final-challenge- 1396

TRANSCRIPT

33 34

54 52

80

22 15 27

18

50 55 49

81 70

130

57

82 79

162

-8 -2 -9

-32(50)

0

50

100

150

200

Mil

lio

n t

on

s

Active plan Underway plan

Iron Ore Challenge

0

1

2

3

4

5

Geological reserve Proven reserve Demand until

2025- based on

Iran steel

comprehensive

plan studies

Remaining proven

reserves

5

3.1

1.21.9

Bil

lio

n t

on

s

Average grade of Iron ore in Iran: about 46%

Iron ore deposits is adequate almost 10 years after 2025

Forecast of Steel Demand up to 1404 (2025) in the Selected scenarios of 4 Methods

1396 1397 1398 1399 1400 1401 1402 1403 1404Average Optimum scenarios of 4 methods Vector Autoregression Model

Optimum scenario of Econometric Method Optimum Consumption Trens Scenario

30.2

Assumptions for the selected scenarios:

considered time period: the last 20 Years;

Growth of per capita income : 2.5% Growth of the Economy :4%

Growth of Industry Sectors: 5.5% Growth of construction Sectors: 2%

Mil

lio

n t

on

s

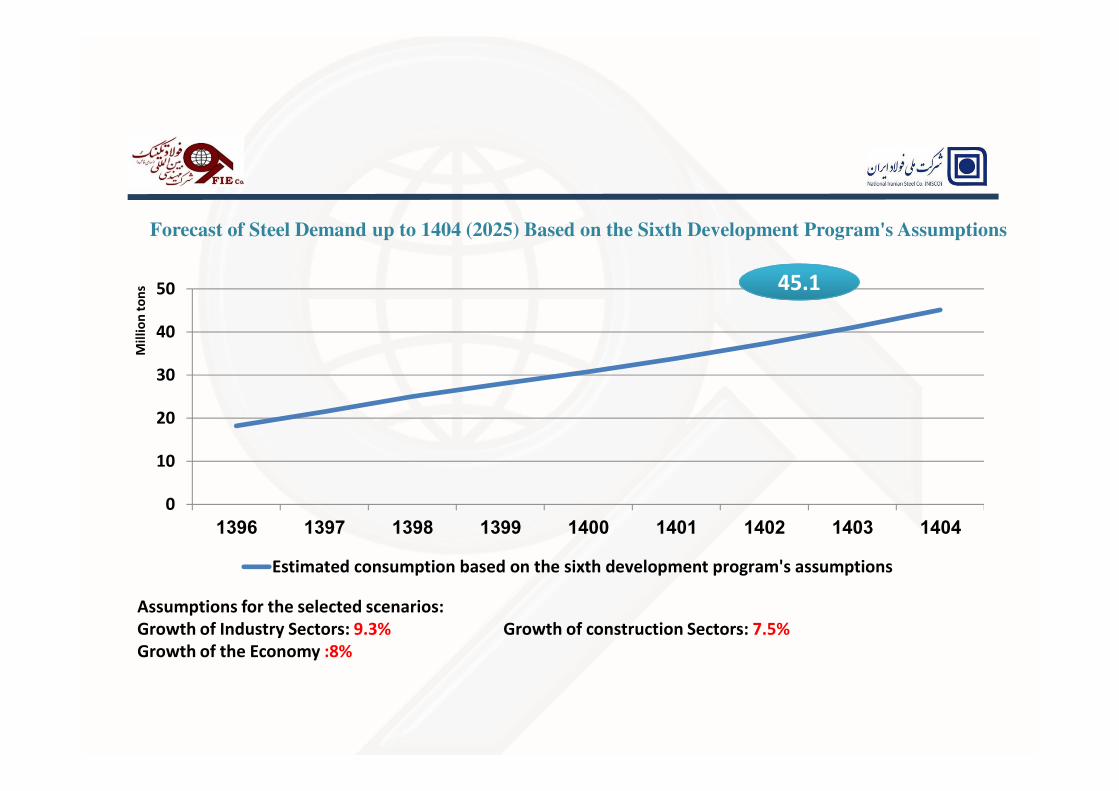

Forecast of Steel Demand up to 1404 (2025) Based on the Sixth Development Program's Assumptions

0

10

20

30

40

50

1396 1397 1398 1399 1400 1401 1402 1403 1404

Estimated consumption based on the sixth development program's assumptions

45.1

Assumptions for the selected scenarios:

Growth of Industry Sectors: 9.3% Growth of construction Sectors: 7.5%

Growth of the Economy :8%

Mil

lio

n t

on

s

1,200

1,300

1,400

1,500

1,600

1,700

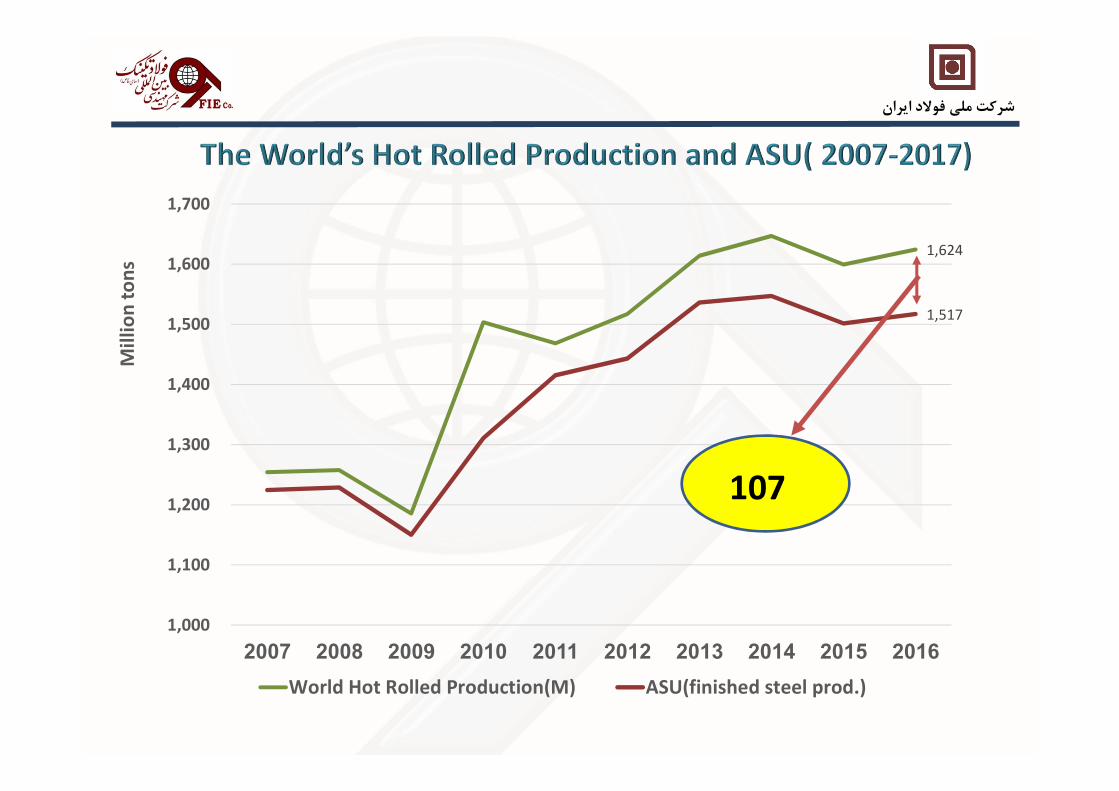

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Mil

lio

n t

on

s

شركت ملي فولاد ايران

1,624

1,517

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

World Hot Rolled Production(M) ASU(finished steel prod.)

Mil

lio

n t

on

s

107

شركت ملي فولاد ايران

808

709

400

500

600

700

800

900

1,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

China’s Production(M) China’s consumption

-0.5%

99

Mil

lio

n t

on

s

93

2

65

12 3

126

78

11

10 10 5 5

4 3 - -

50

100

150

200

250

Total Middle

East

Asia CIS Africa Other

Europe

Nafta Europe Latin

America

Oceania

Mil

lio

n t

on

s

BOF EAF

219

Annouced Investment by Steel Plant (Underway & Planned) 2017-2019

94

.5

2,1

02

2,2

74

2,3

17

2,3

51

2,3

81

0

10

20

30

40

50

60

70

80

90

100

1800

2000

2200

2400

2600

2012 2013 2014 2015 2016 2019

Mil

lio

n T

on

s

planning capacity

2,475

Potential Gross Additions in 2017-2019

0.0

5.0

10.0

15.0

20.0

25.0

based on Export Ratio

to Iran Production

based on Export Ratio

to Global Production

Max. Exp Potantiality based on 1404 vision

of Iran (2025)

14.0

11.210.5

20.4

Mil

lio

n t

on

s

4.1

5.9

7.8

4.7

3.9

3.0

-0.6

2

4.8

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

1394 1395 1396e

Mil

lio

n t

on

es

Export Import Trade Balance

Iran's trade Structure and Comparison with the World (The Ratio of Each Product's Export to Total Steel Export)

13

31

56

67

12

22

0

10

20

30

40

50

60

70

The Ratio of Crude Steel's

Export to Total Steel Export

The Ratio of Long Prod's Export

to Total Steel Export

The Ratio of Flat Prod's Export

to Total Steel Export

Pe

rce

nt

World-2016 Iran-2016 Linear (World-2016) Linear (Iran-2016)

Market Challenge

33.1

55.00 55.00

42

50

26

45

20

25

30

35

40

45

50

55

60

1396 1397 1398 1399 1400 1401 1402 1403 1404

Mil

lio

n T

on

es

Crude Steel Capacity

Sum of Consumption and Trade on based on Ratio Global Export to Prod.

