financial pacific - mobile remain a key opportunity, google (third party)

DESCRIPTION

Visit our website for more information: http://www.investingpacific.com/Financial Pacific: “The Right Wave to Invest”In today’s global economy it is important to be fully aware of the intricacies of international investments and the opportunities that these have to offer. Financial Pacific offers proven overseas investment opportunities.If you are interested in a reliable investment institution look no further because Financial Pacific provides: Wealth Management, Online Trading, Institutional Services and Corporate Finance. With cutting edge technology we are capable to support highly specialized derivatives instruments such as: CFDs, ETFs, CFDs on Commodities, ETCs, Futures and Options. In addition investors have access to a wide range of investment opportunities through: Structured Notes, Fixed Income, Reverse Convertibles, Preferred Stocks, and Institutional Hedge Funds.Fully regulated by Comisión Nacional de Valores de Panama since 2003; allow us to provide you with the necessary tools to take advantage of the global markets.TRANSCRIPT

UBS Investment Research

Morning Expresso - United States

Monday 27 June 2011

Global Equity Research

Americas

Equity Strategy

Market Comment

27 June 2011

www.ubs.com/investmentresearch

U.S. Equity Product Management

212-713-2400

Morning Expresso

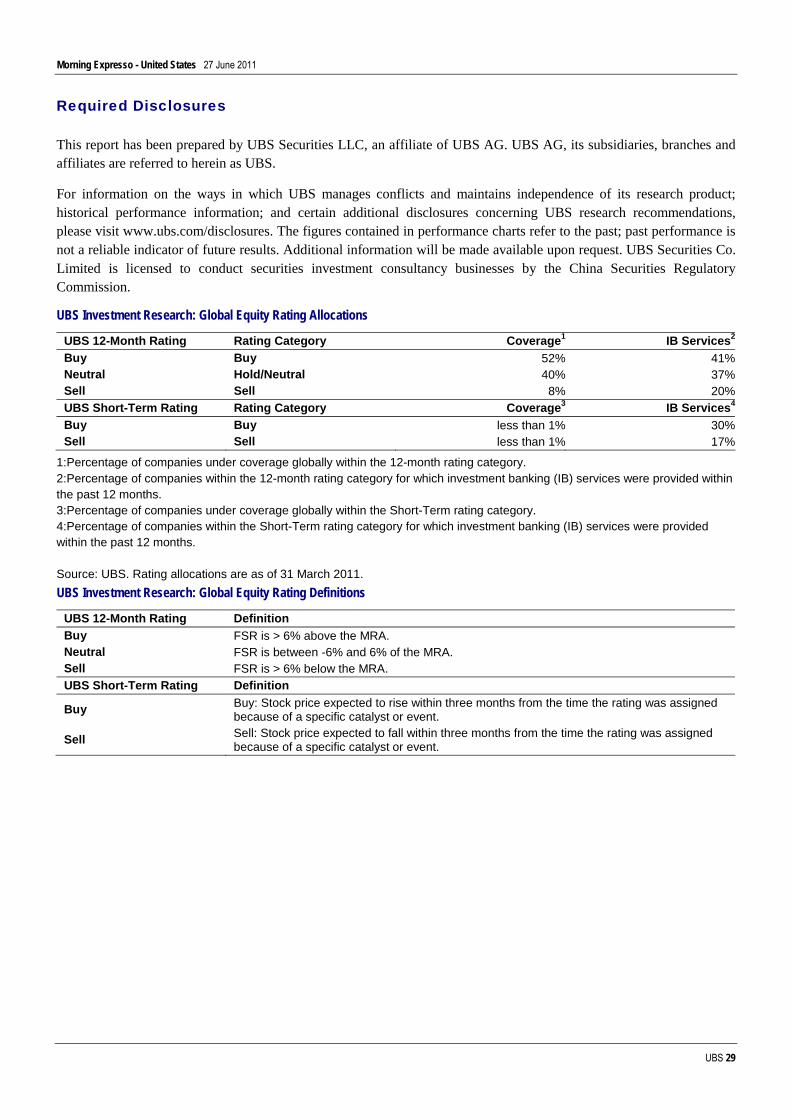

This report has been prepared by UBS Securities LLC ANALYST CERTIFICATION AND REQUIRED DISCLOSURES BEGIN ON PAGE 28. UBS does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

ab

Morning Expresso - United States 27 June 2011

UBS 2

Morning Meeting Agenda Key Call: Google Inc. Rating: Buy Target: US$765.00 Price: US$480.22 RIC: GOOG.O Prior: Unchanged Prior: Unchanged Mkt Cap: US$115bn BBG: GOOG US

Internet Services Analyst: Brian Pitz Tel: +1-212-713 9310

Positive on Key Call GOOG; Reiterate Buy Stock remains under pressure, despite the positive fundamentals While the FTC specter has been a 2011 overhang, we believe near-term

weakness reflects pressure from the (mid-May) Panda update -- while improving relevancy and the user experience over time (deemphasizing sites that solely aggregate content), the changes may pressure some near-term AdSense Network revenue. Note, Google makes constant refinements to the listing / ranking process, and the most recent (Jun 16) ‘Panda 2.2’ update has seen some affiliates recoup traffic.

Our proprietary Product Image Ad data shows accelerating growth Our proprietary analysis of 100K+ commercial keywords (p. 3-5) indicates that 19% of all search results had a Product Image Ad; significant growth from 10-11% in the previous 3-4 qtrs. We believe the format has 40-50% higher click-thru rates vs. text ads (and they are CPA-based); the effect is similar to increasing ARPU.

Mobile remain a key opportunity, while search innovation continues… Mobile search traffic is up 5x in the past two years, a similar trajectory to the early days of the desktop. AdMob now sees ~2.7B+ mobile ad requests / day, up from ~2B in Jan. Our proprietary data suggests volume at AdMob is on track to grow ~120% Y/Y in 2011 ( p. 6-7). Android is seeing 400K+ activations daily, up from 300K in Dec, making it the #1 OS with 34% share. Also, GOOG recently unveiled positive innovations, such as Instant Pages, which saves ~2-5 secs / search by pre-fetching data from top results, rendering sites nearly instantaneously when clicked.

Valuation: UBS 2012 est PE (ex-cash) of ~9x an attractive entry point Our $765 PT is based on our DCF (12% WACC, 3.5% LTGR). Disclosure: Options, structured derivative products and futures are not suitable for all investors, and trading in these instruments is considered risky

and may be appropriate only for sophisticated investors. Past performance is not necessarily indicative of future results. Various theoretical explanations of the risks associated with these instruments have been published. Prior to buying or selling an option, and for the complete risks relating to options, you must receive a copy of "The Characteristics and Risks of Standardized Options." You may read the document at http://www.optionsclearing.com/about/publications/character-risks.jsp #or ask your salesperson for a copy.

Source: The content presented above reflects a front page summary of UBS Research content, UBS estimates based on a share price of US$480.22 on 26 Jun 2011 19:24 EDT

Endo Rating: Buy Target: US$50.00 Price: US$38.63 RIC: ENDP.O Prior: Unchanged Prior: Unchanged Mkt Cap: US$4.49bn BBG: ENDP US

Pharmaceuticals Analyst: Marc Goodman Tel: +1-212-713 1342

Why Endo is Our Top 2H11 Pick What’s new? We detail key catalysts and why Endo is our top 2H11 pick We have been increasingly positive on Endo over the past yr as mgt. has

continued to successfully diversify the business away from Lidoderm (now 25% of 2012E revenue). We see the approval of Opana TRF (12/13/2011 PDUFA), a positive claim construction ruling on Lidoderm (potentially Aug.), low expectations around Axomadol PIIb data (mid-year) and the early closing (and thus higher guidance) and continued execution of the AMS acquisition as positive upcoming catalysts.

Our takeaway: AMS is a strong deal; Lidoderm claim construction key Our deep dive of AMS (inside) suggests that it is a top medtech asset, with best-in-class products and market share (~80% or higher) to back it up. We have raised our 2011E EPS by $0.08 to account for the early closing. We believe 5-6% growth is conservative and anything higher is upside to our model. On Lidoderm, our lawyers expect Endo will win the key claim at issue and thus ultimately the case.

Thoughts on the stock: Under-appreciation creates opportunity With many investors seeing either risk (Lidoderm) or remaining skeptical of the new unfamiliar medtech assets, our DCF suggests the stock is implying a -9% terminal growth rate. We believe as mgt. continues to execute on the base biz, investors take the time to become familiar with key assets such as AMS and risks (e.g., Lidoderm, Opana TRF approval) are overcome, there will be significant multiple expansion in ENDP driving shares higher into next year.

Valuation: We maintain our Buy rating and PT of $50 We apply a 9x P/E multiple to our 2012E EPS of $5.60. Source: The content presented above reflects a front page summary of UBS Research content, UBS estimates based on a share price of US$38.63 on 24 Jun 2011 19:40 EDT

Apollo Group Rating: Neutral Target: US$42.00 Price: US$42.46 RIC: APOL.O Prior: Unchanged Prior: Unchanged Mkt Cap: US$6.26bn BBG: APOL US

Consumer Services Analyst: Ariel Sokol Tel: +1-212-713 8450

Q3 Preview: Very Cautious As 4Q Starts Guidance Could Disappoint Earnings on Thursday; Expecting Q3 EPS beat but weak starts the issue Expecting Q3 EPS beat (UBS $1.41 vs. consensus $1.34). However, we

believe Q4 starts guidance could fall below investor estimates of a 25-30% YoY decline (UBS: down 36% with further downside risk). In our opinion, Q4 starts guidance is more meaningful to investors because it provides insight as to the 1) inflection point of future new start growth (management guided to some point in 2012); and 2) magnitude of 2013 EPS decline (consensus $3.07 vs. UBS $2.78). 3Q11 results June 30th AMC. CC 5PM ET (877-292-6888 code: 71264066).

