fla annual review 2016 - fla – the finance & leasing ... & leasing association annual...

TRANSCRIPT

FLA Annual Review 2016

Contents

4 Chairman’s Foreword

6 Director General’s Report

8 Asset Finance

10 Consumer Finance

12 Motor Finance

14 Westminster and Brussels 16 Research and Statistics

20 Events and Training

22 Members Directory

25 Contacting the FLA

Finance & Leasing Association 4 Annual Review 2016

Chairman’s Foreword

The last twelve months were exceptionally busy for the FLA’s members.

First, and most important, they provided their customers with record levels of new finance: £110 billion in 2015, some 9% more than in 2014. Within that total, new business in the asset finance (leasing and hire purchase) markets grew by 12%, in the consumer finance markets by 8%, and in the motor finance market (business and consumer) 9% by volume.

In the asset finance market, FLA members financed 31.5% of all UK investment in machinery, equipment and purchased software. Nearly 60% of the total – more than £16 billion – went to SMEs. FLA members also provided consumers with £81 billion to support household purchases – almost a third of all new UK consumer credit in 2015, including over 80% of private new car registrations.

This strong performance has continued in 2016. In Q1 2016, the asset finance market reported new business up by 8%; consumer finance new business grew by 14%; and motor finance new business volumes grew by 11%.

Oxford Economics research published in 2015 put FLA members’ contribution to the UK economy into perspective when it showed that the industry’s activities supported more than 330,000 UK jobs. The research also found that the industry’s productivity was five times higher than the national average.

Second, the last year saw a number of important challenges for the industry, which – with strong support from its members – the FLA was well-placed to meet.

High up the list was the exceptional number of regulatory initiatives from the Financial Conduct Authority (FCA), covering key issues like affordability and creditworthiness, sales incentives, and the future of the remaining provisions of the Consumer Credit Act. At the same time, FLA members and their intermediary partners were working hard to gain FCA authorisation, a process which has made serious demands not only on them, but also on the regulator.

During the year, the FLA team established and maintained a very good working relationship with the FCA. The FLA’s ability to collate and distil industry knowledge on behalf of its members and stakeholders is invaluable, and particularly important while the FCA is still learning about what is probably the most diverse of all its markets.

The importance of the FLA’s role was highlighted at the end of 2015, when – following a review by some of the larger banks – plans were announced for the merger of several existing financial services trade associations. The review concluded that, as we had argued, the FLA should remain independent, and continue to provide its membership with a distinct and much-valued voice. We look forward to working with the other financial services trade bodies – both old and new – over the coming months.

Obviously, the FLA’s continued strength and effectiveness depends crucially on the input and support of its members. I was therefore very pleased that our most recent annual membership survey showed further growth in membership and the highest level of overall member satisfaction since the financial crisis.

I would like to express my personal thanks to my fellow Board members, and to all the members of the FLA, for their support over the last year.

Nigel Clibbens FLA Chairman

Finance & Leasing Association Annual Review 2016 5

FLA Board Members As at May 2016

Nigel Clibbens, FLA Chairman Chief Financial Officer The Car Finance Company

Steve Bolton Director of Debt Finance Barclays

Mike Britton Director Barclays Partner Finance

Bill Dost Managing Director D&D Leasing

Gordon Ferguson Head of HP & Leasing Lloyds Bank Commercial Finance Ltd

Steve Gowler Managing Director RCI Financial Services Ltd

Gerald Grimes Managing Director Hitachi Capital Consumer Finance

Ian Isaac Managing Director Lombard Sales Lombard North Central PLC

Richard Jones Managing Director Black Horse Motor Finance

Doug Moody Director Mercedes-Benz Financial Services

Carol Roberts Managing Director Bibby Leasing Ltd

Philip Ross Senior Vice President Honda Motor Europe Ltd Director, Honda Finance Europe plc

Stephen Sklaroff Director General FLA

Tim Smith Head of Motor North Black Horse Motor Finance

Finance & Leasing Association 6 Annual Review 2016

Director General’s Report

As the Chairman has noted, over the last year the FLA’s members showed once again just how important they are for the UK economy. That they were at the same time preparing for authorisation under the Financial Conduct Authority’s (FCA) new consumer credit regime is testimony to the industry’s strength and resilience. Along with all the work this involved, FLA members also had to respond to a huge variety of information requests from the FCA, as it continued to build its understanding of a complex market. Obviously, the FCA has to do this. But we have asked them to give more thought to the burden these – often overlapping – demands place on firms already dealing with the authorisation process and a new system of regulation.

Over the year, our good relationship with the FCA enabled us to organise a number of events at which FLA members could hear directly from the regulator about progress in creating the new regulatory system. We were also able to provide briefings for the FCA on the FLA’s markets, taking the opportunity to dispel any misunderstandings or unwarranted assumptions. Our well-attended member

working groups looking at the new regulatory system helped us to keep the FCA informed of FLA members’ concerns as they prepared for authorisation.

We have been quick to challenge unworkable proposals from the FCA, and – in most cases – they have been willing to listen. As the rest of this report shows, during the last twelve months we have discussed an enormous range of issues with them, including the regulatory boundary in the business finance markets, credit-worthiness and affordability, regulation of the card markets, sales incentives, the transfer of the second charge mortgage sector to the new mortgage regime, the fate of the remaining provisions of the Consumer Credit Act, GAP insurance, customer vulnerability, and many others. We were very pleased by the success of our campaign to persuade the Government that the FCA should take over the regulation of Claims Management Companies (CMCs). We will continue to press for a regime which ensures fair outcomes for the CMCs’ customers.

Finance & Leasing Association Annual Review 2016 7

The last year also illustrated the importance of our good relationships with other parts of Government. We collaborated with the British Business Bank (BBB) on a series of publications aimed at boosting the market for asset finance, and we were extremely pleased when they confirmed that they would work with us to develop an asset finance element within the Enterprise Finance Guarantee scheme.

