financial services tax shari’a compliant funds and islamic finance an irish perspective october...

TRANSCRIPT

Financial Services

TAX

Shari’a compliant funds and Islamic Finance

An Irish perspective

October 2009

2

Ireland – a snapshot from a Fund’s perspective

Ireland – a snapshot from a Fund’s perspective

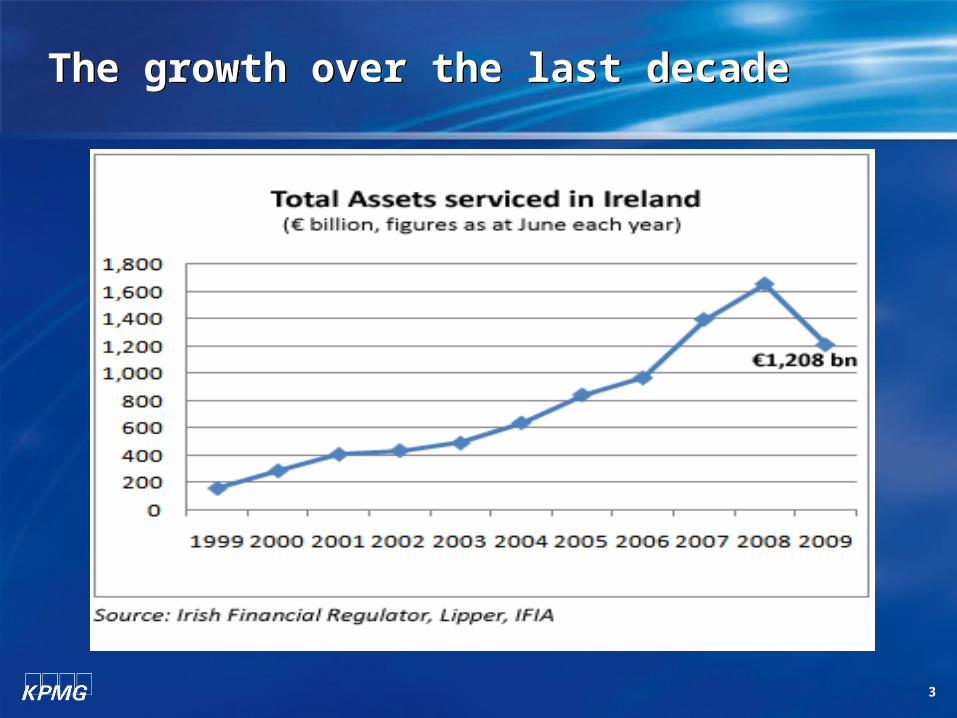

The growth over the last decadeThe growth over the last decade

3

4

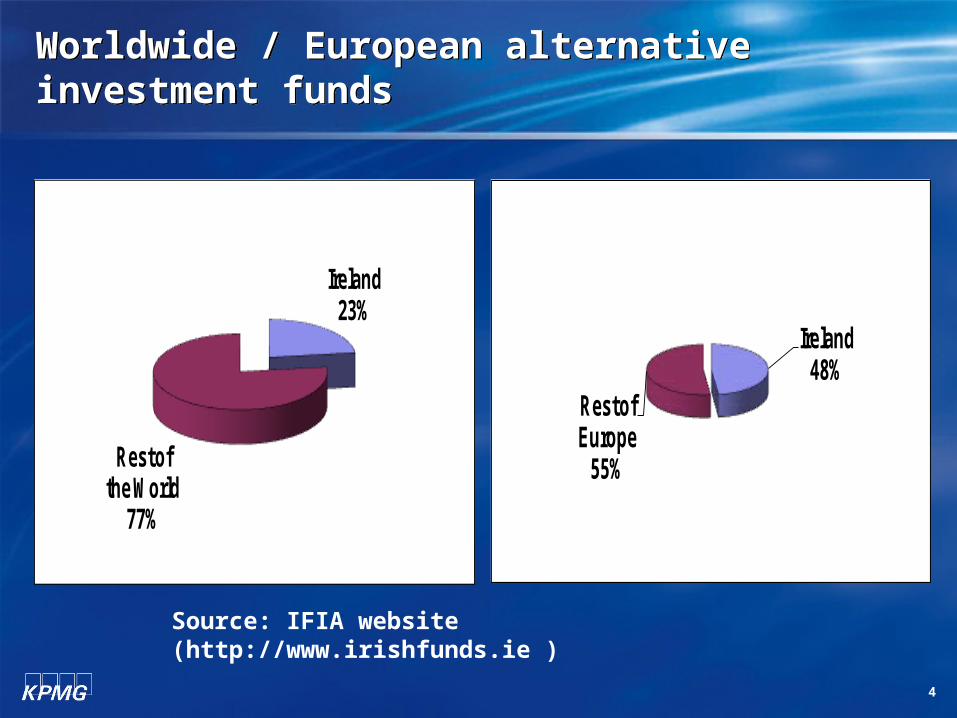

Worldwide / European alternative investment fundsWorldwide / European alternative investment funds

Ireland23%

Rest of the World

77%

Ireland48%

Rest of Europe

55%

Source: IFIA website (http://www.irishfunds.ie )

5

Funds in IrelandFunds in Ireland

