financing, investor protection and online securities offerings chapter 21

TRANSCRIPT

Financing, Investor ProtectionAnd Online Securities Offerings

Chapter 21

Corporate Financing

• Stock - An equity security that represents the purchase of a share of ownership in a corporation by a shareholder.

Corporate Financing

• Common Stock

– Shareholder has a proportionate interest in the corporate with regard to voting, earnings, and net assets.

– Last to Receive Dividends or Surplus on Dissolution

Corporate Financing

• Preferred Stock

– Shares with priority over common stock for payment of dividends and distribution of assets on dissolution.

– May pay fixed dividend

– May not have voting rights

Corporate Financing

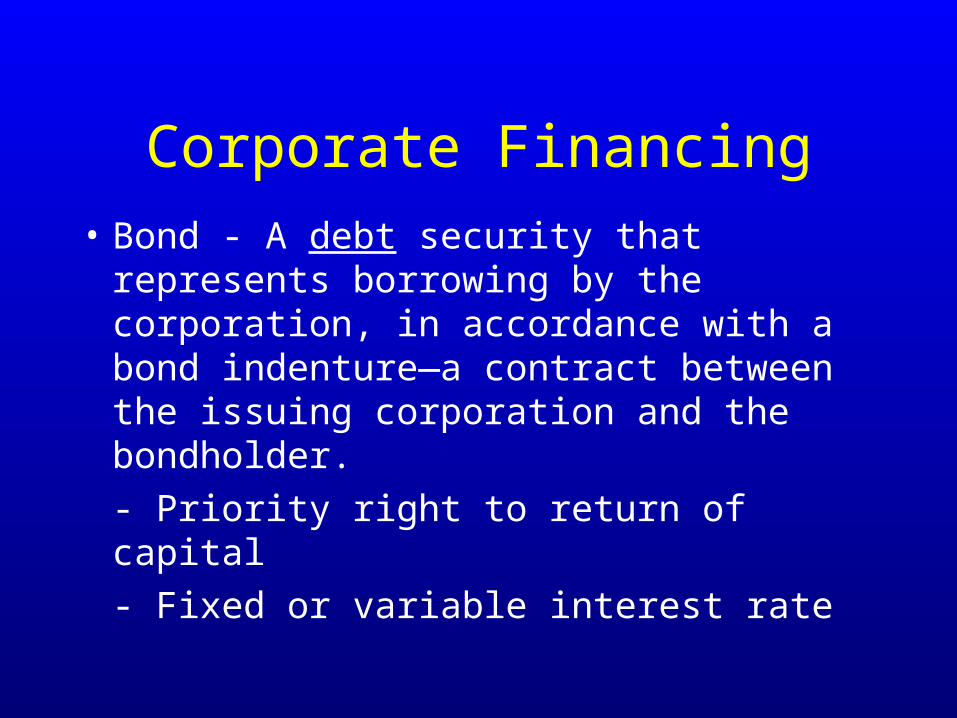

• Bond - A debt security that represents borrowing by the corporation, in accordance with a bond indenture—a contract between the issuing corporation and the bondholder.