Industry trends deteriorating; Further company challenges as well We think the Street assumes easier YoY comps in 4Q11 (starts down 10% 4Q10 vs. up 8% 3Q10), but does not appreciate deteriorating industry trends. Stakeholders suggested to us that industry start trends remain weak, and have in some cases worsened over the past several months (driven by increased competition and changing consumer behaviour). Compensation plan could weigh on enrollment counsellor productivity, while compliance with 90/10 potentially limits associate starts.

Sell July $44 call, consider buying July $42-$38 put spread Options imply 9% earnings reaction vs. UBS view of down 5-10%. Consider selling July $44 call and also buying July $42/$38 put spread ($1.97/$0.65, respectively).

Valuation: Maintain Neutral rating with a $42 price target We base our valuation by applying a 15x multiple to our FY13 estimated EPS. Source: The content presented above reflects a front page summary of UBS Research content, UBS estimates based on a share price of US$42.46 on 23 Jun 2011 19:43 EDT

Morning Expresso - United States 27 June 2011

UBS 3

US Brokers and Universal Banks

Diversified Financial Analyst: William Tanona, CFA Tel: +1-212-713 2325

Agreement on Moderate SIFI Buffer Basel Committee announces SIFI buffer of 100 to 250 bps The Basel Committee announced Saturday that the capital buffer for SIFIs

(“Systemically Important Financial Institutions”) will range from 100 to 250 bps (an additional 100 bps could be applied to banks that materially increase their global systemic importance). According to press reports, the buffer will apply to up to 8 US banks and as many as 30 banks globally.

Requirements are largely in line with our expectations We view this announcement positively, as it relieves fears over more severe requirements. We believe the additional 100 bps surcharge may have been included to satisfy regulators who were pressing for higher requirements, and we expect the effectiveness of such an additional buffer will be dependent upon the details of how it will be enforced.

Building additional capital takes time, but implementation is gradual The capital requirements will be phased in along with Basel III requirements, becoming fully effective in Jan. 2019. We estimate that adding 1% point to Tier 1 common ratios (on a Basel III basis) requires the retention of nearly a year of earnings for companies in our coverage (88% of 2012 estimates on average).

Sector is attractive, see significant upside potential over next few years While the sector is not without its challenges, we believe the stocks have compelling risk/reward tradeoffs and we see significant upside in the group longer-term as we expect improving results to drive higher book value growth and an improvement in sector valuations. The group trades at 0.9x TBV, which we view as attractive given the potential to generate 13% ROTE, on average, in 2012.

Notes:

Source: The content presented above reflects a front page summary of UBS Research content, UBS commentary as at 26 June 2011

Hansen Natural Rating: Buy Target: US$90.00 Price: US$77.96 RIC: HANS.O Prior: Unchanged Prior: US$75.00 Mkt Cap: US$7.30bn BBG: HANS US

Soft Drinks Analyst: Kaumil S. Gajrawala Tel: +1-212-713 9318

Still See Upside Raising Price Target and Longer-Term Estimates on Margin Benefits We are raising our price target to $90 (from $75), or 24.5x our new FY’12

EPS estimate of $3.66 (from $3.57). Given Hansen’s margin performance in the face of previous adverse commodity environment, and with no large sponsorship deals in the immediate future, we believe the company’s margins are not in significant jeopardy. We are reducing our 2011 gross margin erosion estimate from 160bps to 80bps.

Opportunities Being Overlooked or Underappreciated In this note we highlight five areas of potential upside that seem to be underappreciated by the marketplace: 1) US is far from a mature market, with distribution opportunities and new product sales; 2) cost inflation concerns seem overstated as company margins have held in similar inflationary periods; 3) Hansen’s growth has come without improvements to their key demographics; 4) we estimate a more efficient capital structure could add immediate accretion of $0.21 to 2011E EPS; and 5) despite the run, valuation does not look expensive, on par with KO at roughly 12.5x forward EV/EBITDA.

International Thesis Remains Intact While not the focus of this note, we still believe the Int’l rollout is progressing well (reported +92.6% for 1Q), and are estimating 40% growth for the remainder of 2011. This growth implies Monster gains 1pp of share in its Int’l markets in ‘11.

Valuation: Increasing Price Target to $90; Reiterate Buy We are increasing our price target to $90 from $75. Our price target is derived from 15.0x our ‘12 EBITDA estimate of $526m, and is supported by our DCF analysis.

Source: The content presented above reflects a front page summary of UBS Research content, UBS estimates based on a share price of US$77.96 on 24 Jun 2011 16:13 EDT

Option Strategy: Lilly (Eli) & Co.

Strategist: Mitchell S. Revsine Tel: +1-212-713 1416

Not Expecting Much From Analyst Day Shares may lose ground without significant announcement on 6/30 Analyst Marc Goodman wrote in his 6/2 note: Over the last 2 months, we

believe LLY has run in part due to anticipation of an analyst day announcement such as a significant cut to R&D or change in M&A strategy. We do not believe there will be any change announced and expect the CEO to reiterate the current strategy of R&D focus to replace patent losses. Without such an announcement or change in strategic focus, we would expect the stock to give back some of the recent run-up.

Focus on July maturity as longer-term bearish positioning poses risks While we expect management to reiterate their current strategy on 6/30 to the disappointment of some investors who believe value can be unlocked via strategic changes, it is possible over time that management changes their view. Additionally we note shares appear cheap, trading at 8.6x UBS 2011 EPS vs. 10x for the peer group. This valuation, along with a dividend yield of 5.3%, may not only limit downside but also help shares rally in the event of future positive catalysts.

Buy July $36-35 1x1 or 1x2 put spread for $0.21/$0.06 respectively Given the trade is intended to capture a modest stock decline (3-5%), investors may wish to reduce the cost of the $36/$35 put spread. Investors who may be comfortable getting long at $34.06 due to potential future catalysts, cheap valuation and dividend yield, can consider selling an additional $35 put (for $0.15, note $36 put costs $0.36). We do not advocate selling calls beyond July based on the upside risks outlined above. Prices as of 6/24 close, exclude fees/commissions, LLY 6/24 close price is $36.76.

Disclosure: Options, structured derivative products and futures are not suitable for all investors, and trading in these instruments is considered risky and may be appropriate only for sophisticated investors. Past performance is not necessarily indicative of future results. Various theoretical explanations of the risks associated with these instruments have been published. Prior to buying or selling an option, and for the complete risks relating to options, you must receive a copy of "The Characteristics and Risks of Standardized Options." You may read the document at http://www.optionsclearing.com/about/publications/character-risks.jsp or ask your salesperson for a copy.

Source: The content presented above reflects a front page summary of UBS Research content, UBS commentary as at 26 June 2011

Morning Expresso - United States 27 June 2011

UBS 4

Buying Growth — 2011 Update

Strategist: Thomas M. Doerflinger, Ph.D. Tel: +1-212-713 2540

Forty-four M&A Candidates Six Forces Driving an Increase in M&A Activity They have changed little since our Sept. 2010 report on this topic: 1) Firms’ organic growth is

impeded by a secular slowdown in nominal GDP, prompting them to “buy growth” via M&A. 2) Firms have strong balance sheets and ample cash. 3) Interest rates are low. 4) Corporate profitability is high by historical standards. 5) Stocks are inexpensive. 6) With capacity utilization still fairly low, it often makes more sense to buy than build.

Who’s Next? We Ask the Analysts We asked UBS U.S. equity analysts which companies were plausible candidates for acquisition, as well as the likely buyers and the rationale for the deal. The results of our query are shown in Tables 1 and 3. Of the 55 stocks featured in our previous two reports on M&A, five have already been acquired and a number of other deals were in line with UBS forecasts.

M&A Is Bullish for Small and Mid-Cap Stocks The median market cap of the 44 acquisition candidates is $2.8 billion, and 30 have market caps of less than $5 billion. With many large firms “buying growth” in the stock market, deal activity should support the valuations of small and mid-cap stocks over the next few years.

List of forty-four M&A candidates Based on discussions with our analysts, we’ve updated our list of M&A candidates to now include forty-four names.

Notes:

Source: The content presented above reflects a front page summary of UBS Research content, UBS commentary as at 27 June 2011

US Daily Economic Comment

Economist: Maury N. Harris Tel: +1-212-713 2472

Decent ISM and jump in PHSI forecast Preview: Slower May consumption, moderate price increases, Dallas Fed (1) Consumption likely slowed in May (UBSe 0.0%, cons 0.1%),

dragged down by the auto component, while income probably rose solidly (UBSe 0.3%, cons 0.4%). We forecast a 0.2% rise in core PCE prices (cons 0.2%). A 0.3%m/m reading is possible, given the uptick in financial services prices that was reported in Q1 GDP revisions. (2) The Dallas Fed’s manufacturing survey for June will be released.

The week ahead: ISM est 52.5, pending regional reports. PHSI to jump. The manufacturing ISM index for June will be the major focus. We expect a modest decline to 52.5 from 53.5. Regional manufacturing measures fell to relatively lower levels but have been understating strength for some time. Actual output data through May have not suggested the same degree of deterioration. However, regional surveys reported ahead of the ISM may give reason to alter our forecast. Consumer confidence measures (Jun) probably rose marginally to still low levels. Last week’s housing data hinted at stabilization, and we expect a continuation of that theme, with a surge in the pending home sales index (May) and only a slim decline in SP/CS home prices (Apr).

Review: Capex re-acceleration in May, Q1 GDP little revised (1) Durable goods orders rose 1.9%m/m in May (cons & UBSe 1.5%, after -2.7%). Details were strong: Apr orders were generally revised up, and all broad categories of orders improved in May. Orders for nondefense capital goods ex air (capex) jumped 1.6% after -0.8%. This was a solid report, indicating resilience. Capex orders have risen at an 18.1% annual rate so far in Q2, accelerating from a 0.9% pace in Q1, and shipments have picked up to a 7.5% pace from +3.9%. Durables inventories (+1.2%m/m) continued to rise, which may, at least temporarily, assuage fears of an inventory correction. (2) Real GDP growth was revised up minimally to a 1.9% annual rate from 1.8% pace.

