first time buyer seminar workbook

TRANSCRIPT

For the past 15 years, Cindee Stone has been helping people achieve their goals of homeownership. Her motto is 'FINANCING HAS NEVER BEEN SO EASY' and with her years of on hand experience, she helps make this a reality.

Cindee Co-founded People Want Info because she thought it was so important to educate home buyers, about the loan process and what is involved. Whether a first-time homebuyer or just needing a brush up, by getting this education, the borrower will feel more comfortable with the whole process from start to finish.

Cindee's positive attitude and focus on each individual client are the keys to achieving a positive experience with the loan process. She feels 'Success is built one client at a time.'

Cindee Stone is experienced and knowledgeable in all mortgage-lending products. Always keeping the clients best interest in mind and getting the job done quickly has made Cindee Stone a major performer in the mortgage industry in and outside of Utah.

So . . . whether you are looking to purchase or refinance, think of Cindee Stone as your home loan specialist.

ii

PEOPLE WANT INFO SEMINAR SERIES: Building Wealth Through Homeownership & Education......................................1

TOPICS OF DISCUSSION...........................................................................................3

IS HOME OWNERSHIP FOR YOU? BUY VS. RENT.................................................5Buying VS Renting...................................................................................................6Economic Stimulus...................................................................................................7

THE IMPORTANCE OF PRE-APPROVAL...................................................................9Before We Begin....................................................................................................10Loan Programs.......................................................................................................12Credit Overview......................................................................................................13Credit Restoration..................................................................................................14The Ten Commandments......................................................................................15Additional Information Page...………………………………………………………….16

WHY HIRE A REALTOR?..........................................................................................18

iii

Why You Need a Realtor.......................................................................................19

QUALIFYING FACTORS – FOUR “C’s”.....................................................................22

QUESTION AND ANSWER........................................................................................24Extra Articles and information................................................................................25Full Economic Stimulus Article...............................................................................26Full Buy VS Renting Article....................................................................................29Spending Plan........................................................................................................30Full Credit Overview...............................................................................................31Loan Application Checklist.....................................................................................32Application.............................................................................................................34Understanding Loan Costs.....................................................................................38New Good Faith Estimate......................................................................................41Truth in Lending.....................................................................................................46Should I Pay Points................................................................................................47Understanding Agency...........................................................................................48The Main Players...................................................................................................49Glossary.................................................................................................................50

iv

1

2

3

4

5

1) Security!! a. Quality of Life as a homeowner.

2) Build Wealth through Equity Growth: a. Appreciation potential. Why give this to

someone else? Especially now, when we are in a buyers market.

3) Fixed Payment :a. Your payment doesn’t increase when you have a 30-YR

mortgage payment. You don’t have to worry about the rent increasing again. You can count on a certain payment every month.

4) Tax Deductions of Mortgage Interest: 5) Privacy:6) Your Landlord Loves you!

a. The Real Cost of Renting (At $700 per month, with a 6% rental increase per year, you will pay $110,719 over a 10 year period.)

7) Increased Payments: Did you know that if you paid 1 extra principle and interest payment a year, you can shave up to 7 years off of your mortgage? Can you do that with rent?

8) Zero Equity Growth! Once again, when you rent you are building your landlords equity, not yours. You are throwing your money away.

6

Who Gets What?First-Time Homebuyers (FTHBs): First-time homebuyers (that is, people who have not owned a home within the last three years) may be eligible for the tax credit. The credit for FTHBs is 10% of the purchase price of the home, with a maximum available credit of $8,000

Single taxpayers and married couples filing a joint return may qualify for the full tax credit amount.

Current Owners: The tax credit program now gives those who already own a residence some additional reasons to move to a new home. This incentive comes in the form of a tax credit of up to $6,500 for qualified purchasers who have owned and occupied a primary residence for a period of five consecutive years during the last eight years.

Single taxpayers and married couples filing a joint return may qualify for the full tax credit amount.

What are the New Deadlines?In order to qualify for the credit, all contracts need to be in effect no later than April 30, 2010 and close no later than June 30, 2010.

Can Homebuyers Claim the Tax Credit in Advance of Purchasing a Property?No. The IRS has recently begun prosecuting people who have claimed credits where a purchase had not taken place.

Are There Other Restrictions to Taking the FTHB Credit?Yes. According to the IRS, if any of the following describe a homebuyer’s situation, a credit would not be due:

They buy the home from a close relative. This includes a spouse, parent, grandparent, child or grandchild. (Please see the question below for details regarding purchases from “step-relatives.”)

They do not use the home as your principal residence. They sell their home before the end of the year. They are a nonresident alien. They are, or were, eligible to claim the District of Columbia first-time homebuyer credit for any taxable year.

(This does not apply for a home purchased in 2009.) Their home financing comes from tax-exempt mortgage revenue bonds. (This does not apply for a home

purchased in 2009.) They owned a principal residence at any time during the three years prior to the date of purchase of your new

home. For example, if you bought a home on July 1, 2008, you cannot take the credit for that home if you owned, or had an ownership interest in, another principal residence at any time from July 2, 2005, through July 1, 2008.

What are the Income Caps?The amount of income someone can earn and qualify for the full amount of the credit has been increased. Single tax filers who earn up to $125,000 are eligible for the total credit amount. Those who earn more than this cap can receive a partial credit. However, single filers who earn $145,000 and above are ineligible

Joint filers who earn up to $225,000 are eligible for the total credit amount. Those who earn more than this cap can receive a partial credit. However, joint filers who earn $245,000 and above are ineligible.

