forecasting stock market predictions using artificial ... · fundamental analysis involves the...

TRANSCRIPT

International Journal of Emerging Trends in Engineering and Development Issue 6, Vol. 4 (July 2016)

Available online on http://www.rspublication.com/ijeted/ijeted_index.htm ISSN 2249-6149

©2016 RS Publication, [email protected] Page 67

Forecasting Stock Market predictions using Artificial Neural Network Models: A Survey

Dr.P.Karthikeyan*, G.Thamizhendhi**

*School of Management Studies, Kongu Engineering College, Perundurai, Erode-638052,

Tamilnadu, India. Mobile:+919843641321

** PG Department of Mathematics, Vellalar College for Women, Thindal, Erode-638012,

Tamilnadu. India.

ABSTRACT

This paper surveys recent literature in the area of Artificial Neural Networking which is

used to predict the stock market price fluctuations and return. Stock market price prediction is

one of the most recent phenomenon in the field of finance. Many models have been developed

and studies have been made by numerous researchers. Artificial Neural network (ANN) is a

technique that is widely used and perused in stock market prediction [38, 62]. This study also

seeks to explain the various models and applications of Artificial Neural Networks that predict

the stock market returns and price.

Keywords: Artificial Neural Network, Stock market predictions, Genetic Algorithm, ARIMA,

GARCH

1. INTRODUCTION

In recent years, stock markets have become more volatile. The prediction of stock price

movement is a difficult task for any financial analyst. The fundamental analysis works best for

longer period of time, whereas technical analysis is more appropriate for a shorter period. Many

researchers claim that the stock market is a chaotic system, and a non-linear deterministic system

which only appears random because of its asymmetrical fluctuations. The researchers and

academic practitioners have also projected many models using various fundamental, technical

and analytical aspects to give a more or less exact prediction on financial information

particularly stock market behaviour. Fundamental analysis involves the in-detail analysis of the

changes of the stock prices in terms of macroeconomic variables, whereas technical analysis

International Journal of Emerging Trends in Engineering and Development Issue 6, Vol. 4 (July 2016)

Available online on http://www.rspublication.com/ijeted/ijeted_index.htm ISSN 2249-6149

©2016 RS Publication, [email protected] Page 68

centers on using price, volume, and statistical charts to predict future stock movements [56].

Some traditional time series forecasting tools are also used for the prediction of stock market.

The two approaches of time series analysis and forecasting are linear approach [7], and the

nonlinear approach. The linear methods includes moving average, exponential smoothing, time

series, regression and Autoregressive integrated moving average (ARIMA) model. The

nonlinearity of the financial and stock market is propounded by many researchers and financial

analysts [1, 2]. The parametric nonlinear model includes Autoregressive Conditional

Heteroskedasticity (ARCH) [20], and General Autoregressive Conditional Heteroskedasticity

(GARCH) [6] has been in use for financial forecasting.

Many analytical models have formulated by different researchers to study the prediction of

stock price movements. The Artificial Neural Network (ANN) is the one technical tool to

forecast the stock market behavior, trends and its characteristics. A stock market is a public

market for trading the company’s shares at approved stock price. These are called Securities,

listed on stock exchanges. The price of the scripts depends upon the demand and supply gap.

Companies may issue shares to raise capital in stock market is called Primary Capital Market and

shares of respective companies listed, will allow to trade in the stock market is called secondary

capital market.

ANN is the powerful forecasting tool that predicts the stock markets. It is the non-linear

model used to map past and future value of time series data [13, 22, 37, 91]. Lapedes and

Farber [51] was studied the nonlinear time series model with artificial neural networks. The

originality of the ANN lies in their ability to determine nonlinear relationship in the input data

set without a prior assumption of the knowledge of relation between the input and the output

[26]. Artificial neural networks are applied in the fields of Computer science, Medical,

Engineering, Biology and Economic research. ANN is used for analyzing relating of economic

and financial related forecasting [10, 25, 31, 40]. Neural networks are best in discovering non-

linear relationships [9, 28, 78, 80, 87].

There are numerous studies discussed about the predictions of stock market. This paper,

focuses on various reviews in the field of ANNs used in predicting the stock market. Various

applications and models of ANN are also discussed in this paper. Avci [4]; Egeli, Ozturan,

&Badur [18] ; Karaatli, Gungor, Demir, & Kalayci [44] ; Olson & Mossman [65]; White [89]

International Journal of Emerging Trends in Engineering and Development Issue 6, Vol. 4 (July 2016)

Available online on http://www.rspublication.com/ijeted/ijeted_index.htm ISSN 2249-6149

©2016 RS Publication, [email protected] Page 69

; Leung et al., [53] have studied the stock price return based on ANN model. They examined

various prediction models based on multivariate classification techniques.

2. ARTIFICIAL NEURAL NETWORK

Artificial neural networks (ANNs) approach has been suggested as an alternative

technique to time series forecasting and it gained immense popularity in last few years.

W.S.Mculloch and W.Pitts [61] established neural network and its mathematical model,

known as McCulloch-Pitts (MP) model. This model is used for neuron’s formalization,

mathematical description and network construction. During past 70 years, the neural network

was widely used in different fields and has developed several hundred models.

The basic objective of ANNs was to construct a model for mimicking the intelligence of

human brain into machine [36, 39]. Similar to the work of a human brain, ANNs try to recognize

regularities and patterns in the input data, learn from experience and then provide generalized

results based on their known previous knowledge.

Artificial Neural Network (ANN) is a set of interconnected links that have weights

associated with them. The concept of ANN was originally arrived from biological neural

networks. All the ANN can be the deliberation of as a set of interconnected units broadly

categorized into input layer, the hidden layer and the output layer. Inputs are fed into the input

layer, and its weighted outputs are passed onto the hidden layer. The neurons in the hidden layer

(hidden neurons) are essentially concealed from view. Using additional levels of hidden neurons

provides increased flexibility and more accurate processing.