Notes:

Source: The content presented above reflects a front page summary of UBS Research content, UBS commentary as at 24 June 2011

Morning Expresso - United States 27 June 2011

UBS 5

MACRO AND STRATEGY RESEARCH

UBS Client Flow Watch

Strategist: Thomas M. Doerflinger, Ph.D. Tel: +1-212-713 2540

US clients net selling US Client Flow: Still net selling domestic and foreign equities Both US long-only and hedge funds reduced their net selling of US equities, but

overall, US clients continue to be net sellers. Only US corporate clients are net buying. Overseas, US hedge funds were the only client segment net selling, counterbalancing increased net buying by long-only funds, intermediaries, and corporate clients (Table 6).

Sector details of Client Flow: Turning net buyers of tech Both US and foreign clients turned net buyers of US technology. US clients turned net buyers of telecoms both domestically and overseas.

Foreign Client Flow: Sector sea change Foreign clients went from net sellers to net buyers in US materials, energy, healthcare, industrials, and technology and from net buyers to net sellers in US telecoms and utilities.

Source: The content presented above reflects a front page summary of UBS Research content, UBS commentary as at 24 June 2011

Macro Keys

Economist: Larry Hatheway Tel: +44-20-7568 4053 Why profits may be the longest surprise

The next few weeks are filled with key dates. On June 28 or possibly June 30, the Greek parliament will vote on the latest austerity package. Although we expect parliament will approve, recent political defections suggest an uncomfortably close outcome. On Friday July 1 the focus will be on the US manufacturing ISM report, where our US economists expect a further decline to 52.5 from 53.5. The following Friday (July 8) brings the US June employment report. If private sector payrolls don’t rebound from May’s anaemic 83K gain, investors are likely to be unnerved about the prospect of a more prolonged ‘soft patch’, if not outright stagnation. Lastly, on July 12 the US Q2 earnings season unofficially kicks off.

Regular readers will know that we have adopted a cautious tactical stance on markets. We remain wary of ‘buying dips’, given the considerable uncertainties about Greece and the incoming macroeconomic data.

But our near-term caution sits uncomfortably with our more constructive view on risk assets—and in particular global equities—over longer investment horizons. Valuations are one reason. The other is corporate earnings.

The latter may come as a surprise, given that earnings have already posted strong gains over the past two years and many observers are calling for a peaking of corporate profit margins. If that is right, positive earnings surprises will be harder to achieve. Also, if history is any guide, when margins peak, they roll over quickly and begin to decline.

All of which brings us to the five most dangerous words in investing—this time may be different. To see why, look at the chart on the following page. It plots US profit share in GDP on the right-hand axis and the ‘employment gap’ on the left-hand

axis. The ‘employment gap’ is simply the difference between the US natural rate of unemployment and the actual rate of unemployment. It measures, in other words cyclical slack in the US labor market. The more negative the gap, the higher the rate of cyclical joblessness.

It is pretty clear from the two lines that as the observed unemployment rate converges on the natural rate, profits rise as a share of GDP. But as soon as the observed unemployment rate falls below the natural rate (the ‘employment gap’ turns positive), profit share in GDP peaks and starts to decline.

The reasoning is pretty simple. Early in recoveries, when there is plenty of slack in the labour market, profits rise faster than sales (margins expand), as firms enjoy rising revenues without corresponding large increases in costs. In short, early in recoveries the benefits of rising cyclical productivity flow disproportionately to the bottom line.

Source: The content presented above reflects a front page summary of UBS Research content, UBS commentary as at 27 June 2011

Global Emerging Markets Fund Flows

Strategist: Nicholas Smithie Tel: +1-212-713 8679

Outflows from GEM continue Selling worsens in EMEA, LatAm Total GEM funds experienced net outflows of approximately $144 million for the four weeks ending 22nd June

2011. Three of the past four weeks exhibited net selling. These outflows were driven by the withdrawal of $251 million from EMEA and another $96 million from LatAm. Dedicated GEM funds saw inflow of $154mn. Asia ex JP also saw inflows, although small at $50 million.

ETF flows were positive Despite net outflows, ETF flows were actually positive on a 4-WMA basis. ETFs saw inflows of $136 million compared to outflows of $280 million in Non-ETF flows. ETF flow typically makes up 40% of total flow in this dataset.

Money flows out from Peru, gain for Taiwan and Mexico We also look at the biggest movers within the geographical focused funds. The top five destinations for inflows over the past week (as a percent of AUM) were Taiwan, Mexico, Egypt, Philippines and GEM. The biggest net losers of funds were Peru, South Africa, Thailand, Chile and Russia.

Net selling year to date compared to strong inflows last year Total GEM fund flows year to date amount to a withdrawal of $9.0 billion of funds. This compares to total inflows of $84.1 billion into GEM in 2010. On a cumulative basis over $160bn has flowed into GEM funds since January 2006.

Notes: Source: The content presented above reflects a front page summary of UBS Research content, UBS commentary as at 24 June 2011

Morning Expresso - United States 27 June 2011

UBS 6

US Economic Perspectives

Economist: Maury N. Harris Tel: +1-212-713 2472

A Durable(s) Recovery? Goodbye QE The FOMC put an end to QE2 and, with disinflationary pressures having faded, appeared unlikely to engage in further large scale asset

purchases. H1 growth has been disappointing, but the FOMC continues to expect re-acceleration in H2. Higher central tendency forecasts for both unemployment and inflation may complicate the Fed’s policymaking.

Oil: A sheen of support Energy prices weighed on activity earlier this year, and the recent decline in oil prices is a welcome respite. Still, oil prices remain above the $85/bbl we have been expecting for 2011; the decline does not warrant a change to our growth outlook.

The past week The durable goods report indicated strong capex orders so far in Q2, notwithstanding the recent softening in manufacturing surveys. Housing data hinted at a trough in prices and sales. Q1 real GDP growth was revised up minimally. The CBO estimated further deterioration in the long-term Federal fiscal outlook. Separately, negotiations about the budget and debt ceiling stalled.

The week ahead The manufacturing ISM index for June will be the major focus. We expect a modest decline to 52.5 from 53.5. Regional manufacturing measures fell more sharply but have been underestimating strength for some time. Actual output data through May have not suggested the same degree of deterioration. Even so, a number of regional surveys will be reported ahead of the ISM and may give reason to alter our forecast. Consumer confidence measures (June) probably rose marginally, albeit to still low levels. Last week’s housing data hinted at stabilization, and we expect a continuation of that theme, with a surge in the pending home sales index (May) and only a slim decline in the SP/CS home price index (April). Construction spending probably was little changed in May.

Notes: Source: The content presented above reflects a front page summary of UBS Research content, UBS commentary as at 24 June 2011

Morning Expresso - United States 27 June 2011

UBS 7

GLOBAL SECTOR RESEARCH UBS Global I/O®: Cement

Building Materials Analyst: Gregor Kuglitsch Tel: +44-20-7567 3553

Consolidation and pricing resilience Input: local market analysis of major cement markets The recession has led to significant drops in utilisation in a number of countries, especially in

Western Europe and the US; more consolidated markets have shown considerably more resilient pricing and profitability than equivalent fragmented markets. Examples include a significantly better resilience in the UK and France compared to Italy, Spain and the US despite similar falls in utilisation levels. In our view, this is due to the level of consolidation and the major share of global players.

Output: China should benefit from consolidation unlike e.g. India China should see a significant benefit from consolidation as the number of players is decreasing significantly, increasing the market share of leading players and resulting in enhanced pricing power. India suffers from higher capacity additions from smaller players (outside the top-5) which have the potential to destabilise pricing balances and lower utilisation. South Africa, Morocco and Egypt are all seeing new entrants to the market place.

Stock implications As a result of the expected consolidation we favour the Chinese domestic players Anhui Conch (B, Rmb46.45); CNBM (B, HK$27) and Huaxin (B, Rmb48). We like the exposure to the consolidated markets in Indonesia (Gresik, B Rp11,300) and Taiwan (Asia Cement, B NT$42). As a result of likely further fragmentation we are more cautious on the Indian domestic players ACC (S, Rs 960), Ambuja (S, Rs130), India Cement (S, Rs86) and Ultratech (S, Rs1020) and PPC (Sell, RCnt 2500) in South Africa, From the global majors we favour HeidelbergCement (B, €58) over Cemex (N; P11.50), Lafarge (N, €50) and Holcim (N, CH70).

Notes: Source: The content presented above reflects a front page summary of UBS Research content, UBS commentary as at 27 June 2011

UBS Global I/O®: Technology patent battle

Technology Hardware & Equipment Analyst: Arthur Hsieh Tel: +886-2-8722 7348

Impact from Apple’s multi-touch patent Input: Apple received multi-touch patent The US Patent and Trademark office (USPTO) has granted Apple patent rights covering multi-touch

activity without affecting other contents on the display. The multi-touch function is implemented across different applications in the portable devices which could potentially give Apple more control on the ownership of the capacitive multi-touch interface as per media reports.

Increasing uncertainties, but too early to conclude We point out that not all applications may be using the same gesture or potentially not even violate the patent. Google and Microsoft may find work-around solutions in their mobile operating systems to avoid any infringement. Meanwhile, we believe most handsets OEMs have asked the major semiconductor vendors to provide patent indemnification when they designed touch-based user interface.

Collecting royalty is not Apple’s business model While investors are worried about Apple’s potential legal war against rivals, we believe the patents on multi-touch (and more generally) are more for defensive purposes. We believe Apple's core focus is to sell hardware with initiatives such as creating new services (iCloud) and content access (iTunes, App Store, iBook store, etc) to maintain its consumer loyalty and help drive further hardware sales.

Output: Buy TPK, Apple, Samsung, HTC, MMI, Atmel and Cypress With all potential uncertainties, we believe companies with high Apple smartphone exposure such as TPK should be relatively safe. We also remain positive on Apple, Samsung, HTC, Motorola Mobility Holding Inc (MMI), Atmel, and Cypress.