Number of funds administered – approx 10,000Number of funds administered – approx 10,000

Number of people employed in the Funds industry – Number of people employed in the Funds industry – approx 12,000approx 12,000

Largest hedge fund administration centre in the worldLargest hedge fund administration centre in the world

Largest number of stock exchange listed investment Largest number of stock exchange listed investment fundsfunds

Fastest growing European and UCITS administration Fastest growing European and UCITS administration centrecentre

6

Why Ireland?Why Ireland?

7

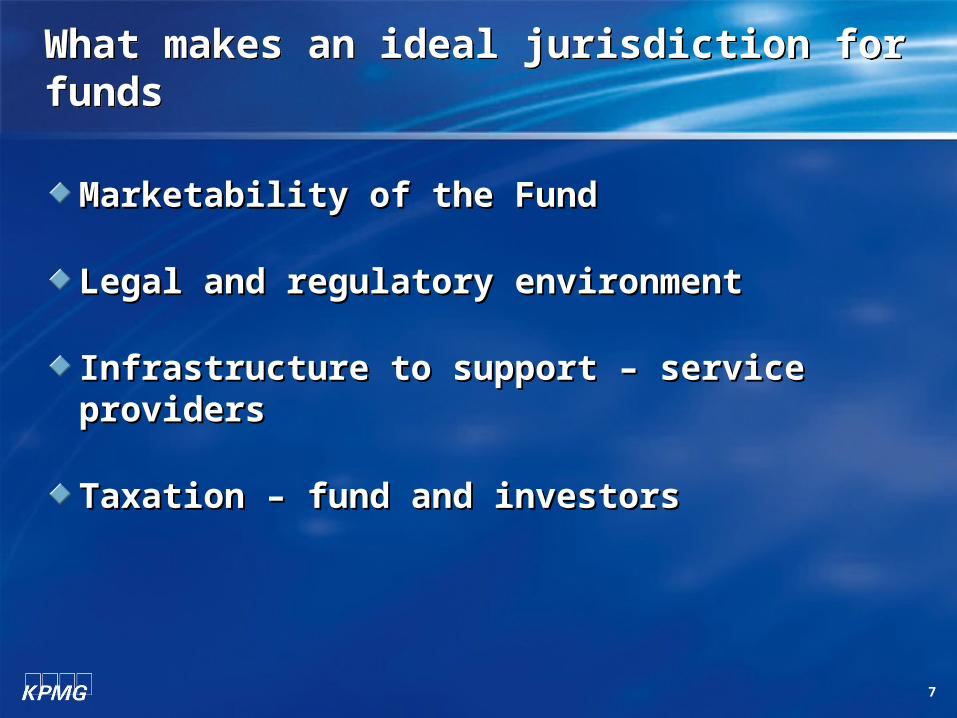

What makes an ideal jurisdiction for fundsWhat makes an ideal jurisdiction for funds