We also worked closely with the Government on the inclusion of asset finance in the new online SME finance referral platforms.

Our promotional work during the year on behalf of the asset finance sector included a very successful first national FLA asset finance conference, a series of roundtable lunches with customer groups – leading to some practical follow-up action – and our stand at the Northern Business Exhibition, where FLA members were able to speak directly to potential new customers. More details can be found in the rest of this report.

The last year also saw the publication – finally – of the International Accounting Standards Board’s new standard for lease accounting, IFRS16. While the new standard does not apply to SME lessees subject to UK GAAP, we are working with the UK Financial Reporting Council to avoid any possible future new burdens

for companies which use leasing or hire purchase. We are also working with the Government to minimise any adverse effect of IFRS16 in the public sector markets, where international standards often apply directly.

As the Chairman has said, FLA members now finance over 80% of private new car purchases. We have worked with members to ensure that the FCA and the Bank of

England properly understand the sector, both in the context of conduct regulation and in the national debate about overall levels of personal credit. We have reminded the media on a number of occasions that motor finance is usually secured on the vehicle. We have also worked with members to help them and their intermediary partners adapt to the new FCA regime.

In the continuing fight against vehicle crime, we have made good progress in discussions with other interested parties on how best to minimise Direct Debit fraud. FLA sponsorship of the National Vehicle Crime Intelligence Services (NaVCIS) is now in its ninth year and has recovered a total of 2,911 vehicles worth over £42 million, and 480 vehicles over the last twelve months.

Ahead of last year’s General Election, the FLA published its own Manifesto 2015. We used it to brief candidates on the FLA’s priorities, and broaden our circle of supportive parliamentarians after the election. At the 2015 party conferences, we hosted joint events with the Manufacturing Technologies Association. Politicians, FLA members and manufacturers discussed how the Government could best support

the funding of high-tech manufacturing. We distributed the findings widely to policymakers and commentators, and included them in our briefings for the Chancellor in advance of his subsequent Autumn Statement and Budget. Our work in Brussels to ensure a sensible outcome for discussions on a new EU Data Protection Regulation reached a successful conclusion, preserving the

industry’s ability to gather and use data for responsible lending and fraud prevention. We are now working with the UK Information Commissioner’s Office on some of the important detail before implementation in 2018. Building on our strong relationship with Eurofinas and Leaseurope, our European federations, we welcomed the appointment of Leon Dhaene as their Director General in December, and have been in close contact with him on a number of issues. We ran 89 training courses in 2015, many of which were over-subscribed. Our conferences and other member events also continued to attract high numbers, and the 2016 Annual Dinner was once again sold out. I would like to echo the Chairman’s thanks to all the FLA’s members for their continued support, and to add my personal thanks to the team at Kingsway for their hard work during an exceptionally busy year.

Stephen SklaroffDirector General

We have worked with members to ensure that the FCA and the Bank of England properly understand the sector, both in the context of conduct regulation and in the national debate about overall levels of personal credit.

Our work in Brussels to ensure a sensible outcome for discussions on a new EU Data Protection Regulation reached a successful conclusion, preserving the industry’s ability to gather and use data for responsible lending and fraud prevention.

Finance & Leasing Association 8 Annual Review 2016

FCA regulationA large number of FLA Asset Finance Division (AFD) members are covered by the new Financial Conduct Authority (FCA) regime for consumer credit, because of the definition of “consumer” in the Consumer Credit Act. While we welcomed the FCA’s recognition of the importance of business plans when assessing credit-worthiness in the business finance markets, we continue to be concerned that the regulatory boundary sits in the wrong place.

The FCA published a discussion paper in November asking about the appropriateness of current levels of regulatory protection for small and medium sized enterprises (SMEs). In our response, we reiterated our belief that the consumer credit regime is not a good fit for the business finance markets. The risk, as we have pointed out to the Government, is that the additional burden of the new regime will encourage some lenders and intermediaries to leave the regulated markets altogether.

We have suggested to the FCA that this be addressed urgently, as part of the review it is conducting for the Government of the remaining provisions of the Consumer Credit Act.

Meanwhile, we have worked closely with AFD members to identify the main challenges and problems they have faced in applying for FCA authorisation. We have also worked with the FCA to improve their knowledge of the business finance markets and of FLA members’ business models.

Promoting the industryWe have continued our wide-ranging programme of activity aimed at promoting asset finance to potential new customers.

Asset Finance

Finance & Leasing Association Annual Review 2016 9

We held our first national asset finance conference in June 2015. Members were joined by speakers from the British Business Bank (BBB), the FCA, ComRes and Google, among others. The response from attendees was very positive, and a second conference will be held this summer.

We also held a symposium for members on the funding of intangibles, where they heard from Innovate UK (one of the relevant Government bodies), and the former Chief Economist of the Intellectual Property Office. The event provided a useful opportunity to discuss the pricing of risk in this developing market. In partnership with the Manufacturing Technologies Association (MTA), we held roundtable discussions at the 2015 Conservative and Labour Conferences about the ways in which asset finance could help increase investment in high-tech manufacturing. When the Government decided to channel further support for local business growth through the Local Enterprise Partnerships (LEPs), we contacted all 39 partnerships across the UK to ensure that leasing and hire purchase played a full part of the financial infrastructure supporting SMEs. This work is continuing with follow-up meetings. Our series of roundtable lunches remains a popular way to bring together AFD members and customer groups, including the ICAEW, the Association of Corporate Treasurers, the EEF and the Road Haulage Association. Discussion so far has ranged from customers’ perceptions and use of asset finance, to the practical steps that the FLA can take to help promote the benefits of leasing and hire purchase to potential users.