Notes:

Source: The content presented above reflects a front page summary of UBS Research content, UBS commentary as at 27 June 2011

Morning Expresso - United States 27 June 2011

UBS 8

BASIC MATERIALS LyondellBasell Rating: Buy Target: US$47.00 Price: US$37.58 RIC: LYB.N Prior: Unchanged Prior: Unchanged Mkt Cap: US$21.3bn BBG: LYB UN

Chemicals, Specialty Analyst: Andrew W. Cash Tel: +1-212-713 2210

Another round of FY EPS cuts Weakening spot market plastic is now expected to impact contract prices Weakness in the Asian market back in early May appeared in the US

spot market in mid May. With our most recent channel checks in hand we now expect weakness in the mainstream contract market. A leading consultant is reporting a 3 ¢ decline in the per pound price of LLDPE from 80 ¢ to 77 ¢, with another 3 ¢ drop in July. See Tables 1-3 for changes in key assumptions to our LYB model.

We currently forecast that ethylene margins soften the impact Given the sour sentiment within the plastic selling channel we are inclined to make a bigger cut to our margins. At the present time, however, the ethylene margins are holding up rather well despite the weakness in downstream derivative products. In fact, we have increased our 2Q11 EPS estimate to reflect this. However, for 3Q and 4Q the weakness in downstream products will likely over-power the potential benefit from an integrated and fairly flexible ethylene position.

Hiccup or longer term softness? In adjusting our EPS estimates as shown in the table to the right we are beginning to worry that a portion of the weakness the industry is seeing may be of a longer term nature. Consequently, we trimmed our 2012 EPS estimate.

Valuation: intrinsic value of $47 amidst uncertainty We are maintaining our $47 target price for LyondellBasell and our Buy rating. Our target is based on our 2-stage DCF model that assumes a WACC of 8.0% and a normal EBIT of $3.0 billion (including equity income) and normal EBITDA of $3.9 billion (including equity income). The EV/ normal EBITDA est. is about 6.5x.

Notes:

Source: The content presented above reflects a front page summary of UBS Research content, UBS estimates based on a share price of US$37.58 on 24 Jun 2011 19:40 EDT

Morning Expresso - United States 27 June 2011

UBS 9

COMMUNICATION Dice Holdings Rating: Neutral Target: US$14.00 Price: US$13.51 RIC: DHX.N Prior: Unchanged Prior: US$19.00 Mkt Cap: US$0.88bn BBG: DHX US

Internet Services Analyst: John Janedis, CFA Tel: +1-212-713 1064

Tweaking ‘12 Estimates Moderating Estimates in Outer Years We continue to favour Dice’s vertical business model and expect it to post reported EBITDA growth of over

40% in 2011. However, we are tempering our growth estimates for 2012+ largely to reflect a more normalized growth rate, particularly in the financed vertical and we are lowering our price target to $14.

Tweaking 2012 Growth Estimates We are modestly lowering our ‘12 growth expectations for each segment, and now forecast revenue growth of 16%/10%/21% for the Tech/Finance/Energy segments, respectively vs. previous estimates of 17%/16%/26%, respectively. Postings in the financials vertical have slowed recently and checks suggest 2012 recruitment budgets, while still strong, could slow somewhat due to a business slowdown for the category. Our ‘12 total EBITDA est is now $82.3M vs. our prior est of $85.3M.

2Q / 2011 Estimates Unchanged We are maintaining our 2Q estimates which are in line with guidance. We forecast revenue of $43.5M (FC: $43.6M, guidance $43.5M); adjusted EBITDA of $17.5M (FC: $17.2M, guidance $17M); and EPS of $0.11 (FC: $0.10, implied guidance $0.10). Our 2011 revenue/EBITDA/EPS ests are also unchanged and roughly in line with guidance at $177M (FC: $177M)/$69M (FC: $73M)/$0.47 (FC: $0.48).

Valuation: Lowering Price Target to $14 Our new $14 price target (was $19) is based on EPS and EBITDA multiples of 24x and 11.5x on our 2012 estimates, respectively. DHX is currently trading at 23.4x and 10.8x our ’12 EPS and EBITDA estimates. We maintain our Neutral rating.

Notes: Source: The content presented above reflects a front page summary of UBS Research content, UBS estimates based on a share price of US$13.51 on 24 Jun 2011 14:42 EDT

Janedis’ Media Matters

Entertainment Analyst: John Janedis, CFA Tel: +1-212 713 1064

Reading Gannett’s Tea Leaves What’s New? What the Job Cuts Mean to Estimates Last week’s announcement by GCI that it would be laying off ~700 employees (we assume

$40-$50M in cost savings) should not have come as a complete surprise (though the furloughs are) given rev. trends and our belief that management would like to keep margins flat in the publishing segment. As recent as early May, GCI’s 10Q indicated that total co. expenses would be flat this year. Given our expectation of softer revs, our model had already assumed a 2.2% decline in expenses for ’11. Our $2.06 ’11 EPS estimate is unchanged (FC: $2.20). Top picks: CBS, VIA, IPG.

Trend Watching in Print After being up 6% through June 17th, pages at the WSJ were down 16% last week, with 5 of 6 publishing days down on a y/y basis. Google remains the 2nd largest advertiser at NYT in June, with more pages than the entire nat’l auto category.

New York Times Linage -6% in June; WSJ -1% June, linage at NYT is -7% with nat’l auto -15%, dept. stores flat, telco -58%, banks/financials -7%, tech +219% (Google/Acer) and movies -17%. Classifieds are -12%, with h/w +17%, r/e -19%, and auto -9%. June linage at the WSJ is -1% on a same days basis (+17% comp) vs. May +8% (+7% comp), April flat (+22% comp).

Valuation Large-cap media is trading at 7.8x our FTM EBITDA vs. 7.7x last week; mid-cap is trading at 9.4x vs. 9.2x; advertising is trading at 6.8x vs. 6.7x; online recruitment is trading at 9.3x vs. 8.9x; and publishing is trading at 4.4x vs. 4.5x.

Notes: Source: The content presented above reflects a front page summary of UBS Research content, UBS commentary as at 27 June 2011

Morning Expresso - United States 27 June 2011

UBS 10

CONSUMER Philip Morris Int'l Rating: Neutral Target: US$66.50 Price: US$66.17 RIC: PM.N Prior: Unchanged Prior: Unchanged Mkt Cap: US$120bn BBG: PM US

Tobacco Analyst: Jonathan Leinster Tel: +44-20-7568 4982

PMI issues statement of claim PMI initiates potential legal action PMI has now served a notice of claim against the Australian government under a bilateral ‘free trade’ treaty with

Hong Kong, in the event that the government enacts legislation requiring ‘plain packaging’ for tobacco products in Australia. The major players in Australian market; BAT, Imperial and PMI have always stated that they would pursue legal action so this will come as no surprise.

Claims on expropriating intellectual property rights PMI (Australia) is a subsidiary of PMI (Asia) based in Hong Kong. The claims appear to centre on the bilateral free trade treaty between HK and Australia which prevents the expropriation of PMI (Asia) investment in Australia, in this case the brand rights. PMI claims those rights will be substantially reduced by the implementation of ‘plain’ packaging. PMI also believes the legislation contravenes treaty provisions covering ‘fair and equitable treatment’ and ‘full protection and security’, and international intellectual property right obligations.

Legislation still likely The Australian government is currently expected to introduce the Bill on ‘plain packaging’ on tobacco products to the Federal parliament in winter 2011 for enactment on 1st Jan 2012 and full implementation on 1st July 2012. The impact of such legislation is unknown since it has not been implemented elsewhere in the world.

Valuation; Price target (PT) $66.5 The PT is based on VCAM, and implies a CY’11 PE 14.5x and c6.9% CFY. Notes:

Source: The content presented above reflects a front page summary of UBS Research content, UBS estimates based on a share price of US$66.17 on 26 Jun 2011 19:24 BST

Food Images

Food Products Analyst: David Palmer Tel: +1-212-713 9315

Navigating Uneven Food Inflation Staying on Course: Retail Prices March Higher According to the latest scanner data for the 4 weeks ending 6/11, overall sales growth across our

packaged food names continues to remain solid (+2% YOY), even as volume growth has weakened a bit. Food stocks are up an average of 16% year-to-date, which makes sense given that we have reached the price pass-through point of the food inflation cycle. However, fortunes seem to be diverging. We continue to be constructive on names such as KFT, HNZ, CAG and K.

Kraft: Gaining Momentum We are raising Kraft’s FY11e EPS from $2.20 to $2.27 (+12% YOY, $2.23 cons) and our target price to $38 from $36 to reflect accelerating top line momentum, an improving relationship between pricing and input inflation, and a currency tailwind. In our view, given: 1) Kraft’s early pricing implementation, 2) recent cost relief in some major inputs, and 3) productivity/synergy savings, the company does not seem to be as vulnerable to a reacceleration in grain-based input inflation.

Diverging Fortunes in Food It appears that companies such as ConAgra (Buy) and General Mills (Neutral) are experiencing a second wave of inflation in grain-based inputs with less of a currency boost to earnings. Meanwhile, companies like Hershey (Neutral) or Kellogg’s (Buy) seem to have strong enough brand momentum to raising prices and meet/beat EPS targets. And others, such Heinz (Buy) or Kraft (Buy), may trail Kellogg and Hershey in US sales momentum, but have aggressive pricing, cooling input costs, international business exposure, and/or productivity savings to achieve EPS goals.

Notes: Source: The content presented above reflects a front page summary of UBS Research content, UBS commentary as at 27 June 2011

Morning Expresso - United States 27 June 2011

UBS 11

ENERGY Energy Sector

Oil Companies, Major Analyst: William A. Featherston Tel: +1-212-713 9701

NYT Shale Gas Allegations Seem Exaggerated NYT article makes harsh allegations toward shale gas E&P companies Citing industry emails, public statements & analyst reports, an NYT article

alleges that natural gas producers are 1) running a “Ponzi Scheme” as shale gas economics do not work; 2) overstating EURs and understating decline rates; & 3) exaggerating shale gas resource potential. While we agree shale gas economics are certainly challenged due to low prices, we believe the story is unduly harsh, and does not address the enormous supply growth in shale gas the last few years.

