financial accounting and accounting...

TRANSCRIPT

Slide

9-1

Slide

9-2

Chapter 9

Plant Assets,

Natural Resources, and

Intangible Assets

Financial Accounting, IFRS Edition

Weygandt Kimmel Kieso

Slide

9-3

1. Describe how the cost principle applies to plant assets.

2. Explain the concept of depreciation.

3. Compute periodic depreciation using different methods.

4. Describe the procedure for revising periodic depreciation.

5. Distinguish between revenue and capital expenditures, and

explain the entries for each.

6. Explain how to account for the disposal of a plant asset.

7. Compute periodic depletion of extractable natural resources.

8. Explain the basic issues related to accounting for intangible

assets.

9. Indicate how plant assets, natural resources, and intangible

assets are reported.

Study Objectives

Slide

9-4

Plant Assets

Determining the

cost of plant

assets

Depreciation

Revaluation of

plant assets

Expenditures

during useful life

Plant asset

disposals

Natural

Resources

Intangible

Assets

Statement

Presentation and

Analysis

Presentation

Analysis

Accounting for

intangibles

Types of

intangibles

Research and

development

costs

Plant Assets, Natural Resources, and Intangible

Assets

Accounting for

extractable

natural resources

Financial

statement

presentation

Slide

9-5

“Used in operations” and not for resale.

Long-term in nature and usually depreciated.

Possess physical substance.

Plant assets include land, land improvements, buildings,

and equipment (machinery, furniture, tools).

Major characteristics include:

Section 1 – Plant Assets

Referred to as property, plant, and equipment; plant and

equipment; and fixed assets.

Slide

9-6

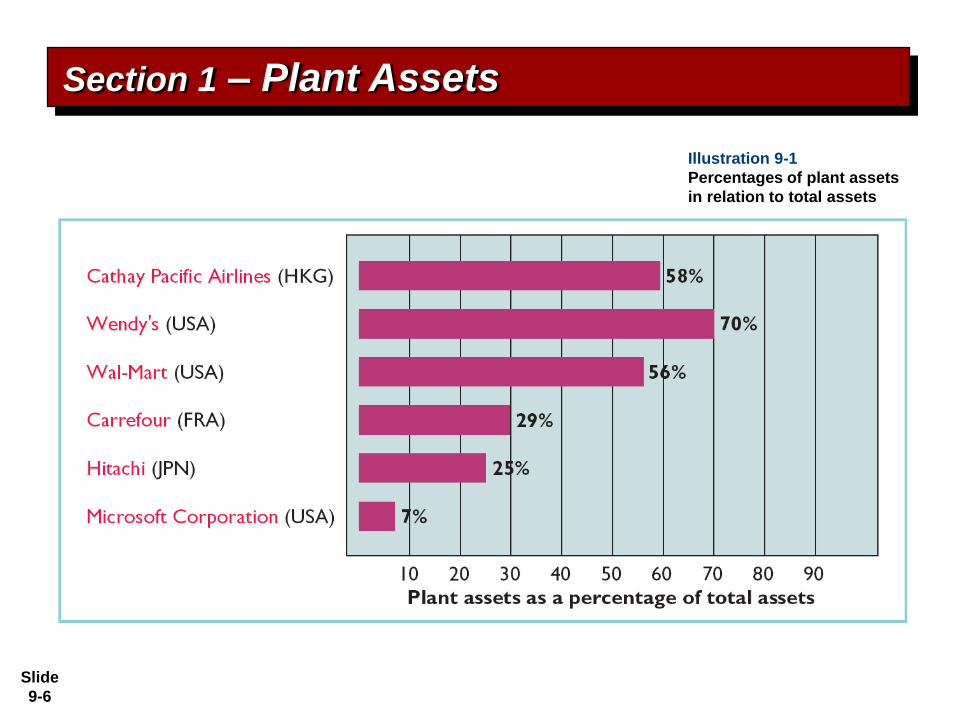

Section 1 – Plant Assets

Illustration 9-1

Percentages of plant assets

in relation to total assets

Slide

9-7

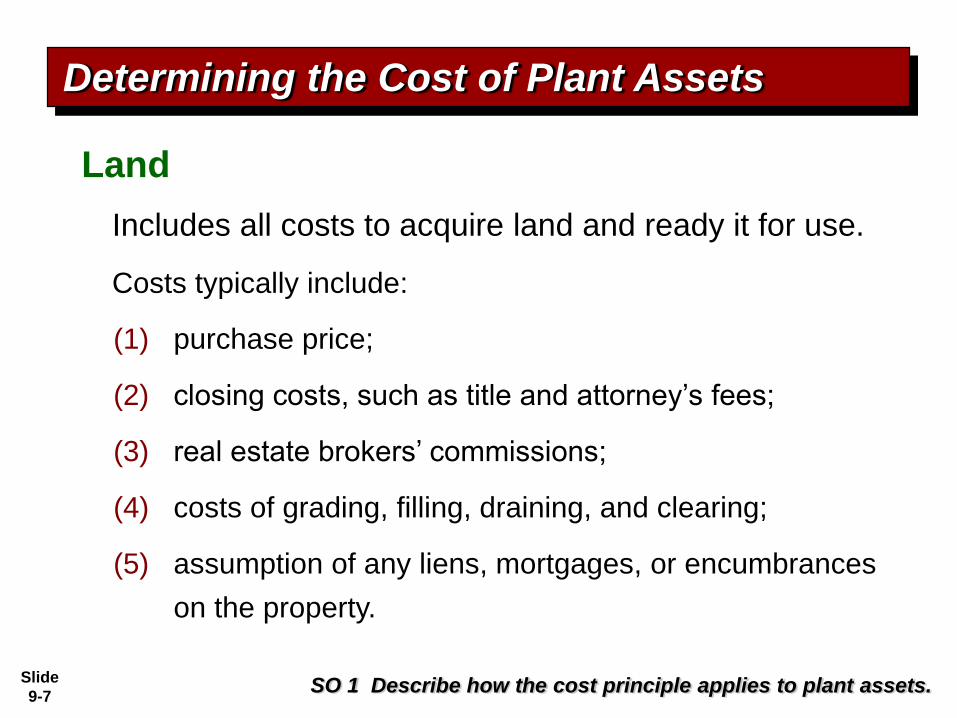

Includes all costs to acquire land and ready it for use.