Marketability of the FundMarketability of the Fund

Legal and regulatory environmentLegal and regulatory environment

Infrastructure to support – service providersInfrastructure to support – service providers

Taxation – fund and investorsTaxation – fund and investors

8

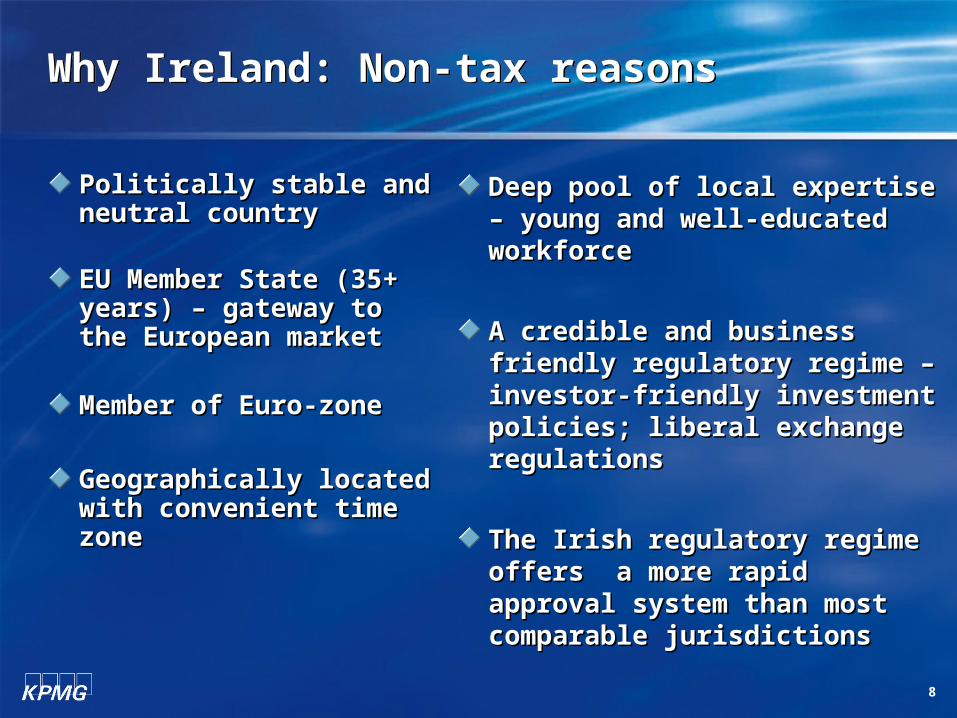

Why Ireland: Non-tax reasonsWhy Ireland: Non-tax reasons

Politically stable and neutral Politically stable and neutral countrycountry

EU Member State (35+ EU Member State (35+ years) – gateway to the years) – gateway to the European marketEuropean market

Member of Euro-zoneMember of Euro-zone

Geographically located with Geographically located with convenient time zoneconvenient time zone

Deep pool of local expertise – Deep pool of local expertise – young and well-educated workforceyoung and well-educated workforce

A credible and business friendly A credible and business friendly regulatory regime – investor-regulatory regime – investor-friendly investment policies; liberal friendly investment policies; liberal exchange regulationsexchange regulations

The Irish regulatory regime offers a The Irish regulatory regime offers a more rapid approval system than more rapid approval system than most comparable jurisdictionsmost comparable jurisdictions

9

Why Ireland: Non-tax reasonsWhy Ireland: Non-tax reasons

Ireland is the only English speaking country within the Euro-zone – Ireland is the only English speaking country within the Euro-zone – Is that important!Is that important!