In recent periods some research works has been reported on the use of ANNs for analysis

of economy and financial markets. Stern[83] provide a introduction of ANNs as follows, the

three essential features of ANN are basic computing elements referred to as neurons, the network

architecture describing the connections between the neurons and the training algorithm used to

find values of the network parameters for performing a particular task. Each neuron performs a

simple calculation, a scalar function of a scalar input. Assuming that we make the neurons with

positive figures and designate the input to the kth

neuron as and the output from the kth

neuron

as then ok= fk(ik) where f(.) is a definite function that is characteristically done but otherwise

subjective. The neurons are connected to each other in the sense that the output from one

component can serve as part of the input to another. The weight is associated with each

construction; the weight from component j to component k is denoted as wjk. Let N(k) denote the

International Journal of Emerging Trends in Engineering and Development Issue 6, Vol. 4 (July 2016)

Available online on http://www.rspublication.com/ijeted/ijeted_index.htm ISSN 2249-6149

©2016 RS Publication, [email protected] Page 70

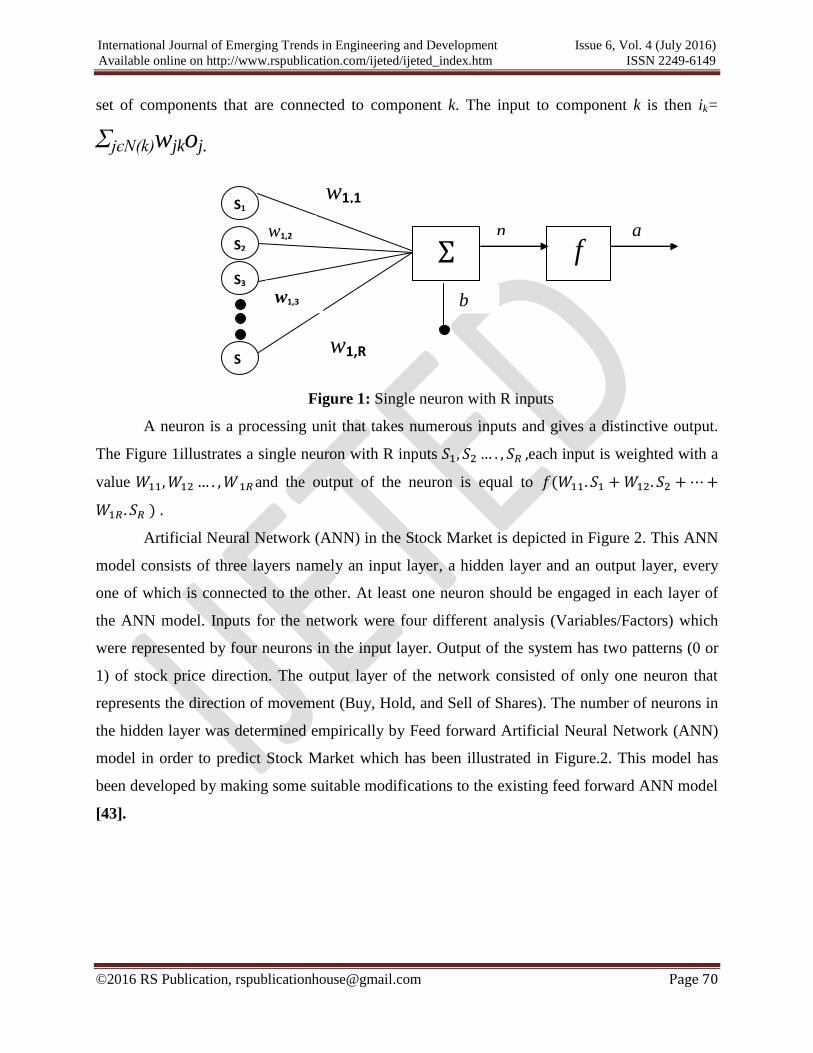

set of components that are connected to component k. The input to component k is then ik=

ΣjєN(k)wjkoj.

Figure 1: Single neuron with R inputs

A neuron is a processing unit that takes numerous inputs and gives a distinctive output.

The Figure 1illustrates a single neuron with R inputs each input is weighted with a

value and the output of the neuron is equal to

.

Artificial Neural Network (ANN) in the Stock Market is depicted in Figure 2. This ANN

model consists of three layers namely an input layer, a hidden layer and an output layer, every

one of which is connected to the other. At least one neuron should be engaged in each layer of

the ANN model. Inputs for the network were four different analysis (Variables/Factors) which

were represented by four neurons in the input layer. Output of the system has two patterns (0 or

1) of stock price direction. The output layer of the network consisted of only one neuron that

represents the direction of movement (Buy, Hold, and Sell of Shares). The number of neurons in

the hidden layer was determined empirically by Feed forward Artificial Neural Network (ANN)

model in order to predict Stock Market which has been illustrated in Figure.2. This model has

been developed by making some suitable modifications to the existing feed forward ANN model

[43].

w1,1

f w1,2

w1,3

w1,R

S1

S2

S3

S

R

n

b

a

International Journal of Emerging Trends in Engineering and Development Issue 6, Vol. 4 (July 2016)

Available online on http://www.rspublication.com/ijeted/ijeted_index.htm ISSN 2249-6149

©2016 RS Publication, [email protected] Page 71

Figure 2: Feed forwardArtificial Neural Network (ANN) Model to predict Stock Market.

3. VARIOUS MODELS OF NEURAL NETWORK

Various Neural network models have been discussed in this paper referring to various

existing literature in the field. The various neural network model used in time series are,

Recurrent [73, 86], Probabilistic [85, 97], Radial Basis Functions [88], Cascade Correlation [21],

General Regression Neural Net [12], Group Method of Data Handling [73], Modular ANNs [47],

Neuro Fuzzy [90]. Here we discuss some of these neural network models.

3.1. Modular Neural Network

Kimoto, Asakawa, Yoda, and Takeoka [47] have studied buying and selling time

prediction system for stocks in the Tokyo Stock Exchange based on modular neural networks.

The authors used a number of learning algorithms and prediction methods for the TOPIX (Tokyo

Stock Exchange Prices Indexes) prediction system. Further the authors applied modular neural

network model to measure the relationships among various market factors. Ramon Lawrence

[52] studied Neural Networks to Forecast Stock Market Prices. He has implemented genetic

algorithms, recurrent networks, and modular networks to predict the stock market. The Modular

neural network was used for predicting corporate bankruptcy [64]. He also discusses about

financial, as well as, political and economic data from the London Stock Exchange, and used

domain expert knowledge to select, and organise data in the modular neural network architecture

constructed for this study. The Modification and acceleration of MNN (Modular Neural

Network) operating principles was described by Schmidt and Bandar [77].

