high-volume financing deals for money market clients.

¬ According to the Austrian Commercial Code, Raiffeisen-landesbank Oberösterreich had total assets of EUR 30.3 billion (2014: EUR 30.5 billion). For short-term financing, we continued to be conscious of capital resources and cost efficiency.

Annual profit rose to EUR 318.4 million ¬ The Raiffeisenlandesbank Oberösterreich Group's pre-tax

profit for the year rose to EUR 318.4 million (2014: EUR 40.7 million). For example, the probability of capitalised com-panies defaulting significantly improved in 2015, which led to reversals in portfolio value adjustments from IFRS. Fur-thermore, the results for companies accounted for under the equity method improved by EUR 47.1 million compared to 2014. Gains/losses on remeasurement of designated fi-nancial instruments due to interest rate and spread effects also had a positive impact on the result.

Increases in the operating profit and Group comprehensive income

¬ Raiffeisenlandesbank Oberösterreich Group reported an operating profit of EUR 281.5 million in 2015 according to IFRS (+4.4 per cent) as well as comprehensive income of EUR 213.2 million (2014: EUR 94.8 million).

¬ In 2015, Raiffeisenlandesbank Oberösterreich AG reported an operating profit of EUR 269.6 million (–6.1 per cent), in accordance with the Austrian Commercial Code, and a result from ordinary operations of EUR 135.6 million (+49.0 per cent), which took into account the integration of the PRIVAT BANK Group into Raiffeisenlandesbank Oberösterreich.

Heinrich SchallerChairman of the Managing Board of Raiffeisenlandesbank Oberösterreich Aktiengesellschaft

Foreword by Heinrich Schaller

8 Annual Report 2015

Reinhard Schwendtbauer Stefan Sandberger Heinrich Schaller Michaela Keplinger-Mitterlehner Georg Starzer Markus Vockenhuber

9Raiffeisen Banking Group Upper Austria Raiffeisenlandesbank Oberösterreich Group General information

Managing Board

Scope of responsibilities of the Managing Board

Heinrich Schaller

Office of the Managing Board

Public Relations and Media

Legal Office

Corporate Governance & Compliance

Public Affairs

Strategy Raiffeisen Banking Group Upper Austria

Corporate customers Raiffeisen banks

Management of Raiffeisen banks

Human resources management

Group accounting and controlling

Group audit

Level 2 (Division)

Level 2 (Subsidiaries)

Staff unit

Michaela Keplinger-Mitterlehner

Treasury Financial Markets

Product management/Sales management Retail and Private Banking/Group marketing

Raiffeisenlandesbank Oberösterreich branches

PRIVAT BANK

bankdirekt.at

KEPLER-FONDS KAG

Stefan Sandberger

Product responsibility Treasury

Cash Management products

Organisation

Operations

GRZ IT Center GmbH

Raiffeisen Software GmbH

Reinhard Schwendtbauer

Tax Office

Collateral

Investment management

REAL-TREUHAND Management GmbH

Georg Starzer

Corporates Market

Product management and Corporates Sales

Factoring

Raiffeisen-IMPULS-Leasing

RVM Raiffeisen-Versicherungsmakler

Markus Vockenhuber

Overall bank risk management

Financing Management

10 Annual Report 2015

Raiffeisen Banking Group Upper Austria stands with its strong client focus for stability, reliability and expertise, as well as integrity in dealing, quality advice and security.

Jakob Auer

11Raiffeisen Banking Group Upper Austria Raiffeisenlandesbank Oberösterreich Group General information

Foreword by President Jakob Auer

The basis of our success at Raiffeisen Oberösterreich is working closely together

2015 was not an easy year. The whole banking sector was faced with a number of major challenges, such as continued weak economic growth, increased expense in the area of controlling as well as excessive bureaucratic demands, and last but not least, changing customer behaviour as a result of digitisation. This makes it all the more encouraging that Raiffeisenlandesbank Oberösterreich and the Upper Austrian Raiffeisen banks were able to achieve such good results in this turbulent year marked by frequent upheaval. Making a profit is never an end in itself at Raiffeisen. As the most import-ant financial services provider, based on our strong customer focus, our reliability and competence as well as our serious outlook and the sense of security that comes with it, we are not only responsible for the economic growth of our custom-ers but also actively contribute towards the sustainable suc-cess of our region.

Developing perspectives for the future through common goals

Good results don't just materialise out of nowhere. An open dialogue, clear strategies, common goals and a willingness to change are essential in order to create the right conditions to meet the challenges of the future. The close collaboration in

the “Raiffeisen Banking Group Upper Austria 2020” project has proven to be a key factor for success in the whole Raif-feisen sector in Upper Austria. The results so far, our consis-tency in implementing the necessary measures and our drive to develop this project, are all strong proof that we in Upper Austria are all pulling in unison. We appreciate that we can only achieve our full strength through working together. This clear process primarily strengthens the trust that our cus-tomers have in us. It should be expected of us as the market leader in Upper Austria that we can develop perspectives for the future and bring them to fruition in a determined fashion.

Carrying on the path to success

I would like to give particular thanks to our customers, who have placed their trust in Raiffeisen Oberösterreich as their banking partner. A special thank you also to the members of the Managing Board of Raiffeisenlandesbank Oberösterreich, and especially to Chairman Heinrich Schaller for his open-ness, his focus on teamwork and his clear decisions based on his foresight and expertise. I would also like to thank the members of the Supervisory Board at Raiffeisenlandesbank Oberösterreich, the managers and all employees at Raiffeisen Oberösterreich for their commitment to customer satisfaction.

Jakob AuerPresident of the Supervisory Board

12 Annual Report 2015

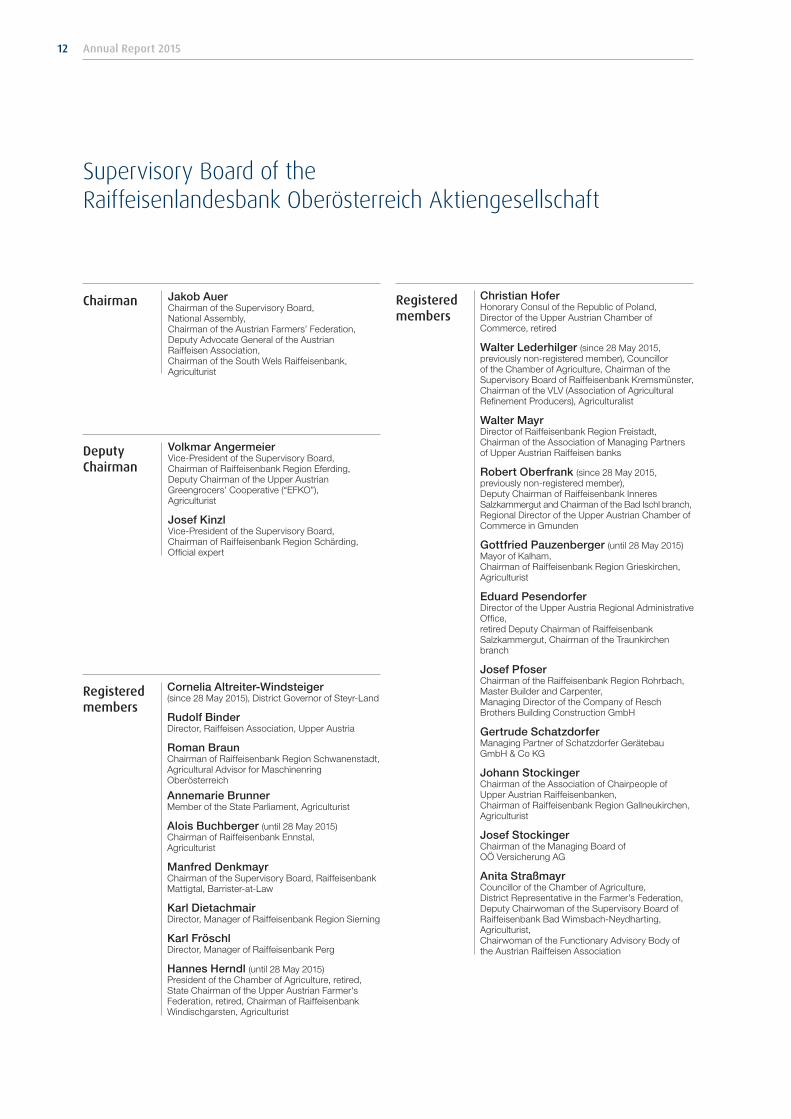

Supervisory Board of the Raiffeisenlandesbank Oberösterreich Aktiengesellschaft

Jakob Auer Chairman of the Supervisory Board, National Assembly, Chairman of the Austrian Farmers’ Federation, Deputy Advocate General of the Austrian Raiffeisen Association, Chairman of the South Wels Raiffeisenbank, Agriculturist