10

Why Ireland: Tax reasonsWhy Ireland: Tax reasons

No Irish tax on income earned No Irish tax on income earned by Regulated Fundsby Regulated Funds

No Irish tax on distribution or No Irish tax on distribution or redemption payments made redemption payments made to investors who are non-Irish to investors who are non-Irish resident resident

No Irish stamp duty or capital No Irish stamp duty or capital duty on establishment of a duty on establishment of a collective investment fund or collective investment fund or on creation, transfer or selling on creation, transfer or selling of units or shares in a fund of units or shares in a fund

Most of the services provided Most of the services provided to a fund are exempt from to a fund are exempt from VAT (sales tax)VAT (sales tax)

Rich network of double tax Rich network of double tax treatiestreaties

In summary, a non-Irish resident does not suffer any Irish In summary, a non-Irish resident does not suffer any Irish tax on any income or capital received from an Irish Fundtax on any income or capital received from an Irish Fund

11

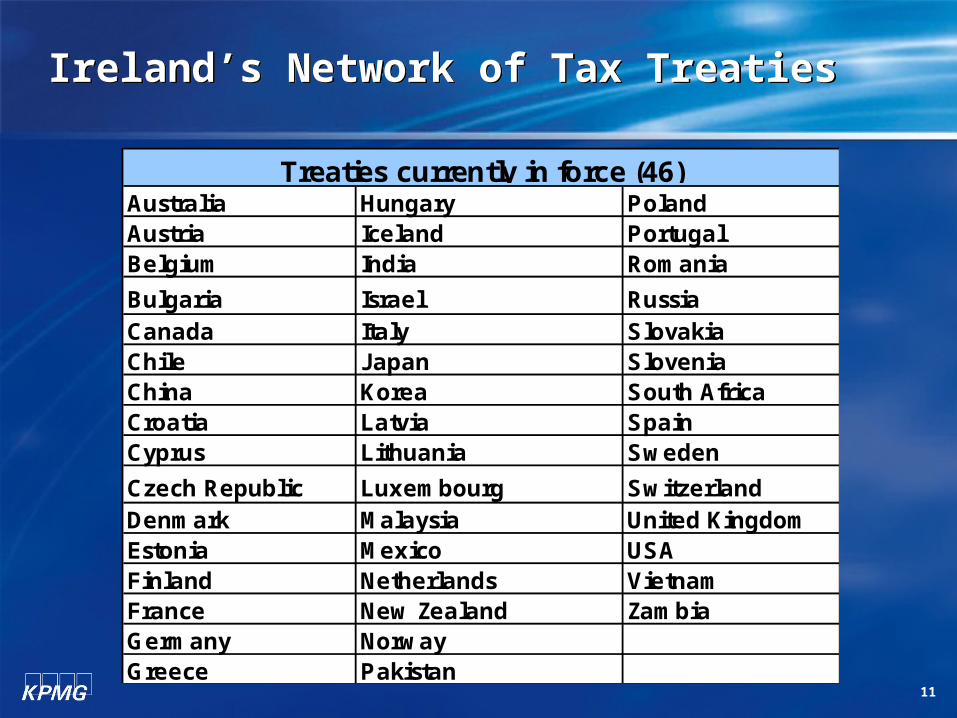

Ireland’s Network of Tax TreatiesIreland’s Network of Tax Treaties

Australia Hungary PolandAustria Iceland PortugalBelgium India Romania

Bulgaria Israel RussiaCanada Italy SlovakiaChile Japan SloveniaChina Korea South AfricaCroatia Latvia SpainCyprus Lithuania Sweden

Czech Republic Luxembourg SwitzerlandDenmark Malaysia United KingdomEstonia Mexico USAFinland Netherlands VietnamFrance New Zealand ZambiaGermany NorwayGreece Pakistan

Treaties currently in force (46)

