fe a tu re s - university of new south · pdf filescada. national electricity market design...

TRANSCRIPT

National E

lectricity Market D

esign & P

erformance # 1

© H

. Outhred 2002

Fundam

entals of

Electricity Industry R

estructuring

National E

lectricity Market

Design and P

erformance

Hugh O

uthredU

niversity of New

South W

ales

Em

ail: h.outhred@unsw

.edu.auT

el: 0414 385 240

THE A

USTRA

LIAN

CRC FOR

RENEW

ABLE EN

ERGY

LTD

National E

lectricity Market D

esign & P

erformance # 2

© H

. Outhred 2002

Electricity industry structure in S

E A

ustralia

Gen 1

Gen 2

Gen X

GenerationS

ector:-large

generators

Gen 3

Transm

issionS

ector

NS

WV

ictoriaS

outh Aust.

Queensland

& possibly

Tasm

ania

Transm

issionS

ector

NS

WV

ictoriaS

outh Aust.

Queensland

& possibly

Tasm

ania

Electricity F

inancial instrument

& R

EC

(emission) trading

Distributor 1

Distributor 2

Distributor Y

Distributionsector

Electricity

Multi-regionN

ationalE

lectricityM

arket(N

EM

)

Intentionsoffers &

payments

Retailer Z

Retailer 2

Retailer 1

Retail

sector

Intentionsbids &

payments

Tx netw

orkpricing

Tx netw

orkpricing

Netw