Economic Variables

GDP, Inflation, Interest rates)

Industry variables (Profitability,

Policy, Competition)

Company variables (P/E Ratio,

EPS, Book value, Dividend)

Technical Analysis (Moving average,

Oscillators, RSI, ROC)

Input Layer 1

2

n

Output Layer

Direction of

Movements

(Buy, Hold,

Sell)

Hidden Layer

International Journal of Emerging Trends in Engineering and Development Issue 6, Vol. 4 (July 2016)

Available online on http://www.rspublication.com/ijeted/ijeted_index.htm ISSN 2249-6149

©2016 RS Publication, [email protected] Page 72

3.2. ARIMA and GARCH based neural network

Jung-Hua Wang and Jia-YannLeu [41], Ahmed Ismail El-Hammady, Dr. Mohamed

Abo-Rizka [19] developed a prediction system in forecasting trend in Taiwanese stock market

and Egyptian stock market respectively based on a recurrent neural network trained by using

features extracted from ARIMA analyses. ANNs are known to provide competitive results to the

traditional time series model such as ARIMA model [13, 22, 37, 45]. The forecasting

performance of ARIMA and ANN models in forecasting Korean Stock Price Index also

compared by C. K. Lee, Y. Sehwan, and J. Jongdae [8].

Merh et al., [63] studied a comparison between hybrid approaches of ANN and ARIMA

for Indian stock trend forecasting with many instances of the ARIMA predicted values shown to

be better than those of the ANNs predicted values in relation to the actual stock value. Sterba

and Hilovska [35] argued that ARIMA model and ANN model achieved superior forecast

performance in many real-world applications.

Manish Kumar and M. Thenmozhi [50] studied the application and development of

hybrid methodology that combines both ARIMA and Artificial Neural Network Model to predict

the stock market index returns. The stock data obtained from New York Stock Exchange was

studied using ARIMA and artificial neural networks [3].

Donaldson and Kamstra [16] proposes a Neural Network modification of a GARCH

model. He used multilayer perception and density estimating neural network is used to forecast

the returns and volatility of the German Stock Index- DAX stock index. R.Glen Donaldson and

Mark Kamstra [23] constructed a semi nonparametric nonlinear GARCH model, based on the

Artificial Neural Network (ANN) literature and evaluated its ability to forecast stock return

volatility in London, New York, Tokyo and Toronto stock exchanges. The use of GARCH-

neural network model for forecasting the volatility of bid-ask spread of the Chinese stock market

[82].

Hossain, A; Nasser, M [29, 20] compare the GARCH and neural network methods in

financial time series prediction and applied GARCH model instead of

autoregressive (AR) model or autoregressive moving average (ARMA) model to compare with

Standard Back Propagation (BP) in forecasting of the four international including two Asian

stock markets indices.

International Journal of Emerging Trends in Engineering and Development Issue 6, Vol. 4 (July 2016)

Available online on http://www.rspublication.com/ijeted/ijeted_index.htm ISSN 2249-6149

©2016 RS Publication, [email protected] Page 73

Jingtao Yao, Chew Lim Tan and Hean-Lee Poh [93] developed a neural network

compared with ARIMA model that was used to predict the stock index of Kuala Lumpur Stock

Exchange, the neural network model have better returns compared with conventional ARIMA

models.

3.3. Genetic Algorithm

In financial market field, the genetic algorithms are very frequently used to discover the

best combination values of parameters in a trading rule, and they can be built into ANN models

designed to select stocks. Several studies have conducted, and these methods are proved

effective for forecasting the financial trends [42, 55]. Kim and Han [46] used neural network

tailored by Genetic Algorithm; the genetic algorithm was used to reduce the density of the

feature space. The other authors also used genetic algorithms in predicting of Stock prices

indexes [14. 59, 84] and exchange market [79]. Hassan et al., [27] projected and implemented

the fusion model by combining the HMM (Hidden Markov Model) and Genetic Algorithm to

forecast financial market behaviour. Wavelet transform to extract the short-term feature of stock

trends was used by Kishikawa and Tokinaga[48].

3.4. Recurrent Network

The finest neural networks tool for non- linear prediction is recurrent neural network

[98]. The development of RNN (Recurrent Neural Network) based on genetic learning algorithm

has a statistically significant and successful predictions [58]. A. Graves, et al., [24] introduced a

universal framework of sequence learning algorithm, evolution of recurrent systems with Linear

Outputs.

3.5.Branch Network

T. Yamashita, K. Hirasawa and Jinglu Hu [92] says that multi-branch neural networks

(MBNNs) could have higher representation and generalization ability than conventional Neural

Networks. Kotaro Hirasawa and Jinglu Hu [92] developed Multi-branch neural networks

(MBNNs) for prediction of stock prices and model were carried out in order to examine the

correctness of prediction.

3.6. Functional Link ANN

FLANN is a single layer, single neuron architecture, which has the exceptional

capability, to form complex decision regions by creating non-linear decision boundaries [12, 57].

International Journal of Emerging Trends in Engineering and Development Issue 6, Vol. 4 (July 2016)

Available online on http://www.rspublication.com/ijeted/ijeted_index.htm ISSN 2249-6149

©2016 RS Publication, [email protected] Page 74

The functional link ANN is a innovative single neuron based architecture first proposed

by Pao [70]. The original architecture of functional link artificial neural network with working

attitude of different models are provided to accomplish best forecasting and cataloging with

increase in accurateness of prediction and decrease in training time [5]. Functional link single

layer artificial neural network (FLANN) was used for long term as well as short term stock

market prediction [66].

3.7.Fuzzy Neural Network

Fuzzy theory was formulated by Zadeh [94, 95, 96] ; Zimmermann [99]. Huarng and

Yu [33] used neural networks to extract fuzzy logical relationships from fuzzy time-series to

forecast the Taiwan Stock Exchange and their model outperformed Chen’s [11] model.

Renato De C.T. and Adriano J.De O [74] presents the results of the application of Fuzzy

Neural Networks to predict the evolution of stock prices of Brazilian companies traded in the

São Paulo Stock Exchange. Pantazopoulos et al., [69] presented a neuro fuzzy approach for

predicting the prices of IBM company stock. Siekmann et al., [81] implemented a network

structure that contains the adaptable fuzzy parameters in the weights of the connections between

the first and second hidden layers. Rong-Jun Li and Zhi Bin Xiong [54] developed a fuzzy

neural network that is a set of adaptive networks and functionally equal to a fuzzy inference

system based on the comprehensive index of Shanghai stock market, designate that the

recommended fuzzy neural network could be an competent system to forecast financial

information.

