exchange rate systems

DESCRIPTION

- PowerPoint PPT PresentationTRANSCRIPT

Exchange Rate SystemsExchange Rate Systems

This chapter deals with exchange rate systems. We first consider the concept of exchange rate, and then discuss the operations and adjustment mechanisms under the floating exchange rate system and the fixed exchange rate system. We also provide a brief history of the international monetary and exchange rate systems, which can help us to examine the advantages and disadvantages of the two exchange rate systems.

Dr. Lam Pun LeeDr. Lam Pun Lee

Advanced LevelMicroeconomicsAdvanced Level

Macroeconomics

2

P.124 -- 12.2 Exchange Rate

• is the amount of domestic currency exchanged for one unit of foreign currency

• is the price of foreign currency in terms of domestic currency

US$1¥100

6

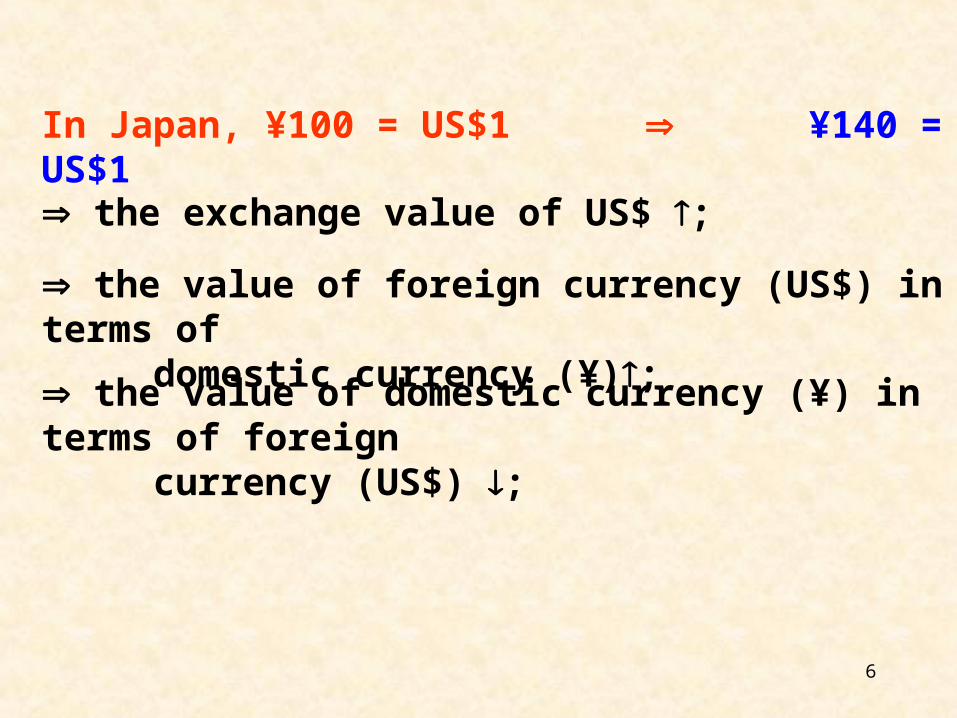

In Japan, ¥100 = US$1 ¥140 = US$1

the exchange value of US$ ;

the value of foreign currency (US$) in terms of domestic currency (¥);

the value of domestic currency (¥) in terms of foreign currency (US$) ;

7

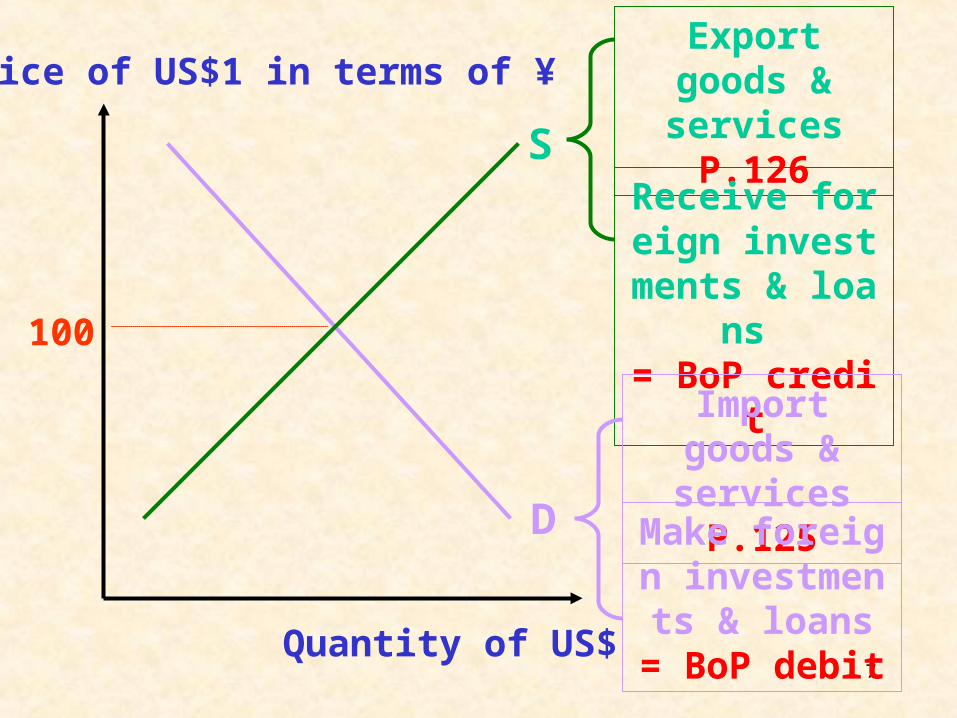

Price of US$1 in terms of ¥

Quantity of US$

100

D

S

Export goods & services P.126

Receive foreign investments & l

oans = BoP credit

Import goods & services P.125

Make foreign investments & loa

ns= BoP debit

8

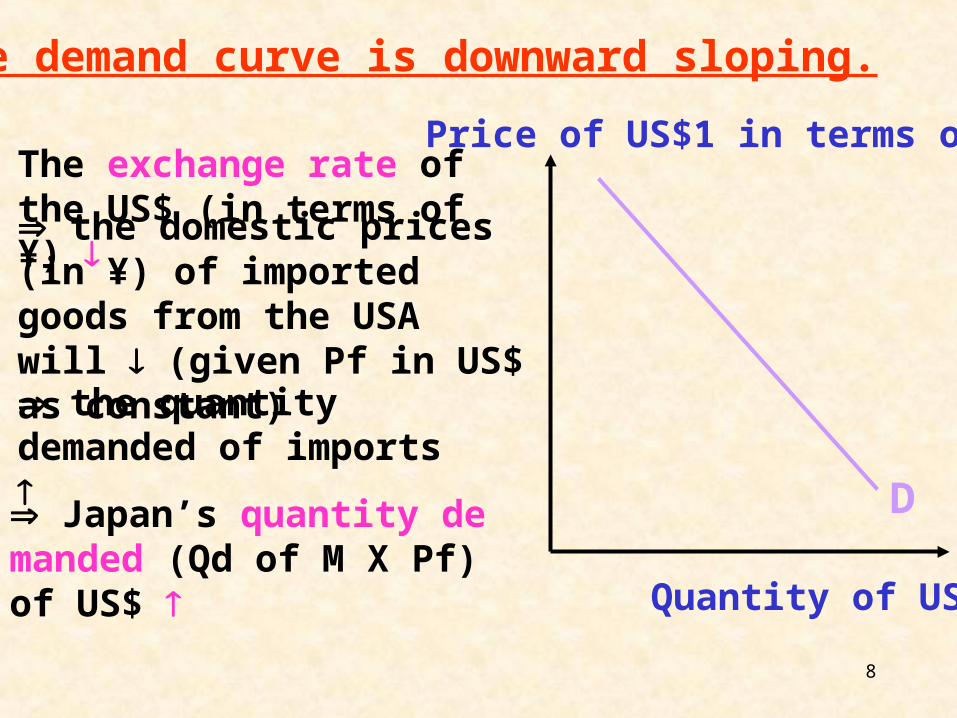

The demand curve is downward sloping.

Quantity of US$

D

Price of US$1 in terms of ¥The exchange rate of the US$ (in terms of ¥) the domestic prices (in ¥) of imported goods from the USA will (given Pf in US$ as constant) the quantity demanded of imports

Japan’s quantity demanded (Qd of M X Pf) of US$

9

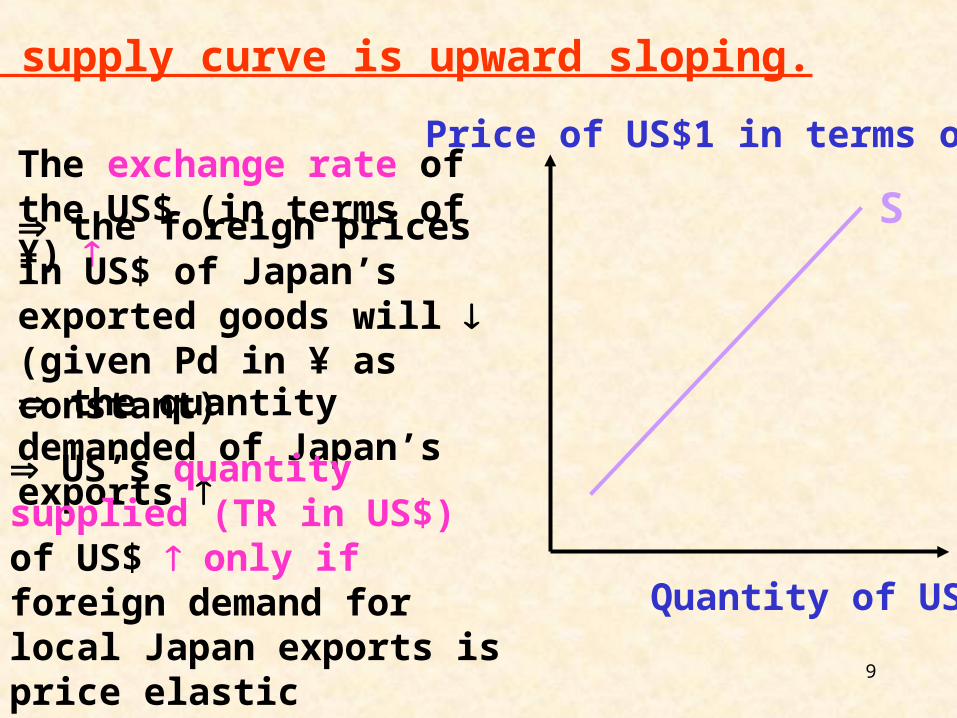

The supply curve is upward sloping.

Quantity of US$

S

Price of US$1 in terms of ¥The exchange rate of the US$ (in terms of ¥)

the foreign prices in US$ of Japan’s exported goods will (given Pd in ¥ as constant)

the quantity demanded of Japan’s exports US’s quantity supplied (TR in US$) of US$ only if foreign demand for local Japan exports is price elastic

10

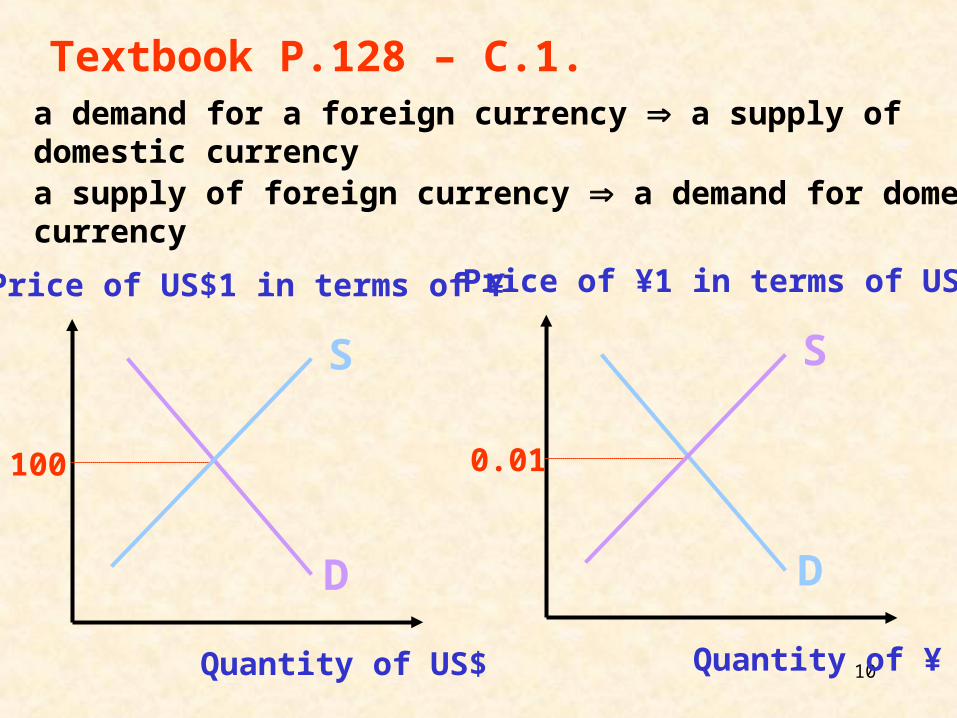

Price of US$1 in terms of ¥

Quantity of US$

100

D

S

Price of ¥1 in terms of US$

Quantity of ¥

0.01

D

S

a demand for a foreign currency a supply of domestic currency

a supply of foreign currency a demand for domestic currency

Textbook P.128 – C.1.

12

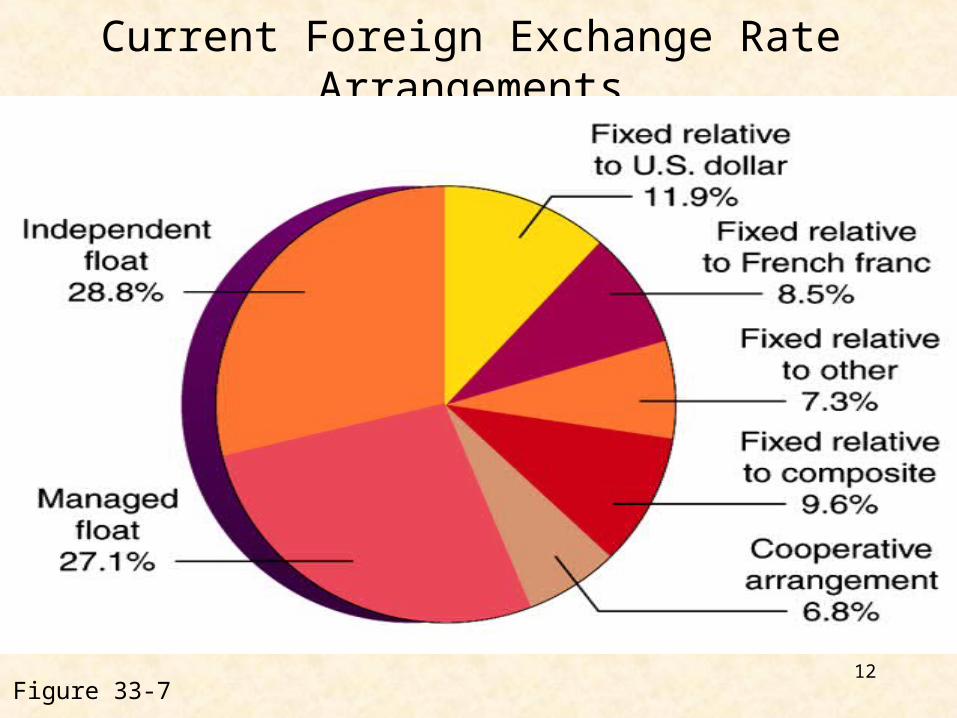

Current Foreign Exchange Rate Arrangements

Figure 33-7

13

15

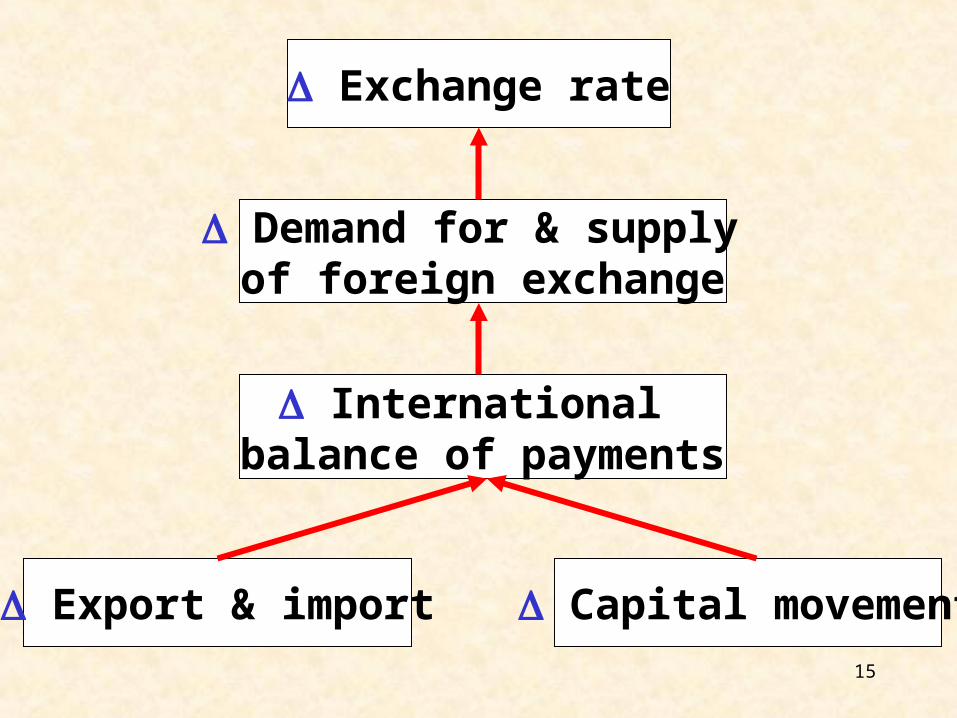

Exchange rate

Demand for & supply of foreign exchange

International balance of payments

Export & import Capital movement

17

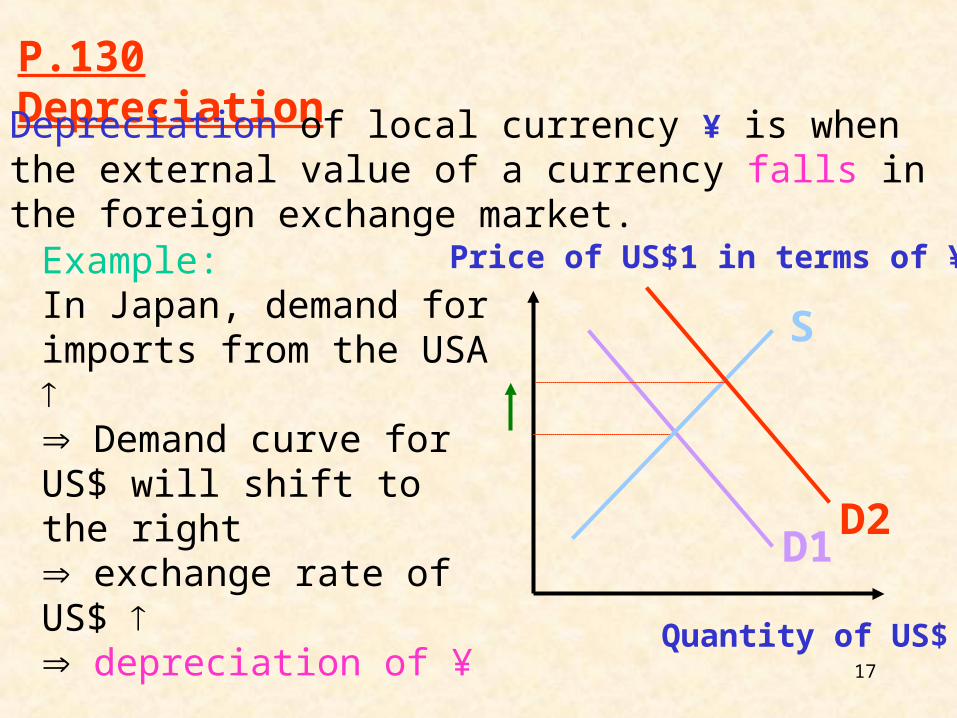

P.130 Depreciation

Depreciation of local currency ¥ is when the external value of a currency falls in the foreign exchange market.

