frankfurt am main 28 november 2006 - nordex · projects to review customer layout supporting...

TRANSCRIPT

Nordex AGEigenkapitalforum

Frankfurt am Main28 November 2006

Page 2

Content

Market Development 2

Business Performance in 20063

4 Outlook

5 Appendix

Company Profile 1

Page 3

Well Positioned for Strong Growth: Value Chain

Wind farmsystem

planning

Technical realisation

Wind farm operation

Service and maintenance

Project development

marketing financing

� Micrositing of 100% of signed projects to review customer layout

� Supporting customers (co-development) to receive necessary approvals and to optimize the park layout

� Core business: WTG assembly, production of selected components, installation on site, initial operation

� 2200 turbines are currently under Nordex service

� Full service contract offering up to 9+3 years duration

� Market leader in France (high margin potential)

� Development of first commercially financed project in China

� Additional service offering: increasing demand due to new wind farm investors, which are only interested in stable cash flow

Page 4

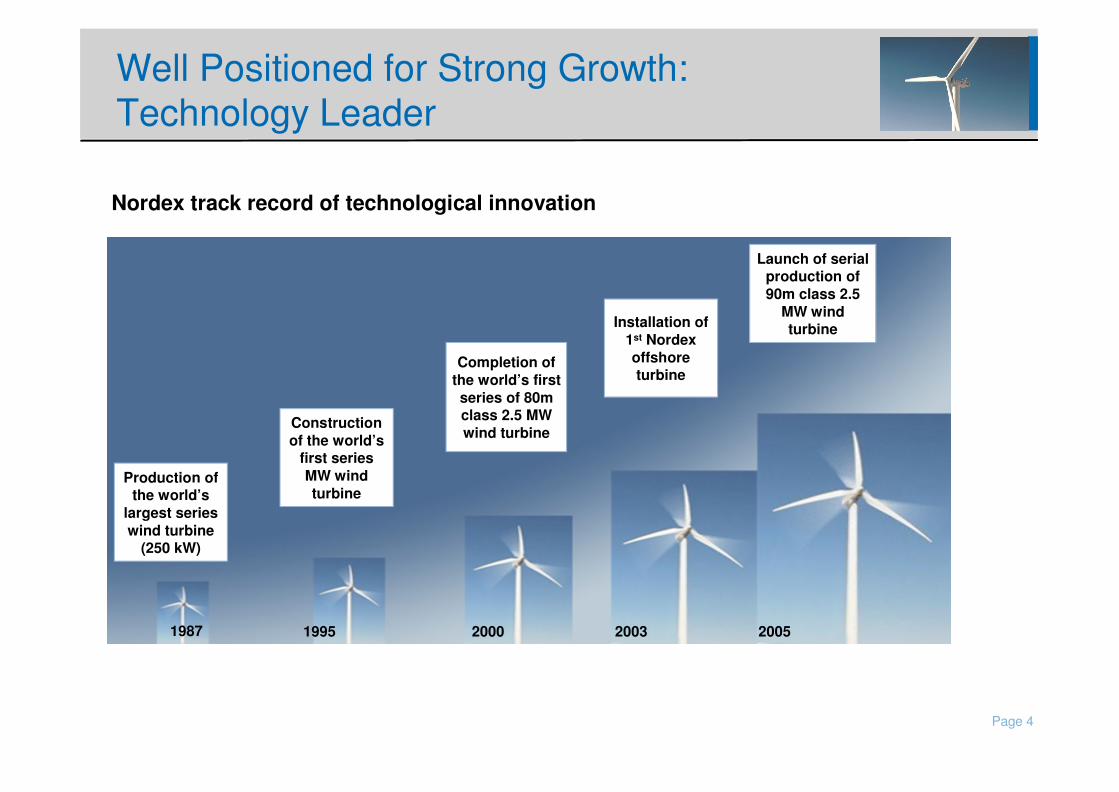

Well Positioned for Strong Growth: Technology Leader

Nordex track record of technological innovation

Production of the world’s

largest series wind turbine

(250 kW)

Construction of the world’s

first series MW wind turbine

Completion of the world’s first series of 80m class 2.5 MW wind turbine

Installation of 1st Nordex offshore turbine

Launch of serial production of 90m class 2.5

MW wind turbine

1987 1995 2000 2003 2005

Page 5

Nordex Worldwide

Headquarter: Hamburg

Production: RostockBaodingYinchuanDongyingXi´an

Nordex France: Paris

Nordex UK: Manchester

Nordex Italia: Milan

Nordex Scandinavia: Kolding

Nordex China: Beijing

Nordex Iberica: Barcelona

Page 6

Content

Market Development 2

Business Performance in 20063

4 Outlook

5 Appendix

Company Profile 1

Page 7

Key Growth Drivers

Growing Energy

Consumption

Rising Energy Costs

Favourable Regulatory

Environment

� Economic growth in 2006 expected to support oil demand further (+2.2% vs. 2005 in volume terms)

� IEA estimates worldwide energy demand may double from 2002 to 2030, especially in Asia

� Oil price more than tripled since 2001, reaching all-time high in summer 2006 with in excess of US$74/barrel

� Market forward curve for oil swaps implies prices at a level of US$70-75 for next three years

� Kyoto protocol supports renewable energy to help countries achieve their targets

� Regulatory outlook worldwide positive:

� PTC in US extended until end of 2007; widely expected to be extended again

� Supportive new renewable energy law in China, France (update), Ireland, Greece.

� European Parliament reiterates position on renewable energy targets (20% by 2020)

Source: Goldman Sachs Commodity Research, Bundesverband Wind Energie, Merrill Lynch Commodities Research

Demand for wind energy driven by renewables regulations, price competitiveness of wind energy and strong worldwide energy demand

