fixed income derivatives - nasdaq€¦ · the exchange rules of nasdaq derivatives markets ... all...

TRANSCRIPT

Fixed Income Derivatives

Functional Changes November 2017 Genium INET 5.0.0201

Document Updated: 16 October 2017

Document Updates

2017-08-30 First version published

2017-09-06 Updated: Trade Report type “NTFI” will not be dismissed in Jan-18 Trade report type “OTC” will not be applicable for Fixed Income Derivatives Pictures of Market models Reference to the exchange rulebook

2017-10-04 Updated launch dates for: 3.3.1 Introduction of two new trade report types - Changed from Jan 2

nd to Jan 3

rd

4.4 Deferred Trade-Publication – Changed from Nov 20 to Jan 3

rd

2017-10-04 Added: - New chapter 3.3.1.2 Change of FIX and OMnet API

trade report Code on NTFI - Information on Change of FIX and OMnet API trade

report Code on EXFI - New chapter 4.7 Trader ID validation

2017-10-16 Added information about new trade report types for Package

Transactions in chapter

- 4.5 and 4.2 for exchange trades - 3.3.3 and 3.3.1.3 for OTC trades

2017-11-07 Updated information on new trade report types for Package Transactions in chapter 3.3.1.3

Table of Contents 1 Introduction ............................................................................................................................................ 3

2 General about the contracts, market and trading ................................................................................. 4

3 Bilaterally Traded contracts ................................................................................................................... 6

3.1 Time limits on clearing of Bilaterally Traded contracts ................................................................... 6

3.2 Functional changes related to bilaterally traded Generic Rates contracts that are subject to

Nasdaq pre-novation collateral check and clearing broker affirmation ............................................... 6

3.3 Functional changes related to bilaterally traded contracts that are not subject to Nasdaq pre-

novation collateral check or clearing broker affirmation ...................................................................... 6

4 Off order book traded contracts ........................................................................................................... 10

4.1 Trade Registration ......................................................................................................................... 10

4.2 Trade report types ......................................................................................................................... 11

4.3 Minimum Block Trade Size............................................................................................................. 11

4.4 Deferred Trade-Publication ........................................................................................................... 12

4.5 Package Transactions .................................................................................................................... 12

4.6 Time of agreement field ................................................................................................................ 13

4.7 Trader ID validation ....................................................................................................................... 13

5 Market Model - Nasdaq Fixed Income Derivatives ............................................................................... 14

1 Introduction The Genium INET 5.0.0201 release introduces several updates to business functionality available for the

fixed income derivatives market. Several of the new features will be activated in January 2018 rather

than in connection with the technical upgrade in November. A draft version of the new fixed income

derivatives market model document is planned to be published during September 2017.

This document outlines planned functional changes focusing on updates to business logic for the

purpose of facilitating implementation and testing of the new release. The information provided in this

document is preliminary and may be subject to change pending, inter alia, completion of or further

guidance in MiFID II related level 2 and 3 texts, and in some cases ongoing discussions or regulatory

approvals.