Example: In Japan, demand for imports from the USA Demand curve for US$ will shift to the right exchange rate of US$ depreciation of ¥

Price of US$1 in terms of ¥

Quantity of US$

D1

S

D2

18

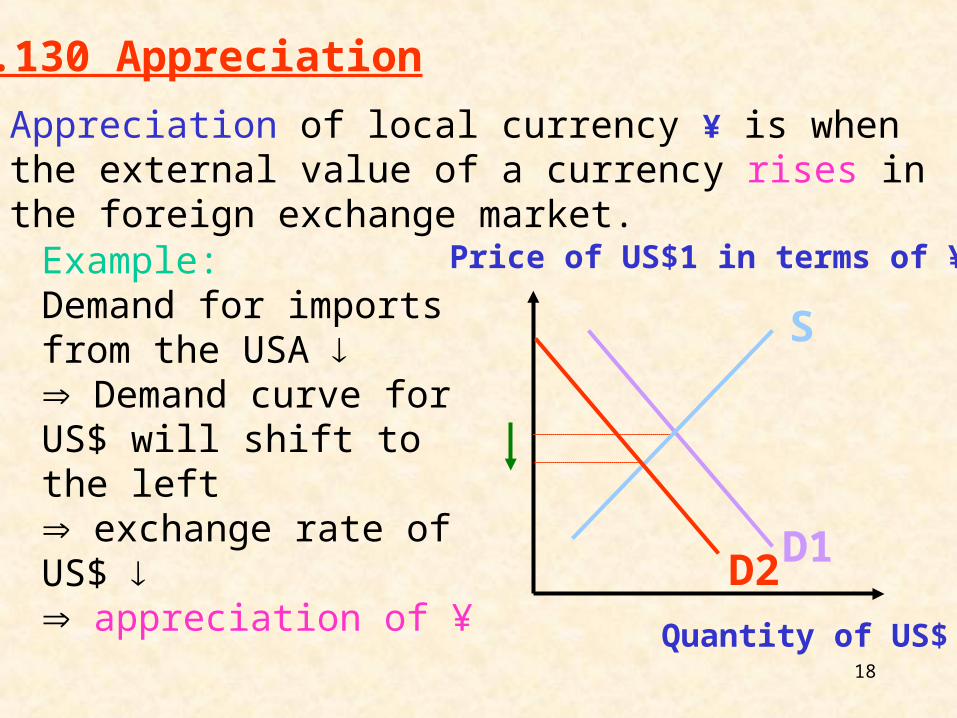

P.130 Appreciation

Appreciation of local currency ¥ is when the external value of a currency rises in the foreign exchange market.

Example: Demand for imports from the USA Demand curve for US$ will shift to the left exchange rate of US$ appreciation of ¥

Price of US$1 in terms of ¥

Quantity of US$

D1

S

D2

20

21

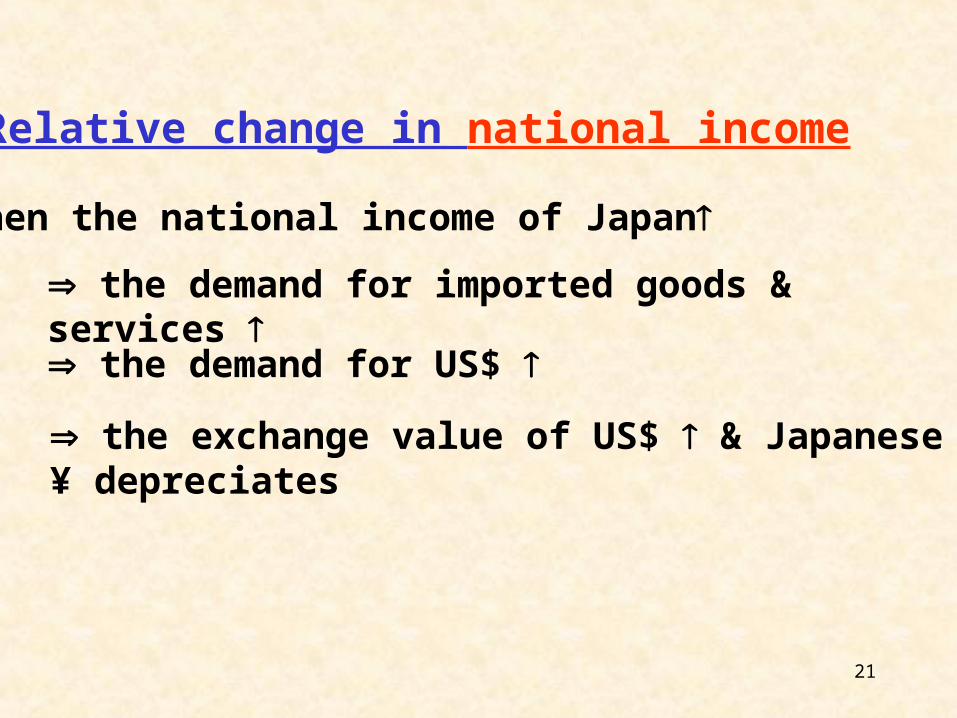

1. Relative change in national income

the demand for imported goods & services

the demand for US$

the exchange value of US$ & Japanese ¥ depreciates

When the national income of Japan

22

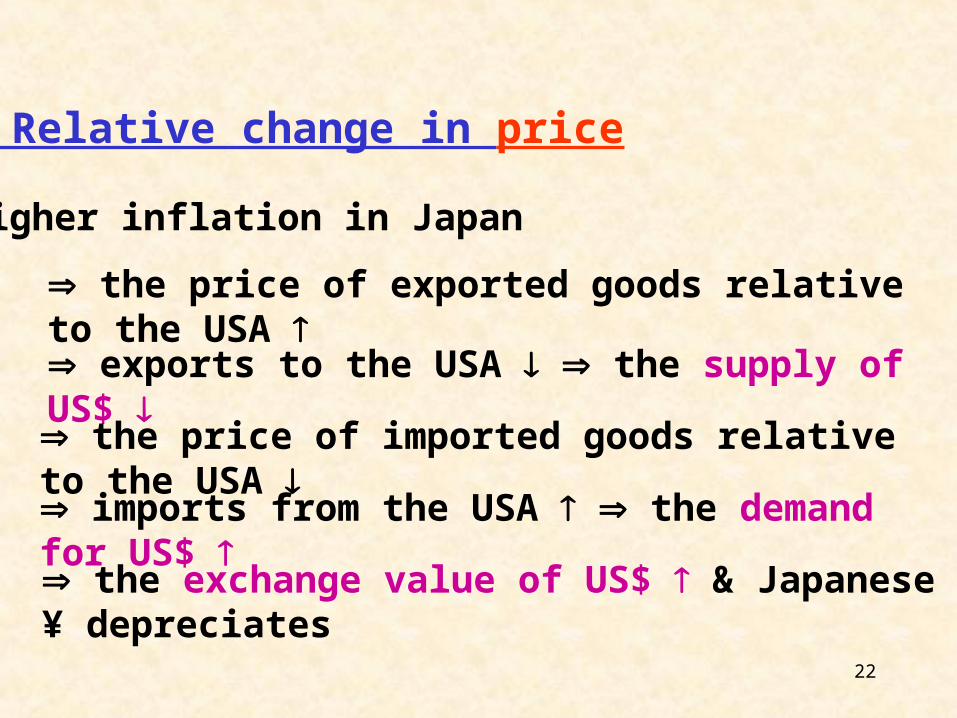

2. Relative change in price

the price of exported goods relative to the USA

exports to the USA the supply of US$

the exchange value of US$ & Japanese ¥ depreciates

Higher inflation in Japan

the price of imported goods relative to the USA

imports from the USA the demand for US$

26

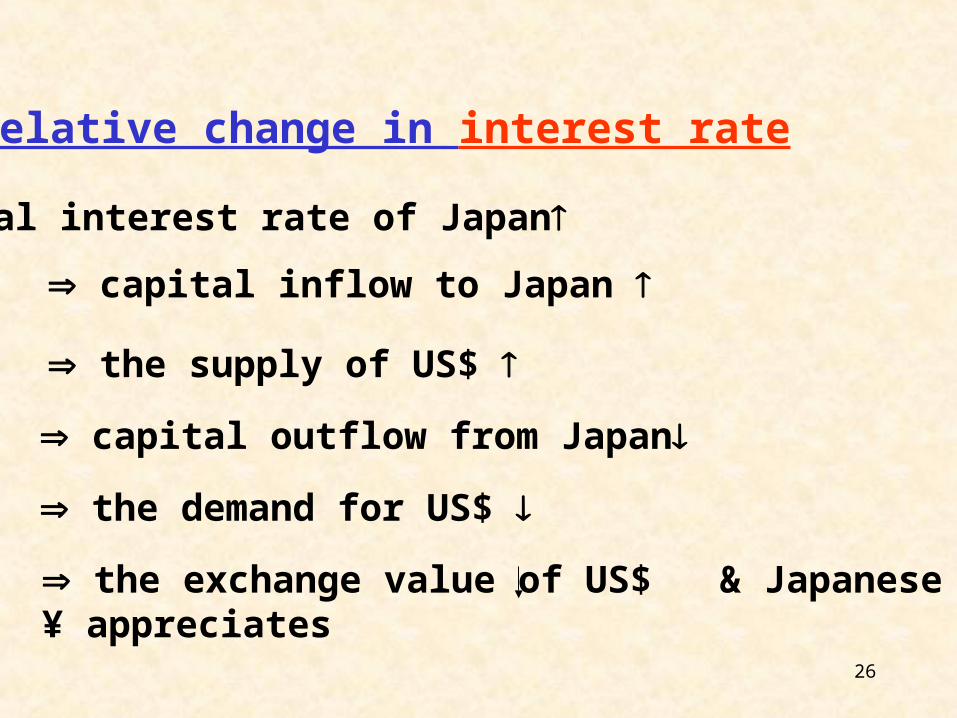

3. Relative change in interest rate

capital inflow to Japan

the supply of US$

the exchange value of US$ & Japanese ¥ appreciates

Real interest rate of Japan

capital outflow from Japan

the demand for US$

27

The Exchange Rate

Interest Rate Parity–Money is worth what it can

earn.

–Interest rate parity means equal interest rates.

28

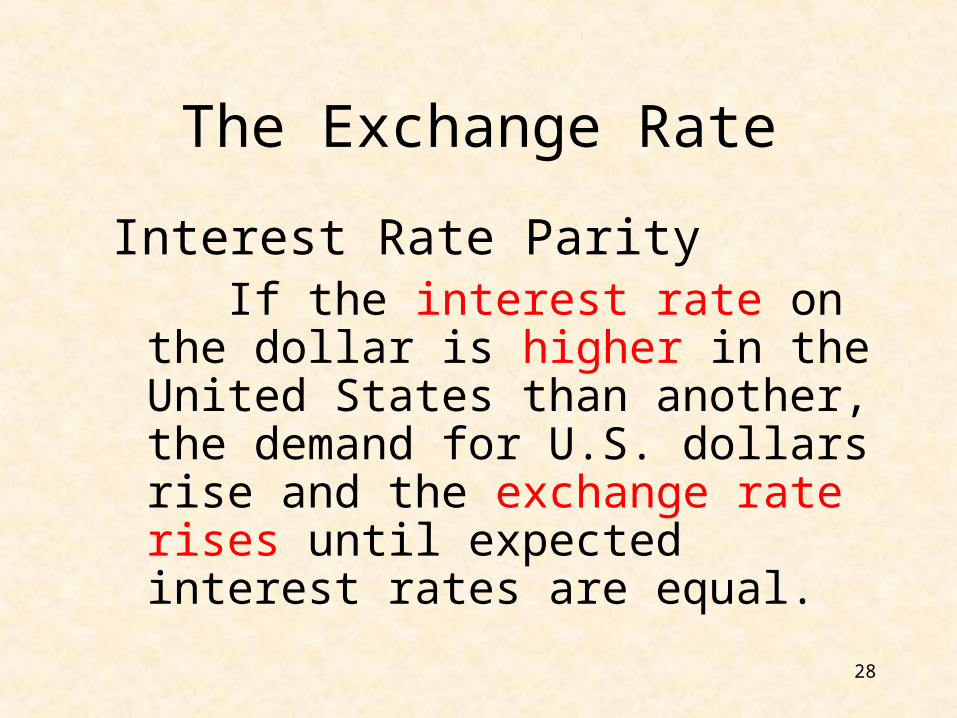

The Exchange Rate

Interest Rate Parity If the interest rate on the dollar is

higher in the United States than another, the demand for U.S. dollars rise and the exchange rate rises until expected interest rates are equal.

29

30

The Exchange Rate

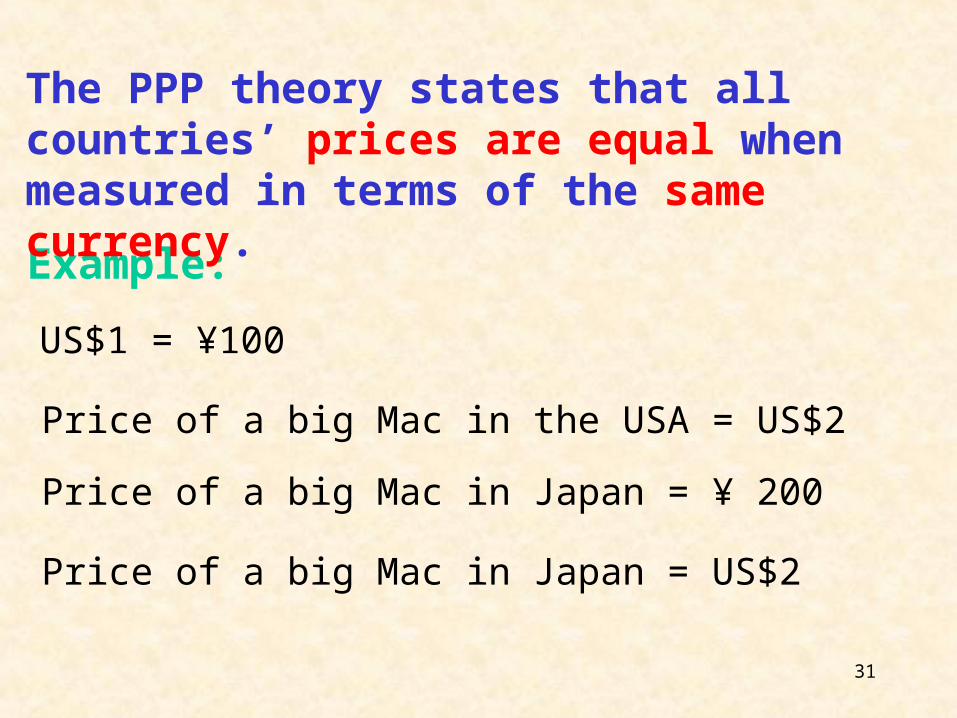

Purchasing Power Parity– Money is worth what it will buy.

– Purchasing power parity means equal value of money.

31

Example:

US$1 = ¥100

Price of a big Mac in the USA = US$2

The PPP theory states that all countries’ prices are equal when measured in terms of the same currency.

