financial administration manual part: financial … · financial administration manual ......

TRANSCRIPT

Financial Administration Manual

Part: Financial Management and Administration Number: 4000 Section: Treasury Board’s Risk Management Policies Date: 2010-01-25 Subsection: Financial Systems Page: 1 of 2

Ministry of Finance, Provincial Comptroller’s Office

Financial Systems

Objective The guidelines under Financial Systems establish the minimum internal control standards to follow in the acquisition, development and operation of financial systems. In most sections, specific standards that are required are noted. Techniques are also outlined as possible ways to achieve the control standard. These are alternative ways of achieving a specific control objective. Not all techniques are appropriate in all cases, nor do they represent a complete list of alternatives.

Definition Financial systems include any systems, both manual and

computerized, that account for any or all of the following: • revenues, including tax revenue, receipts for goods and services,

transfer payments from other jurisdictions, grants received by the Government or gifts;

• expenses, including purchases of goods and services, grants, taxes and tax credits, or transfers to other parties;

• assets, including fixed assets, inventories of goods for consumption or sale, investments, land, accounts receivable, assets held in trust by the Government for other parties; and

• liabilities, including accounts payable, amounts borrowed, pension fund liabilities or liabilities relating to assets held in trust by the Government.

Authority The Financial Administration Act, 1993 (FAA) allows Treasury Board

to direct any person receiving, managing or disbursing public money to keep any books, records or accounts that it considers necessary (clause 5(e)). The FAA requires public moneys to be forwarded, deposited and otherwise dealt with in accordance with any orders and directives of Treasury Board (section 22). The FAA also specifically allows Treasury Board to prescribe the form and manner of financial records and accounting systems of the Government of Saskatchewan (clause 5(c)). The FAA allows Treasury Board to make orders and issue directives with respect to its duties under section 4 of the FAA (e.g., relating to the finances, the administrative policy and management practices, and the accounting policies and practices of the Government) (clause 5(a)).

Financial Administration Manual

Part: Financial Management and Administration Number: 4000 Section: Treasury Board’s Risk Management Policies Date: 2010-01-25 Subsection: Financial Systems Page: 2 of 2

Ministry of Finance, Provincial Comptroller’s Office

The FAA allows the Provincial Comptroller to issue directives to ministries and public agencies detailing the manner in which Treasury Board orders and directives are to be complied with (subsection 10(2)). In addition, the FAA also provides that every payment out of the General Revenue Fund is to be made under the direction and control of the Provincial Comptroller and in the manner that the Provincial Comptroller may direct (section 28). Treasury Board has delegated authority to the Provincial Comptroller to approve all new financial systems and significant changes to existing systems prior to implementation. The Provincial Comptroller may further delegate the authority for reviewing financial systems.

Treasury Board Policies Guidelines are provided for the following: • Section 4005 Acquisition of Financial Systems; • Section 4010 Development of Financial Systems; • Section 4015 Approval of Financial Systems; • Section 4020 System Processing Controls; and • Section 4025 System Security.

Applicability These policies apply to the General Revenue Fund, and special purpose funds and trust money that are administered by ministries. See Appendix C Public Money.

References 3000 Control of the GRF 3400 Control of Special Purpose Funds and Trust Money 3500 Control of Public Money 3600 Control of Bank Accounts 3700 Control of Accounts Receivable 3800 Control of Property

Financial Administration Manual

Part: Financial Management and Administration Number: 4005 Section: Treasury Board’s Risk Management Policies Date: 2008-12-12 Subsection: Financial Systems Page: 1 of 1 Policy: Acquisition of Financial Systems

Ministry of Finance, Provincial Comptroller’s Office

Acquisition of Financial Systems

Objective The objective is to outline the requirements to be met before a new financial system is acquired.

Authority The Financial Administration Act, 1993, clauses 5(a), 5(c), and 5(e),

subsection 10(2), and sections 22 and 28 Applicability This policy applies to the General Revenue Fund (GRF), and special

purpose funds and trust money that are administered by ministries. See Appendix C Public Money.

Treasury Board Policy .01 Ministries are to ensure that the acquisition of a new financial system proceeds only after it is determined that the benefits to be derived justify the cost to be incurred.

.02 Ministries are to ensure there is adequate control over the

acquisition of new financial systems.

Provincial Comptroller .03 Ministries are to ensure that the acquisition of all significant Directives new financial systems is carried out with the knowledge of, and

direction from, senior management of the ministry. .04 Ministries must ensure funding approval is obtained from

Treasury Board and Cabinet as required. .05 Ministries with information technology (IT) investments follow

the Information Technology Office - Call for IT Initiatives process.

References 4000 Financial Systems 4010 Development of Financial Systems 4015 Approval of Financial Systems 4020 System Processing Controls 4025 System Security

Information Technology Office - Call for IT Initiatives

Financial Administration Manual

Part: Financial Management and Administration Number: 4010 Section: Treasury Board’s Risk Management Policies Date: 2008-12-12 Subsection: Financial Systems Page: 1 of 5 Policy: Development of Financial Systems

Ministry of Finance, Provincial Comptroller’s Office

Development of Financial Systems

Objective The objective is to outline the requirements for the development of financial systems.

Authority The Financial Administration Act, 1993, clauses 5(a), 5(c), and 5(e),

subsection 10(2), and sections 22 and 28 Applicability This policy applies to the General Revenue Fund (GRF), and special

purpose funds and trust money that are administered by ministries. See Appendix C Public Money.

Treasury Board Policy .01 Ministries are to establish a management structure for the development of a new financial system to ensure the development undertaken is effectively managed.

.02 Ministries are to ensure financial systems comply with

requirements of relevant legislation and regulations, as well as the relevant financial control requirements of The Financial Administration Act, 1993 and the requirements of the Provincial Comptroller.

.03 Ministries are to ensure the design of a new financial system

meets the needs of the system’s users. .04 Ministries are to conduct sufficient testing of a new financial

system prior to implementation to ensure that the system will function effectively once implemented.

.05 Ministries are to ensure there is no loss or alteration of data in

the process of converting to a new system. .06 Ministries are to avoid disruption of critical financial

processing during the implementation of a new system.

Provincial Comptroller .07 Ministries with information technology (IT) development Directives investments follow the Information Technology Office - Call

for IT Initiatives process.

Financial Administration Manual

Part: Financial Management and Administration Number: 4010 Section: Treasury Board’s Risk Management Policies Date: 2008-12-12 Subsection: Financial Systems Page: 2 of 5 Policy: Development of Financial Systems

Ministry of Finance, Provincial Comptroller’s Office

Management Structure .08 Ministries are to establish an appropriate and effective management structure to control the development of new financial systems. The following techniques are recommended:

• Establish a Steering Committee that reports to senior

management. The Steering Committee is responsible for the successful design, development and implementation of the system and includes representatives from the users, the financial administration unit and the system development team.

• Appoint a project coordinator with responsibility for the

timely and orderly development of the new system which must include:

• ensuring the needs of the ultimate users are met; and • being the liaison with the Provincial Comptroller’s

representatives reviewing the system for the adequacy of the controls.

• Adopt a system life cycle methodology which defines the

project in distinct phases such as the following: • problem identification • system design • system development • system testing • data conversion • system implementation

• Establish a system development plan for use by the Steering Committee to monitor progress and identify where corrective action is required. This plan should include milestone dates for system development and a resource budget.

Problem Identification .09 Ministries are to ensure the system proposal addresses the

needs of, and resolves the issues raised by, the users. Problem identification techniques include requiring users to actively participate in identification of possible solutions and selection of the best alternative.

Financial Administration Manual

Part: Financial Management and Administration Number: 4010 Section: Treasury Board’s Risk Management Policies Date: 2008-12-12 Subsection: Financial Systems Page: 3 of 5 Policy: Development of Financial Systems

Ministry of Finance, Provincial Comptroller’s Office

System Design .10 Ministries are to ensure the system design addresses the needs of system users. System design techniques include:

• requiring users to participate in the design and planning

process; and • obtaining end user ‘sign off’ on the system design before

system development commences.

