federal reserve

TRANSCRIPT

RENAULT GROUP

Goldman Sachs – Annual Global Automotive Conference

DECEMBER 2015 2INVESTOR RELATIONSRENAULT PRESENTATION

Information contained within this document may contain forward looking statements. Although

the Company considers that such information and statements are based on reasonable

assumptions taken on the date of this report, due to their nature, they can be risky and uncertain

(as described in the Renault documentation registered within the French financial markets

regulation authorities) and can lead to a difference between the exact figures and those given or

deduced from said information and statements.

Renault does not undertake to provide updates or revisions, should any new statements and

information be available, should any new specific events occur or for any other reason. Renault

makes no representation, declaration or warranty as regards the accuracy, sufficiency,

adequacy, effectiveness and genuineness of any statements and information contained in this

report.

Further information on Renault can be found on Renault’s website (www.group.renault.com),

in the section Finance / Regulated Information.

DISCLAIMER

DECEMBER 2015 3INVESTOR RELATIONSRENAULT PRESENTATION

2015 OUTLOOK

� The European car market should grow 8% this year, with a French market up 5%. Our main emerging markets should remain adverse and volatile in the fourth quarter.

� Within this context, Renault confirms its guidance:

-increase registrations and Group revenues (at constant exchange rates),

-improve Group operating profit and that of the Automotive division,

-achieve positive Automotive operational free cash flow.

DECEMBER 2015 4INVESTOR RELATIONSRENAULT PRESENTATION

KEY TAKE-AWAYS FROM Q3 RESULTS

� RECOVERY IN EUROPE GAINS TRACTION

� EMERGING MARKETS AND CURRENCIES STILL ADVERSE & VOLATILE

� SUCCESS OF OUR NEW PRODUCTS WITH POSITIVE MIX IMPACT

� STILL STRONG CONTRIBUTION OF SALES TO PARTNERS

� FY GUIDANCE CONFIRMED

DECEMBER 2015 5INVESTOR RELATIONSRENAULT PRESENTATION

RISKS & OPPORTUNITIES FOR THE SECOND HALF

� REGULATORY COST PRESSURE

� EMERGING MARKETS

� SUPPLY CHAIN

� NEW PRODUCTS

� EUROPEAN MARKET MOMENTUM

DECEMBER 2015 6INVESTOR RELATIONSRENAULT PRESENTATION

YTD 2015 COMMERCIAL UPDATE

01

DECEMBER 2015 7INVESTOR RELATIONSRENAULT PRESENTATION

613

318

88 75102

30

621

339

87 72 9727

Q3'14 Q3'15 Q3'14 Q3'15 Q3'14 Q3'15 Q3'14 Q3'15 Q3'14 Q3'15 Q3'14 Q3'15

RENAULT GROUP UNIT REGISTRATIONS Q3 2015 VS Q3 2014

GLOBAL

+1.2%

EUROPE

+6.5%

AMERICAS

-5.3%

ASIA-PACIFIC

-11.2%

AFRICA-ME-INDIA

-4.8%

EURASIA

-1.2%

K units

(PC+LCV)

WORLD MARKET SHARE: 3.01% (+0.04 pts)

-0.2% TIV +9.8% -13.9% -6.6% -12.5% -2.3%

GROUP

DECEMBER 2015 8INVESTOR RELATIONSRENAULT PRESENTATION

1,979

1,094

265 225308

87

1,998

1,188

246 223 26180

09'14 09'15 09'14 09'15 09'14 09'15 09'14 09'15 09'14 09'15 09'14 09'15

RENAULT GROUP UNIT REGISTRATIONS SEPT 2015 (YTD) VS SEPT 2014 (YTD)

GLOBAL

+0.9%

EUROPE

+8.5%

AMERICAS

-15.3%

ASIA-PACIFIC

-7.5%

AFRICA-ME-INDIA

-1.0%

EURASIA

-7.2%

K units

(PC+LCV) WORLD MARKET SHARE: 3.12% (=)

+0.7% TIV +9.0% -18.4% -0.6% -11.1% -0.5%

GROUP

DECEMBER 2015 9INVESTOR RELATIONSRENAULT PRESENTATION

FRANCE01

BRAZIL02

03

ITALY

TURKEY04

SOUTH KOREA

05

06

07

08

09

SPAIN

10

24.4%

4.7%

7.4%

17.1%

GERMANY

8.1%

12.9%

ARGENTINA 14.6%

4.5%

RUSSIA 7.4%

M/S

(PC+LCV)

EUROPE KEEPS PUSHING SALES MOMENTUM – Q3 2015

-1.4 pts

+0.5 pts

+2.6 pts

-1.0 pts

VS.

Q3 2014

UK 4.3%

+1.1 pts

-0.2 pts

-0.5 pts

+0.3 pts

-1.0 pts

+0.2 pts

REGIONAL SALES BREAKDOWN

36% 42%48%

55% 52%48%

Q3 2010 Q3 2011 Q3 2012 Q3 2013 Q3 2014 Q3 2015

42% 48% 52% 48% 45%55%

58% 52% 45% 48% 52% 55%

INTERNATIONALEUROPE

DECEMBER 2015 10INVESTOR RELATIONSRENAULT PRESENTATION

EUROPE REGION – GROUP ORDER BOOK PC+LCV

sept.-07 sept.-08 sept.-09 sept.-10 sept.-11 sept.-12 sep t.-13 sept.-14 sept.-15