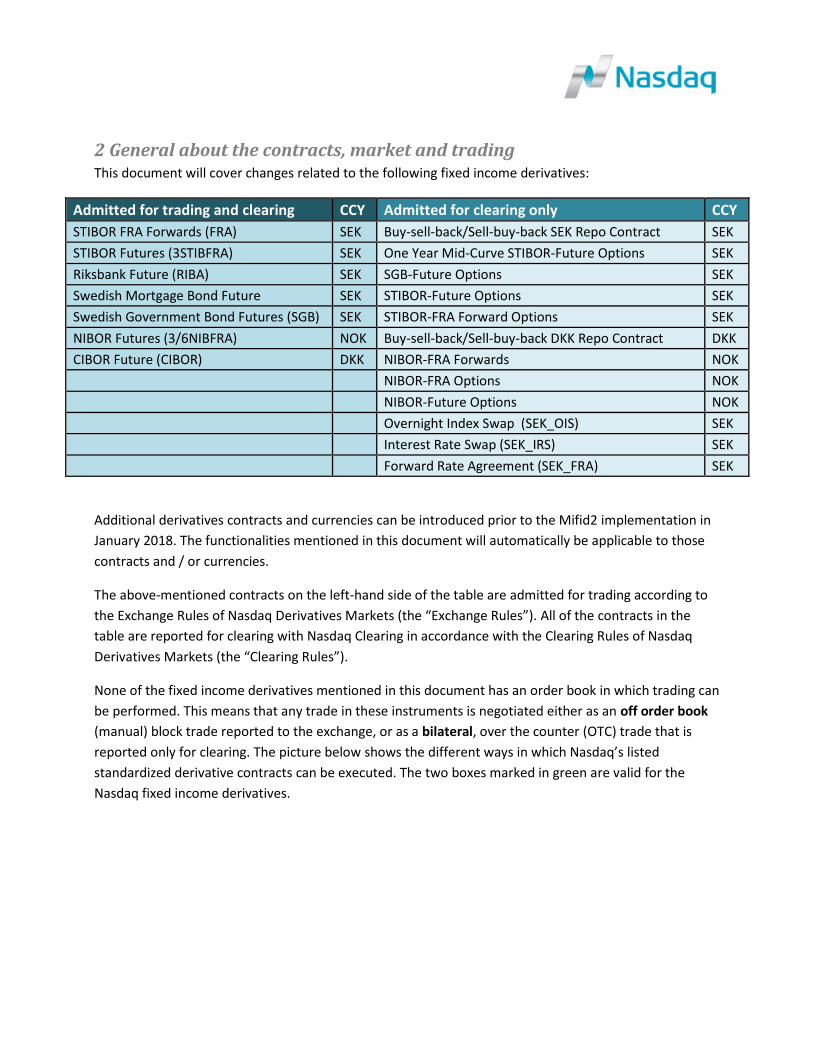

2 General about the contracts, market and trading This document will cover changes related to the following fixed income derivatives:

Admitted for trading and clearing CCY Admitted for clearing only CCY

STIBOR FRA Forwards (FRA) SEK Buy-sell-back/Sell-buy-back SEK Repo Contract SEK

STIBOR Futures (3STIBFRA) SEK One Year Mid-Curve STIBOR-Future Options SEK

Riksbank Future (RIBA) SEK SGB-Future Options SEK

Swedish Mortgage Bond Future SEK STIBOR-Future Options SEK

Swedish Government Bond Futures (SGB) SEK STIBOR-FRA Forward Options SEK

NIBOR Futures (3/6NIBFRA) NOK Buy-sell-back/Sell-buy-back DKK Repo Contract DKK

CIBOR Future (CIBOR) DKK NIBOR-FRA Forwards NOK

NIBOR-FRA Options NOK

NIBOR-Future Options NOK

Overnight Index Swap (SEK_OIS) SEK

Interest Rate Swap (SEK_IRS) SEK

Forward Rate Agreement (SEK_FRA) SEK

Additional derivatives contracts and currencies can be introduced prior to the Mifid2 implementation in

January 2018. The functionalities mentioned in this document will automatically be applicable to those

contracts and / or currencies.

The above-mentioned contracts on the left-hand side of the table are admitted for trading according to

the Exchange Rules of Nasdaq Derivatives Markets (the “Exchange Rules”). All of the contracts in the

table are reported for clearing with Nasdaq Clearing in accordance with the Clearing Rules of Nasdaq

Derivatives Markets (the “Clearing Rules”).

None of the fixed income derivatives mentioned in this document has an order book in which trading can

be performed. This means that any trade in these instruments is negotiated either as an off order book

(manual) block trade reported to the exchange, or as a bilateral, over the counter (OTC) trade that is

reported only for clearing. The picture below shows the different ways in which Nasdaq’s listed

standardized derivative contracts can be executed. The two boxes marked in green are valid for the

Nasdaq fixed income derivatives.