orkaccess

End-use

Equipm

ent&

Distributed

resourcesE

lectricity

End-usesector

Contestable

customers

Franchise

customers

Retail

Markets

Em

beddedgenerators

National E

lectricity Market D

esign & P

erformance # 3

© H

. Outhred 2002

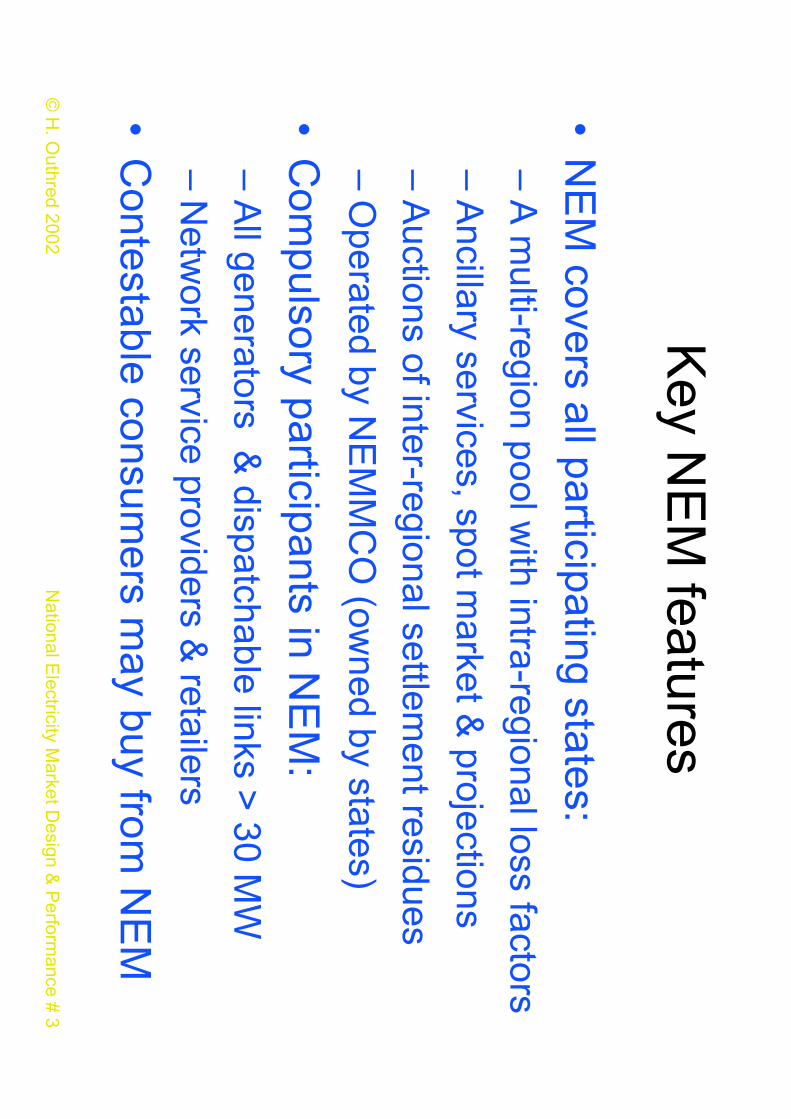

Key N

EM

features

•N

EM

covers all participating states:–

A m

ulti-region pool with intra-regional loss factors

–A

ncillary services, spot market &

projections

–A

uctions of inter-regional settlement residues

–O

perated by NE

MM

CO

(owned by states)

•C

ompulsory participants in N

EM

:–

All generators &

dispatchable links > 30 M

W

–N

etwork service providers &

retailers

•C

ontestable consumers m

ay buy from N

EM

National E

lectricity Market D

esign & P

erformance # 4

© H

. Outhred 2002

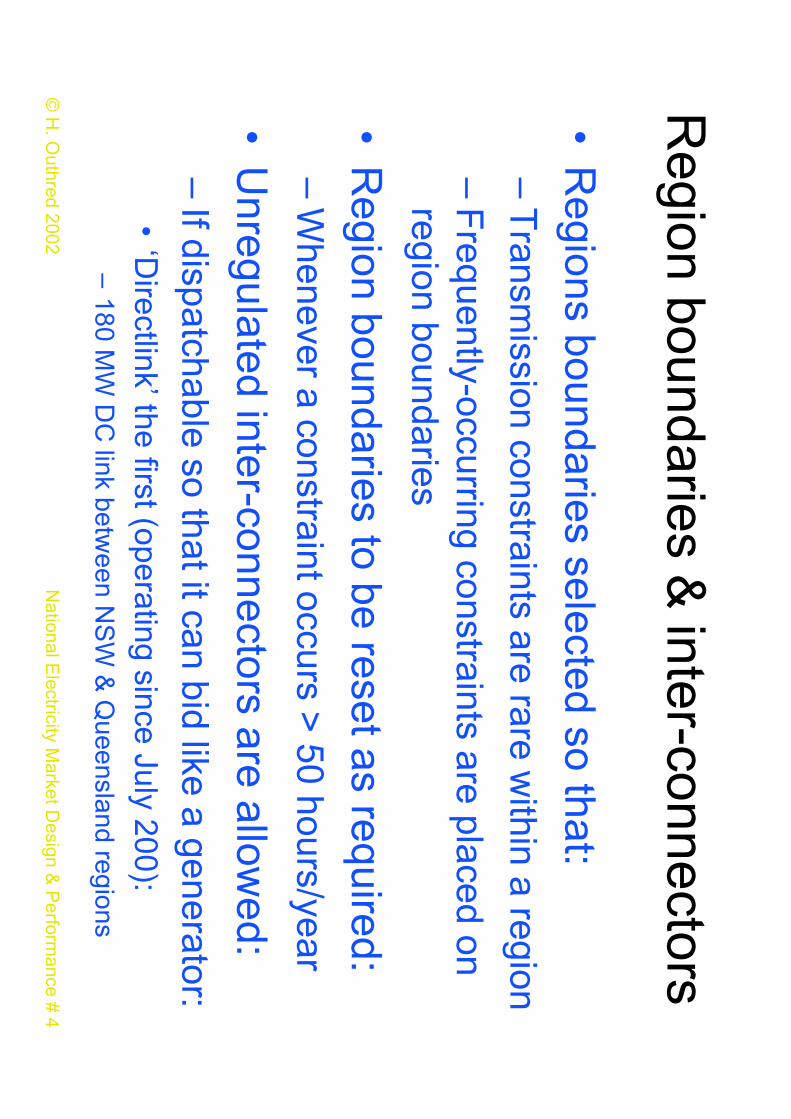

Region boundaries &

inter-connectors

•R

egions boundaries selected so that:–

Transm

ission constraints are rare within a region

–F

requently-occurring constraints are placed onregion boundaries

•R

egion boundaries to be reset as required:–

Whenever a constraint occurs >

50 hours/year

•U

nregulated inter-connectors are allowed:

–If dispatchable so that it can bid like a generator:

•‘D

irectlink’ the first (operating since July 200):–

180 MW

DC

link between N

SW

& Q

ueensland regions

National E

lectricity Market D

esign & P

erformance # 5

© H

. Outhred 2002

States participating in the

National E

lectricity Market

(NE

M)

• Queensland

• New

South W

ales & A

CT

• Victoria

• South A

ustralia• T

asmania (on connection

to the mainland)

NE

M regions are indicated, and their

boundaries need not be on state borders(e.g. tw

o regions in NS

W)

Queensland w

as expected to have 3 NE

Mregions, but transm

ission augmentation

is removing the associated flow

constraints

National E

lectricity Market D

esign & P

erformance # 6

© H

. Outhred 2002

NS

W, S

nowy, V

ictorian & S

A regions of N

EM

:-transm

ission & sub-transm

ission (NE

MM

CO

, 1999)

National E

lectricity Market D

esign & P

erformance # 7

© H

. Outhred 2002

NE

M M

odel(B

ased on NE

MM

CO

, 1997)

1,500 MW

NS

W

Snow

y

Victoria

1,100 MW

3,000 MW

1,100 MW

Queensland

500 MW

1,000 MW

South A

ust

500 MW 250 M

W

300 MW

Tasm

ania480 M

WB

asslink

thermal

or stabilityflow

limits

Directlink

180 MW

DC

(unregulated)

Murraylink (unregulated D

C)

& possibly S

AN

I (regulated AC

)

National E

lectricity Market D

esign & P

erformance # 8

© H

. Outhred 2002 S

pot market offers &

bids

•G

enerators, retailers & consum

ers:–

Price-quantity curve (sell/buy) for each half hour:•

≤ 10 daily prices, quantities changeable until dispatch

–D

emand forecasts ‘bid in’ at V

OLL

•D

ispatchable links between regions:

–F

low offer curve based on price difference

•B

ids & offers ranked to give dispatch stack:

–C

onsidering loss factors & inter-tie constraints

–5 m

inute prices set by economic dispatch:

•H

alf-hourly averages are calculated in ‘real time’

National E

lectricity Market D

esign & P

erformance # 9

© H

. Outhred 2002

NE

M P

re-dispatch, Dispatch &

AG

C

Bid D

atabase

Instructionsto

participants

Forecast

spot prices

Current

spot price

Pre-dispatch

(half-hourly)

Econom

ic Dispatch

(5 minutes)

NE

MM

CO

data(e.g. operating

constraints)

Day-ahead bids

fromparticipants

Continuous

re-bid quantities from

participants

AG

C(2 second cycle)