Costs typically include:

Land

Determining the Cost of Plant Assets

(1) purchase price;

(2) closing costs, such as title and attorney’s fees;

(3) real estate brokers’ commissions;

(4) costs of grading, filling, draining, and clearing;

(5) assumption of any liens, mortgages, or encumbrances

on the property.

SO 1 Describe how the cost principle applies to plant assets.

Slide

9-8

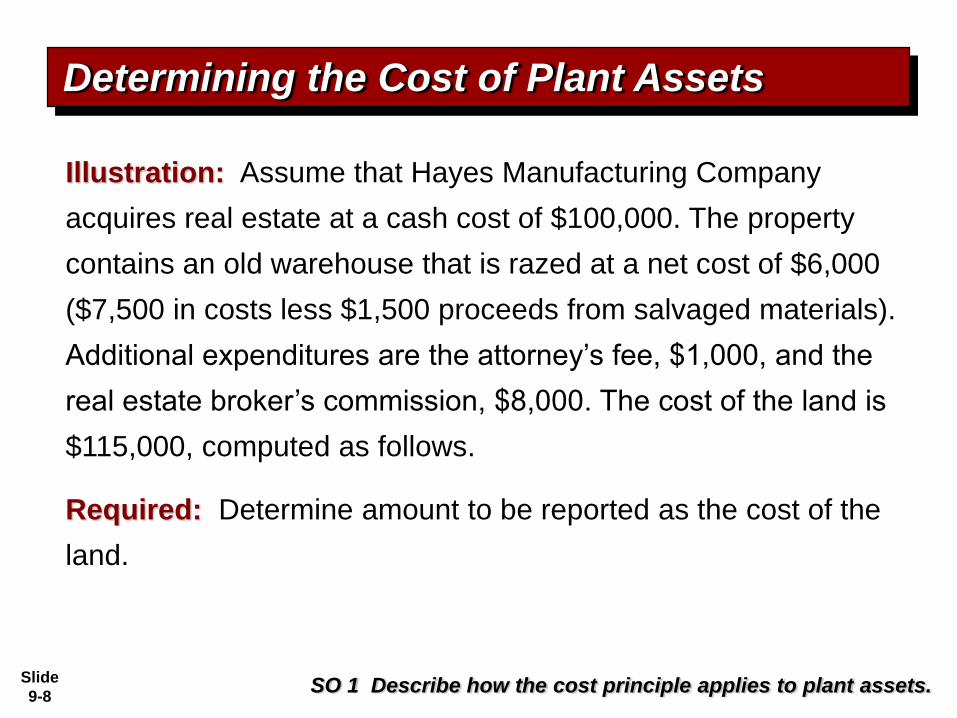

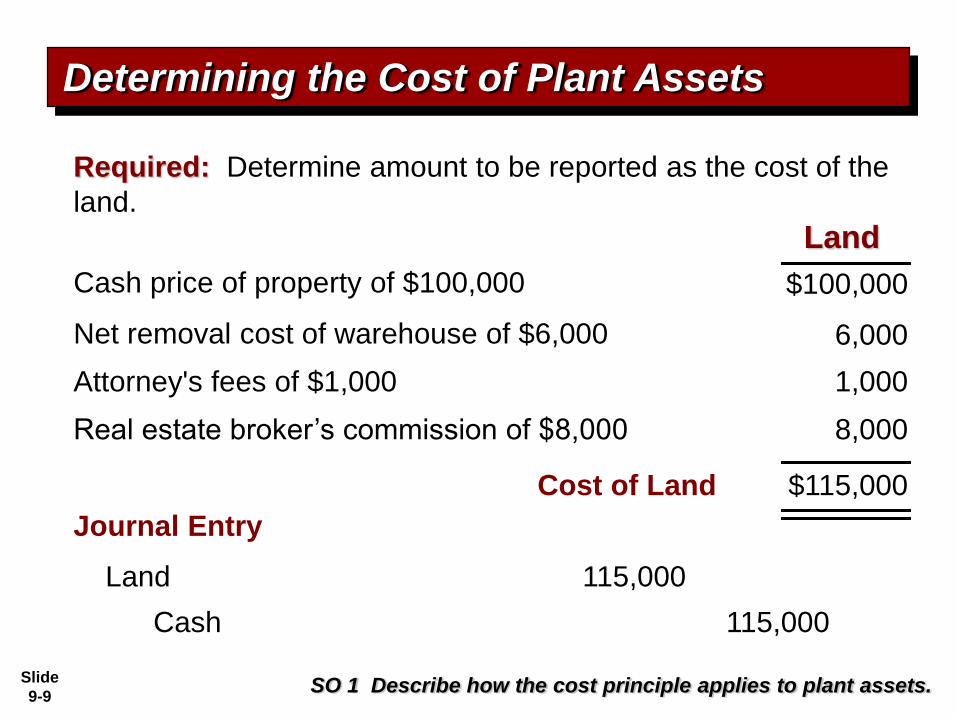

Illustration: Assume that Hayes Manufacturing Company

acquires real estate at a cash cost of $100,000. The property

contains an old warehouse that is razed at a net cost of $6,000

($7,500 in costs less $1,500 proceeds from salvaged materials).

Additional expenditures are the attorney’s fee, $1,000, and the

real estate broker’s commission, $8,000. The cost of the land is

$115,000, computed as follows.

Required: Determine amount to be reported as the cost of the

land.

Determining the Cost of Plant Assets

SO 1 Describe how the cost principle applies to plant assets.

Slide

9-9

Land

Required: Determine amount to be reported as the cost of the

land.

Determining the Cost of Plant Assets

SO 1 Describe how the cost principle applies to plant assets.