3 Bilaterally Traded contracts All fixed income derivatives mentioned in the table in Chapter 2 of this document can be traded bilaterally

(OTC) and in which case they will not be covered by the Nasdaq Derivatives Markets exchange rulebook.

As the bilaterally traded contracts are all eligible for clearing with Nasdaq Clearing, the following changes

will be applicable in the Genium INET clearing system and in the market.

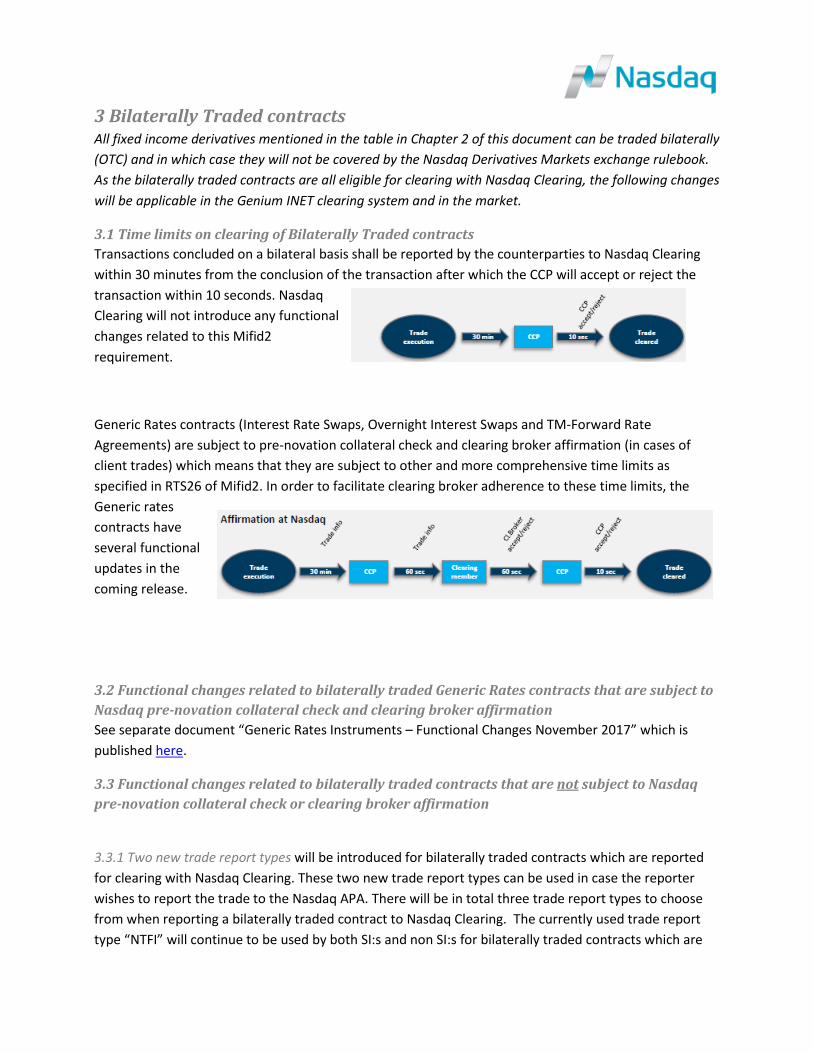

3.1 Time limits on clearing of Bilaterally Traded contracts

Transactions concluded on a bilateral basis shall be reported by the counterparties to Nasdaq Clearing

within 30 minutes from the conclusion of the transaction after which the CCP will accept or reject the

transaction within 10 seconds. Nasdaq

Clearing will not introduce any functional

changes related to this Mifid2

requirement.