System Development .11 Ministries are to ensure that system development proceeds in accordance with the approved system design and development plan. System development techniques include:

• imposing a “design freeze” prior to commencement of

development; • requiring design changes during development to be approved

only on an exception basis, by the Steering Committee; and • monitoring the conformance of the development to the

system plan.

System Testing .12 Ministries are to:

• perform sufficient testing to ensure all system specifications are met before a new system or modifications to an existing system are implemented;

• retain an adequate record of test results to document the situations tested, results obtained and the disposition of errors detected during the testing process; and

• test the manual portions of systems to ensure all required procedures and records are established.

.13 The following techniques may be used to ensure the accuracy

of the system in processing data:

• a test plan; • assigning and training appropriate staff to test; • test procedures and methods such as:

• use of predetermined results with which to compare actual output;

• use of parallel runs; • use of intentionally invalid data; • use of expected types of transactions; • testing of all system checks and controls;

Financial Administration Manual

Part: Financial Management and Administration Number: 4010 Section: Treasury Board’s Risk Management Policies Date: 2008-12-12 Subsection: Financial Systems Page: 4 of 5 Policy: Development of Financial Systems

Ministry of Finance, Provincial Comptroller’s Office

• testing to determine the system’s calculations and accumulative totaling are correct;

• testing to ensure the system can accept and process corrections;

• testing to ensure all files are updated when transactions are processed;

• testing to ensure the system accumulates cumulative totals from several consecutive runs correctly;

• testing to ensure all system-generated control logs and reports are accurate;

• testing to ensure the system is capable of processing expected volumes of transactions without unacceptable delays; and

• retesting to ensure problems encountered in the testing phase that resulted in system modifications have been corrected;

• documentation of the test results; and • control of testing to ensure:

• supervision of staff during testing; • completeness of testing; • supervision and review of test results; • control of change requests; and • submission of changes that have been reviewed and

approved to the system designer.

Data Conversion .14 Ministries are to ensure data conversion from the old system to the new system is planned, complete, accurate and valid. Data conversion techniques include:

• comparing all data in new master files or data bases to

existing records in detail; • comparing transaction counts and control totals for data in

critical fields to detect instances where data has been converted to the new system in error;

• scrutinizing the effective date of data conversion to ensure transactions have been converted in a consistent manner; and

• implementing appropriate authorization procedures to ensure no unauthorized data has been added or legitimate data deleted.

System Implementation .15 Ministries are to ensure a new system is fully functional prior

to placing complete reliance on the system. Ministries may use

Financial Administration Manual

Part: Financial Management and Administration Number: 4010 Section: Treasury Board’s Risk Management Policies Date: 2008-12-12 Subsection: Financial Systems Page: 5 of 5 Policy: Development of Financial Systems

Ministry of Finance, Provincial Comptroller’s Office

the following techniques to ensure the system is successfully implemented:

• involving users in the decision to cut off the parallel

operation of the new and existing system; • providing training to users in the operation of both the

manual and automated procedures of the system; • completing system documentation before implementation;

and • developing procedures for file backup when the system is

operational.

References 4000 Financial Systems 4005 Acquisition of Financial Systems 4015 Approval of Financial Systems 4020 System Processing Controls 4025 System Security

Information Technology Office - Call for IT Initiatives

Financial Administration Manual

Part: Financial Management and Administration Number: 4015 Section: Treasury Board’s Risk Management Policies Date: 2010-01-25 Subsection: Financial Systems Page: 1 of 3 Policy: Approval of Financial Systems

Ministry of Finance, Provincial Comptroller’s Office

Approval of Financial Systems

Objective The objective is to outline ministries’ and the Provincial Comptroller’s responsibilities regarding financial systems.

Authority The Financial Administration Act, 1993, clauses 5(a), 5(c), and 5(e),

subsection 10(2), and sections 22 and 28 Applicability This policy applies to the General Revenue Fund (GRF), and special

purpose funds and trust money that are administered by ministries. See Appendix C Public Money.

Treasury Board Policy .01 Ministries are to advise the Provincial Comptroller of any planned development of new financial systems or major changes to existing systems.

.02 Ministries are to provide the Provincial Comptroller with an

adequate opportunity to review the system and raise internal control or financial administration concerns prior to the commencement of system development.

.03 The Provincial Comptroller is to review new financial systems

to the extent considered necessary to ensure they contain adequate internal controls, and that they conform to legislation, government policy and sound financial management practice.

.04 Ministries are to obtain the approval of the Provincial

Comptroller for each new financial system or major changes to existing financial systems prior to implementing a new financial system.

.05 The Provincial Comptroller may conduct ongoing reviews to

the extent considered necessary to confirm that adequate internal controls continue to exist.

Provincial Comptroller .06 Ministries are responsible for designing, developing, Directives implementing and operating their financial systems.

.07 The chart on the following page summarizes the

responsibilities of ministry officials and staff of the Provincial Comptroller’s Office, Ministry of Finance in the design, development and implementation of new financial systems.

Financial Administration Manual

Part: Financial Management and Administration Number: 4015 Section: Treasury Board’s Risk Management Policies Date: 2010-01-25 Subsection: Financial Systems Page: 2 of 3 Policy: Approval of Financial Systems

Ministry of Finance, Provincial Comptroller’s Office

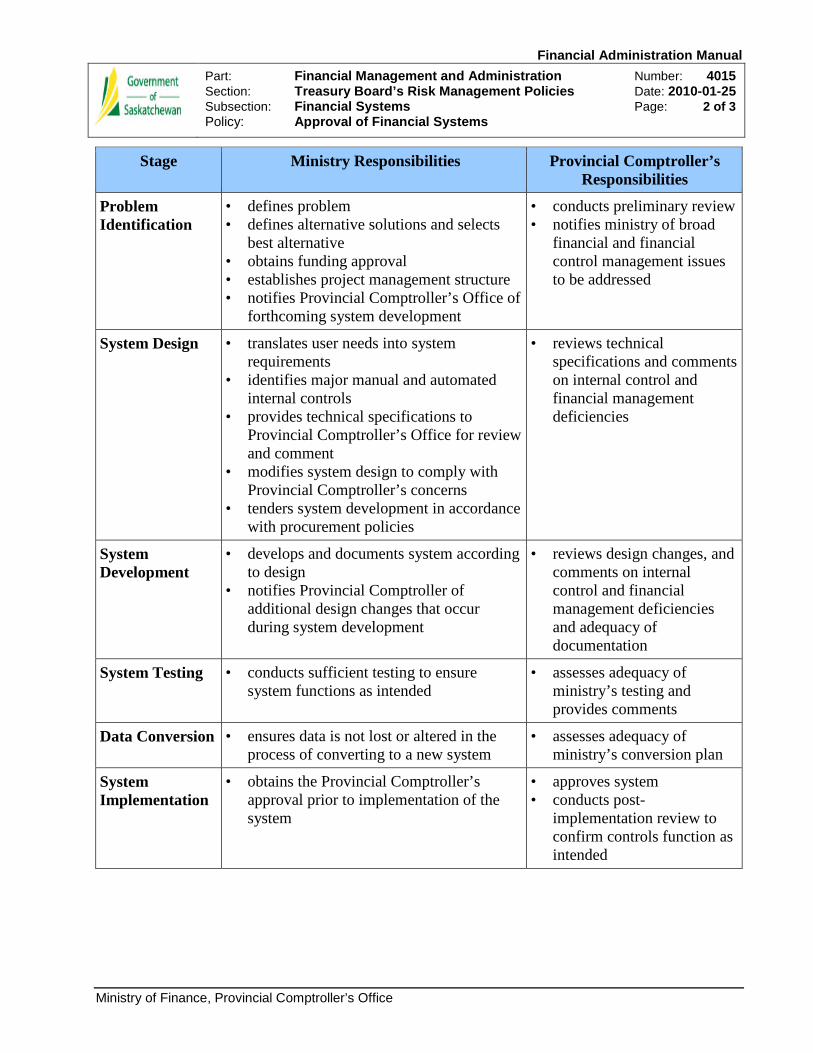

Stage Ministry Responsibilities Provincial Comptroller’s Responsibilities

Problem Identification

• defines problem • defines alternative solutions and selects

best alternative • obtains funding approval • establishes project management structure • notifies Provincial Comptroller’s Office of

forthcoming system development

• conducts preliminary review • notifies ministry of broad

financial and financial control management issues to be addressed

System Design • translates user needs into system requirements

• identifies major manual and automated internal controls

• provides technical specifications to Provincial Comptroller’s Office for review and comment