DECEMBER 2015 11INVESTOR RELATIONSRENAULT PRESENTATION

Q3 2015 REVENUES

02

DECEMBER 2015 12INVESTOR RELATIONSRENAULT PRESENTATION

RENAULT GROUP REVENUES BY DIVISION IN Q3 2015

In million euros Q3 2015 Change (%)Q3 2014

Automotive

Sales Financing

TOTAL

8,802

534

9,336

+10.2%

-2.2%

+9.4%

7,984

546

8,530

DECEMBER 2015 13INVESTOR RELATIONSRENAULT PRESENTATION

RENAULT GROUP REVENUES BY DIVISION 2015 9 months

In million euros

2015YTD

Change(%)

2014YTD

Automotive

Sales Financing

TOTAL

29,867

1,666

31,533

+11.8%

+2.4%

+11.2%

26,723

1,627

28,350

DECEMBER 2015 14INVESTOR RELATIONSRENAULT PRESENTATION

AUTOMOTIVE REVENUE VARIANCE ANALYSIS

7,984

8,802

-173

+45 -45+184

+178

+413+216

Currency

Volume

Geographicmix

Product mix

Price

Sales to partners Others

+10.2%

-2.2 pts+0.6 pts -0.6 pts +2.3 pts +2.3 pts +5.2 pts +2.6 pts

In million euros CHANGE Q3 2015 / Q3 2014 : +€818m

Q3 2014 Q3 2015

DECEMBER 2015 15INVESTOR RELATIONSRENAULT PRESENTATION

AUTOMOTIVE REVENUE VARIANCE ANALYSIS

26,723

29,867

+52

+660 -91+329

+486+1,525

+183

Currency

Volume

Geographicmix

Product mix

Price

Sales to partners Others

+11.8%

+0.2 pts+2.5 pts -0.3 pts +1.2 pts +1.8 pts +5.7 pts +0.7 pts

In million euros CHANGE 2015 / 2014 : +€3,144m

Q3 2014YTD

Q3 2015YTD

DECEMBER 2015 16INVESTOR RELATIONSRENAULT PRESENTATION

DISTRIBUTION STOCK

NEW VEHICLE DISTRIBUTION STOCK (IN K UNITS)

503 488 527 495 493 459 515 510 503

243

100

255

158253

106

251177

260260

388

272337

240

353

264

333

243

SEP'13 DEC'13 MAR'14 JUN'14 SEP'14 DEC'14 MAR'15 JUN'15 SEP '15

GROUP

INDEPENDENTDEALERS

TOTAL

Number of days of sales

(previous period)

75 7663 62 74 57 74 64 75

DECEMBER 2015 17INVESTOR RELATIONSRENAULT PRESENTATION

RCI BANQUE PERFORMANCE

Q3 2015 Change (%)Q3 2014

Revenues (in € m)

Average loans outstanding

(in € bn)

New contracts (in thousand units)

New financing(in € bn)

534

28.8

348

3.8

546

25.6

302

3.2

-2.2%

+12.8%

+15.2%

+21.9%

DECEMBER 2015 18INVESTOR RELATIONSRENAULT PRESENTATION

RCI BANQUE PERFORMANCE YTD

Q3 2015YTD

Change(%)

Q3 2014YTD

Revenues (in € m)

Average loans outstanding

(in € bn)

New contracts (in thousand units)

New financing(in € bn)

1,666

27.9

1,034

11.6

1,627

25.1

902

9.2

+2.4%

+10.9%

+14.7%

+26.7%

DECEMBER 2015 19INVESTOR RELATIONSRENAULT PRESENTATION

H1 2015 FINANCIAL RESULTS

03

DECEMBER 2015 20INVESTOR RELATIONSRENAULT PRESENTATION

H1 2014 H1 2015 CHANGE

Global registrations (units) 1,365,988 1,376,356 +0.8%

Group revenues 19,820 22,197 +12.0%

of which: Automotive 18,739 21,065 +12.4%

Sales financing 1,081 1,132 +4.7%

Q1 Q2

+13.7% +10.8%

H1 2015 GROUP REVENUES

(million euros)

DECEMBER 2015 21INVESTOR RELATIONSRENAULT PRESENTATION

AUTOMOTIVE REVENUES VARIANCE ANALYSIS

18,739

21,065

+615 -46

+145+308

+1,112

+225

-33

Currency

Volume

Geographic

mix

Product mix

Sales to

partners

Others

+12.4%

+3.3pts -0.2pts +0.8pts +1.6pts +1.2pts -0.2pts

Price

+5.9pts

CHANGE H1 2015 / H1 2014: +€2,326m

H1 2014 H1 2015

(million euros)

DECEMBER 2015 22INVESTOR RELATIONSRENAULT PRESENTATION

729

1,069

+236 -17

+28

-283 +263

+1

+112

GROUP OPERATING MARGIN VARIANCE ANALYSIS

Currency

Volume &

partners

Mix / Net Enrichment

G&A

RCI &

Other

activities

COST REDUCTION

+€219m

H1 2014 H1 2015(million euros)

CHANGE H1 2015 / H1 2014: +€340m

Monozukuri

Raw materials

GROWTH

+€264m

DECEMBER 2015 23INVESTOR RELATIONSRENAULT PRESENTATION

DISTRIBUTION STOCK

NEW VEHICLE DISTRIBUTION STOCK (IN K UNITS)

445 481 507 503 488 527 495 493 459 515 510

131

241140

243

100

255

158

253

106

251177

314240

367

260

388

272337

240

353264

333

DEC'12 MAR'13 JUN'13 SEP'13 DEC'13 MAR'14 JUN'14 SEP'14 DEC '14 MAR'15 JUN'15

GROUP

INDEPENDENTDEALERS

TOTAL

Number of days of sales

(previous period)

65 6772 75 7663 62 74 57 74 64

DECEMBER 2015 24INVESTOR RELATIONSRENAULT PRESENTATION

-369

+267

-591

-118

AUTOMOTIVE NET CASH POSITION

Operational

free cash flow

Cash flow

+1,727

Change

in WCR

Dividends

paid

Net tangible

& intangible

investments

- 1,453 Net cash

decrease

Dividends

received

from

listed co.

