frost & sullivan - economic 360 for vietnam - growth prospects and emerging opportunities

TRANSCRIPT

Economic 360 for Vietnam: Economic 360 for Vietnam: Growth Prospects and Emerging OpportunitiesGrowth Prospects and Emerging Opportunities

RhenuRhenu BhullerBhuller

Vice PresidentVice President

Frost & Sullivan AsiaFrost & Sullivan Asia--PacificPacific

[email protected]@frost.comOctober, October, 20122012

Vietnam—Country Overview

Hanoi

Vinh

Hue

Da Nang

Quy Nhon

331 698 km2divided into 59provinces and 5provincial levelmunicipalities

The 14th most

54 officiallyrecognized ethnicgroups, with Vietcomprising 86% ofthe total population

2Not for Distribution

Quy Nhon

Ho ChiMinh City

The 14 mostpopulous country inthe world with apopulation of 91.5million (est. July,2012) and growthrate of 1.1 percentin 2011.

Urbanization rate togrow about 3.3percent annually,reaching an urbanpopulation of 30million in 2014.

One of world’s top exporters of rice, coffee, cashew nuts and black pepper.

Macro-Economic Indicators, 2011

3Not for Distribution

Macro Economic Indicators: Healthcare

Healthcare Indicators 2010

Population (M) 88.3

Population Growth Rate (%) 1.0

Birth Rate (per 1,000) 17.0

Mortality Rate (per 1,000) 6.8

Life Expectancy (Female) (years) 74.7

Life Expectancy (Male) (years) 69.5

Healthcare Indicators: Vietnam, 2010

4Not for Distribution

Key FeaturesKey Features

• Vietnam’s population size is expected to expand about 9.2 percent from 2006 to 2014,

and is likely to grow 1.0 percent annually from 2010–2014.

• The increase of life expectancy (73.9 years in 2006 to 74.7 years in 2010) have led to

an increase in aging population.

• Vietnam’s population size is expected to expand about 9.2 percent from 2006 to 2014,

and is likely to grow 1.0 percent annually from 2010–2014.

• The increase of life expectancy (73.9 years in 2006 to 74.7 years in 2010) have led to

an increase in aging population.

Life Expectancy (Male) (years) 69.5

Source: Datamonitor, Worldbank, http://vietnam.unfpa.org, Frost & Sullivan a

Macro Economic Indicators: Vehicle Ownership

5Not for Distribution

One of the world’s fastest-growing economies - 2010 GDP growth rate @ 6.78%, GDP per capita at ~ US $1,200

Vietnam’s economy has witnessed a structural change from a planned economy to a market-oriented economy. Between 2000 and 2008, several reforms were taken to liberalize and open up the economy to foreign investment.

6Not for Distribution

Government Development Plan: Key SectoralObjectives of the FYP (2006-2010)

7Not for Distribution

Vietnam’s total export revenue in 2010 reached US $71.6 billion, a 25.5% increase compared with that of 2009

15 15IMPORTS EXPORTS

8Not for Distribution

0

5

10

15

0

5

10

15

2010 (US$Billion) 2009 (US$Billion)

FDI in Vietnam has increased considerably. In 2010, foreign investors registered capital of ~ US$18.6 billion, in which the actual disbursed capital came to $11 billion