3.8.Back Propagation ANN

The performance of back propagation network and regression models to predict the stock

market returns was compared [75].

Huang et al., [32] has made comparative study of application of Support Vector

Machines (SVM) and Back propagation Neural Networks (BNN) for an analysis of corporate

credit ratings. The Back Propagation algorithm designed by Rumelhart, Hinton and Williams

[76] is the best appropriate method is being intensively tested in Finance domain. Furthermore,

this method is renowned as a good algorithm for generality purposes.

4. APPLICATION OF VARIOUS ANN TO PREDICT INDIAN STOCK MARKET

Neural networks to estimate stock market actions will be a continuing area of researchers

and shareholders try hard to outstrip the market conditions. The table discusses about the existing

International Journal of Emerging Trends in Engineering and Development Issue 6, Vol. 4 (July 2016)

Available online on http://www.rspublication.com/ijeted/ijeted_index.htm ISSN 2249-6149

©2016 RS Publication, [email protected] Page 75

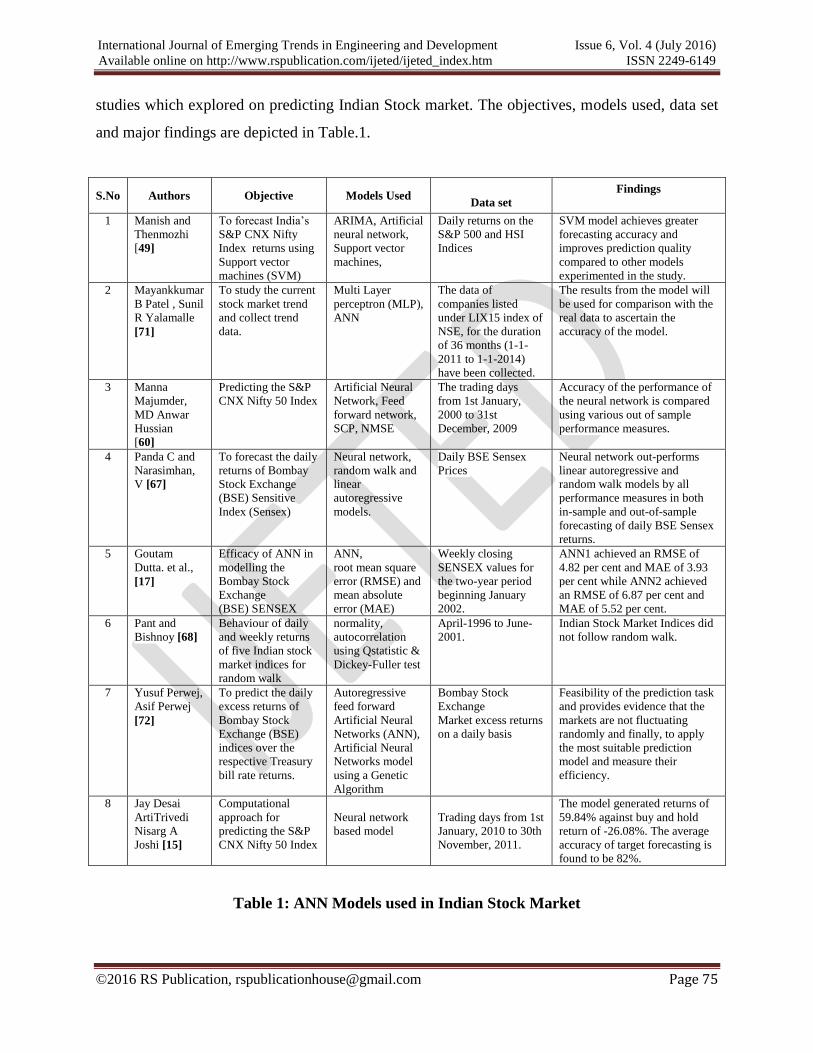

studies which explored on predicting Indian Stock market. The objectives, models used, data set

and major findings are depicted in Table.1.

Table 1: ANN Models used in Indian Stock Market

S.No Authors Objective Models Used

Data set

Findings

1 Manish and

Thenmozhi

[49]

To forecast India’s

S&P CNX Nifty

Index returns using

Support vector

machines (SVM)

ARIMA, Artificial

neural network,

Support vector

machines,

Daily returns on the

S&P 500 and HSI

Indices

SVM model achieves greater

forecasting accuracy and

improves prediction quality

compared to other models

experimented in the study.

2 Mayankkumar

B Patel , Sunil

R Yalamalle

[71]

To study the current

stock market trend

and collect trend

data.

Multi Layer

perceptron (MLP),

ANN

The data of

companies listed

under LIX15 index of

NSE, for the duration

of 36 months (1-1-

2011 to 1-1-2014)

have been collected.

The results from the model will

be used for comparison with the

real data to ascertain the

accuracy of the model.

3 Manna

Majumder,

MD Anwar

Hussian

[60]

Predicting the S&P

CNX Nifty 50 Index

Artificial Neural

Network, Feed

forward network,

SCP, NMSE

The trading days

from 1st January,

2000 to 31st

December, 2009

Accuracy of the performance of

the neural network is compared

using various out of sample

performance measures.

4 Panda C and

Narasimhan,

V [67]

To forecast the daily

returns of Bombay

Stock Exchange

(BSE) Sensitive

Index (Sensex)

Neural network,

random walk and

linear

autoregressive

models.

Daily BSE Sensex

Prices

Neural network out-performs

linear autoregressive and

random walk models by all

performance measures in both

in-sample and out-of-sample

forecasting of daily BSE Sensex

returns.

5 Goutam

Dutta. et al.,

[17]

Efficacy of ANN in

modelling the

Bombay Stock

Exchange

(BSE) SENSEX

ANN,

root mean square

error (RMSE) and

mean absolute

error (MAE)

Weekly closing

SENSEX values for

the two-year period

beginning January

2002.

ANN1 achieved an RMSE of

4.82 per cent and MAE of 3.93

per cent while ANN2 achieved

an RMSE of 6.87 per cent and

MAE of 5.52 per cent.