7

8

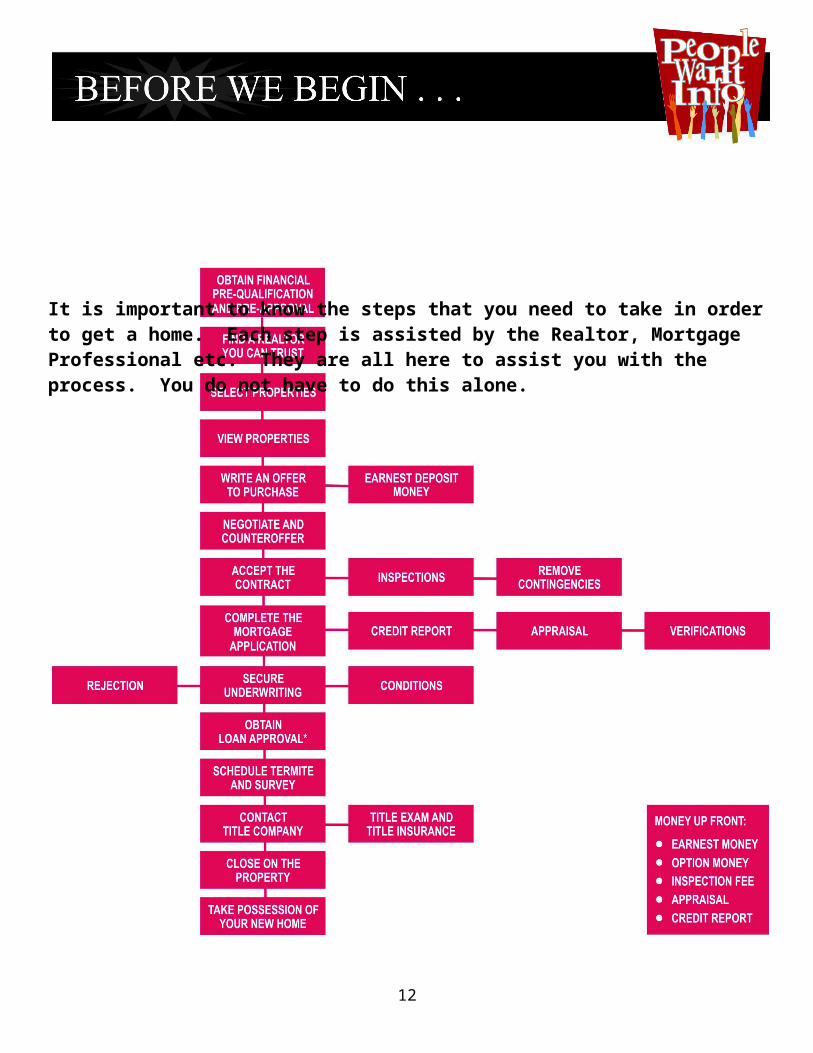

It is important to know the steps that you need to take in order to get a home. Each step is assisted by the Realtor, Mortgage Professional etc. They are all here to assist you with the process. You do not have to do this alone.

9

Why would you think it was important to get pre-qualified or pre-approved?

1) Realistic pursuit of properties : By not doing this first, you will not really know what you can afford. It can be very discouraging if you fall in love with a home that you cannot afford. By being pre-qualified or pre-approved, you can help eliminate this problem.

2) Strengthens buyer power :

a. In today’s market, sellers usually will not entertain an offer if it doesn’t have a Pre-qualification or pre-approval letter attached. This tells the seller that you have met with a mortgage professional and you are able to get a loan to buy the home you are pursuing.

b. A seller may choose to make concessions if they know that your financing is secured. You are like a cash buyer and this may make your offer more competitive

c. Foreclosures and short sales will not look at offers without you meeting with a mortgage professional and having the letter.

d. You can select the best loan package without being under pressure.

Understanding the difference between what you “Qualify” for VS. what you can really afford.

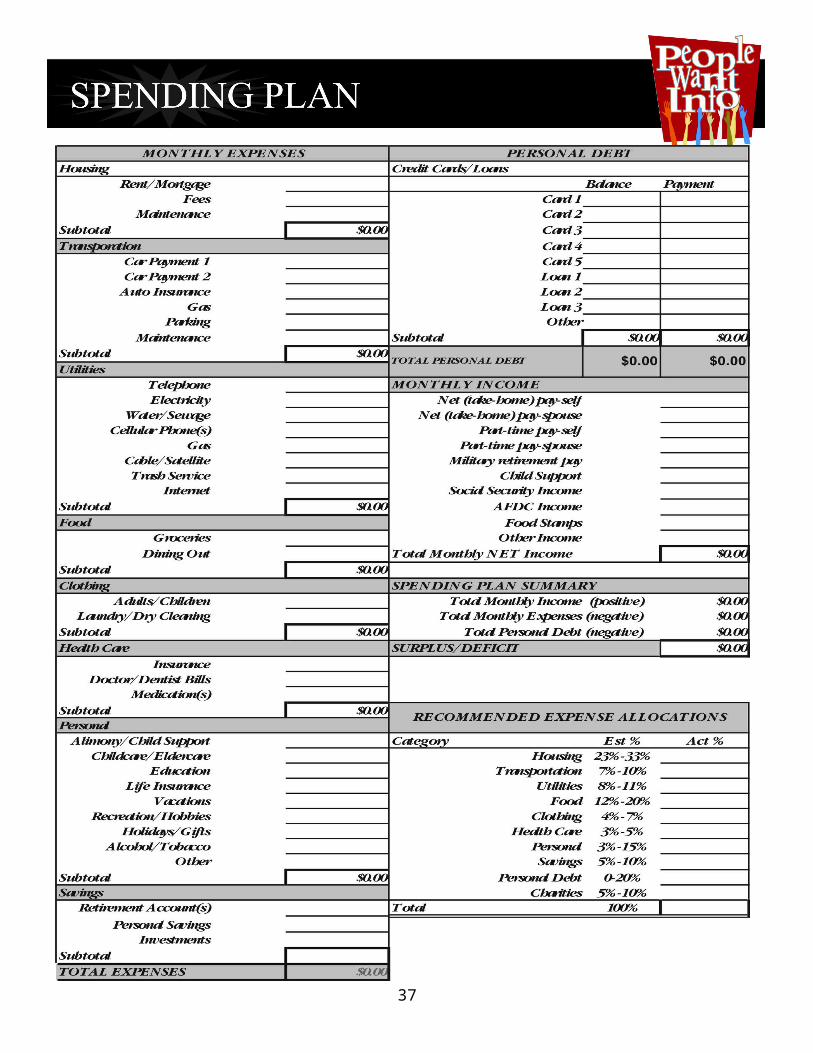

1) Just because you can “qualify” for something on paper, doesn’t mean that it is what you can really afford. Don’t forget that you will have other bills associated with your new home that you didn’t before. Go to page 30 in the back and fill out a “spending plan” sheet.

You can also find it on my website. www.cindeestone.com Take a few minutes and put down all of your expenses to figure out what is best for you.

This packet is designed to assist you with the purchase of your new home. Rest assured that it is my goal to provide you with the most professional service available. I am always just a phone call away!

10

MOST COMMONLY USED LOAN PROGRAMS:

1) FHA 96.5% LTVa. 3.5% down

i. This can come from checking/savings, gift from relative, loan from relative or a grant (see below)

b. 620 minimum scorec. Full Documentation

2) Rural Housing 100% LTVa. Must have a minimum 620 scoreb. It is income sensitivec. Common Areas in Utah are: Eagle Mountain, Saratoga Springs and Tooele. d. Cannot own another propertye. Do NOT have to be a first time homebuyerf. Full Documentation

3) Utah Housing (up to 103%)a. Must be a first time homebuyerb. Must have credit scores of 660 or betterc. Income sensitived. Full Documentation

4) Conventional 95 – 90%a. 5% - 10% down Minimumb. 620 or better credit scoresc. Do NOT have to be a first time home buyerd. Full Documentation

5) VA 100%a. 0% downb. Must be a Veteranc. Full Documentation

6) Grant Moneya. First time homebuyers onlyb. Income sensitivec. Couples with a FHA loan

11

WHY IS IT IMPORTANT?Generally lenders look at several things: your income, your down payment or equity, your credit history, how much money you’ve saved, and the property you plan to purchase or refinance. When studying your credit history, almost all lenders look at your credit score and your debt-to-income ratio. Lenders use credit scores, known as FICO scores, as an important factor in the decision whether or not to offer credit. The scores can range from 375 to 900 points. You’re likely considered to be a better credit risk if your FICO score is high.

CREDIT REPORTSA consumer credit report is a document that contains a record of an individual’s credit payment history. The report contains four types of information: Identifying information, credit information, Public record information, and inquiries.

Identifying information includes your: Name Current and previous addresses Social security number Year of birth Current and pervious employment If your married, your spouse’s name

Credit information Includes credit accounts or loans you have with: Banks Retailers Credit card issuers Other lenders

The information contained on your credit report remains for seven years from the date its first reported, and then cycles off automatically.

Whether you have credit problems or not, it’s a good idea to review your credit report for accuracy and completeness before you apply for a loan. If there is inaccurate information in your credit report, you have the right to dispute it and have it removed.