Price of a big Mac in Japan = ¥ 200

Price of a big Mac in Japan = US$2

32

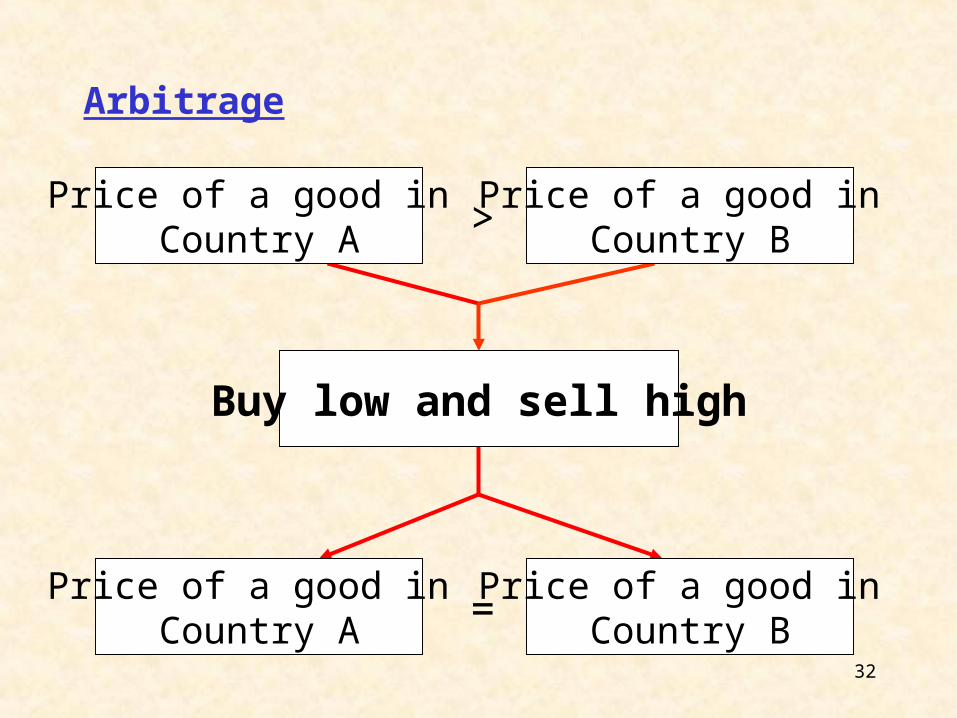

Arbitrage

Price of a good in Country A >

Price of a good in Country B

Buy low and sell high

Price of a good in Country A =

Price of a good in Country B

33

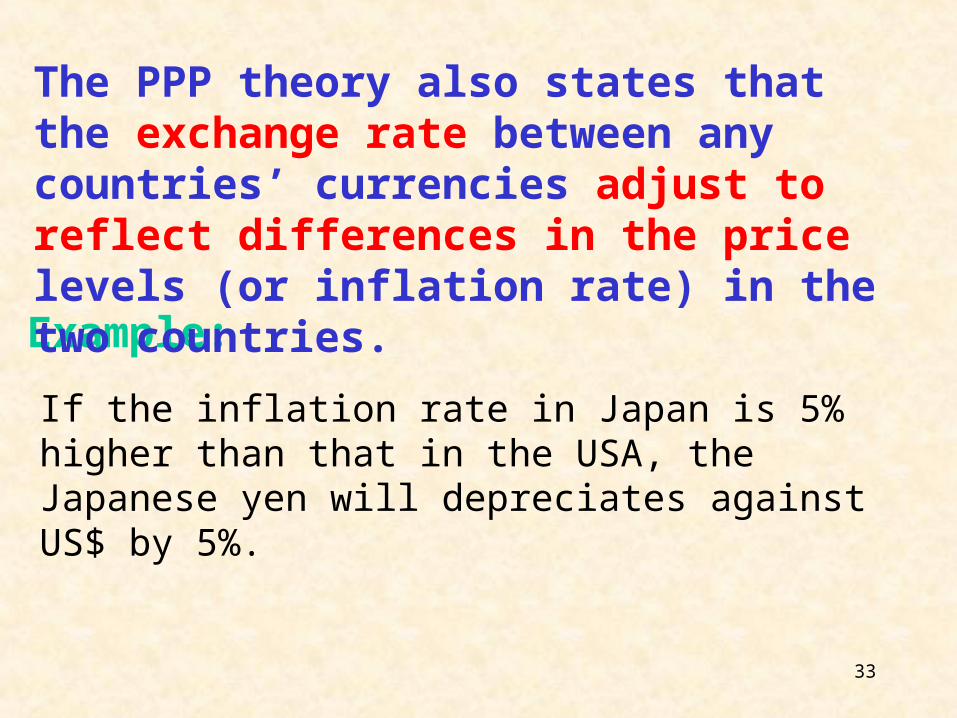

Example:

If the inflation rate in Japan is 5% higher than that in the USA, the Japanese yen will depreciates against US$ by 5%.

The PPP theory also states that the exchange rate between any countries’ currencies adjust to reflect differences in the price levels (or inflation rate) in the two countries.

35

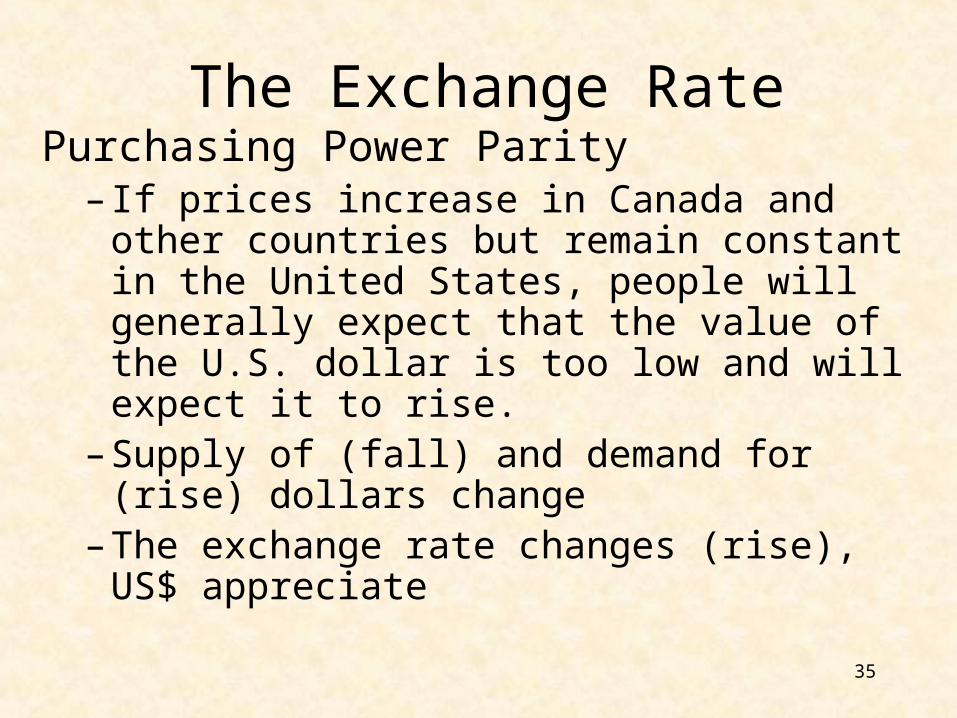

The Exchange RatePurchasing Power Parity

– If prices increase in Canada and other countries but remain constant in the United States, people will generally expect that the value of the U.S. dollar is too low and will expect it to rise.

– Supply of (fall) and demand for (rise) dollars change

– The exchange rate changes (rise), US$ appreciate

36

37

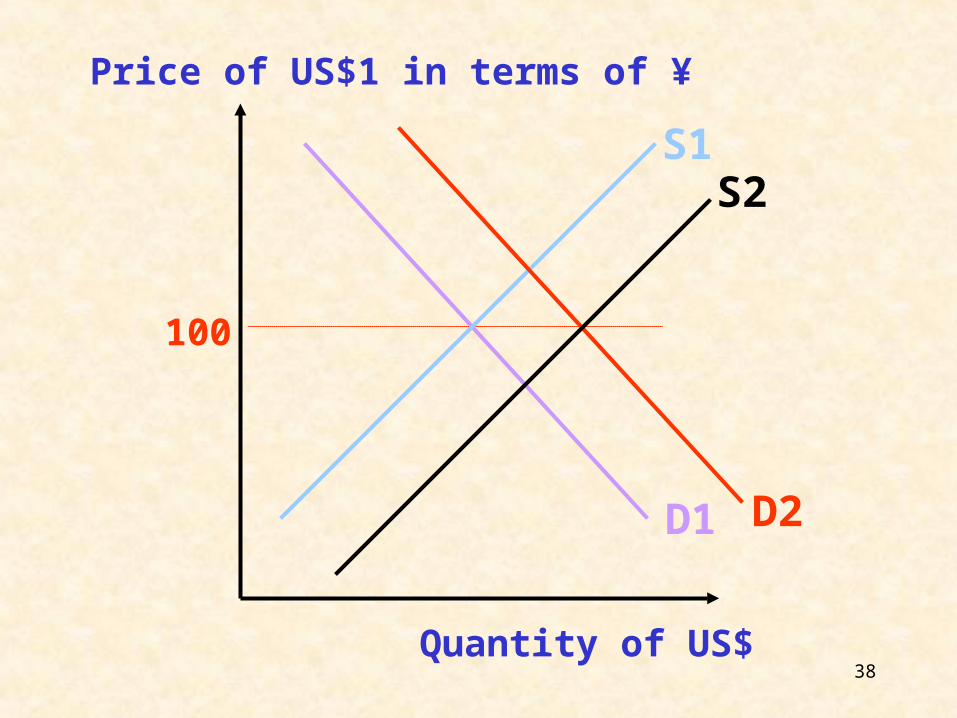

The fixed exchange rate system is the system whereby the exchange rate is set by a government or by agreement among countries (Lam 1996: 297).

In a country adopting a fixed exchange rate system, the monetary authority of the country buys and sells foreign currencies to maintain the value of its domestic currency in the foreign exchange market.

38

Price of US$1 in terms of ¥

Quantity of US$

100

D1

S1

D2

S2

39

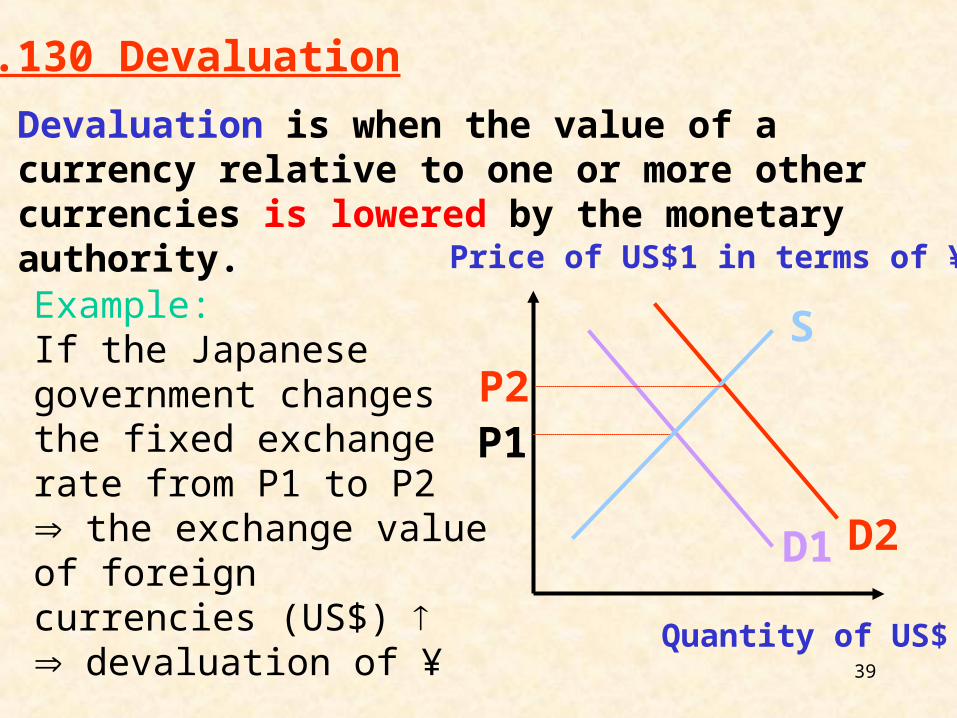

P.130 Devaluation

Devaluation is when the value of a currency relative to one or more other currencies is lowered by the monetary authority.

Example: If the Japanese government changes the fixed exchange rate from P1 to P2 the exchange value of foreign currencies (US$) devaluation of ¥

D2

Price of US$1 in terms of ¥

Quantity of US$

D1

S

P1P2

40

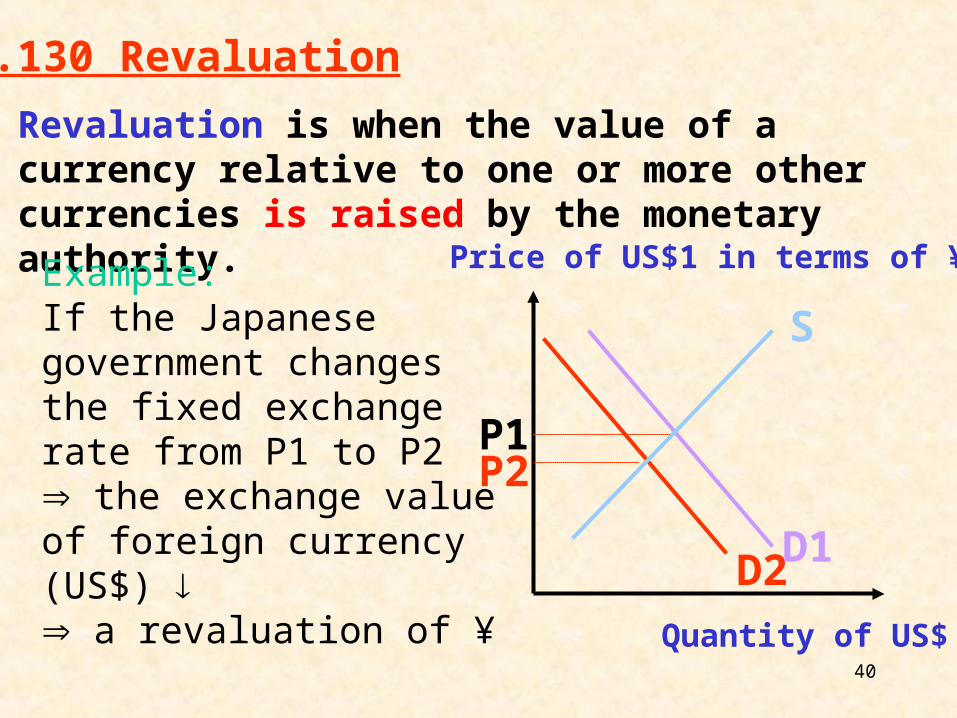

P.130 Revaluation

Revaluation is when the value of a currency relative to one or more other currencies is raised by the monetary authority.

Example: If the Japanese government changes the fixed exchange rate from P1 to P2 the exchange value of foreign currency (US$) a revaluation of ¥

D2

Price of US$1 in terms of ¥

Quantity of US$

D1

S

P1P2

41

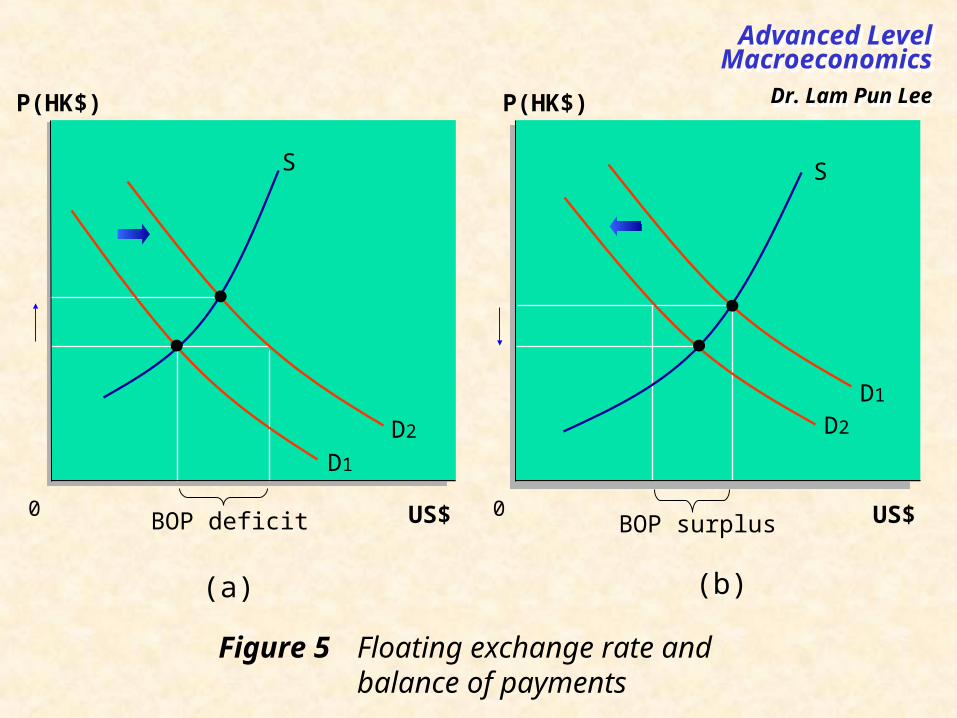

Figure 5 Floating exchange rate and balance of payments

0 US$

P(HK$)

S

D1

D2

0 US$

P(HK$)

S

D1

D2

(a) (b)

BOP deficit BOP surplus

Dr. Lam Pun LeeDr. Lam Pun Lee

Advanced LevelMicroeconomicsAdvanced Level

Macroeconomics

43

Under a floating exchange rate system, the market mechanism would operate to restore equilibrium simultaneously in the BOP and the exchange rate.

Whenever a country experiences a BOP deficit, the country’s currency will depreciate to restore equilibrium in the BOP.

Whenever a country experiences a BOP surplus, the country’s currency will appreciate to restore equilibrium in the BOP.