We have also worked with the BBB on a number of official publications explaining the advantages of leasing and

hire purchase. These included the BBB’s latest Small Business Finance Markets Report, which once again referred to asset finance as a market solution to a market failure in small business lending, and the widely-downloaded BBB Business Finance Guide. Work on a second edition of the latter is at an advanced stage, and will include a digital version housing a wealth of on-demand detail about the finance options available to SMEs. In partnership with the BBB and the Institute of Chartered Accountants in England and Wales (ICAEW), we produced an

additional booklet for distribution through accountants’ offices, specifically covering the benefits of leasing and hire purchase.

In the recent Budget, the Government gave the go-ahead for three online platforms aimed at SMEs looking for alternative finance. We are in touch with the providers to ensure that they include asset finance in their platforms, and we are also discussing the practicalities with FLA members who would like to feature.

The BBB has now confirmed that FLA members will help it to develop an asset finance option for the Enterprise Finance Guarantee scheme, with a view to launching the new facility later in 2016. This is very good news for the industry, and reflects the work the FLA has done to bring this about.

Higher asset finance qualificationWork continued on the re-designed FLA asset finance qualification, which we are developing with ifs University College.

A Chief Examiner has been appointed, and a steering group of FLA members is overseeing the detailed content of the new course.

The FLA Business Finance CodeDuring the year, members have worked on an updated and modernised version of the FLA’s Business Finance Code, taking account – for example – of the new FCA regime for credit. We have also developed operational good practice guidance for FLA members working with intermediaries, and we are collaborating with the National Association of Commercial Finance Brokers (NACFB) to ensure the greatest possible degree of alignment with their own guidance for brokers.

New Lease Accounting StandardJanuary 2016 saw the long-awaited publication of IFRS 16, the new Lease Accounting Standard from the International Accounting Standards Board (IASB). Prior to publication, we had worked hard with Leaseurope (our European federation), the IASB itself, the UK Financial Reporting Council (FRC), the Association of Chartered Certified Accountants, and a number of other bodies to minimise so far as possible the burdens imposed on asset finance customers by the new Standard.

While it is helpful that the new standard does not apply to SMEs, and that the relevant UK GAAP is not due for revision for some time, we remain concerned to ensure that IFRS16’s more complex way of calculating lease-related assets and liabilities does not deter existing or potential asset finance customers. We are continuing to work with the FRC with this in mind. We are also discussing with the Government the way IFRS16 will affect public sector accounting, which often follows international accounting rules. We are continuing to work with Leaseurope to ensure that the European Financial Reporting Advisory Group (EFRAG) Board (which will advise the EU Commission on the implementation of the new standard) is properly aware of the industry’s concerns.

The consumer credit regime is not a good fit for the business finance markets.

The BBB has now confirmed that FLA members will help it to develop an asset finance option for the Enterprise Finance Guarantee scheme, with a view to launching the new facility later in 2016.

Finance & Leasing Association 10 Annual Review 2016

Consumer Finance

FCA Regulation2015 was a particularly challenging year for the credit industry. Firms faced a constant stream of regulatory announcements while they were preparing for, or going through, the Financial Conduct Authority’s authorisation process.

Major developments during the year included thematic reviews by the FCA into early arrears and staff remuneration, an interim report on the FCA’s Credit Card Market Study, a pilot study of how lenders assess creditworthiness and affordability, and the transfer of second charge mortgage lenders from the FCA’s consumer credit regime to its mortgage regime, following the introduction of the EU Mortgage Credit Directive.

The FCA closed its last authorisation “slots” at the end of March 2016, but it will be another year before all applications have been determined. Most FLA members who attended our conferences on the new regulatory system reported that they needed help in understanding exactly what information the regulator required. We hosted a number of workshops for members on the authorisation process, and discussed with the FCA how they might make their requirements clearer, so as to minimise delays.

During the year, consumer vulnerability emerged as a major theme for the FCA. More than 60 members attended an FLA event to discuss how lenders could better identify and assist this customer group. We have now established a Vulnerability Hub on the FLA website to provide

members with a ‘one-stop-shop’ for information and good practice on vulnerability. We have also commissioned (together with the UK Cards Association) some new research from the Personal Finance Research Centre at the University of Bristol, aimed at identifying practical tools that lenders might use in identifying customer vulnerability, and what assistance they could then provide. A report should be available in early 2017. The FCA has now launched its long-awaited review of the remaining provisions of the Consumer Credit Act (CCA). We have already submitted our initial recommendations to the FCA, based on the results of several member workshops. Many of the CCA’s provisions are outdated and not in keeping with modern standards of customer service. The Act’s overly-complex provisions have, on occasion, left customers and firms with no choice but to seek clarity through litigation. The review presents an opportunity to ensure that the new credit regime properly reflects the needs of the credit customers in the 21st Century.

We will be working closely with the FCA and the Government to achieve this.

Second charge lenders successfully transferred from the consumer credit regime to MCOB, the FCA’s mortgage regime, despite having less than a year in which to do so. We worked very closely with the FCA on the implementation process, and we were invited to chair a cross-industry group, including lenders and brokers, to help ensure that any potential problems were addressed quickly. The FLA won an Outstanding Contribution award from Loan Talk for our work in assisting the industry. As the FCA’s regulatory framework is in a state of constant change, we continued to provide members with daily and monthly regulatory updates to help keep them aware of developments as they happened.