• modifies system design to comply with Provincial Comptroller’s concerns

• tenders system development in accordance with procurement policies

• reviews technical specifications and comments on internal control and financial management deficiencies

System Development

• develops and documents system according to design

• notifies Provincial Comptroller of additional design changes that occur during system development

• reviews design changes, and comments on internal control and financial management deficiencies and adequacy of documentation

System Testing • conducts sufficient testing to ensure system functions as intended

• assesses adequacy of ministry’s testing and provides comments

Data Conversion • ensures data is not lost or altered in the process of converting to a new system

• assesses adequacy of ministry’s conversion plan

System Implementation

• obtains the Provincial Comptroller’s approval prior to implementation of the system

• approves system • conducts post-

implementation review to confirm controls function as intended

Financial Administration Manual

Part: Financial Management and Administration Number: 4015 Section: Treasury Board’s Risk Management Policies Date: 2010-01-25 Subsection: Financial Systems Page: 3 of 3 Policy: Approval of Financial Systems

Ministry of Finance, Provincial Comptroller’s Office

.08 The Provincial Comptroller has delegated to the Executive Director, Financial Management Branch (FMB) the authority for reviewing new financial systems and major changes to financial systems.

.09 FMB conducts an initial review of the system and its risks to

determine the nature and extent of the review. The review also provides the opportunity to advise the ministry of any control objectives in the developmental stage.

.10 FMB staff assesses proposed financial systems or proposed

major changes to financial systems on behalf of the Provincial Comptroller to determine whether there is adequate compliance with the control standards specified in this section and with sound financial management practice. This review will result in approval of the system, or recommendations for changes which, if incorporated, will render it acceptable.

.11 The Provincial Comptroller has delegated to the Director,

Internal Audit Branch, Ministry of Finance, the authority for ongoing reviews.

References 4000 Financial Systems 4005 Acquisition of Financial Systems 4010 Development of Financial Systems 4020 System Processing Controls 4025 System Security

Financial Administration Manual

Part: Financial Management and Administration Number: 4020 Section: Treasury Board’s Risk Management Policies Date: 2010-01-25 Subsection: Financial Systems Page: 1 of 5 Policy: System Processing Controls

Ministry of Finance, Provincial Comptroller’s Office

System Processing Controls

Objective The objective is to outline the system processing controls required in a financial system.

Authority The Financial Administration Act, 1993, clauses 5(a), 5(c), and 5(e),

subsection 10(2), and sections 22 and 28 Applicability This policy applies to the General Revenue Fund (GRF), and special

purpose funds and trust money that are administered by ministries. See Appendix C Public Money.

Treasury Board Policy .01 Ministries are to ensure financial systems contain adequate internal controls over the processing of financial information.

Provincial Comptroller Directives Segregation of Duties .02 Ministries are to ensure that the functions of initiation,

authorization and recording of transactions and custody of assets are separated to ensure no employee or group of employees has exclusive control over a financial transaction or group of transactions.

.03 Guidelines for segregation of duties include the following:

• Separate source data generation from other functions such as data entry or custody of associated assets.

• Segregate data processing from users of the data. • Segregate systems design and programming from

operations and data control. • Restrict access to critical forms (e.g., blank cheque stock)

to individuals responsible for initiation of transactions. • Ensure there are adequate computer audit trails and

controls to verify the operator’s adherence to prescribed operating procedures through observation and examination of computer operation logs.

• Ensure there is a supervisory review of key summary reports on a regular basis.

Accuracy of Input .04 Ministries are to ensure that all inputs to the system are

complete and accurate and all transactions are valid and

Financial Administration Manual

Part: Financial Management and Administration Number: 4020 Section: Treasury Board’s Risk Management Policies Date: 2010-01-25 Subsection: Financial Systems Page: 2 of 5 Policy: System Processing Controls

Ministry of Finance, Provincial Comptroller’s Office

properly authorized. Guidelines and techniques to provide for this include the following:

• Provide instructions in documented procedures for the

preparation of documents to initiate transactions. • Train and supervise employees responsible for the

preparation and input of documents which initiate transactions.

• Use specifically designed forms (e.g., pre-numbered forms) for input where appropriate and ensure all input forms are processed.

• Restrict access to accounting source documents and sensitive data input forms.

• Review and approval of transactions by an authorized person to ensure each transaction is valid and adequately supported.

• Incorporate system edit checks (e.g., alphabetical data incorrectly entered into numeric fields) and validity checks of data entered in systems (e.g., comparison of code or account number to a master file of valid or authorized ones).

• Use warning messages or inhibit processing until error is corrected.

• When batch processing is used: • compare system calculated batch control totals to

manually calculated totals; • incorporate system checks to detect alphabetical data

incorrectly entered into numeric fields on an input document;

• design software to inhibit processing of data where batch control totals indicate an out-of-balance condition;

• limit the number of transactions in a batch to simplify correction of errors;

• number batches sequentially to control entry of batches and to detect cases where a batch is not fully processed;

• ensure the system checks for missing document numbers where sequential control numbers on source documents are entered; and

• authorize each batch of transactions.

Financial Administration Manual

Part: Financial Management and Administration Number: 4020 Section: Treasury Board’s Risk Management Policies Date: 2010-01-25 Subsection: Financial Systems Page: 3 of 5 Policy: System Processing Controls

Ministry of Finance, Provincial Comptroller’s Office

System Computations .05 Ministries are to ensure that accuracy of data is maintained during processing and computations are carried out accurately. Guidelines and techniques to provide for this include the following:

• Incorporate system edits to determine if data falls outside

a range of reasonably expected values, and have the system report these to the operator.

• Incorporate system validity checks into the software to compare a code or account number to a master file of valid or authorized ones.

• Incorporate cross-footing (cross-balancing) as an arithmetic accuracy check.

• Incorporate field computability checks, such as a comparison check of different fields within a record, to ensure a valid combination of data or to detect missing data.

• Incorporate file control checks, such as a balancing check of the previous master file and changes to the updated master file.

• Incorporate file completion checks to determine that the application files have been completely processed for both the transaction file and the master file.

• Reconcile input to output.

Error Correction .06 Ministries are to establish procedures to ensure errors are detected, corrected and corrections re-entered into the system.

.07 Guidelines and techniques to ensure appropriate error detection

and correction include the following:

For transaction entry errors • Errors are detected by balancing, editing and validation

routines. • Error listings identify transactions not accepted, the

reasons for the rejection, the specific records in error and the specific data element in error.

• Errors or warnings that are detected are displayed along with the entire transaction.

• Error messages are given for each transaction that contains critical data that does not meet edit routine requirements and causes the transaction to be rejected from further processing by the system.

Financial Administration Manual

Part: Financial Management and Administration Number: 4020 Section: Treasury Board’s Risk Management Policies Date: 2010-01-25 Subsection: Financial Systems Page: 4 of 5 Policy: System Processing Controls

Ministry of Finance, Provincial Comptroller’s Office

• Warning messages are displayed for non-critical data that does not meet edit routine requirements but the data is accepted by the system for further processing.

• Corrected data is subjected to the same balancing, edit and valuation routines as the original data.

For processing errors • Error reports indicate all data fields in the error. • Error reports contain messages that describe the error

condition. • An error suspense file and report are maintained. • The entire rejected transaction appears on a report.