46

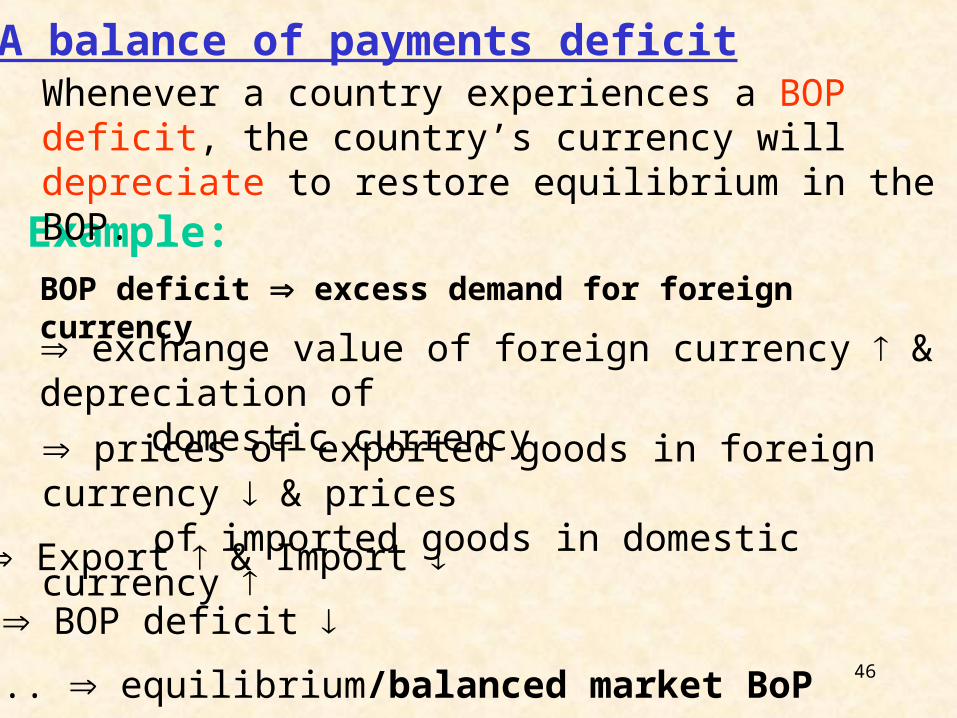

1. A balance of payments deficit

Example:BOP deficit excess demand for foreign currency

exchange value of foreign currency & depreciation of domestic currency

prices of exported goods in foreign currency & prices of imported goods in domestic currency

Export & Import

... equilibrium/balanced market BoP

Whenever a country experiences a BOP deficit, the country’s currency will depreciate to restore equilibrium in the BOP.

BOP deficit

47

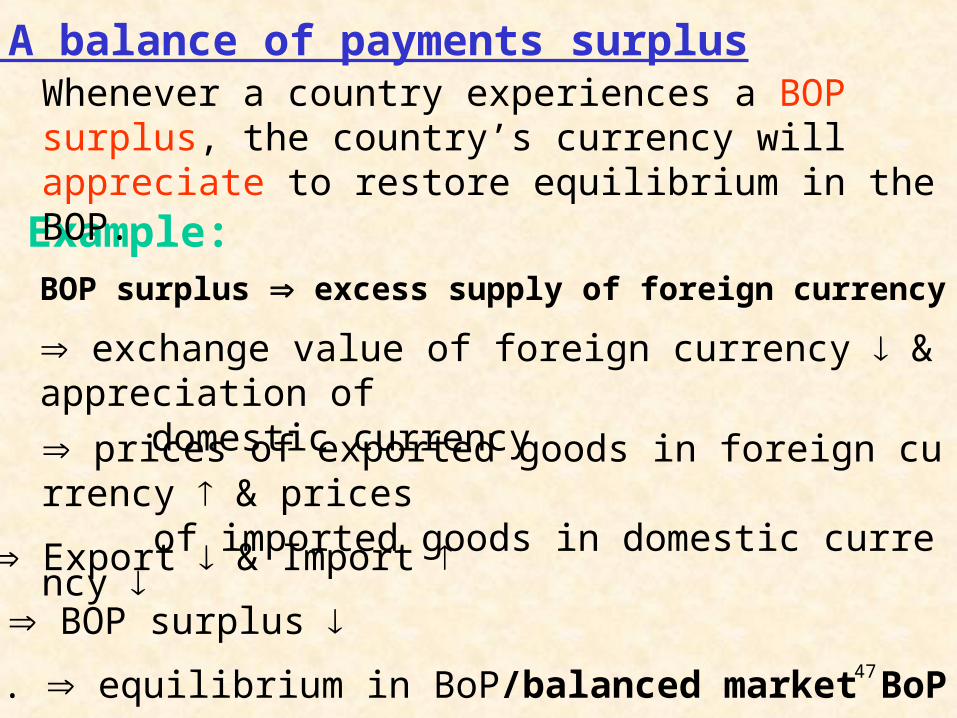

2. A balance of payments surplus

Example:BOP surplus excess supply of foreign currency

exchange value of foreign currency & appreciation of domestic currency

prices of exported goods in foreign currency & prices of imported goods in domestic currency

Export & Import

... equilibrium in BoP/balanced market BoP

Whenever a country experiences a BOP surplus, the country’s currency will appreciate to restore equilibrium in the BOP.

BOP surplus

48

49

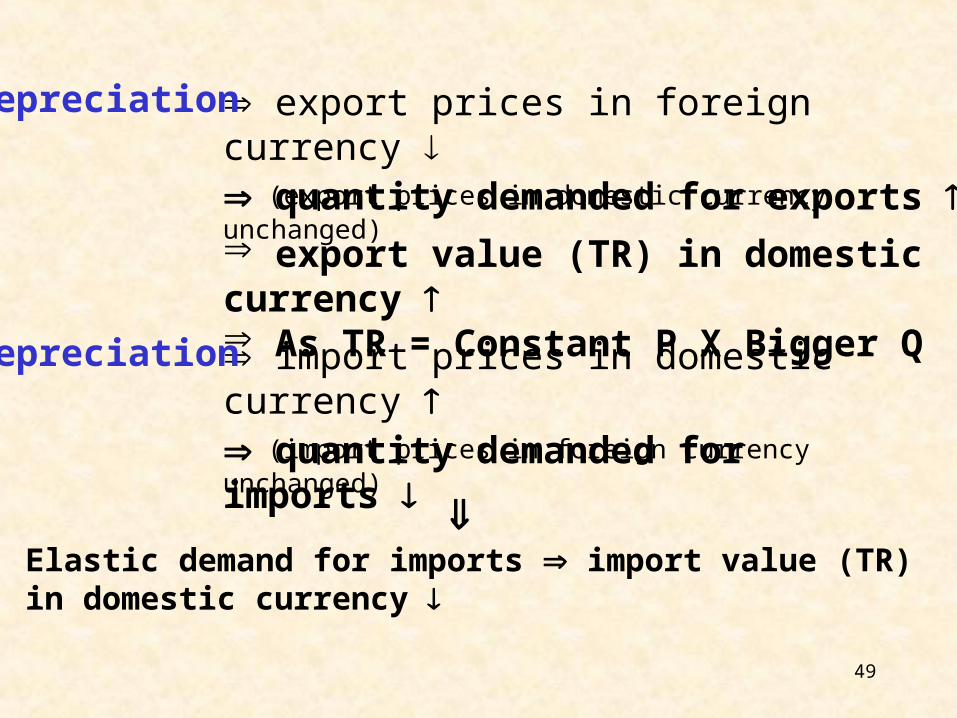

export prices in foreign currency (export prices in domestic currency unchanged)

quantity demanded for exports

Depreciation

export value (TR) in domestic currency As TR = Constant P X Bigger Q

import prices in domestic currency (import prices in foreign currency unchanged)

quantity demanded for imports

Depreciation

Elastic demand for imports import value (TR) in domestic currency

50

The Marshall-Lerner condition says that depreciation (or in fixed ERS, devaluation) will improve the balance of payments position of a countryprovided that the sum of elasticities of foreign demand for domestic exports and domestic demand for imports is greater than unity (1).

51

52

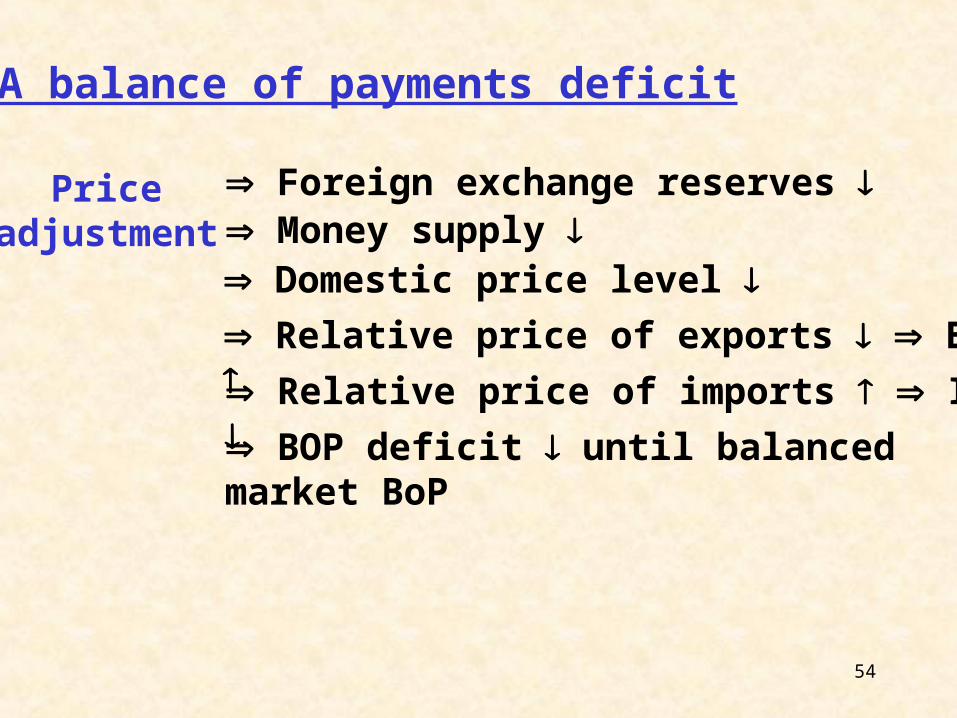

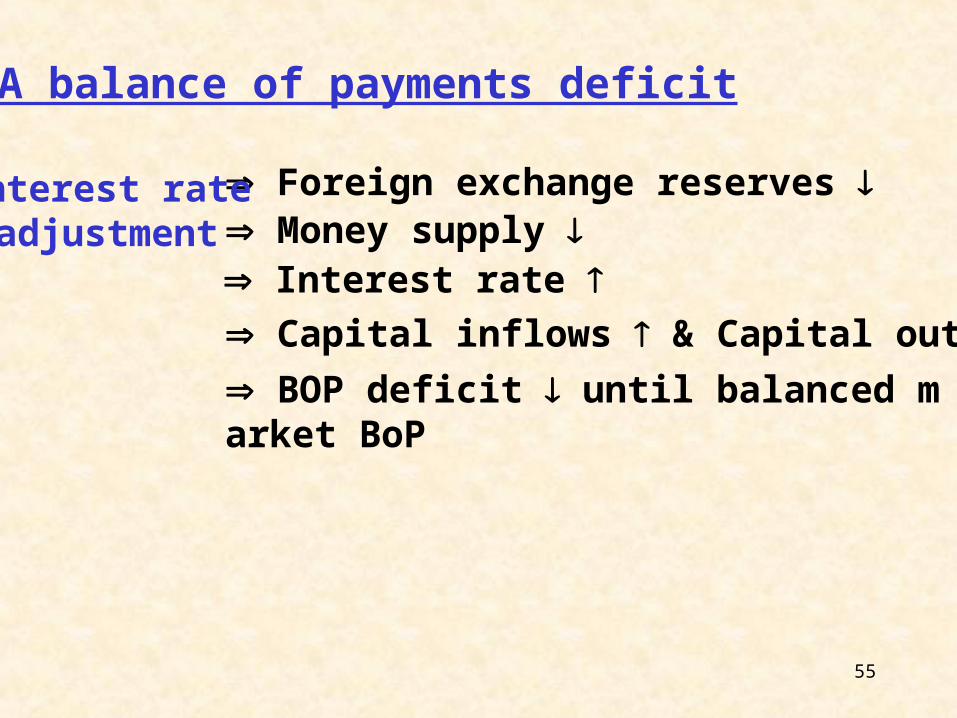

Under a fixed exchange rate system, the country’s currency is backed up with foreign currencies.

53

When there is a BOP deficit (e.g. X < M),

the foreign reserves of that country will fall.

This also implies a fall in the country’s money supply.

Price (fall) and real interest rate (rise) adjustment can restore the BoP to equilibrium/balanced market BoP.

1. A balance of payments deficit

54

Foreign exchange reserves

Domestic price level

Price adjustment

Relative price of exports Exports

Money supply

Relative price of imports Imports BOP deficit until balanced market BoP

1. A balance of payments deficit

55

Foreign exchange reserves

Interest rate

Interest rate adjustment Money supply

Capital inflows & Capital outflows BOP deficit until balanced market BoP

1. A balance of payments deficit

56

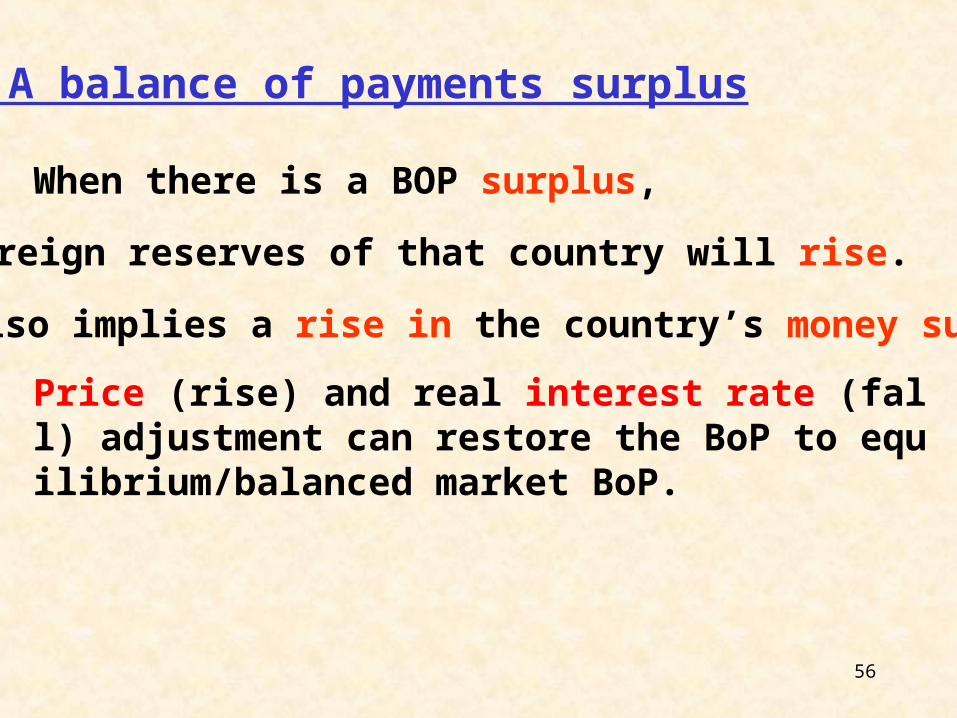

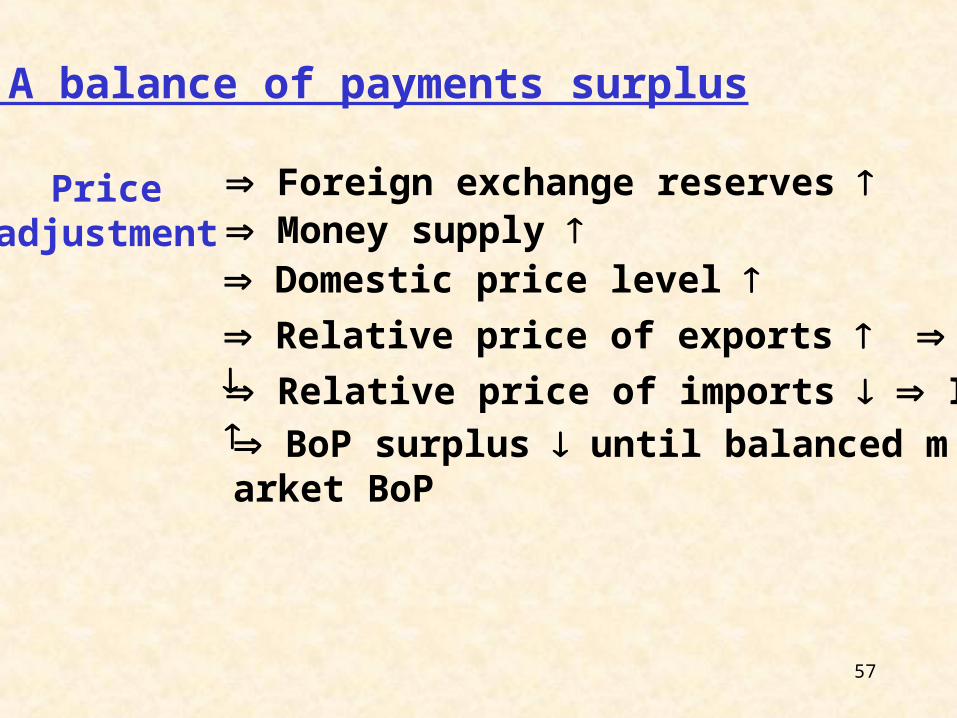

When there is a BOP surplus,

the foreign reserves of that country will rise.

This also implies a rise in the country’s money supply.

Price (rise) and real interest rate (fall) adjustment can restore the BoP to equilibrium/balanced market BoP.