-123

Leased

Vehicles

-431

Capitalized

R&D

Financial

investments

& others

-899

Net capex

DEC. 31, 2014: €2,104m

JUNE 30, 2015: €1,567m

-95

-537

(million euros)

DECEMBER 2015 25INVESTOR RELATIONSRENAULT PRESENTATION

H1 2014 H1 2015 CHANGE

Revenues 19,820 22,197 +12.0%

Operating margin +729 +1,069 +340

in % of revenues +3.7% +4.8% +1.1 pts

Other operating income & expenses -265 -116 +149

EBIT +464 +953 +489

Net financial income & expenses -124 -161 -37

Associated companies +725 +912 +187

Current & deferred taxes -264 -235 +29

Net income +801 +1,469 +668

(million euros)

H1 2015 FINANCIAL RESULTS

DECEMBER 2015 26INVESTOR RELATIONSRENAULT PRESENTATION

OPERATING MARGIN BY ACTIVITY

H1 2014 H1 2015 CHANGE

AUTOMOTIVE +348 +656 +308

% Automotive revenues +1.9% +3.1% +1.3 pts

SALES FINANCING +381 +413 +32

GROUP OPERATING MARGIN +729 +1,069 +340

% Group revenues +3.7% +4.8% +1.1 pts

(million euros)

DECEMBER 2015 27INVESTOR RELATIONSRENAULT PRESENTATION

RCI BANQUE

in % of average loans outstandingH1 2014 H1 2015

New financings (€bn) 6.0 7.7

Average performing loans outstanding (€bn) 24.8 27.6

Net banking income* 5.14% 4.93%

Cost of risk* (customer & dealer) -0.47% -0.31%

Operating expenses* -1.58% -1.54%

Pretax income* 2.92% 3.08%

(* in percentage of average performing loans outstanding)

DECEMBER 2015 28INVESTOR RELATIONSRENAULT PRESENTATION

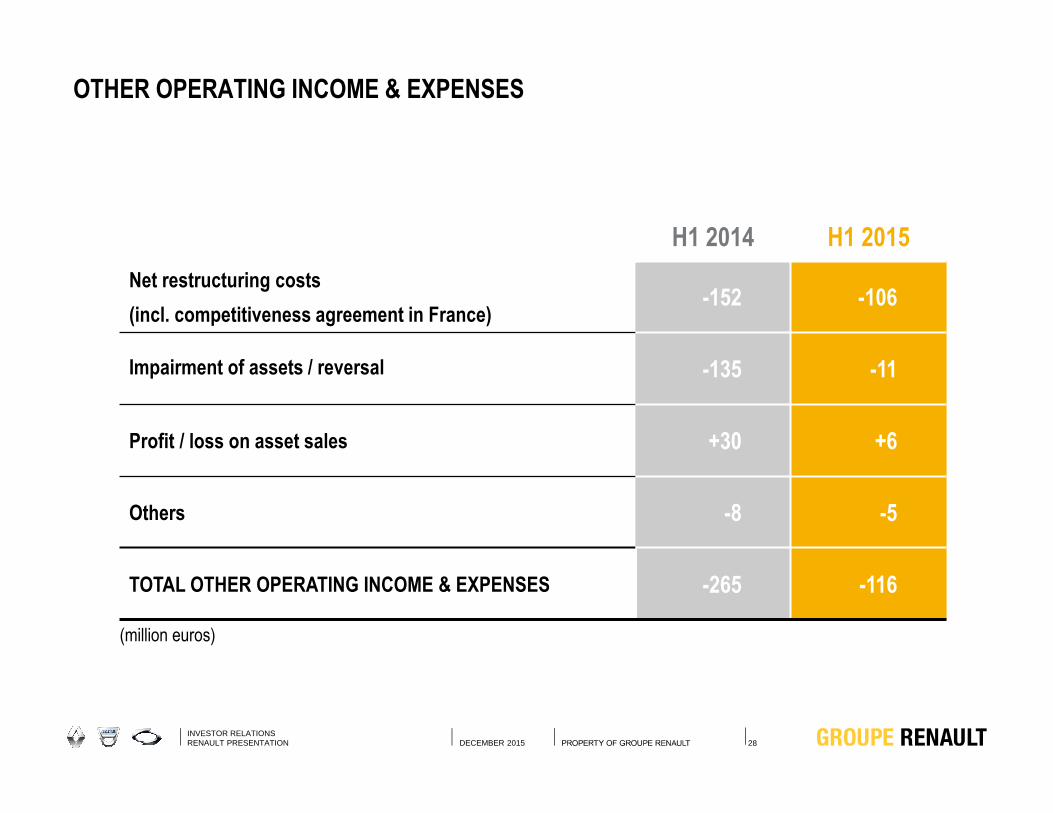

OTHER OPERATING INCOME & EXPENSES

H1 2014 H1 2015

Net restructuring costs

(incl. competitiveness agreement in France)-152 -106

Impairment of assets / reversal -135 -11

Profit / loss on asset sales +30 +6

Others -8 -5

TOTAL OTHER OPERATING INCOME & EXPENSES -265 -116

(million euros)

DECEMBER 2015 29INVESTOR RELATIONSRENAULT PRESENTATION

ASSOCIATED COMPANIES

H1 2014 H1 2015 CHANGE

Nissan +789 +979 +190

AVTOVAZ (1) -55 -70 -15

Others -9 +3 +12

TOTAL ASSOCIATED COMPANIES +725 +912 +187

(1) AVTOVAZ is consolidated with a 3-month time lag

Q1 Q2

494 485

(million euros)