Management Trail .08 Ministries are to ensure the system facilitates tracing of input

documents and transactions through to output reports and vice versa. Guidelines and techniques to provide for this are as follows:

• Uniquely identify each document or transaction. • Reconstruct totals or trace item(s) to the total. • Maintain consistency of the manual filing sequence and

computer file referencing.

Output Standards .09 Ministries are to ensure the system output provides the information needed to ensure:

• all authorized transactions are processed promptly and

accurately; and • adequate consideration is given to the Provincial

Comptroller’s requirements respecting accounting records and financial statements.

The following guidelines and techniques to ensure this may include:

• identification of financial and management requirements

during the design phase of a system; • review of proposed reports with all users including

management before finalization; • reconciliation of output control totals back to input control

totals; and • implementation of a post-audit of a statistically valid

sample of transactions to confirm that they have been processed accurately.

Financial Administration Manual

Part: Financial Management and Administration Number: 4020 Section: Treasury Board’s Risk Management Policies Date: 2010-01-25 Subsection: Financial Systems Page: 5 of 5 Policy: System Processing Controls

Ministry of Finance, Provincial Comptroller’s Office

Documentation .10 Ministries are to ensure that all aspects of the financial system are adequately documented. Document the following areas:

Overall system description • Describe the entire system, including both the automated

and manual segments. • Describe the existing and proposed functions or processes. • Update the documentation as required.

User procedures • Describe user procedures regarding preparation of source

documents, data entry, production scheduling and control. • Prepare procedures regarding the allocation of duties and

responsibilities. • Prepare procedures for the correction of errors. • Describe procedures for the distribution of output. • Prepare information on interpretation of reports and

preparation of reconciliations. • Update the documentation as required.

Computer operations • Describe the system components and their purposes. • Prepare an explanation of the nature of each run. • Identify all input and output forms and media. • Prepare detailed operator instructions for the setup and

end of run. • Provide information on programmed machine halts before

the end of the job and restart instructions for each, and describe the authorization required for system override.

• Update the documentation as required.

References 4000 Financial Systems 4005 Acquisition of Financial Systems 4010 Development of Financial Systems 4015 Approval of Financial Systems 4025 System Security

Financial Administration Manual

Part: Financial Management and Administration Number: 4025 Section: Treasury Board’s Risk Management Policies Date: 2010-01-25 Subsection: Financial Systems Page: 1 of 5 Policy: System Security

Ministry of Finance, Provincial Comptroller’s Office

System Security

Objective The objective is to outline the system security required for financial systems.

Authority The Financial Administration Act, 1993, clauses 5(a), 5(c), and 5(e),

subsection 10(2), and sections 22 and 28 Applicability This policy applies to the General Revenue Fund, and special purpose

funds and trust money that are administered by ministries. See Appendix C Public Money.

Treasury Board Policy .01 Ministries are to incorporate adequate security features into financial systems to prevent unauthorized access to the system.

.02 Ministries are to maintain an appropriate capability to restore

records and processing capability after a processing interruption from system failure or from a disaster which causes destruction of a critical system component.

Provincial Comptroller .03 Ministries are to ensure data files, programs, forms and Directives hardware facilities are adequately secured to ensure

completeness, accuracy, authorization and validity of files and programs. Ministries may use the following techniques:

• Identify sensitive data files and programs and protect them

to an appropriate level of security. • Use software and hardware firewalls to restrict access to

assets, computers and networks by external persons. • Implement virus protection and update it regularly to

protect against viruses and malicious software. • Establish a security profile for each user that details the

information access and transaction processing permitted and complements the appropriate segregation of duties. The security profile is updated when personnel or job duties change.

• Use security passwords to control access to computer files and programs with the system periodically and automatically requesting password changes.

• Restrict access to critical forms (e.g., special paper for cheques) to authorized personnel responsible for the initiation function.

Financial Administration Manual

Part: Financial Management and Administration Number: 4025 Section: Treasury Board’s Risk Management Policies Date: 2010-01-25 Subsection: Financial Systems Page: 2 of 5 Policy: System Security

Ministry of Finance, Provincial Comptroller’s Office

• Restrict access to systems security software and related documentation to authorized personnel.

• Ensure documents, reports and files are placed in adequate storage facilities when not in use and sensitive data is locked up.

• Ensure hardware facilities are physically protected from unauthorized access and deliberate loss or damage.

Service Bureau .04 Ministries are to ensure the requirements of Treasury Board Security Guidelines policies and Provincial Comptroller’s directives are met when

using an information technology service bureau. Contracts with an information technology service bureau should specify adequate security requirements. The contract should require the service bureau to notify the ministry of any changes in the manner in which they are meeting the ministry’s requirements.

Service Bureau .05 Security requirements included in a contract with a service Contract bureau may include:

• organization security controls and administration for

development of policies and procedures to protect facilities, operations and information;

• system access controls for authorizing users and following up unauthorized access and security violations;

• system software controls over development, testing, implementation and documentation of new software and software modifications;

• data communications controls over access and changes to the data communications network through dial back procedures;

• facilities controls restricting access to facilities, physical security (smoke and moisture detectors, air conditioning) over hardware, software and files, proper disposal of confidential waste;

• computer operations controls to prevent/detect processing errors and unauthorized changes;

• personnel controls over segregation of duties, supervision and procedures for hiring, training and terminating employees;

• backup, storage, recovery controls and contingency plans including manual operations;

• resource list of alternate service bureaus capable of handling information processing;

Financial Administration Manual

Part: Financial Management and Administration Number: 4025 Section: Treasury Board’s Risk Management Policies Date: 2010-01-25 Subsection: Financial Systems Page: 3 of 5 Policy: System Security

Ministry of Finance, Provincial Comptroller’s Office

• time frame for restoration of processing applications; • virus protection; • insurance protection program of the service bureau

(although alone, insurance is not deemed to be protection); and

• other controls as deemed necessary and documented in the contract.

.06 The contract with the service bureau should provide for

periodic independent security reviews of the service bureau every three years, with an internal memorandum annually. The security review may involve:

• the service bureau providing the ministry with an

independent security audit report; and/or • the ministry conducting their own review, either through

internal staffing or hiring a third party.

A single audit of a service bureau whose services are contracted by several ministries will be satisfactory.

.07 Ministries should receive a copy of the contracted service

bureau’s financial statements and auditor’s reports annually. .08 The above list of requirements may be included in the standard

Request for Proposal package, as minimum requirements for doing business with the Government, when tendering for service bureau services.

Disaster Recovery .09 Ministries should ensure that critical business processes can be

resumed after operations have been interrupted. The following techniques are used:

• All information and resources required to resume

processing are backed up and stored off site. There should be sufficient off site backup storage of critical systems, data, transactions, files, supplies, documentation and special forms required to allow users to resume operations in the event of interruption.

• Prepare, maintain and periodically test a disaster recovery plan which documents actions to be taken to restore processing on a timely basis. Include procedures in this plan to:

Financial Administration Manual

Part: Financial Management and Administration Number: 4025 Section: Treasury Board’s Risk Management Policies Date: 2010-01-25 Subsection: Financial Systems Page: 4 of 5 Policy: System Security

Ministry of Finance, Provincial Comptroller’s Office

• identify data that has been lost in a processing disruption;

• restore and maintain alternate processing; and • recover processing at the original site.

.10 Ministries are to consider the degree of criticality for

restoration of system processing in determining an acceptable time frame for restoration of system processing. Critical financial systems are those for which a disruption in processing would result in an impairment in the ability to manage financial resources, assets or liabilities under the ministry’s control. Critical financial systems are those where senior management responsible for the system believes that a system disruption would result in one or more of the following:

• loss of substantial revenue or a prolonged delay in

collecting revenues; • significant adverse effect on cash flow; • inability to produce management or financial information

essential to managing a program; • inability to obtain essential goods or services or make

required payments; • inability to meet legislative requirements; • substantial idle staff; and/or • inability to process a backlog when processing is restored.