Volkmar Angermeier Vice-President of the Supervisory Board, Chairman of Raiffeisenbank Region Eferding, Deputy Chairman of the Upper Austrian Greengrocers’ Cooperative (“EFKO”), Agriculturist

Josef Kinzl Vice-President of the Supervisory Board, Chairman of Raiffeisenbank Region Schärding, Official expert

Christian Hofer Honorary Consul of the Republic of Poland, Director of the Upper Austrian Chamber of Commerce, retired

Walter Lederhilger (since 28 May 2015, previously non-registered member), Councillor of the Chamber of Agriculture, Chairman of the Supervisory Board of Raiffeisenbank Kremsmunster, Chairman of the VLV (Association of Agricultural Refinement Producers), Agriculturalist

Walter Mayr Director of Raiffeisenbank Region Freistadt, Chairman of the Association of Managing Partners of Upper Austrian Raiffeisen banks

Robert Oberfrank (since 28 May 2015, previously non-registered member), Deputy Chairman of Raiffeisenbank Inneres Salzkammergut and Chairman of the Bad Ischl branch, Regional Director of the Upper Austrian Chamber of Commerce in Gmunden

Gottfried Pauzenberger (until 28 May 2015) Mayor of Kalham, Chairman of Raiffeisenbank Region Grieskirchen, Agriculturist

Eduard Pesendorfer Director of the Upper Austria Regional Administrative Office, retired Deputy Chairman of Raiffeisenbank Salzkammergut, Chairman of the Traunkirchen branch

Josef Pfoser Chairman of the Raiffeisenbank Region Rohrbach, Master Builder and Carpenter, Managing Director of the Company of Resch Brothers Building Construction GmbH

Gertrude Schatzdorfer Managing Partner of Schatzdorfer Gerätebau GmbH & Co KG

Johann Stockinger Chairman of the Association of Chairpeople of Upper Austrian Raiffeisenbanken, Chairman of Raiffeisenbank Region Gallneukirchen, Agriculturist

Josef Stockinger Chairman of the Managing Board of OÖ Versicherung AG

Anita Straßmayr Councillor of the Chamber of Agriculture, District Representative in the Farmer’s Federation, Deputy Chairwoman of the Supervisory Board of Raiffeisenbank Bad Wimsbach-Neydharting, Agriculturist, Chairwoman of the Functionary Advisory Body of the Austrian Raiffeisen Association

Cornelia Altreiter-Windsteiger (since 28 May 2015), District Governor of Steyr-Land

Rudolf Binder Director, Raiffeisen Association, Upper Austria

Roman Braun Chairman of Raiffeisenbank Region Schwanenstadt, Agricultural Advisor for Maschinenring Oberösterreich

Annemarie Brunner Member of the State Parliament, Agriculturist

Alois Buchberger (until 28 May 2015) Chairman of Raiffeisenbank Ennstal, Agriculturist

Manfred Denkmayr Chairman of the Supervisory Board, Raiffeisenbank Mattigtal, Barrister-at-Law

Karl Dietachmair Director, Manager of Raiffeisenbank Region Sierning

Karl Fröschl Director, Manager of Raiffeisenbank Perg

Hannes Herndl (until 28 May 2015) President of the Chamber of Agriculture, retired, State Chairman of the Upper Austrian Farmer's Federation, retired, Chairman of Raiffeisenbank Windischgarsten, Agriculturist

Chairman

Deputy Chairman

Registered members

Registered members

13Raiffeisen Banking Group Upper Austria Raiffeisenlandesbank Oberösterreich Group General information

Supervisory Board

Helmut Feilmair Chairman of the Staff Council

Gerald Stutz Deputy Chairman of the Staff Council

Dorina Meißl

Dietmar Felber (until 7 January 2016)

Harald John (since 7 January 2016)

Josef Gokl

Karin Hetzmannseder

Christoph Huber

Albert Ruhmer

Authorised representative Hermann Schwarz

Authorised representative Richard Seiser

Josef Nickerl Permanent Secretary, State Commissioner to the Financial Markets, Supervisory Authority

Regina Reitböck Deputy State Commissioner to the Federal Ministry of Finance

Gerhard Ritzberger

Helmut Angermeier

Klaus Ahammer, MBA Director of Raiffeisenbank Salzkammergut

Johann Moser Director, Executive Manager of Raiffeisenbank Region Ried i. I.

Franz Penz (until 28 May 2015) Draper

Non-registered members

Staff Council Representa-tives

State Com-missioners

Honorary presidents

14 Annual Report 2015

RESPONSIBILITY“As the most important financial services provider in Upper Austria, we have a particular responsibility towards our customers, which we meet with our sustainable strategies as well as modern economic and financial services. We don't just focus on the next quarter's results but on sustainable future-oriented development.”

Heinrich Schaller

15Raiffeisen Banking Group Upper Austria Raiffeisenlandesbank Oberösterreich Group General information

Sustainability and CSR

16 Annual Report 2015

PROXIMITY TO CUSTOMERS

“We don't just rely on technical knowledge when working with our customers in a consultancy capacity. Raiffeisenlandesbank Oberösterreich has made proximity to customers and customer focus the most important principle of its business strategy. This is demonstrated in the stability of our relationship with customers.”

Michaela Keplinger-Mitterlehner

17Raiffeisen Banking Group Upper Austria Raiffeisenlandesbank Oberösterreich Group General information

Sustainability and CSR

18 Annual Report 2015

INNOVATION“Raiffeisenlandesbank Oberösterreich is a pioneer in the development and sale of modern banking technology. Innovation and digitisation for us don't mean a way to replace personal contact with our customers, but should serve as an additional, forward-looking means of communicating based on our customer focus.”

Stefan Sandberger

19Raiffeisen Banking Group Upper Austria Raiffeisenlandesbank Oberösterreich Group General Information

20 Annual Report 2015

21Raiffeisen Banking Group Upper Austria Raiffeisenlandesbank Oberösterreich Group General information

Sustainability and CSR

PARTNERSHIP“Our extensive investment portfolio isn't just about yielding good returns. As the parent company of a number of subsidiaries as well as a strong key shareholder in Upper Austria, we are closely linked to the real economy and make a significant contribution towards securing jobs and the economic success of the whole region.”

Reinhard Schwendtbauer

22 Annual Report 2015

23Raiffeisen Banking Group Upper Austria Raiffeisenlandesbank Oberösterreich Group General Information

COMMITMENT“With its strengths – a sound financial base, a particular customer focus and a global network – Raiffeisenlandesbank Oberösterreich has proven itself to be a stable and reliable partner for its customers.”

Georg Starzer

24 Annual Report 2015

25Raiffeisen Banking Group Upper Austria Raiffeisenlandesbank Oberösterreich Group General Information

SUSTAINABILITY:“Economic globalisation as well as new national and international regulations bring a number of changes for Raiffeisenlandesbank Oberösterreich and its customers. In the interests of the financial success of our customers, we embrace these changes with technical competence, open dialogue, and last but not least a strategic vision.”

Markus Vockenhuber

26 Annual Report 2015

2015 in retrospect

Commitment on many fronts

In 2015, Raiffeisenlandesbank Oberösterreich also sup-ported a number of initiatives in the areas of integration, development aid, environmental protection etc. The Raiffeisen Banking Group Upper Austria also launched a major fund-raising campaign for the victims of the major earthquake in Nepal alongside the charity Caritas Upper Austria. A total of EUR 200,000 was raised both from company employees and customers.

Sports day

Marcel Koller, successful manager of the Austrian na-tional football team, paid Raiffeisenlandesbank Oberös-terreich a visit on 4 December 2015 as part of our initiative “Business as a Partner to Sport”. Koller spoke of the “Austrian way” in football and how important reli-able long-term partners are for success. A demonstration of innovative leadership

Contactless payment was introduced with the Raif-feisen bank card in 2013 and since 2015, it has also been possible to use your smartphone at NFC (Near Field Communication)-enabled terminals to make pay-ments quickly, easily and safely. This technology was trialled in Linz during the summer. The technology was rolled out across the whole Raiffeisen Oberösterreich network from October 2015 onwards. A total of 2.1 mil-lion NFC payments were made by Raiffeisen Banking Group Upper Austria customers in 2015.