- Priority right to return of capital

- Fixed or variable interest rate

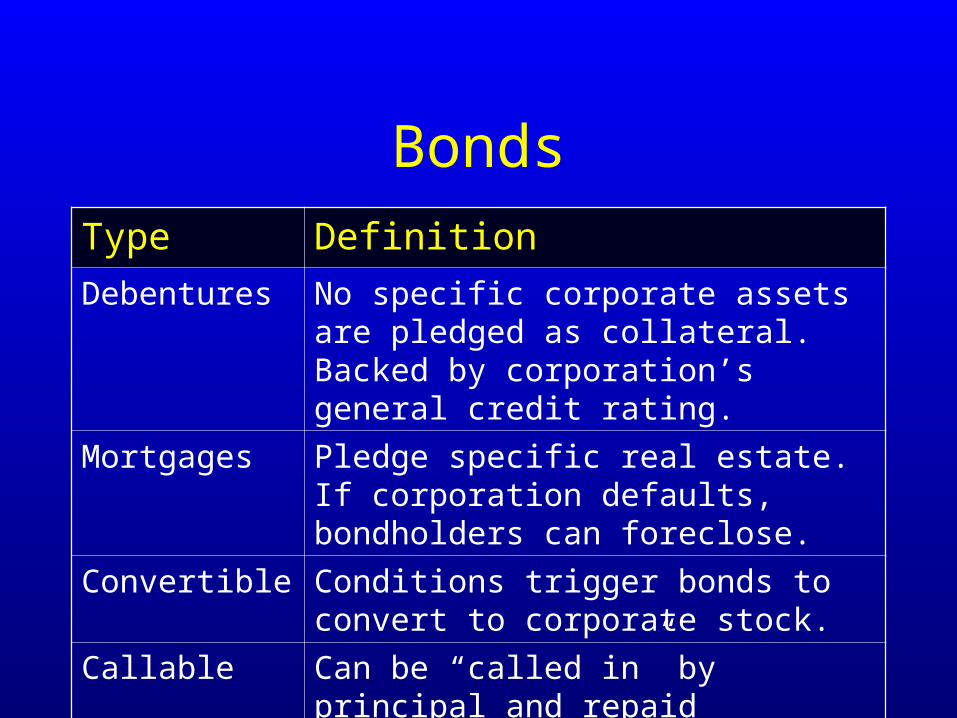

Bonds

Type DefinitionDebentures No specific corporate assets are pledged as

collateral. Backed by corporation’s general credit rating.

Mortgages Pledge specific real estate. If corporation defaults, bondholders can foreclose.

Convertible Conditions trigger bonds to convert to corporate stock.

Callable Can be “called in” by principal and repaid according to bond conditions.

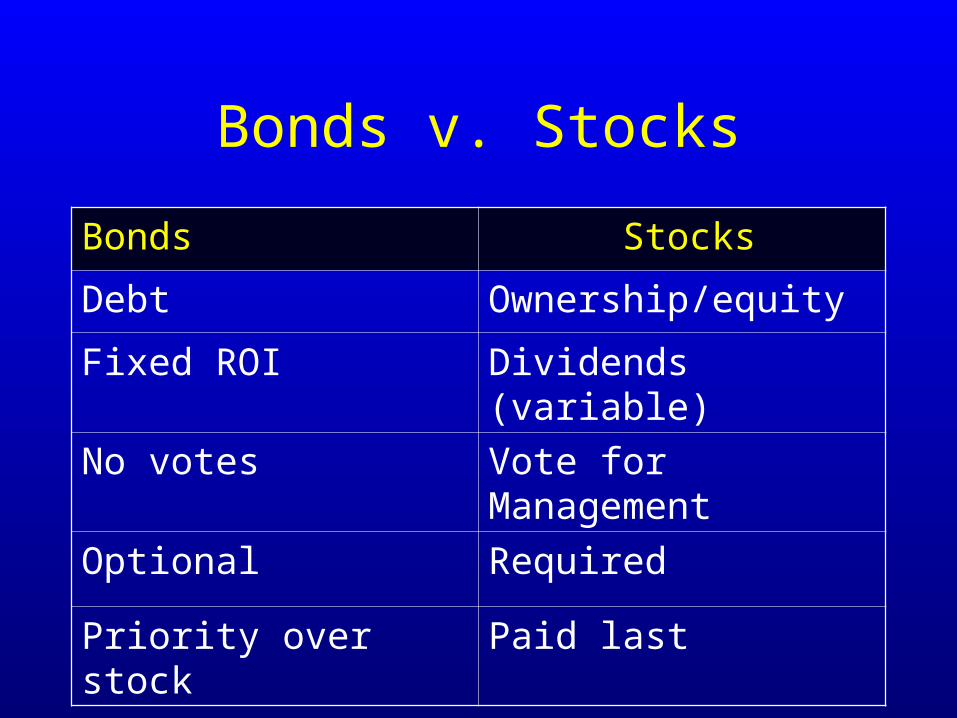

Bonds v. Stocks

Bonds Stocks

Debt Ownership/equity

Fixed ROI Dividends (variable)