Cash price of property of $100,000

Net removal cost of warehouse of $6,000

Attorney's fees of $1,000 1,000

6,000

$100,000

$115,000Cost of Land

Real estate broker’s commission of $8,000 8,000

Land 115,000

Cash 115,000

Journal Entry

Slide

9-10

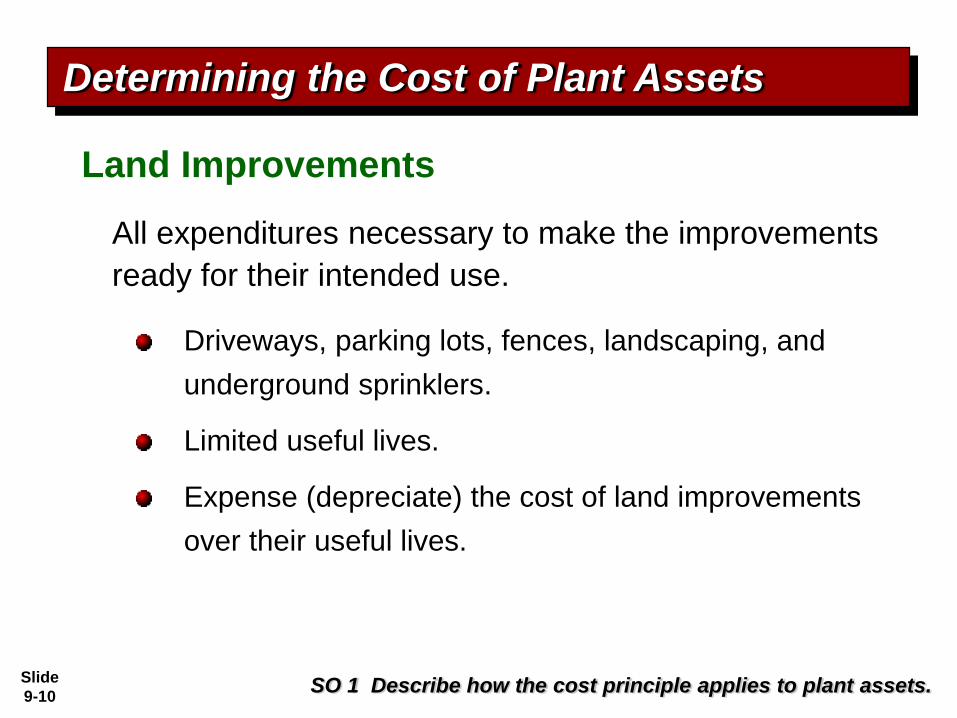

All expenditures necessary to make the improvements

ready for their intended use.

Land Improvements

Determining the Cost of Plant Assets

Driveways, parking lots, fences, landscaping, and

underground sprinklers.

Limited useful lives.

Expense (depreciate) the cost of land improvements

over their useful lives.

SO 1 Describe how the cost principle applies to plant assets.

Slide

9-11

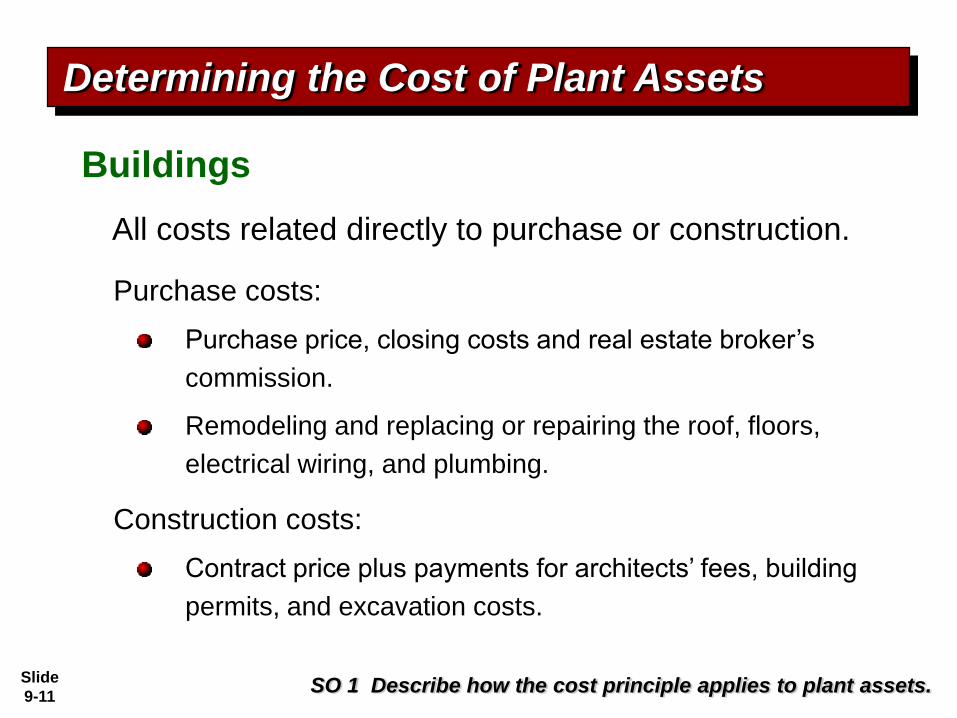

All costs related directly to purchase or construction.

Buildings

Purchase costs:

Purchase price, closing costs and real estate broker’s

commission.

Remodeling and replacing or repairing the roof, floors,

electrical wiring, and plumbing.

Construction costs:

Contract price plus payments for architects’ fees, building

permits, and excavation costs.

Determining the Cost of Plant Assets

SO 1 Describe how the cost principle applies to plant assets.

Slide

9-12

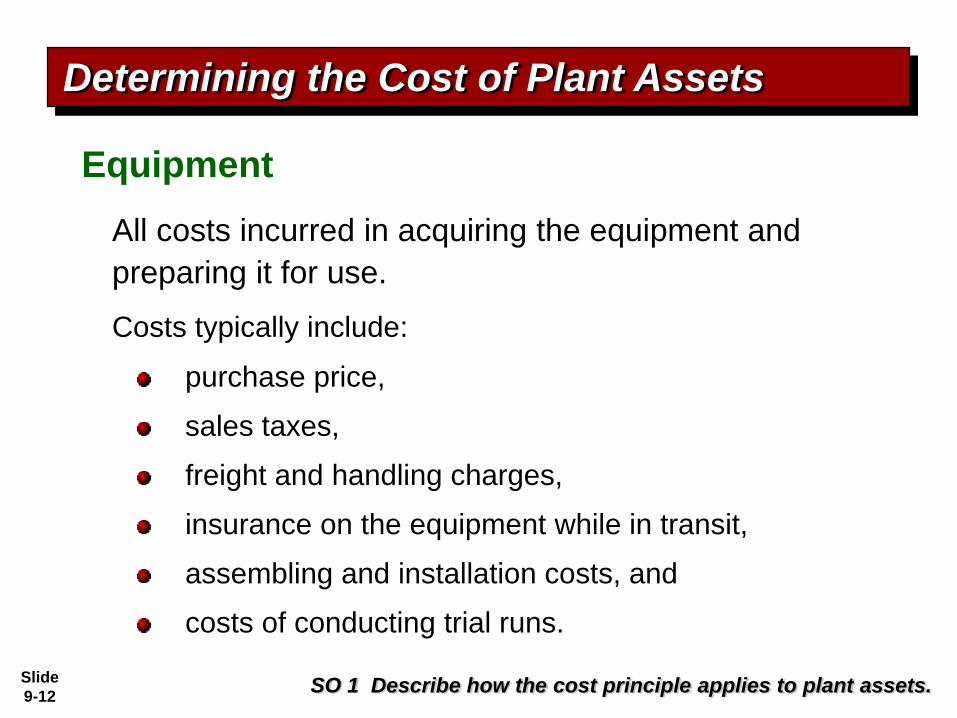

All costs incurred in acquiring the equipment and

preparing it for use.