12

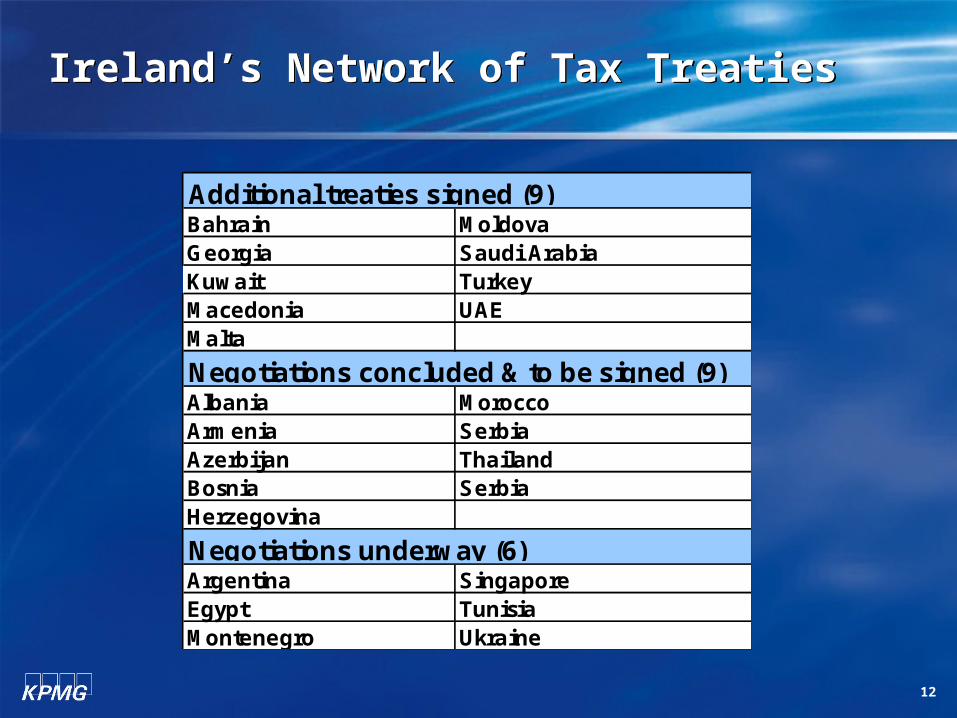

Ireland’s Network of Tax TreatiesIreland’s Network of Tax Treaties

Bahrain MoldovaGeorgia Saudi ArabiaKuwait TurkeyMacedonia UAEMalta

Albania MoroccoArmenia SerbiaAzerbijan ThailandBosnia SerbiaHerzegovina

Argentina SingaporeEgypt TunisiaMontenegro Ukraine

Additional treaties signed (9)

Negotiations concluded & to be signed (9)

Negotiations underway (6)