6 Pant and

Bishnoy [68]

Behaviour of daily

and weekly returns

of five Indian stock

market indices for

random walk

normality,

autocorrelation

using Qstatistic &

Dickey-Fuller test

April-1996 to June-

2001.

Indian Stock Market Indices did

not follow random walk.

7 Yusuf Perwej,

Asif Perwej

[72]

To predict the daily

excess returns of

Bombay Stock

Exchange (BSE)

indices over the

respective Treasury

bill rate returns.

Autoregressive

feed forward

Artificial Neural

Networks (ANN),

Artificial Neural

Networks model

using a Genetic

Algorithm

Bombay Stock

Exchange

Market excess returns

on a daily basis

Feasibility of the prediction task

and provides evidence that the

markets are not fluctuating

randomly and finally, to apply

the most suitable prediction

model and measure their

efficiency.

8 Jay Desai

ArtiTrivedi

Nisarg A

Joshi [15]

Computational

approach for

predicting the S&P

CNX Nifty 50 Index

Neural network

based model

Trading days from 1st

January, 2010 to 30th

November, 2011.

The model generated returns of

59.84% against buy and hold

return of -26.08%. The average

accuracy of target forecasting is

found to be 82%.

International Journal of Emerging Trends in Engineering and Development Issue 6, Vol. 4 (July 2016)

Available online on http://www.rspublication.com/ijeted/ijeted_index.htm ISSN 2249-6149

©2016 RS Publication, [email protected] Page 76

5. CONCLUSION AND FUTUREWORK

The Artificial Neural Network used in domain and it is computer based simulation model

that predicting more accurate stock price along with the movement and decision of buy or hold

or sell shares in the stock market. This paper surveyed the application of neural networks of

financial markets with particular reference to stock market prediction. This paper presents how

neural networks have been used to test the forecasting share prices.In this review of literature,

different applications of Artificial Neural Network models for predicting stock market has been

summed up. This field of research is new and emerging and there is significant enormous future

scope.

The neural network models for forecasting stock market are at a initial phase and there

are potential improvements in the prediction of accuracy and reliability of stocks. The study can

help analyst or investors to understand how the market would behave if the Stock price increases

or decreases. The future study can also focus on using macroeconomic variables to forecast the

interest rate, GDP, etc. In addition, the study should be extended to predict another kind of

financial time series like interest rate, derivative (option and future) and foreign exchange prices.

More authors put emphasis on the obligation for including more data in the models to predict the

exact share price. The researchers also emphasize the integration of neural networks with other

methods. The method of ANN is new, many possibilities for combining with other models

including linear and non-linear.

REFERENCES

1. Abhyankar, A.H., Copeland, L.S. and Wong, W. (1995) ,Non linear dynamics in real-

time equity market indices: evidence from the United Kingdom, Economic Journal,

105, 864-880.

2. Abhyankar, A.H., Copeland, L.S. and Wong, W. (1997) ,Uncovering nonlinear

structure in real time stock market indexes: the S&P 500, the DAX, the Nikkei 225,

and the FTSE 100, Journal of Business and Economic Statistics, 15, 1-14.

3. Adebiyi, A. A., Adewumi, A. O., & Ayo, C. K. (2014), Comparison of ARIMA and

Artificial Neural Networks Models for Stock Price Prediction, Journal of Applied

Mathematics, 2014.

International Journal of Emerging Trends in Engineering and Development Issue 6, Vol. 4 (July 2016)

Available online on http://www.rspublication.com/ijeted/ijeted_index.htm ISSN 2249-6149

©2016 RS Publication, [email protected] Page 77

4. Avci E. (2007) , Forecasting Daily and Sessional Returns of the Ise- 100 Index with

Neural Network Models, Dogus Universitesi Dergisi, 2(8), 128 -142.

5. Bebarta, D. K., Biswal, B., Rout, A. K., & Dash, P. K. (2012), Forecasting and

classification of Indian stocks using different polynomial functional link artificial

neural networks, In IEEE Conference, INDCON (pp. 178-182).

6. Bollerslev, T. (1986), Generalised Autoregressive Conditional Heteroskedasticity,

Journal of Econometrics, 31, 307–327.

7. Box, G. E. P. and Jenkins, G. M. (1976), Time Series Analysis: Forecasting and

Control, San Francisco: Holden-Day.

8. C. K. Lee, Y. Sehwan, and J. Jongdae (2007) “Neural network model versus

SARIMA model in forecasting Korean stock price index (KOSPI),” Issues in

Information System, vol. 8, no. 2,pp. 372–378.

9. Cameron, N., Moshiri, S. and Scuse, D. (1999) Static, dynamic and hybrid neural

networks in forecasting inflation, Computational Economics,14, 219 – 235.

10. Cheh, John J; Weinberg, Randy S; Yook, Ken C (1999). "An Application of an

Artificial Neural Network Investment System to Predict Takeover Targets", Journal

of Applied Business Research, Vol. 15 (4). p 33-45.

11. Chen, C. H. (1996). Fuzzy logic and neural network handbook. McGraw-Hill, Inc..

12. Chen, C.H(1994) "Neural networks for financial market prediction," Neural

Networks,1994. IEEE World Congress on Computational Intelligence.,1994 IEEE

International Conference on(2).

13. Chen, Y., Yang, B., Dong, J., & Abraham, A. (2005). Time-series forecasting using

flexible neural tree model. Information sciences, 174(3), 219-235.

14. Choudhry, R.; Garg, K. (2008) A Hybrid Machine Learning System for Stock Market

Forecasting, World Academy of Science, Engineering and Technology 39: 315-318.

15. Desai, J., Trivedi, A., & Joshi, N. A. (2012). Forecasting of Stock Market Indices

Using Artificial Neural Network. Shri Chimanbhai Patel Institutes, Ahmedabad

Working Paper No. CPI/MBA/2013/0003.

16. Donaldson, R. G., & Kamstra, M. (1997). An artificial neural network-GARCH

model for international stock return volatility. Journal of Empirical Finance, 4(1), 17-

46.