SC

AD

A

National E

lectricity Market D

esign & P

erformance # 10

© H

. Outhred 2002

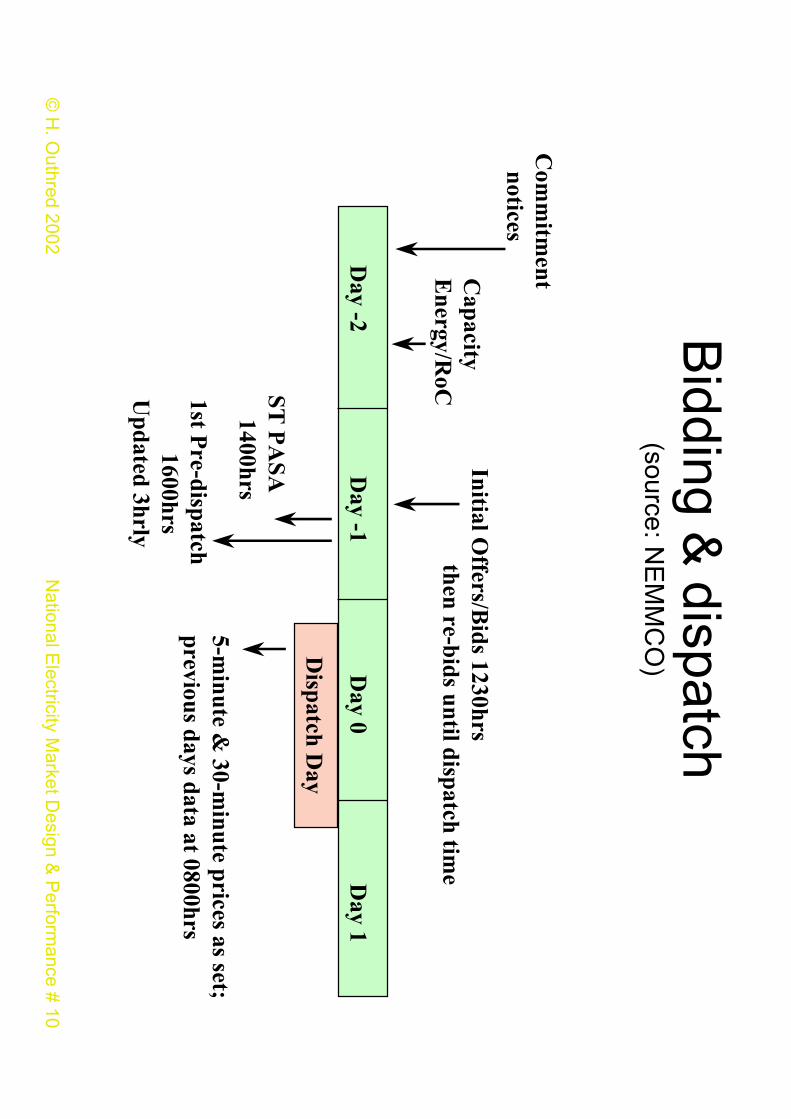

Bidding &

dispatch(source: N

EM

MC

O)

Day -2 D

ay -1 Day 0 D

ay 1

Dispatch D

ay

Com

mitm

ent notices

Initial Offers/B

ids 1230hrsthen re-bids until dispatch tim

e

ST P

ASA

1400hrs

1st Pre-dispatch

1600hrsU

pdated 3hrly

5-minute &

30-minute prices as set;

previous days data at 0800hrs

Capacity

Energy/R

oC

National E

lectricity Market D

esign & P

erformance # 11

© H

. Outhred 2002

Modelling regulated interconnectors

& intra-region location

•R

egulated interconnector between 2 regions

–M

odelled by a linearised marginal loss function:

•A

‘dynamic’ netw

ork loss factor that depends on flow

•F

low lim

its (security or thermal criteria)

•Locational effects w

ithin regions–

Modelled by ‘static’ netw

ork loss factors (LFs)

•A

nnual average of estimated half-hour m

arginal lossesfor each generator node &

group of consumer nodes

–Intra-regional constraints not m

odelled but a‘constrained-on’ generator cannot set price

National E

lectricity Market D

esign & P

erformance # 12

© H

. Outhred 2002

Service territories of N

SW

distributorsshow

ing transmission loss factors

1.0

31.0161

.03

1.0281.001

0.999

0.959

0.970

1.147

Gen

erator-sp

ecific loss facto

rIn

itial un

iform

distrib

uto

r transm

ission

loss facto

r

National E

lectricity Market D

esign & P

erformance # 13

© H

. Outhred 2002

Effect of intra-regional netw

ork lossfactors on spot m

arket outcomes

ReferenceN

ode(price p

r )

Generator

Consum

er

Qg , LF

g

Qc , LF

c

Generator produces Q

g & is paid p

r x LFg x Q

g

Consum

er consumes Q

c & pays p

r x LFc x Q

c

Net incom

e is given to network service provider(s)