No votes Vote for Management

Optional Required

Priority over stock Paid last

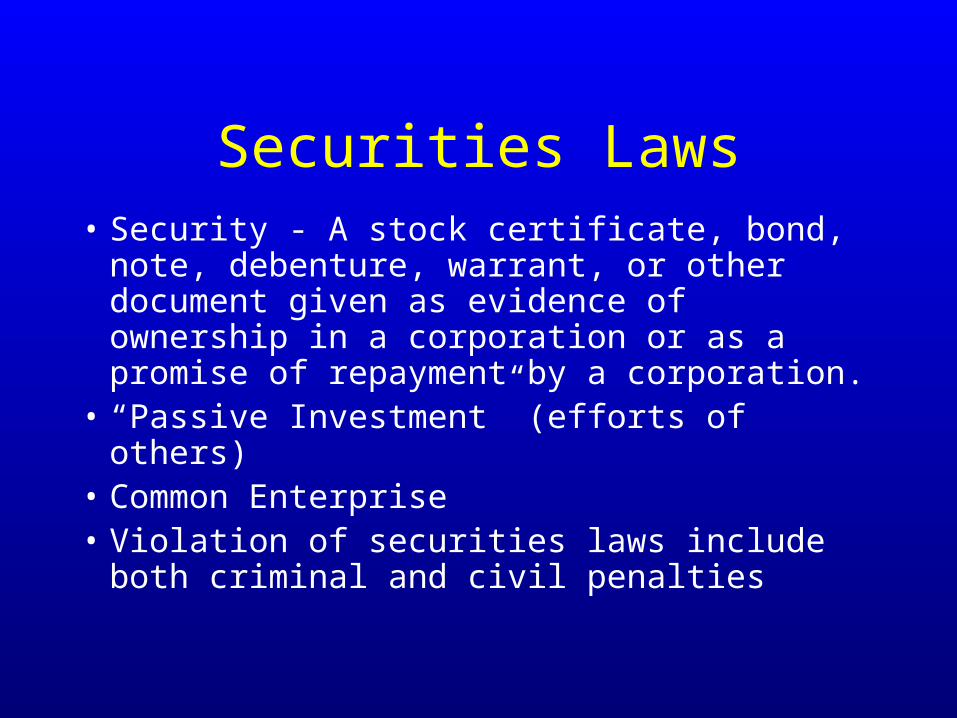

Securities Laws• Security - A stock certificate, bond, note,

debenture, warrant, or other document given as evidence of ownership in a corporation or as a promise of repayment by a corporation.

• “Passive Investment” (efforts of others)• Common Enterprise • Violation of securities laws include both

criminal and civil penalties

Securities Act of 1933

• Governs the initial sale of stock by businesses

• Put in place in response to the stock market crash of 1929 to prevent fraud in the issuance of securities by requiring disclosure of information to the public

Registration Statement

• Generally, a security must by registered before it is offered for sale to the public either through the mails or other facility of interstate commerce, including stock exchanges.

• Requires filing a registration statement (and prospectus which will be later distrubuted to investors) with the SEC

Registration Statement

• The registration statement must include a description of the following:– Properties and business activities– Directors and officers, their compensation,

securities holdings, and other benefits– Pending lawsuits– Financial Statements– Description of risks