We believe the article’s allegations are overstated and misleading The article did not address how shale gas development has contributed to extraordinary production and reserve growth over the past few years. In addition, we highlight that 1) the material resource potential from the gas shales are supported by studies from several independent organizations; 2) proved reserve growth is audited by independent reservoir engineers; and 3) surge in M&A in US shale gas plays attest to viability of the resource potential.

Challenged shale gas economics at current gas price levels…nothing new The allegation that shale gas economics are challenged at current price levels is certainly not new and we largely agree. With perhaps the exception of the Marcellus & core Haynesville & Fayetteville, we believe prices of $5.50-$6.00/Mcfe are required to earn attractive returns. The decline in shale gas rig count (ex- Marcellus) & shift to oily plays over the last 18 months supports this view.

We prefer oil-weighted E&Ps: Discounting $5.05/MMBtu and mid-$70/Bbl Our top E&P picks are oil-weighted APC, NBL, OXY, & APA. Notes:

Source: The content presented above reflects a front page summary of UBS Research content, UBS commentary as at 27 June 2011

Targa Resources Part Rating: Buy Target: US$38.00 Price: US$34.16 RIC: NGLS.N Prior: Unchanged Prior: US$31.00 Mkt Cap: US$2.90bn BBG: NGLS US

Pipelines Analyst: Jeremy Tonet, CFA Tel: +1-212-713 4838

Boosting PT on Favorable Outlook Ability to capitalize on favorable dynamics drives bright outlook We believe Targa enjoys a stronger NGL asset base than many peer MLPs,

allowing the partnership to capitalize on a secular upswing in energy infrastructure development. Targa’s integrated suite of midstream services differentiates NGLS from many peers that cannot offer services after the natgas processing plant tailgate. Specifically, given the tightness in the fractionation market, The partnerships significant fractionation capacity in Mont Belvieu (and ability to expand) provides a key advantage over peers.

Robust organic growth pipeline augmented by opportunistic acquisitions Relative to NGLS’ ~$3bn market cap, we believe the partnership’s ~$600mm portfolio of expansion projects will drive above average distribution growth. In addition, we expect the partnership to acquire more complimentary assets on an opportunistic basis, further boosting our growth outlook.

Raising earnings estimates and distribution growth expectations Based on our expectations that NGLS’ suite of midstream services positions the partnership to capitalize on energy infrastructure development needs, we are increasing our 2011/2012 EPU estimates to $1.60/$1.74, from $1.46/$1.41. Additionally, we now anticipate upper single digit distribution growth over the next two years, versus our prior expectations of low to mid single digit growth.

Valuation: Raising Price Target to $38 from $31 Increasing our growth assumptions and slightly reducing our discount rate due to higher coverage is driving our DDM derived price target to $38 from $31.

Notes:

Source: The content presented above reflects a front page summary of UBS Research content, UBS estimates based on a share price of US$34.16 on 24 Jun 2011 16:13 EDT

Morning Expresso - United States 27 June 2011

UBS 12

HEALTHCARE Abbott Laboratories Rating: Buy Target: US$59.00 Price: US$51.75 RIC: ABT.N Prior: Unchanged Prior: Unchanged Mkt Cap: US$80.0bn BBG: ABT US

Medical Supplies Analyst: Rajeev Jashnani, CFA Tel: +1-212-713 9127

Bardoxolone progressing to Phase 3 52-wk data confirms positive signal observed in earlier data Bardoxolone [B], which recently entered ph3 for chronic kidney disease, may be

ABT's most important pipeline drug. 52-wk ph2 data (n=227) was presented at the ERA-EDTA conference & published in NEJM on 6/24. Similar to previous data, 52-wk data showed significant improvements in eGFR vs. placebo (eGFR is a marker for kidney function). The event-driven ph3 will assess [B] w/ respect to hard clinical outcomes (onset of end-stage renal disease or cardiovascular death); data is expected in ‘13 implying ‘14-‘15 launch.

Overall, we view the 52-wk data as encouraging (Tables 1-3) eGFR improvement differentiates [B] from other CKD drugs, which only slow progression. In add’n to eGFR, improvement in other biomarkers were also observed (BUN), however, [B]-related increase in proteinuria remains an unanswered question (proteinuria is a strong prognostic indicator for CKD progression / CV events). Side effects appeared manageable. Ph2 outcomes (eg ESRD progression) were not presented, but may not be meaningful as most pts had relatively early stage 3 disease (1,600-pt ph3 will enroll sicker pts).

Market opportunity is very large if improved outcomes are shown in ph3 ABT licensed ex-US rights to [B] from Reata in 2H10 for $450M (mix of upfront + "near" upfront pymts & minority equity stake). The unmet medical need in CKD is highly substantial. ABT estimates >800k stage 4 CKD pts in W. Europe; modest 10% penetration into this pop'n yields a ≥$800M opportunity. Pricing is likely dependent on avoidance of dialysis as shown in ph3; dialysis an extremely expensive therapy associated with poor quality of life. Notably, ABT has experience in CKD through Zemplar & also has atresentan in ph2b development for CKD.

Valuation – reiterate Buy rating & $59 price target On ‘12 estimates, ABT trades at 10.4x EPS & 11% FCF yield. Our price target is derived through DCF.

Notes: Source: The content presented above reflects a front page summary of UBS Research content, UBS estimates based on a share price of US$51.75 on 24 Jun 2011 19:40 EDT

Bristol-Myers Rating: Neutral Target: US$30.00 Price: US$28.93 RIC: BMY.N Prior: Unchanged Prior: US$28.00 Mkt Cap: US$49.5bn BBG: BMY US

Pharmaceuticals Analyst: Marc Goodman Tel: +1-212-713 1342

Increasing PT and Apixaban Forecast What’s new? We have re-evaluated our Apixaban ests. post ARISTOTLE In our concurrently published note, “Apixaban Rising” we have increased

our WW forecasts for Apixaban based upon superior efficacy and safety data which Apixaban delivered versus Warfarin in the ARISTOTLE study announced on 6/22. We have built a WW patient-based model and have also conducted a survey of 25 physicians (15 cardiologists and 10 primary care) to gauge Apixaban’s uptake.

Our takeaway: Increasing WW Apixaban sales to $2.4B in 2015E We believe Apixaban can garner ~33% of the combined worldwide branded anticoagulation market (~$7.3B in est. market size) for Afib and VTE by 2015E, implying $2.4B ($2.2B risk-adj at 90%) in sales. By 2020E, we see the market growing to ~$15B with Apixaban having a 37% share. In the US, we estimate Apixaban will have ~34% share of a ~$4B 2015E market (rising to ~$8B by 2020E). See Table 1 for changes from our previous forecast.

Thoughts on the stock: Increasing PT to $30; Significant opportunity Prior to top line ARISTOTLE results, we believe consensus estimates for Apixaban were ~$1.2B in 2015E. Given the robust results, we would expect consensus to move higher throughout the summer. Our changes increase our 2015E EPS by $0.06 to $2.47 and our 2020E EPS by $0.57 to $3.43. Our 2011-2013E EPS remain unchanged as the Apixaban JV isn’t profitable until 2014E. We see the FDA panel on Dapa on 7/16 as the next key event for BMY until ESC.

Valuation: Increasing Price Target to $30 based on DCF analysis Our DCF analysis assumes a $20 for the base business and $10 for the pipeline. Source: The content presented above reflects a front page summary of UBS Research content, UBS estimates based on a share price of US$28.93 on 24 Jun 2011 19:40 EDT

Davita Rating: Buy Target: US$95.00 Price: US$84.39 RIC: DVA.N Prior: Unchanged Prior: Unchanged Mkt Cap: US$8.76bn BBG: DVA US

Healthcare Providers Analyst: Justin Lake, CFA Tel: +1-212-713 2765

FDA Releases Updated EPO Label Updated FDA label provides incremental color on EPO trajectory FDA released new EPO label which includes new Black Box warning and

dosing. That said, according to UBS biotech analyst Matt Roden, new label likely implies hemoglobin mean of ~11 g/dl (vs current 11.2 g/dL) indicating that impact on EPO dose is relatively minimal. Based on the dose-Hb dosing relationship, he estimates a qtr-gram Hb drop corresponds to ~7% lower dose, which he believes is unlikely to happen (we estimate each 1% EPO util decline = $0.03/0.5% to EPS for DVA ex price).

Next step is possible modification of QIP; potential LT AMGN contract Post FDA label, the next event here may be potential CMS modification to QIP (expected 2012). With regard to DVA-AMGN contracting, lack of clarity on FDA labeling until now likely represented the key obstacle to LT contract, with today’s release setting stage for return to typical multi-year contracts (vs more recent 6-month contract lengths). We would expect a multi-year contract to represent a positive to DVA as it would remove uncertainty & provide market with some price clarity.

UBS estimates left intact for DVA While updated FDA label may not be particularly impactful on EPO util, we see optionality here of flat-to-slightly down, w/clarity on EPO label potentially freeing DVA up for further dosing efficiencies w/regard to EPO than previously thought at Cap Markets Day. We leave our DVA estimates intact, and continue to model only modest EPO util declines in 2H’11 (-0.5% seq in Q3/Q4) and 2012 (-0.2% seq decline each qtr).

Valuation: Buy Rating, $95 Price Target Our $95 PT is based on target multiple of ~16x our FY’12 EPS estimate of $6.00. Source: The content presented above reflects a front page summary of UBS Research content, UBS estimates based on a share price of US$84.39 on 23 Jun 2011 19:43 EDT

Morning Expresso - United States 27 June 2011

UBS 13

Pfizer Rating: Buy Target: US$23.00 Price: US$20.08 RIC: PFE.N Prior: Unchanged Prior: Unchanged Mkt Cap: US$162bn BBG: PFE US

Pharmaceuticals Analyst: Marc Goodman Tel: +1-212-713 1342

Increasing Apixaban Forecast What’s new? We have re-evaluated our Apixaban ests. post ARISTOTLE In our concurrently published note, “Apixaban Rising” we have increased

our WW forecasts for Apixaban based upon superior efficacy and safety data which Apixaban delivered versus Warfarin in the ARISTOTLE study announced 6/22. We have built a WW patient based model and have also conducted a survey of 25 physicians (15 cardiologists and 10 primary care) to gauge Apixaban’s uptake.