Dispatch offer price =

DO

Pg

Referred offer price =

DO

P/LF

g

National E

lectricity Market D

esign & P

erformance # 14

© H

. Outhred 2002

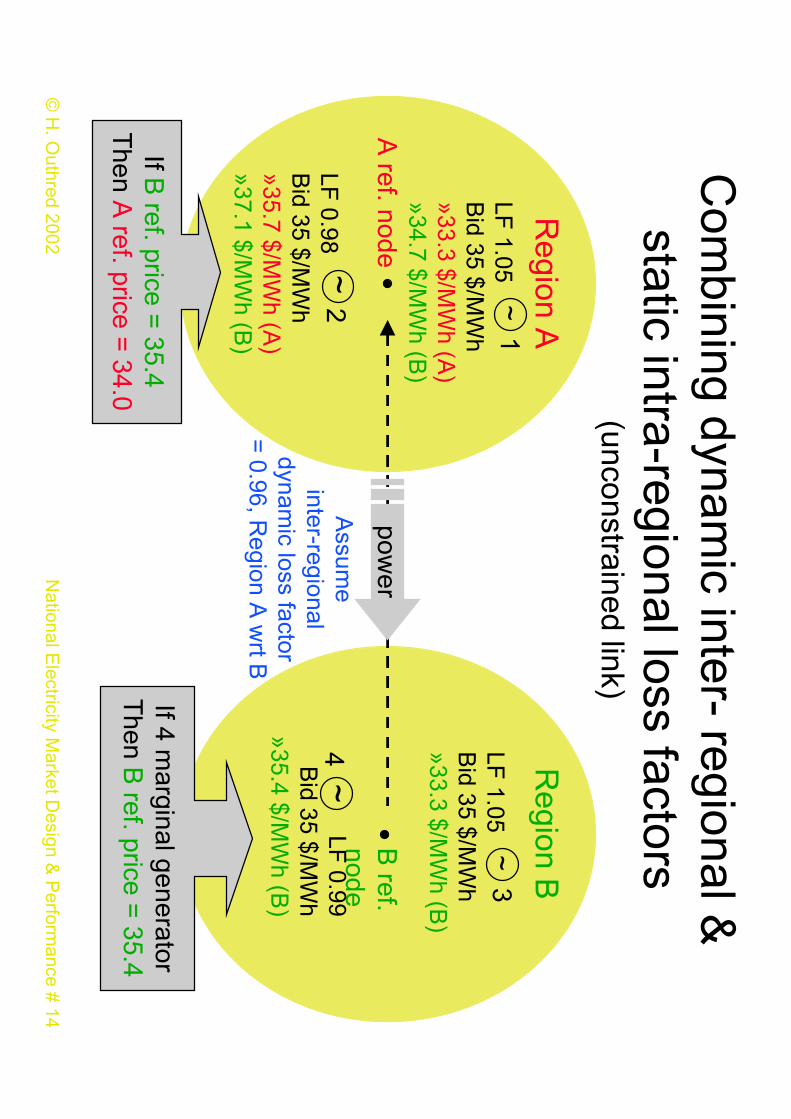

Com

bining dynamic inter- regional &

static intra-regional loss factors(unconstrained link)

Region A

Region B

A ref. node

B ref.

nodeA

ssume

inter-regionaldynam

ic loss factor=

0.96, Region A

wrt B

power

If 4 marginal generator

Then B

ref. price = 35.4

If B ref. price =

35.4T

hen A ref. price =

34.0

LF 1.05

Bid 35 $/M

Wh

»33.3 $/MW

h (A)

»34.7 $/MW

h (B)

~1

LF 1.05

Bid 35 $/M

Wh

»33.3 $/MW

h (B)

~3

LF 0.98

Bid 35 $/M

Wh

»35.7 $/MW

h (A)

»37.1 $/MW

h (B)

~2

LF 0.99

Bid 35 $/M

Wh

»35.4 $/MW

h (B)