Generation Cost in € /MWh

0 50 100 150 200 250

Advanced Nuclear

Conv. Hydro

Geothermal

IGCC - Coal

Wind

Advanced Gas/Oil CC

Biomass

Conv. Gas/Oil CC

Solar Thermal

Photovoltaic

€ /MWh

Page 8

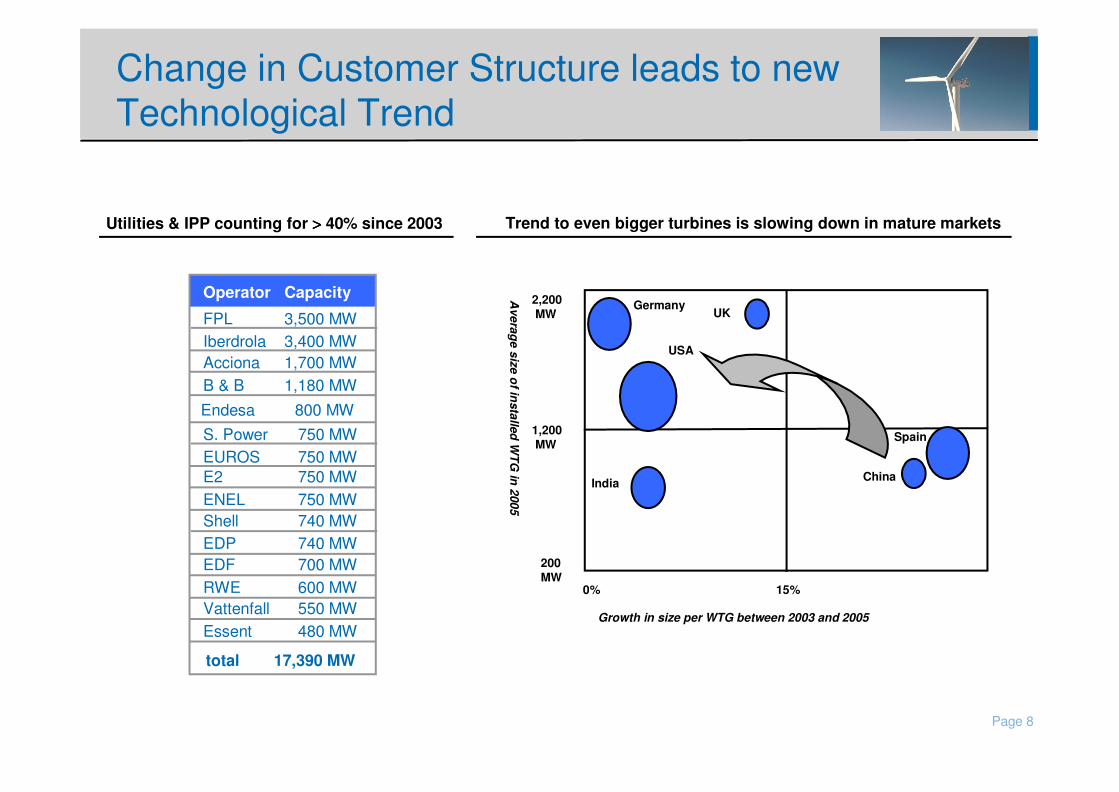

Change in Customer Structure leads to new Technological Trend

Operator Capacity

FPL 3,500 MWIberdrola 3,400 MWAcciona 1,700 MWB & B 1,180 MW

S. Power 750 MWEUROS 750 MWE2 750 MWENEL 750 MWShell 740 MWEDP 740 MWEDF 700 MWRWE 600 MWVattenfall 550 MWEssent 480 MW

total 17,390 MW

Endesa 800 MW

200 MW

1,200MW

2,200MW

15%

Germany

China

Spain

India

UK

USA

Average size of installed W

TG in 2005

Growth in size per WTG between 2003 and 2005

0%

Trend to even bigger turbines is slowing down in mature marketsUtilities & IPP counting for >>>> 40% since 2003

Page 9

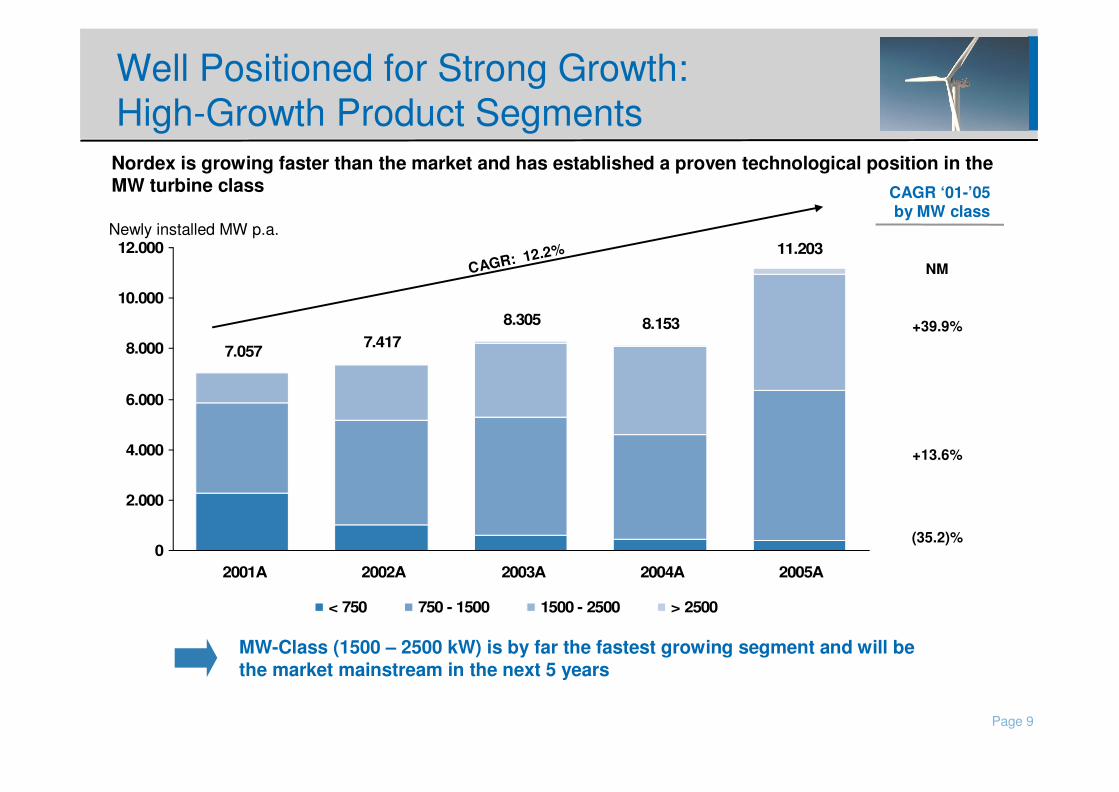

Well Positioned for Strong Growth: High-Growth Product Segments

MW-Class (1500 – 2500 kW) is by far the fastest growing segment and will be the market mainstream in the next 5 years

Newly installed MW p.a.11.203

8.1538.3057.4177.057

0

2.000

4.000

6.000

8.000

10.000

12.000

2001A 2002A 2003A 2004A 2005A

< 750 750 - 1500 1500 - 2500 > 2500

CAGR: 12.2%

CAGR ‘01-’05by MW class

NM

+39.9%

+13.6%

(35.2)%

Nordex is growing faster than the market and has established a proven technological position in the MW turbine class

Page 10

Content

Market Development 2

Business Performance in 20063

4 Outlook

5 Appendix

Company Profile 1

Page 11

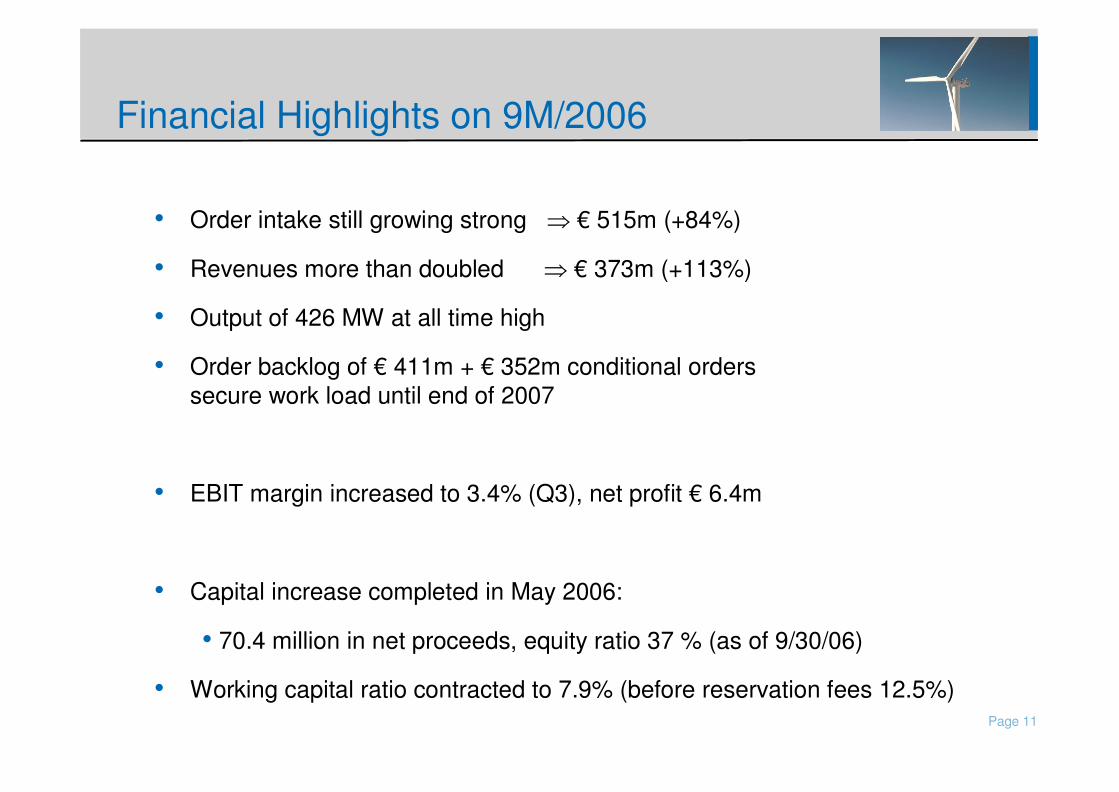

Financial Highlights on 9M/2006

• Order intake still growing strong ⇒ € 515m (+84%)

• Revenues more than doubled ⇒ € 373m (+113%)