13

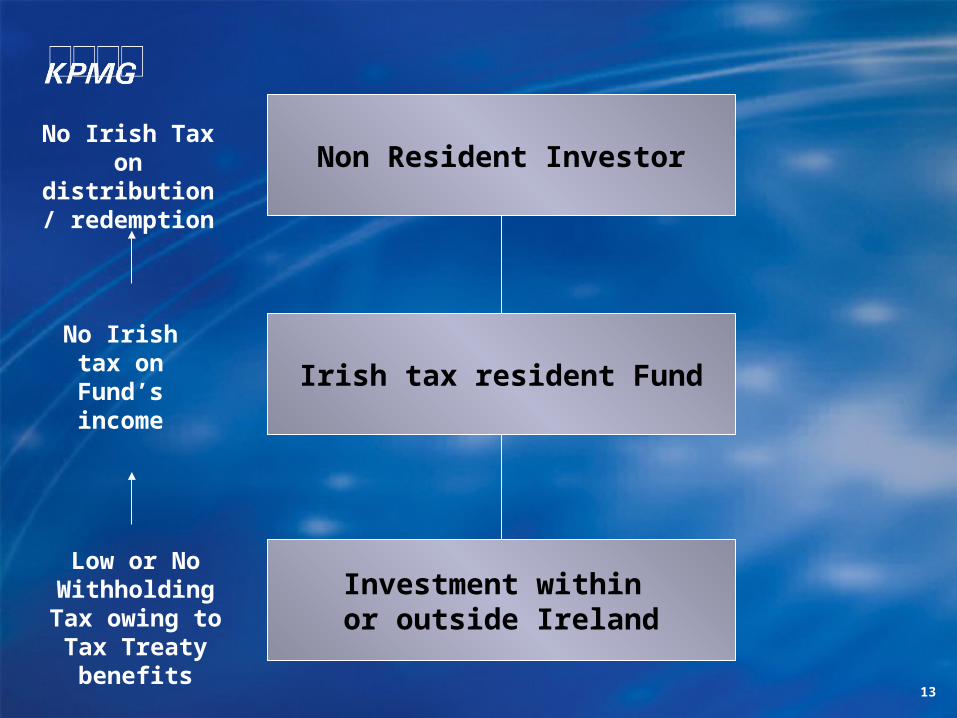

Non Resident Investor

Irish tax resident Fund

Investment within or outside Ireland

No Irish Tax on distribution / redemption

No Irish tax on Fund’s income

Low or No Withholding Tax

owing to Tax Treaty benefits

14

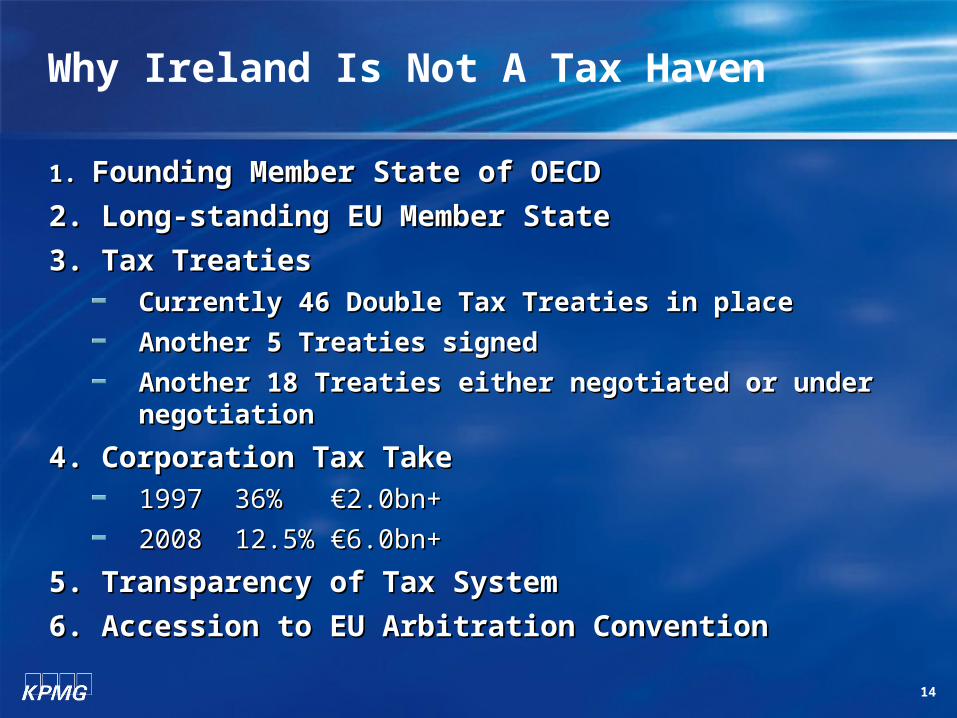

Why Ireland Is Not A Tax Haven

1. 1. Founding Member State of OECDFounding Member State of OECD

2. Long-standing EU Member State2. Long-standing EU Member State

3. Tax Treaties3. Tax Treaties

Currently 46 Double Tax Treaties in placeCurrently 46 Double Tax Treaties in place