DECEMBER 2015 30INVESTOR RELATIONSRENAULT PRESENTATION

LIQUIDITY RESERVES

Cash = €11.6bn

Available credit lines = €3.2bn

TOTAL = €14.8bn

LIQUIDITY RESERVES

Cash = €10.2bn

Available credit lines = € 3.3bn

TOTAL = €13.5bn

AUTOMOTIVE DIVISION LIQUIDITY

DECEMBER 2014 JUNE 2015

DECEMBER 2015 31INVESTOR RELATIONSRENAULT PRESENTATION

RCI LIQUIDITY*

LIQUIDITY RESERVES

Cash = €0.1bn

HQLA = €0.9bn

ECB eligible = €1.9bn

Available credit lines = €4.0bn

TOTAL = €6.9bn

LIQUIDITY RESERVES

Cash = €0.1bn

HQLA = €0.8bn

ECB eligible = €1.8bn

Available credit lines = €4.1bn

TOTAL = €6.8bn

DECEMBER 2014 JUNE 2015

*Central funding perimeter

DECEMBER 2015 32INVESTOR RELATIONSRENAULT PRESENTATION

RCI BANQUE RETAIL DEPOSIT ACTIVITY

Dec. 2014 June 2015

DEPOSITS 6.5 7.0

o/w GERMANY 4.4 5.1

o/w FRANCE 1.8 1.4

o/w AUSTRIA 0.4 0.5

o/w UNITED KINGDOM N/A 0.04

• 2016 TARGET: 30% OF RCI BANQUE OUTSTANDINGS

(billion euros)

DECEMBER 2015 33INVESTOR RELATIONSRENAULT PRESENTATION

DRIVE THE CHANGE

How to get to our targets

03

DECEMBER 2015 34INVESTOR RELATIONSRENAULT PRESENTATION

Kadjar

2015

RENEWING OUR RANGE

OUR MAIN REVENUES OPPORTUNITIES

New Espace C-hatchD-sedan C-MPV

Pick-up 1TPick-up 0,5T

D-crossoverCaptur

2015

2015

2015

2015

New Twingo

A-entry

2014

2014

LCV international roll out

Full cross-over line up for all our markets

A-entry vehicles for emerging countries

New Twingo for Europe

C & D complete renewal

DECEMBER 2015 35INVESTOR RELATIONSRENAULT PRESENTATION

A NEW STEP TOWARDS OUR MID-TERM PLAN TARGETS

RENAULT ESPACE

DECEMBER 2015 36INVESTOR RELATIONSRENAULT PRESENTATION

A NEW STEP TOWARDS OUR MID-TERM PLAN TARGETS

RENAULT KADJAR

KADJAR

DECEMBER 2015 37INVESTOR RELATIONSRENAULT PRESENTATION

A NEW STEP TOWARDS OUR MID-TERM PLAN TARGETS

RENAULT KWID

KADJAR

DECEMBER 2015 38INVESTOR RELATIONSRENAULT PRESENTATION

A NEW STEP TOWARDS OUR MID-TERM PLAN TARGETS

RENAULT OROCH

DECEMBER 2015 39INVESTOR RELATIONSRENAULT PRESENTATION

A NEW STEP TOWARDS OUR MID-TERM PLAN TARGETS

RENAULT TALISMAN

KADJAR

DECEMBER 2015 40INVESTOR RELATIONSRENAULT PRESENTATION

A NEW STEP TOWARDS OUR MID-TERM PLAN TARGETS

RENAULT TALISMAN ESTATE

DECEMBER 2015 41INVESTOR RELATIONSRENAULT PRESENTATION

A NEW STEP TOWARDS OUR MID-TERM PLAN TARGETS

RENAULT ALASKAN REVEAL

DECEMBER 2015 42INVESTOR RELATIONSRENAULT PRESENTATION

A NEW STEP TOWARDS OUR MID-TERM PLAN TARGETS

RENAULT MEGANE REVEAL

DECEMBER 2015 43INVESTOR RELATIONSRENAULT PRESENTATION

65%33%

Millions units per platforms > 2016

CM

F C

-D

CM

F B

Source : VAG,Hyundai,Toyota : IHS / R&N : Alliance plan

2013 > 2016

SHARED PLATFORMS MODULAR APPROACH

80% of future launches 2/3 of value of upcoming vehicles

from standardized modules

0

1

2

3

4

5

CMF C

-D

CMF B

DEVELOPING OUR SCALE AND COMPETITIVENESS

DECEMBER 2015 44INVESTOR RELATIONSRENAULT PRESENTATION

SOURCING OPTIMIZATION INDUSTRIAL CAPACITIES

Local integration rate*> 80 % in 4 major countries

Utilization rate in Europe > 100%

2011 > 2016

Renault for Renault

Renault for Partners

Renault capacity (2 shifts/day)