We provided the FCA with detailed responses to a wide range of consultations, including on their credit card market study, further changes to the credit rulebook (CONC), the regulation of guarantees in the credit markets, competition in the mortgage market, financial crime reporting, lending via tablet and mobile technology, and new PPI complaint-handling rules. Our monthly Regulatory Reform Working Group regularly attracted more than 50 member firms. The FCA provided a number of speakers. Members’ engagement with the issues, and willingness to provide feedback on regulatory responses, helped put the FLA on the front foot in discussions with the regulator. We were able to help

Consumer vulnerability emerged as a major theme for the FCA. More than 60 members attended an FLA event to discuss how lenders could better identify and assist this customer group.

Finance & Leasing Association Annual Review 2016 11

the FCA understand the diversity of the credit market and how it works in practice. This is particularly important for our discussions with the FCA on possible changes to the rules on affordability and creditworthiness assessments, where we are urging a proportionate approach. Overall, our relationship with the FCA remains strong. We are regular attendees at FCA meetings, and also sit on several of their working groups, which allows us to influence debates at an early stage.

Claims Management CompaniesWe have been lobbying over many years for better CMC regulation, with incremental success. The last few months saw a major step forward. The Government has finally accepted our view that conduct supervision for this sector should move to the FCA, a development widely welcomed in the financial services industry.

In the meantime, the Government is consulting on a price cap on CMCs’ charges to their customers, aimed at reducing the proportion of any redress a CMC can take for itself.

Debt ProtocolWe continued to oppose the introduction of a new Pre-Action Protocol for debt claims, on the basis that it would merely duplicate information already sent to customers and add to Court costs. The Ministry of Justice has gone back to the drawing board.

Financial CrimeWe worked with the National Crime Agency (NCA) and the Home Office to influence the future shape of the Suspicious Activity (SARs) regime, which has become too resource-intensive and is no longer fit for purpose. We are also working with partners on the Joint Money Laundering Steering Group’s (JMLSG’s) guidance, in view of the forthcoming 4th EU Anti-Money-Laundering Directive.

Members’ engagement with the issues, and willingness to provide feedback on regulatory responses helped put the FLA on the front foot in discussions with the regulator.

Finance & Leasing Association 12 Annual Review 2016

Motor Finance

FCA RegulationOver the last year, we have briefed FCA policy, supervision and authorisation staff to ensure they understand how the motor finance market works. We have stressed to the FCA the wide diversity of the market, which now funds over 80% of UK consumer purchases of new cars. Customers’ needs and circumstances vary widely, as do the types of credit they seek, and the FCA’s rules on affordability and creditworthiness must continue to reflect this diversity and allow a proportionate approach to each market. The intermediary market was a particular focus of work during the year, including efforts to support regulatory compliance. Building on the extensive work already done in this area, we hope to be able to continue to reassure the FCA about market progress, as the regulator considers possible new rules for sales incentives.

We were pleased that the FCA’s new rules on GAP insurance, which came into effect in September 2015, reduced the compulsory delay between purchasing a car and purchasing the associated GAP insurance from the 30 days initially suggested to 2 clear days.

Vehicle Fraud Vehicle-related fraud remains a concern, and we have monitored levels during the year, highlighting particular problem areas when they have emerged. We have made recent progress in addressing possible abuses of the direct debit system, in collaboration with BACS, the Payment Systems Regulator, and the relevant banks. One result is new guidance aimed at identifying suspicious claims before they are paid.

We have also worked with online vehicle-selling sites to reduce the risk of illegal online ‘conversion fraud’ by ensuring buyers receive targeted communications, reminding them of the potential risk of buying vehicles which may already be subject to a finance agreement.

As the paper counterpart of the UK driving license has now been abolished, we have revised the FLA’s long-standing ‘lamp and stamp’ guidance, and worked with members to update FLA guidance on related fraud issues.

FLA sponsorship of the National Vehicle Crime Intelligence Service (NaVCIS) is now in its ninth year. A total of 2,911 vehicles worth over £42 million have been recovered for our members since the inception of the scheme. Over the last year, 480 vehicles were recovered worth £6.5 million. We are also reworking our contracts with NaVCIS to improve accountability.

Asset ProtectionMFD members participated actively in the FLA’s Asset Registration Group throughout the year, as the processes for registering and protecting their vehicle assets underwent significant change. We worked with members, including our Motor Asset Registration Services (‘MARS’) data agency members, to produce revised guidance and protocols to ensure the continued efficient protection of members’ interests in the vehicles they finance.

Industry skillsThe FLA’s Specialist Automotive Finance (SAF) programme, aimed at improving the understanding of motor finance products among showroom staff, continued to expand. Over 20,000 dealership staff have now signed up to take the SAF test and

most of the larger dealer groups have achieved ‘SAF Approved’ status, indicating that all of their relevant staff hold a current SAF certificate.

A new higher-level certificate for automotive finance specialists (known as ‘SAF Advanced’) was launched in June 2015 by the FLA and ifs University College, and has already attracted 200 students. Equivalent to an A-level, SAF Advanced is aimed at managers and leaders involved in selling motor finance. Work is now in hand to explore possible synergies between SAF training and the Government’s current initiatives on industry apprenticeships.

Customers’ needs and circumstances vary widely, as do the types of credit they seek, and the FCA’s rules on affordability and creditworthiness must continue to reflect this diversity and allow a proportionate approach to each market.

Finance & Leasing Association Annual Review 2016 13

Finance & Leasing Association 14 Annual Review 2016

Finance & Leasing Association Annual Review 2016 15

Westminster and Brussels

The General ElectionThe General Election made 2015 a particularly busy year for the FLA’s parliamentary lobbying. We identified key Prospective Parliamentary Candidates before the election, and briefed them on the FLA’s priorities using our own FLA Manifesto 2015. Following the election, we ensured that new MPs, and the new frontbench teams and their advisers, received tailored briefings.