Our takeaway: Increasing WW Apixaban sales to $2.4B in 2015E We believe Apixaban can garner ~33% of the combined worldwide branded anticoagulation market (~$7.3B in est. market size) for Afib and VTE by 2015E implying $2.4B ($2.2B risk-adj at 90%) in sales. By 2020E, we see the market growing to ~$15B with Apixaban having a 37% share. In the US, we estimate Apixaban will have ~34% share of a ~$4B 2015E market (rising to ~$8B by 2020E). See Table 9 for changes from our previous forecast.

Thoughts on the stock: Nice positive, but BMY more levered We are increasing our EPS forecasts by $0.06 to $2.62 in 2015E and by $0.08 to $3.76 in 2020E driven by higher Alliance Revs from the JV. The added Apixaban sales are worth ~$0.50 on a DCF basis. We still think PFE is undervalued based upon its strong cash flows and pipeline progress, including Apixaban, Tofacitinib, Crizotinib, Axitinib and Prevnar-13 adult. We expect regulatory approvals and communication around the strategic review in 2H to drive shares as well.

Valuation: We maintain our Buy rating and $23 PT based on our DCF The implied P/E multiple from our DCF is 10x our 2012E EPS of $2.26. Notes:

Source: The content presented above reflects a front page summary of UBS Research content, UBS estimates based on a share price of US$20.08 on 24 Jun 2011 19:40 EDT US Large Cap Pharmaceuticals

Pharmaceuticals Analyst: Marc Goodman Tel: +1-212-713 1342

Apixaban Rising What’s new? We publish our Factor Xa survey and market model We completed a survey of 25 physicians (15 cardiologists and 10 primary care)

to gauge the uptake of Pradaxa and potential market shares for Apixaban in different scenarios (superior safety, superior safety and efficacy, etc). Further, we have built both a patient and TRx-based market model for the Factor Xa market. We remain focused on detailed Apixaban data at ESC on Aug. 28 with specific interest in the details vs Warfarin and if Apixaban demonstrated a mortality benefit.

Key survey takeaways: Robust anticoagulation market & Apixaban share (1) Uptake of new agents is strong (65% of patients offered Pradaxa take it, with cost being biggest deterrent); (2) 1/3 of patients new to therapy start on Pradaxa; (3) ~15% of Afib patients are on Aspirin which physicians expect to switch to new agents; (4) Primary care physicians expect to keep more patients on Warfarin (~35%) versus cardiologists (~28%); (5) Physicians predict robust share for Apixaban in Afib (36% vs 27% for Warfarin, 25% for Pradaxa and 12% Xarelto).

Our takeaway: Increasing Apixaban 2015E sales to $2.4B We believe Apixaban can garner ~33% of the combined worldwide branded anticoagulation market (~$7.3B in est. market size) for Afib and VTE by 2015E implying $2.4B ($2.2B risk-adj at 90%) in sales. By 2020E, we see the market growing to ~$15B with Apixaban having a 37% share. In the US, we estimate Apixaban will have ~34% share of a ~$4B 2015E market (rising to ~$8B by 2020E) while J&J’s Xarelto will have ~24%, implying US 2015E sales of $975M. While we believe Apixaban will have greater 2015E share in Afib versus Xarelto (40% vs 19%), we believe Xarelto will take greater share in VTE (40% vs 15%).

Notes:

Source: The content presented above reflects a front page summary of UBS Research content, UBS commentary as at 26 June 2011

US Large Cap Pharmaceuticals

Pharmaceuticals Analyst: Marc Goodman Tel: +1-212-713 1342

More Dapa Details & Concerns at ADA What’s new? New Dapa data, incl. bladder & breast cancer imbalalnce At ADA, Bristol and AstraZeneca’s Dapagliflozin (Dapa) continued to

demonstrate robust efficacy (as previewed in the abstracts), but a new potentially concerning signal emerged. 9 out of 5,478 (0.16%) patients on Dapa were diagnosed with bladder cancer vs. 1/3,156 (0.03%) on control. However, 6/10 had blood in their urine at baseline and 5 patients were diagnosed within 1 yr from starting Dapa. Also, 9/2,223 (0.40%) women developed breast cancer vs 1/1,053 control women (0.09%). Importantly, all women were diagnosed within 1 year of starting Dapa. There was no imbalance in overall neoplasms (1.4% Dapa vs 1.3% control). Preclinical data from 2yr+ carcinogenicity studies with doses >1,000 mg/kg) did not demonstrate any signal of cancer and SGLT2 is not expressed in either the bladder or breast tissue. We expect this signal to be debated at panel.

Our takeaway: New risk for 7/19 panel, but data very mixed. Given the FDA’s safety concern (Actos, Victoza, Byetta), this signal will likely garner significant attention at panel. Nonetheless, the data presented thus far is supportive that this is just a numerical imbalance and not a signal. Specifically, (1) the fact that the tumors were diagnosed <1 year after initiation of therapy suggests it is very unlikely Dapa caused the tumors; (2) the lack of preclinical signal across ~38 different Dapa studies (Actos, Victoza and Byetta all have preclinical signals) makes causality harder to establish; (3) Dapa is highly selective for SGLT2 (poster 987-P) and SGLT2 is not expressed in the bladder or breast; (4) Dapa is a simple channel blocker, which to our knowledge, has never had a cancer associated risk. Nonetheless, we would expect this issue to raise investor skepticism around Dapa; however, with the panel less than a month away we will know FDA’s view soon.

Notes:

Source: The content presented above reflects a front page summary of UBS Research content, UBS commentary as at 27 June 2011

Morning Expresso - United States 27 June 2011

UBS 14

INDUSTRIALS U.S. Aerospace & Defense Playbook

Aerospace Analyst: David E. Strauss Tel: +1-212-713 6185

The Week Ahead What’s next for Aerospace and Defense? We will get May traffic data from IATA on Monday, which we expect to reflect mid-single digit growth given

relatively strong reports so far out of the regions. On Wednesday, we will be attending TDG’s NYC analyst day and will listen for any color on aftermarket trends during Q2 and McKechnie integration progress. SWHC will provide a read for ATK's Security & Sporting business when it reports its Q4 on Thursday. We should also get parked aircraft data early to mid-week and then used bizjets inventory data on Friday. We expect generally negative defense news flow over the near term given debt ceiling debate and as Congress marks up the FY12 appropriations bills.

Still prefer aero aftermarket Aero at a 14% premium to market is in line with similar point in prior up-cycles. We continue to favor aftermarket names over OE as we think increased utilization of out of warranty aircraft can still drive high single digit aftermarket growth in ‘11 despite high oil prices and recent capacity cuts. GR/COL/TDG are our top picks.

Risk to 2011 defense results on lower FY11-12 budgets We see risk to the companies' 2011 guidance from half-year CR and final FY11 appropriations legislation that cuts $10B in modernization funding relative to DoD request, likely followed by further cut in FY12. Valuations not overly attractive at 25% discount to market, high end of prior defense budget downturns. Our only Buy-rated defense stocks are GD/ATK.

Notes:

Source: The content presented above reflects a front page summary of UBS Research content, UBS commentary as at 27 June 2011

Morning Expresso - United States 27 June 2011

UBS 15

TECHNOLOGY Sapient Rating: Neutral Target: US$14.50 Price: US$14.03 RIC: SAPE.O Prior: Sell Prior: US$8.50 Mkt Cap: US$1.96bn BBG: SAPE US

Diversified Technology Services Analyst: Arvind Ramnani Tel: +1-212-713 3517

Upgrading to Neutral; Balanced risk/reward Upgrading SAPE to Neutral Primary reasons for our upgrade are: 1) We believe that F11 non-GAAP operating margins of 12%-14% are achievable

given pricing power (driven by strong demand for their differentiated offerings) and better pricing/utilization. 2) Solid revenue momentum (1Q revenues were up 32% y/y and 8%q/q), and a robust pipeline (in terms of number/quality of deals). 3) Strong growth driven by demand for its interactive marketing solutions.

Raising our estimates to reflect strong demand and better pricing We are raising our revenue forecast as SAPE continues to see strong demand for its services and the quality and numbers of deals continue to improve. We have increased our margin estimates due an improving pricing environment and higher utilization. However, we believe that SAPE is likely to be range bound in the term term, as it looks fully valued at current levels (28x/21x C11e/C12e EPS).

Expect multi-channel marketing solutions to drive growth We expect revenue growth to continue to be driven by demand for SAPE’s multi-channel solutions. We believe that Sapient’s Nitro business (which constitutes about 64% of overall revenues) has differentiated solution sets (i.e. interactive marketing) targeted towards the shift in traditional ad dollars to digital ad dollar.

Valuation: Raise PT to $14.50 from $8.50 We increased our ’11/’12 revenue ests from $992M/$1,149M to $1,035M/$1,231M and our ’11/’12 EPS ests from $0.44/$0.53 to $0.49/$0.68. Our new $14.50 PT is based on 20x C12e P/E (19x C11e P/E prior) and our DCF.

Notes: Source: The content presented above reflects a front page summary of UBS Research content, UBS estimates based on a share price of US$14.03 on 24 Jun 2011 15:12 EDT

Dell Rating: Buy Target: US$18.70 Price: US$15.93 RIC: DELL.O Prior: Unchanged Prior: Unchanged Mkt Cap: US$30.6bn BBG: DELL US

Computers Analyst: Maynard J. Um Tel: +1-212-713 3372

Dell Analyst Day Preview: Not Just a Shiny Box Company Anymore Expect Dell to reiterate FY12 outlook at Analyst Day on June 28/29 We expect Dell to reiterate its FY12 rev growth guidance of 5-9% y/y, provide

color on likely rev drivers, and reiterate op. inc. growth tgt of 12-18% y/y. We do not expect any explicit commentary around gross mgns though expect some commentary around business mix shift benefit & component environment. We maintain our FY12 ests of $64.3b/$1.87 which we think could prove conservative.