Exempt Securities

• Securities issued by states or local governments

• Securities of Charitable Organizations

• Commercial paper maturing in nine months or less

• Insurance contracts

• Instruments issued by banks

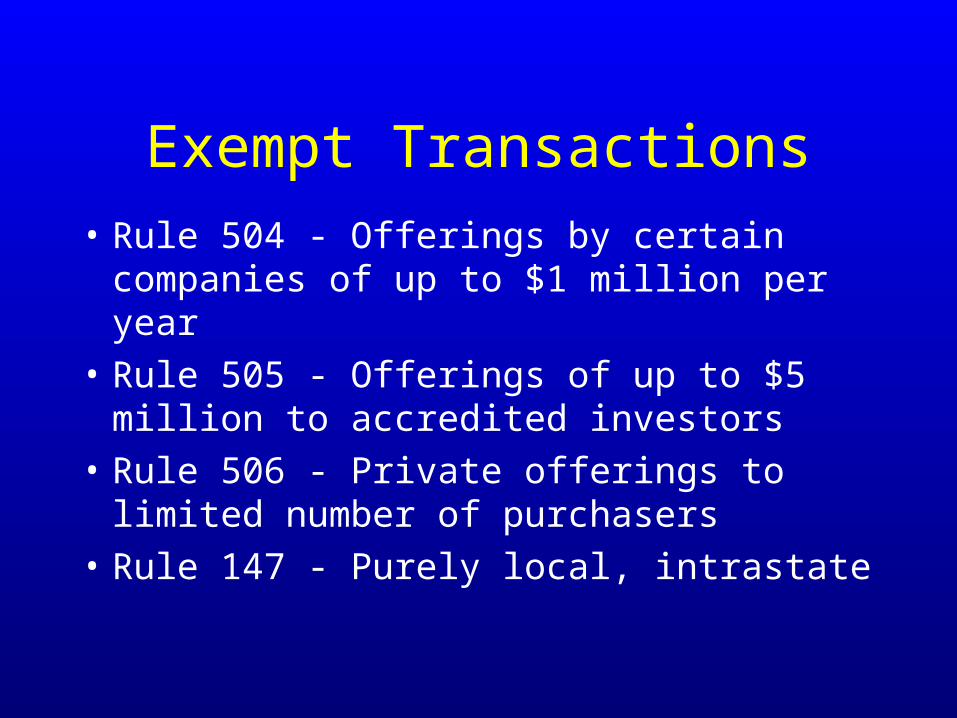

Exempt Transactions

• Rule 504 - Offerings by certain companies of up to $1 million per year

• Rule 505 - Offerings of up to $5 million to accredited investors

• Rule 506 - Private offerings to limited number of purchasers

• Rule 147 - Purely local, intrastate

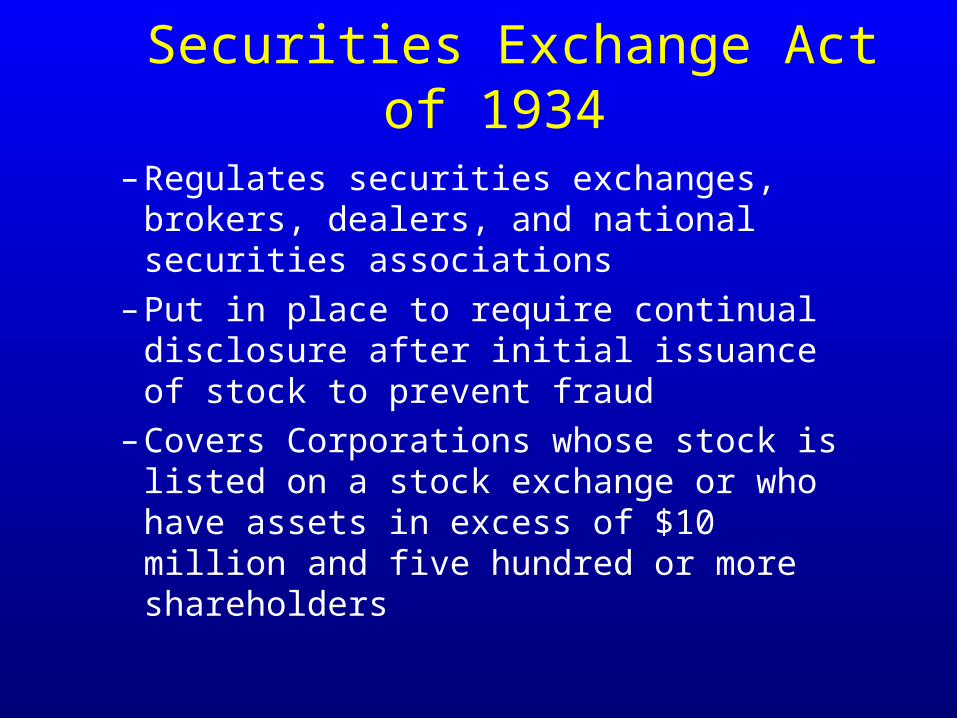

Securities Exchange Act of 1934– Regulates securities exchanges, brokers,

dealers, and national securities associations– Put in place to require continual disclosure

after initial issuance of stock to prevent fraud

– Covers Corporations whose stock is listed on a stock exchange or who have assets in excess of $10 million and five hundred or more shareholders