9Not for Distribution

Opportunities in Vietnam

10Not for Distribution

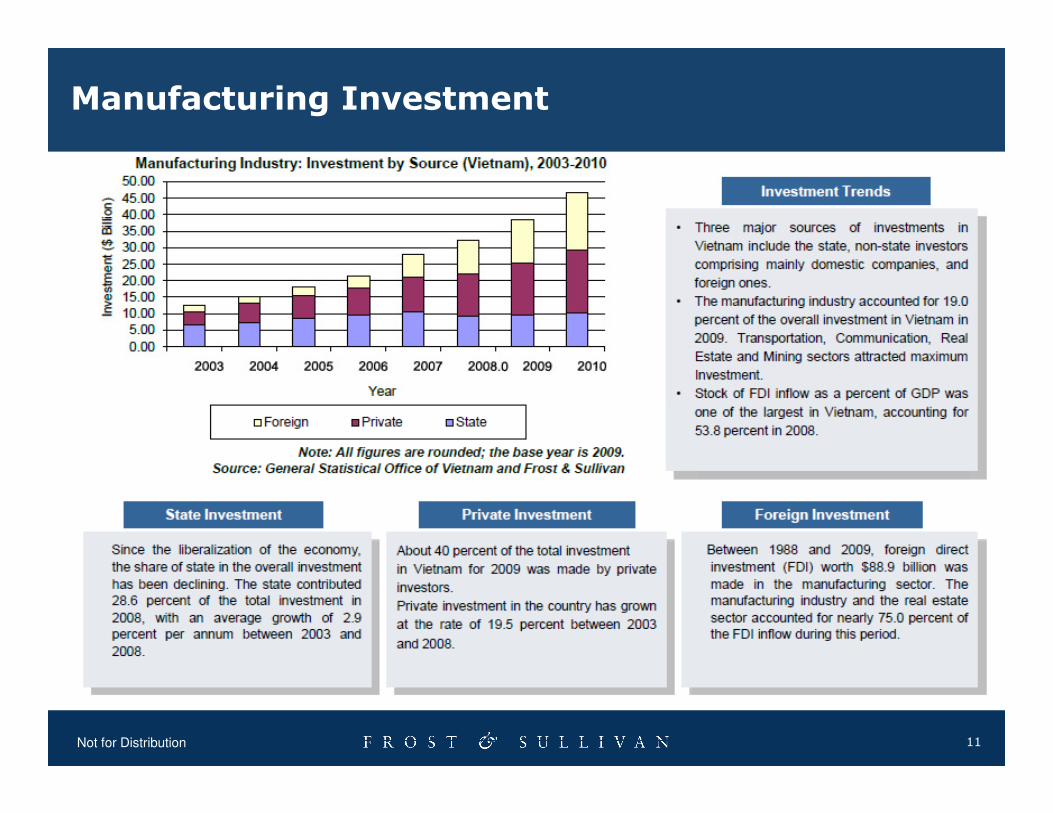

Manufacturing Investment

11Not for Distribution

Manufacturing: Business Opportunities

12Not for Distribution

ICT: A developing market in modern Vietnam

13Not for Distribution

ICT Development

14Not for Distribution

Telecommunications Market

15Not for Distribution

ICT Industry Business Opportunities, 2010-2013

16Not for Distribution

Tourism and Aviation

17Not for Distribution

Tourism & Aviation Sector: Business Opportunities

18Not for Distribution

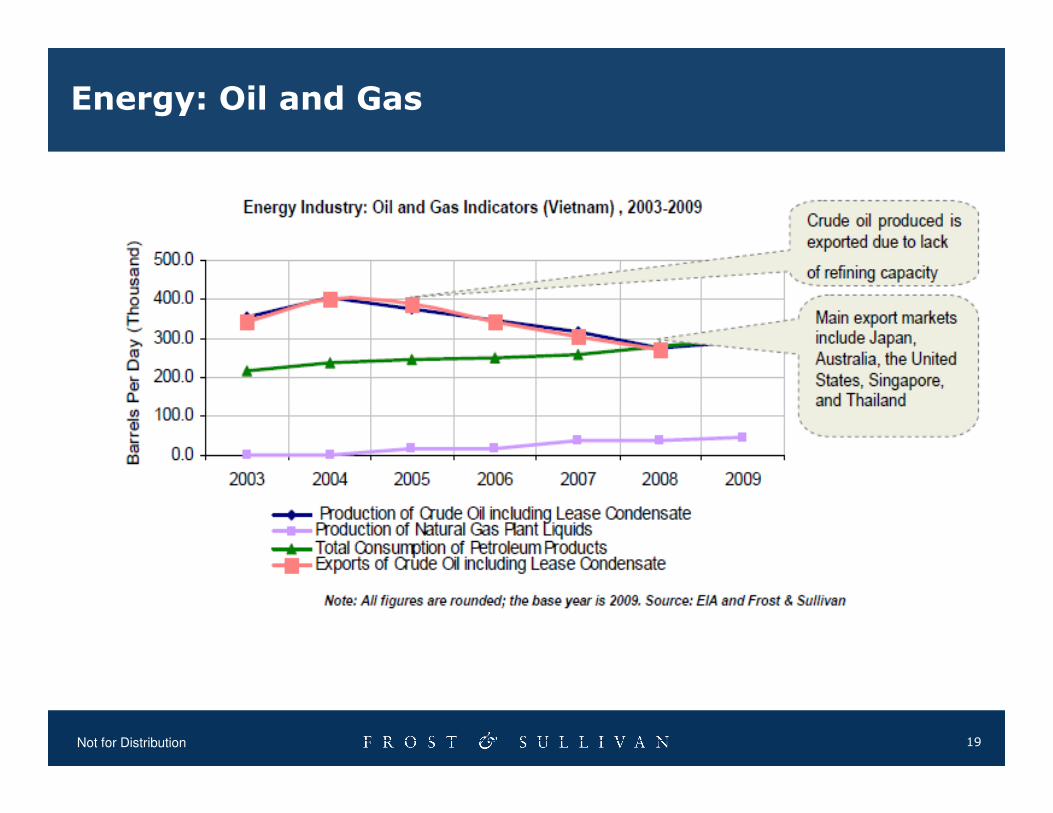

Energy: Oil and Gas

19Not for Distribution

Energy: Key Future Projects

20Not for Distribution

Energy: Government plans and targets

21Not for Distribution

Renewable Energy

22Not for Distribution

Energy Industry: Business Opportunities

23Not for Distribution

Infrastructure: Building Construction Market

24Not for Distribution

Transportation

25Not for Distribution

Transport Infrastructure: Vietnam has a 256,231 km of Road Network

26Not for Distribution

Transport Infrastructure: Future Developments

27Not for Distribution

Planned investment in mass transit

28Not for Distribution

Infrastructure: Business Opportunities

29Not for Distribution

Vietnam: Health Care Delivery System

Healthcare services in Vietnam are dominated by the public sector and as of 2009, approximately 93.0 percent of hospitals were public.