• Output of 426 MW at all time high

• Order backlog of € 411m + € 352m conditional orders secure work load until end of 2007

• EBIT margin increased to 3.4% (Q3), net profit € 6.4m

• Capital increase completed in May 2006:

• 70.4 million in net proceeds, equity ratio 37 % (as of 9/30/06)

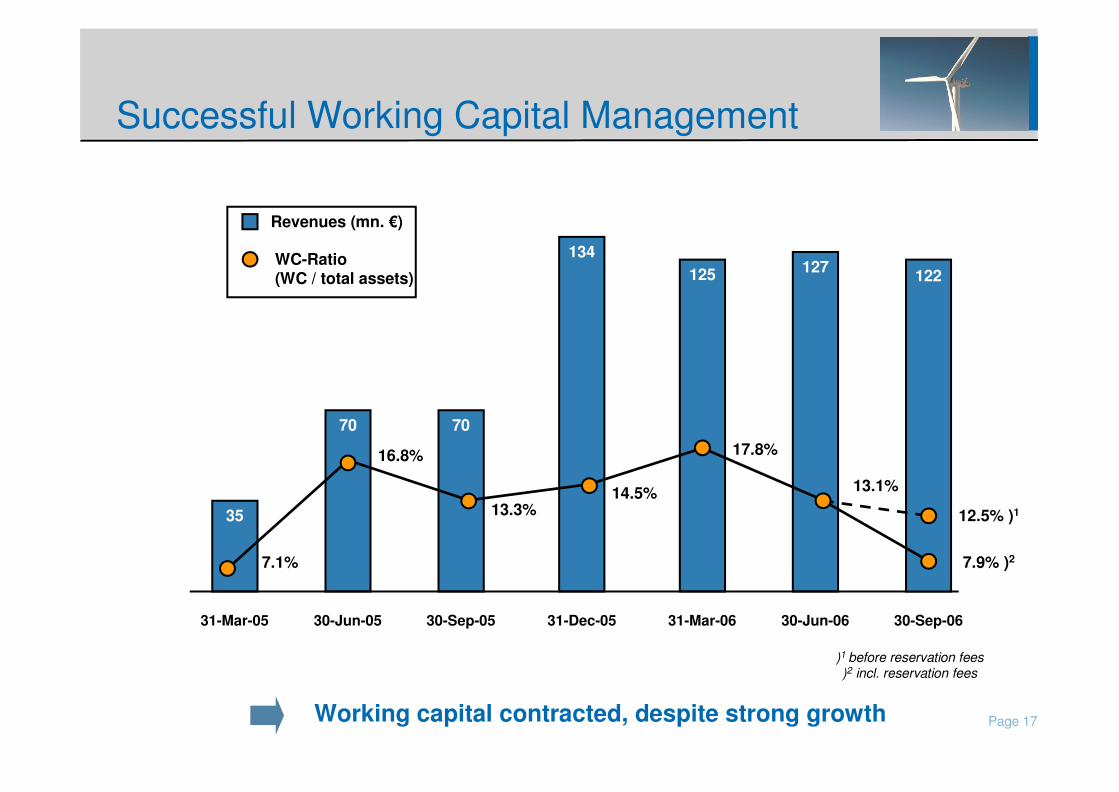

• Working capital ratio contracted to 7.9% (before reservation fees 12.5%)