Costs typically include:

Equipment

purchase price,

sales taxes,

freight and handling charges,

insurance on the equipment while in transit,

assembling and installation costs, and

costs of conducting trial runs.

Determining the Cost of Plant Assets

SO 1 Describe how the cost principle applies to plant assets.

Slide

9-13

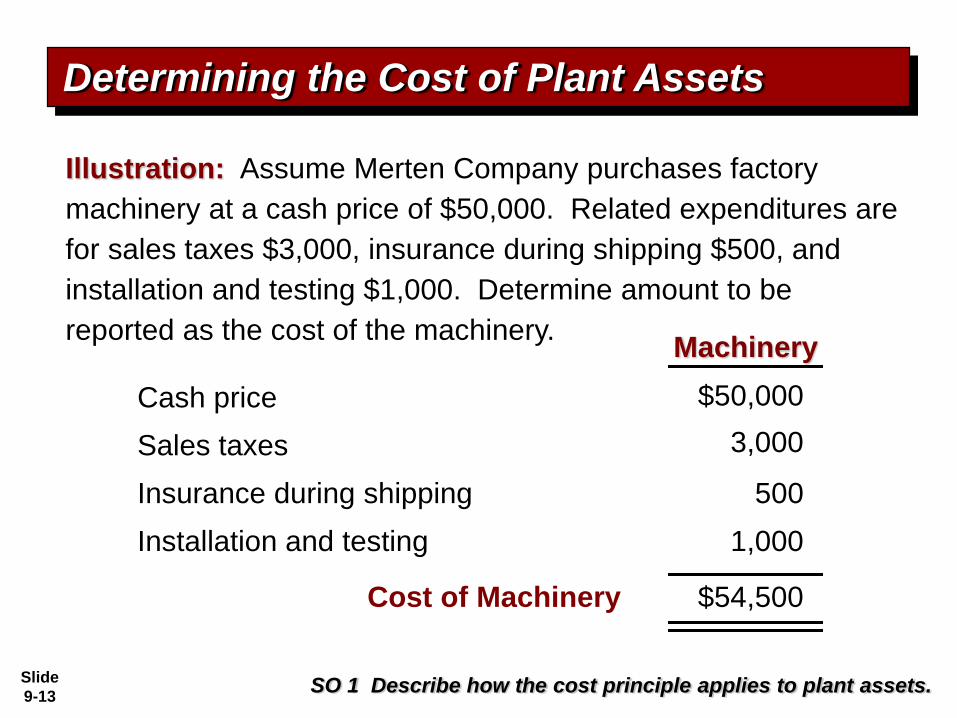

Illustration: Assume Merten Company purchases factory

machinery at a cash price of $50,000. Related expenditures are

for sales taxes $3,000, insurance during shipping $500, and

installation and testing $1,000. Determine amount to be

reported as the cost of the machinery.

Determining the Cost of Plant Assets

SO 1 Describe how the cost principle applies to plant assets.

Machinery

Cash price

Sales taxes

Insurance during shipping 500

3,000

$50,000

$54,500Cost of Machinery

Installation and testing 1,000

Slide

9-14Answer on notes page

Slide

9-15

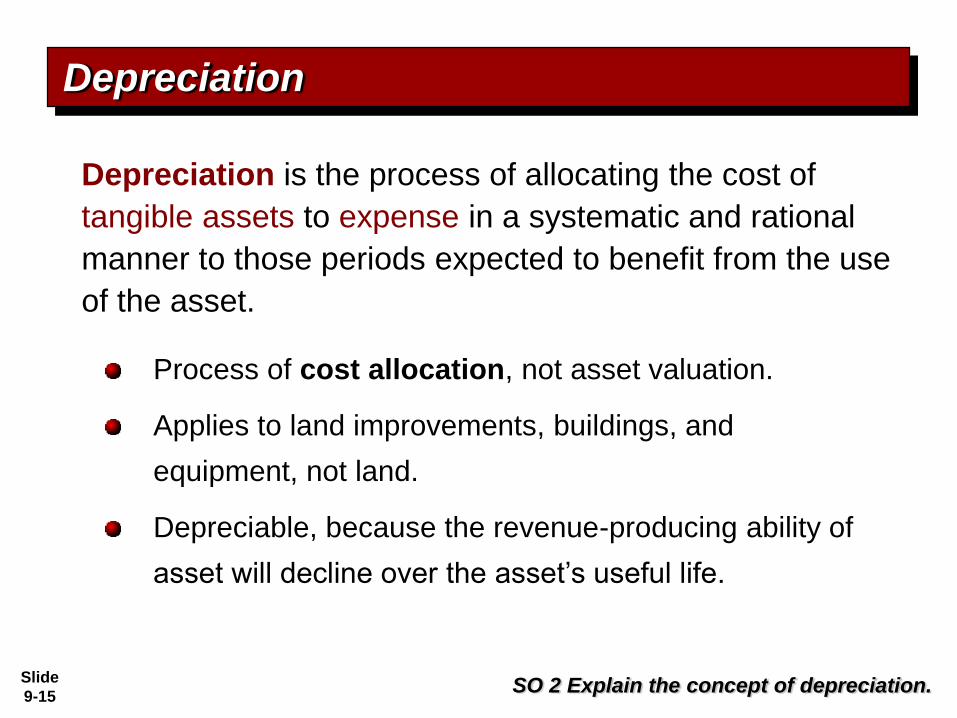

Process of cost allocation, not asset valuation.