.11 Critical financial systems must be capable of being restored to

operation either through access to an alternate processing facility or through alternate means such as the implementation of a manual system on a temporary basis.

.12 Non-critical financial systems are subject to a less stringent

requirement to restore processing. It may be acceptable to implement a totally manual backup system or to discontinue processing for a period of time, if the consequences are not significant.

.13 The permanent head of the ministry approves the disaster

recovery plan. .14 Personnel are to receive adequate training and supervision in

emergency backup and recovery procedures.

Financial Administration Manual

Part: Financial Management and Administration Number: 4025 Section: Treasury Board’s Risk Management Policies Date: 2010-01-25 Subsection: Financial Systems Page: 5 of 5 Policy: System Security

Ministry of Finance, Provincial Comptroller’s Office

.15 Ministries should document the required organizational responsibilities to regain normal operation on a timely basis and store it off site.

.16 Ministries are to identify applications that will be given top

priority in reconstruction.

References 4000 Financial Systems 4005 Acquisition of Financial Systems 4010 Development of Financial Systems 4015 Approval of Financial Systems 4020 System Processing Controls

Financial Administration Manual

Part: Financial Management and Administration Number: 4100 Section: Treasury Board’s Risk Management Policies Date: 2012-08-27 Subsection: Other Risk Management Policies Page: 1 of 1

Ministry of Finance, Provincial Comptroller’s Office

Other Risk Management Policies

Background In the direct and indirect delivery of the Government’s programs and services, losses arising from exposure to various risks may occur. Risk management involves identifying risks and taking steps to minimize their potential impact.

Authority The Financial Administration Act, 1993 (FAA) allows Treasury Board

to make orders and issue directives with respect to its duties under section 4 of the FAA (e.g., relating to the finances, the administrative policy and management practices, and the accounting policies and practices of the Government) (clause 5(a)).

The FAA allows the Provincial Comptroller to issue directives detailing the manner in which Treasury Board orders and directives are to be complied with (subsection 10(2)).

Treasury Board Policies Treasury Board has approved the following risk management policies:

• Section 4101 Incidents of Suspected Fraud or Similar Illegal Acts • Section 4102 Employee Onus to Report Suspected Fraud or

Similar Illegal Acts • Section 4105 Reporting Incidents of Fraud or Similar Illegal Acts; • Section 4110 Compensation for Loss Payments; • Section 4115 Fidelity Bond; • Section 4120 Employee Liability Protection; and • Section 4125 Insurance.

Applicability These policies apply to ministries, except for Section 4105 Reporting Incidents of Fraud or Similar Illegal Acts and Section 4115 Fidelity Bond, which have a wider application.

Financial Administration Manual

Part: Financial Management and Administration Number: 4101 Section: Treasury Board’s Risk Management Policies Date: 2012-08-27 Subsection: Other Risk Management Policies Page: 1 of 8 Policy: Incidents of Suspected Fraud or Similar Illegal Acts

Ministry of Finance, Provincial Comptroller’s Office

Incidents of Suspected Fraud or Similar Illegal Acts

Objective The objective is to help safeguard the Government’s money, property, and information.

Authority The Financial Administration Act, 1993, clauses 5(a) and subsection 10(2)

Applicability This policy applies to ministries concerning suspected or confirmed

incidents of fraud or similar illegal acts:

• by employees appointed under The Public Service Act, 1998 and individuals employed on personal service and fee-for-service contracts with ministries of the Government of Saskatchewan;

• by clients, suppliers, contractors or other third parties. In this policy, fraud is defined as the use of deception with the intent of obtaining an advantage, avoiding an obligation or causing a loss to another party. The term is used to describe such acts as theft, false representation, misappropriation, bribery and corruption. This policy does not apply to acts of negligence or poor performance by employees, which should be addressed through normal human resource management processes.

Background Fraud and similar illegal acts committed against the Government are costly. These acts can result in economic losses, misuse of private or confidential information, and disruption of programs and services. They can reduce employee morale, create recruitment problems, and bring disrepute to the public service and the Government. No organization is immune from fraud or similar illegal acts and no system of controls can provide absolute assurance that such acts will not occur. However, the Government is accountable to taxpayers for ensuring effective and efficient programs and services and safeguarding public money, property, and information. Safeguarding these assets includes implementing policies and procedures to prevent and detect fraud or similar illegal acts.

Treasury Board Policy .01 Ministries are to emphasize an ethical and positive work environment which promotes honesty, integrity, respect, service excellence and accountability.

.02 Ministries are to maintain adequate systems and controls to

Financial Administration Manual

Part: Financial Management and Administration Number: 4101 Section: Treasury Board’s Risk Management Policies Date: 2012-08-27 Subsection: Other Risk Management Policies Page: 2 of 8 Policy: Incidents of Suspected Fraud or Similar Illegal Acts

Ministry of Finance, Provincial Comptroller’s Office

prevent and detect fraud and similar illegal acts. .03 The Government maintains a zero tolerance policy towards

fraud and similar illegal acts. Zero tolerance means ministries are to investigate all suspected incidents of fraud or similar illegal acts and take appropriate disciplinary and legal action in all confirmed cases.

Provincial Comptroller Directives Employee .04 Employees are required to act lawfully and in accordance with Responsibilities government policies and directives. .05 Any employee who has knowledge of a suspicious incident within the Government of Saskatchewan, which may

involve fraud or similar illegal activity, shall report it immediately, as outlined in Section 4102 Employee Onus to Report Suspected Fraud or Similar Illegal Acts.

Ministry .06 Ministries have primary responsibility for preventing and Responsibilities detecting fraud and similar illegal acts.

.07 Fraud and similar illegal acts occur when individuals are motivated by personal and work pressures, have opportunity to commit the acts and are able to rationalize or provide justification for their behaviour.

.08 Ministries reduce the likelihood of fraud and similar illegal acts

by developing and maintaining:

• an ethical and positive work environment; • a sound system of internal controls; and • proper and consistent oversight.

.09 Senior management sets the “tone at the top” by modelling the

attitude and conduct which they expect their employees to display. They are responsible for fostering an ethical climate and positive workplace, which emphasizes honesty, integrity, respect, service excellence and accountability.

.10 It is critical that ministries take reasonable steps, through

training and other communication methods, to ensure that employees are aware of and understand the policies which affect them. This includes internal ministry policies and

Financial Administration Manual

Part: Financial Management and Administration Number: 4101 Section: Treasury Board’s Risk Management Policies Date: 2012-08-27 Subsection: Other Risk Management Policies Page: 3 of 8 Policy: Incidents of Suspected Fraud or Similar Illegal Acts

Ministry of Finance, Provincial Comptroller’s Office

government-wide policies on financial, human resources, information technology, legal and purchasing matters. Particular emphasis should be placed on fraud awareness training, the Government’s zero-tolerance fraud policy and the policy requirement for employees to report suspicions of fraud or similar illegal acts.

.11 Ministries are to design their system of internal controls to fit

their programs and operations. The system should consider the principal risks, the costs to implement controls and existing government policies and directives, particularly the Financial Administration Manual. Specific controls which are important to the prevention and detection of fraud include:

• segregation of duties; • regular and timely accounting reconciliations (e.g., bank

reconciliations); • physical safeguards over money and property (e.g., safes

and locked cabinets, restricted access to inventories); • effective supervision; • effective information system security (e.g., passwords,

encryption, console logs, network security controls, backup); and

• appropriate and current delegations of authority. .12 It is not sufficient to develop and document adequate anti-fraud

controls and processes. Ministries must ensure they are in place and operating as intended. Controls should be monitored through such means as internal audits, review of variance and exception reports by management and general oversight by senior officials. Deficiencies detected should be fixed and controls and processes modified as required.

.13 If incidents of fraud or similar illegal acts occur, managers will

be subject to appropriate discipline if they failed to provide adequate supervision or direction, failed to take appropriate action or condoned improper conduct.