Page 12

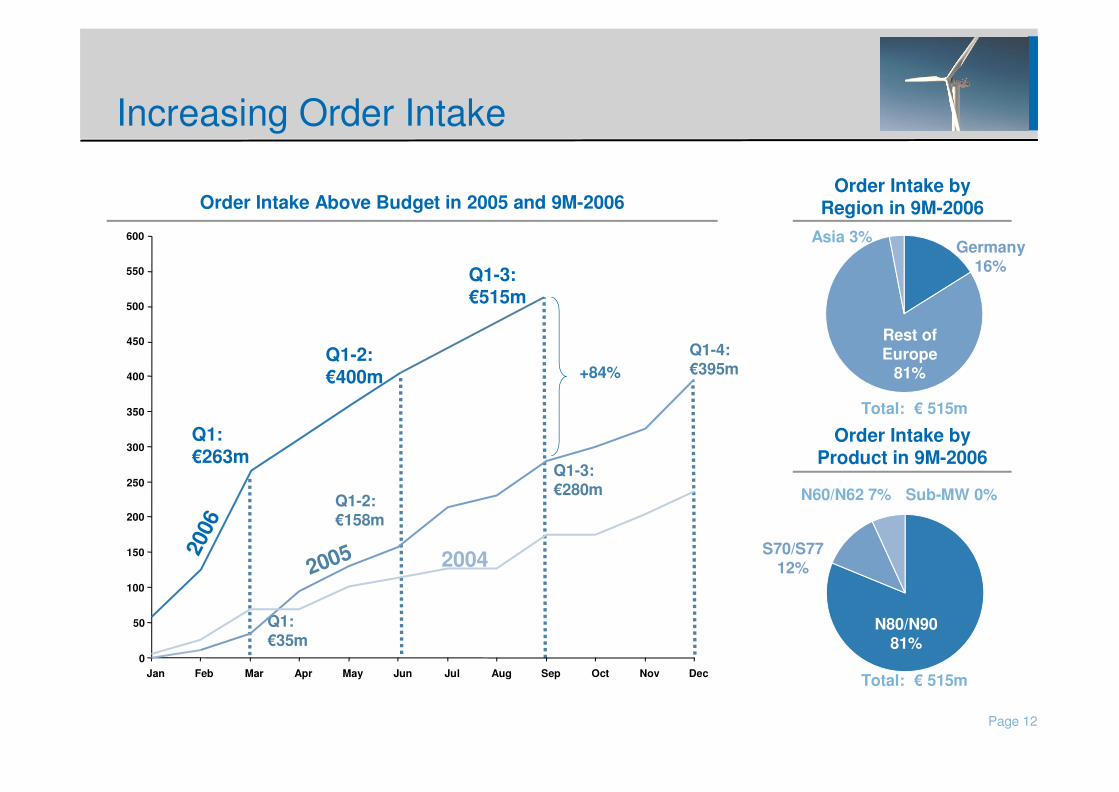

Increasing Order Intake

Order Intake Above Budget in 2005 and 9M-2006

Germany 16%

Order Intake by Region in 9M-2006

Rest of Europe

81%

Asia 3%

Total: € 515m

Order Intake by Product in 9M-2006

Total: € 515m

N80/N90 81%

N60/N62 7% Sub-MW 0%

S70/S77 12%

Q1: € 35m

Q1-2: € 158m

Q1-3: € 280m

Q1-4: € 395m

Q1: € 263m

20052006

+84%

2004

Q1-2: € 400m

0

50

100

150

200

250

300

350

400

450

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

500

550

600

Q1-3: € 515m

Page 13

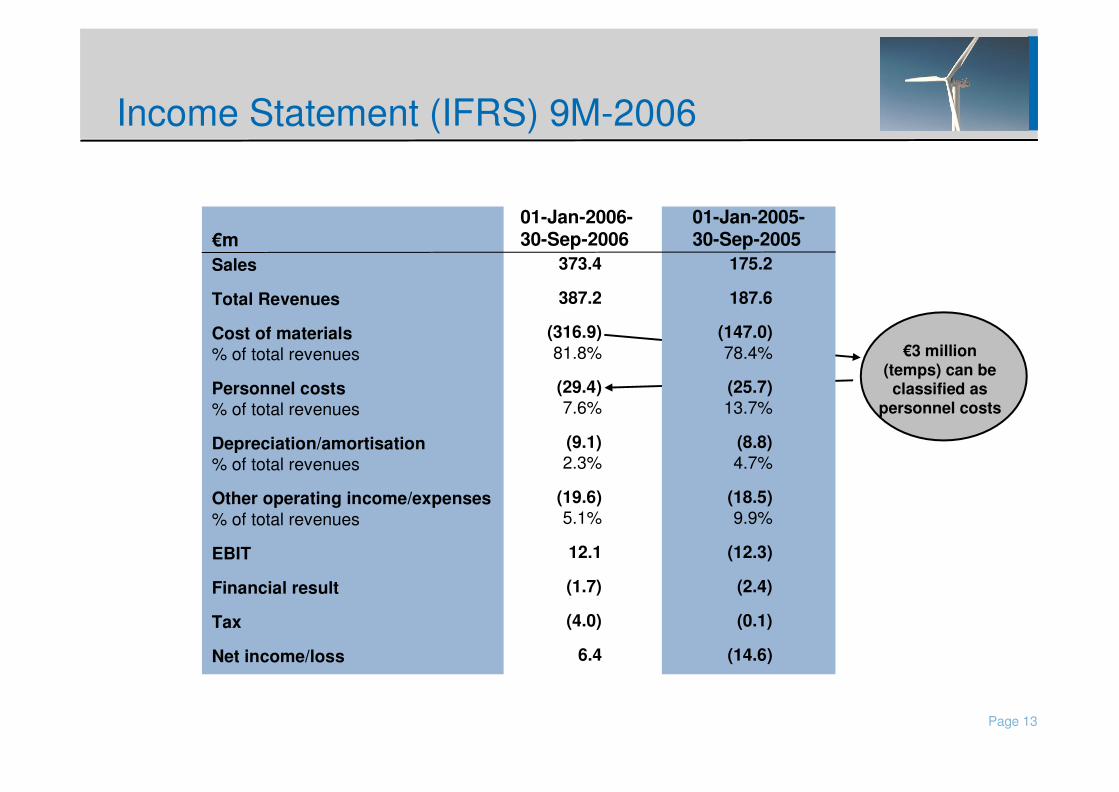

Income Statement (IFRS) 9M-2006

01-Jan-2006-30-Sep-2006€ m

Sales

Total Revenues

Cost of materials% of total revenues

Personnel costs% of total revenues

Depreciation/amortisation% of total revenues

Other operating income/expenses% of total revenues

EBIT

Financial result

Tax

Net income/loss

373.4

387.2

(316.9)81.8%

(29.4)7.6%

(9.1)2.3%

(19.6)5.1%

12.1

(1.7)

(4.0)

6.4

01-Jan-2005-30-Sep-2005

175.2

187.6

(147.0)78.4%

(25.7)13.7%

(8.8)4.7%

(18.5)9.9%

(12.3)

(2.4)

(0.1)

(14.6)

€ 3 million (temps) can be classified as

personnel costs

Page 14

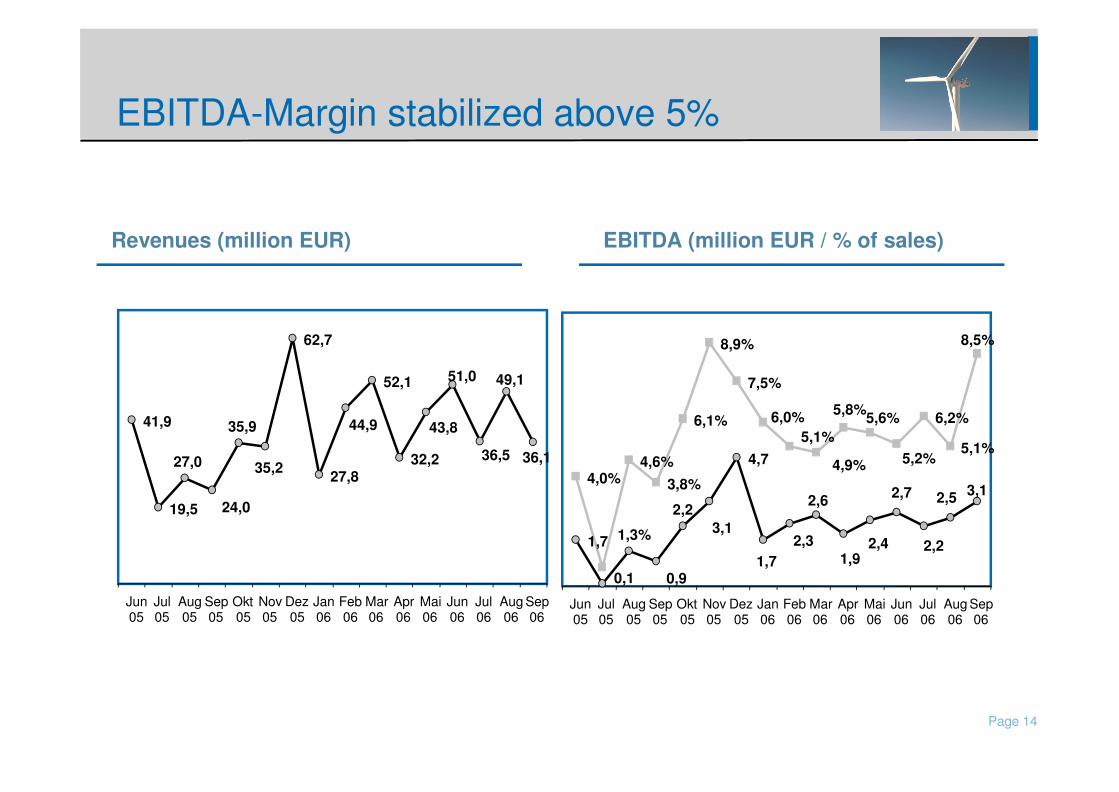

EBITDA-Margin stabilized above 5%

Revenues (million EUR) EBITDA (million EUR / % of sales)