On course for growth in southern Germany

Raiffeisenlandesbank Oberösterreich has been active in southern Germany since 1991 and currently operates eight branches in Bavaria and Baden-Wurttemberg. The commitment to this dynamic economic region is due to be expanded in the near future with increased activity in Stuttgart and Karlsruhe. An additional sign that the company is on the right path was the transfer in autumn 2015 of the registered office of the branch in southern Germany from Passau to Munich, the second most important financial centre in Germany.

Study reveals high level of customer satisfaction

The customer satisfaction survey carried out by Raiff-eisen Oberösterreich in 2015 shows that efficiency also is a sure-fire way to guarantee a high level of customer focus. Around 24,500 respondents gave Raiffeisen Oberösterreich top marks for the quality of advice and customer-friendliness.

Franz Kehrer, Director of Caritas in Upper Austria, and Heinrich Schaller, CEO of Raiffeisenlandesbank Oberösterreich

27Raiffeisen Banking Group Upper Austria Raiffeisenlandesbank Oberösterreich Group General information

2015 in retrospect

Efficient structures created by Raiffeisen Software GmbH

In 2015, both major Raiffeisen IT companies RACON Software GmbH (Linz) and Raiffeisen Software Solu-tion and Service GmbH (Vienna) merged to form Raif-feisen Software GmbH. The core owners of this major software company are eight Raiffeisen state banks. Raiffeisenlandesbank Oberösterreich holds 25.5 per cent of the company, which is headquartered in Linz.

Success for fund subsidiary KEPLER-FONDS

2015 was a successful year for the investment company of Raif feisenlandesbank Oberösterreich. KEPLER FONDS KAG was recognised by the analysts at FERI Eu-rorating Services for the third year running out of more than 200 fund providers. In the “Fund Compass” rating from CAPITAL, the respected German finance magazine, KEPLER-FONDS AG came fifth among the top 100 most important investment companies in Germany.

Traditional World Savings Day

The 90th World Savings Day was celebrated in 2015. This is a special tradition at Raiffeisen Oberösterreich. The Raiffeisen Banking Group Upper Austria used this day at the end of October as an opportunity to empha-sise the personal relationship it has with its customers and to thank them for the confidence they have shown.

New award for our family-friendly policies

For a number of years now, Raiffeisenlandesbank Oberösterreich has had a wide range of measures in place to improve the work-life balance of its employees. In 2015, Raiffeisenlandesbank Oberösterreich and its subsidiaries were given a seal of approval by the Fed-eral Ministry of Family and Youth for the third time for their family-friendly policies.

Realignment of PRIVAT BANK

Raiffeisenlandesbank Oberösterreich stands for cus-tomer focus, efficiency and exploiting synergies. With this strategy in mind, PRIVAT BANK and bankdirekt.at were reorganised in autumn 2015 as independent busi-ness areas of Raiffeisenlandesbank Oberösterreich. This focus of this realignment is on sustainability and continuity.

Har

ald

Sch

loss

ko

Raiffeisenlandesbank Oberösterreich CEO Heinrich Schaller and Austrian national football team manager Marcel Koller

Raiffeisenlandesbank Oberösterreich President of the Supervisory Board Jakob Auer and Raiffeisenlandesbank Oberösterreich CEO Heinrich Schaller with the Sumsi Bee mascot

Sophie Karmasin, Minister of Family and Youth, as well as Raiffeisenlandesbank Oberösterreich HR managers Judith Brandstetter (left) and Johanna Stanek (right)

28 Annual Report 2015

As a strong regional bank, Raiffeisenlandesbank Oberösterreich is aware of its so-cio-political responsibility and sees itself as a partner to the individuals who want to help shape positive development in the region on a sustainable basis. Through its activities, Raiffeisenlandesbank Oberösterreich is also committed to the values of its founder Friedrich Wilhelm Raiffeisen, and therefore places the well-being of other people at the centre and acts based on the values of solidarity, subsidiarity and sustainability.

1. Activities in the areas of sustainability and CSR ________________________ 29

2. Sustainability rating ______________________________________________ 30

3. Stakeholder management _________________________________________ 30

4. Efficient for nature and the environment _____________________________ 33

5. Sustainable finance products _______________________________________ 34

6. Responsibility for employees ______________________________________ 36

7. Commitment ____________________________________________________ 38

Sustainability management and corporate social responsibility

29Raiffeisen Banking Group Upper Austria Raiffeisenlandesbank Oberösterreich Group General information

Sustainability and CSR

Raiffeisenlandesbank Oberösterreich continued to develop the area of “Sustainability and Corporate Social Responsibil-ity (CSR)” in 2015. Stakeholder management was analysed and redesigned. The aim here is to hold a stakeholder dia-logue in the future to expand the development of the sus-tainability management system. A decision was also taken to incorporate an energy management system within the Group

to comply with the legal requirements of the Energy Efficiency Act. A special information page was set up on the Raiffeisen-landesbank Oberösterreich website at www.rlbooe.at/nach-haltigkeit in order to comply with transparency requirements and to be able to report on the latest developments in the area of sustainability management.

The RKI was launched in 2007. It is a platform for 23 member companies from the Austrian Raiffeisen sector

that promotes the exchange of shared knowledge and ex-perience in the fields of sustainability and CSR, coordinates joint activities, and raises awareness of climate protection. As a member, Raiffeisenlandesbank Oberösterreich represents the Upper Austrian Raiffeisen banks and actively participates through work groups and exchange of knowledge and expe-rience to shape the activities of the Raiffeisen Climate Protec-tion Initiative.

www.raiffeisen-klimaschutz.at

Since 2007 respACT has been the lead-ing platform for companies in the area of CSR and sustainable development in

Austria. The name respACT stands for “responsible action” and comes from the purpose of the association, which is to support – from the smallest to the largest company – the aim of achieving self-defined ecological and social objectives. As a member, Raiffeisenlandesbank Oberösterreich benefits from the information provided, as well as participation in various events.

www.respact.at

Promoting a good work/life balance is one of the most important sociopoliti-cal issues of our time. This is why the

Federal Ministry of Family and Youth has set up the “Compa-nies for families” network to create a platform for companies and municipalities who show an interest in family-friendly HR and community policies. As the fourth-largest bank in Austria, Raiffeisenlandesbank Oberösterreich is aware of its respon-sibility and wants to contribute towards the “Companies for Families” network as a supporting partner.

www.unternehmen-fuer-familien.at

The CSR Dialogue Forum developed – as one of the more recent sustain-ability platforms – from an initiative of

Upper Austrian entrepreneurs. The vision of the association is to develop an interdisciplinary platform for CSR as a centre of competence for companies in Austria and neighbouring re-gions. The initiative works, among others, in cooperation with international certification partners on an international CSR and sustainability quality seal. As a charter member, Raiffeisen-landesbank Oberösterreich supports the initiative, in particu-lar, to build and develop the organisational structure.

www.csr-dialogforum.at

UNTERNEHMEN FÜR FAMILIEN

1. Activities in the areas of Sustainability and CSR

Memberships

In order to ensure continued advances in the areas of sustainability and CSR, Raiffeisenlandesbank Oberösterreich has been playing an active part in sharing information in sustainability networks. The bank takes part in the following networks:

RAIFFEISEN CLIMATE PROTECTION INITIATIVE (RKI)

RESPACT – AUSTRIAN BUSINESS COUNCIL FOR SUSTAINABLE DEVELOPMENT CSR DIALOGUE FORUM

COMPANIES FOR FAMILIES

30 Annual Report 2015

3. Stakeholder management

The process

A road map was devised for the development of a Group-wide sustainability strategy that follows the international standard ISO 26000 and the Austrian standard ONR 192500, which is derived from it. Raiffeisenlandesbank Oberösterreich AG intends to use this to gain a better understanding of its stake-holder groups and the effects that its decisions and activi-ties have on them. Based on this understanding, and with the knowledge of how relationships between Raiffeisenland-esbank Oberösterreich AG and the individual stakeholders are formed, the expectations of stakeholders should be ascer-tained and managed systematically.

1. Identification

As a first step, potential shareholders were recorded and ar-ranged into groups as necessary. Based on the following six questions it was analysed whether the stakeholders actually belong to an interest group or stakeholder group and how intensive the relationship is:

¬ Who do they have legal or contractual obligations towards? ¬ Who could be positively or negatively affected by the

decisions taken by or the activities performed by the organisation?