Sum of Consumption and Trade on based on 1404 vision of Iran

Sum of Consumption and Trade on based on Ratio Iran Export to Prod.

World and Iran Steel Capacity

Utilization

71.5%

69.5%

78.0%

68.8%

83.03%

78.17% 77.98%

72.10%

60.0%

65.0%

70.0%

75.0%

80.0%

85.0%

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Iran world

6.173.10

8.357.007.20

3.17.5

9.85

3

less

th

an

0.5

Mt

Be

twe

en

0.5

to

1M

t

Be

twe

en

1

to 2

Mt

Be

twe

en

2

to 5

Mt

Gre

ate

r o

r

eq

ua

l 5

Mt

0

5

10

15

20

Mil

lio

n T

on

s

Active Underway

52.0

5.06.02.01.0

14

1181

less

th

an

0.5

Mt

Be

twe

en

0.5

to

1M

t

Be

twe

en

1 t

o 2

Mt

Be

twe

en

2 t

o 5

Mt

Gre

ate

r

or

eq

ua

l

5 M

t

0

10

20

30

40

50

60

70

Un

it

Active Underway

1 16

66

3 14

9.2710

18.210.6

7.2

101.5

61.4

96.2

64.1

23.116.8

30.9

23.7

77.8

44.6

65.3

40.4

0

20

40

60

80

100

120

Crude steel DRI Pellet Iron ore concentrate

Mil

lio

n t

on

s

Total Underway plans (Realizable) other

شركت ملي فولاد ايران

Dispersion of Steel Units- 2025

The south sea

neighboring provinces

25.1% DRI:

18.9% Crude steel:

Other Provinces

DRI: 74.9%

Crude steel: 81.1%

13,000

25,000

3,145

0

5,000

10,000

15,000

20,000

25,000

30,000

Railway lines

until 2015

Plan in 1404

(2025) Horizon

Railway Lines

expantion for

steel industry

1404 (2025)

KM

Railway lines

4028

202

105

0

50

100

150

200

250

Rail freight total capacity Share of steel Industry in

rail freight

Mil

lio

n t

on

s

Rail freight capacity

Current Situation

1404 (2025) - 55 million tonnes

شركت ملي فولاد ايران

388

66

457

85

0

50

100

150

200

250

300

350

400

450

500

Road transportation total

capacity

Share of steel Industry in road

transportation

Mil

lio

n t

on

s

Current Situation 1404 (2025) - 55 million tonnes

Current Annual consumption:

96.4 billion Cubic meter

Recent ten years period Average:

89.5 billion Cubic meter

per capita renewable

sources of water:

1961 :6000 m3/yr2017: 1100 m3/yr

water consumption of steel chain

in 2025 by 55MT crude steel:257milliom cubic meter

The total needs of

steel industry

(Active+ Underway)

257 Mm3/yr

Units considered in the provinces

adjacent to the Southern Sea

(Khuzestan, Bushehr, Hormozgan, Sistan and

Baluchestan)

Consumption : 46 Mm3/yr (18%)

Units considered in the provinces

non-adjacent to the Southern Sea

Consumption : 211 Mm3/yr (82%)

�Use of wastewater

treatment plants in

cities in limited scale

�Desalination and

transferring water to

the central regions of

the country with a huge cost.

�water Desalination

of Persian gulf and Oman sea.

Water supply sources :

Possible alternative sources for water supply:

Necessity of overview of the methods of supplying water resources for existing

plants, as well as Organizing future plants considering the importance of supplying

water resources.

34

(68%)

(21%)

(11%)(32%)

Others Industry Others Steel chain

(Total consumption: 241092 Million kw/hour annually)

Type of use Comparison with energy per

capita

Agriculture 3.1 times the world average

Household 1.8 times the world average

Public & Commercial 1.5 times the world average

Transport & Industry 1.4times the world average

2858.02018.0

1376.01681.0

238.0

8171.0

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Mil

lio

n E

uro

5053

1245630

1818

3283

1901073

13292

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Mil

lio

n E

uro

Given facilities to the steel and downstream industries

&The required investment to complete the steel chain

2,118

3,374

5,492

8,171

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

capital market2011-

2017

Banking facility2011-

2016

Total 2025

Mil

lio

n E

uro

Country

Financ

ial

marke

t

devel

opme

nt

Compe

titiven

ess

index

Openn

ess

index

Marke

t size

India 4.41 4.31 42 6.4

Turkey 3.84 4.39 49 5.2

Iran 2.92 4.12 39 5.1

0

10,000

20,000

30,000

40,000

50,000

2014 2015 2016

34

,57

7

44

,00

9

44

,45

9

12

,82

8

17

,55

0

12

,30

3

2,1

05

2,0

50

3,3

72

Mil

lio

n D

oll

ar

INDIA TURKEY IRAN

The Global Competitiveness Index

New Technologies

Goals and main approaches:

• Reducing the emission of pollutants such as NOX, SOX, CO2, dust

and ...