Focus on solutions-based offerings, which we believe are margin accretive We believe Dell will highlight the quiet transformation it is undergoing from a transactional point-product to a solutions-focused company. We expect Dell to showcase a number of solutions offerings such as InSite One, data center-in-a-box (cloud), SecureWorks, education-focused netbooks, etal that are differentiated/customized solutions, which we believe hold better margins.

Key messages likely to highlight near-term strength & long-term strategy We expect Dell to highlight generally strong demand for servers (higher ASPs), storage, & services (~30% of rev but ~50% of gross profit) as well as enterprise PCs. We expect more detail on how acquired & organic assets have positioned Dell in data center/cloud w/ key differentiators in openness (multi-vendor via Scalent acq) & simplicity. We also expect updates on M&A strategy (serial acquirer).

Valuation: Reiterate Buy Rating and $18.70 Price Target Our $18.70 price target is based on 10x our FY12 EPS estimate of $1.87. Notes:

Source: The content presented above reflects a front page summary of UBS Research content, UBS estimates based on a share price of US$15.93 on 24 Jun 2011 19:40 HKT

Juniper Networks Rating: Neutral Target: US$33.00 Price: US$30.02 RIC: JNPR.N Prior: Unchanged Prior: US$42.00 Mkt Cap: US$16.5bn BBG: JNPR US

Communications Technology Analyst: Nikos Theodosopoulos Tel: +1-212-713 3286

Lowering Estimates and Price Target 2Q Remains Challenging Our checks continue to show a more challenging qtr for JNPR with both Enterprise and SP demand lower than the

company expected entering 2Q. We believe a product transition within Switching is impacting Enterprise demand. Routing demand is relatively better, but is likely to slow following 3 very strong quarters.

New Reduced Estimates We lower our FY11/FY12 pro-forma EPS to $1.43/$1.70 (vs. prior $1.46/$1.80) and 2011-12 sales growth to 15.5% (prior ~18%). We believe JNPR sales growth will decelerate through 2011 to ~10% YoY growth in 4Q11, and re-accelerate in 1Q12 reaching ~20% by 4Q12 as new product revs become more material in 2H12.

Stock Reflecting CEO Comments Earlier this Month JNPR stock is down over 20% since the CEO commented that 2Q is a backend loaded qtr at an investor conference earlier in June. While the stock is discounting a difficult 2Q in our view, we do not believe business materially improved since the CEO’s comments. While the long term growth story of product innovation remains intact, we do not expect the stock to react positively to 2Q results.

Valuation – Maintain Neutral, Lower Target to $33 from $42 Our price target of $33 is based on ~19.5x (prior 23x) our 2012 pro-forma EPS of $1.70 (prior $1.80). JNPR’s valuation has historically ranged between 15x-25x forward EPS, depending on whether revenue is accelerating or decelerating. We believe the multiple will stay in the lower half of this range until revenue re-acceleration is more visible likely closer to 1Q12.

Notes: Source: The content presented above reflects a front page summary of UBS Research content, UBS estimates based on a share price of US$30.02 on 24 Jun 2011 19:40 EDT

Morning Expresso - United States 27 June 2011

UBS 16

Fairchild Rating: Buy Target: US$21.00 Price: US$16.51 RIC: FCS.N Prior: Unchanged Prior: Unchanged Mkt Cap: US$2.05bn BBG: FCS US

Semiconductors Analyst: Parag Agarwal Tel: +1-212-713 2563

Checks point to robust trends, potential win with Apple; Reiterate Buy Checks point to power management win on iPhone 5 Our checks into supply chain indicate that Fairchild has expanded its presence in iPhone

from MOSFETS to voltage regulators. This win points to continued momentum for Fairchild in handset power management, especially as transition to dual-core processors drive higher need for power management in smartphones. We believe that FCS should deliver strong results for remainder of 2011, & we reiterate our Buy rating and $21 price target.

Industrial related revenue strong, despite economic headwinds We further believe that FCS’ industrial business (~30% of rev) should continue to grow at a healthy clip given company’s exposure to secular growth areas of the industrial market including motor power management, although declining PMI poses a risk to industrial related revenue. Furthermore, given modest (~14%) exposure to PC market, only half of which is to commodity PCs, we don’t expect sizeable impact from soft consumer PC sales.

Upside to margins from mix and fab conversions In addition to healthy revenue growth, margins should expand driven by mix, conversion of Utah & South Korea fabs, & closure of Mountain Top facility. We forecast gross margin expansion of 200 bps in 2011 to 37.3% & 100 bps in 2012.

Valuation: Reiterate Buy and $21 price target Our PT is based on DCF (WACC 11.9%, g 2%) and equates to a NTM PE of ~12x. Notes:

Source: The content presented above reflects a front page summary of UBS Research content, UBS estimates based on a share price of US$16.51 on 24 Jun 2011 16:13 EDT

Molex Rating: Neutral Target: US$28.00 Price: US$25.91 RIC: MOLX.O Prior: Unchanged Prior: Unchanged Mkt Cap: US$4.57bn BBG: MOLX US

Electric Components & Equipment Analyst: Amitabh Passi Tel: +1-415-352 5537

Generally Constructive Tone to Meetings Hosted MOLX Management in Europe; Overall Tone Constructive We hosted MOLX mgmt in Europe for 3 days of meetings with clients. We found

the tone generally constructive, with business trends stable and Japan recovering faster than anticipated. Mgmt was most optimistic about the auto business in CY 2H11 on recovery post-Japan and low inventory levels. Inventories at Distis/VMI hubs remain normal-to-below normal. However, there are signs of excess inventory in the mobile phone (we believe higher end) and consumer (mainly TVs) markets.

14% OM Goal Intact; Though Market Forces Need to Cooperate Mgmt remains committed to its 14% OM goal and we believe there is line of sight to this goal, assuming incr. OM of 25%. However, in the short-mid-term getting to this goal will be predicated on ongoing sales growth and opex efficiencies, as we believe expanding GM will remain challenging in an environment with elevated commodity costs and Fx headwinds. Further, we believe any gains from the pricing optimization software, Vendavo, will likely play out over a longer period of time.

Capital Allocation Priorities: R&D; M&A; Dividend; Share Buy-backs Capital allocation priorities remain as follows: Re-investing in the business; M&A, with a focus on long-cycle markets such as Medical, Industrial; preserving/growing the dividend (current yield 3%), and targeting a yield at a premium to the market; and modest share buy-backs primarily to offset dilution. MOLX also continues to strive to work down inventory to 80 days from about 87 days currently.

Valuation: Maintain Neutral and Price Target of $28 PT based on VCAM: 10% WACC; 7% Rev growth; 12.5% OM (thru-cycle). Notes:

Source: The content presented above reflects a front page summary of UBS Research content, UBS estimates based on a share price of US$25.91 on 24 Jun 2011 19:40 EDT

Rubicon Technology Rating: Buy Target: US$28.00 Price: US$16.54 RIC: RBCN.O Prior: Unchanged Prior: Unchanged Mkt Cap: US$0.33bn BBG: RBCN US

Semiconductors Analyst: Stephen Chin Tel: +1-212-713 4111

Large diameter sapphire still an advantage Well positioned to lead industry shift to the larger 6-inch wafers Our checks find Rubicon’s new sapphire ingot factory in Batavia, Illinois remains

on schedule (installing the newer/bigger 85kg furnaces) and is over 50% complete. We estimate this factory will be 50% of the company’s total capacity. We believe Rubicon’s announcement last week of its first 6” customer qualification at its Malaysia facility will enable it to generate 60%+ of its 2012 sales from 6” wafers as we expect 3 other customer qualifications are possible in 2H11.

2-inch price pressure and new competition remain longer term risks Our checks find prices for 2” wafers are down 15-20% q/q to $24 at present and estimate Rubicon’s 2” core prices are around $16 which is inline with our estimate of 50% price declines by 4Q12. Our checks find 6” prices are still flattish in 2H11 vs 1H11 at $450 each and we still estimate over 50% of Rubicon’s sales will be 6” wafers by 4Q11. We still estimate Rubicon’s 2012 gross margin can be 40% with 2” product at 30% and 6” product at 50% given limited competition near term.

New applications and input materials cost savings are likely in 2012 Our checks find Military/Optical could be a modest incremental sales opportunity for larger sized products ($10M) with the industrial market and enhanced LED sapphire substrates a 2012-13 opportunity. Checks also find efforts to supply its own input material (crackle) are doing well and may lower costs by 20% in 2012.

Valuation: 12-month price target is $28 Our PT is based on applying a 12x P/E multiple our 2012 EPS of $2.30. We still expect 6” customer wins and capacity expansion updates are possible catalysts.

Notes:

Source: The content presented above reflects a front page summary of UBS Research content, UBS estimates based on a share price of US$16.54 on 24 Jun 2011 19:40 EDT

Morning Expresso - United States 27 June 2011

UBS 17

Semiconductor Equipment Industry Update

Semiconductors Analyst: Stephen Chin Tel: +1-212-713 4111

2Q11 Taiwan orders tracking -54% q/q Total Taiwanese semicap orders in 2Q11 tracking down -54% q/q so far Our analysis now shows the 9 major semiconductor customers in Taiwan

have only ordered $834M of semicap equipment so far, with only 1 week left in 2Q11, versus a total of $1.95B last quarter. Our analysis shows Taiwan foundry semicap orders have totalled only $728M so far, down -54% q/q, while Taiwanese DRAM semicap orders are only $106M so far in 2Q11, down -53% q/q. We note that KLA typically has the highest foundry order exposure at 40% while Lam typically has the highest DRAM customer exposure at 40%.