Another 5 Treaties signedAnother 5 Treaties signed

Another 18 Treaties either negotiated or under negotiationAnother 18 Treaties either negotiated or under negotiation

4. Corporation Tax Take4. Corporation Tax Take

1997 1997 36%36% €2.0bn+€2.0bn+

20082008 12.5%12.5% €6.0bn+€6.0bn+

5. Transparency of Tax System5. Transparency of Tax System

6. Accession to EU Arbitration Convention6. Accession to EU Arbitration Convention

15

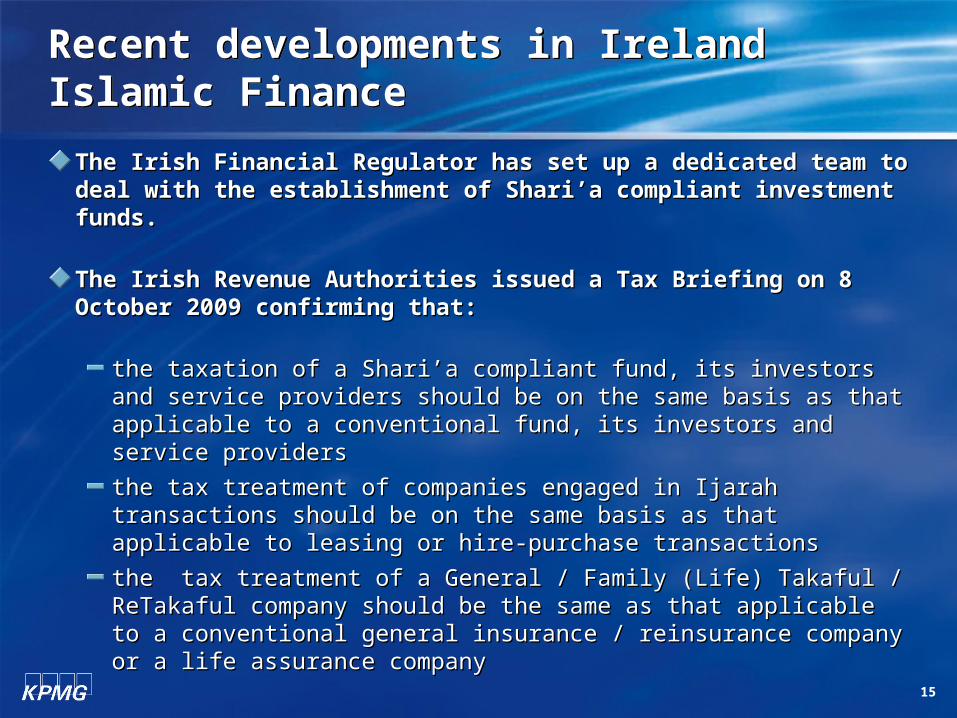

Recent developments in IrelandIslamic FinanceRecent developments in IrelandIslamic Finance

The Irish Financial Regulator has set up a dedicated team to deal The Irish Financial Regulator has set up a dedicated team to deal with the establishment of Shari’a compliant investment funds.with the establishment of Shari’a compliant investment funds.

The Irish Revenue Authorities issued a Tax Briefing on 8 October The Irish Revenue Authorities issued a Tax Briefing on 8 October 2009 confirming that:2009 confirming that:

the taxation of a Shari’a compliant fund, its investors and service the taxation of a Shari’a compliant fund, its investors and service providers should be on the same basis as that applicable to a providers should be on the same basis as that applicable to a conventional fund, its investors and service providersconventional fund, its investors and service providers

the tax treatment of companies engaged in Ijarah transactions the tax treatment of companies engaged in Ijarah transactions should be on the same basis as that applicable to leasing or hire-should be on the same basis as that applicable to leasing or hire-purchase transactionspurchase transactions

the tax treatment of a General / Family (Life) Takaful / ReTakaful the tax treatment of a General / Family (Life) Takaful / ReTakaful company should be the same as that applicable to a conventional company should be the same as that applicable to a conventional general insurance / reinsurance company or a life assurance general insurance / reinsurance company or a life assurance companycompany

16

The importance of the Tax BriefingThe importance of the Tax Briefing

From a fund’s perspective:From a fund’s perspective:

The fund should not be subject to any Irish tax. The fund should not be subject to any Irish tax.