Securities Exchange Act of 1934

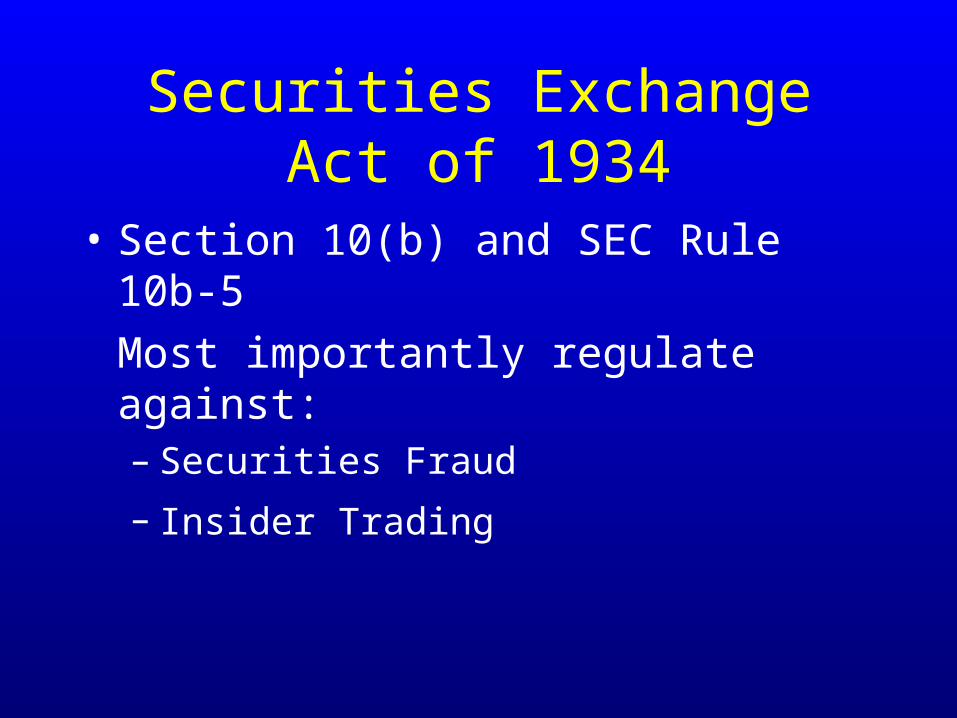

• Section 10(b) and SEC Rule 10b-5

Most importantly regulate against:– Securities Fraud

– Insider Trading

Securities Fraud

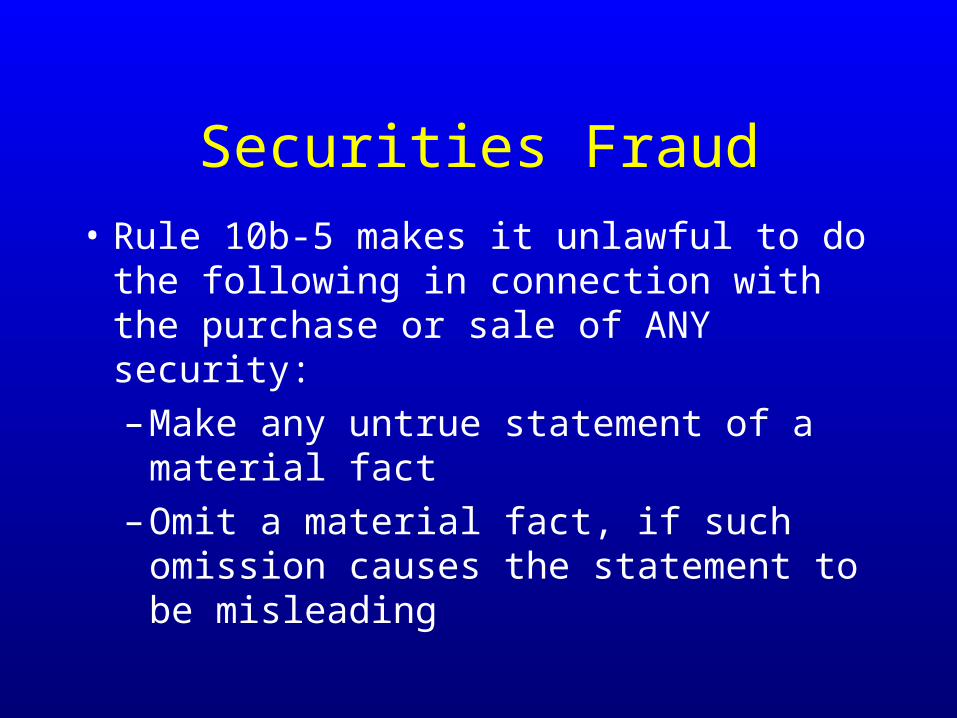

• Rule 10b-5 makes it unlawful to do the following in connection with the purchase or sale of ANY security:

– Make any untrue statement of a material fact

– Omit a material fact, if such omission causes the statement to be misleading

Securities Fraud

• Liability potential for:– accountants who prepare fraudulent or

misleading financials– attorneys who drafted them– ANYONE who participates in fraud, including

• Directors

• Officers

• Other “responsible” parties

Insider Trading

• Insider Trading - Purchase or sale of securities on the basis of information that has not been made available to the investing public.

• Liability extends to anyone who acquires inside information as a result of a insider’s breach of fiduciary duty to the corporation.

Insider Trading

– “Insiders” (Officers, Executives and Directors).– “Outsiders”

• Tipper/tippee theory--insider’s fiduciary duty must be breached.

• Misappropriation theory -- one wrongfully obtains inside info and trades on it. (Court may find a fiduciary relationship where one wouldn’t normally exist.)

Insider Trading

• Corporation may “recapture” any profits realized by an insider on any sale and purchase stock or other securities within any six-month period (Rule 16b)

• Considered “short swing profits”