.14 When incidents of suspected fraud or similar illegal acts are

identified, ministries are responsible for investigating all incidents. Ministries are expected to:

• take disciplinary action against employees, which may

include termination and legal action;

Financial Administration Manual

Part: Financial Management and Administration Number: 4101 Section: Treasury Board’s Risk Management Policies Date: 2012-08-27 Subsection: Other Risk Management Policies Page: 4 of 8 Policy: Incidents of Suspected Fraud or Similar Illegal Acts

Ministry of Finance, Provincial Comptroller’s Office

• proceed with legal action against other parties as recommended by legal advisors;

• pursue recovery of losses; and • implement corrective action to reduce the likelihood of

similar future incidents. .15 Ministries must comply with all applicable laws, policies,

directives and other authorities when investigating, reporting and following up incidents.

Examples of Fraud .16 Fraud or similar illegal acts may not necessarily result and Similar Illegal Activity in an actual loss.

Employee Examples Some examples of employee fraud or similar illegal acts are:

• falsification or alteration of financial records; • misuse of a government purchase card; • theft of government money or property; • unauthorized use of public resources; • misuse or corruption of government files or data; • claiming non-legitimate expenses or unworked hours; • intentional damage of government property; • accepting bribes or kickbacks.

Third Party Examples Some examples of external third party fraud or similar illegal

acts are: • theft of government money or property; • misuse or corruption of government files or data; • deliberate short-shipment by a supplier; • deliberate substitution of inferior quality or defective

goods by a supplier; • intentional damage of government property; • bid-rigging, price fixing, or kickbacks in the

contracting process; • fraudulent claims for social benefits, grants or other

program payments, including refunds and rebates.

Investigation .17 The permanent head or delegate for the ministry shall determine the next step for every reported allegation of wrongdoing.

.18 All incidents involving losses of money or property greater

than $500 must be reported promptly to the Provincial

Financial Administration Manual

Part: Financial Management and Administration Number: 4101 Section: Treasury Board’s Risk Management Policies Date: 2012-08-27 Subsection: Other Risk Management Policies Page: 5 of 8 Policy: Incidents of Suspected Fraud or Similar Illegal Acts

Ministry of Finance, Provincial Comptroller’s Office

Comptroller. See Section 4105 Reporting Incidents of Fraud or Similar Illegal Acts. Early consultation with ministry legal advisors and/or human resources personnel is also recommended but will depend on the particular circumstances.

.19 Ministries may consider contacting Risk Management

Services, Ministry of Central Services, which offers investigative services and security evaluations.

.20 Except in situations involving criminal acts where it is clear

that the police should be notified, ministries should consult with ministry legal advisors to determine whether the police should be notified for any loss over $500 which may have resulted from fraud or similar illegal acts. Ministries should consider contacting law enforcement authorities immediately if a police presence is a matter of urgency (such as incidents involving a theft or break-in) or where assistance is required to secure evidence.

.21 All allegations must be investigated to determine if a fraud or

similar illegal act has occurred. Ministries should exercise discretion, based on the nature and relative size of the incident, to determine the extent of the work to be undertaken.

.22 Ministries must ensure responsibility for investigations is clear.

This is typically done by assigning responsibility to an individual or an oversight committee. Investigations must be objective, regardless of the relationship with a third party or the position, work record or length of service of an employee.

.23 All participants in investigations are to keep the details confidential. Correspondence, reports and other documents related to suspected or actual cases of fraud are to be treated as confidential and kept in secure confidential files. Any issues related to confidentiality should be discussed with ministry legal advisors.

.24 A record of the investigation should be maintained, including details of pertinent telephone conversations, meetings and interviews, as well as working papers and results of audits and similar reviews.

.25 Where a preliminary investigation fails to substantiate that a

fraud or similar illegal act has taken place, the conclusion

Financial Administration Manual

Part: Financial Management and Administration Number: 4101 Section: Treasury Board’s Risk Management Policies Date: 2012-08-27 Subsection: Other Risk Management Policies Page: 6 of 8 Policy: Incidents of Suspected Fraud or Similar Illegal Acts

Ministry of Finance, Provincial Comptroller’s Office

should be documented and the permanent head or delegate should ensure it is communicated to the parties involved in the investigation (e.g., internal auditors, human resources, etc.). No further action is required.

.26 Where a preliminary investigation determines that there are reasonable grounds for an allegation, further work must be undertaken. Where an employee is involved, it may also be appropriate to consider suspending the employee against whom an allegation has been made. This may be with or without pay depending on the circumstances, and should only be done after consultation with appropriate human resources personnel.

.27 Upon completion of the investigation, a written report should be prepared which includes information such as background (e.g., nature of incident and circumstances which permitted it, description and amount of any losses, etc.), a summary of the investigation (e.g., work performed, including audits, interviews, police involvement, etc.), the conclusion and recommended actions (e.g., discipline, prosecution, recoveries, changes to operating practices to mitigate risk, etc.). The content of this report will depend on the particular circumstances.

.28 The report should be provided to the permanent head or

delegate who will determine additional distribution. A copy of this report should be provided to the Provincial Comptroller if the investigation concludes that a fraud or similar illegal act has been committed.

.29 Ministries may establish a standard investigation and reporting process for third party incidents of a more frequent nature related to the ministry’s normal operations. Ministries are still expected to ensure appropriate controls are in place to mitigate the risk of these kinds of losses.

Discipline .30 Where employee fraud or similar illegal activity is confirmed,

disciplinary action, up to and including dismissal, shall be considered by management, in consultation with appropriate human resources personnel. Action should be taken promptly, as any undue delay may adversely affect the right to impose discipline.

Financial Administration Manual

Part: Financial Management and Administration Number: 4101 Section: Treasury Board’s Risk Management Policies Date: 2012-08-27 Subsection: Other Risk Management Policies Page: 7 of 8 Policy: Incidents of Suspected Fraud or Similar Illegal Acts

Ministry of Finance, Provincial Comptroller’s Office

Legal Action .31 The Government’s general policy is to take appropriate legal action in all cases of illegal conduct. Legal action should be taken only after consultation with and approval from the Ministry of Justice. Where an employee is involved, the timing of the legal action need not coincide with internal disciplinary action.

Recovery of Losses .32 If a fraud or similar illegal act has been committed, all reasonable steps, including legal action, should be taken to recover any losses incurred by the Government.

.33 Where an employee is involved, ministries should also pursue

recovery under the Government’s Fidelity Bond. See Section 4115 Fidelity Bond.

Prevention of Future .34 When incidents of fraud or similar illegal acts occur, the Incidents ministry is responsible for taking steps to help prevent a similar

occurrence in the future. These steps include, but are not limited to, improvement of controls, reinforcement of existing policies and procedures, employee training and more careful supervision.

Communications .35 Any communications related to an allegation or investigation should be sensitive to any police investigation, and be in compliance with the privacy provisions of The Freedom of Information and Protection of Privacy Act. Ministries should consult with their legal advisors where there are questions.

.36 Media inquires should be handled by ministry personnel as determined by the permanent head. Ministries should coordinate any external communications with Communications Counselling with Executive Council.

.37 Ministries are required to disclose illegal acts and certain fraud

information to the Provincial Auditor. Ministries should refer to their audit planning memorandum and consult with the Provincial Comptroller’s Office if they have questions.

.38 Ministries are responsible for communicating this policy to all

employees and ensuring a current copy is available for their reference.