Applies to land improvements, buildings, and

equipment, not land.

Depreciable, because the revenue-producing ability of

asset will decline over the asset’s useful life.

Depreciation is the process of allocating the cost of

tangible assets to expense in a systematic and rational

manner to those periods expected to benefit from the use

of the asset.

Depreciation

SO 2 Explain the concept of depreciation.

Slide

9-16

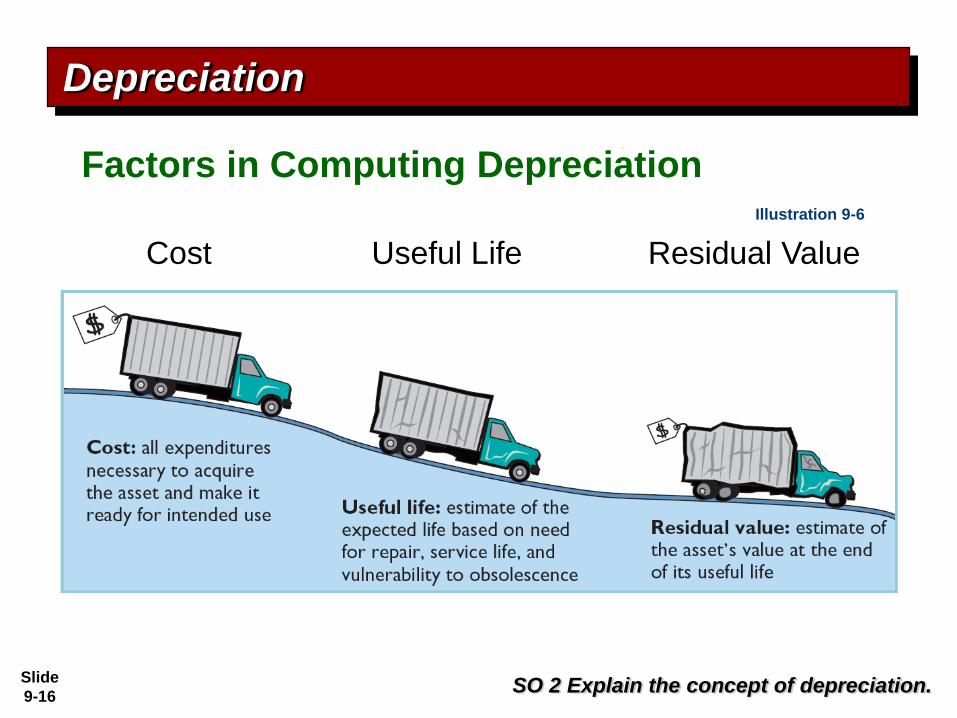

Factors in Computing Depreciation

Cost

Depreciation

SO 2 Explain the concept of depreciation.

Useful Life Residual Value

Illustration 9-6

Slide

9-17

Objective is to select the method that best measures an

asset’s contribution to revenue over its useful life.

Examples include:

Depreciation Methods

(1) Straight-line method.

(2) Units-of-Activity method.

(3) Declining-balance method.

Depreciation

SO 3 Compute periodic depreciation using different methods.

Slide

9-18

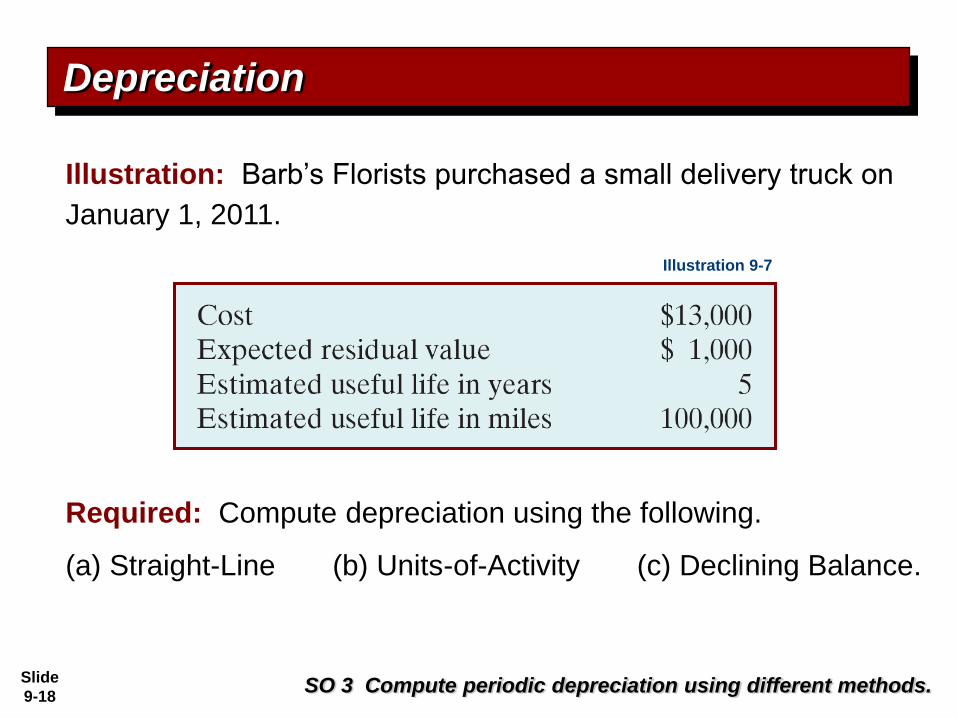

Illustration: Barb’s Florists purchased a small delivery truck on

January 1, 2011.

Required: Compute depreciation using the following.

(a) Straight-Line (b) Units-of-Activity (c) Declining Balance.

Depreciation

SO 3 Compute periodic depreciation using different methods.