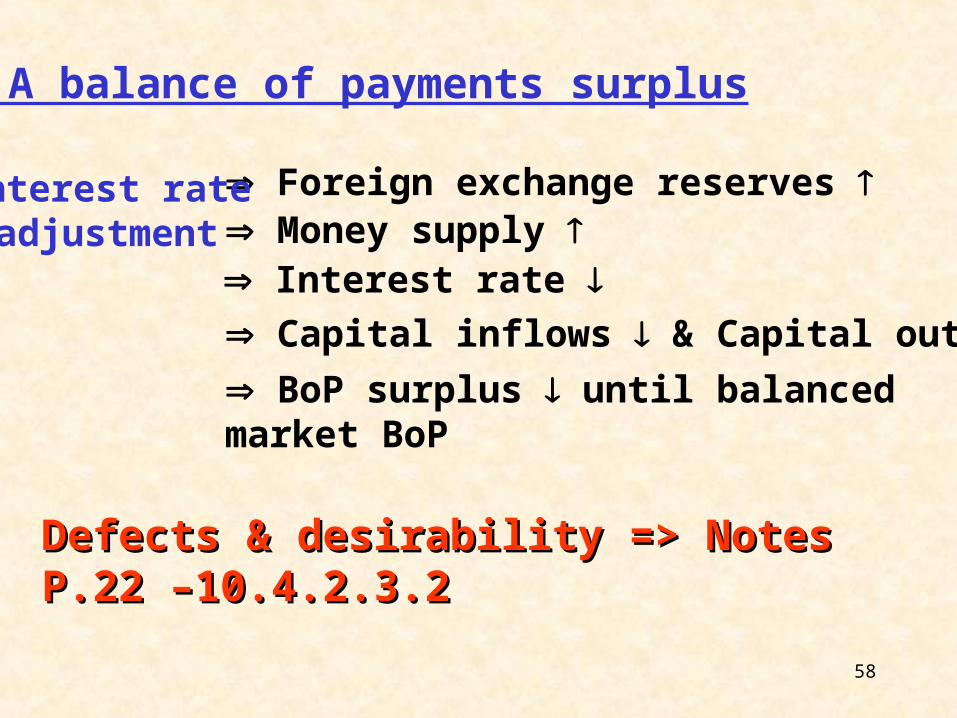

2. A balance of payments surplus

57

Foreign exchange reserves

Domestic price level

Price adjustment

Relative price of exports Exports

Money supply

Relative price of imports Imports

BoP surplus until balanced market BoP

2. A balance of payments surplus

58

Foreign exchange reserves

Interest rate

Interest rate adjustment Money supply

Capital inflows & Capital outflows BoP surplus until balanced market BoP

1. A balance of payments surplus

Defects & desirability => Notes P.22 –10.4.2.3.2 Defects & desirability => Notes P.22 –10.4.2.3.2

59

60

Although there is an automatic adjustment mechanism under a fixed exchange rate system, the system may work very

s…l….o…..w.…..l…….y.

Therefore, some governments would like to employ other measures to help correct the BoP Imbalances more quickly.

61

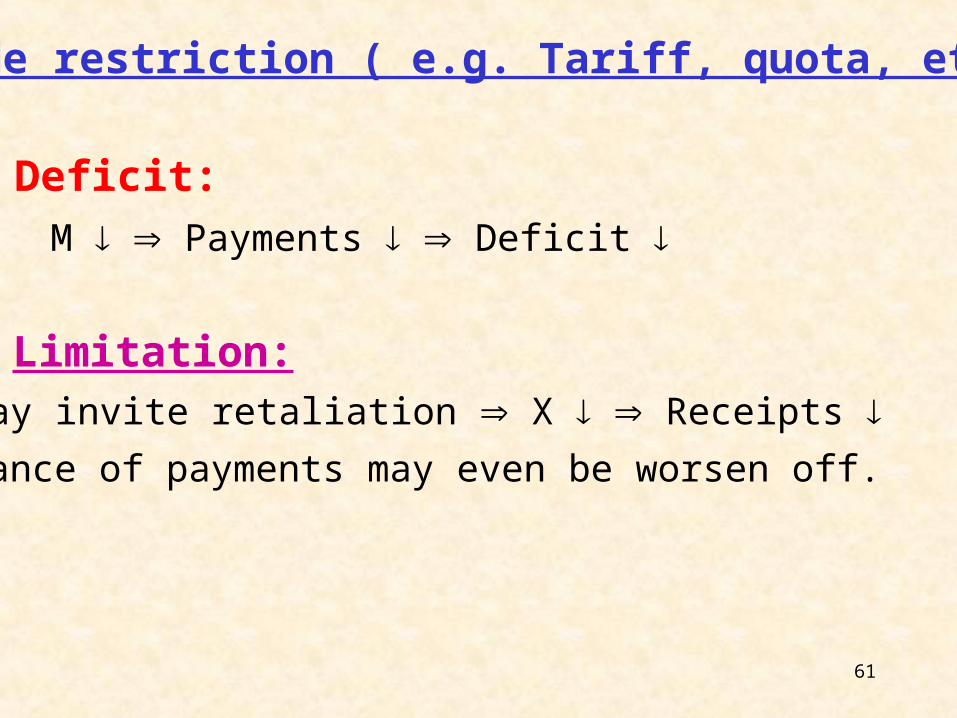

1. Trade restriction ( e.g. Tariff, quota, etc.)

M Payments Deficit

Deficit:

It may invite retaliation X Receipts Balance of payments may even be worsen off.

Limitation:

62

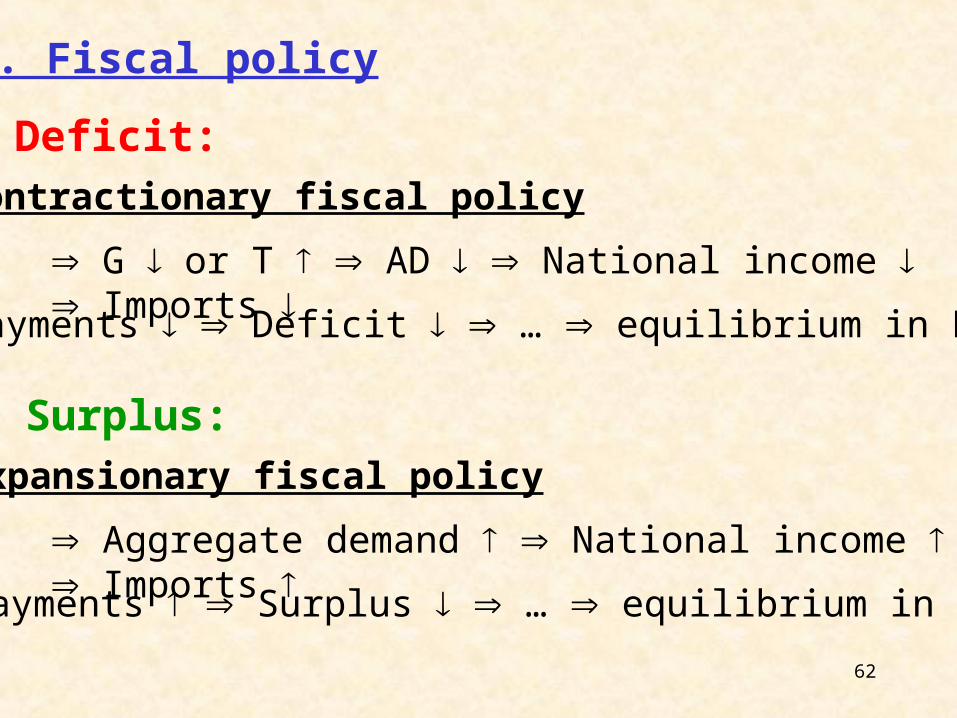

3. Fiscal policy

Contractionary fiscal policy

G or T AD National income Imports

Payments Deficit … equilibrium in BOP

Deficit:

Expansionary fiscal policy

Aggregate demand National income Imports

Payments Surplus … equilibrium in BOP

Surplus:

63

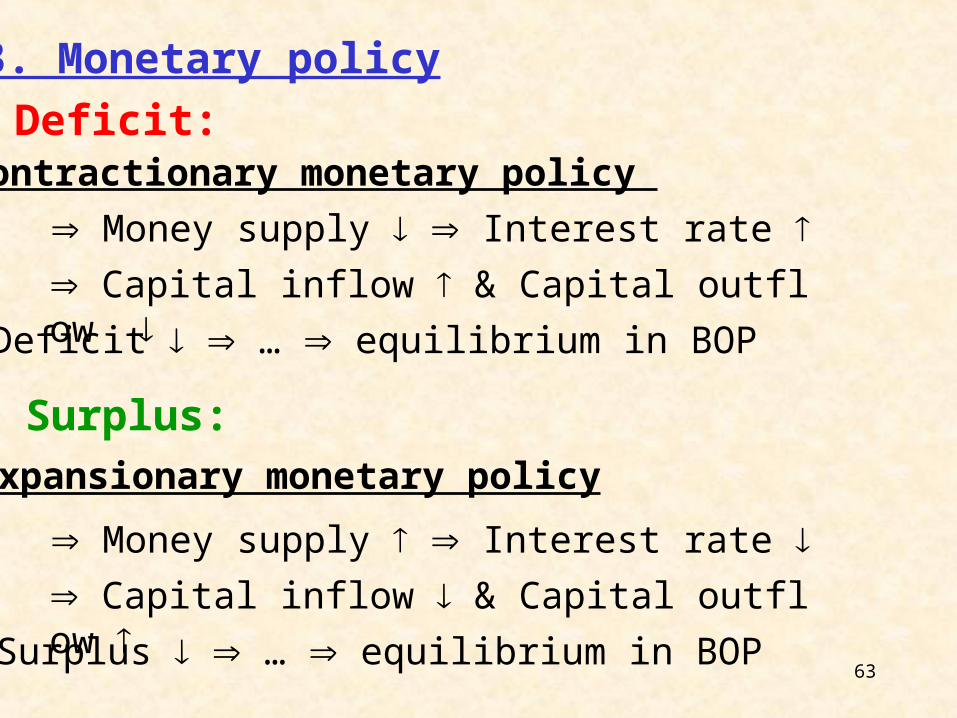

3. Monetary policy

Contractionary monetary policy

Money supply Interest rate Capital inflow & Capital outflow Deficit … equilibrium in BOP

Deficit:

Expansionary monetary policy

Money supply Interest rate

Surplus … equilibrium in BOP

Surplus:

Capital inflow & Capital outflow

64

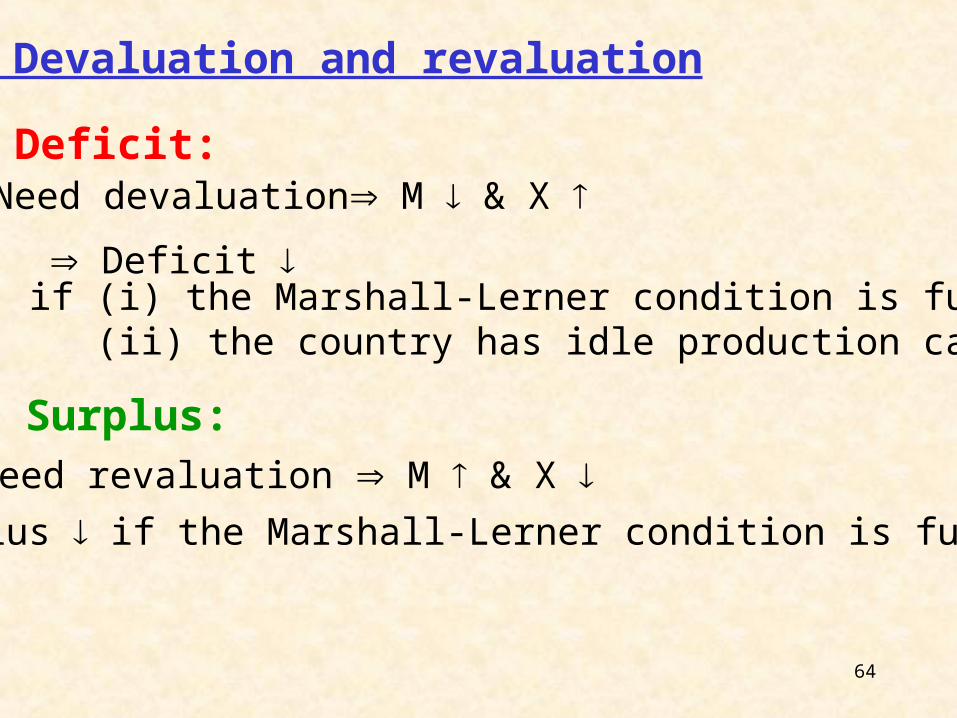

4. Devaluation and revaluation

Need devaluation M & X

Deficit if (i) the Marshall-Lerner condition is fulfilled (ii) the country has idle production capacity

Deficit:

Need revaluation M & X Surplus if the Marshall-Lerner condition is fulfilled

Surplus:

65

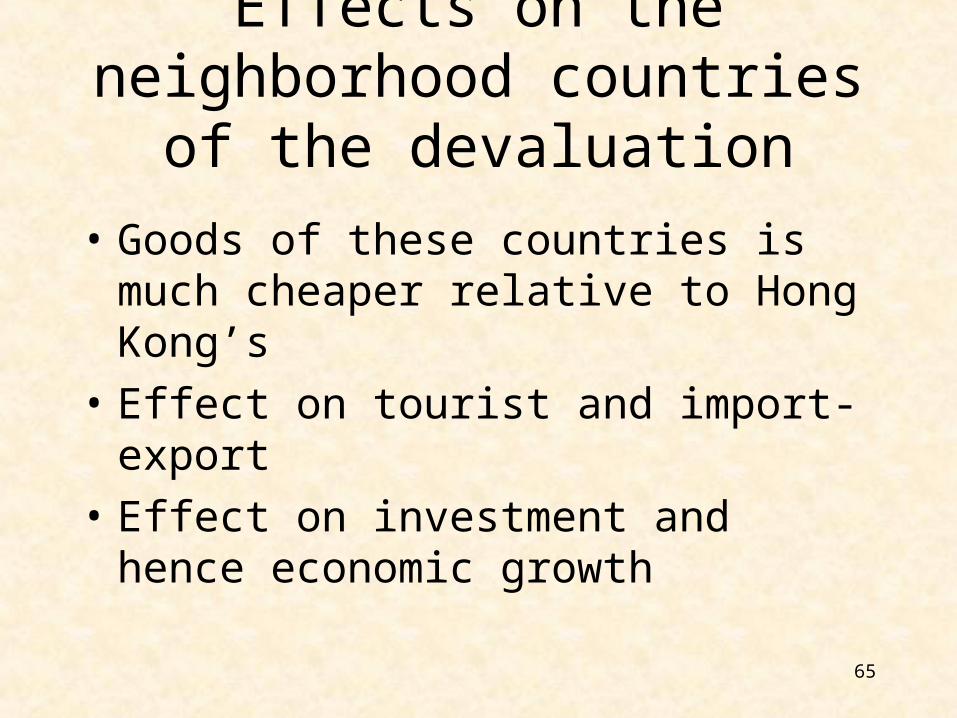

Effects on the neighborhood countries of the devaluation

• Goods of these countries is much cheaper relative to Hong Kong’s

• Effect on tourist and import-export

• Effect on investment and hence economic growth

66

67

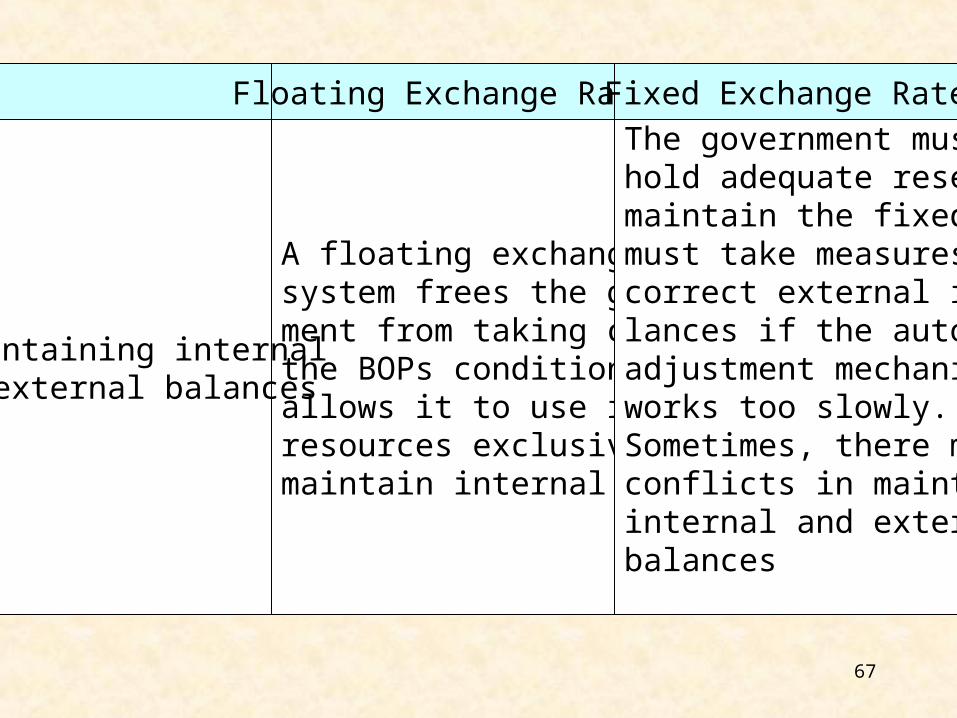

Floating Exchange Rate Fixed Exchange Rate

A floating exchange rate system frees the govern-ment from taking care of the BOPs condition and allows it to use its resources exclusively tomaintain internal balance.