TIP: Beginning December 1, 2004, consumers are allowed to order one free copy of their credit report. To order a copy of your credit report, contact

Equifax @ www.equifax.com or call 1-800-685-1111 Experian @ www.experian.com or call 1-888-397-3742 Transunion@ www.transunion.com or call 1-800-916-8800

If you’ve been denied credit because of information on your credit report, the lender is required to provide you with the credit bureau’s name, address, and telephone number- and you’re entitled to a free copy of your report from that credit bureau. The credit reporting industry is regulated by the federal Fair Credit Reporting Act, which is administered by the Federal Trade Commission.For more information about your credit rights as a consumer visit, www.ftc.gov.

12

Having good credit is a necessity these days and if you do not have good credit it can have a major affect on your life in a negative way. That’s why Nitro Credit is here to help.

From late payments to charge offs to bankruptcies, we've challenged and deleted items in the past and average a 46.77% deletion/fix rate in just the first round due to the proven methods we use to help clients every day.

HOW MUCH DOES BAD CREDIT COST?The chart below shows how much someone with a lower credit score would pay over the term of a 30-year conventional mortgage loan for $200,000. (05/2009)

Nitro Credit not only focuses on Credit Repair, but also Credit Education and Management. We focus on our client’s credit picture as a whole. We work to get misleading, unverifiable and inaccurate items removed and missing –valid- information updated. We teach you how to maintain and manage your credit and also how to build/establish new credit without damaging your credit file. Nitro Credit also works with your creditors on negotiating debts and/or settlements. During our process you can log in to our website and monitor your account as well.

Don’t settle for less than perfect credit.Contact our office for a free consultation.

Credit Score Interest Rate Cost of your credit

720-850 4.75% $0.00

700-719 5.125% $16,668.00

640-699 5.675% $41,392.80

600-639 6.50% $79,506.00

13

888.75.NITRO (64876)visit www.nitrocredit.com Or email: [email protected]

8941 S 700 E #103, Sandy UT 84070

14

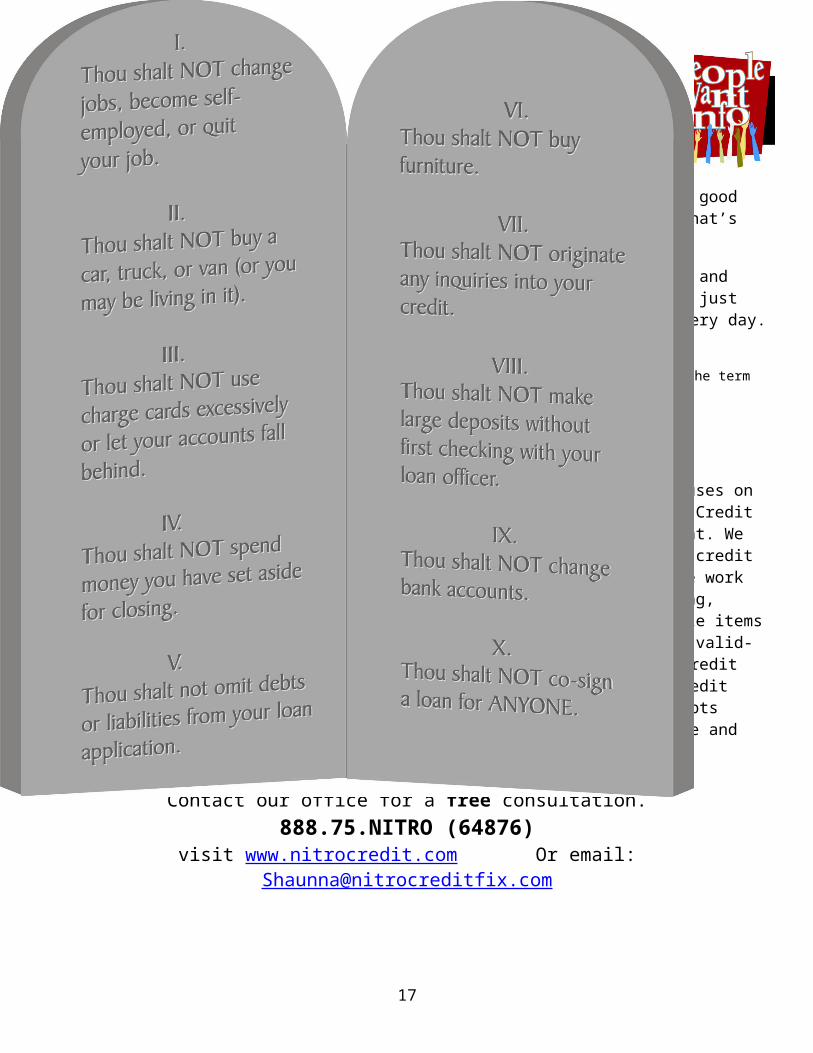

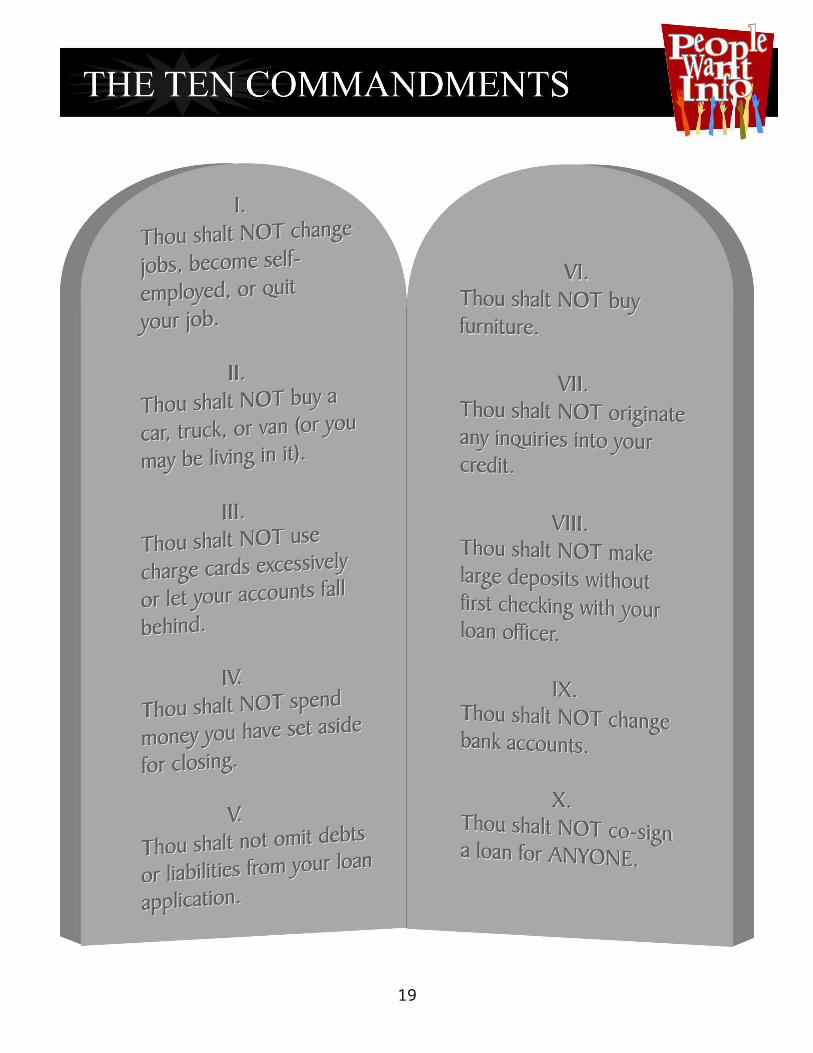

15

Additional information and full articles can be found at the back of the book regarding these topics and more:

Page 31

Page 32

Page 34

Page 38

Page 41

Page 46

16

17

1)Your Time is Valuable!

a. THEY ARE EXPERTS IN UNDERSTANDING OF LAWS AND BUYERS RIGHTS!

i. Real estate agents have to do continuing education all year to keep up with the many changes that are constantly happening. You need to have the right representation to make the transaction go smoothly.

b. NEGOTIATIONS:i. A Realtorâ is experienced at presenting your offer to the homeowner and

can help you through the process of negotiating the best price. He or she brings objectivity to the buying transaction and can point out the advantages and the disadvantages of a particular property.

ii. If you don’t have an agent working on your behalf, you can lose out on benefits of maybe having the seller pay closing costs. If there are issues with the property, they negotiate with the seller to have these items fixed. You need a professional that does this full time and has your needs first.

iii. Bank owned properties will not take an offer from a buyer without representation.

iv. They are the navigators with making the transaction flow smoothly. They work hand in hand with all of the professionals that are associated with the transaction.

1. Borrower (that’s you)2. Selling agent (this is the role they take on with representing you as

the buyer). The listing and selling agent may be the same person or company.

3. Listing agent (represents the seller)4. Mortgage professional5. Title Company6. Appraiser7. Inspector

18

c. EXPERT IN LOCAL REAL ESTATE MARKET

i. A Realtorâ knows the housing market inside and out and can help you avoid the “wild goose chase.”

ii. A Realtorâ can help you with any home, even if it is listed elsewhere or if it is being sold directly by the owner.

d. SELLERS PAY THE REALTORS, NOT YOU!i. Isn’t this wonderful! The agent does all of this for you and you don’t have to

pay them. They get paid when the transaction closes from the seller. Don’t be fooled into thinking if you buy a “for sale by owner” that you will save yourself that commission. Without the proper negotiator chances are high you will pay too much for the house and not really have any savings.

Licensed real estate professionals provide much more than the service of helping you find your ideal home. Realtors® are expert negotiators with other agents, seasoned financial advisors with clients, and superb navigators around the local neighborhood. They are members of the National Association of Realtors (NAR) and must abide by a Code of Ethics and Standards of Practice enforced by the NAR. A professional Realtor® is your best resource when buying your home.

19

20

make an educated decision.

TRANSACTION BROKER (Dual Agency) Agent represents both the buyer and the seller

equally. Agent’s objective is to get a mutually satisfactory

agreement among all parties. Agent gives all options to the buyer and the seller. Depending on the local market, all parties may be

present at contract presentation to negotiate on their own behalf.

All parties have confidentiality – agent may do nothing to the detriment of either the buyer or the seller.

Both the buyer and the seller have a right to counsel. Before making any decisions, both parties have the right to seek family, religious, legal, or financial counsel.

IN ALL RELATIONSHIPS, AS YOUR AGENT I HAVE A DUTY TO ACT HONESTLY WITH BOTH THE BUYER AND THE SELLER.

21

22

23

Extra Articles and Additional Information

24

TAX CREDIT OVERVIEW

Who Gets What?First-Time Homebuyers (FTHBs): First-time homebuyers (that is, people who have not owned a home within the last three years) may be eligible for the tax credit. The credit for FTHBs is 10% of the purchase price of the home, with a maximum available credit of $8,000

Single taxpayers and married couples filing a joint return may qualify for the full tax credit amount.

Current Owners: The tax credit program now gives those who already own a residence some additional reasons to move to a new home. This incentive comes in the form of a tax credit of up to $6,500 for qualified purchasers who have owned and occupied a primary residence for a period of five consecutive years during the last eight years.

Single taxpayers and married couples filing a joint return may qualify for the full tax credit amount.

What are the New Deadlines?In order to qualify for the credit, all contracts need to be in effect no later than April 30, 2010 and close no later than June 30, 2010.

What are the Income Caps?The amount of income someone can earn and qualify for the full amount of the credit has been increased.

Single tax filers who earn up to $125,000 are eligible for the total credit amount. Those who earn more than this cap can receive a partial credit. However, single filers who earn $145,000 and above are ineligible

Joint filers who earn up to $225,000 are eligible for the total credit amount. Those who earn more than this cap can receive a partial credit. However, joint filers who earn $245,000 and above are ineligible.

What is the Maximum Purchase Price?Qualifying buyers may purchase a property with a maximum sale price of $800,000. What is a Tax Credit?A tax credit is a direct reduction in tax liability owed by an individual to the Internal Revenue Service (IRS). In the event no taxes are owed, the IRS will issue a check for the amount of the tax credit an individual is owed. Unlike the tax credit that existed in 2008, this credit does not require repayment unless the home, at any time in the first 36 months of ownership, is no longer an individual’s primary residence.

25

How Much are First-Time Homebuyers (FTHB) Eligible to Receive?An eligible homebuyer may request from the IRS a tax credit of up to $8,000 or 10% of the purchase price for a home. If the amount of the home purchased is $75,000, the maximum amount the credit can be is $7,500. If the amount of the home purchased is $100,000, the amount of the credit may not exceed $8,000.

Who is Eligible fort FTHB Tax Credit?Anyone who has not owned a primary residence in the previous 36 months, prior to closing and the transfer of title, is eligible.

This applies both to single taxpayers and married couples. In the case where there is a married couple, if either spouse has owned a primary residence in the last 36 months, neither would qualify. In the case where an individual has owned property that has not been a primary residence, such as a second home or investment property, that individual would be eligible.

As mentioned above, the tax credit has been expanded so that existing homeowners who have owned and occupied a primary residence for a period of five consecutive years during the last eight years are now eligible for a tax credit of up to $6,500.

How Much are Current Home Owners Eligible to Receive?The tax credit program includes a tax credit of up to $6,500 for qualified purchasers who have owned and occupied a primary residence for a period of five consecutive years during the last eight years.

Can Homebuyers Claim the Tax Credit in Advance of Purchasing a Property?No. The IRS has recently begun prosecuting people who have claimed credits where a purchase had not taken place.

Can a Taxpayer Claim a Credit if the Property is Purchased from a Seller with Seller Financing and the Seller Retains Title to the Property?Yes. In situations where the buyer purchases the property, even though the seller retains legal title, the taxpayer may file for the credit. Some examples of this would include a land contract or a contract for deed.

According to the IRS, factors that would demonstrate the ownership of the property would include:

1. Right of possession, 2. Right to obtain legal title upon full payment of the purchase price, 3. Right to construct improvements, 4. Obligation to pay property taxes, 5. Risk of loss, 6. Responsibility to insure the property, and 7. Duty to maintain the property.

Are There Other Restrictions to Taking the FTHB Credit?Yes. According to the IRS, if any of the following describe a homebuyer’s situation, a credit would not be due:

26

They buy the home from a close relative. This includes a spouse, parent, grandparent, child or grandchild. (Please see the question below for details regarding purchases from “step-relatives.”)

They do not use the home as your principal residence. They sell their home before the end of the year. They are a nonresident alien. They are, or were, eligible to claim the District of Columbia first-time homebuyer credit for any taxable year.