Illustration 9-7

Slide

9-19

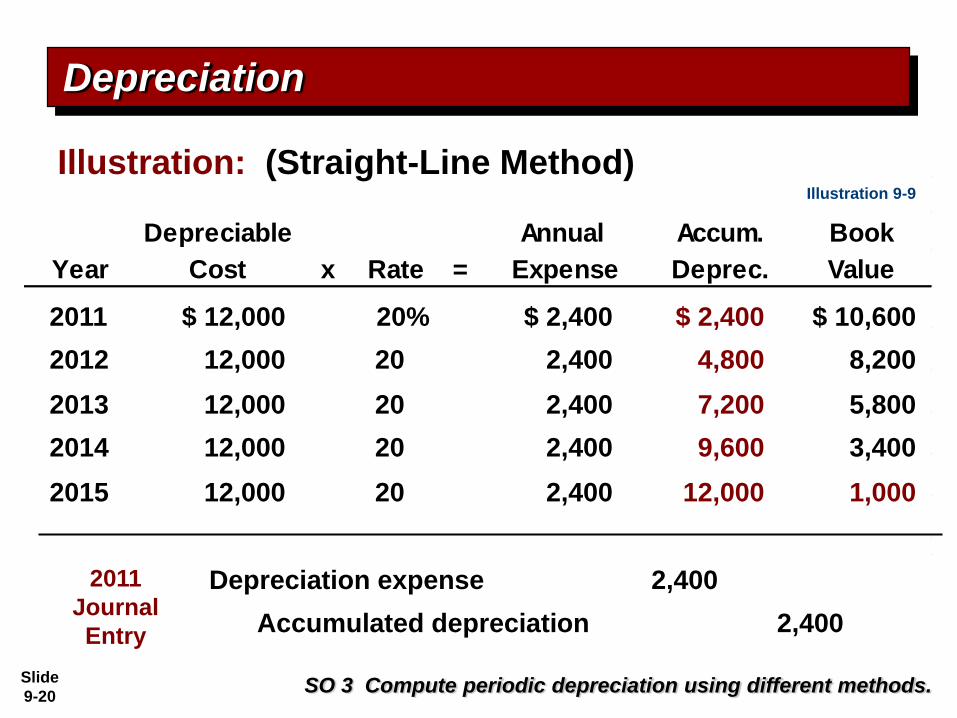

Straight-Line

Depreciation

SO 3 Compute periodic depreciation using different methods.

Expense is same amount for each year.

Depreciable cost - cost of the asset less its residual

value.Illustration 9-8

Slide

9-20

Depreciable Annual Accum. Book

Year Cost x Rate = Expense Deprec. Value

Depreciation

SO 3 Compute periodic depreciation using different methods.

Illustration: (Straight-Line Method)

2011 $ 12,000 20% $ 2,400 $ 2,400 $ 10,600

2012 12,000 20 2,400 4,800 8,200

2013 12,000 20 2,400 7,200 5,800

2014 12,000 20 2,400 9,600 3,400

2015 12,000 20 2,400 12,000 1,000

2011

Journal

Entry

Depreciation expense 2,400

Accumulated depreciation 2,400

Illustration 9-9

Slide

9-21

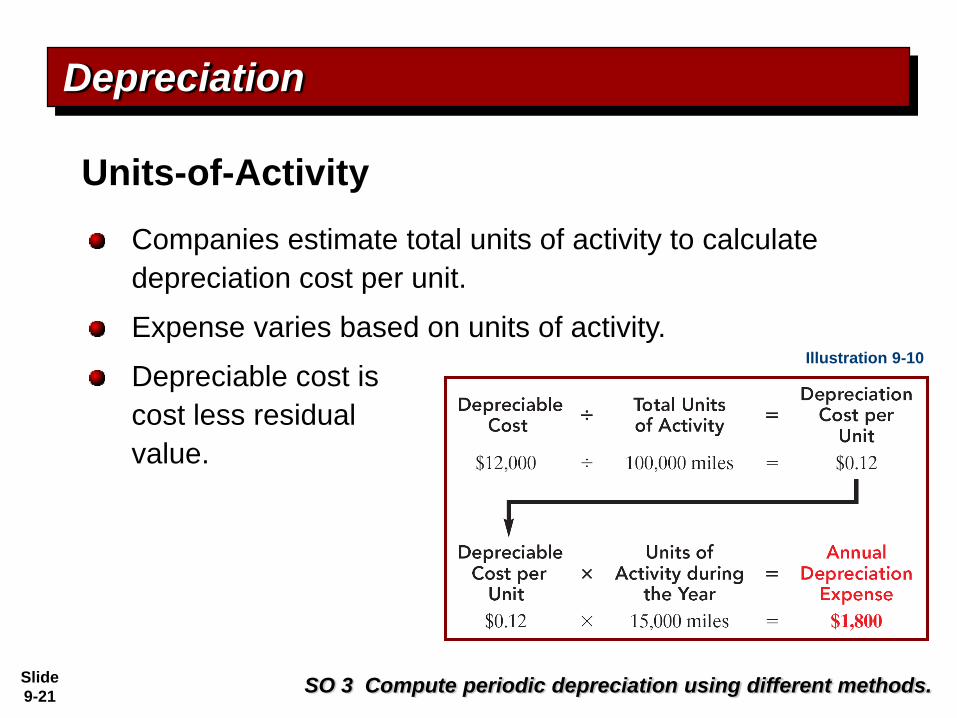

Companies estimate total units of activity to calculate

depreciation cost per unit.

Expense varies based on units of activity.

Depreciable cost is

cost less residual

value.