0,1

4,7

1,71,91,7

2,63,12,5

2,2

2,7

2,42,33,1

2,2

0,9

1,3%

4,0%4,6%

3,8%

6,1%

8,9%

7,5%

6,0% 6,2%

5,1%5,1%

4,9% 5,2%

5,6%5,8%

8,5%

Jun05

Jul05

Aug05

Sep05

Okt05

Nov05

Dez05

Jan06

Feb06

Mar06

Apr06

Mai06

Jun06

Jul06

Aug06

Sep06

41,9

19,5

62,7

27,8

52,1

32,2 36,1

49,1

36,5

51,0

43,844,9

35,2

35,9

24,0

27,0

Jun05

Jul05

Aug05

Sep05

Okt05

Nov05

Dez05

Jan06

Feb06

Mar06

Apr06

Mai06

Jun06

Jul06

Aug06

Sep06

Page 15

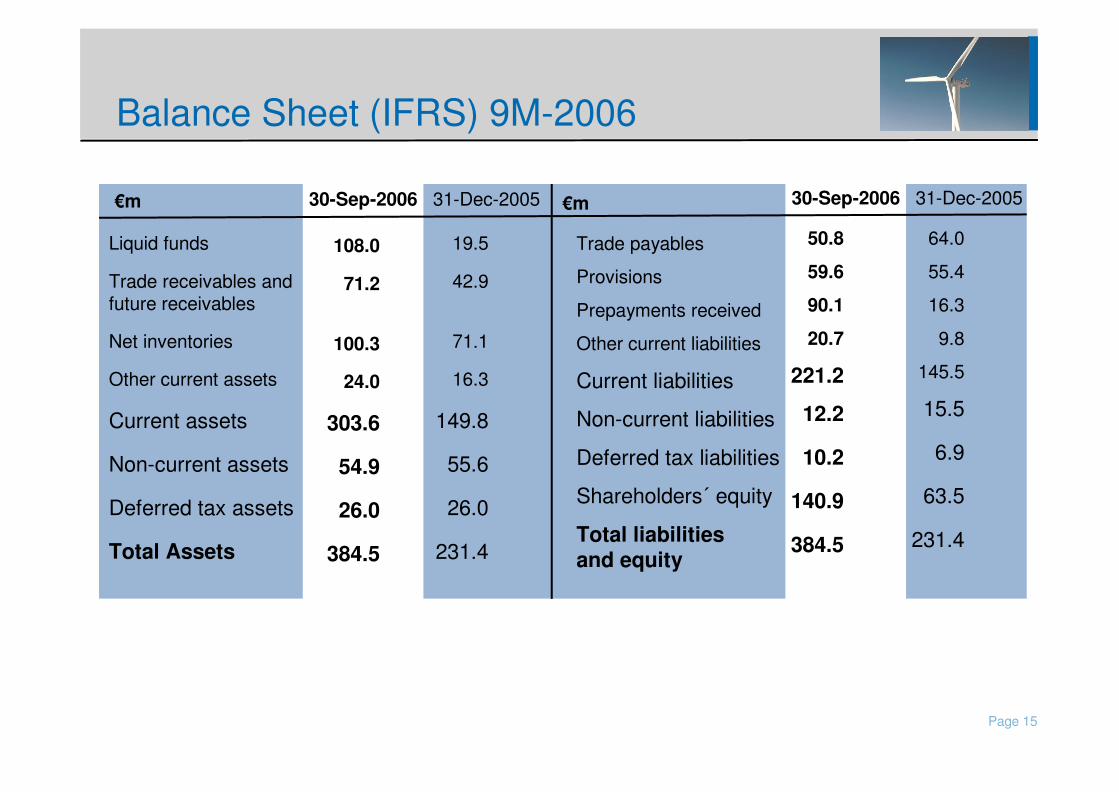

Balance Sheet (IFRS) 9M-2006

€ m 30-Sep-2006 31-Dec-2005

Liquid funds

Trade receivables and future receivables

Net inventories

Other current assets

Current assets

Non-current assets

Deferred tax assets

Total Assets

Trade payables

Provisions

Prepayments received

Other current liabilities

Current liabilities

Non-current liabilities

Deferred tax liabilities

Shareholders´ equity

Total liabilities and equity

19.5

42.9

71.1

16.3

149.8

55.6

26.0

231.4

108.0

71.2

100.3

24.0

303.6

54.9

26.0

384.5

30-Sep-2006 31-Dec-2005

50.8

59.6

90.1

20.7

221.2

12.2

10.2

140.9

384.5

64.0

55.4

16.3

9.8

145.5

15.5

6.9

63.5

231.4

€ m

Page 16

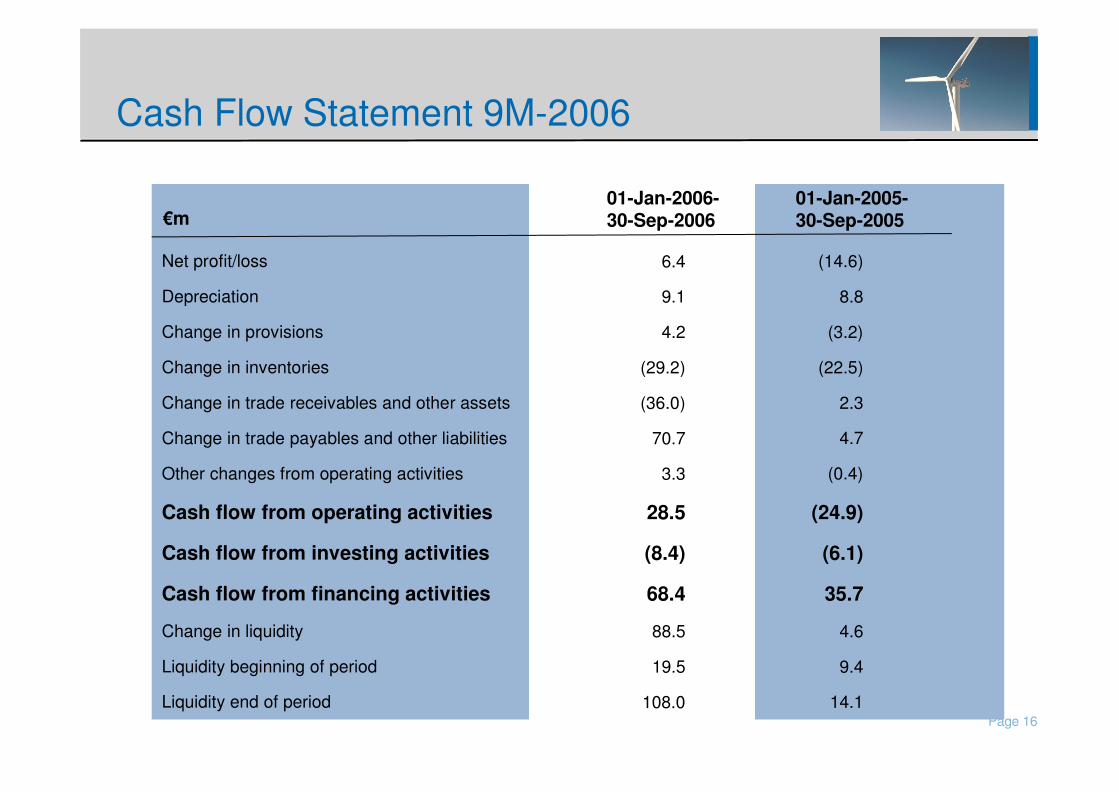

Cash Flow Statement 9M-2006

01-Jan-2006-30-Sep-2006

Net profit/loss

Depreciation

Change in provisions

Change in inventories

Change in trade receivables and other assets

Change in trade payables and other liabilities

Other changes from operating activities

Cash flow from operating activities

Cash flow from investing activities

Cash flow from financing activities

Change in liquidity

Liquidity beginning of period

Liquidity end of period

01-Jan-2005-30-Sep-2005

(14.6)

8.8

(3.2)

(22.5)

2.3

4.7

(0.4)

(24.9)

(6.1)

35.7

4.6

9.4

14.1

6.4

9.1

4.2

(29.2)

(36.0)

70.7

3.3

28.5

(8.4)

68.4

88.5

19.5

108.0

€ m

Page 17

Successful Working Capital Management

31-Mar-05 30-Jun-05 30-Sep-05 31-Dec-05 31-Mar-06 30-Jun-06

35

70 70

134125 127

7.1%

16.8%

13.3%14.5%

17.8%

13.1%

Working capital contracted, despite strong growth

WC-Ratio(WC / total assets)

Revenues (mn. € )