~4

National E

lectricity Market D

esign & P

erformance # 15

© H

. Outhred 2002

Dispatch, P

re-dispatch & P

AS

A

0 day 1 day 2 week 1 m

onth 1 year 1 year 2

Medium

Term

PA

SA

Pre-dispatch, re-bid &

final dispatch schedule

Short Term

PA

SA

National E

lectricity Market D

esign & P

erformance # 16

© H

. Outhred 2002

PA

SA

& reserve trader

PA

SA

•Energy

constraints•D

emand

forecasts•N

etwork

capacity

Registration of

available capacitiesD

ay-ahead O

ffers & bids

Pre-dispatch

thendispatch

Invitation to provide m

ore capacity

Purchase of

more capacity

NE

MM

CO

Expected

inadequacy

Purchased capacity

offered to market

(usually at VO

LL)A

vailablecapacity

Settlem

entsP

ayment for

purchased capacity

National E

lectricity Market D

esign & P

erformance # 17

© H

. Outhred 2002

VO

LL, VoE

G &

market intervention

•R

egional ref. spot price cap at ‘VO

LL’:–

‘value of lost load’, initially $5000/MW

h:•

No single correct num

ber

–A

pplies if load is involuntarily curtailed in a region

–O

ther regional reference prices ≤ VO

LL

•R

egional ref. spot price floor at ‘VoE

G’

–‘value of excess generation’ initially -$1000/M

WH

•C

ap & floor m

ay be reduced after 24 hours:–

If (price x hours)> 300,000 $/M

W then cap/floor

set to ±$300 $/MW

H daytim

e, ±$50 off-peak

National E

lectricity Market D

esign & P

erformance # 18

© H

. Outhred 2002

Financial instrum

ent trading in supportof N

EM

•T

rading in hedges & options:

–B

ilateral trading

–O

ver-the-counter instruments

–E

xchange-traded CF

Ds

•Inter-regional hedges:–

Specialised form

of financial instrument:

•to m

anage regional price difference risks

•funded by interconnector settlem

ent residues

–N

EM

MC

O intercon. settlem

ent residue auctions•

Com

menced in 1999

National E

lectricity Market D

esign & P

erformance # 19

© H

. Outhred 2002

Sydney F

utures Exchange C

FD

s for NS

W&

Victorian regional reference prices

Ba

se lo

ad

ele

ctricity futu

res

(since

Se

pt. 1

99

7)

Pe

ak p

erio

de

lectricity fu

ture

s(sin

ce M

arch

19

99

)U

nd

erlyin

gco

mm

od

ityN

EM

reg

ion

en

erg

yp

er ca

len

da

r mo

nth

Mo

nth

ly en

erg

y,7

am

-10

pm

, WW

Ds

Co

ntra

ct un

it5

00

MW

h5

00

MW

h

Tick size

$2

5$

25

Tra

din

g h

orizo

n13 m

onth

s1

3 m

on

ths

Se

ttlem

en

t price

Ave

rag

e sp

ot p

riceo

ver th

e m

on

thA

vera

ge

spo

t price

,7

am

-10

pm

, WW

Ds

National E

lectricity Market D

esign & P

erformance # 20

© H

. Outhred 2002

Market perform

ance

•S

eparate NS

W &

Victorian m

arkets:–

June 1996 to May 1997

•Interim

National E

lectricity Market (N

EM

1)com

bining NS

W &

Victorian m

arkets:–

May 1997 to D

ecember 1998

•N

ational Electricity M

arket (NE

M)

–F

rom D

ecember 1998

National E

lectricity Market D

esign & P

erformance # 21

© H

. Outhred 2002

Co

mp

arison

of W

eekly Vo

lum

e Weig

hted

Averag

e SM

P

0

10

20

30

40

50

60

70

80

Date

Vic S

MP

NS

W S

MP

Separate N

SW

& V

ictorian markets

Weekly average prices, 6/96 - 2/97

Victoria

NS

W

National E

lectricity Market D

esign & P

erformance # 22

© H

. Outhred 2002 C

omm

ents on outcomes in

separate NS

W &

Vic m

arkets

•Long term

average prices were sim

ilar:–

Average prices both ~

$23/MW

h for 7/96-5/97

•P

rices in Victoria m

ore volatile than in NS

W:

–W

ider variation in underlying operating costs

–Inflexible base load plant:

•V

ictorian pool price was zero on occasions

–V

ictorian market sm

aller than NS

W (~

70%)

–S

umm

er demand m

ore temperature sensitive in

Victoria than in N

SW

National E

lectricity Market D

esign & P

erformance # 23

© H

. Outhred 2002

Victorian price-dem

and relationship

•T

he following graph show

s Victorian

demand &

price data sorted by demand:

–H

alf-hourly data pairs for July 1997 - June 98:•

prices are in $ per MW

h, demand is in M

W

•S

ome correlation betw

een price & dem

and

•E

ffective floor price of ~6 $/M

Wh

•P

rices vary for similar load levels

•P

rices often low but som

etimes high:

–Less excess base load capacity than in N

SW

National E

lectricity Market D

esign & P

erformance # 24

© H

. Outhred 2002

1997/98 Victo

rian L

DC

with

Price

(trun

cated at $200/M

Wh

)

0

10

00

20

00

30

00

40

00

50

00

60

00

70

00

80

00

12

00

14

00

16

00

18

00

11

00

01

12

00

11

40

01

16

00

1

Half hours

MW

0.0

0

20

.00

40

.00

60

.00

80

.00

10

0.0

0

12

0.0

0

14

0.0

0

16

0.0

0

18

0.0

0

20

0.0

0

$/MW

h

De

ma

nd

Price

Floor price for Vic ~$6

National E

lectricity Market D

esign & P

erformance # 25

© H

. Outhred 2002

Daily average prices, 1/97 - 11/97

(NE

M1 joint m

arket comm

enced May ‘97)

National E

lectricity Market D

esign & P

erformance # 26

© H

. Outhred 2002

Daily average prices, 12/97- 11/98

(change in NS

W vesting contracts)

National E

lectricity Market D

esign & P

erformance # 27

© H

. Outhred 2002

Victorian Price D

uration Curves, 94/95 -97/98(truncated at $300 M

Wh)

0.00

50.00

100.00

150.00

200.00

250.00

300.00

% Tim

e value exceeded

$/MWh

94/9595/9696/9797/98

National E

lectricity Market D

esign & P

erformance # 28

© H

. Outhred 2002

Com

ments on N

EM

1

•P

rior to NE

M1:

–P

rices were m

ore volatile in Victoria than in N

SW

•D

uring NE

M1:

–N

SW

& V

ictorian spot prices usually similar

–A

verage spot prices fell•

Additional com

petitive pressures–

even the Victorian m

arket with 5 com

peting base load plantm

ay not have been ‘fully’ competitive

–V

icpool 3 in 1994 still had one-week offers

–N

et flow on inter-connector from

Victoria to N

SW

National E

lectricity Market D

esign & P

erformance # 29

© H

. Outhred 2002

Price history since N

EM

inception(Q

uarterly averages, 12/98-6/02) (NE

CA

, 2002)

National E

lectricity Market D

esign & P

erformance # 30

© H

. Outhred 2002

Price-dem

andplots for N

EM

Queensland &

NS

W regions

Sept-D

ec 2000($/M

WH

vs MW

)(N

EC

A, 2000)

National E

lectricity Market D

esign & P

erformance # 31

© H

. Outhred 2002

Price-dem

andplots for N

EM

Victoria &

SA

regions S

ept-Dec 2000

($/MW

H vs M

W)

(NE

CA

, 2001)

National E

lectricity Market D

esign & P

erformance # 32

© H

. Outhred 2002

BC

A concerns about m

arket power

•B

CA

concerns about EI restructuring:

–Insufficient disaggregation of generation:

•In N

SW

, Queensland &

South A

ustralia

–N

ew interconnectors face too m

uch uncertainty

–N

etwork pricing distorted

–R

egulation cumbersom

e

•H

owever B

CA

recomm

ends improvem

entrather than radical change:–

Market design is basically sound

National E

lectricity Market D

esign & P

erformance # 33

© H

. Outhred 2002

Generator energy m

arket shares (%)

in NS

W &

Victoria, 1997-98 (E

SA

A, 1999)

