firm complexity and pead - faculty support sitefaculty.ucr.edu/~abarinov/pead (06-14).pdf · firm...

TRANSCRIPT

Firm Complexity and PEAD

Alexander Barinov; Shawn Park; Çelim Yıldızhan

Terry College of BusinessUniversity of Georgia

June 12, 2014

Barinov, Park, Yıldızhan (UGA) Firm Complexity and PEAD June 12, 2014 1 / 23

Motivation

Firm Complexity

Cohen and Lou (JFE 2012) show that themarket has trouble digesting the informationabout multi-segment firms

They show that returns to a pseudo-conglomerate consisting of single-segment firmspredict returns to the real conglomerate

We are trying to understand what (other?) kindof information about multi-segment firms themarket has trouble digesting

Barinov, Park, Yıldızhan (UGA) Firm Complexity and PEAD June 12, 2014 2 / 23

Motivation

Three Measures of Complexity

Conglomerate dummy (Conglo) - 1 if the firmhas multiple segments, 0 otherwise

Concentration (Complexity) - our main variable,equals to 1-HHI, HHI is based on segment sales

HHI=1 is a single-segment firm, HHI=0.5 - a firmwith two equal segments, HHI=0.1 is a firm withten equal segments

Number of segments (based on 2-digit SICcodes)

Barinov, Park, Yıldızhan (UGA) Firm Complexity and PEAD June 12, 2014 3 / 23

Motivation

Complexity and PEADWe consider information in earningsannouncements: the market is known to be slowto incorporate it into prices (post-earningsannouncement drift, PEAD)The main hypothesis that complicated firmshave stronger PEAD, because it takes themarket longer to figure them outWe are fighting an uphill battle here, because allanomalies should be stronger for smaller,illiquid, more volatile firms, and complicatedfirms (conglomerates) are exactly opposite ofthat

Barinov, Park, Yıldızhan (UGA) Firm Complexity and PEAD June 12, 2014 4 / 23

Firm Characteristics

Complexity andEarnings Announcements

Panel A1. Raw Values

Single Conglo All S-C A-CSUE 0.172 0.155 0.169 0.017 0.014t-stat 7.60 4.27 5.61 0.94 1.22EA 0.079 0.151 0.114 -0.072 -0.037t-stat 1.47 3.10 2.79 -1.82 -1.46

Panel A2. Absolute Values

Single Conglo All S-C A-CSUE 0.834 0.787 0.785 0.048 -0.002t-stat 16.9 18.5 18.5 1.76 -0.13EA 3.798 3.042 3.322 0.757 0.281t-stat 13.2 15.2 15.4 5.88 3.79

Barinov, Park, Yıldızhan (UGA) Firm Complexity and PEAD June 12, 2014 5 / 23

Firm Characteristics

Complexity and Liquidity

Single Conglo All S-C A-CGibbs 0.695 0.449 0.612 0.246 0.162t-stat 10.1 20.3 11.1 4.48 4.08Spread 1.032 0.650 0.877 0.382 0.227t-stat 12.3 13.5 13.0 5.43 4.33Roll 1.824 1.342 1.650 0.481 0.308t-stat 14.7 20.2 16.5 5.19 4.43Amihud 0.040 0.020 0.028 0.020 0.008t-stat 4.55 3.46 4.55 5.98 10.22Zero 0.165 0.135 0.157 0.030 0.022t-stat 5.98 6.13 6.10 4.35 4.95

Barinov, Park, Yıldızhan (UGA) Firm Complexity and PEAD June 12, 2014 6 / 23

Firm Characteristics

Complexity and Information

Single Conglo All S-C A-CSize 0.304 0.600 0.361 -0.296 -0.239t-stat 5.25 5.64 5.16 -5.54 -5.55IO 0.404 0.452 0.394 -0.048 -0.058t-stat 6.76 8.17 7.14 -6.97 -9.40# An 4.748 5.414 4.513 -0.667 -0.901t-stat 11.7 16.1 13.2 -5.28 -9.68IVol 2.033 1.598 1.854 0.435 0.255t-stat 14.6 21.2 17.5 4.73 4.20Turn 7.633 6.941 7.019 0.692 0.078t-stat 4.91 5.07 5.04 2.38 0.75

Barinov, Park, Yıldızhan (UGA) Firm Complexity and PEAD June 12, 2014 7 / 23

Firm Characteristics

Characteristics: Summary

Conglomerates are more liquid thansingle-segment firms or Compustat firms

Conglomerates exist in a more transparentenvironment (more institutional ownership, moreanalysts, higher market cap, lower volatility)

Conglomerates witness smaller (in absolutemagnitude) surprises at earningsannouncements (and these surprises areprobably more positive)