122

12.5% )1

7.9% )2

)1 before reservation fees )2 incl. reservation fees

30-Sep-06

Page 18

Content

Market Development 2

Business Performance in 20063

4 Outlook

5 Appendix

Company Profile 1

Page 19

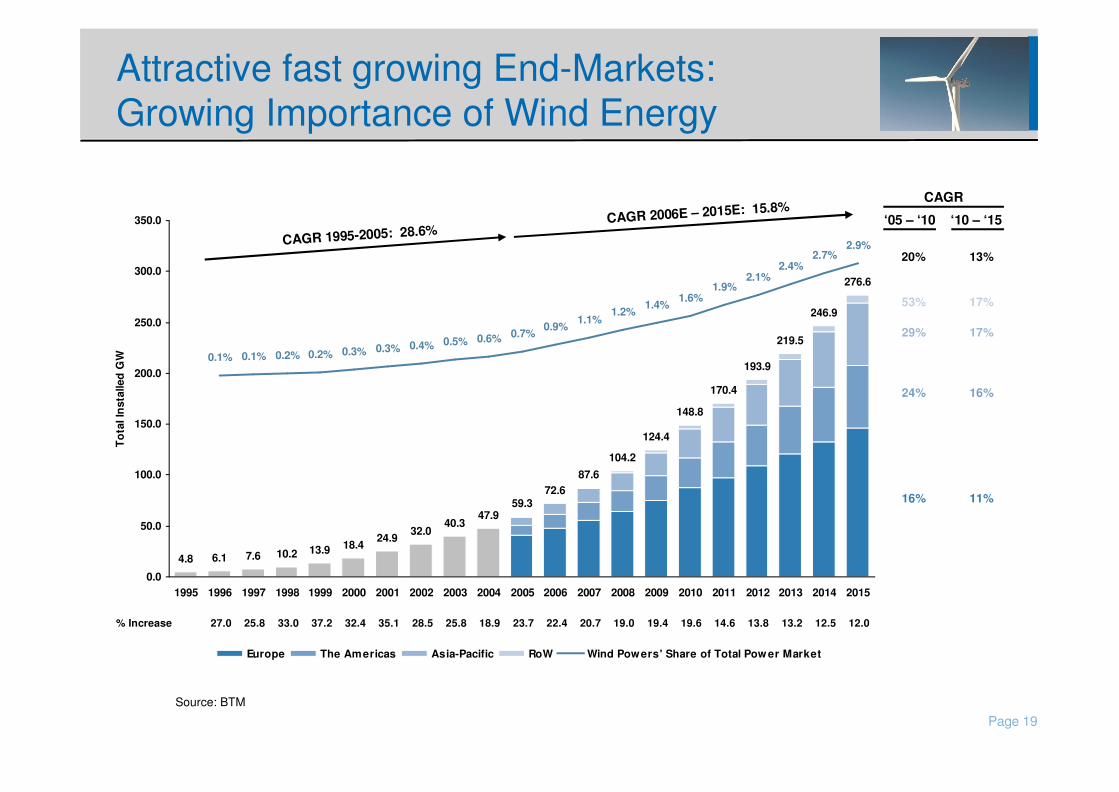

Attractive fast growing End-Markets: Growing Importance of Wind Energy

4.8 6.1 7.6 10.2 13.9 18.424.9

32.040.3

47.959.3

72.687.6

104.2

124.4

148.8

170.4

193.9

219.5

246.9

276.6

0.1% 0.1% 0.2% 0.2% 0.3% 0.3% 0.4% 0.5% 0.6% 0.7%0.9%

1.1%1.2%

1.4%1.6%

1.9%2.1%

2.4%2.7%

2.9%

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

To

tal I

nst

alle

d G

W

Europe The Americas Asia-Pacific RoW Wind Powers' Share of Total Pow er Market

CAGR 1995-2005: 28.6%CAGR 2006E – 2015E: 15.8%

12.012.513.213.814.619.619.419.020.722.423.718.925.828.535.132.437.233.025.827.0% Increase

CAGR

‘05 – ‘10 ‘10 – ‘15

53% 17%

29% 17%

24% 16%

16% 11%

13%20%

Source: BTM

Page 20

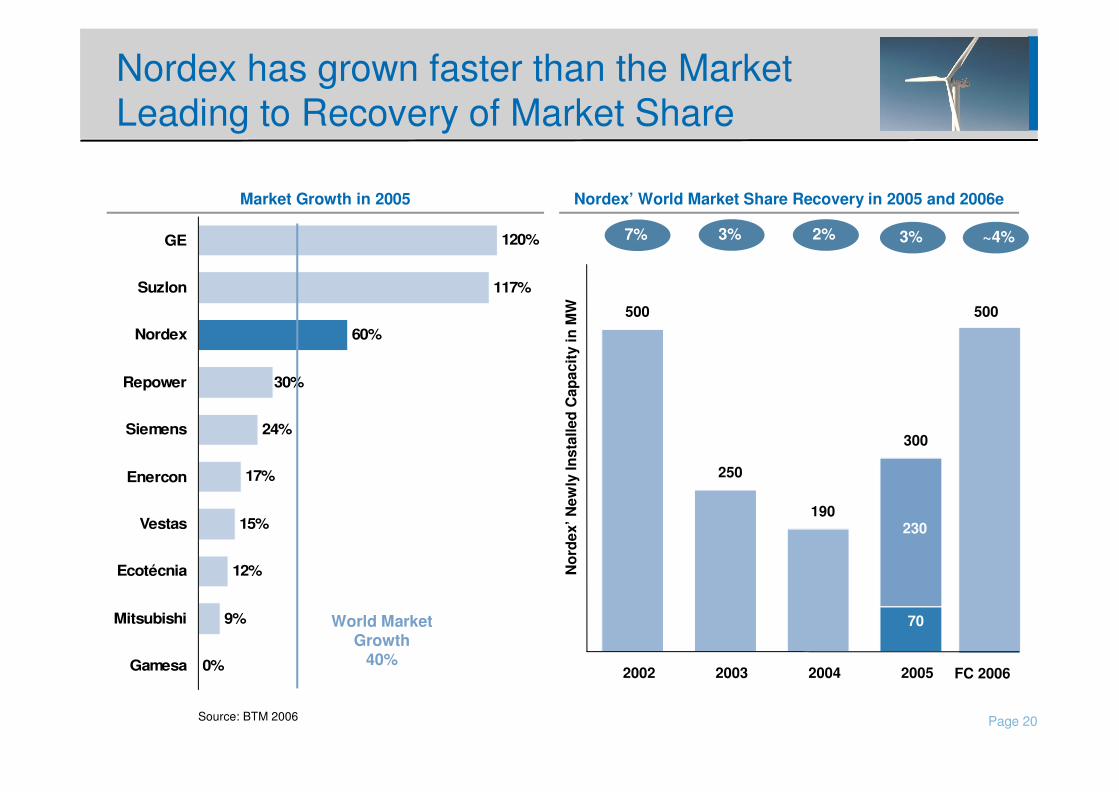

Nordex has grown faster than the Market Leading to Recovery of Market Share

0%

9%

12%

15%

17%

24%

60%

117%

120%

30%

Gamesa

Mitsubishi

Ecotécnia

Vestas

Enercon

Siemens

Repower

Nordex

Suzlon

GE

Market Growth in 2005 Nordex’ World Market Share Recovery in 2005 and 2006e

7% 3% 2% 3%

2H

1HWorld Market

Growth40%

Source: BTM 2006

Nor

dex’

New

ly In

stal

led

Cap

acity

in M

W

70

230

500

250

190

300

2002 2003 2004 2005

500

FC 2006

~4%

Page 21

Market Initiatives for International Expansion

China: � Set-up of local production

� Local partners to secure order intake

� Increase of market share

� Intensify projects developed,

� Increase market share

� Increase market share

� Market entry

� Market re-entry

Country Activity

USA:

France:

UK:

Italy:

Implementation

� 2nd blade production: Start 1/2007

� JV assembly: Start 11/2006

� Supply chain: 70% localised

� Rise in installation 2006e to ~300 MW

� New orders € 226m in 2006

� € 110m order intake from UK in 2006

� Expected market share in 2006 >10%

� € 73m order intake from Italy in 2006

� 1st turbine in 2007 (test site)

� 1st contract in 2007 expected

Page 22

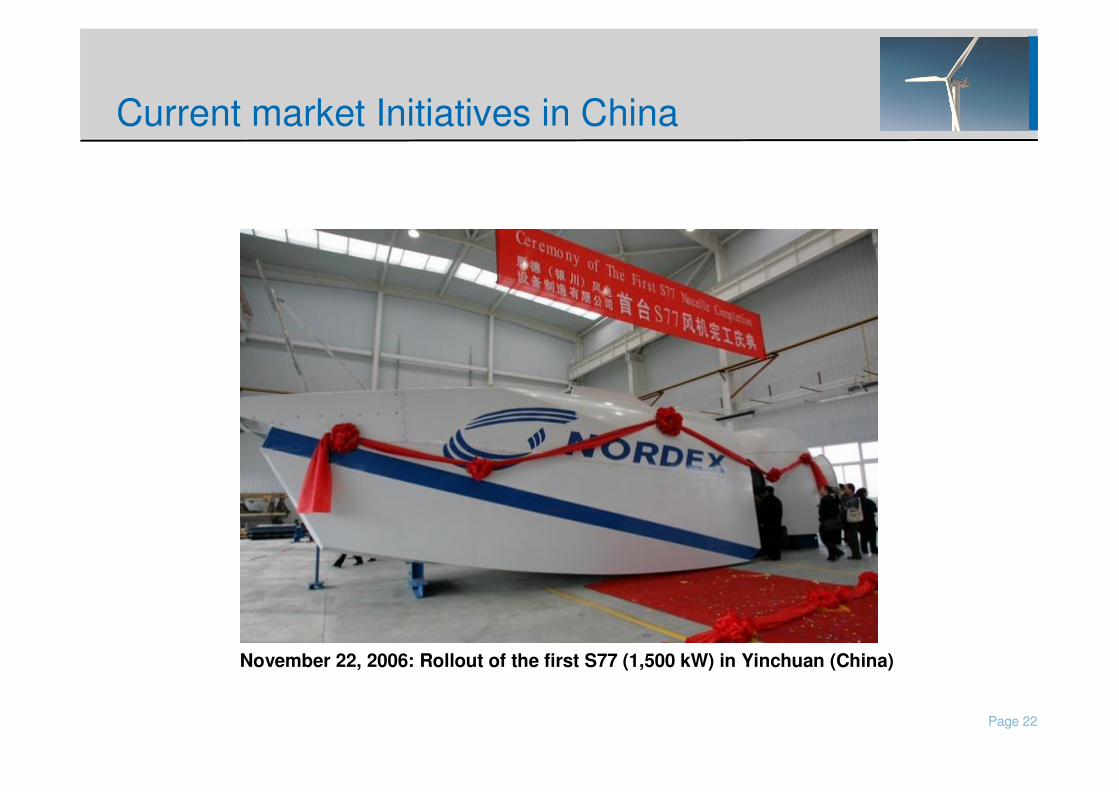

Current market Initiatives in China

November 22, 2006: Rollout of the first S77 (1,500 kW) in Yinchuan (China)