Healthcare Delivery System: Vietnam, 2010

Government

MINISTRY OF HEALTH•14 Department and Administration•The Cabinet•Inspectorate

Provincial People’s Committee

PROVINCIAL HEALTH SERVICE

Professional Units under Ministry •Curative:30 hospitals with beds

•Preventive:17 institutes or centres

•Quality Control: 5 institutes or centres

•Training:14 schools or colleges

•Centre for health education and communication

:17 units

Professional Units under the PHS •General and specialized hospitals for curative care

•Preventive Health Centres

30Not for Distribution

Public sector offers healthcare services through four tiers: commune, district, provincial, and central. The Ministry of Health (MOH), which is part of the central tier, handles health policies and administration.

Source: Department of Health, Vietnam; Frost & Sullivan analysis.

SERVICE•Office•Inspectorate

PROVINCIAL HEALTH SERVICE•Office•Inspectorate

People’s Committees at District

People’s Committees at Communes

COMMUNAL HEALTH CENTRES•Head•Healthcare Workers

•Preventive Health Centres

•Quality Health Centres

•Training Middle Level Schools or Colleges

•Centre for health education and communication

•District General

hospitals

•Clinics

•District Preventive

Health Centres

Village Health Workers

Healthcare Expenditure

Government and Private Expenditure on Health: Vietnam, 2006–2012

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

He

alt

hc

are

Ex

pe

nd

itu

re($

Bill

ion

)

31Not for Distribution

• Driven primarily by the state's healthcare insurance scheme, the share of total healthcarespending accounted for by the public sector will continue to rise.

• The share of total out-of-pocket private healthcare expenditure is expected to fall in thecoming years. According to WHO, in 2008, 90.0 percent of total private healthcare expenditurewas out of pocket. However, due to growing concerns over long-term health protection, privatehealthcare insurance will become increasingly popular, a trend that will be supported by awider array of health insurance options and greater prosperity in urban areas.

Source: WHO, Frost & Sullivan analysis.

2006 2007 2008 2009 2010 2011 2012

Private Expenditure 2.63 2.98 3.98 4.19 4.53 4.77 5.02

Government Expenditure

1.29 1.99 2.05 2.52 2.76 3.01 3.25

0.00

Healthcare: Business Opportunities

In Vietnam, new health service facilities are expected to be charged an enterprise income tax of 10percent rather than the previous 28 percent.

The quality of public hospitals in Vietnam is likely to improve following the establishment of private hospitals by Singapore-based Thomson International and Pacific Healthcare, Malaysia-based Columbia Asia, and the French Hospital of Hanoi, owned by the French company Eukaria S.A.

32Not for Distribution

The Vietnamese government’s healthcare development plan, extending to 2020, aims for a doctor-patient ratio of 8:10,000, pharmacists of 2:10,000, and 25 hospital beds per 10,000 patients.

Vietnam’s healthcare expenditure will grow over the next five years with its healthcare spending as a percent of GDP surpassing most ASEAN countries and growing up to 8.3% of the GDP in 2014.

The Vietnamese government aims to modernize traditional medicine by 2020. According to Ministry of Health, hospitals that offer traditional alternatives to patients will receive new equipment in 2015

Source: Frost & Sullivan analysis.

Case Study: Unilever Vietnam – Key Learningsfor Success

LONG TERM INVESTMENT

LOCAL PARTNERSHIPS SKILLS TRANSFER

33Not for Distribution

NATIONAL PRIORITIES BEYOND URBAN

Follow Frost & Sullivan on Facebook, LinkedIn, SlideShare, and Twitter

http://www.facebook.com/FrostandSullivan

http://www.linkedin.com/companies/4506

34Not for Distribution

http://twitter.com/frost_sullivan

http://www.linkedin.com/companies/4506

http://www.slideshare.net/FrostandSullivan

Additional Information

Donna Jeremiah

Director Corporate Communications, Asia [email protected]: +61 (02) 8247 8927

Rhenu Bhuller

Vice President, Healthcare PracticeAsia Pacific [email protected]

35Not for Distribution

Jessie Loh

ManagerCorporate Communications, Asia [email protected]. (65) 6890 0942

Carrie Low

ExecutiveCorporate Communications, Asia [email protected]. (603) 6204 5910