In the autumn, we co-hosted two very successful events with the Manufacturing Technologies Association at the Labour and Conservative Party conferences, exploring how asset finance could help fund high-tech manufacturers. The recommendations from these events were used to brief the Chancellor, MPs and policy-makers ahead of the 2015 Autumn Statement and 2016 Budget. The Chancellor pledged a two-year extension to the Enterprise Finance Guarantee scheme in his March 2016 Budget statement, which the FLA warmly welcomed. We were also pleased with his announcement that the FCA would take on the regulation of claims management companies, a subject of FLA lobbying for a long time.

Access to Finance In its strategic review of the Enterprise Finance Guarantee Scheme (EFG), the British Business Bank (BBB) announced that it had invited FLA members to participate in a working group to develop a leasing and hire purchase element within the guarantee scheme. This very welcome move reflects discussions we have had with the Government and BBB, and we look forward to the launch of the new EFG facility later in 2016.

In February, the Business, Innovation and Skills Committee’s inquiry into access to finance looked at the evolution of the business funding landscape since the end of the financial crisis, and the extent to which Government intervention had helped businesses to raise funds. Our submission called on the Government to consider an effective replacement for the Regional Growth Fund, and we are now discussing with Local Enterprise Partnerships (LEPs) how they can best involve asset finance providers.

EU Data Protection RegulationFour years of FLA lobbying on the proposed new EU Data Protection Regulation resulted in a much better text, which will continue to allow credit providers to gather and use customer data for the purposes of responsible lending and fraud prevention. The new wording was adopted in May 2016, and must be implemented by the UK and other EU Member States by 25 May 2018. To minimise any adverse market effects, we will be working with the UK Information Commissioner’s Office, the FCA, and relevant Government departments in the lead-up to this date.

SecuritisationAt the end of September, the EU Commission published plans to revitalise the European securitisation market as part of its Capital Markets Union Action Plan. We broadly supported the proposed standard framework, but argued that broader criteria were needed to allow the inclusion of more FLA-type assets in short-term securitisations. We have made good progress in discussions with the national governments, which reached an informal agreement in December. We are now briefing MEPs in advance of debate in the European Parliament later in 2016.

EU Retail Financial Services Green PaperIn December, the Commission published a Retail Financial Services Green Paper. We argued in response that there was little consumer demand for cross-border loans, and that further regulation in this area was unlikely to be helpful.

Finance & Leasing Association 16 Annual Review 2016

Research and Statistics

The UK Economy In 2015, the UK economy grew by 2.3% compared with the previous year. Domestic demand again drove the economy, as growth in household expenditure reached an eight-year high of 2.8%. Business investment grew by 5.2%, its fastest rate since 2010. The goal of rebalancing the economy to ensure a greater contribution from net trade remained elusive. The slowdown in emerging markets in 2015 and a weak recovery by the major Eurozone economies meant the contribution to GDP growth from net trade last year was negative, at 0.5 percentage points.

Consumer confidence reached a fifteen-year high in 2015, supported by further improvements in the unemployment rate, a weak inflation rate and a low interest rate environment. In the final quarter of 2015,

the unemployment rate reached a decade low of 5.1%, while further falls in oil and commodity prices during 2015 meant the inflation rate was only 0.2% by the end of the year. As a result, the Bank of England kept Bank Rate at 0.5% for a sixth consecutive year.

The risks to the outlook for consumer and business spending have increased in the first quarter of 2016. A weaker global economic outlook and the uncertainty about the result of the European Union membership referendum may dampen confidence in the near term. The most recent Oxford Economics forecasts suggest that the economy will grow by 2.0% in 2016 as a whole. Private consumption and business investment are each expected to be 2.5% higher in 2016 than in the previous year.

2.0%2016 GDP growth forecast*

2.5%Business investment growth forecast*

2.5%Private consumption growth forecast*

*Oxford Economics May 2016 forecasts

Finance & Leasing Association Annual Review 2016 17

£29.1bnnew business in 2015

In 2015, the asset finance market reported its second year of double-digit growth. New business increased by 12% compared with 2014, to reach a seven-year high of more than £29 billion. The IT equipment finance sector reported the strongest rate of growth, as new business grew by 38% compared with 2014. Other strong performers included the commercial vehicle finance and business car finance sectors, with new business up by 14% and 11% respectively over the same period.

The industry saw a further increase in its contribution to the funding of UK investment in 2015, as the percentage of UK investment in machinery, equipment and purchased software financed by FLA members reached 31.5%, a six-year high. The success rate of SMEs when applying for asset finance also increased to 94% in 2015. Of the total new asset finance provided to businesses last year, more than £16 billion went to help SMEs invest in equipment.

The asset finance market continued to grow in the first quarter of 2016, with new business 8% higher than in the same quarter in 2015, at £7.5 billion. The vehicle finance sectors reported relatively strong growth, as business car finance and commercial vehicle finance each increased by 9% compared with Q1 2015. By contrast, new business reported by the business equipment finance and plant and machinery finance sectors grew by only 3% and 1% respectively over the same period. The Q1 2016 figures suggest that business confidence remains relatively robust despite increased uncertainty about the economic outlook, and are in line with the industry’s expectations of single-digit new business growth in 2016 as a whole.

Research and Statistics Asset Finance

Asset finance new business written by FLA members(£ billions)

Percentage of UK investment in machinery, equipment and purchased software financed by FLA members

2011 2012 2013 2014 2015 2011 2012 2013 2014 2015

35

30

25

20

15

10

5

0

35

30

25

20

15

10

5

0

Finance & Leasing Association 18 Annual Review 2016

FLA consumer finance new business (£billions)

There is a break in the time series in 2012 due to changes in FLA membership

100

80

60

40

20

0

In 2015, FLA consumer finance new business increased by 8% to £80.9 billion. This was in line with growth in new consumer credit for the UK overall, which grew in 2015 by 9% to reach almost £245 billion. FLA members’ share of UK new consumer credit in 2015 was 33.0%, down slightly from 33.5% in 2014.