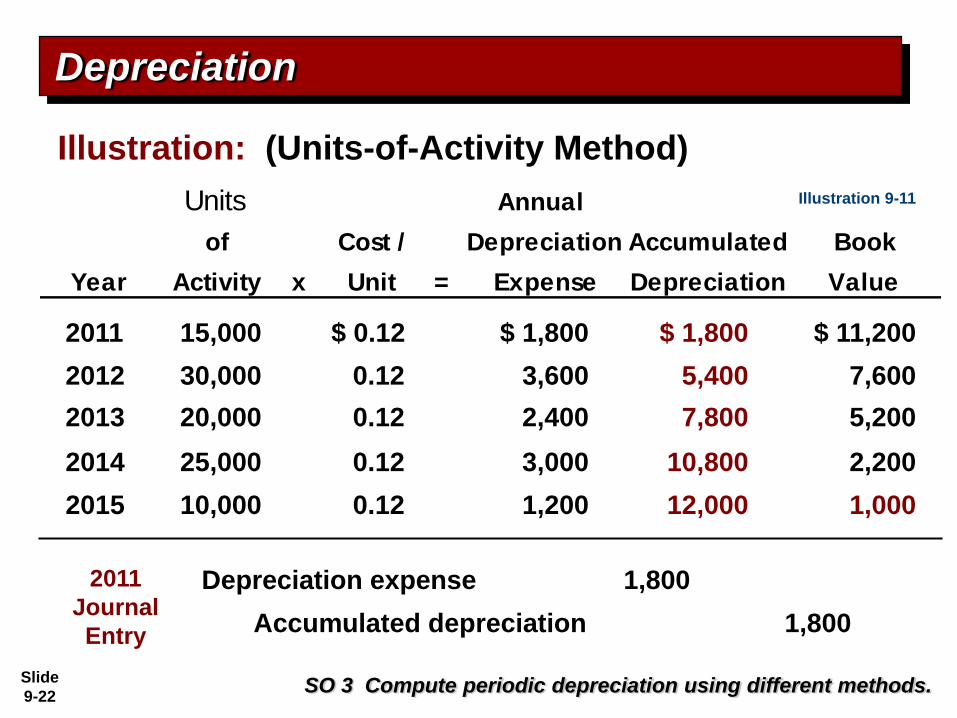

Units-of-Activity

Depreciation

SO 3 Compute periodic depreciation using different methods.

Illustration 9-10

Slide

9-22

Units Annual

of Cost / Depreciation Accumulated Book

Year Activity x Unit = Expense Depreciation Value

Depreciation

Illustration: (Units-of-Activity Method)

2011 15,000 $ 0.12 $ 1,800 $ 1,800 $ 11,200

2012 30,000 0.12 3,600 5,400 7,600

2013 20,000 0.12 2,400 7,800 5,200

2014 25,000 0.12 3,000 10,800 2,200

2015 10,000 0.12 1,200 12,000 1,000

Depreciation expense 1,800

Accumulated depreciation 1,800

2011

Journal

Entry

Illustration 9-11

SO 3 Compute periodic depreciation using different methods.

Slide

9-23

Decreasing annual depreciation expense over the asset’s

useful life.

Declining-balance rate is double the straight-line rate.

Rate applied to book value.

Declining-Balance

Depreciation

SO 3 Compute periodic depreciation using different methods.

Illustration 9-12

Slide

9-24

Declining Annual

Beginning Balance Deprec. Accum. Book

Year Book value x Rate = Expense Deprec. Value

Depreciation

Illustration: (Declining-Balance Method)

2011 13,000 40% $ 5,200 $ 5,200 $ 7,800

2012 7,800 40 3,120 8,320 4,680

2013 4,680 40 1,872 10,192 2,808

2014 2,808 40 1,123 11,315 1,685

2015 1,685 40 685* 12,000 1,000

* Computation of $674 ($1,685 x 40%) is adjusted to $685.

Depreciation expense 5,200

Accumulated depreciation 5,200

2011

Journal

Entry

Illustration 9-13

Slide

9-25SO 3 Compute periodic depreciation using different methods.

Comparison of Methods

Depreciation

Illustration 9-14

Illustration 9-15

Slide

9-26

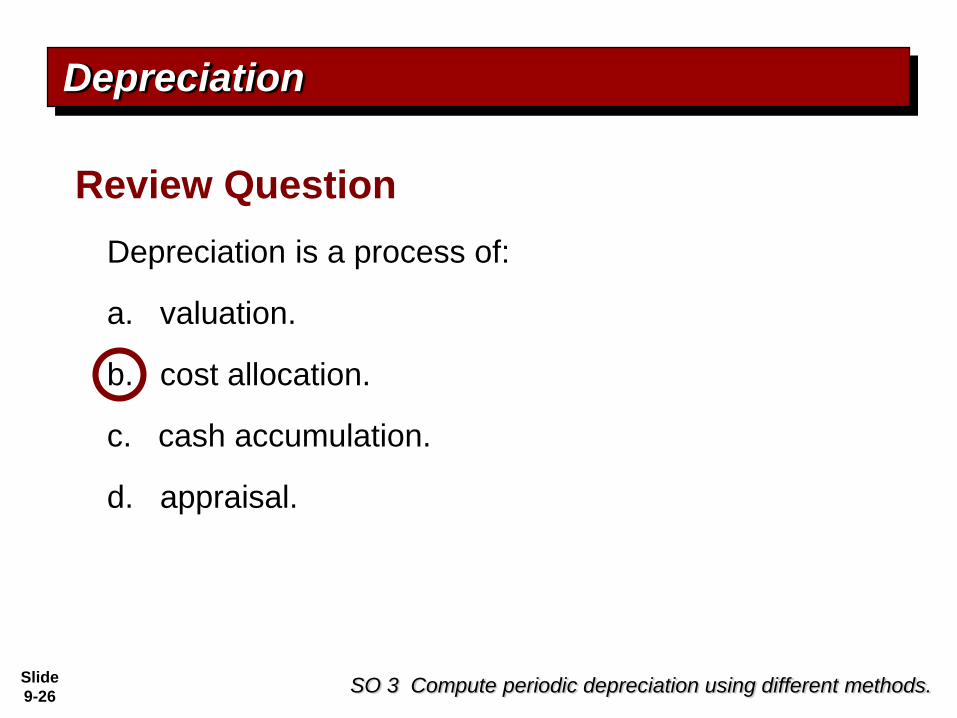

Depreciation is a process of:

a. valuation.

b. cost allocation.

c. cash accumulation.

d. appraisal.

Review Question

Depreciation

SO 3 Compute periodic depreciation using different methods.

Slide

9-27

The following four slides are included to illustrate the

calculation of partial-year depreciation expense.

The amounts are consistent with the previous slides

illustrating the calculation of depreciation expense.

Depreciation for Partial Year

SO 3 Compute periodic depreciation using different methods.

Slide

9-28

Illustration: Barb’s Florists purchased a small delivery truck on

October 1, 2011.

SO 3 Compute periodic depreciation using different methods.

Depreciation for Partial Year

Required: Compute depreciation using the following.

(a) Straight-Line (b) Units-of-Activity (c) Declining Balance.

Illustration 9-7

Slide

9-29

Current

Depreciable Annual Partial Year Accum.

Year Cost Rate Expense Year Expense Deprec.

2011 12,000$ x 20% = 2,400$ x 3/12 = 600$ 600$

2012 12,000 x 20% = 2,400 2,400 3,000

2013 12,000 x 20% = 2,400 2,400 5,400

2014 12,000 x 20% = 2,400 2,400 7,800

2015 12,000 x 20% = 2,400 2,400 10,200

2016 12,000 x 20% = 2,400 x 9/12 = 1,800 12,000

12,000$

Journal entry:

2011 Depreciation expense 600

Accumultated depreciation 600

Depreciation for Partial Year

SO 3 Compute periodic depreciation using different methods.