Barinov, Park, Yıldızhan (UGA) Firm Complexity and PEAD June 12, 2014 8 / 23

Complexity and PEAD

Fama-MacBeth Regressions

CAR+2;+60 = γ0 + γ1 · SUE0 + γ2 · Comp0 + γ3 · SUE0 · Comp0

γ1 > 0 - PEAD, γ3 > 0 - stronger PEAD for complicated firms

Defining PEAD as a coefficient in FM regressions meansmeasuring PEAD per unit of SUE

"Stronger PEAD for complicated firms" then does notnecessarily mean that the trading strategy based on PEADwill yield more if done for conglomerates only, becauseconglomerates have less extreme SUE

Rather, "stronger PEAD for complicated firms" means that ifone takes a conglomerate and a single-segment firm with thesame SUE, the conglomerate will have stronger PEAD

Barinov, Park, Yıldızhan (UGA) Firm Complexity and PEAD June 12, 2014 9 / 23

Complexity and PEAD

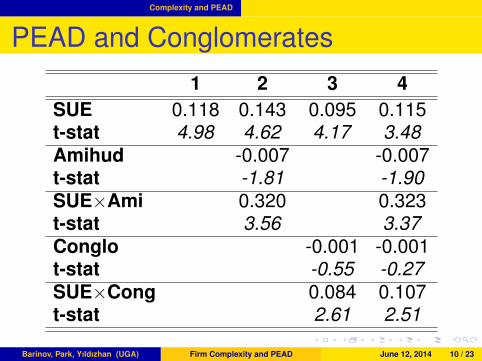

PEAD and Conglomerates

1 2 3 4SUE 0.118 0.143 0.095 0.115t-stat 4.98 4.62 4.17 3.48Amihud -0.007 -0.007t-stat -1.81 -1.90SUE×Ami 0.320 0.323t-stat 3.56 3.37Conglo -0.001 -0.001t-stat -0.55 -0.27SUE×Cong 0.084 0.107t-stat 2.61 2.51

Barinov, Park, Yıldızhan (UGA) Firm Complexity and PEAD June 12, 2014 10 / 23

Complexity and PEAD

PEAD and Complexity

1 2 5 6SUE 0.118 0.143 0.099 0.123t-stat 4.98 4.62 4.36 4.00Amihud -0.007 -0.007t-stat -1.81 -1.91SUE×Ami 0.320 0.335t-stat 3.56 3.54Complexity -0.003 -0.002t-stat -0.64 -0.38SUE×Comp 0.184 0.218t-stat 2.73 2.70

Barinov, Park, Yıldızhan (UGA) Firm Complexity and PEAD June 12, 2014 11 / 23

Complexity and PEAD

PEAD and Complexity: Conclusions

The spread between 2.5th and 97.5th percentileof SUE is 0.27 - all slopes on SUE have to bedivided by roughly 4 to figure out PEAD

In the regression without control the slope is0.118 - that is, PEAD, on average, is roughly 3%(in the quarter after the announcement)

The slope on SUE × Conglo is 0.084 - PEAD isby roughly 2% stronger for conglomerates

Controlling for stronger PEAD for less liquidfirms increases the latter estimate by about 25%

Barinov, Park, Yıldızhan (UGA) Firm Complexity and PEAD June 12, 2014 12 / 23

Complexity and PEAD

Complexity Matters

Full Sample 0<Comp<Med Comp>MedSUE 0.099 0.131 -0.074t-stat 5.26 3.04 -0.55Complexity -0.003 -0.012 0.002t-stat -0.64 -1.44 0.22SUE×Comp 0.184 0.448 0.458t-stat 2.73 2.03 1.71

1-HHI has a large mass at 0 - so, is it just conglomeratesversus standalones?

No, if we restrict the sample to conglomerates only, morecomplex conglomerates do have stronger PEAD

Barinov, Park, Yıldızhan (UGA) Firm Complexity and PEAD June 12, 2014 13 / 23

New Conglomerates

New ConglomeratesConglomerates are different from standalones in manydifferent aspects

To make sure that it is the conglomerate status, andnot those differences that drive stronger PEAD forconglomerates, we look at PEAD in the two years afterthe new conglomerate is formed

We find that PEAD is stronger during the first twoyears of conglomerate’s life

Conglomerates still have stronger PEAD thanstandalones even as they get older

Interestingly enough, there is no stronger PEADpost-M&A - stronger PEAD for new conglomerates isdriven by "growth from within"

Barinov, Park, Yıldızhan (UGA) Firm Complexity and PEAD June 12, 2014 14 / 23

New Conglomerates

New Conglomerates

1 2 3SUE×Cong 0.100 0.100 0.100t-stat 2.91 2.91 2.91SUE×New 0.158t-stat 2.13SUE×M&A 0.046t-stat 0.39SUE×NoM&A 0.452t-stat 2.08