International Journal of Emerging Trends in Engineering and Development Issue 6, Vol. 4 (July 2016)

Available online on http://www.rspublication.com/ijeted/ijeted_index.htm ISSN 2249-6149

©2016 RS Publication, [email protected] Page 78

17. Dutta, G., Jha, P., Laha, A. K., & Mohan, N. (2006). Artificial neural network models

for forecasting stock price index in the Bombay stock exchange. Journal of Emerging

Market Finance, 5(3), 283-295.

18. Egeli, B., Ozturan, M., & Badur, B. (2003) Stock market prediction using artificial

neural networks, In Proceedings of the 3rd Hawaii international conference on

business, Honolulu, Hawaii

19. El-Hammady, A. I., & Abo-Rizka, M. (2011). Neural network based stock market

forecasting. IJCSNS, 11(8), 204.

20. Engle, R. F. (1982), Autoregressive Conditional Heteroskedasticity with Estimates of

the Variance of UK Inflation, Econometrica, 50, 987–1008.

21. Ensley,D., and Nelson,D.E (1992) "Extrapolation of Mackey-Glass data using

Cascade Correlation,"SIMULATION (58:5) p 333.

22. Giordano F, La Rocca M, Perna C (2007) Forecasting nonlinear time series with

neural network sieve bootstrap.Computational Statistics and Data Analysis,51(8):

3871–3884

23. Glen Donaldson, R., & Kamstra, M. (1999). Neural network forecast combining with

interaction effects. Journal of the Franklin Institute, 336(2), 227-236.

24. Graves, A., Fernández, S., Gomez, F., & Schmidhuber, J. (2006). Connectionist

temporal classification: labelling unsegmented sequence data with recurrent neural

networks. In Proceedings of the 23rd international conference on Machine learning

(pp. 369-376). ACM.

25. H. White (1996). Economics Prediction Using NN; The Case of IBM Daily Stock

Returns. In R.R. Trippi, E. Turban, ed., Neural Networks in Finance and Investing,

Irwin Professional Publishing, Chicago, pp. 469-481.

26. Hagan, M. T., H. B. Demuth, and M. Beale, (1996): Neural Network Design,

International Thomson Publishing Inc.

27. Hassan, M. R., Nath, B., & Kirley, M. (2007). A fusion model of HMM, ANN and

GA for stock market forecasting. Expert Systems with Applications, 33(1), 171-180.

28. Hoptroff, R.G (1993) “The Principles and Practice of Time Series Forecasting and

Business Modelling Using Neural Nets,” Neural Computing and Applications, 1, 59-

66.

International Journal of Emerging Trends in Engineering and Development Issue 6, Vol. 4 (July 2016)

Available online on http://www.rspublication.com/ijeted/ijeted_index.htm ISSN 2249-6149

©2016 RS Publication, [email protected] Page 79

29. Hossain, A., & Nasser, M. (2011). Comparison of the finite mixture of ARMA-

GARCH, back propagation neural networks and support-vector machines in

forecasting financial returns. Journal of Applied Statistics, 38(3), 533-551.

30. Hossain, A.; Nasser, M.(2008), "Comparison of GARCH and neural network methods

in financial time series prediction," Computer and Information Technology, 2008.

ICCIT 2008. 11th International Conference on , vol., no., pp.729,734, 24-27.

31. Howley, D.D., Johnson, J.D., and Raina D. (1990) Artificial Neural Systems: A New

Tool for Financial Decision-Making Financial Analysts Journal,

November/December: 63-72.

32. Huang, Z., Chen, H., Hsu, C. J., Chen, W. H., & Wu, S. (2004). Credit rating analysis

with support vector machines and neural networks: a market comparative study.

Decision support systems, 37(4), 543-558.

33. Huarng, K., & Yu, T. H. K. (2006). The application of neural networks to forecast

fuzzy time series. Physica A: Statistical Mechanics and its Applications, 363(2), 481-

491.

34. Hung, Y. C., Huang, Y. T., Ho, M. C., & Hu, C. K. (2008). Paths to globally

generalized synchronization in scale-free networks. Physical Review E, 77(1),

016202.

35. J. Sterba and K. Hilovska (2010). “The implementation of hybrid ARIMA neural

network prediction model for aggregate water consumption prediction,” Aplimat—

Journal of Applied Mathematics, vol. 3, no. 3, pp. 123–131,

36. J.M. Kihoro, R.O. Otieno, C. Wafula, “Seasonal Time Series Forecasting: A

Comparative Study of ARIMA and ANN Models”, African Journal of Science and

Technology (AJST) Science and Engineering Series Vol. 5, No. 2, pages: 41-49.

37. Jain, A. and Kumar, A.M (2007), Hybrid neural network models for hydrologic time

series forecasting, J. Applied Soft. Computing, 7(2), 2007, pp.585-592.

38. Jang Bahadur Singh, “Current Approaches in Neural Network Modeling of

Financialtime Series”, Working paper, Indian Institute of Management Bangalore.

39. Joarder Kamruzzaman, RezaulBegg, RuhulSarker, “Artificial Neural Networks in

Finance and Manufacturing”, Idea Group Publishing, USA.

International Journal of Emerging Trends in Engineering and Development Issue 6, Vol. 4 (July 2016)

Available online on http://www.rspublication.com/ijeted/ijeted_index.htm ISSN 2249-6149

©2016 RS Publication, [email protected] Page 80

40. John Cooper, (1999). "Artificial neural networks versus multivariate statistics: An

application from economics," Journal of Applied Statistics, Taylor & Francis

Journals, vol. 26(8), pages 909-921.

41. Jung-Hua Wang; Jia-Yann Leu (1996)., "Stock market trend prediction using

ARIMA-based neural networks," Neural Networks, IEEE International Conference

on , vol.4, no., pp.2160,2165 vol.4, 3-6 Jun 1996, doi: 10.1109/ICNN.1996.549236

42. Kanungo, Rama. P. (2004). Genetic Algorithms: Genesis of Stock Evaluation.

Economics WPA Working Paper, (0404007).

43. Kara, Y., Acar Boyacioglu, M., & Baykan, Ö. K. (2011). Predicting direction of stock

price index movement using artificial neural networks and support vector machines:

The sample of the Istanbul Stock Exchange. Expert systems with Applications, 38(5),

5311-5319.

44. Karaatli, M., Gungor, I., Demir, Y., & Kalayci, S. (2005) Estimating stock market

movements with neural network approach, Journal of Balikesir University, 2(1), pp.

22–48.