Generic Rates contracts (Interest Rate Swaps, Overnight Interest Swaps and TM-Forward Rate

Agreements) are subject to pre-novation collateral check and clearing broker affirmation (in cases of

client trades) which means that they are subject to other and more comprehensive time limits as

specified in RTS26 of Mifid2. In order to facilitate clearing broker adherence to these time limits, the

Generic rates

contracts have

several functional

updates in the

coming release.

3.2 Functional changes related to bilaterally traded Generic Rates contracts that are subject to

Nasdaq pre-novation collateral check and clearing broker affirmation

See separate document “Generic Rates Instruments – Functional Changes November 2017” which is

published here.

3.3 Functional changes related to bilaterally traded contracts that are not subject to Nasdaq

pre-novation collateral check or clearing broker affirmation

3.3.1 Two new trade report types will be introduced for bilaterally traded contracts which are reported

for clearing with Nasdaq Clearing. These two new trade report types can be used in case the reporter

wishes to report the trade to the Nasdaq APA. There will be in total three trade report types to choose

from when reporting a bilaterally traded contract to Nasdaq Clearing. The currently used trade report

type “NTFI” will continue to be used by both SI:s and non SI:s for bilaterally traded contracts which are

reported for clearing only but it will be subject to some amendments described in detail in 3.3.1.2. The

two new trade report types can be used in case the reporter wishes to use the Nasdaq APA for

publication:

OTFI: To be used for OTC traded contracts which shall be cleared and then disclosed through the

Nasdaq APA.

SI: To be used for OTC traded contracts which shall be cleared and then disclosed through the

Nasdaq APA, where the reporting party is a Systematic Internaliser (trade report type is also valid

for equity derivatives).

Trade Report ID OTFI (new) SI (new)

Description OTC Disclosed, FI

Systematic Internaliser Disclosed, EQD & IRD

Asset Class IRD EQD & IRD

On/Off Exchange Off Off

OMnet API Trade report Code 113 155

FIX trade report Code 113 155

Exchange Statistics None None

o Implementation: The two new report types will be introduced on 3rd of January

2018.

3.3.1.2 Changes to currently used trade report Code NTFI: The code for the currently used trade report

type NTFI will be changed from 0 to 111. This change will affect all members who are reporting trades

through OMnet API or FIX.

Trade Report ID NTFI (current) NTFI (Updated 20th of Nov 2017)

NTFI (Updated 3rd of Jan 2018)

Description Normal Trade Report Normal Trade Report OTC Non Disclosed, FI

Asset Class IRD IRD IRD

On/Off Exchange Off Off Off

OMnet API Trade report Code 0 111 111

FIX trade report Code

0 111 111

Exchange Statistics Turnover Turnover Turnover

o Implementation: The trade report code will be changed from “0” to “111” on

November 20th 2017.

o Description will change on 3rd of January 2018

3.3.1.3 Trade report types for Package Transactions reported from CW1

If the reporting party is reporting their trade for clearing through CW1, the member can choose to tag

the trade with a “TPAC” flag by choosing other trade report types than the ones specified above. More

information in chapter 3.3.3.

It should be noted that these trade report types are identical with the trade report types specified above

(NTFI, OTFI and SI), with the exception of that they will add a TPAC flag to the trade.

Trade Report ID OTPF (Instead of OTFI)

SIPF (Instead of SI)

NTPF (instead of NTFI)

Description OTC Disclosed Package, FI

Systematic Internaliser Disclosed Package, FI

OTC Non Disclosed Package, FI

Asset Class IRD IRD IRD

On/Off Exchange Off Off Off

OMnet API Trade report Code 118 119 117

FIX trade report Code 118 119 117

Exchange Statistics None None None

o Implementation: The package trade report types will be introduced on 3rd of January

2018.