Maintaining internal& external balances

The government must hold adequate reserves to maintain the fixed rate & must take measures to correct external imba-lances if the automatic adjustment mechanism works too slowly.Sometimes, there may be conflicts in maintaininginternal and external balances

68

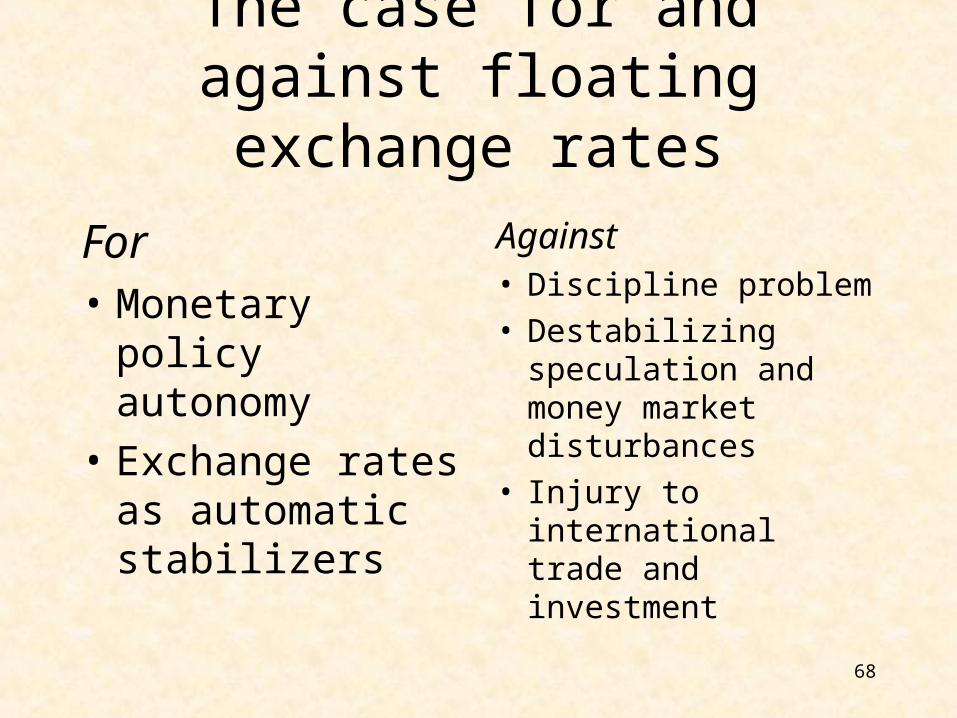

The case for and against floating exchange rates

For • Monetary policy

autonomy

• Exchange rates as automatic stabilizers

Against• Discipline problem• Destabilizing

speculation and money market disturbances

• Injury to international trade and investment

69

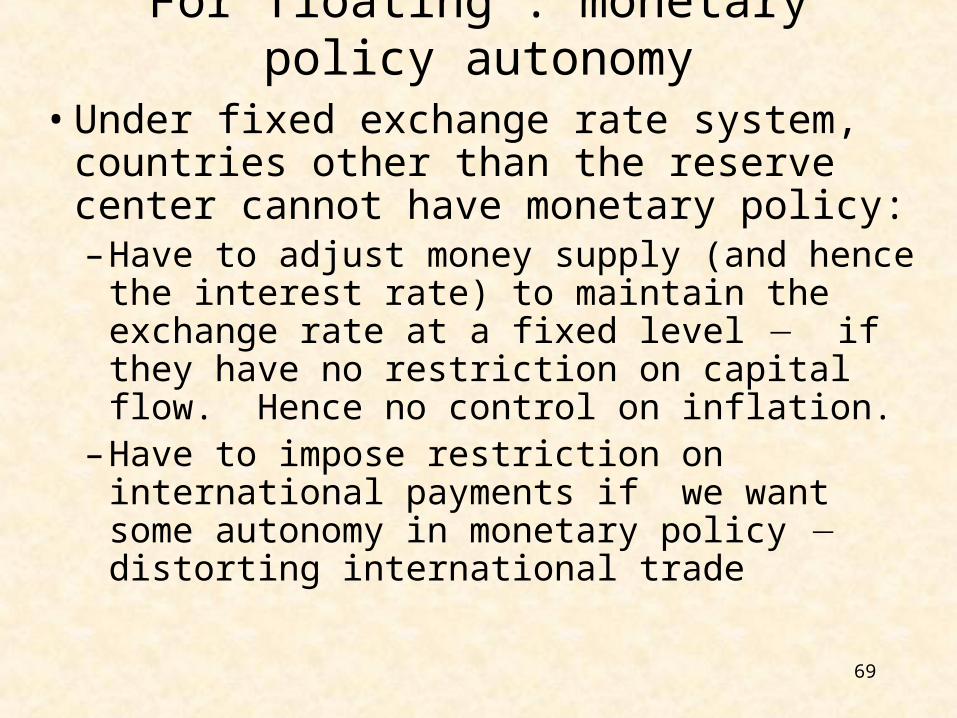

For floating : monetary policy autonomy• Under fixed exchange rate system,

countries other than the reserve center cannot have monetary policy:– Have to adjust money supply (and hence the

interest rate) to maintain the exchange rate at a fixed level if they have no restriction on capital flow. Hence no control on inflation.

– Have to impose restriction on international payments if we want some autonomy in monetary policy distorting international trade

70

Against fixed : Tradeoff between fixed exchange rate regime and monetary policy autonomy

• Under fixed exchange rate regime, a country cannot use monetary policy to affect output

• Monetary policy, if any, serves to fix the exchange rate

• In other words, for fixed exchange rate regime, we sacrifice monetary policy as a tool to affect the economy

• Currency board system is one form of fixed exchange rate regime.

71

For floating: Exchange rates as automatic stabilizers

• A temporary fall in export demand => fall in domestic currency demand => domestic currency depreciates => cheaper export => more Qd for export

72

Against floating : Discipline

• Government might embark on over-expansionary fiscal or monetary policy, falling into the inflation bias trap because no need to worry about losses of foreign reserves.

73

Against floating : Destabilizing speculation and money market disturbances

• Anything that fluctuates, including floating exchange rate, can be speculated.

• Speculation may lead to – instability in foreign exchange markets and hence – negative effect on countries’ internal and external

balances.

• Disturbances (temporary) to the home money market could be more disruptive under floating than under a fixed rate.

74

Against floating : Injury to international trade and investment

• Fluctuating exchange rates implies more uncertain returns on investment and prices of goods traded internationally.

• Theoretically, exchange rate risk may be avoided through a transactions in the forward exchange market. – May be costly to use.

77

78

External Balance occurs when a country’s BOP position is in balance.

Internal balance occurs when a country can attain low unemployment and low inflation.

79

It can happen that a country pursues fiscal and monetary policies to achieve internal balance, but that these may have the opposite effect with respect to external balance.

Whether there is a conflict between the objectives of internal and external balance depends on both the initial payments position and the domestic situation.

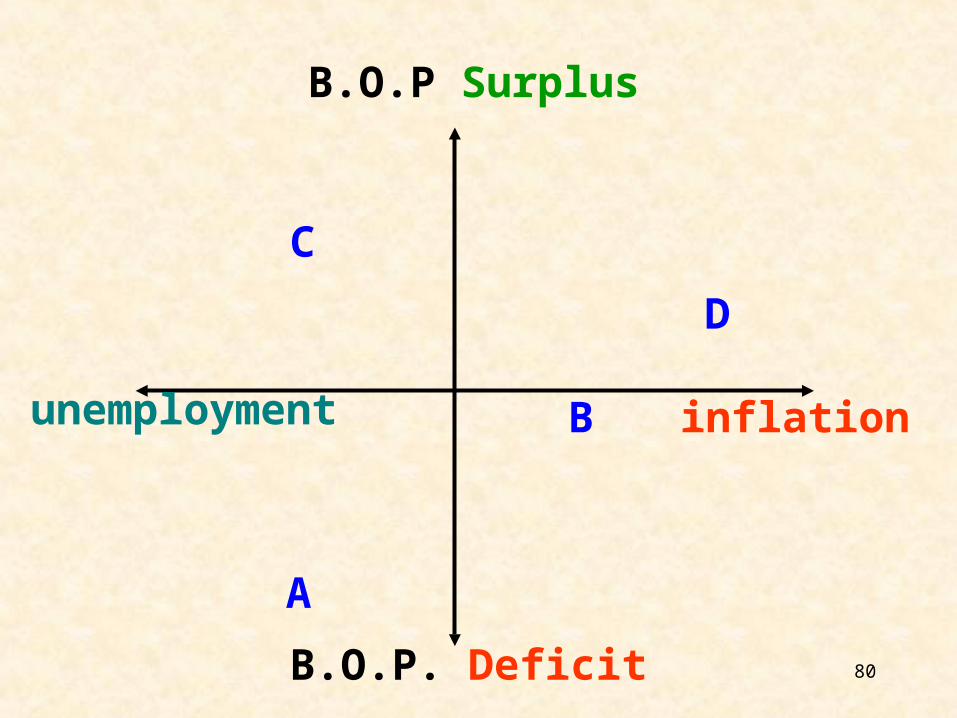

80

inflationunemployment

B.O.P Surplus

B.O.P. Deficit

C

D

B

A

81

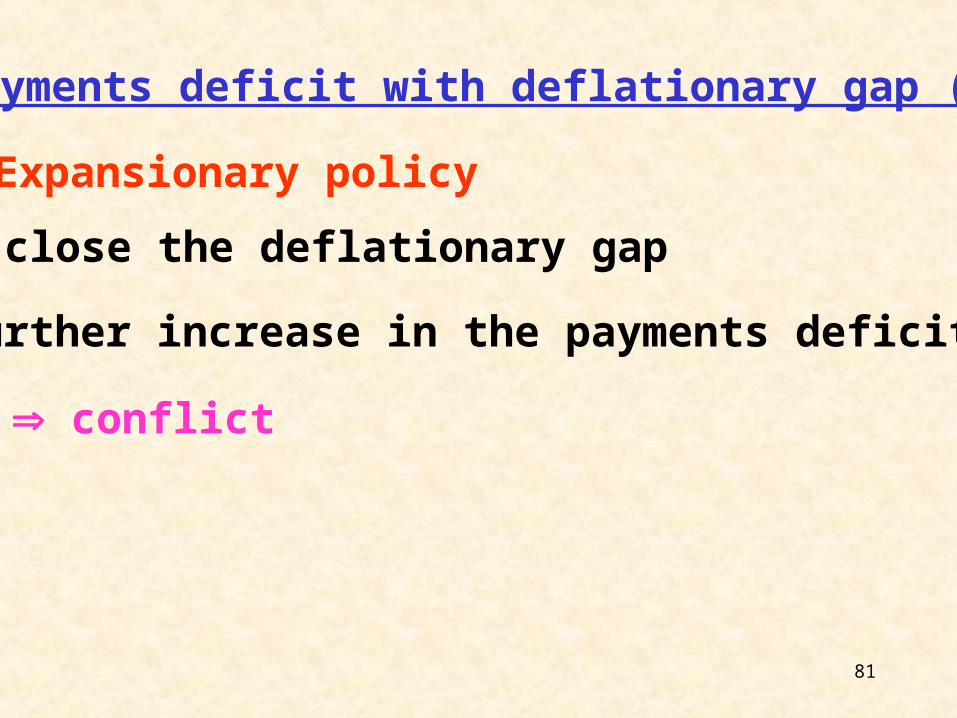

1. Payments deficit with deflationary gap (A)

close the deflationary gap

Expansionary policy

further increase in the payments deficit

conflict

82

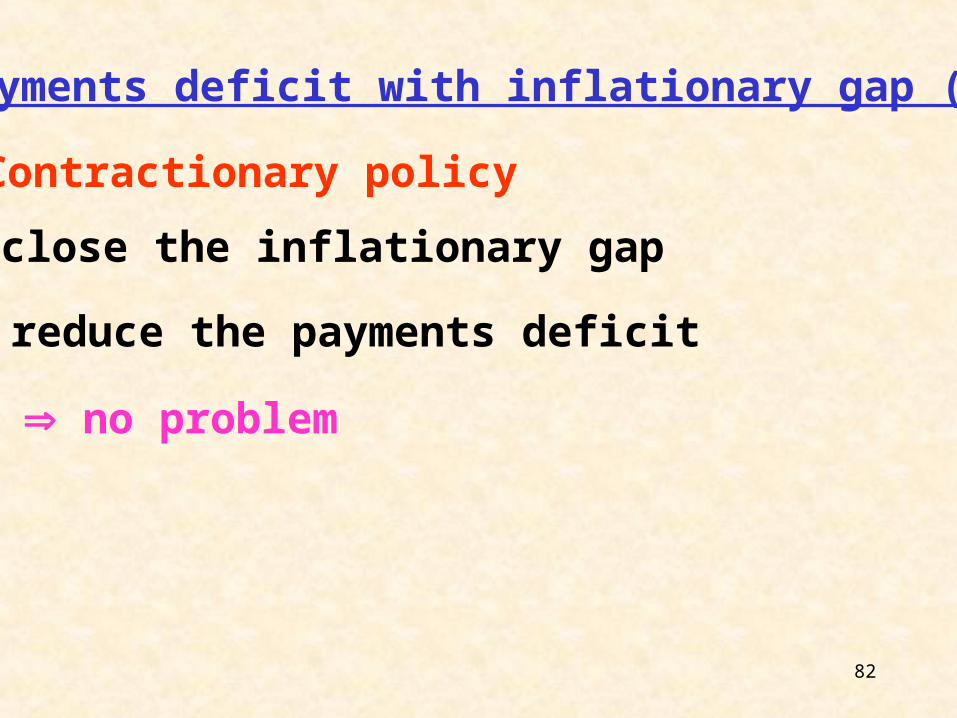

2. Payments deficit with inflationary gap (B)

close the inflationary gap

Contractionary policy

reduce the payments deficit

no problem

83

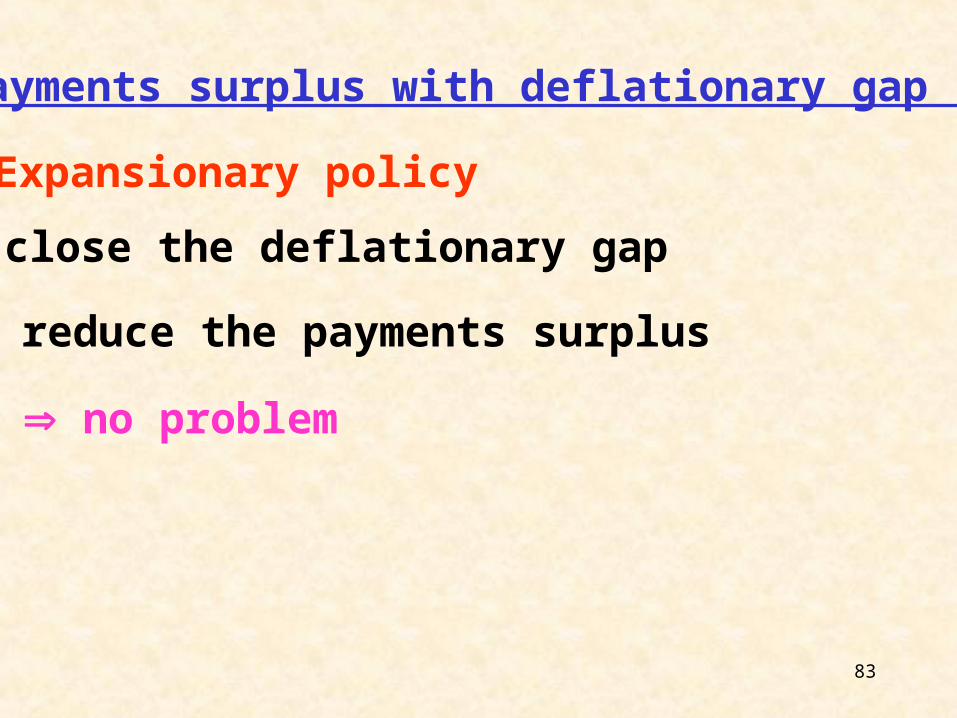

3. Payments surplus with deflationary gap (C)

close the deflationary gap

Expansionary policy

reduce the payments surplus

no problem

84

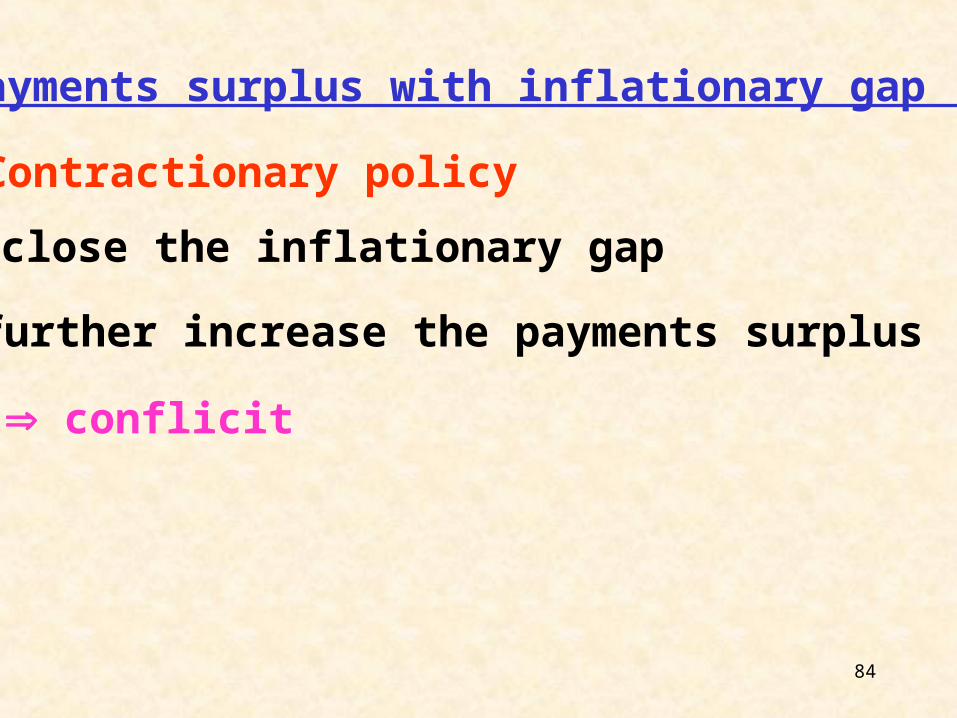

4. Payments surplus with inflationary gap (D)

close the inflationary gap

Contractionary policy

further increase the payments surplus

conflicit

86

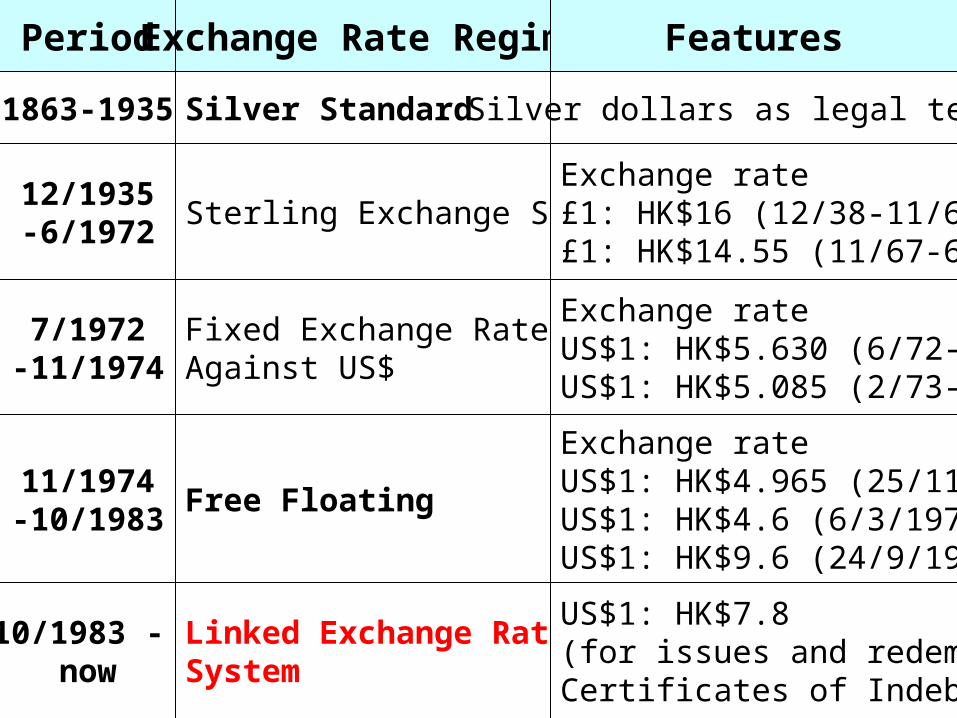

Period Exchange Rate Regime Features

1863-1935 Silver Standard Silver dollars as legal tender

12/1935-6/1972

Sterling Exchange StandardExchange rate£1: HK$16 (12/38-11/67)£1: HK$14.55 (11/67-6/72)