¬ Who has an interest in the decisions or the activities of the organisation?

¬ Who can influence the decisions or the activities of the organisation?

¬ Who would be disadvantaged by being excluded? ¬ Who is affected within the value chain?

The analysis is carried out with the help of the internal sustain-ability network. This network is comprised of representatives of the various specialist departments in the Raiffeisenlandes-bank Oberösterreich AG Group and is brought together as an expert panel to analyse and prepare specific topics. The network also serves as a point of contact for department-spe-cific topics. As a consequence, partial strategies can be de-veloped and projects initiated with them.

A detailed definition of each individual stakeholder was then made as a conclusion to this analysis, which served as a basis and an explanation for the valuation analysis of the stakeholders.

Analysing and rating its own stakeholders and engaging in di-alogue with those groups are central cornerstones of a holistic sustainability management system. In its activities Raiffeisen-landesbank Oberösterreich AG is committed to the values of its founder Friedrich Wilhelm Raiffeisen. It therefore places the wellbeing of other people at the centre of its vision and acts based on the values of solidarity, subsidiarity and sus-tainability. Based on this understanding, Raiffeisenlandesbank

Oberösterreich not only takes into account the interests of shareholders, such as in a typical shareholder approach, but also takes care to create a future-oriented restructuring, con-sidering all relevant interest groups. Since the middle of 2013, Raiffeisenlandesbank Oberösterreich AG has also been occu-pied with stakeholder management in the context of building up its own sustainability management system. The individual stakeholders have been analysed as part of this process.

Raiffeisenlandesbank Oberösterreich has been rated by the international ratings agency oekom research AG in the area of sustainability efforts. An extensive rating process was set up by oekom research AG in autumn 2015 that rates the

measures that have been taken and the new method of re-porting on the Raiffeisenlandesbank Oberösterreich website. The final rating is expected in early 2016.

2. Sustainability rating

31Raiffeisen Banking Group Upper Austria Raiffeisenlandesbank Oberösterreich Group General information

Sustainability and CSR

External stakeholders

all private customers, private banking customers and corporate customers of Raiffeisenlandesbank Oberösterreich

CUSTOMERS

Agencies such as Moody‘s (credit rating), oekom research (sustainability rating), etc.

RATINGS AGENCIES

Advocacy groups which represent the Raiffeisenlandesbank Oberösterreich (e.g. WK, IV, etc.) or the interests of its members towards the Raiffeisenland-esbank Oberösterreich (e.g. AK)

ADVOCACY GROUPS

Education and research institutions in schools, universities and technical colleges

EDUCATION & RESEARCH

Institutions and projects funded in ac-cordance with the sponsoring strategy in place

SPONSOREES

Media that cover the activities of the Raiffeisenlandesbank Oberösterreich Group

MEDIA

Suppliers of Raiffeisenlandesbank Oberösterreich

SUPPLIERS

legally assigned but also voluntary auditory and supervisory bodies (e.g. EBA, OeNB, FMA and auditors)

SUPERVISORY AND MONITORING BODY

All banks that do not belong to the Raiffeisen sector Austria

COMPETITORS

Public as an influential abstract entity

PUBLIC

Public administration as an important point of contact for Raiffeisenlandes-bank Oberösterreich

PUBLIC ADMINISTRATION

Non-profit organisations and NGOs that predominantly focus on the financial sector

NGOS/NPOS

Capital market in its entirety with all its participants

CAPITAL MARKET

in contrast to the internal stakeholder group “Subsidiaries” – all investments held by Raiffeisenlandesbank Oberös-terreich with a holding of under 50%

EQUITY INVESTMENTS

contracted consultancy firms

CONSULTANCY FIRMS

Political systems in the domestic mar-kets Austria and southern Germany

POLITICS

Local residents who are directly affected by the activities of Raiffeisen-landesbank Oberösterreich

RESIDENTS

2. A brief summary of our stakeholders

Board members and directors of the 94 Upper Austrian Raiffeisen banks

RAIFFEISEN SECTOR IN UPPER AUSTRIA

Around 5,000 employees (total of all fully-consolidated companies in financial year 2013)

EMPLOYEES

42 members of the Supervisory Board of Raiffeisenlandesbank Oberösterreich

SUPERVISORY BOARD MEMBERS

GROUP SUBSIDIARIES

Owners of the 94 Upper Austrian Raiffeisen banks

CO-OWNERSRAIFFEISEN

SECTOR AUSTRIA

Internalstakeholders

Raiffeisenlandesbank Oberösterreich subsidiaries who serve the special customer and product groups or provide services to them

All independent Raiffeisen banks, Raiffeisen state banks, RZB, RBI and the corresponding specialised institutions (Raiffeisen Bausparkasse, Raiffeisen Capital Management etc.) and investments (AGRANA etc.)

32 Annual Report 2015

STAKEHOLDER MATRIX OF RAIFFEISENLANDESBANK OBERÖSTERREICH AG

¬ Internal stakeholders External stakeholders

3. The valuation

As a second step, an online survey was created to assess the stakeholders identified. Senior management were requested

to estimate the interest in and the influence on the Raiffeisen-landesbank Oberösterreich AG on a scale between 0 (very low) and 10 (very high) for each stakeholder. The results were transferred over to the following stakeholder matrix:

Based on the results from the previous steps the sustainability network was asked to submit proposals for future activities. These are then checked for plausibility and feasibility in the following section.

4. The result

The result serves as the basis for optimis-ing the individual dialogue strategies and the activities derived from them. It also provides the foundation for a planned materiality analysis, an additional step towards the development of a Group-wide sustainability strategy.

EXTERNALSTAKEHOLDERS

Upper Austrian Raiffeisen banks

Supervisory &monitoring

bodies

customers

Ratingsagencies

Capitalmarkets

Raiffeisen sectorAustria

Politics

Media

Public

Local residents

NGOs/NPOs

Education &Research

Spon-sorees

PublicAdministration

Advocacygroups

Compe-titors

Suppl-iers

Consultancycompanies

Invest- ments

Co-owners

SupervisoryBoard members

Staff

Groupsubsidiaries

Inner circle high level of influence on Raiffeisenlandesbank Oberösterreich

Middle circle medium level of influence on Raiffeisenlandesbank Oberösterreich

Low circle low level of influence on Raiffeisenlandesbank Oberösterreich

Partnership-based dialogueDialogue through consultation

Dialogue through observation

0 5

5

10

10

Dialogue through information

Local residents

NGOs/NPOs

Education & researchPublic administration

Advocacy groups

Sponsorees

SuppliersConsultancy firms

CompetitorsEquity investments

MediaPublic

Politics

Co-owners

Group subsidiaries

Staff

Supervisory Board members

Upper Austrian Raiffeisen banks

Supervisory and monitoring bodies

Customers

Ratings agenciesCapital market

Raiffeisen sector Austria

Shares in Raiffeisenlandesbank Oberösterreich

Influ

ence

on

Rai

ffei

senl

and

esb

ank

Ob

erö

ster

reic

h

INTERNALSTAKEHOLDERS

33Raiffeisen Banking Group Upper Austria Raiffeisenlandesbank Oberösterreich Group General information

Sustainability and CSR

Energy Efficiency Act

On 1 January 2015 the En-ergy Efficiency Act (EEffG) came into force in Austria. This law aims to increase energy efficiency across Austria by 20 per cent, to increase the share in re-newable energy sources, to improve the reliability of their supply, and to reduce green-house gas emissions. We also expect a positive stimulus for the economy.

Large companies must either carry out an energy audit every four years or introduce a certified energy management sys-tem. The Managing Board of Raiffeisenlandesbank Oberös-terreich has decided to introduce an energy management system for the whole Group to be able to record energy con-sumption precisely and to realise any savings potential. An energy policy was adopted across the Group at the end of 2015 and all the work in establishing an energy management system was completed. It was certified according to interna-tional standard ISO 50001 at the beginning of February 2016.

Life cycle assessment

The series of CSR reports for Raiffeisen Banking Group Austria was resumed this year with the Life Cycle Assessment 2014. The study was created by the Austrian Federal Environ-ment Agency on behalf of the sustainability management de-partment of Raiffeisen Zentralbank Österreich AG. The report

systematically records the greenhouse gas emissions directly and indirectly caused by the activities of the company. A indi-vidual report was also produced for each federal state, as was the case with the Value Creation Report 2013.