There was growth across the main finance products in 2015. The point-of-sale finance sector (primarily car finance) grew by 14% to £32.1 billion; personal loans and credit card new business together increased by 4% to £41.4 billion; and retail store and online credit grew by 2% to £6.5 billion.

1%

40% 51%

8%

Distribution of FLA consumer finance new business by channel in 2015

Research and Statistics Consumer Finance

Personal loans and credit cards

Point-of-sale finance

Retail store and online credit

Second charge mortgages

2011 2012 2013 2014 2015

£80.9bnnew business in 2015

The second charge mortgage market reported new business up 34% by value to £844 million and 9% by volume to reach 20,647 new agreements in 2015. Although new business in this market was at its highest annual level since 2008, it remained significantly below pre-crisis levels, when it peaked at over £5 billion by value and 200,000 by volume.

In Q1 2016, FLA members providing consumer finance reported new business up by 14% to £22.1 billion, with further growth across all the main finance products.

Finance & Leasing Association Annual Review 2016 19

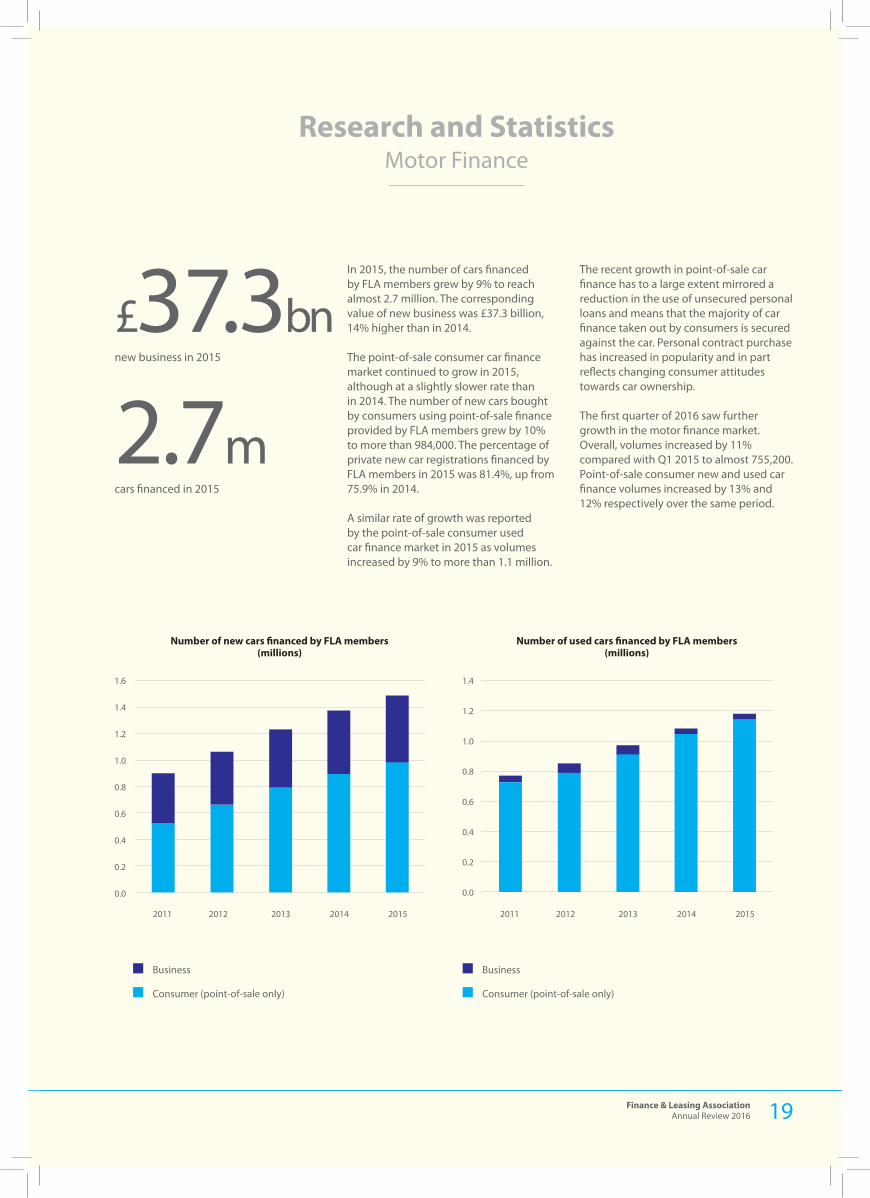

In 2015, the number of cars financed by FLA members grew by 9% to reach almost 2.7 million. The corresponding value of new business was £37.3 billion, 14% higher than in 2014.

The point-of-sale consumer car finance market continued to grow in 2015, although at a slightly slower rate than in 2014. The number of new cars bought by consumers using point-of-sale finance provided by FLA members grew by 10% to more than 984,000. The percentage of private new car registrations financed by FLA members in 2015 was 81.4%, up from 75.9% in 2014.

A similar rate of growth was reported by the point-of-sale consumer used car finance market in 2015 as volumes increased by 9% to more than 1.1 million.

The recent growth in point-of-sale car finance has to a large extent mirrored a reduction in the use of unsecured personal loans and means that the majority of car finance taken out by consumers is secured against the car. Personal contract purchase has increased in popularity and in part reflects changing consumer attitudes towards car ownership.

The first quarter of 2016 saw further growth in the motor finance market. Overall, volumes increased by 11% compared with Q1 2015 to almost 755,200. Point-of-sale consumer new and used car finance volumes increased by 13% and 12% respectively over the same period.