3.3.2 Time of agreement field: There will be a new field in which the reporting party can enter the time

when the trade was originally agreed upon. This field is not mandatory since the trade is cleared-only.

o Implementation: The new field will be available from November 20th 2017

3.3.3 Package Transactions

It will be possible to report package transactions for clearing only or publication to the Nasdaq APA by using a new multi leg trade report transaction. A multi-leg trade report transaction consists of at least two different series and may contain up to 10 component trades. It will be possible to report two entries for the same series, to be used when splitting one component into two prices.

A multi-leg trade report will be validated as a whole with regards to any pre- and post-trade

transparency thresholds and the resulting trade legs will be assigned the relevant package transaction

flag as well as a unique strategy ID linking the legs together.

It should be noted that the multi-leg trade report will be supported in OMnet, FIX protocols, Trading

Workstation and Nasdaq’s new user GUI Q-Port, but not in CW1.

Any member that is using the CW1 for trade reporting can although use CW1 to tag the trades with the

Package Transaction Flag (TPAC) by using any of the new trade report types for Package Transactions

Fixed Income Derivatives as specified in table in chapter 3.3.1.3. It should be noted that the trade report

types will only add the TPAC flag, it does not support the “Complex trade component id” which links the

trades together, and neither will any validations be done as a whole with regards to any pre- and post-

trade transparency thresholds. If such is needed, a multi-leg transaction is required.

o Implementation:

It will be technically possible to register multi-leg transactions in all systems

except from CW1 from November 20th 2017

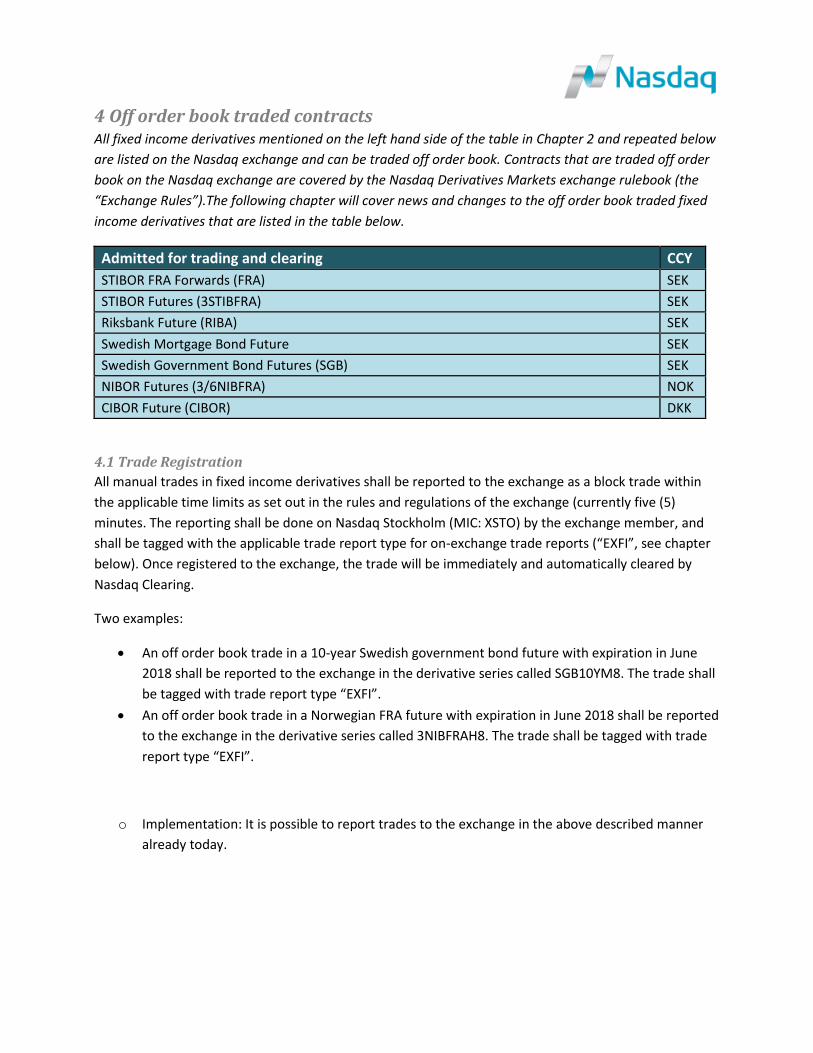

4 Off order book traded contracts All fixed income derivatives mentioned on the left hand side of the table in Chapter 2 and repeated below

are listed on the Nasdaq exchange and can be traded off order book. Contracts that are traded off order

book on the Nasdaq exchange are covered by the Nasdaq Derivatives Markets exchange rulebook (the