• Inside information presumed

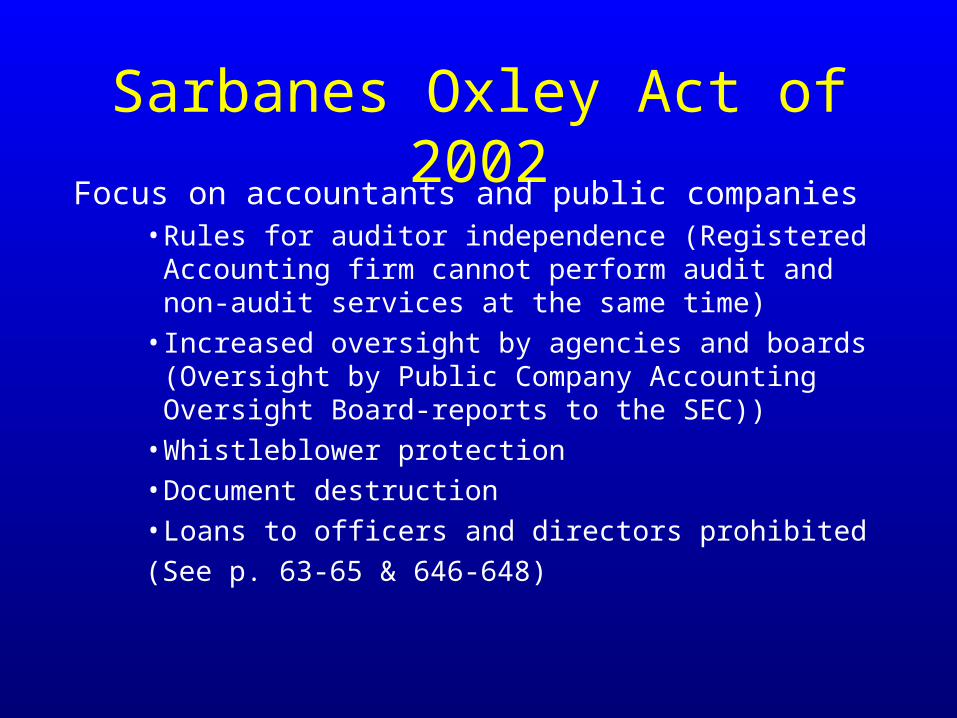

Sarbanes Oxley Act of 2002Focus on accountants and public companies

• Rules for auditor independence (Registered Accounting firm cannot perform audit and non-audit services at the same time)

• Increased oversight by agencies and boards (Oversight by Public Company Accounting Oversight Board-reports to the SEC))

• Whistleblower protection• Document destruction • Loans to officers and directors prohibited

(See p. 63-65 & 646-648)

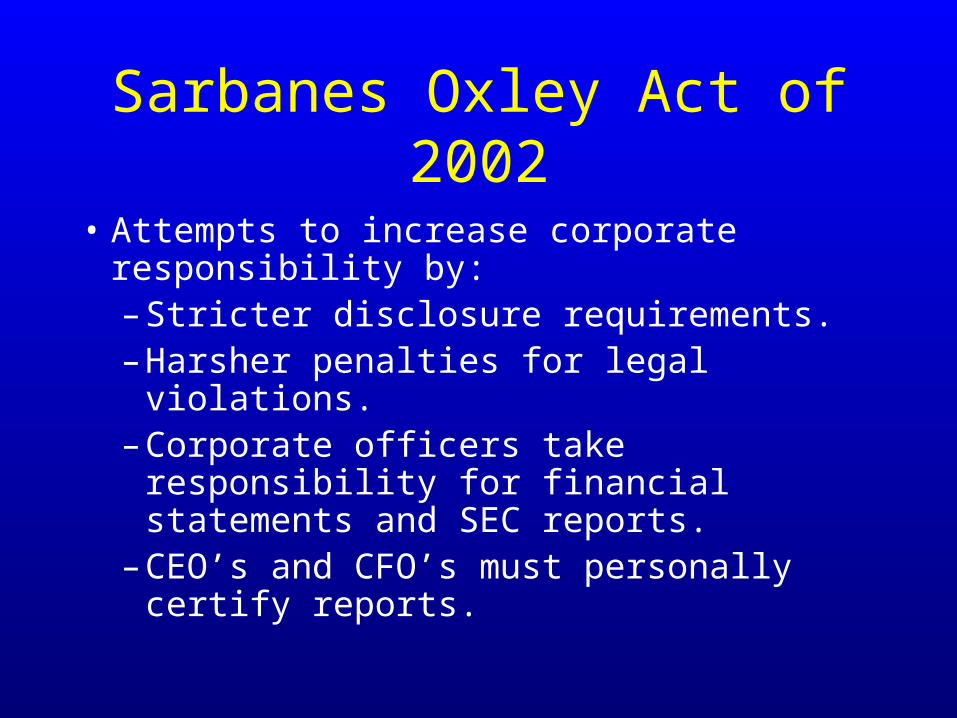

Sarbanes Oxley Act of 2002

• Attempts to increase corporate responsibility by:– Stricter disclosure requirements.– Harsher penalties for legal violations.– Corporate officers take responsibility for

financial statements and SEC reports.– CEO’s and CFO’s must personally certify

reports.

Financing, Investor ProtectionAnd Online Securities Offerings

End of Chapter 21