Alliance for Renault

>2016

2013

2010

China

Russia

India

Brazil

(*) including powertrain group

Production

5%

17%

REDUCING COST OF VEHICULES

DECEMBER 2015 45INVESTOR RELATIONSRENAULT PRESENTATION

2009 2010 2011 2012 2013 2014 2016e

Renault Nissan

> €4.3bn

ALLIANCE SYNERGIES

€3.8bn*

(*) estimated

ACCELERATING ALLIANCE SYNERGIES

4 KEY-FUNCTIONS CONVERGENCE

PURCHASING UPSTREAM ENGINEERING

HUMANRESOURCES

MANUFACTURING& LOGISTICS

DECEMBER 2015 46INVESTOR RELATIONSRENAULT PRESENTATION

CAPEX AND R&D CAPPED at 9%

2008 2009 2010 2011 2012 2013 20142015

H1

2015-

2016e

NET CAPEX 5.6 % 4.4 % 2.5 % 3.1% 4.3 % 3.8 % 3.4% 3.6%

NET R&D 5.5 % 4.5 % 4.0 % 3.8% 3.8 % 3.7 % 4.0% 4.4%

TOTAL 11.1 % 8.9 % 6.5 % 7.0% 8.1% 7.5% 7.4% 8.0% < 9%

% OF GROUP REVENUES

ALLIANCE BENEFITS TO RENAULT: R&D AND CAPEX

INVESTOR RELATIONSRENAULT PRESENTATION DECEMBER 2015 47

A LEADER IN CO2 EMISSION REDUCTION

DECEMBER 2015 48INVESTOR RELATIONSRENAULT PRESENTATION

PREPARING FOR THE FUTURE

EOLAB

DECEMBER 2015 49INVESTOR RELATIONSRENAULT PRESENTATION

OPERATING MARGIN IMPROVEMENT

3.0 %

> 5 %

VolumeCostreduction

Enrichment Net

Raw material

ProvisionFOREX

FY2013 > FY2016

DECEMBER 2015 50INVESTOR RELATIONSRENAULT PRESENTATION

2015 H1: A ROBUST MILESTONE FOR OUR MID-TERM PLAN

MARGIN IMPROVEMENT

1,9%

3,0%

3,9%

4,8%

0,1%

1,3%

2,2%

3,1%

2012 restated 2013 2014 2015 H1

GROUP OPERATING MARGIN

AUTOMOTIVE OPERATING MARGIN

> 5% in 2017*

* target

INVESTOR RELATIONSRENAULT PRESENTATION DECEMBER 2015 51

DIVIDEND POLICY

0,00

0,30

1,16

1,72 1,721,90

2009 2010 2011 2012 2013 2014

DIVIDENDS PAID IN € PER SHARES

� First phase of the plan, dividend paid based on dividends received from shareholdings in listed companies, with a one-year time lag.

� The purpose of that policy was to raise the profile of the dividend while achieving the debt reduction target.

� For the second phase of the plan, pay-out policy independent of the dividends received on holdings in listed companies.

� Aim of this policy : offer returns at least equivalent to the average of European automakers .

� The dividend will be paid on May 15 (or the following working day).

DECEMBER 2015 52INVESTOR RELATIONSRENAULT PRESENTATION

NEW FRONTIERS: CHINA

2013 2014 2015 2016 2017 2018 2019

Industrial projectSignature New plant � 150,000 veh./year

C crossover

D crossover

Vehicle in study

WITH OUR PARTNERS

2nd step

DECEMBER 2015 53INVESTOR RELATIONSRENAULT PRESENTATION

PREPARING FOR THE FUTURE

WUHAN PLANT

DECEMBER 2015 54INVESTOR RELATIONSRENAULT PRESENTATION

FY 2014 FINANCIAL RESULTS

03

DECEMBER 2015 55INVESTOR RELATIONSRENAULT PRESENTATION

AUTOMOTIVE REVENUES VARIANCE ANALYSIS

38,775 38,874

-1,150

-327 +64-33

+311

+1,248

-14

Currency

Volume

Geographic

mix

Mix

Sales to

partners

Others

+0.3%

-3.0pts -0.8pts +0.2pts -0.1pts +3.2pts 0.0pts

Price

+0.8pts

CHANGE 2014 vs 2013: +€99m

FY 2013 FY 2014

(million euros)

DECEMBER 2015 56INVESTOR RELATIONSRENAULT PRESENTATION

OPERATING PROFIT BY ACTIVITY

FY 2013 FY 2014 CHANGE

AUTOMOTIVE 495 858 +363

% Automotive revenues 1.3% 2.2% +0.9pts

SALES FINANCING 747 751 +4

GROUP OPERATING PROFIT 1,242 1,609 +367

% Group revenues 3.0% 3.9% +0.9pts

(million euros)

DECEMBER 2015 57INVESTOR RELATIONSRENAULT PRESENTATION

1,2421,609

+778

+66+134

-226+121

-35-471

GROUP OPERATING PROFIT VARIANCE ANALYSIS

Currency

Volume &

partners

Mix / Net Enrichment

G&A

RCI Banque

&

other activities

COST REDUCTION

€844m

FY 2013 FY 2014

CHANGE 2014 vs 2013: +€367m

Monozukuri

Raw materials

GROWTH

€86m

(million euros)

DECEMBER 2015 58INVESTOR RELATIONSRENAULT PRESENTATION

CONTINUING COST REDUCTION

COST REDUCTION CONTRIBUTION TO OPERATING PROFIT IMPROVEMENT

+ 430

-107

+ 397

+ 58+ 66

Purchasing Warranty Manufacturing& Logistic

R&D G&A

+€844mvs 2013

DECEMBER 2015 59INVESTOR RELATIONSRENAULT PRESENTATION

OTHER OPERATING INCOME & EXPENSES

FY 2013 FY 2014

Net restructuring costs

(incl. competitiveness agreement in France)-423 -305

Impairment of assets / reversal -488 -153

RCI Banque (mainly change in regulation) - -50

Profit / loss on asset sales +153 +7

Others -518 -3

Total other operating income & expenses -1,276 -504

(million euros)

DECEMBER 2015 60INVESTOR RELATIONSRENAULT PRESENTATION

ASSOCIATED COMPANIES

FY 2013 FY 2014 CHANGE

Nissan 1,498 1,559 +61

AVTOVAZ (1) -34 -182 -148

Others -20 -15 +5

Total associated companies 1,444 1,362 -82

(1) AVTOVAZ is consolidated with a 3-month time lag . Adjustments have been made to take into account significant transactions and accounting entries that occurred between September 30, 2014 and December 31, 2014.