“Exchange Rules”).The following chapter will cover news and changes to the off order book traded fixed

income derivatives that are listed in the table below.

Admitted for trading and clearing CCY

STIBOR FRA Forwards (FRA) SEK

STIBOR Futures (3STIBFRA) SEK

Riksbank Future (RIBA) SEK

Swedish Mortgage Bond Future SEK

Swedish Government Bond Futures (SGB) SEK

NIBOR Futures (3/6NIBFRA) NOK

CIBOR Future (CIBOR) DKK

4.1 Trade Registration

All manual trades in fixed income derivatives shall be reported to the exchange as a block trade within

the applicable time limits as set out in the rules and regulations of the exchange (currently five (5)

minutes. The reporting shall be done on Nasdaq Stockholm (MIC: XSTO) by the exchange member, and

shall be tagged with the applicable trade report type for on-exchange trade reports (“EXFI”, see chapter

below). Once registered to the exchange, the trade will be immediately and automatically cleared by

Nasdaq Clearing.

Two examples:

An off order book trade in a 10-year Swedish government bond future with expiration in June

2018 shall be reported to the exchange in the derivative series called SGB10YM8. The trade shall

be tagged with trade report type “EXFI”.

An off order book trade in a Norwegian FRA future with expiration in June 2018 shall be reported

to the exchange in the derivative series called 3NIBFRAH8. The trade shall be tagged with trade

report type “EXFI”.

o Implementation: It is possible to report trades to the exchange in the above described manner

already today.

4.2 Trade report types

When reporting trades to the exchange via any trade registration facility, members are required to

identify block trades using the relevant trade report type and attributes as prescribed in the market

model document.

All trades in any fixed income derivative that have been traded according to the exchange rulebook shall

be tagged with the trade report type “EXFI” when reported to the exchange.

If the reporting party is reporting through CW1 and the trade has been negotiated as a package

transaction as defined by ESMA and Mifid II, the member can choose to tag the trade with “EXPF”

instead of “EXFI” which adds a “TPAC” flag to the trade. More information in chapter 4.5

The FIX trade report code on the current trade report type “EXFI” will be changed from 2106 to 110. This

change will affect all members who are reporting trades through FIX. More details are found in the table

below.

Trade Report ID EXFI (current) EXFI (Updated) EXPF

Description On Exchange Trade Report On Exchange Block, Fixed Income

On Exchange Block Package, FI

Asset Class IRD IRD IRD

On/Off Exchange On On On

OMnet API Trade report Code 110 110 116

FIX trade report Code 2106 110 116

Exchange Statistics Price, Qty, Turnover Price, Qty, Turnover Price, Qty, turnover

o Implementation:

o The exchange trade report type “EXFI” is available in the production system already

today.

o The FIX trade report code for “EXFI” will be changed from “2106” to “110” on November

20th 2017.

o The exchange trade report type “EXPF” for package transactions will be made available

in the production system on January 3rd 2018.

4.3 Minimum Block Trade Size

The fixed income derivatives products are expected to qualify for the illiquid waiver in which case the

minimum block trade size will be 1 contract. In case any contract is deemed to be liquid, the minimum

number of contracts in respect of each derivatives sub-class that can be negotiated outside the order

book as a block trade will be determined by the exchange from time to time based on the regulatory LIS

pre-trade threshold value.