Illustration: (Straight-line Method)

Slide

9-30

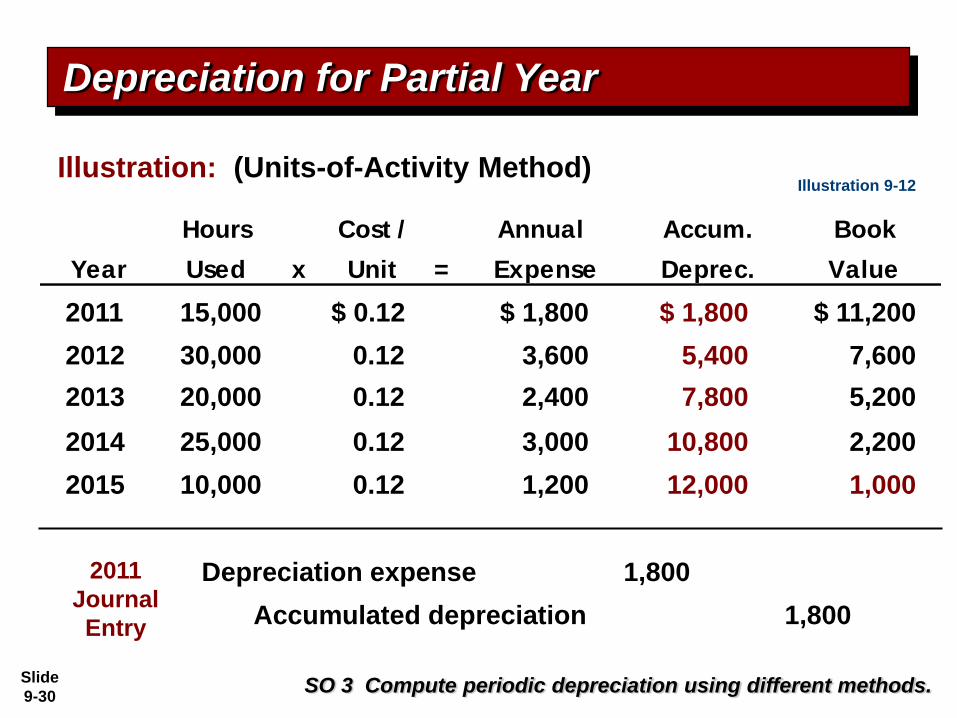

Hours Cost / Annual Accum. Book

Year Used x Unit = Expense Deprec. Value

Illustration: (Units-of-Activity Method)

2011 15,000 $ 0.12 $ 1,800 $ 1,800 $ 11,200

2012 30,000 0.12 3,600 5,400 7,600

2013 20,000 0.12 2,400 7,800 5,200

2014 25,000 0.12 3,000 10,800 2,200

2015 10,000 0.12 1,200 12,000 1,000

Depreciation expense 1,800

Accumulated depreciation 1,800

2011

Journal

Entry

Illustration 9-12

Depreciation for Partial Year

SO 3 Compute periodic depreciation using different methods.

Slide

9-31

Illustration: (Declining-Balance Method)

Declining Current

Beginning Balance Annual Partial Year Accum.

Year Book Value Rate Expense Year Expense Deprec.

2011 13,000$ x 40% = 5,200$ x 3/12 = 1,300$ 1,300$

2012 11,700 x 40% = 4,680 4,680 5,980

2013 7,020 x 40% = 2,808 2,808 8,788

2014 4,212 x 40% = 1,685 1,685 10,473

2015 2,527 x 40% = 1,011 1,011 11,484

2016 1,516 x 40% = 607 Plug 516 12,000

12,000$

Journal entry:

2011 Depreciation expense 1,300

Accumultated depreciation 1,300

Depreciation for Partial Year

SO 3 Compute periodic depreciation using different methods.

Slide

9-32

Tax laws often do not require the taxpayer to use the

same depreciation method on the tax return that is used

in preparing financial statements.

Many corporations use straight-line in their financial

statements to maximize net income. At the same time,

they use an accelerated-depreciation method on their

tax returns to minimize their income taxes.

Depreciation and Income Taxes

Depreciation

SO 3 Compute periodic depreciation using different methods.

Slide

9-33

Revising Periodic Depreciation

Accounted for in the period of change and future

periods (Change in Estimate).

Not handled retrospectively.

Not considered error.

Depreciation

SO 4 Describe the procedure for revising periodic depreciation.

Slide

9-34

Illustration: Assume that Barb’s Florists decides on January 1,

2014, to extend the useful life of the truck one year because of

its excellent condition. The company has used the straight-line

method to depreciate the asset to date, and book value is

$5,800 ($13,000 - $7,200).

Questions:

1. What is the journal entry to correct

the prior years’ depreciation?

2. Calculate the depreciation expense

for 2014.

No Entry Required

Depreciation

SO 4 Describe the procedure for revising periodic depreciation.

Slide

9-35

Depreciation

Depreciation expense 1,600

Accumulated depreciation 1,600

Journal entry for 2014

SO 4 Describe the procedure for revising periodic depreciation.

Book value, 1/1/14 $5,800

Residual value

Depreciable cost

Useful life (revised) /

Annual depreciation

First,

establish

Book Value at

the date of

change in

estimate.

- 1,000

4,800

3 years

$ 1,600

Illustration 9-17

Slide

9-36

When there is a change in estimated depreciation:

a. previous depreciation should be corrected.

b. current and future years’ depreciation should be

revised.

c. only future years’ depreciation should be revised.

d. None of the above.

Review Question

Depreciation

SO 4 Describe the procedure for revising periodic depreciation.

Slide

9-37

“Copyright © 2011 John Wiley & Sons, Inc. All rights reserved.

Reproduction or translation of this work beyond that permitted in

Section 117 of the 1976 United States Copyright Act without the

express written permission of the copyright owner is unlawful.

Request for further information should be addressed to the

Permissions Department, John Wiley & Sons, Inc. The purchaser

may make back-up copies for his/her own use only and not for

distribution or resale. The Publisher assumes no responsibility for

errors, omissions, or damages, caused by the use of these

programs or from the use of the information contained herein.”

Copyright