7/1972-11/1974

Fixed Exchange Rate Against US$

Exchange rateUS$1: HK$5.630 (6/72-2/73)US$1: HK$5.085 (2/73-11/74)

11/1974-10/1983

Free Floating

Exchange rateUS$1: HK$4.965 (25/11/1974)US$1: HK$4.6 (6/3/1978)US$1: HK$9.6 (24/9/1983)

10/1983 - now

Linked Exchange Rate System

US$1: HK$7.8(for issues and redemption of Certificates of Indebtedness)

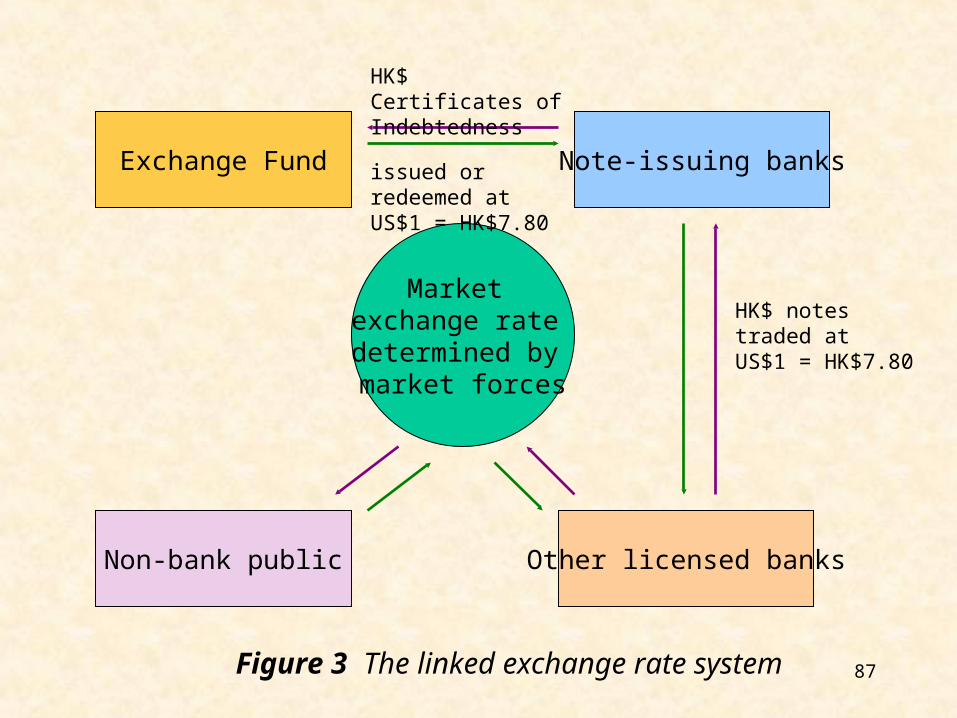

87Figure 3 The linked exchange rate system

Market exchange rate determined by market forces

Note-issuing banksExchange Fund

Other licensed banksNon-bank public

HK$ notes traded at US$1 = HK$7.80

HK$ Certificates of Indebtedness

issued or redeemed at US$1 = HK$7.80

88

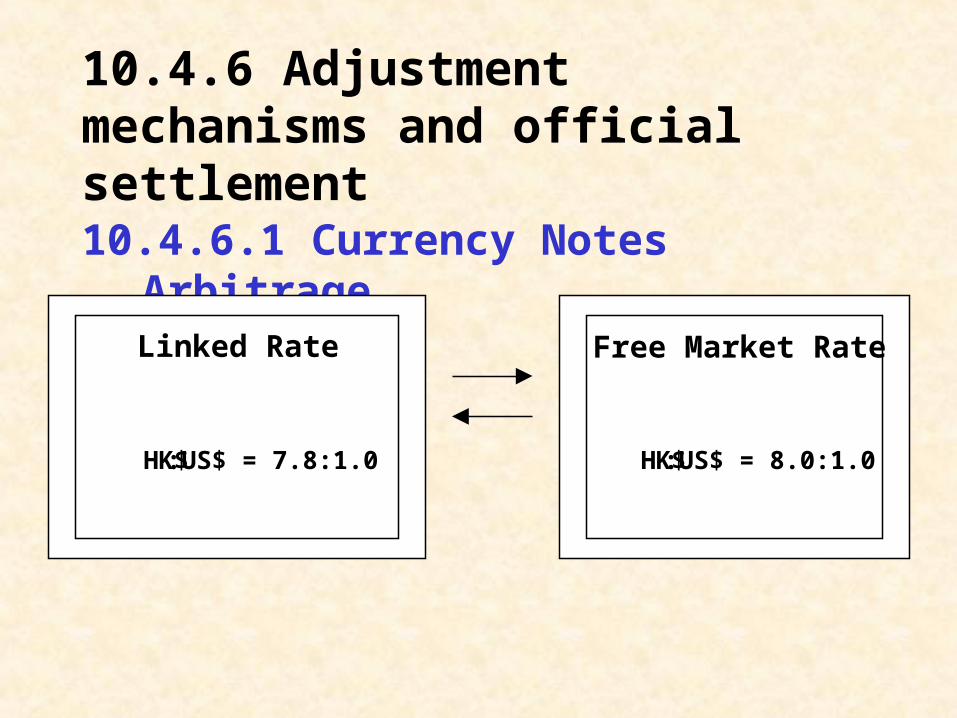

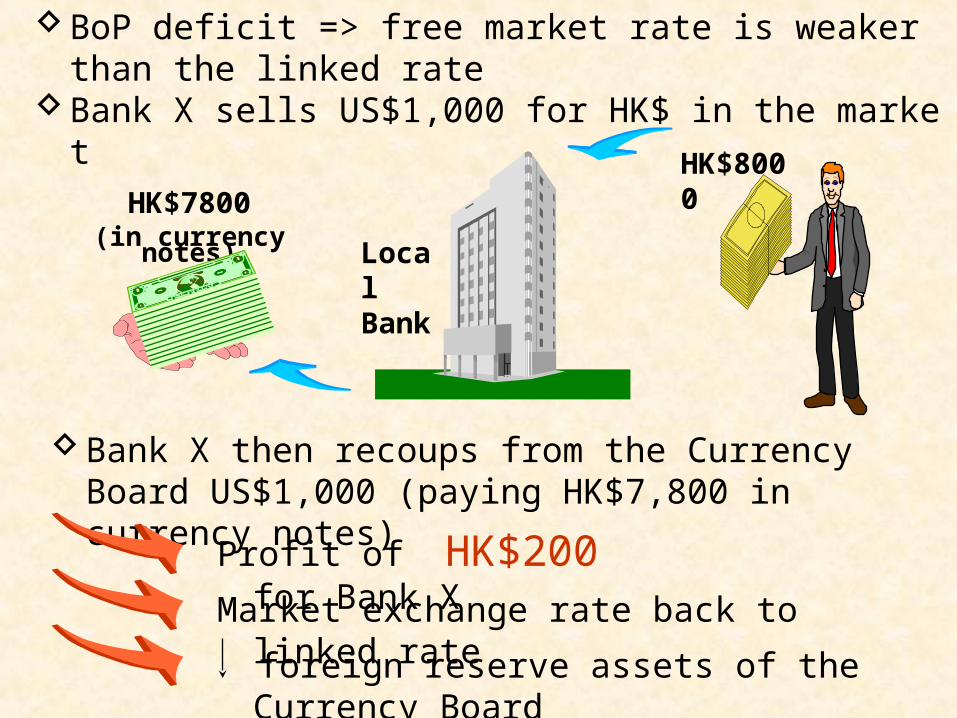

10.4.6 Adjustment mechanisms and official settlement

10.4.6.1 Currency Notes Arbitrage

Linked Rate

HK$ :US$ = 7.8:1.0

Free Market Rate

HK$ :US$ = 8.0:1.0

BoP deficit => free market rate is weaker than the linked rateBank X sells US$1,000 for HK$ in the market

Local Bank

HK$8000HK$7800

(in currency notes)

Bank X then recoups from the Currency Board US$1,000 (paying HK$7,800 in currency notes)

Profit of HK$200 for Bank X

Market exchange rate back to linked rate

foreign reserve assets of the Currency Board

91

92

93

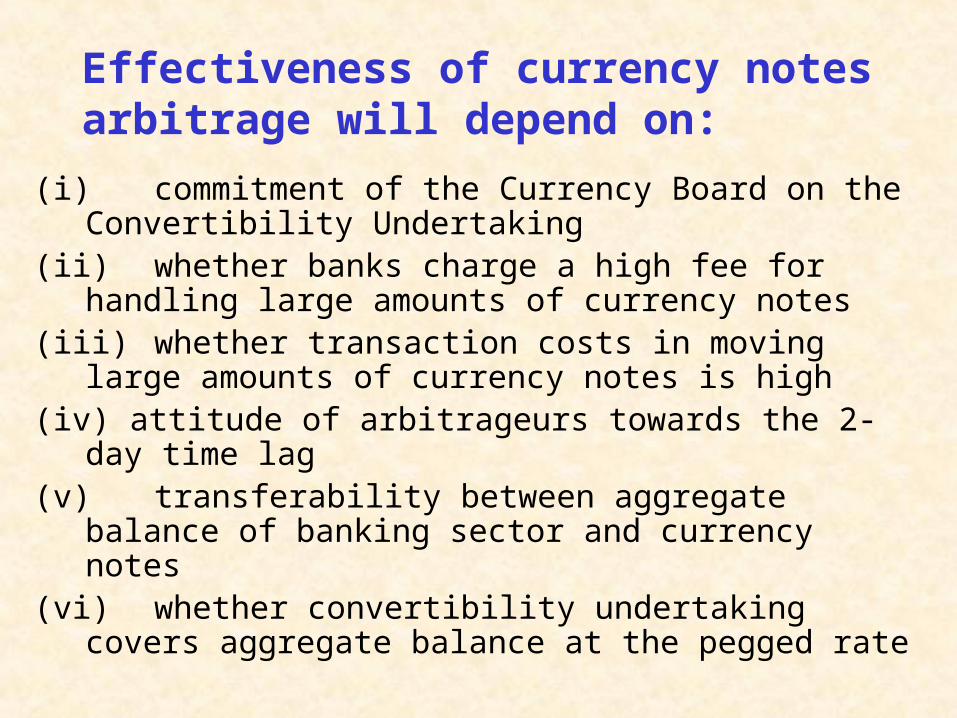

Effectiveness of currency notes arbitrage will depend on:

(i) commitment of the Currency Board on the Convertibility Undertaking

(ii) whether banks charge a high fee for handling large amounts of currency notes

(iii)whether transaction costs in moving large amounts of currency notes is high

(iv) attitude of arbitrageurs towards the 2-day time lag (v) transferability between aggregate balance of banking

sector and currency notes(vi) whether convertibility undertaking covers aggregate

balance at the pegged rate

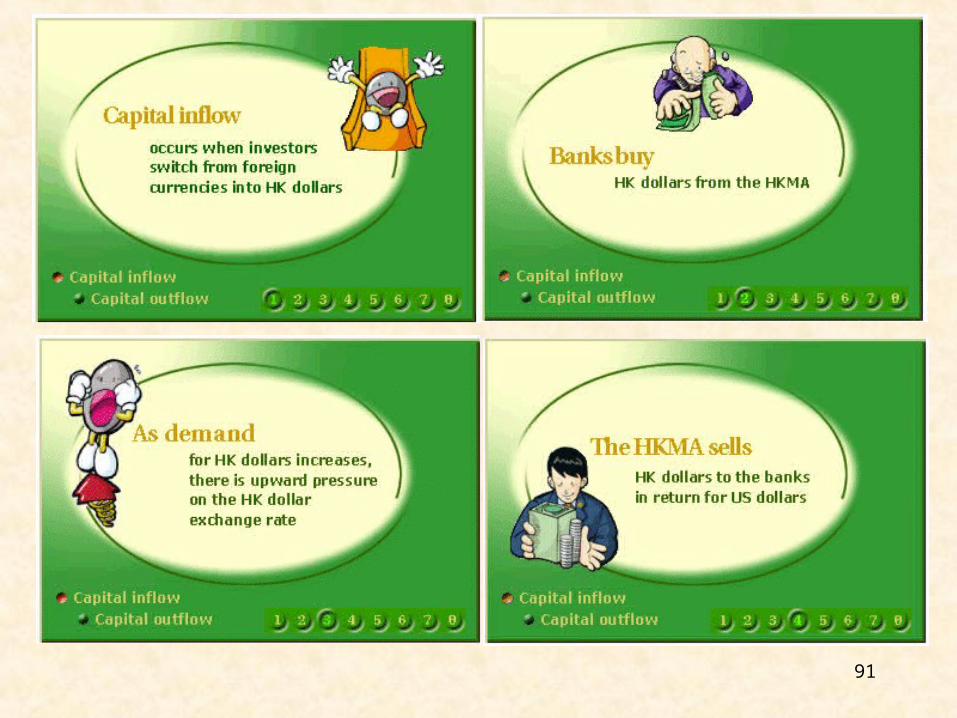

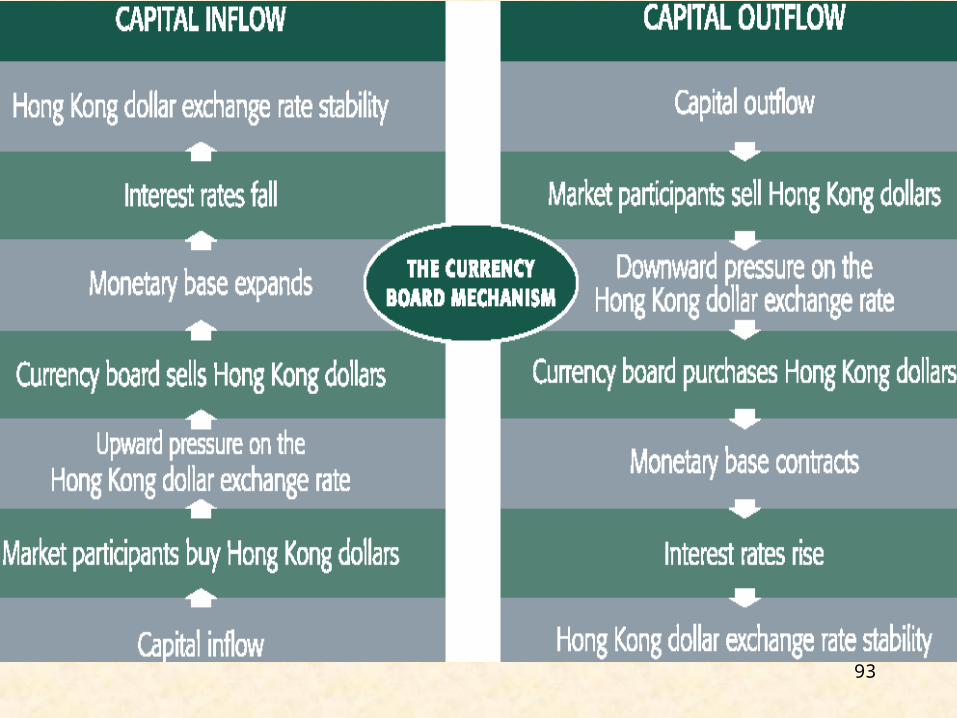

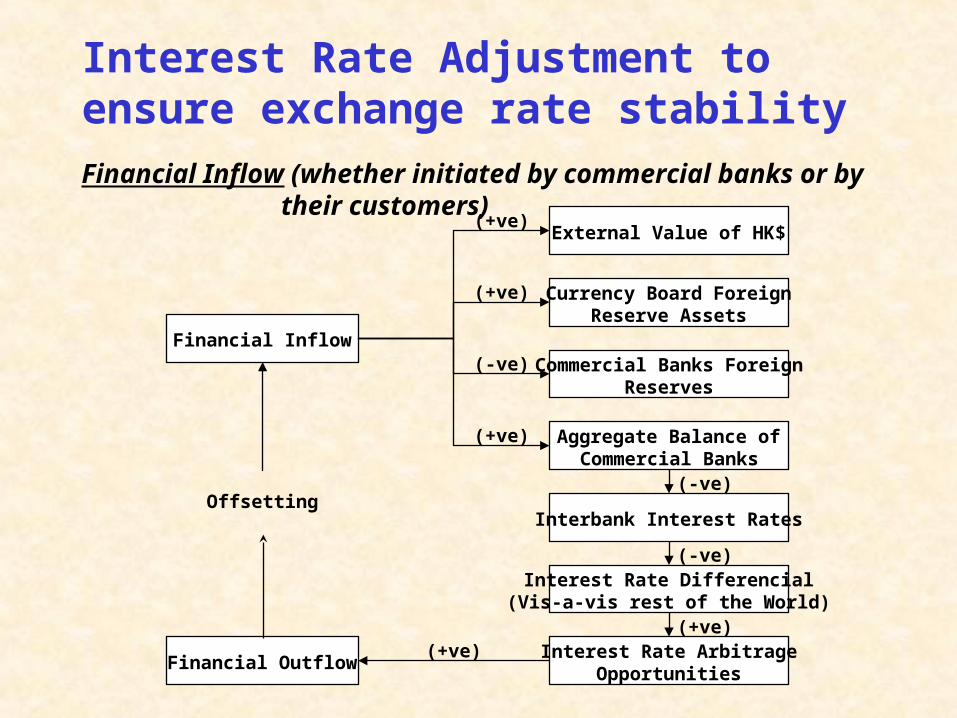

Interest Rate Adjustment to ensure exchange rate stability

Financial Inflow (whether initiated by commercial banks or by their customers)