No Irish tax should arise on distributions from the fund No Irish tax should arise on distributions from the fund to non resident investors. to non resident investors.

An Irish regulated fund can be marketed throughout the An Irish regulated fund can be marketed throughout the EU without requiring any further authorisations.EU without requiring any further authorisations.

17

The importance of the Tax BriefingThe importance of the Tax Briefing

From a leasing (Ijarah) company’s perspectiveFrom a leasing (Ijarah) company’s perspective

Ireland is considered an ideal location for international leasing, particularly aircraft Ireland is considered an ideal location for international leasing, particularly aircraft leasingleasing

As Ireland does not apply any withholding tax on outbound lease rentals, most Irish As Ireland does not apply any withholding tax on outbound lease rentals, most Irish tax treaties contain favourable provisions in respect of withholding taxes on lease tax treaties contain favourable provisions in respect of withholding taxes on lease rental payments (nil or reduced rate of withholding tax)rental payments (nil or reduced rate of withholding tax)

Taxable trading (business) income of the leasing company should be subject to tax Taxable trading (business) income of the leasing company should be subject to tax at 12.5%at 12.5%

The company should be entitled to tax depreciation at 12.5% p.a.The company should be entitled to tax depreciation at 12.5% p.a. on the cost of its on the cost of its plant & machinery (leased asset).plant & machinery (leased asset).

No Irish withholding tax is applied on dividend payments to a shareholder that is No Irish withholding tax is applied on dividend payments to a shareholder that is resident in an EU Member State or in a jurisdiction with which Ireland has concluded resident in an EU Member State or in a jurisdiction with which Ireland has concluded a double tax treatya double tax treaty

There are no Controlled Foreign Corporation (CFC) rules in Ireland. Moreover, There are no Controlled Foreign Corporation (CFC) rules in Ireland. Moreover, Ireland has a very limited transfer pricing regimeIreland has a very limited transfer pricing regime

18

The importance of the Tax BriefingThe importance of the Tax Briefing

From an insurance (Takaful) company’s perspectiveFrom an insurance (Takaful) company’s perspective

Ireland is becoming an increasingly popular location to locate Ireland is becoming an increasingly popular location to locate insurance and reinsurance companies insurance and reinsurance companies

An Irish regulated Takaful / ReTakaful company should be able to An Irish regulated Takaful / ReTakaful company should be able to sell insurance policies throughout the EU without seeking any sell insurance policies throughout the EU without seeking any further authorisations. further authorisations.

It should be possible for an Irish regulated Takaful / ReTakaful It should be possible for an Irish regulated Takaful / ReTakaful company to set up its presence in any EU Member State without company to set up its presence in any EU Member State without requiring any regulatory approvalsrequiring any regulatory approvals

Taxable trading (business) income of the Takaful / ReTakaful Taxable trading (business) income of the Takaful / ReTakaful company should be subject to tax at 12.5%company should be subject to tax at 12.5%

19

The information contained herein [or insert the title of the presentation, report, or talkbook] is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

Contact detailsContact details

Kashif JahangiriKashif Jahangiri

Director, Financial Services TaxDirector, Financial Services Tax

KPMG IrelandKPMG Ireland

+353 1 700 4060+353 1 700 [email protected]

www.kpmg.ie

http://www.kpmg.ie/industries/fs/islamicfinance/index.htm

© 2008 KPMG Ireland, the Irish member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in Ireland.