Checks find UMC placed 2 orders for $42M last week; TSMC had none We found UMC’s new semicap orders last week included $18M with Novellus and $24M with ASML. Our analysis shows UMC’s semicap orders in 2Q11 are only $110M, which are tracking down -24% q/q. We found TSMC did not place any new semicap orders last week (7th time in 2Q11). Our analysis shows TSMC’s total 2Q11 semicap orders are only $618M or down -57% q/q. With TSMC’s total 1H11 semicap orders at $2.2B versus its 1H11 capex guidance of $5.3B, we believe there could be downside to TSMC’s 2011 capex guidance of $7.8B.

Checks find Rexchip placed a DRAM semicap order last week Our checks found Rexchip placed an $18M semicap order with KLA-Tencor last week, its first semicap order with KLA since 2010. We expect Taiwanese DRAM semicap orders to remain muted near term and our 2012 total semiconductor capex estimate remains -15% yoy with DRAM up 8% yoy and NAND down -30% yoy.

Notes:

Source: The content presented above reflects a front page summary of UBS Research content, UBS commentary as at 26 June 2011

US Internet and Interactive Entertainment

Internet Services Analyst: Brian Pitz Tel: +1-212-713 9310

Pitz & Fitz’s Internet / IE Weekly Facebook to emerge as top US display-ad seller in 2011 According to the latest report by eMarketer, Facebook will overtake Yahoo to emerge as

the biggest display ad seller in 2011. Facebook will have a 17.7% share of the US display market ($2.2B), ahead of Yahoo’s 13.1% share. Facebook’s ad revenue more then doubled in each of the past two years and is expected to grow +81% in 2011. The report projects Google will increase its display ad sales by 34% this year, for a 9% share of the US market.

Ebay plans fulfillment service for sellers According to the Wall Street Journal, Ebay will start testing a fulfillment service for its sellers later this year. This would sellers to send the goods directly to eBay’s fulfillment centers, which would then take care of storage, packaging and delivery. This would help the online marketplace in standardizing delivery times for its merchants. The company hopes to cut down delivery time for China based sellers by more than half from the current average delivery time of 18 days. It is still unclear whether eBay will use a contractor or use its own warehouse.

Electronic Arts reportedly in talks to acquire PopCap games According to reports in TechCrunch, Electronic Arts is in an advanced stage of talks to acquire PopCap games. According to the reports the deal could be worth over $1B, which would be at a 10X multiple to Popcap’s revenue estimates of $100-150MM. EA had earlier acquired Playfish in 2009 for over $400MM. PopCap is known for hit casual, mobile, and social titles Plants vs. Zombies and Bejeweled, which has reportedly sold over 75MM units and been downloaded over 500MM times.

Notes: Source: The content presented above reflects a front page summary of UBS Research content, UBS commentary as at 27 June 2011

Morning Expresso - United States 27 June 2011

UBS 18

UBS Key Calls - US Live Key Call Portfolio

Stock Name RIC Rating Price Target Date of call Current Price Analyst Apple Inc. AAPL.O Buy US$510 2-Jun-11 US$331.23 Maynard Um

Baker Hughes Inc. BHI.N Buy US$95 7-Jun-11 US$70.25 Angie Sedita

Cardinal Health, Inc. CAH.N Buy US$51 18-Jan-11 US$44.31 Steven Valiquette

Celgene Corporation CELG.O Buy US$69 9-Dec-10 US$59.89 Matthew Roden, PhD

Citigroup Inc C.N Buy US$56 3-May-11 US$39.41 William Tanona, CFA

Deere & Co. DE.N Buy US$115 18-Jan-11 US$81.73 Henry Kirn, CFA

Dow Chemical DOW.N Buy US$46.5 21-Mar-11 US$35.62 Andrew Cash

Ford Motor Co. F.N Buy US$22 10-Jan-11 US$13.47 Colin Langan, CFA

General Electric Co. GE.N Buy US$23 10-Jan-11 US$18.38 Jason Feldman

Google Inc. GOOG.O Buy US$765 10-May-10 US$480.22 Brian Pitz

Joy Global Inc. JOYG.O Buy US$112 28-Feb-11 US$87.74 Henry Kirn, CFA

McDonalds Corp. MCD.N Buy US$93 9-Feb-11 US$82.29 David Palmer

Prudential Financial Inc. PRU.N Buy US$77 19-Apr-10 US$60.4 Andrew Kligerman

Qualcomm Inc. QCOM.O Buy US$70 26-Apr-11 US$54.96 Parag Agarwal

SanDisk Corp. SNDK.O Buy US$62 21-Mar-11 US$42.88 Uche Orji

Source: Reuters, UBS. Prices as at market close on June 24, 2011.

Morning Expresso - United States 27 June 2011

UBS 19

Rating & PT Changes Key Rating and Price Target Changes: US

Company Name Directional Indicator/Rationale Reuters Code Current Share Price

New Rating New PT Prior

Rating Prior PT

Bristol-Myers Squibb Maintain Neutral, increase PT BMY.N US$28.93 Neutral US$30 Neutral US$28

Dice Holdings Inc Maintain Neutral, lower PT DHX.N US$13.51 Neutral US$14 Neutral US$19

Hansen Natural Corporation Reiterate Buy, increase PT HANS.O US$78.05 Buy US$90 Buy US$75

Juniper Networks Maintain Neutral, lower PT JNPR.N US$30.02 Neutral US$33 Neutral US$42

Kraft Foods Inc. Reiterate Buy, increase PT KFT.N US$34.6 Buy US$38 Buy US$36

Sapient Corp. Upgrade to Neutral, increase PT SAPE.O US$14.11 Neutral US$14.5 Sell US$8.5

Targa Resources Partners, L.P Reiterate Buy, increase PT NGLS.N US$34.14 Buy US$38 Buy US$31

Source: Reuters, UBS. Prices as at market close on June 24, 2011.

Markets, Events and Newsflow Today’s Company Events

Company Name Event Reuters code Rating PT Notes

Nike Earnings Release NKE.N Buy US$90

Source: Reuters, UBS. Prices as at market close on June 24, 2011.

Today’s Macroeconomic Events: US

Indicator Time (ET) UBS forecast Previous Consensus

Personal Income (May)mom 9:30 0.3% 0.4% 0.4%

Personal Spending (May)mom 9:30 0.0% 0.4% 0.1%

Core PCE (May)mom 9:30 0.2% 0.2% 0.2%

Texas Mfg. Outlook Survey (Jun)index 11:30 na -7.4 na

Source: Bloomberg, UBS

Morning Expresso - United States 27 June 2011

UBS 20

Today’s UBS Hosted Corporate Roadshow: Company Event Location None

Today’s UBS Hosted Fieldtrip:

Company Event Location

None

Today’s UBS Hosted Conference:

Company Event Location

None

Morning Expresso - United States 27 June 2011

UBS 21

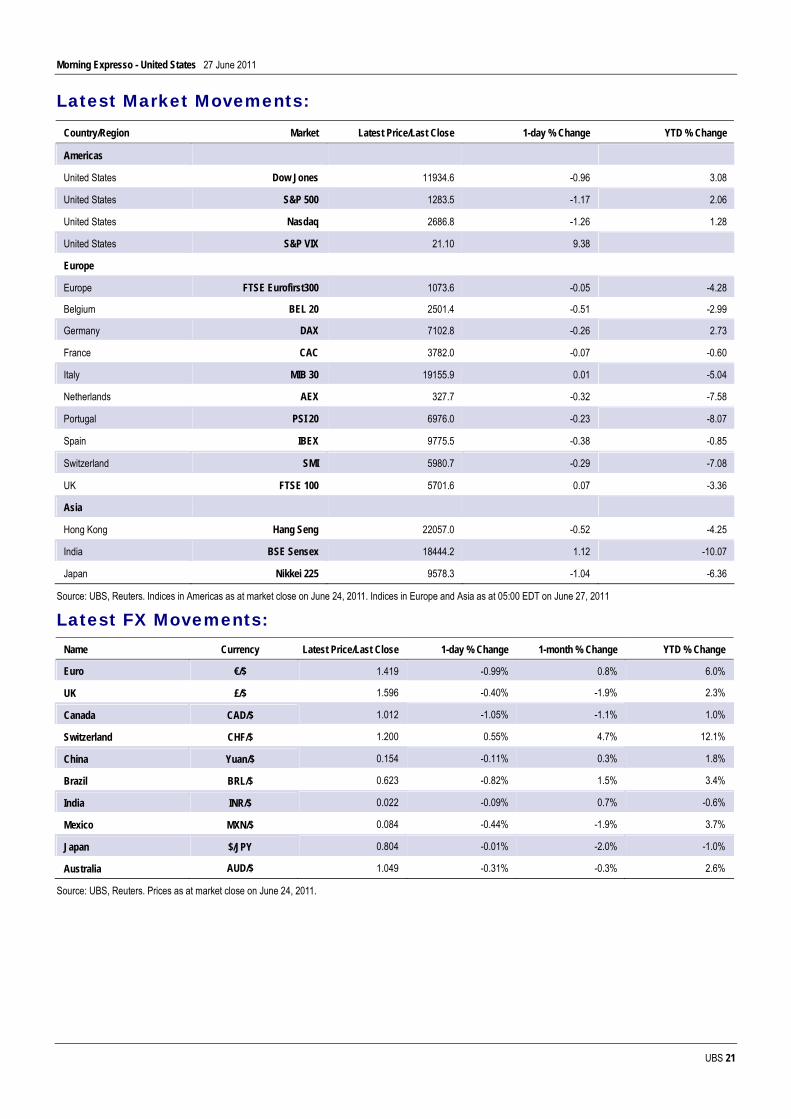

Latest Market Movements: Country/Region Market Latest Price/Last Close 1-day % Change YTD % Change

Americas

United States Dow Jones 11934.6 -0.96 3.08

United States S&P 500 1283.5 -1.17 2.06

United States Nasdaq 2686.8 -1.26 1.28

United States S&P VIX 21.10 9.38

Europe

Europe FTSE Eurofirst300 1073.6 -0.05 -4.28