Financial Inflow

External Value of HK$

Currency Board ForeignReserve Assets

Commercial Banks ForeignReserves

Aggregate Balance ofCommercial Banks

Interbank Interest Rates

Interest Rate Differencial(Vis-a-vis rest of the World)

Interest Rate ArbitrageOpportunities

Financial Outflow

Offsetting

(+ve)

(+ve)

(-ve)

(+ve)

(-ve)

(-ve)

(+ve)(+ve)

96

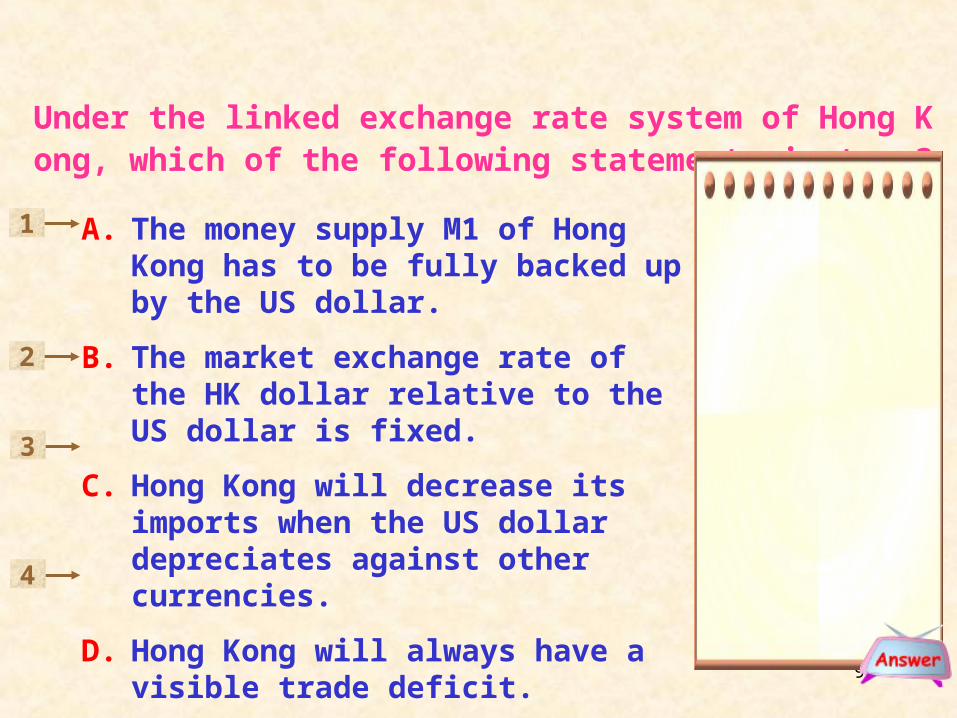

A. The money supply M1 of Hong Kong has to be fully backed up by the US dollar.

B. The market exchange rate of the HK dollar relative to the US dollar is fixed.

C. Hong Kong will decrease its imports when the US dollar depreciates against other currencies.

D. Hong Kong will always have a visible trade deficit.

Under the linked exchange rate system of Hong Kong, which of the following statements is true?

2

1

3

4

97

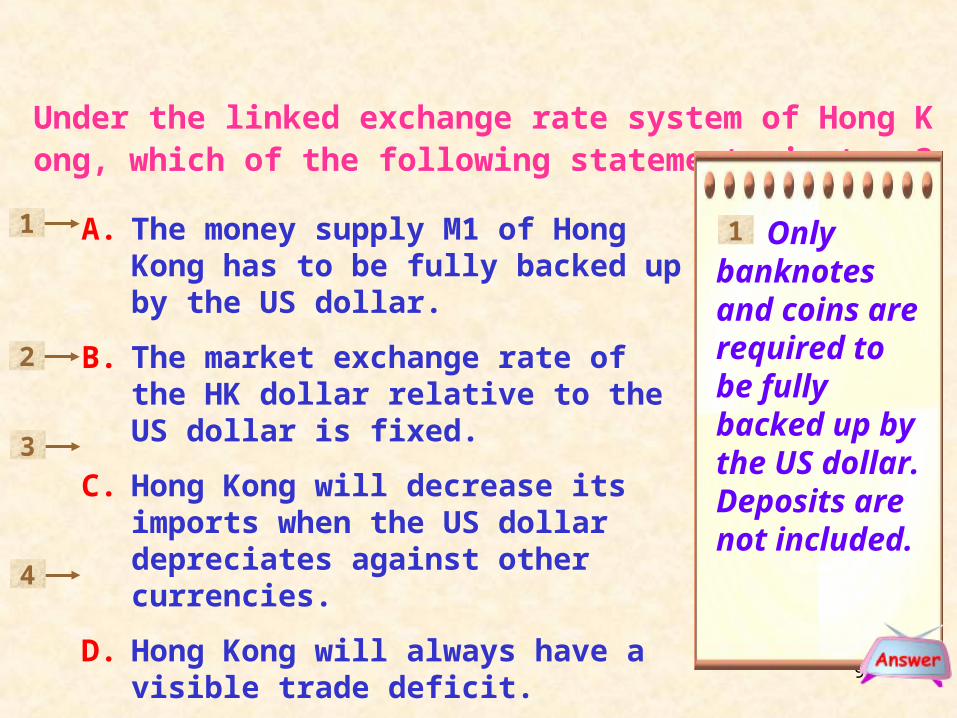

Under the linked exchange rate system of Hong Kong, which of the following statements is true?

1 Only banknotes and coins are required to be fully backed up by the US dollar. Deposits are not included.

A. The money supply M1 of Hong Kong has to be fully backed up by the US dollar.

B. The market exchange rate of the HK dollar relative to the US dollar is fixed.

C. Hong Kong will decrease its imports when the US dollar depreciates against other currencies.

D. Hong Kong will always have a visible trade deficit.

2

1

3

4

98

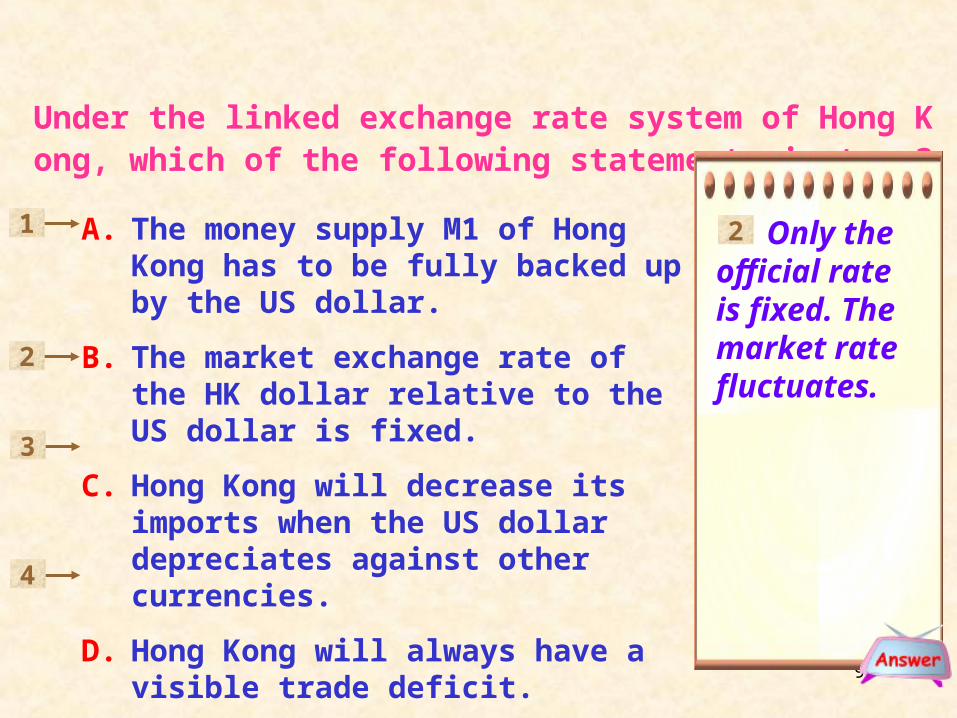

Under the linked exchange rate system of Hong Kong, which of the following statements is true?

Only the official rate is fixed. The market rate fluctuates.

2A. The money supply M1 of Hong Kong has to be fully backed up by the US dollar.

B. The market exchange rate of the HK dollar relative to the US dollar is fixed.

C. Hong Kong will decrease its imports when the US dollar depreciates against other currencies.

D. Hong Kong will always have a visible trade deficit.

2

1

3

4

99

Under the linked exchange rate system of Hong Kong, which of the following statements is true?

The depreciation of the USD against other currencies implies more expensive imports to Hong Kong, as the external value of the HK dollar against other currencies must follow that of the USD.

3A. The money supply M1 of Hong Kong has to be fully backed up by the US dollar.

B. The market exchange rate of the HK dollar relative to the US dollar is fixed.

C. Hong Kong will decrease its imports when the US dollar depreciates against other currencies.

D. Hong Kong will always have a visible trade deficit.

2

1

3

4

100

Under the linked exchange rate system of Hong Kong, which of the following statements is true?

The balance of visible trade is not directly determined by the exchange rate between two currencies.

4A. The money supply M1 of Hong Kong has to be fully backed up by the US dollar.

B. The market exchange rate of the HK dollar relative to the US dollar is fixed.

C. Hong Kong will decrease its imports when the US dollar depreciates against other currencies.

D. Hong Kong will always have a visible trade deficit.

2

1

3

4

101

Under the linked exchange rate system of Hong Kong, which of the following statements is true?

C

A. The money supply M1 of Hong Kong has to be fully backed up by the US dollar.

B. The market exchange rate of the HK dollar relative to the US dollar is fixed.

C. Hong Kong will decrease its imports when the US dollar depreciates against other currencies.

D. Hong Kong will always have a visible trade deficit.

2

1

3

4

102

103

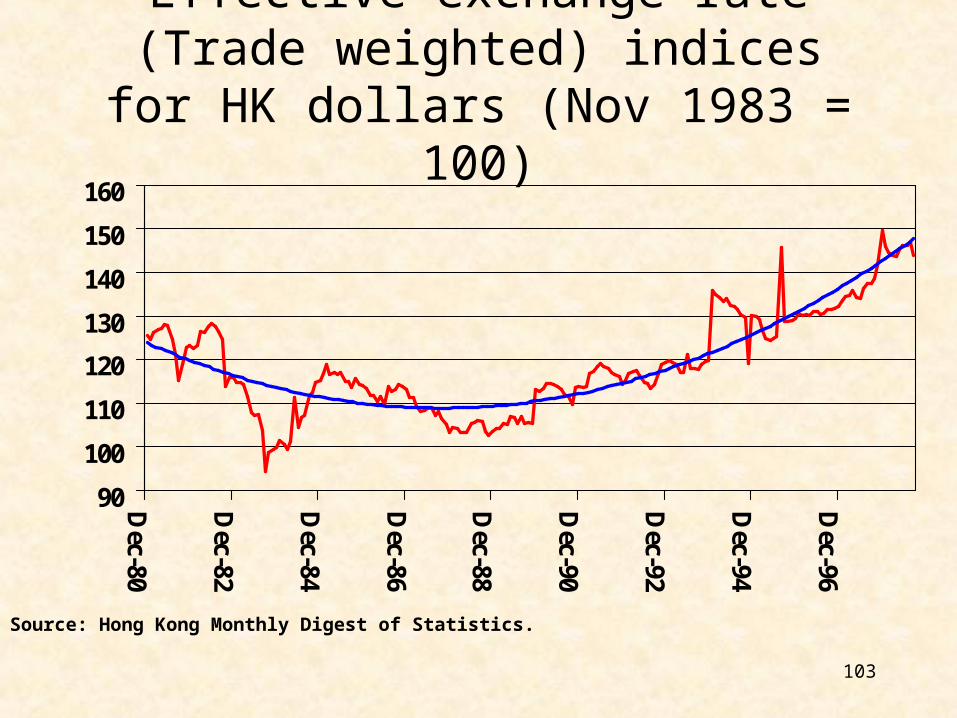

Effective exchange rate (Trade weighted) indices for HK dollars (Nov 1983 = 100)

90

100

110

120

130

140

150

160

Dec-80

Dec-82

Dec-84

Dec-86

Dec-88

Dec-90

Dec-92

Dec-94

Dec-96

Source: Hong Kong Monthly Digest of Statistics.

104

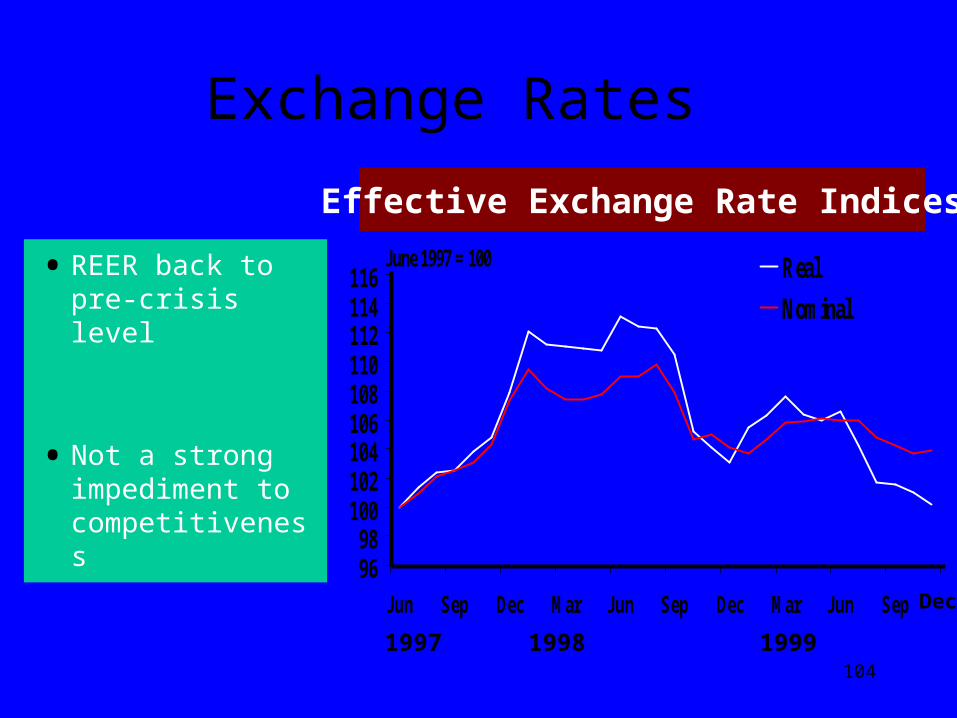

Effective Exchange Rate Indices

• REER back to pre-crisis level

• Not a strong impediment to competitiveness

Exchange Rates

9698

100102104106108110112114116

Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep

June 1997 = 100 Real

Nominal

1997 1998 1999

Dec

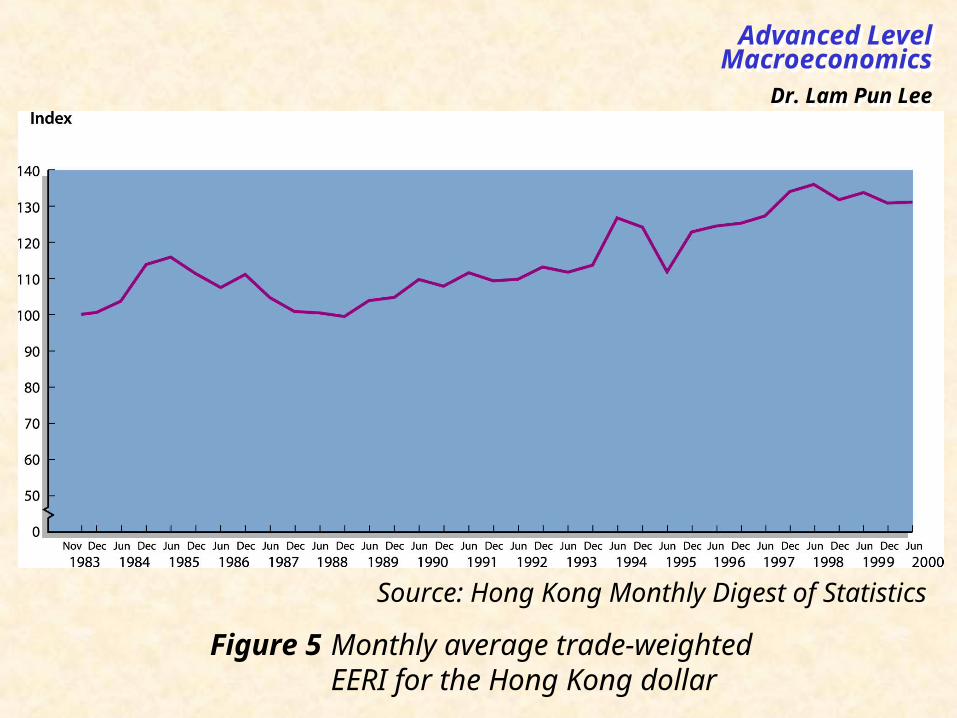

Figure 5 Monthly average trade-weighted EERI for the Hong Kong dollar

Source: Hong Kong Monthly Digest of Statistics

Dr. Lam Pun LeeDr. Lam Pun Lee

Advanced LevelMicroeconomicsAdvanced Level

Macroeconomics