Page 23

Outlook 2006

� Projected revenues secured by order backlog:

� 100% of 2006 revenues secured by unconditional orders

� Unconditional and conditional orders secure workload until end of 2007

� Mid-term annual growth target of 50%

9M-2006 2006e

Order Intake € 515m ≥€ 700m

(Y-on-Y) +84% +77%

Revenues € 373m ≥€ 500m

(Y-on-Y) +113% 62%

EBIT Margin 3.1% ≥3.0%

Page 24

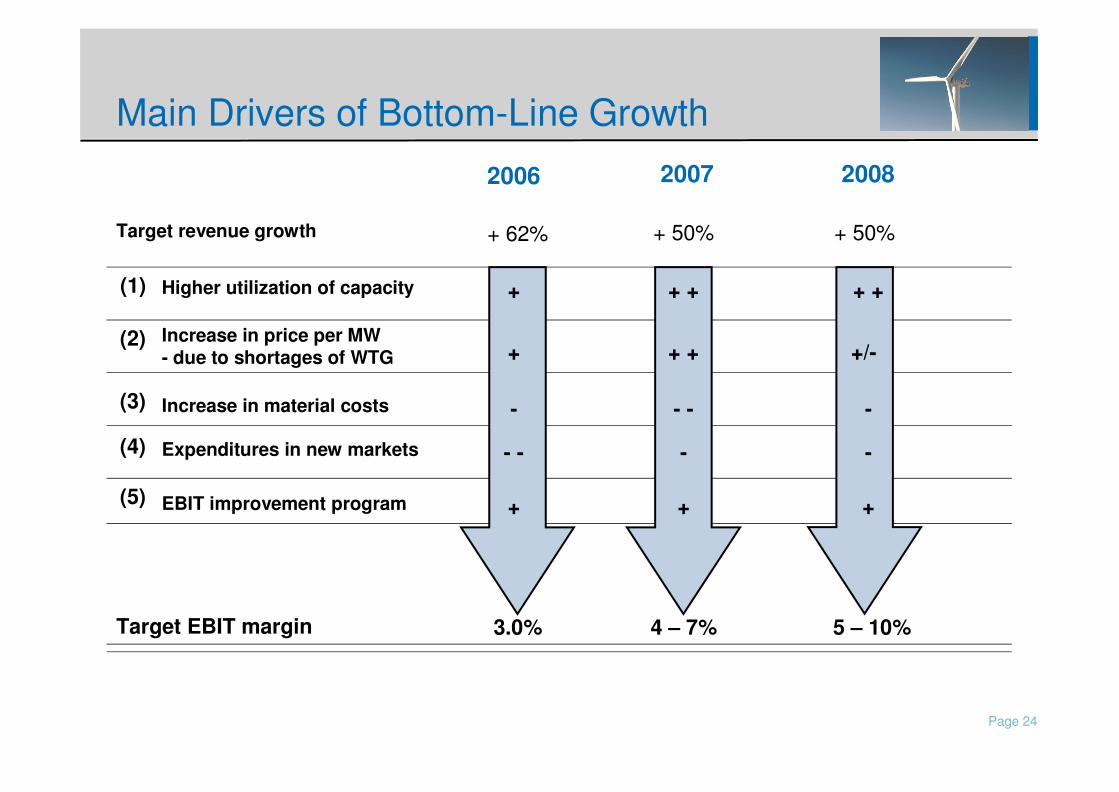

Main Drivers of Bottom-Line Growth

Increase in price per MW - due to shortages of WTG

2006 2007 2008

+ + + +/-

EBIT improvement program + + +

Increase in material costs - - - -

Expenditures in new markets - - - -

Target EBIT margin 3.0% 4 – 7% 5 – 10%

Target revenue growth + 62% + 50% + 50%

(1) Higher utilization of capacity + + + + +

(2)

(3)

(4)

(5)

Page 25

• Nordex has left the restructuring phase, on a sustainable basis

• Arrangements have been implemented to recover market share. Also in 2006, Nordex will grow faster than the market

• Measures to preparing Nordex for an international business volume of € 1bn in 2008 are right on track

• Further EBIT improvement steps will lead to sustainable profitability on the high end of our industry benchmark