• Improving efficiency and increasing production speed

• Reducing energy consumption and using renewable energy sources

• Reducing the amount of required investment and maintenance costs

• Reducing production and raw material costs

• Improving the quality of steel products to meet new and future

needs

• Iron production using low-grade minerals and non-coking coal

Using new technology

New technology in the coal based direct reduction including ITMK3 method in order to use thermal coal fine

(instead of natural gas) and iron ore concentrate (instead of pellets)

1

New methods of melting and reduction process, including FINEX method for producing hot metal for BOF, which

leads to reduction of required investment, possibility of using lower quality materials (thermal coal fine and iron

ore fine), decrease of energy consumption, and improvement of environmental index (By omitting coking ,

sintering or pelletizing plants).

2

New technology of thin slab casting and hot rolling mill using Endless Strip Production (ESP) method.

Improving production of HSM with extending casting length and also implementation of Simatic TDS control

system which brings about an increase in speed of the line from an average of 3.5 to 6 m/s.

3

New technology of casting and hot rolling mill similar ESP method using Win Link method .4

DescriptionOCT+OCT

(Option 1)

AFC+OCT

(Option 2)

AFC+STG - HCS

(Option 3)

AFC+HCT

(Option 4)

Cooling mode

� Using wet cooling tower forEAF, LF and FTP.

� Using wet cooling tower forAuxiliary.

� Using wet cooling tower for

direct cycle of secondary

cooling.

� Using air cooler for EAF, LF

and FTP.

� Using wet cooling tower forAuxiliary.

� Using wet cooling tower for

direct cycle of secondary

cooling.

� Using air cooler for EAF, LF

and FTP.

� Using air cooler and wetcooling tower for Auxiliary.

� Using wet cooling tower for

direct cycle of secondary

cooling.

� Using air cooler for EAF, LF

and FTP.

� Using hybrid cooling towerfor Auxiliary.

� Using wet cooling tower for

direct cycle of secondary

cooling.

Water consumption for

EAF,LF,DDShr/3m70 /hr3m3 < /hr3m3 < hr/3m3 <

Water consumption for

auxiliaryhr/3m67 /hr3m67 hr/3m26 < hr/3m50 <

Make Up Water

Consumptionhr/3m137 hr/3m70 < /hr3m28 < hr/3m52 <

Water saving - 50% 50%+19% 50%+12%

Absorbed Power 141 KW 520 kW 1070 KW 744 KW

Additional

Cost(mechanical)0.0 € 1,409,000 € 4,054,000 € 3,043,000 €

Additional cost (electrical) - - 65,000 € 21,700 €

Initial investment for

reducing 1 cubic meter

per hour of water

consumption

- 21,030 € 37,788 € 36,055 €

Total one year operating

cost128,628 € 112,307 € 134,557 € 120,623 €

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

0

20

40

60

80

100

120

140

160

var.1 var.2 var.3 var.4

10

00

Eu

ro E

xstr

aIn

ve

stm

en

t,

Po

we

r C

on

s. K

W

Wa

ter

con

s. M

3/h

r

Water cons. M3/hr

Power cons.(kw)

Extra Investment(1000 Euro)

329m3/h118 m3/h105 m3/h

Using air cooler for EAF, LF and FTP

Improving the quality

of makeup water using demine water

Project Type: Steel making using EAF

Project Capacity: 800,000 tons per year

Required water using common technology: 329 m3/h (Industrial water)

� In this project, due to environmental conditions, using hybrid cooling towers was

not possible.

68% water saving

1800KW increase in power consumption4 million Euro increase in investment

جمع بندي :الزامات رسيدن به اهداف سند چشم انداز

تدوين استراتژي هم آهنگ در زنجيره فولاد از معدن تا محصول با نگاه به بازار بويژه صادرات

تامين منابع مالي بويژه در زير ساختها

تامين خوراك با پي گيري اكتشافات ، مشاركت در طرح هاي معدني ديگر كشور ها

ادغام واحدها بمنظوررسيدن به مقياس هاي مطلوب

ه بر طرح جامع فتعيين تكليف مجوز هاي اضا

:رقابت پذيري با

افزايش بهره وري توليد ، انرژي ، نيروي انساني

توليد محصولات با ارزش افزوده بالا براي صادرات

و بازسازي هااستفاده از تكنولوژي روز آمد در توسعه ها

باز سازي ونوسازي واحد هاي قديمي و افزايس سطح اتوماسيون

شركت ملي فولاد ايران