This shows Raiffeisenlandesbank Oberösterreich and the Upper Austrian Raiffeisen banks that environmental responsi-bility has already been assumed, but there is still potential for improvement from both ecological and economical perspec-tives. The majority of emissions are produced as the result of energy consumption, and the Transport department also has further potential for reducing its carbon footprint. The prem-ises are already largely heated in an eco-friendly way. Further information is available at www.rlbooe.at/oekobilanz2014.

ÖBB Green Points

Raiffeisenlandesbank Oberösterreich is also campaigning for nature conservation measures as part of the ÖBB “Green Points” project. The Raiffeisenlandesbank Oberösterreich Group managed to save a total of 166.5 tonnes of CO2 emis-sions in 2014 through the use of rail travel, which corresponds to 1,067,170 “green points”. In 2015, Raiffeisenlandesbank Oberösterreich then invested these in the most popular of the eight projects available for selection as part of the “Austria

in Bloom” initiative. The “Blossoming landscapes” bee con-servation project works towards creating a sustainable intact ecosystem, actively contributes towards protecting the most important pollinators and gives them a new home. Bees' nests from this project were offered to customers, and one bees' nest was placed on the roof of Raiffeisenlandesbank Oberösterreich.

4. Efficient for nature and the environment

ÖB

B

Raiffeisenlandesbank Oberösterreich CEO Heinrich Schaller and General Director of ÖBB Christian Kern being awarded the Green Points certificate and the wild bees' nest.

34 Annual Report 2015

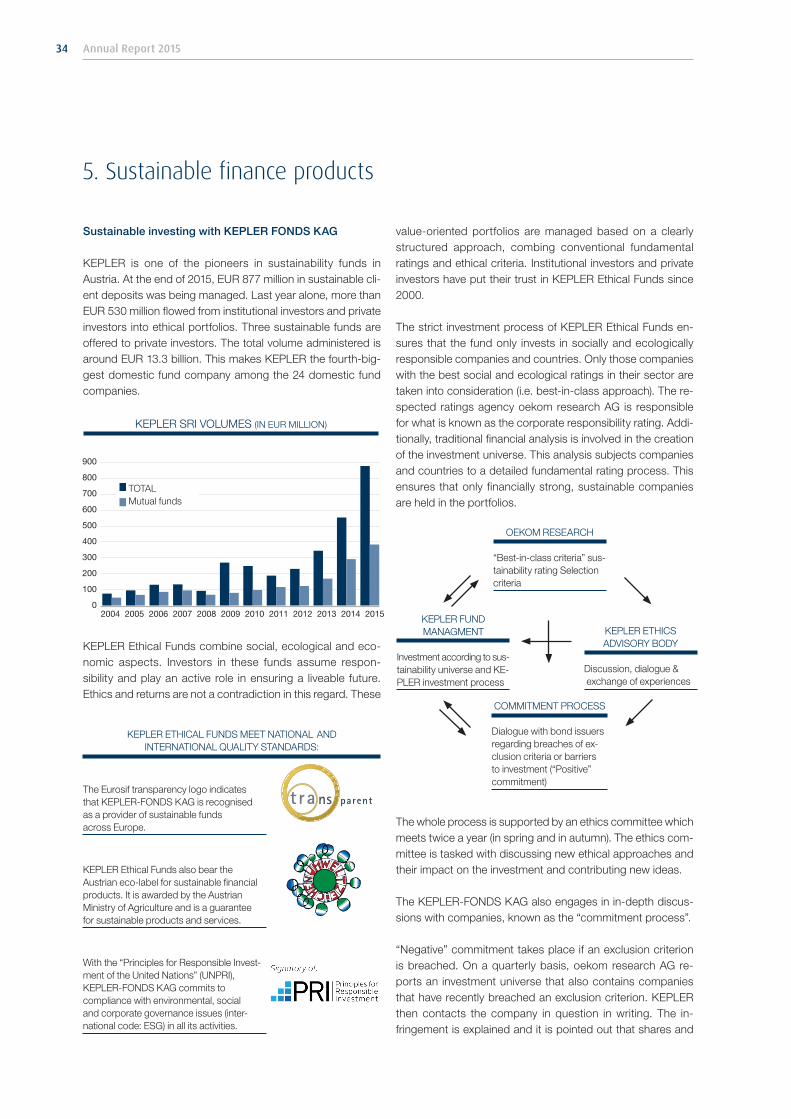

Sustainable investing with KEPLER FONDS KAG

KEPLER is one of the pioneers in sustainability funds in Austria. At the end of 2015, EUR 877 million in sustainable cli-ent deposits was being managed. Last year alone, more than EUR 530 million flowed from institutional investors and private investors into ethical portfolios. Three sustainable funds are offered to private investors. The total volume administered is around EUR 13.3 billion. This makes KEPLER the fourth-big-gest domestic fund company among the 24 domestic fund companies.

KEPLER Ethical Funds combine social, ecological and eco-nomic aspects. Investors in these funds assume respon-sibility and play an active role in ensuring a liveable future. Ethics and returns are not a contradiction in this regard. These

value-oriented portfolios are managed based on a clearly structured approach, combing conventional fundamental ratings and ethical criteria. Institutional investors and private investors have put their trust in KEPLER Ethical Funds since 2000.

The strict investment process of KEPLER Ethical Funds en-sures that the fund only invests in socially and ecologically responsible companies and countries. Only those companies with the best social and ecological ratings in their sector are taken into consideration (i.e. best-in-class approach). The re-spected ratings agency oekom research AG is responsible for what is known as the corporate responsibility rating. Addi-tionally, traditional financial analysis is involved in the creation of the investment universe. This analysis subjects companies and countries to a detailed fundamental rating process. This ensures that only financially strong, sustainable companies are held in the portfolios.

The whole process is supported by an ethics committee which meets twice a year (in spring and in autumn). The ethics com-mittee is tasked with discussing new ethical approaches and their impact on the investment and contributing new ideas.

The KEPLER-FONDS KAG also engages in in-depth discus-sions with companies, known as the “commitment process”.

“Negative” commitment takes place if an exclusion criterion is breached. On a quarterly basis, oekom research AG re-ports an investment universe that also contains companies that have recently breached an exclusion criterion. KEPLER then contacts the company in question in writing. The in-fringement is explained and it is pointed out that shares and

5. Sustainable finance products

KEPLER ETHICAL FUNDS MEET NATIONAL AND

INTERNATIONAL QUALITY STANDARDS:

The Eurosif transparency logo indicates that KEPLER-FONDS KAG is recognised as a provider of sustainable funds across Europe.

KEPLER Ethical Funds also bear the Austrian eco-label for sustainable financial products. It is awarded by the Austrian Ministry of Agriculture and is a guarantee for sustainable products and services.

With the “Principles for Responsible Invest-ment of the United Nations” (UNPRI), KEPLER-FONDS KAG commits to compliance with environmental, social and corporate governance issues (inter- national code: ESG) in all its activities.

Gradient

Flat

Grey

Black & White

C 49,5M 35K 31Y 26

C 71,5M 50,5K 44,5Y 37

C 85M 60K 53Y 44

C 2M 0K 47Y 0

C 30M 38K 98Y 3,5

C 17M 31K 94Y 0

C 49,5M 35K 31Y 26

C 71,5M 50,5K 44,5Y 37

C 85M 60K 53Y 44

C 2M 0K 47Y 0

C 30M 38K 98Y 3,5

C 17M 31K 94Y 0

N 64,5 N 76 N 100 N 6 N 49 N 33,5

900

800

700

600

500

400

300

200

100

0

KEPLER SRI VOLUMES (IN EUR MILLION)

TOTALMutual funds

OEKOM RESEARCH “Best-in-class criteria” sus-tainability rating Selection criteria

KEPLER FUND MANAGMENT

Investment according to sus-tainability universe and KE-PLER investment process

KEPLER ETHICS ADVISORY BODY

Discussion, dialogue & exchange of experiences

COMMITMENT PROCESS Dialogue with bond issuers regarding breaches of ex-clusion criteria or barriers to investment (“Positive” commitment)

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

35Raiffeisen Banking Group Upper Austria Raiffeisenlandesbank Oberösterreich Group General information

Sustainability and CSR

bonds will ultimately be sold. Any response from the company is forwarded to oekom research. The maximum time period between the notification of a breach and the actual sale is four months. A “positive” commitment results in the compa-nies becoming motivated to improve themselves as an entity worth investing in. This process is carried out on a half-yearly basis. As part of the process, a list of companies is created with whom a positive commitment should be made. A list of items where there is potential for improvement is sent to each company by oekom research AG.