2.7mcars financed in 2015

Research and Statistics Motor Finance

Business

Consumer (point-of-sale only)

Business

Consumer (point-of-sale only)

Number of new cars financed by FLA members(millions)

Number of used cars financed by FLA members(millions)

2011 2012 2013 2014 2015 2011 2012 2013 2014 2015

1.6

1.4

1.2

1.0

0.8

0.6

0.4

0.2

0.0

1.4

1.2

1.0

0.8

0.6

0.4

0.2

0.0

£80.9bnnew business in 2015

£37.3bnnew business in 2015

Finance & Leasing Association 20 Annual Review 2016

Events and Training

The FLA ran 89 courses during 2015, nearly a third of which were tailored specifically for individual member companies, and delivered in-house on company premises. Our public courses were often over-subscribed, and additional courses were scheduled to meet demand. The same trend continues into 2016.

We organised and hosted a number of events for members during the year, including our first National Asset Finance Conference, additional conferences and

workshops on the FCA’s new system of credit regulation, and the annual Motor Finance Convention. All were very well-attended, and the feedback was excellent.

We also hosted a number of events regionally, including popular receptions in Manchester and Birmingham for locally-based members. More are planned. The 2016 Annual Dinner was one of the most successful ever. We welcomed 1,500 guests to Grosvenor House, where John Humphrys and Gabby Logan spoke.

Finance & Leasing Association Annual Review 2016 21

Key Dates for 2016/172016

2 JuneGolf DaySt George’s Golf Club Weybridge, Surrey

7 JuneFLA Regulation Conference The IET, Savoy Place, London

23 JuneAsset Finance ConferenceBarber Surgeons’ Hall, London

2 November Asset Finance ConferenceVenue TBC

24 NovemberMotor Finance ConventionF1 Centre, Oxfordshire

1 DecemberChristmas Drinks ReceptionBrewers’ Hall, London

2017

28 February2017 Annual DinnerGrosvenor House, London

Finance & Leasing Association 22 Annual Review 2016

Members DirectoryFULL MEMBERS118 118 Money

1st Stop Group Ltd

A

ABN AMRO Lease NV

Advantage Finance Ltd

ALD Automotive Limited

Aldermore

Allied Irish Bank (GB)

Alphabet (GB) Ltd

Arkle Finance Ltd

Asset Advantage Limited

Azule Limited

B

Bank of London and The Middle East

Barclays Asset Finance

Barclays Partner Finance

Bibby Leasing Ltd

Billing Finance Ltd

Black Horse Motor Finance

Blue Motor Finance

BMW Financial Services (GB) Limited

BNP Paribas Leasing Solutions

Briggs Equipment UK Limited

Brighthouse

C

Cambridge and Counties Bank

Caterpillar Financial Services (UK) Limited

Central Trust Limited

Charter Court Financial Services Limited

CHG-MERIDIAN UK Limited

Churchill Finance Group Ltd

Close Brothers

Close Brothers Motor Finance

Clydesdale & Yorkshire Bank Asset Finance

Commerzbank AG

Compass Business Finance Ltd

Conister Bank Limited

CSI Leasing UK Ltd

D

D & D Leasing UK Ltd

Danske Bank

Deutsche Leasing (UK) Limited

DLL

E

Evolution Banking Ltd

Express Gifts Limited

F

FCA Automotive Services UK Ltd

FCE Bank plc

Ferrari Financial Services AG

First Response Finance Ltd

Future Finance Loan Corporation

G

GE Capital UK

GE Money Home Finance Limited

Genesis Capital Finance and Leasing Ltd

Girbau UK Limited

GM Financial

H

Hampshire Trust Bank plc

Harley-Davidson Financial Services Europe Limited

Haydock Finance Ltd

Henry Howard Finance Group

Hitachi Capital (UK) plc

Home Retail Group Financial Services

Honda Finance Europe plc

HSBC Asset Finance (UK) Ltd

HSBC Bank plc

Hyundai Capital UK Limited

I

IBM United Kingdom Financial Services Limited

Ikano Bank UK

Innovent Leasing Limited

Investec Asset Finance plc

Iveco Capital Limited

J

JBR Capital Limited

JCB Finance Ltd

John Deere Bank S.A.

K

Kennet Equipment Leasing Ltd

Kingsway Asset Finance Ltd

L

LaSer UK

LDF Operations Ltd

LeasePlan UK Limited

Leasing Programmes Limited

Lloyds Bank Commercial Finance Ltd

Lombard North Central plc

London and Surrey Motor Finance

LRUK (Retail) Limited

Asset Finance Consumer Finance Motor Finance

Finance & Leasing Association Annual Review 2016 23

Shire Leasing plc

Shop Direct Finance Company Limited

Siemens Financial Services Ltd

SMBC Leasing (UK) Limited

Société Générale Equipment Finance Ltd

Startline Motor Finance Ltd

Step One Finance Limited

Syscap Limited

T

Telefonica UK Limited

The Car Finance Company

The Funding Corporation Limited

Together

Toyota Financial Services (UK) plc

Triple Point Lease Partners

U

UK Credit Limited

United Trust Bank Limited

V

Vehicle Trading Group

Virgin Media Mobile Finance Limited

Volkswagen Financial Services (UK) Ltd

W

Wonga Group Limited

X

Xerox Finance Ltd

ASSOCIATE MEMBERSA

Acquis Insurance Management Limited

Addleshaw Goddard LLP

Allen & Overy LLP

Anglia (UK) Limited

Arrow Global Limited

Au10tix

Auto Trader

Autoprotect MBI Ltd

B

BenchMark Consulting International

Bermans LLP

Blake Morgan

British Car Auctions

Brodies LLP

C

Cabot Credit Management Limited

Callcredit Information Group

cap hpi*

M

Macquarie Equipment Finance (UK) Ltd

MAN Financial Services plc

Marsh Finance Ltd

Masthaven Secured Loans Ltd

Maxxia Limited

MBNA Limited

Mercedes-Benz Financial Services UK Ltd

Metro Bank Asset Finance

Moneybarn

Moneyway

MotoNovo Finance

N

Nemo Personal Finance

Neopost Finance Ltd

NewDay Limited

NextGear Capital UK Ltd

Northridge Finance

Norton Home Loans Limited

O

Omni Capital Retail Finance Ltd

Optimum Credit Ltd

P

PACCAR Financial plc

Pan European Asset Company (PEAC)