(This does not apply for a home purchased in 2009.) Their home financing comes from tax-exempt mortgage revenue bonds. (This does not apply for a home

purchased in 2009.) They owned a principal residence at any time during the three years prior to the date of purchase of your new

home. For example, if you bought a home on July 1, 2008, you cannot take the credit for that home if you owned, or had an ownership interest in, another principal residence at any time from July 2, 2005, through July 1, 2008.

Can Homebuyers Purchase a Home from a Step-Relative and Still be Eligible for the Credit?Yes. As long as the person they buy the home from is not a direct blood relative, the purchase would be allowed.

If a Parent (Who Will Not Live In The Property) Cosigns for a Mortgage, Will Their Child Still be Eligible for the Credit? Yes, provided that the child meets the other requirements for the tax credit.

27

Nearly a full third of households are still renting. If you’re one of them, you could be paying a hefty price.

Before talking about purchasing a house, it’s important to note two things. First—and this is extremely important—the housing market is actually localized. So the outlook in your hometown may be different than another city across the state or on the other side of the country. Second, home prices are tied to employment. For example, if someone feels like their job is in jeopardy, it might be enough to stop them from making a move. So, if your local job market is feeling a pinch, the home prices in your area may be down as well.

But with all those factors under consideration, it still makes sense to buy instead of rent. In fact, renting may be costing you a bundle.

Let's look at an example…

If you are paying rent at $1,500 per month and your landlord increases your payment by a modest 5% each year, you would wind up paying just about $100,000 over a 5-year period! Worse yet, after forking over $100,000, you still would have nothing to show for it.

And speaking of having nothing to show for it, how about any improvements you might make to a rental property? It's not uncommon for renters to freshen up the paint, install new light fixtures or plant some nice flowers outside. But guess what… all your efforts, labor and the benefit of that improvement belong to the landlord, not to you.

With convenient down payment options still available for qualified buyers, affordable home prices and low interest rates, the very same money could have been used towards home ownership.

Even using a standard 30-year fixed program, a mortgage of $300,000 could be obtained with a total monthly mortgage payment—including property taxes and insurance—of around $2,200. Assuming a 25% tax bracket, this would be equivalent to the average amount spent on rent during the same period after your tax benefit.

And the benefits of home ownership are quite considerable. Because the mortgage is being paid down each month, equity is being built. After 5-years, the $300,000 mortgage could be reduced to $279,000, adding $21,000 to your net worth!

But if laying out the initial increase in monthly payment and having to wait for your tax benefit to show up next April is a tough nut to crack, the IRS wants to help. Instead of waiting to file for the tax benefits derived from your new home purchase, you can simply adjust the amount of your withholding. This allows you to have less tax withheld from each paycheck so you can handle the new mortgage payment more comfortably throughout the year. In essence, you are taking your tax refund as you go instead of letting Uncle Sam hold it all year, interest free.

Visit www.irs.gov and use the IRS withholding calculator. This very handy tool can quickly show you the impact that a change in withholding will do to your net paycheck. Remember to balance this with the expected refund and it is always a good idea to check with your tax advisor.

Don't fall victim to the national headline hype. Talk to a professional who understands your local market. And remember, buying a home is a big step, but it is almost always one in the right direction.

28

29

The concept of credit--the reputation for paying your bills on time- makes it possible for you to acquire merchandise or money with the understanding that you will repay later. Your history for paying your bills on time is collected by a credit bureau or credit-reporting agency. These businesses gather, maintain, and sell information about consumers’ credit histories. They collect information about your payment habits from banks, credit unions, finance companies, or retailers.

WHY IS IT IMPORTANT?Generally lenders look at several things: your income, your down payment or equity, your credit history, how much money you’ve saved, and the property you plan to purchase or refinance. When studying your credit history, almost all lenders look at your credit score and your debt-to-income ratio. Lenders use credit scores, known as FICO scores, as an important factor in the decision whether or not to offer credit. The scores can range from 375 to 900 points. You’re likely considered to be a better credit risk if your FICO score is high.

CREDIT PROBLEMS?If you have a lower credit score, don’t assume that your choices are limited to high-cost lenders. If your credit report contains negative information that is accurate but stemming from unique circumstances such as illness or temporary loss of income, be sure to explain your situation to the lender or broker. Don’t assume that the only way to get credit is to pay a high price. Take the time to shop around and negotiate the best deal for you. It may be that your past credit record is not as good as you might wish. If you’re currently having credit problems, may not be in a position to buy a house until they are resolved.

The following conditions will play a factor in your mortgage lender’s decision to provide you with a loan:

Bankruptcy: In most cases, lenders prefer that you wait at least two years after a bankruptcy is resolved before taking on another large debt such as a home loan. Bankruptcies can remain on your credit report for up to 10 years. It may be helpful for you to explain the circumstances to the lender under which you declared bankruptcy.

Foreclosure: Having a foreclosure on your records doesn’t mean that you can never buy another house. The mortgage lender will, however, want to know the reasons for your foreclosure. Most lenders will expect you to wait three years after a foreclosure before you apply for a new mortgage. Debts: Having too much debt may lower the chances for you to buy a home or refinance a mortgage. Making late payments or skipping payments will show as derogatory or negative items on your credit report. Taking steps to improve your credit record is one of the most important things you can do.

30

GENERAL Picture ID with Social Security Number. Payment to cover application fee. Name and complete address of all landlords (past 2 years).

INCOME Employment history, including names, addresses, phone numbers, and length of

time with that company (past two [2] years). Copies of your most recent pay stubs or one full month W-2 form (past two [2] years). Tax returns (past two [2] years) Verification of other income (social security, child support, retirement). If you are self employed: Copies of signed tax returns including all schedules

(past two [2] years), and a signed profit and loss statement of the current year. If you are retired: Tax returns (past two [2] years). If you have rental property income: Copies of all lease agreements.

ASSETS Copies of all bank statements from checking/savings accounts (past three [3]

months). Copies of all stock/bond certificates and/or past statements/retirement accounts. A list of household items and their values. Copies of title documents for all automobiles, boats, or motorcycles. Face amount, monthly premiums, and cash values of all life insurance policies.

(Cash value may be used for closing costs or down payments. You need documentation from the carrier indicating cash value.)

31

CREDITORS Credit cards (account numbers, current balances, and monthly payments). Installment loans (car, student, etc.). Same details as for credit cards. Mortgage loans (property address, lender with address, account numbers, monthly

payment, and balance owed on all properties presently owned or sold within the last two [2] years). Bring proof of sale of properties sold.

Childcare expenses and/or child support (name, address, phone number).

OTHER Bankruptcy—bring discharge and schedule of creditors. Adverse credit—bring letters of explanation. Divorce—bring your Divorce decree(s), property settlements, quitclaim deeds,

modifications, etc. VA only—bring Form DD214 and Certificate of Eligibility. Retirees—bring retirement and/or Social Security Award Letter.