In 2015 Raiffeisenlandesbank Oberösterreich continued its support of SOS Kindersdorf, with a contribution of EUR 5,000. Flyers printed according to the Austrian eco-label's guidelines were used as were Christmas cards for customers which were designed by the children at SOS Kinderdorf.

New student account = Goats for Burundi

Instead of vouchers or presents, if you opened a student ac-count at Raiffeisen Oberösterreich from the beginning of Sep-tember to the end of November, you received goats – at least in spirit. The animals were given to families in the small African country of Burundi, where they are helping make the lives of many people more secure. This project was carried out jointly with Caritas.

Raiffeisen Oberösterreich donated 30 euros for every new stu-dent account opened and put one of the core principles of cooperative banks into practice: helping people to help them-selves. The 30 euros helped to fund the purchase of a goat, appropriate training for the future owner as well as veterinary costs. After successfully completing the 50-day training pro-gramme, the participants in Burundi each received two goats.

This is an important foundation for generating an income for themselves.

The donation made by Raiffeisen Oberösterreich for each stu-dent account went directly to Caritas, who are carrying out this project. The goats were purchased on site at markets in Africa. A total of 78 students decided to take part in this scheme.

Industry projects and projects in the field of renewable energy

Raiffeisenlandesbank Oberösterreich has a professional team with extensive, long-standing experience in the financing of complex structured industry projects and projects in the area of renewable energy. A number of industrialised nations are faced with the challenge of adapting their energy policy in an era of weak economic growth to meet the prescribed cli-mate protection objectives. In 2015 in Paris, a comprehensive global climate protection agreement was signed which aims to keep global warming to under 2 degrees Celsius – if possible to under 1.5 degrees Celsius. In the near future, this means that the efforts to change how energy is produced must be stepped up and more projects aimed at producing renew-able energy must be implemented. Despite the oil price being very low – at least for now – reducing our dependency on fossil fuels such as oil and coal is still essential. Likewise, the key political decisions must be taken, particularly in Germany, where there are calls for nuclear energy to be phased out. The related need for investments requires efficient solutions in financing.

Arti

st's

impr

essi

on o

f Pre

tul w

ind

farm

/Rob

ert L

eitn

er

36 Annual Report 2015

6. Responsibility for employees

Raiffeisenlandesbank Oberösterreich therefore provides fi-nancing solutions for projects and investments in biogas/bio-mass, hydropower and photovoltaics in the domestic market and supports clients abroad. In the last few years, a number of financing arrangements for project developments in the energy sector have been made in the European Union and Turkey, and also through the financing of exports. In 2016, Raiffeisenlandesbank Oberösterreich will join forces with the European Investment Bank (EIB) to finance the Pretul wind farm belonging to the Austrian Federal Forestry Company in the Fischbacher Alps in the state of Steiermark. An innovative structure was designed with the EIB that can also be used to support similar projects of its kind in the future.

The Austrian Advertising Council ethical seal of approval

Raiffeisenlandesbank Ober- österreich is well aware of its responsibility to society as a partner to people in the re-gion. As a consequence we place a great emphasis on social responsibility, including in our marketing activities.

In this context, Raiffeisenlandesbank Oberösterreich has committed itself to complying with the Code of Ethics of the

Austrian advertising industry. Companies subject themselves to quality criteria based on these guidelines – which are not legally binding – which have been defined by the Austrian ad-vertising industry for the “Ethics and Morals” department and which exceed current legal requirements.

Raiffeisenlandesbank Oberösterreich was awarded the eth-ical seal of approval after being considered by the Austrian Advertising Council. This seal is a clear sign that a company is compliant with ethical principles in all its advertising activities. It is awarded for a period of two years.

The Austrian Advertising Council awards companies in this way who

¬ support the ethical and moral principles of the Code of Ethics of the Austrian advertising industry (FOR advertising ethics);

¬ share the collective social and ethical beliefs of the com-munications industry (FOR self-regulation);

¬ and in this way, advocate FOR freedom of advertising and AGAINST advertising bans (FOR freedom of advertising)

Further information on the ethical seal of approval and the Code of Ethics of the Austrian advertising industry can be found online at www.werberat.at.

Work/life balance audit

The work/life balance audit – as part of an audit process – assists companies in developing individual family-friendly measures that are customised to meet the needs of their em-ployees. After an positive assessment by an external audi-tor, the company is awarded with a government quality label by the Federal Ministry of Family and Youth. Studies show that companies that introduce family-friendly initiatives see in-creased levels of motivation, loyalty and dedication as well as lower sickness and staff turnover rates and shorter periods of parenting leave.

Raiffeisenlandesbank Oberösterreich took part in the work/life balance audit for the first time in 2009 and was awarded the basic certification. In the subsequent few years, measures were adopted in the areas of health management, dependant relatives and childcare. These successful measures were taken into account when the company was recertified in 2012.

37Raiffeisen Banking Group Upper Austria Raiffeisenlandesbank Oberösterreich Group General information

Sustainability and CSR

In the years after that the focus turned to topics like family-ori-ented leadership, the working world of the future, workshops for those returning to the workplace as well as part-time work and management. Likewise, talks were conducted with female employees with special attention given to the topics of “child care provision for school-age children” and “dependant rela-tives” as part of the “Work and Family” information platform created by Raiffeisen Oberösterreich.

The actions taken were reviewed again in 2015. The upgrad-ing of our certification in 2015 was not just a recognition of the good work already done but also an incentive and motivation to carry on towards reconciling the demands of work and fam-ily life in the interests of employees and customers alike.

Employee survey 2015

Banks have been faced with a challenging environment for several years now. Stringent regulations and supervisory red tape as a result of the economic and financial crisis, increased taxes, the low interest-rate environment and the sluggish economy. So far, the Raiffeisenlandesbank Oberösterreich has dealt well with all of this, as well as additional external influences. However, this environment continues to pose chal-lenges. The commitment shown by our employees has been extremely strong in the past few years. This special willingness to get involved will also be needed in the challenging years ahead of us.

The employee survey 2015 was carried out externally by the Jaksch & Partner GmbH institute for statistical analysis. Em-ployees were asked a total of 206 questions about job sat-isfaction, internal cooperation and management as well as workplace health impacts. Further goals were then set based on the results of the survey, and individual measures were developed between management and staff.

Careers – best recruiter

The 500 largest employers in Austria were tested on the quality of their recruiting process for the sixth time as part of the “BEST RECRUIT-ERS AUSTRIA” study and the best companies were rewarded. Raiffeisenlandes-bank Oberösterreich impressed with its sustainable recruit-ment process and was awarded the silver certification. We managed to move up to fourth place in the list of the top Aus-trian banks.

Kununu

Raiffeisenlandesbank Ober-österreich welcomes feed-back from competitors as well as employees, and be-cause of this, in March 2015 it was given the accolade of “Open Company” by the company assessment plat-form Kununu.

best recruiter

aut15 |16

38 Annual Report 2015

7. Commitment

EUROPEAN FORUM ALPBACH

The income gap is growing and posing a threat to eco-nomic growth. At the same time, differences in wealth provide a boost to the economy. Experts from the fields of economics, politics and science came together to discuss this as part of the economic discussions at the European Forum Alpbach 2015. A discussion of the topic “Equality – Location Dependent” discussed the conflict between urban and rural areas.

UPPER AUSTRIA STATE EXHIBITION 2015DIAKONIEWERK GALLNEUKIRCHEN,

HAUS BETHANIEN

The history of social democracy was documented and staged for visitors in the time-honoured fashion. It also went into the history of social initiatives and institutions such as the Diakoniewerk charitable organisation as well as how culture shapes the solidarity and help we give to people in difficult circumstances.

TEACH FOR LIFE

With the “Teach for Life” initiative, the BezirksRundschau newspaper honours those teachers who go the extra mile every day to bring the best out of our children and who have made a special contribution. Raiffeisenlandesbank Oberösterreich has supported this important initiative for a number of years.