Barinov, Park, Yıldızhan (UGA) Firm Complexity and PEAD June 12, 2014 15 / 23

Analyst Coverage

Specialists and Conglomerates

Information about conglomerates is hard toprocess, which should make analysts reluctantto cover them

In particular, we wonder whether specialists(covering five or more firms in the sameindustry) tend to abandon conglomerates

Specialists for conglomerates are defined basedon the largest segment, but defining them basedon all segments yields similar results

Barinov, Park, Yıldızhan (UGA) Firm Complexity and PEAD June 12, 2014 16 / 23

Analyst Coverage

No Size Matching

Panel B2. No Matching

Conglo Simple diff t-stat# Analysts 5.4 4.7 0.7 5.28# Specialists (SIC2) 4.3 4.0 0.3 2.41# Specialists (SIC3) 3.6 3.6 0.1 0.74% of Specialists (SIC2) 0.70 0.77 -0.07 -12.63% of Specialists (SIC3) 0.57 0.66 -0.09 -14.45Forecast Error 0.59 0.63 -0.04 -1.88

Despite conglomerates being larger, they are covered by thesame number of specialists as standalones

The fraction of specialists in their coverage is smaller

Barinov, Park, Yıldızhan (UGA) Firm Complexity and PEAD June 12, 2014 17 / 23

Analyst Coverage

Size Matching

Panel B1. Size Matching

Conglo Simple diff t-stat# Analysts 5.4 6.6 -1.2 -7.53# Specialists (SIC2) 4.3 5.8 -1.5 -10.01# Specialists (SIC3) 3.6 5.2 -1.6 -11.06% of Specialists (SIC2) 0.70 0.81 -0.12 -12.42% of Specialists (SIC3) 0.57 0.71 -0.15 -14.46Forecast Error 0.59 0.50 0.09 3.29

Comparing conglomerates to standalones of the same size,their analyst coverage is much worse on all dimensions

Conglomerates are covered by less analysts, less specialists,smaller fraction of specialists

Barinov, Park, Yıldızhan (UGA) Firm Complexity and PEAD June 12, 2014 18 / 23

Analyst Coverage

Analyst Coverage and PEAD

1 2 3SUE 0.066 0.091 0.083t-stat 3.03 4.36 3.86Complexity 0.000 0.002t-stat 0.03 0.30SUE×Comp 0.259 0.207t-stat 2.93 2.19# An 0.001 0.001t-stat 1.21 1.10SUE×# An -0.022 -0.021t-stat -4.71 -4.10

Barinov, Park, Yıldızhan (UGA) Firm Complexity and PEAD June 12, 2014 19 / 23

Analyst Coverage

Specialist Coverage and PEAD

1 4 5SUE 0.066 0.091 0.084t-stat 3.03 4.39 3.94Complexity 0.000 0.003t-stat 0.03 0.53SUE×Comp 0.259 0.186t-stat 2.93 1.88# Spec2 0.001 0.001t-stat 1.50 1.40SUE×# Spec2 -0.020 -0.020t-stat -3.69 -3.39

Barinov, Park, Yıldızhan (UGA) Firm Complexity and PEAD June 12, 2014 20 / 23

Analyst Coverage

Analyst Coverage and PEADWe use residual coverage (residuals fromcross-sectional regressions of number ofanalysts/specialists on size) to control for sizeeffects

We find that firms with worse coverage (comparedto their peers of the same size) have strongerPEAD

Conglomerates have worse coverage too - is thatthe reason of stronger PEAD for conglomerates?

No, the relation between complexity and PEADweakens by only 25% after we control for therelation between PEAD and analyst coverage

Barinov, Park, Yıldızhan (UGA) Firm Complexity and PEAD June 12, 2014 21 / 23

Other Results

Other ResultsThe relation between PEAD and complexity isconcentrated in the first 40 days after the announcementand dissipates afterwards (together with PEAD forstandalones that disappears after 40 days too)

Stronger PEAD for complex firms does not overlap withthe original Cohen and Lou effect (returns toconglomerates are predictable using returns topseudo-conglomerates)

Announcement returns are somewhat stronger forconglomerates too (their earnings are "moreinformative"), but the difference in the announcementeffects between conglomerates and standalones is notstrong enough to explain the difference in PEADs

Barinov, Park, Yıldızhan (UGA) Firm Complexity and PEAD June 12, 2014 22 / 23

Conclusions

ConclusionsPEAD is stronger for complicated firms(conglomerates), despite conglomerates generallyhaving low limits to arbitrage

PEAD is stronger for more complicatedconglomerates

PEAD is stronger for new conglomerates,especially if they are not created through M&A

Conglomerates have worse analyst coverage, butcomplexity is broader than just the amount andquality of analyst coverage

Firm complexity is a new limits-to-arbitrage variableBarinov, Park, Yıldızhan (UGA) Firm Complexity and PEAD June 12, 2014 23 / 23