32

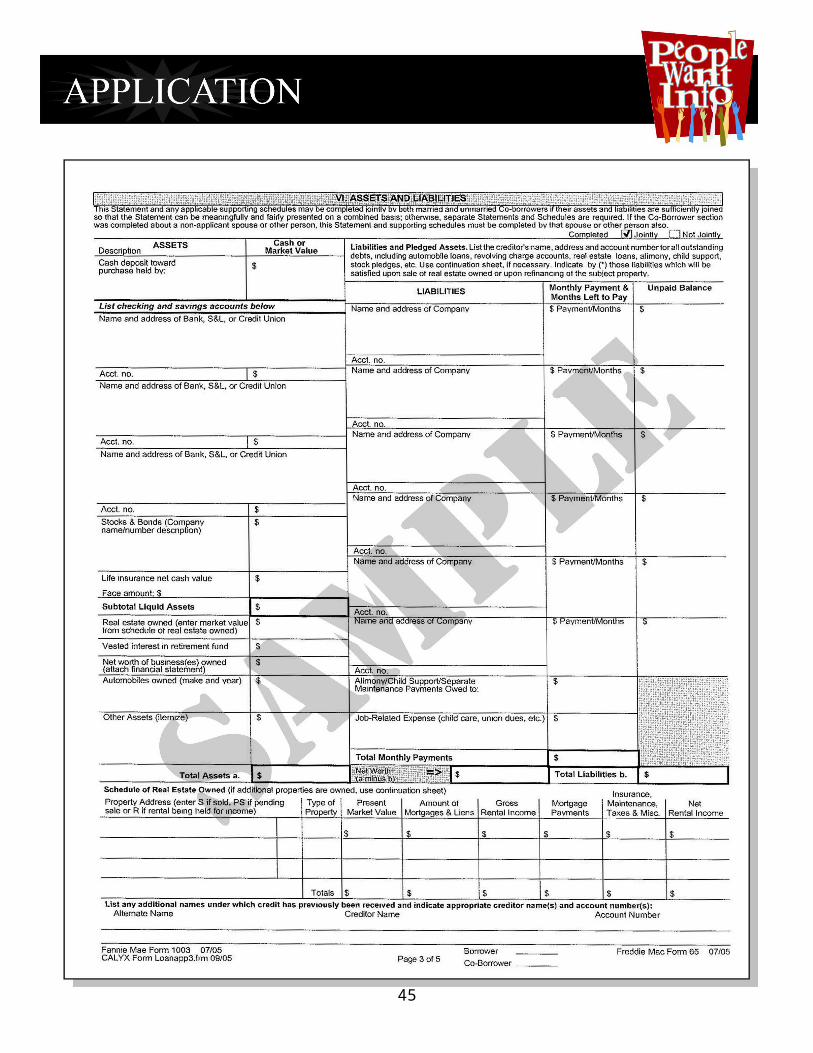

33

34

35

36

Down payments, rates, points, and fees can make a loan that looks good at first glance into something else once all the facts are known. Knowing the amount of the monthly payment or the interest rate is not enough. Be sure to get information about potential mortgages from a lender you trust and find out all of the costs involved with a loan. When Comparing loans, make sure you’re reviewing the same information in each loan such as (loan amount, loan term, type of loan, monthly payment, penalties, features, and annual percentage rate {APR}). All of these attributes can be compared with a Truth in Lending Statement for one option vs. another.

Ask about the loans annual percentage rate (APR). The APR takes into account not only the interest rate but also points, broker fees, and certain other credit charges that you may be required to pay, expressed as a yearly rate. This will specifically tell you the cost of what you’re borrowing and will allow you to compare the costs of one loan to another.

TIP: Note everything in writing. A daily journal of all conversations can be a powerful tool in resolving conflicts later.

Never take the loan officer’s verbal promise on any detail or feature of the loan that matters. You have a right to receive commitments in writing and a professional should never hesitate to provide this. If your loan officer is unwilling to put his or her promises in writing, you should not rely on those promises.

Be sure to get, gather, and compare the following information from each lender and mortgage broker.

RATES Ask each lender and broker for their current mortgage interest rates and whether the rates

being quoted are the lowest for that day or week. Ask whether the rate is fixed or adjustable. Keep in mind that when interest rates for

adjustable-rate loans go up, so does the monthly payment. If the rate quoted is for an adjustable-rate loan, ask how your rate and loan payment will

vary, including whether your loan payment will be reduced when rates go down. Ask what index and margin will be used. Find out how frequently your rate can adjust (monthly, 6months, or yearly) and how much it

can change at each adjustment (yearly caps, lifetime caps).

POINTSPoints or discount points are fees paid to the lender or broker for the loan and are often linked to the interest rate. Usually, the more points you pay, the lower the rate. Ask to see exactly how much your rate will be dropped based on the amount of discount points you pay. For example, paying 0.50% of the loan amount in discount points may adjust the loan rate downwards by

37

025%. Each program and lender will use a different formula and the amounts of points will change daily as market rates change.

Note the tradeoff between points and rates and compare your short-term needs against your long-term needs. Here is an example based on $100,000. 30yr fixed rate mortgage at a 6.5% interest rate: With Discount Points With No Discount points

$ Amount of points$250 $0.00

Interest Rate6.25% 6.5%

Monthly payment$616 $632

In the above example, it would cost you $250 to save $16 a month in your payment. Only you can determine if this is a beneficial trade off for you. Ask yourself whether you can afford the extra cash upfront right now and then note the following. (Amount to buy down .25% - changes daily.)

1. The $250 repays itself in approximately 16 months (dividing $250 by $16 equals 15.63 months). Every month you keep the loan after this point you will be “making” an extra $16 per month. Over the next 344 months this equates to $5,504.

2. Over the life of the loan, this $250 investment also saves you approximately $5,886 in

interest.

Check your local newspaper business section for information about rates and points currently being offered.

Ask for points to be quoted to you as a dollar amount- rather than just as the number of points--so that you will actually know how much you will have to pay.

FEESA home loan often involves many fees, such as loan origination or underwriting fees, broker fees, transaction, settlement, and third party costs. Every lender or broker must give you an estimate of its fees when you apply for a mortgage loan. Many of these fees are negotiable. In some cases, you can borrow the money needed to pay these fees, but doing so will increase your loan amount and total costs. “No cost” loans are frequently available, but they usually involve higher rates.

Ask what each fee covers. Several items may be lumped into one fee. Ask for an explanation of any fee you don’t understand. Third party costs should be charged to you at the actual cost of service. Ask to see

invoices if you feel you’re paying too much.

38

39

DOWN PAYMENTS AND PRIVATE MORTGAGE INSURANCESome lenders require 20% of the home’s purchase price or value as a down payment or equity in the loan. This requirement is known as the loan to value or LTV. A 20% down payment or equity equates to an 80% LTV. Your lender will tell you their LTV requirements for each type of loan.

Most lenders offer loans that require less than 20% down- sometimes as little as 0% on conventional loans. If a 20% down payment is not made, lenders usually require the borrower to purchase private mortgage insurance (PMI) to protect the lender in case the borrower fails to pay. When government- assisted programs such as Federal Housing Administration (FHA), Veterans Administration (VA), or Rural Development services are available, the down payment requirements may be substantially smaller.

Ask about the lender’s requirements for LTV including what you need to do to verify that funds for your down payment are available

Ask your lender about special programs that they may offer.

If PMI is required for your loan:

Ask for the total cost of the insurance. Ask how much your monthly payment will be when including the PMI premium. Ask how long you will be required to carry PMI and how it can be removed later.

TAXES AND HOMEOWNER’S INSURANCEMany lenders will require your monthly loan payment to include an additional amount to cover annual property taxes and homeowner’s insurance. The amount is deposited into an account commonly called a reserve. Be sure to ask if taxes and insurance payments are required or optional by the lender. Typically, lenders will require monthly real estate taxes and homeowner Insurance payments if the LTV is greater than 80%. When comparing monthly payments from various lenders, be sure to ask if the lender included monthly taxes and insurance costs in the total payment. If they are included, ask for the costs to be broken down in the following manner.