Pia

Od

oriz

zi

foto

-rei

ter.c

om |

A. R

eite

r

Raiffeisenlandesbank Oberösterreich CEO Heinrich Schaller, host Barbara Guwak, Infineon Technologies Austria AG CEO Sabine Herlitschka, Simone Schmiedtbauer, CEO T-Mobile Austria, Andreas Bierwirth and host Richard Hubner

Raiffeisenlandesbank Oberösterreich Deputy CEO Michaela Keplinger-Mitterlehner and BezirksRundschau chief editor Thomas Winkler at the awards ceremony honouring committed teachers

39Raiffeisen Banking Group Upper Austria Raiffeisenlandesbank Oberösterreich Group General information

Sustainability and CSR

HÖHENRAUSCH 2015

The art festival Höhenrausch took place from the end of May to mid-October. It is one of the best-loved cultural events in Austria and also beyond Austria’s borders. This year, the mysterious world of birds was unveiled.

LENTOS KUNSTMUSEUM LINZ

The theme of death and decay brought a new approach and a revolutionary new aesthetic to western fashion in the 1980s. The “LOVE & LOSS – fashion and transience” exhibition delved deeper into the topic. Raiffeisenlandes-bank Oberösterreich has been a partner of the art mu-seum Lentos since it opened.

HARTLAUER FOTOGALERIE

The Hartlauer Fotogalerie offers a new platform for pho-tography enthusiasts. Four exhibitions a year, each with its special theme, should stir people's interest in modern yet timelessly beautiful photography from both inside and outside Upper Austria.

KLASSIK AM DOM

Klassik am Dom celebrated its fifth year in 2015 by once again inviting some of the world's biggest stars for three extraordinary concert evenings on the stage in front of the New Cathedral in Linz. 3,300 guests enjoyed the eve-nings beneath the unique backdrop of the New Cathedral with Paolo Conte and Max Raabe and, as part of the “Klassik am Dom” gala, with Angelika Kirchschlager, Mi-chael Schade and Theresa Grabner.

LINZFEST

Austrian musicians took centre stage at LINZFEST, which was held under the slogan of “The Sound of Austria”. Alongside the varied music programme, a wide array of cultural activities was put on for children of all ages.

Ott

o S

axin

ger

Lent

os K

unst

mus

eum

Lin

z/A

PA-F

otos

ervi

ce/H

artl

Har

tlaue

r

Litz

lbau

er

c_zo

e_m

_rie

ss

Exhibition curator Ursula Guttmann, Raiffeisenlandesbank Oberösterreich Deputy CEO Michaela Keplinger-Mitterlehner, artistic director Stella Rollig and Deputy Mayor Bernhard Baier

40 Annual Report 2015

20TH RAIFFEISEN SECURITY PRIZE

As part of Raiffeisenlandesbank Oberösterreich’s 20th awarding of the Raiffeisen Security Prize, 11 people from Upper Austria were rewarded for showing cour-age in helping crimes to be solved successfully. In the presence of Minister of the Interior Johanna Mikl-Leit-ner, the prize winners were congratulated for their bravery and courage. The awarding of the Raiffeisen Security Prize was the highlight of the Raiffeisen Secu-rity Day, which represented the start of the wide-rang-ing “Safety starts at home” campaign.

10TH STUDENT OLYMPICS

14,000 fourth-grade students from primary schools across Upper Austria began the 10th Student Olym-pics, whose motto in 2015 was “70 years of the Second Republic”. On 23 April, the top 20 teams met at Raif-feisenlandesbank Oberösterreich in Linz for the final. The winners this year were the team from Volksschule Aschach an der Donau.

THE CLEVELAND ORCHESTRA

The Upper Austria-born star conductor Franz Wels-er-Möst enjoys a high level of recognition worldwide for his work with the Cleveland Orchestra. Works by Oliv-ier Messiaen, Wolfgang Amadeus Mozart and Richard Strauss were played at the concert held on 23 October 2015 at the Brucknerhaus.

CLOSING EVENT OF THE OÖN STOCK MARKET GAME 2014

In the 13th OÖN stock market game, which was held in cooperation with Raiffeisen Oberösterreich, participants had eight weeks to show their stock market savvy and gain experience. Each of the roughly 15,000 people who took part was able to invest their pretend start-up capital on the international stock markets completely risk-free!

VICE-CHANCELLOR IN TALKS

Reinhold Mitterlehner appeared in his position at Vice-Chancellor of Austria for the first time before around 1,300 guests at the RaiffeisenForum for a discussion with Minister for Economy in the State Government of Upper Austria Michael Strugl, Chief Economist at the Federa-tion of Austrian Industries Christian Helmenstein as well as Raiffeisenlandesbank Oberösterreich CEO Heinrich Schaller.

The winners of the Raiffeisen Security Prize

Star conductor Franz Welser-Möst and the Cleveland Orchestra

Raiffeisenlandesbank Oberösterreich CEO Heinrich Schaller, Vice-Chancellor Reinhold Mitterlehner, MP Michael Strugl and Federa-tion of Austrian Industries chief economist Christian Helmenstein

A Citroën C4 Cactus for the overall winner Martin Laber (second from left), awarded by France Car Managing Director Andreas Parlic (left), Raiffeisenlandesbank Oberösterreich Deputy CEO Michaela Keplinger-Mitterlehner, Kepler-Fonds KAG Managing Director Andreas Lassner-Klein, OÖN Chief Editor Dietmar Mascher

The regional finalists at the Student Olympics

41Raiffeisen Banking Group Upper Austria Raiffeisenlandesbank Oberösterreich Group General information

Sustainability and CSR

START SCHOLARSHIP PROGRAMME

The programme was created in Upper Austria two years ago. At the beginning of the third year of the suc-cessful “START Upper Austria” initiative, 11 additional young people with immigrant backgrounds were in-vited to take part in the development programme and given the support they need to prepare them for the school-leaving Matura exams. Nineteen talented and socially involved young people are currently being sup-ported. Five scholarship winners have already passed their Matura with the help of START Upper Austria. Raiffeisenlandesbank Oberösterreich sponsors the programme alongside the state of Upper Austria.

EMPLOYEES SUPPORT ULF

INITIATIVE FOR REFUGEES

Some of the refugees who were temporarily housed in two Linz schools during the summer were lacking even the most basic things. This prompted the Independent State Volunteer Centre, a platform for voluntary social engagement, to launch a collection drive. Employees of the Raiffeisenlandesbank Oberösterreich Group took a very active role. A total of 18 large boxes and 25 travel bags filled with donated goods were handed out.

THE “COMPUTERS FOR CLASSROOMS” CAMPAIGN

As part of the “Computers for classrooms” campaign, Raiffeisenlandesbank Oberösterreich offered 200 used, but fully-functioning PCs free of charge to partner primary schools in the Union of Upper Austrian Schools.

The START scholarship winners in Upper Austria

The dedicated employees of Raiffeisenlandesbank Oberösterreich making a donation.

Raiffeisenlandesbank Oberösterreich CEO Heinrich Schaller handing over a computer.

42 Annual Report 2015

SPORT

Investing in young people isn't just so that we are seen as being socially responsible. It is essential for the future prospects of society. In sport, both the health benefits as well as the social benefits are key. Raif-feisenlandesbank Oberösterreich is a partner to the Raiffeisen Junior Wings Academy, which is currently in the process of being set up. Soon the ideal condi-tions will be in place for the most promising youngsters from the junior section of the two-time Austrian cham-pions LIWEST Black Wings Linz to become the Aus-trian ice hockey stars of the future. A strong emphasis will be placed on education as well as sports training. Raiffeisenlandesbank Oberösterreich also supports other sports clubs in Upper Austria in their success-ful work with young people, such as for example the Basket Swans Gmunden, the Upper Austria Football Association, LASK Linz, SV Ried, HC Linz AG, Linz AG, Froschberg table tennis and the Upper Austria ski pool.

CELEBRATING 25 YEARS OF THE GENERALI LADIES LINZ

The WTA international tennis tournament was held at the Gugl for the 25th time in 2015. In mid-October, spectators at the TipsArena were treated to top-level international women's tennis. A number of top stars took part in some exciting matches. As a partner of many years, Raiffeisen Oberösterreich was also in at-tendance this year with its own Raiffeisen Oberöster-reich Day, which among other things, gives youngsters the opportunity to meet the pros and have a go for themselves.

LINZ FROSCHBERG TABLE TENNIS

Raiffeisenlandesbank Oberösterreich has been a suc-cessful partner of the Linz Froschberg table tennis tour-nament for many years. The women, with four-time Olympian Liu Jia, have walked away with the Champions League trophy on two occasions.