Financial Administration Manual

Part: Financial Management and Administration Number: 4101 Section: Treasury Board’s Risk Management Policies Date: 2012-08-27 Subsection: Other Risk Management Policies Page: 8 of 8 Policy: Incidents of Suspected Fraud or Similar Illegal Acts

Ministry of Finance, Provincial Comptroller’s Office

References 4100 Other Risk Management Policies 4102 Employee Onus to Report Suspected Fraud or Similar Illegal

Acts 4105 Reporting Incidents of Fraud or Similar Illegal Acts 4110 Compensation for Loss Payments 4115 Fidelity Bond 4120 Employee Liability Protection 4125 Insurance 4210 Personal Service Contracts

Fraud Awareness (Government Training) Appendix F Summary of Delegations

The Collective Bargaining Agreement between The Government of Saskatchewan and Saskatchewan Government and General Employees’ Union The Union Management Agreement between The Government of Saskatchewan and The Canadian Union of Public Employees, Local 600-3 Saskatchewan Public Service Commission Human Resource Manual, PS 803 Corrective Discipline Policy, PS 816 Criminal Records Check Policy, PS 1103 Information Technology - Acceptable Usage The Freedom of Information and Protection of Privacy Act The Public Interest Disclosure Act The Public Interest Disclosure Regulations The Public Sevice Regulations, 1999, including Oath or Declaration of Office Website: Information Technology Office – Security https://taskroom.sp.saskatchewan.ca/Pages/IT-Security-Services.aspx

Financial Administration Manual

Part: Financial Management and Administration Number: 4102 Section: Treasury Board’s Risk Management Policies Date: 2010-01-25 Subsection: Other Risk Management Policies Page: 1 of 3 Policy: Employee Onus to Report Suspected Fraud or Similar Illegal Acts

Ministry of Finance, Provincial Comptroller’s Office

Employee Onus to Report Suspected Fraud or Similar Illegal Acts

Objective The objective is to outline the expectations of employees in the reporting of suspected fraud or similar illegal acts.

Authority The Financial Administration Act, 1993, clauses 5(a) and subsection 10(2)

Applicability This policy applies to ministry employees appointed under The Public

Service Act, 1998, and individuals employed on personal service and fee-for-service contracts with ministries of the Government of Saskatchewan.

In this policy, fraud is defined as the use of deception with the intent

of obtaining an advantage, avoiding an obligation or causing a loss to another party. The term is used to describe such acts as theft, false representation, misappropriation, bribery and corruption. This policy does not apply to acts of negligence or poor performance by employees, which should be addressed through normal human resource management processes.

Treasury Board Policy .01 Any employee who has knowledge of a suspicious incident within a ministry of the Government of Saskatchewan, which may involve a fraud or similar illegal act, shall report it immediately. This includes incidents which involve an employee, a client, a supplier, a contractor or other third party.

.02 No employee who has acted in good faith shall be subject to any reprisal for reporting, or proposing to report, a suspected fraud or similar illegal act.

Provincial Comptroller Directives Employee .03 Employees with knowledge of a suspicious incident within Responsibilities the Government of Saskatchewan, which may involve a fraud

or similar illegal act, should contact their immediate supervisor. The supervisor will then contact the permanent head or delegate for the ministry. Where there is reason to believe an employee’s supervisor may be involved, the employee should contact directly the permanent head, their delegate or the Director of Human Resources (or equivalent) for the ministry.

Financial Administration Manual

Part: Financial Management and Administration Number: 4102 Section: Treasury Board’s Risk Management Policies Date: 2010-01-25 Subsection: Other Risk Management Policies Page: 2 of 3 Policy: Employee Onus to Report Suspected Fraud or Similar Illegal Acts

Ministry of Finance, Provincial Comptroller’s Office

.04 Employees should provide as much relevant, factual detail as possible in their reports but should not undertake their own investigation to collect evidence or information.

.05 Allegations made under this policy are serious. Employees are responsible for respecting the reputations of individuals. Any malicious unfounded reports will be reviewed and considered for appropriate discipline of the reporting employee.

.06 Employees reporting suspicious incidents under this policy should treat the matter as confidential and not discuss it with anyone other than their immediate supervisor, the permanent head (or their delegate) or the Director of Human Resources (or

equivalent) for the ministry. Ministry .07 The permanent head or delegate for the ministry shall Responsibilities determine the next step for every reported allegation of

wrongdoing. All allegations of fraud or similar illegal acts must be investigated. See Section 4101 Incidents of Suspected Fraud or Similar Illegal Acts. Also, see Section 4105 Reporting Incidents of Fraud or Similar Illegal Acts for specific reporting requirements.

.08 At the completion of an investigation, ministries may advise employees reporting suspicious incidents under this policy, that no wrong doing was found or that their report was acted upon. However, specific details should not be provided.

Confidentiality .09 Reasonable measures shall be taken to maintain confidentiality and to protect, to the extent possible, the identity of employees reporting suspected offenses under this policy. Ministries should consult with their legal advisors where disclosure is necessary to conduct an effective investigation, for disciplinary or legal proceedings, or where there are questions related to privacy or freedom of information requests.

Employee Protection .10 No employee who has acted in good faith shall be subject to any reprisal for reporting, or proposing to report, a suspected fraud or similar illegal act under this policy. Prompt action, including appropriate disciplinary action, will be taken in response to any harassment, discrimination or other retaliation.

Financial Administration Manual

Part: Financial Management and Administration Number: 4102 Section: Treasury Board’s Risk Management Policies Date: 2010-01-25 Subsection: Other Risk Management Policies Page: 3 of 3 Policy: Employee Onus to Report Suspected Fraud or Similar Illegal Acts

Ministry of Finance, Provincial Comptroller’s Office

.11 Protection from employer reprisal for individuals reporting unlawful conduct is provided in section 74 of The Labour Standards Act.

.12 Any employee who reasonably believes that he/she is being

subjected to retaliation by another employee, including their supervisor, as a result of reporting or proposing to report a suspected offense under this policy, should contact the permanent head (or their delegate), the Director of Human Resources (or equivalent) for the ministry or their union representative.

.13 Employee questions regarding this policy should be directed to the employee’s immediate supervisor or to the permanent head or delegate for the ministry.

.14 Ministries are responsible for communicating this policy to all

employees and ensuring a current copy is available for their reference.

References 4100 Other Risk Management Policies 4101 Incidents of Suspected Fraud or Similar Illegal Acts 4105 Reporting Incidents of Fraud or Similar Illegal Acts 4210 Personal Service Contracts

Fraud Awareness (Government Training)

The Collective Bargaining Agreement between The Government of Saskatchewan and Saskatchewan Government and General Employees’ Union The Union Management Agreement between The Government of Saskatchewan and The Canadian Union of Public Employees, Local 600-3

Saskatchewan Public Service Commission Human Resource Manual, PS 803 Corrective Discipline Policy

The Labour Standards Act The Freedom of Information and Protection of Privacy Act

The Public Sevice Regulations, 1999, including Oath or Declaration of Office

Financial Administration Manual

Part: Financial Management and Administration Number: 4105 Section: Treasury Board’s Risk Management Policies Date: 2018-05-31 Subsection: Other Risk Management Policies Page: 1 of 3 Policy: Reporting Incidents of Fraud or Similar Illegal Acts

Ministry of Finance, Provincial Comptroller’s Office

Reporting Incidents of Fraud or Similar Illegal Acts

Objective The objective is to outline reporting requirements for incidents of fraud or similar illegal acts involving money and property administered by ministries and Treasury Board Crowns.

Authority The Financial Administration Act, 1993, clauses 5(a) and 5(d) and

subsection 10(2) Applicability This policy applies to ministries and Treasury Board Crowns (see

Appendix B Public Agencies). Definition In this policy, fraud is defined as the use of deception with the intent

of obtaining an advantage, avoiding an obligation or causing a loss to another party. The term is used to describe such acts as theft, false representation, misappropriation, falsification of documents, bribery and corruption.

Treasury Board Policy .01 Ministries and Treasury Board Crowns are to maintain

adequate systems and controls to prevent and detect fraud and similar illegal acts.

.02 Ministries and Treasury Board Crowns are to report incidents

of fraud and similar illegal acts to the proper authorities.

Provincial Comptroller .03 Ministries and Treasury Board Crowns are responsible for Directives investigating, reporting and taking follow-up action on

incidents of fraud or similar illegal acts. Ministries should refer to Section 4101 Incidents of Suspected Fraud or Similar Illegal Acts and Section 4102 Employee Onus to Report Suspected Fraud or Similar Illegal Acts.