Principal and Interest Real Estate Taxes Homeowner’s insurance Private Mortgage Insurance

40

The Good Faith Estimate or GFE provides you with estimates of the charges you are likely to pay at closing. Remember, the fees listed are only estimates. The actual charges may be more or less but, in general, they should be pretty close to what you’ll pay at closing. Keep in mind; your transaction may not involve a fee for every item listed in this document.

The new GFE that went into effect January 1st, 2010 is very confusing and unclear of the final costs. It is important to sit down with your mortgage professional and go over the costs in detail so you are clear.

In the new GFE there are a few things to watch for that can be confusing:

1) It only shows the principle, interest and mortgage insurance on the payment mentioned on the “summary of your loan” on page 1. Please remember that there are taxes and insurance on top of that number. Your full payment will include: principle and interest, taxes and insurance and any mortgage insurance that may apply.

2) It shows the “owners” (sellers) title insurance policy (section B) in addition to your title policy and numbers in the bottom line. This is not a fee that is paid by the buyer in Utah. Since the GFE is a nationwide form and most of the other states the buyer does pay for the owners/sellers title insurance, we must show it. Your mortgage professional should give you the bottom line figures without this fee. Remember, it must show on the GFE, we cannot take it out.

The GFE is broken out into major costs areas:

Section A: These are items payable in connection with your loan. Here you will find your loan fee, credit fees, appraisal fees, processing fee, underwriting fee and other costs directly related to obtaining a loan. It is all lumped into one sum and not broken out.

Section B: These items are required by your lender to be paid in advance. These are items such as interim daily interest, title insurance policies (both buyer and owner), Transfer taxes, any required services, and government recording charges, upfront mortgage insurance, taxes and home owners insurance.

Section A & B This is the two sections totaled at the bottom. This should be your total number but it is not. Please have your mortgage professional break out what are you real numbers to bring in to closing.

Settlement Service Provider Statement: This shows the fees that are being charged for the title insurance fees and who your title company will be for your transaction.

Remember, more than any other time it is important to work closely with your Mortgage professional to avoid any confusion.

41

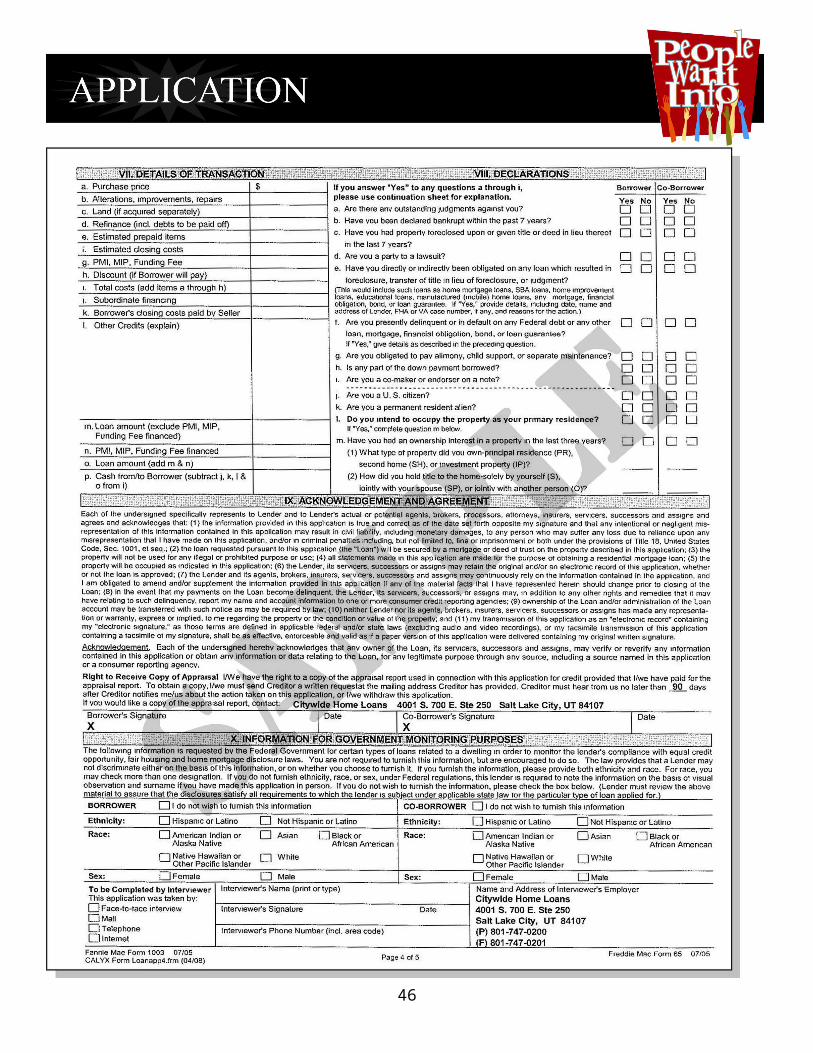

42

43

44

45

46

This is a question asked by every borrower these days. Because no one wants to pay anything unnecessary, the prospect of paying a couple of thousand dollars never appeals to anyone. Consequently, a lender’s offer of a zero point loan sounds enticing. Indeed, they are very popular with borrowers these days. One lender recently told me that in over 80% of refinance transactions, the borrowers are paying no points. We both said, “How sad. Too bad they didn’t get better advice.”

Now it seems like a zero point loan is a good deal. What’s wrong with Free? And it is a good deal, but for the lender, not the borrower. Here’s why. Borrowing and lending is what is called a zero sum game, like poker. What one player wins, the other loses. As the borrower, you are playing poker with the lender and if the lender can talk you into paying more money, he wins.

So why would the lender be willing to do something for FREE? Well, you probably heard that they raise the interest rate to do zero point loans, a case of pay me now or pay me later. The lenders always use the word “slightly” as in, “the rate for a zero point loan is slightly higher.” When you look at the dollars, however, it’s not “slightly more, you’re paying a lot more, thousands of dollars more.

To demonstrate that, when you compare two transactions with and without points, the differences are startling. On a loan amount of $200,000.00 and using a period of eight years (the period many people own their homes these days) by talking you into a zero point loan, the lender receives $7,548 more in interest and you still owe them $7,549 more, a total benefit to them of $15,097 and all they gave up was $2,000 in the first year. Of course, it being a zero sum game, YOU paid $7,548 more in interest and YOU still owe $7,549 more.

Now I know that many people find it difficult to comprehend that there could be this much difference. It’s also not easy to make those calculations. The lenders are counting on that. They just love it that people seem to want to choose the loan which is so much more profitable to them.

That’s exactly why you should go through the mortgage process with someone who is willing to help you make these decisions in the most intelligent way. Getting a mortgage is a process, not buying a thing, and your search should start with getting referrals for someone to help you through the process.

Finally, there are people for whom a zero point loan does make sense, usually those who will only be in a property for less than three years. But for most people, it makes more sense to pay points.

47

WHO WORKS FOR WHOM?

SELLER AGENCY (Single Agency) Agent will represent the best interests of the seller. Agent will owe the seller fiduciary duties. Agent must give the buyer all material facts so that

the buyer can make an educated decision.