EH

C L

iwes

t Bla

ck W

ings

Lin

zP

ictu

re /

Joh

anne

s K

iene

sber

ger

City

foto

/Rol

and

Pel

zl

Ski

MS

© H

aral

d D

osta

l / 2

015

LA

SK

Austria's golden girl Lui “Susi” Jia

Raiffeisenlandesbank Oberösterreich CEO Heinrich Schaller handing the winner's cheque to champion Anastasia Pavlyuchenkova.

43Raiffeisen Banking Group Upper Austria Raiffeisenlandesbank Oberösterreich Group General information

Sustainability and CSR

LONG NIGHT OF YOUNG ENTREPRENEURS

Raiffeisenlandesbank Oberösterreich and Young Econ-omy Upper Austria invited young entrepreneurs to at-tend the Long Night event at the Raiffeisen Forum. At the event, the entrepreneurs and company founders of the future were able to develop their business skills and their knowledge by attending informative lectures.

PEGASUS – THE BUSINESS PRIZE OF THE UPPER AUSTRIA NEWS SERVICE

The Pegasus award is now 21 years old and has become a firm fixture in the business calendar. The best com-panies in the country have been honoured. Raiffeisen-landesbank Oberösterreich CEO Heinrich Schaller sang the praises of Michael Teufelberger, who received the Pegasus in crystal for his life's work.

AGRICULTURE FORUM 2015

Austria has been a member of the European Union since 1995. Alongside the core aspects such as peace and freedom, Austria has also benefited economically, ac-cording to calculations made by the Austrian Institute for Economic Research (WIFO). More growth, more jobs, lower unemployment and lower inflation. Agriculture has also been able to grasp the opportunities available de-spite massive cutbacks and a long-term structural trans-formation. The first Austrian EU Commissioner, Franz Fischler, discussed this topic with a high-quality panel at the Raiffeisen Agriculture Forum.

UPPER AUSTRIAN CRAFT PRIZE

The 26th awarding of the Upper Austrian Craft Prize took place to honour outstanding workmanship. Top quality, innovation and technical skills were shown in all areas of handicraft.

CORONA

Every year the Federation of Austrian Industries in Upper Austria awards a prize in the categories of improving Upper Austria as a place to do business and CSR. For several years, Raiffeisenlandesbank Oberösterreich has been a valuable partner and has helped to put Upper Austria's top companies into the spotlight.

OÖ

N/V

olke

r Wei

hbol

d

Wol

fgan

g K

unas

z-H

erzi

g/ev

entf

oto.

atK

rone

n Ze

itung

/Chr

is K

olle

r

JR P

HO

TOG

RA

PH

Y

Raiffeisenlandesbank Oberösterreich CEO Heinrich Schaller awarding the crystal Pegasus to Michael Teufelberger.

Jakob Auer, Max Hiegelsberger, Michaela Keplinger-Mitterlehner and Franz Fischler

Awarding the most sustainable industrial companies in Austria

The winners of the Upper Austrian Craft Prize 2015

The new Chairman of Young Economy Upper Austria Bernhard Aichinger (right) and his team

44 Annual Report 2015

1. Business development and the economic situation ______________________ 45

2. Report on the company’s prospective trends and risks ________________________________________ 55

3. Research and development __________________________________________ 58

4. Main aspects of the internal control and risk management system _________ 59

Group management report 2015Raiffeisenlandesbank Oberösterreich Aktiengesellschaft

45Raiffeisen Banking Group Upper Austria Raiffeisenlandesbank Oberösterreich Group General Information

Group management report 2015 _ Business development and the economic situation

1.1. Economic background 2015

2015 was another turbulent financial year. Defining events that characterised international developments included the fall in oil prices as well as the extremely lax monetary policy by the European Central Bank (ECB), while a tighter money market policy was implemented in the USA. There were also consid-erable signs of weakness in China and other emerging na-tions, along with a range of ongoing geopolitical tensions. The crisis in Greece dominated the first six months of the year in Europe. This was then followed by the issue of refugees as a particularly dominant topic.

Global economic growth turned out to be somewhat weaker in 2015 than it had been in the previous year. Although perfor-mance improved in the industrialised nations and in particular the USA, the emerging nations suffered from cyclical weak-ness coupled with far-reaching structural problems. Brazil and Russia slipped into a deep recession which was accompanied by high inflationary pressure. The slowdown in the Chinese economy continued as the government and central bank im-plemented stimulus measures in an attempt to counteract this.

The USA once again acted as the engine for the global econ-omy in 2015. Figures from the labour market in particular were consistently very positive. The upturn managed to be consol-idated, which ultimately resulted in implementation of a long discussed reversal in interest rates by the Federal Reserve. Private consumption experienced particularly strong growth in the USA, while the export sector suffered from the strong dollar and the oil industry from the low prices.

The eurozone lost some of its steam once again in the sec-ond half of the year compared with the first half. Growth was based almost exclusively on private consumption, while any propensity to make investments remained restrained. How-ever, early indicators in the middle of the year pointed to more robust economic activity towards the end of the year: numer-ous framework conditions such as favourable financing condi-tions, a weak euro as a result of the lax ECB policy, low costs for raw materials (particularly for crude oil) and significant im-provements in the labour market should help to support the economy.

Inflation in the eurozone was very low to negative as a result of the low cost of raw materials. The ECB attempted to fix medium-term inflation expectations at its goal of close to (but below) 2 per cent with an extremely expansionary monetary policy (lowest interest rates and quantitative easing).

Austria also benefited from the general structural conditions that stimulated the economy (price of oil, ECB policy). Never-theless economic growth in Austria was unable to keep up with the eurozone average for 2014/15. Investment activity by companies only recovered very hesitantly from the second quarter of 2015, while private consumption continued to stag-nate. Analysts expect Austria to catch up with the average eurozone growth levels once again for 2016. The private con-sumption stimulated by the income tax reforms and the ad-ditional expenses for asylum seekers will be critical with this.

Industry in Upper Austria which is highly focused around exports recorded a significant upturn in 2015, and was well above the national average of 1.7 per cent with growth in pro-duction of 6.3 per cent in the first three quarters. The service sector was also on course for growth. Production in the con-struction sector on the other hand fell by around 4 per cent in the first three quarters in 2015 compared to 2014. The labour market proved to be comparatively strong with growth in em-ployment above the Austrian average. Upper Austria still has the second lowest unemployment rate of all the federal states. Analysts in the state expect growth of 2 per cent for the 2016 financial year, which is slightly above the national average, al-though this relies above all on increases in consumption levels and higher demand for investment.

The global economy slowed down again somewhat at the end of 2015. The USA recorded a dip in the economy in the fourth quarter with 0.7 per cent growth in GDP, although this is not expected to persist. Figures from the emerging nations remain weak: there is still no end in sight to the recessions in Brazil and Russia, and growth in China in the fourth quarter was a moder-ate 6.8 per cent. The eurozone recorded growth in GDP of 0.3 per cent in the fourth quarter of 2015, with Spain once again recording the strongest growth at 0.8 per cent. Germany was exactly at the average level at 0.3 per cent, while France (0.2 per cent) and Italy (0.1 per cent) lag further behind. Austrian GDP grew by 0.3 per cent in the fourth quarter of 2015, as had also been the case in the second and third quarters. This re-sults in economic growth of 0.9 per cent for the full year 2015. Investments as well as private consumption and government spending provided support towards year end, although there was a trade deficit.

1.2. Business development

Raiffeisenlandesbank Oberösterreich saw the tasks required due to the turbulent 2015 financial year, which involved

1. Business development and the economic situation

46 Annual Report 2015

historically low interest rates accompanied by a slowdown in the economy, as an opportunity and adapted well to the on-going changes in the structural conditions with a strategy of continuous renewal and sustainable consolidation. Against a backdrop of restrained economic growth and subdued sen-timent among companies and the wider population, it either initiated, continued or implemented a large number of action plans and projects in 2015 with a view to actively managing its costs and risk, providing the basis for the best possible level of support for its customers.

As Austria’s fourth largest bank, Raiffeisenlandesbank Oberösterreich also intends in future to outperform on the high standards imposed on a “significant” bank by the European Central Bank. Particular attention is paid here to compliance with all new statutory regulations, and in laying the foundations for compliance with the statutory requirements that will be im-posed on banks in Austria and the rest of the European Union in future, such as in relation to equity/own funds and risk man-agement. Raiffeisenlandesbank Oberösterreich is also ready to make the appropriate contributions for the deposit guaran-tee and the European resolution funds.