Paragon Bank Business Finance plc

Paragon Group plc

Pitney Bowes Ltd

Praetura Asset Finance Ltd

Premium Credit Limited

Premium Plan Limited

Prestige Finance Ltd

PSA Finance UK Ltd

R

Raphaels Bank

RCI Financial Services (GB) Ltd

Renaissance Asset Finance Ltd

Ricoh Capital Limited

S

Samsung Capital

Santander Asset Finance plc

Santander Cards (UK) Ltd

Santander Consumer (UK) plc

Santander UK plc

Secure Trust Bank plc

Shawbrook Asset Finance

Shawbrook Bank Limited

Finance & Leasing Association 24 Annual Review 2016

Capita Asset Services - Treasury Solutions

CDL Vehicle Information Services*

CHP Consulting Ltd

CMS Cameron McKenna LLP

D

D&B (Dun & Bradstreet)

Dains LLP

Dealflo

Deloitte LLP

DLA Piper UK LLP

DWF LLP

E

Equifax Ltd

Equiniti

Eversheds LLP

Experian Ltd*

F

Financial Insurance Group Services Ltd - UK

G

Gateley PLC

Glass's Information Services

GMG Asset Management UK LTD

Gowling WLG

Grant Thornton UK LLP

Great American Lease & Loan Insurance Services

H

Hilton-Baird Financial Solutions

HITEC (Laboratories) Ltd

Hogan Lovells LLP

Huntswood CTC Ltd

I

International Decision Systems Ltd

Invigors EMEA LLP

ITC Compliance Ltd

J

JCA Associates

K

Kee Resources Limited

KPMG LLP

L

Lester Aldridge LLP

Link Financial Ltd

Locke Lord (UK) LLP

Lowell Financial Limited

M/N

Max Recovery

McManus Kearney

Morton Fraser Solicitors

National Association of Commercial Finance Brokers

NetSol Technologies Europe Ltd

Nostrum Group Limited

O

Oyster Bay Systems Ltd

S

Shoosmiths LLP

Solutions Asset Finance Ltd

Sopra Group

Sword Apak

T

Target Group Limited

TLT LLP

Total Car Check Limited

V

VIP Apps Consulting Limited

W

Walker Morris LLP

Welcom Digital Ltd

White Clarke Group

* Members of Motor Asset Registration Services

Finance & Leasing Association Annual Review 2016 25

Contacting the FLA

DIRECTOR GENERAL’S OFFICE Stephen SklaroffDirector GeneralT: 020 7420 9660E: [email protected]

Haidee WyattExecutive AssistantT: 020 7420 9606E: [email protected]

CONSUMER FINANCEFiona HoyleHead of Consumer and Mortgage FinanceT: 020 7420 9635E: [email protected]

Richard BostockSenior Policy AdviserT: 020 7420 9605E: [email protected]

Henry AitchisonSenior Policy AdviserT: 020 7420 9661E: [email protected]

Patsy CalnanCode Compliance OfficerT: 020 7420 9612E: [email protected]

Hanifa TeladiaSenior AdministratorT: 020 7420 9637E: [email protected]

BUSINESS FINANCESimon Goldie Head of Asset FinanceT: 020 7420 9610E: [email protected]

Nicholas Smith Senior Policy AdviserT: 020 7420 9668 E: [email protected]

MOTOR FINANCEAdrian DallyHead of Motor FinanceT: 020 7420 9658E: [email protected]

James MarquetteSenior Policy AdviserT: 020 7420 9613E: [email protected]

Stephanie CookAdministratorT: 020 7420 9657E: [email protected]

GOVERNMENT AFFAIRSEdward SimpsonHead of Government AffairsT: 020 7420 9654E: [email protected]

COMMUNICATIONSAndrea Kinnear Head of Communications T: 020 7420 9664E: [email protected] Jack HarveyPress OfficerT: 020 7420 9656 E: [email protected]

RESEARCH AND STATISTICSGeraldine KilkellyHead of Research and Chief EconomistT: 020 7420 9630E: [email protected]

Christopher McFaulStatisticianT: 020 7420 9629E: [email protected]

Paulo Rosario EconomistT: 020 7420 9632 E: [email protected]

FINANCE, RESOURCES AND MEMBER SERVICESJanet EdwardsHead of Finance and ResourcesT: 020 7420 9615E: [email protected]

Beverley GordonAccountantT: 020 7420 9604E: [email protected]

Linda Charles-Richards Events Manager T: 020 7420 9626 E: [email protected] Jon DearCommercial Services ManagerT: 020 7420 9623E: [email protected]

Tara BorehamCommercial Services Team AdministratorT: 020 7420 9643E: [email protected]

Cherie NichollsIT and Facilities ManagerT: 020 7420 9611E: [email protected]

Elaine BushnellAdministratorT: 020 7420 9619E: [email protected]

Finance & Leasing Association Imperial House15-19 KingswayLondonWC2B 6UNT: 020 7836 6511F: 020 7420 9600E: [email protected]: www.fla.org.uk

Finance & Leasing Association Imperial House, 15-19 Kingsway, London WC2B 6UN

T: 020 7836 6511 | F: 020 7420 9600 | E: [email protected] | W: www.fla.org.uk

www.fla.org.uk