BUYER AGENCY (Single Agency) Agent will represent the best interests of the buyer. Agent will owe the buyer fiduciary duties. Agent must give the seller all material facts so that

the buyer can make an educated decision.

TRANSACTION BROKER (Dual Agency) Agent represents both the buyer and the seller

equally. Agent’s objective is to get a mutually satisfactory

agreement among all parties. Agent gives all options to the buyer and the seller. Depending on the local market, all parties may be

present at contract presentation to negotiate on their own behalf.

All parties have confidentiality – agent may do nothing to the detriment of either the buyer or the seller.

Both the buyer and the seller have a right to counsel. Before making any decisions, both parties have the right to seek family, religious, legal, or financial counsel.

IN ALL RELATIONSHIPS, AS YOUR AGENT I HAVE A DUTY TO ACT HONESTLY WITH BOTH THE BUYER AND THE SELLER.

48

Whether you’re buying a home for the first time or refinancing a loan for the third time, it’s important to know who the main players are and what roles in the transaction they play.

Here are some initial introductions:

Borrower: A person who has been approved to receive a loan and is then obligated to repay it, plus any additional fees according to the loan terms.

Selling Agent: The real estate agent working for the buyer rather than listing the property. The listing and selling agent may be the same person or company. Listing Agent: A real estate agent who represents the seller.

Mortgage Broker: An individual or company which brings borrowers and lenders together for the purpose of loan origination, but which does not originate or service the mortgage. The broker might also negotiate with the lender to try and find the best possible financing deal possible for the borrower.

Lender: Any person or entity loaning funds which are to be repaid.

Title Company / Title Insurance Company: A company which issues insurance regarding title to real property. The title company will insure the title to the home is clear of any liens not pertaining to the new purchaser.

Appraiser: A qualified individual who uses his or her experience and knowledge to determine the value of a home and prepare the appraisal estimate. The appraiser works for the lender to protect their interest in the property, not the brokers, the buyers or the real estate agents

Inspector: A designated agent who inspects and documents the physical condition of the property as described and verified in an inspection certificate.

Escrow Agent/Agency: The person or organization having a fiduciary responsibility to both the buyer and seller to see that the terms of the purchase/sale (or loan) are carried out. Often referred to as “closing” the loan, title companies, attorneys and even the lender may serve in this role. The escrow agency will handle all of the funds for settlement and closing.

49

ACCEPTANCEThe date when both parties, seller and buyer, have agreed to and completed signing and/or initialing the contract.

ADJUSTABLE RATE MORTGAGEA mortgage that permits the lender to adjust the mortgage’s interest rate periodically on the basis of changes in a specified index. Interest rates may move up or down, as market conditions change.

AMORTIZED LOANA loan which is paid in equal installments during its term.

A.P.R. (Annual Percentage Rate)A term used in the Truth in Lending Act. It represents the relationship of the total finance charge (interest, discount points, origination fees, loan broker, commission, etc.) to the amount of the loan.

APPRAISALAn estimate of real estate value, usually issued to standards of FHA, VA, and FHMA. Recent comparable sales in the neighborhood is the most important factor in determining value. This should be contrasted against the home inspection.

ASSUMABLE MORTGAGEPurchaser takes ownership to real estate encumbered by an existing mortgage and assumes responsibility as the guarantor for the unpaid balance of the mortgage.

BILL OF SALEDocument used to transfer title (ownership) of personal property.

CLOSING STATEMENT (HUD 1)A financial statement rendered to the buyer and seller at the time of transfer of ownership, giving an account of all funds received or expended.

CLOUD ON TITLEAny condition that affects the clear title to real property.

COMPARABLE SALESSales that have similar characteristics as the subject property and are used for analysis in the appraisal process.

CONTRACTAn agreement to do or not do a specified action.

50

CONSIDERATIONAnything of value to induce another to enter into a contract, i.e.; money, services, a promise.

DEEDWritten instrument, which when properly executed and delivered, conveys title to real property.

DISCOUNT POINTSA loan fee charged by a lender of FHA, VA, or conventional loans to increase the yield on the investment. One point = 1% of the loan amount.

EASEMENTThe right to use the land of another.

ENCUMBRANCEAnything that burdens (limits) the fee title to property, such as a lien, easement, or restriction of any kind.

EQUITYThe value of real estate over and above the liens against it. It is obtained by subtracting the total liens from the value.

ESCROW PAYMENTThat portion of a mortgagor’s monthly payment held in trust by the lender to pay for taxes, hazard insurance, mortgage insurance, lease payments, and other items as they become due.

FANNIE MAENickname for Federal National Mortgage Corporation (FNMA), a tax-paying corporation created by congress to support the secondary mortgages insured by FHA or guaranteed by VA, as well as conventional home mortgages.

FEDERAL HOUSING ADMINISTRATION (FHA)An agency of the U.S. Department of Housing and Urban Development (HUD). Its main activity is the insuring of residential mortgage loans made by private lenders. The FHA sets standards for construction and underwriting but does not lend money or plan or construct housing.

FHA INSURED MORTGAGEA mortgage under which the Federal Housing Administration insures loans made, according to its regulations.

51

FIXED RATE MORTGAGEA loan that fixes the interest rate at a prescribed rate for the duration of the loan.

FORECLOSUREProcedure whereby property pledges as security for a debt is sold to pay the debt in the event of default.

FREDDIE MACNickname for Federal Home Loan Mortgage Corporation (FHLMC), a federally controlled and operated corporation to support the secondary mortgage market. It purchases and sells residential conventional home mortgages.

INVESTORThe holder of a mortgage or the permanent lender for whom the mortgage banker services the loan. Any person or institution that invests in mortgages.

LOAN TO VALUE RATIO (LTV)The ratio of the mortgage loan principal (amount borrowed) to the property’s appraised value (selling price). Example: On a $100,000 home, with a mortgage loan principal of $80,000, the loan to value ratio is 80 percent.

MORTGAGEA legal document that pledges a property to the lender as security for payment of a debt.

MORTAGE INSURANCE PREMIUM (MIP)The amount paid by a mortgagor for mortgage insurance. This insurance protects the investor from possible loss in the event of a borrower’s default on a loan.

MORTGAGORThe borrower of money or giver of the mortgage document.

NOTEA written promise to pay a certain amount of money.

ORIGINATION FEEA fee paid to the mortgage for paying the mortgage before it becomes due. Also known as prepayment fee or reinvestment fee.

PRIVATE MORTGAGE INSURANCE (PMI)See Mortgage Insurance Premium.

52

PROMISSORY NOTEA written contract containing a promise to pay a definite amount of money at a definite future time.

REALTORA member of local and state real estate boards, which are affiliated with the National Association of Realtors (NAR).

SECOND MORTGAGE / SECOND DEED OF TRUST / JUNIOR MORTGAGE / JUNIOR LIENAn additional loan imposed on a property with a first mortgage. Generally, a higher interest rate and shorter term than a “first” mortgage.

SEVERALTY OWNERSHIPOwnership by one person only. Sole ownership.

SURVEYThe process by which a parcel of land is measured and its area ascertained.

TENANCY IN COMMONOwnership by two or more persons, who hold an undivided interest without right of survivorship. (In the event of the death of one owner, his/her share will pass to his/her heirs).

TITLE INSURANCEAn insurance policy which protects the insured (purchaser or lender against loss arising from defects in the title).

53