(million euros)

DECEMBER 2015 61INVESTOR RELATIONSRENAULT PRESENTATION

FY 2014 FINANCIAL RESULTS

FY 2013 FY 2014 CHANGE

Revenues 40,932 41,055 +0.3%

Operating profit 1,242 1,609 +367

in % of revenues 3.0% 3.9% +0.9pts

Other operating income & expenses -1,276 -504 +772

EBIT -34 1,105 +1,139

Net financial income & expenses -282 -333 -51

Associated companies 1,444 1,362 -82

Current & deferred taxes -433 -136 +297

Net income 695 1,998 +1,303

(million euros)

DECEMBER 2015 62INVESTOR RELATIONSRENAULT PRESENTATION

3,138

1,083

343

+596

+463 -542

-661

AUTOMOTIVE NET CASH POSITION

Operational free

cash flow

Cash flow

Changein WCR

Dividendspaid

Net tangible& intangible

investments

-2,651

Net changeIn cash

Dividends receivedfrom

listed co.

Capitalized

R&D

-845 Financial investments & others

Net capex

-1,571

DEC 31, 2013 : €1,761m

DEC 31, 2014 : €2,104m

(million euros)

LeasedVehicles -235

DECEMBER 2015 63INVESTOR RELATIONSRENAULT PRESENTATION

LIQUIDITY RESERVES

Cash = €10.7bn

Available credit lines = €3.4bn

TOTAL = €14.1bn

LIQUIDITY RESERVES

Cash = €11.6bn

Available credit lines = €3.2bn

TOTAL = €14.8bn

AUTOMOTIVE DIVISION LIQUIDITY

DECEMBER 2013 DECEMBER 2014

DECEMBER 2015 64INVESTOR RELATIONSRENAULT PRESENTATION

FUNDING & LIQUIDITY PROFILE

� RSA total funding : 7.6 billions €In million euros at December 31, 2014

Bonds, Banks & assimilated (in millions euros *)

� Liquidity reserve: - Available back-up lines : 3.2 billions €- Cash & cash equivalents: 11.6 billions €

Automobile Division

* fx rates as of 12/31/14

DECEMBER 2015 65INVESTOR RELATIONSRENAULT PRESENTATION

RCI BANQUE

(in percentage of average loans outstanding)

2013 2014

New financings (€bn) 11.4 12.6

Average loans outstanding (€bn) 24.2 25.4

Net banking income* 5.04% 4.98%

Cost of risk (customer & dealer) -0.42% -0.43%

Operating expenses* -1.56% -1.58%

Pretax income* 3.07% 2.95%

Operating profit (€m) 747 751

* Excluding non recurring items

DECEMBER 2015 66INVESTOR RELATIONSRENAULT PRESENTATION

End 2013 End 2014

DEPOSITS 4,33 6,53

o/w GERMANY 3,05 4,38

o/w FRANCE 1,28 1,78

o/w AUSTRIA - 0,37

RCI BANQUE RETAIL DEPOSIT ACTIVITY

• 2016 TARGET: 30% OF RCI BANQUE OUTSTANDINGS

(billion euros)

DECEMBER 2015 67INVESTOR RELATIONSRENAULT PRESENTATION

04RENAULT IN BRIEF

INVESTOR RELATIONSRENAULT PRESENTATION DECEMBER 2015 68

RENAULT – IN BRIEF

� Renault was founded in 1898 and is listed on the Paris NYSE Euronext since 1995

� Renault created an Alliance with Nissan in 1999

� Renault has strategic cooperation with Daimler

� Market capitalization of €17.9bn as of Dec 2014 (€21.9bn as of Aug 2015)

� Renault employs 117,395 employees worldwide

� 2,712,432 vehicles sold worldwide in 2014

� The Renault brand is ranked # 3 in Europe

� The company is a bond issuer via two entities:

Renault, rated BBB- by S&P (stable outlook)/BBB-(stable outlook) by Fitch / Ba1 (positive outlook) by Moody’s

RCI Banque, its financing arm, rated Baa1 (stable outlook) by Moody’s / BBB (negative outlook) by S&P

OWNERSHIP OF CAPITAL AT END 2014

Treasury stock 2

0.86%Employees

2,97%

Nissan 1

15.00%

French State15.01%

Public63.05%

1 Nissan does not exercise the voting rights attached to these shares2 Shares acquired for the purposes of stock option programs. These shares have

no voting rights attached3 A strategic cooperation between the Renault-Nissan Alliance and Daimler AG was

announced in April 2010;

Total share capital €1,127mm

Total number of shares 295,722,284

Daimler 3

3.10%

Source: Renault SA

INVESTOR RELATIONSRENAULT PRESENTATION DECEMBER 2015 69

GROUP STRUCTURE

RCIBANQUE

RENAULTSAMSUNGMOTORS

AvtoVAZ

OTHER COMPANIESindustrial, commercial,

refinancing and cash management concerns

RENAULT S.A.S.