& possible T

asmania scenario

0 20 40 60 80

12

34

5o

ther

NS

W Victo

ria

Tasm

ania

Theory & experience suggest ≤ 20%

share to avoid market pow

er

National E

lectricity Market D

esign & P

erformance # 34

© H

. Outhred 2002

Reducing generation to raise spot m

arket price(dem

and-side response: forward contract or reduce dem

and)(source: E

risk & B

ardak Group quoted by J W

ashusen, Pareto)

LY

A cap

acityred

uced

in re-

bid

to raise

spo

t price

National E

lectricity Market D

esign & P

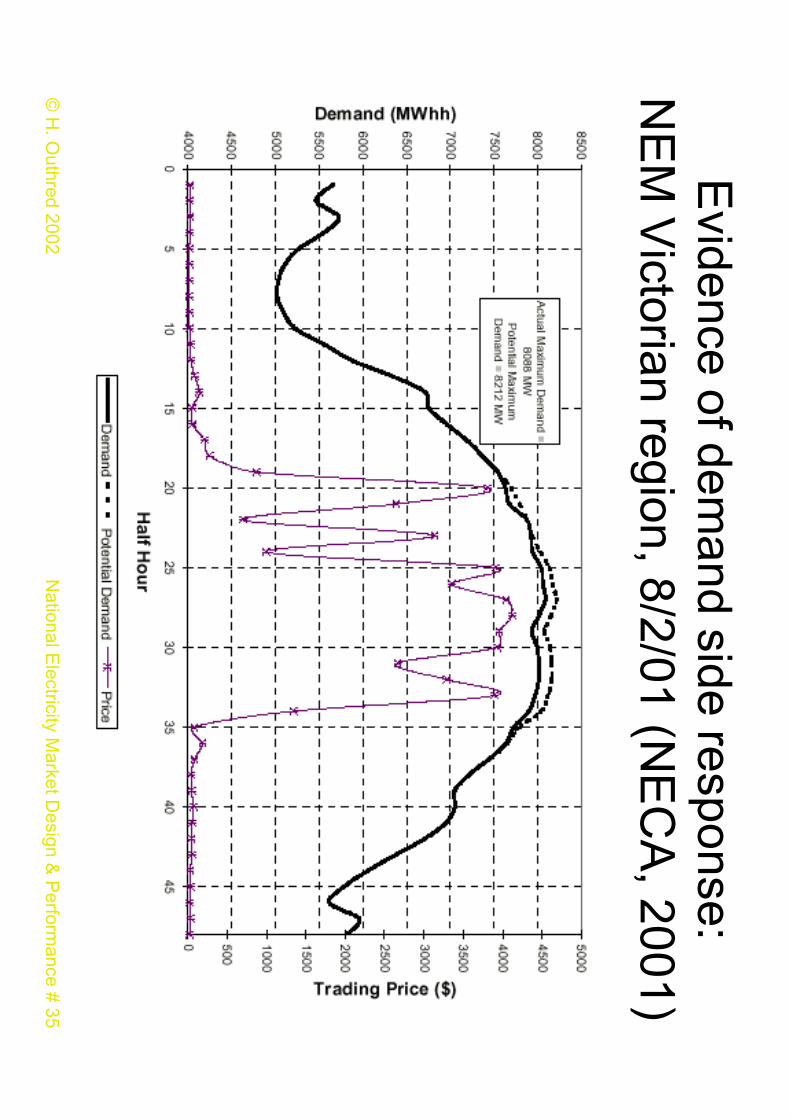

erformance # 35

© H

. Outhred 2002

Evidence of dem

and side response:N

EM

Victorian region, 8/2/01 (N

EC

A, 2001)

National E

lectricity Market D

esign & P

erformance # 36

© H

. Outhred 2002 F

uture directions for NE

M

•Im

proved network representation:

–M

ore (smaller) m

arket regions–

More m

arket network service providers

–B

etter locational signals for distributed resources

•Im

proved ancillary service arrangements:

–Increased use of com

petitive tendering &“causer pays”

•Im

proved bidding arrangements

•C

OA

G R

eview