• Strategic plan for the years beyond 2008 is in process of consolidation

Summary

Page 26

Content

Market Development 2

Business Performance in 20063

4 Outlook

5 Appendix

Company Profile 1

Page 27

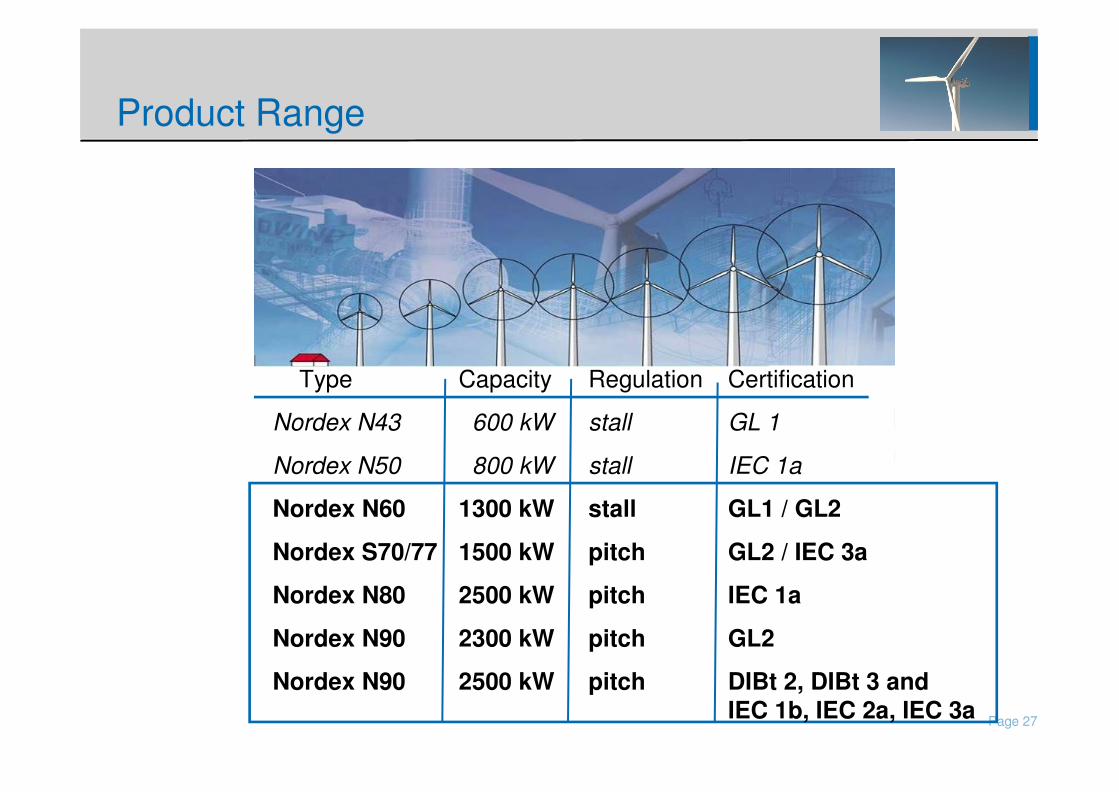

Product Range

Type Capacity Regulation Certification

Nordex N43 600 kW stall GL 1

Nordex N50 800 kW stall IEC 1a

Nordex N60 1300 kW stall GL1 / GL2

Nordex S70/77 1500 kW pitch GL2 / IEC 3a

Nordex N80 2500 kW pitch IEC 1a

Nordex N90 2300 kW pitch GL2

Nordex N90 2500 kW pitch DIBt 2, DIBt 3 andIEC 1b, IEC 2a, IEC 3a

Page 28

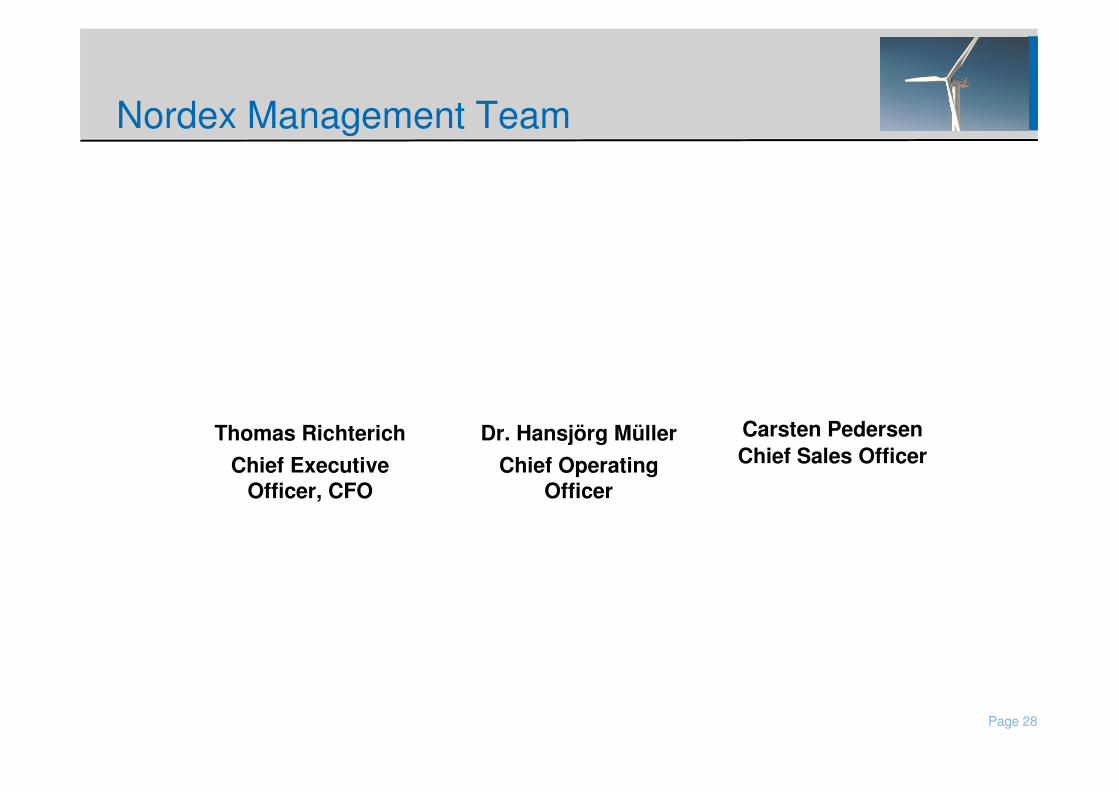

Nordex Management Team

Thomas RichterichChief Executive

Officer, CFO

Carsten PedersenChief Sales Officer

Dr. Hansjörg MüllerChief Operating

Officer

� Previous positions with MAN, Ferrostaal and Babcock Borsig

� CFO since 2002, CEO since 2005

� Managing Director of Nordex Energy GmbH since 1987 and Board Member of Nordex

� Responsible for Sales, since 2001

� Previous positions with Siemens and Roland Berger

� Since 2004 Nordex board member for Operations

Page 29

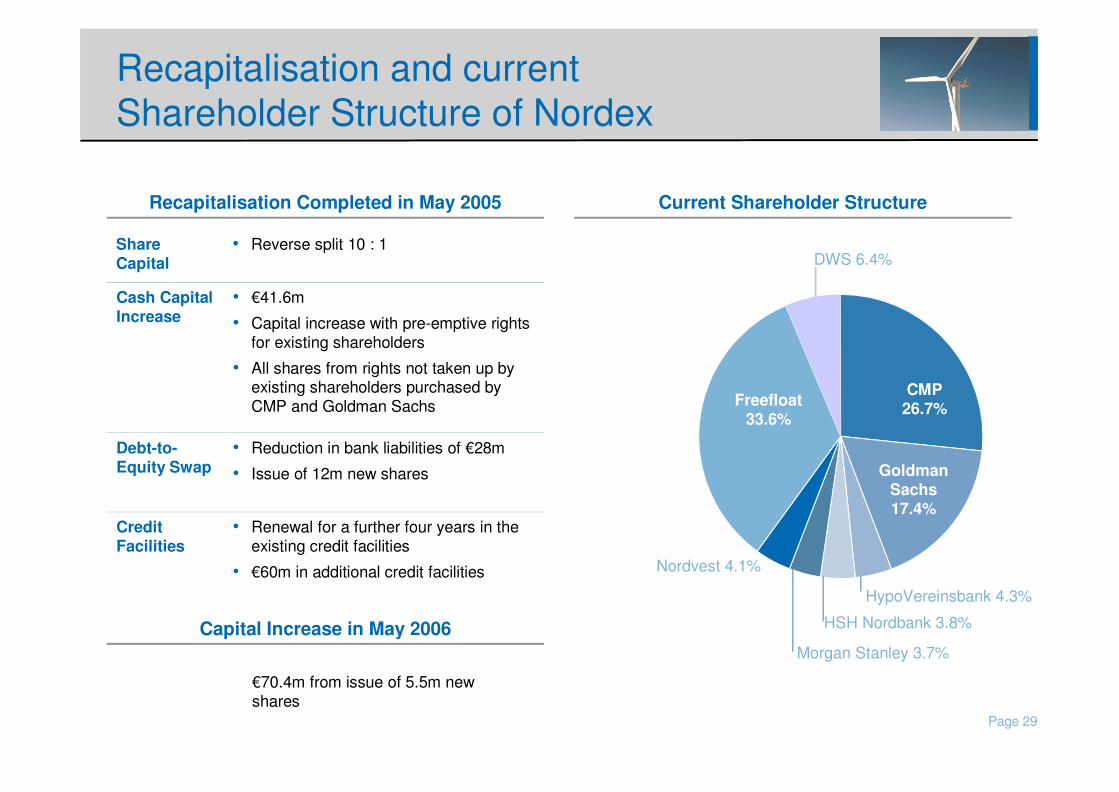

Recapitalisation and current Shareholder Structure of Nordex

• Reduction in bank liabilities of € 28m

• Issue of 12m new shares

Debt-to-Equity Swap

• Renewal for a further four years in the existing credit facilities

• € 60m in additional credit facilities

Credit Facilities

• € 41.6m

• Capital increase with pre-emptive rights for existing shareholders

• All shares from rights not taken up by existing shareholders purchased by CMP and Goldman Sachs

Cash Capital Increase

• Reverse split 10 : 1Share Capital

CMP26.7%

GoldmanSachs17.4%

HypoVereinsbank 4.3%

HSH Nordbank 3.8%

Morgan Stanley 3.7%

Nordvest 4.1%

Freefloat33.6%

Recapitalisation Completed in May 2005 Current Shareholder Structure

Capital Increase in May 2006

€ 70.4m from issue of 5.5m newshares

DWS 6.4%

Page 30

Financial Calendar

� Forecast on fiscal year 2007 December, 2006(conference call)

� Report on fiscal 2006 April 26, 2007

� Annual general meeting May 15, 2007

Page 31

Contact

Ralf Peters

Head of Corporate Communication/ Investor Relations

Phone: +49 (0)40/500 98 522

Fax: +49 (0)40/500 98 333

eMail: [email protected]

Nordex AG

Bornbarch 2

22848 Norderstedt

Germany

www.nordex-online.com