DACIA

NISSAN MOTOR

RENAULT SA

100 %

43.4 %

99.4 %

1.55 %

100 % 80.1 %37,25%

DAIMLER AG

Renault GroupAlliance and Cooperation

INVESTOR RELATIONSRENAULT PRESENTATION DECEMBER 2015 70

A MAJOR ALLIANCE IN THE AUTOMOTIVE LANDSCAPE

52 5254

56 56 56 57

6163

6568

6563

71

75

7982

85

51

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

10,1 9,9 9,98,5

7,7

6,35,3

4,6 4,4

2,9 2,7

0,0

1,0

2,0

3,0

4,0

5,0

6,0

7,0

8,0

9,0

10,0

11,0

TOYOTA

VW-Porsche

GM-Wulinng

ALLIANCE

HYUNDAI

FORD

NISSAN

FIAT-CHYSLER

HONDA

PSA

RENAULT

RenaultNissanAvotvaz

8,470 million units sold in 2014

TIV (PC+LCV) IN MILLION UNITS

MAIN CARS SALES IN 2014 (PC+LCV) IN MILLION UNITS

448 5%

5 310 63%

2 712 32%

INVESTOR RELATIONSRENAULT PRESENTATION DECEMBER 2015 71

62%12%

11%

11%4%

Sales by Region

Europe

Americas

Africa - ME

-India

Eurasia

Asia-Pacific

RENAULT SALES IN H1 2015

76%

21%

3%

Sales by brand

Renault

Dacia

RSM

4%

27%

40%

14%

3%

12%

Sales by segment

A B

MO C

D/E LCV

MAIN CARS SALES IN H1 2015 (PC+LCV) IN KUNITS

237

171 168 147 145 12876 54 47

0

100

200

300

400

500

CLIO - B

seg

SANDERO - M

O

DUSTER - M

O

MEGANE/SCENIC - C

SEG

LOGAN - M

O

CAPTUR - B

SEG

KANGOO - L

CV

TWINGO - A

SEG

MASTER - L

CV

INVESTOR RELATIONSRENAULT PRESENTATION DECEMBER 2015 72

HEADCOUNT EVOLUTION

74 73 71 70 70 68 63 60 55 54 55 50 49 46

2624 24

22 20 2018 17 20

3531 31 28 33 35 43 45

44 49 5356 56 51

28 2423 26 24

0

20

40

60

80

100

120

140

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

France EUROPE Outside Europe

129 130 129121 123

128

Headcount excluding early retirement schemes

137

128 125 127 127117

124 122

INVESTOR RELATIONSRENAULT PRESENTATION DECEMBER 2015 73

INTERNATIONAL SALES EXPANSION

11%

17% 17% 17%19%

23%27%

30%

35%37%

34%37%

43%

50% 50%

46%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

% OF UNIT SALES OUTSIDE EUROPE

INVESTOR RELATIONSRENAULT PRESENTATION DECEMBER 2015 74

ENTRY PROGRAM SALES EVOLUTION –OVER 1M UNITS IN 2014

23145

248367

510 535687

814954

1 084 1 142

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

IN K UNITS

INVESTOR RELATIONSRENAULT PRESENTATION DECEMBER 2015 75

M0 PLATFORM : THE RIGHT TOOL FOR INTERNATIONAL EXPANSION

% OF INTERNATIONAL SALES UPON M0 PLATFORM

63%

37%

MO Others

INVESTOR RELATIONSRENAULT PRESENTATION DECEMBER 2015 76

ENTRY PROGRAM RECIPE FOR SUCCESS

� Two different business models:

� Dacia Brand in Europe and Euromed(45% of the sales)

� Renault Brand for International development (55% of the sales)

� The “right” level of vehicle content

� Adjusted for the different markets

� High carry-over to minimize investment

� Seven bodies on the same platform

� Localization

NEW LOGAN

DUSTER

INVESTOR RELATIONSRENAULT PRESENTATION DECEMBER 2015 77

RENAULT RANGE

INVESTOR RELATIONSRENAULT PRESENTATION DECEMBER 2015 78

RENAULT RANGE

INVESTOR RELATIONSRENAULT PRESENTATION DECEMBER 2015 79

DACIA & RSM RANGE

INVESTOR RELATIONSRENAULT PRESENTATION DECEMBER 2015 80

P&L STATEMENT SINCE 2000

* with Renault VI

PUBLISHED

2000* 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014in K units

Registration 2 289 2 409 2 404 2 389 2 489 2 533 2 433 2 484 2 382 2 309 2 626 2 722 2 550 2 628 2 712production 2 348 2 375 2 344 2 385 2 472 2 516 2 385 2 659 2 421 2 199 2 599 2 637 2 725 2 520 2 574

in€ m

Revenues 40 175 36 351 36 336 37 525 40 715 41 338 41 528 40 682 37 791 33 712 38 971 42 628 41 270 40 932 41 055o/w Automotive 31 486 33 841 34 456 35 535 38 645 39 458 39 605 38 679 35 757 31 951 37 172 40 679 39 156 38 775 38 874

o/w sales financing 1 656 1 828 1 880 1 990 2 070 1 880 1 923 2 003 2 034 1 761 1 799 1 949 2 114 2 157 2 181Cost of goods and services sold -30 214 -28 240 -28 17 8 -29 273 -31 162 -32 137 -32 499 -31 408 -29 659 -26 978 -30 620 -33 848 -33 017 -33 611 -33 310

o/w Research and development expenses -2 048 -1 935 -1 143 -1 243 -1 383 -2 034 -1 963 -1 850 -1 858 -1 795 -1 834 -2 017 -1 915 -1 812 -1 721o/w SG&A -4 838 -4 538 -4 363 -4 452 -4 581 -4 918 -5 018 -4 949 -4 770 -4 382 -4 605 -4 751 -4 534 -4 267 -4 415