45. Khashei, M., & Bijari, M. (2010). An artificial neural network (p,d,q) model for

timeseries forecasting. Expert Systems with Applications, 37(1), 479-489.

46. Kim, K. J., & Han, I. (2000). Genetic algorithms approach to feature discretization in

artificial neural networks for the prediction of stock price index. Expert systems with

Applications, 19(2), 125-132.

47. Kimoto,T.,Asakawa,K.,Yoda, M., and Takeoka,M (1990)."Stock market prediction

system with modular neural networks,"Neural Networks, IJCNN International Joint

Conference ), pp 1-6.

48. Kishikawa, Y., & Tokinaga, S. (2000). Prediction of stock trends by using the

wavelet transform and the multi-stage fuzzy inference system optimized by the GA.

IEICE TRANSACTIONS on Fundamentals of Electronics, Communications and

Computer Sciences, 83(2), 357-366.

49. Kumar, M., & Thenmozhi, M. (2007). Support vector machines approach to predict

the S&P CNX NIFTY index returns. In 10th Capital Markets Conference, Indian

Institute of Capital Markets Paper.

International Journal of Emerging Trends in Engineering and Development Issue 6, Vol. 4 (July 2016)

Available online on http://www.rspublication.com/ijeted/ijeted_index.htm ISSN 2249-6149

©2016 RS Publication, [email protected] Page 81

50. Kumar, M., & Thenmozhi, M. (2012). Causal effect of volume on stock returns and

conditional volatility in developed and emerging market. American Journal of

Finance and Accounting, 2(4), 346-362.

51. Lapedes, A. S., & Farber, R. M. (1987). Nonlinear signal processing using neural

networks: prediction and system modeling, Los Alamos Report LA-UR 87-2662.

52. Lawrence, R. (1997). Using neural networks to forecast stock market prices.

University of Manitoba.

53. Leung, M., Daouk, H. & Chen, A. (2000).Forecasting Stock Indices: A Comparison

of Classification and Level Estimation Models.International Journal of Forecasting,

16(2),173-190.

54. Li, R. J., & Xiong, Z. B. (2005). Forecasting stock market with fuzzy neural

networks. In Machine Learning and Cybernetics, 2005. Proceedings of 2005

International Conference on (Vol. 6, pp. 3475-3479). IEEE.

55. Lin, L., Cao, L., Wang, J., & Zhang, C. (2004). The applications of genetic

algorithms in stock market data mining optimisation. In Proceedings of Fifth

International Conference on Data Mining, Text Mining and their Business

Applications (pp. 273-280).

56. Louis B. Mendelsohn(2000), Trend Forecasting with Technical Analysis: Unleashing

the Hidden Power of Intermarket Analysis to Beat the Market, Marketplace Books,

Incorporated, 2000.

57. Majhi, B., Shalabi, H., & Fathi, M. (2005). FLANN based forecasting of S&P 500

index. Information Technology Journal, 4(3), 289-292.

58. Maknickienė, N., Rutkauskas, A. V., & Maknickas, A. (2011). Investigation of

financial market prediction by recurrent neural network. Innovative Technologies for

Science, Business and Education, 2(11), 3-8.

59. Mańdziuk, J., & Jaruszewicz, M. (2011). Neuro-genetic system for stock index

prediction. Journal of Intelligent and Fuzzy Systems, 22(2), 93-123.

60. Manna Majumder and MD Anwar Hussian, “Prediction of Indian stock market index

using artificial neural network"

International Journal of Emerging Trends in Engineering and Development Issue 6, Vol. 4 (July 2016)

Available online on http://www.rspublication.com/ijeted/ijeted_index.htm ISSN 2249-6149

©2016 RS Publication, [email protected] Page 82

61. McCulloch, W, and W. Pitts. (1943). A logical calculus of the ideas immanent in

nervous activity. Bulletin of Mathematical Biophysics 5:115-133. Reprinted in W. S.

McCulloch (1965/1988), Embodiments of Mind. Cambridge, MA: MIT Press.

62. Mizuno, Kosaka, Yajima and Komoda, (1998), “Application of NEURAL

NETWORK to technical analysis of stock market prediction”,Vol.7, pp. 111-120.

63. N. Merh, V. P. Saxena, and K. R. Pardasani(2010). “A comparison between hybrid

approaches of ANN and ARIMA for Indian stock trend forecasting,” Journal of

Business Intelligence, vol. 3,no. 2, pp. 23–43.

64. Nasir, M. L., John, R. I., Bennett, S. C., & Russell, D. M. (2000). Predicting

corporate bankruptcy using modular neural networks. In Computational Intelligence

for Financial Engineering, 2000.(CIFEr) Proceedings of the IEEE/IAFE/INFORMS

2000 Conference on (pp. 86-91). IEEE.

65. Olson, D.&Mossman, C. (2003). Neural Network Forecasts of Canadian Stock

Returns using Accounting Ratios.International Journal of Forecasting,19(3), 453-467.

66. Padhiary, P. K., & Mishra, A. P. (2011). Development of improved artificial neural

network model for stock market prediction. International Journal of Engineering

Science and Technology, 3(2), 1576-1581.

67. Panda, C., & Narasimhan, V. (2007). Forecasting exchange rate better with artificial

neural network. Journal of Policy Modeling, 29(2), 227-236.

68. Pant, B., & Bishnoi, T. R. (2001). Testing random walk hypothesis for Indian stock

market indices. In Research Paper Presented in UTI Capital Market Conference

Proceedings (pp. 1-15).

69. Pantazopoulos, K. N., Tsoukalas, L. H., Bourbakis, N. G., Brun, M. J., & Houstis, E.

N. (1998). Financial prediction and trading strategies using neurofuzzy approaches.

Systems, Man, and Cybernetics, Part B: Cybernetics, IEEE Transactions on, 28(4),

520-531.

70. Pao, Y. H. (1989). Adaptive pattern recognition and neural networks. Addison-

Wesley Longman Publishing Co., Inc..

71. Patel, M. B., & Yalamalle, S. R. Stock Price Prediction Using Artificial Neural

Network.

International Journal of Emerging Trends in Engineering and Development Issue 6, Vol. 4 (July 2016)

Available online on http://www.rspublication.com/ijeted/ijeted_index.htm ISSN 2249-6149

©2016 RS Publication, [email protected] Page 83

72. Perwej, Y., & Perwej, A. (2012). Prediction of the Bombay Stock Exchange (BSE)

market returns using artificial neural network and genetic algorithm.