Police Involvement .04 Except in situations involving criminal acts where it is clear

that the police should be notified, ministries and Treasury Board Crowns should consult with legal advisors to determine whether the police should be notified for any loss over $500 which may have resulted from fraud or similar illegal acts. Ministries and Treasury Board Crowns should consider contacting law enforcement authorities immediately if a police presence is a matter of urgency (such as incidents involving a theft or break-in) or where assistance is required to secure evidence.

Financial Administration Manual

Part: Financial Management and Administration Number: 4105 Section: Treasury Board’s Risk Management Policies Date: 2018-05-31 Subsection: Other Risk Management Policies Page: 2 of 3 Policy: Reporting Incidents of Fraud or Similar Illegal Acts

Ministry of Finance, Provincial Comptroller’s Office

Provincial Comptroller’s .05 Ministries and Treasury Board Crowns are to notify the Office Involvement Provincial Comptroller of all losses of money or property over

$500 that are due to fraud or similar illegal acts. This includes special purpose funds and trust funds they administer.

When reporting the incident, the following information should be provided:

• the nature of the incident, including when and how the

incident was detected and the time period over which the incident occurred;

• if employees were involved, the position and the location/branch of the employee and if any disciplinary action was taken;

• the amount of the loss; • preventative and detective controls that would have

reduced the risk of loss; • the action that management is taking to correct any

deficiencies in internal controls; • insurance claims/recoveries; and • the police involvement.

.06 Losses reported to the Provincial Comptroller should be the

actual or estimated direct costs attributable to the incident excluding any costs related to the investigation, reporting and follow-up. Property damage or loss should be valued at the estimated cost to restore or replace the property to a pre-incident condition. All losses should be reported gross of any recoveries.

.07 Incidents should be reported to the Provincial Comptroller

promptly as soon as ministries and Treasury Board Crowns are able to determine:

• an incident of fraud or similar illegal act has likely

occurred; and • the actual or reasonable estimate of the loss exceeds $500.

.08 Notification of incidents should be made directly to the

Provincial Comptroller in writing (memo, fax, or e-mail). Report to PAC .09 Losses of money and property over $500 that have been

reported by ministries and Treasury Board Crowns, and that are

Financial Administration Manual

Part: Financial Management and Administration Number: 4105 Section: Treasury Board’s Risk Management Policies Date: 2018-05-31 Subsection: Other Risk Management Policies Page: 3 of 3 Policy: Reporting Incidents of Fraud or Similar Illegal Acts

Ministry of Finance, Provincial Comptroller’s Office

due to fraud or similar illegal acts by employees, suppliers or contractors are reported by the Provincial Comptroller to the Standing Committee on Public Accounts (PAC). Information related to other incidents may also be reported to PAC where the Provincial Comptroller deems that it would be in the public interest to do so.

Recovery of Losses .10 If a fraud or similar illegal act has been committed, all

reasonable steps, including legal action, should be taken to recover any losses incurred by the Government. Ministries and Treasury Board Crowns should determine if insurance exists and if there is potential for recovery. If so, they should proceed with a claim. Where an employee is involved, ministries should refer to Section 4115 Fidelity Bond.

Prevention of .11 When incidents of fraud or similar illegal acts occur, ministries Future Incidents and Treasury Board Crowns are responsible for taking steps to

help prevent a similar occurrence in the future. These steps include, but are not limited to, improvement of controls, reinforcement of existing policies and procedures, employee training and more careful supervision.

References 3112 Petty Cash and Cash Register Float Losses 4100 Other Risk Management Policies

4101 Incidents of Suspected Fraud or Similar Illegal Acts 4102 Employee Onus to Report Suspected Fraud or Similar Illegal

Acts 4110 Compensation for Loss Payments 4115 Fidelity Bond 4120 Employee Liability Protection 4125 Insurance

Financial Administration Manual

Part: Financial Management and Administration Number: 4110 Section: Treasury Board’s Risk Management Policies Date: 2018-05-31 Subsection: Other Risk Management Policies Page: 1 of 3 Policy: Compensation for Loss Payments

Ministry of Finance, Provincial Comptroller’s Office

Compensation for Loss Payments

Objective The objective is to outline the policy for providing compensation for loss payments.

Authority The Financial Administration Act, 1993, clause 5(a), subsection 10(2) Applicability This policy applies to ministries.

Treasury Board Policy .01 A Treasury Board Order is required for compensation for loss

payments not provided for in legislation or in accordance with the policy outlined in .02.

.02 Compensation for loss of personal property not otherwise

authorized may be approved by the permanent head in conjunction with their legal representative when the following criteria are met:

• reasonable compensation, not exceeding $1,000 for one

individual; • compensation is based on reasonable replacement cost

where supported by a receipt or other evidence that goods were replaced;

• if an employee, reimbursement is provided only where Workers’ Compensation Board reimbursement is not applicable;

• if an employee specifically required the item (of reasonable value) to perform their job, or the ministry specifically required the employee to place personal property at risk due to the nature of the employee’s duties; and

• if in-scope, conditions of employment are met. .03 Safekeeping of personal property is the employee’s

responsibility. Any items of a personal nature such as purses or radios kept in offices or at a worksite are kept at the employee’s risk.

Provincial Comptroller Directives Evaluating Requests .04 Determine if there is legislative authority for payment where

there is actual or implied responsibility of the ministry.

Financial Administration Manual

Part: Financial Management and Administration Number: 4110 Section: Treasury Board’s Risk Management Policies Date: 2018-05-31 Subsection: Other Risk Management Policies Page: 2 of 3 Policy: Compensation for Loss Payments

Ministry of Finance, Provincial Comptroller’s Office

.05 Consult with the ministry solicitor where responsibility is unclear and obtain a legal opinion where there are substantial claims.

.06 Ministries analyze each request to ensure it is reasonable and

that reasonable care has been taken to protect against the loss. .07 Ministries determine whether the loss is covered by insurance.

Refer to Section 4125 Insurance and Section 4115 Fidelity Bond for more information.

.08 Where the loss relates to personal property, require individuals

to use their own insurance when possible and reasonable. Ministries may pay individuals for their deductible.

.09 Ministries request the assistance of the Ministry of Justice in

cases involving a legal claim against the ministry. .10 Ministries are to determine whether the loss is covered by

Workers’ Compensation Policy No. POL 11/2016, which provides that the Workers’ Compensation Board may, in addition to any other compensation, assume the expense of the replacement or repair of broken dentures, eyeglasses, artificial eyes or artificial limbs when breakage is caused by an accident in the course of the worker’s employment.

.11 Ensure the police investigate all cases of suspected theft before

making a compensation payment. .12 The safekeeping of personal property, including cash, is the

responsibility of the individual and losses will be considered for reimbursement only under exceptional circumstances (e.g., hold-up, prison riot).

Compensation Payment .13 Prepare a Compensation for Loss Statement if responsibility

for payments is specifically covered by legislative authority. The Compensation for Loss Statement, which may be in any form, is retained with the payment documentation and includes at a minimum the following:

• date loss occurred or was discovered; • nature of loss, including a list of items; • summary of the incident; • names of parties and witnesses involved;

Financial Administration Manual

Part: Financial Management and Administration Number: 4110 Section: Treasury Board’s Risk Management Policies Date: 2018-05-31 Subsection: Other Risk Management Policies Page: 3 of 3 Policy: Compensation for Loss Payments

Ministry of Finance, Provincial Comptroller’s Office

• amount or value of loss; • authority for payment; • if there is an insurance claim; and • signature of the permanent head or delegate.

.14 Where a Treasury Board Order is required as per .01, the

permanent head requests, in writing, a Treasury Board Order that includes the steps taken to report and recover the loss, the vote and subvote to be charged as well as the information included on the Compensation for Loss Statement.

.15 The payee signs a waiver of further claim to losses, prior to

receiving compensation.