Operating margin 2 022 473 1 483 1 402 2 418 1 323 1 063 1 354 212 -396 1 099 1 091 729 1 242 1 609o/w Automotive 1 574 216 1 189 1 035 1 974 858 571 882 -275 -902 396 330 -25 495 858

o/w sales financing 253 252 294 367 444 465 492 472 487 506 703 761 754 747 751Other operating income and expenses -319 231 -266 -168 -270 191 -186 -116 -329 -559 -464 153 -607 -1 276 -504Operating income 1 703 704 1 217 1 234 2 148 1 514 877 1 23 8 -117 -955 635 1 244 122 -34 1 105Financial expense -69 -64 -91 -71 -348 -327 61 76 441 -404 -37 6 -121 -266 -282 -333Capital gain on sale of shares in Volvo AB 2 000 924Share in net income of companies accounted for by the equity method

89 380 1 331 1 860 2 020 2 597 2 260 1 675 437 -1 561 1 289 1 524 1 504 1 444 1 362

o/w Nissan 56 497 1 335 1 705 1 767 2 275 1 871 1 288 345 -902 1 084 1 332 1 234 1 498 1 559o/w Volvo -26 71 175 240 308 384 352 226 -301 214 136 80

o/w AvtoVAZ -370 -21 49 186 -34 -182Current and deferred taxes -649 -67 -447 -510 -634 -331 -255 -255 -162 -148 -58 -508 -549 -433 -136Group net income 1 074 953 2 010 2 513 3 186 3 453 2 943 2 734 599 -3 068 3 490 2 139 1 735 695 1 998Renault net income 1 080 1 051 1 956 2 480 3 119 3 367 2 869 2 669 571 -3 125 3 420 2 092 1 772 586 1 890EPS 4,5 4,4 7,5 9,3 11,7 13,2 11,2 10,3 2,2 -12,1 12,7 7,7 6,5 2,2 6,9Number of shares 239 798 239 998 259 560 265 960 265 960 255 177 256 994 258 621 256 532 257 514 269 292 272 381 272 256 272 290 273 049

workforce 166 114 140 417 132 351 130 740 130 573 126 584 128 893 130 179 129 069 121 422 122 615 128 322 127 086 121 807 117 395

BEFORE IFRS IFRS

INVESTOR RELATIONSRENAULT PRESENTATION DECEMBER 2015 81

CASH FLOW STATEMENT

PUBLISHED

IFRSin € m 2000* 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014AUTO EBIT 1 467 458 928 858 1 710 1 058 303 767 -608 -1 457 -78 478 -615 -770 389Depreciation & amortization 1 817 1 683 1 938 2 117 2 133 2 658 2 817 2 815 2 892 3 124 3 045 2 820 3 299 3 164 2 702AUTOMOTIVE EBITDA 3 284 2 141 2 866 2 975 3 843 3 716 3 120 3 582 2 284 1 667 2 967 3 298 2 684 2 394 3 091

Cash flow 3 027 1 290 2 919 2 806 3 798 3 589 3 288 3 616 2 373 1 386 3 074 2 910 2 577 2 914 3 138Change in WC -1 657 1 751 322 239 401 -533 -346 -26 -2 704 2 923 395 627 922 790 596Capex and R&D cost -2 289 -2 546 -2 968 -2 533 -2 823 -2 879 -3 585 -3 565 -3 385 -2 054 -1 644 -2 212 -2 674 -2 543 -2 416

CAPEX -2 253 -2 497 -2 284 -1 927 -2 035 -2 046 -2 494 -2 278 -2 260 -1 465 -978 -1 325 -1 910 -1 811 -1 571CAPITALIZED R&D -36 -49 -684 -606 -788 -833 -1 091 -1 287 -1 125 -589 -666 -887 -764 -732 -845

Others 135 -248 -155 -241 -228 -334 -235OPERATIONAL FCF -919 495 273 512 1 376 177 -508 25 -3 716 2 007 1 670 1 084 597 827 1 083

Dividends received from Nissan 99 183 267 345 383 431 456 418 0 88 274 427 406 432Dividends received from Volvo 0 77 77 208 120 158 477 258 81 0 38 47Dividends received from Daimler 22 27 27 32Dividends received from others excl; RCI 7 6 13 13 3 12 0 0 1 6FCF -912 600 533 856 1 929 693 94 961 -3 028 2 088 1 758 1 419 1 077 1 260 1 547

DIVIDEND PAID 183 219 258 316 383 493 684 883 1 054 0 0 88 -402 -537 -542

BEFORE IFRS

INVESTOR RELATIONSRENAULT PRESENTATION DECEMBER 2015 82

-919

495273

512

1377

177

-508

25

-3716

20071670

1084

597827

1083738

-1256

-49

273

845 710

-162

51

-1012 -916

1275

457

-325

37487

-4000

-2000

0

2000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Operational Free Cash Flow Operational Free Cash Flow excluding WCR evolution

(million euros)

A STRONGER FCF MANAGEMENT

INVESTOR RELATIONSRENAULT PRESENTATION DECEMBER 2015 83

8,29,7 10,1

11,813,6

15,9

19,721,2 22,1

19,416,5

22,824,6 24,6

23,224,9

-2,7

-4,8-3,9

-2,5 -1,7

-1,6

-2,3 -2,4 -2,1

-7,9-5,9

-1,4-0,3

1,5 1,8 2,1

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Shareholders' equity

Automotive Net cash

AUTOMOTIVE DIVISION FULLY DELEVRAGED

(billion euros)

FormerGAAPs

IFRSGAAPs

INVESTOR RELATIONSRENAULT PRESENTATION DECEMBER 2015 84

RENAULT INVESTORS RELATION CONTACT

Thierry Huon

Investor Relations Director

+33 1 76 84 53 09

Nicolas Chaillan

Investor Relations

+33 1 76 83 05 13

Clémentine de Quatrebarbes

Investor Relations

+33 1 76 84 60 89

Investor relations internet site: http://group.renault.com/finance