73. Pham,D.T.,and Liu,X (1995) Neural networks for identification, prediction,and

control,Springer-Verlag, New York.

74. Raposo, Renato De CT, et al. (2005). "Using multi-agents to predict the stock market

evolution based on fundamentalist analysis and fuzzy-neural networks." Proceedings

of the 5th WSEAS International Conference on Applied Informatics and

Communications. World Scientific and Engineering Academy and Society (WSEAS).

75. Refenes, Zapranis, and Francis, (1994) Journal of Neural Networks, Stock

Performance Modeling Using Neural Networks: A Comparative Study with

Regression Models, Vol. 7, No. 2,. 375-388.

76. Rumelhart, D. E., Hinton, G. E., & Williams, R. J. (1985). Learning internal

representations by error propagation (No. ICS-8506). CALIFORNIA UNIV SAN

DIEGO LA JOLLA INST FOR COGNITIVE SCIENCE.

77. Schmidt, A. L. B. R. E. C. H. T., & Bandar, Z. U. H. A. I. R. (1998). Modularity-A

concept for new neural network architectures. In IASTED International Conference

on Computer Systems and Applications (CSA'98) (pp. 26-29).

78. Shachmurove, Y., & Witkowska, D. (2000). Utilizing artificial neural network model

to predict stock markets. University of Pennsylvania, Center for Analytic Research in

Economics and the Social Sciences.

79. Sher, G. I (2011) Evolving chart pattern sensitive neural network based forex trading

agents.2011arXiv1111.5892S

80. Shtub, Avraham; Versano, Ronen (1999). "Estimating the Cost of Steel Pipe Bending,

a Comparison between Neural Networks and Regression Analysis", International

Journal of Production Economics, Vol. 62(3). p 201-07.

81. Siekmann, S., Kruse, R., Gebhardt, J., Van Overbeek, F., & Cooke, R. (2001).

Information fusion in the context of stock index prediction. International journal of

intelligent systems, 16(11), 1285-1298.

82. Si-ming, L., Zhang-xi, L., Zhong-yi, X., & Jun-wei, M. (2012). The use of GARCH-

neural network model for forecasting the volatility of bid-ask spread of the Chinese

International Journal of Emerging Trends in Engineering and Development Issue 6, Vol. 4 (July 2016)

Available online on http://www.rspublication.com/ijeted/ijeted_index.htm ISSN 2249-6149

©2016 RS Publication, [email protected] Page 84

stock market. In Management Science and Engineering (ICMSE), 2012 International

Conference on (pp. 1899-1903). IEEE.

83. Stern,H.(1996)Neural networks in applied statistics(with

discussion).Technometrics,38,205-220.

84. Szeto, K. T.; Fong, L. Y. (2000). How Adaptive Agents in Stock Market Perform in

the Presence of Random News: A Genetic Algorithm Approach, in IDEAL'00

Proceedings of the Second International Conference on Intelligent Data Engineering

and Automated Learning, Data Mining, Financial Engineering, and Intelligent

Agents. Springer-Verlag London,UK 2000: 505-510. ISBN:3-540-41450-9.

85. Tan,H.P.,Wunsch, D.V.,and Dc,II (1995). "Conservative thirty calendar day stock

prediction using aprobabilistic neural network," Computational Intelligence for

Financial Engineering,1995.,Proceedings of the IEEElIAFE 1995),pp 113-117

86. Tenti,P."Forecasting Currency Futures Using Recurrent Neural Networks, "Proc. 3rd

International Conference.

87. Wasserman, P.D (1989).Neural Computing: Theory and Practice, Van Nostrand

Reinhold: New York.

88. Wedding,D.K.,and Cios, K.(1996). "Time series forecasting by combining RBF

networks, certainty factors, and the Box-Jenkins model, "Neurocomputing (10:2) pp

149-168.

89. White, H. (1988). Economic prediction using neural networks: The case of IBM stock

prices.Proceedings of the Second Annual IEEE Conference on Neural Networks,pp.

II:451–458. New York: IEEE Press.

90. Wong, F.S., Wang, P.Z., and Goh, T.H (1991). "Fuzzy neural systems for decision

making," Neural Networks, 1991. 1991 IEEE International Joint Conference) pp

1625-1637

91. Y. Chen, B. Yang and J. Dong (2005). ”Nonlinear System Modeling via Optimal ...

Flexible Neural Tree Model”, Information Science, 174(3-4): 219-235.

92. Yamashita, T., Hirasawa, K., & Hu, J. (2005). Application of multi-branch neural

networks to stock market prediction. In Neural Networks, 2005. IJCNN'05.

Proceedings. 2005 IEEE International Joint Conference on (Vol. 4, pp. 2544-2548).

IEEE.

International Journal of Emerging Trends in Engineering and Development Issue 6, Vol. 4 (July 2016)

Available online on http://www.rspublication.com/ijeted/ijeted_index.htm ISSN 2249-6149

©2016 RS Publication, [email protected] Page 85

93. Yao, J., Tan, C. L., & Poh, H. L. (1999). Neural networks for technical analysis: a

study on KLCI. International journal of theoretical and applied finance, 2(02), 221-

241.

94. Zadeh, L. A. (1976). A fuzzy-algorithmic approach to the definition of complex or

imprecise concepts (pp. 202-282). Birkhäuser Basel.

95. Zadeh, L.A. (1975). The Concept of Linguistic Variable and Its Application to

Approximate Reasoning I. Information Sciences, 8, 199-249

96. Zadeh, L.A., (1975). The Concept of Linguistic Variable and Its Application to

Approximate Reasoning II. Information Sciences, 8, 301-357.

97. Zaknich, A., de Silva, C.J.S., and Attikiouzel, Y.(1991) "A modified probabilistic

neural network (PNN) for nonlinear time series &nalysis,"Neural Networks,1991.

1991 IEEE International Joint Conference ) pp 1530-1535.

98. Zhang, J. S., & Xiao, X. C. (2000). Predicting chaotic time series using recurrent

neural network. Chinese Physics Letters, 17(2), 88.

99. Zimmermann H. J. (1991).Fuzzy Set Theory and Its Applications, Dordrecht, Kluver

Academic Press.