Applicable block sizes will be appended to the fixed income derivatives market model document and

available in the exchange’s reference data. Illiquid products will be flagged in the reference data

accordingly.

Block trades in packages (strategies) can be reported using the new multi-leg trade report messages.

Such trade report will be accepted if at least one leg satisfies the minimum volume condition. See further

details on package transactions in the section below.

Indicative block sizes will be configured in the member test environment to facilitate implementation

and testing. Final levels will be communicated in an exchange notice closer to go-live and appended to

the market model document.

o Implementation: Configuration of block trade size limits will be done on January 3rd

2018

4.4 Deferred Trade-Publication

As the fixed income derivatives products are expected to qualify for the illiquid waiver, it is also expected

that the any trades above the minimum block trade size (1) will be eligible for deferral.

In case of liquid products, the minimum number of contracts in respect of each derivative sub-class

required to qualify a trade for deferred publication will be determined by the exchange from time to

time based on the relevant regulatory post-trade threshold value. To prevent manual errors, trades

requested to be deferred but not satisfying the deferral threshold volume will immediately published.

The deferral period (whichever gets approval from the FSA) will be applied per instrument. Applicable

deferral threshold volumes as well as applicable deferral period will be appended to the market model

document and available in the exchange’s reference data.

Block trades in packages (strategies) can be reported using the new multi-leg trade report messages. It

will be possible to defer the publication of all component trades if at least one leg satisfies the deferral

threshold volume. See further details on package transactions in the section below.

o Implementation: The configuration of deferral threshold and deferral period per

instrument will be applied on January 3rd 2018

4.5 Package Transactions

To support the new package transaction regime and comply with trade flagging requirements, the Exchange will require members to report any such transactions negotiated off order book by using a new multi leg trade report transaction. A multi-leg trade report transaction consists of at least two different series and may contain up to 10 component trades. It will be possible to report two entries for the same series, to be used when splitting one component into two prices. A multi-leg trade report will be validated as a whole with regards to any pre- and post-trade

transparency thresholds and the resulting trade legs will be assigned the relevant package transaction

flag as well as a unique strategy ID linking the legs together.

It should be noted that the multi-leg trade report will be supported in OMnet, FIX protocols, Trading

Workstation and Nasdaq’s new user GUI Q-Port, but not in CW1.

Any member that is using the CW1 for trade reporting can although use CW1 to tag the trades with the

mandatory Package Transaction Flag (TPAC) by using the new trade report type for Package Transactions

Fixed Income Derivatives as specified in table in chapter 4.2. It should be noted that the trade report

types will only add the TPAC flag, it does not support the “Complex trade component id” which links the

trades together, and neither will any validations be done as a whole with regards to any pre- and post-

trade transparency thresholds. If such is needed, a multi-leg transaction is required.

o Implementation: It will be technically possible to register multi-leg transactions in all systems

except from CW1 from November 20th 2017

4.6 Time of agreement field

It will become mandatory to submit the time of agreement. The time stamp will be required to match with date granularity on both sides.

o Implementation:

The time of agreement field will be technically available in the system from

November 20th 2017

The time-stamp verification will start from January 3rd 2018

4.7 Trader ID validation

The Exchange will assign each registered Exchange Trader with a personal trader ID, and the Trader ID

must be submitted to the exchange in all trade reports that are registered.

o Implementation:

The Trader ID field will be technically available in the system from November

20th 2017

The verification of Trader ID will start on January 3rd 2018

5 Market Model - Nasdaq Fixed Income Derivatives The picture below outlines the different ways in which the fixed income derivatives contracts that are

mentioned in this document can be traded and processed. More detailed information regarding products

can be found in the respective market model documents that will be published by the exchange.

6 Glossary of Terms

Term Definition

IRD Interest Rate Derivatives

CW1 Clearing Workstation 1, one of the clearing user interfaces that is currently offered by Nasdaq.